And it’s structural. Variable-rate CRE mortgages and much higher rates just speed up the process.

By Wolf Richter for WOLF STREET.

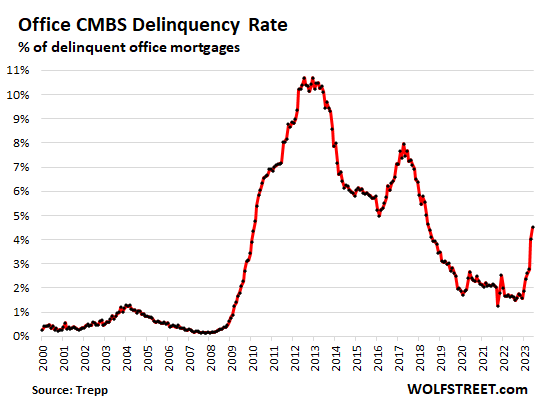

After blowing through the pandemic with no more than a squiggle, the delinquency rate of Commercial Mortgage-Backed Securities (CMBS) backed by office properties jumped to 4.5% by loan balance in June, up from 1.6% just six months ago in December 2022, according to Trepp, which tracks and analyses CMBS.

Office mortgages that had been packaged into CMBS went through a horrendous default cycle following the Financial Crisis, with the delinquency rate topping out at over 10% in 2012/2013.

But this current six-month 2.9-percentage-point spike from 1.6% to 4.5% is the fastest six-month spike in Trepp’s data going back to 2000.

So this is going to be interesting because we’re just at the beginning of a massive structural change – not a temporary blip – that is impacting office towers; turns out, companies have figured out they won’t ever need this vast amount of vacant office space.

Trepp considers a loan “delinquent” after the penalty-free 30-day grace period ends and the borrower still hasn’t caught up with the interest payment.

This delinquency rate does not include properties that are still paying interest but are past due on paying off the mortgage on maturity date. This includes the interest-only mortgages, when the whole amount is due at maturity, and mortgages with a balloon payment at maturity. As long as landlords are making interest payments, Trepp doesn’t consider the mortgages delinquent, but tracks mortgages that are past their maturity date separately.

For example, Trepp’s overall delinquency rate for all types of CMBS rose to 3.90% in June. Including the loans that were past their maturity date but were still paying interest, the delinquency rate would have risen to 4.66%.

CMBS have real advantages. They allow lenders, such as banks, to sell high-risk commercial mortgages during times of low interest rates to yield-chasing investors, such as bond funds, life insurers, etc. For banks, these mortgages might be too risky to keep on their books.

So they package them, sometimes just one big mortgage, but often several or many mortgages, into a pool of mortgages that then gets structured into different slices that investors buy, with the junk-rated slices taking the first losses in return for slightly higher yields. The top-rated slices have an A-rating or AA-rating, solidly investment grade (here’s my cheat sheet on bond credit ratings by rating agency), with the idea that the lowest rated slices will absorb any losses while the top-rated slices remain unscathed.

The mortgages – as we have seen in the current wave of defaults, including those where the landlord has just walked away from the property – are often variable-rate. Landlords liked variable-rate mortgages because they offer a lower interest rate, compared to fixed rate mortgages. And investors liked them because when rates go up, investors get a higher return, and the market value of the mortgage is largely protected.

But when rates go up a lot, as they have done since March 2022, the interest payments go up a lot, and by late last year, these interest payments began to double, and suddenly the building doesn’t pencil out anymore because rents, especially at office towers that are partially vacant, won’t cover the interest payments.

And then landlords might walk away and lose the equity. And CMBS holders end up with a defaulted mortgage and an office tower whose price at a sale will be far below the loan value. We have discussed the revenge of variable-rate office mortgages here.

And so even landlords – giant landlords such as private equity firm Blackstone and private equity firm Brookfield – have defaulted on the mortgages and then walked away from the property. They lose the equity in the property, and the lenders then have to sell the office tower for whatever they can get.

But whatever they can get for older office towers is a lot lot less than anyone had imagined a few years ago when the CMBS were issued. The losses on the mortgages for CMBS holders are huge, such as 88% and 82% by two Class-A office towers in Houston, or even a total loss, with the proceeds of the foreclosure sale just paying for fees and expenses, which happened with the vacant 46-story former One AT&T Center in downtown St. Louis. Two class-A office towers in San Francisco sold at 70% off the pre-pandemic price estimates, though they didn’t involve mortgages. Other office towers were sold with 40% to 50% in losses.

So these older office towers create some serious investor-bloodletting – but it’s thinly spread around the globe, from the bond fund in your portfolio to a pension fund in a foreign country.

