Spring selling season was a dud. But what comes next may be worse, that’s what mortgage applications and investors tell us.

By Wolf Richter for WOLF STREET.

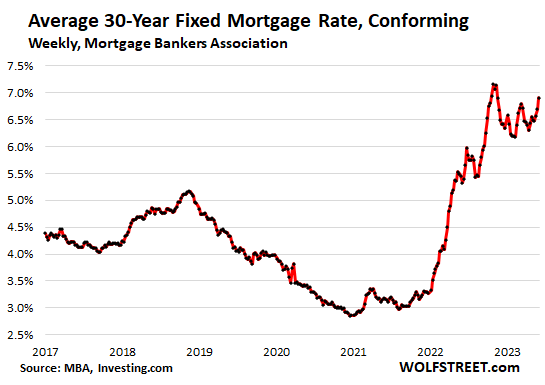

The 7% mortgages are back. The average interest rate on 30-year fixed-rate mortgages with conforming balances jumped to 6.91%, the highest since November, according to the weekly measure by the Mortgage Bankers Association today.

The daily measure by Mortgage News Daily already went over 7% a few days last week and earlier this week.

“Inflation is still running too high, and recent economic data is beginning to convince investors that the Federal Reserve will not be cutting rates anytime soon,” is how the Mortgage Bankers Association explained today what has been obvious to us here for months.

And so, with these kinds of mortgage rates, spring selling season – the time of the year when sales and prices nearly always rise from the dreary days of the winter – has turned into an amazing dud.

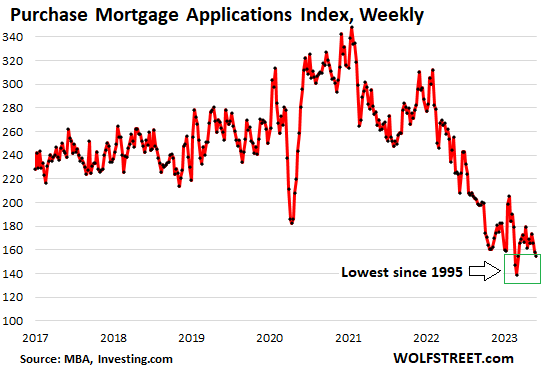

Applications for mortgages to purchase a home dropped for the third week in a row, from already low levels, to the third-lowest volume since 1995, the two lowest volume-weeks having been in late February this year, according to the MBA today.

Purchase mortgage applications plunged, compared to the same week in:

- 2022: -31%

- 2021: -41%

- 2019: -40%.

What comes next may get sloppy. Mortgage applications to purchase a home are a forward-looking indicator of where home sales as measured by closed deals are headed in a month or two. The 7% mortgages are indigestible at current home prices – something has to give, and it’s not going to be mortgage rates.

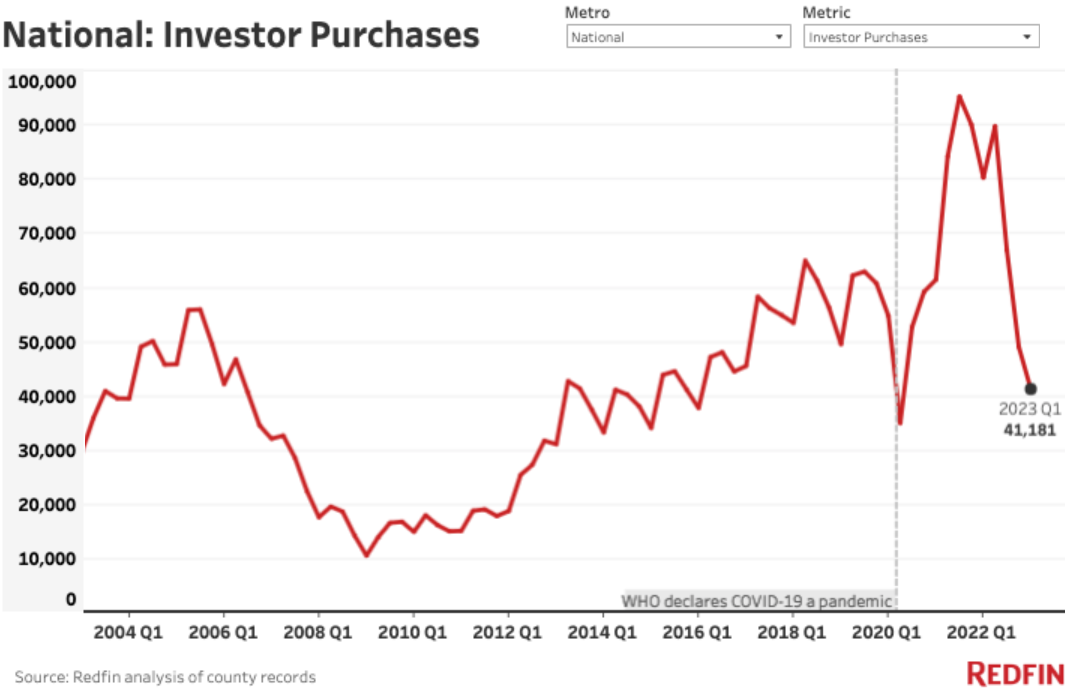

And the backward-looking data on sales volume, such as those by the National Association of Realtors, has already been lousy, amid rising supply, plunging volume, and increased days on the market, while even investors pulled out.

That investors pulled out of the housing market was confirmed by Redfin today: Purchases by investors plunged by 49% year-over-year in Q1 in the metros tracked by Redfin.

“Widespread economic uncertainty and recession fears are also prompting investors to pump the brakes. Some investors may be moving their money into other asset classes that offer better returns, such as stocks and bonds,” Redfin said.

The biggest year-over-year drops of purchases by investors:

- Nassau County, NY: -67.9%

- Atlanta, GA: -66%

- Charlotte, NC: -66%

- Phoenix, AZ: -64.2%

- Nashville, TN: -60.4%

- Las Vegas, NV: -60.2%

- Jacksonville, FL: -56.6%

- Philadelphia, PA: -56.5%

- Tampa, FL: -54.8%

- Orlando, FL: -54.7%

“Borrowing costs climbed even higher in May, meaning investors may pull back from the housing market further in the second quarter. Investor home purchases typically rise on a quarter-over-quarter basis in the spring, but we may see them fall flat or decline when second-quarter data comes in,” Redfin said.

So there goes that. The high mortgage rates had given rise to the theory that investors, who wouldn’t need a mortgage as they can finance at the institutional level, would just swoop in and pick up the pieces left behind by potential buyers staying out of the market. But that’s not happening. Investors don’t like to overpay for properties.

With the 7% mortgages now hammering the end of spring selling season, and investors pulling out on a large scale, home sales going into the summer could turn out to be dismal.

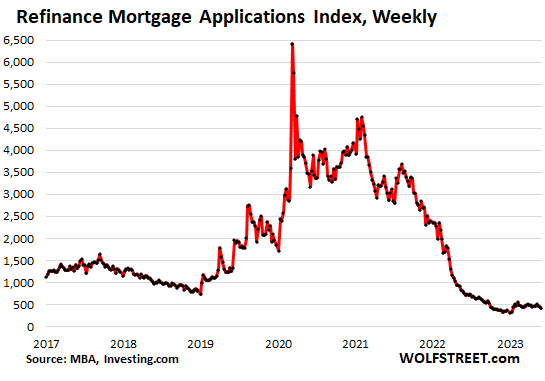

Applications to refinance existing mortgages collapsed in 2022, as mortgage rates surged, and have since then been wobbling along at the lowest volume since January 2000. The mortgage industry was among the first industries to announce mass layoffs in late 2021 and into 2022. Refinancing mortgages was a huge portion of the revenues for mortgage lenders and brokers, and it vanished.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wow, who could have predicted the rate of YOY rental price increases needed to meet the interest rates of a mortgage loan before this market would dry up?

As long as there are some folks with good credit, who can arbitrage the difference in payments, while socking away some equity, housing prices are going to stay up.

“…housing prices are going to stay up.”

