LNG Glut in China, suddenly?

By Wolf Richter for WOLF STREET.

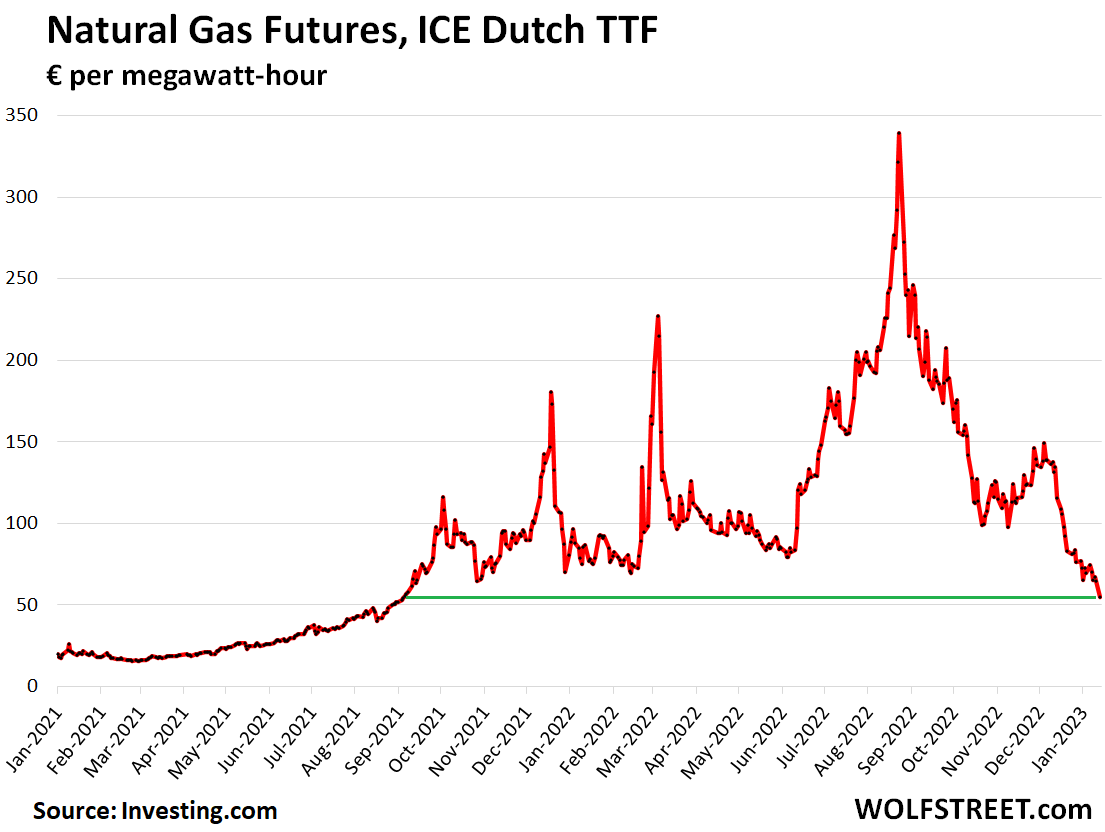

The price of Dutch front-month TTF Natural Gas Futures – a benchmark for northwest Europe – plunged 15% today to €54.85 per megawatt-hour (MWh), and has now collapsed by 84% from the crazy spike in the summer of 2022. The price is now back where it had first been in early September 2021 (data via Investing.com):

What spooked the European natural gas market today into the 15% sell-off were reports that Chinese importers of LNG were trying to divert February and March LNG shipments from China to Europe, as they were sitting on large stockpiles of LNG amid dropping prices in China.

There had been fears that the reopening of China’s economy would put further strain on the global LNG markets. Or was that just hype all over again?

In 2022 and into 2023, several factors came together to avert what had been seen as a potentially dreadful energy crisis:

- Surging supply of LNG from the US and other locations around the world.

- Rapid deployment of floating storage and regasification units (FSRU) in Europe to offload this LNG supply, including in Germany.

- Pipeline natural gas from Norway to the rest of Europe grew by 4% year-over-year in 2022 113 billion cubic meters (Bcm), according to S&P Global. Norway is now Europe’s largest supplier. Norwegian gas deliveries to Germany reached historic highs.

- A large-scale effort by households and businesses particularly in Germany to reduce natural gas consumption (heating, hot water), motivated also by the big price increases of natural gas.

