Wait a minute… It still “believes in” crypto? Is crypto now a religion that a bank “believes in?” FDIC, did you read this?

By Wolf Richter for WOLF STREET.

Silvergate Capital, which owns Silvergate Bank, is a tiny bank holding company that had gone public via IPO in November 2019, and got into crypto to become a big crypto bank, serving crypto companies, such as FTX, which started to implode as part of the crypto implosion. Today, it reported on a preliminary basis some details of its crypto-disaster in Q4, including huge losses on the sale of securities that it had to sell to deal with a massive run on the bank. It will report actual results later this month.

The FDIC, which insures dollar-deposit accounts at Silvergate Bank, is likely getting very antsy because today, Silvergate reported a laundry list of Q4 losses and write-downs that could wipe out most of its equity capital. Typically, when the FDIC takes over a bank, shareholders get bailed in first.

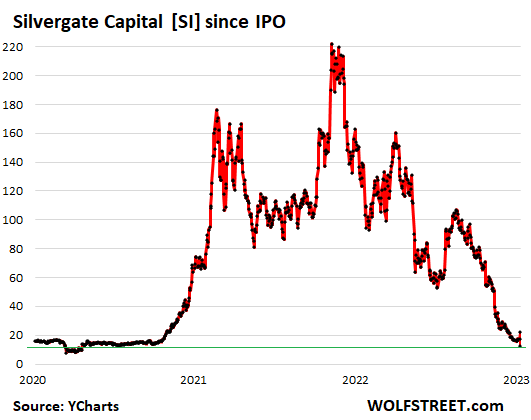

And the shares [SI], a hero in my pantheon of Imploded Stocks since last year, kathoomphed another 43% at the moment, and are down 95% from their high in November 2021 (price data via YCharts):

This was just a tiny bank: On its early published financial statements for the years 2017 through 2019, Silvergate’s total assets were in the $2 billion range. But then, as it got into crypto, they ballooned by a factor of 8, to $16 billion at the end of 2021, after which it began to fall apart.

Losses and write-downs to wipe out much of its equity capital.

Silvergate reported a loss of $718 million on the sale of securities in Q4, a huge loss for a tiny bank like this.

It said it will incur more losses on the sale of securities. And it may have to mark to market the securities it doesn’t sell, for a loss possibly as high as another $300 million. It will book an impairment charge in Q4 to reflect some or all of this.

It took a $196 million loss in Q4 to write off the crypto technology it had bought from Facebook back when Facebook skuttled its own efforts to build the Diem stablecoin.

And it disclosed other write-offs and charges today that we’ll get to in a moment.

So, let’s see… Silvergate started out Q4 with $1.33 billion in equity capital:

- Minus $718 million due to the loss on the sale of securities;

- Minus a portion or all of $300 million on the loss from securities that it will sell, or that it may have to mark to market;

- Minus $196 million on the write-off of the crypto technology it bought from Facebook;

- Minus the other losses and write-downs we’ll get to in a moment.

Combined, this could wipe out much of Silvergate’s $1.33 billion in equity capital.

The magnitude of the crypto-run it experienced:

Silvergate experienced a massive run on the bank as crypto companies, including its customer FTX, collapsed: Total deposits from “digital asset customers” plunged by 68% in the quarter, or by $8.1 billion, from $11.9 billion at the end of Q3 to $3.8 billion at the end of Q4.

This disclosure comes just two days after the three US bank regulators, the Fed, the FDIC, & the OCC, Warned Banks about Contagion from Cryptos, with Laundry List of Sordid Stuff Inherent in the Crypto Scene.

So it had to raise lots of cash fast.

At first through wholesale funding. “As customers began to withdraw deposits during the fourth quarter of 2022, Silvergate utilized wholesale funding to satisfy outflows,” it said today.

- It sold short-term CDs through brokerage firms to the public (“brokered CDs”). By December 31, it held $2.4 billion of these CDs. If buyers stay within FDIC rules, their CDs are FDIC insured.

- It borrowed $4.3 billion in short-term advances from Federal Home Loan Bank of San Francisco.

When that wasn’t enough, it sold securities, at a huge loss. “Subsequently,” when wholesale funding wasn’t enough, Silvergate sold $5.2 billion of debt securities, such as Treasury securities, “for cash proceeds.” And it booked a loss of $718 million on the sale of those securities “and related derivatives.”

It has to sell more securities to pay down the wholesale funding, for another big loss: Silvergate still holds $5.6 billion in Treasury securities and agency-backed securities, with unrealized losses of $300 million due to the yields that have risen. It expects to sell “a portion” of those securities in 2023, to pay down its $6.7 billion wholesale funding ($2.4 billion brokered CDs and $4.3 billion FHL Bank advances). And so it will recognize the anticipated losses as an “impairment charge” in Q4.

Since these securities are now held “for sale” instead of “hold till maturity,” it may have to mark to market even the securities that it doesn’t immediately sell, bringing the total write-down possibly to as much as $300 million.

Cash not enough to pay off short-term wholesale funding.

