He who panicked first, panicked best? Some of the charts are just kind of funny.

By Wolf Richter for WOLF STREET.

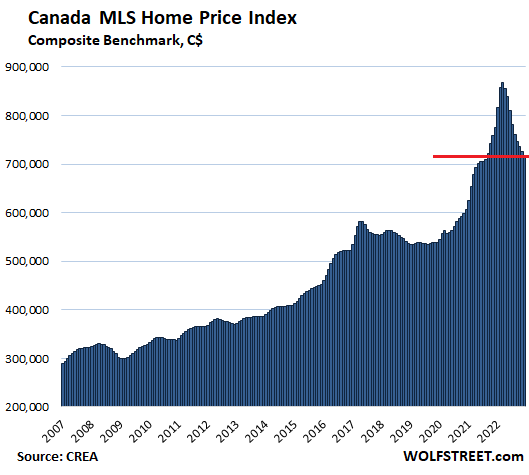

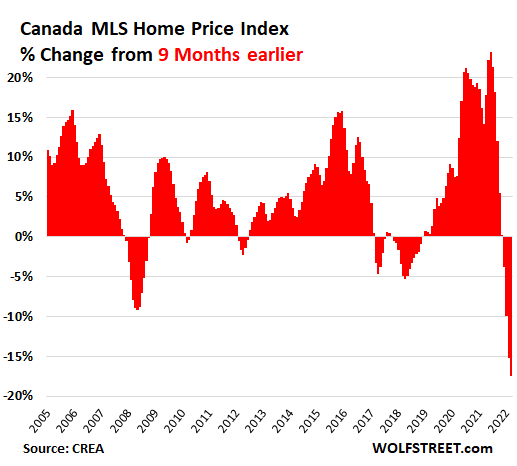

Home prices in Canada dropped 1.2% in December from November, the ninth month-to-month decline in a row, and are now down 17.4% from the peak in March 2022, and down by 7.5% from a year ago, according to the Canada MLS Home Price Index by the Canadian Real Estate Association (CREA). Sales plunged by 39% year-over-year.

In the two years from the beginning of the Bank of Canada’s money-printing binge in March 2020 to the beginning of the rate-hike cycle in March 2022, the composite benchmark price had spiked by 54%. This spectacular housing bubble, on top of an existing housing bubble, was entirely fabricated by central bank money-printing and interest rate repression. This was a global phenomenon, triggering massive global inflation. So now comes the invoice for the drunken money-printing party.

The composite benchmark price of the Canada MLS Home Price Index for all types of homes has now dropped by C$151,300 in the nine months, to C$717,000.

That 17.4% drop in the benchmark price from the peak in March was by far the largest and fastest nine-month drop in CREA’s data going back to 2005. In Canada, there wasn’t much of a housing bust during the Financial Crisis, but now the housing bust is here, and it’s real, and it’s not seasonal or whatever. Homes are being repriced on a large scale:

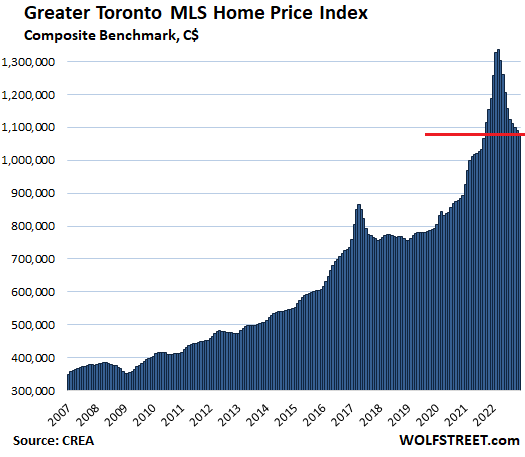

Greater Toronto Area: The MLS Home Price Index composite benchmark price dropped 0.8% for the month to C$1.08 million:

- From peak in March 2022: -19.0%

- Year-over-year: -8.9%

- Drop in 9 months from peak in March 2022: -C$253,600

- Jump in 9 months to peak in March 2022: C$313,000

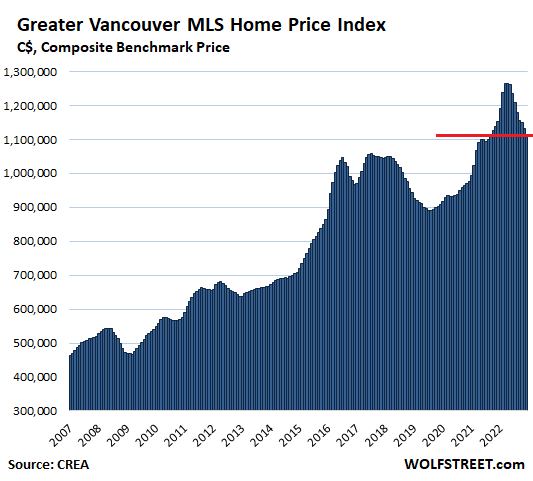

Greater Vancouver: The MLS Home Price Index composite benchmark price dropped 1.5% for the month to C$1.11 million:

- From peak in April 2022: -11.9%

- Year-over-year: -3.3%

- Drop in 8 months from peak in April 2022: -C$150,400

- Jump in 8 months to peak in April 2022: +C$163,300

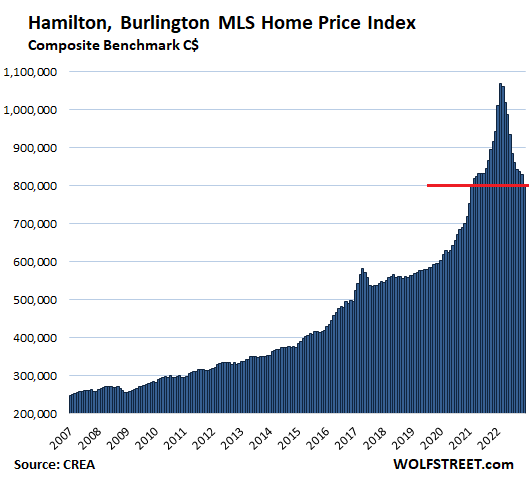

Hamilton-Burlington metro: Prices made even more spectacular moves than those in Toronto during the pandemic: From the beginning of the Bank of Canada’s money-printing binge in March 2020 to the price peak in February 2022, the composite benchmark price spiked by 70%. Now they’re heading back down even faster and more spectacularly.

The MLS Home Price Index composite benchmark price plunged another 3.3% for the month to C$803,200, the lowest since February 2021:

- From peak in February 2022: -24.9%

- Year-over-year: -14.8%

- Drop in 10 months from peak in February 2022: -C$265,600 – going down faster than up.

