Inflation is an enemy of the people, but it’s a friend of government recklessness.

By Wolf Richter for WOLF STREET.

We have a situation here. Folks are out there promoting the idea that the Fed cannot keep interest rates at 4.5% for long, and that it certainly cannot hike interest rates to 5.0% or 5.5%, because the amount that the federal government pays in interest expense is spiking and the government cannot afford to pay the spiking interest expense, and the Fed will have to pivot any moment now and cut interest rates because otherwise the government would go bankrupt or whatever.

This stuff is now everywhere, propagated by all kinds of newsletters, and by bond fund managers and hedge fund managers that are losing their shirts with these higher interest rates, and the pivot mongers have grabbed a hold of it, and they’re on TV with this stuff, pushing the idea that the Fed must cut interest rates or else the government will go broke or whatever.

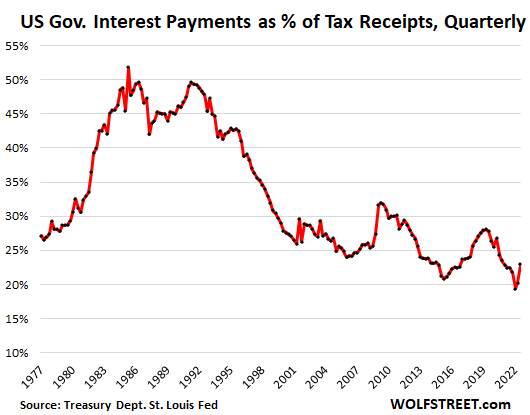

What these pivot mongers are willfully omitting is that tax receipts – which pay for the interest expense – have spiked by a huge amount, and that interest expense as a percent of tax receipts had hit a historic low in Q1 2022, and has ticked up from that historic low but remains near historic lows. Interest expense as a percent of tax receipts is the primary measure of whether or not the government can afford the interest expense: It was around 50% in the 1980s; in Q3 2022, it was 22.9%:

The thing is, inflation has been huge. Inflation means that government tax receipts are spiking, thereby lowering the burden of paying for the existing debt, thereby allowing the government to borrow more because the burden of the old debt gets extinguished by surging tax receipts due to inflation, which is why governments love inflation.

But inflation is an enemy of the people. And when inflation rises beyond certain low-ish levels – the Fed thinks that’s about 2% per its core PCE measure – it will ultimately tangle up the economy, leading to all kinds of long-lasting damage. And that puts the brakes on the government’s wishes to inflate away the results of deficit spending, namely ballooning debts and interest expenses.

What happened is this: The government’s debt spiked by 34%, or by $8 trillion, in three years, from $23.2 trillion Q1 2020 to $31.4 trillion today. In 2020 alone, $4.5 trillion were added to this debt. In 2021 and 2022, a combined $3.5 trillion were added (a rate of about $1.75 trillion per year). And it continues. This spike in the debt was caused by ridiculous amounts of stimulus spending, handed to businesses, state and local governments, and consumers.

This additional $8 trillion in debt, that 34% spike in total debt, quickly added a lot of interest expense for the government.

In addition, and gradually, old Treasury securities mature and are replaced by new Treasury securities with higher interest rates, and the higher interest costs of those new securities are filtering into the interest expense.

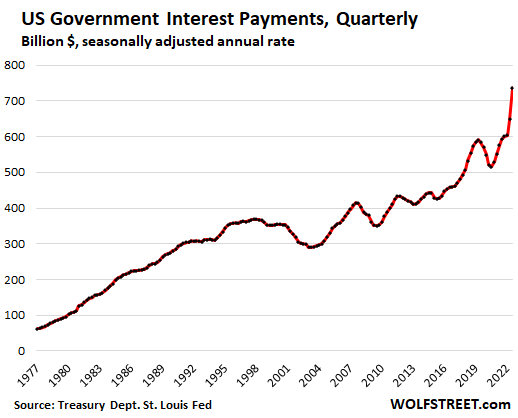

Fueled by the 34% in additional debt, and now gradually further fueled by the higher interest rates spreading into the overall debt, total interest expense in Q3 spiked by 24% from a year ago and by 43% from two years ago.

And this is the kind of scary chart the pivot mongers are circulating while omitting the huge spike in tax receipts and the historically low burden of this interest expense as a percent of tax receipts that we saw in the chart above:

Don’t get me wrong: This amount of deficit spending is nuts, it’s very inflationary and contributed to the spike in inflation we have now. It’s a terrible policy that Congress pursued. And there are a lot of issues with that. But the burden of this interest expense is not one of them – thanks in part to surging inflation.

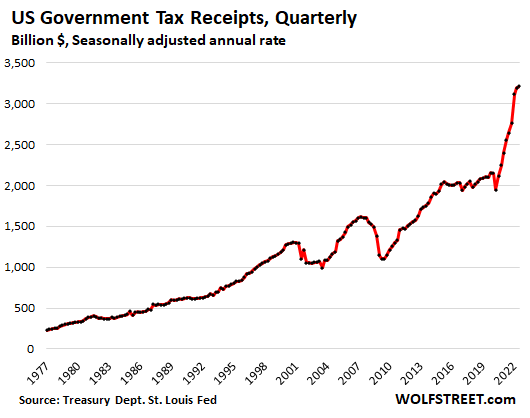

Tax receipts spiked by 21.5% year-over-year and by 52% from two years ago. This is what pays for the interest expense:

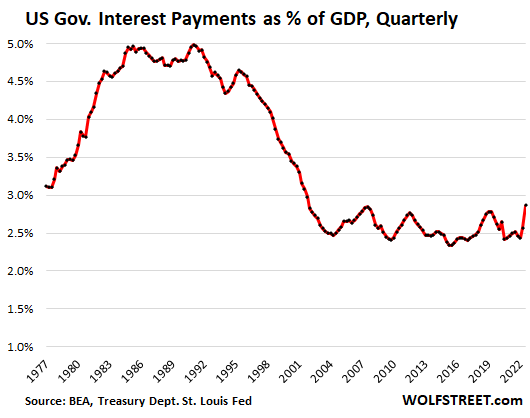

Government interest payments as percent of nominal GDP, a classic measure of the burden of government interest expenses on the overall economy, plunged to historic lows during the era of Easy Money after the Financial Crisis, and it’s still in that low range, but has risen to the upper end of that low range:

Inflation will further eat into the burden of this monstrous debt. A big bout of inflation is the best thing that happens to the burden of government debt. That’s why governments love inflation.

This government love of inflation and deficit spending is precisely why modern central banks are supposed to be “independent” from the government so that they can tamp down on inflation, and let the government struggle with their deficits and debts.

And all this ongoing deficit spending, and the money from the prior stimulus spending that is still sloshing around at state and local governments, at businesses, and at consumers, will provide further fuel for spending, taxes, GDP, and inflation.

The path that government spending has been on for the past three years is clearly wrong-headed. And maybe someday, when interest expense eats up 50% of tax receipts as it did in the 1980s – and not 22.9% as it does today – then just maybe we might see some real discussion and action in Congress about curtailing these ridiculous deficits. But we’re a million miles away from that. And the Fed is doing exactly what it needs to do — hiking interest rates — to curtail inflation and to gently begin nudging Congress to take the deficits a little more seriously.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

That interest rates have to stay lower because of the debt burden is an appallingly shallow suggestion to begin with. Years of artificially low interest rates conjured the excessive debt into existence in the first place.

You cannot escape an excessive debt problem by making debt more comfortable to have.

“You cannot escape an excessive debt problem by making debt more comfortable to have.”

Absolutely correct.

A government that prints dollars out of thin air to meet its expenses and liabilities, can also print more dollars to service higher interest payments.

So, when it comes to this:

1. In mathematical sense, this means that debt will increase exponentially.

2. In logical sense it means government will always remain solvent wrt dollar debt, even if peasants die of hunger.

yes, a government that controls its own currency will always remain solvent. But inflation will ruin the party. That’s the problem now.

The USG will remain solvent in accounting sense as long as the country exists in anything resembling its current form.

That’s not the real question, to those with the most influence.

It’s whether the US can maintain its current leading geopolitical role or loses it to a competitor, presumably China.

China has a debt problem too, but its currency isn’t the global reserve currency.

The American imperial state cannot exist without the ability to use the USD to pay for things the US economy does not produce.

