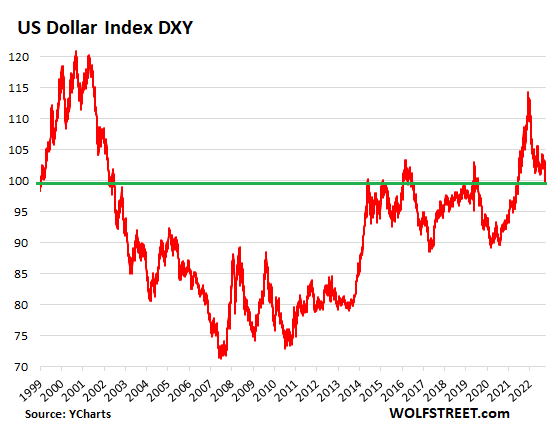

In other words, after a spike, the dollar dropped back to the higher end of the normal 20-year range. But the yen is a sloppy mess.

By Wolf Richter for WOLF STREET.

The dollar-collapse and dollar-crash folks are out in force. “The dollar crashed to its lowest in more than a year on Wednesday after data showed the rise in U.S. consumer prices moderated in June, suggesting the Federal Reserve may have to raise interest rates only one more time this year,” Reuters said, which put one of those lopsided dry grins on my face.

And the dollar has dropped a bunch, but since September last year, off a majestic spike and two-decade high against a basket of other currencies, tracked by the Dollar Index (DXY), which is dominated by the euro and the yen. And that spike had worried a lot of people, companies, and governments around the world because all heck breaks loose when the dollar gets strong – especially in emerging markets.

So after this fearsome plunge, the dollar is now back where it was at the high in April 2020 and at the highs in the years 2015-2017, and it’s back where it had been in 1999. And it was a LOT lower in between. In other words, the dollar is back at the higher end of the normal range over the past 20 years (data via YCharts):

Both the euro and the yen had been plunging through October 2022: The Fed had been hiking rates since March 2022 and cranking up QT since July 2022, and in 12 months hiked by 5 percentage points, while the ECB just started hiking rates out of the negative in July, and it only announced QT in October, as inflation was already raging; and while the Bank of Japan was – and is to this day – still clinging to its negative-interest-rate absurdity and its yield curve control even as inflation is spiraling higher. So the dollar battered their currencies last year.

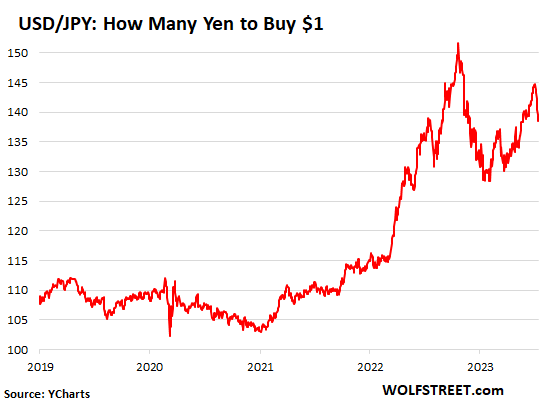

The yen has become a sloppy mess.

Last year, the yen dropped in a huge slide, from ¥110 per dollar in 2021, to ¥151 per dollar by October 2022, triggering verbal and finally actual interventions in the currency markets by the Ministry of Finance, which blew $68 billion in USD assets to buy YEN, spread over three days, which caused the yen to recover some before losing more ground again this year. By June, when the yen pushed again over the 140-line, there was more talk of interventions by the MoF (data via YCharts):

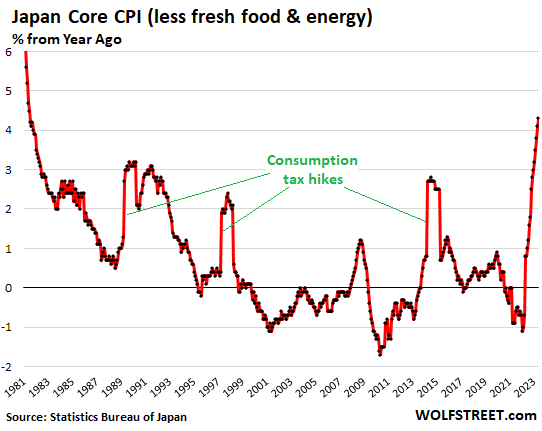

The problem for the yen is the toxic mix of inflation and the Bank of Japan’s decision to let inflation rip. Japan’s core CPI spiked to 4.3% year-over-year, the worst since 1981. Month-to-month, the three-month moving average of core CPI spiked to an annualized rate of 6.6%. Food inflation spiked to 8.6% year-over-year, the worst since 1976.

And yet, the Bank of Japan decided to keep its short-term policy rate in the negative, and to keep repressing long-term rates via its yield curve control, capping the 10-year yield at 0.5%, though it had raised the cap from 0.25% late last year. Japan now has the worst negative real rates in the developed world.

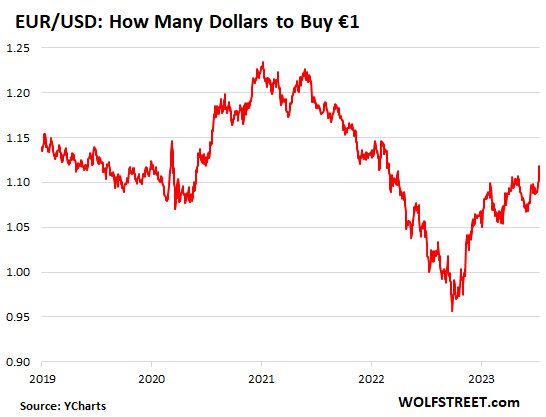

The euro recovered after the ECB began to tighten.

The euro had dropped as low as $0.96 by October 2022, from the $1.20 range in 2021, as raging inflation had broken out worse even than in the US. But by that time, the ECB became hawkish. It has by now hiked by 4 percentage points; and it has shed €1.6 trillion in assets from its gigantic balance sheet, and euro traders noticed. The euro has surged against the dollar, from $0.96 per euro in October 2022 to $1.12 today, and is now back in the historically normal range against the dollar:

Inflation in the US isn’t going to just vanish. What had pushed down overall CPI on Wednesday was mainly the plunge in energy prices. Core CPI came in at 4.8%, higher than overall CPI. The all-important core services CPI (without energy services) was a still red-hot 6.2%. And there are several factors in the second half that we already know today that will provide upward momentum to CPI, and we discussed this whole situation here.

So the idea was to enjoy these still bad CPI readings as long as we can, before they take another turn for the worse again? In terms of the dollar, any reason why it does whatever it does on a particular day is a good reason, but it’s now back where it sort of belongs, at the upper end of the normal 20-year range.

Central banks that were able to read the tea leaves correctly and front-ran the Fed with big rate hikes were able to protect their currencies while getting a handle on inflation – letting these two get away can lead to a currency crisis in emerging markets where governments and companies have debt that is denominated in dollars. A sinking local currency makes these debts devilishly hard to service. And a number of central banks managed this precarious situation reasonably well.