- Jump in 10 months to peak in February 2022: +C$244,400

Charts like this are just kind of funny:

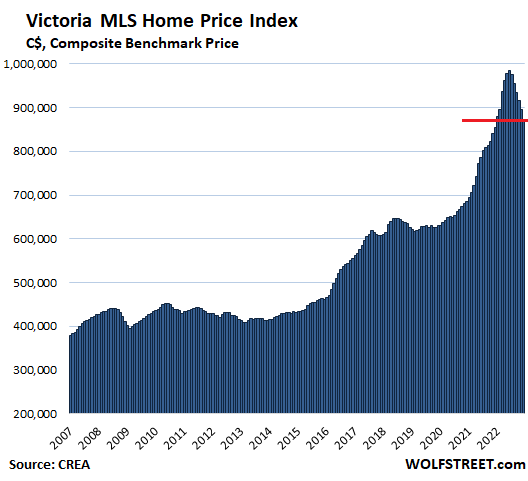

Victoria: The composite benchmark price dropped another 2.4% for the month to C$872,700:

- From peak in June 2022: -11.4%

- Year-over-year: +2.3%

- Drop in 6 months from peak in June 2022: -C$112,800

- Jump in 6 months to peak in June 2022: +C$132,200

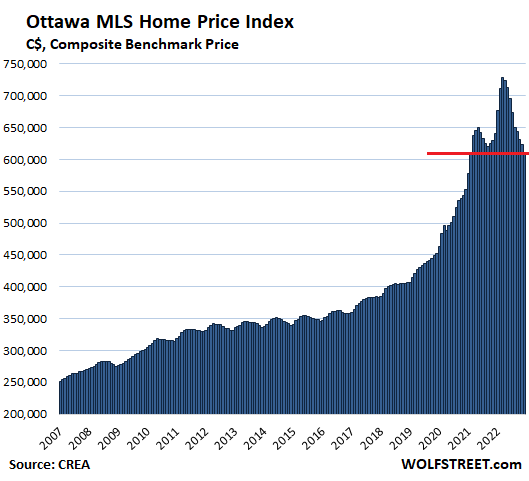

Ottawa: The composite benchmark price dropped 2.0% for the month to C$610,800:

- From peak in March 2022: -16.1%

- Year-over-year: -4.6%

- Drop in 9 months from peak in March 2022: -C$117,400 – going down far faster than up

- Jump in 9 months to peak in March 2022: +C$85,500.

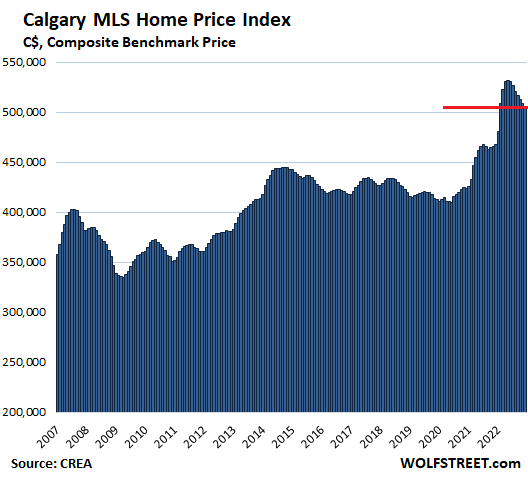

Calgary: Despite the oil boom, home prices are now falling in Canada’s oil capital. The composite benchmark price dropped 0.6% for the month, the seventh month in a row of declines, to C$506,400:

- From peak in May 2022: -4.8%

- Year-over-year: +8.1%

- Drop in 7 months from peak in May 2022: -C$25,800

- Jump in 7 months to peak in May 2022: +C$67,200:

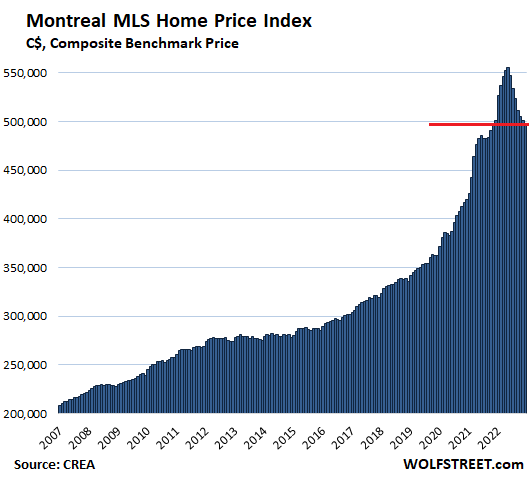

Montreal: The composite benchmark price dropped 0.6% for the month to C$497,800:

- From peak in May 2022: -10.4%

- Year-over-year: -0.7%

- Drop in 7 months from peak in May 2022: -C$57,800

- Jump in 7 months to peak in May 2022: +C$64,600:

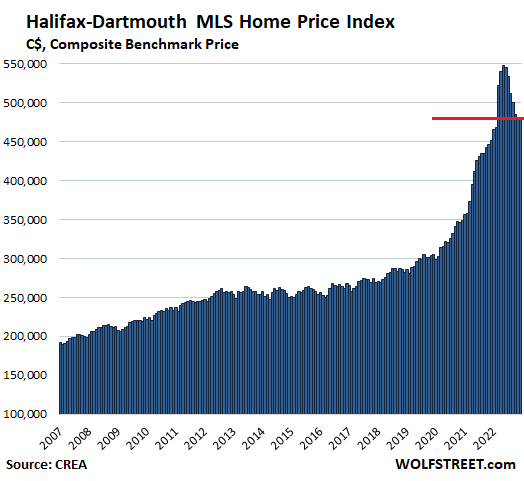

Halifax-Dartmouth: After years of housing sanity, the money-printing bug turned buyers’ brains to mush. From February 2020 to the peak in May 2022, the benchmark price spiked by 81%.

The composite benchmark price, after huge plunges in the prior months, ticked up a hair in December (+0.2%), to C$480,600:

- From peak in May: -12.3%

- Year-over-year: +6.3%

- Drop in 7 months since peak in May: -C$67,200

- Jump in 7 months to peak in May: +C$105,200:

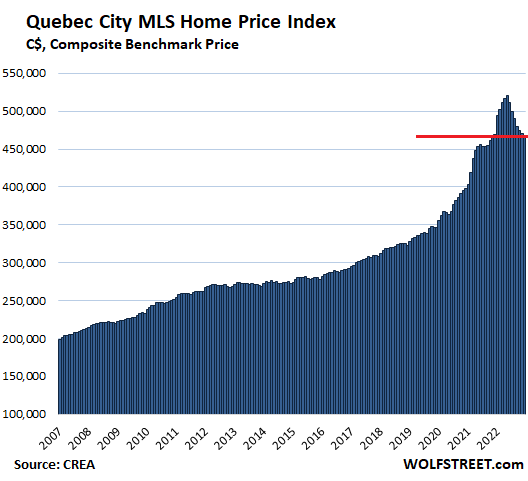

Quebec City: The composite benchmark price dropped 0.6% for the month to C$468,100:

- From peak in May: -10.0%

- Year-over-year: -0.3%

- Drop in 7 months since peak in May: -C$52,200

- Jump in 7 months to peak in May: +C$59,400:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

And another 25-30% to go!

