Short-term yields spiked from the pause-low in March of 4.0% to 5.3% today, mortgage rates with them: First results of the Bank of Canada’s unpause.

By Wolf Richter for WOLF STREET.

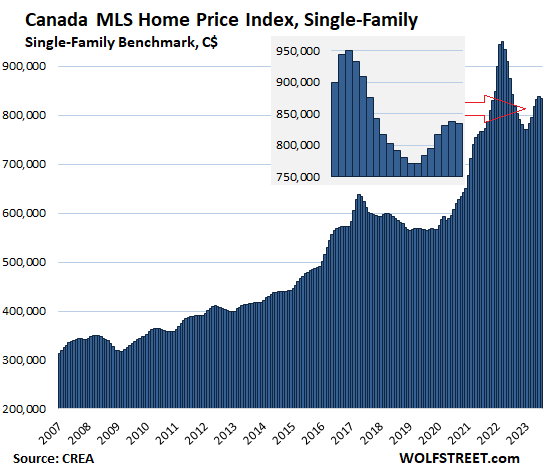

The spring selling season, or rather the Bank of Canada “Pause” season, which had been a rocking and rolling hoot, is over, and the first price declines are here. The Canada Home Price Benchmark Index for single family houses fell by 0.5% in July from June, and by 0.9% year-over-year, to $834,500 (all prices in Canadian dollars), the first decline since January, according to data from the Canadian Real Estate Association (CREA) today.

Note in the insert the rise in the prior month, June, of 0.8%: it had been the slowest rise in the entire upswing, with the others being two to three times as big, producing a classing rounding off pattern.

Since the peak in March 2022, the index has now dropped by 12.2%, or by $116,100. These kinds of free-money-spike-charts are just sort of funny.

Canada’s housing market reacts quickly to changes in shorter-term interest rates since mortgages are typically variable-rate or fixed-rate for short periods, such as five years. For a look at the complexities of the Canadian mortgage market, see our Introduction to Canadian Mortgages and Mortgage Insurance.

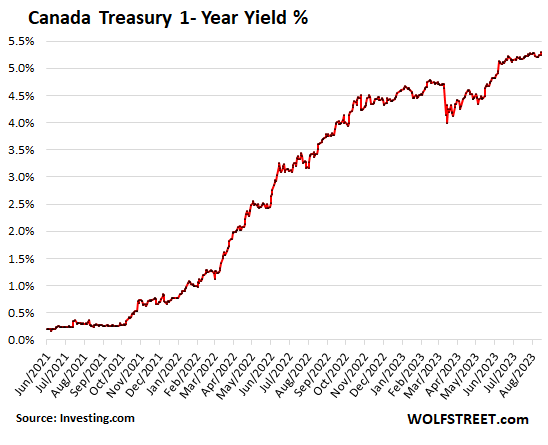

The Bank of Canada announced in January that it would “pause” its rate hikes at 4.5% going forward to see how much more it needed to do, which was then followed by a four-month-long pause, the result of which was the conviction in the markets that the next moves would be cuts, the result of which was a drop in short-term interest rates, with the 1-year treasury yield dropping from 4.75% in January to 4.0% in mid-March, the result of which was the rocking and rolling BoC pause season in the housing market.

The Bank of Canada also noted this rocking and rolling BoC Pause season and in June unpaused by hiking 25 basis points, and in July hiked again by 25 basis points to 5%.

And we’re now seeing the first signs in the housing market of this new interest rate environment of higher for longer. Today, the 1-year yield reached 5.3%:

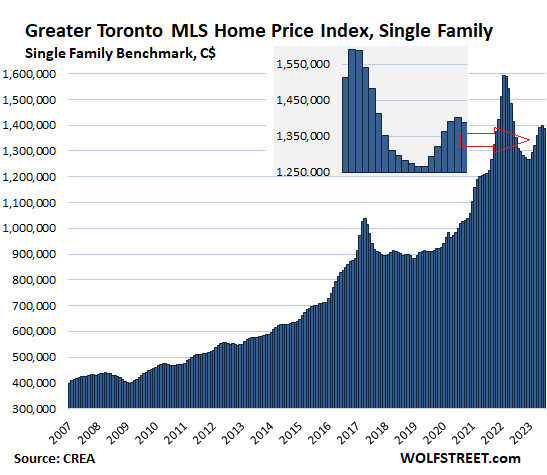

Greater Toronto Area: The MLS Home Price Index for single-family houses fell by 0.8% in July from June, the first decline since December, to $1.389 million.

- From peak in February 2022: -12.7% or -$202,100

- Year-over-year: -2.9%

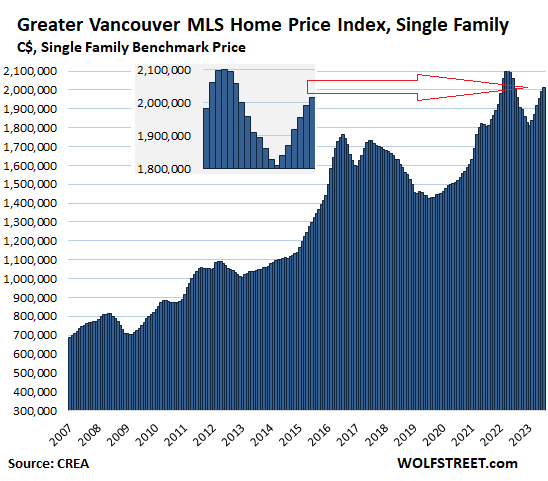

Greater Vancouver: The MLS Home Price Benchmark Price for single-family houses rose by 1.1% in July from June, to $2.015 million:

- From peak in April 2022: -4.1% or -$87,200

- Year-over-year: +0.7%

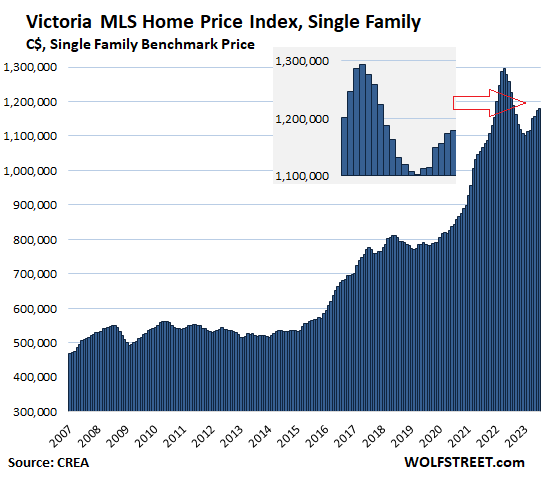

Victoria: The single-family benchmark price rose by 0.5% for the month, to $1.178 million:

- From peak in April 2022: -9.0% or -$116,000

- Year-over-year: -3.8%

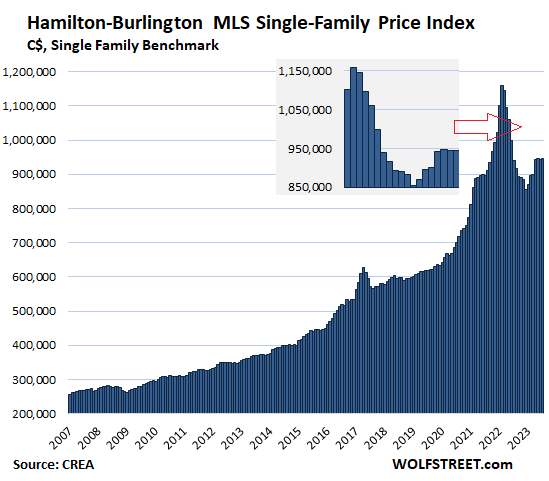

Hamilton-Burlington metro: The single-family benchmark price inched up 0.1% for the month, to $943,300. Note in the insert that the price has been essentially flat for the fourth month in a row:

- From peak in February 2022: -18.4% or -$213,600

- Year-over-year: +0.6%

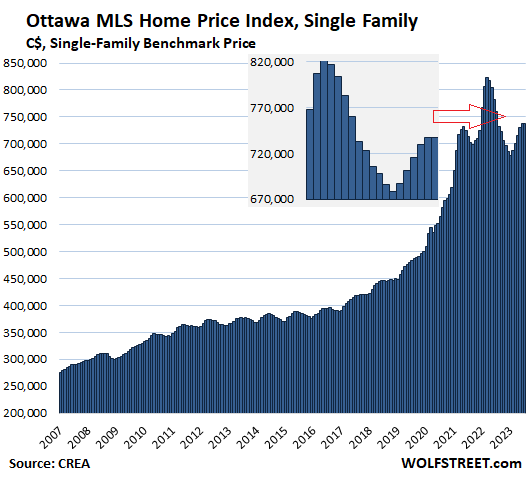

Ottawa: The benchmark price of single-family houses dipped by 0.1% for the month to $737,700:

- From peak in March 2022: -10.5% or -$86,200

- Year-over-year: -3.1%.

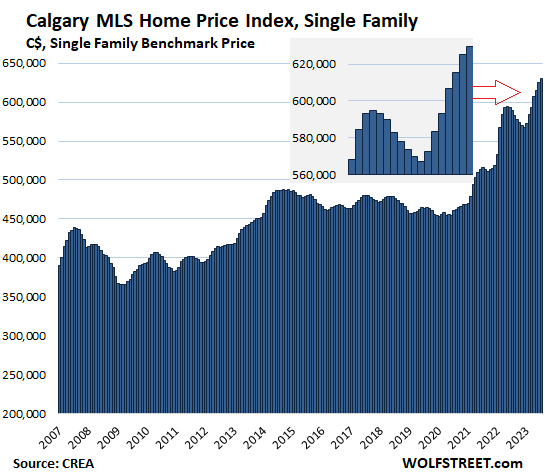

Calgary: The single-family benchmark price rose 0.8% for the month, and by 6.2% year-over-year, to a new record of $629,800:

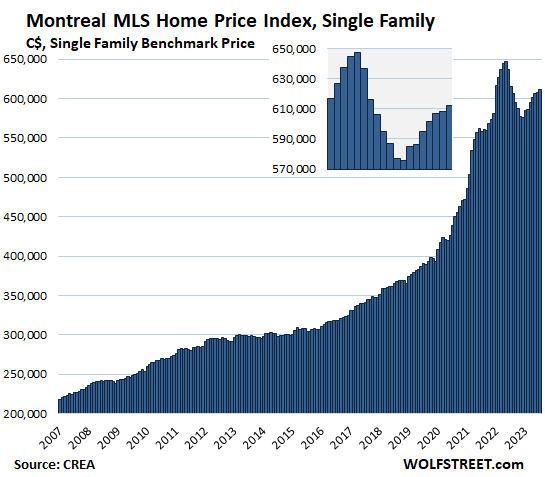

Montreal: The single-family benchmark price rose 0.6% for the month to $611,900:

- From peak in May 2022: -5.5% or -$35,700

- Year-over-year: -0.7%

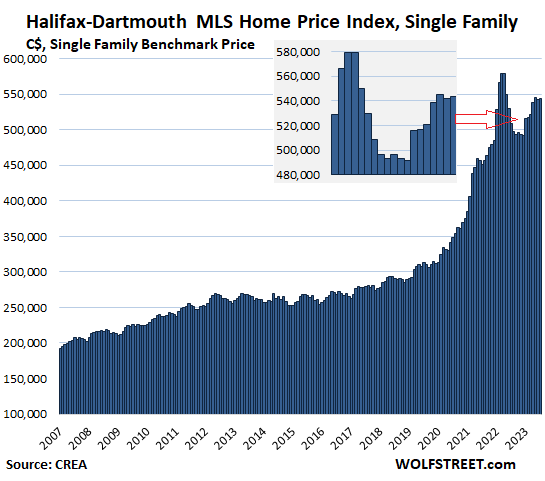

Halifax-Dartmouth: The single-family benchmark price inched up by 0.2%, after having dropped by 0.5% in the prior month, to $543,500:

- From peak in April 2022: -6.2% or -$36,200

- Year-over-year: +6.9%.

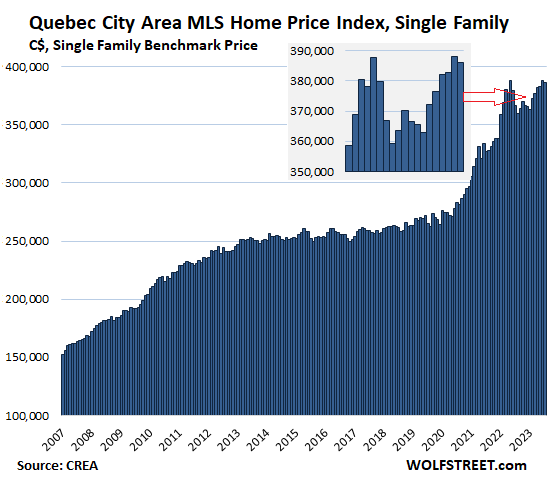

Quebec City Area: The single-family benchmark price dropped 0.5% from the record in June, to $386,200, and was up by 5.3% year-over-year:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

new bull market started.