Housing prices are ALREADY DOWN year-over-year. Go have a look?

https://wolfstreet.com/2023/05/18/home-sales-plunge-supply-rises-prices-drop-year-over-year-most-since-2012-even-investors-pull-back/

I think what he meant to say is the price to RENT a house is going to stay up.

limited supply since those who owned for over 3 years have nice equity and 3% loans

I might have to consider carrying mortgage at 8%

make more on interest than higher price

Then you have California. In Los Angeles…if property is priced right – you’re getting multiple offers….and inventory is low…so across the board – not all things are equal…but I understand across the country the market is not as competitive…

If it is priced right is the key word. Meaning, below last years prices.

Chill, Wolf.

The latest Freddie Mac National Home Price Index (FMHPI) shows the SoCal area (Los Angeles-Long Beach-Anaheim) as only 4.6% down from its peak in 2022. It was down 6.7% from peak in January 2023 but continues to climb back up the past several months.

For all intents and purposes, I can we can all agree 4.6% from peak can be considered “staying up” despite the mortgage rate nearly tripling.

Wake me up when we’re 10% down from the peak, and then I’ll agree with your statement that “housing prices are already down.”

Careful here. The Freddie Mac National Home Price Index” only covers home prices as they appear in mortgages guaranteed by the the GSEs. Prices based on cash deals, jumbo mortgages, etc. are not in the index.

A 2.9% drop nationally after a year of rising mortgage rates is nothing to really crow about. I know you like to revisit topics, but thus far residential housing isn’t nearly leading us into a recession. Let’s see how everything reacts in mid June. I for one am hoping for more inflation & rate increases. A recession is the only thing that’s going to break this cycle. And, the UniParty just wrote a blank check for two years. That’s going to be a crap ton of inflationary federal spending.

Price declines in residential housing will be limited. Rents are far too high and the labor market is still some what strong. Lose your job and can’t afford the mortgage? Rent it out and hang on to the low interest rate and make some profit on top.

Commercial is where the real price declines will happen.

C#dev

Hate to break it to you, but it is far less expensive to rent right now than to buy in many places.

This is Colorado for some crazy reason the prices there are down right ridiculous. Other states in West not so much. Makes no sense

Other states in the West not so much? Rolling eyes at this one.

“housing prices are going to stay up.”

You got it right, infact they are going higher as we speak. Check Zestimate, my Seattle house went up by $200,000 in last 2 months. At $100,000 / month, my house earns more in a quater than an average doctor earns in a year!

My house will earn more than a $1 Million this year. How many people is US earn as much? I now spend the whole day at Golf Course (working from home).

Only check Zestimates for true house value. Wolfstreet is fake news.

#Sarcasm.

tulips anyone?

Ain’t it the truth. The media acts like business cycles nd recessions don’t happen anymore. It has already started.

Seattle is San Francisco twenty years ago and not nearly as cool. Tech money+international

Investment makes owning home in the city limits a million dollar proposition. With the property taxes to prove it.

Hi Wolf, do you know how to invest in the government guaranties MBS? Are their yields at around 7% now?

I have been amazed at how much owners of properties believe that prices can only go up. There needs to be alot more properties on the market before the big price declines take root.

In my community there are a huge number of short term rentals that have completely distorted the housing market. This means that real people who want to actually live in a house are up against short term rentals that average around $700 to $1,000 per weekend. I’m in the market to buy, and there is nothing in my price range that is even worth looking at. This leaves me rooting for a bad recession that will kill the tourist short term rental market and force a lot of these homes back on the market.

Some people in my extended family are selling. They don’t have the 2.5% mortgages to worry about. In fact, they don’t have any mortgage. They want to capitalize on the high prices and sell while there are still buyers out there, rent, and put the proceeds into a 5% CD. The idea is to add to the nestegg and buy stocks when they tank, for potential huge gains.

Down to 6.88 in an afternoon update.

Ten year has fallen a tad, but the tsunami of new debt to soon be issued is still approaching the fan…

I think this may actually have the opposite impact to what you’d expect from a supply flood with money moving out of stocks and into t bills. Time will tell

Yes, time will tell. I’ll be surprised if demand grows more than supply, but I suppose it could. I wonder how the longer duration debt will be affected.

Like Wolf say, high yields solve demand issues. So it’s reasonable to think there’s going to be very strong demand at least domestically. High demand, leads to higher prices which pushes down yields. So over the summer, yields are likely to fall. More to follow.

Ben, are you suggesting that rising rates would lead to so much new demand that it would cause rates to decline more than they rose in the first place? That would really wacky. A more rational theory would be that rising rates will cause demand to grow, which limits the amount of the rise, but doesn’t cause it to reverse direction. As such, the increase in supply would still lead to higher rates, just not as high as they would gave gone if demand had remained fixed.

What happens to treasury yields when the fed starts flooding treasuries into the market?

Unless demand grows as much as the supply, rates will go up.

You mean the Treasury?

Expect Inflation to jump by 2% atleast.

The spending and inflation already happened. Issuing the treasury bills has the opposite effect by pulling trillions of cash (mostly bank liquidity) out of the economy.

The FED will lower the award rate on O/N RRPs to offset the gain in the Treasuries General Fund Account. Rates will fall as money flows falls.

There’s a surfeit of excess savings over real investment outlets. It’s called secular stagnation.

Nothing goes down or up in a straight line.

Except meme stocks, regional bank stocks, Nvidia, etc etc

I heard it said the stock market is priced 6 months out. So if/when housing stocks turn downward, I guess that’s when we will see significant price decreases.

Apple and Microsoft have been pushed to their limit and the FED wants the market higher still, soo they just switched to NVidia. When they pump that he moon, there will be another Wall St religion to take its place. And so on and so on as the S&P drills into the sky.

But when your layoff happens and you run out of Unemployment, it rather follows that if you have a Mortgage or pay rent, you a going to have to move. Then and only then will you see the animal spirts stir and House prices adjust according to the cloth available.

Only problem is there havent been that many layoffs and wages keep going up, so don’t ont hold your breath.

Maybe Nvidia induced AI can find the solution that our beaurocrats and politicians can’t.

Bernanke did a good job lowering housing prices in a straight line.

Wolf I know you are a man of precision so I am obligated to make you aware of a missing negative symbol on the last line item involving Orlando’s percentage.

Orlando, FL: 54.7%

For posterity’s sake.

Thanks for all you do.

Thanks! That negative sign fell through the cracks.

Can’t help but make the pun. That’s a negative sign for housing

Golf clap!

HaHA multiplied by all the other negatives = a + for a recession

Prices will give, but when?

Can’t get the price you want? Sit on it.

Don’t think you’ll get the price you want? Sit on it.

Layoffs of a larger scale will be the only thing I think that can move the needle here.

Prices are already down year-over-year, nationally. Even in San Diego, where prices never drop. Did you already forget?

There’s one place where I invest where prices are still up year over year, and that’s the Manchester NH market. Up 3.2% according to Zillow. Listings go to pending in 5 days on average. I’ve sold some properties and protected my gains- it’s hot now but I suspect eventually the price reduction wave will come there too.

Southern NH has long functioned as an outer Boston suburb for those people who can tolerate a 90 minute commute (each way) or only need to go into Boston occasionally. The epidemic drove a massive increase in demand for housing in the area as people fled Boston prices and the area is now supply constrained for housing.

Unclear what the longer-term picture will be as companies start to try and pull people back into their Boston offices. The Boston-based company I work for has gone from “will hire remote anywhere” to “Must be local to Boston, but can work remote”. I’m expecting that to morph into a full return-to-office in the next year or so.

My prediction is that the combo of return-to-office and high interest rates will crash NH real estate prices, it’ll just take a little longer.

Not sure how many Boston offices still allow remote work, but based on rush hour traffic on 128 and the expressway, I’d say enough folks are already back working in-person…

Zillow, thanks to Zillow sold home for a 74% markup. Zillow has a large hand in the RE mess and all you need is one idiot. Lots of smarts are sitting on the cash patiently. Renting is so easy and negotiable with great credit scores.