And it’s structural, not a market blip; it’s an issue that will have to be dealt with over many years, such as by tearing down office towers or by converting them into residential buildings where possible.

Even lower interest rates won’t make vacant or half-vacant office towers economically viable. Markets, if allowed to do the dirty work, are good at pricing those situations, and providing a low cost-base for developers with an appetite for risk to redevelop those properties, at the expense of existing investors.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“Even lower interest rates won’t make vacant or half-vacant office towers economically viable.”

I am seeing a huge pushback by employees to return to office. Those companies that are forcing employees to return are seeing massive defections. Many of these offices and towers were built when technology did not exist for remote work, which is making the situation even worse for CRE.

Let’s see how long these games plays out.

“An AT&T mandate calling 60,000 managers to work in-office three days a week is seen by at least one of them as “a layoff wolf in return-to-office sheep’s clothing,” according to Bloomberg. The ask coincides with a nationwide effort to consolidate the phone giant’s 350 offices into just nine — meaning thousands of managers must consider either relocating or resigning. CEO John Stankey has said he expects 9,000 employees to face that choice, but AT&T insiders put the number closer to 25,000, with a majority of affected staffers ineligible for relocation stipends.”

T is on the forefront of discovering new and worse ways to run a business.

You know the ONE objective ROI that keeps me from buying commercial property

REAL ESTATE TAXES

I can put out shingle with name on HOME I LIVE IN

but put it out on COMMERCIAL PROPERTY

bingo $25000 annual is minimum in taxes

I retired from them with 34 years of service and I can assure you they have been leaders in mismanagement for a long time.

AT&T has been a mess since Day 1. My grandparent took their splendid pension and retired after a lengthy bell career in the late 80s and not a moment too soon. Not an MCI commercial aired on our TV that I didn’t hear the lamentations.

lol, so true and couldn’t of said it better. Funniest part is that for cases like that, the return to office push would just result in even higher overhead costs for positions that don’t really need it, not to mention a lot more wasted time and less getting done with the commutes and sheer stress levels with the horrible traffic in a lot of those cities. Would be an even bigger irony if a lot of what’s motivating that bad policy is the companies themselves clumsily getting themselves into getting overleveraged into becoming owners of their own useless office buildings they never really needed in first place

AT&T and Comcast are continually locked in battle for the title of “Most Vile Company on Earth”!

I’m curious what it is these 60k managers do. I bought a couple pay as you go cards from them to test their service and when I tried to activate them via their website it was painful.

Back to office and AI are going to cause a lot of layoffs, even though they’re really just excuses for declining business conditions

here in Arizona we’ve had GET BACK TO OFFICE stuff year ago

no one here I know of works from home

and my son – works for city water – had to go full time 1st of year

One of my Tucson friends is still working from home, except for those days when she has to go to the office. She says that she’s much more productive at home, and her employer agrees.

They go to meetings. Lots of meetings. Many meetings. :-)

I can tell you from experience that a lot of companies are using RTO mandates as a way of helping employees to self-select out.

This is especially prevalent in the higher-technology firms that over hired during the pandemic…particularly those in California who have to jump through hoops to fire people.

What hoops? Everyone I know in tech is an “at will” employee. People are “let go” all the time.

Anyone know what it costs to demolish a tower that is surrounded by others, with the usual minimal space between?

I don’t see how you could do one of those controlled demos with explosives. To use a wrecking ball would you have to block off the street? Looks not just very expensive but risky.

A 767?

Too soon.

Will never be the right time.

Yup – its well established that hitting a building from the side is the best way to collapse it straight down into its own footprint.

It was just coincidence I tell ya!

try 285 Fulton Street demo

see how they did that

it’s special though

Have been wondering that same thing too. Some contractor we used to work with offhanded mentioned something about a multi step demolition done more finely that what you see in the videos, thinking they find a way to put like a shield around the main building in layers and then take it down in steps to minimize the debris to the buildings close by it. Probably doubles the cost of the process

I had an answer to your question but i guess it wasn’t politically correct. But there are some real estate guys who know the answer; and heck, you may even get the entire thing covered by insurance. Twice.

How can I (if that is even possible) tell if this crap is in my 401k, or the kid’s 529?

SomethingStinksC

It’s in there, you can be sure

You can start by seeing what funds your 401K is invested in. For example it might be invested in the “Blackrock Total Return Fund”. Then you start looking into what that fund is invested in. You gotta do some digging. The fund mentioned is one of the choices of my company’s 401K plan. It is down 6.5% from its inception back in 2000.

my retirement funds are entirely in REAL ESTATE

that I BUY

and rental income is TAX FREE

so are capital gains

if I need few $$ (which I don’t) I just pull out few $$$ tax free

Damn… I am going to do some research tonight. Probably too late, taking any corrective action at this point might end up being a “buy high sell low” situation. We should be allowed to sue money manager.