“In logical sense it means government will always remain solvent”

Germans had that same belief between 1921 and 1923,

What happens with tax receipts in recession?

mentality of people for economic success is important.

Only as long as the dollar remains the world’s reserves currency.

Augustus has gotten to the crux of the crisis, which true conservatives (not Republican spending mafiaoso) have been warning about for *decades*.

Zimbabwe controlled it’s own currency and became insolvent. Printing your own currency and maintaining solvency has been a luxury for the main currency that the world values. How long that ‘values’ will sustain is the question. But we do know that all fiat currencies printed by the strongest nation of an era is eventually replaced

Good to see I sparked an interest article by posting John Mauldin’s “US Interest Payment” chart in the previous article forum.

I personally have no agenda as I actually make way more in the markets when they are volatile, versus just going up 100% of the time.

I do think a lot of the tax receipts are a by-product of Wall Street gains. For example, CA seems to have a budget deficit issue currently that is being blamed on less capital gains taxes from stock and bond losses, etc. Not sure if the Gov is lying or telling the truth but that seems to be “the story”. I had assumed such a mechanism would exist over time with all states if the markets have multi-year negative or multi-year low percentage gains, or simply traded sideways for a few years. I’d be curious what percentage of the tax receipts are from capital gains taxes versus income taxes.

I see your points in the article, with the only real disagreement being the “US Govt Interest Payments as a % of GDP, quarterly”.

Per Saxo Bank’s Steen Jakobsen, intangible assets (patents, data, ,brand value, etc) made up around 17% of the world’s wealth in 1975, and the rest was tangible “real stuff”. By 2020, intangible asset wealth was 90%. Thus just one of numerous reasons “GDP” is not a realistic way to measure actual wealth accurately as it can be fudged easily via bloated valuations for “intangible” things versus “real” things. Therefore the visual of that GDP chart going horizontal can be misleading as the entire world is cooking the books in order to continue the gravy train of infinite cheap money and debt. At some point it won’t work, but that could be a hundred years for now so we play the game we are given, and hope for the best while owning some “tangible” assets just in case…

Good observation, as I depreciate my goodwill against my cash income. Sorry to impact the tax receipts.

“But we’re a million miles away from that.”

That’s hyperbole. America is OFFICIALLY on a much shorter path to a debt bomb than you’re willing to admit. The reason is simple. Congress is drunk on profuse spending which to credit you’re calling them out on. And there appears to be no relief in sight, but I won’t use the million miles away analogy which is utterly silly.

And those tax receipts will drop just as quickly as they rose once a moderate recession hits. The next 6 months will confirm a soft landing is taking place. Inflation will plateau and then slowly start rising again. By the end of the year, the Fed will be forced to start raising the FFR up towards 6% with 7% being a real possibility. Last, I predict they’re forced to start selling MBS by September 2023.

Can you do a write up on how often the treasury must “roll over” the national debt. From what I understand, the average maturity time for a treasury is about 5 years. So, from today’s date, over the next 5 years, the treasury must re-issue the entire principal + deficits + interest of the current national debt in new bills, bonds, and notes – to pay off what was issued before. (using a new bigger credit card to pay off an older one) How much does the treasury need to borrow per day, and what are the projections given our current fiscal deficit? How much QE will be required to fund it?

GDP is up about 18% since 2019.

I looked at Texas sales tax collections, they are up about 26% since 2019. This is mainly nominal, due to the increasing costs of goods and services (inflation).

US Govt tax collections at $4.9T are up about 40% since 2019. If you tack on 18% from the base rate of 2019 (to match the increase in GDP), which was $3.5T, you come up with about $4.1T in tax collections for USG. This assumes we don’t enter recession.

Aggregate interest on the Nat’l debt a year ago was 1.33%. In Oct it was 1.82%. November, 1.92%. December was 2.01%.

Wolf, I think you are wrong on this. Peter Schiff is right. Debt holders will panic at some point and dump Treasuries once they finally figure out 2% CPI is never happening again. It is a matter of time. When the Fed loses control, USG interest costs will explode.

Bond holders have gotten killed in terms of purchasing power. They won’t be this dumb much longer.

Peter Schiff, who is selling gold, has been predicting the collapse of the dollar and the US debt for as long as I’ve ever heard of him. It’s always the same, but the yada-yada-yada reasons change. So enjoy what he says.

It is very difficult to deal with excessive debt in a democracy. It probably has to get to a sovereign debt crisis, then “temporary” semi-legal actions can be taken like FDR and Nixon did. That’s when you can get a new tax, reset pension promises or reset real value of savings thru interest rate caps.

I think even Dalia says this is the way the system works. You grow debt faster than GDP. Once you have done too much, you have to flush the debt somehow to begin the process again. I guess he assumes politicians and central banks have to run a dishonest monetary system to keep empire running.

The only reason a country needs to grow debt (and counterfeit their own currency) is that country has lost its “value-added producers.

I know of no country in History that willingly lost her value-added factories, along with the technology and entrepreneurs that support that very same value-added.

In losing the hard profits, in people and in manufacturing, the USA is but a shell of what she once was. Now, we have had more than an entire generation that has been partying like the nightclubs in Berlin in the 1920’s.

An economy of trading paper. Paper claims on more paper. The Fed prints and borrows, the Government spends and borrows, as they hollow out the core of the nation and throw another wet, bale of hay onto the back of the American camel.

But it takes real money to produce the whiskey for the party.

Is there an American Politician in power anywhere that has the mile-high perspective of the USA following the path of the end of Rome?

The US still the second-largest manufacturer in the world, behind only China (4x the population), and way ahead of Japan, Germany, et al.

The US is the largest producer of petroleum and petroleum products in the world. The US is the largest natural gas producer in the world. This falls under industrial production.

Ag is also huge in the US. Construction is huge. etc.

So sure, it would be nice to have more manufacturing in the US, but it’s not like the US has stopped manufacturing.

Right there is little in the the DOW that manufactures hardcore. It’s offshored. Boeing is a joke self destructed by the money guys. Taiwan Semi blew past Intel 3 years ago, the rest is finance and advertising.

Moi,

LOL.

Manufacturing companies or oil and gas extraction companies of the 20 DOW stocks.

1. Amgen – pharmaceutical products

2. Boeing – planes, discount them all you want, but this huge

3. Caterpillar -heavy equipment for construction, ag, mining, etc.

4. Cisco Systems – tech – manufacturing plants in Kansas City, Irvine, Sunnyvale, Lehigh Valley, NC, Portland, and Waukesha,

5. Chevron – oil and gas extraction

6. Honeywell International – automotive, other – manufacturing plants in the US

7. IBM has manufacturing plants in the US, including one it just opened in Poughkeepsie, N.Y.

8. Intel has chip plants in the US

9. Johnson & Johnson manufacturs products in the US

10. Coca-Cola makes stuff in the US

11. 3M manufactures in the US

12. Procter & Gamble manufactures products in the US

13. Dow manufactures all kinds of products in the US

> “temporary” semi-legal actions can be taken like FDR and Nixon did. That’s when you can get a new tax, reset pension promises or reset real value of savings thru interest rate caps.

This makes me think of Bernanke 2006 and post, or rather, what the western democracies (principally USA) did: they (we) re-papered the financial system, filling massive private debt holes with invented dollars, and shifting a lot of private losses onto sovereign balance sheets. That works maybe once in a half-century, not sure about more often. Inflation now is the end-game many anticipated every since 2008. I never underestimate the card tricks possible to central banks, but at some point, printing without new productivity (and some minimal level of effective wide distribution of rewards) hits a wall. maybe the latest Chinese bout with COVID gave us a reprieve.

I have watched a lot of Marc Faber videos. He has read all the older economists multiple times and I think he has the best advice. Nobody can know the future, so you must diversify in a wide variety of assets and jurisdictions to truly protect yourself if the SHTF.

The Federal Government can never have a “excess” debt payment…… There’s nothing, in history, that is evident of this, or Wolf’s headline. If there is, please enlighten us, dummies. Interest payments on Federal finance vehicles, ( Treasury bonds, etc.) are added income to the economy held by private interests…. There are only two ways that new dollars are added to a growing economy and for a growing population. Private bank loans which must be paid back with additional interest, dollars perhaps reinvested in the economy, and Federal “deficits”, which are never paid back, add security to the value of the dollar, via savings in Federal finance vehicles, again Federal Bonds, etc..