Yes, we’ll see massive price drops in the coming months; it’s already well-underway here in Greater Vancouver…

Feel free to join the Metro Vancouver Housing Collapse Facebook group and share in the daily market updates/analysis and discussions with thousands of others.

The realtors will suddenly flock this article with following misleading comments:

1. The inventory remains super low.

2. The inflation has been defeated and Fed is ready to Pivot.

3. Here in socal, the sun never sets……

4. My neighbor just sold his house at twice the 2019 price! So there is no price correction.

5. Housing remains a great investment, the rent will offset the fall in prices.

6. My own data shows that the puny drop in mortgages have made housing affordable again.

7. Buy now or Miss out forever.

Statements about the future are statements of opinion, in a general legal sense, and not fact. Everybody talks their book, you don’t? (Of course the freedom and asymmetry of this setting means you don’t have to make rigorous disclosures on your own stakes and interests behind your expressions here.) There are future possible states of the world in which those opinions come true. That is the essence of a free market, free trade, a free country. Do you want some cop on the beat to remove these uncertainties? Ask Xi.

Sure, but some outcomes are more likely than others.

One thing is for sure we’ll see a lot more foreign students coming to Vancouver this year now that the foreign buyers’ ban is in place.

Soon to be coming to a US city near you!

But, but but, there will be Pivot soon!

/s

> coming to a US city near you!

And high time, though it means I will be missing some frothy imaginary profits. I will continue to live according to my means, and not anchor on some zooming upward fantasy chart reading, which we had.

I think “Bernanke” implementing the idea of the wealth effect will go down as the worst idea in central banking policy in 100 years.

You can’t say the policy is a success til you complete the unwinding of it.

@Old_School To my knowledge, the Fed has been milking the wealth effect since the 1990s under the “leadership” of Alan Greenspan. These guys don’t seem to understand various adages like chickens coming home to roost, pay the piper, etc. IMHO, these guys are not leaders, just political hacks who just do the expedient thing – and don’t have the interest of the country or people at heart.

The problem with the “wealth” effect is that it will disproportionally benefits the rich who own most of the assets. However, if you are a renters, you’re screwed!

Then line about backstopping any losses in the stock market in 2012 was the real clincher.

From the greater fool blog

Motivated Seller of the week

This is a very high value part of Downtown Toronto

And check out this vendor, which agent Stephen Glaysher chooses as his “motivated seller of the week.”

Motivated seller chops the price by $1 million

“As the calendar has turned to 2023 there have already been 100s of price drops signifying motivation and the realization of buying power amidst rising interest rates!” he tells clients. “Take this Summerhill listing in midtown Toronto for example… Originally listed at $4,999,990 this listing is now available with a 1 million dollar price drop to $3,990,990. Expect to see a large # of price drops as well as relistings at reduced prices following the holidays as sellers come to realizations of BUYERS MARKET Conditions!!”

Remember that interest rates go up again in a few days. It’s been 22 years since the prime rate at the banks has hovered in the 7% range. But back in 2001 properties in Toronto sold for an average of $251,500. Now the number is $1,189,850. Two mill is the new one mill.

The bank cop thinks that’s crazy risky. What if the bottom falls out? It believes people should be held back from financial suicide. And so they shall.

Did I mention selling?

And all through those years when housing and rents were climbing so quickly, the Bank of Canada said inflation was 2% +-.

Here is a recent article about Canadian housing written by a Canadian and former member of parliament.

https://www.greaterfool.ca/2023/01/15/when-buyers-rule/

That will only get you to maybe beginning of Covid so most would still have lost nothing. Pretty wild statement hey 🤔

I wonder how much exposure the large Canadian Banks have to the Canadian housing market. Unlike the US, I believe most mortgages re-set every few years.

I am wondering this as well. When these things reset these people will be in really bad shape. Ouch!!!

Two types of mtg:

– fixed rate: typical 5 years, then renews with new rates

– variable rate: bank prime + x% (changes with BoC rates)

Canadian Banks are very exposed.

CMHC

Our banks are solid.

It is on the taxpayers.

CMHC sells additional, mandatory mortgage insurance against the default of homebuyers who put less than 20% down. While it is a Crown corporation, it is not related in any way to taxpayers bailing out the banks. Anybody can go bankrupt, but here is their latest financial report, they run a tight ship.

https://assets.cmhc-schl.gc.ca/sites/cmhc/about-cmhc/corporate-reporting/quaterly-financial-reports/2022/quarterly-financial-report-september-2022-en.pdf

My bank had a variable with me for some years, then thankfully I switched to a fixed, ten years ago. Not such a great look for years, until now it is. It was a reasonable trade all around.

I am glad the banks are too big to fail. I don’t want to be in a line of angry depositors at the busted local bank! Last time that happened, we were circling the drain toward global war. The various backstops spread the risks and losses across time and persons — that what insurance does. That’s what finance does.

Phleep,

Banks can fail without the financial system crashing or angry depositors lining up at the local failed bank. It happens all the time. Failure is a fundamental feature of capitalism. Nothing should be too big to fail, and particularly big banks, if their actions have placed them in a position to fail.

Saying you’re glad banks are too big to fail, and thereby not responsible for their actions, is such an odd comment from someone who is quite vocal about living within their means and not taking undue risk (even just within this comment thread). It’s so absurd, I’m wondering if you’re trying to provoke a reaction like the one you just got from me.

Yes they reset, longest term is five years. Banks hold the note unlike US where it is sold off in an MBS. People who closed on new builds are truly screwed, losing deposits upwards of $300K on ridiculous $1.6 million dollar suburban homes. CMHC is a mandatory government insurance. The banks just seize the place.

They had stats out on that and vast majority have years left at low rates so by the time they are up I’m sure the Gov has rates back to nothing to keep Ponzi scheme alive

Loving the trajectory of that drop…come one Murica, don’t let little brother Canada outshine you om the bust, let’s make it bigger for us, especially in SoCal….

Interestingly, Opendoor is still in the game. On Saturday 1/14/2023 I got a flyer in the mail from them telling me how to sell my house to them. YOY their stock is down 84%, but they’re not quitting yet!

Opendoor is in a really bad spot and will probably have to pivot to a traditional “marketplace” strategy, which will not be successful because they have not built up the website traffic of Zillow and they dont have the unique business model of Redfin and they dont have any other hold on agents.

The only real value of a site like Zillow is the buyer traffic that comes to the site. Without that, it is worthless. Opendoor simply cant make the business model of flipping homes work in this type of market. They could possibly do quite well at the market bottom, as they purchase homes with no buyers at big discounts and fix them up a little to sell them. But the core problem of Opendoor is that they need to be able to scale the business for different types of real estate markets and that is really impossible.