- A shift in power production from natural gas to other energy sources, including coal, also motivated by big price increases of natural gas through the summer of 2022.

- A warm winter.

All of this worked together to reduce demand for natural gas and increase supply to replace pipeline natural gas from Russia.

Natural gas storage facilities in Europe are in exceptionally good shape for this time of the year. In the European Union overall, storage facilities were 81.7% full on January 14, according to GIE (Gas Infrastructure Europe). This is how the 916 terawatt-hours (TWh) of natural gas in storage on January 14, compares to the levels at the same time of the year in prior years:

- 76% above 2022

- 32% above 2021

- 1% above 2020

- 30% above 2019

- 44% above 2018

Storage levels differed by countries, but all of them were in great shape, particularly in Germany, which has managed to actually increase its storage levels over the past few weeks during a period (winter) that would normally be the withdrawal period. As of January 14, per GIE:

- Germany: 90.5% full

- France: 79.7% full

- Italy: 79.3% full

- Spain: 93.6% full

- Netherlands: 75.8% full

- Poland: 95.6% full

- Sweden: 88.4% full

- Belgium: 88.6% full

- Austria: 87.3% full

- Denmark: 91.5%% full

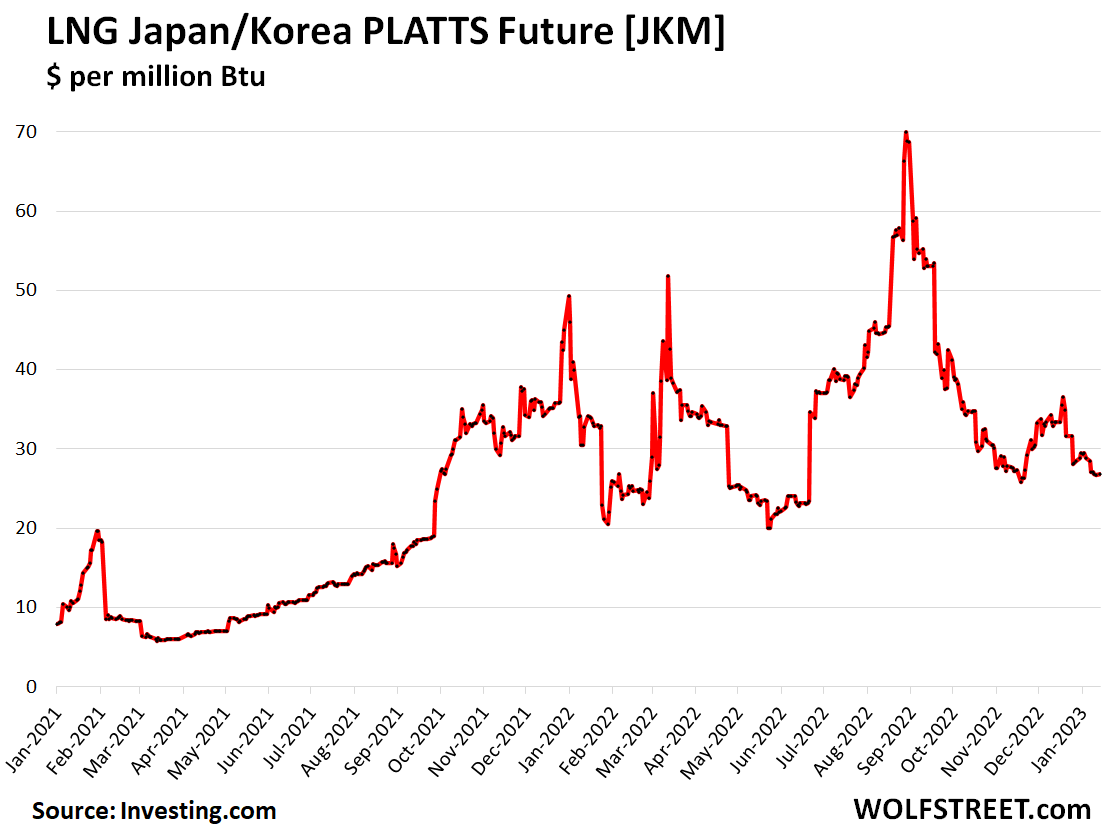

In terms of LNG pricing, the pressure has come off too. The price of the Japan Korea Marker (JKM) futures contract, at $26.80 per million Btu has plunged 62% from the crazy peak on August 31, 2022 (data via Investing.com):

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It seems to be a squeeze if you look at options data from EU, even TSX… Put sellers are getting demolished, the big boys with volume went for easy money.

