The Fed has now shed 20.5% of the Treasury securities it had bought during pandemic QE.

By Wolf Richter for WOLF STREET.

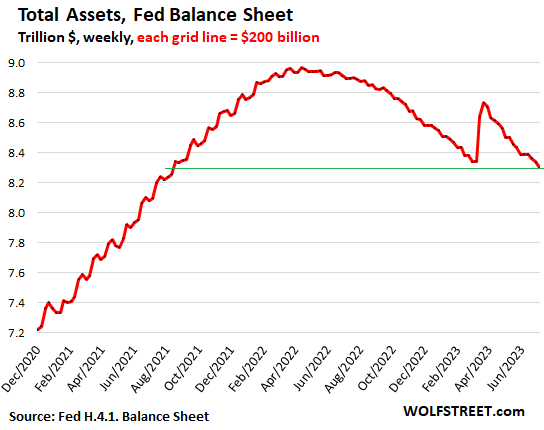

The Fed’s total assets dropped by $87 billion in June, and by $667 billion since the historic peak in April 2022, according to the Fed’s weekly balance sheet today.

In the 15 weeks since the height of the bank panic in March, the Fed has shed $435 billion in assets, the fastest-ever 15-week drop, as Quantitative Tightening (QT) continued on track and bank liquidity support measures continued to unwind.

At $8.298 trillion, the balance sheet is now at the lowest level since August 2021. This chart shows the details of the banking crisis, and how it is being unwound:

From crisis to crisis to raging inflation. Note QT #1 in 2018-2019, which removed $688 billion from the balance sheet. By the end of this month, 12 months into QT #2, the Fed will have unwound more of its assets than in the entire period of QT #1, despite the bank-panic bailout that at the peak had added $391 billion to the balance sheet.

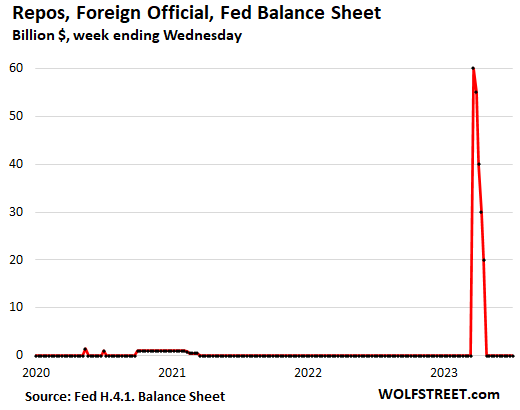

The banking crisis measures.

Repos with “foreign official” counterparties: $0. It was paid off in April. The Swiss National Bank likely leaned on this program to fund the dollar-liquidity support for the take-under of Credit Suisse by UBS.

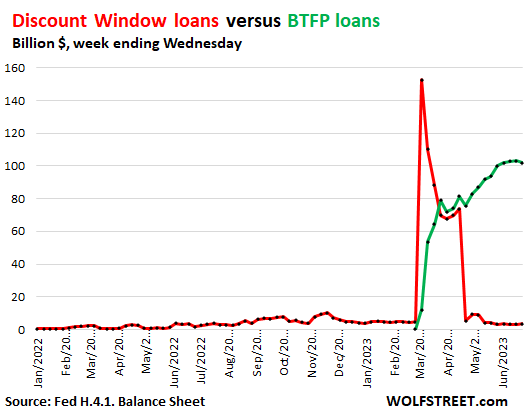

Bank liquidity programs.

Discount Window: $3 billion, down from $153 billion in March. Since the last rate hike, the Fed charges banks 5.25% to borrow at the Discount Window ( “Primary Credit”). In addition, banks have to post collateral at “fair market value.” This is expensive money for banks that should normally be able to borrow for less from depositors without having to post collateral. So they pay it off as soon as they can.

Bank Term Funding Program (BTFP): $102 billion, declined by $1 billion in the week, first decline since May. Banks can borrow for up to one year, at a fixed rate, pegged to the one-year overnight index swap rate plus 10 basis points. Banks have to post collateral, but valued “at par.” Still expensive money, but less expensive than at the Discount Window. It seems banks paid off the Discount Window loans with proceeds from BTFP loans.

Both facilities combined: $105 billion, down from $165 billion in mid-March. The chart shows loans at the Discount Window in red, and the loans at the BTFP in green:

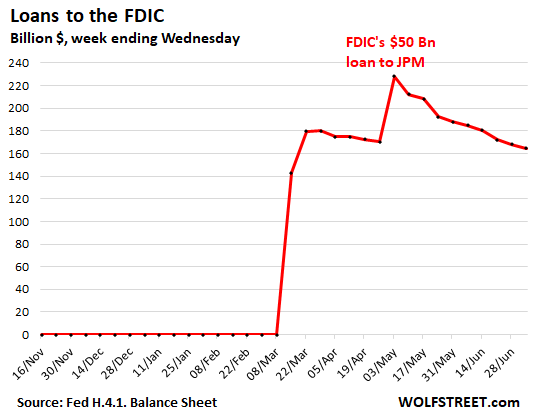

Loans to FDIC: $188 billion, down by $4 billion in the week, and by $23 billion in June. That spike in the week through May 3 was caused when JP Morgan acquired the assets of First Republic from the FDIC for $182 billion, and borrowed $50 billion from the FDIC to help fund the purchase. The FDIC then borrowed from the Fed (we walked through the details here).

The FDIC is now methodically selling the loans and securities it took over from the collapsed Silicon Valley Bank and Signature Bank. As the FDIC returns those funds to the Fed, the loan balance declines.

QT continues.

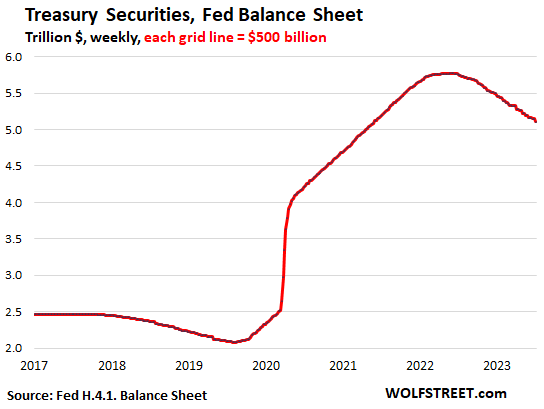

Treasury notes and bonds: $5.11 trillion. Down $58 billion in June, down $665 billion from the peak in June 2022.