Agreed, opendoors business model is a bust and they can’t pivot. They’re dead and their stock reflects that.

Zillow must be sucking wind with transactions down so much. Stock price has spiked like all the other profitless unicorns. Redfin and compass in the same boat, just a matter of time until they go bust.

Canadian Housing Bubble & Beyond 2023

What if, there’s no catalyst (in 2023) to bring a massive amount of people from the sidelines, to invest or speculate on anything? That none-activity will be driven by a lack of capitulation (fire sales) offset by repetitive, cycling volatility that bounces around within a tight range, which will be absolutely nebulous.

The Schrödinger’s cat alive/dead state of ambiguity will persist, as inflation remains elevated longer, decreasing cash flow, decreasing profits, prolonging the stalemate. As in chess, this will increasingly become Zugzwang, a state where any move makes matters worse.

That suspended state, between growth and decay will play out on every level of the spectrum (globally) from small (passive) 401k participants to government treasuries, and all the witches breweries of hedge fund ventures and entities. Those pretending to do well, will mask macroeconomic struggles by amplifying good bets and obfuscating losses. The rest will be fully naked on a low tide beach.

The thawing of glacial global liquidity will take the form of tender green shoots that slowly hesitantly unfold, adjusting to steadily rising temperatures and the permanence of deeper roots.

However, that creates a model, with too much unproductive capital sitting idol, somewhat reminiscent of banks hoarding capital ( for decades) as they become overly dependent on Fed overnight repo heroin, which addicted an entire generation to a substance they can’t live without.

Housing Bubble, Canadian overreach, global pandemic excess and still, money on sidelines anxiously waiting for fire sales, for crypto, stocks , rentals, bonds, AI-biotechnology, AI-etf financial private investment — a virtual candy store filled with exciting investment choices — and long lines of customers lined up for endless fire sales, waiting to make a killing, getting richer than everyone else in the queue.

If I were placing a bet today, on anything, I’d bet the cat in the box, dies from starvation, primarily because, while everyone is looking to get rich quick, the owners will forget to feed the kitty.

Nostradamus

The early bird gets the worm. The afternoon cat gets the early bird.

“I’d bet the cat in the box, dies from starvation, primarily because, while everyone is looking to get rich quick, the owners will forget to feed the kitty.

Nostradamus”

Does it die in the morning or the evening? I have my eye on the afternoon cat!

But the second mouse gets the cheese

The seventh shrimp gets the leftover algae

The money on the side-line is debt and do vanish before it ever will circulate again. Capital in the form of money will then either be in short supply or of little value. Little will be invested and capital in the form of natural resources scarce. There will be fire sales, some takers and then less left.

The cat in the box was the Cheshire cat, it may have been in the box, it may appear other places. Alive if it is, still a mirage.

My bet is between the binary alternatives: stumbling along. That’s a bet too. Maybe the occasional black swan opens up anomalies/opportunities/collapses.

1) The Dow is down, because it need some rest. The Dow 30 members by weight :

UnitedHealth : 9.4%. GS : 7.2%. HD : 6.4%…JPM : 2.7%. UNH is losing strength.

2) The regional banks aren’t investment banks.

3) The primary banks might use their excess reserves and RRP to lend, to increase assets, to make more money.

4) When the 10Y breach the 6M and normalize the yield curve, the primary banks will use what they got in the Fed and lend. Gravity will lift the German 10Y above the 1Y and start to normalize things in Europe.

5) Madam ECB will be able to raise rates again, risk free. The BOJ might follow.

6) TSX, in trading range since May 12, might popup soon !

GS just reported awful numbers and HD likely to wither along with the housing bubble popping.

Banks borrow short to lend long but with the yield curve inverted that doesn’t work. Plenty of people walking from their car loans obtained during covid, same thing will happen with RE, hence the increase in loss reserves. They know it’s coming.

I noticed the reference to increased LLRs in the GS article on CNBC. It definitely piqued my interest. Something must be afoot already.

but but…bitcoin is now back above $21k….talk about insanity….tightening financial condition? Not for the tulip market in Jan of 2023 or maybe one last hooray before ultimate rug pull…nothing goes to heck in a straight line right?

the wolves are trying to suck in new money from retail. the BTC ‘price’ is nothing like that found in real markets. highly manipulated by a few ‘big’ players. it’s only eye candy. just look away.

The jumps were so obvious, with no change in underlying “fundamentals,” so it sure looks like bait is being dangled to clean out whoever still harbors leftovers of the 2021 sentiments. The marketing was so powerful back then, I reckon the insider whales reckon they can relight the nervous systems of the bigger fools, and cash out some more.

But the weather….oh wait it’s Canada

Two seasons…Fourth of July and Winter.

Meaning big energy price dependency too. At least that paused from screaming upward.

In Toronto the two seasons are road repair and winter …

I’m really liking these graphs, Wolf. Looks like we’re on the back half of these pyramids! I hope they continue going down the same rate as they went up!

Generally, we’re looking at a doubling of price (I refuse to use the word ‘value’) in only 5 years to reach that top, which looks to have occurred in the summer of 2021.

Wondering: Could it take another 5 years from that point to unwind whatever absurdities created that increase?

THANK YOU for noting the disconnect between price and value! +100

Price – dollars you pay

Value – utility you receive

The value of a home doesn’t double just because the price does.

Next question is whether these charts will look like the Canadian Rockies – typically steeper on one side than the other…

Price is a beauty contest. Value is marrying the right one. Sadly, I never got that right with romance. But more thankfully, I did OK with finance.

All the other pyramid schemes based on infinite growth collapse fast when they run out of steam, eg fiat to burn. This is true of markets and entire civilizations eg running out of cheap energy invariably leads to swift collapse. Therefore, I expect financial crashes followed by fast pivot, followed by… the end game?

Same dilemma of growth and survival since the first cell differentiated itself from the surrounding ooze. So far, the aggregate has survived and still produced considerable thriving amidst pratfalls. Embedded in our mutant brains however is the recurrent awareness of personal extinction which, IMO, pings us, and expresses itself as various recurrent doom fantasies on various scales.

Or – Generally, we’re looking at a massive 50% collapse of the currency’s real estate purchasing power. The house didn’t do anything. It’s the currency that’s getting gashed.

The currency itself is going up, relative to houses. Those with currency can buy more house than last year. Classic diversification problem of keeping enough reserves, against a very illiquid asset. Or not.

Jeremy Irons in Margin Call said it best:

“If you’re first out the door, that’s not called panicking.”

The psychology here in terms of housing is stronger than ever. Nobody believes house prices will go down. When I share these charts with friends they laugh it off and tell me I’m crazy to even question the housing market. “Always people with money who will buy”, they tell me.

Hopium is a powerful drug. Time is the great equalizer. Home prices are built on comps, not on an econometric view of affordability that is founded in income levels for an area.