Silvergate said it held total cash and cash equivalents of $4.6 billion, which exceeds the $3.8 billion in “deposits from digital asset customers,” it said. Meaning, if the run continues, it could meet that cash outflow.

But it also has $6.7 billion in short-term funding (the brokered CDs of $2.4 billion and the FHL Bank advances of $4.3 billion) coming due, likely later this year.

That’s why it wants to keep selling securities to be able to pay off the short-term wholesale funding when it comes due.

Sheds 40% of remaining employees: Cost $8 million.

It said today that it will lay off another 40% of its remaining staff, another 200 employees, “in order to account for the economic realities facing the business and industry today.” The to-be-laid off people got their notice yesterday. It estimates that the costs of the severance packages and benefits will amount to $8 million, to be incurred mostly in Q1 2023.

Exited “warehouse” lending to non-bank mortgage lenders: Cost $4 million.

Silvergate said it got out of mortgage “warehouse” funding in Q4, at a cost of $4 million, which it will book as a restructuring charge in Q4.

Non-bank mortgage lenders temporarily fund the mortgages they write until they get enough mortgages together to package into mortgage-backed securities or sell them to Fannie Mae et al. This type of “warehouse” funding is provided by banks. But the mortgage business collapsed [see Mortgage Lender Woes]. So Silvergate got out of it.

But hey, it’ll stick to crypto until the bitter end?

Big mess, no problem: “Its mission has not changed,” it said: “Silvergate believes in the digital asset industry and remains focused on providing value-added services for its core institutional customers” – namely crypto companies that are now toppling.

Wait a minute… “believes in” crypto? Is crypto a religion that a bank “believes in?” FDIC, are you reading this?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Since the actual value of its “institutional customers” has always been zero, “value-added services” could mean dropping a penny in their begging bowls.

Drop a penny similar to going to the bathroom in UK.

1) Know that “bailed in” comes from “bailed out” – but we need a better term. Maybe “shot first” or “first off the gangplank”.

2) Not sure how the taxpayer backed FHLB and FDIC don’t come in for a ton of criticism too – how exactly does a bank focused on the burning sun of controversial assets, manage to get 4.3 billion in FHLB loans/”advances” or even “average” OCC/Fed/FDIC regulatory scrutiny?

(Plain vanilla banks go through regulatory colonoscopies every single single year – at least post Implosion 1.0 – and banks with wonky assets get much, much worse. Look at the tiny, tiny number of new banks that have been allowed by the G post Implosion 1.0…and yet this worthy is getting G loans? How does that work?)

3) re “Believe in crypto” – C’mon man you know what they mean, no matter how incompetent or corrupt they were in practice.

What they mean is, “Everybody knows DC won’t stop manipulating the economy until the USD is destroyed, so everybody is desperately searching for an alternative. If it is a religion, it is one born out off massive worry and very well founded fear.

Nobody (*nobody*) is orgiastic over AltAnything…they simply loathe what has been done to the dollar for decades and are looking for a Plan B escape pod.

That applies to precious metals, other currencies, SARS, diamonds, oil, prison cigarettes, etc.

There appears to be a whiff of political / regulatory favoritism in the air. The scent was all over FTX. Is Silvergate similarly blessed?

“For a successful technology, reality must take precedence over public relations, for the underlying math (nature) cannot be fooled.”

The CEO and execs probably sold at the top and the employees got whacked while the depositors are praying that they would get their money back. What a bunch of “Jenius”.

My guess is that a year from now, Bitcoin will still be standing, everyone else, history

Wild-ass guess here: besides crypto, they also believe in the tooth fairy & Santa Clause

Crypto Clause…

Let’s see, the assets and liabilities will get sorted out by 2028, FDIC will acknowledge the losses in 2034 and start payments in 2043. No problem.

Nah, the FDIC is quick on this stuff. I have been through 3 bank wind-downs by the FDIC, one of which was the second-largest at the time, M Bank of Texas. My money was at another bank the next business day. The FDIC then starts selling the assets. This is a small bank and most of its assets are securities. So the FDIC can sell them quickly. It then pays the proceeds to the creditors based on their place in the capital structure, including its own account for the deposits it paid off.

Stockholders lose 100%. Some creditors and some uninsured depositors might lose some. And that’s essentially it.

Looking at the numbers, the FDIC isn’t going to lose much if it steps in now. If it waits another year before it steps in and lets the losses drag out, it may lose more.

Wolf, does the FDIC have lots of discretion on when to step in, or are there rules that limit when it can step in to resolve a bank? In other words, why wait in a case like this? I’m guessing that getting FDIC insurance requires the bank to submit to FDIC resolution at the FDIC’s discretion but don’t really know.

Wolf is 100% correct. I have been a banker for 34 years and the FDIC usually comes in on a Friday evening(holiday weekends are very common) and will arrange a liquidation very quickly. MLK Day is coming up soon.

I’m a nobody. Wonder if the FDIC has to pay out if the bank operated in “Underland” and run by the Three Stooges.

