The Fed’s cumulative losses reached $20.5 billion.

By Wolf Richter for WOLF STREET.

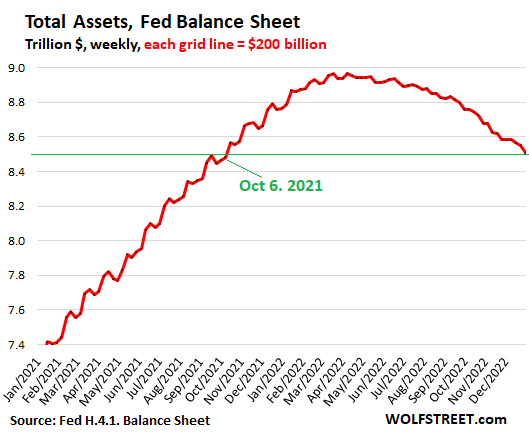

Total assets on the Federal Reserve’s balance sheet dropped by $458 billion since the peak in April, to $8.51 trillion, the lowest since October 6, 2021, according to the weekly balance sheet released today, with balances as of January 4.

Compared to a month ago (balance sheet released on December 8), total assets dropped by $75 billion.

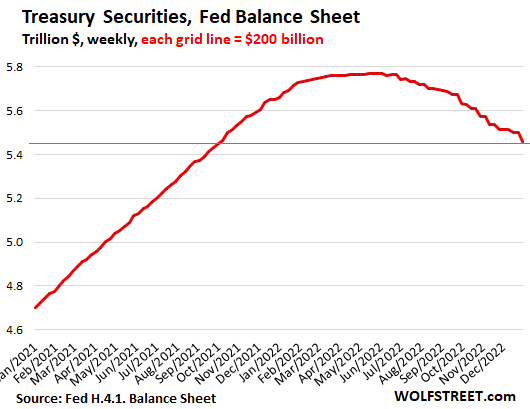

Treasury securities: -$314 billion from peak.

Treasury notes and bonds mature mid-month and at the end of the month, at which point the Fed gets paid face value for them, and they roll off the Fed’s balance sheet.

Since the peak in early June, the Fed’s Treasury holdings fell by $314 billion to $5.48 trillion, the lowest since October 6, 2021. Over the past month, the Fed’s holdings of Treasury securities fell by $57 billion, near the cap of $60 billion.

About half of the $3 billion difference between the cap and the roll-off is due to $1.5 billion of income from inflation protection that is not paid in cash but is added to the principal of Treasury Inflation-Protected Securities (TIPS).

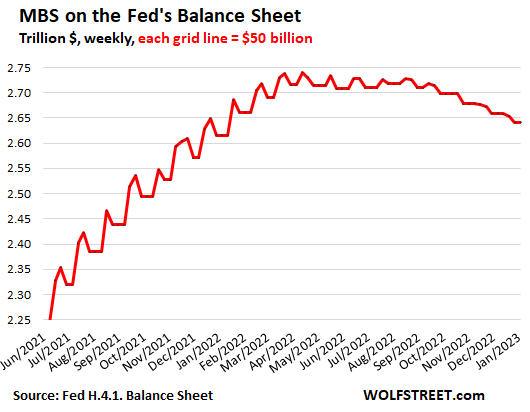

Mortgage-backed securities: -$99 billion from peak.

The balance of MBS dropped by $99 billion since the peak, to $2.64 trillion. Over the past month, the balance dropped by $17 billion, below the cap of $35 billion.

MBS come off the balance sheet largely via pass-through principal payments as mortgages are paid off or are paid down. But these pass-through principal payments have turned into a trickle after mortgage rates spiked, causing refinancings of existing mortgages to collapse and home sales to swoon. These pass-through principal payments, which reduce the MBS balances, are the downward zigs in the chart below.

The Fed stopped buying MBS entirely in mid-September, after having already cut its purchases to near nothing in the prior months. These inflows are the upward zags in the chart, which ended in September.

There have been some mentions by various Fed governors about the possibility of selling MBS outright to get somewhere near the cap of $35 billion a month – which means that the Fed might have to sell between $10-$20 billion a month in MBS. There was no mention of this in the minutes of the December meeting. So we’ll see if we get more discussions of this cropping up.

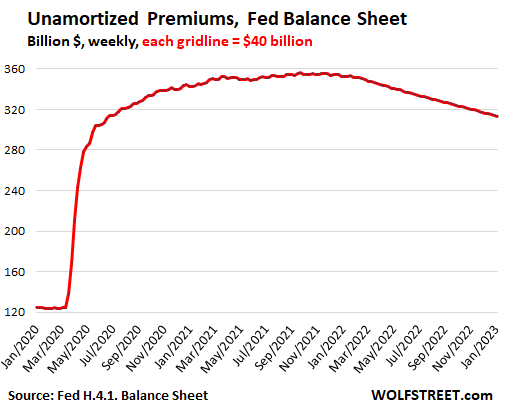

Unamortized Premiums: -$42 billion from peak.

The securities that the Fed bought in the secondary market, at a time when market yields were lower than the coupon interest of the securities, the Fed, like everyone else, had to pay a “premium” over face value. But when the bond matures, the Fed, like everyone else, gets paid face value. In other words, in return for the above-market coupon interest payments, there will be a capital loss in the amount of the premium when the bond matures.

Instead of booking the capital loss when the bond matures, the Fed spreads the write-off over the life of the bond by amortizing the premium in small increments every week. To show the process of this, the Fed accounts for the premiums in a separate account, called “Unamortized Premiums,” which has been steadily declining as the premiums are written off.

Unamortized premiums dropped by $42 billion from the peak in November 2021, to $314 billion:

Keeping an eye on potential warning signs.

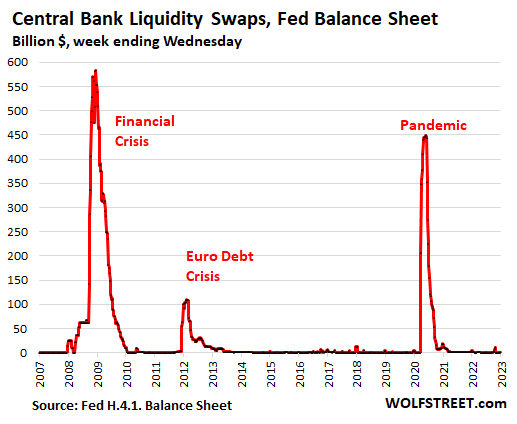

1. Central Bank Liquidity Swaps. The Fed has long had swap lines with a number of other central banks, where the Fed can swap dollars for their local currency, via swaps that mature over a certain time period, such as seven days, at which point the Fed gets its dollars back and the other central bank gets its currency back. There are currently only a minuscule $412 million in swaps outstanding. But you can see why they might be a warning sign:

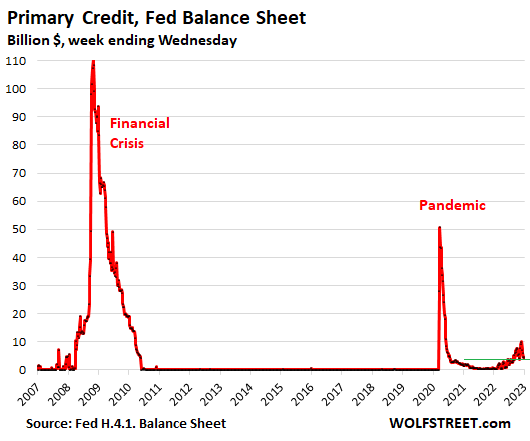

2. “Primary Credit.” The Fed lends money to the banks at the “Discount Window,” for which it charges banks currently 4.5% in interest.

