But for Treasury, the gravy train has now ended: Fed released preliminary info on interest income, interest expense, other expenses, profit, and dividends.

By Wolf Richter for WOLF STREET.

The Federal Reserve released unaudited preliminary financial information for 2022 today (audited financial statements will be released in a few months). And we knew what would happen, we discussed this a few times before: In September 2022, the Fed started losing money on a weekly basis. In the four months from September through December 31, the Fed lost $18.8 billion, the Fed reported today.

But its net income for the first eight months of the year amounted to $78 billion, far bigger than the loss of the last four months in the year, and for the year as a whole, it had a net income of $58.4 billion (-46% year-over-year).

In 2022, the Fed hiked all its policy rates by 425 basis points, including the interest rates it pays the banks on their reserve balances and the interest rate it pays its counterparties of the overnight reverse repurchase operations. And that’s where the losses are coming from.

The problem that has arisen is that the interest it pays on about $5.2 trillion in combined reserves and RRPs started to exceed the interest it receives from its securities that it bought when interest rates were far lower, and which QT has reduced from nearly $9 trillion at the peak in April, to $8.5 trillion now.

The losses don’t matter to the Fed. The Fed creates its own money, and so it cannot become insolvent. And its capital, which is capped by Congress, is not impacted by the losses because the Fed carries the losses as a “deferred asset” on its balance sheet, rather than taking the losses against capital. You can see this on the balance sheet: Since the losses started on a weekly basis, the Fed’s capital has remained unchanged at $41.8 billion.

When the Fed starts making money again in the future – after QT has sufficiently reduced the reserves and RRPs, which reduces interest expenses – its net income will then be taken against that deferred asset until the deferred asset is extinguished.

The losses do matter to the Treasury Department – which is no longer getting the weekly remittances from the Fed.

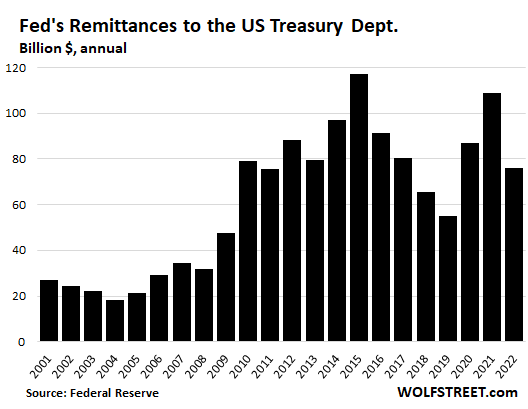

Every week, the Fed has to remit its estimated income to the Treasury department, and those remittances stopped in September when the Fed started losing money. The remittances won’t get going again until the deferred asset has been fully wiped out by future net income. So it could be years before the Treasury gets any remittances again.

During the first eight months of 2022, until the losses started in September, the Fed remitted $76 billion to the Treasury Department. However, the Treasury Department isn’t sending back any money to compensate the Fed for the losses; these remittances are a one-way street, from the Fed to the Treasury Department.

Instead of having to pay income taxes, the Fed sends all of its income to the Treasury Department. Since 2001, the Fed has remitted $1.36 trillion to the Treasury Department. In 2022, it remitted $76 billion.

In 2023, given the expected losses and the trend since September, remittances will likely be zero.

Interest income surged by 39% to $170 billion in 2022 on its holdings of securities, mostly Treasury securities and MBS, up from $122 billion in 2021.

In addition, the Fed made some small amounts – small by Fed standards – including $500 million in fees from services, mostly paid by the banks, and $108 million in net income from its pandemic era emergency programs.

But interest expenses exploded by a factor of 19 to $102.4 billion in 2022, from $5.7 billion in 2021. This is the amount it paid on reserves and RRPs.

In addition, the Fed had other expenses – bringing its total expenses to $112 billion:

- $5.6 billion in operating expenses of the 12 regional Federal Reserve Banks.

- $1.8 billion in mark-to-market losses on foreign-currency denominated investments.

- $1 billion in costs related to producing, issuing, and retiring USD currency (the paper dollars, aka Federal Reserve Notes).

- $1 billion in costs of the Board of Governors (the government agency).

- $700 million to fund the Consumer Financial Protection Bureau.

