One reason why the drunken sailors are in no mood to slow down. Lots of them make a lot more money on T-bills, CDs, money-market funds. Others pay more.

By Wolf Richter for WOLF STREET.

Treasury bills up to six month all yield over 5.5%. One-year T-bills yield around 5.4%. This is money that is deemed to have no credit risk, and minuscule duration risk. Lots of FDIC-insured brokered CDs (sold through a broker), and some CDs sold directly by banks are offered at around 5.5%. Money-market funds yield over 5%. FDIC-insured high-yield savings accounts yield over 4%. Consumers have many trillions of dollars in these investments, especially older consumers that are more conservative with their nest egg.

And after having gotten ripped off for years by the Fed’s interest-rate repression and QE, and after having gotten screwed by their banks that pay 0.2%, they’re taking their money where the income is, and this movement of funds has forced banks to pay more or lose deposits and collapse, and interest income has surged.

Consumers, lots of consumers, with many trillions of dollars in these instruments are finally breathing a sigh of relief, and they’re spending some of this money, which is in part why consumer spending has grown, despite the higher interest rates.

On the other side are the consumers that are paying higher interest rates on money they borrow. But 70% of household debt is in mortgages, and after the refinancing boom in 2020 through 2021, the typical mortgage is a 30-year with a fixed rate of about 3% or even less. Those rates won’t change: 70% of the consumer debt won’t get higher interest rates until the homeowner sells the home, and the buyer has to get a 7.2% mortgage, but purchases of previously owned homes have plunged; or unless the homeowner refinances the loan, but refis have collapsed.

With the biggest portion of household debt just about locked in at these 3% rates, only new auto loans, interest-bearing credit-card debt, personal loans, etc. have seen higher interest rates and higher interest payments.

So how much more interest income did consumers earn from higher interest rates on their interest-bearing assets, and how much more in interest payments did they make due to these higher rates on their debts?

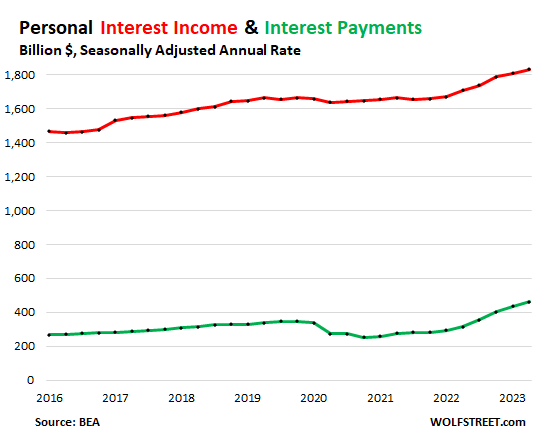

Interest income earned by consumers on their assets jumped to $1.82 trillion seasonally adjusted annual rate in Q2, according to data from the Bureau of Economic Analysis. Note, this is their interest income on tens of trillions of dollars in interest-paying assets. This income was up by $175 billion since the beginning of 2022, when the Fed started hiking interest rates (red in the chart below).

Interest payments on consumer debt rose to $462 billion seasonally adjusted annual rate in Q2, up by $180 billion since the Fed started hiking interest rates (green):

Red (interest income) went up by $175 billion and green (interest payments) by $180 billion since the beginning of 2022. All data below in seasonally adjusted annual rates.

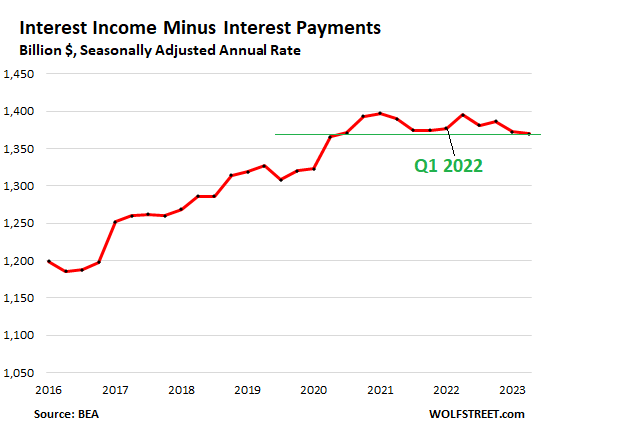

Interest income is always much higher than interest payments. About one-third of households own their home free and clear. Another third has substantially paid down their mortgage over the years, and the interest portion of their mortgage payment has become much smaller. Over one-third of households are renters. Many of them are “renters of choice” that live in higher-end houses, rented condos, and higher-end apartment buildings. Many of them have plenty of assets and no debt. Then there is a smaller portion of households that is up to their eyeballs in debt, including recent homebuyers. And a small portion of households is drowning in debt.

So, the growth of interest income (+$175 billion) is nearly the same as the growth of interest payments (+$180 billion).

And total interest income of $1.83 trillion minus total interest payments of $463 billion leaves American consumers in aggregate $1.370 trillion in net interest income in Q2, which has changed very little and is just a hair where it was on the eve of the rate hikes:

Not the same people, but in aggregate…. Consumers with credit card debt at usurious interest rates and expensive auto loans, and especially consumers with subprime credit ratings, are not the same people as those that have a lot of money in T-bills, CDs, money-market funds, and savings accounts, though there surely is some overlap. But in aggregate, all consumers combined, that’s what matters for overall consumer spending, inflation, and the economy.

In other words: higher interest rates are not constraining consumer spending in aggregate: they constrain the spending of some consumers, and are filling the wallets of other consumers.

This additional spending power is particularly important for retirees who are on a fixed income, such as Social Security or a pension. If they have $300,000 in savings, two years ago they earned nearly nothing from it, and now they’re earning $15,000 in interest income a year, and they’re plowing some of that interest income back into the economy, creating new demand.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Canadian banks give around 4-5% on 5-year guaranteed investment certificates. There are tax-free options.

The stonks like that guy mentioned in a previous blog post has gotten me cognizant that many new companies were in it to get investors’ money to talk on YouTube all day.

Stonks are too risky. I read the news, and there are a lot of delistings and bankruptcies like the bed, Bath & Beyond stonk.

Canadian dollar is also down around 30% vs. USD over the past ten years. Ouch.

If 4800 was top in SP500, then t-bills might be the place to hide out. It has worked so far from the top this time. If you stayed in sp500 in Feb, 1962 it took 20 years, 5 months to beat someone who just rolled t-bills. It took 13 years after tech bust. A lot of it is stock multiple going from too high to too low.

Bonds could be better, but you are dependent on government policy to kill inflation quickly, and that’s not a slam dunk as inflating away debt is government go to.