There have been numerous long term trends that have played out to support real estate prices over the past 30 years. The biggest trend was the continual reductions in interest rates, accompanies by less diligence on the part of financiers. The other big trend was toward multi-income families, as wives entered the workforce, although that trend got played out years ago.

The future of real estate is totally dependent upon whether central banks truly bleed the world economies of debt bubbles, or chicken-out and add back the debt.

I suppose the one other factor is immigration. If anyone really wonders why the liberals want immigration so badly, they need to understand that the new liberal movement is effectively owned by billionaires. The billionaire class own businesses and real estate and they NEED population growth to increase their revenues and profits. Flooding the country with poor illegal immigrants might be bad for the middle class, as they compete for scarce resources in healthcare, education, etc. But it is damn fine for the billionaire class who profit from more people in the US.

Comprehensive immigration reform?

No, just build a wall, it is so much easier for the masses to understand.

It is the liberals and billionaires that want immigration so badly…What?

There is only one party that controls them all. Go back to sleep!

“There is only one party that controls them all. Go back to sleep!”

And that would be “The War Party Of The Rich”.

Demopublicans and Republicrats together as always.

“But it is damn fine for the billionaire class who profit from more people in the US.”

Only until the asset and credit mania are confirmed as over.

At that point, they become economic deadweight.

Back in SWFL in ’92, less than 10% of construction work force other than black or white folks.

Last involved directly in field in ’99, Hispanic and other recent immigrant ( SE EU ) was 40-50%.

Last involved in large projects, 2006-8, it was closer to 75%.

Only delta was most in ’06-08 were in SWFL legally, and many had achieved field supervisor levels as well as journey level skills and appropriate pay.

IOWs, NOT dead weight.

Very similar in CA and NV even longer probably.

The ruling elites will do whatever is necessary to keep the hordes of foreigners coming in.

Immigration, like offshoring, was deflationary: driving more goods and services into my hands for fewer dollars. This was at the cost of broadly lower wages. But in general for a long while it made life pretty comfortable in CA here, getting various services at modest prices. Who was cutting our lawns, fixing our cars and houses, and not complaining about it? Maybe at last a balance has tipped. But those dead-set against it are sometimes free-riders who want nanny to set aside for them a cushy job and high-riding lifestyle for less work. I saw the 1960s-70s when the US labor force curdled, many turning into a bunch of stoners, shirkers and spoiled brats.

I bet the Native Americans said the same about your ancestors. Who let these Eurotrash in?

Who mows your lawn? Who builds your house? Who picks your fruit and vegetables? Who works in the slaughterhouses? So much ignorance so little time.

The absolute biggest thing I’m curious about, regarding the theme of home prices falling or stocks, is what’s motivating buyers today.

That question is clearly curious with Canadian values, but in general, if a home has doubled in value over a few years and now is 16% off, that’s still absurdly overpriced by old fashioned standards.

Obviously the same is easily said for stocks. The S&P is hovering around 4000, but because it’s down 1% apparently there’s a tsunami of people buying the dip, but why?

I realize that’s all rhetorical but, stocks are hovering within an overvalued range that hasn’t moved in any meaningful way, even after a big Fed PR effort.

Valuation has always been subjective, but I seriously don’t get what’s motivating so many people to disregard the concept that we’ve been in a huge global bubble, that can’t continue going up and up.

Why would any young couple feel compelled to think a home falling 10%+ is an exciting opportunity?

All the generational polarization that was amplified during the pandemic, seems crystallized in financial planning. One generations foundation was to think about investing and careers in decade long periods, while this period seems to be far more related to attention deficit hyperactivity connected to a total lack of due diligence,

I’m not hoping for a severe market crash, but I do wonder why anyone on earth thinks a small decline in prices is an opportunity.

Only answer I can give you: the cost of renting.

Aside from the obvious obscene rents, the cost of relocating, moving expenses. Plus the little but necessary purchases that come with changing your space every year or so, such as now the couch doesn’t fit, there’s w/d hookups but no machines, all that can add up to the rental deposit and by the time you calculate all those expenses plus rent, you might as well buy and be done with a landlord.

If I wasn’t rushed out of my last rental (landlord sold) I’d still be on the market to buy now, sadly deposit’s been mostly chewed up to having to move to yet another rental. Its a miserable cycle.

rents are insane right now..I’m paying close to $30,000/yr renting a 2 bed apartment in texas.. that’s not fun..as much as I want to wait it out..this number in the back of mind keeps me awake at night..I have to constantly remind myself that all is well.. to prevent me from making any stupid moves. it’s tough.

wolf, typo:

“Halifax-Dartmouth: After years of housing sanity, the money-printing bug turned buyers’ brains to much.”

Thanks!

:-]

1) Morgan Stanley earning and revenue positive surprises. MS BB ;

Aug 13/19 2021, 104.77/98.71. MS gap up pricked the BB, but close below, on huge vol.

2) GS closed Jan 6/9 gap and popped up, on the highest vol. since 2020.

3) JPM inside bar. In order to move up there must be a close above

Mar 22 high. If done JPM might close Feb 25/28 gap.

4) BAC inside bar. In order to move up there must be a close above Sept

12 high.

5) SPY & IWM : in order to move up there must be a close above Sept 12 high.

6) TSX : in order to move up there must be a close above the May 12/17 high.

Hmm, I’m not an expert but didn’t I read somewhere recently that the Canadian government is making significant policy changes regarding who is eligible to buy houses in Canada?

Limiting the pool of potential buyers just after a major bubble pops…. would seem to be a recipe for making sure prices really come down hard.

From Jan 1 of this year the government is preventing foreign buyers from purchasing real estate. There are exceptions for people on temp visas and students and such.

There are also new taxes put on vacant properties, making it more expensive for investors to hold onto homes without at least renting them out.

For sure this’ll speed the crash. But at the same time Trudeau has brought in record numbers of immigrants each year for a while now. Like 400,000+ per year in a country of under 40 million.

I bet the crash will continue, but I wonder where the bottom is when so many new people (many with money) keep immigrating. It seems to me the country will be healthier if prices drop at least 45% from their peak last year. At least then younger people will have a chance to get their foot in the door again. Time will tell I guess.

You bet that the Canadian govt is trying their best to prevent a calamity for their home-owning voter base.

The politicians insist that they have to bring in 500,000 permanent residents a year because there is a labour shortage.

Yet in the past few years, rent prices have skyrocketed in urban centres.

Last year, Canada admitted 425,000 permanent residents, and half of them went to Toronto. That’s almost a 10% increase in population.

Instead of propping up the housing market bubble, the government is creating a system of haves and have nots. Who own rental property and earn rental income are benefiting from this “labour shortage”.

You are off by a decimal.

1%

And

75% of those 500,000 were already living here.

Just changed their status.

Correction.