The Fed paid $1.2 billion in statutory dividends in 2022 to the shareholders of the 12 regional Federal Reserve Banks. These 12 FRBs include the New York Fed, the St. Louis Fed, the San Francisco Fed, the Dallas Fed, etc. Their shareholders are the largest financial firms in their districts.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Can I buy these shares too? Are they audited? GAAP, SEC and fraud regulations apply?

Or am I not in the club?

“The Fed paid $1.2 billion in statutory dividends in 2022 to the shareholders of the 12 regional Federal Reserve Banks. These 12 FRBs include the New York Fed, the St. Louis Fed, the San Francisco Fed, the Dallas Fed, etc. Their shareholders are the largest financial firms in their districts.”

You and me, both, we’re not in the club. There are lots of clubs we’re not in, according to sources familiar with the matter.

Yes, they are the Trillion dollar clubs

name must be Rothschild, J.P. Morgan

otherwise don’t bother us

Fiscaldata shows we’re at $210B in interest expense for the 1st Qtr of 2023 and $421B budget deficit. Now that’s a great start to the year. And the Treasury’s daily statement says we’re down to our last $310B. Yellen says “extraordinary measures” are coming. A debt limit fight (which I know you think is a farce) is looming. Lot’s of GOP House investigations are spinning up.

2023 is shaping up to be a banner year!

Fed is a complete failure by following metrics:

1. Inflation remains way over Fed’s target despite BLS health insurance adjustments.

2. Housing remains unaffordable.

3. Even worthless crypto companies have not gone bankrupt yet!

4. Productivity in units in US keeps decreasing.

5. Gold and commodities keep rising at worst possible time: High inflation with negative real rates and reduction in both stocks and bonds.

They should have raised 75 last meeting. And again this meeting. Jerome soiled himself again. This guy is a complete and total failure. Should have been fired long, long ago.

MMT or bust, baby! He’s now on the 25-bp trajectory up to about 5.25% before he pauses. The 30YFRM is about to drop below 6%, meaning housing is going to start to stabilize by April.

2023 is going to be mild. 2024 or 2025 is when the crap really starts to hit the fan. I fully expect by 2025, the SSTF Annual Report will show the SSTF going red four years earlier, 2030, that anticipated.

I second that observation

Yes but the military is able to get funded at a real growth rate while real wages are down 21 months in a row.

Welfare state is able to keep growing with 100 million people on Medicaid sometime in 2023.

The Fed has fed the resources through DC and if you work for a living they have been your enemy with $3 eggs, $3 gas and $45,000 cars.

Good Point OS, re military funding keep track with realized inflation in stead of the BS from the BLS, etalia GUV MINT.

When and IF WE, in this case WE THE WORKERS of the entire World Who actually make stuff for our species to continue to IMPROVE actually are able to benefit directly and entirely for OUR WORK,,, then and only then will our world come to balance…

Until then, no matter what massive resources the oligarchy brings to this battle, they, the oligarch they, will lose eventually.

This balance will occur when the funding for theoretical physics and the engineering following that physics matures sufficiently to harvest all solar, tidal (lunar), and wind energies to make TONS and tons and tons more electricity and other, coming, transferable ”energy” SO abundant to all species as to equate to the peace and prosperity and probably personal problems at a balance.

Balance folks, balance!!!

IF, for some reason, you have not balanced your portfolio NOW,,, suggest you consider doing so ASAP, or, whenever,,,

Good Luck and may the Great Spirits bless your every effort.

More people on Medicaid than Medicare now. You all got your socialized medicine. Now you have to pay for it.

Leo:

You forgot to include in your very good list ( IMHO ) the very stone cold FACT that the value of USD has gone down 99% since the FRB was started by the oligarchy of the world to make sure THEY, in this case the oligarchs They, were able to screw WE the PEEDONs of USA…

Hasn’t stopped even one bit since then.

Bend over and get ready for another such ”magnanimous” gesture from oligarchy, ( AKA owners — of almost everything.)

Not really much different between early ” middle ages”, 800-1100 current time scale, and now IMHO, except for the music now available to WE the PEEDONs,,, which, for that alone,,, seems as though there might be SOME progress being made.

” middle ages”, 800-1100 current time scale, and now,,, should read:

, ( 800-1100 current time scale, AKA: CE, AD, etc.,)

One more reminder, as, ( ” my time is growing short.” )

Oligarchs of many centuries past, likely at least 1,000 years, maybe double that and more in some places, ARE going to get their investments back,,, along with very possibly their entire expectations.