I’m old school (and old) too. But seems I stayed there…sorta..ie, never totally “grew up” in all aspects of it, and still don’t want to, because it would mean believing/doing a lot of horse shit. I’d rather unwind the planet unfriendly beliefs for SURE, and a lot of other stuff that is just plain wrong……or nasty and unfair and ALL written into “grown ups” minds and laws. It is also extremely hard not to be a hypocrite in this culture and that bothers me. A lot of it IS just language/culture, and ADVERTISING, I suppose, which I CAN’T avoid….I THINK, write, and speak USING it. Quite a pickle, eh?(although I SURE am damned immune to ads)

Anyway,

Maybe stocks are staying/going up contrary to older “fundamentals” because, considering total national household net wealth, ($150 TRILLION!!!), there are plenty of people who can leave a quarter to 2 M$++ there till hell freezes over, (for the family, beating cap gains and other laws/tricks I don’t know/understand but hear about), or when we go totally to the system of government all too many would like to see…..and I’m not sure what all they have planned, (or expect to see, for the MANY with nothing $s who are BSd by the REAL players). This IS NOT a conspiracy theory because LUCKILY they still fight with each other as one gets closer to the top. But they do agree on and lobby towards a LOT of stuff, like privatizing/monopolizing EVERYTHING, and inventing new privatized industries like schools.

Maybe I should quit wasting my small savings on Adrenochrome?

Tax free options are for the poor who haven’t maxed out their TFSA’s and their RRSP’s. The rest pay tax.

Disgusting, aren’t they? Those lazy poor people.

Poor people do not buy TFSAs and RSPs because they are poor.

Poor people that have a lot of income pay a lot of taxes.

Poor people that make little or no income pay no income tax.

Hmmm, so it would seem there isn’t much need to hurry up and cut rates. :-)

“would seem there isn’t much need to hurry up and cut rates”

This is also the reason why long term bond yield keep increasing.

Taking a step back, no one could have predicted this economic scenario. Like it or not I’d say that it’s here to say for awhile…

Mosler did — he’s been banging on about it for months now.

Mosler is an MMT proponent. Of course he spotted the poor policy choice made by the Fed, which in raising interest rates this high has created housing price and rents inflation. If the Fed simply stops raising rates about 90% of the housing component inflation would recede. Poor economics still being taught.

“If the Fed simply stops raising rates about 90% of the housing component inflation would recede.”

Nah. The housing factors in our inflation measures are based on rents, not home prices and not on mortgage payments. Rent inflation is determined by market forces, such as rising wages and supply and demand in the specific rental market.

That’s hilarious! Change that sentence to start with:

If the Fed successfully induces a moderate recession, then 90% of the housing component inflation would recede.

My hope is the Fed is forced to continue raising rates at least up to 6%. I want all of this massive government borrowing to really catch people’s eye as it races past $1T in annualized interest expense in Q3.

You’ve got everything ass-backwards.

The inflation is still running through the system. Three of my friends just got their property tax increase and all was up about 17% y/y. Electric utility is trying to get through a 3 year rate increase that works out to 6% per year.

My utility company just announce a 10% rise in rates going forward. Local state colleges announced a 5% tuition increase for 2023.

Rents in my area are going up still.

Could be. Especially if the government is going to step in and insure everyone’s savings 100% no limit. Janet has no choice now.

Great charts and very insightful comments and I agree with everything you said. I have no doubt the Fed will continue to look foolish as it tries to reduce inflation while not understanding what the cause and effects are of their policies. This article points to a major lack of understanding by thr FOMC. Yields were pushed too low during COVID and then raised so quickly to 5% that the Fed caused the failure of 2 large banks and started a major banking crisis that required special programs to address. This committee has proved over and over that it is incompetent but nobody will change it. Expect more policy mistakes. (I have 50 years of experience in high finance)

I think rates are a much smaller part of it. I think it’s the $5 trillion they printed in a year and a half. Only $750 billion of that has been “unprinted.”

Correct. Follow the money. Always. We are here –> absolute power corrupts, absolutely.

Jack,

No, higher rates are NOT inflationary. Rising rates impact the economy in various ways, including opposing ways, with #1 being the far larger effect than #2:

1. They should tighten credit, and make borrowing more difficult and expensive, which should constrain business investment and business and household consumption, which puts downward pressure on demand and inflation. That’s the biggest effect.

2. They also have the effect that they spread more income to people with money, which increases demand for consumer products, but that is a much smaller effect.

What I discussed here was about #2.

Total BS. There are a privileged few who have benefited tremendously from the actions of the Fed. They have BOUGHT your representation, and hence these “mistakes” will continue.

Please, don’t be such an idiot.

Agree 100%. Corruption, corruption, corruption. Apparently, a common human trait. Very sad.

Jack,

I would be curious to get your take on whether this is due to the inverted yield curve.

Given that you have 50 years finance experience, what did you observe in the 1970s that is the same/different to now?

What mistakes were made then, and do you see something similar now?

Back in the 1970’s the inflation rate was the actual inflation rate unlike today where the inflation rate is grossly understated. All this means is today we still have negative interest rates.

Exactly everybody likes to compare inflation to the seventies. The CPI gets adjusted so much if inflation is to high they just change the playbook. Re weight it. Technology goes up so they weight it for advances in technology. Car prices have gone up by a factor of twenty but inflation barely shoes up because that car has a computer in it. But how many new cars will be on the road 50 years from now? None they are all as any mechanic will tell you, throw away cars. Unibody cars have a short life span. This isnt your 69 chevy that was built to last just like everything its all throw away junk. That washer and dryer throw away after a couple years. You use to buy products that we’re quality built and made to last. Now they are made to break down so you have to buy another one. You can’t compare historical inflation to present day inflation. Its a different world. That $1000 cell phone is obsolete next year. So all these charts mean absolutely didley!

Jack-

Just curious… what differentiates “high finance” from “low finance?”

…cannabis arbitrage???

may we all find a better day.

Nah, that’s for poor people. COCAINE driven multi-tasking or you are OUT!

Jack said: “the Fed caused the failure of 2 large banks”

———————————————–

those two banks caused their own failures

Interest payments are going to be going up dramatically pretty soon with student loan payments resuming

LOL. I will believe that federal student loan payments resume when I see lots of payments being made. Until then, I will consider these things grants, rather than loans.

I hope you’re right.. I’d imagine a majority is owed by the percent with the most outstanding debt, namely millienies and Z’ers

Agree with wolf on the payment side . Just read about an actress searching for work from Baylor University with 225k student loan debt who is still in her 20s. Earns around 3k a month but her student loan payment is2/3 if her low end income. The math does not add up for repayment . Turnips have a better chance of making these payments .

She should be allowed to have the loan discharged in bankruptcy.

An actress… with $225K in loans…. what the eff was she thinking? Who approved such nonsense? The school should be required to repay the loan on her behalf and whoever (the person or persons) approved it should be thrown in the clink. Not fined. Jail. Busting rocks. Digging holes and then filling them up. Only to dig them and fill them up again… ad nauseam.

And she should not get off Scot free. Reduce it, but don’t eradicate it… otherwise the only lesson learned is that there are no consequences of bad decisions and someone else will eat you bad cooking.

There’s a belief among certain demographics that the “government” can pay for everything and living should be *free*. They don’t realize the government produces nothing and extracts the funds spent from the productive class who, when taxes become intolerable, refuse to produce because it’s fruitless.

I bet she has a room full of participation trophies too. Just a hunch.

Wonder what highly lucrative career path her $225k degree(s) prepared her for??

“She should be allowed to have the loan discharged in bankruptcy.”

In exchange for forfeiting the degree, absolutely. But absolutely NOT if she gets to keep the degree. No freebees. Nope.

Lauren when people make dumb choices ,as in student loans (predatory) they should be paid back . Us boomers had to pay back our loans . There’s no free rides !!!