The recent tiny moves down on the housing price chart are barely perceptible when compared with the massive price increases since mid-2020. In my drowsy and relatively inexpensive flyover market prices jumped 40 to 70 percent during Covid and the true bargains, once fairly common, have become extinct. Did something fundamentally change? Was the Covid stimulus large enough to permanently alter the residential price level with WFH permanently altering demand? We’re going to find out, slowly.

“are barely perceptible when compared with”

Sure, it took five years last time. RE is not crypto. This stuff doesn’t move 50% overnight.

Actually, last time it took 3 years peak to trough and there were already plenty of deals after just a yer and a half

Now you’re trolling me. To your point, though, things are definitely lower here, not by huge amounts, but lower. inventory is about as low as it’s ever been.

Just imagine how it would be with a normal inventory.

Lower inventory is our legislator’s’ fault. Since the GD, our recessions are not self-correcting.

2.9% – Big deal! And so what that San Diego & 8 or so of the highest priced markets have dropped 13-18%? Overall, housing is holding its own just like the labor market. The parallels are very similar. Big drops in a handful of areas that have slowed with the rest having small declines. Core Inflation has found its floor resistance level. Everything points to small increases in inflation as the summer progresses, but you already know that.

As Richard Russell told me, La Jolla is getting crowded. I lived across the street from Children’s Beach when I grew up.

You people with your crypto attitudes are so funny. If something doesn’t collapse by 50% in three hours, you don’t take it seriously? LOL

This stuff in RE takes YEARS, not weeks or months. Last time it took five years. The RE industry spent the entire first year of it talking about the “high plateau.” Instant gratification is for cryptos.

You’re 100% right, I should’ve clarified a little better. When will prices get back down to affordable levels.

I’ll do some annualized forecasts today and see where we could be at the end of the year.

Wolf, with the economy cooling by the day, consumers very uncertain about their financial futures, and Washington burning almost to the extent of the War of 1812’s visit by the arson prone Brits, it is hard to believe that home prices will hold up in the months ahead. And I don’t think we have seen the top in mortgage rates either, 8.5% to 9% are not out of the realm of possibilities. I personally am looking to buy when prices are down 20% to 30% from the local peak: Take a Zillow price graph, fit in a non-spiked normal price trend before Bubble Two struck, and see where that normalized price should be today.

Home builders for New Homes are much more pragmatic on home pricing than the majority of Existing Home owners in this crumbling real estate environment. Many building supplies, esp. lumber, have come back down to earth, some flat to below the pre-Pandemic supply chain and production shortfalls price levels. And national level builders have rather deep pockets so they can bargain with the dwindling numbers of prospects that show up, so that a deal will more likely than not get done. They can throw in “soft money” like a free sunroom or mother-in-law suite over the garage to sweeten a deal. They can even rent you a more good-natured mother-in-law to occupy that space!!!

So Americans in the market for a new home should go beat a home builder up (figuratively, only, please!), and not look to spoiled existing home sellers to get real on their asking price anytime soon.

I am starting to believe that home builders might be in a very good place right now. There is such a dearth of properties for sale and so potential buyers are pushed into new home purchases. And if people are leaving high price urban areas for more rural areas, where there is more land to build, that keeps the land cost down for developers.

I also heard on a conference call talk about going in and renegotiating all the of costs of building a home downward, so they can reverse some of the price escalation.

When you think about asset prices, you need to realize that everything is priced on recent sales, which account for a tiny portion of the overall asset base, so what will really change prices in stocks or real estate are rather small changes in the supply demand curves.

My theory now is that higher long term interest rates will be driven by too much supply of Treasuries once the Treasury starts to sell them again. This leads to much higher interest payments that cause an unsustainable deficit burden.

Game, the problem with home builders is margins are declining rapidly because they are buying down mortgages in order to sell homes. It’s the equivalent of eating large price declines. Despite that effort, backlogs are declining. Lower price and lower volume is not a good mix.

When the downward price trend is more evident, existing homeowners will increase selling, and builder share of home sales could decline from current elevated levels.

Layoffs of a larger scale will be the only thing I think that can move the needle here. ==> I don’t think so as the prices are already down from the peak.

Even with no lay offs, prices would come down gradually. The simple reason is un-affordability.

At the same time, we need more and more suckers to enable price discovery.

The vast majority of home owners can’t “sit on it” when they have to sell for a myriad of reasons that have nothing to do with layoffs.

Many posters here are ignorant of the true financial condition of most Americans.

Yeah yeah, salad days…

Ever been divorced?

Took 5 years from the start of the SHTF last time for prices to hit bottom, so figure just as long this time. Higher rates really haven’t worked their way thru the system at this point, figure it’ll be a while before defaults, foreclosures, layoffs, etc, all spike.

Took just over a year from when the Fed stopped raising rates for them to start slashing too, and at this point they see no emerging crisis yet, so tack on another year.

The interest rate cycle is just getting started, unless someone believes it’s another “head fake” and rates are going negative, below 2020 levels.

The last up cycle to 1981 started in the 1940’s. Given the much worse fundamentals now vs. then, rates are destined to “blow out years from now.

No, it won’t happen necessarily overnight, but any surprises are almost certainly going to be higher.

>Layoffs of a larger scale

So I had to visit quite a few places around lately – from local DMV and local schools here in NC to some landscaping and related businesses.

One common theme I keep hearing EVERYWHERE is along the lines of “staffing levels are terrible / we only have 2 people in a 7-people office / we can’t hire anyone even for the summer” etc.

I honestly don’t understand what’s going on. Have people all of a sudden become VERY rich and just quit working? Or are they all concentrated in some industries (that should then be “oversaturated”) leaving other places catastrophically underserved by able-bodied individuals?

I mean, if all those places are really struggling to hire, then how can we even talk about “layoffs”? Yes, of course, I get it that someone laid off from a $250k white collar job in finance would unlikely to apply to DMV to work as an intake clerk for $16/hr, but I don’t see that person dying from hunger either.

I am genuinely confused, probably to the extent I’ve never been all my life.

Yes, I’ve seen the same!

As long as the FED can keep juicing the market higher, then the wealth effect ghost will keep people on the treadmill. As long as the corporates can keep turning one full time job into to part time jobs, then the job market will continue to look super.

7% is a very low, stimulative interest rate historically in inflation periods like today. The 1980 approximately 14% housing interest rate coupled with lending standards of payments no more than 20% of gross income had a calming effect under Volcker, something that worked very well for a decade when 1989 was still 10%.

The Federal Reserve has a long, long, long way to go, especially at a 0.25% snail 🐌 rate. How those who were alive then realize what a strong, bold. genius that Volcker was.

Couldn’t of said it better. The current Fed needs to do take a course on the teachings of Paul Volcker, said in full seriousness. He understood how to run a central bank, above all the top rule that you never, ever “go slow” to coddle the speculators or you risk permanent damage from the inflation and even worse, a steady erosion of the currency and confidence in the country. Doing the right thing, and not coddling elite speculating pals and corruption is what differentiates a first-world central bank (or at least it used to).

We’re seeing that heavy damage from inflation in the US now, the writer’s strike in LA is direct result of the inflation and the writers there practically starving as rent and grocery prices soar and incomes don’t keep up. Shoplifting is epidemic and American homelessness are soaring. And foreign countries are gradually losing patience with the US dollar and USD denominated assets–they can’t risk exporting inflation or they’ll face social unrest, that’s why Bloomberg’s been reporting on so many countries in Asia and the Middle East refusing the dollar for transactions that used to be standard, requiring local currencies or other alternatives. (Again it’s not a matter of a single other currency replacing USD, it’s the death by 1,000 cuts to USD as they lose more and more confidence and look for multiple alternatives)

If Volcker was the Fed boss today, it’s possible he might’ve also been cautious about pushing the rates up too fast when SVB and the bank failures started (although those failures were their own fault like Wolf said, for buying into the dumb “pivot hype” and not preparing their reserves properly). But at the very least, he almost certainly would be much more aggressive with QT like other central banks even Canada have been. That’s a much more obvious call and it’s better targeted at the asset pumping of the speculator class. And he certainly would be starting the tightening a lot earlier and not brushing off the inflation as “transitory” the way Arthur Burns did. Powell at least has been taking action against inflation which isn’t something that Greenspan, Bernanke or Yellen did, but so far it’s still been way too little too late and still too much coddling of the speculator class with the slow walk of QT.

