Only a couple of smaller banks have significant exposure to cryptos, and their shares have collapsed.

By Wolf Richter for WOLF STREET.

Following a series of bankruptcies of crypto companies, and following the total collapse of some stablecoins, and following the general collapse of crypto prices, and following revelations of all kinds of imaginable and previously unimaginable shenanigans, scams, and frauds in the entire crypto and DeFi space, the US banking regulators today issued a warning to banks about the crypto and DeFi space, amid fears of contagion to the banking sector.

So far, crypto has been like a giant videogame where nothing is really illegal because it’s just a videogame, and where players are having lots of fun clicking on buttons and watching flashing screens while scamming and defrauding each other, a videogame where people in the end lose all their money if they don’t get out in time. And no big deal because it’s just a videogame, with no real consequences on the economy, other than a profuse waste of energy, because there is nothing crypto is actually needed for outside of the videogame.

But contagion spreading from the beloved and fun crypto videogame to the despicable fractional-reserve fiat banking system could be a real mess.

So the Federal Reserve, the FDIC, and the Office of the Comptroller of the Currency (OCC) – the three banking regulators in the US – issued a joint-warning today to banks, with a laundry list of “key risks” associated with cryptos – in effect, enumerating sordid stuff that is standard practice in the crypto videogame, and why banks need to protect themselves.

This is their laundry list of stuff that’s going on in the crypto videogame that banks “should be aware of,” quoted verbatim from their joint statement:

- Risk of fraud and scams among crypto-asset sector participants.

- Legal uncertainties related to custody practices, redemptions, and ownership rights, some of which are currently the subject of legal processes and proceedings.

- Inaccurate or misleading representations and disclosures by crypto-asset companies, including misrepresentations regarding federal deposit insurance, and other practices that may be unfair, deceptive, or abusive, contributing to significant harm to retail and institutional investors, customers, and counterparties [for example, now-bankrupt Voyager was advertising that customer deposits were covered by the FDIC!]

- Significant volatility in crypto-asset markets, the effects of which include potential impacts on deposit flows associated with crypto-asset companies.

- Susceptibility of stablecoins to run risk, creating potential deposit outflows for banking organizations that hold stablecoin reserves [remember stablecoin Terra Luna, which collapsed to nothing in no time when there was a run on the stablecoin].

- Contagion risk within the crypto-asset sector resulting from interconnections among certain crypto-asset participants, including through opaque lending, investing, funding, service, and operational arrangements. These interconnections may also present concentration risks for banking organizations with exposures to the crypto-asset sector.

- Risk management and governance practices in the crypto-asset sector exhibiting a lack of maturity and robustness.

- Heightened risks associated with open, public, and/or decentralized networks, or similar systems, including, but not limited to, the lack of governance mechanisms establishing oversight of the system; the absence of contracts or standards to clearly establish roles, responsibilities, and liabilities; and vulnerabilities related to cyber-attacks, outages, lost or trapped assets, and illicit finance.

And the joint statement added that “issuing or holding as principal crypto-assets that are issued, stored, or transferred on an open, public, and/or decentralized network, or similar system is highly likely to be inconsistent with safe and sound banking practices.”

And the statement said that the bank regulators “have significant safety and soundness concerns with business models that are concentrated in crypto-asset-related activities or have concentrated exposures to the crypto-asset sector.”

I get the message that it’s OK for the videogame players to lose all their money on this stuff; but that it’s not OK for banks to lose all their money on this stuff.

No major US bank has picked up life-threating exposure to crypto, but some small banks have in a videogame-like effort to become a big bank in no time, and their stocks soared while what I call consensual hallucination still reigned as the Fed’s money printing was turning investors’ brains to mush.

But since November 2021, the Fed has been talking about, and then started doing, some real tightening, and the party was over, and cryptos crashed, and everything around them crashed, and the banks that dealt with cryptos, their stocks crashed too. Here are the two main ones:

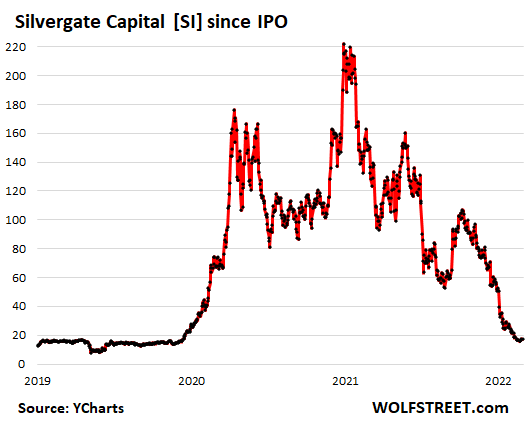

Silvergate Capital [SI], which had gone public via a classic IPO in November 2019, became a poster girl of the principle of consensual hallucination. It owns Silvergate Bank, “the leading provider of innovative financial infrastructure solutions and services to participants in the nascent and expanding digital currency industry,” it said at the time.

Its shares started spiking in October 2020, from around $15, and a year later, by November 2021, had multiplied by a factor of 15, to $220. Then they kathoomphed, became a hero in my pantheon of Imploded Stocks, and today closed at $17.27, down by 92.8% from their November 2021 high:

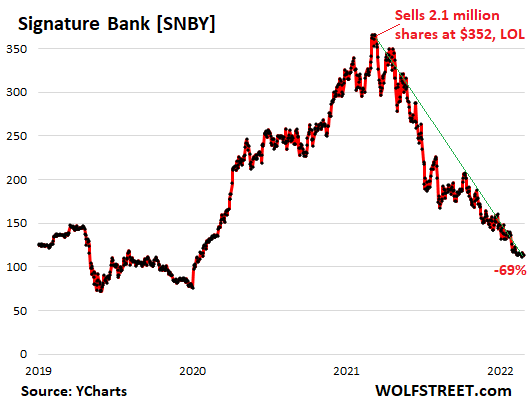

Signature Bank [SBNY] made a genius Wall Street move. It was just a small bank until it tied its fortunes to cryptos, and its shares spiked from around $120 a share at the end of 2019 to $374 on January 18, 2022. On the very day that its shares peaked, it sold an additional 2.1 million shares at $352 a share, extracting $739 million from folks that bought those shares in a final paroxysm of consensual hallucination. Those folks got instantly crushed, and at today’s closing price of $113.17 are down 68.9% in ten months. Crypto hype-and-hoopla just keeps on giving.

Since the intraday peak of January 18, shares are down 69.8%, and there’s a spot for them in my pantheon of Imploded Stocks (minimum requirement: -70% from peak):

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

What about entire countries in the video game…like El Salvador?

Yes, they’re paying the price for having played it. Practically no one in El Salvador is using it, and the price has plunged by 66% since they bought into it. That’s a lot of inflation in a short time.

The investors on the way up are often different from the ones on the way down, as any other classic pump and dump scheme.

Meanwhile a look at mainstream pump and dump on Apple and Tesla recently. The mainstream media has been calling China slowdown to claim wallstreet innocence. How about calling valuations for Tesla and the inevitable stock buyback end for Apple as it runs out of cash?