Its funny when people who paid for their house and college with a sack of potatoes talk about free rides.

Meanwhile the generation theyve saddled with insurmountable debt in housing and education will likely never receive social security or medicare when it comes time.

No the financial tough luck is only for the 18 year olds with 200k in debt, never the banks that gleefully issued such loans.

The world managed by the leaded gasoline generation has been a disaster for the human race.

If younger people went on buyers strike and refused to buy houses for several years in a row, house prices would collapse. The dominant buyers are younger people — they’re driving up prices, not older people who’re selling and dying.

All you people ever do is trample all over each other to buy and drive up prices.

STOP BUYING. ALL OF YOU. AND PRICES WILL COLLAPSE. That’s all it takes, and then you can ease into it. During the housing bust, the Gen Xers and Boomers went on a buyers strike. And it worked.

https://wolfstreet.com/2023/07/25/younger-people-drove-the-increase-in-homeownership-rates-over-the-past-few-years-census/

Teaching degrees cost the same amount at Baylor.

It doesn’t make financial sense to become a school teacher either.

The payments millenials and gen zers now have to make include graduate loans at 8%+ that were not refinanced at low rates. Income-based repayment plans will be lower but should make an impact on housing prices and overall discretionary spending for this demographic. In fact there will be a lot of people (myself included) who will make big payments on prinicipal this month before interest starts to accue again. And no I don’t own a house (and won’t be buying soon) yet despite making a good amount a year. Not a good deal to buy.

Now that everyone has had their fun, would it be too much to ask BS ini for a link to this “reading” of his?

Otherwise I would suggest a most obvious, but small screen name change.

If a link is provided, I will bear the full shame of not trusting a WS regular.

ATL Fed GDPNow is tracking towards 5% for Q3.

I love all this inflation!

JPowell needs to break this economy.

And by economy I primarily mean housing.

Prices remain astronomical.

Cheers!

What about the entities and institutions holding the student debt expecting interest payments and return of their principal?

I wish. I hope. If SCOTUS would rehear the 1980s Chevron case sooner rather than later, maybe we can rein in this government that has become out of control at the agency level, i.e., Dept of Ed. That would rein in some of the vote buying capabilities. I keep hoping.

Student loans should not be made by the government. They should be made by universities, colleges, banks, brokers, family members, friends. Anything except the government.

“This additional spending power is particularly important for retirees who are on a fixed income, such as Social Security or a pension. If they have $300,000 in savings, two years ago they earned nearly nothing from it, and now they’re earning $15,000 in interest income a year, and they’re plowing some of that interest income back into the economy, creating new demand.”

This hits the nail on the head. Unless this wealth is somehow sequestered, consumer spending will not decline. Though asset inflation a tremendous amount of paper wealth was created, and this wealth is now generating revenue via interest. It would seem the asset inflation of the past couple decades may not continue in the future.

The people who are sitting around with $300,000 in savings, after previously earning zilch for far too long, are not awash in inflated earning. This is not PPP money or any other pandemic stimulus – it is a reversion to mean for people that live and save conservatively. Yes, after waiting many years of having no spending power, surely some are spending this interest income.

Sure some of it is from sales of inflated assets, but people who played that game are largely not conservative financially – it’s hard to imagine that they are just sitting on this money in insured accounts en masse. Plenty of them are full of themselves and vision themselves as great investors, so they continue plowing on and paying slightly less inflated prices for new assets.

Wolf hits on the fact that a lot of inflation is driven by mindset, such as FOMO. You can’t believe that a decade and a half of very loose monetary policy and the effects of that policy will suddenly turn reckless people into savers.

I wanted to say this, specially the first two paragraphs. I could not have said it any better.

Ditto on the first two paragraphs.

We fit into that category…. I agonized over spending $249 for a new router….. (the old one was 10 years old and couldn’t be updated any longer) and then drove back to Costco a few days later to get a $30 refund because the price dropped by that amount. My kids wouldn’t have bothered. I did.

It’s not those who earned and saved the cash in their accounts that are the problem. In order to put together more than two nickels, you have to exhibit some fiscal discipline. Not all of it is “luck”. Hunter/gatherer habits are hard to change. How many of you spend/spent your bonuses or overtime money? Blew the money you made on side gigs? I never did. I invested it… and then never touched it but to *loan* ourselves money which we then paid back to ourselves – with interest. We adjusted lifestyle with the arrival of salary increases while still maintaining our savings goal (a percentage of income… the amount of which grew as income grew). We also started saving for retirement at the ripe age of 23.

So, sequester your own money…. keep your mitts off of mine. Envy is one of the seven deadly sins.

Hunter-Gatherer habits were more frugal than we can even imagine….every day they “budgeted” to just stay ALIVE.

Learn some history.

You are talking post mass media/advertising habits…..but wouldn’t even a farmer on the plains in the roaring 20’s be ridiculously more frugal than you are? Hell, I am. You are a spendthrift.

Don’t forget that theoretical “retireee” now with additional $15k income off his $300k “pot of gold”, means he has increased his income off that “investment” by 5%.

One must also consider that his “fixed income” sources have remained just that, -fixed-, and his inflated cost of living has likely soaked up or even exceeded that “new” income.

Inflation affects people differently, depending on their spending habits.

William-

Good point.

Inflation’s effect on the individual also depends on the individual’s accumulated savings, portfolio structure, financial acumen, debt structure, industry of employ, job mobility, and ability to substitute consumption goods.

Interest payments on a percentage basis increased about 50%. Interest income on the other hand only increased about 10%. Does this indicate that a substantial portion of interest income is termed out and only a few are able to capture the large increase in interest rates?

Your math is defective…..

I had CDs in the two’s that are now in the five’s. Hardly a 10 percent increase.

The situation discussed is exactly the reason why a Gold based BRIC currency will be good for both American tax payers and American interest payers (or in general any user of USD) besides protecting the economic interests of the country that will use the BRIC currency. In economics, we call this phenomenon a positive externality (when economic benefit or loss is reaped by the third person).

BRICS Currency will end up protecting USD users residing in America from Congress and FED, thought that is not really the intent of BRICS currency.

Such nonsense. It’s not even a currency, and people will never be able to use it or hold it or pay for anything. It’s a unit to settle trades between countries, and it’s not backed by physical gold either, such BS. Get your fantasies straight.

Big story today; China stopped officially reporting on youth unemployment rate. They simply won’t report it any more. The numbers, of course, are rising.

Argentina devalued their currency 18% yesterday.

If you want to save yourself from corrupt governments, you can’t save in their currency.

The interest income plateau, in the last chart, does show this wonderful spike in Fed graciousness, but the sad reality is, this flood of income started as a trickle a little over a year ago, and has increased at a glacial pace. Sure, it’s been nice to get a little pop from a money market fund each month, but unless you’re sitting on a million buck account, that extra couple of hundred bucks a month isn’t exactly a huge windfall.

Yes, I’m thrilled to be making more than I used to get at a bank, and I’m thrilled to feel fairly safe, but I’m not thrilled that every corporation in America is gouging as much profit out of every product and service that exists.

