Cutting prices on dropping unit sales causes revenues to plunge.

By Wolf Richter for WOLF STREET.

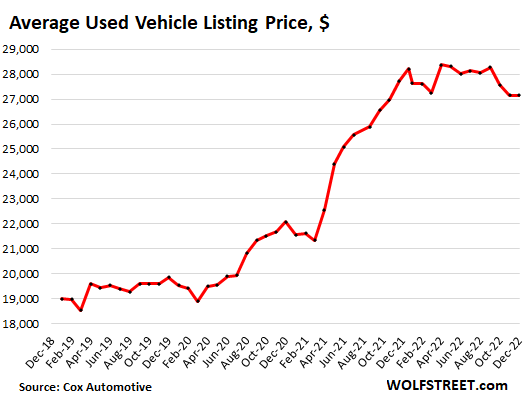

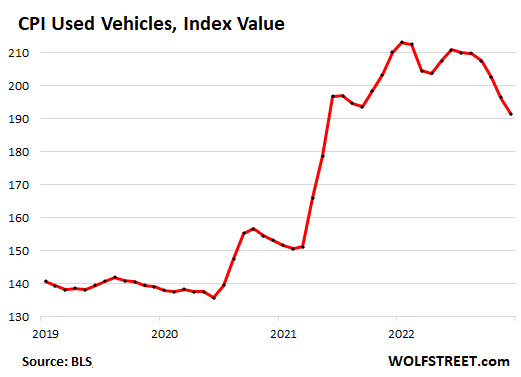

The used-vehicle market now has a huge hangover: The price spike from August 2020 till early 2022. Over this period, retail prices spiked by mind-boggling ridiculous amounts – 40% per the average used vehicle listing price, according to Cox Automotive; 53% per the used-vehicle CPI, according to the Bureau of Labor Statistics – though there never was a shortage of used vehicles.

But now there is increasing resistance in the market against these prices, and used-vehicle retail sales in December dropped 10% year-over-year, to about 1.29 million vehicles, according to Cox Automotive.

Wholesale prices – reflecting the cost for dealers – have dropped 15% year-over-year in December, according to Manheim, the largest auto auction house and a unit of Cox Automotive.

Retail prices have dropped too, but have been stickier than wholesale prices, as dealers are trying to hold the line and slow-walk this process.

The average used-vehicle listing price dropped just 4.3% in December from the peak in April, to $27,140, roughly unchanged from November, and down 3.8% from a year ago, according the Cox Automotive. But that’s far less than the 15% drop in wholesale prices.

Just three years ago, in December 2019, the average listing price was $19,900. It’s hard to wrap your brains around these kinds of price increases. Most people can continue to drive what they already have, but that they chased after these prices in this manner is one of the big phenomena that developed during the pandemic.

And dealers made hay while they could, and bid up wholesale prices at auctions because they were confident they could sell those vehicles at even higher prices because consumers were suddenly willing to pay whatever. And prices exploded higher. But now is hangover time.

The seasonally adjusted CPI for used vehicles in December has dropped 10% from the peak in January 2022, and 9% year-over-year. It’s still less than the 15% drop in wholesale prices:

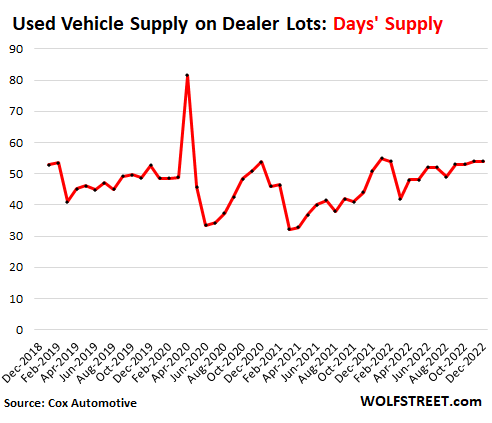

Independent dealers (such as CarMax and Carvana or the small dealer at the corner) and franchised dealers (such as Ford dealers) ended December with 2.32 million used vehicles in stock, according to Cox Automotive, which is plentiful, given the decline in sales.

At the current rate of sales, supply in December remained at 54 days, same as in November, and up from 53 days three years ago in December 2019, and up from 48 days on average in 2019:

Hangover time for used-car dealers.

During the era of the price spike, enough American used-vehicle buyers, for the first time ever, were willing to just pay whatever. Now, fewer used-vehicle buyers are willing to pay whatever, and more buyers are resisting those prices and are looking for deals, and unit sales have dropped 10% year-over-year, and dealers are having to deal with a nasty hangover.

Dealers have already dialed back their enthusiasm at the auction, and so wholesale prices plunged 15% year-over-year in December. This means that their costs of new inventory are going down. But they still have some inventory that they bought a few months ago and that is now getting stale and that they’d paid too much for. So that’s an issue they’ve got to deal with.

When dealers cut their retail prices to stimulate sales or halt the decline, their dollar-sales will go down even if unit sales stay the same. And if they cut their prices, and unit sales still decline, then their dollar sales plunge. And this is now happening.

For example, CarMax, the largest used-vehicle dealer, reported a 24% plunge in revenues in the quarter ended November 30. Its gross profit plunged 31%, and its net income plunged 86%.

Cutting prices in the face of falling unit sales is the hardest thing to do because it entails a plunge in revenues. So dealers attempt to hold the line as long as possible, which makes retail price sticky on the way down.

But prices have spiked so far, so furiously, that holding the line for long isn’t possible. In addition, interest rates have risen, and more potential buyers are resisting those prices. For buyers, patience will pay off. And for people who bought in 2021 or in 2022, well, it’s not the end of the world; their vehicle is just depreciating a lot faster than in normal times.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Looks like the simple law of physics is finally in effect. I can finally buy a decent vehicle for my college bound kid.

Yes prices are coming down on cars over 25k but if you want something nice under 15k keep dreaming

My old truck finally died last week at 180K hard northeast miles and 12 years of no payment. I thought I could find a reasonable winter beater for around $5000(may need a little work but no major issues). I am a competent shade tree mechanic (repaired all my cars and maintenance always) and I was hopeful.

NOPE, NO WAY, NADA!!

What I have found is patently absurd for the price. When I moved my search to max $10K I was still over 125,000 miles and literally strewn with garbage and once in a while you find something actually properly maintained.