That would certainly include IMHO almost the entire SW portion of current USA ”lower 50”

Can’t say as I blame them at all for wanting back what they spent SO many gazillions to improve.

Keep in mind these old and older oligarchy folks think in terms of thousands of years in general, and only think down to centuries when they must to do to safe guard their wealth.

Supposedly shares of the SNB can be bought, in Switzerland. But it’s not like other shares.

And don’t forget these:

* $5.6 billion in operating expenses of the 12 regional Federal Reserve Banks.

* $1 billion in costs related to producing, issuing, and retiring USD currency (the paper dollars, aka Federal Reserve Notes).

* $1 billion in costs of the Board of Governors (the government agency).

I’m sure Mr. Musk see these numbers and thinks: “I can reduce these by 65%. No problem”

But where would the savings go? Oh yeah…

So not much incentive to tighten operations, is there? I especially like the $1 billion to burn old money. Somehow fitting.

There’s to much $ in crime these days.

Anyone notice old fashioned “stick em up” bank teller crimes are a thing of the past?

The ultra rich are the new crime wave.

I don’t want to be part of that club.

Wait, what? They can just make up money out of thin air. And they pay dividends? Didn”t Bernie Madoff try this already?

But when crypto does it, we should all know better.

I understand everything you say about the Federal Reserve and how losses dont matter. I get it. But at the same time, I think it is emblematic of the core moral hazard that is at the very heart of our economy.

Millions of jobs shipped overseas to low wage countries has stripped our country of productivity in many sectors. Massive consolidation of industries and government policies that give other companies massive windfalls at the expense of the consumer/taxpayer (I’m looking at you healthcare industry). And all of this largesse is piled into government debt that future generations will have to pay. Of course, we have a higher education system that has taught these same students that debt simply doesnt matter, so look the other way kids, nothing to see here!

No one will pay this debt. Our children will not be born int slavery to serve thes banks as their masters.

This defunct system will crumble or will be taken down and a new better one will be formed. This has happened many times in human history.

true. why do you think Europe has such good infrastructure, quality of life and food supply today? because it defaulted countless times in the past. much pain to get to the present moment. we need to take a historical view. defaults bring progress but not for an individual lifetime

Yes central banks can’t go bankrupt, but they are established by governments and can totally debase the currency if they screw up, bankrupting many citizens who expected their currency to be able to pay for their future needs.

Mild inflation allows people to make choices in how they are going to lower their standard of living, but double digit inflation is a destroyer of people’s lives if it hangs around a few years.

We could always go off the ROTHSCHILD DOLLAR,but look where it got RUSSIA . Be careful what we wish for

$5.6 billion in operating expenses of the 12 regional Federal Reserve Banks. What are they doing that costs $5.6 billion?!

They’re managing the interior plumbing of the US banking system. They have lots of research functions and publish lots of data about their districts and nationally. The New York Fed manages a portfolio of $8.5 trillion. etc. etc.

Operating costs of $5.6 billion … that sounds like a lot, but there are lots of small-ish US companies that have that kind of costs. The big companies have 10x to 40x the costs. Alphabet had $200 billion in costs in 2021.

Sure, but Alphabet provides value to the average Joe at nearly no cost. All the Fed is doing has done is make inflation worse by excessive yield curve manipulation & excessive asset purchases. The Fed created the current stock market & housing asset bubbles.

Alphabet has set out to destroy publishers and the free-internet model with its monopolistic control of much of the internet advertising infrastructure. It’s is currently being sued for that and a bunch of other stuff by the government and the biggest publishers in the world, including Newscorp (includes the WSJ). It needs to be broken up into lots of little pieces. Terrible example you picked there.

And what good did that $5.6B expenditure get taxpayers, besides harmful policies that produced three bubbles in 25 years, highest wealth concentration ever, generational favoritism, high debt, low productivity, pension crisis, and moral hazard up the ying-yang?

I have a feeling there is a lot of useless fat within central banks that cannot be justified based on policy results.

Wait a minute… the 12 FRBs are privately held banks. The taxpayer doesn’t pay for any of it. The Federal Reserve System is self-funded. In fact, since 2002, the Fed sent $1.3 trillion TO the taxpayer. So don’t complain.

Untimely bank bale out time arrives.

