Spooked by relentlessly raging inflation in services, ECB puts QT into higher gear.

By Wolf Richter for WOLF STREET.

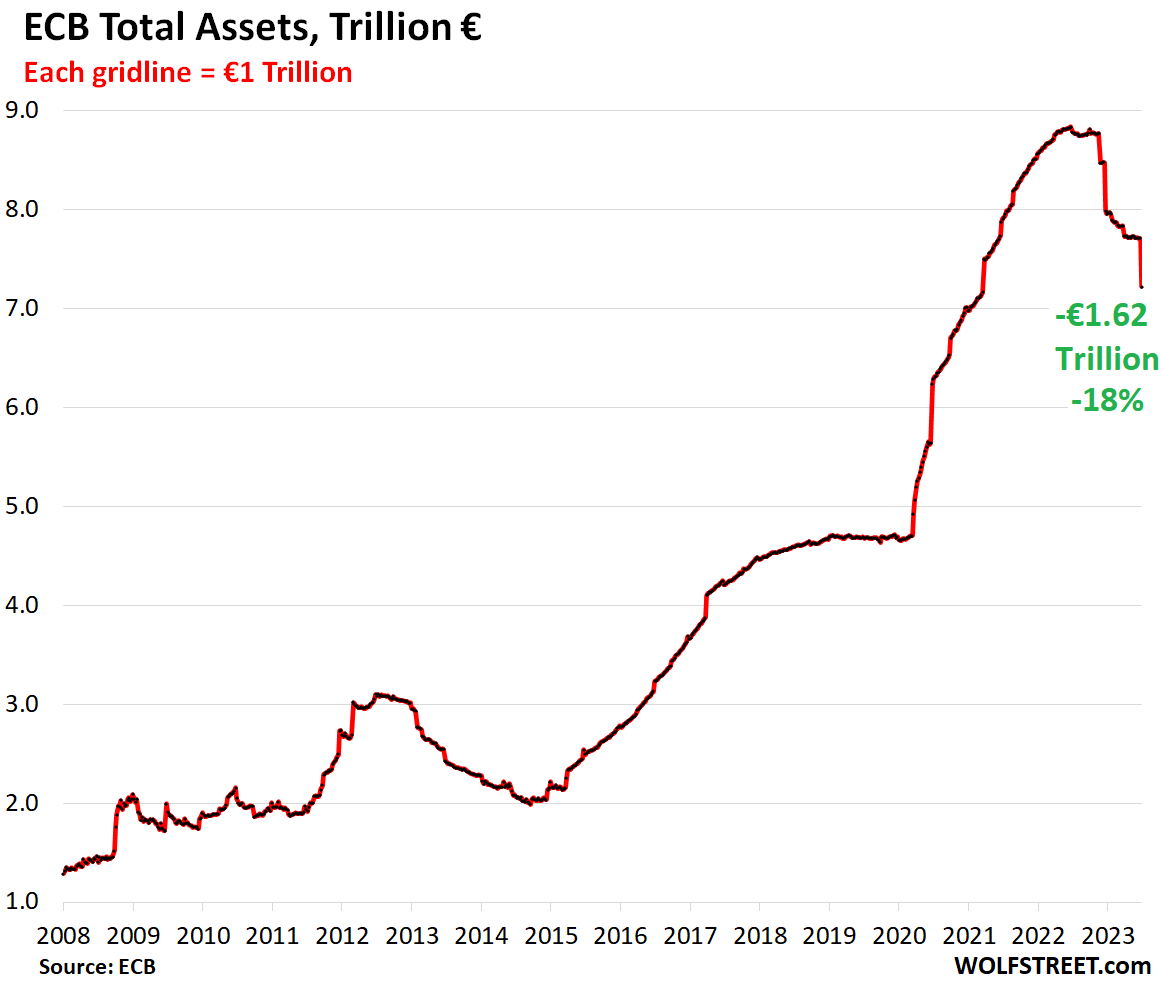

Total assets on the ECB’s balance sheet as of June 30, which was released today, have plunged by €1.62 trillion, or by 18%, from the peak in June last year, to €7.22 trillion, the lowest level since March 2021.

