From huge to somewhat less huge? Because they’re still six times the magnitude of the prior worst-record in 2018

By Wolf Richter for WOLF STREET.

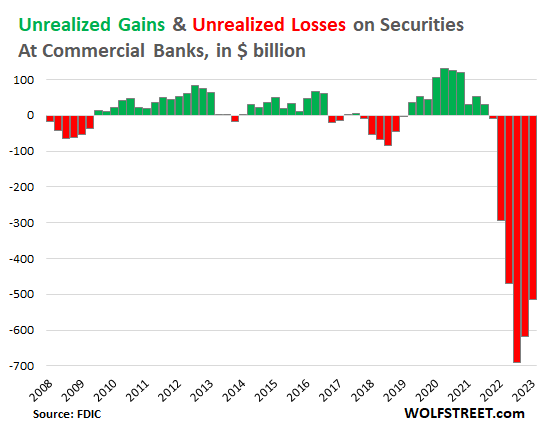

“Unrealized losses” on securities – mostly Treasury securities and government-guaranteed mortgage-backed securities – held by all FDIC-insured commercial banks in Q1 fell by $102 billion from the prior quarter, to $516 billion. This is a cumulative loss over time on all securities from the purchase, and not an additional loss incurred in the quarter.

It was the second quarter in a row of declines: They have now dropped by $174 billion, or by 25%, from the peak in Q3 2022, when unrealized losses had hit $690 billion, according to FDIC data on bank balance sheets released on Wednesday. In other words, unrealized losses are still huge, they’re still six times the magnitude of the prior worst-record in 2018, when the Fed also hiked rates. But they’re 25% less huge than they had been.

The bank collapses since March this year in the US – Silvergate Capital, Silicon Valley Bank, Signature Bank, and First Republic – all involved lightning-fast and record-huge bank runs by electronic means, that were triggered by sudden concerns about those banks’ “unrealized losses” on their securities. The chart shows “unrealized gains” in green and “unrealized losses” in red.

These unrealized losses of $516 billion in Q1 were spread over two categories of bank accounting treatments:

- Unrealized losses on held-to-maturity securities: $284 billion

- Unrealized losses on available-for-sale securities: $232 billion.

The six quarters of unrealized losses during this rate-hike cycle follow 10 quarters in a row of unrealized gains during the Fed’s pandemic-era QE and rate cuts.

When the banks collapsed, the issue wasn’t credit, such as defaulting loans due to imploding real estate prices and a tsunami of foreclosures, or defaulting corporate loans, as during the Financial Crisis.

Instead, the issue was a huge pile of pristine long-term Treasury securities and government-guaranteed mortgage-backed securities that lost market value due to higher interest rates.

As these bonds approach maturity, their market value returns to face value because face value is what the holder will ultimately get paid when the bond matures, or every time pass-through principal payments are made to MBS holders. This is the rationalization for allowing banks, under the “held-to-maturity” accounting treatment, to not “mark to market” those securities that they don’t trade.

So bank income statements look good because they don’t show the market losses on their vast securities portfolio. But they have to disclose these losses as “unrealized losses” on their balance sheets. And that turned out to be a problem too…

When uninsured depositors – who never ever look at bank balance sheets – got wind of these huge unrealized losses suddenly via media reports and social media posts, they got spooked and yanked their money out, causing the banks to collapse because they could not come up with the cash to fund the withdrawals because they could not sell those securities for prices anywhere near what they had valued them on their balance sheets, and because they didn’t have enough capital to eat those losses and live through it.

So now we keep an eye on banks’ unrealized losses because they’re one of the weak points in the financial system.

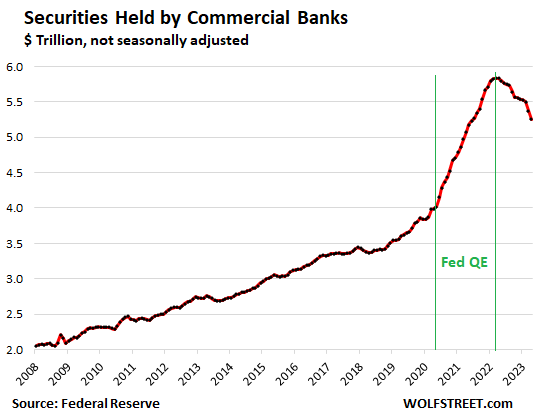

The total balance of securities held by all commercial banks – mostly Treasury securities and government guaranteed MBS – declined by $582 billion, or by 10%, to $5.25 trillion in April, 2023, from the peak in March 2022 ($5.83 trillion), according to monthly data by the Federal Reserve on bank balance sheets.