I’m a scientist and one of my wisest mentors shared this advice with me when I used the word ‘believe’ in a meeting… “save your beliefs for Sunday. From Monday through Saturday, all I want to hear us what you think or know.” Best advice I ever received.

Classic !!

Good advice.

I’ve also been told “Hope is not a strategy”.

Run away if you hear “I hope the Fed pivots. I believe they will be forced to in 2023.”

HA, I worked at a company that was acquired and later spun out from AON, then was sold to a PE Firm. We got a new CEO and new mgmt team (definitely not a dream team). At one point, the new CEO who reminded me of Al Bundy from married with children, actually stated several times “Hope is a strategy” during a town hall. People actually applauded that! That was my sign to run not walk away. PS 3 years later still have a friend that works there and it is a hollow shell of a company barely surviving from old relationships.

Benjamin Franklin, always the diplomat, recommended the use of ‘I believe’ rather that offering an opinion as fact which invites conflict.

The use of ‘I believe’ has become quite notorious in the last generation; if giving testimony under oath that proves to be a falsehood all you have to say is ‘I believed it when I said it at the time’.

If I hear it from someone I always consider that they mean ‘I don’t really know’ because they haven’t done their homework.

“Is crypto now a religion?”

Yes. The answer is yes.

That was true from Day 1 for anyone who did diligence. A financial asset is a claim on something. Even a US dollar has some claim on future productivity of the US economy (subject to dilution). What is crypto a claim on? The hope, faith and belief of others (and various fruits of evasion of the financial system).

This go-round, as in various financial collapses past, all sorts of other quasi-legitimate-looking structures (such as banks or “exchanges” or mortgage derivatives) were piled atop such a shaky base. In recent years, the crypto community was breathlessly piling all this on when the base cracked, while singing the PR song at the top of its lungs.

Never invest in something the seller says you are too dumb to understand.

Every bank today operate on the same principle:

“borrowing short and lending long”

this “borrowing” is usually Your money, used by the bank without your knowledge and lended somewhere to make profit for the bank.

…or that the seller says they don’t understand.

“Never invest in something the seller says you are too dumb to understand.”

Is that you, Fed?

It’s me, Margaret.

I think Einstein once said that if you can’t explain something to your plumber, you don’t understand it yourself.

And that really is true, because the plumber will ask, “What do you mean by A,B, and C?” and “How about X, Y, and Z” – which “educated” people gloss over in their own minds.

And journal articles just enable this dysfunction, focusing almost exclusively on long, long, long mathematical derivations that few (including Ph.D’s) can follow every step of the way and…predicated upon multiple assumptions that are themselves unproven anyway – rendering the mathematical marathons fairly dubious/pointless.

I think anyone who has ever read an academic journal article has asked themselves, “Is this author trying to baffle us with bullshit?”

This is true of supposedly transparent code that is in fact opaque to the understanding of most users, and also, thus, has vulnerabilities apparent to hackers but not most users. Billions have been disappearing out of this leak every year, sometimes with the “help” of insiders, sometimes not.

Thanks Wolf.

I bought a silvergate 3 month cd in November so I just called to make sure I am FDIC insured. Never thought I would be exposed to the Crypto meltdown.

You probably got a good deal on the rate. If it is FDIC insured, and $250k or less, you’ll be fine.

When you buy a brokered CD, the “FDIC insured” is the first thing to look for — well before you hit the buy button.

That’s the problem. Reckless banks get funding at low rates.

Reminds me of First Plus Freedom (?) borrowing at roughly 5% when their stock was selling @ 25c around 1998. It was the one with Dan Marino pitching their mortgages.

I am looking at these FDIC stickers on lots of juicy bank offers in a slowing economy and thinking the FDIC’s buffer must be getting riskier. I guess it all depends on how much buffer they have, and how slow things get.

Burner cell phone…

Why not burner US Bank ?

BCCI comes to mind…

Nugant Bank comes to mind too…

During 2022 there was abso-f…- lutely no demand for BTC. All BTC ATM’s in Chicagoland are abandoned and/or vandalized. When you see yellow BTC sticker in the window of small business it means only that somebody paid them $5 to put it there AND NOTHING MORE.

1.China kicked BTC miners out

2.Generous big-hearted Texas decided to save them because it is Da Future…

3.BTC miners like Core Scientific, unable/unwilling to sell BTC had no choice but to accumulate it. Because selling means finding somebody willing to buy (ha-ha). Also selling BTC means price starts plummeting.

4.The only choice left was milking banks for more loans to pay ERCOT, using BTC as collateral.

More on this:

“Bitcoin mining in the crypto crash — the mining companies’ creative accounting” by Amy Castor, Aug 4, 2022

Yeah you are correct. (except #3 as I read today all major BTC miners have sold most all the BTC in order to pay bills)

It is crazy that this BTC price seems to have stabalized? WTF?

Has to drop soon.

-BTC price seems to have stabalized? WTF?-

It is not hard to stabilize when only whales trade piddling amounts between themselves. Last time I checked the average trade was $50.