The ECB had two major types of QE that are now unwinding: It offered free loans under very favorable conditions to banks, ultimately handing banks €2.22 trillion in cash to deploy. And it handed €4.96 trillion in cash at the peak to the bond market by purchasing government bonds, corporate bonds, and asset-backed securities.

In October, the ECB announced the first steps of QT, when it made the loan terms unattractive which caused the banks to pay back those loans, thereby removing liquidity via the banks. It later announced the initial steps on unwinding its bond holdings, which started in March. Since then, the ECB has unloaded them at a faster rate than announced.

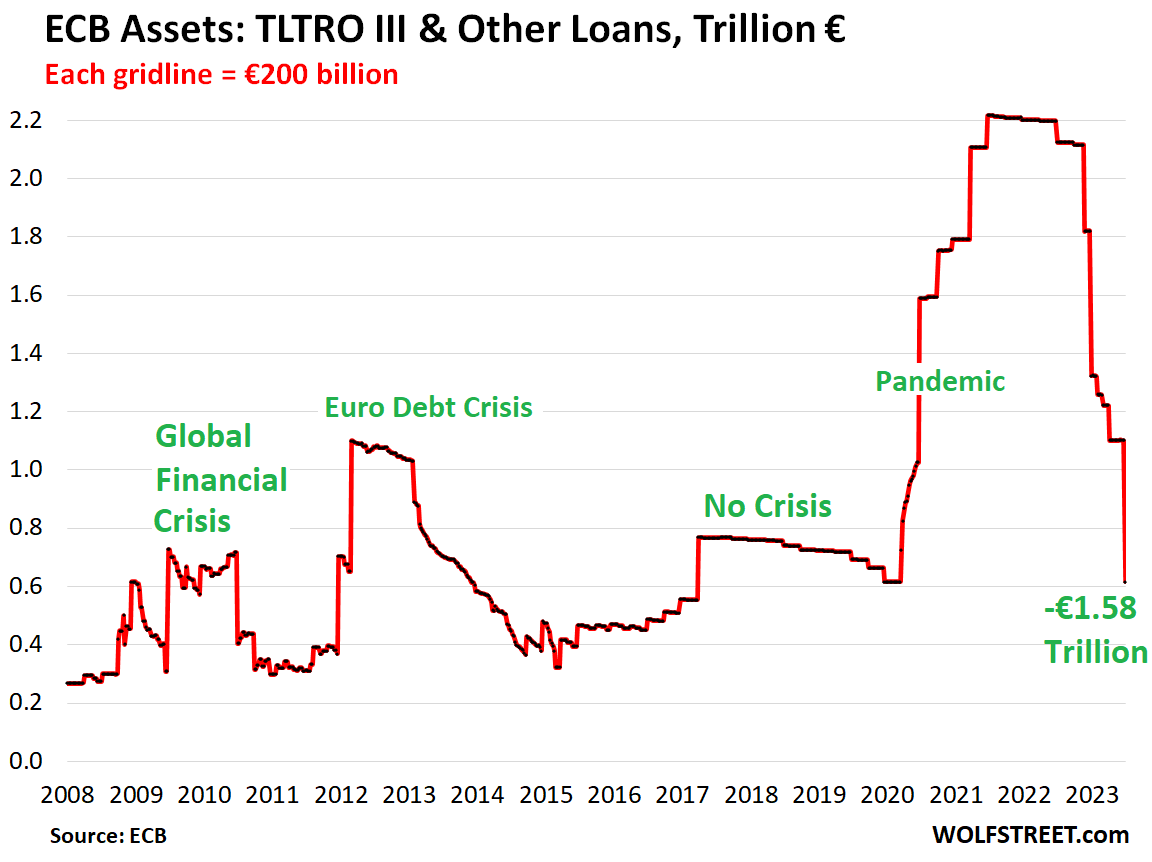

The pandemic-era loan QT unwound: -€1.58 trillion

The ECB has always handled QE via loans – various generations of Longer-Term Refinancing Operations – including during the Financial Crisis and the “whatever it takes” moment of the Euro Debt Crisis in 2012.

During the pandemic, the ECB further expanded these lending operations, called them Targeted Longer-Term Refinancing Operations (TLTRO III), and endowed them with complex incentives for banks. Banks took them and ran with them, to plow this money into whatever. These pandemic-era TLTRO III loans amounted to €1.6 trillion at the peak, which came on top of the still outstanding prior loans, to total at the peak €2.2 trillion.