In the chart, you can see the big drops in March (-$130 billion) and April (-$120 billion). The drops were in part due to the bank failures, when some of their securities were transferred to the FDIC, rather than to other banks. The FDIC is now selling those securities to investors, and those securities have come off the bank balance sheets. Securities from failed banks that were sold to other banks remain in this total balance, but their losses were wiped out as the banks bought them from the FDIC at somewhere near current market value.

In the chart, you can also see how banks gorged on these securities as a result of the mindboggling money-printing by the Fed starting in March 2020 through early 2022, which had the effect of repressing long-term interest rates.

By August 2020, the 10-year Treasury yield had dropped to 0.5%, and banks – these morons! – were buying those long-dated securities with ultra-low yields, either not thinking at all, or thinking that yields would turn negative. And when yields began to rise in September 2020, they didn’t take it seriously, and continued to gorge on long-dated securities. And when the Fed started talking about rate hikes and ending QE in the fall of 2021, the banks still didn’t take it seriously, and it wasn’t until March 2022, after the initial lift-off rate hike, that the banks — some banks — timidly began reducing their massive holdings of now overpriced securities.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Removing mark to market rules was the biggest crime against free market capitalism.

Treasury rates were down this quarter. Give it time.

The day they removed mark to market and replaced with “mark to fantasy”, I had a friend who is an economist who called me and was freaking out, saying I should buy precious metals, etc. Yes it was a sad day for capitalism, for sure, but I told him that they changed the rules so play by the new rules without thinking about it too deeply. So instead of filling the bunker with gold coins, I bought multiple bank OTM calls and watched them spike 7-8 fold in a few days. I cashed out in disbelief of the returns and then my Citibank calls continued to spike over 100 fold in the following weeks after I sold…HA. So now I cost in and out of positions as I could have made enough to buy a house at the time had I held, live and learn.

What!!! When were mark to market accounting rules eliminated?

At the same time as Paulson saved Goldman with the $23 billion bailout, including AIG and Buffet.

How so? If the banks had to report this as real losses, more people would be spooked and the runs would be worse.

“When you drive interest rates down all the way out, it forces investors to take bigger steps on the risk spectrum.” former Fed Governor Fisher

Fisher admitted, boasted of this in the PBS documentary “The Power of the Federal Reserve” which can be seen on their web site.

The key word here is “Force”….. a curious activity of the Federal Reserve. Is the word “force” anywhere in the Federal Reserve Act? Did this ‘forcing” skew historical risk return considerations?

Banks, and investors were “forced” to take more risk, ie buy long term paper with paltry yields. How did that work out?

Eastern Bunny

All done to bailout TBTF Banks, to keep their ‘loss’ hidden until ‘maturity’ in the March of ’09. And still going on!!

Fed also bought MBSs, NEVER done before! Same with QEs

Rules of the game uprooted and the assets value zoomed and almost held, as of now. The financial illiteracy so high, even among the educated, this went unnoticed, unaccounted and unchallenged. Crony Capitalism replaced our good ole, genuine, free mkt capitalism. No one cares b/c Wall St and the Congress are complicit.

If they didnt gorge on these long dated securities, who would have? Does there have to be a buyer?

If the yield is high enough, the entire world gets in line to buy them.

Buying by banks was in part responsible for yields being so low at the time. They should have dumped those securities at these huge prices, and yields would have shot up then, and banks that dumped securities wouldn’t have those problems today. This is all self-inflicted stuff.

Some of it is Fed-inflicted.

How high does the 30 year mortgage rate hit before the Fed gets concerned on the impact on the economy and panic buys MBS once again??? In many ways, housing “IS” the retail economy, so how does that work out politically, socially, economically if allowed revert to the mean, or lower?

Historically, the rate at the start of the decade and the rate at the end of the decade shown below:

1970s 7.31%/7.48%

1980s 7.48%/9.78%

1990s 10.13%/8.06%

2000s 8.06%/5.14%

2010s 5.14%/3.72%

2020s 3.72%/???????????????

So if the 30 year hits 8%, that seem historically high. I’m betting the govt and Fed get nervous approaching 8%, as 9-10% would be generational high when looking at the previous decades.