So a few months ago, we started seeing Primary Credit ticking up just a little. Still nothing to worry about. This peaked at $10 billion in late November and has since dropped back to $4 billion. Just keeping an eye on it:

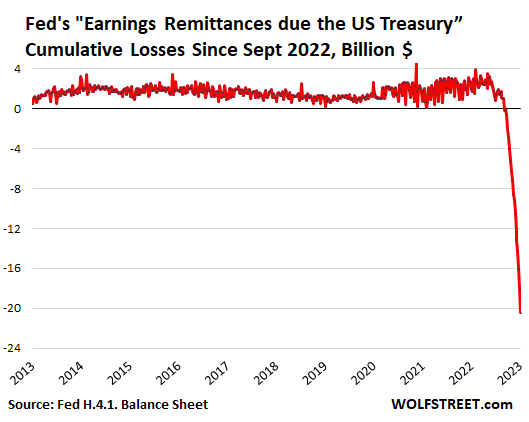

The Fed’s cumulative losses.

The Fed has revenues from the interest it earns on its $8.5 trillion in securities, and it earns fees from services it provides to the banks. And it has expenses, including the interest it pays the banks on reserves and the interest it pays its counterparties, mostly Treasury money market funds, on overnight Reverse Repos. By raising its rates, the amounts it is paying out in interest started exceeding what it is earning in interest, and it has been racking up losses since September.

The cumulative losses since September reached $20.5 billion on the current balance sheet.

But the Fed is not like any other place. It creates its own money and can never run out of money, and so it can never go bankrupt, and this is just an accounting issue: where do we stick the losses, rather than booking them embarrassingly against capital?

So since September, when the losses started piling up, its Total Capital account has remained unchanged at $41 billion.

Those losses show up instead in the account, “Earnings remittances due to the U.S. Treasury.” I explained all this stuff in detail here.

The interest expenses will come down as QT further reduces the combined balance of reserves and overnight repos, and so the losses will come down. But this will take time.

Meanwhile, here is the Fed’s “Earnings remittances due to the U.S. Treasury” account, showing the cumulative losses since September, which hit $20.5 billion as of the balance sheet today. This is probably the funniest looking account the Fed has on its balance sheet:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

QT is way too slow. And they wonder why their inflation fight is not working?

The markets are reacting to it just fine. Look at the drops, plunges, and collapses. Any faster, and we’d have total chaos. QT is designed to run for years, it’s not a short-term thing. This is why the market downturn won’t be over any time soon. There will be bear-market rallies, but overall, while there is QT, markets are heading down.

Why chaos if QT was equally fast as QE?

Why chaos if the ride down was equally fast as the ride up?

And why not adjust laws and regulations to contain any collapses in the financial sector to the financial sector of the economy?

Would maybe be brutal to finance and their topp earners, but if production and distribution of goods continue unaffected socitety would go on.

Exactly 👍🏻

“And why not adjust laws and regulations to contain any collapses in the financial sector to the financial sector of the economy?”

You’re joking right?

You believe in magic too, right?

I don’t think that is how anything works or could work.

The core problem here is that the American economy has become dependent upon central bank and federal government cash infusions to not plunge into recession. Our brilliant MBAs have all shipped production offshore, reaped massive gains, and left the overall economy with minimal ability to produce goods and services equal to the value of what we consume.

Honestly, so many people i know buy stuff they just dont need. On a yearly basis we keep stripping this nation of the wealth that was built up over decades and plunge ourselves into more and more governmental debt.

The voracious industries that feed off of government largess – military, healthcare, housing (through gov financing), higher education (student loans) – among many others, just dont care if they wreck the economy and they have the lobbyists and media power to stop anyone from questioning what is happening. Have you ever wondered why student loan forgiveness has such broad support in DC? Because the higher education industry wants potential future students to take out more loans and not question the cost and value of the education.

People NEVER make good economic decisions with OPM (other people’s money).

“why not adjust laws and regulations to contain any collapses in the financial sector to the financial sector of the economy?”

For the same reason you can’t ‘adjust laws and regulations’ to contain damage from jumping off a building. Laws and regulations aren’t magic.

Why fast QE and slow QT?

It’s called financial engineering. When you don’t produce anything and everything is financial paper, crypto, magic hats and derivatives, you need to be careful, in order not to destroy the 1 %’s wealth.

30 trillion debt and counting … and when you add all the companies debt, the FED debt etc … that’s nitroglicerin and that’s what you must not play with.

The real underlying issue is debt. Debt is always someone else’s income. Once debt is created, raising the interest rate devalues the asset. Assets are used to justify (back) the debt. Lower asset values mean a bunch of bad things. In some cases, debt is called. In others, you can not refinance. But in general it is the reverse of the Wealth Effect. Doing it slowly is painful enough.

There is a pyramid of debts. Much of it was built upon the assets on the FED’s balance sheet. Removing them too quickly could or probably would cause the entire pyramid to collapse.

If the FED doesn’t own the debts, someone else has to. Where would all that liquidity come from as everyone’s assets are devalued?

I’m beginning to believe that a ‘soft landing’ is what we are going through. If you really look at the ANFCI since when it was -0.60 in Jan22 it went to +0.16 in June and then -0.13 in Aug, back to +0.16 in Oct and we are now down to -0.21.

Obviously this trending down since Oct. indicates probably more loosening of financial conditions than the Fed would like. Leverage is still high, but it’s almost like an airplane landing on a runway at 0.0… it just bounces up and down trying to get on the ground.

Interest rates have to keep going up to wring the leverage out of the markets, but I bet we’re on our way to smaller increases. Inflation is coming down and I believe the Fed might actually have some control over what they are doing.

My 2 cents, which ain’t worth what it use to be!

Index Suggests Steady Financial Conditions in Week Ending December 30

The NFCI was unchanged at –0.21 in the week ending December 30. Risk indicators contributed –0.05, credit indicators contributed –0.06, and leverage indicators contributed –0.09 to the index in the latest week.

The ANFCI edged down in the latest week to –0.21. Risk indicators contributed –0.03, credit indicators contributed –0.03, leverage indicators contributed –0.05, and the adjustments for prevailing macroeconomic conditions contributed –0.10 to the index in the latest week.

Inflation is not going to come down with Congress having passed an over $1.7 TN spending bill. They are operating at cross purposes with the Fed. I think this will force the Fed to tighten even more. I also think that governments will try to pressure central banks to pivot because they are heavily indebted and their interest payments are rising to eye popping levels.

Soft landing wouldn’t have been soft if Bank of England had not intervened in their impending pension crisis though. That sort of contagion would go global fast.

Like Japan backing off and stimulating their QE (still) with the highest monthly purchases in their history last month. They are the one final bastion of easy liquidity in international markets and when they bumped their rate limit for yields stuff started to go sideways again.

You can see the fragility of markets but it is being met with flexibility whenever impending crisis rears its head. Estimates exist that the total value of global derivatives is ~1 quadrillion dollars (1,000 trillion). When you bear that in mind, it makes the whole deck of cards look very unstable.

Reply to Bobblehead – The core problem of repressing volatility is that you end up stoking moral hazard, where people take risks that outweigh the benefits and that leads to malinvestment.

I see people are still buying homes at ridiculous prices that cant be supported at these interest rates. They are betting that the interest rates will need to plunge in the future. Either that, or completely ignorant.