I am borrowing an extra car from family and waiting this BS out now, and I am very fortunate to have this ability. I feel sorry for anyone who needs a car today

I was in a similar situation about 7 years ago when my pickup blew a head gasket after 16.5 years of reliable daily driving. Luckily that’s before the world went crazy, so I was able to find a decent 1997 Honda Accord on Craigslist for $1,900 (19 year old vehicle at the time!) With some minor home mechanic work, that car limped me along for a few years until the wife got a new vehicle and I took her old Civic as a hand-me-down.

Then I decided I need a truck again for home maintenance projects, so I placed an order for a midrange Ford Maverick ($24K) in July 2021. 6 production bumps and multiple delays later, my initial order is finally getting built next month, February 2023, with an estimated delivery of March 2023, a short 20 months after my original order date lol. At least Ford gave me a “special offer” of bumping me up to the 2023 model at the cost of the 2022. I’ve been hauling lumber and materials in my hand-me-down Civic with the seats laid down in the interim.

Joe. Here in SE under $12k used 4X4 full size pickups are falling now and will fall faster in next 3 mos. I am in market for under 150K miles on F-150’s and every day the search engines I use report price drops…..just waiting them out. The recent additions to the used list are cleaner, in better shape and lower mileage. They are now concerned they waited too long…..which they did. My price range for above? $5500 to $7500. Smacking my lips.

Way, way too soon to buy. As the article states, retail prices are barely off their highs.

So as the Fed returns to a (relatively more) sane policy, prices retreat from the WTF runups and overhands, in cars as in houses. the pain is for those who bought late, and overextended. Supply and demand start working more normally. Bravo! I’m just sorry for those not positioned to wait, during the crazy price runups.

Saw a reputable guy say by his model CPI will be around zero in 6 months due to the lag in housing data.

It wouldn’t surprise me as M2 has dropped really quickly. He also uses a 3 factor model for liquidity with M2 being the largest factor as a leading indicator. Things are going to look a lot different in 6 months. I think bond market has already sniffed this out.

Care to share how accurate this model was 6-12 months ago?

Bond market is likely making a floor for the next move higher

You don’t get overall inflation without excess money. M2 growth rate blew up from trend rate of around 6% to 20% plus. It is falling through zero right now heading negative.

But the leading economic indicators are saying recession is most likely weeks away.

3 month / 10 year inversion has never been wrong at predicting an imminent recession.

Copper/ gold ratio says 10 year too high

Recession will be nearly over by the time it shows up big in unemployment numbers as that is a very lagging indicator.

See my response below. That reputable guy is probably trying to screw others as he rotates out of his shit into commodities, and you buy his shit hoping inflation will fall to gather big losses.

Conflict of interest.

Let’s assume, for the sake of argument, that this is true. Wall Street seems to be convinced that if inflation drops back down to 2%, it’ll be time to lower rates and start printing again.

I’m skeptical. For many years, ZIRP and QE was sold as a way to help the economy. I think the COVID response has led to there being a larger sense that ZIRP and QE benefits the stock market and housing prices, and nothing else.

In other words, I don’t think that era is coming back. I think the political pressure will be too great this time, and that’s not just in the U.S., but throughout the developed world.

Therein lies the rub. This is arguable the first time in the last 20 years the Fed and government is doing the right thing. Now that said, 1%’ers are taking it on the chin. They are crying the loudest. Given the government represents the rich, I keep expecting that pivot. So does Wall Street.

Inflation blows out big time but what do they care about the common man?

I agree. Even if the Fed stops raising or even lowers rates, it doesn’t mean we’re right back to ZIRP and QE. Given the current inflation disaster, I suspect those policies are out except under very dire circumstances which no one should be hoping for.

Einhal- I really hope you’re right, but fear you will be wrong.

The Fed is glued pretty much to the rich guys, not the ones working at Walmart–or even the middle class as high as the 90% wealth level. When the top 1% guys and banks start to yell about how terrible it will be for them, unfortunately I think somehow their desperate cries will be the ones that the Fed will believe they must save. Look what happened in 2007–you will hear “they absolutely had to give them more cash to save the whole world from financial disaster. “

Einhal has it right. Seems clear to me the fed was uncomfortable with QE and ZIRP for years even before the pandemic. On top of that. ‘respectable opinion’ is coming down against not only QE but QE *retroactively*. It was paywalled but Bloomberg ran a big opinion headline to the effect that QE was not worth the damage it caused. This was a few months ago and I am still gobsmacked.

And no, the fed does not work for ‘the rich’ and no, ‘the rich’ are not some monolithic hive mind. Many of ‘the rich’ are much worse off for QE and ZIRP particularly banks.

Altogether there is little reason to believe we’re going back. I am inclined to think that the more we leave the cheap money era behind the more comfortable and happy everyone will be with leaving it behind. The novelty of a serious GIC return for one thing!

so my son is in NEED of vehicle

old one has no AC, was in minor accident 6 months ago(other guys insurance not even making offer so they got lawyer)

worth maybe $3k on trade in

thought they found one on internet(local dealer)

they go there and try making deal only to find out it required they finance thru them with massive fees, etc.

of course bank of papa only makes 1 payment – and I get 3%

On the south side / burbs of Chicago if the AC goes you just keep driving it without a shirt on in the summer. Next time it’s 90+ degrees out and see an Illinois plate out of state, look at the driver.

I see what he is saying, but the fed will shock and awe by going back to 75 instead old 50 or 25 basis points.

The graph of the CPI with the huge drop in Velocity of M2 (VofM) will reach a new equilibrium well after this first big drop in VofM shown recently.

VofM will meet CPI at a permanently higher inflation rate than has bee seen in the past over the next 5 years. The new unnormal normal will show the CPI and VofM again following the same path with the CPI lagging 4 months, and a long term higher inflation rate.

It would be nice to see a chart of this to see what happens with the fed fund rate as a 3rd variable

Why? Why any of this? Where has Powell or anyone come out for higher inflation?

He’d rather have higher inflation longer term than deflation.

The price that will be paid for too much money created from nothing.

The rich would rather inflation than deflation. They own the assets.

Oldschool, that reputable guy can’t be more wrong.

CPI is not affected by home prices. It’s based on “equivalent rent shit”, that allows Fed to keep pumping housing through MBS purchase. Fed is still not selling MBS and is afraid to even talk about it.

Rent is a service and service inflation is still running high. Also CPI today doesn’t even account for rent increases due to another shit prorated model that BLS uses, that means that CPI increase from rent has a long way to go.

Bitcoin crossed 20K and now the scammers are already giving targets of $50k to $100k.

All this tells me that inflation is going higher in 6 months!

Fed was too late and now all options are very painful for middle class and working class.