Oh no, those facts can indicate complicity of wallstreet. Bitcoin crashed 75% and SEC woke up. Will SEC wake up regarding Tesla, Meta, Beyond Meat……..

No.

I was just in el salvador on vacation. Few people use BTC but there were some and it appeared you could use it in many places.

El salvador was very nice, small country but nice places to see and seemed very safe. They rounded up most of the gang members.

As for BTC I am perplexed why it has not dropped like it should Staying very stable last 2-3 months. Oh well that is for sure transitory.

Big Kudos to Wolf for never selling out his readers by pumping scams like crypto for his own benefit unlike wall street or the majority of blogs!

+1

How would the Financial system have been different if we still had something like the Gold Standard. And Full Reserve Banking?

Lots of current problems come from Money Magic.

I think a super-inflexible currency has equal and opposite problems: deep deflationary crashes (accompanied by banking panics) as occurred 1819, 1837, 1873, 1897, 1907.

Also, many unmonitored banks in those days issued their own paper “currencies” that were in no sense “full reserve.” There was a polyglot of paper from faraway places (“wildcat banks”) with dubious “gold reserve” backing. So the actual use cases had major, catastrophic failures. not to see the idea couldn’t be revisited with modern tweaks in accountability.

The major inflexibility with a gold standard is that no interests can be added. If interest is added, inflation of paper money have to be compensated with an ever lower fraction of gold backing.

Actuallu leaving each bank to have their own paper “currencies” could work for society as a whole. Laws and regulations could then be made in such way that the demise of a bank and their money had little impact.

Little impact, systemically, but BIG impact on the local depositors.

You and Sams have it correct IMHO phl:

Remembering the early 1950s when I first started working for pay selling newspapers on a street corner for one nickel I would have 50 cents if I sold them all and was considered quite wealthy by my age peers.

Surely there was a TON LESS CREDIT those days, and every adult with any sense put at least some money in a jar or under their mattress because of the bank failures of their past.

Limiting money to hard coins of value, copper pennies and nickel nickels, then on to weight of silver and gold, with clear rules and regulations for banks would stop a lot of the insanity and put the thrifty and savers back in the drivers seat where we belong.

That, and, (going out on a limb here,) constitutionally mandated fiscal responsibility by the GUV MINT would be of great help to WE the PEEDONs, far damn shore.

I read these comments a lot on this blog.

Are you really ready for cuts in government spending though?

If the government balanced the budget this year, how deep and how long of a depression would the country enter?

How well would senior citizens tolerate cuts to SS and Medicare ( queue Lt Gov Dan Patrick quote)?

Bring. It. On. Real money keeps government honest.

You’re conflating multiple things that don’t have anything to do with the gold

standard.

Regulating banks has nothing to do with the gold standard. Banks can be regulated with or without a gold standard. Neither does privately issued currency (notes).

The only actual objection to the gold standard is that it won’t accommodate the pretense of something for nothing. That’s it and nothing else, to anyone who really understands the subject.

The complaint about the prior financial and economic instability, it’s based upon the belief that the current fiat currency regime is exempt from it forever due to supposed omnipotence of central governments and central banks.

It’s a complete lie of course but we’ll all get to experience the consequences of the prior recklessness in real time later.

Without fiat currency and fractional reserve lending, there can be no activist semi-permanent expansionary welfare and warfare state as there is no mechanism to pay for it.

It’s not possible to steal saver’s and property owner’s wealth, without directly taking it.

I think you’re reading your own ideological viewpoint into Phleep’s comment. Phleep never said anything to suggest that his reference to prior economic instability under the gold standard is “based upon the belief that the current fiat currency regime is exempt from it (instability) forever…” Nothing in Phleep’s comment implies the current fiat regime isn’t subject to instability or that central banks are omnipotent. Recent history shows the opposite to be the case.

I read Phleep’s comment as saying we’d be trading one set of problems under a fiat regime for another set of problems under a gold standard or some similarly inflexible currency regime. I think the saying “be careful what you wish for, you just might get it” applies here. There is no perfect answer because ultimately any monetary system ran by humans is bound to be flawed, manipulated, and corrupted.

I will add that without fiat currency and fractioanl reserve it wil be very difficult to be rentieer.

A monetary system with a finite amount of money do only work if there is no interests as interests add to the amount of money on the books.

Landowners can still live like rentieers by rent of the land, but in the end that is more work than just collecting interest on fiat currency.

Rentieer activity by landowners is also transparent and with democracy earninsgs may be regulated.

Sams, and AF, review some of the “rentier” issues in ancient Rome where they did have a gold standard. Their currency was in gold coins. They debased the coins over time with alloys. And, when people who bought farm land on credit (gold), if crops failed or something else caused them to fall behind in payments, farm families were known to sell their children into slavery.

These are historic problems and some b.s. belief in returning to a “gold standard” is just that, b.s.

If you’re really serious about it, just deal in gold for all of your purchases and exchanges. You can do it, but maybe not at your local grocery stores and not with average “city dwellers”. And you’d have a bit of trouble with most people who are selling things, even the country folk.

Our currency, as hated as it is by some of the stalwart, stopped clocks here on this site, our currency, in our country at the least, still works. That’s what a currency is supposed to do.

Reply to #HowNow;

What hardship debtors endure if not servicing their debt is no function or related to the monetary system.

That is regulated by how the law balances power between debtor and credior.

Sams, this is what you said: “I will add that without fiat currency and fractioanl reserve it wil be very difficult to be rentieer.”

Roman coins were “fiat” – they just had diminishing amounts of gold in them.

@HowNow

It is no longer working not since the 70’s when off the Gold Standard.

Inequality exploded since then.

Printing too many dollars, creating too much debt, killed the Gold Standard in the end. As we know there will be always reasons to skip spending discipline. Politics can end any system and if we had a Gold Standard today it could be killed in the same way. Because of the pandemic, elections, anything.

More likely, it was the printing of too many German marks during World War I that started the collapse of the Gold Standard. Germany was probably the only major belligerent that did not raise taxes to help pay for its war related expenses in WWI. Germany had already experienced considerable inflation relative to the US by June 1922, when the price of a Berlin newspaper announcing the assassination of Walter Rathenau cost 1 mark (almost 25 cents under the gold standard) vs the price of the NY Times at that time (5 cents). After the assassination of Foreign Minister Rathenau, the German inflation rate picked up speed as more investors moved out of the mark and into dollars.

Less than a century later, the US not only failed to raise taxes to help pay for its Middle East Wars, it actually cut them. The jury is still out as to how long the US$ remains the world’s major reserve currency. In November, 2023, it will be 100 years since the final collapse of the old German mark.

You forgot the creation of the Fed 1913.

US banks lent to Britain and France big loans that would default if they would loose the war.

A lot of that freshly created money never left the US but weapons did.

In the Versilles treaty Germany had to pay some eight times the pre WW1 annual GDP in hard currency.

Such an amount was impossible to pay, thus the default.