The loans have dates at which they can be paid back. After the ECB made the loan terms unattractive last October, banks began to pay back those loans. On today’s balance sheet, which is as of June 30, banks paid back another €485 billion in loans, bringing the total reduction of loans to €1.58 trillion so far, with only €617 billion in loans outstanding.

The ECB has now unwound the entire pandemic-era loan pileup and is back at the level where the loan balance was before the pandemic:

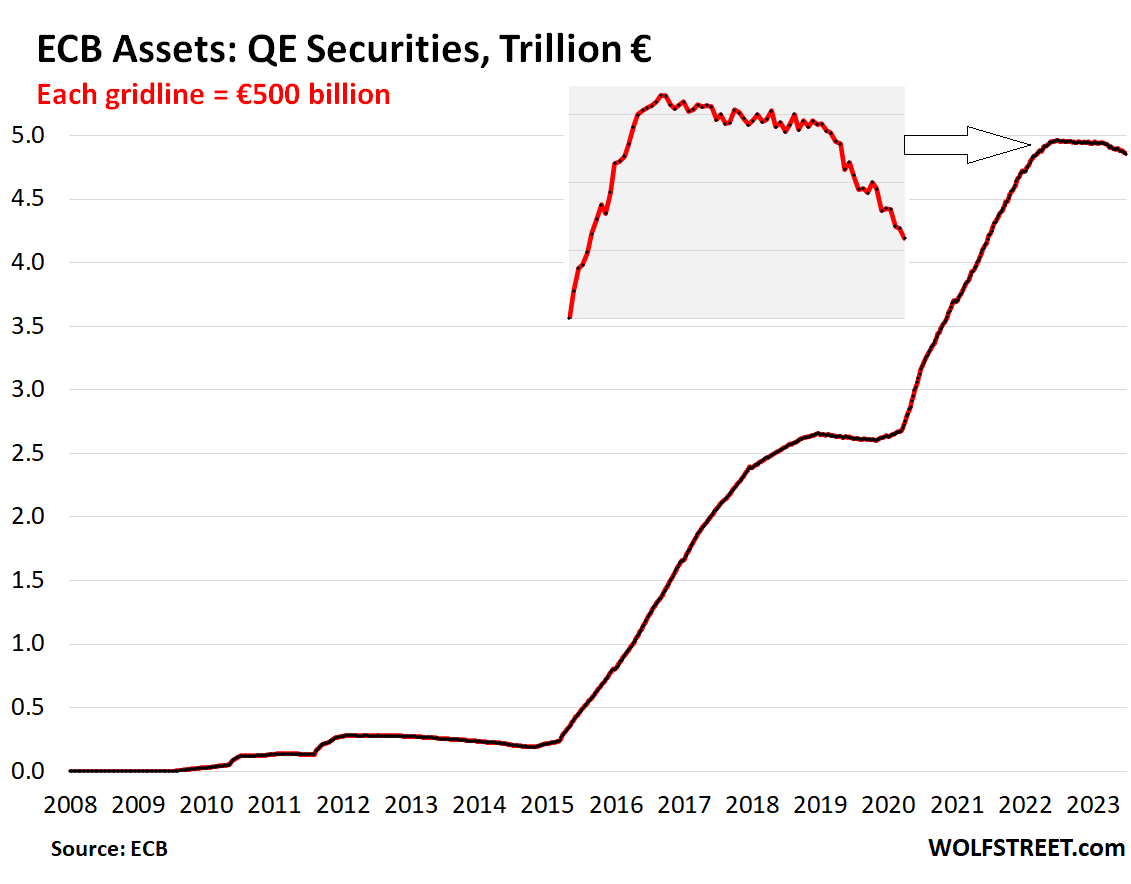

Bond QT faster than announced: -€105 billion

The ECB announced in December that it would let some of its bond holdings roll off, starting in March. It had bought bonds under two programs: APP (asset purchase programme), starting in 2014; and PEPP (pandemic emergency purchase programme), which started in March 2020.

The current roll-off concerns the APP bonds. It said it will maintain its PEPP bond holdings for now.

The APP roll-off was initially capped at €15 billion a month when it started in March through June. At the June meeting, it said that in July it would remove the €15 billion cap from the roll-off of the APP bonds and just let them roll off as they mature.