Agree. Inflation not going away anytime soon. It will take years. Just received both Gas (Heating) & Electric Bills for last month. Usage was slightly lower for both YOY. However, Gas Bill increased 82% and Electric Bill increased 93%. It’s going to take quite some time before the consumer Stops getting hosed. These times today are Far worse than the’70’s.

Natural gas is down about 60% from this last summer.

“Inflation not going away anytime soon.” Inflation will go away when they (the Fed) say it will go away. To many people trying to use reality to form their conclusions.

@Apple – what counts is the wallet-pain. Most people use hardly any NatGas in the summer, so high prices didn’t hurt. High prices in the winter will dent wallets enough to shift thermostat settings and curtail other spending, except on sweaters.

If the Fed goes 25 basis points, the inflationary embers will be stoked; the inflation lovers are looking for a catalyst.

The M2 reading will probably not not be the conductor of deflation at this time. The vix still sleeps

They need to go 75 again. Sentiment drives prices and inflation as much as anything. As Wolf has highlighted in this article, the “pay anything” mindset ran prices up over 50% on used vehicles. It was not based upon low supply, which there was plenty of.

The same thing is going on in commodities, stocks and other assets. There is too much bullish sentiment based upon expectations of a FED pivot and the real kicker – waayyyyy too much money still sloshing around. They goofed when they cut back to 50. They know, they just would never admit it.

Pretty sure the fed is letting MBS roll off. 95 billion a month is nothing to sneeze at.

So true, like to see them do the “real” opposite of QE and sell MBS outright not just let it roll off, that might give the RE market the nudge it needs, and the rest would follow.

95 billion a month might have been the dream when they started, but it’s not anywhere close to reality.

It you look at the Fed MBS holdings, they’ve dropped about 100 billion since the peak in April 2022. That’s nothing relative to the 2.6 trillion they still hold.

If you consider the real roll off to have started in September, that’s still only about 25 billion a month….100 months to go?

Total assets are down $450 billion from the peak, including, as you said, about $100 billion in MBS. The Treasury roll-off hits the cap of $65 billion a month every month. The MBS roll-off is not hitting the cap of $35 billion, running between $15-25 billion a month, as pass-through principal payments from mortgage payoffs have collapsed.

Stay tuned. Y/Y CPI is extremely lagging due to the way housing is calculated.

Housing CPI is NOT lagging. That’s a red herring. The CPI rent index reflects the ACTUAL RENTS that these tenants paid during the survey period, and how they compared to what they paid earlier.

What you’re thinking about are “asking rents” (advertised rents, such as the Zillow rent index), and the spike in asking rents never even made it into actual rents, so actual rents didn’t spike when asking rents spiked. CPI reflects actual rent increases, paid for by actual tenants, and people are getting actual rent increases, even if asking rents (advertised rents) have stopped spiking.

“Housing CPI is lagging” is one of the worst pieces of nonsense out there right now.

All the people that are seeing rent increases would disagree with you.

I don’t understand this bs narrative.

What part doesn’t make sense???

People can’t sell there home right now because of declining demand and higher rates so they rent it out based on what they wish they could sell it for or they try to rent it out for that. Steering the crazy home mania into renting.

People I know are doing this, the people I’m renting my current residence from are doing this and when you look at Airbnb’s there is a lot of new listings.

What’s lagging is the inevitable need for higher rates and lower housing valuations to then turn into less rent increases.

This is going to take time because people like you are stubborn and greedy.

Weeks away from a recession??? Ha

Not with 10.5 million job openings and 3.5% unemployment

We’re weeks away from another interest rate hike… Idiot

When you consider that the Fed still has 8 trillion of debt on the balance sheet, you have to reconsider whether Fed policy can yet be called “sane”. Plus the fact that they have a unrealized loss of one trillion on that debt means that they simply cant liquidate the balance quickly and must let it roll-off (unless they want to realize those losses).

The FED can lose as much money as they want. They have a printing press.

Last paragraph:lone->long

Great article!

Nitpick edit — because I love your stuff. But no hard feelings if you delete it.

“holding the line for lone” = long.

This is what happens when the masses get free and or fraudulent Covid $$

Yes, that’s what always happens when the poors get money.

“The poors,” as you call them, were not the major recipients. PPP loans for the wealthy, and asset price spikes thanks to trillions in QE, resulted in the top 1% gleaning over 75% of the entire largesse.

Funny how this works…hopefully these greedy dealers, especially the ones that are still asking sky high prices now instead of cutting their loss and get out while they can will take in the chin soon enough, much like home sellers that are still dreaming of prices from last year even now.

Cherry on top that Tesla is now cutting prices, surely won’t be doing the market any favor. Really funny to me seeing Tesla FOMO buyers that bought in early Dec of last year, how does that FOMO taste now?

They probably don’t care or are oblivious to MSRP. The upper middle class is full of such poor consumers these days. They’re likely more concerned with getting what they want and the image they are projecting. Consequence of too much money floating around the type of people that mainly buy Teslas.

Many of them lease… so it’s only the monthlies that matter. MSRP going down wouldn’t affect the payment much as the residual on the higher MSRP would offset it.

It’s those who bought during the pandemic (I saw a used 3 YO Tesla on the showroom floor of a dealership @18 months ago for above Tesla’s new MSRP – the excuse was “we have one and you can’t get one from Tesla) that took it in the kazoo.

A friend of mine had a Range Rover… he bought the vehicle for residual and immediately flipped it…. cleared $18K after paying sales tax on the purchase, plates, etc.. What did he do? Pulled out his 17 year old BMW 6’er and drove it for the past 10 months. You can pay for a lot of repairs on a BMW with $18K, which he would have done anyway because – as his wife says – they’ll bury him in that car.

Imagine being the poor schlub that paid over list for a 3 YO Range Rover that spent more time on a hook than it did on the road under it’s own power.

Your friend is smart, but his wife is smarter !

HaHa flippin cars, lagging flippin houses.

I’m sure my wife thinks she will bury me in my 01′ bmw (bring my wallet)

Actually, he *flipped* one car because it was entirely too juicy. Blame his SIL who put him up to it.

Thanks for your informative posts on the auto business El Katz. Always interesting.

Why does someone’s misfortune/regrettable decisions make you happy, or make you think it is funny?

Because those people’s “regrettable decisions” did severe damage to society. Their stupidity didn’t just affect them. Collectively, THEY are the ones who have driven housing prices into the stratosphere out of reach of many normal people. THEY are the ones who made it such that a 23 year old out of college can’t afford a basic car.