Governments just need to let it all come crashing down and DO NOTHING.

Everything our government does leads to increased wealth inequality and a lack of happiness. A large middle class should be the top goal of our economy.

I was watching some CNBC clips from 2007 and they were very fond of the “soft landing” phrase then as well. They were all convinced that the Fed had achieved this “soft landing”

We all know how that turned out…

It started as a “housing correction” and then progressed to a “credit crunch” and eventually became a full blown “financial crisis” over a period of at least 18 months

As long as the labor market remains strong and growing, we’re not in a soft landing. A soft landing requires a modest amount of job losses. We don’t get to the other side without going through a real recession.

Hey Wolf, I don’t know if you follow or have any insight into the NFCI/ANFCI… but I wonder what the ‘Adjustment for Prevailing Macroeconomic Conditions’ is?

I always thought it reflected what the Fed was doing with rates, but I noticed that it has trended DOWN since a high of +0.16 in June to now being -0.10.

Is this reflecting perhaps a wide range of things such as Commodities and the like?

This is the best description I could find:

The adjusted National Financial Conditions Index (ANFCI) removes the variation in the individual indicators attributable to economic activity and inflation before computing the index.

And for those who wonder what the heck I’m talking about:

https://www.chicagofed.org/research/data/nfci/about

I don’t pay detailed attention to the index, I just look at it. So I can’t answer your question.

I think I’m maybe getting it: “removes the variation in the individual indicators attributable to economic activity and inflation”… so yeah operable word is ‘inflation’.

Inflation in June was pretty high and as it has decreased to our current condition the ‘adjustment’ to a looser condition has trended with it.

Depth Charge is a big boy, so I’ll let him speak for himself, but I don’t think it’s the markets he’s referring to regarding “inflation fight not working,” but general inflation in the economy.

A drop in stocks makes it easier for people to buy stocks, but it doesn’t help us with our rent, energy, haircuts, etc.

Yield curve inversion must be the worst since the early 80’s if not ever. Measured by percentages, I don’t ever recall it being larger, except maybe 1980 or 1981.

That’s going to cause a problem at some point.

Yes, today’s inversion action especially is a bit extreme.

Wolf – If at some point in time, if they bring down interest rates but continue the QT, do you expect the market to still keep going down?

What I am trying to understand is what has the most effect on the market, interest rates or QT?

I think a lot will depend on where the market will be at that time. If the S&P500 is down 50%, QT continues, and rates drop, the market might go up some, but forget the QE-style craziness. QE has been a HUGE force in the market since 2009. Without QE, the S&P500 should grow somewhere near the pace of the economy 0-3% a year in real terms (after inflation).

To me the big issue with the stock market is going to be what happens in real estate. If interest rates remain elevated, it will continue to kill demand and eventually, sellers will need to get much more aggressive to sell homes. Even if a homeowner has positive equity and doesnt sell their home, they are impacted by lower values, as their perceived wealth has dropped. Spending will dry up.

I think real estate could drop 50% from peak to trough, with massive foreclosures and short sales at the end of the cycle. We simply need to reach that point where prices have remained on a downslide for long enough that owners finally collapse on the idea that real estate always goes up. That takes time.

When you look at the monthly payment for homes at even the current reduced prices, they are simply unsustainable, given local income levels.

Keep in mind, stocks and bonds and real estate are priced based on the latest sale, which is a small fraction of the total inventory. It takes time for the overall level of prices to reach a new level of equilibrium.

Sucking 75 bilion out of the markets every month will have a cumulative effect over time. And that is only the US central bank, the other central banks are also shedding assets.

The stock market is not the FEDSs concern. It is inflation and employment.

They did in 2009 through 2015ish to drop employment. If you look at notes, they knew it would make a small percentage of people much more wealthier but in their mind that was a better outcome then having a lot of people struggling and out of work.

Now they have high inflation as a result of QE but at least people are working and can still buy food and have shelter. But now inflation is hurting the working class thus the FEDs next goal is to reduce inflation but keep full employment. They just try to turn the levers to make these two things happen. The outcome is some people benefit much more than others if you can guess the FEDs game plane and front run it.

If the stock market drops…no big deal unless it starts to effect the economy via fear, over reaction, etc.

You say that QT is designed to run for years, but the market is telling us that it believes there will be interest rate cuts by the end of this year, and I assume that the market assumes QT will be stopped as well.

All this fake money needs to be taken out of circulation and the Fed mandate needs to be severely restrained. But I really doubt that will happen.

@gametv – I agree. It will be difficult to remove all of the QT in one program/task. I am guessing they will try and there will be some start and stops over time depending upon the economy. It took them 10 years to get to 9 trillion. It could take 10 years to reduce it and there will be more bull and bear markets along the way.

In reality, they may never be able to reduce to zero unless they come up with some other type of financial engineering algo. Maybe they create a new government entity or bank that just absorbs all the balance sheet so it disappears. Don’t count it out as I am now quite amazed and what the FED can do. LOL Afterall, we never new of QE until 2010.

“reduce to zero”

They CANNOT reduce to zero. The Fed has had assets from day one. A bank MUST have assets, even a central bank.

This might be helpful for your understanding. Give it a careful read:

https://wolfstreet.com/2022/09/05/by-how-much-can-the-fed-cut-its-assets-with-qt-feds-liabilities-set-a-floor/

There is NOTHING more stupid than the “market.” The “market” believed that the 10-year yield would go negative in mid-2020 and pushed the 10-year yield to 0.5%! And whoever bought got their face ripped off. It was the stupidest move ever. The “market” is so incredibly stupid that it hurts.

But wait a minute… every trade has another side.

A stupid trade is a smart trade from the other side. Those people that SOLD the 10-year in mid-2020 made a killing. Today, those who DUMPED the bonds at those prices, those are the smart ones, not the idiots who bought them. Same in mid-2020.

If you listened to Professor Jeremy Siegel on CNBC, you might have heard inflation has diminished. This is subject to change due to war, sanctions, demographics, climate change, monetary and fiscal policy, etc.

Yep, Core Inflation has come down from about 12% in Mar22 to about 6% now. So your point is inflation will change?

Probably. The will come up with a new calculation for core inflation. They will not include food. They will only include HDTVs. LOL

/sarc

Sorry. I just lost that 458b. My bad.

Swept it under the rug maybe?

I was planning on starting my own country, Powello.

Ooo, Powello sounds nice. Anything like Cryptoland?

Come one! Come all! Plan your visit to Powello! Everything is free! Sleep on a bed of dollar bills! (Cheaper than buying the bed.) Enjoy a backyard bbq of grilled NFTs fired up by — you guessed it — lit dollar bills. (Cheaper and more sanitary than gas.) Come to our family tavern and drink gas. (Not needed for cars since only EVs are allowed in Powello.) Attend our investment seminar and learn how to lose 8% of your money every year. Hahahahahajajaja

Will house still be overpriced like it is in SoCal? I assume people will justify it by saying because of the weather..

It’s OK Merlin, I’m still impressed that you created 5 trillion out of thin air in just 2 years.

DOW was 29k in Feb 2020, 19k in March 2020 covid, 28k Sept 30, and is now 33k as of today.

Of course in inflation adjusted amounts, the market is down, but anyone holding on to cash is just losing because the market may not crash lower (except in inflation adjusted dollars).

Fed Reserve seems to be manipulating cash holders to buy. Nowhere to hide. Instead they seem determined to allow inflation to take hold to preserve the numbers in the market. Nasdaq, s&p500 are still above pandemic highs.