Agreed. You won’t hear this on regular media outlets. It would be considered “mis-information” by the AI’S before it was released.

My mentor was flown to meet with Paul Volcker in early 1980. Volcker was as ignorant and arrogant as his predecessors.

You can’t compare current Fed leadership to Paul Vocker because the goals have changed. The goal in Volker’s day was to foster economic growth consistent with long-term economic potential. Today, the Fed’s goal is to avoid recession no matter the consequences.

1) The biggest y/y drop is concentrated in FL : Jacksonville, Tampa and

Orlando are over 50% down. Hurricane Ian hit that region last Sept.

2) In the last year and a half “Real Consumer Spending” is slightly up from :

$14T to $14.35T. Gov debt is rising faster. High Input / Low Output.

3) Long Island Nassau county home owners have a target on their back for decades. Nassau county got respect, a symbol of success.

4) As long as home prices were rising, reaching the millions and tenth of millions, home owners didn’t care. WFH was great. But things changed. Owners started to complain about the high assessments, high mortgage rate, high inflation, slow traffic ==> after home prices start falling. Nassau RE market is dead.

Actually, Ian affected the Naples/Ft. Myers area. Further south of Tampa.

Good. I live in Nassau County, let all these investor fcuks gtfo and let prices come down so some of us hard working blue collar folk can have somewhat of a normal life without spending every last dime and dollar we have just to pay the mortgage and utilities. It’s 599-700 starting prices for homes in the Bellmore/Wantagh area, and with crazy taxes plus the interest rates, it’s unaffordable.

Mind you a lot of these homes were built in the 1920s, and another boom starting in the early 50s. $550,000 for a 1923 home that hasn’t been renovated in some 30-40 years. Of course you gotta go through all sorts of back channels to reach the owner directly and maybe strike a deal because RE Agents want no part of that, they want you to believe the seller will not negotiate because their profits are at stake.

Not sure you fully understand the real estate agent “beast”. They traditionally get 2-3% commission per side (listing agent/buyers agent). They’d blow the sellers brains out to garner a sale. After all, $100K reduction only produces $2-3K for the agent (unless they’re on both sides of the sale). However, they’re not going to blow a $15K commission to make an additional 3.

The old “bird in hand” theory in practice.

Just like inflation I think ppl will adjust to mortgage rates and those that need to move on will sell, and price discovery at the margins may have a loosening effect on sellers price expectations. Then, perhaps, the maxim that those who panic first, panic best.

It’s gonna be a few years and the high rates are gonna slow.price discovery. I just wish the fed would sell bonds for reasons of.price discovery and overall economic health now while consumer and job market is strong. They are procrastinating to protect the ownership classes. Just bad for the economy.

You wish the fed would sell bonds during a booming, healthy economy so they have room on the balance sheet to buy them again when SHTF as it always inevitably does in our boom and bust cycles of capitalism?? No wey, José, the fed doesn’t think logically like that. THE CLOWN SHOW MUST GO ON!

“We have tools” – in other words Fed just pushes a button when it’s macro-prudential time and voila, everyone is flush. The younger generations already accepted the magic money tree snow job, so nothing to fear there as they get further behind the asset inflation curve. No need to sell bonds; I can readily imagine them doubling the balance sheet again. Which Congress critter would get in their way?

“I just wish the fed would sell bonds for reasons of.price discovery and overall economic health now while consumer and job market is strong. They are procrastinating to protect the ownership classes. Just bad for the economy.”

Agree totally with this. Even though JPow gets credit for at least taking action on the interest rates, it still hasn’t been enough and it’s the QT even more where the action has been terribly inadequate. The Fed should have never been in the business of buying MBS’s to begin with but once QE began to reverse, should’ve been a lot more aggressive with QT. Even Bank of Canada has been doing more aggressive QT despite Canada’s mis-allocation of it’s economy and near reliance on a constant housing bubble. US inflation is still way too high and it’s crushing millions of Americans, rents, cars and groceries are ridiculous, homelessness and people living in vans is hitting record levels, shoplifting and crime are up so much that shops are changing their customer policies.

The writer’s strike in LA is a direct result of the Fed’s failure to control inflation, people just can’t afford these soaring rents out there and there’s no end in sight. Homeless tents everywhere throughout the LA county now. Talked to some people in the industry out there and the writer’s strike is doing permanent damage to US film and entertainment industry, a lot of it’s going to move abroad and tons of projects getting cancelled. Strikes and work stops now forming in other industries too. And then if that wasn’t bad enough, countries in Asia and oil producers dumping the US dollar for transactions, moving to local currencies or other alternatives for good. They can’t stay with a currency that’s losing value and exporting inflation to them.

If Powell is slow-walking QT to protect the asset speculator class, then he’s sacrificing whole American industries, shops and the USD itself to do it, which would qualify as the worst monetary policy choice in modern history. He can help a few thousand rich speculators make even more billions or he can save US industry and the dollar, he can’t do both–monetary tightening is supposed to put a brake on the wild speculation, that’s how inflation is broken to begin with. Volcker would’ve easily known what choice to make. The interest rate hikes need to be more aggressive but that’s especially true for the QT.

Perhaps sellinh mbs would be even bettor.

Great article. Will not make real estate speculators or agents very happy. But they had one heck of a run.

If I am not mistaken, all interest payments are a write off / tax deduction for investors. So, if prices go down but rates are high, wouldn’t I make sense to buy as an investor. And have the option to refinance in the future.

Properties need to cash flow.

Properties need to cash flow. Yes. But isn’t that a function of how much you put down? If you buy in all cash at a lower price (and higher rate) you have cash flow…..and you have the opportunity to do a cash out refi later and re-use the cash. My whole point is: yes, investor purchases are waaaay down. But since rents haven’t really come down significantly, it seems to me lower RE prices are a reason to buy more RE not less or even sell?! If you are an investor.

What’s the difference between that and buying TLT, then selling when (if) bond prices increase? If cap rate on RE is low or negative, why buy what looks to be a falling asset? Sounds like a headache.

Oh, I know, a 30y fixed and low/no down could reduce liability and loss, while multiplying with margin. It’s only predatory lending if RE prices tank, right?

“Investor purchases are way down, [yet investors should be buying more.]”

Sounds like an arbitrage opportunity if I’ve ever heard one. How many properties do you plan on purchasing?

Keep in mind, 5% risk-free rate of return is a game-changer.

Why should anyone invest in and landlord a property, when they could earn a similar yield investing in treasuries and not have to do any work?

If you bought your house to actually live in, its different.

It really depends on the market you’re investing in. In some markets the rent one can get on a new investment doesn’t have a great cash on cash return. The market rents one could realistically get haven’t gone up enough to keep up with the sharp increase in prices.

I agree Rick – hence my firm position that home prices must come down, AND rents must come up for things to be more in balance.

No, it doesn’t make sense “when prices go to down.” They just started going down. This will stretch out over years.

It makes sense “after prices have gone down all the way.” Or at least close enough.

The PE firms that jumped into it, didn’t jump into it in 2007, just after the top. They jumped into it in 2012, just after hitting bottom.

This will take years. People don’t get it. It took over a decade of free money to build this inflation and asset prices, and it’s going to be a long decade going down.

Thanks Wolf,

Yeah, that makes sense to me: if investors believe prices continue to fall, then why buy now. But that sounds to me like timing the market.

@Ltlftc

I am not buying investment properties. In fact we just bought our first house and I consider myself house-poor. It doesn’t stop after buying the asset…..backyard/landscaping, furniture and a million other small things.

I am just interested in hearing/understanding the subject. You said, “when cap rates are low”. But if net income on rentals remains elevated (since rents haven’t come down significantly) why would cap rates be low? Prices have come down some so cap rates would be higher. The only reason I see why investors don’t buy right now is if they believe prices continue to fall. That would make sense to me. From what I have seen (and I was in the market to buy) …..it’s been very competitive out there. There isn’t much choice (low inventory). Basically, very low demand and very low supply. Agents and brokers are hurting due to extremely low transaction volume. Wouldn’t be surprised if there are more RE agents than buyers out there ;)

You know, someone here told you that you picked the wrong time to buy. I don’t understand since you have already bought why you are on this forum, you should be enjoying your new house and life.