Picking up pennies in front of a steam roller does backfire once in a while. At least that’s what its looking like… Some trading desks are celebrating, reminds me of the LNG options blow up few years ago from that guy in Florida. He blew his entire clients funds and owed more millions by selling deep out of money calls and got taken to the woodshed!

transitory for sure

I personally have found that natural gas futures are highly correlated to the amount of beer I pour into my Wolfstreet mug the night before an important Fed meeting. Typically we raise rates based on the amount of natural gas I produce. I know this may seem “random” to others, but I haven’t been able to come up with a better way…

That joke made my day!

Meanwhile, here is what the Pivot lobby will say: See NG prices are down. Inflation has been defeated already. Time to lower rates and start QE again.

Next Fed meeting is Jan 31- Feb 1.

I highly encourage you to start drinking beer on Jan 30th

He he.

A quick reminder that commodity futures do not trade anything real. Buy or sell to open, and sell or buy to close – no actual gas is purchased to sell or delivered to those who purchase.

Based on that reality, it is impossible for any natural gas futures to correctly price real world supply and demand.

Conclusion: no one knows what is really going on. My guess, like eggs, is we are close to something snapping. There is certainly not a glut.

Your comment remind me about what I did read in a small logal newspaper years ago.

Commodity exchange price in aluminum was at an all time low or close.

The local smelter did well anyway, the price difference between commodity stock exchange “aluminium” and aluminium with a quality to actyally make something of delivered to a customer had never been larger.

If you keep your futures contract, instead of rolling it over or just selling it, you are ‘standing for delivery’, and if you are at the right place and time with the appropriate storage you will receive it. That is in fact the underlying legitimate purpose of futures.

One real purpose for sure D.

Remember discussing buying diesel futures when preparing bids for projects with gazillions of gallons over 18 months as an attempt to limit risk.

Another is ability for farmers and other producers to stabilize their risks/incomes by hedging.

Not so sure. In any event, Europe is adding more and more FSRUs especially Germany and poor Vlad badly miscalculated on this blackmail too. Couldn’t happen to a nicer dictator, wouldn’t you say?

Well let’s see. When his ‘term’ ended he exchanged jobs with the # 2 and became #2 himself. Then after that term ended, he came back as Pres for another term. Nice of the then #1 to step down to make room for Vlad eh? Probably a healthy decision.

But when THAT term ran out, kind of hard to swap jobs again, so he altered the constitution to give himself ANOTHER term.

His only serious opposition is in jail for years after surviving poisoning.

So what do we call him: democratically elected?

Prominent French economist Piketty thinks Russia’s financial reserves should be ten times what they are. He estimates 2 trillion dollars has been drained out of the country, to end up in things like London real estate. He describes its govt as a kleptocracy, with P as capo.

Glad to see we’re bailing out the rest of the planet while Americans scrounge — and freeze. Here in San Diego out wonderful utility provider SDG&E greeted us for the new year with a doubling of gas prices. While not exactly Minnesota, it does get cold here in the winter.

Maybe prices will come back down once we get rid of all these toxic gas stoves?

https://www.sdgenews.com/sites/sdge-news/files/inline-images/SDG%26E%20NATURAL%20GAS%20PROCUREMENT%20COST-WHITE-BG%2003.jpg

The Pivot lobby doesn’t care about the prices paid by US consumers. As per thier narrative, inflation has been defeated and Fed must Pivot to take bitcoin to $100,000.

It’s not only gas that is understated in CPI. See my second comment on previous article for more such things.

The issue affecting SoCal natgas prices is largely one of maldistribution, as I have read it. Decreased supply to SoCal has largely occurred due to a pipeline explosion that killed two people in Arizona last August, hence the price increases in that region:

https://www.reuters.com/markets/commodities/kinder-sees-blast-damaged-part-arizona-natgas-pipe-down-months-2021-12-01

Seems like a very long time to get a gas pipeline back on line again. Meanwhile, SoCal is paying the price for limited supply.

There are probably other factors at work as well.

Minneapolis has CenterPoint Energy, headquartered in Houston, Texas as the nat gas supplier to residential customers.

January 2022, the average temp was 11 F; my nat gas bill was $170. December 2022, the average temp was 18 F; my nat gas bill, which I just wrote, was $212.