Once in a blue moon this crap goes up 8-10% overnight, fails to gain traction then reverts back to normal or to whatever goes by the name of “normal” in this clown world.

I incorrectly named Nugan Hand bank. Green Beret John Hand won every medal there was in Vietnam then decided to become Australian Banker…

That’s my kind of Banker…

Those were the days…

All those pathetic Crapto shills would not make a pimple on John Hand’ steely butt.

An FDIC insured bank is up to its butt in crypto?

Are they part of its ‘assets’?

When I first read the headline, I thought the word ‘bank’ was a self- description of whatever this outfit was: as in food bank, blood bank, crypto bank.

I am pretty sure that no such creature exists in Canada. Self- described, sure, but not chartered or govt insured.

Crypto is like any other religion. After all, it is “safe and effective.”

Silvergate’s liabilities will drain all existing 1.3B in capital so they “issue” 2.4B in CDs and “borrow” 4.3B from FHL Bank ? I ain’t no See Pee Eh – but how do they intend to pay back the P&I on the CDs and the FHL Bank loan ? Are they actually telling everyone ahead of time to hope for the FDIC to pay them back…..whenever the FDIC gets around to it ?

it seems you’re confusing “equity capital” with “assets” and “cash.” And “liabilities” with “losses.”

equity capital = assets minus liabilities.

Silvergate sold $2.4 billion in CDs, so it increased its cash (asset) by $2.4 billion, and it increased its liabilities by $2.4 billion. No impact on “equity capital.”

But the losses and write-down drained the equity capital (by reducing the assets without reducing the liabilities).

I was thinking the same thing. Because you are “FDIC Insured” does that mean you can raise money, that you have no way of paying back?? (asking for a friend…)

When they raised cash by selling CDs and getting FHLB funding, to pay for the deposit outflow, they in effect paid off one liability (deposits) and took on another liability (CDs and FHLB advances). So that doesn’t change their overall liabilities. They just changed the type of liability. With no impact on capital.

When they sold securities, they changed one type of assets (securities) for another type (cash). Then they used that cash (asset) to pay off deposits (liability). This move, reduced their assets AND their liabilities by the same amount. With no impact on capital.

Neither one of them is a problem.

The problems are the losses — assets dropped, but liabilities stayed the same.

Their equity capital is designed to absorb losses. And their equity capital cushion did absorb the losses, but in doing so it got eaten up. So now there is very little equity capital left, if any, to absorb future losses.

In terms of liquid assets, they still have about $10 billion: $4.6 billion in cash and $5.6 billion in Treasury & agency securities. But they have lots of liabilities too. So they’re not out of good liquid assets. But they’re nearly out of equity capital – which is normally when the FDIC steps in and takes over.

Yes, FDIC insurance allowed them to raise $2.4 billion by selling FDIC insured CDs at a low interest rate. The risk for the bank is that the FDIC is now even more motivated to cut its losses by shutting the bank down. The bank is in survival mode. There is no profit motive here; it’s only survival motive. When the FDIC steps in, it’s game over. The executives get fired, stockholders lose 100%.

The bank needs to raise $1 billion in equity capital by selling more shares. But that is likely no longer possible, in this market, during the crypto collapse.

I think what we are objecting to is the fact that they may have been able to move their loss to the taxpayers. If the deposits weren’t fully FDIC insured and they were able to sell FDIC insured CDs to pay off the deposits, then they essentially paid the deposits off with money that will ultimately be paid by tax payers. It made sense for the bank to do this to kick the can down the road and keep paying their executives those fat bonuses. It made sense for the people buying the CDs as they probably got good rates and the money is FDIC insured. But how does it make sense to let a bank that has more liabilities than assets sell CDs to begin with?

“…that they may have been able to move their loss to the taxpayers.”

Yes, it smells bad. I agree. But the FDIC isn’t funded by the taxpayer unless it exhausts its own funds as it did during the Financial Crisis. It’s funded by fees that member banks are paying to the FDIC on their deposits to buy the deposit insurance. FDIC insurance is not free to banks. The FDIC has a system of assessment rates that depend on various factors, such as size, complexity, and risk of the bank. All banks pay into the system, and when there is a failure with a loss, it comes out of that fund – like normal insurance.

SWE,

Do you mean like when the TOO Big TO Fail banks got bailed out by the taxpayers? It wasn’t the FDIC but Unlimited, All you want printed cash for these guys… um, the same guys there now.

“FDIC, are you reading this?”

No, like regulators always do historically, they will be busy closing the barn door after the horses have bolted.

Where to begin?

For starters, a $16B asset bank with 500 employees. It’s certainly unusual and I’d expect it to be heavily reliant on wholesale funding.

Second, this is what happens when the wheels fall off, either due to excessive credit risk or asset-liability mismatches. In Silvergates’ case, I’d love to know their “L” (liquidity) CAMELS rating in 2022 Q3. Same thing for the risk management rating at the holding company.

So, what would be the normal number of employees for a $16B bank?