Had people not latched on to FOMO, the inflationary mindset, and other destructive habits, inflation wouldn’t have taken off like it did.

It makes me happy when people who do bad things are punished for it.

Exactly, if most people that have money now or had money last 2 years can actually exercise some level of self restrain we probably wouldn’t be where we are now will asset prices in cars and houses wildly overpriced. Then again here we are so exercise me while I express a little joy in seeing these same people now pay the price while the whole time I grinded and stayed patience even though I easily could have participated in the collective hallucination.

Hopefully my dry powder will come in handy soon when I get a good view of seeing who’s been swimming naked all these time..

Buying a repossessed property is a business deal. If it saves me money, it makes me happy. Nothing personal.

These are all just business deals. Wolf points that out that there’s always two sides to a transaction… and one or the other wins.

So, it’s not “joy”, it’s more an affirmation of a personal strategy to use your money wisely – even if people think you’re “cheap” because you’re savvy enough to walk away from a bad deal.

ElK – well said. Could be why the overused term ‘win-win’ is misinterpreted and that result assumed to be more prevalent than in reality.

There ain’t no magic, other than our apparent undying belief in it (ref: Wolf’s coinage of ‘CH’…).

may we all find a better day.

And the older you get, esp. very old, you don’t really gara about what other people think.

@mmc1968, I like that somebody actually asked this question. Good on you.

Just curious. How much money did a typical recipient family receive in Stimmys? How about a small business owner PPP grand total? (My family received none, and no PPP). But it must have been considerable, for folks to drive up those prices that quickly. Amazing.

I know of a small business that raked in huge PPP $$ that they ended up NOT NEEDING, which was ultimately a huge handout to the haves. Sad, really. We’re all paying for that gift to the well to do right now via inflation.

That was Congress’ stupidity for not requiring that businesses show they lost revenue to have the loans “forgiven.”

I get that it was a rapidly changing situation, and I can understand not having those requirements to get the money out the door quickly, but if a business didn’t lose money, they should have had to pay the loans back.

The fact that it was a rapidly changing situation is no excuse. They should have had all this stuff all planned out before a crisis starts. A competent government doesn’t just think of something like PPP Program off the cuff, then try and implement it without any checks.

What are these 2,000 PhD’s doing all day?

PPP was huge for small and midsize companies. Not the best use if the one of the goals was to deflate the income disparity,

however, if I was a young man with a growing family and my ppp employer gave me a big raise, I’d be happy. It is all relative.

The small mom and pop shops and low income areas did not get that help from the fed/banks. There could have been a push for vetting small low income areas by the gov./fed/and banks, but there were just words.

The banks gave the money to their best customers.

PPP employers didn’t give anyone raises, they cut to the bare minimum needed for forgiveness and paid themselves huge, record-setting (for the company) dividends.

I saw it with my own eyes, multiple times, with the line of work I was in at the time.

Many of them got to double dip with the ERC too.

My brother got 300k ,loan forgiven bought a house with proceeds

Same with other companies. Look at the airlines, Southwest, billions in forgiven PPP money and didn’t spend a dime on software to be able to schedule their planes.

AA, Delta, UA, billions in PPP they used to offer early retirement to their senior employees and then don’t have enough to run their operations.

The airlines did not get PPP loans.

They got $50 billion specially allocated to them by Congress.

My old business partner bought all kinds of toys. I’m the stupid guy for being ethical. He looked at me like I was speaking another language when I told him I just didn’t need the help like others did.

Phil – this.

may we all find a better day.

PPI was based upon business revenue (not bottom line), and the number of workers.

Any business that employs hundreds could collect a lot of money, and any business that was not actually impacted negatively by COVID (think private practice doctors, construction) simply pocketed all that money and carried on.

It was also tax free, so if you had 10x employees working for you as a medium-sized contractor, then you just took in $200k+ in total PPP funding that you can punt into whatever you want with out consequences come tax day, or to your normal bottom line.

This small manufacturer took $0.

We did apply for a “just in case” loan and were approved for $500K, but we didn’t need it. We didn’t apply for the PPP, and everyone in this office made too much to get the welfare checks.

We crushed it in 2020 partly due to the economy being flooded with welfare checks, and our state was the last to close and the first re-open.

At the end of 2020, we were scrambling to get rid of about $600K, so we didn’t get taxed.

Just in PPP loans, something like $800 billion was handed out. Then there were other emergency loans (someone I know got an EIDL of over $1 million for a nothing-business). Then there were the stimmies, the extra unemployment benefits, the eviction bans and mortgage forbearance programs that allow people to spend their money somewhere else, then there were the stimmies and programs that state government paid for with federal pandemic funds, etc. etc. That’s just the money consumers got. Then there was the money that big corporations got and spent – including on employee buyouts which these employees then spent, see the $50 billion for just a handful of airlines…. This was a huge gigantic amount of money that was suddenly flooding the land.

There is a lot of discussion of the damage caused by COVID, but the damage was actually cause by the govt reactions to COVID and the forced shut downs of the economy and supply chains, none of which was necessary and none of which a single one of them will ever be held accountable for.

The excess deaths from 2020-on in the US are well over 1.5 million people — this with the lockdowns in place. (I work in healthcare, and I personally know three providers who died) These lockdowns kept the healthcare system from collapsing and allowed opportunities for the vaccines to be developed without mass casualties.

The idea that none of this was ‘necessary’ is such an insult and so f-ing stupid I never bother to respond to trolls like you when I read their covid Hot Take online, but because I think this is a decent site, full of decent people with actual things to contribute the the conversation, I am making an exception. I’m 100% sure that twenty years from now the world will somehow still be reading this garbage online – but please be sure to understand that anyone who knows anything, who actually did anything to help, thinks you are a titanic loser.

Zagreb, I worry that you’re reading too much into Isaac’s comment.

He didn’t say that all lockdowns were unnecessary, he said that forced shutdowns of the economy and supply chains were not necessary. There’s a lot of daylight between those two statements. He’s saying the economic damage was caused more by poor policy reactions than by the actual disease – which history is going to agree with.

The healthcare system absolutely needed to be protected, but that doesn’t mean that the entire economy needed to be shut down. There were MANY options to minimize damage to the healthcare system from COVID; the ones we chose were often not the best. To protect the healthcare system, one mainly needed to isolate the elderly and others at high risk, but for everyone else other methods beside lockdowns would have sufficed. Some nations did much better at this than others.

What I’ve read suggests that around half of the US’ excess deaths are not due to COVID at all, but other medical issues that people weren’t able to take care of because of the COVID policy responses. Most of that non-COVID half could have been avoided.