Still, a pretty good deal, I reckon.

Looking at the invoice:

156 Therms @ $142

Delivery & Basic charge @ $48

Extras, including “Feb 2021 Weather Event of $7” @ $22

Bottom line for just the gas itself, is 91 cents per hundred cubic feet.

Texas thanks you for paying free market prices for natural gas back in February 2021.

Two things:

1) Welcome to capitalism.

The price differential between the US and the rest of the world is so great that it would be stupid by the gas producers to not export. Just the EU was/is willing to pay an average of four times what the gas price on average is in the US, even if you factor in the costs of transporting the gas it would be fiduciary malpractice to not sell outside of the US if export is possible at all.

2) It is not just the exports that cause the rise in prices

The facilities needed for this don’t appear overnight. Most of them were being planned/built when the fracking boom started to export the excess production (the export of natural gas has quadrupled in the period 2015/2016-2020/2021) without people in the US noticing it.

Do note that as the fleet of LNG tankers (the EU ordered 10 billion worth of regasification plant ships and there is also an increase in orders for LNG transports to match) expands the price of US natural gas will rise to get closer to the point where US natural gas price plus export costs gets to around the world average.

Outside of a spike in Jan 2021, the price is still up 3-4x the price of 2 years ago. Not sure if we should be jumping for joy just yet.

Doesn’t matter to the Pivot Lobby. For them, the inflation has been beaten and not its time to take bitcoin to $100,000.

“J-Pow” should not be operating based on his beer and gas!

“not its time” => now its time

And LNG is still pricier than gas by pipeline?

In the end Europe have got higher energy costs, China have not and may get lower energy costs as they get pipelines in place from Russia. That do not bode well for industry in Europe.

Anybody on the board have semi-detailed knowledge of the history of Euro gas exploration in Europe itself?

I have some knowledge of oil exploration in this area and have been struck by its comparative paucity (compared to US, say), especially in given countries (Spain for instance).

I chalked up the apparent lack of exploration to my possible ignorance and/or state ownership of subsurface minerals in Euroland (destroying private exploration incentives).

I’m guessing that similar issues pertain with NG…for instance I know that historical oil power Romania somehow allowed a fracking ban…a somewhat incredible political decision (Russian fingerprints and walking around money?)

Dutch NG is off- shore and I think so is Norway’s. The Dutch struck shallow off- shore NG in the sixties.

These wells are far more productive and long- lived per investment than fracked wells.

There is a pipeline from Norway to the UK.

42% of gas is produced by EU countries, rest is import.

29% import is Norway, 11% is Great Britain, 11% is North Africa (but due to lack of pipeline capacity from Spain & Italy that is supply for the south EU), Russia down to 9% (replaced by among others more Norwegian gas & LNG), 4% the different middle Asia -stans, 36% LNG.

Norway is capped on production, the North Sea in total is a large field but it consists of a lot of small bubbles, making it relatively expensive and time consuming to extract so GB & Netherlands won’t get more out of that in a time frame that matters. There is a large (in area) field in France but it is fairly shallow and even with extraction there France was importing gas. Spain & Portugal have a smaller one that is for internal use, they import from North Africa for the rest. About the only large field (Slochteren) that has easy access and has the ability to ramp up is deliberately put in hibernation since extraction started to damage the housing it is under.

There are no other large fields that would allow the EU to become independent or rather less dependent on imports.

Gas extraction through fraccing has been banned in most locations that have shale that contains gas (thank mismanagement of early fraccing in the US and the less then positive results being used to scare EU citizens into successful NIMBY protests. And where US shale is largely farm/empty land the major shale locations in the EU tend to have cities on them) and/or are in expensive locations (in the Balkans for example).

The main import pipeline for France from Germany has been retrofitted to allow export from France to Germany, Spain is building a pipeline from Barcelona to Marseilles so that North African gas can be exported to the rest of Europe, Italy is considering the same but then for transferring Egyptian LNG (eventually to be replaced by a pipeline).

That is roughly the state of gas production in the EU.

One large field that can be reopened. No real other options in the form of one or more large gas fields or lots of smaller ones.

Fraccing mostly banned due to horror stories from the US or in locations that are even today too expensive to exploit. Rescinding bans and building will take years.

Pipelines to import gas from North Africa and transport it all the way to Germany are to be built but won’t be ready before middle 2024 at the earliest.