…Anon – quite right. OUR contemptible lie of ‘guns and butter’ from so many decades ago continues to ravage the nation in both human and economic aspects…

may we all find a better day.

Some rich person once said, ” Give all our money to the poor people and then give us five years. We will have it all back again.” The same goes for printing money. It doesn’t matter who you give it to, it will end up in the usual suspects’ hands. If the usual suspects actually control who the newly printed money goes to in the first place, it just saves them five years, and they get it given to them. They then make dashed sure that they then get an annual return as well. Plus they get the money that the poor people have to give them through their cash flow businesses. So they get richer and the poor get even poorer, relatively.

Where were they a year ago?

A warning would have been a lot more useful … once the collapse of a bubble is making headlines the risk is kinda obvious…

I was asking the same question, because there was a time when anyone who tried to buy crypto had their accounts closed with a letter stating a bunch of laws, in particular complying with the AML under “suspicious transactions”.

It was extremely difficult to buy these bag coins when they were cheap.

But recently, they want everyone to buy it at the top, and now because a few rich people likely got scammed in the FTX, they want to enact laws.

Pathetic.

No one was going to take action while the collective hysteria was going on and everything was going up. No one is going to take action until it affects them directly, either financially or with regards to their reputation.

A homeless person on a street, you ignore. A homeless person on *your* street, well, different story.

The powers that be are reactive to systemic and structural issues and address symptoms, not proactive and addressing root causes & engaging in preventative medicine. The status quo serves them until it doesn’t.

Yeah, hyper-generalizations up the wazoo, but give me evidence otherwise.

Correct. That’s why the Fed and other regulators don’t care about obvious bubbles forming (like housing bubble #1). They only care when they pop. Their “intervention” into markets is to set a floor, not a ceiling.

The thing is I wonder if the politicians and the billionaires were the whales and they were pumping the manure coins to get more suckers to buy into the scam?

In the early years of the last decade, anyone who tried to buy crypto had to risk getting flagged by FINTRAC, had their bank accounts closed, or banned from conducting such transactions.

A few months ago, the banks were like, this manurecoin is at its peak, and we want you to buy it.

But many years ago they treated you as if they found a letter of your plans to beat the Prime Minister in his office or something.

Manurecoin has been on a death march to try and legitimize its own existence, including celebrity endorsements & long-term strategies like getting the naming rights to the Staples Center (smh).

So yeah, it wouldn’t surprise me if the people who used to keep a tight lid on it either retired and were replaced with disciples or were paid off in some fashion, because we live a society where people will say *fucking anything* that money puts in their mouth. Professional script readers and hype men.

* It’s as much a technology as it is a societal-wide influence campaign to wrest people into their ecosystem that they control (thus building their power) and outside the current, *regulated* financial world order.

The lack of guardrails was obvious to anyone who bothered to do any diligence. I think greed and haste of the “victims” was a huge factor. If it had come up roses (and the punters had won their little part of these Ponzi games), the winners would have ghosted with their gains, no complaints. Now to blame government makes me laugh.

How about shoveling money to some unreachable offshore party with no credible financials? It’s as foolish as buying some pill off so;me person on the street. That’s government’s fault?

You mean the Nigerian Prince isn’t legit?????

“So far, crypto has been like a giant videogame where nothing is really illegal because it’s just a videogame, and where players are having lots of fun clicking on buttons and watching flashing screens while scamming and defrauding each other, a videogame where people in the end lose all their money if they don’t get out in time. And no big deal because it’s just a videogame, with no real consequences on the economy, other than a profuse waste of energy, because there is nothing crypto is actually needed for outside of the videogame.”

A common mentality amounst youth in many realms. I think school shooters have the same attitude.

The messaging coming out of the crypto space is addressing the insecurities and vulnerabilities of an abused, distraught generation of people who, IMO, question where this is all leading.

It’s a false hope, but no one else is offering any.

Amusingly, the messaging is coming from people who see the biggest problem with today’s financial system is that they aren’t the ones on top or in power. It’s not like they want a paradigm shift, that’s all just bullshit to get other people to elevate them. Blame 2008 and how everything got swept under the rug, just as those who are going to be destroyed by Crypto will be too.

Agreed. We’ve spent the last 60 years throwing the guardrails off society and now we’re shocked, just SHOCKED, that things are collapsing.

Young people are desperate and dejected at the neoliberal he’ll boomers condemned us to. Hopelessness pushed Young people to alternative assets because the ‘official’ ones simply do not work for them. The work/invest game is too rigged against us and we choose to not participate.

So wait, bitcoin actually does exist?

It’s a character in a videogame?

And as long as it stays in that videogame, it’s fine. The problems arise when real-life banks expose themselves to that videogame and take it on their balance sheet as if it were reality.

Treating casino chips like appreciating assets. I wonder if the people involved know about the psychology behind it and how it is being leveraged by Mobile Gaming & other outfits to convert real money into company scrips, or if they just stumbled into repeating history.

Kinda reminds me of Tron!

All I can think of is the monetization of the gaming world like candy crush where you paid real money for upgrades. My thought is what if we created a game called “tales of the crypto” and you traded crypto. And the more you made you could buy digital yachts and digital land in the game. Also for real money you buy upgrades that gave you access to congressional staff, senators, celebrities, the Fed, and presidents. But if you fail you end up broke, in prison for fraud, or dead because you ticked off the Clintons, I mean mob boss. Essentially a game within a game. You could even have little avatars and people could buy nft Nike shoes and the whole lot but without any of the consequences because it’s just a game.

I was 19 when that movie came out. A student working part time at a movie theater. 1981/82… those were the days!

:-)

Sir, it is not only banks participating in ‘videogames’ we must worry about. The crazy climate police may come after banks – see * . The ESG movement is scary in that legitimate investments in fossil fuels are deemed ‘bad’ and could be forced out of banks’ portfolios.

The climate police are real look at CA with the mandate for the ICE elimination for new vehicles. One of my many grievances with Blackrock

“So far, crypto has been like a giant videogame where nothing is really illegal because it’s just a videogame, and where players are having lots of fun clicking on buttons and watching flashing screens…”

Is the stock market any different? Is the US financial system any different in general?

Much of our shortages come from the fact that people just don’t want to work for a living anymore and produce actual physical products. They have been taught that speculation is the way to riches.

From LinkedIn:

The number of people trading stocks and dabbling in crypto soared during the heart of the pandemic, but last year’s unevenness and instability took the fun out of amateur trading for many. Following the S&P 500’s worst showing since 2008 and Bitcoin’s plummeting value, many hobbyists have called it quits, according to The Wall Street Journal. Further, many of those who spent their days trading in front of a computer after work opportunities dried up during the pandemic are also increasingly looking for new opportunities.

Nobody doesn’t want to work for a living anymore — that’s a wearisome generalization that keeps getting parroted by GOML types & it needs to be shut down. There is not some sudden wave of laziness or entitlement infecting the able-bodied population — it’s just disillusionment. The inducements to fritter away the youth dew toiling away for the ownership class have lost a lot of their luster.