Also, absent the overzealous economy-destroying lockdowns, most of the “stimulus” payments would’ve been unnecessary as well. And then we wouldn’t have the social injustice of scammers picking the pockets of the Federal Government at public expense, nor the resulting inflation from having wasted waaaay too much money.

In hindsight, a lot of the choices made by humanity were pretty dumb. But perhaps we should be glad that the damage wasn’t even worse. And we should be grateful that the healthcare system didn’t crumble. It’s tempting to add COVID healthcare workers to the honor rolls for Memorial and Veterans Day – that war against disease is at least as important as any of the military conflicts!

The COVID was real and dangerous but the response to it caused a lot of unnecessary damage. Kind of like an aberrant immune response to a pathogen causing pathology.

The nations to emulate more or less were Singapore and South Korea. The latter learned so much from the MERS outbreak and as a result their COVID response was primo.

Get off your high horse and wake up.

Thank you ZagrebZagreb — that desperately needed to be said.

Zagreb,

I spent 6 months in the Covid ICU (RN) at a level 1 trauma hospital in Philadelphia. The deaths were real, the fear was real, and we did not know how to handle the cases in the beginning, as all our usual critical care intervention(intubation/sedation/IV ABX killed them. You would STAT intubate and 2 hours later you were coding them. The worst part was no family allowed so these people died alone and the efforts at resuscitation was not nearly as vigorous as pre pandemic resuscitation attempts.

There was a logic behind abbreviated resuscitation attempts, since we were at risk of infection and dying as well, and we were the last line of defense. But many people died because we allowed it, horrible as it sounds(and was).

Every day I came home and worried I would spread covid to my family, it sucked.

As a side note, most of the people who died had co-morbidities that made them VERY FRAIL to covid. And many people put off regular HC needs to avoid hospitals which caused more deaths. I am not sure how often Covid was blamed for death when in reality the death could have been due to other conditions already present, but I am sure it happened.

Look at the bright side, Dave. Iatrogenesis has been a major part of health care delivery for thousands of years, and you are in one of the very very few strong unions presently left.

I agree with you, but don’t ride in any convertibles in Dallas.

History has shown that it was a conspiracy to sy it was not a conspiracy!

Totally agree. It was shameful what they did, and it is coming to light slowly.

Totally agree

Looks like we’ll need a new ‘Cash for Clunkers’ type Federal program except this time to bail out the dealers. Hell, why not? We gave don’t-worry-about-paying-us-back money to just about everybody else, even if we borrowed the money to begin with. But I admit it would bring a tear to my eye watching them crush up stuff nicer than what I’m driving now.

Might be able to throw a student loan on the back seat while it goes in the crusher.

Many of the dealers already got their stimmy money in the form of PPP loans. Time for them to give some of it back.

I recall the last Cash For Clunkers program paid $1500/vehicle.

I’d happily buy it back for $2k now.

Wasn’t it $4,500?

@Crazy Chester,

“But I admit it would bring a tear to my eye watching them crush up stuff nicer than what I’m driving now.”

Lol! isn’t that the truth.

Wake me up when index value retreats to 140 pre pandemic level.

And it seems a sub compact type I would be interested in are hard to find (new or used it seems)

Patience is a virtue

(What’s up with BTC? Won’t lay down and die)

Takes a little bit to boil away the feathers on some of those larger turkeys.

Sucking them in one last time for exit liquidity.

“(What’s up with BTC? Won’t lay down and die)”

Did you miss the fact that “Mr. Wonderful” from Shark Tank lost a boatload on the FTX collapse, and that his buddy who sits in a chair next to him, Mark Cuban was out shilling for BTC shortly thereafter, slamming gold? Interface that with the fact that more than 75% of all of the “stimulus” went right into the pockets of the top 1% and it doesn’t take a rocket scientist to figure out what’s propping it up – billionaire crypto speculators who are angrily manipulation the price to not lose even more.

1) In mid 2020 dealers parking lots, including safe parking lots, were loaded with brand new and used cars to the rim..

2) The CPI of used car reached it’s lower point in mid 2020.

3) Within few months inventories flipped from peak to 30 days. Dealers made tons of money selling used cars, especially pickup trucks.

4) In 2020 crude oil futures slumped to minus (-)40. Price reached $120 in mid 2022.

5) BART fart. If we enter recession dealers inventories might test the peak. Dealers will cut prices, sell at cost or below cost, to liquidate what they got. Many bad items on dealers lots indicate that they might go out of business, but BART and NYC subway will keep running.

Car dealers do not make money on selling cars any more. They are salespersons for the financialization crowd that buy the car loans once the ink is dry and package them in an Asset (Auto) Based Security with AAA rating no questions asked. Dealers make money on the fees hidden in the loan. No money down and 120% loan to value, you can “always refinance” carrying some “value” into the next loan, sound familiar ? Just ask Michael Burry.

Higher interest rates on other financial instruments and deflation, M2 and M3 shrinking, may bring an end to the market for Asset (Auto) Based Securities.

The crash may ovetake the recession and come first.

Franz – just following the past lead of the banks re: fees, nay?

may we all find a better day.

Which means cash is still king.

Not necessarily true. There’s a lot of factory funny money that flows back to the dealerships. When they add a $5K ADM sticker, it’s profit. When they add “doc fees” that’s profit (can’t legally sell a car without processing the “docs” so how they get away with that is a mystery). The “protection packages” are profit (usually BS stuff that you can buy for $39).

Keep in mind that the profitability of a dealership is easily manipulated, based on rent factor, “management” company fees, the Lea Jet and yacht on the floor plan, number of ghost family employees, and a variety of other factors. The joke was that, if you were in dealership management, you never negotiated a pay plan based on “net” but on “gross” – even at a lower percentage as the “net” is easily turned to zero.

The “doc fees” are the hidden fees i mentionned, the “doc” being the loan to be securitized in an ABS.

It probably won’t ever be this good for car purchasers, but I must report it is an absolute pleasure buying lumber again. Waiting it out was worth every minute. Retail prices are still dumping, there must be a glut. Back up the truck.

I live in timber country and there are lumber mills everywhere. To my knowledge they still haven’t slackened their pace of output, but it is only a matter of time. Then the layoffs begin.

What do you think the effect is on lumber retailers & home improvement stores in terms of profit? Do they hold the prices and capture the wholesale price differential? I imagine that the retailers pass along some of the cost deflation, but they’re in it for the money – no one dressed in a red and white outfit with a white beard – so their margins improve??