One of our partner firms did a study on this and apparently Europe and specifically EU countries have huge untapped natural gas reserves, by some calculations (there’s a lot of uncertainty about the accessibility) among the highest in the world, but the anti-fracking sentiment and extraction concerns are so strong, they’ve been reluctant so far to go forward. Even Germany of all countries is sitting on huge natural gas and oil shale reserves, a lot more than previously though, as our the Netherlands and Sweden, even outside the North Sea and Baltic regions. It’s maybe an additional card they’re keeping in mind, though given how long it takes to develop the fields, there may be at least some contingency-based planning for those fields.

Of course it’s higher than 2 years ago when the country was closed down for Covid and you couldn’t give the oil or gas away.

And who paid those high prices?

The panic stricken German and other European governments… as usual opm

Well, yeah, but you gotta give credit for the very, very fast standup of floating intake facilities.

If it were the US, the G would still be debating about how many “protected class” designers would have to be hired for the design phase – est project completion 2030.

At 27 times original budget.

After which the first three facilities would sink upon launch.

Fortunately, by that time Russia had been dismembered by China in 2028.

From our last visit there, some of the EU governments were able to get more reasonable deals and spread out the costs, but yes, they were eager to get the deals inked fast, restart nuclear and “clean coal” sources and up the wind power and tidal generators wherever they could. The big factor here is the provincial elections in Europe which are much more common than the US, and threat of no-confidence votes. The smaller parties are chomping at the bit and with all the increased additional costs of so many millions of refugees from the conflict in eastern Europe coming in–now millions of Russians, perhaps over 11 million from the region in span of a year–the local populations are demanding more balanced energy policies if the ruling parties want to stay in office.

Seems to me that Russia might be really screwed if much of the world has figured out how to do without their energy production.

Would be nice if US suppliers were given incentives to increase production more. After all, it really doesnt help the environment if the oil is pulled out of the ground in the US versus the middle east.

The incenative needed for increased oil extraction in the USA is a stable higher price for oil.

That will not come before sources of cheaper oil around the world are depleted.

After that the question is, how large market is there for oil at US$ 200 a barrel?

Well, post 2014 fracked oil breakeven was mid 40s in some good sized fields.

Not $200.

ZIRP pumped a lot of gas (as it were) into commodity asset values – like every other asset class. Financial speculation mostly has accounted for oil prices north of mid 60s since then.

Current production breakevens *now* are likely under $65.

I have heard another story on how oil field developers made money on fracking oil at $40 a barrel.

They made money on selling financial instruments to investors desperate for interest/dividends due to ZIRP.

If current break even is around $65 a barrel, the price may be expected to stay above $100 to make investment interesting.

Yep, yet another needless distortion of price discovery from ZIRP and QE. Interesting the effect it’s been having on fracking and coal production and shipping in the US, several of us have been looking at commodities investing and the breakeven points for the miners and extractors, but the rates environment is still so out of kilter that it’s hard to make real estimations of value or smart investments in the sector or in other commodities. The commodities volatility is another by-product of those policies.

really does not help the environment shipping lng. huge co2 emissions. nat gas through pipelines is most efficient –much less co2

– The Alps are undressed. In the northern hemisphere snow accumulation reached a 56 years high. Cheniere supply LNG to our friends in Europe. Norway became LNG wholesaler.

– NG future : Oct/Nov 2021 trading range is key. It was touched many times, but Jan 2023 lower low might be a spring. The peaks are rising in a linear line. Next time around Sept peak might be breached. Lower highs are good enough for energy speculators.

– Don’t bet that Europe will escape again. China openness and US first might hurt Germany and Ukraine next summer and winter.

Yet the U.S. keeps producing record amounts of Nat Gas

OPEC: “We need to invent a satellite freezer that will engulf earth with freezing temps so that we can become richer with natural gas demand”.

As a consumer, I don’t like oilgopolies, especially when the majority of OPEC are either corrupt or pariah states.

I doubt that the citizens of Equatorial Guinea benefited from the 2003-2007 oil boom.

Next time my brother-in-law buys or sells a stock I’ll post it here. He bought Enbridge stock at the very peak price of natural gas.

Was he into Enron when they caved? That was fun to watch, unless you owned the stock or held it in your retirement account as an employee or retiree.

Owned a Fidelity mutual fund stock during this period. It began climbing and shortly before 2000 I sold. This made a substantial contribution to my company stock fund.

I truly felt for those still in the fund. Company policy was to not disclose how one benefited or lost. So remained quite and retired in April.