Silvergate would have been much better off buying the element they espouse upon in their name.

Waiting for the FDIC to show up, to ask the Federal Reserve Board why they’ve been granting banking licenses to casinos. Although I’m not able to review everything, it’s my general understanding that no casinos in Nevada are currently banks? I also don’t get the connection about the Silvergate Casino having a taxpayer backed line of credit with FHLB and of course the FTX links. Obviously everything is fine, nothing to see.

At December 31, 2022, the Company (Silvergate)held $4.3 billion of short-term Federal Home Loan Bank advances.

Just read Genesis is considering bankruptcy. A couple more nails in the crypto coffin… BTC still going nowhere though, maybe NFP breaks the dam tomorrow 🤷

Amazing to see a bank losing $1B (718M + 300M) on treasury securities because of a run on the bank and due to a mis-match of long-term investments and short-term liabilities. Could happen to any bank but most are more diversified in terms of liabilities and customers.

Crypto didn’t need religion when everything kept going up. Now the HODL’rs are huddled in their crypto churches waiting for the end of the world as we know it (BUT with the power grid in tact so they can get to their wallets and use the chain). Any mention that crypto can drop to zero (quoted in any hated fiat currency) and will never be useful for anything, brings them scurrying out with pitchforks and clubs to capture non believers and burn them at the stake. What they don’t realize is that they are living in the land of wolves and they are not wolves.

Crypto churches, serving tasty mugs of Kool aid.

Zealots are like moths driven to flames and it’s very likely, that after all these churches and casinos burn to the ground, there’s gonna be a long line of new customers waiting to put all their energy into rebuilding a happy community.

Apparently, some regulations will be spun out, after the nuclear meltdown, and the FTX drama will be a funny footnote and all the lobby groups will learn how to be even less transparent, as a new charlatan king claims the crown, while worshipping congregation members pontificate and crow about making a fast buck.

Lots of sad drama ahead, but hail to the king!

Caveating with 1) I’m not saying it’s not a crap bank/business, 2) that it won’t untimely be closed by FDIC, and 3) there are some incremental #’s from 4Q22 changes in the curve that would have flowed through into unrealized losses.

I just wanted to make you aware that your #’s and assessment of impacts to capital above from impairments and losses on securities above are not correct. TSE, TCE, and Regulatory Capital are not the same and you’re overstating the hits to Capital as well. For example, think about how TSE and TCE have seen sequential declines each quarter since 4Q2021 through 3Q22 while at the same time SI still experienced positive NI and NI to Common. That might help you with where your math and analysis went wrong.

In terms of your paragraph #1: OK

In terms of your paragraph #2: not so fast.

1. Note that I used “equity capital” throughout to distinguish it from regulatory capital, because regulatory capital is harder to ballpark without a balance sheet, and we don’t get the balance sheet for another 2 weeks.

2. Regulatory capital Tier 1 was $1.67 billion in Q3; ratio of 10.7%; minimum requirement is 4%. So now ballpark from here:

Sold $5.2 billion and lost $718 million on it: meaning that it carried most of those securities on its balance sheet as hold to maturity and that they were not marked to market. When it sold them, it had to take an actual loss. Because Treasury and agency securities are core holdings in regulatory capital, the loss went straight to regulatory capital.

It holds another $5.6 billion in Treasury & agency securities, part or all of which it’s going to have to sell… same thing, most are not marked to market, and now it has to sell them at a loss, and mark others to market. Those losses, when the securities are sold, are real and go straight to regulatory capital. That takes about a billion off its Tier 1 capital, leaving it with $600 million.

Granted, in terms of your point about the ratios, it also shed $8 billion in deposits, so that’s going to support the ratio from the other direction. But with its Tier 1 down to around $600 million, even after that drop in deposits, the ratio is going to take a big hit.

A lot of long verticle lines in that SI stock price chart. Large, quick moves in price, up an down.

All this carnage and loss of capital in the crypto space. And somehow a similar situation (collapsing housing market and home valuation) is unfolding with homebuilders, largely ignored by Wall St. LEN, TOL, DHI, TMHC, KBH, MTH all trading a nose-bleed levels. When will the horrible new home sales figures and 2023 housing forecast derail the stock price?

I’m just curious if Wolf shorted any of the tech high-flyers that are now down 95%? And who’s the next to fall…BBBY and then?

Remember the mantra that “Bagcoin [was] a hedge against inflation”.

At least a 5% guaranteed return on a one-year GIC in Canada is better than losing 80% from the peak in early 2022.

Wait a minute… It still “believes in” crypto? Is crypto now a religion that a bank “believes in?”

Why not? The Fed is a religion that the banks all believe in.

Casually equating everything based on trust to a religion erases all meaning. A failing crypto bank and the Fed are not equivalent institutions.

Oh to live on Sugar Mountain

With the barkers and the colored balloons

You can’t be twenty on Sugar Mountain

Though you’re thinking that you’re leaving there too soon

You’re leaving there too soon.