On the balance sheet released today, as of June 30, the balance of bond holdings was down by €105 billion from the peak a year ago.

The roll-off is proceeding faster than the €15 billion a month pace: Over the past four weeks, its bond holdings fell by €22 billion. Over the four months of bond QT since the beginning of March, its bond holdings fell by €84 billion, averaging €21 billion a month.

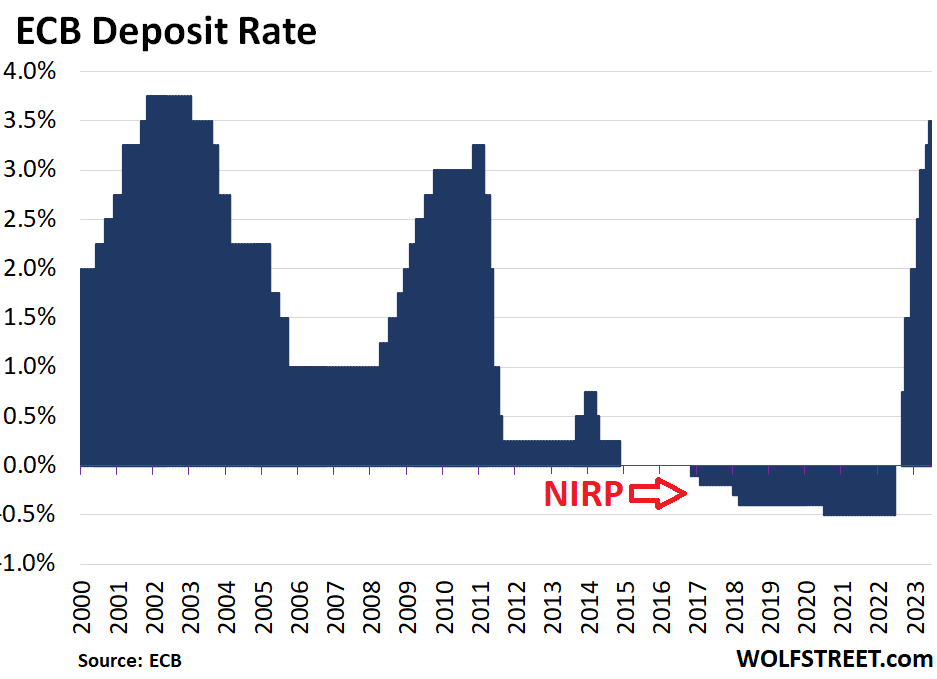

Rate hikes…

The ECB has hiked its policy rates by 4 percentage points in 12 months, bringing its Deposit Rate from -0.5% to +3.5%, the highest since 2003. More hikes are on the table:

Spooked by inflation in services…

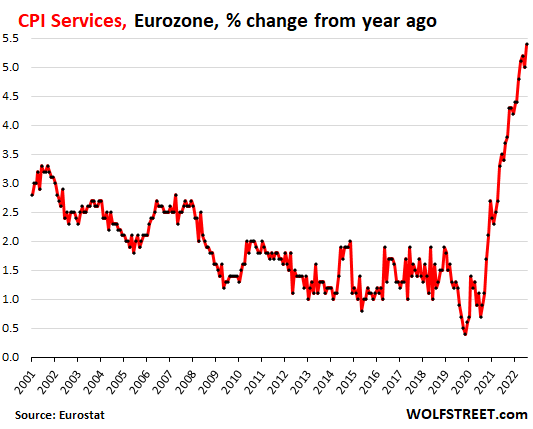

ECB president Christine Lagarde keeps hammering on inflation in services which continues to get worse relentlessly, though energy prices have plunged, red-hot food inflation has started to back off, inflation in goods has moderated, and the overall CPI for the Eurozone has cooled from 10% early this year to 5.5% in June.

But consumers spend the majority of their money on services, and the Eurozone CPI for services in June spiked to 5.4%. In services, inflation is hard to stamp out. This relentless inflation in services explains the continued rate hikes and the large-scale balance sheet reduction.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Seems like over leveraged economies are too unstable for central banks to successfully manage.

They were not overleveraged till central banks were given Powers to buy assets!

Never underestimate the capacity of these institutions to eff up and deny all accountability.