I saw “Kinder” named above in reference to Arizona NG pipelines. Remembering Rich Kinder who got out of Enron timely and with good reputation, and built Kinder Morgan.

AA – watched Enron drop from mid 80’s to low teens. Bought a few shares just for kicks just under $10. I think 3 weeks or so later, they declared bankruptcy. So much for buying low…

I called it my MAC trade, middle aged carelessness…

My understanding is US LNG is priced relative to the Henry Hub spot price. You can find this data and trends on the US Energy Administration web site. Looking at the tools they provide one can see the price increases began when the latest monkey business started in Ukraine.

My question is will spot prices (also dependent on weather) decline once the issues in Europe are settled? i.e. maybe US LNG will not be in as great demand

Re: All of this worked together to reduce demand for natural gas and increase supply to replace pipeline natural gas from Russia.

Is it possible, Russia supply is still a supply factor dynamic that’s adding to price instability? There has to be an imbalance of some sort, maybe.

Sorry Wolf, off topic, relates to yesterday’s post (folks move on)… Just watched a YT video of a guy with a used car dealership. He went to new car dealerships (today) and still seeing “market adjustments” (up). Tacking on all kinds of BS. At the same time, he’s seeing new vehicles at auction!! In particular, the “I didn’t think you could get one even close to MSRP” Ford bronco… He’s seeing new at auction. That’s crazy.

The other thing that amazed me… He showed stickers on new Jeep Cherokees… 70k. Wtf? That was without “market adjustments”. Imagine what they end up doing to you if they can get your braindead self to come inside and have some coffee???

People need to be careful out there if they need a new car.

From The Economist

All told there could be enough new lng infrastructure in the world to handle 260 mtpa more than the industry deals with today, a 74% increase (within 7 years).

Germany is burning more coal. France is splitting uranium. Norway sells more electric cars than gasoline ICE cars.

US natural gas futures are up 7% this evening.

More sanctions against Russia take effect in February.

All the hypes by media, speculators & market once again shown how this casino is operating for decades. The market is always full of speculative elements to exaggerate the pricing, only cool minded folks will not pay premium for these manipulated pricing.

I do see all these as an unproductive but more on casino likes betting, which already formed part of the economy.

The volatility in the futures market, ground zero for the wagers by the coordinated money, is an excellent indicator of excess liquidity in the system.

I’m not convinced that a world of ample reserves Central Banking philosophy that has supplanted the tried and trued, fractional reserve model, is as corrupt as it has proven to be.

There is always hope. A human attribute that has an enviable win/loss ratio.

I would like to wish my fellows, good sailing.

Each separable feature of your graphic of CH4 futures, showing a mountain in the middle of the plain, sets off a kaleidoscope of emotional distress. After all this is our ” precious”, at risk, even though I don’t have one single penny at risk in the methane futures market. The vulgar volatility of the QE excess liquidity on display on the corporate media sites disturbs me.

Should I buy, sell, hedge, etc. A foreign language to most people

Unfortunately the lower prices are not seen on my gas bills in the northeast from Eversource.

My heating costs are the highest they have ever been at it has been a mild winter here on the northeast. I can’t imagine if it colder

So now we know, Germany Spain Poland Denmark wear wool clothes. Thanks Wolf!

Wolf, I think you buried the lede…. (My guess is #6 > 1-5)

n 2022 and into 2023, several factors came together to avert what had been seen as a potentially dreadful energy crisis:

1 Surging supply of LNG from the US and other locations around the world.

2 Rapid deployment of floating storage and regasification units (FSRU) in Europe to offload this LNG supply, including in Germany.

3 Pipeline natural gas from Norway to the rest of Europe grew by 4% year-over-year in 2022 113 billion cubic meters (Bcm), according to S&P Global. Norway is now Europe’s largest supplier. Norwegian gas deliveries to Germany reached historic highs.

4 A large-scale effort by households and businesses particularly in Germany to reduce natural gas consumption (heating, hot water), motivated also by the big price increases of natural gas.

5 A shift in power production from natural gas to other energy sources, including coal, also motivated by big price increases of natural gas through the summer of 2022.

———————————–

6. A warm winter.

———————————–

Everyone has their own favorite. LNG exports from the US to the EU have exploded, so to speak. That’s my favorite.

I have relatives and friends in Germany, and they have cut natural gas consumption dramatically in ways I wouldn’t want to do. That’s their favorite.