Freedomnowandhow,

I generally delete comments that show that the commenter has only read the headline, and is reacting to the headline, and doesn’t know what they’re talking about. If you’re too lazy to read the article, don’t comment on the article. Commenting guideline #1. You have no clue what the article says, to use your own term, “you dummy”

The Fed creates “new” dollars every time it purchases government or private debt. Whatever the net liabilities on the Fed balance sheet are at any given time represent new dollars in the economy created out of thin air. You are correct that private bank loans also create “new” dollars less bank reserve requirements.

“Inflation is an enemy of the people, but it’s a friend of government recklessness”

It’s a sickening situation when the government financially benefits from hurting and destroying the very people who they are elected to serve and protect. I believe the system is beyond repair. The entire Federal Government, nevermind state and locals govs (the same, oftentimes worse), is shot through with corruption on every level.

The working class and the poor are getting absolutely demolished as I type. Financially ruined. It doesn’t happen overnight, it’s a long, grinding, soul-destroying road down to destitution. For most, there is no road back. A life of poverty until death is their future.

Very sad but unfortunately very true.

all I can say is that I have LOTS and LOTS of tax deductions in 2022

Who thought that in this “information age”, there would be so much misinformation to allow oligarches to screw the masses this way!

Too many smart people are getting screwed, and this can turn bad quickly. System seems be unstable.

Don’t underestimate the brainwashing power of the culture industry. Most people can find ways, through entertainment and consumption of popular culture, to numb their pain and suffering and justify their servitude in the current system.

And drugs – both legal and illegal.

Yes, it’s not actually the government, as it isn’t a person.

It’s the elites who run it.

We’re just getting what we voted for.

“Who thought that in this “information age”, there would be so much misinformation to allow oligarches to screw the masses this way!”

If you want a clear explanation, there’s a good book worth reading: “Amusing Ourselves to Death” – public discourse in the age of showbusiness. There’s a free .pdf if you search.

We’ve had entertainers for leaders since Reagan. That whole “voodoo economics” thing was spot on, and now we’re getting to see it play out in real time. Pay no attention to the man behind the curtain.

NO DC, it, the system of GUV MINTY and the following capitalism for ALL folks is absolutely NOT beyond repair…

Don’t even go there, especially on WS, where relative reason prevails over hysteria, at least SO FAR…

Hysteria has and does put many folks behind the eight ball in their own minds…

Please DO NOT let that happen to you, and don’t encourage such thinking for anyone else…

Other than that piddling detail, I agree with you so much you must be a very intelligent person — ( to agree with me so much,) eh

Use a little imagination and expect the new ways the government will use to increase spending: more statutory laws with penalties, more civil forfeiture, real estate confiscation for late tax payments, fines for unsightly property, local contracting of services with direct citizen billing, tolls, road and parking access fees, new licenses and fees for everything with required classes and inspections (gas stoves?).

Got to pay those govsalaries.com somehow. Look their salaries up.

Banks say earnings are OK, consumer balance sheets are slightly worsened lately, but better than pre-COVID. Jobs are still strong, consumers are spending. Bank CEOs then are lying? Because they can (theoretically) be sued for that, unlike some commenter voicing opinions here of end times.

Not all of their futures. The working class and the poor will eventually respond by demolishing another class of people in their proximity. Dog eat dog. And we all know the hungriest dogs are gonna eliminate those hunger pains one way or another.

So true. Sadly, the majority of our citizens are not trained to think in terms of inflation adjusted dollars. So if two years ago they were earning $40,000 and they are now making $44,000 they think they are making more money when in fact, there has been 13.1% inflation since 2020 and to even break even they would have to be earning at least $45,230.69. Similarly, since government and most main stream media outlets have almost completely been comparing expenditures to GDP (which is not only meaningless but easily manipulated) instead of revenues which are both meaningful and not easily manipulated, thus lulling them into a false sense of security.

Paul Sommerville,

Revenues is probably one of the worst measures of an economy because it excludes investment activities, such as building factories, infrastructure, etc. and would be totally meaningless. If you want to look at revenues, there are business revenues data that you can look at.

In addition to GDP, the Bureau of Economic Analysis releases the corollary economic measure, based on INCOME: Gross Domestic Income (GDI).

I meant government tax receipts when I said revenue.

So the fed plan is?

1. Keep raising rates

2. Real economy falters

3. Tax receipts drop

4. % of interest payments to tax receipts spike

5. Government forced to stop deficit spending

6. Prices come down

7. Economy recovers wholistically

Nice plan if they stick to it

AS

The gubment is GTG with #1 through #4. They claim #5 through #7 is part of the overall plan but then a new slew of legislators get elected in the plan gets revised to only #1 through #4. Lather, rinse and repeat.

Arya Stark,

You’re compressing many years into months. That’s not how it happens. Look, it took 6 years to go from interest expenses of 27% of tax receipts to 40%. And that included the massive double-dip recession.

I was just trying to understand the mindset of the fed. I realize it would take quite a while.

Wolf,

That bit about where inflation (reliably, sustainably) “fixes” G deficit nightmares (50 years and counting for both trade and budget deficits) is where you lose me.

Inflation destabilizes everything by disrupting price signals – that is *bad* for the level of overall, taxable activity.

And aren’t some tax brackets, for some parties *indexed to inflation*? The G can’t get bracket creep windfalls if income is indexed to G inflation

But pls keep posting these type of articles – the issues here determine the survival of the US as currently politically configured.

Beware of “emergencies”. Governments love “emergencies” (which call for immediate irresponsible spending) as much or more than they love inflation (which also encourages irresponsible spending but at a much slower pace absent hyper-inflation).

So does that mean, the government should be doing more to beat tax cheats?

Because I don’t actually understand who is the debtor in this situation, except for other facets of the government.

What exactly is the problem here, because it seems the government’s loss is my gain?

There is no revenue problem.

If tax receipts equaled 100% of all income, politicians would still find a way to run massive deficits.

The pyramids always engorge to meet the number of slaves.

The problem, Wolf, is that if we have a recession – or even an extended economic slow down – tax receipts will plummet, but the interest payments are forever. Thus, the pivot mongers may be operationally early (and as you point out, they do have an agenda), but their overall methodology is correct; it simply might take longer to play out.

The charts include the worst recessions in our lifetimes, the Double Dip and the Great Recession. So you can see how the relationship changed in chart #1 during those huge recessions.

The burden of the existing debt will decline with each month of inflation. A recession is going to reverse that for a few quarters, and so what? See chart #1.

The burden of this interest expense won’t be a real issue for years.

And the ONLY thing that will put some discipline on Congress are higher interest rates and higher interest expenses.

The pivot mongers are wrong all the way through. They don’t give a crap about the economy or America or the people; all they care about are their trading positions and an end to losing their shirts.

That includes all of the idiot commenters at Marketwatch, as well as “celebrated” professors like Jeremy Siegel.

Wall Street and the stonk market are the only things they care about.

I notice BTC spiking (to a suspiciously round number, circa 20,000), and reckon it is a similar thing: whales are doing some signalling (buys) to lure the dumb money back in. The touts won’t give up: their free riding depends on it.

What do they call it when you have high inflation *and* high interest rates? A complete breakdown? 😂

Nah. “high inflation *and* high interest rates” – that’s kind of a normal situation.

The abnormal situation is high inflation *and* low interest rates, which is what we still have now, with the EFFR still negative, which would cause the “complete breakdown.”

EXACTLY

They’re going to magically make 2022 disappear, like it never happened, and gaslight you by telling you that inflation is lower than it is and disappearing. This is the government’s version of moving the goal post wide left and backwards when the kick is already in the air:

“The Bureau of Labor Statistics will change the method of calculation of inflation data from 2023. The release of the January 2023 CPI data, which is slated for Friday, February 10, 2023, will mark the beginning of the switch to yearly weights. With the release of January 2023 in February, the CPI for ‘new vehicles’ will introduce a methodology improvement to the time series filter that estimates the most recent cyclical trend and short-term fluctuations.”

*2021 disappear. Please correct if you can, Wolf.

Weights are changed all the time, every year, as consumer spending shifts, and as higher prices change where the dollars go, and the weights are based on where the dollars go.

For example, housing weights INCREASED in 2022 because a larger portion of spending went into housing, and housing inflation is what is spiking! And this increase in housing weights made CPI worse in 2022.