This is a slow pressure release at the cost of cash assets and to the benefit of long term debt. Without political pressure to stop inflation by US citizens (which does not appear likely to happen with ever increasing spending by the government for benefit programs whether requested or not), I worry that simply waiting for the bear market to take its course will not be sufficient and that the Fed Reserve will continue to intentionally “be surprised” by the inflation that will not return to 2% or lower…

Either that, or there is tremendous resistance in the markets and as many of you say hopium or at least hopium to find other bagholders and catch the falling knife. Problem is nobody but insiders know the timing…

If the system weren’t rigged by insiders who can print money or increase or decrease interest rates and at least influence inflation/deflation rates (Thomas Jefferson’s quote on inflation and deflation come to mind) and benefit their friends, I would feel more confident on how to protect my money but… Look at FTX. Many from State Street SSGA.

The largest holders of shares in Vanguard, State Street, and Blackrock are each other. Will they really let each other fail? Or leverage their massive political and personal connections to block the fed reserve from raising interest rates in a meaningful manner aka Volcker to crush inflation. Having leveraged up, instead of being forced to leverage down, they spread out the pain they are supposed to eat for their role in this and spread it out to the peons who get paid in cash…

I think in so much as Democrats hold office, they will print money and this stock market won’t crash and money will inflate instead. I would like to be wrong, but I worry I am not. Real estate may deflate in real terms but although I wish for itdon’t expect anything like 2008. And if today’s Republicans come to power, I’m not confident they will maneuver for fiscal constraint although there is maybe a higher chance since their constituency seems less centered in industrial/education centers (excluding military).

Instead the average person will eat inflation and learn to be happy with 4-5 dollar gas at the pump (CA), grocery bills that used to be 50 now costing 120… services inflation everywhere, and learn to request along with all the other slaves in metro areas for government assistance programs so they can pay rising rent to the landowner class that will cheer the government on for subsidies for these peasants knowing full well that money will end up in their hands eventually…

This system is grotesque with only one end… collapse. A cancer has taken hold of the body and is eating more than what the body can sustain, starving off the real economy until it is forced to outsource, mechanize, insource cheap labor via immigration, and then play interest rates with exaggerated real estate values while pretending everything is worth more than it is in the a large bubble.

Like the very wealthy can buy their children into prestigious universities but the lower upper and upper middle class when they try to do the same they get hammered by the law, there are insiders that go to jail and insiders that we don’t hear about that are already part of the system.

At this point, we are all slaves of the Fed whether we believe it or not. If we want inflation to come down, they need to be abolished. As for whether more serious things should happen to these “conscientious” central bankers, I’m not radical enough to want to disturb my quiet life. I just want to not be a bag-holder through inflation or a bag-holder via stocks or a bag-holder via real estate. Only choice I have is to a partial bag-holder and work harder with no deals to be found. Unbelievable…

Hear, hear! Couldn’t have said it better!

Bush spent $2 trillion in Iraq, Trump spent $7 trillion bailing out junk bonds during the pandemic, Clinton is the only president to produce a surplus.

Stop the political gaslighting, you’re not fooling anyone.

If you really believe market is going down buy puts and dividend stocks. There is always a way to make money in all market conditions.

Anon,

“Trump spent $7 trillion bailing out junk bonds during the pandemic”

You may want to check your source. The entire US junk bond market is only about $1.5 trillion.

Stop it Anon, those are 20 year old talking points.

Presidents have some authority over the budget, but Congress is in charge of the purse.

It was the Gingrich Congress that produced the surplus. But it wasn’t that much of a surplus, because a lot of that was capital gains from the easy money of Greenspan.

And I’m hoping to see the DOW <8K… For me, another fellow bag-holder (aka modern slave), that would be fun.

Yes! The Central Scrutinizer has been in control for a long time.

“If the American people ever allow private banks to control the issue of their currency, first by inflation, then by deflation, the banks and corporations that will grow up around them will deprive the people of all property until their children wake up homeless.” – Thomas Jefferson

It has really come true 😡

Inflation and deflation are going to be either the balancing things keeping things within limits, nudging back and forth (i.e., regulation, like your heartbeat or global temp), or steering them out of limits (i.e., runaway processes, veering to chaos).

So who or what is to do the (absolutely needed, indispensable) “regulation”? This blithe quote glosses right over that, reflecting Jefferson’s gross idealism and naivete on things financial. Such talk sounds ponderous and meaningful but is, IMO, cheap. It poses no solutions. It is classic Jefferson hand-waving, windy idealism. No wonder he loved the French Revolution, which veered into over-idealistic chaos.

And look at the wonderful job done by the latest postured alternative, crypto. Total clown show, plus theft.

Jefferson was in debt when he died. A genius in many categories, but not in finance, and there was no FED to blame.

The human temptation to print money instead of work and moral hazard needs to be restrained. That’s what a metal standard was theoretically for. Understandably there is going to be some fluctuation in the value of currency based on perceived worth and stability but the human component must be minimized or balanced.

Fiat currency means whoever controls the fiat currency is master and whoever doesn’t but is forced to use the fiat currency is slave.

For example, health insurance.

Insurance company may contract with major employer corporations to provide HMO or PPO insurance. Physicians cannot get good rates because insurance company owns all patients so they join hospitals and medical groups. Hospitals aren’t strong enough so they merge into systems or alliances. Some cities there are only 2 major hospital alliances with almost all physicians vs 3 insurance companies with almost all people as patients… minus medicare and medicaid etc.

If you’re outside this system as a patient or a doctor, you have no access except the emergency room and you get a million dollar hospital visit bill or a 5 dollar reimbursement/no patients to take care of. The systems make you a slave and the executives may or may not make the money depending on how much they deny their human temptation to not skim. There are good execs out there but like with all things, comes at a personal price.

You lose control over price and are forced to hope they will price/negotiate reasonably without any winking to each other. You and physician are slave to both insurance company who doesn’t work for you and the hospital who doesn’t work for you since insurance company will ignore you to raise insurance premiums using the hospitals/physicians as an excuse and the hospitals will charge you a million dollar bill if you don’t pay the insurance premiums out of pocket because that’s what they bill the insurance company but receive only 10% for.

The physician will be told to accept 5 dollar payment or leave it or accept a salary from the hospital or leave.

VA pays academic hospitals 75k for a same day transfer for a $150 dollar physician procedure that they can just pay the physician for because of the many layers of rules/bureacracy/ medicare paying % of cash rate, etc that exist in the USA. Yet you are forced to use this system.

A universal healthcare system would be even worse IMO because you have even less leverage as its the final consolidation. Breaking the monopoly and competition is what can fix this but do you have idea of the lobbying dollars behind this system? Do you feel free and in power or do you feel a slave? Im guessing when you look at your premiums if you are self employed you do. If you are employed w2 with benefits, you should realize those benefits are worth far more to you in cash because the middle man takes such a huge cut.

Federal reserve controls the supply and interest and therefore value of money. They own you. They are outside the system. They are supposed to be governed/monitored by the government but the problem is that they are not. 2008 great financial crisis was proof of that. QE is proof of that. Dragging their feet on QT is IMO proof of that.

Banks used to fail in the past but some. Not the whole country and possibly world. Not those who were forced to buy into a system that doesn’t work for them. When Lehman went down, the effect was catastrophic and many lost their stuff precisely because of the systems failure.