If anything, I have to continually look at the stock indexes, and realize the five year average performance is almost as bad as my money market fund. The only thing that really makes me happy, is to review the 5 or 10 year performance of almost any vanguard mutual fund, and be grateful to not be paying them fees to burn cash. I’d probably be happier owning Apple and just shutting up…

Yes, I’m pessimistic!

“the growth of interest income (+$175 billion) is nearly the same as the growth of interest payments (+$180 billion)”

But isn’t the income growth taxed? Even taking tax into account I suppose it remains a small difference, but doesn’t it suggest that hiking even higher could work and cool down the economy? Or at least to some extent mitigate the gigantic budgetary splurging?

“But isn’t the income growth taxed?”

Excellent point.

Worth considering how DC as tax extractor/master forger may be able to work both/all sides of any macro situation/environment under its fief/fiat

To the disadvantage of its “citizen” drones/cattle.

Worth closer examination/step-through.

Hi Wolf

If I sold my house back in 2021 and got $1million for it and the purchaser who bought my house borrowed the money at 3%. They then pay the bank $30k in a year in interest.

The $1 million I got from the sale back then is deposited at the bank and gets 0.2% interest, which was the going rate back then, therefore the bank pays me $2k a year.

So from the banks perspective; $30k in and $2k out. The bank is $28k ahead.

I now take my money out of the 0.2% savings account and reinvest back with the bank into a 5% interest savings account.

So from the banks perspective; $30k in and $50k out. The bank is now out of pocket by $20k on that $1million mortgage.

Do you reckon the bank might be buggered.

That’s not how banks work.

You’re letting the bank invest your money in 7% notes to give you back 5%. They’re ahead by 2%.

How is the coleman tent you are living in?

Is the realtor your forgot to pay hunting you down in the tent village?

Lol

Except that most banks do not keep much of the Mrtg loans they originate on their balance sheets. They are packaged up and sold. Maybe it’s different for jumbos ? Banks make their money from Mrtg loans in fees and servicing. Banks that held those 3% on their balance sheets now have huge unrealized losses on those balance sheets.

So rising interest rates are inflationary, right?

Wolf, I understand your argument but unless you also have data that shows how much of the earned interest is spent, rather than accrued, I believe you’re getting caught up in your math.

“So rising interest rates are inflationary, right?”

NO, THEY’RE NOT. I never said that.

Rising rates impact the economy in various ways, including opposing ways, with #1 being the far larger effect than #2:

1. They should tighten credit, and make borrowing more difficult and expensive, which should constrain business investment and business and household consumption, which puts downward pressure on demand and inflation. That’s the biggest effect.

2. They also have the effect that they spread more income to people with money, which increases demand for consumer products, but that is a much smaller effect.

What I discussed here was about #2.

Wolf,

Do you think the strange issues are due to lack of credit spreads opening up and the failure of the long end of the curve to go up?

Bill Gross was talking about this happening in the 1970s and that when it suddenly happened it was like a sledgehammer. People weren’t ready for it.

Do you see history repeating itself?

I was sarcastic, Wolf. Sorry if I didn’t manage to convey that in writing :)

Re. the second point: I am one of those “people with money”. Meaning I’m in short term securities. I do not see the interest I get as income. Just lousy compensation for the erosion of my money’s purchasing power. After tax I’m still below the actual rate of inflation, but, as you said in other articles, it’s still better than a substantial loss in the stock market, for example.

Your point about the retirees spending all this newly earned money is well taken. However I wonder how many of them actually are invested in bonds now, after being abused by the Fed for so many years. Also, I wonder how many actually spend that money, rather than saving them because they expect the rates to go down again, for example.

Best regards.

Awesome article.

We’re talking taxable income on the 15k?

And if (for example purposes) someone did have 300k in savings. What would they have left in their 401k, on average?

Or maybe their 401k is the savings.

My savings is 401k savings in money market accounts . Taxable when I spend

Government has got some tax traps for you depending on your income. You have to use a good software to figure out how to get it out of tax deferred at a reasonable tax rate. Get a plan in your 50’s on how to get it out.

Fair return on money IS an economic engine.

Suppressed rates take this away and place the benefits in the hands of the government and other borrowers.

We saw this for 13 years…..and the mantra was “low rates stimulate”. But in fact there is a depressing factor with low rates on the consumer, conveniently lost on those who push the suppressed rates to the benefit and delight of leverageres and govt spenders.

Things would be better NOW, IMO, if Fed Funds had stayed at 2% and 30yr mortgages at 5% for that Fed manipulated period from 2009 to 20221.

Central bankers believe themselves smarter than free market forces….free market forces have cleansing cycles and self correct. Central bankers will have none of that.

So there is a tipping point for interest rates to fail to cool inflation, whereby they increase disposable income and create additional demand.

This is just another angle that interest rates are not the tool to control inflation while QT isn’t finished.The additional money supply has to be shrunk back in and the US taxpayer stiffed for the losses. The UK faces a 10K per worker loss for reversing QE, the BoE having got indemnification against losses. Over the last 5 years UK rpi inflation is at a stunning 37%. US cpi (typically lower) at 21% over the same period. US actually increased the money supply less dramatically than the UK so I think would be lower anyway.

The tragedy of course is that unprinting money requires foregone consumption, so you can’t achieve without the involvement of the government, and the Fed imagines that they can simply book the loss as deferred, but if its deferred its not unprinting.

High inflation over 5 years is going to set the base for a generation. I’m starting to wonder if they can ever get inflation under control, presumably Argentina thought ah inflation is easy to control like Bernanke with all the policy tools. If the US government doesn’t forego consumption then how can it happen?

“they increase disposable income and create additional demand.”

Agreed. It really is a matter of who gets to spend the money.

Suppressed rates put money in the hands of the borrowers and govt.

Fair returns puts the money in the hands of the saver, earner, consumer.

Either way the money gets spent. IMO.

For every action there is an equal and opposite reaction.

The strong Dollar is crushing everyone, particularly developing/emerging economies. Not a problem if if you have lots of Dollars of course.

These morons do the same stupid thing over and over again: they borrow in dollars because they destroyed their own currencies and cannot cheaply borrow in it, but they can cheaply borrow in dollars, and then the dollar rightfully whacks them. Investors in the US and elsewhere that lend dollars to emerging market governments and companies should lose all their money. The Wall Street goons that arranged those loans should spend some quality time in the hoosegow. And emerging market governments and companies should learn how to live with their shitty currencies, and be barred from borrowing in dollars or euros, and they should manage their currencies properly so that they’re not shitty and so that they can be used for borrowing at a reasonable cost.

Agree, and the IMF needs to cut its losses and exit these countries. Argentina, I’m looking at you.

*And emerging market governments and companies should learn how to live with their shitty currencies, and be barred from borrowing in dollars or euros, and they should manage their currencies properly so that they’re not shitty and so that they can be used for borrowing at a reasonable cost.*

A good way is the currency board.

One was introduced here (Bulgaria) in 1997.

From then until now, the local currency has not changed.

First it was tied to the German mark and now it is tied to the euro.

Finally savers like me are getting rewarded. But I’m not spending. I don’t trust them to not screw us again. Plus, I’m the type who enjoys watching my accounts grow more than I like buying stuff.

Except that, due to inflation, your interest income after taxes likely does not maintain the purchasing power of your nest egg. People who are spending their interest receipts are really spending capital.

So! I manage it well, so I’m doing great.