I found a lot of really bad stocks in mine, including CCP, Ponzi stocks. A lot of well known companies are now CCP owned.

Nevertheless, I suspect many pension managers will get rewarded, like Fed leaders getting $200,000 to $400,000 per boring speech, for having invested so “foolishly.” The losses will, as usual, be suffered mostly by pensioners, since the bankers’ “Fed” cartel will create US dollars and use its credit to bail the bank owners out as in 2008, etc. It is a corrupt fix almost as irritating as the truth that a John Alite just revealed about a famous event. I also hear from others the exact same thing that he revealed, but they were too scared to speak up. May he live.

“Markets, if allowed to do the dirty work… ”

And, as Shakespeare said, ” ay, there’s the rub.”

I think it would be a really good idea if the gummint got involved with this problem. Markets can’t be trusted, right?

How ’bout the FED? They seem so competent.

This would explain the recent op ed push trying to paint remote work as a failure.

Longtime Listener

I could list a dozen reasons why most remote work has been a failure, but I’m afraid most of the people on this site would not agree with me. Let me just say that many of these remote jobs are just one short step away from being outsourcing to a third world country with cheap labor.

A dude at my supermarket fish counter just had claim for an auto accident which was not his fault. He had to go through a claims adjuster in India. The service stunk to high heaven. Be careful what you wish for.

If the job can be outsourced does it really matter whether the

employee to be affected is in the office or at home ?

exactly – why so FEW jobs are safe – ie nearly impossible to outsource

Outsourcing has been going on since the 1990’s. I’m not sure why people think this is a new phenomenon.

Packing people into cubicles to stare at computer screens makes them more productive?

Oh, please. Do tell.

Yes, requiring people to actually go to work does tend to make them more productive.

my job is for you to come to me for my services / rent

ie you make 1st contact in 99% tries

got low cost rentals

The smell of burnt popcorn and smelly fish lunches must give workers super powers.

WaterDog

The heck with cubicles. Just put a long table picked up from a Jr High school surplus sale. Install a dozen phones on each side of the table with chairs. Hire some recent college grads and tell them to start selling gold coins on commission only and there you have it.

Believe it or not this is the business model I witnessed here several decades ago. I saw it first hand when I went to pick up my gold coins. The company has since gone bankrupt and took everyone’s money with them. I was lucky and got my gold coins before they went under.

4 hours of meetings, drinking coffee, dealing with constant interruption and gossiping at the water cooler is called productive? Really?

I think we should all get Wolf an office to go to so that he can be more productive.

Haven’t been in an office in over 3 years. Always amused on early Friday afternoons when the indispensable managers did laps around the cubic farm like Secretariat before leaving for the weekend. I’d try to stop one to strike up a conversation about some technical matter I was working on in hopes they’d miss their train home or flight to Aruba.

WaterDog is suspicious about WHY people packed into office cubes are more productive than people who work-from-home.

I’ll start off by saying since I am long retired I don’t have “a dog in this fight”.

I can tell the THEORETICAL reason this is “true”.

Accidental interactions between office workers is supposed to spread important knowledge INDIRECTLY. Also, talking with someone in person, face-to-face gives participants more information about … stuff.

No idea if either of these theories are correct. Or if any of the others are either.

Personally, as a life-long “computer geek” if I had work best performed without interruption I could do it better at home. Alone. If I could get my family and pets to just ignore me 🤪

I am retired and play golf on Thursdays (unless it’s over 100 F that day).

I meet people “working from home” at the course on a regular basis. I am not playing at night. Where were these jobs when I was in business? Must be the cell phone that makes it work for them.

No wonder these office buildings are becoming redundant.

They’re at the coffee shop gossiping, they’re at the gym, they’re at a campsite with a sliver of cell service. Everywhere except at work, and doing everything except working. Of course it’s a plum gig, and of course they want to keep it that way. I would too if I were one of them.

But it’s a question of how long they’ll be able to get away with it. If the job market ever actually tightens up meaningfully, their employers will have more leverage, and they won’t have to resort to pathetic RTO incentives like donating to charity every time an employee comes in. The incentive will be “you get to keep your job.”

I’ve been a telecommuter most of my professional working life. The allusions here to surreptitious leisure and aestivation have never been my experience. The biggest perk when I’m at home is avoiding traffic & getting to stay in my shorts all day.

A life of crime is more attractive than working day in/out in an office.

Anthony A.