Yes, the public certainly pays for the Feds operations and mistakes through higher inflation. Duh!

The US Govt Interest Payment Chart has a lot of people much smarter than I thinking the Fed can’t keep 4% or higher rates for too long. Hundreds of billions of interest payments that Congress needs to buy off voters, so question remains is how long can it last??? And thus one reason the markets are playing chicken with the Fed as the interest payments go exponential quickly at 4% or higher rates, as seen in the chart below:

US Govt Interest Rate Bill History and future projection Chart:

https://images.mauldineconomics.com/uploads/newsletters/Image_5_20230113_TFTF.png

Simply put, the Fed is going to have a lot of pressure from Congress, Wall Street, Corporate America, to reduce interest expenses.

How brave is Jay Powell??? Personally I think he keeps “higher for longer” interest rates until something big breaks, then he reverses course. Such an event could be months or years from now, only time will tell…

Yort,

That’s all BS. You need to look at government tax revenues, which spiked much more than interest expense: In Q3:

Tax receipts: +21% year-over-year, +52% from two years ago.

Interest payment: +24% year-over-year, +42% from two years ago.

In other words, the BURDEN of interest payments has dropped over those two years because revenues have spiked more than interest expense. This inflation is the best thing that ever happened to government debt (that’s why governments like inflation, duh).

People who post charts like Maudlin did are either totally ignorant or they’re SELLING stuff. Mauldin is selling newsletters, and they want to scare you with this braindead BS, and they will lie to you to sell newsletters. Don’t fall for it.

This chart goes over the same time frame as Mauldin’s chart of interest expense that you linked:

What we will see are some epic fiscal policy battles in Congress. The speaker fight set up a very interesting house and committee composition that should cause fireworks. To be honest I am looking forward to the show.

Wolf, what a coincidence, was just looking at the tax receipts chart this morning… What drove the most recent leg up? Was personal investment income realty THAT good over the period? Or was it something else?

You know who also lost money in 2022? ARK Innovation ETF (ARKK) down ~60%.

And yet my financial news feed somehow still thinks I give a %$#@ what Cathie Wood has to say about the Fed.

Cathie Woodshed is the epitome of failing up.

So many of these public financial guru figures have elements in common. Elizabeth Holmes, Sam Bankman-Fried. There must be an image, like a novelty haircut. A special sound of the voice. A ridiculously optimistic pitch. Then, once the cash has been harvested, it all heads for zero.

So much of the financial industry are just asset gathers to collect the 1% skim every year. Over a lifetime they have half your money even if they match the sp500 which 80% do not.

“Instead of having to pay income taxes, the Fed sends all of its income to the Treasury Department. Since 2021, the Fed has remitted $1.36 trillion to the Treasury Department. In 2022, it remitted $76 billion.”

I believe the 2021 => 2001

Thank you for the update.

Yes, those dang decades. Thanks

The stock markets didn’t care about Jamie Dimond. The weekly Dow : in order to move up there must be a close above Mar 28 high. Breaching or closing above Dec 12 high isn’t good enough.

If the Dow fail, it might start a downturn, possibly a second rd trip to Feb 2020 high.

I’m guessing you’re trying to speak some technical analysis, which I don’t follow. However, I did laugh today at close when the S&P500 closed at 3,999. Seems so rigged to me at least. Same when it reversed hard at 3,500 last year. Shaking my head…

I see Yellen is back at it about raising the debt limit again…she probably wishes the Fed was turning a profit right about now.

Yes, those big round numbers (BTC too) strongly suggest there is something other than fundamentals at work: psychology alongside too much loose cash looking for a place to go. Which sort of backs the technical analysis approach if for no other reason than, finding patterns in the above, and out-guessing it. Fundamentals may fluctuate randomly, crowd psychology less so.

But I don’t get ME’s quirky syntax. Is that like a novelty haircut? There obviously is enough cerebral wattage to get the syntax right.

Flip, I know u don’t get it, but u are not the target of my comments.

Yep. Heard Jim Rogers and Marc Faber both say they had to learn the lesson that the market can take your money even if you are right on the fundamentals of an investment.

Buffet gets around this by saying his holding period is forever and the market will get to the correct value at some point in time.