Nothing maintains the purchasing power unless the value rises with inflation. Doesn’t matter what it is. But the value has not risen with inflation: stocks, housing, cryptos, gold are all down from their peaks before this inflation started. People lost purchasing power on all of them, but they didn’t get paid interest on them. In fact, the carrying costs of RE are fairly big. Inflation is a bitch.

These capital losses are on top of the losses in purchasing power due to inflation.

So in this environment, something that doesn’t lose value but earns 5% is a pretty good deals.

kramartini…. that’s worn out trope. “inflation erodes… blah blah blah”. It’s naive financial advice.

I’d still rather have what I have invested “eroding” and available for deployment than a bunch of trinkets of little to no value, other than to impress people I don’t care about.

I have the misfortune of cleaning out my sister’s house after she suffered a debilitating stroke. She has a bedroom set that she paid $30K+ for (Josef Stickley – the real solid walnut wood stuff, not the veneered wannabe). She has @20 hand made Tiffany lamps scattered around the house that she paid multiples of hundreds, and sometimes thousands, for each. All unsellable as it’s a design niche. Essentially worthless as it’s not a hot item in the land of the pink flamingo. So did she gain anything as a result of spending that money vs. it “eroding” in her accounts? No. The $100K car worth $25K suffered a $75K “erosion”. Did she benefit by not buying a Toyota? A like Toyota is worth the same amount and arguably just as comfortable. So, nope. A $25K diamond necklace I found tossed on a shelf (found the receipt)? I’d guess it’s *worth* $5K based on the scrap value of the gold and wholesale on the diamonds. Erode much? What’s the value of a Louis Vuitton purse after it’s used? 1/10th of the *stupid* price? Goodwill’s gonna make a bundle (my wife wouldn’t be caught dead with a LV purse).

Money in the stock market “erodes” and carries risk. Real estate values can “erode” and carry risk. It all “erodes”. Pedestrian vehicles erode. Gold “erodes” (it’s valued in fiat). So what is the difference? Not a dang thing.

If spending money on certain things (travel for example) brings you joy, then go for it. But the value of that is “eroded” too. And don’t cry when you’ve got the shorts because your grocery costs inflated. You made a choice on how to deploy your capital. Or a dumb decision with consequences. Or tried to get rich quick on a “sure thing” and lost your shorts.

A long winded non response to my point. Spending interest in an inflationary environment is spending capital.

She shoulda bought Chanel purses and solid gold jewelry sets.

Lab diamonds are pulling down the value of mined diamonds.

Sorry about your sister.

Sounds like she had some fun hobbies.

Can’t take it with you!

I am sorry for your loss.

I hope her spending choices made her happy in her final days.

“I’d still rather have what I have invested “eroding” and available for deployment than a bunch of trinkets of little to no value, other than to impress people I don’t care about. ”

Personally, I agree with your statement above. I do treasure an antique lamp that my grandparents left me that I remembered as a child. I value trinkets as memories.

However, when I pass away into the great Colorado sunset, I really won’t care if I have trinkets or if I have millions stashed away in eroding investments, as long as I’ve enjoyed life before I leave and left some to help the kids.

Sorry to get philosophical. News of death does that to me.

BobE

Sorry? Why?

“The unexamined life is not worth living for man” -Socrates

It’s not like EVERYTHING has been figured out and is now common black and white knowledge……….

“Common sense is a collection of prejudices usually accumulate by about age 18.” -Einstein

Fed up

Ditto. Just letting the newfound interest bulk up my nest egg. After years of ZIRP this money almost seams like a windfall. Who knows if and when they may drop rates again. You just can’t take anything for granted anymore.

Argentina is a great example of a country under siege from inflation. Spent 6 months there in 2019 as inflation took off. The locals were desperate and every dime was spent on food . Yet things still functioned though I don’t know how. From my observations the elderly were struggling for sure . Higher for longer and continue Qat please which I do believe will continue.

If democratic governments get it right and allow lighted regulated capital investments then society can improve standard of living every generation. Political corruption is the norm and can send it all down the toilet which is kind of the norm.

Bless you, Wolf, for disaggregating the issue and showing that the rate increase (removal of rate repression) helped some, while HURTING others.

This is the bugaboo with monetary policy: Fed policy actions in the form of rate manipulation picks winners and losers.

As Hayek demonstrated, Fed intervention in the interest rate markets (by manipulating rates and bond prices down or up) has short circuited the transmission of market information necessary for good decision-making by savers, consumers and business people.

Time to re-think the role of the central bank…

Above comment referenced this quote from article:

“Not the same people, but in aggregate…. Consumers with credit card debt at usurious interest rates and expensive auto loans, and especially consumers with subprime credit ratings, are not the same people as those that have a lot of money in T-bills, CDs, money-market funds, and savings accounts, though there surely is some overlap. But in aggregate, all consumers combined, that’s what matters for overall consumer spending, inflation, and the economy.”

Allow me to simplify, governments around the planet have been corrupted and have been rewarding bad behavior for a very long time. It should not surprise anyone that we have more bad behavior, that’s what we have been “selecting” for.

Absolute power corrupts, absolutely.

Wolf, in the article you reference “Then there is a smaller portion of households that is up to their eyeballs in debt, including recent homebuyers”. Do you have any data about how much these recent home purchases are causing people to effectively be house poor because of this higher priced/higher mortgage rate environment? I find it incredible to hear about people earning modest incomes with $4000-$5000 mortgage payments (which includes escrows for taxes and insurance).

Would love to see an article on mortgage and rent payments respective to income over time.

Subprime auto lending is about 15% of total balances outstanding. Borrowers are rated subprime for reasons, including having too much debt and being behind on payments. The percentage is smaller for home mortgages.

That people are “house poor” for a few years after they buy a home is not a recent phenomenon. That’s been around forever. When I was house poor, I already knew the expression. It’s generally how it is unless you’re born rich.

With sales having plunged over the past 18 months, there are fewer people on the house-poor list than there would be otherwise. They also have the problem of having bought just before, during, or just after the peak, so they have a long rough ride ahead of them. But that’s also not new. Over the past many decades, housing markets have crashed at the local level all over the country. And people in those markets have to deal with that. It’s just rare that the entire US housing market crashes at the same time. So we don’t see it that much in the aggregate numbers.

I think the hammer on the economy will be when higher rates bite into new home construction. In my area a new home is about $450,000. When you buy a new home, that is a lot of consumption that gets booked into the economy immediately, even though you are going to be paying for it a long time.

450k is cheap. Here in British Columbia Canada new home construction is at least $300/sq ft. A 2000 square foot 3 bed house with lot will set you back $800k or more .

Wildfire concerns: CA, CO, UT, NV, OR, WA, ID, MT (states) and yes BC (British Columbia) province.

Believe it was 3 years ago BC had the most fires in 70 years. And the heat dome that sat over the Pac NW and BC two (?) years ago the last week in June… Lytton BC some 100 (?) miles northeast of Vancouver set an all time record high temperature for Canada…

a shocking 49.6° C, 121.3° F.

Here in Spokane, WA we had 5 days over 100°, topping out at 113° (per accuweather).