🤣❤

DM: Michael Burry’s BIG SHORT – Famed investor takes out $1.6 billion position against the S&P 500 and the Nasdaq as he bets on US market crash

Burry held bearish positions against the S&P 500 and Nasdaq 100 Index worth a combined $1.6 billion at the end of the second quarter, according to securities fillings released Monday

Looks like Canada pulled forward an entire generation’s worth of demand. They’ve spent the future. Now what?

Import massive amounts of immigrants and keep the money printers humming?

Regarding immigrants in Canada –

About 12 years ago took family vacation to Toronto including Canada’s Wonderland amusement park in Vaughn. Stayed at Hilton Garden Inn near hwys 400 and 407. Walked across side road and took the family to what I thought was a convenient and fancy restaurant. Turned out to be a nightclub with smoking Eastern European ladies.

Weird comment, Canada is quite socially liberal. We aren’t Utah. But yes, Toronto probably has the most diverse population of any major city in North America.

Smoking Cuban cigars? The nerve of those Eastern European ladies!

Or perhaps they smoking illicit weed because the Canadian weed grown in legal warehouses on the frozen tundra can’t compete.

Or you just mean they were smoking hot?

Truly nosebleed prices.

What is the point of this policy anyway?

Most Canadians view real estate as their pot of gold, ticket to a good retirement.

Unlike the US, Canada does not tax capital gains on owner-occupied homes if the owner has lived in the home for at least 2or 3 years (I am not sure which) at the time of sale. I am facing a deferred capital gains tax of hundreds of thousands of dollars if I sell my owner occupied home in the San Francisco area.

“Unlike the US, Canada does not tax capital gains on owner-occupied homes if the owner has lived in the home for at least 2or 3 years (I am not sure which) at the time of sale. I am facing a deferred capital gains tax of hundreds of thousands of dollars if I sell my owner occupied home in the San Francisco area.”

It’s 1 year on your primary residence. It’s how I was able to scratch together enough for a place of my own, bought “fixer uppers” with a friend and we lived in them while doing the work and working our day jobs full time, the renos only made enough to pay off the RE thief.. I mean agent, but it was the only way, I couldn’t qualify for anything on my own or put that much money away while renting.

So what is going on in Alberta that Calgary is at an all time high? The Feds are in full-on greeny-induced attack on the energy industry which is the foundation of the Alberta economy. Or am I missing something?

Check the price of oil. It’s high. The industry is making lots of money.

People are moving from other high cost provinces to buy in slightly cheaper Calgary and Edmonton — compared to Vancouver….very tempting if you want a bigger house. Of course, cost of living in Alberta isn’t drastically cheaper, it’s quickly catching up. Oh yes… They also get 6 months of winter and -40C temperatures. Plus now that climate change is taking holds, major forest fires are also a concern. An area the size of London is burning in NWT/Northern Alberta right now.

yeah, climate change, that the “cause”.

even 3 months and no less than -29.99 might come sooner than later if various and sundry and IMHO obvious deltas continue, eh

Forests have been burning in Canada, and everywhere else, for thousands of years. Mother Nature used to put them out. Now Government does the job, a slight improvement, sometimes, over Mother Nature. Maui, a Canadian vacation land, ran out of water in their hydrants!

In Canada, the immigration targets are the only real growth industry. So Southern Ontario and Greater Vancouver (the Fraser River Valley) get squeezed hard – more people on the same small patch of land.

Very few people immigrating from Warm Climates want to settle where you get extreme cold for 4 to 6 months of the year. Every decent patch of dirt is built on, and now, high rises are the only option. Hence, Hong Couver. A fringe, dense population on about 2% of Canada’s land base.

Lots of buyers cashing in at the highs of Toronto and surrounding areas and moving to Calgary and Canmore. Better quality of life with zero provincial sales tax, close proximity to the mountains and a welcoming spirit that Alberta is known for.

Calgary home prices are not high in comparison to Vancouver, Toronto or Hamilton (which is about 40 miles from Toronto).

That “attack” is more noise than action at this point still, oil industry is making a lot of money it’s not like policy announcements translate to crippling the industry the very next day. The fed targets are for 2035 and we don’t even know if that’ll happen or if there will be any concessions for the prairies in the end. Another thing to look at is average RE prices, from the lows after the crash in ’08 Calgary nearly doubled in RE, but Toronto basically quadrupled from those lows to highest peak. Wages in AB are definately not 3x lower than comparable jobs in ON and in fact if you’re oil and gas you’ll be making significantly more than just about any “blue collar” I know of in Ontario.

If the next question is then why Cowtown prices are nowhere near TO prices you’ll usually get an answer claiming immigration, but take a close look at pop growth over last 10 years and beyond, relative growth in % is about double in Calgary every single year what it has been in TO. Total newcomers might be a greater number but that’s also a larger labour force so to me it comes down to other factors. Previously “wealthy foreign investors” were the scapegoat, now it’s zoning and immigrants, not enough housing starts, but housing starts have historically always been lower than most developed countries as per the same analysts who point to those as the problem, doesn’t seem to explain the current “affordability crisis” in relation to previous periods then. IMO Toronto and Vancouver just see a lot more speculative activity in RE, we’ve had super low interest rates in last 10 years and that dynamic is reflecting in the prices, that’s how I’m interpreting the data anyway. Now the higher interest is going to be a harder kick in the nuts for the speculators, especially those leveraged up to their eye balls so I’d expect TO and Van prices to slide more than Calgary next few years. If we see a big recession then it’ll probably hit Calgary too because oil will go down with rest of economy.

Resale Condo townhouses in Edmonton today are still selling at half what they sold for way back in the spring of 2007. Resale apartments today are selling for less than half what they sold for back in 2007. In 2021 almost 100 resale apartments sold for less than $40,000 in Edmonton. None of them were leasehold. The difference between new and resale is night and day different in all of Alberta. Anyone who bought new in the past 16 years lost the maximum amount of money. Top date all the people who live in Alberta still haven’t figured it out but the people moving there from other provinces know it right off the bat. It’s been that way in Alberta since the 1970’s but no where else in Canada.

…what happened to the good ol’ days of anglophone/francophone blaming of each other???

may we all find a better day.

Funny “haha” or funny “strange?”

Maybe a little of both…

“These kinds of free-money-spike-charts are just sort of funny.”

Thanks for reporting on Canadian data, nice that it’s noticed south of the border.