In my opinion, correct me if I’m wrong, you have realized that you were wrong with this rash purchase and now look for someone to back you up and convince you that you were not wrong.

Hi Juliab,

Yes, of course “someone” said I bought at the wrong time or at the peak. “Someone” who believes prices will crash hard, will tell you this. Has happened on many forums/websites/blogs. In fact, I believe people buy and sell daily and when you share your purchase story online you get comments like “you will lose your equity”, “you will regret your purchase”, “you must be an undercover RE agent”, etc, etc.

Yes we are enjoying our home. Why can’t I post here anymore while enjoying our home at the same time? I never advise anyone to buy or predict the market. Truth is, I have been following the market for quite some time and have done a lot of research. I am very interested in the subjects pertaining to the economy, markets, stocks and RE. For us, buying was the right decision because we could afford it and we were longing to have our own house. For others the situation might be very different. You have to do what’s right for you. Making assumptions about people who bought or don’t want to buy are silly because you simply don’t know that person. For instance, you said I made a rash decision but the reality is we were wanting to buy for years. We just weren’t in the financial position to buy sooner. I see this “mind-reading” all the time. I asked a question about investors and was quickly asked how many homes I am planning on buying. I am in no financial position to buy homes but if you have a different view or ask questions from a different angle you often get judged too quickly. That’s just how the internet works nowadays :)

Richard

I understand, I didn’t mean to offend or criticize you for anything.

My experience in this field is recent. In 2013 I sold a property and I was very happy about it. Until I realized I had sold it at the bottom of the market. Of course I found out about it years later. And then I started reading about this market. I learned that it is the slowest market and that there are always alternating peaks and troughs. The trend is positive over the years, but it always happens that the mass of people buy at the peak and sell at the bottom. This is because most of them are not clear about this market like I was. What I know for sure is that we will never see the prices of 2012 again, but I am also sure that the current prices will not last long.

So I’m really happy for you.!

If you are going to live in your new home for a long time,

I would advise you not to follow the price movement in this market anymore. It was my mistake that makes me still follow these prices and blame myself for making this mistake.. So just enjoy life.

Richard:

Apologies if I come off a bit rash.

“why would cap rates be low?

…

Prices have come down some so cap rates would be higher.”

If someone is purchasing a property all cash, sure. If someone is financing, they’d have increased finance costs eating into their cap rate. Taxes and upkeep costs would have most likely risen as well.

“The only reason I see why investors don’t buy right now is if they believe prices continue to fall. That would make sense to me.”

That would be my thoughts as well. We will see.

You are talking about cash flow not cap rate. Cap rate is NOI/purchase price.

Some calculate it by dividing NOI by market value of the asset.

Richard:

Thanks, I stand corrected on cap rate not including financing.

@MM

“ Why should anyone invest in and landlord a property, when they could earn a similar yield investing in treasuries and not have to do any work?”

You can be an investor in rentals and not “landlord” the place simply by hiring a property manager. As far as the yield goes. Say your cap rate is similar to treasury yields, why even bother? Well there are other reasons why: interest payments are a tax write off. Housing value of the investment is being depreciated (lowers your taxable income) and you pay 25% down on the property (typical for investors) but you pocket 100% of the appreciation of the asset. I am not saying to do either or. I have some money in CD’s myself and I don’t own rentals. I am just saying there are other reasons why RE investors prefer to invest their money in RE instead of high yield CD’s.

It would, the best time would be to buy the property at the height of interest rates before they start decreasing. Theoretically it would be when home prices have ranked the most and then refinance the debt as interest rates drop.

That’s right, but you’re missing one detail, which is that housing prices must be at or near rock bottom

While prices are down year over year, according to the Case Shiller indexes nearly every major city is going back up now. Even places like Seattle, Phoenix, LA, and San Diego. A few saw month over month increases of over 1%. Some cities have been going up for several consecutive months.

So the question is…is this just the last hurrah before the crash?

Nothing goes down in a straight line.

We need suckered for price discounts.

It would happen even without big job losses but it’d be slow process

Spring bump. IIRC it also happened after HB1 popped. Housing is a very slow, lethargic market with a sunny-breakfast-nook mentality.

Kernburn,

“Spring selling season” during which prices almost always go up.

But prices went up LESS than last year at this time, and so year-over-year, prices declined even more.

“But prices went up LESS than last year at this time, and so year-over-year, prices declined even more.”

That’s a plain lie. Go check Redfin data center and look at median sale price or median sale PPSF.

www dot redfin.com/news/data-center/

Both metrics are rising much faster than in 2022 and 2023. I really believe that all RE crash forecasters will be proven wrong in the end. RE prices are rising at the fastest pace right now.

San Diego, median price, month-to-month, from the California Association of Realtors:

Mar 2023: +4.6%

Apr 2023: +1.6%

both months: +6.2%

Mar 2022: +7.0%

Apr 2022: +2.6%

both months: +9.6%

Year-over-year:

Feb: -1.5%

Mar: -3.7%

Apr: -4.6%

Adios.

Kunal — you’re just rude.

It’s the spring season when prices and deals always go up. It was the same during the bubble of 2007.

And yet, this spring season has been a disaster

Disaster for those that profit from high sales volume and hurt when sales are down. We have/had too many RE agents anyway. Sucks for them but there were just way too many. I’ll never forget my conversation with our first “buyers agent” many years ago. “People buy and sell every 5-7 years”…..I said, why? If I buy I have no interest in selling that quickly, I might never sell and try to rent the property out if I have to move. He didn’t like that answer at all. Of course they want you to buy with them and then sell after a few years so they become the listing agent. Lots of transaction volume means $$$ for them. Now this has all changed. People stay put. Higher rates encourage people to not sell unless they have to. This trend of moving-up-the ladder and selling for tax free profits after staying two years in your primary residence has ended. And many RE agents and brokers have to find a new career.

Where the heck are all the foreclosures? We had years of moratorium and high flying prices to all but eliminate the need to foreclose but now with prices falling and banks given the all clear it baffles me why we don’t see at least foreclosure numbers back to 2018-19 levels? As an agent I make some income from commissions but the lions share comes from purchasing foreclosures at the court house steps, repairing/upgrading and reselling. Flipping. I prefer a falling market as it is easier and almost no competition.

Back in the day ( 2008-2013) banks refused to approve most of the short sales and my insiders told me they would have to log the loss so they would rather have a vacant home with all the expense not to mention the loss in value each month as homes declined rather than approve the sale and stop the bleeding. One underlying reason was bonus’s are tied to the departments profit / loss so with no skin in the game department heads would serve them selves and decline as many short sales as possible never thinking about what is best for the bank as a whole.

Could this be happening all over again with foreclosures? The bank doing everything possible to not get the house back and log a loss. This fall and winter could get ugly and you most certainly will see the words ” Short Sale ” in the news and who knows maybe the word ” Contained”.

The banks are just the servicer so they really are telling the investors ” No need to sell now just wait till this little Gully clears up and you will be just fine”

Lol, in 2008-2011 you could literally walk into Wells Fargo and ask about current foreclosures. They had thick binders full of them (saw personally).

Not quite sure what approval you are referring to. One thing is that, they preferred to package them into a portfolio of properties, so maybe that was the holdup.

Short sale approvals, not approvals for foreclosures. I was deep into short sales as was most realtors at the time. Sometimes I just ramble. Funny how most realtors wouldn’t lower themselves to handle a short sale at first, then fought over them two years later. We may see them do the same thing this go around. I’m not one to think this is just a speed bump or gully. It will take years to play out. We are already one year in.

My first attempt at buying was around 2012-2013, and we were told to ignore short sales beause the bank sits on the application for months on end before inevitably rejecting the app over any little thing.

Back then, short sales made up almost half the listings in our price range, it was quite frustrating, we didn’t bother viewing any of them. What was left available was rough, but not like these days.