Why might that be? Perhaps it’s a trauma response. After all, the entire planet is emerging from the quietly anarchic landscape of a major pandemic, where loads of loved ones died. For many, this had the effect of cantering their world on its axis; it forced them to reevaluate and overhaul everything from their personal relationships to their worldviews and their value systems. Couple this with the in-your-face smash-n-grab economy of the last 23 years and the unreality of things like flippers & “influencers” and very quickly one can appreciate the collective sense of inertia among the working class.

I’ve experienced the shitty service at restaurants, the understaffed garages & the long lines at places, too. Its inconvenient, but I see it as the byproduct of a global upset, which I welcome. What it morphs into from here is unknowable. A proliferation of coops? Nomadism/van life as a viable & even enviable ambition? Roycrofter or Manson Family type communes (with all the buckskin gear, cute chicks & dune buggies, but none of the homicide)? Wherever things land, it’s not going back the way it was; not ever. Whether you think that’s a good or a bad thing just depends on which side of the street you were born on/which side of the bed you wake up on. Personally, I feel hopeful.

Every entity I have ever seen wants something for nothing if it is feasible. All living things are energy-conserving, meaning, in some sense, lazy and free-riding, in some increment and based on circumstances. I am not going to declare some demographic or generation as saints or the opposite. Not do i engage a binary that things are “hopeful” or the opposite. There is a constant scatter across all these things. IMO the world does not dance to such simplistic models.

You’re being a little too cerebral about it. Sure, the larcenist premium of something for nothing is universally tempting, but scale is everything in such a discussion.

Something for nothing isn’t what’s driving labor shortages: you had a catastrophic once-in-a-lifetime event which knocked people — from their waking sleep. Many are in recovery or in discovery/ rediscovery mode; they’re reflecting & making assessments. Some are retooling or dropping out entirely. This is a phenomenon which is readily perceptible, yet the only thing you hear anyone moaning about are the byproducts of the thing; the long lines, the shortages & the rotten service.

The spoiled first world SoB in me bristles at the flat affect from the checker at the grocery store as I bag up my groceries; but the realist in me knows that she’s being treated & remunerated as the infinitely replaceable resource she is. The automated checkout lane just behind her probably isn’t a huge boon to morale either. Critical workers, indeed.

You call it simplistic — I call it obvious.

The political response to the pandemic was optional. It wasn’t a “black swan”. At minimum, there was certainly some middle ground between doing nothing and what was actually done.

Wealth disparity may be a part of the “doesn’t want to work for a living”, togheteter with seeing how people get rich.

It is not by working on the low levels of hiarcy. Trade, speculate and have others working for you and you get ritch.

Why slave for 20 dollar an hour when thosands can be made in minutes speculating on Wall Street?

The american dream have become the dream of beeing rentieer. And slowly the rentieers will kill of the economy like vampires slowly sucking the blod of their victims.

You should take this up with the Sumarians and Mesopotamians. I think they started this mess…

I hear there’s even an app underway for decrypting Linear Elamite

AGREE, like Totally bf on the optimism:

Almost all of the young folks I have worked with the last couple decades have been hard workers, willing and able to work as hard as I have done until retiring at age 75.

And I see it continuing in my ”working class” hood these days, and although to be clear the hard workers are more diverse than 50-60 years ago, most houses have no cars M-F except for us retirees.

OTOH, the few rentals in the hood have gone from around $6-700 for 2/1 to triple that in couple of years which is totally not fair to younger and family folks.

Well in 1957 when I was born we had 3B people on this planet… we’re now closing in on 8B… I’m not feeling to ‘hopeful’!

Then again, I don’t have much more time to live!

The age of global population increase is about to end. Possibly as soon as 2030.

If nanoseconds were seconds, there would be 32 years in one second.

It is just a matter of time, space and energy, and people will be living in spaceships for long periods to find a new earth like planet.

I don’t want to work for a living, if by that you mean making a physical product to sell. I’ve done that for 15 years already. I pay considerably more in taxes when I actually work versus capital gains, especially if trading something like SPX with 60/40 cap treatment.

We shouldn’t incentivize non-productive BS like the entire world of finance if we don’t want to lose bright minds and useful hands to it. Set cap gains back to 35-40% like it was in the 70s and see what happens.

“Much of our shortages come from the fact that people just don’t want to work for a living anymore and produce actual physical products”

You mutter this in the name of the lowest unemployment % in history?

I wonder where you get the facts to support your other opinions.

Look at the labor participation rate.

Too many seniors left the workforce during the pandemic(voluntarily and involuntarily).

Getting them back to work has proved difficult.

You want facts, here are some sobering facts for you:

1. 70% of the US economy is a consumer economy.

2. Over 80% of jobs are service jobs.

3. We have the largest trade deficit of any nation.

1. The US is the second-largest manufacturing country in the world, behind only China (which has about 4x the population), and quantum leaps ahead of Germany, South Korea, etc.

2. Manufacturing in the US is largely automated, so there are not that many jobs in these huge manufacturing plants.

3. The jobs in manufacturing today are skilled labor, not basic manual labor. Many jobs in manufacturing require engineering degrees, including in robotics, software, etc.

4. There is nothing wrong with a service job. My job is a service job. This website is a service. The fact that you can comment here depends on all kinds of services, all in technology, including internet services, telecommunication services, software in every server that your text gets routed through, software on my server, firewall services, off-site backup services, the services provided by the data center where my server is located, etc.

5. Engineering is a service, developing software is a service, architecture is a service, healthcare is a service, education is a service, trucking is service, housing is largely a service….

I’m surprised that the SEC hasn’t been going after crypto shills who were pumping up the dog coins and bag coins on the mainstream media.

Because if a medical doctor went on TV and said that drinking and driving is okay, they would be hauled into the regulatory body for discipline.

Funny how there wasn’t any enactment of AML, PATRIOT Act and other laws during the crypto bubble?

I remember a few years ago that crypto was for the nefarious and criminal. I also remember a bank closing my account for using my linked Paypal to buy bagcoins.

“Because if a medical doctor went on TV and said that drinking and driving is okay, they would be hauled into the regulatory body for discipline.”

States can go after them, and class action suits are already pending.

“On Wednesday an FTX investor sued Bankman-Fried as well as several celebrities who have endorsed the platform, including Tom Brady, Gisele Bundchen and Steph Curry. “The deceptive FTX platform maintained by the FTX entities was truly a house of cards,” the proposed class-action lawsuit states.”

I agree. I’d like fraud punished.

Do you happen to know of someone who lost an election in 2020, then collected contributions to “stop the steal”, knowingly misrepresenting the lost election?

The outcome of the lawsuit is more important. Wouldn’t be surprised if the funds that were allegedly embezzled from FTX victims were used to fund the legal defence.

The warning is late and unnecessary. Now that interest is back in style, banks won’t feel a need to pursue stupid get-rich-quick schemes, whether crypto or fiat.