The Fed has now shed 20.5% of the Treasury securities it bought under the pandemic QE ($3.25 trillion).

Treasury notes and bonds “roll off” the balance sheet mid-month or at the end of the month when they mature and the Fed gets paid face value for them. The roll-off is capped at $60 billion per month, and about that much usually rolls off, minus the inflation protection the Fed earns on TIPS (Treasury Inflation Protected Securities) which is added to the principal of the TIPS.

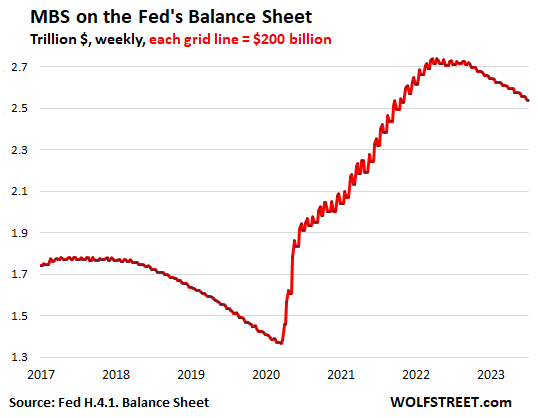

MBS: $2.54 trillion, down by $20 billion in June, down by $202 billion from peak. The Fed only holds government-backed “Agency MBS,” where taxpayers carry the credit risk, not the Fed.

Mortgage-backed securities come off the balance sheet primarily via pass-through principal payments that holders receive when mortgages are paid off (mortgaged homes are sold, mortgages are refinanced) and when regular mortgage payments are made.

The reduction in MBS has been well below the cap of $35 billion per month because passthrough principal payments to the Fed have been slow, as fewer mortgages are getting paid off because home sales have dropped and refis have plunged:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I am sure the Federal Reserve officials are proudly waiting for fawning supplicants to applaud them for reducing their balance sheet by only 38% of what the European Central Bank did. Looking at the larger balance sheet of the Federal Reserve it is even more pitiful. Supposedly the #1 economy and it is a fraction of the EU’s collage of economies, including many weak ones.

Just an FYI: The ECB’s balance sheet at the peak was €8.8 trillion, which was about $9.6 trillion. So it was larger in absolute terms than the Fed’s balance sheet.

And because the Eurozone economy is quite a bit smaller than the US economy, the ECB balance sheet was proportionately, far bigger than the Fed’s balance sheet.

The biggest balance sheet of all, in proportion to the size of the economy, is that of the Swiss National Bank.

When the GDP in 2008 was ~$15 Trillion, Fed balance sheet was ~$1 Trillion. In 2022, GDP was ~$25 Trillion, Fed balance sheet is ~8 Trillion.

Simple math would yield that Fed balance sheet must be < $2 Trillion today. However, I see questionable claims that Fed balance sheet must be decreased only to $5 Trillion.

Looks like they are lobbying for bigger Fed!

Here is the “simple math” of the Fed’s balance sheet and how low it might go. It’s a function of the liabilities the Fed has (cash in circulation, TGA, reserves, RRPs, etc.). Read this; I wrote it specifically for you:

https://wolfstreet.com/2022/09/05/by-how-much-can-the-fed-cut-its-assets-with-qt-feds-liabilities-set-a-floor/

Leo: great point.

Post 2008, Fed started mad experiments with QE. Walstreet figured it is great for them via asset bubbles. Now walstreet/financial media completely took over this narrative and cornered Fed, and Fed obliges with ZIRP and QE to pump up bubbles. listen to CNBC, almost every segment is when Fed pivot and when QT ends, when QE begins.

No one cares about consequence for general public. Take housing as example. It is very hard to buy house. They built massive bubble. On top of it Fed pushed mortgage rates to ~3% during pandemic. As a consequence those who have 3% mortgages are not selling resulting housing supply. Whole thing is messed up.

Does Fed to any retrospective for their actions. Hell no. They army of Phds. All they do push some BS to support why ZIRP and QE are needed.

End result is going to socialism in this country.

The EU has done $1.6 trill in QT while the Fed has pumped over $300 billion of QE again in loans this spring to bail banks out already – net QE is only $300 billion.

The Fed never is able to do QT. If they really wanted to tighten financial conditions they would have done trillions at this point.

This reminds me of bleeding of patients ,didn’t work . Some survived,some did not .Kind of like fed .

So they’ve reduced the balance sheet ~8% from the peak of ~9 Trillion. Respectable, but not significant.

This level of reducton is not sustainable in the long term, but for now, the optics are good.

The balance sheet will never go to zero. It was never zero. It cannot go to zero. So your top-to-zero change is misdirected.

The balance sheet should grow with the economy and with inflation. It might go back to $5 trillion in a few years.

So a better way to look at it is in terms of pandemic QE. the Fed cut the Treasuries it bought during pandemic QE by 20.5%.

In the long ago antiquated good ol days of 2002 to 2008, the Federal Reserve’s balance sheet was about 1 Trillion dollars. Who made the Federal Reserve the central marketplace of financial securities as the main and perhaps only buyer and seller.

I’d say: “Paying Interest on Reserve Balances: It’s More Significant than You Think” Scott Fullwiler

I really wonder how we survived before 2008.

One way of looking at it is in terms of total assets as a percent of nominal GDP:

Wolf – is it right to read that chart as we are now more govt driven economy than we were before 2008?

Vlad the Impaler,

That’s not a topic that this chart addresses. The chart expresses the Fed’s assets as a percentage of nominal GDP, instead of in dollars. The Fed’s asset are a “stock” — an inventory of assets denominated in dollars. But GDP tracks a “flow” spending and investing denominated in dollars. Expressing something as a percent of GDP is a common way to show the magnitude compared to the overall size of the economy. But these comparisons say nothing about what drives the economy; that’s not their purpose.

When government is so heavily involved, all metrics become obfuscated.

Fed owns 20% of all US MBS.

Why should Fed balance sheet never go to zero? What have the Fed achieved in the last decade with its balance sheet? Asset bubbles, stealing from the savers, concentration of TBTF banks and unending financial experiments.

Nacho Bigly Libre,

“Why should Fed balance sheet never go to zero?”

What aggrieves you are the Fed’s asset purchases during QE and its interest rate repression. Agreed, the Fed doesn’t have to do that, and shouldn’t do that, but it would still have a balance sheet (assets and liabilities).