Jefferson was wrong about many things but it doesn’t mean he’s wrong about everything. Yes, he denied that the French revolution he idealizes so much was guillotining people and tried to accuse opposition parties of making it up. But I think he understood the danger of human temptation and that’s the point of the quote. Do you feel the Fed Reserve has demonstrated serious commitment to fighting inflation to get down to 2% over the last 2 years.

If the answer isn’t abolishing the federal reserve, then an answer to monitor it better with severer punishment for corruption/manipulation needs to be in effect. Until recently, Fed Reserve officials were permitted to play the stock market. Human factor.

Crypto is a bad example as are NFTs. Using tulip mania to justify central bank excess is misleading. Central bank and government should have come down hard on crypto when it started. As it should have on inflation. As it should have on that casino called the stock market.

Thomas Jefferson died in extreme debt. Best not to listen to his advice on finance…

Dying in extreme debt is not bad if you had fun with the money. After all, no one will come after you to get the money.😉

Actually, as the monetary system is rigged, going down in extreme debt having spend way more than earned is a rational thing to do.

And because you believe things are “rigged”, you can do whatever, as long as it feels good.

Maybe something to be said for that; hell, if you’re at the thin edge of your mortal wedge anyway, why not spend it all & then some? Solvency is an earthbound fixation.

Jefferson — another one of these over-revered powdered effete types who ‘owned’ better than half a thousand slaves. I think we can find a better Thomas to quote on the state of things.

Wow just wow You shouldnt hate on TJ just because he was right and warned us

Congress has the fiscal tools to control the money supply. It’s a monopoly given in the Constitution to Congress. But one of the best tools for doing that is to raise taxes on the rich. Which won’t happen because the rich (by definition) own most of the assets and credits and Congress too. Like having a gun but no bullets. So after four decades of tax cuts and loophole dodges–all of which are inflationary–we have inflation just about everywhere. Covid just lit the fuse. Blame the Fed if you want, but the Fed is the central bank for the Treasury, doing what the Treasury approves. Said Treasury is controlled by Congress, supposedly. But Congress is AWOL. Biden is the first President since, Jesus I don’t know,–maybe FDR– to raise taxes on wealth and corporations.

Re” The largest holders of shares in Vanguard, State Street, and Blackrock are each other. ”

I don’t believe this is true, do you have any evidence or a reference?

Vanguard is owned by the investors in its funds. Vanguard owns a lot of everything because it’s too big. But I don’t think either State Street or Blackrock own a lot of Vanguard.

Interested in learning more but not sure where to start.

More and more my peers (men in their 40s) are quitting and going on the gov. dole. It appears to be very easy these days. There used to be some shame about getting government hand-outs, but that is not the case anymore.

Shame used to be an effective way of keeping society intact. But now we have a preponderance of political leaders who are sociopathic. If they amoral, it’ll be very hard to get the average bozo to be concerned about feeling a sense of shame. When leadership is openly and obviously lying, and not getting punished for the lies… good luck.

IIRC hn, it was Herb Caen who wrote in his column in the Chronicle, ”Politics is the last refuge of the scoundrel.”

Certainly seems true these days, when we have SO many outright thieves in office at all levels.

Maybe these upstart GOP ”rebels” have a good idea, eh?

Constitutional Convention anyone??? LOL

guaranteed ticket to sustained poverty …

anyone who wants to be working full time is able to do so.

Wait a minute, I thought it was “you know who” driving pink cadillacs on the dole what ruined everything.

And that idiot Jefferson made the Louisiana Purchase and is credited as the principle author of the Declaration of Independence of the United States. What an idiot.

@ Anonymous….”The largest holders of shares in Vanguard, State Street, and Blackrock are each other. Will they really let each other fail?”

B.S. They do not hold any stakes in each other. None. Zero. They are competitors. Their CLIENTS hold shares of those companies, largely via index funds. Take an even closer look and you’ll probably find that BLK is the biggest shareholder of lots of things, including BlackRock itself, for that exact reason. Sheesh.

The manipulating is to the entire Market , Not to the average Buyers > they the responsible party’s are the Buyers! And Bought Lot’s & Lots of Homes that are now rented out or sold at market top / An instant Replay will most likely happen after the Market Collapse another Pump and Dump IE Rate Drops > Buying > Ramp up in Prices again all over again Then same thing all over again > Better get used to it or ? What are you going to do anyway ? No I don’t have the Answer no control Here sorry

Perhaps someone here or silent reader has the Answer LOL but I won’t hold my breath

Prices fluctuated wildly up, it only stands to reason they will fluctuate somewhat erratically down. There were excesses, but they are thankfully being corrected. So prices are correcting. So here we are. Some wealth effect will go away, as it should, in this process, as it was largely fake to begin with (the real “transitory”). Most people who have been sane and careful, long term, have not yet found their world ending.

Yet in 2022, cash actually gained purchasing power if you’re in the market for certain assets like stocks and real estate. This site’s author once said “forget the Dow” as it is a narrow index and only a few stocks. Look at the S&P 500. Down 20% ish. Nasdaq even worse.

The strength of the DOW will fade once investors realize this isn’t going to be over quickly. It’s the safe haven index but it’s not immune to recession and higher rates. The beaten down value investors have been laughing so far but they’ll be crying eventually. Apple is cracking finally and that lack of confidence in safe havens will trickle through to others

My thoughts too. During the ’22 investors rotated into top 20 names, thus the slower Dow slide compared to the wider market and the tech. For the ’23 I predict that Dow will slide faster on a steeper slope.

You can’t compare the DJIA to the S&P500 and Nasdaq index. They are calculated differently. The Dow30 is price-weighted and the others are market-cap weighted. For example in the Dow30, AAPL is 10x larger than AMGN on market cap, but less than it on price so AMGN has a 2x higher weighting on Dow30. It’s dumb. The DJIA ended 2022 less than 10% down on price-weighting, but over 15% down on market-cap weighting.

@Z33

Off course I can compare them. You can too. Thats what you just did.

The Dow has always been part of the Mug’s Game Circus. As soon as a Dow-included Corporation gets a bit of tarnish on its once shiny image, they get booted out of the Dow and a new up and comer gets dragged in.

Great con to trick the Retailer sucker.

Is this why Exxon got booted?

In January of 2001 the 30 year fixed mortgage rate reached an all time low of 2.65%. The mortgage rate doubled in less than two years. What will the next two years bring?

Do you mean 2021?

DH must mean that R, cause the 1st mortgage we got that year was held by seller at 8% to make the deal work, and the 2nd we took a bit later to rehab and update the house was at 14%…

Love these updates, when we’re taken under the hood to watch the arcana of the system.

Seems the rate of change of the Fed balance sheet, and especially for Treasuries, is accelerating? Maybe someone geekier than i can check that out.

The dual mandate of the Fed is to also manage unemployment. As long as the labor market is holding steady, the Fed probably feels like everything is going just fine, thank you very much. Some of the analysts i follow and respect believe that the demographic situation of the United States is a buffer against big increases in the unemployment rate, unlike in previous eras. So is it possible that the Fed can be raising rates this time, and may not see huge jumps in UE? It’s hard to believe that Fed Funds can go to Volkeresque levels without blowing up the labor market, but maybe we’ll be finding out.

It will also be interesting to watch how the new Congress plays along, now that the House will be far less stimulative fiscally than the previous one.

Interesting times to be alive, for sure.

With the Monetary Politburo (the Fed) having created Excess Demand, while Government Edict(s) reduced Supply over the past 2 years, businesses have fooled themselves into thinking there is going to be an on-going Labor shortage forever.

Musk has already shown how much Dead-Weight payroll exists inside the Tech World.