Yes, these banks were based on that bubbly paradigm. But the crypto touts are still out there, cowed but unbowed, and waiting for another turn. Japan just issued more accommodating regulations for crypto. Plenty of global governmental figures are saying it is here to stay. Some march toward documenting this stuff, detailing the problems, reflecting on what it means for regulation going ahead, and readying for the next bubble, makes sense.

About 2 months ago, my daughter told me that she was introduced to a guy who makes a living with bitcoin. I told her to run away from him. Now I am not so dumb in the eyes of my child.

@Nancy,

“Now I am not so dumb in the eyes of my child.”

You’re not dumb in my eyes either.

Last week I was talking to one of my friends. While we were having some casual conversation he mentioned that he was closing his Robinhood account. I stopped and thought for a minute, then I asked him if he by any chance bought Bitcoin. He sheepishly said that he did. He said that his daughter’s ex-fiancee got him started with Bitcoin. I don’t know how much money he lost (I didn’t want to go there), but it’s probably quite a bit.

I knew crypto was about to tank when my coworkers started buying in 2021.

I knew the top was in when my friends in Cuba were starting to buy it as someone, somehow started advertising it there.

It truly was the top!

It was already near the peak when Saturday Night Live started doing sketches on NFT’S and Matt Damon and Steph Curry were extolling the virtues of investing in cryptocurrency. We didn’t quite get to the 30 minute infomercials promising to get rich quick in crypto or the hot #1 hip-hop tune with the rapper bragging about his shawty wanting to ride his loin because he was stacked with bitcoin, but it was definitely a massive bubble.

…for newcomers to Wolf’s most-excellent establishment who might presume he’s only hindsight reporting, he’s called the results of this particular episode of CH from its beginning…

may we all find a better day.

Nice! I bet a acquittance $100 in 2019, that an ounce of Gold would be worth more than a bitcoin in 10 years. Three years in, I am still happy with my bet.

I dropped a few Benjamins into Bitcoin 10 years ago. I’m still waaaay ahead of the game. Safely tucked into a cold wallet.

A lot of other folks out there like me. There is nothing that would make them cash out.

The stocks and derivatives markets are gambling casinos. Regulators are overwhelmed by corporate CPAs and lawyers. The little fish are chum. I’d say capitalism is a global Ponzi.

One must wonder what $100 will buy in 2029.

Interesting that they published this, “Joint Statement on Crypto-Asset Risks to Banking Organizations”, on the 3rd of January, which is bitcoin’s birthday. I wonder if they know.

Not sure what to make of their statement, “Based on the agencies’ current understanding and experience to date, the agencies believe that issuing or holding as principal crypto-assets that are issued, stored, or transferred on an open, public, and/or decentralized network, or similar system is highly likely to be inconsistent with safe and sound banking practices.” I mean, what’s the problem with having transactions on an open public ledger that anyone can view and verify? And that anyone can help update[1]. At least that’s how bitcoin works. As the mantra goes, “Don’t trust, verify”. Is it that these agencies prefer only they should be able to vet and verify the system?

Also somewhat interesting these veterans are, of late, so worried by a 14 year old. By the new kid on the block. But then these are odd times, we’ve all been through so much, it’s understandable they want back the status quo. Not everyone does though, even if it were possible, which it isn’t. The times are a’chanin’.

[1] So long as you follow the rules. And you cannot not follow the rules, in case you’re wondering.

They’re not worried about crypto, they’re going to let it implode just fine. But they don’t want banks to get hit with the debris.

They have been warning banks for years about it, it’s just that now, the warning has gotten very specific and public.

Is there are reliable way to know which banks (or companies – e.g. Tesla) might have a load of crypto on their books? Would it show in an annual report? That is, would assets, like cash, be separated from Crypto holdings? I doubt it… but don’t know.

The CFO of Tesla is Zachary Kirkhorn (37). His title is: Master of Coin and Chief Financial Officer.

While looking at Tesla, I didn’t find crypto specifically, just “Cash and Cash Equivalents” which is the usual item on a balance sheet.

Tesla discloses it. Go to the 10-Q filing

https://www.sec.gov/ix?doc=/Archives/edgar/data/1318605/000095017022019867/tsla-20220930.htm

and search the page (ctrl f) for: bitcoin and for: digital assets. You will see lots of numbers and discussion on it.

HowNow,

Block (SQ) is one other publicly traded entity that provides extensive disclosure of its bitcoin holdings in SEC filings.

However, Block does not classify its bitcoin holdings under Current Assets but rather lumps it in with Intangible Assets. Which demonstrates the confidence level in these “assets”.

The following is from page 34 of Block’s most recent 10-Q (filed 03 Nov 2022):

“The Company invested an aggregate $220.0 million in bitcoin in 2020 and 2021, with no additional investments made during the nine months ended September 30, 2022. Investment in bitcoin is accounted for as an indefinite-lived intangible asset, and does not include any bitcoin held for other parties…The Company recorded an impairment charge on its investment in bitcoin of $1.6 million and $37.6 million in the three and nine months ended September 30, 2022, respectively, due to the observed market price of bitcoin decreasing below the carrying value during the periods…the cumulative impairment charges to date were $108.7 million and the fair value of the investment in bitcoin was $156.0 million based on observable market prices…”

I will find out the underwriters for the Signature Bank IPO, and follow their careers closely. If Signature wasn’t a one-hit wonder, I’m going to do everything they do: Sell whatever they’re selling, buy whatever they’re buying.

Either they’re very talented, or very lucky. We need to find out which.

Report back!

I thought Signature Bank was mostly into credit cards for retailers, particularly those mall store retailers. Then again a lot of those stores went out of business, so they went into cryptocurrency to build back their balance sheets.

Doing nothing for 10 years and then letting everyone know there is trouble when it’s obvious is not being a regulator.

No one gives you the hard-truth like Wolf.

Minor typo:

“Controller of the Currency” should be “Comptroller.”

Should “Life-threating” should be “Life-threatening?”

This is one where I genuinely don’t know. A dictionary search shows some uses of “threating,” but I’ve never heard it. Thank you.

“because there is nothing crypto is actually needed for outside of the videogame”

…and criminal acts.

I love all the push back from an obviously new breed of commentors to the notion that the fiat system is something worth holding on to. All the back room double dealing, inflation that steals your $$ to finance wars that benefit the ,01%, if you ain’t a widget you ain’t with it mentality.. last year at this time I was about the only guy commenting about this paradigm shift.

No system is perfect.

The “fiat system” beats crypto, where inflation = 75% or more, and where scams, fraud, double-dealing, manipulation, theft, etc. are part of the rulebook. People are getting wiped out left and right. I have no idea why people are still defending this cesspool.

The “fiat system” works fine if you regulate it properly, if you punish perpetrators, if you let investors take the losses, and if the central bank stays away from interest rate repression and asset purchases. The problem is that not all of those four things are adhered to — and that’s when we get issues.

I like this when speaking about fiat.

The problem with fiat money is that it rewards the minority that cannot handle money, but fools the generation that has worked and saved money. — Adam Smith

We want a gold standard, not crapto

No, not all of us. I want a marktet regulated in such a way that there is competition between multiple providers of money of different kind. Crytpto is just another kind of fiat currency.