The Bank of Mexico stands out. It never did QE in the first place. It started hiking in mid-2021 and hiked relentlessly by 725 basis points to 11.25%. In May it paused. Core CPI has come down to 6.9%, though this is still very high, but down from the 8.5% range. And the peso has regained all the value against the dollar it had lost during the pandemic, plus some, and is back at 16.75 pesos to the dollar, where it last had been in 2015.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf, can you give a fair comparison of Gold vs Dollar denominated assets for this millenium, i.e. 2020 to 2023.

Gold price increase in dollars in last 23 years compared to:

1. Nasdaq

2. S&P 500

3. 10 year treasury avg return in this period

4. US case shiller index.

5. San Francisco case shiller index.

Gold is not an investment, just a store of value. Let’s see how a non-investment compares with investment in last 23 years.

I know I am cherry picking the timeliness, but last 23 years has been big Fed intervention years beginningwith dot com bust, hence its worth Cherry picking.

The 700 million tons of mined copper in the world is valued at $4.5 trillion.

The 202 thousand tons of mined gold is valued at $13 trillion. The real practical value of the total copper is at least 250 times that of the gold. This is the scale of the anachronistic absurdity of relative metal valuations.

Read the Wikipedia article on the history of the gold standard. Comedy.

Interesting. Do any of the central banks stockpile copper?

Copper will continue to be used in manufacturing way more than gold.

“The base metal-copper is 15,000 times more abundant in the Earth’s crust than the precious metal”, and always will be a lot less expensive.

Gold does not oxidise, and always maintains it’s composition, and therefvore is a store of value. And because of this, it is used in certain application like behind the solar panels on the James Webb telescope, It never degrades even with extreme tempertures

.

It is birthed from the tempertures and pressures of black holes.

“birthed from the tempertures and pressures of black holes.”

Reminds me of the sales puffery of DeBeers, in the service of their twinkly glass-like rocks (not salt, salt has utility).

Actually, I’m just kidding…copper, gold, diamonds, salt all have *some* utility and their near term supply is comparatively fixed…whereas the fiat currencies birthed by political organizations…

Gold has utility as a noncorroding conductor–in teeny, teeny, teeny tiny amounts.

Cas, good insight about marketing. I can get a 1ct diamond dressing stone for $29.99.

The “practical value of the total copper is at least 250 times that of the gold”. Gold is a better conductor, more ductile, better corrosion resistance. It has more practical value than copper. If they were the same price and availability your house wiring would be gold.

OK. Basic shelter: a copper roof can last generations, certainly over 100 years. Gold is a bit heavy for some common applications.

The fact is, we are living in an electronic extension of the bronze age. Copper is king.

Here is the last 23 year data without any coloring for benefit of wolfstreet readers (mostly from macrotrends):

Gold went up “6.9” times from $284 to $1954

Nasdaq Index went up “3.6” times from 3940 to 14138

S&P 500 Index went up “3.2” times from 1394 to 4505

US Case Shiller Index went up “3” times from 100 to 301

San Francisco Case Shiller Index went up “3.4” times from 101 to 339

10 Year treasuriy yielded 3.22% average returning “2.1” times from $100 to $207

Copper went up “4.6” times from $0.83 to $3.78

Wheat went up “2.4” times from $2.86 to $6.93

Oil went up “2.6” times from $28.7 to $75.3

No opinions, you conclude.

Leo,

Now redo the calculation, with a starting point “20” years ago (not “23” years ago) in July 2003. 23 years ago was near the peak of the dotcom bubble. Three years later, the Nasdaq was down 78%, and the S&P 500 was down 50%. So now use those as a starting point. And it changes your comparison dramatically.

The reason you own gold is as a hedge against this kind of plunge in stocks or bonds or whatever. Gold is a hedge, it’s diversification. The price of gold can plunge, but hopefully it doesn’t plunge at the same time that your other assets plunge. That’s diversification. Hedges and diversification have a cost. And sometimes they don’t work. But that’s the role of gold for investors. As soon as people think it’s something else, such as an income-producing asset, or something that will make them rich, or whatever, they’re speculators in no man’s land.

“Three years later, the Nasdaq was down 78%, and the S&P 500 was down 50%.”

So what I am inferring is:

1. If stocks go cuckoo (crazy P/E), Gold is good hedge.

2. Fed intervened multiple times to save stocks by printing money. Without these interventions, Gold would outperform Nasdaq by much bigger amount even when its not an investment. That really says something about our economy.

That’s the best gold summary I’ve ever read.

+1

“S&P 500 Index went up “3.2” times from 1394 to 4505”

This ignores distributions (dividend and capital gain payouts).

The S&P has returned approximately 11% over the last 20 years (taking into account distributions).

(1.11)²⁰ = 8.06

Even at 10%….

(1.10)²⁰ = 6.73

Considerably more than 3.2 times.

When a mutual fund pays out a distribution (dividend or capital gain) its share price is decreased by the per share payout amount (hence terminology “ex dividend date”).

So if a fund had a NAV (net asset value) of

20.00 start of the year and finished the year at 22.00, its return is more than 10% if it had any distribution during the year.

I believe this also happens with the S&P (daily modified per S&P company distributions ? Not sure, perhaps some other timeframe for updates. Its explained somewhere on the web, came across detailed explanation a year or so ago).

By my calculations, gold in US dollars has returned an approximately 7.5 percent compounded rate of return the past 25 years. I tried not to cherry pick lows and highs. I am not an accountant, so Wolf my have a different result if he weighs in on the subject.

1970 is a better starting point. The S&P 500 and NASDAQ indices started with base values of 100, while Nixon ended the convertibility between gold & USD (previously fixed at $35/ounce.)

Since then, the S&P 500 index has risen 45X (+4400% return)

Gold has risen 55X (+5400% return.)

Gold is a far superior investment compared to stocks, right?

But the problem is gold doesn’t pay dividends. If you reinvested all S&P 500 dividends since 1970, the total return is approximately +21,500%.

Redo your calculation back to 1900.

Gold was $20 per oz in 1900.

Gold was $35 per oz in 1969.

Thanks

You can calculate returns on stock index with considering dividends.

Stock index massively outperformed Goldand and is the true picture.

Gold bugs miss this.

Hi Jackson,

See my comment… agrees with yours with some further detail.

Currently being moderated.

As an example:

S&P index close 12/31/2020: 3756.07

S&P index close 12/31/2021: 4766.18

Index gain:

100 * (4766.18 – 3756.07) / 3756.07 =

26.89%

Including distributions the S&P

total return was 28.71% (reported 2 places,

28.75% one other place).

So we see that about 1.82% of the S&P total return was due to distribution payouts.

The. ASIC problem with the reinvestment hypothesis is that unless you own a mutual fund that mimics the exact S & P performance your numbers fail.