No bank and no company can have a balance sheet that is “zero.” The Fed is a “bank,” though a special bank. There wouldn’t even be money to pay rent or utilities. Every commercial entity has a balance sheet. Even your own household has a balance sheet, even if you don’t write it down.

If you ask an accountant to do a balance sheet for your household, he’ll ask you a bunch of questions about your assets (amount of cash in the drawer, cash in the bank, of stocks, bonds, and CDs, value of home, etc.) and liabilities (unpaid bills, credit card balances, mortgage, auto loan, student loan, money you borrowed from your brother, etc.), and he’ll build a balance sheet from that info, including what your net worth is (“capital” or “equity” on business balance sheets).

When the Fed was created, a balance sheet was created. I have addressed the specifics of the Fed’s balance sheet and how low it might possibly go here. Please read this:

https://wolfstreet.com/2022/09/05/by-how-much-can-the-fed-cut-its-assets-with-qt-feds-liabilities-set-a-floor/

The broader view of Fed asset growth is informative, and helps explain the growth in leverage in general in the US.

For an even broader view, check out McKinsey Institute’s 2010 piece on world debt, including US. ( https://www.mckinsey.com/~/media/mckinsey/featured%20insights/employment%20and%20growth/debt%20and%20deleveraging/mgi_debt_and_deleveraging_full_report.pdf ). The piece is very readable, though dated.

See especially the chart on page 59, where it shows total US debt, by sector, as % of GDP growing from:

1960 – 134%

2009 – 196%

Of special interest is the US government debt portion which has ballooned from 67% (2009-Q2, roughly the start date of Wolf’s nearby chart), to over 120% today.

This debt growth has been brought to you courtesy of Fed interventions in the rate markets, in my opinion.

Obviously lower interest rates since 2008 destroyed the entire world economies. They did the same as Japan and got the exact same result.

Appreciate the details but that’s like missing the forest for the trees.

With that question I wasn’t showing academic curiosity.

It was more in line with “why do we need the Fed and its huge balance sheet? what good has it done to us?”

Pre 1997 economy did not survive, it’s dead.

We now have a land backed society as fiat doesn’t store purchasing power.

Land value tax would render the unimproved value of land at zero, the polar opposite of the current nightmare.

MIKE R. didn’t say it was going to zero. I don’t know why are you so obsessed with this “going to zero”, Wolf. He didn’t write that. He said it was reduced by only 8 % and that is not sustainable, as it obviously isn’t, because there is going to be another recession, and everyone, including the FED will panic.

And you can not ignore the fact, that doing 10 years of QE has triggered disbelief in people, that the FED will try to fix problems in other was than QE.

As Keynes said, we are all dead in the long term, but the US doesn’t have a bright future ahead.

As I wrote before: All you need is another war and the debt will be 50T.

Well said, although it’s not that I think the Fed should try to fix problems in ways other than QE. It’s more that I don’t think the Fed should try to fix problems at all.

Their “cures” are far worse than the diseases.

No one here ever wants to talk about the reason we’ve had unorthodox money printing for going on almost 20 years now. You all know it, but ya just don’t want to admit it: We’re bankrupt and all the funny accounting does is keep those in power who do not deserve it. Those who make peaceful change undoable and all that.

Einhal,

Well said? Which part? It’s quite clear Asul either doesn’t understand or misrepresented Wolf’s reply to Mike R.

Rojo, the part about the reduction being embarrassingly small, and not being enough to really do anything to deflate the asset bubble. Also, the part about the Fed having no credibility such that the markets believe they’ll restart QE as soon as the going gets tough.

The U.S. has a brighter future (as measured over the next 30 to 40 years) than almost every country on the planet. Sure, there are issues, but every country has issues.

What other country do you think is going to be better over the next 40 years?

To JimL

Simple answer is Japan.

Better educated, safer, a more homogeneous country and society compared to most other countries, a language that acts as a barrier to entry, and healthier too.

Before 2008/2009, the balance sheet was below 1 Trillion.

The economy has not seen the level of real growth you’re postulating to support a 5T balance sheet.

The US economy is mickey mouse. It is wholly dependent on debt to sustain the “American way of life”. The rest of the world is sick and tired of supporting us.

Mike said 8% which was a measure against the top ($9T) vs zero. If it were top vs $5T then it would be 18%.

But wolf,

If I’m under delusion it’s about economic health why don’t they sell mbs into the market, rates are already high, force the reits and funds to dump bonds, force.properties to change hands and become economically productive assets.

Given all the halcyon, can’t the economy absorb these write downs and still be fine?

Fed cannot sell MBS right now. If they do they will lose principle.

Losses don’t matter to the Fed. A central bank that creates and destroys money on a daily basis as part of what it does will never run out of money, and so losses just don’t matter, and “capital” is irrelevant too since the Fed can create unlimited amounts of it if it wants to. “Losses” don’t figure into the Fed’s decision-making process since they’re irrelevant.

But a concern might be that mortgage rates will blow out if it sells MBS. They’re already over 7%.

I think 7% mortgage rates will put the final nail in the Summer selling season.

That in turn should slow the rest of the economy eventually.

We can only hope. I look forward to seeing as many Realtors(TM) standing in bread lines as possible.

That would be one of the greatest things that could happen to America.

Probably can skip the bread lines though – plenty of lawns that need mowing.

They don’t do bread lines, they do OnlyFans.

You have just won the internet for the day with this comment!

And

“Donate to my free money account because I’m a broke loser who wants to do nothing all day but buy Amazon crap and play video games”

I actually had someone I know send me a link to that. With no reason other than “woe unto me!”

people take the donations too far these days.

at least sing or dance. Do something!

Exactly. Instead of sitting around crying find opportunity, like the guys who stole the HVAC system from our local library.

They started the Fed in 1913 to put an end to constant boom and bust financial cycles. Thank goodness we don’t have those anymore…

Well I don’t know about anyone else but it has been a long time between drinks with my 2010 purchase of a leased MB with very low klicks, still under warranty, Off a very distressed RE agent. It had all the Fruit as well.

This is 2023 and 13 years on it was a great buy but now, sadly it must be replaced. Bring the Recession on, in all its glory.

I will relieve you in cash and your credit blackmark by screwing the Finance company big time while the lessee can shop freely for a used Hyundai

Naw They’re all on YouTube telling you how all the other agents only care about themselves.