Other people’s favorites are simplistic answers they can believe in.

In reality, as I said, it all came together. It was actually quite amazing.

FYI: it’s still winter in Germany, just somewhat less cold than normal. But most of Germany doesn’t get very cold to begin with — just miserable… rainy miserable short dark days. The Alpine regions are a little different, but that’s just a small corner of Germany. You need to spend a winter in Berlin to get the drift.

Vlad shot his wad. No more holding Europe hostage for his winter. He will surrender and now is a periah forever….

I guess the Global warming situation caused by the Petro states turned into a virtue for Europe and the US.

Where is the out control inflation hysteria in 2022.

Look at United States Natural Gas Fund (ticker: UNG). Its almost at its all time low since its creation in 2007 and down about 70% from its 52 week high.

I wonder how short lived this is for natural gas, as just like any other commodity, it will rebound within the next 6 months as part of financial asset rotation and cycling.

However, its not like I am going to see Florida Power and Light lowering electric utility rates anytime soon.

Look at how the US dollar index (ticker: DXY) has dropped about 11%, while gold and silver have rebounded. A stronger US dollar (relative to the EU) was depressing gold and silver prices.

Careful there with UNG. UNG eats itself up due to the way it is structured in that it rolls expiring front-month contracts to the next-nearest month, which causes a systematic decay. So look at a chart that goes back to its beginning in 2007.

UNG is only for short-term bets on the direction of NG futures. If you try to think of it as a long-term bet, your investment will be eaten alive by the built-in decay.

So long-term, UNG doesn’t tell you anything about the price of US natural gas.

thank you for the information

Our electric bill has gone up slightly from 2019. Nothing to complain about.

Salt River Electric’s current average bundled electricity rate is 8.77 cents per kilowatt hour (¢/kWh), compared to the average Kentucky bundled rate of 11.51 cents and the average nationwide rate of 13.55 cents.

SRP in a nonprofit. Each user is a shareholder with voting rights.

Hmmm – Europe should probably save as much as they can in preparation for filling the reserve tanks for next Winter.

Yet, we see another story headline from today. Perhaps this one is forward looking rather than back?

“French And German Power Prices Soar As Cold Sweeps Europe”

Need hundreds more windfarms for the EU since daily data on their actual production is at only 33.9% of installed capacity. More windmills than trees in the future, all running full out and producing at 1/3rd of their capacities.

The “fuel” for wind turbines is FREE. No need to buy wind from the US or Russia. No need to pipe it in or bring it by tankers or railroads. Why is this so hard to understand? Sure, there are costs in building the wind turbines, but there are equivalent costs in building fossil-fuel power plants. Nuclear is by far the most expensive source of power, and we’re not even paying all the costs upfront; much of the costs come afterwards when it’s time to decommission the plants and deal with the nuclear waste, which we still haven’t done, and still haven’t paid for.

So you get as much power as you can from this free “fuel,” and then you supply the rest of the power demand from other sources. I’m really getting tired of these dumb comments about wind farms. These comments stopped being funny a long time ago. Now they’re just dumb.

That’s to much common sense.

Hard to drive home the need for base load, and sources that provide it.

Wind and solar are definitely the future, as is nuclear, and currently NG.

Amen, Wolf. We had the same foolish comments about wind power in Texas after snow-mageddon in February 2021. Politicians who should have known better claimed that our power failed because of unreliable wind energy. Not so.

These numbers are off the top of my head, and rounded, but are close enough to make the point. Texas has about 140GW of generating capacity from all sources. About 30GW of this capacity is wind. However, no one expects the wind to blow 100% of the time. (nor does anyone expect natural gas plants to run 100% of the time – they are taken down for maintenance from time to time if not for cost-curve reasons).

During snow-mageddon, wind generated about 4GW of power used during that time. Politicians would pontificate that wind was thus unreliable – after all, who could on something that only generated 13% of its capacity?

Instead, the reality was that we only expected wind to generate 6GW under normal conditions during this time. So the wind shortfall was 2GW, not 26GW. This was not great, but the failure of wind power was not responsible for that disaster.

Wolf

I am not disagreeing with you. But as devil’s advocate, does the ‘fuel’ to produce, replace and maintain these wind farm come from the ‘fuel of wind power’?

My understanding is that fossil fuel are necessary for the above, may be less(?) but still cannot be written off in the short term future

B/w the rotor+plus wings of wind farm(s) was built in Texas (Dec ’21) on the assumption that temp will be 45F or above, but not for subfreezing temp!