It also ignores fund fees and taxes which have to be paid on most investments.

Why compare the dollar to other fiat currencies that happen to be depreciating faster than the dollar? In terms of purchasing power, the dollar has been weaker every year save a short time in 2008-2009.

Americans don’t typically trade euro or yen but have or pay rent, buy food and gas with a weaker dollar.

Well, most of that stuff is covered in Wolf’s numerous and excellent articles on housing, labour and inflation. I’m sure some Americans take interest in world affairs beyond their borders, while other Wolfstreet readers, like me, are not Americans at all.

I love it the MEXICAN Peso is now 17:1

2 years ago it was 25:1

talk about corrupt govt winning

During the early 20th century, the peso was on par with the dollar. Silver pesos were about the same weight as silver dollars. Then came the base metal and “trust me” coinage.

U are right Seba,,, at least for this old and elderly one:

I at least TRY to read at least six or more news sources from ”around the world” daily because of reading WS constantly,,, as in, Wolf does the work to send me to regard as much as possible, the WORLD influences on our USA finance and money, eh?

Please give us, in this case the WS us, the best reporting of YOUR local situation,,, IMHO the very best use of WWW.

Thank you

The value of other countries is important to monitor for a number of reasons,

The less the value of the dollar vs other countries , the more imported goods cost

The less the value of the dollar , the less likely foreign buyers will be to purchase our debt.

The more the dollar is worth , the more expensive it is for foreign governments, private banks and individuals to pay back debt denominated in dollars. Thus can an international financial crisis .

I think you have to compare long term gold vs. t-bills not dollar as in cash. Over long term t-bills have roughly kept up with inflation. Zirp was a temporary exception.

T-bills and gold have different purposes in your portfolio. T-bills are interest paying dollars and its all Buffet uses as systemic risk reduction. Gold has no counter party risk, but has risk of theft if you hold it.

Would that comparison deduct income tax on the interest t-bills pay? Guessing not.

DM…. BECAUSE WE LIVE IN A CONNECTED WORLD & what happens in VEGAS does NOT stay in VEGAS! As Wolf explained in this post…the repercussions outside the US are amplified especially in Emerging Markets

and we are still the world’s reserve currency!

Wolf, you point out Mexico didnt do QE. What countries have? I thought it was the Fed, BoE, ECB. Did Australia, Canada, others do it? It would be interesting to see a chart of the countries that did and the amounts over time to compare the who, what and when of QE.

Yes, Japan, Australia, Canada (I covered their balance sheet here a lot), New Zealand, Switzerland, Sweden… a bunch of European countries that have their own currencies.

The Swiss National Bank was the biggest QE hog when compared to the size of the economy.

Yes and their CB not only did the most, they bought US equities with their printed money.

Of course, there were accolades galore.

Just an observation, but it seems that the countries that didn’t do QE have no inflation, and the ones that did have inflation.

The whole world experienced massive inflation last year, but that was primarily because of the supply chain disruptions worldwide following COVID19. Coupled with that, in the USA in particular, both the Trump and Biden administrations printed money and put it directly in the pockets of the population. This had the effect of shifting traditional spending patterns into products in which the world didn’t have adequate production capacity. Those were the two things that finally lit the fire, forcing the Fed to move towards QT.

That’s clearly not true.

If inflation were caused by temporary supply chain disruptions, prices would have come down as supply chains normalized. That did not happen.

The inflation is clearly caused by the monumental increases in the money supply.

There days, you shouldn’t readily believe what you hear from politicians. The are spouting narratives to avoid responsibility for inflation.

For us that live on the border between Mexico and the US (El Paso-Juárez) the appreciation of the peso has been a pain, we used to be able to cross the border and visit the doctor, dentist, heck even get groceries and other things from the Mexican side and be able to save plenty of money, now crossing the border for such things has become less attractive. At the same time, I can see more people from the mexican side crossing over and spending more money due to this.

Wolf, have you noticed that some YouTubers have been using your website and analysis to create content? RJ Talks is one of those.

More accurately: the depreciation of the dollar due to thieving liars at the Fed has been a pain.

1) The dollar made a round trip to Mar 2015 high. It might further drop to

Feb/May 2004, 84.5/92.3.

2) DXY 1M : BB : July 1982 hi/lo, 121/116. The BB stopped 2000, 2001 and 2002 highs. The BB was followed by a buying climax and the response : 126/115.

3) Sept 2022 high was : 114.78 < 115 the response.

Wolf,

2 Qs:

1) Thoughts on the expanding labor strikes (UPS, Hollywood, UAW)? This might be the beginning of widespread labor unrest, a la 1970s.

2) What happens if Japan changes course and drops interest rate repression? Are we going to see a ton of money flow out of US stocks and bonds back to Japan (finally getting us the correction in asset prices everyone on this site other than the ZIRP advocates are looking for)?

#1. I don’t see that. Currently, the strikes are important issues for this particular industry, but the numbers are small. I don’t see a lot of labor unrest in the US. If you get a national strike by the airlines unions that shut down air traffic over Independence Day, well then you know you’ve got a problem; or a teachers’ strike in a big school district… there are some dockworkers now striking, but wait till you get a strike that paralyzes the railroads nationwide. Union membership keeps dropping from record low to record low.

#2. If Japan changes its monetary policy, it will be in very small steps. This will cause some upheaval of a few days in exchange rates and JGB yields, but I don’t think it will change global money flows. They’re going to move very slowly.

#1 UAW and Teamsters are talking tough so far. I know that’s standard negotiation, but it seems different. I think there’s a lot of anger about working through a pandemic while corporate profits were sky high. The problem is that profits are coming back to earth, so there might be a disconnect that I think might lead to at least one more major strike (in addition to the 160k actors and writers). If UPS and the US auto industries both face prolonged shutdowns, that could trigger the recession everyone has been talking about. Incidentally, labor could cost their Democrat allies in 2024 if so. Lot of ifs, but I think many workers are itching for a fight and feel emboldened by how tight the labor market is.

Seems to me Ford is in trouble financially again ,always bad management.Maybe Ivy League schools and there country club buddies are idiots ,lived on the silver spoon .

Labor needs to find out ASAP, along with all the minorities, , left wing IS and HAS BEEN playing them for suckers,,, FOR EVA…

Otherwise, minorities continue to be ”marginalized” as has been the intent of liberals who are focused on continuing employment of ”providers for, etc.”

And very clearly do not care at all about homeless, etc., because providers lose their jobs if homeless, etc., go away.

Hard core, AKA tough love,,, far shore, but been the case since for eva,, or at least since I was on welfare in mid 1970s.

I think in 1997 UPS went on strike for 15 days and that was before we had plenty of options for shipping as we do now. Just like in the pandemic UPS strike would hurt the internet buying but plenty of options for shopping at storefronts

Does the amount of ZIRP and NIRP sovereign debt held by BOJ impede or prevent Japan from raising rates? Or is it that they could raise rates, but they just want to inflate away their debt burden?