Last 10 years definitely hotter summers than usual and wildfire effects started about 7 years ago. We get smoke blowing in from all directions: California, Oregon, Idaho, British Columbia, north central Washington especially and other parts of Washington. Typically starts latter part of August off and on thru early mid October. Toxic smoke occasionally, AQIs 300 to 500. Actually had 4 such days one year, topped out the chart at 499… orange air.

Hoping this year no major fires but we’ve (Spokane) only had about 6.9 inches precipitation all year (about 3 inches below average) so very concerning. High temperature today forecasted 102 today.

I would honestly be leery of buying a home in any western state, province until wildfires are better managed or reduced in number.

And there are the drought conditions… two years ago (?) we were in the most extreme drought catagory for a number of months.

How the PaciNW seems to have changed.

No I’m not a climate alarmist. Just concerned. I am toying with moving back east but am going to give it another couple of years and see how the summers unfold.

Berkshire Hathaway (buffet) just invested a lot ($770 Million, I think) in house builders.

They may be ok.

No, it didn’t “just”… I bought sometime in Q2 which was disclosed now.

Berkshire has investments in so many industries, they know what is hot. They own the largest mobile home builder, a brick manufacturer, a bracket manufacturer that is used in framing, a carpet manufacturer and bought some small stick built home builders starting about 5 years ago, plus they have a large residential real estate agency.

Buffet probably is just reacting to the demand that he sees in his businesses and is trying to get a bigger piece of it. If he sees demand crater, he might dump the home builder stocks like he did airlines when pandemic hit.

Interest received by one party is interest paid by another. There should be no net effect on the ecomony from this aspect of rate hikes as one party’s increased cash flow is matched by a reduction for another party.

That assumes that everyone spends every dollar of cash flow. They don’t. There is a huge segment of America that will spend every dollar they have and every dollar they can borrow, and not on worthwhile expenditures.

The “savers” won’t, so if the reckless borrowers are paying them an extra $50,000 in interest, they will only spend say $10,000 of it. So, in my example, assuming just one borrower and one saver/lender, that is $40,000 less in consumption.

kramartini,

Interest earned on the products listed is mostly paid by the government and by banks, and to a smaller extent by corporations issuing corporate paper. So that’s how that cash gets transferred to consumers.

I also showed interest paid by consumers (green line in the first chart), and it’s a much smaller amount than interest earned.

With respect to banks and corporations, increased interest paid reduces earnings that can be paid to investors via dividends and share buybacks. So no net effect. Interest paid by government increases borrowing that drains money from investors.

LOL. Share buybacks give zero money to consumers. Their intent is to drive up market value of the shares, and if that doesn’t happen, good luck. You will never see a dime arriving from share buybacks into your brokerage account.

You might have a theoretical argument with dividends, but in reality, the amount in dividends paid has been minuscule in recent years, with many companies not paying any dividends at all, not even during the 0% era… Dividend yield for the S&P 500 companies is about 1.6%. And it has not gone up to match the 5% T-bill yields. Companies have not paid out more or less in dividends because of higher rates.

” one party’s increased cash flow is matched by a reduction for another party.”

agree mostly

One never hears about the depressing factor upon the saving consumer when rates are CUT to stimulate.

Rate construction is all about WHO gets to spend the money. For 13 years it was upside down, IMO.

Hayek said that when central planners decide, they intentionally assist one group to the detriment of another. The “assisted” group from 2009 to 2022 is clear, as is the group harmed. Decided not by the market but by committee.

No. This is simply plain wrong in a debt-based fiat money system.

That’s the whole point of it.

You might be right. My understanding is banks create 75% – 80% of money as they make loans. If higher rates slow down loan growth, then it should hurt the real economy, mainly homes and autos.

You can’t quickly improve productivity or workforce once you are at full employment. Politicians who are short term focused know the only quick lever is debt growth. Fed is trying to sand bag growth with the right amount of interest rates to slow lending and real economy.

There are a lot of unknowns created by ZIRP like people being locked in place on housing or political consequences as losers of zirp policy demand redress.

I still think the biggest mistake Fed made is generating the wealth affect. Markets can generate bubbles without being encouraged by Fed policy.

Along with that, they thought asset inflation was not inflation. I think they still make that mental error. They believe 300% asset inflation is OK, so long as it doesn’t appear in CPI.

They care nothing about generational consequences and debt buildup.

The Fed can’t reduce debts to a sustainable level, while artificially propping asset values. The inflated asset prices lead to inflated debts. Even if the Fed brushes aside generational theft, CPI inflation inevitably results.

“My understanding is banks create 75% – 80% of money as they make loans.”

Your understanding is wrong. A bank creates zero money. It cannot create money. It has to borrow to lend. That’s why banks collapse if they cannot borrow anymore. If a bank could create money, it could never collapse (the Fed does that).

The banking system overall creates and destroys money with the ebbs and flows of asset prices (collateral values).

I don’t believe you are correct, but I don’t come to argue. If you want to do an article on the subject I would be interested.

I no longer give a hoot about what people believe banks do. I normally just delete that BS. I’m done wasting my time with this BS. I’ve spent hours and hours in the comments hashing it out. It never ends. People have their beliefs and stick to them. I should have deleted your comment. People can believe whatever they want, but they cannot spread their believes here.

Sorry, but it is long past time that my savings earns a decent return. Remember when banks use to actually be responsible stewards/intermediaries of eCONomic activity and currency…?

Yeah, me neither. F’em.

Can’t wait until they bring back the free toaster!

When and if that happens (again) it might be the time to go long as possible on CDs?

You’ll get a free pack of gum and like it!

Toaster?! What are we made of gold?

Haha

“Can’t wait until they bring back the free toaster!”

Haven’t figured it out yet? Bank clients ARE the ‘free toaster’. For them, that is.

…toaster or just toast?

may we all find a better day.

I seem to remember reading somewhere that the free toasters and such thing were offered at a time when interest offered by banks to gain customers was limited by law to low rates. Not sure, but I still have a blender I got to open an account a very long time ago.

Nice to see rates go up, I have all the appliances I need.

My view is that most small and regional banks would be belly-up if not for the Bank Term Funding Program. It is currently scheduled to end on March 11, 2024. Likely it will be renewed. I would like to see a list of the banks who have been using it and how much they have been getting out of it.

“…most small and regional banks would be belly-up if not for the Bank Term Funding Program.”

Nah. You misunderstand the program. It’s a cheaper version of the Discount Window.

If the BTFP ends, those banks can borrow at the discount window, but the rate will be higher (5.25% currently), and variable, meaning that the next rate hike will increase the rate of existing advances, whereas the BTFP keeps the rate fixed for the term of the loan, and the rate is lower to begin with. In addition, collateral requirements are easier for the BTFP. It’s just a lot cheaper for banks to use the BTFP than the Discount Window.

In addition, the $105 billion borrowed at the BTFP is minuscule for the $23 trillion US banking sector.

Okay, most small and regional banks would be belly-up if not for the Bank Term Funding Program and the Discount Window.

If it is so miniscule, why have it?

Hey Wolf. Speaking of interest, please remind us exactly where the interest paid to the Fed on the debt actually goes again.