How many extra heads exist draining cash, while bring in zero revenue at all companies?

The Fed has killed Price Discovery.

Kevin W. “less stimulative?” You haven’t been paying attention. Republicans cut spending that would go to the working people. Republicans cut taxes and regulations that benefit the 1% Oligarchy. That’s where all the effing inflation comes from–half a century of tax cuts for the wealthy, plus loopholes–all of which create inflation and the ‘boom and bust’ cycles.

Um, inflation has been created by the Fed pumping trillions into the economy, and secondarily by both parties giving away vast sums during the pandemic in individual payments, PPP loans, and rent, mortgage, and student loan forbearance. Letting people keep the money they earn has zero to do with this.

@Kevin W,

Demographic trends have been providing headwinds keeping the unemployment rate subdued for some time. This aging trend has been kicked into overdrive within the last three years when excess deaths jumped dramatically and long-term disability claims spiked. So the Fed can continue hiking at its current glacial pace yet the impact on the unemployment rate should be next to nil.

Likewise, raising rates at this pitifully slow pace has also proven ineffective at reducing inflation. Service inflation shows no signs of slowing.

IMO, accelerated QT might be the tool that works faster in reducing the inflation rate. Once these securities mature the principal is then extinguished and M2 money supply decreases. Selling MBS outright at a clip of $35 B per month, combined with approx. $15 B per month in principal pass-through payments ought to be considered by the FOMC.

“This aging trend has been kicked into overdrive within the last three years when excess deaths jumped dramatically and long-term disability claims spiked.”

——

I have been going crazy, wondering if I’m the only one who has noticed that?

To your next point though—won’t excess deaths be doing even more of the Fed’s job for them, deflating the economy and pushing down asset prices, even while the lucky few still healthy and on the job are making a little more money?

At least the CEO sold a good chunk of the stock close to the top.

Vanguard index funds was biggest bag holders it looks like. It’s why I don’t index anymore. Indexing gets abused by Fed induced speculation.

Indexing gets abused by Fed induced speculation. O Ya

As well as the whole worldwide Population lol

Here in the Philippines for some month’s now it seems many I talk to have no idea what’s happening or I should say about to happen over the next Year + > This Mindset seems to come from a Good place ironically ( my impression ) that being the Non Capitalist mindset living Day to Day mostly in as example in 3 to 5 Generational Homes to Squatters Camps and Tax Declaration Properties > Taken over from unknown Owners land build a house and pay Land tax on it then becomes a Tax Declaration Property ( that a Tax paid Receipt) something anyone can do Evan you and after many years you can get a Real title for the place in fact . ( Wow a free House )

This relaxed Filipino Mindset once the Inflation sets in place is going to create a sort of similar situation As China with the 2 Baby Law has with another mindset to take over Taiwan and the Philippines something they have been doing for years now Buying all the Shopping malls and putting up Hundreds of Skyscraper Condo Building in the Philippines totally Illegal like the China Warships in the Philippine Fishing waters pointing guns at fishermen You think the USA Has problems ? Look at China’s Over

population. But wait unlike China the Philippines has No Massive Army or Pot of Gold to go around Evading and taking over other Countries now

Do they . The Answer in not Eating Mostly Rice that’s what I Know

“There have been some mentions by various Fed governors about the possibility of selling MBS outright”

To quote from one of the greatest and most under-appreciated movies ever made:

“But Jay – even if we were to pull that off -and that is saying something”

(Janet in the Background is cluelessly shrugging her shoulders)

“The question is: who are we selling Them to ?”

“The same people we’ve been selling them to for the last 14 years – and whoever else will buy them”.

“But Jay – that was us. If you do this, it’s over”.

“I understand. This is it. Let’s get some more pieces of paper with pictures on it. Neil, you have till ten to draw me a plan and fire up the printers. It’s just money”.

These MBS are backed by the government and have similar risks as Treasury securities. If the price is right, and the yield high enough, there will be lots of buyers, just like there are for Treasury securities. That’s why the 10-year Treasury yield is STILL so low — too many buyers jostling for position to buy them.

These no-one-will-buy-them folks don’t understand the principle of yield: Yield solves all demand problems. It the yield is high enough, I will buy them.

There is one difference which most people don’t know.

As the mortgage gets paid off, the residual of the MBS goes down until at some point, you can’t sell it because there are no bids. It’s presumably not an issue for institutions because of the volume they own but is for individuals.

My mother whose account I started managing five years ago has about $5800 left across multiple securities.

I’d have to count the number but it’s about 20 or so. Only “stubs” left of the original issue with no bids.

Yes, but that is why agency MBS are callable (not sure when that started). So Fannie Mae, et al., when the MBS has been whittled down by years of pass-through principal payments, will call it and repackage the remaining mortgages into a new MBS.

This call feature is an additional way by which MBS inch off the Fed’s balance sheet after some years.

@Wolf – “if the yield is high enough”, which equates to if the price is low enough. I know its not quite that simple, but the Fed helped drive the price up on the buy side, and will likely depress the price on the sell side. The whole idea of buying was to suppress yields; if they start start adding to the sell side, the likely yields rise. These guys are not wizards.

“and will likely depress the price on the sell side”

They would have to actually sell first. And there is simply no sign of them doing that. Meeting after meeting goes by without even any discussion of it. And the last time Powell was asked about it by a reporter at a press conference, he dismissed the idea out of hand.

Wolf:

Could all this new Government Debt be bought up from that $2 Trillion in Private Savings we once had?

Oh No ! Private Savings were conjured up from Government Debt.

And last you published that Magical Savings was heading to zero.

I still see lots of ledger cash in the hands of a few, but the bottom 95% won’t be buying long term debt that the Government spends on Instant Gratification.

JMO

What you’re referring to is the difference in personal income per quarter and personal spending per quarter. This personal savings you are referring to is NOT an amount of money, but a flow of money that was earned in that quarter but was NOT spent. And it’s annualized. So in terms of what you’re trying to say – money available to buy Treasuries – it’s totally irrelevant.

You need to look at actual cash balances in various accounts, including bank deposits, money market funds, cash in brokerage accounts, etc. Alone bank deposits at commercial banks are nearly $18 trillion, waiting for a better place to go.

The question is not who will buy them now. The question may be who will buy a 2.5% MBS bond in the future? The Fed may see this and that is part of their consideration on selling these MBS’s at a smaller loss than if they waited 25-30 years for them to roll off.

Wolf has a good point that anything will sell at the right price.

Augustus has a good point that balances on all mortgages are declining over time.

Mortgages held by lenders/MBS holders are high maintenance. They have a higher cost than typical bonds.

1) Lenders pay loan servicers to collect mortgage payments. These servicers have rising services costs to hire people to handle the IT and to collect payments from mortgage holders.

2) The lender or servicer are also employing high cost lawyers to handle the unwashed mortgage holder masses who aren’t paying. You can’t easily kick a deadbeat mortgage payer out of their beloved home without legal effort.

3) The current cost of money means holding a 2.5% medium risk possibly long term bond is a losing proposition. As a mortgage holder, I’m putting my money into 4.7% guaranteed bills/CDs instead of paying off my sub-3% mortgage. The lenders are losing since the US had long-term fixed rate mortgages at sub-3% rates when I refi’d.

4) The MBS holder is likely holding a bond that is paying less than 2.5% since Fannie and Freddie have skimmed some expenses out of the mortgages with packaging them up into an MBS. This makes the MBS much less attractive.