If the BoJ were to increase interest rates, the Yen will rally and the stock market will drop. I mean it’s clear that market participants have been borrowing Yen to finance their speculation. It will be like a bomb, but there’s no way that’s going to happen, and that’s good for me somewhat because I am heading to Japan in less than 3 months time.

Nice! Going to Canada soon and hoping the usd can bounce vs cad before it drops lower.

Maybe the Fed can give it a little bit of a lift but after falling through 100 it looks to be headed to the lower end of the last ten year range.

A trip down to the low 90’s won’t help commodity prices or CPI

Early innings of this massacre

Time will tell

You’ll find Canada expensive, because we’re taxed to death and most sectors have barely any competition.

Don’t feel bad.

https://paradigmlife.net/ready-to-get-depressed-how-many-different-taxes-do-i-pay/

What aren’t you able to do financially because of taxes? Because I’ll tell you a bunch you can’t do without taxes.

Yes exactly this. The yen will snap back hard, all the -extreme- Japanese external savings eventually buy back to yen one way or another, leaving aside eventually they have to drop the yen slide.

Plus there are deflationary forces there still in housing, I saw one place in Sapporo (admittedly needed work) with three bedrooms for 30,000 US.Those property prices only going down now.

But when?? Like all the banks the BOJ will lose control of inflation but when will they be forced to act. I doubt this year.

If, as is being projected increasingly now, the soft landers are gaining the upper hand, will a spike in inflation as indicated by you bring about a crash in EM assets as dollar weakness reverses sharply.

I will be very surprised if we get a soft landing. To me this is typical end of cycle narrative and with zirp for so long, fiscal spending running so high and with pandemic damage to economy, the odds of smooth landing seem slim.

Unemployment continues to be at record lows despite hikes in interest rates. Inflation is slowing.

Soft landing is approaching.

It was just as low in 2007 at the beginning of the GFC crash.

Also similar is how stocks are popping back to record highs one year after a dip.

Also similar is a rise in fed rate causing failures in real estate (commercial this time).

That’s because the full impact of rates hasn’t yet made its way through corporate America yet. Do you realize just how many people are employed by zombie corporations that don’t make money? What happens when their 2 or 3 year debt instruments mature and they have to refinance them at rates 5% higher?

“Unemployment continues to be at record lows… Inflation is slowing.”

Low unemployment is why inflation is *not* slowing. The recent CPI was only pulled down due to plunging energy prices and the health insurance adjustment.

Core CPI and services inflation are still well above the Fed’s target.

What landing?

I think it has been cancelled, according to Wall St.

In the air refueling so no landing at all?

In-the-air refuelling into a leaking tank.

Last news conference Powell said he expects next FOMC meeting to be live; distributing attention o

the whole committee instead of Powell. Federal Reserve governor Waller said that he expects a July rate rise and a following one this year. Don’t hear anymore word salad about transient, tools, data driven, won’t hesitate. Perhaps all the tens of millions of Americans whose lives are being ruined or on hold is getting to them. Don’t see cartoons anymore of money printing, it just isn’t funny now. Long story short plug that into a estimate of the strength of the dollar.

The benefactors of the greatest wealth transfer in US history continue to pour their unearned free money into all assets and durable goods, driving those prices into the stratosphere. It’s The United States of Let Them Eat Cake at this point. And they are also greedily jacking rents up on the have nots. A large portion of the working class, the young and the poor are absolutely miserable and hopeless. The asset holders are largely going through life with perma-grins on their smug faces.

Depth ….

You see the truth. Most people can’t face it .

If you start a web page/blog, I’ll be the first to subscribe .

Depth Charge: It’s not even a new story. Oligarchs eventually take over democracies and become the de facto State. Both the Greek and Roman experiments in democracy collapsed under the weight of a super rich Oligarchy. You want some nation or other to recover from debt, you wipe it off and start again with a ‘clean slate.’

Depth, there’s also a sense among these people that they’re brilliant investors. No humility at all. No “I got lucky being born before 1975 and being able to gain obscene wealth by being the beneficiary of reckless monetary policies.” It’s always “I invested in the U.S. economy and it’s done great.”

No, you didn’t invest in the U.S. economy. You invested in money printing, and it worked out for you.

There weren’t reckless polices before 75. When Reagan took office the accumulated DEBT of the US was one trillion.

The biggest factor the US had going for it in the fifties and sixties and well into the 70’s was being the only commercial power left standing after WWII.

Who are the competitors for US autos? A competition largely over btw. Germany and Japan. They weren’t until- mid sixties for Germany, later for Japan. Please note, auto buffs, I’m talking volume.

Here I’m switching to an aspect I know about in Canada, but I understand is similar or worse in the US. Back then the education system still functioned.

Nick, I agree with this. America’s 1950s and 1960s prosperity was an accident of history. That said, I’m not referring to monetary policies before 1975. I’m referring to the last 20 years, which has mostly benefited the older. Putting a little money “to work” in the S&P has caused enormous wealth gains to those people, and it wasn’t because of their brilliance, or because the U.S. has been growing in productivity.

“It was the best of times, it was ….”

Ending yet to be determined.

…the blurst of times?!”

The Govt with the Fed have stolen from the future to fluff the present.

The future they have stolen is that of the generations behind us older folk.

And that money has been used to “lock out” many of those in those generations from home ownership and reasonable purchases of other assets.

Their own future has been used to “steal it” FROM THEM, IMO, by the greedy ….and I have names!

Yes. Things take a long time to play out. But the effect of borrowing vast amounts of money – moving it from the future to the present – is becoming evident in the homelessness, drop in the standard of living, and hopelessness leading to drugs and despair.

I have been to many countries and you can taste either the joy and hope of improving economic conditions or the despair of economic depression and hunger. Sometimes in the same country at different times.

In the US it is masked by by obscene payments to the loud ones to suppress the cries of the shy ones.

It doesn’t have to be this way.

joe2, yes. I’ve talked to a lot of what you would call “common people” in the past year due to my job. They don’t feel rosy the way the media is portraying.

Let Us see the names.

Your exaggerations are getting more extreme.

Regarding the wealth conspiracy, I know someone who owns and rents a few mobile homes. He’s lower-middle class but inherited these dumpsters and is elated that he can increase rents. And, by the way, he only watches Fox news.

So your friend is movin on up in the world on penny increases in rent? Until zoning or environmental rules or getting sued takes care of that.

How is this anecdote a refutation of 1% owning 80% and 80% owning 1%?

Does he take a helicopter from his yacht for lunch like DiCaprio?

No. But if people worship DiCaprio and the whole galaxy of celebrities, and people shop at Walmart in spite of the catatonic workers and cheap Chinese crap throughout the store, and people can’t wait to hear the latest conspiracy from the likes of M. T. Greene, then don’t blame the .01%. At some point, the middle-class doofus has to look in the proverbial mirror.

I don’t disagree but you are missing the bigger picture.