In the U.S., reserves requirements against interbank demand deposits were removed in 1965 for member banks.

“They were not overleveraged till central banks were given Powers to buy assets!”

Exactly the same as DC perpetually saying spending “has to” go up because of inflation.

The question that everybody wants to hear:

How much of PIGS QE has been rolled off?

Those charts look like a roller coaster. Bouncing from one crisis to the next.

How can these money printors keep the plates spinning with so little staff.

Jerome, please take note. You are way behind the curve and you just paused.

Not gonna happen. Problem with J Pow is not lack of observation.

The problem is to protect the fake values of assets (stocks, bonds, mbs, cmbs, RE, cryptos) that are used as collateral. The correction of value of these bloated assets will crash the financial system because there the balance sheets will be come unbalanced.

“The problem is to protect the fake values of assets (stocks, bonds, mbs, cmbs, RE, cryptos) that are used as collateral.”

Certainly the crux of the problem!

This is a global problem,when economies start to fall apart it will be worse than Great Depression,Warren warned about derivatives destroying the world long ago. Now errily silent . Not good

Definitive the problem, money is debt and assets are the collateral (backing) of debt (money). Crash the asset values and there goes the collateral (backing) of debt (money).

You took the words out of my mouth. The Fed is talking a good game while going weak in the knees. It just skipped a rate hike and its balance sheet is obese with MBS. Too much talk.

Also it keeps getting worse. Wallstreet keeps spinning up rallies (recent 30% rally on Nasdaq) daring Fed with a bigger correction. In response, a scared J Pow speaks some big words, but then instead of taking required action, he hides in a corner.

Probably going to go up another 30-40 % ,then biggest deflation in mankind’s history ,blackrock has to get assets for at least 50% off blue light sale ,

Yes. Powell is trying, like Volcker, to just let the economy burn itself out, to affect a “soft landing”.

The problem is that Powell doesn’t know money from mud pie. And even if Powell understood money, he wouldn’t get the distributed lag effect right.

He’s about to ‘unpause’ to use a word coined I think by WR.

Perhaps the ECB is rolling off the bonds faster knowing that locked in inflation (% multiplied by time duration) and higher overall interest rates will make the bonds have a higher loss than they have right now. Perhaps the ECB has to “mark to market” like other European banks?

According to a Barron’s website:

“…sun is shining on European banks. It may not last.”:

“European and U.K. regulators also require all banks to regularly mark to market their securities holdings. This arcane nuance has become critical, as the U.S. exempted houses with less than $250 billion in assets from the requirement in 2019.May 5, 2023.”

I think that the resolution of the obvious pain the market place is inflicting on the dumb bunny candidates. Probably Canadians, who routinely fleece anyone dumb enough to believe that they’re kinder and more empathetic than your average American lout,

Which it turns out, that they may be more aggressive toward off-the-wall concepts.

How nasty! Hey we won’t shoot you.

Personally, the change from the wacky monetary policy prescribed by the likes of Milton Friedman back to a world of Keynesian accounting standards, as flimsy as they are.

The drama in the financial markets are exactly what they seem. A synthetic charade of make believe.

dang

“the change from the wacky monetary policy prescribed by the likes of Milton Friedman”

I would be interested in a more precise detail of what you describe as a “wacky” Friedman monetary policy. Do you have one?

Friedman was “one dimensionally” confused.

“Friedman was “one dimensionally” confused.”

Lots of declarations about Friedman and not ONE example of where he was wrong or “wacky”

Lame.

Spencer,

Friedman believed in minimal governmental intervention in markets. It was his central tenet. An ethos we largely maintained outside of wars from the 1780’s until the 1930’s. Then we largely shifted to a Keynesian lite version. We never have once cut spending when economic growth recovered. And that’s the problem with Keynesian philosophy (much like communism) it looks great on paper but politicians crave power, influence, and it’s various trappings. It’s just never going to work with humans at the helm. It will always be a bastardized version of it.

And…there are relative degrees of “wackiness” too…

Dang,

1) First off, what is a Keynesian *accounting* standard? Keynesianism addresses itself to macroeconomics, not accounting.

2) Did you mean “accountability” Dang? In theory, Keynesianism demands government spending *reductions* at certain points in the cycle.