Is it true that the golf course are jammed down there because no one works anymore. You have to get up at 3AM and put your phone on speed dial for an hour just to get a tee time?

It might be that remote work is one short step away from outsourcing to somewhere cheaper.

Another possibility is that it was just bullshit work when done in the office and no less bullshit work if done remote. And with remote work it become obvious that the “”work” and “workers” was ther so some manage had some to “manage”. Expect some cost cutting to happen.

I’m still hanging on to my remote job but my company is pushing RTO pretty hard. It works well for many people but not for others. But if a company could figure out how to outsource your work offshore, it would have done it by now whether you were in the office or remote. Remote employees in the US are still in a reasonable time zone compared to those in the office and don’t have a communication issue. Those are the 2 biggest reasons more jobs aren’t outsourced offshore already. Note if you believe the AI hype, more of the jobs may get outsourced (to offshore or to the AI) in the future.

I just got back from the office… we are supposed to do atleast 2 days a week. Its a sad scene, complete ghost town. Cafe is closed, there is not even coffee available. Phoenix is at 110 degrees today, so I had to get out of the building, drive the car half a mile to pickup a sandwich for lunch. Meantime, everything I did in the office today can be done from home. Might not work if you were on an assembly line, but for some tech areas, remote makes sense. Here’s the hypocrisy; CA claims to be all for reducing pollution, hollering about human actions amplifying climate change. So why not embrace WFH? Less number of cars on the freeways in endless traffic jams. But since we need to shore up CMBS all that is ignored.

I believe it’s true that many jobs CAN be done from home. I also believe most people will abuse the privilege.

The company I work for has fully embraced WFH in both policy changes and downsizing the office environment to support group meeting and collaboration. The employees love it and our overall productivity has stayed at BC (“Before COVID”) levels or is even up.

We are in tech and can’t see going back to the BC era of everyone driving to an office plus the flexibility of hiring someone from pretty much anywhere is great.

I WFH and admit I abuse the privilege.

I worked remotely a few days a week back in 2000-2001. Trust me it was not glamorous, I kept in constant contact with the office over adsl, and yes if I wanted to take a two hour break in the middle of the day I could just as long as I had everything completed by midnight so that everything could be passed along in the morning. If the job could have been offshored it would have been, just like the people doing remote work now.

The impressions that are fooling around all day coming from the posters on this forum whose timestamps are usually during working hours is highly amusing. Thanks all for the laugh.

The commenters here are all old people so they’re probably retired.

LOL about that retired part. Lots of commenters here talk about their work (from home or otherwise).

Speak for yourself?

Dozen? I challenge you to list 5!

FWIW my own experience working hybrid, it’s managers, both senior and junior, who abuse remote the most.

Read Arnold’s comment. Outsourcing has been going on since the 1990s. Nobody thinks it’s new. Anyway, only the most automatic tasks can be sent to the third world and performed there. Good luck finding very specialized professional services in the third world. Many work from home workers today are not going to have viable equivalents in low wage countries.

WFH is not going away and corporations do not have the leverage to stop it.

Swamp, you totally missed the MSM/Op ED/Gummmt Interference in free market, conspiracy theory. (the usual reason, too anxious for personal whine….not that it isn’t justified)

Also, Bcramp, I thought it was kinda decided (in general here) the Fed is more a Banking Cartel than it is Gummmt? Maybe not.

But again, I never took any Econ classes….dropped one once….I think.

But it was really interesting to read about office life. I only worked in factories or construction. Thanks for missing the theory, which was weak, anyway.

Yeahr—and Martha Stewart openly castigating the very idea of remote work as being (shudder) French in nature.

Related, but it takes a minute to get there –

Duke Energy is selling its renewable unit. They have taken a bunch of write downs on the units, and it is hard to find specifics.

Since a solar field is a bond, if interest rates go up, the “bond” value goes down.

What I can’t figure out is if Duke didn’t match the funding of their renewables to the length of their purpa (power purchasing) agreements with the end users. The renewables aren’t part of their normal grid operations, so they would normally sell the output to whomever is in the market at some rate that is guaranteed to keep the renewables in the positive in an absolute sense.

One of the immediate reasons for the write offs is the claw back of tax write offs because they aren’t holding them long enough.

But it does seem like they are really taking a beating – $1.5MMM new book price versus $5MMM original. And why the need to get our of them? They may not have tenant issues, but it does seem like they are in some sort of squeeze like the landlords.

Best I could find on it: https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/duke-dominion-digest-large-impairments-from-commercial-renewables-value-74269693

I recently found a book in the library called Running Remote. It is about transitioning from office work to remote work for organization. But it is about much more than reducing expenses, it is about increased efficiency from going from synchronous work to asynchronous. Working “async” means that everyone can work on their part of a job and that management systems and processes are put in place to coordinate all that work more productively.