That is, a set of regulations where fiat currencies, gold backed fiat currencies and hard money like gold all can compete against each other for customers.

That implies no central bank and regulations that ensure that if a bank with their money or a currency system goes down it do not have serious negative impact on the economy.

“Multiple providers of money”? Think about that for a moment. Then tell: are you a scammer or a scammee? Will your face be on your personal currency? Will it be printed on waxed paper or toilet paper or just agreed upon as a general idea, with your approval, of course?

A quick Google search: there are 20,268 cryptocurrencies currently. Maybe more have been hatched since I posted.

Gold coins are more difficult to falsify.😉 When it comes to fiat currencies it would be all about reputation.

The big difference may be that different types of currencies would be used for different purposes.

To store value over time gold and other metals may be the prefered choice.

In payment transfer some kind of crypto would be more suitable. If say Visa did have its ovn currency for payment transfer people would probably use it, but they may not hold a large amount over a prolonged time. Others would compete in this market segment.

Jim Cramer was pushing Salesforce.com and other imploded stocks yesterday on CNBC. He said 2023 will be a good year for them. Next, he will be pushing Crypto. This guy is a f$ckin lunatic.

He is a very successful entertainer. The lunatics are the ones who follow his advice…

Cramer was saying buy signature bank as well and I know folks that pay to follow him. I don’t think he has any ill will towards people and his intent I think is honest but I can’t read minds. His job is to help sell add revenue and get listeners so he does his job well

The Chinese government saved the people of China by banning Bitcoin. It may well have reached one million dollars or more the value of Bitcoin had the Chinese been in the market. Anything that starts to skyrocket in price the Chinese piles into the trade.

Interesting point here ^^^^. Well done.

Ah, a million dollars isn’t what it used to be anyway.

I wonder if this also includes banks who have made loans and mortgages relating to crypto real estate. Many of the companies engaged in crypto constructed data centers (and often even bought dedicated power plants), necessitating outlays for the building, equipment, servers, etc. With the value of crypto plummeting, these data centers will likely follow suit, which means whoever loaned money, is also at risk of losses. I could imagine some smaller banks potentially making large loans relative to their size and being in trouble if when the crypto firms can’t make payments.

Great point. One thing I was floored about when I did some research is that the computers used for data mining are literally useless for anything else. I had assumed that they could be repurposed into supercomputers for other uses, but that’s apparently not the case.

So if the value of crypto goes to zero, and the companies that loaned against the equipment have to foreclose, the collateral won’t be worth anything except as scrap metal.

If the collateral is real estate, banks would get the real estate. This would be like any foreclosure proceeding. And the banks would likely lose some money when they sell the RE.

But the crypto-miner data centers were generally not funded with bank loans, but with money from investors. For example, in the bankruptcy filing of crypto miner Core Scientific, the big creditors were all investors. No banks were involved in the debt.

https://wolfstreet.com/2022/12/22/eleven-months-after-going-public-via-spac-texas-based-bitcoin-miner-core-scientific-files-for-bankruptcy/

Please please please let the Mafia be one of the investors. Then it will be interesting.

I would wager a large sum that the underworld lost a ton of money in FTX

Just another bubble like all bubbles, I liked it at 10k, narrative or sell side, was compelling. Found a kiosk did not feel right. Looked into RobinHood too, I took no action, I would have sold the rip way before 67k I know that.

It is never right or wrong just people talking their book, and finding out it was a bad trade.

As an observer of the passing Crypto show, one message keeps popping up from all who operate in this space. “Don’t invest anything you can’t afford to lose”.

All fun and games, like a video game, but there is the real up front fiat currency cost to get into the game in the first place.

Seems like many of the exchange T&Cs say coins deposited there become their property. Allowing them to leverage borrowing against YOUR coins. Borrowing continues as “your” coins get transferred down the line to affiliates of the exchange, plus each takes its “fees”. What is left of a coin invested in FTX after passing down 134 affiliates? Granted, a slight exaggeration, but not much.

I keep coming back to Wolf’s excellent description of “Consensual Hallucination” Syndrome. (CHS) I feel certain that psychological texts will have many chapters on this in the future and should give Wolf full credit for discovering this disease.

Do these banks follow the common advice not to invest anything they can’t afford to lose?

What happens to Crypto when the game gets unplugged? “Poof” ? Perhaps as Wolf more aptly puts it “kathoomphed”.

“Do these banks follow the common advice not to invest anything they can’t afford to lose?”

Better yet. Don’t invest in anything you don’t understand.

My Libertarian buddies were all over this crypto stuff when it first came out. It was supposed to be a “private money” and better than Gov Mint fiats. Blah-blah-blah. But I never understood their thinking.

“My libertarian buddies were all over this…”

Thank God for small favors.

Your only error is using the word “invest” instead of “gamble” when referring to crypto.

Wolf, I know you’ve mentioned in the past that the overall size of crypto isn’t large enough to cause real financial contagion.

My concern would be large, heavily leveraged hedge funds, where a relatively small loss on the crypto side (i.e. due to a scam etc) could cause the whole fund to topple, LTCM-style.

Could that in turn spill over into the broader banking sector?

Who knows what COULD happen… But crypto already shed the first 75%, and nothing bad happened. So if the remaining 25% goes to zero, it’s going to have a smaller overall impact than we have already seen. In other words, the bulk of the collapse is already behind us, and things are fine. The remaining portion just isn’t that big anymore. Plus, this is global. Only a portion is in the US.

Some crypto hedge funds and trading houses have already collapsed (Three Arrows, Alameda, etc.), and nothing bad happened outside of crypto.

Crypto was on my worry list when it was $3 trillion and with lots of companies getting involved, and with SPACs and IPOs, and banks ogling it, etc. Now that it’s down to $800 billion and some of the big players already in bankruptcy court, and nothing bad happened, I took it off my worry list.

Sure, the smaller banks tied to crypto, such as Silvergate and Signature, might collapse, and that’s not a biggie at all. That’s a routine procedure for the FDIC. It will come in on a Friday evening and take over the bank, stockholders will get bailed in instantly, some bond holders will get bailed in, depositors with fiat deposits will benefit from the FDIC insurance, and whatever other creditors will be dealt with as those banks are “resolved.”

Genesis and the Winkelvii are still highly likely to fall. I don’t think it’s over just yet. Hope you’re right.

$800 Billion???

DanRo – somewhere, ol’ Ev Dirksen’s ghost read your comment and is chuckling…

may we all find a better day.

Yes, thanks.

I remember opening up my Voyager app right before the bust last year and seeing FDIC all over everything and thinking this can’t be legal or a good sign.

I had already transferred and sold so didn’t hit me much but it’s really a shame that there wasn’t more oversight.

Goes to show that yet another law enforcement agency doesn’t really care about protecting and serving.

This is another example of the regulators closing the barn door after the proverbial horses have bolted. Yet so many people, including numerous commenters on this site, still have faith in the regulatory process.