Given the reckless mortgage rates of sub-3% during the pandemic, the first 10 year interest payments may still be high enough since the life of the loan has just started. However, since Wolf pointed out, these mortgage holders are reluctant to give up this rate unless it is out of their cold dead/divorced/unemployed fingers. (Hence the Fed is targeting rising unemployment as a good thing).

My observation is that maybe now is OK to buy an MBS. However, if cold fingers don’t appear, the last 10 years of a mortgage looks grim for loan holders and servicers.

For example, if during the last 10 years of an mortgage/MBS 25 years from now, there is a balance of 100K on the 2.5% loan. The total interest paid by the mortgage holder is about $2500/year or $200/month.

Servicers and lenders have to first pay their high overhead costs to their staff and lawyers. What is left of that $200/month? If you hold a 2.5% MBS too long, there is no price that will avoid a negative return. The MBS will become worse than worthless with MBS defaults.

Cynical me thinks this is why the Fed (and Fannie and Freddie) need some unemployment pain (or a good mass plague die-off of homeowners). They need to get people out of these loser low rate mortgages.

The other option is to increase refi’s by lowering rates again below 3%. Inflation may go to the moon if that happens but they won’t lose too much money.

A third option is to incentivize people to pay off their loser mortgages. The incentives could be financial (ie pay off now and we will forgive 10% of your mortgage balance. Take it now or else), or they could be government enforced (Those 3% mortgage holders are not paying their “fair” share and we must waive all legal mortgage contracts to raise their rates to 5% for the good of society. If this happens, I expect the US will join the rest of the world and abolish 15/30 year fixed rate loans. ) To be less alarmist, when my parents were making 12% in long term bank accounts in 1981, they never received a killer offer to pay off their 6% mortgage. My parents finally paid off their mortgage when saving rates dropped to below their mortgage rate 10 years later in the 1990’s.

The future could go any way.

There is yet one twist to the real estate mortage development. If many have to sell their real estate because of unemployment, there may be few buyers at anything but fire sale prices.

The mortgage holders then lose anyway as the value recovered in a sale do not cover the outstanding debt.

It is the old adage, if the debt is large enough it is a problem for the lender.

Sams,

Good point. millions walking away and foreclosing like in 2008 will hurt the taxpayer. Unlike 2008, the taxpayer owns most of the loans this time.

The taxpayers back most of the conventional loans and MBS’s held by Fannie and Freddie this time.

The Fed and other MBS holders will get their principal back. The taxpayer will pay them. Taxpayers will take out retribution on politicians.

Maybe this is an evil bank/Fed conspiracy.

The GSEs have been financing and backing 98% of all mortgage since 2009.

My guess is they will offer payment moratoriums to prevent and 2008 housing crash. Similar to the COVID moratorium and Student debt payment pause.

Any debt owed to the Government can sort of be paused with no ill effects….. so it appears.

As the Fed’s balance sheet “rolls off” some of those trillions in treasury bills it owns, you should look at how the reported “net interest” figure paid on the national debt, calculated by the Treasury and widely reported as our actual interest on the debt costs will also be affected.

In a few days, the Fed is going to release the annual profits it remits to the Treasury department for 2022. For 2021, it remitted $107 billion of its profits. Since 2009, it remitted $1.1 trillion. These remittances reduce the net interest expense of the US. And those remittances will go to zero, maybe already for 2022, and for sure in 2023. So that will be reflected in higher net interest expense at the Treasury Dept.

The roll-off itself has no impact on the Treasury’s interest expense.

Higher interest rates will gradually over the years phase into actual interest paid on the debt, as maturing old bonds are replace by new bonds with higher rates, and that will increase the interest expenses.

The biggest part of the increase in the interest expense comes from the 30% explosion since March 2020 of the debt.

“The roll-off itself has no impact on the Treasury’s interest expense.”

Yes, because the Treasury and FRB are considered to two distinct entities which they are in a sense and aren’t in another. (Yes, I understand the distinction between the district banks and the BOG.)

It still impacts the amount which must be financed by actual market participants, since government “trust funds” and the FRB aren’t one. Both are going to by UST, no matter what happens.

This is the real national debt, not the gross notional amount normally reported. The net amount is a lot lower, which means the actual fiscal position of the government is actually noticeably better than most believe it to be, even though it’s still easily the worst since at least WWII.

I always appreciate your explanations of the actions of the Fed. What I am referring to is in the Treasury’s closing statement for FY 22, gross interest costs were listed at $717 billion, and considering they are financing a debt of $30+ trillion like you said is not surprising. However what is widely cited in publications is the “net interest” figure which the CBO estimated would be about $400B, and was eventually reported at $475B. Apparently “net interest” is when you take the $30+T of debt and then you subtract the amounts “internally” borrowed, like from the Fed, SS, etc they are able to hide the true costs of our debt, unless I misunderstand how “net interest” is calculated. My point is that as the Fed’s balance sheet shrinks and more of our debt is financed by private/commercial/international buyers then the “net interest” amount will grow faster than our annual deficits. For instance a reduction of $1T from the Fed, assuming a going rate of 4.5%, that’s an extra $45B in “net interest” expenses. It will be interesting to see the next CBO projection of interest costs of the debt, ultimately I expect us to breach the $1 trillion in annual interest expenses quicker than most are expecting and maybe then public outrage will grow.

Yes, I didn’t quite get the drift from your first comment. This is correct, this “debt held internally,” when removed from the total “public debt” (the gross national debt = $30 billion), lowers the debt called “debt held by the public” (=$24 billion) and lowers the interest paid on this debt owed to the public.

This debt held internally is still owed, but it is owed to the beneficiaries of the pension funds, Social Security, etc. It’s real debt. The government does NOT “owe this to itself.”

The real losses of the fed, as opposed to nominal, come from the real value of dollar holders, aka the US public amongst others. Inflation is a tax after all.

Excellent great article.

What’s going to happen over the next ten years when the Japanese savers drop out (as many others will) and the cost of borrowing which must be set at the margin, goes up? Are we in for a decade of rising borrowing costs?

Also can I put in a reminder that as I pointed out a long while ago the end of this fiasco is a substantial dollar devaluation, same as Volcker.

Losses for the Fed seem like five billion a month. I wonder where the curve is on the Fed funds rate going out in years, being qt will take years?

On my assessment, the Fed is not poised to sell any of its MBS holdings.

Under the sub-heading of “Committee Policy Action” on Page 10 of the latest FOMC Minutes, the Federal Reserve reaffirmed its commitment to the “Plans for Reducing the Size of the Federal Reserve’s Balance Sheet,” published in May 2022. There is no mention of selling MBS in this document.

Moreover, the emphasis in this May 2022 document is placed firmly on “primarily adjusting the amounts reinvested of principal payments received from securities…..to the extent that they exceed monthly caps”.

In other words, there has never been a policy objective to meet the caps or to sell assets into the market. There is only a commitment to reinvest subject to whether those caps are exceeded.

The policy objective is to reduce the Federal Reserve’s securities holdings AND adjust the amounts reinvested. Maybe the Fed’s original intention was to maintain some, albeit a reduced, level of liquidity support to MBS, which would make sense when you look at the housing horror show. It is equally valid to speculate as to whether the Fed may revert to a $17.5 billion cap on MBS. This is not a prediction. It’s only mentioned to balance perspective.

Good point: “Maybe the Fed’s original intention was to maintain some, albeit a reduced, level of liquidity support to MBS, which would make sense when you look at the housing horror show.”