Future generations have been robbed off the essentials of life.

But I don’t expect you to see beneath the superficial surface.

My wealthy friends are doing extremely well and are very happy with what is happening all around them.

Their stocks and real estate portfolio is going up and up.

What can go wrong.

The “future generation” that was launched from our home is doing just fine. Both of them made multiple financial/career mistakes along the way and recovered due to their own hard work and commitment. One got married and divorced in record time. They’re both now about to enter their 4th decade of life and have strong incomes, accumulated investments, one owns a home (second home – first one was a FHA crapbox and he refurbished it over a period of years). The current one, too, had “some assembly required” and is now valued @ $1M. The other sold her house to fund her career change.), plowing the money back into herself to advance her earning potential. And, no, they’re not an aberration. They have plenty of friends that are in similar stead. And, I wrote no checks that weren’t paid back. They did it on their own.

IMHO, the “future generations” that are presently struggling likely mirror those who struggled in any prior generation – mine included. Those that aren’t, likely mirror those who weren’t in previous generations.

The kids I grew up with in my ‘hood turned out all over the map. Some landed in jail. One died in the WTC. Others went BK. Some drifted from job to job and people lost contact with them. Others ended up with significant assets as business owners, landlords *gasp* in their 30’s. We all started in the same place. How did it happen that we all turned out so differently?

If you believe that you don’t have any opportunity, how hard will you work to prove yourself wrong? “So I’m gonna buy some weed, whine, and do nothing about it. See? I proved my point!”

The meme that all “future generations” are destroyed is a story that seemingly won’t die. Do you somehow think that all prior generations didn’t have people that were “destroyed” at some point in time? Inflation in the 70’s, 80’s, crazy mortgage rates in the early 80’s, housing collapse in the 1990’s, blown up portfolios in the dotcom collapse, lost retirement money in the GFC. The home my parents bought when I was hatched quadrupled in value by the time that I bought my first home at the ripe age of 23 (yes, we started adulting that early). Both were of similar size (1,100 square foot ranch on a concrete slab) with one three piece bath. Many of the harpy’s in the current “destroyed” generation wouldn’t buy either of those houses because they aren’t not good enough for them. They want the HGTV dream house and lament that those houses are $6-700K and anything less is a sh*thole. As a Hawaiian-Japanese friend of mine once said, “Brah… you thinkin’ WAY too big”.

And not all geezers were “brilliant” investors or beneficiaries of the time in which they were born. Some lost their butts. The one’s who (in my experience) fell into the latter category were those that started believing their own autobiographies, lived large, and blew their own brains out when things went pear shaped. Those that did manage to hang on often were conservative in their spending habits…. despite their ability to do otherwise.

Not likely. They keep close track on any emergent leaders and go to extreme lengths to eliminate them like Stalin did.

It will be the infighting that destroys them. If you are despicable enough to cause mass suffering to obtain power, you will not hesitate to stab competitors in the back. And you cannot stop, it is your nature scorpion.

May take some time tho.

There’s some truth to that, e.g. January 6. But it only works right now because the elite control the media. At some point, the common man will snap out of it. I just don’t know when.

You are one of the proper here who can truly see whats really happening.

BTW… my home insurance renewal in September just increased by 77 %.

Auto insurance increased by 50 percent last year .

Yeah inflation is going down

Pay off loans dump insurance ,become self insured

Did you bother to research why car insurance is skyrocketing? It’s because many of these new cars (specifically EV’s) are totaled, even in the most minor of accidents. These cars are not designed to be repaired. They’re designed to be thrown away. Rather than replacing a front fender for a few grand, they eat $60-70K and send it to a salvage auction so they don’t have to worry about the thing bursting into flames after the repair and assuming future liability for the shoddy repairs. It’s got nothing to do with “da Fed” nor inflation. It’s product design.

Homeowner’s? Depends on where you live. If you’re in CA, it’s fires, landslides (Palos Verde is a recent event) and replacement costs have skyrocketed. If you’re in FL, it’s fraud from roof replacement scams and hurricanes. The guy who brags about how he got the insurance company to eat a “loss” he participated in with an unscrupulous contractor is the one you should blame.

In FL, premiums are skyrocketing on homes without the hurricane clips and updated underlayments are seeing significant increases or having their policies CX’d outright. Some companies won’t insure a house in FL that’s older than 14 years unless the roof has been replaced (the realtor I’m working with to dispose of a property down here told me that little jewel this AM).

Some of the blame goes to the reinsurance companies that aren’t regulated the same way as a consumer insurance company is. They are raising rates…. and someone has to pay.

My auto insurance is downright cheap vs. what we were paying in CA. Why? Fewer uninsured drivers. Neither of “our fleet” of vehicles has an annual premium of over $1,000…. and all have full coverage – including glass replacement and $500 deductibles, comprehensive coverage with $50 deductible, and $500K liability (coupled with a $3M umbrella policy that costs about $400 per year).

Then there’s risk for crappy drivers who simply cannot bear the though of not checking their phone while driving a moving weapon, high theft, catalytic converter thefts, window smash and grabs…… It all adds up.

He has already appeared, but was foiled in his first attempt to overturn democracy (as was H itler).

I will never understand and the tin foil hatters. Why is it so attractive to some people?

St Louis Fed member Ballard, the only hawk on the Fed is retiring. Expect more loose money policies emerging in the very near future. July will be the last rate hike. The cowards on the Fed have no stomach for anything that will look like tightening. They are all politicians first and foremost.

Calling him a hawk is being generous. He was a supporter of this liquidity hose up until maybe a year ago.

He was a nonvoting member this year.

Swamp Creature,

Nah. Your logic went way off the rails.

1. There are only two voting doves on the FOMC this year, and both voted for all rate hikes so far. The rest have been hawks so far.

2. Bullard was non-voting in 2023 and in 2024, so he would have had no impact on the FOMC decisions.

3. He took a great job that he can do for the rest of his life: the inaugural dean of the Mitchell E. Daniels, Jr. School of Business at Purdue University, effective Aug. 15, 2023.

When money is printed out of nothing it must be worth nothing

As long as you can lay your taxes with it, money is worth something.

When printed money causes business owners to increase production to get that money in their pockets, that money is worth the increased production.

Why don’t you give me your worthless money?

I would get you rid of them for free.

Silly comment.

Not silly, but a translation issue. Rejigger the words, and you’ll see what Juliab meant.

It’s a joke I have made many times here when people tell me that the dollar is “worthless” or “toxic” or whatever.

Cheaper dollar is great for US companies overseas and abroad , specifically speaking for agricultural exporters and commodity trading foreigners countries will have more buying power, could set up another boom and inflation skyrocketing. Oh well plan for the worst and hope for the best. We only here on earth a short time to be so entrenched in the political satire of US economics. The rat race has given and inflation has taken away. If only QT could continue for 10 years.