And note that was when a houses had half the square footage, cost half as much per yearly income, and thus the impact of 8% rates now versus 1970 has a greater percentage wise impact on consumer standards of living.

So far Vanguard MBS ETF is showing investors are not freaking out as bad as earlier this year at the moment. I’ve been placing my chips between 7-8%, will double bet at 8.75%, and double again at 9.5%. Pre 2024 election time frame is my escape hatch as the Fed will be burnt at the stake with 10% rates close to 2024 elections. Obviously not a high gain or high stakes gamble, just one skewed by politics, and thus slightly more predictable due to the “buy a voter” scheme predictability.

Plus I’m feeling lucky after having sold my NVDA for 198% gain in 8 months today at $399.20. I bought it for the love of their products, I sold it to the A.I programs after-hours as A.I. loves the A.I. bubble. Now playing with the Casino’s money with MBS. So many thanks to the A.I. bot who bought my shares after hours at a measly 36.1 P/S ratio…¯\_(ツ)_/¯

Help me with this Wolf, the Fed is sitting on ~$8T of Gov’t debt. Your chart above seems to indicate that Commercial Banks are sitting on another ~$5.2T… is that ~$13T of our overall $31T US Debt? That would be 1/3 of all outstanding debt embedded in the banking system?

The chart above includes: $1.6 trillion of Treasury securities, plus “Agency” MBS, plus non-agency MBS, plus other securities that banks hold. But only the $1.6 trillion Treasury securities are “government debt.”

The Fed holds $5.2 trillion in Treasuries. The rest is other stuff.

Combined they hold $6.8 trillion in Treasuries, of the $31 trillion total.

Foreign entities hold $7.4 trillion in Treasuries.

Insurance companies, pension funds, bond funds, lots of us here, companies such as Apple… hold a whole bunch. The SS Trust Fund, and other government pension funds hold a whole bunch.. They’re everywhere.

Thanks, makes sense!

Beyond the nightmare of the aggregate $31 trillion debt number itself (relative to arguable GDP numbers, say) are the potentially toxic macroeconomic “rules” that some of those large holder groups operate under.

For instance, the MMT deceivers would have you believe any level of DC debt is irrelevant…because DC can/will just have the Fed buy *any* level of Federal debt, thereby fully (and impliedly, forever) controlling US interest rates.

Where does that Fed “superpower” come from?

Why, unbacked money printing of course.

But while the Fed can print money at will…it can’t “print” real world assets…and it is the ratio between aggregate money supply and aggregate real asset supply that determines macro price levels. This is how you get 25% rent hikes in 1-2 years across the US…”poof” the money appeared – but “pffft” the housing didn’t.

Similarly, changes in vast Treasury holdings by foreign gvts have huge impacts on macro foreign exchange rates and therefore intl trade levels/direction. And the Fed can’t really control those forever either, without again provoking inflation.

The Fed ain’t a magical unicorn that can alter reality by applying ink to paper. The MMT school is basically Hogwarts.

How about banks? Well, other utterly undisciplined nations have historically ordered “privately owned” banks to hold their own equivalent Treasury notes…when natural demand falls short and would otherwise spike domestic interest rates. That is pretty close to de facto nationalization of all savings (you get to keep your savings…but can only invest them in government securities via the compelled banks).

Bottom line, when G debt occupies a sufficiently high share of true GDP/aggregate savings – bad things start happening because big, bad actors really don’t hold themselves to the “rules” they claim to…or that they hold others to.

It is good to be King.

Wait for the shake.

Do banks have regulatory requirements like pension funds, where they are told what sort of assets they can/must hold? It seems no one would buy 10 year paper at 0.5% when 1 or 2 year was paying close to the same yield, unless they were feeling some sort of external pressure.

“Tangible book value” an important regulatory number reflects a banks unrealized losses that are “available for sale “ BUT does not reflect a banks unrealized losses on securities “ held to maturity “.

Banks are probably even *more* directly incentivized to hold certain investments than pension funds (which mostly just have to adhere to “prudent man” guidelines and whatever rando ERISA statutes/rules that may apply to certain institutional investors).

Banks on the other hand, have their mandatory regulatory capital (which affects everything including profit margin) directly impacted by the “risk weightings” of their investments (loans to commercial borrowers, securities holdings – including a buttload of US Treasuries, etc.).