My thought was, MBS dumping into the market would lower liquidity for housing credit going forward, and perhaps drive prices (too) steeply down. The Fed would not suddenly forget its big constituency is people with some assets and wealth effect concerns, i.e., holding stocks and houses. All these strident supposed libertarians and rebels would start screaming the moment their precious (subsidized, protected) wealth effect started ebbing.

phleep

Yes, selling MBS to contribute to exceeding the cap would undermine the objective of reinvesting in MBS.

The caps appear to be a calibration tool – a mechanical instrument – to achieve the policy objectives of reducing the Fed’s holdings of Treasuries and MBS and adjusting the amounts reinvested of principal payments received from securities.

With regard to MBS, they are not set at the optimal level to achieve the Fed’s policy objectives.

You’d make a good economics professor.

hahaha, no. In grad school, economics (which I had to take way too much of) was the only topic that I didn’t like. Just not my cup of tea. And I don’t think I ever learned anything about the Fed in my economics classes. At least nothing sticks to my mind.

“And I don’t think I ever learned anything about the Fed in my economics classes. At least nothing sticks to my mind.”

Oh, I don’t know. They say you can learn a lot if you go to the lectures really stoned and just listen!

As an engineer, I took a basic Macro and Micro economics course as General Ed. My school considered Economics undergrad as a humanities course and not a science course.

I loved it since I thought it was interesting and easy. Nobody else in the class at the time had to take calculus so they didn’t know derivatives or slopes of lines so I thought the math was easy.

We didn’t learn anything about the Fed in our class. I rely on Wolf to teach me the practical real-world side of economics. Wolf’s charts are amazing for the math side of my brain. Thank you!

I thought engineering would pay better.

However, one of my classmates achieved a PhD in Math and went on to join a major bank making millions in High Frequency Trading of stocks.

I was right at the time but wrong with the future.

Walter Heller was my Econ 101 professor at the U of MN. He was a Keynesian with one heck of curriculum vitae. I was an 18 year old freshman with five years hustling sporting event tickets on the street as my guide to free-market supply and demand economics being the best system.

At the time, spring 1981, I did not really understand what this man had accomplished in his career, and I do now, but to this day, I do not think Keynesian policy is the way to go. We had some good debates, and he gave me time and respect — even though I argued against his teaching and philosophy of economics.

Fiscal and monetary policy working together in a coordinated way? Now with the Fed tightening monetary policy and the U.S. government fueling fiscal policy, Professor Heller is probably laughing at the current state of affairs.

I always look forward to Wolf’s articles but I would have to say that I enjoy reading the comments equally. I consider myself a financial hobbyist at best but all you people make me look smart when I talk to others…Thanks to all.

Wolf taught me about TBA activity by the Fed. Thank you. It looks like there is a TBS futures product now that appears new. Is this correct?

Look at those yields crash. The pivot is nigh!

I had a sarcasm tag in there but it disappeared when I posted

Let me also add that purposely or not, the Fed has done an incredible job of threading the needle for the past 6 months. Orderly declines without killing the economy. If they can keep it going we may have that soft landing afterall.

I believe this is something people will think has happened for roughly the first half of this year. The market will go up to SPX 4300 – 4500, rates will flatten out and real-world rates (mortgage, etc) may actually come down.

But some time later this year or early next year, it’s going to fall on its head and we will have a crash-like move that is going to make most people’s head spin (rates spiking, market crashing).

This is just the sentiment pattern playing itself out. I wish we weren’t so predictable.

Six months is an incredibly short amount of time. The Fed started hiking rates in mid-2004 and the crisis didn’t happen until over 4 years later. Way too soon to be patting anyone on the back.

Cumulative losses now exceed $20B just on the rollout which i think we all support.

There is little reason and absolutely no need to compound this by selling MBS at a loss.

Thanks for another great update on the QT Wolf. Well worth my annual subscription cost.

“Total assets on the Federal Reserve’s balance sheet dropped by $458 billion since the peak in April, to $8.51 trillion, the lowest since October 6, 2021, according to the weekly balance sheet released today”

Is it a coincidence that the inflation rate officially broke 6% in October 2021 before ramping up to 9.1% in June 2022 (which coincided with a near peak in the Fed balance sheet)? Now the inflation rate is expected to be in the 6% range with the same balance sheet of October 2021.

How much correlation does the Fed balance sheet have with inflation?

It looks very correlated from charts. Much better correlation than with interest rates.

Maybe I’m being optimistic for 2023 and steadily declining Fed balances?

MBS are going to devalue as the housing market falls victim to higher mortgage rates. Fed will be the loser of last resort.

It won’t be FED but tax payers collectively be the loser.

Fannie and Freddie have to convince people to give up their cheap 3% mortgages so the MBS’s will roll off early.

Death/divorce/unemployment/disaster would get people selling their houses and buying new houses with higher mortgage rates to keep the MBS’s rising. I don’t think it is a crisis yet. The taxpayer will continue to pay 4+% in Treasuries while collecting 3% in mortgages through Fannie and Freddie (minus fees) . It is likely current MBS’s will be worthless in 10-20 years if people don’t sell. People typically sell within 7-10 years without the drastic incentives above.

All MBS that the Fed holds are guaranteed by the government. The taxpayer is on the hook for the credit risk, not the Fed.

Total SOMA Holdings 7,998,667,021.5 January 4, 2023

7,998,667,021.5 still to go…lol

“7,998,667,021.5 still to go…lol”

You’re being silly. Do you think that even a tiny bank can have zero assets??? No assets, no bank. The Fed had asset from day one over 100 years ago. Sheesh. This might be helpful for your understanding. Give it a careful read:

https://wolfstreet.com/2022/09/05/by-how-much-can-the-fed-cut-its-assets-with-qt-feds-liabilities-set-a-floor/

It seems that much prognosticating on current financial risk is based off the treasury yield curve … however we know that the curve as presented is FALSE, not truly market based as the fed owns 8 trill in bonds.

Maybe Wolf could construct a true curve that would approximate yields if the fed owned NO bonds, an adjusted curve so to speak, or REAL curve

We know the overnight rate from money market funds is 4.5%, from here it must go up for longer maturities.

Ten year fair market at least 5%. Ill buy at 5.

30 year at least 7%….. probably higher. Fed owns mostly long bonds.

Buying any lower yield across the curve is a guaranteed future loss.

If don’t take anything else away from this article, reverberate truth lies within Wolf’s comments. “ QT is designed to run for years, it’s not a short-term thing. This is why the market downturn won’t be over any time soon. There will be bear-market rallies, but overall, while there is QT, markets are heading down.”

If the Fed creates its own money and can never run out of money, and can never go bankrupt, and losses are inconsequential because they are just an accounting issue, why does it need a Total Capital account of $41 billion that it could remit to the Treasury?

The Fed does not “need” this capital. The Fed has a “statutory capital,” set by Congress. Congress passed legislation that tells the Fed how much capital it can have, and the Fed has to remit the rest to the Treasury every year.

re “the possibility of selling MBS outright to get somewhere near the cap of $35 billion a month – which means that the Fed might have to sell between $10-$20 billion a month in MBS.”

My understanding is that no one will buy the Fed MBS ever since they started QT. So, why would anyone buy it now, ahead of SFH housing price collapses and possible deep recession to come?

BS. The MBS that the Fed holds are government guaranteed, and the credit risk is carried by the government. These “Agency MBS” constitute a HUGE market, with lots of institutional buyers, and that’s why the yields of these MBS are STILL SO LOW, which tells you that investors are jostling for position to buy them.

This nonsense about the Fed’s MBS is really getting old.