Read “New Confessions of an Economic Hitman” for a new perspective on Friedman. Not good.

so there is an opinion of a man who is no longer around to defend himself?

This article is very informative and shows the impact of the ECB’s bond roll-off on its balance sheet. I think the ECB is trying to normalize its monetary policy and reduce the risks of inflation and asset bubbles. However, I wonder how this will affect the eurozone economy and the recovery from the pandemic. Will the lower liquidity and higher interest rates hurt the growth and employment prospects? How will the markets react to the shrinking balance sheet? Will there be more volatility and uncertainty? These are some of the questions that I have after reading this article. Thank you for sharing it.

Thanks AI bot.

The component of the ECB’s assets I’m interested in is sovereign debt. As long as these various governments are running deficits, I remain skeptical.

Didn’t they have a QE/QT plan to sell German debt and buy Italian debt? There still seems to be a concern on sovereign interest rate spreads between their various countries. I think sovereign debt is what to keep an eye on.

They have a plan (a tool, as they call it) to keep the German-Italian spreads from blowing out. In other words, if the spreads start blowing out, they might replace maturing Italian bonds and not replace maturing German bonds, that kind of thing.

Just the fact that they announced this tool last fall has kept the spread from blowing out (jawboning).

The tool is the PEPP (1850 billions) you quoted at the beginning of the article. ECB stated it will stay at least until end-24.

It is becoming tricky – ECB need states to keep cool on deficits but politics or population are used to subsidization.

pop corn ready

Yes, Italy has always been the canary in the EU coalmine.

Italy has “exorbitant privilege” running ~10% fiscal gov deficits at a 3.5% rate!

Exact ! Heavily indebted state in eurozone with a wealthier population than germany asking for a bailout via supressed rates.

I think it’s interesting (pun intended) on how there’s almost no coverage of the individual countries debt issues. Italy, Spain, Turkey, etc.; the issues those countries had 10 years ago have not been addressed, just kicked down the road. inflation is going to make this problem a lot worse when the reckoning comes due.

European countries are starting to look at budget projections that show cuts in services and entitlements with an aim to cut sovereign debt. I just can’t see Congress doing that in the USA.

I guess the fed would love to see only 2-3% deficit (defense included). Plan like the IRA are stimulative which is a nonsense in a high inflation economy.

I think USA is the same than Europe : both population and politicians are now used to subsidization

(free money, NIRP) and it will be very painfull to change this mindset.

This thinking is already changing. Germany is in a technical recession and loans everywhere in Europe have fallen dramatically

Everyone talks about inflation. Is there a scenario that debt deflation comes along, not inflation?

Yes, absolutely.

I agree with SoCalBeachDude on this point. The question I have is what is the policy response if it happens. Will the Fed attempt reflation in the manner they did after 2008? Or will they let the defaults and bankruptcies happen and allow the system to purge the bad debt as investors absorb the losses? Some policy response will occur, but I’m not convinced they’ll return to ZIRP and QE unless the crisis is enormous.

They are all indebted but Turkey is a special case. It is not in the EU and not able to draw on the ECB.

It is almost if not actually broke, not in the sense of having no Turkish lira, in freefall anyway, but in fully convertible forex. Apparently some loan approvals are requiring a source of income other than lira.

Erdogan has very unconventional ideas about the economy. He goes thru central bankers almost yearly, especially when they tell him the best way to fight inflation, now over 40%, is to raise interest rates.

Normally this would be time to start talking to the IMF, the lender of last resort, but as even the UK found out, there will be conditions.

How Erdogan scraped in the last election while presiding over this mess is for a Turkey specialist to explain.

“QT into higher gear”

A welcome phrase …. and here’s hoping.

What difference would that make at all?

“What difference would that make at all?’

Well, the supply that the Fed “hid” from the market by purchasing and putting it on the balance sheet (about $4 Trillion) will return to the market place.

QT might mean more than rate talk going forward.

Any thoughts out there on $/Euro over next few years?

Or European stocks or bonds as medium-term investments for a US investor?

I’m glad that the ECB did not make the mistake of the Fed to throw money from a helicopter to every individual and presented these loans to the banks. So now it is ahead of the Fed by qt.

But all in all, it is still far behind with interest rate hikes.

Fed did the same thing as ECB. 4 trillion created and given to banks.