And now they’re trying to live on your ouTube clicks, warning you about all those other realtors who don’t care like they do.

Perfect.

They’re all “earning” big bucks.

Efficient market theory states that the best people are in the best paid jobs.

Therefore realtor layoffs would unleash some of the best minds into the rest of the economy.

We would have a second industrial revolution and growth would rocket.

That or economics is a meme degree, completed by bog standard people who don’t question content.

You decide.

My brother listed his house in MA on Wednesday. Had 17 showings on Thursday. Today and tomorrow are the open house. They already have two offers. Builders are the only thing that will stop this madness.

Yeah, I’m still seeing houses in Southern NH and Mass going for 8-10% over asking. It’s really insane- and inspections are being waved according to people I know in the business.

My son’s tree house sold for 15 times the list price.

He’s retired. True story!

Last week, I sold my 2,000 sq.ft., 20 year old house in Texas in a 55+ community (north side of Houston).

Since my wife passed last December, I decided it’s time to downsize and I am looking for a smaller place. The house was on the market one day and had several offers. I took the one that was 5% over asking, and asking was at the top of the historical sales range for the area. Cash sale by retirees.

Madness is going on in RE for this area. But, then again, we are not Ca, Boston, or NY and nice houses in decent neighborhoods are still selling here for under $200 per sq. ft.

Yes, it’s hot here and we have high property tax (2% area average), but no state income tax or property tax on autos. Energy prices are low here too. I’ve lived in both California and Connecticut and prefer here. (I’m not looking to start a discussion on where to live.)

I am looking to buy north of here in a new area with many new homes and looking at 1,200 – 1,300 sq. ft. for around $200 K. Hundreds of them are being built 10 miles north of me. Lots of them will be rentals I am sure.

A nice rental house here (1,500 – 2,000 sq, ft.) is running $2+ K/month. That’s insane in my opinion, but it’s what’s happening. Rather than rent, I’ll buy the new house and when I leave this earth, my daughter can turn it into a rental.

HerpDerp,

I’m not sure what can really stop the

real estate market in this (Boston) area.

It’s clear that interest rates at the current

level isn’t slowing the market down.

I know I vented here about contacting

a Realtor the same morning a place went

on the market with a question, only to be

told that they had already accepted a offer.

I’d really like to buy a place, but it’s just

stupid out there. And it has been, for a

long time. How long can a market stay

irrational?

J

Realtors are moving to NJ. That’s the only state where you can’t pump your own gas. Plenty of job vacancies in that career

Swamp – Oregon is/has been a ‘full service only’ state, as well (have had a few fraught encounters when refuelling a moto there over the years…).

may we all find a better day.

Yes, and 79.5% of the pandemic flood of federal paper is still floating out there and feeding the inflation beast. Rates are going higher for much longer, until the system breaks. Look at today’s ADP payroll data. The fact is the Fed is moving too slowly, even if Wolf is impressed by the effort. I understand pausing rates to assess where we are at, but if we won’t do more intense QT now, when will we ever? I suppose I answered my own question— never.

At the rate the Fed is moving to tighten lending conditions we will be in a recession long before they even scratch the surface in removing the excess liquidity. Then we will be back to QE, especially in an election year. The only thing you can be sure of is. Your dollar will lose purchasing power and you will be worse off than you are today. In fact, you will look upon the current Stagflation economy as “The good old days”.

I suspect rates will stay high until a major g7 pops.

Front runners?

Japan

Canada

Uk

what is the time frame by when Fed will own more MBS than treasuries.

Won’t happen because the Fed really doesn’t like MBS on its balance sheet (for a variety of reasons that it spelled out). It’ll figure out a way to get rid of them. Last time it ended QT in July 2019, but it kept running off the MBS at a rapid clip until March 2020, and added Treasuries to replace them.

At least back then there were structural reasons why MBSes could roll off quickly (ie the hot housing market and low refi rates).

The Fed Reserve’s QT and the Fed govt need to refill its cash account and fund its deficit spending should drain liquidity from the market and pressure new debt investors to want to receive higher interest rates for loans. I expect dramatic consequences from the liquidity drain and the upward interest rate pressure, both short term and for 10 year bonds. This week has started the trend but I am not sure what to expect over the next few months as liquidity / M2 goes down and interest rates, both short and long term, trend up.

I look forward to Wolf’s comments in coming weeks!

The current way the Fed is getting rid of MBS appears to be a plan to hold to maturity. Only 25+ years to go on a lot of those loans.

“Maturity” is irrelevant for MBS. They’re self-liquidating long before maturity through passthrough principal payments as mortgages are paid down or are paid off. In addition, when the underlying mortgage pool has dwindled enough, Fannie Mae or Freddie Mac, et al. will “call” the MBS for the remaining face value and repackage the remaining underlying mortgages into a new MBS with other mortgages and sell that to the bond market.

If the Fed doesn’t do anything at all and just collects the passthrough principal payments, and takes the cash when the MBS are called, the MBS will likely be gone in something like 7-10 years. If mortgage rates drop, they’ll be gone far faster because refis will surge.

It doesn’t like them yet it bought several trillion dollars worth in three phases. Assuming the next “once in a lifetime” economic shock comes in 4-5 years for one reason or another the fed will certainly buy more than it will be able to burn down in that period. The ride will not end.

For decades the Fed stayed out of long term paper (like MBSs)…and for good reason. Bernanke won the Nobel for what he did, and we still deal with the ramifications.

Having Trillions in long paper….and having to raise rates to fight an inflation partially attributed to the purchase of long term paper (and forcing a yield curve inversion) is an unenviable position. Though the Fed’s losses are “paper” and can be plugged into special accounting categories, those current losses are a “win” for those on the other side of the trades….and quite a stimulus.

Imagine the mortgage owner at 2.8% taking his extra cash and lending it to the Treasury at 5.25%. That’s quite a stimulus.

“Imagine the mortgage owner at 2.8% taking his extra cash and lending it to the Treasury at 5.25%. That’s quite a stimulus.”

My mortgage is 2.7%, and the average yield on my bond ladder is 5.2%. Quite the spread.

But don’t worry – most of that profit is getting siphoned off by the city from increased property taxes.

Housing needs to come down a lot more at current rates.

I can assure you in the bear future fed would find excuse reasons to buy all kinds of bonds.

Their balance sheet would only go up with time.

In 2008 their balance sheet was 1 trillion.