This is a long term trend, not short term. Some companies will be office bound, but not many.

Waaaaay back in the mid 1990s, the multi national I worked for came down off a 15 year acquisition binge that created the globe’s largest producer of a commodity. Shedding of this and that became annual “special projects” including closing offices followed by firing office staff.

We determined that a “remote work” capability would be necessary for survival for our relatively small financial department including conversion of file rooms of paper files and obtaining remote capablilities for the staff members. Took us almost 8 years but by the time local accounting offices were closed, our staff remainedv 100% viable as “remote” workers 10 years before this “pandemic” panic. It was not intelligence, or anything other than necessity which was the mother of this invention,… for us anyway. The next gen of my staff continue to work “remote” quite successfully.

AT&T developed the Picturephone back in 60s. Little tv’s on phone lines. Flopped. No electronic bandwidth for it and people didn’t like the idea of being seen during business calls. Plus: expensive. Long distance subsidized local back then.

T was just early. Plenty of cheap bw now and so what if you can see me on Zoom if I don’t have to make a hellish body-and-soul-sapping 3-hr roundtrip commute to a cubicle.

My Insurance company went remote after the pandemic hit. All 25,000 employes are working from home. They bragged about it in their annual report. Their service was bad before they went remote, and after the pandemic ended they stayed remote and their service went from bad to worse. I cancelled my insurance with them. Most insurance companies are doing the same thing. Their main purpose and mission is to collect premiums and deny claims, and sell other services that you don’t want.

This. More this.

There are some people who are much more efficient working remotely. There are others that are much less efficient working remotely. Some tasks are better done remotely, some are better done with people sitting in the same room.

Companies are not dumb. They are going to eventually figure out what works and what doesn’t. They will figure out ways to track the efficiency of remote employees versus on-site employees on various tasks.

Companies are just starting to really figure out remote work versus on-site work. The smart ones will figure it out. The dumb ones won’t. That is capitalism.

Some interesting questions will arise.

Working from home is so attractive to many employees that they will accept lower pay to be able to work from home. This is already happening. My wife was looking for jobs that were work from home and she noticed that there was a difference in pay.

That said, an employee working from home in a job that is more efficient working from home, is also a huge benefit to the company. No need to pay for office space to house them, no need to pay for the electricity they use, bathrooms, kitchens, etc. Plus studies are already starting to show that highly efficient WFH employees actually put in more time because they put in some of the time savings from the commute into working longer.

It is an interesting time. It will be interesting to see who figures it out.

Fed minutes lean toward more hikes. Longer bonds down quite a bit. Dollar up.

My guess is that with inflation now more than halved the FED will lean toward protecting jobs and the economy and will be willing to take years if necessary getting back to 2-1/2%. MBS, long bonds, and junk will suffer.

“My guess is that with inflation now more than halved…”

Not sure about this, especially in the service sector.

well except in things you need

TRY COPPER FITTINGS – up only 100%

Electrical – well homeless depot puts it behind wall that only their personnel has

then again ask any major manufacturer if they are going to raise prices

“My guess is that with inflation now more than halved”

Lol

“Pea Sea”

What’s with the LOL?

I remember inflation peaking around 10%. Now it’s around 5%. That’s about half

If inflation was 10% one year and 5% the next year that =15% above what the prices were 2 years back…

Thomas Curtis,

This issue is “core” inflation. We all know that energy prices plunged, which took down overall inflation readings, but core inflation is very sticky. Here is the Fed’s favored Core PCE price index. It has moved sideways for the sixth month in a row:

“My guess is that with inflation now more than halved”

If you go fro, 60mph to 30mph, your speed halved but you’re still moving forward.

The RATE of price increases has slowed, but prices are still increasing.

I said rate, and rate is change/time. So, inflation is half what it was

Service inflation, most of economy, has leveled off around 5%, not going down at all.

The word rate is not in your original comment.

I am using the government’s numbers. What numbers are you using?

The Needle and the Damage Done.

Evelyn WoodHead

“If inflation was 10% one year and 5% the next year that =15% above what the prices were 2 years back…”

Yes prices are ~16% higher today than they were 2 years ago but the inflation rate today is about half of what it was in December if 2021 when it hit a max of 10%.

So the FED is over half way to their goal rate of 2% which I don’t think is sustainable in our now supply constrained world. I think 2-1/2 to 3-1/2% is more likely. Further I think it will take longer to get to 2-1/2% than it took to go from 10 to 5.