Plus this money to the banks, the US government sent checks to almost every American citizen. Fortunately, this did not happen in Europe

Easy reductions in ECB balance sheet being made. Optics only.

Long term and signficant reduction impossible. Same as in US.

Interest rates will stay about here for long time. Inflation will continue via wage demands but will come down with commodity price declines as the western economies go into deeper recession. Planned.

Deeper recession approved by Central Banks to put China, Russia and pals on their knees, economically. Particularly Russia. US will run deficits to keep the pitchforks out of the poor people’s hands.

The problem is that the base rate is ineffective against QE money. -IF- you have a corresponding debtor and creditor then increasing the base rate affects both, but QE essentially increases the base money supply i.e. its unencumbered.

I realise this article is about the ECB but they have seen the lesson of the UK, which is that you -cannot- unwind QE fast enough because in the case of the UK there is 400 billion outstanding. This means your levers to control inflation don’t work. The UK is now in a horrific debt trap I think.

That the ECB is tightening great but like the UK they don’t have the time. They have to reverse 8 years! of QE just to re-establish control. They do not have the time.

There are also lessons for Japan, which clearly (well imo) won’t be able to control inflation when it gets going.

Powell to be fair to him, after the thus far devaluation of the dollar, has brought USA inflation under control. My measure for this is the direction of the 10 year treasury yield. In the US its falling. In the UK going up, so interest rates not high enough. Its scary now for the UK if you look at debt servicing and government debt costs.

In the Eurozone there is also the different countries to consider so its a bit murkier unfortunately, but Italy depends on ECB easing. Inflation is going to be around for years.

Take another look at those yields. I suggest using core inflation measures, service inflation and inflation expectations to judge inflation.

Those 10 year treasuries just went up over 4%

Remember that inflation in Spain is already below 2 percent – 1.9% on an annual basis

But the dynamic in the eurozone is that the uncompetitive economies deflate with respect to the successful ones. Money is always leaving Spain for Germany and others, but really its how inflation in Germany is managed. For sure the incompatibilities of different rates is the famous problem and rates are probably damagingly high for Spain but there can’t be an inflationary spiral in Germany which is what the ECB has to manage.

That aside, core inflation (stripping out volatile prices) is at 6% anyway, way over target. You refer to the headline rate. This measure in Germany is trending UP still.

sorry to double post. I meant to say the core inflation in Spain is at 6% (trending down), way over target, while for Germany 6% trending up. The ECB is in no way on top of reaching their inflation target at their current base rate.

A lot of services are driven by wages and I think that is why we are on the services inflation hamster wheel. Might be tough to get off, but with interest rates as the main hammer it will be autos and residential construction that get hammered.

Seems like policy makers are nuts with estimated $50 Trillion capital investment required for net zero while governments are already hitting a wall on existing promises. Maybe tighter money will force governments to have to say no to something.

MW: 2-year US Treasury note yield hits highest level since 2006 after topping 5.100%

Is the previous 10% the raging amount or the 5.5 in June?

“Raging inflation in services,” it says in the subtitle.

If you go down all the way down to the last paragraph, it says this right above the chart of services inflation:

“But consumers spend the majority of their money on services, and the Eurozone CPI for services in June spiked to 5.4%. In services, inflation is hard to stamp out. This relentless inflation in services explains the continued rate hikes and the large-scale balance sheet reduction.

I would imagine that the lighter Central Bank balance sheets will come handy when it’s time to fund the re building of Ukraine and trillions that will have to be backstopped by the Central banks, for the private sector to rebuild

On day one of the war I said US would spend at least $1T. Fast forward I have alread heard rebuilding is estimated at over $1T and I think war materials are about $200B. As always I have under estimated government’s ability to spend OPM. My new estimate is $10B.

I think the latest tally was:

~$130Bn US (already spent)

~$115Bn (IMF) [ a peaceful institution]

~$23Bn (WB) [ a peaceful institution ]

==========

$270Bn. total.

JP Morgan and Blackrock are already “all in” on the Ukraine rebuild and have set up mechanisms for the transfer of “public and private” investments into Kyiv,…

The World Bank estimates are around half a Trillion dollars needed to rebuild Ukraine.

These guys seem to show up when there are large quantities of money moving at the discretion of the government.

Is the war ending with Ukraine the victor a foregone conclusion?