So does this gradual unwinding of the balance sheet, that it appears will take at least several years more, imply an elevated fed funds rate and market interest rates for the same period of time?

If so, it seems we’re looking at 2026 or so before interest rates turn lower, unless we get the long predicted and long overdue recession

I went out and bought loads of something I don’t like, didn’t need to buy, nobody expected me to buy it, nobody asked me to buy it and it wasn’t in my remit to buy it.

Boy I kinda wonder why I did it now.

Could I be misrepresenting in one or more of my above declarations?

…gotta lotta risk to socialize! (…and welcome to the club…).

may we all find a better day.

Observations from the charts:

1. Rate of QT is slower than rate of QE, and much slower for MBS case.

2. The long term chart of Fed assets seems to be continuously increasing despite intermittent QT periods.

No wonder despite slowly crawling QT, the long term treasury yields show a distrust of Fed.

The balance sheet should grow and in the past has grown with the economy (such as nominal GDP). The problem is that since 2008 it grew a lot faster than nominal GDP.

I think *a lot* isa bit of an understatement.

Maybe “increased insanely, ending price discovery and causing an everything bubble”?

It went from a rounding error to the only game in town.

Whoever created the BTFP at the Fed should get the Wizard of Oz award. They stopped an old fashioned financial panic and bank run dead in its tracks by waving away interest rate risk on long duration instruments posted as collateral by dumb and dumber banks. The BTFP is likely to last a lot longer than one year if higher for longer is for real. It’s much easier on banks than the discount window.

Right. The discount window during Paul Volcker’s reign was not a penalty rate.

BAGEHOT’S DICTUM: the central banks should lend early and ‘without limits’ to solvent firms at a ‘higher interest rate’ with ‘good collateral’.

Discounting was made a penalty rate on January 6, 2003

Yes.

But this is much more in line with what the Fed’s real purpose is…..preventing banking crises ….rather than the antics of pumping the money supply and pounding long term interest rates, which is what they did from 2009 to 2020, and becoming central planners.

Every time price discovery rears its head they ban it.

Same in other countries

USA: bond price discovery banned

UK: repossessions banned (temporarily!)

UK: gilt market bailout

Canada: mortgages extended

Canada: demand drop banned via massive immigration

Every crack will be plugged until income is meaningless.

Wolf, you may have already covered this but I can’t find your article. Why did the balance sheet spike by about 300 billion in the June-July timeframe?

It spiked in “March” — not “June-July timeframe” — by $390 billion because of the bank-panic bailout and liquidity support, when SVB, Signature Bank, and the First Republic failed.

I explained this again in the article. All you have to do is read it.

The balance sheet dropped in June (not “spiked”). We don’t have the July balance sheet yet.

Reverse Repos dropped below $2T. I guess that money is going back into the banking system?

The FED says it’s just a liability swap. But the reality is that it adds liquidity.

It makes a difference where the funds are held. Holding funds at the Reserve banks reduces the money stock in the commercial banking system/payment’s system.

Case in point, the O/N RRP facility. Aug, 9 WSJ:

“In their Aug 6. letter in response to our op-ed “How the Fed Is Hedging Its Inflation Bet” (Aug. 2), John Greenwood and Steve Hanke argue that the Fed’s sale of a trillion dollars of reverse repos does not in and of itself reduce the deposit liabilities of banks and money-market mutual funds, and that the money supply is unaffected. By that logic, none of the monetary tools of the Federal Reserve Bank would affect the money supply.”

1) Fed Total Assets – RRP = Fed net. Since RRP is down Fed net ==> no change.

2) The Fed needs your money. Both Fed and the banks seduce

investors with higher rates. The regional bank charts look like Ford in 2008.

3) TNX in 8 months trading range. It reached 4.05%. It might be in distribution.

4) A major correction might start in July.

Hi Wolf. With ST and LT rates going up again in response to high job numbers and higher for longer thought process, do you see more banks reaching out to the Fed facility for liquidity? If yes, any thoughts on timeframe? Thanks

Question:

Are the banks losing liquidity due to the “sport of the day”…..taking money from your money market or savings account and buying treasuries?

It would seem so.

If that is the case, the government is pulling money from the private sector …crowding out private sector activity. The big spending and big borrowing of the government seems unbridled.

Banks just have to pay their depositors more to get liquidity. And they’re doing it. All it means is that banks will earn less, and depositors will earn more. The free-money rip-off era for banks is over. It may be a bitter pill to swallow for banks and their investors, but that’s how it’s supposed to be, and how it used to be before the Fed decided to get into the business of brutally repressing interest rates.

How about the impact on balance sheet with decreasing bond valuation? That will question their lending capacity and solvency. Is this situation better than earlier when special measures were introduced by Fed.

Any thoughts? Thanks

Slow and Steady Wins the Race!

In case you didn’t know, the Fed’s website has a link for sending comments to the Board of Governors. Unlike the White House, which limits comments to a mere 2,000 characters, the Fed’s limit is a more reasonable 15,000 characters. I do not know whether comments from the public become part of a public record.

https://www.federalreserve.gov/apps/ContactUs/feedback.aspx

TNX in 8 months trading range :

May 26 hi – May 11 lo = 5.14.

June 1 lo + 5.14 = 40.84 min target.

Yesterday high : 40.83, or 4.83%.

QQQ might reach Nov 5/10 2021 BB : 400.99/387.53. Correction might follow .

Enjoy your work. Have you done or do you know where we can find total estimated Treasury issuance over the next three months and the composition of this issuance?

With TBAC guidance of 20% short term issuance (currently at around 17%), and as the months go by with more and more Tbills being rolled over, and with MMF not being able to go long duration, I am trying to understand when long duration rates will be forced to go higher and buyers coming from bank reserves instead of RRP.

I doubt with the large boost in manufacturing and construction jobs as plants are added to the economy will have an effect on the core CPI which is not reported . Could be that goods inflation had dropped significantly because of the ultra high base comparison figures. Deflation I read and understand is much worse than inflation . The fed has paused . CPI out next week . Core CPI will remain sticky . I expect a raise in interest rates in July regardless of the cpi close to 2 percent . The Fed has been very transparent. Wolf called the rise in long term rates that’s happening this week just a couple of weeks ago . Great call Wolf .