NY

An interesting dynamic in this, is the “talent pool” connected to the madness and the tsunami of unwanted, unnecessary crypto geniuses that are this generations carnival barkers, who will drift around looking for new circus tents. Maybe, a small fraction of them will find their calling in market regulation and forensic auditing, versus the greater likelihood they’ll supercharge their exploits as criminals?

There is already a revolving door starting between crypto law-enforcers and the industry (as with most other industries), but I think that is slowing for the time being. There was a famous IRS enforcement guy who jumped over to work for Binance compliance while crypto was still hot, and I’ll bet he is starting to regret it.

> the tsunami of unwanted, unnecessary crypto geniuses that are this generations carnival barkers

Good news, they can move over to this generation’s other form of financial “innovation” crack, online sports betting.

Sports betting

I strongly believe, after a recession and long period of economic decline, the next big thing will be crypto backed betting, especially in the metaverse. Crypto laundry tokens will fuel the global desire to make stupid bets, to get rich quick.

Will it make sense or be regulated, absolutely not. Web3 will fade away and out of those fragmented ashes will be born the equivalent of crystal meth metaFi — a quantum quicksilver connected to real-time AI.

My company used Silvergate for residential tract construction financing years ago. Before they went IPO they were a very reasonable business friendly bank. Things started to change and it became clear they were actively driving away existing customers to focus on crypto. In fact my company ended up hiring their construction loan officer to launch our own private construction lending platform. They looked like heroes while their stock price was skyrocket but oh how the mighty have fallen.

I recall in the 1980s S&L debacle, there was a southern California Savings & Loan known for its careful, old school lending disciplines. Some of its execs were tapped to be in the Reagan admin. But as the industry got deregulated and the hot-shots moved in, and pressures mounted to move into more risk, it joined the hot-shot risky lending crowd and was soon defunct. Its former flagship building overlooks the San Diego bay, as a reminder.

Those of us recalling it, also recall what all that cost the taxpayer: astronomical sums (as did the subprime debacle). That’s why having federal insurance on sketchy things like this is dangerous. Crypto infiltrating the financial system is still quite dangerous, IMO.

The existence of government deposit insurance is a form of moral hazard. It incentivizes people to ignore what banks do with their money.

Most people (including many here) seem to think that the existence of regulation magically solves the moral hazard problem. Your posts indicate you’re one of them. Look at the history of regulation versus prior scandals and (supposed) crises. Regulators are either “asleep at the wheel”, didn’t see it coming, or subject to political influence.

There are legal reforms which can substantially make the banking system a lot safer without exposing the taxpayer or the currency (to debasement), but no one with influence is for it and it has nothing to do with the current regulatory framework or any supposed “reform”.

For starters, properly defining a deposit. You and I don’t have funds on deposits with a bank, we’ve made a loan to a bank. There is zero reason for the government to guarantee any loan, other than political.

If the public could actually deposit their money instead of lending it to banks, then most of the risk would be eliminated.

“…government deposit insurance…”

To make sure we’re all clear here, I will just repeat what I said a little while ago: this is a bank-funded insurance program, run by a banking regulator.

The FDIC isn’t funded by the taxpayer unless it exhausts its own funds as it did during the Financial Crisis. It’s funded by fees that member banks are paying to the FDIC on their deposits to buy the deposit insurance. FDIC insurance is not free to banks. The FDIC has a system of assessment rates that depend on various factors, such as size, complexity, and risk of the bank. All banks pay into the system, and when there is a failure with a loss, it comes out of that fund – like normal insurance.

“…is a form of moral hazard.”

Does flood insurance create “moral hazard?” Does auto insurance create “moral hazard?” Does health insurance create “moral hazard?” In a way, yes. But it beats the alternative.

Cryptobanking meet 2008. Sigh. Again.

And we go boom with real estate again. Who holds all that paper on those dang Airbnbs? Really, the USG has insured it again.

Sigh.

Countrywide, IndyMac, they all were bigger than these minnows. It is the hedge fund crowd that really went big into FTX- so I guess there will be cheap bloomberg terminals again.

Sigh.

Leverage kills, baby. Juices returns on the way up, and kills equity on the way down.

Nothing new under the sun, but how many times over the last few years have we heard “This time is Different!!” You don’t understand the new way of it all, etc, etc, etc.

Why is everything from Wall Street and Now Silicon Valley larded with bezzles? Influencers, gurus, meh. Same old stuff. Might as well just buy BRK and go to sleep.

Someday this war’s gonna end…

“Might as well just buy BRK and go to sleep.”

Been a “lea$t common denominator” for a loooooong time.

Nothing la$t forever … $ad

Wolf,

You previously mentioned institutions that gave loans with crypto as collateral. Would that be a bank like Silvergate or did those loans originate from shadow banking? When will those losses be realized?

Like I’ve been saying the bottom is in. Buy buy buy. I’ve seen this since 2011 it’s always the same. Crypto is dead it’s over never coming back. Buy buy buy.

Sorry for your losses. My thoughts and prayers go out to you.