Thomas and Evelyn,

You are both right. Even if we print a zero CPI the cumulative effects of inflation are still felt in the economy. However, this is a very slow process. Here’s why:

When prices rise so dramatically our wages also go up in similar fashion. We feel so much richer when we get a 7-8% raise when we are used to a 2-3% raise. This raise feels so good that we really don’t care that inflation is so high. Let’s face it, we all know exactly what we make but we do not know exactly what we spend. Until…

we eventually realize that we are outspending our raises. So we are forced to question whether or not we really need that new gadget or frequent food delivery. So we cut back, the economy weakens, prices fall, jobs are lost and recession sets in.

This is on top of the damage that higher rates have already done to CRE, housing and some large banks. It’s a devastation one two punch of cumulatively higher inflation on top of higher rates.

Thanks, and I very much agree with you.

Yes CPI and PCE. I prefer CPI because it carries more information but the PCE is certainly easier to work with.

Thetenyear

“we are forced to question whether or not we really need that new gadget or frequent food delivery.”

Need to discern between NEED and WANT in our consumption based economy. The choice is yours. Most of us accumulate ‘junk’ more than we need. Minimalists will not have that problem

Long bonds were UP when I saw this yesterday afternoon TC,,, and this morning UP again/even more???

You might want to review Wolf’s recent article re bonds.

The older office towers are easier to convert to residential as they have more concrete and less glass. I worked in one for 6 years which was converted to condo about 20 years ago. It’s still there and the new landlord is raking in big bucks. It was called the Grammax building at the time and was the HQ of the National Weather Service.

A week ago, my local newspaper had a story about the recent sale of LaSalle Plaza in Minneapolis. This is a 30-story tower with “… more than 620,000 square feet of space, not including 60,000 square feet of retail space.” Built in 1991.

The building is about 68% occupied, it’s connected to Minneapolis’ skyway system and is in a good location, 800 LaSalle Avenue.

Sale price was said to be $46 million. Hennepin County records had the value at $103M in 2020, and the “current estimated market value” was $87M, the article reported.

Twin Cities-based Hempel Real Estate bought the tower.

A good synopsis from the article:

“According to recent data from the city assessor, the most expensive downtown office buildings in the Central Business District (CBD) are tumbling in value, draining millions of dollars of property tax revenue from the city.”

Your last paragraph brings another aspect to this discussion.

Dwindling tax base is a concern. There is no telling what desperate and damaging measures might be tried by cities, counties, and states to keep tax revenues coming in even while the very base of taxation may be tanking. (ex; Could they be eyeing the $7.3 trillion in our 401k balances?)

Frankly, I’ve not seen a goverment entity ever really cut spending and it gives me the shivers thinking about what measures they may put in place to keep the tax gravy train going. Heck, it may make a real estate bust seem like a party by comparison. Hope I’m wrong.

Have you never seen a government entity cut spending?

I have and it goes like this: Interstate road get reclasified to state road, state road to county road and county road to private road.

Every such move shift the cost of maintenance get shifted to someone else and cut from federal, state or county budget.

Public service is cut and privatized. Easy targets are roads, watersupply, sewer and trash collection.

I don’t understand that last sentence. Property tax dollars are based on government budgets and voter approved surcharges. Property values only change the allocation of the pie. Governments don’t lose property tax revenue when property values fall. A common misconception.

Say what now? I’m not even sure what you are saying. Maybe it’s me. Otherwise, what you are saying sounds dangerously ignorant. Again, maybe I’m wrong and not understanding what you are really trying to technically say.

Cookdoggie is correct where municipal real estate taxation is concerned — the budget is set first, and then a mill rate is applied to the assessed value of properties so as to yield that sum.

for eg:

Depends HUGELY on the location.

Some places we’ve lived in the last 50 years, county exec first determined what tax money is likely and built the budget allocations accordingly,,, other places usually go through a now fairly transparent process before any adjustments to millage, etc., especially if millage going up.

Everywhere we have owned, there have been paths to protesting tax increases, both individual and municipality level.

Really not the same old ”good ol’ boys in the backroom” deals anymore, though it certifiably used to be that way.

Okay, I can see what you guys are saying about how the funding is planned for. It stills seems like such short term fixes that they really don’t prevent what is a large loss of revenue and the situation still stays on a path of mounting problems financially that is directly tied to tax sources. I think saying you can just ask for those that remain to make up for the losses leads to an exponential function if it is the only solution.

I just inquired about this from my neighbor who is on the City Council.

The current ratio of commercial real estate taxes to residential is 40 to 60%. Many years ago, due to state tax policies, that ratio was reversed to have 60% or so from commercial going into the city’s revenue.