Options. Options are at work, and people gravitate to numbers like that when they sell or buy them. It’s nothing sinister.

plp:

Crowd ”psychology, AKA MOB psychology” does clearly fluctuate even MORE in my clear experience of local and tragic events per earthquakes, mud slides, many floods and hurricanes over the last 70+ years

No matter ”the plan” all real warriors agree with boxer Tyson” Every one has a plan until the first (enemy) blow lands.”

VERY clear lesson in WW2 and boxing..

Apparently forgotten by modern military, so far to the great detriment of Russia fighting the last war, as have SO many since Alexander.

Crypto going parabolic. It may be crap but good times seem to be back. The trend it your friend.

BBBY and CVNA went parabolic a LOT more than cryptos and both face bankruptcy. BBBY +230% in two days, before giving up some. CVNA +78% in 2 days before giving up some. Those are my favorite “bankruptcy stocks.”

But the trend wipes you out: BBBY dropped 35% today in the last 5 hours, giving up half of the 230% gain in a few hours. Monday morning, you wake up and the other half is gone. Easy come easy go. As far as I’m concerned, people just need to have fun and get this out of their system until all their money is gone.

The only you should have added /s (sarcasm)

This is horrible this castrations of hard working honest plebs.

Have mercy!

These plebs are driven by something for nothing: fast money. Greed. Overconfidence. Let’s not declare them saints too readily. Nothing forces them to punt their hard-earned money on get-rich-quick schemes, but themselves.

I see a dominant theme nowadays (across any political mythologizing persuasion) of shifting responsibility from the self, to blaming someone else for outcomes in which one actually had a heavy hand, blaming the evil carny hucksters, evil corporations, evil government (especially evil Fed), etc.

Yep, phleep.

Crop failures? “Witchcraft”!

Still-birth? “Witchcraft”!

Ignorance isn’t bliss. It’s lethal.

phleep – one should practice extreme caution when tasting the liquor of victimhood, the inclination to guzzle that bottle further is its sinister feature, not its bug (like all mind-altering substances…).

may we all find a better day.

I read somewhere today that this is the biggest bear market rally in history. I simply call it “way too f***ing much speculative activity due to money printing.” That’s what the FED is missing. They JUST.DON’T.GET.IT. I’m looking for the DOW to set new all-time highs very soon – the exact opposite of the massive recession the pivot people and alarmists have been warning of. Because again, there is just too much printed money out there. It has not even come close to being exhausted. Jerome Powell must have failed math.

I think in a true bottom, about 80% of people capitulate and say the stock market is a racket. A lot of marriages fail as the financial “genius” becomes the idiot that gambled away our future.

Ah, that’s what happened to Tom and Giselle.

Try zooming out on the charts if you want to see the actual trend…it’s not up.

LOL. All this stuff is a horror show if you look at a 1 year chart.

Totally. These moves are incredible and frustrating to watch. I was shocked when I saw BBBY yesterday. FOMO is a bitch. Like anyone else, I’d love to make 300% in 2 days.

I really hope Powell has the cajones to stand up to these market vigilantes.

I like “Buffet’s” take that you should be professional about it and treat buying a stock like buying a business. Do a lot of homework on the company and industry otherwise just buy an index. If we like to gamble, do it somewhere else than the stock market.

FED bought Trillion of treasury from government and these products pay interest. At the end when there is a PROFIT, FED remit the profit to US Treasury. Real magic game of create something from nothing.

Just wondering if all other major centre banks around the world play the same game or is it only the privilege for the FED only because of USD status?

It’s quite simple: The Fed holds $5.5 trillion in Treasuries and $2.6 trillion in MBS, and earns $170 billion in interest on them.

But wait… the Government pays all holders of Treasury securities, such as me and the Fed, interest on our holdings. This is interest income for us, the holders. The government might pay the Fed $110 billion in interest on its $5.5 trillion in Treasury securities. I get somewhat less because I don’t quite hold $5.5 trillion in Treasuries. But everyone who holds Treasuries gets this interest from the government. But the Fed then PAYS THIS INTEREST BACK TO THE GOVERNMENT (the taxpayers), plus a bunch more. So on the Treasury securities the Fed holds, the government (taxpayer) essentially doesn’t pay interest because it gets the interest back via these remittances.

That’s how it has been through 2022. In 2023, the government might not get its interest money back because the Fed will lose money.

All major central banks distribute their gains back to the government (taxpayers). In Switzerland, the SNB distributes it to various public entities at the national level and to the Cantons.