A friend managed to get approval on a short sale a few years later after viewing well over 100 homes, and it still took the bank almost 6 months. She said in more than a few homes, the places were trashed and previous owners would flush concrete down the toilets in angry spite. Crazy stuff back then.

I knew a guy who ripped copper pipes, counter tops etc. Then did the trick with concrete in sewer pipes. That is of-course after living there for 3 years without paying mortgage, taxes etc, since he got a lawyer to keep extending it as long as possible.

He didn’t hurt bank, he only hurt the next schmuck that had to rip out sewer pipes. For that one, i hope Karma gets his as* one day. Then bought another house under his wives name when it was all said and done. Crazy times indeed.

Saw a few instances of ripped out copper, sabotage and straight abandonment of belongings, in our price range what wasn’t short sale was pre-foreclosure desperation sales, or renters bagging out as landlords sold. Guess people didn’t want to pay movers to move their stuff so they sold as is, loaded up the car and drove off leaving what they couldn’t fit. Lots of abandoned flips as well. Something in my gut tells me this will happen again someday.

You make a great Point.

The main reason why house prices have not fallen off a cliff is banks refusing deals because that means they would have to mark to market their entire RE or MBS portfolio which would be, let’s say, nasty. This is the “hold to maturity” scam , the RE / MBS version.

This will continue until someone blinks and decides to sell it all, today.

Shouldn’t the banks/MBS holders *want* people to stay in their homes?

If I suddenly couldn’t afford my entire mortgage payment, but could still afford 75% of it, I imagine my mortgage servicer would rather take what they can shake out of me, than take the house itself.

That’s pretty much what banks are doing in Canada already

The bank will squeeze every last penny out of you, rest assured. You will pay for everything with the interest, they will just give you more time, a lifetime

Good, would love to see 10% or more for 30 yrs fixed. Maybe then it will have a chance to bring prices in SoCal more in line with reality…as always not holding my breath on that though…

When interest rates rise, housing prices do see a drop, but you have to do the math. Low interest rates balance a lot of higher home prices. A 10% mortgage would have to see a much lower house price than I believe they would end up dropping to.

Right now house prices have fallen, but the total cost to the buyer is not any less. go to a Mortage calculator and play with the numbers to see how much a mortgage actually costs over several years. It is often shocking to see what the house actually costs compared to what you thought you paid for it.

Yes, when rates go up, prices fall, but they fall to a degree that you still have a higher monthly payment than when rates were lower. We recently sold our house, and all offers were from people pretty dependent on financing (20-35% down payment). For buyers like this, rising rates create urgency. For people closer to cash buyers, it’s the opposite.

An actual end to the asset mania (which includes housing) would go a long way to achieving that. There is a lot of fake wealth supporting higher real estate prices and it’s not just in NYC or Silicon Valley.

Out here in my little slice of flyover.

The slow down started in early spring.

Typical backlog at this time of year would be 4-6 weeks.

We are back down to that time frame.

If we were youngsters that backlog would be less than 1-2 weeks.

For health & sanity, we have reduced hours, and increased rates.

Majority of work is still new construction.

Average age of my clients has dropped significantly with

the higher rates. Kids who can do, along with friends & family. Most builds are back down to that 1800ft2 or less. And of course

a lot of shouses.

Charting 05-06 rate increases – to collapse v.s. 22-23 rate increases…

would appear the impact is sooner….severity…yet to be determined.

I believe the reason one of the reason’s prices haven’t fallen significantly is that the builders are buying down the first few years of the mortgages, thus instead of 7% they are paying 3-4 % until it resets in a few years.

I doubt a prudent bank would make such loans as these borrowers are counting on the rates dropping by reset time, and if they don’t I imagine there are going to be a decent amount of defaults- however Fannie and Freddie buy the mortgages so the banks don’t need to care. Also, if the rates do drop in a few years then prices will have likely also dropped and those sales today at high prices are going to be underwater and will be difficult to refinance as well. Also looks like some of the major builders have their own financing divisions also willing to make these bought down loans that otherwise won’t make sense to be allowable.

Point being this is preventing higher rates from bringing prices back to the pre pandemic levels. Which is not a good thing for the percent population that wasn’t lucky enough to already have a home locked in at a low rate, and are now paying more and more for rent.

That’s something I’ve noticed in my part of NC. I saw a listing for a new construction ‘move in ready home’ offered with a 30 year fixed at 4.99% (BTW I hate numbers like that) when financed by the builder. Based on current rates I believe that essentially drops the P&I by about 25%. That’s a pretty big deal for the buyer, and it seems like the builder is absorbing a risk associated with future cheap money availability.

Hello Wolf, Just wondering if you have read John Hussman’s last 2 market comments in regards to inflation? Thanks!

I always enjoyed Hussman’s writings, especially his last one. I don’t think that this cycle will be over til he makes a come back. It must be tough for him to watch financially ignorant people stay all in on the stock market and get bailed out by Fed every single time. Making money can’t be that easy.

I once admired Hussman until I recognized that he (and I) are so last century before the benighted notion of scarcity was overcome for once and for all. SVB in trouble? Pshaw! We have tools!

Hussman’s old school.

It now takes increasing infusions of Reserve Bank credit to generate the same inflation adjusted dollar amounts of GDP.

Old school

He (Hussman) under estimated the speculation mania based on ZRP and multiple QEs. I am also a victim of similar thinking, until too late.

The rules of the investment GAME got abruptly changed in the March of ’09. I also, under estimated the the effect on assets with the ‘prolonged’ very low price of the capital (ZRP, rate suppression by multiple QEs) I also under estimated how the Fed murdered the free mkt capitalist system, in order to bail TBTF Banks. All these were/are alien to me (being in the mkt since ’82)

Look at the S&P Chart and starting points of institution of various QEs, stimuli, twists and what NOT! Uncanny correlation!

B/w Fed had bought NO MBSs in it’s entire history since 1913 until ’09. QE is/was neither based on past record or a research but product originated from the seat of pants of Barnake. There had been no suspension of mkt to mkt accounting standard until March ’09. Credit mkt is the foundation of Equity mkt. Debt/Credit became the panacea for all the financial problems through out the world for all most 14 yrs, with 2% inflation.

Now the counter effects of those monetary decisions are being un-winded slowly with ‘reversion to the mean’ with mirror reflection of the past decade.

How serious and how long the consequences of ‘insane credit’ creation and distortion by the CBers, will be on the US/Global economy, is any one’s guess!? Will there be SOFT, HARD landing or worse? Hope for the best and prepare for the worst.

I do my own research.

What makes your ‘research strategy’ different from that of Hussman’s?

just curious!

Thanks.

They will drive those mortgages sub 7%, just like they did last year. Lenders figured out that 7% is no mans land. Based on my observation, 6.69% is apparently make it or break it for many homebuyers…

How are these borrowing rates are set in general? Supply and demand? We are 2 or 3 FED hikes later and just now mortgages rates are back to 7% territory, so they aren’t quite corresponding to FED rate.

6.69%?? Giggity!

Don’t hold your breath. Rates are going to be around 8% by Christmas if the FED does one more increase this year.

Believe me, i wish they were 8%. There is still too many sellers getting above “asking price” and getting rewarded by buyers.

Zoning will always be a big factor in real estate prices. Its just a supply and demand thing. The purpose of zoning is to restrict what kind and how much can be built. I dont know why people keep forgetting that.

Id say affordability is the biggest thing in real estate.

Affordability is defined by mortgage rates

Most people forget about this

I don’t think it’s one sided. Price and Rates determine affordability. Case in point back in the 70s when rates were high… I remember my dad saying there was no way in heck to get a mortgage… you just couldn’t borrow money at the rates. So was it the rates that made things unaffordable, or the rates at the prices? His ol man was doing just fine as a WW2 generation, getting nice returns having bought his house 20 years prior. Point is that the coin has two sides, and they are inseparable. At least as I see it.

When I say affordability it means both price and rates

If rates are high then prices need to come down or people need to get big raise .