But there will be a shift to put more of a burden on residential property taxes, and my neighbor thinks that it won’t be long before it is 70 to 30%, with homeowners having their taxes go up.

The tax assessments for commercial buildings such as office towers is done every year in Minneapolis. So, yes, the values will be reduced to reflect the market, and taxes generated for the city from these structures will be reduced.

To me, since I’ve lived in my home for 28 years, don’t plan on moving, and have owned “free-and-clear” for years, the market value means only one thing: how much property tax do I have to write a check for twice a year? The answer is no surprise. More taxes are on the way.

P.S. My neighbor has decided not to run for reelection and will finish this year’s session with ten years on the Council. He’s been a common-sense and practical Councilman, but his life will be a hell of a lot less stressful when he finishes out his run. I’m happy he represented me. But I’m happy he’s stepping aside, too.

In my locale, the residential real estate taxes are based upon a mill rate for various purposes that voters approve and are put up for renewal or increase periodically. The assessed value of residences is reset annually by the assessor’s office.

The assessed values general increase annually, some years more that others. I’ve had only one rural property whose assessed value leveled off and reduced for one year. First time ever happened in my lifetime. Should assessments flatten or in rare cases reduce, the mill rate applied will yield less in tax revenue. Unless as often happens, new or increased millages are approved by voters. I would guess that with such highly publicized CRE devaluations, watched by owner’s accountants and lawyers, that their appeals of assessed values might reach record proportions soon. Unless CRE assessments and tax rates are done differently than residential. Maybe someone can chime in on that.

Wolf thanks for this! How will this affect REITs?

I understand the CMBS holders will take possession and eat the loss, but how will REITs be affected by the equity losses? Any predictions?

Just check their share prices. They’ve been getting crushed over the past 12 months.

They’re losing the money they put into the building, and they’re losing the income from the building.

I did an article on a bunch of them a few weeks ago:

https://wolfstreet.com/2023/06/09/commercial-real-estate-woes-in-the-stock-market-office-reits/

They’ve rallied since then. BXP rose 10% in a day after an office block somewhere sold for much more than expected.

Hah. A rally — like a jolt of adrenaline shot through the carcass of the wildebeest as it tries to lurch free from the hippopotamus’s maw…

Maybe office REITs are getting crushed. VGSLX REIT index, a diversified index which I own, is down 9% over the past 12 months and up 2% YTD.

VGSLX is down 27% from the peak in Dec 2021. So maybe that’s not “crushed” yet, but it’s still down 27%.

I have a tiny amount of Vornado because I see it as a bet on flight to quality. I’m personally shocked at all the new office construction going on elsewhere though.

Should be a huge feeding frenzy for the vultures who know how to value this stuff. Consider looking for BDCs with solid track records.

Wait until the SHTF

Wolf

Who is buying the 30 year bond?

Bloomberg had a persuasive article arguing that it was the 30 year bond that was holding up the housing market which makes perfectly good sense to me. The yield is currently ~3.79 % which makes no sense to me, to believe our world is that stable.

I was asking Wolf about this as well– Bill Gross, Ray Dalio, Stan Druckenmiller and Warren Buffet have all said buying 30 year Treasuries makes no sense at these interest rates. Since these are some of the best investors ever, why are 25 year old finance guys pushing this crap?

An amazing psychology question.

One possible explanation is Japanese investors who buy them, then pick up the interest plus the currency appreciation because the yen is falling faster than the USD.

Given Wolf’s time in Japan, I was hoping he could give us more detailed insight into the mechanics of this.

At present, Japanese investors can essentially get close to 10% on this investment between the yield and the currency arbitrage.

When it reverses, watch out because it will be brutal.

can’t have that

Bond Vigilante Wannabe

“Since these are some of the best investors ever, why are 25 year old finance guys pushing this crap?”

Here is another guess: Modern Monetary Theory

What is it that you think you know about Modern Monetary Theory?

Michael Burry is buying them with 10 to 1 leverage. When the recession/depression hits he will be sitting pretty. I’m thinking of doing the same. You can’t get hurt.

That’s a heck of a bet. I think he will lose it. I think the fed is going to drag this out and protect labor and earn themselves fame for their soft landing.

Any idea how much he is betting?

When has the fed ever protected labor?

Phoenix

“When has the fed ever protected labor?”

Not sure, but I think they are doing it now. Full employment is half of their mandate and while PCE has not fallen in half CPI has. They are making progress on inflation and it is growing more likely there will be a soft landing.

It certainly feels lonely being a bull right here.

Bottom line:

with Govt deficit running trillions of dollars per year, FED won’t have any option but to reduce rates and start doing QE. it’s a matter of time.