If we want to regain a healthy economy, we need to export more than import, thus a “weak” dollar is GOOD. The media and experts who insist that we need a “strong” dollar are working for China.

More energy exports greatly benefits the USA and needs to accelerate. EV is becoming more acceptable and if low cost then export more oil and gas . We do need some cheap nuclear generation facilities .

If the Fed continues its slow tempo of interest rate hikes, won’t that help the strength of the dollar?

The dollar is “toast”.

The Canadian dollar?

Low interest rates on Japanese debt just means the yen is cheaper to finance. Japan owns all its own debt. And it doesn’t appear Japanese businesses are pushing out on the risk curve, which is where you end up with asset price inflation, which can (if allowed to) leak into other economic sectors. So, inflation remains a supply issue. And possibly in the U.S. a lack of regulation issue as well. IMO most of the U.S. problem is a lack of competent regulation. Hiking interest rates supports the currency because foreign investors will seek higher returns. The US dollar has one additional advantage. It’s reliable and always ready. That said, when the cat’s away the mice will play.

The Dow 1M flipped up in June. The Dow 1W flipped up this week.

If the Dow will pop DXY will drop.

The surest bet on Earth is still to short the U.S. dollar down to the 74 area on the dxy index and take half profits along the way. With the U.S. election next year interest rates will magically fall no matter what the inflation rate is.

Is that the way you are betting your money?

I hope not for your sake. Given everything the FED has said, the next interest rate moves will be higher, not lower. Higher interest rates will only lead to a stronger dollar, still the best store of value on this earth. There are reasons people around the globe hide dollars under their mattress.

The Dollar will just rally again when the Pivot Crowd and the “Inflation is Gone” crowd are proved wrong.

When inflation comes back this Fall/Winter (Oil/Energy) and the FED keeps hiking.. Dollar rallies

Only wrench would be a serious recession starting.

Would the FED cut or pause for Stagflation??? IDK

There’s a set of wrenches, not just one. That’s the problem with economic prognosticating. There’s, “If the FED… yadda”, “but then if… yadda, yadda,” and the beat goes on. One has about a 50% chance of getting it right.

Japan started all of these nuevo Central Banking schemes…

and if it blows up, it will they who ignite first.

One morning….on the news

Their rise in stocks is a result of just what the Fed did when they dropped rates….

INTENTIONALLY FORCING the investor to take more risk….get out of the currency and negative rates. A manipulation of risk return considerations by decree.

WOLF – as you mentioned, the FED’s QT has been weak/puny. Home prices have been bouncing higher since JAN 2023. In my market, this demand and low inventory of existing homes, seems much more than “seasonal”. Any thoughts on retracting/adjusting your call of home prices falling? Again, not homes sales, and not list prices, but actual sales prices. As a buyer, I am not seeing these prices come down at all. Thank you

If you really loon around then you’d realize that home prices won’t be allowed to fall neither any other assets.

This is by design by fed and govt to help wealthy

Don’t believe my bs.. just look around and look at the data.

Also look at what fed and govt is doing .

Don’t fall for what they are supposed to do or for their mandate or what they say.

Da’ Fed doesn’t give a rat’s patoot about your perceived “wealthy”. Nor do they give a rat’s patoot about you. Do you honestly think Jay Powell wakes up and considers who’s he’s going to hose on that day?

If you do, you have a high opinion of your self worth.

It’s greater good.

Wolf has most certainly not mentioned the FEDs QT as being weak/puny. You are making that up.

As for home prices and your anecdotal stories, why not look at actual data?

Home prices are again flirting with all time high.

You’d come to come in next month or two.

Lets revisit it after few months with soaring home prices

And your point is exactly what? It’s the housing market. Not your perceived “butt hurt” view of the world.

It’s a willing buyer and a willing seller. You’re in short pants? Learn to deal with it.

(PS: If you’re looking for sympathy you’ll find it in the dictionary between sh*t and syphilis.

El Katz,

I lived in Jersey for 3 years. You remind me of some…not all… the people from Jersey to Boston. Lots of gusto.

Like some of the info you share …really do… antidotes for instance… but wish it came in a more serene fashion.

And I’m quite the cynic but guess that isn’t relevant.

My comment applies to a lesser extent to Wolf as well.

Lived in TX for 11 years… they can have healthy egos too but it comes across less in your face. Less brash more wit.

Bush Jr. aside perhaps.

As for home prices… one of your posts indicates you did quite well with a home you owned and sold. Good.

Probably not a home in Peoria or Youngstown (40 miles from my hometown)…yea probably not.

I on the other hand lost 8% in 10 years. Not looking for sympathy or whatever… I like people to know that it can happen…yes after 10 years one can still lose $ in a house.

New home, 89k in 86, appraised 67k in late 89 or early 90, sold for 82.5k in 96.

Neighbor, an accountant, lost 23% in 3 years. Had to sell.

TX economy took a hit.

Lots of giddy homeowners these days like to brag on the internet.

I empathize instead with renters who haven’t gained from asset increases even though I have benefitted from it somewhat. Mostly in urban areas, large rent increases, they couldn’t afford to buy.

I left Seattle (outskirts) in 2000 for a cheaper city in NW. Roughly speaking have saved 180k to 200k in rent over 23 years. Lest some wise xxx chime in “idiot should have bought a home”…oh but I tried for 3 years (Eugene to numerous trips to Whatcom County… Bellingham Lynden Frrndale). At least one realtor (north of Lynnwood) kept me from owning a condo.

Had it inspected was ready to close but something happened….

Well I mostly believe that is true, 90% confidence level. Spare the details.

But I was picky too… hard to know how objective one is being.

But yes hard work certainly matters, brains too but luck does play a role in life for sure.

Very unlucky Syrians, Ukrainians, east Africans, Venezuelans, etc … no fault of their own terrible events.

If QT was indeed tightening, the U.S. $ would rise.

The dollar did rise a lot against many other currencies, including the EUR and JPY until late 2022. Then the ECB started tightening, including with large-scale QT, and the EUR rose again against other currencies, and the euro-dollar relationship returned to normal. This is what the ECB has done in QT and the euro has responded, just like the USD responded to the Fed’s QT. But when both central banks do QT, the currency relationship goes back into balance:

I think the normal exchange rate of the euro to the dollar is 1/1.2. At least it was when there was no QE and interest rate suppression

re: “until late 2022”

Money flows, proxy for inflation, underweights Vt:

2/1/2022 2.005

3/1/2022 1.639

4/1/2022 1.384

5/1/2022 1.317

6/1/2022 1.226

7/1/2022 1.188

8/1/2022 1.269

9/1/2022 1.131

10/1/2022 1.086

11/1/2022 0.840

12/1/2022 0.525

1/1/2023 0.498

2/1/2023 0.429

3/1/2023 0.354

4/1/2023 0.306

5/1/2023 0.249

6/1/2023 0.198

Wolf, this is the timeframe I would like you to use when presenting the Fed’s assets as well – not starting with the Pandemic. You jump around on that, but what really matters is the bloat since 2008 and the charts look much different depending on which start date you use.