Bahaaaabaaahaa & Bahaaaabaaahaa …

Wolf; Forgive me for being naive,but where do the Cryptos come into play in all this? All this talk of assets matching liabilities. Are the Cryptos in either of these categories, or are they considered part of the bank’s capital? If so, how can their value be assessed in a meaningful way, seeing how volatile they can be? Marking to market would be darn near impossible on a meaningful basis. Anything that you can add for clarification would be appreciated.

“It took a $196 million loss in Q4 to write off the crypto technology it had bought from Facebook back when Facebook skuttled its own efforts to build the Diem stablecoin.”

———

Wow. When Meta is the smart money in a trade, things must have really gone off the rails.

You’re making a fundamental accounting error saying “minus $718 million due to the loss on the sale of securities”. Realized losses aren’t synonymous with the change in book value because losses on available for sale securities were already largely in book value as other comprehensive income. OCI was around 500m at the end of Q3 (note this is an after tax figure so not directly comparable to realized losses, though the deferred tax asset should be marked to zero). Asset management was actually pretty good and allowed them to fully meet the run on the bank while FHLB and brokered CDs gave them time to unload securities. Contrast this to the rest of the banking system that is insolvent and would need a FDIC bailout with this kind of bank run. The business is a mess as in AML/KYC but that’s an entirely different story.

You’re making a very basis error: Not reading its statement that it issued and which I linked. And so your assumptions are wrong.

Only some of those securities it sold were held for sale and marked to market, and they did NOT incur the loss.

But the held to maturity securities were not marked to market, and when it sold them, that caused the loss, and it’s an actual loss and it’s a loss to Tier 1 capital. Same with the remaining securities it will sell: it said specifically that a portion was classified as held to maturity, and not marked to market, and that now it has to sell them at an actual loss.

It said so in its disclosure.

This is what it said about the securities it sold and took the $718 million loss on:

“During the quarter, Silvergate sold available for sale securities, as well as certain securities that were previously identified as held to maturity.”

And this is what it said about the securities it will have to sell and take the $300 million loss on:

“At December 31, 2022, the Company held $5.6 billion of total debt securities at fair value, all of which are U.S. government or agency-backed and available for sale, and which include unrealized losses of approximately $0.3 billion. The Company anticipates selling a portion of these securities in early 2023 to reduce wholesale borrowings, which will result in the recognition of a fourth quarter impairment charge related to the unrealized loss on those securities expected to be sold.”

I did read what you wrote and the PR and understand this accounting clearly. I’m happy, maybe even eager, to make a wager about this! The call report will tell us soon enough.

>> Only some of those securities it sold were held for sale and marked to market, and they did NOT incur the loss.

This statement reflects your misunderstanding. The AFS securities sales run OCI through the income statement while equity doesn’t change. The PR wording is inexact but the 718m can only reasonably be interpreted as all realized losses. There was ~400m of mark-to-market loss in HTM that wasn’t in equity at the end of 3Q. It’s implausible this ballooned to 718m given HTM is primarily duration UST and munis and that market was up in 4Q.

Observer is correct. Part of the $700 million in realized losses, was already accounted for in equity as an unrealized loss of available-for-sale securities.

That may not contradict what Wolf actually wrote, because he doesn’t venture a guess at Silvergate’s December 2022 equity. He said it could “wipe out much” of the equity, and that is accurate, as far as the balance sheet accounting.

Anyway, what’s interesting to me, is real, tangible equity stayed about the same. The goodwill and the decrease in value of held-to-maturity bonds were already noted in the 3Q balance sheet.

Even more interesting, is these losses are primarily the result of borrowing from overnight depositors, and lending it long-term, a fundamental duration mismatch. If Silvergate had bought 0% t-bills a year ago, these losses would not have happened.

Perhaps this is because the CEO hired his son and two sons-in-law to manage the risk department.

This (terms of service) tidbit is something to keep in the back of your mind, if you’re shopping for cool places to store crypto laundry tokens, and unfortunately, I haven’t looked into Silvergate TOS or other similar entities.

Celsius’ terms of service for Earn accounts said that the company owned deposited cryptos — despite Mashinsky’s statements to customers that these were their own cryptos. The judge ruled that the terms of service took precedence. The assets are now part of the general bankruptcy estate

I think the crypto, silver gate, ftx area that’s likely to be unwinding is near the leverage relationships connected to collateral and the complicated (hidden) custody level 2 stuff. The unobservable off balance sheet stuff that tends to explode. The stuff, eventually discovered in real audits.

Here’s a hint:

“Silvergate is now expanding access to SEN Leverage by partnering with Anchorage, to offer its customers access to increased trading capital by providing leverage on assets held in custody. ”

It’s possible that this leverage, that’s most likely related to money laundering, isn’t a contagion issue, but as cash becomes more and more scarce, and as regulators start looking deeper, a lot of unconnected crypto puzzle pieces will become worthless.

Finally?

From David Gerard blog

“The bad thing Silvergate did seems to be that money FTX customers deposited for FTX went straight to Alameda — which was fine with everyone, until bankruptcy filings showed that these two entities are utterly separate. Silvergate should never have done this.