WOLF – this QT is anemic and pathetic. Where are the MBS sales (not just rolloff)? Housing prices continue to be solid in most markets. Homes sell quickly at very sticky high prices. FED funds is still negative and stimulative, not restrictive enough. In my market: Teslas everywhere, bars and restaurants are packed, no inventory of homes available and new listings at record lows, jobs a plenty, still don’t have to pay student loans (new plan will kick the can at $0 payments for most to buy votes) …what recession?…not even close.

Housing was going to go down so they threw everything at it, yet again.

There will be no price discovery.

The Fed bought MBS to prop up prices.

That’s how they force people to work in the economic war.

The elimination of Reg. Q ceilings was vitiated on the largely false premises on which deregulation is based, viz., that bank deposits in commercial banks constitute the “savings” of the depositors, that these are “lent” to the banks, and that the commercial banks are only a “medium” through which this end is affected [sic].

No one remembers the old days: “ONE CREDIT CRUNCH TOO MANY”. Re: “Richard P. Cooley’s 1974 speech: “Raise Interest Rates for Home Money” (President and CEO of Wells Fargo advocating raising Reg. Q ceilings – to steal another bank’s deposits).

But then we got Bernanke’s Romulan Cloaking device, the payment of interest on reserves, which induced nonbank disintermediation by giving the banks a preferential interest rate differential, the opposite of the solution for the first “credit crunch”. That will be the effect of an inverted yield curve.

Is it possible to break out the Bank Liquidity facilities in a separate chart rather than incorporated into the total Fed Balance sheet??

Or might be a separate blog entry on slow news day.

Chart #4 from the top.

Oh, the Green line! Many thanks.

$100B is sticky.

The Fed’s gradual interest rate increases are actually exasperating the very inflation problem that they are trying to correct. For example, as mortgage rates approach 8% the difference between the legacy mortgage holder rates of 3 1/2% and the current rate approaching 5% makes it completely uneconomical to sell or refinance your house. Moving, or trading up has been slowed to a trickle. Thus, no homes for sale. No homes for sale and increasing demand = higher prices.

Ignores the fact prices exploded when rates were low, and have been trending above the rate of inflation for a decade.

This ignores the fact, however, that those people not “trading up” are also not potential buyers, so there’s one fewer buyer on the demand side.

One other thing that is going on that no one is talking about. Banks and Mortgage Cos are not paying their bills on time. We have receivables that are 30 to 60 days overdo from major mortgage lenders. We are creating a “blacklist” of deadbeats.

I suspect some of that isn’t due to them not having the money, but deciding that they’d rather pay as late as possible given that they’re getting real returns on cash now.

I don’t believe in the price fixing of anything, including interest rates. The history of the Federal Reserve clearly indicates that it has repeatedly failed to maintain stability.

While there were some fools who bought those 30 year low interest mortgages, the biggest buyer by far was the FED, the very body who set those low interest rates in the first place. And who’s money did they put where their mouth was?

The free market would never set ridiculously low interest rates. But the FED did.

The free market could always set the cost of capital much closer to reality then the FED could ever do it.

Artificially low interest rates definitely hurts senior savers. Plus it motivates the movement of capital into much riskier investments. I don’t support artificially low interest rates.

I believe in the free market setting realistic interest rates, not some FED bureaucrats fixing interest rates far too low or far too high.

History us marked by repeated FED failures. They don’t deserve to continue to exist. Especially since they’re the complete opposite to a free market.

I believe in a free market economy, not a government controlled one.

The Federal Reserve does not set or even influence mortgage interest rates as those are all keyed off the yield on 10 year US Treasuries plus about 3% and have nothing to do with any rate set by the Federal Reserve. Most mortgages are only held about 10 years before they are paid off in any event.

What would you have instead of the FED? (Please don’t say gold standard….)

Also, you need to look at history. Sure the history of the FED has included some large mistakes and problems, but it was far, far, far worse before the FED. Before the FED there were regions of the country that would be devastated for a decade.

False. There were more panics pre Fed than post but they corrected quickly and overall growth was much faster. The Great Depression happened on Fed watch. We would be far better off on Gold Standard.

Any bets on what the unforeseeable crisis will be in 2024?

More inflation?

I was thinking more along the lines of corporate/government sponsored riots or perhaps a meteor falls from space and has some unimaginably horrible virus embedded in it.

The Bank Panic Support is not ending. It has been and continues to expand through the lender of “second to last resort” – the Federal Home Loan Bank.

You should do a write up on this bank, its branches, members, and it’s expanding “advances” to commercial banks. As of the end of Q1 2023, those advances topped $1 trillion.

The FHLB is a second Federal Reserve System financed with agency securities and treasuries. They can’t print money like the Fed, but they issue what the Fed prints to buy. Borrowing from the FHLB has currently topped the amount borrowed during the 2008 financial crisis.

In 2008, The FHLB borrowers list told the market who was going to fail first. SVB and First Republic were highest in loan size for the San Francisco Branch in Q1. Charles Schwab, US Bank, and Wells Fargo are in the top ten borrowers by loan size for the FHLB as a whole. Wonder what happens next.

This is a policy issue for regulators and Congress to address: Who should the FHLBs be allowed to lend to, and at what rate? Should they even still exist? Their original purpose wasn’t at all what they’re now doing.

The FHLBs borrow to lend. They can borrow at a lower rate — issuing bonds at a lower yield since they are “agency” securities — than troubled banks can, and then they can lend to banks at a lower rate than banks could borrow at in the market. That’s what is going on here.

For banks, it’s a cheaper source of funds than the bond market or depositors. Investors love those FHLB agency securities because they pay a little more yield than Treasuries.

Banks could still borrow in the market or from depositors but they’d have to pay more in interest. It’s padding bank profits by lowering the cost of funding. That’s all this is doing.

This issue is not a biggie on my list. It’s just another preferential treatment that banks get from the government, and just another way to help banks avoid market interest rates.

jimbo (Wolf)

We must have listened to the same podcast. Great summary, BTW. FHLB advances now exceed a trillion dollars (and they have not even reported Q2 yet). Wolf, would this be considered a bank liquidity program? If it is it’s already 10X what you reported under bank liquidity programs.

The following quote from FHLB’s website really grabbed my attention when you consider that current FHLB advances are higher than they were in 2008 and 2020:

“In the 2008 and 2020 crises, the FLHBanks were lenders of first resort and stepped up to keep liquidity in the market when other funding sources dried up”

Makes me wonder what they will say once this episode passes. Are other funding sources drying up?