MW: ADP reports U.S. private sector added 497,000 jobs in June — double economists’ consensus forecast

First they rob the poor by conjuring money for their high and mighty friends to front-run asset purchases.

Then, once inflation sets in, they rob from you again as nominal wages put you in to a higher tax bracket.

Costco Toilet paper. Price up 11%, volume per roll down 12%. Therefor price per wipe up 26%.

Never, ever trust Government numbers and you might, just maybe have a chance.

Your Costco toilet paper example is ignorant BS and only discloses that you’re totally clueless about how the government measures inflation, and so your conclusion about the “government numbers” are also clueless BS.

Prices are measured by quantity, not packages, such as square feet of toilet paper (look on the package of the Costco toilet paper, it’s right there), or ounces of cereal, ounces of milk, etc. And for inflation measures, it doesn’t matter how big or small the package is, DUH!!!

I have explained this a gazillion times here. It sure is a lot easier to make up BS than it is to actually learn something.

If you don’t like data but prefer BS, you’re in the wrong place here. There are plenty of other places that suit your preferences.

But isn’t he talking specifically about Costco toilet paper, not government measures in general?

Both. Read his last line.

Kam,

It’s been well documented that consumers change their behaviors when prices change. For example, beef goes up but chicken doesn’t, so people eet mor chikin. Gasoline prices skyrocket, people stop buying gas guzzlers and buy cars with better MPG.

Have you thought about going to the bathroom 26% less? Or maybe buying washable toilet paper? It wasn’t that long ago that cloth diapers were used for babies instead of disposable Pampers. My final question, have you thought about just not wiping at all? That woukd solve your toilet paper inflation issue AND put money back in your pocket.

The payback on a bidet keeps improving. Time to check YouTube for a demo.

The fact that people change behavior in response to inflation doesn’t change the fact that inflation makes everyone poorer.

I’m surprised not to see the same run on deposits in Europe as we experiencing in the US. EU bank assets, specifically sovereign bonds, should be far below par given their long history of NIRP.

Wolf,

You mention just two separate bond purchase programs, the APP and the PEPP. However, the ECB press release shows more categories:

1) Covered bond purchase programme 3: 296.7 B

2) Public sector purchase programme: 2530.9 B

3) Corporate sector purchase programme: 338.9 B

4) Pandemic emergency pur programme: 1672.1B

Are items 1 thru 3 above all sub-headings of the APP? Also did the ECB provide any rationale as to why the PEPP assets won’t be allowed to roll off?

The first three are types of securities that the ECB purchased: covered bonds (explanation here), government bonds, and corporate bonds.

And there is a fourth category of securities that you didn’t list: asset-backed securities purchase programme

All four categories of securities are included in APP and in PEPP.

APP and PEPP are essentially the same in their functionalities, but where started at different times for different purposes.

The APP is the larger of the two: total €3.18 trillion

The PEPP is the smaller of the two: total €1.67 trillion

Modern finance = raining acronyms.

Or…reigning.

According to ADP, the jobs market in the US is like a July 4th holiday display, but the stock markets are acting like the fireworks backfired into the crowd today. Perhaps that is because that means that the Federal Reserve will only quicken and increase its tightening moves!

Good news is bad news.

Wolf – Thanks for the info, I had thought the ECB was moving alot slower. But the amount of QT aimed at financial markets (bonds), is still pretty meager. I assume that will continue to ramp up.

The banks are the middlemen for asset purchases. The ECB lent them €2.2 trillion and they bought assets with them so that the ECB doesn’t have to decide which asset to buy, anything from Italian government bonds to whatever. So this money too went into the markets, but via the banks. The money ends up in the same place, but it’s routed differently. This is the important thing to understand about the loans.

Yes, but now that those loans are almost gone, the question is whether the ECB will start selling the market securities. At the pace of 20 billion a month it would take 20 years to clear the whole balance.

Not that they plan to do that.

I meant, “selling them faster”.

And just like the US, Eurpoean stocks have been going up in 2023 straight into QT. Anyone with a good explanation?

European stocks TANKED today: -2.6% Dax, -3.1% CAC40, -2.2% FTSE… Do you have a good explanation?

MW: ‘Complacent’ stock-market investors start to ‘respect’ higher-for-longer U.S. interest rates…