Affordability basically comes down to monthly payment

This is what the urbanists in Seattle keep saying, they are not entirely wrong, but NEVER would look past supply and demand to consider what low rates and easy money did to all assets in the everything bubble. IMHO There is no supply that would have solved this problem. Housing became a commodity to hold, and borrow against so you could buy more of it.

What the heck is an urbanist in Seattle ? Never heard of such a discipline but it certainly makes sense. However, I think that your overthinking the issue.

Conflict is inevitable when the fresh air from the ocean spray convinces the bold to act.

I wouldn’t be surprised if mortgage interest rates went up to 8% by the end of the year.

Yes, I think that’s the direction.

Hi Wolf, do you know how to invest in the government guaranties MBS? Are their yields at around 7% now?

“something has to give, and it’s not going to be mortgage rates”.

Reading that made endorphins shoot off in my head. Finally, housing prices will go down. I am rooting for a significant decline.

In 1979 I bought a house in Sacramento with a $50K 7.5 percent mortgage. After a time I realized I had paid $100K in interest even after a 5.5 percent refinance, so I paid the balance off and never was in debt again. But rates kept rising. Two married friends bought a house in Oakland near the Grand Lake Theater with a 13.5 percent rate mortgage.

We all survived.

1979 was close to the end of the rising interest rate cycle (peaked in 1981) and bear market in stocks, 1979 or 1982 depending upon how measured.

We’re at the beginning the bear market now in at least bond prices, not the end. This is still the biggest asset, credit, and debt mania in the history of human civilization.

Economy and “growth” has mostly bene fake since 2009, from ZIRP and higher government deficit spending. Recent inflation is the fruit of this monetary and spending binge.

There is a long way down to go.

So the “Soft Landing” was getting to this high level of interest rates so slowly it is like getting squeezed by a giant anaconda. With that said, the low interest rates of the recent past give many homeowners powerful options to hold on to their homes. In addition, all Federal guarantors have policies in place that almost FORCE lenders to work out people staying in their homes another way (with many options to do so even with loss of income). Add to that in California, the new Homestead Act clearly gives people who face the loss of a home powerful set of tools to thwart those who could benefit from this situation. The rules have changes such that my neighbor, the “flipper” who mostly flops flies his drone around the neighborhood to sniff out the status of peoples’ situation. Because the options for investors are clearly shrinking and with most not able to track info and understand its meaning like Wolf the future does not bode well…. I am amazed at the concept of German Precision plays out in this ongoing analysis of the craziness of it all. Unfortunately, you cannot divorce politics from business and it appears The Capitalists’ are going to rarely make any money and the future will be more of trying to maintain capital rather than increase it for the investing class…. Great stuff here….

No need to worry about the interest rate from HUD (US Government website) looks like “from each according to their ability, tobacco according to their need.”

HUD text: May 31, 2023, FHA INFO #23-44 announced the posting of the Draft Mortgagee Letter (Draft ML), Payment Supplement Partial Claim. Through the proposed policy provided in this draft ML, FHA proposes to create a new loss mitigation option to assist struggling borrowers that are delinquent on their mortgage payments. This option is targeted to assist borrowers in default who are unable to obtain a significant payment reduction through other loss mitigation options.

The Draft ML proposes policy that would allow mortgagees to use available partial claim funds to:

cure mortgage arrearages and

temporarily reduce the principal amount of the borrower’s monthly mortgage payments for three to five years.

Pump that leaking bubble.

Read the whole text and try to understand it. It’s not that hard to do. Your conclusion is braindead BS you picked up on some financial-fiction site that I won’t name here:

1. FHA mortgages only. That’s a small share of total mortgages. FHA is focused on shaky (often subprime) borrowers.

2. What the text says: if standard efforts fail to modify the defaulted mortgage, the FHA may offer a second mortgage (in addition to the original mortgage) to fund the arrearage and reduce the payments over a period of 3-5 years. In other words, if an FHA borrower falls behind and cannot make the complete mortgage payment every month, the mortgage payment will be reduced, and added to the second mortgage; and the arrearage will be added to the second mortgage. After 3-5 years, when this grace period ends, the borrower has to deal with both mortgages. If they sell the house, they have to pay off both mortgages.

3. FHA mortgages are government insured high-risk mortgages. Curing a mortgage deficiency with a mortgage modification or a second mortgage can possibly prevent a foreclosure. During the last mortgage crisis, lenders lost 50% to 70% when the home was sold in a foreclosure sale to PE firms – at ultimately a huge cost to the government. This is an attempt to prevent a 50% to 70% loss to the taxpayer due to a foreclosure sale.

Prices are still calibrated from the 3% rates. At 7% the cash flow doesn’t work. Prices must come down. And they will. Bigly. It’s mechanical. Best to stay away for a while and rent. When sellers get tired of bleeding that’ll be the bottom. Not before desperation sinks in. Always the same story.

You youngins ain’t seen nothing yet. Know your history? Epic events take years or decades to play out? Stock up on your favorite food and watch the show.

The “Old Way” does not work anymore. To understand the New History read “HOMO DEUS” by Yuval Harari. Here you will see how history is not so much about the past as it is about the future. I read an excerpt in this book that state Harari did not believe in “free will” and instead (I paraphrase) people are just Pavlovian Dogs that can be conditioned, by technology, to believe and think as desired by those who “own the data” which is the tech sector tied to the political. In other words, history now will be “created” in a manner that a few will control all and the many will struggle to have any free will at all. This is why the youth, all around the University of California Campus at UCLA are all looking at their phones and computers all day and night. My point to you is it is a time for a software update for those of us in old age…. This book is the number 1 international best seller and these are the people who are going to shape the future how they want it not how we hope it will be. Go to any college campus and you will see the world they are creating…. Not like us AT ALL.

You left out the word ”SOME” before people in the quote below AS:

“(I paraphrase) people are just Pavlovian Dogs that can be conditioned, by technology…”

In fact, it has always been that way and it always will be that way.

Old Abe Lincoln phrased it exactly correctly IMHO.

These higher rates will definitely continue to let some air out of the housing bubble. I doubt it will crash the system and probably will help those trying to get into housing for the first time to some degree because it will slow/stop some real estate “investors” from consuming inventory and allow for regular folks to have more of a chance.

The economy is definitely slowing and going to slow further. The Fed will not likley raise from here for awhile but wait to see how things respond for a few months. Again, our economy is much different than the 1970’s and early 80’s so all this talk about needing interest rates higher than the rate of inflation is not valid, in my opinion.

And regarding ongoing inflation (upward wage adjustments), that is baked in and will continue for some time; something the Fed is quite aware of and planned for.

Remember, they have to “talk” against inflation but have every desire to inflate away a good portion of the debt to create some breathing room in the economy.

And particularly now, they also need to “talk” a good line about reducing/controlling inflation for all the foreign ears out there that are using the dollar. Of course, most of those folks know the game all too well, so it’s largely theatre.

We’re in a protracted sideways/down trajectory over the coming months.

The debt ceiling agreement ended up being very lopsided for more debt approval and I would guess that McCathy got a serious dose of economic reality during his discussion with the White House. They are going to need that 4T over the next 2 years to help those impacted by the recession that is starting. It shows again how totally messed up and dependent our economy is on free money to survive.

To my mind, this will all not end well, of which I recommend folks secure some physical gold and silver as an insurance policy (not investment). Most long term analysts recommend at least 15% of total net worth in PMs.

The fundamentals now are far worse than the 70’s.

It only looks different now because of much higher government spending and the loosest aggregate credit conditions in human history.

Both of those will change eventually, spending when the macro effects generate “growth” that still leaves most or at least the “wrong” people poorer and the USD needs to be rescued.

Peter Schiff doesn’t even recommend 15% metals.

My impression is most intelligent analysts limit metals to 5%.

Metals are speculative assets that do not generate reliable income.

The following is 100% TOTALLY anecdotal …

We go to our friend’s BBQ every Memorial Day Weekend. They live in a DuPage county suburb somewhat east of us. We drive the same route every year.

And each spring, as we drive, my wife counts the “for sale” she spots in that suburb on our way to the BBQ.

The usual number is between, say, 15 to 25.