People said the same braindead BS in late 2021 about 2022, that some kind of strategic shift in weights away from items with lots of inflation will miraculously repress CPI. And we ended up getting the worst CPI readings in 40 years.

Depth Charge, I love you, but spreading stuff like this, in this ignorant manner, and with stupid conclusions, turns your whole comment toxic. There comes a time when you just need to slow down and take a deep breath!

“People said the same braindead BS in late 2021 about 2022, that some kind of strategic shift in weights away from items with lots of inflation will miraculously repress CPI. And we ended up getting the worst CPI readings in 40 years.”

I guess the question is “would the CPI been even worse had they not instituted the change?” That’s the data I’m interested in. Because everything I’ve read indicates that the way CPI is calculated today, never mind these latest changes, has led to the appearance of more muted inflation versus the old way it was calculated in the 1970s, when Volcker headed the FED.

Further, I found that quote from a financial article. Drawing my own conclusions from a quote doesn’t seem like “spreading BS,” it was simply my interpretation of the motive behind the change, and the likely conclusion the new data would arrive at.

You may not like people like me, Wolf, but we are a byproduct of this raging inflation and the war on the middle class by the FED and the government itself. We have lost all trust in the government and their lies and statistics. You can go ahead and delete the comment. It’s not really important to me.

1. “I guess the question is “would the CPI been even worse had they not instituted the change?””

I already gave you the answer in my comment: “And this increase in housing weights made CPI worse in 2022.”

2. “You may not like people like me…”

I diligently explained in my comment: “Depth Charge, I love you, but…”

3. “You can go ahead and delete the comment. It’s not really important to me.”

No, not gonna. If I delete it, someone else will post the same thing. And I have to explode all over again.

4. I track the weights (copy and paste over to my spreadsheet late in the year and early in the year to see the direction. So I have these columns of all the weights side by side going back to Oct 2021 when that started becoming a talking point.

And I can tell you, the changes in weights make sense to me: For example, housing components increased in weight because housing got more expensive and people spent a bigger portion of their total spending on housing. That’s how it works.

Shelter: Oct 2021: 32.4%; now: 32.9%

People also spent more money of food because food inflation was out the wazoo, so the weight of food at home increased, which made CPI a lot worse, given the huge food inflation and the big weight of it:

Food at home: Oct 2021 7.73%; now 8.53%

But I guess men spent less on clothing, now that they’re working from home. So men’s apparel lost weight (LOL):

Men’s apparel: Oct 2021: 0.69%; now 0.60%

Unfortunately, the weights stuff requires a big spreadsheet to see: there are 345 categories, each with its own weight, so my spreadsheet has 345 lines, across a bunch of columns. And I cannot post this stuff here on my site. It’s just too boring, a gazillion little bitty numbers. And the changes are really small, and no one would look at the article, and people would think I totally lost it. It’s just a lot more fun to read an article about how the BLS is going to lie again, than to actually deal with this stuff.

But but, but... if people here tell me that they’re interested in an article on the weights in a couple of months, when the weights are embedded, with a gazillion little bitty numbers, 340 lines in total, and some key items pulled out and discussed, just Like I did here, well then, if there is popular demand, then I might do it. So everyone, if you’re interested, please let me know here by replying to Depth Charge’s comment above.

I for one would only be interested if there was hard data that supported a government conspiracy to skew the data to show lower inflation numbers.

It appears this is not the case based on wolf’s comment.

However I think they already did this with the way they calculate technology.

Iphones are in no way deflationary. Use to be $650 for top line phone now it’s $900-$1200 and most people have to finance it over 2-3 years. I get the tech improved thing but that’s what tech is suppose to do improve. Tvs are dirt cheap though so maybe they balance out but I’d say people spend more on iphone then TV’s for sure

I would certainly be interested in seeing how the weights have changed.

“No, not gonna. If I delete it, someone else will post the same thing. And I have to explode all over again.”

Haha, you did make me laugh. And I totally understand where I goofed on my hot take. In retrospect, it was silly. It all makes sense to me now. See, that’s why I come here anyway. A good scolding actually taught me something.

Here’s a simplified example showing that updating the weights might seem weird, but (to my surprise) does in fact work reasonably well – at least, if Consumers Can Afford The Inflation:

Imagine a simplified CPI with only 3 items in it: Shelter, Stuff, and Services. (Stuff being things like food, energy, clothing and WolfStreet Mug Production. Services being things like healthcare, travel, haircuts, Donation to WolfStreet and so on.)

Now consider a scenario where, to start with, all 3 items are equally weighted in the CPI for Year 1. So the “CPI Basket” is 1 unit each of Shelter, Stuff and Services. 3 units total.

But we’re about to have an inflationary wave sweep through the economy, first in Shelter, then in Stuff, then in Services. When all is done, all prices will have doubled, but they won’t all double simultaneously. Will the CPI capture this correctly?

During Year 1, Shelter prices double (100% inflation in 1/3 of the index), while the other prices don’t change. Overall inflation is calculated at 33%, since with Shelter prices doubled, it now costs 4 units to buy the basket that used to cost 3 units. 4/3 = 1.33; up 33%.

At the end of Year 1, the CPI Basket is updated to show 2 units of Shelter, 1 unit of Stuff and 1 unit of Services. That is, Shelter is re-weighted at 50%, Stuff at 25%, and Stuff at 25%, since that’s how people spent their money in Year 1. (Remember, we’re assuming people can afford the inflation and just “pay whatever” to maintain a constant lifestyle.)

During Year 2, Shelter and Services prices don’t change, but Stuff prices double. Overall inflation is therefore calculated at 25%.

At the end of Year 2, the basket is updated and now has 2 units of Shelter, 2 units of Stuff, and 1 unit of Services, for a total of 5 units. So Shelter is 40%, Stuff is 40%, and Services is 20%.

During Year 3, Prices of Services double in turn. Overall inflation is therefore calculated at 20%.

Over the 3 years, prices have doubled, so True Inflation is 100% total. You might look at the 33%, 25% and 20% from those 3 years, add the up, and think the CPI would only show 78% inflation “they’re lying to us again!” … but you’d be wrong, because the 25% inflation is on top of the 33%, and the 20% is on top of the other two. So you have to write the math out like this. If the CPI to start was 100, the CPI after Year 3 becomes 100 * 1.33 * 1.25 * 1.2 and guess what… the CPI is 199.5, just about the 200 that you’d expect for a 100% inflation (doubling of all prices).

BUT WAIT – what if we’re not living in a Middle Class World where Consumers Can Afford Inflation by Cutting Savings or Borrowing?

Let’s revisit that scenario … where we have a CPI basket consisting of 1 unit of Shelter, 1 unit of Stuff and 1 of Services. And an inflation wave is coming.

In Year 1, Shelter prices do go up by 100%, and CPI inflation is reported at 33%, same as in the other scenario. But people don’t actually pay 100% more for Shelter – they can’t afford to. On a fixed budget, they can only afford 3 units of consumer prices. Facing higher Shelter prices, they have to rebalance their spending. They cut back on Stuff and Services spending, and downsize their abode (or take on a roommate) to be able to make rent. Shelter doesn’t become 50% of the CPI, just 40%. Stuff and Services come out at 30% each (not 25% as in the other scenario).

On to Year 2. Stuff doubles in price, but it’s now 30% of the index, so CPI is reported at 30% inflation. But people don’t pay more for Stuff they can’t afford! They cut back spending, again, wherever they can. While Stuff does go up due to inflation, it only becomes 40% of spending. Shelter drops from 40 to 35%, and Services from 30 drops to 25%.

On to Year 3. Services doubles in price, so CPI is reported at 25%. And you know what people will have to do. Cut back again.

But when we look at the big picture, we see actual prices having doubled, but because people rebalanced and adapted and changed their spending baskets, the CPI doesn’t quite come out right. CPI thinks 33%, 30% and then 25% inflation works out to 1.33*1.30*1.25 = 116%! But it should be 100%!

So – changing the CPI basket in the middle of an inflation wave CAN result in a poor measurement of inflation, but it can be an overstatement as well as (presumably) an understatement, depending on how people react to the inflation.

Wolf, I think an article which demonstrates how many categories make up the CPI — 345! — would be valuable if only to emphatically demonstrate the complexity of the economy which ought to inspire a little humility where predicting what is going to happen based upon a handful of desperately reductive aggregates where our economic indicators are concerned.