I would be interested to hear anyone’s opinion on gold and silver at this point, if we truly do not believe in this system is it not a decent idea to hold these commodities or are they still too manipulated to be worth it at these prices now?

Ownership of PMs is too big of a subject to try addressing in a short comment here. I have been studying it since I retired 23 years ago and still am scratching my head whether it was better to get in or stay out. Price of Gold hit a peak of 800 in 1980, was around 250 in 2000, now it’s at 1900+/-. What will it be in 2046? If you can figure that out or make a good guess, you will have your answer.

There is so much quirky psychology in it, IMO. My fear is that stock markets have become like that too: too much loose money and weird ideas may unhinge it from fundamentals for longer than an “investor” can stay solvent. Then it (whichever asset) takes on a casino quality, and the surest profiters are those running the plumbing and extracting fees. Like a sports book, everybody else is just guessing and providing those fees. Hopefully in stocks, these are enough rises innovation and rises in productivity to sensibly raise assets prices, outside of financial manipulation.

But now that crypto has taken a belly flop, maybe (at least for awhile) precious metals resume their fad status?

Physical gold does not have to be complicated. Once you are a net saver you purchase a little bit regularly over a 30-40 year period. Keep it safe and be happy if you never need it. In an unstable system it offers stability that acts as an insurance policy. Sometime in the future when gold gets above $2100, it won’t matter how much you paid per ounce, just how many ounces you accumulated during your working career.

By this, “Sometime in the future when gold gets above $2100, it won’t matter how much you paid per ounce, just how many ounces you accumulated during your working career.” Do you mean similar to when FDR confiscated ALL the gold of WE the PEEDONs?????

One can hope and suppose that does not happen again, eh?

BTW, Love the Flashman series, especially his moves to get out from Afghanistan, eh???

VintageVNvet, I can’t help but think if G W Bush had read Flashman, maybe USA wouldn’t have moved into Afghanistan. The Flashman series is great and completely unique. A gut splitter no matter how many times I have read them.

I don’t think anyone can accurately price gold. Cost to mine an ounce is in the $1200 range last I checked. But minors have to pay taxes so in reality it’s probably higher around $1600 for them to make a decent return.

I think it is about protecting individual from complete system failure which has happened a lot in history.

It can be looked at as a stabilizer for a portfolio if small percentage is added because gold is not very correlated to other assets.

It’s easy to get frustrated owning precious metals because they can under perform for many, many years.

I had a chance to buy some from a family member who needed cash and I took it. About 2.5% of my portfolio.

Jim Rogers said he always took gold coins when he traveled around the world because they were universally accepted as payment if you needed to bribe someone in a corrupt country if you got in trouble.

Why would minors have to pay taxes, aren’t you exempt till you’re an adult?

FD: i’m a myrrh man

Actually gold is very much correlated to other assets classes.

The moment you put in anything to asset it becomes correlated.

Retired gold exploration geologist here and I have commented on PM’s before but it may be worth repeating a few key points. (source, World Gold Council):

– In 2014 India and China alone accounted for 54% of all gold demand. Both have a deep and growing cultural affinity for gold. Dowry gold demand in India is facing a huge demographic surge from a young, of marriage age population.

– In 2014 10.4% of all gold demand was for high tech applications.

– Gold is a key and essential asset to technology and gold unlike silver and copper, does not oxidize (react, tarnish or corrode) and therefor it is critical to vital applications in the high tech, space, communications, medical, industrial and military fields.

– For important electrical connections that cannot fail, gold is used, for example in ABS brakes, air bags, car keys, cell phones, smoke detectors, pacemakers, satellite dishes, lab and medical equipment, PC’s, TV’s, jet engines, EV’s, fuel cells, crypto mining and of course many MIC applications.

[In that regard and interestingly enough, crypto needs gold but gold does not need crypto, much to the chagrin of crypto wet dreams!]

I’ll stop there, (without even discussing the increasing rarity vs. the mounting environmental regulatory challenges) but when you think about it, nearly two thirds of all gold demand is either solid cultural or technology driven. Gold demand is a growth story.

When gold surpassed $1,000 on the way to $1,900 14K jewelry became too expensive for consumers and for mfg to produce.

India shifted to silver jewelry.

If the tech sector will slump demand for gold will plunge.