Both renting and buying in Toronto are difficult these days.

Our anecdote — We were “reno-victed” from our lovely rental in downtown Toronto in Dec 2020, and then bought a 2bdrm condo Feb 2021 for $850K in order to stay in our son’s school district. It was the most affordable option to own. Our unit sold for $350K a decade ago. Maintenance fees are $1000 per month, and our 1.5% 4-yr rate will be up in 2025. Emergency low interest rates for 13 years, FOMO speculative mania, foreign money, and investor friendly regulations really juiced RE prices this past decade, and there really wasn’t any correction during the GFC 2008-2010. Toronto RE just kept rising from the low in 1996 after the last crash that began in 1989.

I’m not Canadian but I watch some utube videos by various people… presentations good, but find their predictions, in general, haven’t been that accurate. Hit and miss i suppose.

I live in eastern Washington but was curious about the Canadian market and came across Team Sessa based in Toronto. He does a pretty factual assessment of Toronto RE market though I haven’t watched any of their utube videos in half a year. Ontario real estate is certainly more expensive than my home state Ohio on the other side of Lake Erie. Of course the nation’s capital Ottawa is there as is Toronto.

Some pretty unhappy renters in Ontario just like in expensive US cities from what I gathered.

Being in the north side of Lake Erie I noticed Toronto gets considerably less snow than Cleveland, which can average anywhere from 59 inches on the west side (John Hopkins Intl. Airport) to 101 inches (Chardon, southeast suburb) annually. Lake effect.

Toronto averages 48 inches snow annually and gets only about 65 to 80% as much precipitation as most eastern US cities at 32 inches annually.

(E.g., Canton Ohio 41, Atlanta 49, Tennessee cities in the mid to upper 40s).

Seattle gets 36 inches, few thunderstorms but frequent drizzle thru 8 to 9 months of the year.

L

Good day, mate ! Oh wait that’s that big island, eh ? They playing England tonight in Women’s World Cup soccer semi. .. lively entertainment that.

I grew up in southern ON between London amd Toronto, they’re only about a 2 hour drive apart but London most years would get absolutely dumped on and Toronto was usually spared. It’s funny because all those years living there I never found out why that is 😂. I’ll say though, the winds off the lake in TO especially around the skyscrapers downtown are brutal, you’ll walk the block in fairly calm air and as soon as you step into a corner of a major intersection you’ll nearly be knocked to the ground.. leave the intersection and things get calm again lol. This year will be the first in 8 that I’ll be back there in the winter, see how I fare after getting softened up just north of you in metro Vancouver 🙂

Toronto still has largest number of active tower cranes in north America. The RE boom will boom.

Legal immigration to Canada reached an all time high in 2022 (over 500,000). The prior record was set way back in 1913 when some of my older relatives came over from Old Europe. 2023 is expected to be another bumper year for immigration to Canada. Many of them will settle in the Toronto area because that is where many of the job opportunities are.

Aren’t a huge number of those immigrants going back to their home countries now mainly because Canada’s home prices have got so wacky though? Unless you’re willing to put up with like 5 roommates in a filthy basement bungalow Toronto esp is unaffordable, so it’s not like they’re coming out ahead economically anymore. So even though the initial immigrant numbers are high, far fewer stay in Canada now, esp a lot are going back to India and China after maybe 1 to 2 years if they can save up anything because cost of living is a lot lower.

Also been hearing even a lot of Canadians are leaving too because cost of living is too high, ex there was an article in one of the overseas living magazines about the flood of Canadians moving into Europe lately. Some using ancestry, a lot though going to France since they can use relatively good knowledge of the country and culture to advantage. (Not even coming from Quebec, it was mostly other parts of Canada because so many start French and learn the culture at a very young age) Then add that to fact that Canada’s birth rate is also falling to the ground (those home prices hurt that too) and Canada’s overall population may not be changing all that much. A lot of French have already been complaining about the flood of rich Americans bidding Paris real estate to the moon, now looks like Canada might also be spreading the housing bubble contagion to the some of the same places.

Every single one of those projects will have been initiated under zirp.

very nice new bull market started :)

“Note in the insert the rise in the prior month, June, of 0.8%”

Note the rise in June, the prior month, of 0.8%

“a classing classic rounding off pattern”

classic

Thanks for the update Wolf. Calgary keeps on truckin’ on demand from in-migration relative to supply, but I have to wonder how long it will take for prices to flatten there too.

Inform all your Calgarians to buy resale not new. No one in Alberta has ever figured it out since way back in the 1970’s The entire rest of Canada knows it so obviously the people moving to Alberta from other province will bid up the price of all the resales and none of them will buy new unless they don’t care about money. In the rest of Canada a resale detached house costs about 25 percent more than a resale townhouse but in Alberta a resale detached house costs at least twice what a resale townhouse costs. In Edmonton a resale detached houses cost about triple what a resale townhouse costs.

We’ve seen many Canadians owning or looking for snow-bird properties in SW Florida are over last several years.

Last season there seemed (anecdotally, of course) to be less.

I suppose the uncertainty created by the rise in Canadian rates is a primary reason.

If true, a good example of “transmission” of regional monetary policy and RE activity?

We have tons of Canadians where I live. 2nd houses. They come for ~3 months. Own a car they leave here etc.

We even rent our condo from Canadian owners.

New fam from… Calgary haha (but they’re permanent). That’s a first tbh.

Usually they’re Toronto or Vancouver.

I keep (selfishly) waiting for Canada to crash and burn :P

“I got 5 houses? Good for me!!!” -SNL

A falling Canadian dollar was probably part of the reason for less buyers.

From today’s Globe and Mail:

> “They also see the downside, which is putting further pressure on the housing market and pressure on health care.”

> Miller said the federal government needs to carefully examine reports on housing and population growth, but he also raised concerns that some of the critiques are motivated by bigotry.

> “The wave of populist, opportunist sentiment that does at times want to put all of society’s woes on the backs of immigrants – I think we need to call that out when we see it,” he said.

That’s Canada. Nobody believes the above but they do know that they can say something similar to continue to vote for their own children to suffer and claim the moral high ground.

Canada is absolute lunacy. At my employer in IT the vast majority of people are on work visas. They can’t switch employers , they can’t argue about low pay rises. They are stuck for years, exploitable.

Government loves jacking up real estate prices. More property tax.

Under the illusion of increasing “wealth” higher property taxes fund gross Government.

And in Canada, even Minimum Wage workers +/- $16/hour pay about 15% income taxes, and their employer pays +/- $15% more on top of that. Comfortable Government Apparatchiks are always bleating about raising the minimum wage to fund Government Employee Pension funds.