First of all DC: Wolf has proved to me without a shadow of a doubt that he loves each and every one of us who at least try to contribute with honest anecdote or honest attempts to help him help us.

And, as noted above ( earlier ) , I think you must be fairly intelligent because you agree with me so much…

Let’s be clear about at least one thing:

Any and Every ONE is a product of their own choices.

OK, two: any and every deviation from that basic law of physics, chemistry, biology, biochemistry, etc., etc.: e.i. THE Hard Sciences, will lead to confusion AND correction.

Trying to make it easy here folks, for some on here as well as me own self, eh

Thank you for your updated comment, Wolf. Your site and data mean more to me than you will ever know. I have probably done a very poor job of showing that but I will do better this year, you will see.

Re: This government love of inflation

The last 40 years have been fairly low in inflationary terms and the burden of government debt has done nothing but explode. I guess I’m missing something?

There is one thing: that exploding debt could, in recent years, be created at very low interest rates. That would seem to be as advantageous to government as inflation to the principal amount owed: cheaper principal, or else cheaper interest, are incentives to borrow (which was reflected in the private sector as inflation in asset prices like houses.)

One thing to keep in mind…those low interest rates *are the result of G money printing/consumer inflation*.

The G drove the borrowing interest rates down by using its own printed money to buy its own new debt – if it didn’t interest rates would have been much higher because private parties – scared to death of a USD death spiral default – would have demanded higher lending rates.

But the G can print at will to “fix” such crises.

At the cost of injecting unbacked money into an economy…ie, consumer inflation.

So the G got to borrow cheaper…by making everything more expensive.

There is no magic in economics – no secret diamond pooping unicorn owned by the G.

Is it possible to forward this column directly to Janet Yellen?

Is it possible to forward Janet Yellen (and Helicopter Ben Bernanke) to Zimbabwe?

They have both long been the professorial painters of patina on America’s economic turd sandwich.

What horrible crime did the people of Zimbabwe commit to deserve having Yellen and Bernanke dumped on them?

1) US gov interest payments as % of the GDP is breaking out after 20Y

in a trading range.

2) US tax receipts are in a bubble.

3) The Fed raised interest rates to fight inflation. Central banks holdings of gov bonds and notes are bleeding. The Fed might pay the primary banks over $100B/y on reserves, excess reserve and RRP. Things are tough for JP for keeping us and our businesses alive. US gov financed it’s multi stimulus and relies with higher debt ceilings.

4) In her letter Dr. Yellen warns of a growing risk of “events”. She noted dozens ways to cut expenses before bad things happen, after Jan 19.

5) The refusniks and the dbl McC might use this data to bend the will of the other side in repetitions.

For many years i always thought Government debt would eventually matter. Now i am under the conclusion it will not in my lifetime.

I have seen it go from 1 trillion to 31 trillion and it on the path to 40 trillion by 2030. Maybe sooner.

There is a supply vs demand component for available capital. There might be more borrowers looking for loans when interest rates are low than when rates are high. This is especially true for loans of greater duration, the long end of the curve. During the 1970’s interest rates rose, so did the value of a home. A home was a hedge against inflation and better than an RV campsite where the landlord always increases the rent. People took money out of the stock market and bought bonds. Owning a 30 year AA bond paying 12% interest would have been a nice thing once interest rates dipped below 9%.

Yield solves ALL supply and demand issues. Higher yields generate demand.

Wolf,

Appreciate the article. It puts the present in the proper prospective and I note you are not suggesting continued large deficit spending is good for the future.

Thanks for writing it.

So, how does the calculations play-out if the interest rates were at 10 or 15% where they should be if Banana-republic Jerome was serious about fighting inflation? As you are well aware Wolf, as interest rates drop so does the US$ and inflation roars back with a vengeance.

As I have said over the past year there’s a good chance oil spikes higher than the 08 $150 high, as well as big spikes in other commodities.

Inflationary gvt-deficit spending will continue until the system breaks!

The Fed and Fed gvt are monetary and fiscal clowns driving the clown car off the cliff!

With 7% CPI, we don’t need the Fed to hike to 15%, that’s just nonsense.

But if CPI goes to 15%, which might require the Fed to hike to 15%, the entire burden of the debt and interest payments would be wiped out in just a few years by inflation. Tax receipts would spike like you’ve never seen in your life before, even during a recession. 15% inflation is HUGE. everyone who holds any kind of fixed interest debt will be wiped out in a few years.

Wolf, hope you are enjoying the football game. seahawks14to13 as I type. Keeps you on the edge of your seat.

“15% inflation is HUGE. everyone who holds any kind of fixed interest debt will be wiped out in a few years.”

I’m not understanding this statement.

I would think fixed interest debt would benefit from high inflation as you are paying that debt back with cheaper money.

I would think fixed interest assets would be wiped out by high inflation because it would make your assets worth less and less.

The way I read it “holds” is the key word. Someone holding (i.e. owning) fixed interest debt will be wiped out in a matter of years with 15% inflation.

You have to look at duration, folks. Investors with a 7-10 year duration will be wiped out. Debt Investors with 1-2 year duration will be hurt but not wiped out.

“…who holds any kind of fixed interest debt” = investors who hold these assets, such as Treasury securities.

What you said is correct for the borrowers, such as the US government. Borrowers don’t hold debt. They owe debt.

Wolf

During Volcker era (early 80s) the inflation did reach to 15% and the rate got hiked almost to 20%.

I had started my ‘deferred retirement plan’ by investing in 30yr with 14%

Debt to GDP was around 35% compared to now nearly 130%.

I read some where (warren Buffet ?correct me if I am wrong) that once the DEBT exceeds 90% of GDP, it will be a drag on the economy. B/c of inflation this matters little?

“So, how does the calculations play-out if the interest rates were at 10 or 15%”

I’ll tell how that scenario would play out – I would be killing it with my beloved T-bills while RE and the markets get crushed. Bring it!

Wolf, I always respect your opinion. A lot of thought, experience and intellect goes into every article. Have you thought about what America would look like if America lost reserve currency status or even a substantial reduction in the use of the US$ as reserve currency.

I think the Chinese RMB should become a much larger reserve currency at the expense of the dollar. This is a huge economy and should have a big reserve currency. This might take the US share from 60% to 40%; it might leave the euro share the same at 20%, and put the RMB share at 20%. This would take many years, and it would be good for the US and for the global economy. But it cannot happen as long as China has capital controls in place.

https://wolfstreet.com/2023/01/01/status-of-us-dollar-as-global-reserve-currency-usd-exchange-rates-hit-foreign-exchange-reserves/

If US gov debt deflate in real terms due higher inflation rates and gov

spending will be cut in stepping stones ==> we might not have a recession. It might start a prolong bull market. JP will be a hero.

Once again, love the perspective on the issue. But the one problem I have with this comparison is it doesnt really tell me if that 52% spike in tax receipts is durable. My guess is that it is not.

I assume that tax receipts will fall based on:

– Receipts from investment gains will fall precipitously due to the market decline in both equities and bonds. my thought is that the markets fall much further this year (spreading to p/e declines in quality assets) basically just compressing p/e ratios

– Receipts from income includes income from government employees and companies that generate revenues from government spending. that is going away and will lead to reduced employment.

– Receipts from businesses will fall once we head further into stagflation

I also had looked at the projections from the CBO in the past and over the next decade the percentage of the GDP dedicated to interest repayments goes up alot. I would have to look at that info.

I’m not arguing with Wolf’s point that this is not a short term issue, just pointing out that over the longer term, the trends are really bad and we need to solve them with changes to polcies.

i actually re-read the last paragraphs and Wolf already addressed my points. wolf, if you want to delete my posts, please do. nice article.

Yes, but also think of it in these terms.

What do you think would happen to the US economy and by implication, government budget, if the annual increase in the national debt and the FRB’s balance sheet resembled pre-GFC?

l imagine the growth in revenues will come from growth in profits and/or wages, which are increasing on a nominal basis, from inflation.

Really????20% of companies in NYC are fake,they will be gone in 2023,no more free money,they got financing from.So all those lazy and spoilt millenials and gen Z(much worse work ethic) will lose their fake jobs and move back to parents basements.My business was down 10%(both gross and volume).But i am totally o.k,i have a frozen rent till 1st of October(rent control) and my car payment is the same.