Cookdoggie

1. “What really matters” is that you look at the charts in my Fed articles before you post this stupid BS. You are not even LOOKING at the Fed articles or else you’d know that I show the long view going back to 2007 — in addition to, and often with focus on, the detail view so you know what’s going on in recent months. Most recently:

Long view 1st chart at the top – day before yesterday:

https://wolfstreet.com/2023/07/14/the-feds-liabilities-qt-pushed-down-reserves-rrps-by-865-billion-tga-gets-refilled-currency-in-circulation-hits-record/

Long view 2nd chart near the top, 10 days ago:

https://wolfstreet.com/2023/07/06/feds-balance-sheet-drops-667-billion-from-peak-to-8-3-trillion-below-aug-2021-as-qt-continues-bank-panic-support-unwinds/

2. “What really matters” is what the Fed has been doing recently. History doesn’t change. If you look at a chart I posted three years ago, the early parts are the same. The events of 2008 aren’t going to change the market tomorrow.

3. “What really matters” is that this is my site, and I decide “what really matters” every day which is perhaps the hardest and most crucial part of my job, and I choose my topics on that basis, and what data I present, and how I present it.

“Honey, the Dollar’s Collapsing Again”

I do not see anyone out there crazy enough to want their currency to be the global reserve. Hence, that maybe the wrong question.

Earlier this year, it was reported the share of US dollar in global trade went below 60% for the first time (59%, EU 19% – ?). The global south have in recent times been making their desire very clear. To have other “OPTIONS” in their global trading. Perhaps, the more proper question maybe, What happens when the share of US dollar in global trading goes below 55% or even 50%? What happens when some of those treasuries and dollars from foreign countries come back home!

From a domestic U.S. view? Nothing.

When I look at the first graph, I wonder if dollar is going to crash similar to 2001-2008 as the tech bubble burst, assuming it will.

I’ve never bought into central bank currency intervention, which today is for the main purpose of evading hard decisions that should be made, as well as building moats for a privileged class of asset holders.

It makes you wonder if money printing and forced inflation is a symptom of a larger problem, which is an over influence of wealth that suppressed equal opportunity and competition.

There is equal opportunity. Just not equal outcome.

Managing your money is a full time job. Playing video games need not apply.

The US Dollar has been remarkably steady over the past few decades and will be remarkably stable over the coming decades. No other currency can even come close to challenging the US Dollar for global transactions and stability and that will continue to be case throughout this century.

Commodity-based currencies backed by gold will take over. That process will take some time, but will prevail. Essentially all balance of trade will follow this path.

You should consider accumulating 15% of your assets in physical gold in your possession.

You are welcome.

Commodity based currency is a pipe dream people are dreaming about

This would never happen

Mike R:

Hahahahahaha!

I’ve been listening to the gold bugs for years. I stopped seriously considering their opinion somewhere about 1982. Why? I’ve done better elsewhere. I still have the gold doubloons I bought – but I won’t buy any more. Just like I won’t buy any more scrap silver coins. It’s a waste of time.

Amen!!!

If I was going to be randomly dropped somewhere on this earth, there is literally no other currency I would want in my wallet.

As someone who has traveled fairly extensively for both pleasure and for work, there is no other currency which is accepted unconditionally worldwide.

In almost every 3rd world country you can easily find someone who will gladly provide 8+ hours of hard labor for a single $100 bill.

No other currency can provide the same.

The U.S. dollar is stable? LOLOLOL!

No it’s not. But it’s more stable than the alternatives.

LOLOLOLOLOL!!!!!

(PS: Let’s see you buy a bottle of Coke with your gold coins. Hahahahaha. Or is it LOLOLOLOL

It is pretty bad when the Bank of Mexico has a better feel for what the Fed will do next than all of the “Masters of the Universe” on Wall Street.

Wall Street has a much better feel for what fed would do next.

Wall Street knows for whom the fed works and now every one relevant has declared inflation is going down big time

It does not matter what you wolf or I think about inflation

What matters is what govt and fed think about inflation

Fes has already paused and showed dovish color.

Govt is on non stop spending binge on borrowed money .

Always a good time for wealthy.

Jon:

Please define “wealthy”. Is that someone that has more than you or?

The stench of the system is now too strong to ignore. A monetary system that prints money to artificially support asset prices. A tax system that allows the wealthiest to avoid taxes and evade enforcement. An antitrust system that allows for ridiculous consolidation of network control and profit. A political system that completely relies on support from billionnaire donors. Runaway wealth concentration and asset inflation, supported by formal mandates. Regular bailouts of speculative interests, at the expense of prudent decision makers.

Good grief! Is there anything not rigged in favor of existing wealth holders?

Yep the PPE pandemic employee payroll relief was 28 billion mailed out to business owners and asset owners while subsidies on the SNAP program dropped (food stamps) not that I’m for large food stamp programs either . But btm line more stimulus available for services

You nailed it Mr Bobber!

He didn’t nail squat.

The main issue is the lack of law enforcement. Think about Richard Nixon vs…… Laws for thee, but not for me.

And you voted for it and/or continue to support it. Otherwise, you’d be in the streets. Just a bunch of paper tigers. Keyboard warriors. Yee haw.

We need a counter revolution

I find it hilarious when people start posting the Fed will save asset prices. The widow across the street has cut her sale price by 8%, and now is 10% below the exact same house that sold next door early last year. From 760 to 710, and the neighbor has sold for 805k. Bring on the pain baby, now $250 per sq ft. Needs some TLC, but really good bones. Ha. Her realtor was pretty bad as well. Told her get a real one after the listing expires next month. Simply amazing.

Houses that need updating will take a bigger bath with the new higher costs of improvement. Now we have a real market again, and all those empty houses will now have a real carrying cost again.

Meanwhile, the Airbnb disaster continues to unfold…

Yep. Just because a house is next to another house doesn’t mean it’s worth the same. Only an idiot would make that assumption.

To wit: House across the street from where I am sitting sold for $1.8M a few months ago. Do I think this place is worth that much? No.

Things are only worth what someone is willing to pay for it. Not a scintilla more.

I appreciate your push back against all the click-bait headlines. The commercial incentives in almost all “information sources” in the West means we will always get highly colored stories posing as information.

I think your message generally is: “the sky is not falling…for now”

However, what does it all mean? Clearly the federal government cannot sustain interests payments of 900 billion or a trillion USD/year. The answer for some period of time can be that the interest can just be converted to new debt. But for how long ?

The rest of the world can be fooled into taking USD paper in exchange for their commodities and goods. In the perspective of a single person, the time that can continue seems like a long time. But in history 100 years appears to be the natural tick of the clock.

The great rule of events like this seems to be: “slowly at first and then all at once”. It would be delightful for us to hope that we are still living in the “slowly at first” part of the curve.

I’m thinking 2023 and 2024 will be ok, but the strain on the system will start demanding relief in 2025.