Not surprisingly, US Treasuries have the most advantageous risk weighting (“The Feds can always print more, yadda yadda yadda”).

Ironically, that enormous bias wasn’t enormous enough to shelter banks from the vast stupidity of their Treasury maturity selection (apparently somebody at the Fed forgot to send out the secret decoder ring, heads-up email to the bank flock…)

The Treasuries didn’t default but there were huge (and easily predictable) unrealized losses once the Fed raised rates (rendering ZIRP era Treasuries burnt toast…unless held to maturity).

So, yep, Treasuries receive very favorable treatment when held by banks. Which sorta makes sense unless you think about that whole worldwide, systemic, ruthless inflation thing it incentivizes.

Wolf is correct in calling the bankers “morons” when they bought very long

duration bonds with a tiny yield to maturity at the all time historical low in interest rates. Did they not think that interest rates would ever rise again?

Smart bankers bought very short term US treasuries in anticipation of rising interest rates when the inevitable inflation genie woke up.

Well, yes, I guess some banks were a little slow on recognizing the upward trending rates and unwilling to taking some early losses. But ZIRP was getting alot of attention, so I understand why some banks (wonder how many still are holding) went with the longer term bonds as a rational strategy at the time. But looking at the Fed’s and Treasurer’s hands in this, they were instrumental for the low, low rates at the front and then waiting so long to see what was heading their (our) way with all the pandemic trillions printed – to me the blame is on FED/Treasurer for this mess.

If a hedge fund or investment bank wanted to trade bonds, they basically had 40+ years of very high confidence that the price would go up before maturity. QT and higher fed funds rates for longer takes that trade and throws it out the window. This is the 1st time the 10 year bond has broken out of a downtrend channel that started in 1981, and it’s already causing instability. I wonder if some banks were under the impression that negative rates were not only a possibility but a probability.

Look at bank balance sheets in 3Q22, then 4Q22. The problem was that bank exec’s thought they were being clever by moving large portions of cash and available-for-sale securities to held-to-maturity securities as they thought the fed was done raising rates.. they weren’t and they probably aren’t.

The average duration on these held-to-maturity securities is currently around 4 years, so over time this becomes less-and-less of a problem. This, combined with the fed’s Bank Term Funding program has largely plugged the hole for now, but the much more expensive debt (versus free deposits) will put the hurt on bank earning for quite some time.

“The average duration on these held-to-maturity securities is currently around 4 years,”

Maybe. Maturities of all securities and loans on their balance sheets, % share of total

3-5 years: 8.6%

5-15 years: 15.4%

Over 15 years: 14.5%

You’ve spent entire blog posts explaining average and median. This entry suggesting some average exposure is welcome for its factual content but the banks that are over their ski tips are the ones that are concerning. Who’s too far out on the curve? Which is the next one to get Marked to Market for its HTM portfolio? I think we find out soon. I worry.

We already found out who some of those banks were. We’re going to find out who the others were when they collapse. The process should just weed out the badly managed banks.

There are bank failures nearly every year (except during the pandemic). So we’re going to get a few more.

Yeah, but “maturity” and “duration” are two entirely different animals. Duration is just a measure of sensitivity to changes in interest rates. A UST with a maturity in 2027 doesn’t have a duration of 4 years, nor does a UST that matures in 2033 have a duration of 10 years. Your reply is conflating the two terms.

When the FDIC acquires these securities at par and then sells them at market, what happens to the resulting loss at the FDIC? Where does it show up?

The FDIC doesn’t “acquire” securities at all. It takes them along with all other assets the bank has when it takes over the bank. It then “sells” those assets to other banks or whoever. It then has to pay off the insured (and maybe not so insured) deposits, which are liabilities for banks. If the amount of the deposits the FDIC pays off exceeds the amount in proceeds from the asset sales, the FDIC has a loss. This loss normally comes out of the FDIC’s deposit insurance fund.

wolf: The maturities cited by you and bought by bankers represent a total of 38.5% of the total bonds bought. This means that 100% – 38.5% = 61.5 % of the bankers were intelligent enough to buy very short term bonds less than a 3 year maturity. The short term bond holders (especially less than a

one year maturity) have very little unrealized losses whereas, the “morons”

that bought long term bonds at historical low interest rates are praying they do not have a run on the bank caused by capital concerns by depositors. Thank goodness the smart bankers substantially outnumber the ones thinking that rates would never rise again.