Ah yes, those pesky kids really got spoiled by coming of age in the biggest asset bubble this country has ever seen. Surely those already holding assets had it tough.

Your comment is trash. You should reexamine your thinking.

Just to give you an idea:

1. During normal times such as as in fiscal 2018, capital gains tax receipts were just 9% of total federal tax receipts (Tax Foundation)

2. Lots of stuff that will be sold will be sold at a profit, despite the recent market declines, because it was bought years ago. Look at a 10-year chart of the S&P 500, and a lot of this stuff is long-term holdings that will trigger big realized gains despite the recent declines.

3. The Congressional Budget Office projects that total tax receipts will RISE over the next few years, with big jumps in 2025-27 due to changes in the tax law that will take effect then, despite a decline in capital gains tax receipts from the record levels in 2021 and 2022.

Per CBO: Tax revenues, 2022, by category, in billions:

Individual Income Taxes: 2,623 — less than 1/2 from these massive capital gains taxes

Payroll Taxes (paid by employer): 1,465

Corporate Income Taxes: 395

Excise taxes: 88

Customs duties: 95

Estate and gift taxes: 27

Miscellaneous fees and fines: 34

What is also driving tax receipts are the most massive pay increases in decades (wage inflation), so that’s individual income taxes and payroll taxes. And they continue to be inflated. Corporate income is also being inflated by price increases (inflation).

Inflation is a huge driver of tax receipts.

you are not quite right. both the USA and other Developed nations have indexed tax brackets to inflation. there is no higher tax receipts coming up.

Nominal tax receipts will increase with inflation. At least, the comments I recall have referenced percentages and nominal values.

Imagine you made $100k in 2021, but $115k as a job hopper in 2022.

Payroll taxes, which are not adjusted for inflation, just shot up. The highest bracket for this individual is still 24%, but only above $89k in 2022, while above $86k in 2021.

There, see? Easy to just look at real numbers and see how mistaken you are. Tax receipts will increase with wage increases.

mike,

Cap gains are *not* indexed for inflation. That’s ostensibly why they are taxed at a lower rate.

No. They’re taxed at a lower rate to encourage capital investment (that is, for people to take risks). Of course, if the Fed is going to backstop all risk, then that subsidy doesn’t make sense.

If it was due to inflation, interest income would be taxed at a lower rate too, and it’s not.

Capital gains? Tax rates?

“I have accountants pay for it all

They say I’m crazy, but I have a good time

My Kawasaki’s done 145

Still have my license; I’m still alive

They say I’m lazy, but it takes all my time

Life’s been good to me so far”

Perhaps slightly off-topic (though it is all related):

I watched that dismal Karine Jean-Pierre at the WH state several times “We believe the debt limit [or debt ceiling] should be raised without condition.” And that it would be irresponsible for the Repubs to play politics with it.

At the same time when asked if Biden thinks the debt limit should be removed altogether she declined to answer or restated the above.

What is the point of a “debt limit” or “debt ceiling” if it is automatically raised without debate every time it is reached?

I wish someone (Bueller?) would just ask these politicians just *once*: Who, precisely, is going to pay for all these $1.7 *trillion* dollar budgets?

Do the millenials and Gen Z and their new offspring understand what future they face? I have a nieces and nephews with kids aged 2 through 10 and I shudder to think what their financial futures will be like.

Wolf, thanks for all you do. I know this has been one of your main concerns. Apologies if this rant is off topic!

The kids really are too busy on social media to care. We are raising a bunch of social media crack addicts.

Pavel,

“Do the millenials and Gen Z and their new offspring understand what future they face?”

NO, they do not. Nor do nearly all Americans of all ages. They just want their stonks and houses to go up, damn the torpedoes.

Many Millennials and even more Gen Z don’t HAVE stonks or housing. It’s the Gen X and older that want their assets to go up, regardless of the pain it inflicts on everyone else. Look who is writing all of the trash on WSJ, Marketwatch, CNBC, etc.

I thought that the US income tax system is indexed for changes in the CPI.

So If the CPI increases by 10% don’t all the personal deductions and brackets also increase by 10%?

If that is so the only way to increase tax receipts from increasing income is to have the increase in wages larger than the increase in the CPI adjustment and move people into higher brackets?

Corporate taxes are not adjusted, but I believe that they only make up a small % of US government receipts compared to personal income taxes.

I also think that the entire premise of your article to base the ability to pay interest on the debt against tax receipt is wrong.

The ability to pay interest on the debt is, given the current debt situation in the USA, is based on a couple of things:

1. The ability of the US government to sell debt at a cost that increases less than the increase in those tax receipts.

2. The hope that those increases in tax receipts continue to be big enough to offset the increase in interest payments.

I seriously doubt that the increase in tax receipts will continue to increase as rapidly as the increase in interest payments.

I also doubt that those tax receipts will continue to increase as much as they have been over the past couple of years either. For one, capital gains taxes are going to fall as the value of the stock market in the US falls.

Taxes from gains on real estate will also fall as house prices continue to fall as well.

I seriously doubt that the cost of issuing debt will slow any time soon.

Furthermore, the Fed will pivot. It is a given that it will pivot. It may take 3, 4, or even 5 years from now, but at some time in the future it will pivot.

And nobody knows what the future actually will be like so nobody can say when they will pivot or what reasons they will pivot.

“If that is so the only way to increase tax receipts from increasing income is to have the increase in wages larger than the increase in the CPI adjustment”

LOL, I wish this were so. But it’s not.

I gather you’re not familiar with the US tax system. It’s very complex, so I cannot explain it to you here. But I can give you a couple of basics. So this is super-simplified. There are many elements to taxes, and nothing is etched in stone. So I’m just going to simplify it down to the absurd. But that’s not really how taxes work. If you really want to find out, get a tax preparation software, such as Turbo Tax, and run through some income figures for different years. You’ll see.

1. If you earn more taxable income, you will pay more taxes. Your taxable income is NOT indexed to CPI, LOL. So if your taxable income increases by 10%, you’re going to pay more in taxes.

2. While “income” is not indexed to inflation, some things are indexed, such as tax brackets, IRA and HSA contribution limits, the standard deduction, etc.

3. The effect of this indexation is that when your income goes up by 10% you don’t suddenly pay 20% more in taxes because you moved into a higher tax bracket and your deductions didn’t keep up. The idea is that if your income goes up by 10%, you pay 10% more in taxes, not 20% more in taxes.

4. If your income goes up by 10% from $40,000 a year to $44,000 a year, when CPI is 10%, you pay more taxes because you have $4k more in income (personal income taxes).

5. In this scenario, your employer pays you $4k more in wages, and so he pays about 7.5% of $4k more in payroll taxes (Social Security, Medicare, FUTA, SUTA).

6. Individual income taxes (#4 above) and payroll taxes (#5 above) are the two biggest federal tax receipts categories. And they grow with wage inflation.

7. The “tax brackets” are indexed to inflation to protect the taxpayer from “bracket creep.” If there is 10% CPI inflation in 2023, and your pay goes from $40k in 2022 to $44k in 2023, you would move into a higher tax bracket: meaning, in 2022, all your income falls into and below the 12% tax bracket (below $41,776). But in 2023, with a 10% raise to $44K, the last $2.2k of your income would be taxed at 22% instead of 12%. Indexing the tax brackets to inflation keeps you in the 12% bracket.

8. But even after indexing of the tax bracket, you’re paying 12% on 44K in 2023, and in 2022 you paid 12% on $40k. So you’re paying $480 more in taxes.

9. If the tax brackets were not indexed, you’d pay $700 more in taxes on your $4k more in income, due to bracket creep.

That’s an excellent simplification of the tax system. The key is that inflation inflates everything, including tax receipts. just as you describe very well in point 8.

Yes, Wolf, that helped…and gives me more to mull.

by this twisted logic a wage price spiral would be amazing benefit for the government tax wise!

Yes.

Tax complexity means a lot of individuals play the tax game. I am in sweet spot before RMD’s so I manage my Fed taxes to the number I want like a lot of people.

I roll over enough into a Roth to pay about a $1000 in Fed taxes every year. I am happy living a modest lifestyle and hope that if I end up with a lot of funds I don’t need in old age I can find a really worthwhile cause to leave it to and keep it out of the politicians hands.