“The rest of the world can be fooled into taking USD paper in exchange for their commodities and goods”

Don’t you think it is pretty arrogant to think you know more than “the rest of the world”?

Do you really think billions of people are taking the USD because they are fooled and only you can see it?

JimL,

Anybody with a brain knows the US is headed for financial disaster, but few in the financial media admit it, because they are too busy profiting from it. They must pretend there are no problems and the status quo is sustainable.

I think Jerome Powell and Yellen know it too, and they are pretenders as well.

Why not divest yourself of any dollar based assets? If you’re so pessimistic it would benefit you to invest in pazoozas…. I think it was the currency in Rocky and Bullwinke’s fracture fairy tales.

Sometimes the smartest people make the most stupid mistakes.

Don’t give too much credit to people’s intelligent.

Fed hires 100s of economic phds from top schools

Yes they had been parroting transitory inflation for quite some time

May be it was on purpose ?

Howdy Folks, Higher for longer, pivot, soft landing, take yourn pick. Lots of things will happen in the next decade. None of US will have the answer for a long long time……..Meaning, this lady aint gonna start singing for a long long time.

About the last thing the Fed needs. Inflation is after all depreciation of the currency … when it declines in real time against foreign currencies, stocks, bonds & commodities, that’s the leading edge of another impulse going into the pipeline where it eventually emerges as a decline against consumer goods and services.

The DXY (US Dollar Index) is just a tiny fraction below 100 and closed on Friday, June 14, 2023 at 99.96 which is excellent and well-balanced.

The BART subway/train system in the SF Bay Area is an example of how high fixed costs and declining ridership creates a “doom loop”–a “doom loop” that hollows out downtown office towers and the small businesses that depend on thousands of commuting office workers, and the transit systems that bring the workers to the office towers.

BART ridership has fallen precipitously, from 400,000 riders a day pre-lockdown to 166,000 today. This 60% decline in rider-paid revenue is far below the system’s fixed costs, and so somebody somewhere has to be taxed more to subsidize the system.

But in the high-wage, high-cost Silicon Valley counties, the decline in wages is staggering:

San Francisco: -22.6%

San Mateo: -20.7%

Santa Clara: -15.0%

High-cost states suffered significant wage declines:

California: -6.9%

New York: -5.1%

15% to 20% declines in wages paid are absolutely monumental. They add up to billions of dollars that are no longer available to pay taxes or fund city-centric “pleasures.”

Who’s going to be left who is willing and able to pay much higher taxes and fees to pay the sky-high legacy costs built up during the glorious 30 years of urban expansion fueled by speculative bubbles?

In terms of wages, you picked up some context-less garbage (I deleted the links).

Wages in the SF Bay area had experienced a HUGE bubble during the pandemic, and they’re coming down from that bubble and are returning to trend. Everyone knows that.

Yes, BART rider ship plunged during the pandemic, and has recovered some but is still about 60% of the pre-pandemic levels, which is not a sustainable level of ridership.

But employment is now higher than it was at the peak before the pandemic with 2.527 million employees now, up from 2.522 million at the peak before the pandemic in the San Francisco-Oakland-Hayward metro. Contrasted with Bart ridership, it shows you the effects of working from home and additional driving.

Ridership is down because: 1. The Bay Area is the epicenter of working from home (employment now exceeds pre-pandemic peak); and 2. since roads seems to be still less crowded than before, it’s easier to drive to the office 2-3 times a week, and people seem to be doing that. Here’s the Bart ridership:

Thanks for the details I appreciate all the facts and probably are missing more but I don’t know what . An assessment of Mtg size and potential leverage issue if HELOC is still driving the spending would be helpful but I don’t know how to retrieve that data . Employment and wages nationwide are holding steady

Information has become increasingly difficult to obtain or maybe that’s always been the case. For sure news print would only print the stories they wanted out for decades or centuries. Now we at least have more avenues for information

Hey Wolf, what are your thoughts on rents. I think they are going down due to all the multi family supply. Am I misguided?

Going up this year. They went down a little late last year. Landlords are in no mood to cut rents, neither multifam nor SFR.

Over at ZooH they are always yapping about the US$ being replaced by consortium of the BRICS issuing a gold- backed currency. Funny thing about this is that only one that is a major economic power is China. And it looks like it is going to need a major stimulus as deflation approaches its colossal RE sector. It will not do this by issuing paper convertible to gold.

Russia is an economic basket case, at least compared to where the first power in space could be now. Its economy is the size of Canada’s, but supporting 140 million people. So mathematically, other things being equal, there should have been many more Canadians than Russians bidding up London RE.

We speak the language, sort of.

Its gold hoard? The public, private citizens of a real economy, Germany, own more gold than the Russian central bank.

Is India the next super- power now it has largest population? Its manufacture exports are tied with Vietnam. Be interesting to know the amount of its remittances, the money sent home by Indians working abroad. To add irony, all recent Indian governments, but especially Modi’s have a special hate of gold or at least personal gold. It just had a major gov ad campaign urging citizens to be patriotic and sell their gold to the gov. For rupees.

South Africa? This could get ugly. One test of an economy is the electrical grid: most businesses other than the street vendors etc. require a standby generator.

Brazil like Argentina is saved by its ag sector, huge in soybeans, has had problems with drought, recently a lot of political upheaval. But I’d rather be there than Russia.

Instead of issuing a currency ‘backed’ by gold, but not convertible to gold, the group should issue a new digital coin: the BRICS coin.

Brice is a joke ,they’re going to have a consortium of countries combined to ge a financial powerhouse ,will never work for long. Just like people countries all have their own agenda. Unless China and Russia keep them in line ,not good

Argentina, Egypt, Indonesia, the UAE, Saudi Arabia, Algeria, Bangladesh, and Iran are all interested in joining the BRICS group of countries. It might take China and Russia combined all their time to manage that bunch. The gold-backed currency is intergovernmental trade use only and may be 40% backing, not a significant innovation, if I read it right. It’ll end up being paper gold anyway. Basel III was supposed to be a big deal too. It’s a nicer world in general when gold is boring, and numismatic gold is a little more affordable then as well.

I think I have figured out BRICS,not a gold backed currency but a OIL backed currency . Kicking USA in the nuts

Flea,

You’re funny. Just a reminder: the US is the largest petroleum and petroleum products producer and the largest natural gas producer in the world. And the US is a net exporter of both. And the US petrochemical industry is the largest in the world…. Aside from the silliness of your suggestion of an “oil backed currency,” why would it kick the USA in the nuts, LOL?

Can anyone explain why homeowners insurance in Florida is going up 25% or more in one year? There were hardly any hurricane losses last year. I live in Maryland. Mine went up 300% between 2020 and 2022. No hurricanes or tornados or major flood losses here. No claims filed. I asked my insurance representative why the big increases and he lied right to my face, blaming the Maryland Insurance commission. I cancelled my policy with them and went with another company for half the price.