250,000 newcomers in Toronto is 10% growth. Which is why there is chaos in the rental markets across Ontario.

There is no “labour shortage” in Canada. Just employers can’t find people who will settle with minimum wage dead-end jobs. Which is why the government wants to flood the country with people to drive down wages and jack up rent prices.

As far as I’m concerned, Toronto residential real estate was already overpriced in 2008.

you are exactly right, john.

2008 was a super bubble.

to get back to the historical mean, prices would likely need to go back to early 2000s level (when adjusted for inflation).

CHMC was saying this at the time. Harper gave them 25 billion to shut up essentially. When in reality it was Canada’s chance to let the housing bubble pop with Americas.

Here is an article outlining how the Conservative party worked their mortgage scheme. Quite delusional imo…

https://www.cbc.ca/news/business/25b-credit-backstop-for-banks-not-a-bailout-harper-1.726162

not only this, but the FED infused/rescued canadian banks with “money” at this time.

These are great charts as usual, Wolf!

Here is my theory again.

Inflation is rising and housing prices are falling.

Inflation is rising. Some say up to 20% by the end of 2023. If due to inflation, labor and materials cost 20% more to build a house by the end of 2023 compared to 2019, then the price floor for house has risen 20%. If most of this inflation is labor cost, then the future homeowners will be making 20% more.

If a good baseline for a crash is 2019 prices (before the huge ramp-up in house prices) , then housing prices do not have as far to fall due to rising inflation.

For example, in Vancouver from Wolf’s chart, the price of a home was 900K in 2019. 20% of 900K is 180K. The new baseline is 1.08M (900+180).

After a dramatic fall in 2022, Vancouver’s current price index is 1.1M from Wolf’s chart. Not far from 1.08M.

If inflation has raised wages and the cost of a house by 20%, Vancouver is almost at 2019 prices now. There won’t be much more to fall if prices level off at 2019 pre-HB2 bubble prices.

What would be more interesting is to chart the CPI from 2000 to today and correlate house prices with inflation longer term. In the US, the inflation line (from 2000) intersected with the house price line in 2012. Right at the bottom of HB1 bubble. That is when I would buy a house. This means housing prices are tracking inflation and most of the speculation has been removed.

I thought there was a bubble in 2019. After seeing 2020-2021, I was proven wrong. Maybe I was only partially wrong.

Wages are increasing only for the lower end of the wage spectrum who can’t afford these inflated homes anyway.

Also, we all know, homes are priced not on the basis of what it costs but what people can afford.

IN essence, unless mortgage rates falls big time, I see home prices going down a lot.

I see a lot of price reductions in my hood/so-cal and I think show has just begun.

Zillow reports my home has lost 25% value from its peak., Not that I trust Zillow but still just a data point.

I see home prices going down quite a lot .

On the West Coast, including Vancouver, it’s interesting to see how much has already been lost by people who bought homes at the 2022 peak. In Seattle, some buyers who paid $2-3M for homes are now down $500-700k in terms of Zillow value. We’re talking 25-30% losses in less than a year. Ouch.

Add to that, some of these people didn’t even like the homes they bought and have buyer’s remorse, attributable the hidden problems you always find with a home that’s 40 years old.

By the time this selling wave is done, these people could be down 50% or more. And I don’t think central banks will care about them, because their numbers are too few.

FOMO can be costly.

Shame on the Federal Reserve for artificially suppressing interest rates and raising home prices to astronomical levels, without adequate consideration of long-term generational consequences and basic fairness.

@Bobber They have no shame, no conscience, and not even an ounce of fairness across the entire Federal Reserve. They are political hacks who bend to every will of the banksters and the corporate class. Let the country and the common man go to hell, they won’t shed a single tear.

Just thinking about the cost structure we have as a country – and how we would be able to compete with other countries in future gives me shudders.

“Shame on the Federal Reserve”

They have no shame. The Fed exists to service the banking cartel and the rich. Period.

That’s funny, I have sometimes benefited and sometimes suffered from Fed policies. But I guess the world is black and white, huh? Especially with a catchy conspiracy theory behind it.

Forbes had a fairly recent article about Seattle regional home prices.

At the extremes: Enumclaw (south of Seattle) up 51% YoY to Oct, 2022. Same timeframe Lake Forest (just north of Seattle) off 41%.

Seven cities had price reductions of over 10%, five had increases or over 10%.

It might appear Enumclaw’s gain (51%) outweighs the Lake Forest loss (41%), but as most here realize it would take a 69.5% gain for the Lake Forest homeowner to get back to even.

I know Wolf isn’t fond of links but I’ll include it…he can feel free to delete it at his discretion.

(I was able to read the article w/o a subscription).

https://www.forbes.com/sites/andrewdepietro/2022/12/07/seattle-housing-market/?sh=3237f1e45b26

Wait a minute…. Small towns like Enumclaw (population 12,700) DO NOT HAVE ENOUGH HOME SALES in a month to give a meaningful median price.

A town like that may only have 2-10 home sales per month. So the median price — the price in the middle – is totally meaningless. If two expensive homes sell, and two lower-end homes don’t sell, the median price spikes, though actual prices may have fallen. You cannot draw ANY conclusions from the “October” median price of a handful of sales.

You will have to look at a long-term chart, and it’s likely all over the place, with huge spikes and plunges from month to month. So to draw ANY conclusions from the year-over-year change of the median price of a handful of home sales is silly.

That opinion piece in Forbes was silly – ignorant actually, because it showed complete ignorance about the nature of median prices when there are only a small number of sales. That’s why some of the towns and areas in the article had these huge gains in median prices, and why others had these huge plunges. To draw conclusions from that is BS.

Here is my favorite chart of the median price and how it is impacted by a change in mix, in this case when two houses at the low end don’t sell. This chart reflects the size of Enumclaw’s market with 7-9 sales per month. Here the median price jumped by 12.5% because two lower-end homes didn’t sell; but the actual prices remained the same:

Wolf,

Good comments.

The author provides the numbers. He might have caveated them as you have but I still find it interesting to see the variations. I like his article. I did wonder why Lake Forest had declined so much more than the other cities. Strictly a statistical quirk or not ? I am not interested enough to investigate.

Your points are well taken, yet we don’t know that there isn’t something that could be responsible for the difference in price changes. I’m definitely no statistician but am somewhat familiar with the law of large numbers, central limit theorem, the sampling distribution of means (assumes independent events), etc.

I think its reasonable to believe the Enumclaw market has been kinder to sellers, at least in the last year, than Lake Forest, but for the reasons you pointed out, perhaps not nearly so exagerrated as the numbers might suggest.

To one of your points, if Enumclaw only had only 10 sales its median sales price would be less reliable as a measure of home price increases than were there 100 sales. Sampling theory is relevant here. Again, not my specialty, but as you probably know it allows inferences, with degrees of confidence, to be drawn with appropriate assumptions.