I bet by the end of this decade, FED balance sheet would add few more trillion dollars although they are reducing at this time.

Another way is : Govt reduces their spending. Do you think it is possible ?

Long term: Debts would be defaulted by way of currency devaluation. It is already happening for last few decades. Dollar has lost lot of value in last 30 years., QE and low rates made it much worse. I see this trend to continue more and more if not in the near future then after couple fo years.

Closed at 3.94% today

I wonder how much of these defaulting loans are beneficially owned by the Fed…

ZERO.

The only CMBS that the Fed holds are $8.3 billion in government-guaranteed “agency” CMBS (Fannie Mae mortgages) on multifamily buildings.

Since the banks offloaded a lot of these while rates were low, they’re no longer at risk, so I guess the question is, who now holds most of the CRE-heavy CMBS?

And then, what, if any, effects are likely to ripple through to other parts of the economy as those CRE-heavy CMBS holders feel the pain?

I think it is safe to assume that the Commercial Real Estate Mortgage market will have the opposite of “the wealth effect”.

Any chance the commercial market could pull the residential market down with it?

I don’t know, Painted Pony, but it seems like cities would need to make up the tax revenue loss from commercial, maybe by increases to residential housing taxes. Seems like this would make residential more expensive overall, so maybe sales price would have to fall to compensate for taxes. Or they don’t make up the revenue difference, and schools/public services suffer, so the cities become less nice places to live.

Residential real estate would be put down by high rates and large scale unemployment.

Also residential real estate is painfully slow.

The commercial market usually leads the residential market by a year or more. I’ve seen that happen here over the years. If there are no jobs downtown, why would people pay top dollar for a property near the downtown where there are no jobs.

Yellen to save CMBSs like she saved the SVB depositors?

And what of FTX and SBF?

Protecting discretion….kinda like prosecutorial discretion

With respect to Yellen, the far more likely outcome is what happened to SVB bondholders and shareholders. As investors, they were left to take their losses. There’s nothing to suggest CMBS bondholders will be treated any differently.

Futures and options for the leveraged 30year treasury? Is that easy to do?

ZB is the symbol of 30 year treasury bond Futures,

It trades 24 hours like ES (mini s&p futures) ,YM (mini dow futurs)etc.

there must be options on ZB in CBOT /CME.

if your brokerage account is enabled for futures and options, check at your brokertrading site.

TLT (30 year treasury bond fund ) trades like a stock. (only usa regular trading hours) . you can puy Put or sell calls on TLT also.

you can check the ZB hourly/30 min chart at Investing dot com web site.

Is there any sign of this happening with housing? Are there many big residential buildings that are funded the same way with these CMBSs?

I think that the commercial real estate market is at a massive inflection point. There are going to be some cities where the downtown is going to end up looking like 1990’s/early 2000’s Detroit. A desolate wasteland. Any investment will get crushed. There will also be some cities where people will figure out alternative uses for the valuable excess commercial space and thrive. Those investors will do extremely well.

I know it is complicated turning commercial space into residential space. Hard, but not impossible. There is also someone somewhere, who will find incredibly smart uses for prime (valuable) downtown commercial space.

Those that figure it out are going to cash in buying distressed properties for pennies on the dollar. They will look like geniuses years from now.

I just wish I had better insight and knowledge in this sector, but I do not.

It’s cost inefficient to turn high rise commercial space into residential, seen this over the last 10 years where one developer thinks they can buy a commercial building and turn it into residential until they get the fee’s from everyone involved and it’s cheaper to demo and rebuild at that point.

That was at sub 4% commercial rates, which are the way of the dodo bird now.

Just look at the design phase of a commercial building vs. Multifamily or Hi-rise and you’ll quickly see plumbing and heating / cooling issues on a massive scale.

In the Swamp they’ve turned Church rectories into condos. The conversion is pretty easy as the buildings are mostly solid concrete and have the plumbing already in place.

Not mentioned in article is buyers of distressed property have competitive advantage in offering low lease rates, huge concessions, TI allowances, etc… they can steal best tenants and cause stress on currently performing competing projects. Happened 30 years ago and once that trend increases just LOB.

2 things I’ve noticed since the pandemic/WFH really kicked in:

-Home prices here(Bend, OR) are doubled

-weekday skiing at Mt. Bachelor is MUCH more busy

Whatever it takes, get these city folks BACK TO THOSE OFFICES!

There are lots of people doing less for more money that are being propped up by the masses doing more for less money.

It’s fueling a lot of inflation, in travel and leisure. Basically, these people are on a giant walkabout, not willing to work anymore.