This year, 2023 Memorial Day, she saw just 1 “for sale”.

Take that totally anecdotal report as you wish.

Well in California I think they are saying about a 38% drop in sales volume yoy. What your wife counted would be about a 93% drop (best case). Which could be in that particular suburb. I bet there are pockets in Las Vegas and Phoenix that are like that.

Anyone who is in the market to purchase experiences this (currently): very low inventory. Any article or statistic you look at shows a shortage of active listings (by historical standards). Those that don’t believe it, go to a new construction community, take a pic of the map of what’s available to purchase today and then come back in a month to see how many more homes got sold. I am not an agent, not a cheerleader. I am a recent buyer who had to experience this crap first hand. It totally sucks for buyers.

Homes have a very high carrying cost. People will sit on them for a time, but eventually the sellers will accept the “new normal”.

Assuming rates stay high I personally expect a slow and orderly decline in prices for a couple of years, but not getting anywhere near 2019 prices even.

Homes in my area that I watch used to go for $165 per SQ ft. They peaked at about $300 and are now at $265. At $200 I’d probably be a buyer myself which is ironic because we looked at homes January of 2020 and decided we didn’t want to pay those prices.

USA has high carrying costs for real estate in the form of high mortgage rates and high real estate taxes.

It also has other high imbeded carrying costs in the form of restrictions on ownership rights such as eviction restrictions, rent control, and recapture of depreciation taxed at high rates.

From a foreign perspective one has to also consider the possibility of a falling US dollar.

Add in factors such as crime and drugs and one wonders why people would want to buy real estate in the USA in the first place.

Hopefully they stay at 7% and take some buyers out of the market. I made three offers last month and was outbid on all of them. Ive now re-signed a lease (with only a 8% increase over my last lease!) to try and wait out the nonsense a bit more.

Random thought: A neighborhood or city could legally protect itself against investor takeover by charging a cash penalty. If you want to pay cash, you have to pay us the same total amount that a mortgage would cost over its full term.

This wouldn’t work for a single seller.

Not all cash buyers are investors. Some are just people with cash.

So the right idea would be to buy the house with a mortgage and invest the remaining cash to offset the mortgage interest. This accomplishes what, exactly?

“Mortgage Rates Re-Spike to 7% Range as it Sinks in that the Fed Won’t Cut Rates “Anytime Soon”

The jobs numbers just came out, and again “surprised” to the upside. The economy remains grotesquely overheated. The FED has quite simply completely failed to remove the excess liquidity from the system. It is doing extreme damage.

Don’t keep your hopes too high on Powell.

He is sold out. He has already declared pause and partial victory on inflation.

On top of this, he is citing these banking issues as a way of more tightening happening.

On top of these, wall street cry babies are fear mongering and begging Powell for a pivot that rates these high, something would break.

We should all know for whom Powell works for.

One look at the FED’s balance sheet tells a person everything they need to know about what the FED is actually doing.

The market is up again today with hope that a pause or pivot is coming.

Collective Market is smarter than us for sure :-)

“The market is up again today ”

I suspect the market is global now in the same sense that real estate is. All these extremely wealthy people and wanna-be extremely wealthy people around the world want to own a small piece of the US or London or Sydney or Vancouver. Like a fashion statement. It’s a status thing. Or a money parking thing. Or a weird belief that if you follow the mob it will result in riches. It has nothing to do with real value. It has nothing to do with use.

Personally I think it stems from a lack of real culture, but that’s a whole other ball of wax.

In my area, a mortgage + taxes costs 30-50% more than the rent, depending on the property. And you also lose the interest you could have earned from the 20%+ down payment, which adds another absolute 10% or so to the comparison (and you also no longer have easy access to that money)

Rents are going mad in response. But ultimately, people were already pretty stretched, and you (usually) have to satisfy very similar affordability criteria to rent as you do to buy. It seems impossible the gap could close just by rising rents.

Surely a (further) big drop in house prices is inevitable?

Further drops in homes prices are inevitable, unless everyone gets a HUGE raise to keep up with inflation.

Blurb recently reprinted in “Professional Builder” magazine…..

“Throughout the U.S., buying a home is roughly 25% more expensive than renting one, but in just four metro areas, ownership is cheaper, according to Insider. In Detroit, Philadelphia, Cleveland, and Houston, monthly mortgage costs are lower than monthly rental costs by as much as 24%.

In contrast, it’s twice as expensive to own than to rent in California cities such as San Jose, San Francisco, and Oakland.

In Detroit, the typical home is 24% less expensive to buy than rent — the largest percentage discount among the 50 most populous metros, Redfin said in a report Friday. The median mortgage payment for homebuyers there is $1,296, while the average estimated rent hovers at $1,697.

Philadelphia offers a 7% discount, and it’s followed by Cleveland (4% discount) and then Houston (1% discount).”

An odd thing happened on Tuesday that I have not seen before.

A whole bunch of folded over notes were posted on apt doors with some sort of candy attached them. Maintenance notices are usually folded over but no candy is ever attached.

From the little I could see, these were lease renewal reminders including an explanation of the option to go month to month and the corresponding increase in monthly rental fees associated with choosing that option.

There were a lot of these notices posted, more than I have ever seen.

Lower than normal inventory is partly because many people have locked in low, like 3%, mortgage rates. While they like to crow about it, the fact is they are imprisoned in their little castles. They cannot move because their mortgage would double for the same price house.

As for investors, buying a $500,000 house with cash means you are immediately out $25,000 a year with today’s 5% interest rates. Then all the other crap, closing costs, property taxes, insurance, time spent looking, HOA for some, moving costs, knowing home prices are going down, worrying about the neighborhood deteriorating. I see why builders are building houses to rent. Rent-to-own might be interesting, if there is a reasonable deal.

It makes perfect sense to rent and earn 5% on your wad, while avoiding a huge risk of loss. Such nimbleness will allow a person to capitalize on great deals in RE or stock markets down the road. Retire early, say good-bye to the boss man.

I can confirm the investor part, as an investor backed out of a contract to buy raw land in Charlotte from me. Investor backed on the LAST DAY of the due diligence period. jerk

Perhaps the investor wants you to lower your price.

Someone buying a home can only pay the same payment at 7% what the seller is paying at 2.5%. There is a conflict in the price and they are way far apart.

In one scenario, the price of housing has too fall 40+% before normal people can afford to buy.

In another scenario, the Fed caves to the pressure by the wall street wankers and excretes a “pause” at the June 14th meeting.

From all indications, the milk toast Fed seems to prefer the second scenario. No surprise there.

An alternative resolution of the ” FOMC ” is the “Friends of Many Corporations”. Perhaps a more fitting understanding of who they are than the official title suggests.

I am about to reveal what I think the FOMC should accomplish and declare as the law of the land:

a 25 bpt in the FFR and

an unambiguous statement that the FFR rate will increase as long as the prices increase.

I think that inflation is a greater threat than the repricing of assets for the following reasons:

Most people don’t own assets and any aspiration they clung too growing up as being able to afford a house as an American are dashed.

Well, it’s essentially, the conversation going on in the halls of power, ruled over by idiots.

The amount of speculation that continues is indicative of excess liquidity in the system. Distorting the self regulating feature of a market equalibrium that we all rely on.

my opinion, the Fed needs to pierce the stock market bubble that continues to invest workers savings in an overpriced asset.

Another reason they should increase the FFR in June, July, September, until the price increases stop.

Spring selling season is up, but….

Wells Fargo, based on nearby sales, says my hovel is up by 20k in the last two months, but only after declining by 100K. I have a feeling these “increases” are just Seasonal noise.

At 74 my gut feeling is at least 3 more years of decline unless the FED does a huuuuge pivot.

Interesting…. One thing I never see in these conversations is housing values corrected for inflation. If that was done then instead of a nationwide ave of 4% decline it would be more like 8% – 10% in real terms. Wny no comments on that?

As to the pivots, job hires are more than double what was expected, but everywhere I see the hopium being ingested and a rate reduction right around the corner.

I also saw an investment brochure titled “We are finally turning the corner”. The date was Sept. 1929. So much for Wall Street prognostications.