FHLB advances to banks are not a “liquidity program.” They doesn’t change liquidity. Banks just shift their borrowing from one source to another to save some money on their funding costs.

FHLBs are part of “wholesale funding” for banks. Some banks can now borrow more cheaply from the FHLBs than from depositors. So they go to the cheapest source because it saves them some money. Liquidity remains the same.

Every dime that the FHLBs lend, they have borrow by issuing bonds. It doesn’t change anything, except the funding costs for banks.

So I just looked it up: The FHLB borrowed $1.46 trillion in the bond market, by issuing:

1. Short-term “discount notes”: $515 billion

2. Bonds: $944 billion

Like Treasuries, interest income that investors earn from FHLB securities is exempt from state and local taxes.

Just to note here: this $1.46 trillion in FHLB debt (“agency securities”) is not counted as part of the US national debt though the US government is on the hook for it.

Same with other “agency securities”: they don’t count as part of the official US national debt.

///

When you add 200lbs to your wight I am not sure a balanced and steady diet will do the job to get you back on track. But then again, it seems the FED has a weak spot for her abusive boyfriend from Wallstreet (he is somehow always in need of money)…I am not sure this relationship is going to turn out good for her.

///

that last spike in assets is going to be in the system for a long while. At the moment bond yields are rising as if the Fed’s two more rate hikes have anything to do with it. The Fed will probably dribble out enough rate cuts to make it look like forward (reverse) guidance, and pump the stock markets like it was 1995. The Fed is taking liquidity out of the system with an eye dropper, while supply chain issues and inflation put lift in the money supply and deflate the debt bubble. The real downside is zombie bank apocalypse with YC deeply inverted, there will be a recession, as this plays on main street, where Fed keeps driving up the cost of money.

I am waiting for FEDNow to be available so that I can transfer money between banks instantaneously.

This way, I keep very little in my checking account and keep most of my money in savings account giving me high yield.

I already try not to keep any money in checking which gives me peanuts in interest.

Financial innovation hasn’t changed money flows. Virtually all demand drafts still clear through DDs.

One of the reason SVB and other banks were in trouble because of bank run which was facilitated by online banking.

Now people don’t need to stand in line outside bank to take their money out. It all can be done with an app on your cell phone.

You should already be able to use Zelle for instant (free) money transfers between accounts at various banks. You can link savings accounts too, so that it would be transferred from savings to savings, etc.

Some brokers are also part of Zelle (Schwab Bank). I have not tried this function, but I’ve seen it there. You should be able to get money in to and out of a brokerage account a lot faster.

The FedNow system is going to be a lot broader than Zelle. It might finally move US transaction methods into the 21st century.

Thanks,

I have used Zelle but have very limited experience.

I should look into it.

I am amazed today with the dollar falling as it is, currently down .93 %, the FED hasn’t walked out a speaker to secure or drive it back up.

The hike or lack of a hike will be historic in many ways this time.

Do we save the 50% ish in trouble now or do we let them fall further and deal with the fall out later.

Have a nice sleep Jerome….let’s see who you REALLY answer to.

I often look at plots of value over the last 15 years and wonder why it all boomed around 2013.

I couldn’t remember much happening back then.

Then I saw Wolf’s article the other day about CMBS delinquency rates, and how it spiked into 2013.

BoJ and FRB went crazy on the QE kool aid in 2013.

What exactly was going on back then?

When you stand back and look at this what you realize is that there is a core problem – moral hazard.

All these Fed programs to offset market risk are exactly what causes the market to take on too much risk and then go into a tailspin. When people can lose all their money, they will stop with the financial manipulation.

The Fed is a private central bank and it is operated by bankers, for rich people. It doesnt care about anyone else.

We should not allow this institution to set monetary policy for the nation. The Fed should be wound down and ended and we should put in place a real monetary system that provides a currency that is 1) stable, averaging zero inflation 2) a good store of value.

Economist rail against deflation because it supposedly causes people to put of consumption and therefore leads to a lower GDP. I think that is a good thing. We have over-consumption. We need to focus on efficiency and savings, not more consumption. The tech industry has raging deflation – better products for lower costs – and it is the most dynamic industry in our country. So why is deflation bad? Deflation is only bad for monopolists that want to keep earning more and more money for less and less value creation.

Bring manufacturing back to the US by reforming tax policy and trade policies and labor policies (and healthcare costs) that push jobs away from our shores. That will be sufficient to maintain a robust economy.

Your characterization of the Federal Reserve is laughably false BS.

Nope. gametv is much more right than wrong.

SoCal…

Try watching the PBS documentary “The Power of the Federal Reserve” on the PBS web site.

Take note of former Fed Gov Fisher saying the Fed intentionally pounded long rates to FORCE investors to take more risk….ie skew traditional risk/return relationships.

BTW, the Fed is charged with keeping “moderate” long term interest rates…..ie moderate = not too high or too low. All time lows, pressed down by Fed suddenly delving into the long end of the market dropped rates to ALL TIME LOWS….and that ain’t “moderate”.

Great points and commentary.

“…are exactly what causes the market to take on too much risk and then go into a tailspin. ”

For the older folks, we know the Fed did not operate pre 2009 as it did since…..a new “ilk” took over the Fed and broke the rules, mandates, and traditional policies.

Do you guys think QE* as a policy tool to stimulate the economy is gone for the near future? The Federal Reserve will have at least 5.5% of rates to cut in the next recession. Especially if it’s a garden variety one, they shouldn’t need to cut more than 3%.

* referring to traditional bond-buying to lower yields, not Section 13 programs that might enlarge the balance sheet but are created for specific emergency purposes

The US moral hazard started when Nixon took us off the gold standard. What that really meant was the US was going pure fiat. It has taken some decades for us to dig the really big hole, but we’ve done it, just as a few had predicted.

All this is nothing new under the sun. Study history.

But pay close attention to what is happening in the rest of the world.

I am curious, what do you think is happening “in the rest of the world”?

Almost all other 1st world countries also have fiat currency. In fact, most countries have fiat currency (1st world or not).

Maybe you need better sources when you study history.

JimL,

Lemme guess what Mike R is thinking: The Russian toilet paper, aka ruble, is going to become the next global currency, supported by the Chinese RMB, and all of it backed by gold, LOL.

China is absolutely the last country on earth interested in switching to a gold-backed currency. China has built its enormous economic growth and development over the decades on a currency that can be created in unlimited amounts to expand with the economy.