How much of the rising tax receipts in years prior to 2022 were due to capital gains on investments, and how much effect on tax receipts will the reduction in market values of stocks and bonds have on tax receipts from 2021? I expect lots of investors, including Nancy Pelosi, chose to harvest losses for tax purposes in 2022, I know I did. What effect on the ratio of tax receipts to debt servicing cost will this have?

So there is something sinister about Pelosi doing it, but not about you doing the same thing? Why even name drop it here? Asking for a friend.

Because Pelosi created/runs the system (such as it disgustingly is) much, much, much so than the poster.

There are those who create the nightmare and those who just try to survive it.

They are not the same.

There are those who create the nightmare and those who just try to survive it

Exactly +1 People in Power need to be named + or – as they are not only the public Eye but in it .

To Expose or express feelings is the Democratic way ? .

The Ostrich with the head in the sand may lead the Country and may not hear But people will Talk and be heard by everyone listening

The increase in govt. revenues over the past few years is stunning. It would be interesting to see a breakdown of the trend by revenue source and also to compare against FICA (capped) and Medicare (uncapped) collections to possibly glean some insight into the sustainability of these wild revenue increases.

OK, we have to agree to stop with the simplistic linear thinking exhibited by so many when the Fed is mentioned. I blame Ron Paul for poisoning so many with the idiotic thought that hyperinflation will be here next year, just like Weimar. For the last 40 fricking years.

Stop with any thought the dollar *has* to be stable. It is floating, and Fed is managing that float through some pretty crude tools. There is no credible challenger to the international trade and buying status of the dollar, nothing, zip- nada. So. Now think. Every single alternative is either waaay too small, or ridiculous like bitcoin. The Euro is even worse. The Yuan is not freely traded, so no China. Japan and Korea, no way. Mercosur- ug no.

Further, the exorbitant privilege continues, as well as setting the terms of trade. The only savvy central bank that has done better is the SNB. So, deficits don’t yet matter. On the flip side, Congress is totally ridiculous. The House will force the ridiculous $1 trillion coin. Now that is a truly dangerous moment, because it would be a huge crack in the PERCEPTION of dollar safety.

Then there is the American Bond Market. Higher interest rates will restore the terror the market used to wield over the US Government, along with a large number of the biggest companies in America. Think the government is the most vulnerable entity in America to rising interest rates? No, the business world has blasted along on low rates rockets for years. Now higher rates are going to wreck businesses with a lot of debt.

And that is the real driver of damage from higher rates. Everything valued explicitly or implicitly from a *riskless* interest rate will lose current value. These lower prices in everything from houses to commercial property, everything is worth less due to simple math. These losses on anything with a long term duration are going to be brutal.

Besides thinking that huge debt is a problem Ron Paul also speaks out against the military industrial complex and perpetual war. What a fricking loser.

I didn’t criticize him for being right about a few things. It is the overwhelming gold buggery that grates, along with the libertarian fantasy propaganda machine. Same reasons why I call Reason Magazine, *Treason Rag*. Simple solutions always appeal to mechanistic minds.

So much MAGA is rooted in the Music Man and Elmer Gantry.

Hold it…so the entity (DC) promising endless “gifts” (on the back of endless debt) is supposed to be the anti-Gantry Music Man?

Really?

Really?!

I think most libertarians are too idealistic. Extreme socialists as well.

That aside, what do you mean by:

“The House will force the ridiculous $1 trillion coin. “

Why would Governments care as the Tax Receipts are way much more than the interest payments ?

We all know they dont care about the people

Why is it a problem for them to to pay debts?

I feel like I am not getting it?

Most everyone with a 3% mortgage should not be too unhappy with 7% inflation.

Tangentially, Bill in Congress wants to switch from income to consumption tax.

Good idea but they whiffed, you have to rebate the bottom half to make it progressive.

And if they did that, inherently resistant to inflation economy.

What if a billionaire with huge US income goes and buys all foreign stuff. Would that be taxed ?

What if she doesn’t buy hardly anything ?

I dont buy much stuff beyond the very basics so it would work for me. But would it be a huge drop in revenue for the government ?

Bye bye SS, Medicare ?

Just wondering…

“Tax receipts spiked by 21.5% year-over-year and by 52% from two years ago. This is what pays for the interest expense”

Wolf, capital gains tax has certainly contributed to the spike in tax receipts. Once the economy eventually rolls over those taxes will dry up and affect the ability to pay the interest on national debt–that is what the pivot crowd in banking on for the Fed to step in and start QE and ZIRP.

In my opinion this time the Fed will have to choose between saving the stock and asset markets or the destruction of the currency, and these people believe that the Fed will choose the former as usual.

The White House has already communicated to Republicans that they want the debt limited lifted without any conditions. 15 Republicans got guarantees from McCarthy that he would become the Speaker only if he did not allow a debt ceiling deal without huge cuts in spending.

A fight is surely to ensue and possibly crash the market, and perhaps Powell will put the blame for a market crash on that.

One party wants to cut taxes but never is able to cut spending and the other is still basically continuing MMT plus with tax hikes that don’t even come close to slowing deficit growth let alone starting to slowly reduce deficit spending. Too many people and companies depend on federal largesse so after the theatrics the republicans will fold.

It doesn’t take a genius to determine printing wealth is not a sustainable policy. When you go too far, it all collapses as confidence in the monetary system collapses.

“printing wealth is not a sustainable policy”

Do foreign governments have the ability to print $$$s (counterfeit), give them to citizens, and send them to US to buy ? Silly me, just buy online.

I know nothing of this but it seems like a very serious matter. They can create the $$$s digitally I suppose as well.

How much of a problem is this currently ? Ever so often I hear of a US organization (govt. or not) out large sums of $$$ due to organized crime.

All this talk about inflation & the real issue is Deflation. Inflation has been caused by supply shock & now we are in a period of demand destruction. When the U.S.D. loses its reserve currency status, it’s game over for the economy. They won’t be able to print debt out of thin air anymore to finance the ever increasing debt burden.

The BRICS are poised to implement a new “gold-backed” reserve currency serving a majority of the worlds population. Trade in $USD will plummet. The petro dollar will no longer exist.

The U.S. government will no longer be able to inflate the dollar to keep the economy propped up. The ponzi will have reached its apex.

Regardless of

OK, but I’ve been hearing this for decades. I’m thinking first I heard it was Pete Peterson in, like, 1970s. Doesn’t mean it can’t happen. But what (aside from the standard, unchanged repetition here) in the facts says it is now? Millions of bucks have been lost taking that bet, for decades. Millions of (wrong) books have been sold.

Would it be fair to use tax receipts as an approximate estimate for real inflation instead of using a basket of consumer items? Except for changes in gdp, tax rate, and population, it seems like it would be a good measure.

Another way to monitor sustainability of debt service is debt to GDP ratio.

Also, monitor the percentage of the discretional budget that goes to debt service, as well as percentage of total budget that is allocated to debt service.

The ratio and percentage have not yet reached the point where taxes have to be increased and/or significant spending cuts implemented.

DEPTH CHARGE,

In their inflation calculations, the Fed might raise the weighting of some components somewhat if their prices rise; however, thanks to hedonistics adjustments (where the Fed claims prices are actually lower arguably due to quality improvements that are meaningless to most people, such as computers with more memory, or cars with more annoying gadgets), the prices the Fed takes into account are rigged from the beginning. When the are dice are loaded from the start, the outcome of Fed/government inflation numbers will not reflect reality.

So ultimately you’re not wrong in your assumption that inflation numbers are manipulated lower.

“Fed claims prices are actually lower arguably due to quality improvements that are meaningless to most people, such as computers with more memory, or cars with more annoying gadgets)”.

How pervasive is this practice ? It certainly lowers one’s confidence in the stated inflation numbers. My computer absolutely does not need more memory; I drive an 1988 car and cringe when I hear about all the bells and whistles that, I guess, can be forced on a car buyer today.

RANDY,

How do you think they get 6-7 percent inflation instead of the 15 percent that it is, if calculated like they did it in the ’70s or ’80s? It’s not just pervasive, it is entirely a fraud, the way they calculate inflation. Lies upon lies.

“The root problem with conventional currency is all the trust that’s required to make it work. The central bank must be trusted not to debase the currency, but the history of fiat currencies is full of breaches of that trust. Banks must be trusted to hold our money and transfer it electronically, but they lend it out in waves of credit bubbles with barely a fraction in reserve. We have to trust them with our privacy, trust them not to let identity thieves drain our accounts.”