My one son is an electrician who used to work for a local mill (large regional company) that supplies places like Home Depot and Lowes. He said that their purchase contracts, e.g. HB, are only six months in duration.

Where I work (government entity) we use a fleet management / leasing company. We lease (20) 1/2-ton trucks each calendar year. This past year, it was Chevy Silverado. These are the base models. We also lease additional vehicles. Our annual average miles per vehicle is roughly 4k.

Part of the program is we flip these 1/2 ton vehicles about each 12 months. We started the program in spring of 19’ and on average paid roughly 4k in annual lease payments after turning in the vehicles and clearing sales at auction thereafter.

We just finished reselling our 2022 fleet. We made 225k to drive brand new vehicles around this past year. That’s insane.

Wolf is the go to Car Man!

High cost of living country and sheet fiat $$, but stronger than other fiat scams, will lower exports and widen the already country-destroying trade deficit. But the washington, fiscal-clowns will keep pumping the country with fake fiat$$$ to slow the onset of the inevitable 2008 2.0 wicked crash!

Color me skeptical about vehicle prices falling back in line with historical trends. The dealers and manufacturers knew there was a contingent of the buying pubic who had been conditioned to be poor consumers. What they didn’t know was how large this class of buyers was. Turns out it is so large that the sweet spot on the profit curve comes with a lot less production volume.

As someone that started tearing apart cars in the driveway as a teenager, and still does several decades later, I can tell you that the percentage of people who work on their own cars has fallen greatly.

Vehicles have also gotten much more electrified and complicated. A side effect of this trend is that they are looked at as appliances and conveniences where luxury of features and comfort matters most to their owners. Which explains the trend to taller, heavier and larger vehicles versus efficient cars with great driving dynamics.

What people want from their cars and their relationship with them has shifted greatly and we ain’t going back.

@Digger Dave,

“What people want from their cars and their relationship with them has shifted greatly and we ain’t going back.”

I agree 100% with everything you said. Regarding the last sentence though, maybe at some point enough people can no longer afford the taller, heavier and larger vehicles.

DiggerD – the ‘appliance mentality’ does more every day to divorce the general population from an active consciousness of the ever-present, harsh realities of our physical environment, frequently resulting in that dreaded term: “…who knew???…”.

may we all find a better day.

If the manufacturers make and sell fewer units – and cut out the cheaper less profitable cars – aren’t they hurting the dealers who make a steady income servicing those vehicles? I mean, a cheap car might not make anyone rich when it is sold, but the service over the lifetime of that vehicle might help make up for it. I’m just thinking along the lines of total cost of ownership. Maybe Wolf already wrote some time about car dealers business model as it relates to parts and service.

I don’t think individual dealerships or groups have much say on which manufacturer models get prioritized or cut. And besides, do car dealerships strike you as businesses concerned about long-term viability? Perhaps somewhere higher up the owner does but definitely not the sales force on the ground floor. That’s definitely “what can I sell now for the most profit?”

But here’s another rhetorical question…If a dealership sells half as many cars as it used to but they’re twice as difficult to work on and thus twice as likely to end up at the dealership for repairs when needed and also twice as time-consuming to repair due to electrical mysteries, won’t they increase repair profitability without having to work as hard for it??

Well I’m not a car mechanic for a living, I have two friends that are car mechanics who run their own shops. When they get in trouble with electrical mysteries they usually call me up because I have a knack for troubleshooting modern electrical gremlins because I have a lot of experience working with controls. If they didn’t have me to help them with these types of repairs they would just tell the clients to take them to the dealerships. There’s quite a few small mechanics that do that already.

Savvy dealers always considered the “lifetime value of a customer”. That’s why some dealers choose not to “pump out” (aka sell out of market) hot vehicles for excess one and done profits. They knew the customer, long term, was worth more than the sale to some clown 1,500 miles away who he’ll never see again.

The loss of warranty work, CP labor (customer pay), parts, and so on.. plus the loss of the trade cycle (in the dark ages, dealers used to run a ledger of “wash out gross” that showed all the revenue generated from the sale of a car. Example: Profit on first sale, profit on trade when sold (and internal labor), then the profit on the trade that comes in on the first trade, etc….. If you look at stock numbers you’ll sometimes see 1234A, 1234B, etc. That shows which deal sired the car you’re looking at. A “P” prefix usually denotes a used vehicle that was purchased (auction, Craigslist, Faceplant Marketplace, at the curb).

Parts and service is where the profit is in the current dealer model. Vehicle sales at times is lucky to bust out – most of the new car dept profit (pre-pandemic) was F&I and aftersale. Car gross was usually influenced by cash incentives and volume bonuses from the manufacturer. Used cars could be more profitable in terms of gross profit because there’s no “used car factory” and the price paid for two nearly identical cars can vary greatly.

Appreciate the answer. “lifetime value of a customer” – exactly.

The goal is fewer drivers and no more car ownership for a large percentage of people, the globalists just won’t say that out loud. The way to achieve that is to make driving so expensive that it is reserved for the well-heeled. They sped it up greatly with this massive inflation zephyr they just dropped onto the world.

Hard materials costs may be coming down, but services inflation still rages. Suppliers are still holding tight to their high prices. I build houses for Habitat and costs are less, but not enough to party about.

Oil and gas prices still way volatile. Don’t believe that the inflation fat lady is singing yet.

Automation is key to reducing wage inflation. McDonald’s is experimenting with robotic drive-through restaurants. The auto makers have been using robotic assembly lines for years.

Some urban areas have bus and/or subway systems. The airlines are faster and in some cases cheaper than Greyhound long distance bus transport, or Amtrack.

@David Hall,

“Automation is key to reducing wage inflation.”

If I had kids, and if they had any interest in Electronics, I would be trying to steer them towards a career in Automation/Industrial Controls.

At this point supply is normal and prices are in a new trading range.

It’s a gully.

I guess CarMax and Carvana are now joining the “bankruptcy equities” club.

When they have to Liquidate everything that will be some religious experience for the holders of those “Auto Backed securities”. Maybe Michael Burry already put up a spreadsheet.

Carvana yes, CarMax no. CarMax is still profitable even now. It has been very profitable for many many years, and it can afford to lose some money, no problem, if it does. They’re the adults in the room. They know how to manage through something like this, and they have the resources to survive – even though their stock gets battered. But Carvana always lost money even during the best of time, lots of money, and now it’s at the end of the rope.

I had to buy a used vehicle in September. The car has been waiting more than a month at tge dealer and tge dealer was quite motivated to sell. Now I understand the reason. That was a smart decision for him.