There could be a reversion to the mean type effect and a year from now (actually October 2023 to October 2024) Lake Forest YoY sales prices changes are more positive than Enumclaws. But I’d guess a less dramatic difference than per the previous year’s difference.

Whatever the causes, the folks who saw their homes sell on average for 51% more than than they were selling a year prior probably felt better than those who sold for 41% less than a year ago.

Their joy could be mistaken if the 2 cities previous years results were considerably reversed.

As to the housing mix issue… true we don’t know if Enumclaw had more high end sellers, Lake Forest low end.

One would need to determine where the sold homes fit historically (price wise) to infer if the sales were skewed to the high or low end. But again the larger the number of sales, the less likely such a skew exists. Or even if it exists… is of much significance.

Thank you for the useful response.

A brief followup to my other comment.

In case reader’s might be interested in sampling theory and no I don’t gave a degree in statistics.

But relevant subject natter:

Estimation theory. Confidence intervals for means. The student t distribution (if it is still called that, I’m looking at a stats book from the 70s).

The idea would be to estimate the true sales price (e.g. for Enumclaw or Lake Forest) given the sample.

And then calculate YoY difference.

This stats book i am looking at, 1975, not my favorite (though loaded with example problems !) makes a distinction for smaller sample sizes. It says to use the t distribution and one must estimate the population sales price standard deviation using the samples std. deviation. A simple formula and student t table reference allows one to calculate with chosen degrees of confidence what the actual population (Enumclaw or Lake Forest) sales prices would be.

The above comments however do not address the possible issue of housing mix distortion you mentioned.

This is no small concern.

Neither Lake Forest Park nor Enumclaw are meaningful independent markets. Enumclaw should be combined with at least all the other small towns and unincorporated areas near Mount Rainier, and Lake Forest Park should be combined with other nearby suburbs like Shoreline.

Should have been more precise, and wrote:

A simple formula and student t table reference allows one to calculate with chosen degrees of confidence what the

RANGE OF actual population (Enumclaw or Lake Forest) sales prices could be. Its not called Confidence INTERVALS for nothing.

(Obviously i don’t dabble in this area n a daily basis !).

No more updates, I promise.

One last response. This is meant to illustrate, on a simple basis (I’ve studied basic statistics, nothing more) how statisticians might reason with the Enumclaw and Lake Forest Park data given the rather small sample sizes involved.

1. Looked at one major real estate website: Enumclaw had approximately 16, 30, and 19 SFH sales for December, November, October of 2022. More than I would have expected.

The median sales price though looked lower than that reported by the article (per Redfin… perhaps they used a 3 month average centered about October, who knows, I doubt it). But no matter. I was just interested in number of sales.

So for simplicity sake let’s say we have 20 sales for October 2022 and 10 sales for October 2021.

2. I mentioned the t distribution in a previous post. Yes relevant but it makes more sense to use the formula for confidence intervals for differences (a similar one exists for sums as well). Its a pretty simple formula.

It assumes the sample medians come from an underlying distribution that is approximately normal. Is this true for home sales prices in a given month ?

I dont know. Probably… but what constitutes approximate ?

For now (this is only for illustrative purposes) let’s assume the sample medians do come from near normal distributions.

3. The sample median difference is

828k – 547k or about 280,000.

Our sample sizes are 10 (2021) and 20 (2022).

We need to estimate the standard deviation for the sales prices in a given month. One can use the sample data to do this (its a biased estimate, multiple by n/(n-1) for the unbiased estimate). Or perhaps one can use historical sales data for Enumclaw to provide an accurate value.

In any case, suppose we calculate October 2021’s std. deviation to be 150,000 and October 2022’s as 200,000.

If we plug these numbers into the confidence intervals for differences formula we have:

280,000 +/-

z × [sq. root (

(150×10³)²/10 + (200×10³)²/20 ) )]

in which z represents the confidence coefficient (well, that’s what it was called in the 1975’s terminology)

which = 280,000 +/- (z × 65,000)

If we take z to be 1.0 (one standard deviation out) this corresponds to a 68% confidence interval;

to be 2.0 this corresponds to a 95.5% confidence interval;

and to be 3.0 to a 99.7% confidence interval.

Substituting the values of 1, 2, and 3 in our equation we get:

1. 68% confident that the true difference in median prices is in the range (215,000, 345,000)

2. 95.5% confident that the median price lies in the range

(150,000, 410,000)

3. 99.7% CI (confidence interval) is

(85,000, 475,000).

Intuitively this makes sense.

The more confident you wish to be in your belief (99% say) the greater the range of possibilities for which one must make allowance.

4. The above hinges on the sales data being near normal. If it isn’t then one can attempt to find a (so called)

non-parametric procedure to support degree of belief inferencing.

5. And, if there is no non parametric procedure … and it is sufficiently important … an expert statistician (researcher) might be able to create her own non parametric procedure specific to this task.

6. I also briefly looked at Lake Forest Park sales data at the same real estate website. It had 5, 15, and 13 sales respectively for December, November, and October 2022.

Somewhat less than Enumclaw. In itself this reduces confidence in results. Its standard deviation of sales price data would also come into play though, too.

7. My guess is statisticians might not use these formulas anymore… all data look up instead. But the idea of confidence intervals presumably lives on.

I think the Central Banks sacrificed the FOMO lemmings during the last few years. Hopefully, the sacrificial lemmings qualified for the overpriced houses they bid up. And hopefully during the last few years, the sales volume was low so only a few lemmings were caught. The reward is an extremely low interest rate on an underwater house that buyers can enjoy for a long time.

My recommendation is exactly the same as HB1. Buy a house for the long term and don’t panic sell before 12-15 years. I would bet anyone that if you follow these guidelines, after 15 years, you will not be underwater. Just enjoy the house you worked so hard for and paid so much for. Otherwise, why did you buy it in the first place? I don’t pity anyone who purchased a house to make a fast buck.

Sure time in the market beats timing the market unless, say, the Japanese top. Then who the fuck knows, I guess.

But that’s a long time to hold. People tend to move in less the timescale you are proposing.

Congratulations, buyers at the top. You are potentially a great real world example of opportunity costs. Feel better, now? Hope you did not overextend in carrying that debt!

20% downside left. Til then, raise cash and get ready to buy.

I am house hunting in southwestern Ontario, kinda where the US is visible on the other side of Detroit River.

On one house I put a bid after taking a close look. Quite a few things would need fixing or upgrading but it seemed doable.

Asking was 400k, bid 400k, another bid over 500 k, both declined.

The realtor then explained that the house was bought a year ago by a company for 700 k and the seller expected an offer 250 above asking.

Few days later it was re- listed for 600 k.

The only houses I have seen here selling in this area are 400 to 500 k asking and decent shape.

Most offers are from 650 to 900 k. Not many bids for them.

Quite a few “new” listings show pictures from the summer. That indicates a re-listing.