It’s worldwide but the crackers are starting to show ,these fake monetary policies will probably create chaos .Seems to be end game of elites . Founder of Microsoft is in on it big time ,also starting to think Warren is too

Tim Horton’s is known for hiring ‘international students’ and TFWs on their team. Walmart is also doing the same thing.

Even “Canadian” businesses named from Canadian landmarks like Hudson Bay hire almost entirely ‘international students’ in their fulfillment warehouses across the Greater Toronto Area.

Grocery stores where you’d meet the friendly cashier in the community has been replaced by ‘international students’. It’s gotten so bad that if you YouTube search “Brampton long lines Fortinos”, you see a long line of mainly ‘international students’ waiting for a job at a job fair. The line was at least a mile long.

These sort of jobs are what Canadian high school students did during the summer to save for their fresh years at university.

Yeah Canada’s policy has gone totally nuts, as bad as the bubbles are in the US the Canadian government seems determined to run it’s entire economic policy on desperately inflating one bubble or another esp the housing bubble. Xenophobia has nothing to do with it, people in Canada know the country just can’t handle this many people coming in too fast after the loose monetary policy of past few years, just drives down incomes and pushes up cost of living, a disaster for almost everyone.

It’s not even helping Canada’s overall situation much, most of the immigrants don’t even stay long in Canada any longer because it’s too expensive for them too. But now more and more Canadians are leaving Canada for good, and the birth rate just keeps dropping more and more as cost of living goes up. Politicians never seem to actually think these things through.

Canada is an insane, extreme experiment.

A land pyramid scheme in the second largest country on earth with a tiny population.

Lunacy.

It more or less mimics the Chinese housing bubble in China.

Agreed on the China syndrome. Citizenship in Canada is for sale.

Students sign up for good unis to get the visa then switch to a cheap course for subsequent years. They never wanted the course, they wanted the visa.

Canada has created a huge mess here. They constantly have articles in their news about “Chinese interference” but apparently making life impossible for all Canadian young isn’t “interference”, so long as there are huge fake profits to be made.

The news is also chock full of stories like “I went to the grocery store in the USA and got shot” to dissuade brain drain.

Most of the new workers I’m seeing are from Nigeria and very few are from India and Pakistan.

The housing market in Canada has been the holy grail the past 30 years and far too much is dependent on it.

Thus it is truly “too big to fail” or fall heavy at any cost.

The banks are fully protected for a bail in that will never happen, thus the only risk is an honest government that ever changes the rules to be pro homeowner, vs pro bank and we all know that will never happen…

Waiting for a mean reversion drop for potential buyers? Good Luck.

Our home equity will be our 25 yr old daughter’s future equity. Making over $100,000 in a small northern Ontario city as a lawyer, she is shut out.

Please consider that many folks like you and me, our

Home equity may go towards our retirement costs, God forbid we need one if the amica homes.

I am seeing this happening already. Retirees with very good pensions cannot afford some of these residences.

These retirement homes never rebounded from Covid. More seniors in their 80’s and 90’s must be staying in their homes.

The idea that the Canadian government can somehow protect housing is I’m afraid very misguided. CAD is a very small currency. You simply cannot just print like the big boys without massive impact. Given Canada’s demographics any significant inflation would then kick of a second set of issues around those on fixed income.

They can’t just smooth this over, it’s not magic.

RE in Canada has been an enigma.

Over the last decade, I watched it go up and up, defying gravity.

The math still indicates that it must crash back to earth.

I have friends all around me who are loaded up with debt, and I am talking 400 to 500k.

They are in their 50s and 60s and are now unable to retire.

I am seeing lots of stress in the RE now, maybe this is the 11th hour, but who knows.

Time will tell.

In many jurisdictions the median price has doubled in about 7 years. Incredible. If Canada had deployed a new invention that boosted productivity, such as in the past, the steam engine, this could be reason for such gains. But no, this is just created by inventing money from thin air. This can only end badly. How and only the future remains to be seen. Canada is not alone, Many other countries face the same predicament.

The elephant in the room are the home lines of credit the boomers use to live like movie stars or just survive. To the detriment of future generations. Complicity for comfort!

Kanada. Someone has to live there.

I don’t really understand how the relationship between the banks and the government come to be so buddy buddy tight to the detriment of living standards for the population. Canadians like the USA have few real options voting against big money interests. For all their superior education system, they remain ignorant of the true political underpinning of their society.

Somehow the Federal government is deathly afraid of fixing the housing bubble by allowing price drops. I don’t think you lose votes by allowing prices to return to already high 2019 levels. Instead they have encouraged the banks to flout the impact of Bank of Canada interest rates on housing specifically. As noted presumably to hold power for the current party.

However the inherent government bailout of housing in Canada if there is a significant downturn would be incredibly healthy long term for the country economically but painful when the government insures 80-100 percent of mortgage loans at risk of failure.

The federal government has nothing whatsoever to do with prices of housing which are set in the markets by supply and demand. The only ones to blame for high prices are morons who have bid housing prices up to as much as 1000% over what they were 10 years ago.

Federally run mortgage programs, federal flood insurance, tax preference, and money printing all encourage citizenry to buy houses.

It seems far-fetched to call those programs “nothing whatsoever.”

What am I missing in your statement?

This for me is the most depressing thing about Canada: my kids are going through a similar school system to you.

I’ve yet to see a home price the Chinese won’t buy at. They’ve never read the definition of the word “valuation” and likely never will. Their hobbies in life are are waiting for the second the sales office opens to buy up everything and then sell to the ones near the end of the lineup a couple of hours later.

When the federal government keeps giving tens of billions to CMHC they are the ones to blame!

It is true that federal and other levels of government do not actually set the prices of housing. However, all levels of government together control virtually every other aspect of residential real estate, including land use, building codes, taxation, mortgages, demand (immigration), etc. To hold government blameless for Canada’s housing bubble is to be very generous to them.

The last major bank to fail in Canada was the Home Bank, back in 1923. The failure also took down the fortune of Sir Henry Pellatt, the guy that built Casa Loma (the largest private residence in North America, when Sir Henry and his wife lived there) and lost it to the City of Toronto for failure to pay his property taxes.

Canada has a long history of trade protectionism via high tariffs and quotas. Other sectors of the economy, including banking, are largely closed to foreign investors. NAFTA was a blessing for average Canadian consumers as it significantly closed the price gap between Canadian and American consumer prices, adjusted for currency differences.