I’m curious to know what was so bad about the economy in 2013 to require further QE so many years after the financial crisis. At that point unemployment had been steadily falling for 3 years, housing prices were finally starting to go up, stock market was well off 2009 lows etc. How did they justify it at the time?

Because you didn’t understand the significance of 2008. See my first comment on this article.

They thought they had found a magical elixir. Drive up stock prices and other assets for the rich, keep inflation low, the rich gets richer and everyone is happy. Or so they thought.

As I pointed out just a few posts up, something happened in 2013.

CMBS default rates spiked.

I’d prefer a “Wolf” revisit of what was going on back in 2012-2014 period, not speculation but the numbers that drove the policy to mean QE kept rising so fast.

Note the BofJ also spiked QE at this time too, even more than the FRB.

The unemployment rate was 8% in January 2013 & declined to 7.2% by October, when tapering was announced. This was still considered an elevated unemployment rate, so Bernanke had political cover to do it.

“I’m curious to know what was so bad about the economy in 2013 to require further QE”

Party on Ben! That was the deal. And the MMT attitude was in full play.

Bernanke promised, when QE was implemented in July of 2009….that rates would “normalize” and that QE would end when unemployment dipped below 6.5%. It went to under 4% and they kept the pedal to the metal. I consider that a broken promise…and not worthy of a Nobel Prize winner.

Normalized rates are rates, IMO, equal to or in excess of the inflation rate.

Trivia: there was no Nobel prize for economics in the original prizes, I believe selected by Alfred Nobel, the inventor of dynamite, but not sure if the types of prize were his personal selections: eg: chemistry, physics, etc.

But economics was not one of them, apparently last minute idea of the Bank of Sweden. I have also read that the Nobel family, his ancestors, want the prize for economics cancelled. This may have been influenced by the fact that Nobel laureates in economics were the brains behind LTCM. The latter almost crashed world finance when a Black Swan, the Russian default, sent its wagers, massively leveraged via derivatives, into reverse.

Looking at the bigger picture, here are my comments/opnions:

1. FED was quick to do QE and rate down but when it comes to QT and rate hike, they have been painfully slow and looking at the current economic picture, this slow QT and rate hikes are not as effective as one would think.

2. From 2008, the FED balance sheet have been on upward trend.

3. Although, it has gonw down some in last 1 year or so, I see the larger trajectory to continue i.e. FED balance going up and up.

4. It means the FED would start QE and rate decrease at some point in near future. It is needed to fun Govt massive deficit and sustain the wealth of their wealthy friends.

5. It also means that inflation may go up but inflation ( ie dollar losing value ) is going up for last 20 years. Just look at the numbers to see how much purchasing power dollar has lost in last 20 years.

6. Inflation can be easily controlled by manipulated govt metric. The true inflation is quite more than what the govt publishes.

7. In the larger scheme of things, currency devaluation is the ultimate goal which is happening slowly/fastly ( in alst 3 years ) but for surely.

8. Regarding #7, don’t take my words, just see how much value dollar has lost in last 20 years.

The dollar has been losing value since WWII. This has absolutely nothing to do with U.S monetary policy or even fiscal policy as practiced by congress and the president.

It is simply because after WWII the U.S. was the only 1st world economy standing. The rest were either 3rd world shithole economies or 1st world economies that were devastated by war (most of Europe and Asia). There was literally nowhere for the dollar to go but down. Eventually Europe and Asia were going to rebuild their economies and eventually economic evolution was going to come to the 3rd world shitholes.

The dollar is going down simply because the U.S. is no longer the only game in town. Other countries are modernizing and catching up. This shouldn’t be surprising.

The U.S. still has huge economic advantages and will for a long time. It is still one of the most dynamic economies in the world and can still provide huge economic upside if we ever get over the anti-immigrant flu many are suffering from.

I’m surprised you didn’t mention the Reverse Repo balance drop that almost mirrors the drop in the balance sheet.

It is around $1.8T dollars now, once that shock absorber is reduced to $0, we should see QT and deficit spending really soak up USD from the system.

I’m guessing we have 9-12 months left before the upward pressure on rates really kicks in.

Reverse repos are a LIABILITY on the Fed’s balance sheet. This article discussed the Fed’s ASSETS.

Aren’t liabilities just negative assets? If liabilities went down, doesn’t that count as negative negative asset growth, or in other words an asset growth?

Does it not work that way from the perspective of money added to the economy?

I highly recommend that everyone take at least a very basic accounting course at the nearest junior college. That’s really all you need.

So many mistakes were made.

1. Massive QE.

2. Massive QE after vaccine discovery.

3. Massive QE expanding despite inflation (transitory argument).

4. Continuing massive QE even after inflation proved non-transitory, into April 2022.

5. Keeping interest rate at zero till 2022.

6. Being self-deceived by the CPI number that gov had intentionally rigged in the eighties (real rate of inflation never went below 7% since 2009, was 18% in 2021, and is now at 10%).

7. QT done by raising interest rates too fast with a banking system not equipped to handle them.

8. Banking system not equipped because of regulations that incentived banks to hold treasuries.

9. Self-deception continues by looking at lagging indicators for the economy, masking inflation by draining the SPR, and mis-interpreting employment data.

10. Enabling unsustainable massive deficit spending by government despite it feeding inflation.

We are getting close to the end of a 40 year secular bull market. The secular bear will start soon, and it will be a completely different world in a few years.

Your post on Fed assets along with the 9/5/2022 post on Fed liabilities is a great primer on the balance sheet of the Federal Reserve. I would note that the drop in Fed Total Assets of $667 Billion in 15 months is only 7.4% of total QE so there is a looooooong way to go, and they are just back to level that caused SVB to implode.

Forget that 7.4%. That calculus assumes that they should take it back to zero. The Fed NEVER had a “zero” balance sheet, not even 100 years ago. The liabilities explain how low the assets might go. Inflation, economic growth, etc. keep pushing up the lower limit – and always have. The lower limit in a few years will be in the $4-5 trillion range. So what you SHOULD look at is the percentage decline from the peak to the possible low. And so the balance sheet decline by about 17% of the total amount it might ever be possible to decline.

Good point, but still a loooong way to go to erase QE. Interest rates are just reaching the levels again that caused the implosion of SVB and Signature Bank after the Fed’s BTL program jacked up liquidity. 2 year, 5 year, 10, year and 30 year Treasury rates are approaching new highs this past week. Could get interesting in credit markets soon.