Interest rates for buyers isn’t the only factor. It also costs more for the dealer to carry inventory.

There is also a limit to how long used car buyers can continue to afford to buy a car at all. At $27K average and rising rates, the pool of potential buyers who can actually afford it must be shrinking.

It’s also substantially contingent upon very loose credit standards.

I saw a local dealer ad this weekend. The featured cars only had payment prices listed ($150-$350). The fine print said the prices were biweekly payments based on an 84 month loan. That’s how people are “affording” these high prices. And they will be underwater almost immediately.

Well, no one get away from this world taking anything with them. Neither do the creditors wait on the other side. So why not leave on others expense? 😉

Sams:

That strategy only works if you die before the debt crushes you.

That is true El Katz, the key is to plan the cash flow to last as long as you live.

There was an interesting book on this approach a while back, called “Die Broke”. Much better than the title should have been “Live Rich and Die Broke” – worth a read!

Advocated for annuities and other measures that would give you a better payout while living (than having a huge pile of savings) without burdening your next-of-kin with any debts.

AF:

Not all of the heavies (large dealerships) finance/floor all of their inventory. They are contractually obligated to have a floor plan for cash draft purposes (manufacturer pays themselves from the dealer’s line of credit) based on their volume potential. These “minimum requirements” cover a variety of things like floor plan, showroom size, storage space, parts space, number of stalls, etc..

A well financed dealer can immediately pay off *most* of the car on his credit line, thereby pocketing the manufacturer’s floor plan assistance (usually enough to cover @3 months on the lot). The dealer will not pay off the entire amount because there is traditionally hazard insurance (usually at no cost to the dealer) that covers the vehicle on the floor plan so, if the vehicle gets stolen, flooded, hail pocked, vandalized, etc., it’s not entirely the dealership’s problem.

The dealer can also control what hits his floor plan by putting himself on voluntary credit hold… but that only works for a limited amount of time due to the dealer agreement T&C’s.

Used cars are becoming one year older each year in the third Qt.

In the first Qt sales slump. Later on, they have to survive new last year models. There are certain cutoff days that dealers must obey. Thereafter

they have to a discounts…

There’s this auto industry finance rule of “curtailment” which requires the dealer to pay down any vehicle on their floor plan once it has a model year birthday plus a buffer of time (2-3 months). The cash poor stores, will dump inventory to not have to tie up capital on the remaining turkeys (which is usually what’s left).

You and Wolf should co-author a book on “Car buying for dummies” or, better yet, “Car buying for those who absolutely hate car buying.”

I used to purchase a new or slightly used vehicle every 2-3 years.

But the ridiculous inflation for both new and used has been a paradigm shift for me as I will now repair what I already own until the wheels fall off.

> I used to purchase a new or slightly used vehicle every 2-3 years.

Why? Isn’t that time consuming and costly when it comes to transaction costs? Part of why I would only buy real estate and cars and never sell.

Because I could afford to; not because it was financially savvy. I also had a family situation that required a very low mileage new vehicle.

Retired at 55 and while I didn’t exactly follow a FIRE plan, it just worked out that way.

Insurance is also a large expense that is not often included in the purchase price of cars.

There are huge risks in driving a beater car like I do. But if the car is paid off you can run liability insurance, I pay just $31 a month. If I purchase a new/used car with a loan, I would be required to purchase comprehensive insurance coverage and my monthly insurance premium would likely increase by $100 a month or more.

By law, I need liability insurance and I currently carry the lowest deductible allowed for property $15,000.

My liability insurance will not cover the cost of repairing/replacing most used cars and a mere fraction of the costs of all new cars.

I carry “full glass” insurance as well. It’s cheap and, if you’re in a state that has inspections, a star in the windshield can cause your vehicle to fail. Here in the desert (and anywhere else there’s gravel), yearly windshield replacements are not uncommon. For what it costs, it’s a no brainer.

You can also get a fix-it ticket in states without inspections – which could cost more than the full glass coverage in inconvenience alone. There is no deductible on full glass….. it’s exactly what it says.

But what about the tripling of your premium if you have an insurance claim?

Lol this guy does insurance.

All these tiny comp claims and people are shopping around like nuts wondering why the annual is too damn high.

Teehee says the insurance man.

Get premium AAA and stop throwing away money on small claims.

The “full glass” is like comprehensive. Doesn’t impact your rates.

The technomobile is on it’s third windshield. My daughter’s CUV is on it’s 5th. It’s 4 years old. We rarely replace it on the first star unless it’s directly in the line of vision or it begins to crack… which can get you a ticket.

Issue is that even if you are one of the mega lucky ones who works remotely, if you have kids in most of the US you need a car.

So you cannot always time buying a used car.

Correct. That applies to some people, those that you mentioned, plus people whose car got totaled, etc. But that’s a relatively small portion of potential buyers who cannot wait. Most buyers have a pretty decent trade-in when they buy, and they could drive that trade-in for a while longer. It’s that large number of buyers who “want to buy” that drive the market, not the smaller number of buyers who “need to buy.”

Horrible government policies have trashed market driven capital allocation so that no one knows where to invest capital. EVs, the next big wave, then what? Facilities and the very energy to charge them already stressed beyond capacity and the main energy sources being closed down.

Meantime the Green crowd burn their bridges as they go. This is a problem of looking at all new tech through rose colored glasses while completely ignoring the significant down sides. Those down sides, come as reality checks later, after the whole thing is a smoking dumpster fire.

The age of a used car on the road is growing. There are two extremities in the market : brand new cars and antique cars. The rest are used cars.

Every third Qt a brand new car become used car. The one year become two years.

The eight/ nine year approach the ten to eighteen years.

The eighteen/ nineteen is almost classic at twenty and the classic become antique at age twenty five.

Every state might have a different range. Wolf can adjust the suggested categories.

I want a good, reliable used ride .. one that also has the gas stove option… ‘;]

Well, not used car news, but farm equipment news just off the Grand Forks News Network:

‘A Supply-Demand Tug-of-War’

The used machinery market remains hot. BigIrons Auctions Territory Manager Eric Kaczmarski says tight supply will continue to keep used machinery prices high. “Prices will remain strong as long as customers still struggle to get equipment at dealerships.” Kaczmarski says BigIron Auctions is coming off a record year. “Our sales were through the roof and we were constantly breaking records every week.”

Land prices for good crop-growing acres in the northern plains has been up quite strongly too.

Was curious to see if demand had cooled & inventory had increased.

Checked a few dealers….still 12+ months out.