If you say that Indian businessmen are as price sensitive to the $Au/Ag as they have ever been, I agree with you but if I was to ask a young Indian bride and her family which is the only acceptable dowry Au or Ag?

Also, when this businessman saw gold surpass $1,000 on the way to $1,900, I was buying 24K, just like the central banks were.

A few cyclical percentage point differences in a 10% high tech Au demand market will not cause a price plunge.

You forgot to mention that Gold also is a Tier-1 asset as per the Definition of the BIS, meaning it is the best asset in risk terms for any bank to hold on their books in order to prop up their risk Profile. It could do wonders to any balance sheet or Value-at-Risk model.

Unfortunately, not too many bankers have yet gotten this message.

The price of Silver Screams “undervalued” in every conceivable way. If anyone hesitates to buy silver at these firesale prices and put a few bucks in it, they never will.

OK waterfowl:

IMHO, and trust me that after many decades of ”investing” in dirt, RE of other kinds, stocks, and MEs, gold and silver are very pretty to look at when processed appropriately.

Other than that, just another case of, ” one’s trash is another’s treasure )…

US gov will reach it’s debt limit of $31.381T by Thur Jan 19.

Non event as congress will eventually raise the limit, but we will once again see the farce from both parties. It is only matter when the day the market said, this currency is worthless.

Actually debt limit is a big deal. It takes a vote by Congress to authorize any additional borrowing. You will know that Congress is serious when and if a Congress says we are not raising it.

That will only happen when market says you have borrowed enough and we don’t want treasuries without a big risk premium. Then Fed can choose to do interest rate control or not. We will hit that breaking point before 2030 I think.

1) If the refuseniks and the double McC cause troubles US bonds value might plunge.

2) If the Dow make a second rd trip to mid 2020 commodities, including oil, might deflate.

3) RRP might rise to $5T providing worthless collateral in the O/N market.

4) Shadow banks and regional banks might not be able to re-finance.

5) Fed Assets minus RRP = Net Assets.

6) In 1919 Liberty bonds became worthless. Fed assets became worthless.

It led to a deep recession that lasted until 1921. The copper kings were

nakeded.

7) It cleansed the garbage and led to the 1920’s bull run.

As a thought experiment, let’s say the Fed decides it wants to limit its losses and starts charging big banks for some of the important services it provides. What services would be included in the list of services and what might be appropriate rates for each service? If the Fed did this, what may be its monthly income? The Fed has pulled many a big bank’s fat out of the fire. What are its services really worth?

1) In the 1920’s there were four deep recessions : Jan 2020/Jan 2021, (-)38% ; May 1923/ June 24, (-) 25.4% ; Oct 1926/Nov 27, (-)12.2% and Aug 1929/Mar 33. (-)26.7%.

2) President Harding, a lady’s man from rural Ohio, was elected in rd ten.

3) He nominated Andrew Mellon to the treasury. They didn’t stop chopping & cutting, including US naval power. Harding released political prisoners, had a mistress.

==> 4) Coolidge was even more frugal. He supported the crumb people. For him natural disasters and RE collapse were state matter. During his era there was no SS, medicare, snap, entitlements, gov & state unions pensions. His small gov shrank further.

5) They rebooted the deadwood FED. The shadow banks were booming, financing speculations, until the collapse.

6) In 1930 the flyover Fed regional banks divorced NY Anglophile Benjamin Strong.

Wish Coolidge were still the model for US government, we are almost a century away from a sane Federal government model now.

Chairman Paul Volcker, in a 1982 WSJ article was quoted as saying that he “believes in principle the Fed should pay interest on reserves held against deposits on rounds of equity” and “as a matter of principle favors payment of interest on all reserve balances”.

And Friedman’s tax is actually “Manna From Heaven”.

All you really to know is the dollar has lost over 96% of its purchasing value since 1913. Today’s dollar would be worth less than 4 cents back in 1913. These are facts and today with MMT, the situation will only grow worse. There is no end in spending increases as the real federal budget continues to increase, there is no possibility of the US becoming debt free unless we enter some Weimar period. The Federal Reserve system is supporting the destruction of the dollar in my opinion.

My gut suggests that a decline in Fed receipts, with higher interest obligations is a potential future concern, especially if the highly telegraphed recession continues to unfold (as stocks apparently go to the moon, again)?

1 bill to the board of governors? Awfully high salaries.