“I don’t really understand how the relationship between the banks and the government come to be so buddy buddy tight to the detriment of living standards for the population.”

I’m told by others better informed than I and in a position to judge such matters: “because nothing happens in Ottawa without the Big 5 banks signing off on it”.

Wolf,

Unrelated to housing, but a topic of interest on your blog. As you point out, there is still plenty of liquidity/stimulus coming from the government. You point out the (albeit it, pathetically slow/minimal) decrease in the Fed’s balance sheet trends. However, I was looking at the total Federal Reserve assets (QBPBSTAS), which is only down 1% (growing again) from it’s peak in Q1 of 2022. What is this actually reflecting? It’s growing again.

Your problem is that you’re following moron bloggers who don’t know what they’re talking about, and who are feeding you a bunch of clickbait BS. And the fact that you’re eating it is your fault.

The least you could do is google the data reference you cite (QBPBSTAS). Click on the first link (from the St. Louis Fed FRED data base). And then read the “source” info below the chart, which tells you it’s from the FDIC. And then read further down the section below the chart.

The QBPBSTAS you’re referring has zero to do with the Fed, but is the FDIC’s count of total assets in the US banking sector. Commercial BANKS! This $23.72 trillion in total assets at banks is a measure of the size of the US banking sector. DUH.

Don’t go back to the sites that fed you this braindead clickbait BS. They’re lying to you on a daily basis.

When I see these articles I always think of the guy building 150 – 400 sq ft homes in TN for $15,000 -$100,000 and will rent you a lot for $200 or $300 per month if can’t find a place to put it. He has had people move there from as far away as Hawaii who felt they were trapped with exploding cost of living.

There are a lot of older women who need a safe place to live, but only have $1,000 – $2,000 per month of income. Most women have the gift of being able to make something modest a comfortable and inviting home.

The key to making a home cheap is for it to be small enough that you can run it down an assembly line like a car.

Yes, we could easily house low-income people in small (tiny) houses but governments will not re-zone property to allow these sense communities. The few that have been allowed are usually luxury and expensive on a psf basis. America needs to allow more “do it yourself” housing like in the past and small houses for smaller households.

Many trailer parks have been bought up by private equity firms, which have jacked up the lot rents. Government is reluctant to permit new trailer parks and mobile home communities.

As an unqualified, ignorant onlooker of pandemic economics, and a Fred enthusiast, my initial observation is that as Canadian home prices drift lower, Canadian GDP will trend lower as well.

I think the variable and insane lags of global financial tightening, with extremely uncertain inflation dynamics, paint a background layer of declining global growth, seemingly contributing to recessionary outcomes.

However, this post-pandemic Schrödinger Cat simultaneous state of drunken sailors ignoring prior patterns of economic behavior, probably will continue to play a role in delaying and dampening future economic shock — however, as the entire global banking segment falls into insolvency, it’s hard to imagine that as serious economic global stress intensifies, that the drunken sailors will continue to party and spend infinitely. I think the sailors will eventually decrease consumption and become far more insecure and hesitant, as dominoes fall around them.

I think Canada housing is a great way to think about global dynamics.

I’m getting old and memory is not what it used to be.

Somewhere I got the idea that Canadian housing didn’t take the hit that the US housing did back in the 2008 timeframe. Maybe I’m just wrong.

I wonder if there a comparable US housing price histoy chart 2007-2023 that could be overlaid on the Canadian MLS Housing price chart. More out of curiosity than anything else.

Your articles are a welcome, and refreshing view of current financial affairs. Thank you.

I have overlaid the Canadian Teranet series with the US Case-Shiller series a few years back. Both are comparable in their method (sales pairs method, not median price). Overlaying data sets in a chart is always an iffy exercise for a variety of reasons. This one is from June 2019. It shows the % change since 2002 for Vancouver (black) and San Francisco (red). Enjoy with a grain of salt.

Until some massive external event causes a large percentage of current homeowners to put their homes on the market for sale prices appear to want to move higher, regardless of interest rates, same as in the US and worldwide.

What could that event be? Until now, war, shortages, inflation, elections, high mortgage rates, high energy prices, tight budgets, stock market corrections, bond market drops, crypto implosions, increased taxes, double digit insurance premiums and more have all been unable to stop the runaway train.

Housing will drop because many of the SAME people who bought in the 2020 to 2023 time frame will be selling. These were the people who drove prices up, and they will drive prices back down.

Look at the composition of the listings. People who bought recently are making up a greater share of listings, and that share is growing. They know prices are dropping, they bought at the top, and they don’t want to get into financial trouble.

Right now, most of them are trying to capture a small gain, while avoiding large losses in the future. As prices continue downward, we will see them start to panic and sell out at prices to avoid large loss.

In addition, a lot of these recent buyers turned sellers may be returning to office work, and they can’t handle the harsh commute times.

CCCB-

My guess is that at some point corporate earnings (or at least earnings growth) go sideways for a spell, leading to job loss.

Could the 1970’s double whammy of inflation (accompanied by high interest rates) and unemployment be the “event” you expect?

Stagflation is a harsh mistress!

(Check out Arthur Okun’s original “Misery Index” from 1970’s, or Steve Hanke’s modified index.)

“What could that event be?”

Airbnb hosts losing money on their vacation rentals?

Lots of complains about that already. I know a guy with four condos in SF on Airbnb. He’s complaining about the competition. These vacation rentals are everywhere, gazillions of them. While there are lots of tourists now, there aren’t nearly enough for the gazillion vacation rentals. Then the tourist season ends, and vacancy rates jump, while expenses continue. At some point, it’s not fun anymore.

@Bobber

Yes, totally this. Starting to see signs of this in the US too as rates rise and becomes clear JPow is not going to stop turning the screws, the wave of FOMO homebuyers and other asset buyers are realizing that all those delusions about a pivot are just fantasy tales, told to make them the bag-holders when things return to valuations that even start to make sense. The idiot pivot-mongers and squawkers (and this includes the once respectable Wall Street Journal and other big financial media) did everyone disservice by continuing to cast doubt on Powell’s resolve to fight inflation. The Fed will pivot and starting cutting interest rates back down like crazy! QE back on the way, uncontrolled liquidity again!

These idiots failed to realize that ZIRP and QE in the pandemic were acknowledged by the Fed itself as a disaster, and the Fed couldn’t let inflation keep running hot without permanently crushing the US economy and the US dollar. Not to mention all this just made Powell even more angry and determined to prove the pivot-mongers wrong. Even if he isn’t our generation’s Volcker, Powell knows how dangerous all this inflation is and that’s why he hasn’t taken his foot of the gas pedal on interest rates and QT. It seems like only now it’s finally sinking in that the good ol’ days of ZIRP and especially QE will likely never be returning. And that without the easy money policy, that the ones who panic first panic best when it comes to selling off overvalued assets. Especially housing across the US markets.