The farmers won their “right to repair” suit against John Deere. Should help by reducing the stranglehold the equipment dealers had on the repair market.

One of the new technology applications that Deere was promoting at the recent CES in Las Vegas is pretty cool, but yeah a computer science degree comes in handy.

Herbicide spray rigs are quite wide, and typically the farmer douses everything in the path. Roundup ready corn and beans allow this. A lot of other crops have “traits” in them to allow similar applications.

But using this new tech, as the tractor moves forward fairly slowly, a set of cameras looks at everything and the hardware/software figures out what is a weed to be sprayed & what is part or the row of crops. Bingo, the herbicide is applied directly down to the weed. Much less herbicide is used, much less gets into the food chain and into the field’s runoff.

2023 will be interesting to watch how this plays out, and much of the trials will be done at state university crop extension facilities. (Crookston, Minnesota is one of the prominent ones) My Farm Net News arrives every Monday via email, and I will report back to WOLF STREET when and if any news comes along.

Soon to be viewed on Larson Farms, and Millennial Farmer.

The good ole days of holding the flag for the crop duster, and upgrading to a 4 row head.

Chips shortages kept new and used cars prices high when supply

diminished.

Used car dealers might forge car’s birthdays to survive.

Good luck with that, LOL

A criminal chop shop might try to do that by disassembling stolen vehicles and putting them together differently. Every car has a VIN. The VIN has codes for the model year, the automaker, model, etc. And the VIN is on every legal document of the car, including the title, the registration, the insurance documents, etc. And the car itself has to match the VIN.

If sales slump dealers might get permission to change the year,

keep the VIN, the mfg, the model and the rest of the details, in order to save both the dealers and the mfg, to help them dump last year leftovers…

Hmmm, I understood that comment 100%

Where is the real Michael Engel and what have you done with him?

Dealer’s can’t change the year. Only the manufacturer can by issuing a new MSO (Manufacturer’s Statement of Origin). It was not uncommon for the imports, back in the dark ages, to issue a new MSO, a new invoice, replace the Monroney, and voila… next year’s model! With the laws governing equipment, emissions, etc., changing like socks, it’s kinda hard to do that today.

The VIN is not only on the vehicle, car, title, it’s also stamped into the body in several places as well as programmed into many of the modules on the car. That’s why you can’t go to the boneyard and grab a new DME (Digital Motor Electronics) for your car….. because it likely won’t run. It can’t talk to the other modules because they’re “furreners”. Your DME also has the VIN, the mileage and other particulars related to your specific vehicle. Even my early 2000’s car has this data on the key (not a smart key either…. still has a steering column key tumbler). I didn’t know that until the infamous airbag recall and I watched as the service writer stuck the key into a reader and all the data showed up on the screen – including if any CEL codes were recorded.

Volume is missing from the article:

total Retail

2013 35,815,352 15,794,570

2014 36,664,097 16,462,180

2015 38,023,344 17,604,808

2016 38,602,178 18,336,035

2017 39,399,875 19,345,339

2018 39,428,579 19,596,004

2019 39,966,172 20,942,274

2020 37,305,877 19,824,345

2021 40,552,577 21,196,846

2022 36,200,000 19,100,000

Note total market is back at 2013 level.

Note retail is generally less than half total – expect retail to continue tanking…

Column formatting gets killed in the comments. So let me clarify. There are three columns here:

1. Year – 2. retail plus wholesale – 3. retail only.

Column #2 is kind of double-counting because a dealer buys at auction and then sells the unit retail, and it counts as two sales in column #2.

Note that column #3, retail sales, at 19.1 million was higher than 2016 and prior years.

Also, FWIW, column #3 shows change in ownership of existing vehicles, and mediating and effecting that change in ownership is of course what used-vehicle dealers do for a living. This is different from new vehicle sales which follow production or imports.

Between 2019 and 2022 retail sales are higher than wholesale,

even without the dbl sales. Where are the 19M coming from : retail

to retail flipping ?

Trade-ins.

Finally some great news concerning used cars prices. I have been surfing Craigslist for sale owner for used low mile F150. Private party values are very high as the liens have folks up against the wall. I never seen this many trucks for sale with salvage titles …must be new trend for affordability. I will continue too wait for the fire sale, with more Fed rate hikes and talks of recession by 3rd QT.

Salvage titles aren’t that rare because many of the vehicles cannot be properly repaired and the insurance company simply totals it. If it gets wet, the corrosion on the wiring can get expensive and the car unreliable.

Add to that, the amount of aluminum panels, subframes, suspension components, etc., now in trucks (like your target F150), there aren’t many certified repair shops that have the necessary equipment and expertise to repair it properly. The days of a gorilla with a sledge hammer and a gallon can of bondo are gone.

The real fright of buying a used vehicle with a salvage title is that the safety systems are often compromised. Airbags are expensive and so are the tensioning seat belt retractors (they have a charge in them to pull you back into the seat). You will find, from time to time, unscrupulous people who put a resistor in line to trick the vehicle into thinking that the airbags work and the tensioners are operational. I recently watched a video on how that was done and what it took to discover it.

The electronics are also expensive. My wife got clipped in the RF fender this summer. Should have been a $1,500 repair (new wing, bumper cover, paint and labor). Turned out to be over $8K because of all the sensors on the front of the car that took flight when the bumper cover got launched. One wiring harness…. maybe 4 feet long…. was $85 my cost (I can still buy direct from my ex employer) and the dealer couldn’t even get one (the value of staying connected with old friends). Someone entered a critical parts order for an employee sale. Clerical error, I’m sure.

So much for the out of control inflation hyteria of 2022. As Team Transitory said, it was a supply chain issue. Now , the Fed should stop raising interest rates. It should declare victory.

I suspect that Wall Street wants higher unemployment so they can cheap nannies and cheap uber rides.

The number of new cars in my neighborhood and amongst my friends over the past few years has been staggering and i cannot think of a single instance where it was a “need to buy” situation, and in many instances it was an extra car purchase to add to the stable. “I wanted a truck just for camping”. “I have always wanted a Jeep”.

I’m still on the sidelines with my lexus as I close in on $250K miles. Going to have a few door dings knocked out and replace the floormats and driver’s seat and keep it on the road.

Funny reading this article after I received a call from a car dealer for the first time in ages. Seems they’re starting to get a little desperate.

Adam Taggert of Wealthion is discussing this topic with a car dealer today. You can listen to it on Youtube. The title is “Car-mageddon?? Auto Insider Predicts Car Prices To Fall This Year.”