Go look at the history of regulation. This is how it always works. A mania or bubble followed by widespread fraud that is supposedly “shocking” to the politicians and public. This is followed by regulatory “reform” to “prevent” the crisis or fiasco that just happened.

No amount of regulation can prevent manias or regulate moral hazard. It’s not possible to fix stupid either. In the case of crypto, the stupid is believing that nothing is something. It’s also stupid to pretend that nothing (crypto) is something and then regulate it, yet this is virtually guaranteed to happen.

There is no need to pass some statute or write endless pages of regulations for anything that is fraud or theft. That’s already covered by English Common Law, the foundation of the US legal system.

“Following a series of bankruptcies of crypto companies, and following the total collapse of some stablecoins, and following the general collapse of crypto prices, and following revelations of all kinds of imaginable and previously unimaginable shenanigans, scams, and frauds in the entire crypto and DeFi space, the US banking regulators today issued a warning to banks about the crypto and DeFi space, amid fears of contagion to the banking sector.”

Ugh! “Go look at the history of regulation. This is how it always works. A mania or bubble followed by widespread fraud that is supposedly “shocking” to the politicians and public.”

“Always” is a long time, and if regulation “always” works this way, we’d have no social order at all.

Some regulations are pure crap, some are full of holes, but many work, even if they aren’t optimal.

Get real.

Yep, another trade gone bad=Time/dust.

There was no reason to “regulate” crypto and any type of regulation of crypto would have been resisted vociferously buy the purveyors as well as the customers.

I have dollars in a bank that I am 99.9% confident I will be able to access when I want them. Thanks to regulation.

Not to be excessively contrary but there are a lot of crypto “investors” right now who retrospectively wish for regulation. But just like virtually ALL regulation is an attempt to prevent a calamitous situation from recurring, it has to occur first.

I’m looking for a blend of crypto leverage and real estate value collapse to take out one of the big houses before June. Batting averages being what they are the hot hand is only hot during bull market tops. The thing about genius gamblers is they confuse luck, skill and timing. Nothing like overlapping margin calls and coincidental client redemptions to create a short squeeze. Risk management strategies are in a Claymation death match this year with the margin/earnings.

Crypto videogame vs fractional reserve fiat currency

Hhhhmmm,,,

To what extent are we talking about the same thing?

I’ll just repeat it here.

No system is perfect.

The “fiat system” beats crypto, where inflation = 75% or more, and where scams, fraud, double-dealing, manipulation, theft, etc. are part of the rulebook. People are getting wiped out left and right. I have no idea why people are still defending this cesspool.

The “fiat system” works fine if you regulate it properly, if you punish perpetrators, if you let investors take the losses, and if the central bank stays away from interest rate repression and asset purchases. The problem is that not all of those four things are adhered to — and that’s when we get issues.

Wolf, “beats the alternative”….should we be supporting a FIAT System that has inherently and regularly created destructive Asset and Consumer Inflation and that is run by an academic unelected group whom have constantly proved to be incompetent but un-fireable ? The System has also clearly proved to create constant and very destructive ‘Boom and Bust’ that only benefits Speculators and not long-term investment. IMH(humble)O it needs to be improved or changed asap and not defended.

It’s a quantum leap better than the unspeakable cesspool of corruption and crime and fraud that is crypto. I have never ever lost a single cent in a bank. And inflation of the dollar is minuscule compared to the collapse of crypto. Note that crypto collapsed against your hated dollar.

This comparison is just silly. It’s a FALSE EQUIVALENCY. Go look it up.

I am not saying Crypto is the answer Wolf, though it has some very interesting and beneficial attributes but surely we should consider either going to a rule based Interest Rate System or a tangible Asset based System ? P.S. In relation to lost Bank money , a large group of ‘bail-in’ Bank Depositors in Cyprus would disagree

Then, what when the banks start to write the rules regulating them?

Still properly regulated, to the banks. They will then thrieve. Same will those regulators that symbiose with the banks.

Perpetrators are punished, that is those oposing the system. Investors take losses, that is those not within the system. And for now the central bank is out of rate repression and asset purchases. Bait, switch and the banks win again. All good. /s

“ The “fiat system” works fine if you regulate it properly…”

The fiat system is law of the jungle. Ruled by whales. The other 99% are bleeding slowly. It’s a totally rigged game and corporate whales pay off the regulators. It’s gotten much worse since we left the gold standard in 1971.

Perps are not punished. No jail time for perps, only a fine from the corporate petty cash. Shareholders take the hit.

As for central bank restraint, forget it. The meddling of politicians can’t or won’t be stopped.

Your description sounds like heaven, compared to the sordid gangster shitshow that is crypto.

I’d rather lose a little of my money slowly than all of my money fast, tbh.

As typical the US government has come to the rescue after the damsel has been take away by the dragon!

Hahaha, no they’re not coming to the rescue. They’re telling banks to shut their doors and don’t let in the dragon. They’re letting the dragon eat the damsel just fine.

LMAO! So true!

Even though I’m like a broken record (are those like vintage albums?) of beating a dead horse, I do want to express my fear, that very few crypto impairments have been recognized by wall street corporations or pension funds, or other creative entities like special purpose vehicles.

Granted, there is an increasing string of crypto related bankruptcies, there’s still the exciting business of sorting out losses in real Dollars and understanding how to follow that cash, which is connected to collateral structures that are currently unwinding.

I suspect there’s a massive amount of accounting fraud, primarily because very few, if anyone involved in crypto has more than a 4th grade concept of generally accepted accounting reality, including pension fund managers.

GAAP FASB rules probably won’t be involved in forensic audit analysis for most of this crypto contagion, but eventually, there will be teachers, firemen, state employees that will be curious about future losses in their retirement accounts.

Per FASB:

In practise, crypto assets are impaired to the lowest observable fair value within a reporting period.

The thesis that crypto is contained and not connected systemically to Dollars and the real global economy is a matter of concern.

I don’t have the data to support my thesis that there are thousands of pensions, banks and investment vehicles that aren’t reporting impaired crypto losses, but I have one example that is representative of why there’s good reason to suspect that crypto losses are currently not being recognized.

It is a disservice to not report on this risk! This is one pension fund in Wisconsin. Do you really think it’s the only fund connected to crypto regaled speculation?

SWIB held 358,400 shares of the ARK Next Generation Internet ETF valued at $17.6 million. The filing also indicated that SWIB continued to hold shares of both the ARK Innovation ETF and the ARK Genomic Revolution ETF. Together, the dollar value of the shares of the three ARK ETFs SWIB held as of June 30 totaled just under $109 million.

Containment at Fidelity? Seems like crypto laundry coins are very connected to lots of real money and collateral….

Fidelity, which was working on its bitcoin fund before the Labor Department published its memo, believes it structured its bitcoin fund in a way that addresses the agency’s criticisms.

For example, workers can’t choose to allocate more than 20% of their paycheck contributions or total 401(k) savings to the bitcoin fund. (Employers can opt for a lower cap.) Assets are valued daily, like a typical mutual fund. Fidelity provides education material for would-be investors. In addition, Fidelity keeps track of the private keys that have bedeviled other retail investors who’ve lost them, Gray said.