The govt will get more desperate, and they will probably ramp up immigration and international student permits just to keep the housing bubble going.

Unlike America where one can move to at least one major city in any of the 50 states, Canada is just Vancouver, Calgary, Edmonton, Winnipeg, Greater Toronto Area, Ottawa, Montreal and Halifax, with Toronto, Vancouver, Calgary and Montreal the only major cities in Canada where there are jobs.

Which will make the Canadian policy fail even harder. Now the immigrants themselves realize that Canada is fast becoming unaffordable and a greater proportion are going home, even Canadians are leaving Canada for good in larger numbers and then the birth rate is also falling. Now the government’s opening the door even wider for immigrants mainly from Nigeria which is being seen as the biggest new source (since so many from India and China are returning) but that won’t work either–they’re quickly seeing the country isn’t the land of milk and honey, and if they can’t afford rents and housing, they can’t afford it.

Applies to the USA too, and even a lot of those other cities are also getting to be unaffordable with their cost of living with less income to afford the homes there. This is why inflating bubbles is just stupid economic policy, you can’t delay the inevitable correction in prices and trying to do so just means things are even worse when the rug is pulled out and the bubbles pop all at once.

The Canadian govt is acting reckless because they are aware that they did not get enough housing for newcomers.

Canadians see right through the politicians. They want to use human beings as a crutch to economic growth, and fatten their portfolios.

The asylum homeless crisis is another stain on Canada’s image. People fleeing persecution for their views or their personal preferences living on the streets.

Agreed Canadians see immigrants as a resource to be exploited to the max.

What is up with Warren Buffet buying an $800 million stake in a lot of the biggest U.S. Home builders. He must be bullish? He is buying near ATHs.

1. He is not “buying.” He “BOUGHT” months ago, sometime in Q2, and it was disclosed on Monday.

2. He is sitting on a huge pile of cash (T-bills, etc.) and has got to do something with it.

3. His purchases helped DRIVE UP prices of homebuilders in Q2 — DR Horton soared 42% in Q2. Now he is done buying them… so DR Horton peaked in early July and has since wandered lower.

Warren has been divesting many stocks ,he knows world is becoming bifurcated.China created a mess with there political domination nonsense .This will lead to WAR .God save us

Yahoo: US Mortgage Rates Climb to Highest Since 2001…

Average mortgage rates in US rapidly headed to over 8%

Wolf didnt mention the scam that has been pulled to keep the bubble intact. Canadian mortgages are being rolled over to longer terms to keep the payments from ballooning when these short term loans need to be refinanced.

Some loans might even go into negative amortization, where the monthly payment is less than the interest paid, so it climbs above the trigger rate and results in a loan balance that climbs over time.

This is so typical of liberal economic policies – allowing the fraudulent banker class to once again do things that prop up the bubble and prevent accountability for the economic mess they have created.

It is my opinion that these insane economic policies will only forestall the crash and will lead to a much bigger and more painful crash in the future. Canada better hope the price of oil moves higher, because the rest of the economy is built on real estate speculation.

Oh yes, the infamous 75 year and 90 year amortizations. If only renters can delay their rent payments using perpetual amortizations.

There appears to be a concerted effort to maintain bubble prices, while in America, rents are going down and Americans just shrug their shoulders.

But the govt here in Canada; anything to protect the value of a C$700,000 shack in the middle of Manitoba, while at the same time insourcing temporary labor to drive down median wages.

The unspoken event in the Canadian job market is that government is relying more and more on temporary contracts and staffing agencies, rather than direct hires with defined pension benefits, higher wages and union benefits.

According to some banker talk, the variable rate mortgages that now barely cover interest rate payments, will have to come to compliance when the five-year mortgage is renegotiated, no matter what the lunatic fringe has legislated. That means huge payment when the five year term comes due.

I was thinking infinite mortgages, too, but there might still be some financial sanity left, even though not close to government.

Agree that beside forestry and oil/gas, there is no economy but housing bubble.

gametv

“mortgages are being rolled over to longer terms …”

The amortization period of existing mortgages is being lengthened. This is one of the typical ways in which a mortgage can be modified to reduce the risk of default.

These are Canadian mortgages, not 30-year US fixed-rate mortgages. When interest rates go up, mortgage payments of existing mortgages go up fairly quickly, depending on the mortgage type. This increase in mortgage payments of existing mortgages can be prevented if the lender agrees to lengthen the amortization period of the mortgage. So the payment remains the same, but the principal portion of the payment shrinks, or vanishes, and in some cases, the mortgage payment no longer is enough to pay the interest, and the mortgage balance actually increases with each payment as the unpaid interest portion is added to it. This increases the longer-term risk for lenders, but it beats having to deal with a default now. The hope is that rates will drop fairly soon, and then the mortgage can be reverted to shorter amortization.

Mortgage modifications are very common. The lenders want payments, not the house.

Housing is no more of a bubble than the value of the loonie (the scarcity of productive assets and government deficits destroying the currency), The Canadian banks are far more conservative than their US counterparts and they have far more control over policy making, i.e. land available for development, immigration, building permits, etc. It’s a command economy. More than half the country is mortgage free and the population of Canada is less than Cali. It’s very unlikely there will be a crash in real estate until a global systemic collapse happens. The market in Canada is tiny and private lending for real estate has exploded over the past year. The currency is absolutely garbage, we just use it to transact, I expect the cost of production to double in 10 years and the production of detached homes to decline dramatically (minus 30% this year to date). The banks will gear the supply and demand fundamentals to defend the market. Land is not available like it is in the US market and the banks won’t finance raw land. I’m not trying to defend the market I live in, I prefer a free market with deflationary cycles. You have to have enough confidence in the loonie to bet on a housing crash. Personally, I’d much rather hold a diverse selection of real estate and maintain manufacturing assets for income, I only hold enough currency for 3 years of crisis because the loonie supply is still growing substantially. A measure of money supply supersedes the effect of interest rates.

Wolf, since you don’t cover little crappy towns that nobody wants to live in (cough, cough, Nanaimo, cough), I’ll throw in my two cents and mention Nanaimo is down around 5% in July alone. That’s year-over-year and also from June, so recent buyers can pick whichever Time Frame Hammer they’d like to use to crack their heads. I’ll also mention that decline comes after a ridiculous free money party-time atmosphere in the first two weeks of July, i.e., until the BoC ruined the show. So, who knows what the actual peak was in July.