Satoshi Nakamoto, February 2009.

So I should trust bitcoin and the entire crypto scam instead?

LOL

//So I should trust bitcoin and the entire crypto scam instead?//

Speaking to Bitcoin, now I am tempted to short it (I bet the price will go down), when possible. Bitcoin is currently around $20K price!

No. Absolutely not. Don’t trust any crypto that requires you trust it, that’d be plain daft, I agree. That leaves just bitcoin, it requires no trust[1].

[1] Can’t say the same about the exchanges you buy through, though. Best pick one that allows immediate transfer to your own wallet. Or use a decentralised exchange, such as Bisq, they never hold your funds.

But you must also “trust” (rather, speculate) that a bigger fool will come along and buy it from you at a higher price. because it does not represent a claim on anything, apart from the confidence of others (or its other “use case,” crime).

No Bitcoin conversation would ever have existed if the G has not eagerly accelerated its bad faith relationship with savers.

Your implicit assumption is that the gubment is free in its decision what to spend the tax receipts for.

That’s wrong. Most of them – all lf them – are already earmarked for some gubment program. Even the ones that do not yet exist.

The idea that any gubment does anyrhing else but “pay as you go and the hell with it” is, frankly speaking, unrealistic.

Thanks Wolf!

The noise in this market is so frustrating to figure out! All your writings, (scolding, corrections) and guidance has lowered the noise and BS. I think I just want the rates higher now! Pronto to 7%!!

1) WTI is down from $120 to $80. Demand for Iranian oil is rising.

2) In the last year oil prices in Syria are x5 times higher.

3) Iran, in the last two months, doubled the price and demand cash in

advance.

4) With friends like that the Syrian people are freezing this winter. Many factories shut down for lack of energy. Syria entered recession, but their sponsor

don’t care.

5) Putin is boasting that the Russian economy is better than expected.

6) Lithuania & Latvia NG pipeline blew up today.

#6: NO IT DIDN’T “BLOW UP TODAY.”

It blew up Friday. Services were restored on Friday at a parallel pipeline. What actually happened:

Friday 5 pm local time: A gas pipeline sending gas from Lithuania to Latvia was hit by an explosion, but there was no immediate evidence of an attack, Lithuania gas transmission operator Amber Grid said.

Amber Grid: “The gas transmission system at the site of the incident consists of two parallel gas pipelines running towards Latvia. The incident occurred on one of them, while the other pipeline was not damaged.

The gas supply to Pasvalys district and other consumers in Northern Lithuania was ensured through a parallel pipeline. Gas supplies to Latvia were also restored the same evening.”

Announced today, Sunday morning, local time: Gas transmission system operator Amber Grid replaced a section of a gas pipeline damaged in an incident in Pasvalys district. During the work, which lasted until Sunday morning, the damaged ten-metre-long pipeline was cut out, a new section was installed and the installation seams were X-rayed. Other sections of the pipeline close to the incident site are currently being further inspected. Once all the inspection work has been completed, the gas supply will be restored through the restored pipeline.

Meanwhile, the parallel pipeline provides the services.

https://www.ambergrid.lt/en/news/pressrelease/amber-grid-restored-damaged-gas-pipeline-in-pasvalys-district-nearby-gas-pipeline-sections-to-be-inspected

Something I did not know was Ukraine is third in natural gas resources to Russia and Norway. Says Daniel Lacalle.

“Lather, rinse, repeat”

This is our world and I suspect it will continue to be until it does not. That’s something we should consider, what is out there that will break this cycle.

Progressive consumption taxes plus capital transfer securities give a stable inflation resistant economy that supports domestic production.

Theorem of Proper Taxation.

Do your interest payment charts take into account the Federal Reserve interest rebates to the Treasury ?

The interest that the government pays the Fed is included in the interest payments (money going out).

The Fed remittances back to the government are included in the tax receipts (money coming in).

Wolf: Former Chairman of Federal Reserve of New York Beardsly Ruml in a speech to the Bar Association in 1946 claimed that income taxes to fund the US government were obsolete due to the dollar no longer being tied to gold. In short the government did not need the income tax for its support. That the purpose of income tax was no longer to fund the government but to control inflation and to re distribute income.

What are your thoughts on that?

It was simply a smart man seeing the first whiff of Exorbitant Privilege, which the former head of world trade has enjoyed for over a century. How long does the US dictate terms of trade for the world? That is how long the dollar has to be The TRADE UNIT and reserve currency.

I don’t see a viable end to that. Above is a further lol comment about a gold backed BRIC currency- a Russian fantasy- like the Chinese or the Indians would ever let a foreign power dictate the value of their money. As for the Brazil part, eh, really?

As Wolf points out, lol, BitCoin.

Now tell me some real choices that don’t involve Congress coming to reality this year. Our long term five to ten years involves strangling inflation and then the boom after they finally start lowering rates. That boom is going to be epic, but the starting point is the hardest part. The Fed has told everybody what they intend to do, and the hard part is you just have to watch the chips fall. And fall, and fall. The housing crisis never really ended. Remember when CR posted the question of when we would see the return to the peak of housing construction seen in 2005? The answer was never. hence our housing shortage and high prices.

But in flyover country, there are really cheap dilapidated houses that need people……

Someday this war’s gonna end…

To me, the concern isn’t so much that the dollar will be supplanted by another currency, but that people worldwide won’t want to hold ANY currency, and will insist on real assets.

The U.S. is only “strong” relative to other fiat currency.

Treasury-Federal Reserve collaboration like in 2020-2022 didn’t previously exist after the 1951 Treasury-Federal Reserve Accord, because whenever in the past the FED’s responsibilities were subordinate to the Treasury’s, this country experienced intolerable rates of inflation.

Just a couple observations about tax bracket indexation and cpi:

1. the Trump tax cut of 2017 changed the cpi metric for indexing to the “chained cpi” which will subtly move income tax payers into higher brackets if their wage increases ever actually regularly increase by cpi-u.

2. the “combined income” thresholds for taxing social security benefits have never been adjusted for any measure of cpi since they were first introduced decades ago.

The velocity of M2 (V 0f M) money vs. the lagging CPI rate shows a historically similar pattern with Vel. of M2 leading the way by about 3-4 months.

“Money velocity drives inflation because the more times currency changes hands, the more robust the economic activity, thereby increasing competition for goods and services and driving prices higher. M1 money understandably has a higher velocity ratio than “stickier” M2 money: a one-dollar bill in your pocket, for example, is much more likely to be “turned over” in a transaction compared a single dollar held in your savings account.

A particularly important distinction is that money velocity is not constant, as it is made of up of multiple parts. In fact, the most recent velocity of M2 money supply registered 1.191…well below its 50-year average of 1.7811 and its 10-year average of 1.4060.2”

The 2-3 years of pandamoneum pandemic (PP) shows a the big spike in v of m2 and CPI. However the past 3 months shows a huge drop in V of M.

This data was obtained from a First National 1870 Market Commentary.

I am thinking the graph will resolve itself when the two lines on the graph meet again over the next 5 years with interest rates around 5%.

Just a guess, but I find the data interesting

GC gold futures weekly reached WTC Sept 11 2011 high. It might be breached for fun and entertainment.

In order to move higher there must be a close above Aug 3 2020 high.

If GC fail to close above Apr 18 2022 high, it might turn down after forming

three top, indicating lower/or negative y/y inflation ==> deflation.

Keep it simple : if u bought a house for 300K in 1995, sold

in May 2022 for 1M, u pay taxes on 700K, because realized gains are not indexed to the CPI. The IRS is positively biased !

This is a perfect example of the point I made earlier about people not thinking in terms of inflation adjusted dollars. If you bought a house in 1995 for $300,000.00 the inflation value of that investment in 2023 dollars is $576,092.52 so your actual capital gain is $423,907.48, not $700,000.00. The IRS is taxing you for a supposed $276,092.52 capital gain that does not exist. There is little difference between this and having the IRS impute an additional $276,092.52 to your paycheck without telling you what they did or why and then just sending you an additional tax bill to pay or else.

But you’re paying for those inflated capital gains taxes with equally inflated dollars. So it washes out, no?

That’s the thing about inflation: the dollar loses purchasing power, and this affects everything that is denominated in dollars.

Collections from capital gains have gone up almost 40% in the last 2 years. I’m guessing that’s going to drop precipitously for 2023!