An average 2 bedroom condo in Toronto market rents for about $3,200 CAD per month. Current market value would be around $750k CAD. That’s a 3.35% cap rate. Cash earns 4.5-5% at the moment. Valuing it at a 5% cap rate gives a value of just over $500k. Looks like a Mexican standoff:

– A condo like that at $500k would bring us to 2015 prices. A huge proportion of homeowners would be underwater. Developers would default left and right.

– Rising rents to justify the market value seems unrealistic. Rent is what the market will bear and people are approaching their limits.

– What’s left is adjusting interest rates. More rate hikes from the BoC are expected but the market is calling a bluff with Canadian government bonds at 4.55% 1 year, 3.38% 3 year, and 2.93% 5 year.

Would not want to be a Canadian residential landlord right now.

When you look at the house prices as a short-term investment, and the numbers don’t make sense, it is time for primary homeowners to start looking for homes to purchase for the long term.

1) Fixed mortgage rates mean fixed payments for 30 years.

2) Rents always trend up. Fixed rate house mortgages do not.

IMHO, a house purchase is for living in long term. It should not be a speculative short term investment. Sadly, it has become a short term speculative investment which is now ending abruptly. Housing prices will settle down to the inflationary mean. This means no speculation.

Long term homeowners, enjoy your low mortgage rates and don’t panic.

You will have a happy home for the next 10 years before considering selling and moving. You may have done cheaper by renting for the next 5 years, but you will not be building enormous equity with low rate mortgages, Long term, you will be ahead. Short term, just enjoy your house and don’t panic. Good things happen to those that wait.

Long term house investors, take your yearly tax deductions. Hang on for 10 years and when you retire and you will be OK for rental income. Don’t panic and any extra cash you need to pump into the house to keep afloat will be worthwhile. Nothing ever goes as planned.

Don’t worry!!! All the fired H1Bs will flock to Canada and pick up the slack. Keep the faith!!! Never surrender!!!

The real pain has not started here in Canada yet. There are very few homes for sale right now, as sellers want the old peak price and new buyers are waiting for a bottom. Plus its winter here, and not the best time to sell a house in Canada. As spring approaches and mortgages have get renewed, and prospective buyers try to get pre-approved mortgages, well watch out below. The only pivot I see coming will be from denial to panic.

“The only pivot I see coming will be from denial to panic.”

Ah that’s sheer poetry , too !

“So now comes the invoice for the drunken money-printing party,” this statement is priceless, thanks for the chuckle ;)

Which would be which “party,” in the years since 2016? Which “party” in 2008? I like to laugh at oversimplifications too!

It’s a hilarious quote from the article. Read the article and your questions will be answered.

According to The Telegraph Sweden, where I live, is the country where housing prices fall the fastest in the developed world.

Look for: “Inside Sweden’s collapsing housing market – and how Britain could be next”

It’s only the first inning. Be patient, young Padawan, when the bottom really falls out later on, many countries throughout the world will be vying for the title of the world’s worst housing market.

Seoul is also falling. Think it’s gonna be bad here since they’ve built way too much, and prices are way too high.

This story would be repeated all over the world as the cheap money was available to all, irrespective of the location.

Santo Sessa (Sessa real estate) has a very nice weekly update of the Toronto RE market.

Breaks it down: west, central, east and then

SFH (detached), semis (duplexes ?), townhouses,

condos.

Just out of curiosity I check out his Utube video every couple of months. (I live in eastern Washington, not a Canadian citizen).

His statistical coverage usually starts a few minutes into the overall presentation, e.g., it was about 5 minutes into the last one I recently viewed. Nice presentation.

Just hoping this reset goes all the back to 2020 and beyond, depends how long they can stomach the interest rate pushback from the wealthy asset gamblers, sorry I mean investors. Flipping houses quickly disappears when money borrowed has a legitimate value.

It’s not a housing market “collapse”. It’s a central bank folly.

It is little wonder life expectancy is plummeting. Living on debt, variable interest rate loans, borrowing 110% against future equity to feed opportunity FOMO, losing at the crypto wheel of fortune, how can anyone live like this?

Good old Aesop’s Grasshopper’s word continue to ring loud on a daily basis.

“I didn’t have time to store up any food,” whined the Grasshopper; “I was so busy making music that before I knew it, the summer was gone.”

Hey, all you sentient beings out there,

WHY are long-term yields dropping and 10-year Treasury prices are rising

IF

The Fed REALLY were executing QT?

HELLO?

(The Fed and the bankers are lying about QT. The Fed is executing stealth QE still, buying long-term Treasuries hand over fist. Raising short-term interest rates only hurts the little people, NOT the big investor/banker classes, who finance their deals with long-term debt)

Holiday sales numbers were below expectations. I think both the bond and stock markets are beginning to see that a recession may be in the offing (as some banks have already prognosticated.) How severe or shallow it is going to be remains to be seen.

Even if there’s going to be a recession, only an idiot or central banker who prints money out of nothing, would buy 30-year bonds with yields only half the official (fake) inflation rate.

CREDIT CARD,

Why did the 10-year yield drop to 0.5% in the summer of 2020? Weren’t YOU running around at the time promoting some BS about the Fed pushing long-term yields into the negative? People who believed that and bought at those yields got their faces ripped off.

There is nothing stupider than markets under consensual hallucination, as I call it.

HELLLO?

WOLF RICHTER,

That there are people stupid enough to buy long-term bonds yielding only 0.5% ought not deflect from the fact that ONLY central bankers have the ability to push yields that low. ONLY central banks have the power to issue currency in unlimited amounts and commit massive fiduciary fraud via purchase of long-dated Treasuries and MBSs, ONLY for purposes of artificially reducing long-term interest rates — in other words, to manipulate the markets expressly to induce malinvestment.

Some of those people you look down upon, were small investors who were misled by the Fed and their Wall Street partners, into purchasing bonds and bond funds with their retirement money, suffering in the process catastrophic losses.

Are you going to blame the people for believing in their leaders and make their investment decisions based on what the Fed and Wall Street are telling them? That the currency is sound, inflation is transitory, and that low-yielding bonds are a natural phenomenon, and not caused by Fed buying behind the scenes?

If the new OSFI rules about debt not being more than 4.5 times income are implemented the real estate market will collapse especially in places like Brampton, Mississauga and Milliken Mills.

Bubble here Bubble Their Up then Down

If the shoe fits try it on Humm not again !

If the Fed only tickles The rate increases all over again by caving in soon reducing the increases before Inflation is under control Pacifying the upcoming election well what then ?

You can’t effectively stabilize rates if Inflation is still in place unless you find additional tools > other ways and it works

But as the Fed created , allowed all this anyway if they do Tame inflation away then what ? Not do it again because so much money was already made ? or simply do it all over again > start all over again recreating Inflation again Needs new shoes ? I wish I had the answer