I am also seeing a lot of empty houses hitting the market, so maybe some of the shadow inventory you mention often is finally showing up. Anything over 800k (in Nanaimo, LOL) seems to rot on the MLS (as it should). Lots of price reductions, and the highest number of listings I have seen since the Peak Fool dearth of listings back in 2021.

Can’t say I mind. I have been wanting to buy a house for the longest time and haven’t been able to (moving around for work, etc.), and now mostly because I don’t want to commit financial suicide. So, fingers crossed there is sufficient return to sanity and I can finally look for a place without being outbid by fools, “investors” and money launderers.

TEMPLE

Didn’t the previous mayor robertson of Vancouver say foreign money wasn’t an issue when he was in office…. All while having a girlfriend who was worth North 70m and whose mother embezzled 350m rmb (yuan) was sentenced to death and under house arrest in China (one of China’s methods to try to recoup some funds in the game of pay for the hostage tactics)

In the past few years, the media is just starting to talk about snow washing a method used to launder and obfuscate funds into Canada (and the the g7 at large). The media is just reporting history. Snow washing of Chinese funds has been going on since the mid to late 90s as a hot money laundering method. The Canadian government, politicians and law enforcement are aware of this… They just turn a blind eye and keep it on the low down, in hopes that the general public doesn’t pick up on it. This hot money got the ball rolling early on in the mid to late 90s and as a snowball it kept getting bigger and pulling in more of the general populace to buy into the belief that the average home prices in Toronto will hit $5.3m by 2053.

Canada if run properly for the past 50 years could’ve been a global powerhouse if they optimized their human capital (instead of the brain drain to the south or immigrants returning home), if they optimized the effective and efficient use of capital on improving efficiency and innovation, and if they optimized the use of the natural resources they were endowed with.

Canada is like a cook with all the ingredients to pull off the best meals ever…. But instead they turn that meal into over cooked charcoal by make wrong decision after wrong decision (I know sounds like a lot of the g20… Hahaha)

The pretend and extend game had a limit… They the refractory phase kicks in and then even more Viagra doesn’t help…. As per Hugh Hefner…. 😢😢😢

Lots of stress to come. I know of several couples already trapped. The variable rate, i.e., can change anytime, was VERY popular. Folks who bought condos ‘off plan’ to be built also stressed. Lots of these were ‘sold’ two years ago, to lock in the price. They qualified then, not now. One Punjabi guy put 250K down on a 1.7 mil condo in TO area. Now can’t get financing at new rates.

But worse in China. Aug. 15 Globe and Mail piece in Biz section: ‘China’s property sector crash intensifies’. Giant Evergrande woe is old story but larger giant Country Garden was thought different. Now it is delaying payments. Its stock is down by 50% in last month.

Worse, contagion is spreading to financial/ banking with

huge Trust Zhongong missing payments to 2 other fincos.

But isn’t that China, not here? After the GFC, the Chinese stimulus was the largest in the world, and boosted all markets. That tide is going out faster than any other in G7.

An incidental effect could be probs for NA manufacturing. China was always the lowest price, but quality was iffy. But quality has improved, not just because Xi personally lectured a meeting of industry re: quality. With youth unemployment over 20%, China has room to cut wages.

Will inexpensive Chinese E-car arrive here and maybe do to NA what Japan did to ICE makers ?

Here yah go, it’s the damn Boomers, yet again, destroying the world!! Article from the Globe in May:

The percentage of singles and couples who live in homes that have a minimum of three bedrooms increased to 29 per cent in Canada in 2021, according to an analysis by The Globe and Mail of census numbers for that year. That compares with 26 per cent in 2006, according to the corresponding census.

The numbers suggest a growing proportion of people are living in homes that are larger than they require and staying in place as they age, rather than downsizing. The trend is driven by an aging population, the lack of suitable housing for seniors and the high cost of smaller housing alternatives, experts say.

“I’ve been told by many seniors that none of these options are attractive,” Ms. Bednarski said, adding that most want to stay in their neighbourhood, shop at the same grocery store and stay near their community.

CMHC’s Mr. ab Iorwerth expects the unused bedroom trend to grow. “It will accelerate with an aging population, particularly if there is no significant change in zoning those areas to allow higher density,” he said.

“I don’t think we’ve reached the peak of elderly living alone, since we still have a lot of the baby boomers aging ahead of us,” he said.

==#. This makes me think of Japan demographic stuff and all the vacant, abandoned homes in USA. Interestingly, the whole commercial office space disaster in many ways is driven by this same demographic engine. Too many buildings, too many buildings, too many strip malls, too many karate studios, too many over leveraged bad investments in decaying society — even though, things are booming and everyone has infinite income and no debt (just ask a bank). Everyone is anxiously awaiting the next leg up in these bubbles.

Funny how Quebec City area has the lowest housing prices of the areas covered. Something to do with speaking French?

It’s to do with Anglo culture being defined primarily by a love of rentier activity.

Same taxes. Very similar legally. Same interest rates.

Yet the insane housing bubble began in the Anglo side.

I hope prices here in Canada end up like Detroit where $150,000 homes were worth $10,000. They might be what $40,000 now I am not informed about Detroit real estate but a big crash is needed.

I personally own a Home in a big Canadian city and I do not personally care if I lose $500,000 or more in my house’s value. It is not worth that in the first place and prudently, disciplined for 35 years saved diligently and now have 2 times 6 figures in my GICs, RRSPs, TFSA, savings accounts, cashable GICs so I do not think my home is an investment but just an asset to sell when or if I decide to move. This whole real estate hype pump up in prices in Canada and around different parts of the world is a big scam.

Weird comment. Canadian RE is not a scam. Indeed, it’s one of the best investments in the world. Anyway, there may be a correction…or not. Prices have doubled in the past ten years, a reduction of 20% is nothing to be concerned about. ….well, for anyone who didn’t buy during the height of the pandemic mania.

FYI: Cryptos were also “the best investment in the world.” Now they’re down by 50%-plus. A bunch of them blew up and are essentially worthless now.

The trick is in the fact that people believe that prices are only going up and are afraid of missing the train. (FOMO)

But buying the property is not buying a pair of pants, it’s a lot of money. When most stressed buyers buy the market calms down. The scam no longer works and prices are going down.

Canadian RE is a giant game of hot potato. If you bought in the last 10-20 years depending on location, you are holding the hot potato. Scam / game / ponzie / pyramid call it what you must.