“…does the ‘fuel’ to produce, replace and maintain these wind farm come from the ‘fuel of wind power’?”

Sheesh. Where does the fuel come from to build a NG-fired powerplant? Where does the fuel come from for anything you build? It’s ALL the same thing! But with a windfarm, after you build it, the fuel is free, and with a NG plant, after you build it, you have to BUY and PAY FOR fuel for the rest of its life. DUH.

I have seen 0 comments in the media -or for that matter anywhere stating the hilarious fact that global warming has saved the europeans from their own poor decisions on russian energy and fossil fuels/nuclear energy – which they made in the cause of stopping global warming ! there new slogan said very softly is – Burn that coal !

People have got to learn the difference between “weather” and “climate.”

Wolf – I can’t thank you enough for your comment. Ultimately, ignorance of climate effects on the planetary (not just the anthropotechnic one) biosphere, akin to the law, will be no excuse…

may we all find a better day.

Maybe partly this but it’s a lot of factors though. EU countries did reasonably well in many cases adding wind, solar and tidal sources, and some of those renewables did provide extra wiggle-room and additional backup sources. Plus there’s the fact that Russia is exporting so much oil, natural gas and coal itself to China–basically boosting up their economy and resources as a counterweight, that it’s contributed to a global glut. Though agree with you that Angela Merkel’s policies esp were short-sighted, they’re having to fire up the nuclear plants again in parts of Germany and basically tossing Merkel’s failed Energiewende out. She had some good ideas and goals but she and her group totally failed to plan out and provide for contingencies in their plans.

Plus there’s still a lot of oil and natural gas getting to the EU from Russia and the Iran even if under the table. Black markets tend to be pretty thriving and lucrative for that sort of thing

It is not just China.

Exports to India have increased by 30 times or so.

And since most of the world (around 50 countries out of 190ish) isn’t playing the game the US demanded a lot of the -stans are also buying (and then as in your post below among other tricks mix it with their own to send of to the EU anyhow).

Heck even Saudi Arabia is buying. Their refineries can handle Ural grade crude, which is worse then the stuff they have in the ground. So they buy that at a lower price level to their own before the discount the Russians offer, refine that for local use, and then export their premium crude to the EU.

erm, missed a one:

around 150 countries out of 199ish

The so-called LNG glut in China is primarily composed of Russian LNG exports. And it seems that these are fated to be re-sold to an increasingly-desperate Europe for diplomatic gains.

The post by “Who Cares” above is, as far as I can tell, accurate. The upshot is that while Europe does have the means to replace Russian gas exports in the fullness of time (if only at greater cost) – the options cannot be deployed in time to avoid severe economic disruption.

Thus China will increasingly become the “supplier of last resort” absent a reconciliation with Russia. I wish it were otherwise.

Right, and again a lot of Russian and Iranian oil and natural gas still gets to the EU, even if through black markets, it’s too lucrative to pass up. Especially from Iran, Europe’s never had the hangup about Iranian supplies that the US has had, and with priorities as they are, there’s little stomach to enforce embargoes on it.

The Quatar gas field supplying Europe is half in Iran waters. And Quatar and Iran share the income…

This still means prices are about double what they were in 202, a fact not lost on the European working class….

LNG should have the desired effect of creating a uniform global market. I think Japan is the most overpriced user. Chinas economic head, Lui He, made some uber dovish comments at Davos, he says the Maoist experiment is over, and it’s back to business. Wall St didn’t exactly run with the news.

As I read this, solar panel propaganda pop-ups surround it..

Several of my “arithmetic challenged friends ” have taken the

$60 K dive to shingle with solar, claiming their grid tie inverters

have zero’d there energy costs… but none of them will boast about

power companies buying back power @ .03 cents per kilowatt hour

that’s sold to them @ ,15 cents per kilowatt hour ! ummmmmm, guys?

your making payments on $60K to take an 80% hit! maybe you should find an unvaccinated K-2 elementary student to explain that to you!

The only way to get back all .15 cents is to borrow $60 K more for the

battery bank the offer… then you can get all .15 cents to make payments on the $120 K you foolishly borrowed, and watch your $60K batteries begin to die after 4 to 6 years. I had solar and wind for 10 years…I took

it all down! before doing solar, talk to somebody who already did it!

and come make an offer on mine…. it’s in the way.