Based on several comments that you posted on this over the past few hours, you seem a little confused about some of the basics here.

1. Companies like Fidelity are earning fees, and their CUSTOMERS are taking the risk. NOT Fidelity. Fidelity has systems in place to where its customers’ big losses are very unlikely to translate into even small losses for itself. All Fidelity wants is earn fees. It doesn’t take risk on assets. Its customers do. There is no contagion to Fidelity.

2. If all of crypto goes to zero today, all global crypto holders will lose $800 billion GLOBALLY. Only part of those losses are in the US. Compared to $2.2 trillion in crypto losses already incurred through today, and compared to tens of trillions of non-crypto market losses, it’s just small fry. Get a grip on the magnitude of crypto. It just isn’t there!

3. Are people going to lose their money? Sure. They already lost $2.2 trillion on crypto from the peak, and they’re going to lose the remaining $800 billion, and then it’s over. Amazon’s stock alone lost over $1 trillion. And nothing bad happened. Get a grip on the magnitude of things.

4. Are companies and banks going to lose some money on cryptos? Sure, if they have exposure. Tesla lost a bunch of money on crypto. So what? MicroStrategy could collapse into bankruptcy under its leveraged crypto bets, shareholders will lose all their money, and bondholders will lose some of their money. So what? That’s has been happening ever since there were bonds and stocks. That’s how it goes. That’s NOT contagion. That’s a bad investment. Happens ALL THE TIME.

5. Big banks are set up to lose huge amounts of money, and a few million or even a billion in losses from some crypto thing they got tangentially exposed to isn’t going to faze them. But we have zero indications that big banks put any of their capital at risk with cryptos, and it’s likely that cryptos can go to zero with big banks not losing a dime.

6. You’re just having fun fantasizing about contagion, I think. Fantasizing and creating imaginary scenarios is a huge amount of fun. People do it all the time. Something like “contagion porn?” But Spreading those fantasies beyond the privacy of your own home is a different matter.

“The 9 stages of Big Con” (googling that will lead to the website where those steps are explained in detail):

1. Putting the mark up

2. Playing the con for him

3. Roping the mark

4. Telling him the tale

5. Giving him the convincer

6. Giving him the breakdown

7. Putting him on the send

8. Taking off the touch

9. Blowing him off

BTC Con augmented this classic SOP by adding extra step:

Even the scammiest scummiest shittiest Crapto Exchanges featured USDOJ logo and stern warning:

WE ARE IN STRICT COMPLIANCE WITH ALL FEDERAL AND STATE KYC LAWS

There is “The Beverly Hillbillies – S8E7 – The Clampetts in New York” episode on YT.

Fast talking Noo Yawker in fancy suit and two-toned shoes sells to Jed Clampett Brooklyn Bridge and many other things without asking him to produce 2 forms of government ID.

No matter what all of you say – things are advancing and evolving while basically remaining the same.

Also remember the legal maxim:

LAW ABHORS VOLUNTEERS.

Unless damage is done and cattle start mooing – doing nothing is the only option.

Three republican members of Congress presented a bill, named the Retirement Savings Modernization Act, designed to enable investment managers to offer bitcoin and cryptocurrencies in their 401(k) plans, per a Congressional filing.

Relax, there’s not contagion

I enjoy your sense of humor Wolf. It helps to make my day.

Yet, today, Bitcoin is UP 1% to $16,815/coin (at 2:30pm ET) – so the game rolls on, and the participants don’t seem to be overly concerned about government ‘warnings’….

“Yet today” Bitcoin is down how much from the top?

Bitcoin still has a lot of uses like money laundering, drugs, etc. Those industries still need Bitcoin.

” Those industries still need Bitcoin.”

No, they don’t. They need cash. Cash is anonymous. Bitcoin is not, as lots of folks have found out.

There are other cryptos besides BTC specifically built for anonymity. Cash can be difficult, bills can be marked.

Dear Wolf,

Thank you for your replies above. It’s a cruel lonely world and challenging to be the boy who cries Wolf, during choir practice.

I think you have summed up the crypto risk situation very well, however, as I return myself, to the gutter, in shame, I’m sure my brain will continue to think about contagion drama, that’s currently not on the stage.

Perhaps crypto has been entirely ring fenced, but as a card carrying skeptical boy, I can’t help but dream about derivative connections that have been engineered and written into our unfolding drama.

It’s stuff like the following, that’s entertaining and plants seeds of doubt, about how the crypto creature isn’t dead ….

A bankruptcy judge ruled that digital coins deposited in Celsius Network LLC’s interest-bearing accounts belong to the firm, ruling against thousands of customers and deciding a key legal issue in crypto-related insolvencies.

Peace, love, happiness and continued blessings

“…bankruptcy judge ruled that digital coins deposited in Celsius Network LLC’s interest-bearing accounts belong to the firm…”

Yes, this was based on the Terms and Conditions that everyone who used Celsius had signed. The judge just upheld the language. This was a dose of reality for account holders at Celsius who somehow thought that the Terms and Conditions didn’t apply to them.

Thanks for your posts. However you stated

“[Silvergates] shares started spiking in October 2020, from around $15, and a year later, by November 2021, had multiplied by a factor of 15, to $220. Then they kathoomphed, became a hero in my pantheon of Imploded Stocks, and today closed at $17.27, down by 92.8% from their November 2021 high:”

Not so much $17.27, more like $12.65….!

hahaha. yes that price was when the article was published two day ago (Jan 3).

Your price is today’s price. And this article is today’s article (Jan 5) about Silvergate:

https://wolfstreet.com/2023/01/05/crypto-bank-silvergate-details-its-own-implosion-much-of-its-equity-capital-wiped-out-im-waiting-for-the-fdic-to-show-up/

I’ll bet Wolf is getting plenty of liquidity (rain) about now! 🌧

It’s been a mess. But now the sun came out. Let’s see how long it will last.

I’m not crying wolf or screaming contagion, but found this interesting that in addition to crypto customer accounts losing their assets in many recent crypto bankruptcy proceedings, crypto customer funds can also be subsumed. I’m sure all of this money being vaporized is probably nothing?

The Silvergate Capital seizure was apparently part of a larger initiative by Federal authorities to subsume assets tied to the FTX collapse. Assets of Robinhood Markets (HOOD) were also targeted

Interesting that both Silvergate Bank and Signature Bank’s stock price is basically back to what it was in 2019 with the wild up / down ride from 2019 to 2023. They must have some viable non-crypto assets if their stock is still worth something. Imagine if you were a “set it and forget it” investor in 2018 / 2019, had these stocks and then looked at your account 3 years later. “…Crap – I bought Silvergate (SI) at $16 / share in 2019 and it’s only up to $17.27…All my friends made like 20% per year in that same time…why am I the idiot…?” That kind of blissful ignorance would be precious.

These imploded (from the peak) stocks are a sight to behold.