This is one of the stupendous range of things that is a Bank Secrecy Act violation, especially if you’re literally a chartered, FDIC-insured bank with an account at the Fed. This is the kind of thing that Silvergate could lose its charter over.”

Hmmm, looking back at Enron or any other fraudulent economic implosion, is there hidden contagion or risk, beyond the doors of small organizations like Silvergate? Is it time to relax and accept that the burial of crypto is now an opportunity? Is it worth waiting on the FTX outcome and all the details related to this mess, or is that priced in?

I think it’s a bit early to be walking over the burned down crypto casinos with metal detectors, looking for fragments of melted laundry tokens, but as Mr Twain said:

Buy land, they’re not making it anymore.

Addendum I think is somewhat interesting, especially with the Silvergate EJF Venture thing, run by an ex-SEC enforcement dept head, with trading in London, china, etc … Probably nothing and probably not related to fraudulent crypto or anything that might be whatever…

EJF Capital LLC has disclosed 116 total holdings in their latest SEC filings. Most recent portfolio value is calculated to be $ 645,739,000 USD. Actual Assets Under Management (AUM) is this value plus cash (which is not disclosed). EJF Capital LLC’s top holdings are PowerShares QQQ Trust (US:QQQ) , Silvergate Capital Corp (US:SI) , Jackson Financial Inc – Class A (US:JXN) , First Bancshares, Inc. (The) (US:FBMS) , and Plug Power Inc (US:PLUG) . EJF Capital LLC’s new positions include PowerShares QQQ Trust (US:QQQ) , Concord Acquisition Corp. (US:CND) , Marqeta, Inc. Class A (US:MQ) , Heritage Financial Corp (US:HFWA) , and LINKBANCORP INC (US:LNKB) . EJF Capital LLC’s top industries are “Hotels, Rooming Houses, Camps, And Other Lodging Places” (sic 70) , “Railroad Transportation” (sic 40) , and “Coal Mining” (sic 12) .

I focused on Robinhood shares being grabbed, but totally missed that Silvergate shared that fate too. Probably nothing, didn’t see the amount….

Shapiro also said prosecutors had seized U.S. bank accounts affiliated with FTX’s Bahamas-based business, known as FTX Digital Markets. Court records show the accounts at Silvergate Bank and Farmington State Bank, which does business as Moonstone Bank, held about $143 million

Clarification of a finer point:

The amounts paid out to insured Silvergate depsitors from the FDIC kitty is socialized amongst all FDIC insured premium paying banks. If and when the drain on the reserve is severe enough, FDIC insurance premiums could go up. Implications to follow from there.

wait

what “amounts paid out to insured Sivergate depositors from the FCIC.”

when did this happen?

the actual “fine print,” is this has not actually happened.

Although the concept of believe has been associated for centuries to religion, is actually a regular practice in economics, science and philosophy.

Meanwhile, in the depths of hell:

“They’re clearly not using this borrowed money for home loans, they’re using it to build up their capital levels,” said Todd Phillips, a policy advocate in Washington and a former attorney at the Federal Deposit Insurance Corp. “Why is the Federal Home Loan Bank lending them this money? It doesn’t make a lot of sense. And that’s why the FHFA is doing its review of the FHLBs right now.”

Wolf, did you see the piece at Naked Capitalism yesterday? They were claiming that Silvergate backboored a loan through the Federal Home Loan Bank since they used to write mortgages and retained that certification. Pretty nifty trick if it’s true

RockHard,

I covered this A WEEK AGO when Silvergate reported it, right here in this article above. You got tripped up by clickbait BS at Naked Capitalism that they posted a week behind?

You posted this comment here WITHOUT EVEN READING THE ARTICLE ON WHICH YOU POSTED THE COMMENT.

The FHL Banks do ONLY ONE THING: lend to smaller banks and credit unions. Silvergate got a loan from them, just like a gazillion credit unions. Silvergate doesn’t lend to homeowners, it lends to the US government since most of its assets are Treasury securities and government backed MBS rather than mortgages.

It took money (deposits) from crypto companies and lent this money to the government by buying Treasury securities and also government-backed MBS.

I never lent money to crypto companies.

When the crypto companies imploded, they yanked $8 billion in cash (their deposits) out of the Silverbank, which had to come up with this cash by selling these Treasury securities, and by borrowing from retail customers (selling CDs) and by borrowing from the FHL Banks.

READ THE ARTICLE ABOVE (published January 5), of if you don’t want to scroll up, you can click on this link:

https://wolfstreet.com/2023/01/05/crypto-bank-silvergate-details-its-own-implosion-much-of-its-equity-capital-wiped-out-im-waiting-for-the-fdic-to-show-up/

I actually did read the article, American Banker published theirs Jan 10 and Yves published hers Jan 11 so I thought this was new information, but yours mentioned the same 4.3 billion 5 days earlier.

I figured that since NC occasionally republishes your articles they might not be “clickbait BS”, duly noted.