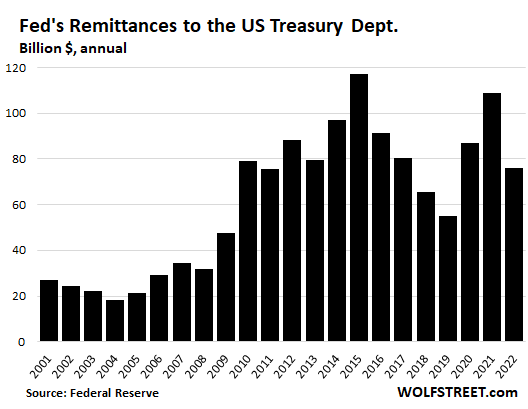

More than 94% of the interest paid on US Treasuries and other assets owned by the Federal Reserve goes straight back to the US Treasury as the Federal Reserve has ALWAYS rebated around 94% of its profits to the US Treasury ever since its inception.

When the Fed is making money (through Aug 2022), that interest was remitted back to the US Treasury.

Since the Fed started losing money (since Sep 2022), it has been paying out more in interest than it earns, and it has a deficit. So nothing goes back to the US Treasury. The entities that it pays this interest to are the banks and money market funds. This is where you can benefit from the Fed’s policies.

Here is my annual update about the Fed’s remittances to the US Treasury Dept:

https://wolfstreet.com/2023/01/13/despite-losses-since-september-the-fed-still-made-a-profit-for-the-whole-year-2022-remitted-76-billion-to-us-treasury-dept/

It includes this chart, which shows the remittances by the Fed to the US Treasury:

Will need to update the chart for 2023

Yes, on around Jan 7, 2024, when the Fed releases the annual financial numbers. The annual amount will be $0 (not negative), I already know that.

The Fed is already $70 billion in the hole so far. But the chart reflects remittances of profits to the Treasury. No profit, no remittance. The remittances will be $0 for 2023 and the next few years. It will be a very boring chart. Because the Fed parks the losses on its balance sheet, and when it starts making profits again, it will fill those holes on its balance sheet first before it remits anything.

Thanks Wolf, I knew the banks were doing well as a result, but didn’t realize that the interest payments also benefited money market funds.

With no mortgage to pay off, I am one of those that are salivating over the higher interest rates. I am now getting another income stream that I can use to spend on necessities. Keep up the good work J Powell. The higher the better.

I am ok with this thesis: “Lots of them make a lot more money on T-bills, CDs, money-market funds.” as a partial explanation for ‘drunken sailor’ spending. I would add that many of these ‘drunken sailors’ have never been through a bad recessionary period so they don’t understand the value of money well enough .

Further, I think those that are paying 5% for the use of other people’s money

are pretty certain that they can get 8-9% with it.

Was listening to Bill Gross talk about one of his MLPs that he gets a tax deferred 8-1/2% from. He said that this works out to more like 11-1/2% when his taxes are considered.

The real value of money is considerably more than 5% but you have to study and work at it to get it.

Don’t fight the Fed we are reminded, but here we are in an epic world war where there’s an army of people that have been converted to the religions of FOMO, YOLO, BTFD, TINA and of course ZIRP.

Those people fighting Fed rate hikes, ignoring potential consequences, are betting on speculative excess, while an army of investors, or specifically savers, believe in interest income.

Both sides eventually lose, as the Fed achieves its strategic goals of manipulating economic policy.

There will be a time, probably next year, when these glorious money market rates crash lower, in unison with every asset value. All the boats are rising today from the tsunami pushing cash into the economy, but as that great wave crashes the other direction, the naked warriors will be scattered everywhere.

I still contend, that the increase in monthly income is chicken feed for most people, and as usual, in this casino, circus world, the rich are getting far richer, while the vast majority of people are barely surviving.

I think if you are a relative value long term investor money markets are paying you a fair historical rate which is a little higher than inflation. Long term treasuries are not paying you for taking duration risk. Most stocks are at extreme valuations on many measures especially price to sales.

Isn’t this a demographics issue? Millennials and younger (under 40) are not the ones collecting interest income. Is this how it has always been? Seems a little more dramatic these days.

The ZIRP and bottom mortgage rates were a boon for the retiring generation to lock in low rates. I guess one silver lining is its less of a tax burden on the working-class, right?

There are definitely interesting demographics at play here.

Zirp, allowed Boomers to initially obtain homes at lower cost, lower mortgage rates, then in stage two, see those homes doubling in value, while their excess income goes into money markets paying much higher rates.

That trifecta has shut down the existing home market, allowing new homes to be bought by Millennials who probably don’t have stable and reasonable cash flow, to support their new lifestyle. As a group, this new round of buyers are overwhelmingly over leveraged, probably using financial innovations to borrow against collateral from a stock portfolio. Needless to say, if equities eventually sink, we’ll see cascading collateral dynamics.

In addition, within that witches brew, there’s a boatload of highly leveraged Airbnb type home investors that are being impacted by higher borrowing rates and cap rates, etc., all that inventory is increasingly dangerous.

Meanwhile, the banks are watching their long treasures decrease in value along with their commercial real estate portfolios.

With all that crap, it’s easy to feel good about a money market chugging along at 5%.

Add in geopolitical craziness, deficits, election cycle… and, what’s truly amazing is the amount of people that believe the Fed will immediately go into QE at the first whiff of a crash. I think that’s an insane mindset that isn’t going to happen.

I wonder if any data crunchers could figure out if we would be better off if market set rates and not the Fed.

I guess I missed the *benefit* of ZIRP allowing me to get a house cheaper…. as whatever benefit I gained, I lost from ZIRP keeping the returns on my savings low. I haven’t had a mortgage since the 80’s so there was no benefit to me as one of the hated “boomers”.

And those boomers that were invested in the market when the GFC hit, in many cases, have yet to fully recover from that event. Those in MM funds that limited withdrawals also took it in the shorts. (Note to those stuffing those accounts because they’re “easy money”)

Just because this stuff is in YOUR face at this particular moment doesn’t mean that others didn’t get screwed in the past.

People talk on here like housing is fungible… and every Boomer bought new homes, moved, refinanced, has unaccounted for income that can be used to fund the lifestyles of the rich and famous at the expense of younger people.

It seems – at least in my circle – that the Xers and the Millennials are doing okay. My daughter just got a large raise (30%), has a few hundred grand put aside, and zero debt. Other couples I know are making low six figure incomes and own homes, taking spa vacations, driving Tesla’s and BMW’s. I have a friend who just switched jobs and is making $700K plus performance bonuses and his wife makes $200K. He’s 44. Another just took a job in Tampa (moved from Atlanta). He makes @ $500K. Another is a big shot for Subaru and bought a beach house in Margate, NJ for $1M+ in addition to the $1M+ house he already had. He’s 43. My son and DIL making in the mid-upper six figures and planning to blow $1M on a home renovation (it would make more sense to move but…. ).

So, IMHO, there are as many well-to-do younger people as there are well-to-do geezers. And the geezers getting thrown out of their rentals by Tarek El Mousa (who’s 42) likely have equivalency in the younger generations. That’s what happens in a meritocracy. Some do better than others.

In many cases, it’s expectations. Most people have eyes bigger than their wallets. I, for some reason, never got caught up in that nonsense. Yes, we have nice things and have had a knack for picking the next “up and coming” area to buy a worn out house in and restore it, but we never attempted to keep up with the Jones’ as that was never that important for us to gamble our future on it.

When I am derided for being a ‘Boomer’ by a younger person I ask them what they have done. Then I tell them we fought the Vietnam War (from both sides) and they are not drafted.

Today’s sub 40s will fight but it will be when they are old.

El Katz, I’ve read your comments for a long time now. You’ve told us (multiple times) how much your children and others in your circle of contacts earn. You may not realize it but your comments come across at best as boastful and at worst as obnoxious. Just something to think about.

Proud dad?

I also would like to see gas prices go much higher. I am getting sick of all this post pandemic traffic on the road. I almost long for the days of the pandemic when we had the roads all to ourselves.

Drive less. I mean…where do you have be so badly that you need to subject yourself to freeway traffic jams? Order online, use facetime/microsoft teams/google chat ect…. It’s 2023; no one has to leave the house.

Ha! Those complaining about traffic are typically and ironically a contributor of “the traffic”

Ninety percent of the inflation is coming from the housing sector. The Fed raising interest rates have aggravated that problem. Poor policy choice, in other words. Cities that offer affordable housing are not suffering from the same inflation rates.

Thanks for this Wolf, great stuff, you can’t get this type of information, presented so clearly, anywhere else on the internet.

So if people’s ability to spend isn’t impacted by rising rates, how is it we are expecting rates to flow through to slow down inflation?

Lower commercial borrowing?, greater defaults from debtors slowing down bank lending, government cutting back spending to manage interest payments (haven’t seen any sign of that so far)?, lower residential construction because nobody can afford to buy new homes at current interest rates?

As always, I guess time will tell. Given the usual lags in monetary policy, whatever impact we are expecting should be starting to show up in the data relatively soon, somewhere, right?

“Treasury bills up to six month all yield over 5.5%.”

The investment rate is close to that, but the high rate is lower, closer to 5.2-5.3% and we only get the high rate on T-bills. Unless you reinvest same term for a year and the coupon compounds, I don’t see rates that high yet.

Am I missing something here?

“Am I missing something here?”

Yes, look at the market yields.

To give you a real-world example: In late July, I bought 1-year Treasuries at auction and paid $947.80 for each $1,000 in securities. Next year at this time, I will be paid $1,000 for each, for an interest income of $52.20, on a $947.80 investment. So this is a return on investment of 5.5%.

But it’s not quite that simple because the time period doesn’t match 365 days, so the actual 365-day yield is slightly different, but it’s close. And with a coupon security, I would have gotten one interest payment after six months and the second after one year, so this changes the comparative yield as well.

Market yield at the time I bought it was about 5.4%.

Thanks, understood. Shorter term T-bills less than one year are a bit confusing because the rates are always annualized. I was off a bit in my own calculations.

If you buy at auction and hold to maturity, you get the investment rate on T-bills. I just bought a six month T-bill and got an investment rate of 5.53 percent. I did the math and that is the APY, e.g., the APY equivalent on a six month CD.

My understanding, and it could be incorrect, is that the investment rate represents the rate of return if the amount invested were to be held for one full year with the coupon compounded. Not something that occurs with a short-term bill such as a 4 or 8 week term. The “investment rate” is provided to allow a comparison with other returns that are based on APY.

No compounding on T-bills. The investment rate is provided for all T-bills, 4 week to one year. As you say, the “investment rate” is provided to allow a comparison with other returns that are based on APY.

I had thought the economy would sour much sooner than it did, but what I was not accounting for is the interest income increase that comes with higher interest rates.

So where does this money come from? Some of it is paid by financial institutions and higher interest loans are created, but alot of it is interest paid by the federal government for the massive overspending. We are now at 1 trillion in annual interest payments from the Treasury. I have not seen the total when interest payments from state and local entities are also included.

So while the Fed is pulling about 1 trillion out of financial markets over the course of a year with QT, the Treasury is offsetttng this by paying out all that interest. But what makes this stimulative is that taxpayers are not required to increase their taxes to pay for that extra interest, it goes into increasing the already enormous debt.

When we look back at the last time the Federal Reserve tried to reduce the balance sheet we see that it rather quickly started to hit the markets, but there was not as much interest being paid out to offset it, so i think it will take longer for the markets to get really hit hard this time around.

Any economist who parrots the idea that deficits dont matter is an idiot. The only question is the timeframe on which deficits do matter.

Borrowing from the future continues unabated.

When are we getting a wealth disparity update?

YES! I have been meaning to mention that.

Reflecting the impact of increased interest income, a robust labor market, and a generally okay economy, retail sales MoM were up .7% (expected .4%) and retail sales excluding gas and auto were up 1.0% (expected .1%). It would be nice to get these data by age group to see how much boomers have increased spending.

The average federal fund rate from 1971 to 2022 was about 5%, and the average rate of a 30 year fixed rate mortgage 1971 to 2022 was about 7%. We are very close to these averages now. Seems unlikely the economy will be slowing much.

Sorry, Mr. Powell. Higher, longer.

Hi,

How can the personal income side only gone from $1.6 trillion(2020) to $1.8 trillion (2023) as interest rates on MMFs, CD’s, T-Bills, etc. have gone from basically 0% to 4%-5%?

Thanks,

Here is a portion of the answers:

There are about $55 trillion in interest-earning US securities, many of them with long maturities. For example, 10-year Treasury notes that were bought in mid-2020 will pay a coupon interest of 0.5% until 2030.

In addition, there are $17 trillion in deposits out there, and a big portion of them still pay little or no interest. The average cost of funding for the big banks is around 2%.

It’s the short-term T-bills that went up quickly and a lot. And some CDs followed. Money markets followed the T-bills. And that’s not a big portion.

So true. My wife and I are making 22x on our cash in new treasuries compared to early last year. However, our 401ks are in Stable Funds that are fixed income based with varying maturities up to 3 years. That’s making only 2.8% currently, but increases slightly each time something matures and is reinvested at higher rates by the fund.

As such, I’d expect interest income in Wolf’s graph to keep rising even if the fed simply sticks with “higher for longer” w/o any further increases.

Feels good to finally be making some $$.

Ben retired over 10 years and just told my son that my savings increased three thousand last month. He looked dumbfounded.

The interest income is about 1.8T or about 5K per man/woman/child in the US. For a family of 4, that is about 20K/yr.

How many here collecting this kind of interest income? I would say the median for this “interest income” per family is like $500/yr. It really just the income for the top 1% or 10%.

I know I am speaking to the choir, but the lost interest on savings cost many half of their wealth. My elderly mother left money in a CD account for those 13 years, I did the math and her account would have doubled the funds if they had not repressed rates… and be earning double the interest income today.

The wealth was transferred to those who refinanced their homes at 3%.

Refinancers still have their lower payments and retirees now have interest… so it is those who hold the debt that are in trouble today… banks and passive bond index investors.

Maybe a dumb question, but… if the US consumer (in aggregate) earns that much more interest than they pay, then who is paying out more interest than they earn?

Also, very minor typo: below the first graph, “renters of choice” is missing its open-quote.

The higher short-term interest is paid by the US government (T-bills), by banks (savings products), and by corporations that issue short-term corporate paper. And also by the Fed that pays over 5% on reserves (to banks) and RRPs (to money market funds).