Commercial banks total assets : $23T. Unrealized loss : $500B.

500B/23,000,000B isn’t much.

500 / 23,000 no?

Also, some banks holding a higher percentage of unrealized losses compared to others.

Welcome, my real American banker.:)

23T is not 23,000,000B

The ratio is 1/46!

$23,000,000B is so next decade…=D

The small and medium banks have $1.5T CRE to roll over in 2025, but I think Wolf pegged it when he commented that the banks cherry-pick the loans, and sell the rotten pits to retail investors. And some of those rotten cherries have parasites’ that could infect a lot of investors.

The panic recently wasn’t just about a few small and mid size banks failing in Cali, it was the fear what unknown dominoes are going to fall next in a possible global chain reaction.

Plus the rumor is size doesn’t matter, as the Fed is omnipotent and/or impotent, right???

Interest rates are determined by the supply of, and demand for, loan funds. There’s so much money circulating that the FED has to pay fund managers to park their money in O/N RRPs.

Case in point, the O/N RRP facility. Aug, 9 WSJ:

“In their Aug 6. letter in response to our op-ed “How the Fed Is Hedging Its Inflation Bet” (Aug. 2), John Greenwood and Steve Hanke argue that the Fed’s sale of a trillion dollars of reverse repos does not in and of itself reduce the deposit liabilities of banks and money-market mutual funds, and that the money supply is unaffected. By that logic, none of the monetary tools of the Federal Reserve Bank would affect the money supply.”

There is no need for concern, the Federal Reserve can buy all of the assets at face value. Yes, it will add to inflation, but the Fed has been worried for years about getting to their 2% theft rate, now it is raining gold coins for them. Anyway, the losses are only a few hundred billion a quarter, maybe a couple trillion that the Federal has in petty cash sloshing around in their “tools.”

Wolf, I have to ask. If you were running SVB and the CFO of a tech start-up walked into you bank and made a $20 million deposit, what would you have done with the money?

Put it on deposit at the Fed and collect the interest on reserves. This is totally liquid money. When I have demand for loans, I would have used some of those funds for loans, but keep a minimum of 20% on deposit at the Fed (the Fed call this the “reserves”). If these banks had kept 20% of their deposits from their customers on deposit at the Fed (“reserves”), they’d still be around.

That is such a logical way the manage to cover the possibilities. How could the board of directors and the bank managers all have their collective heads up their asses. (Rhetorical)

Or, more recently, SVB and others could have bought (and rolled daily) Reverse Repurchase (RRP) arrangements.

So the the question is: why didn’t they? Were they strong-armed not to do this? And why?

Banks wouldn’t have done ON RRPs, and they still don’t, because they have a better deal: their reserves account at the Fed. Reserves pay more and are instantly liquid. These accounts are also used to transfer money between banks for transactions.

Interest the Fed pays the banks on reserves: 5.15%.

Interest the Fed pays on overnight Reverse Repos: 5.05%.

https://wolfstreet.com/2023/05/03/fed-hikes-by-25-basis-points-to-5-25-top-of-range-says-the-extent-to-which-additional-policy-firming-may-be-appropriate-instead-of-pause-qt-continues/

The question you should have asked is why they bought long-dated Treasury securities instead of putting cash on deposit at the Fed. The answer is that when the 10-year yield was 0.5% in August 2020, the interest on reserves was 0.15%. They went in front of a steamroller to pick up some pennies.

A lot of FIs are running perilously low liquid liquidity ratios. A lot of the ones I work with are running 3-5% (on balance sheet liquidity). Had they all had 20%, my goodness, their financial performance and interest rate risk would be so much better. Earning 5.25% on overnight funds in a tightening liquidity environment is exponentially better than those MBS/CMO/UST portfolios they bought a few years back that are yielding <2% (or worse). I see some FI investment portfolios hovering around 0.5%.

You don't say it, but a LOT of the blame rests on investment brokers peddling terrible investments to these FIs regardless of the rate environment. It's way too easy for them to call up their pool of CFOs and sell them on duration, convexity, and a yield that's barely higher than the overnight rate because, well, they get paid on churn and don't get paid when that FI holds 20% of their assets in overnights.

Wolf,

Didn’t Fed (Mr. Powell) reduced the ‘reserve’ requirement for the banks to ZERO during the March of 2020?

This is FED inflicted disaster to Banking industry with no accountability. Hardly any discussion in the MSM.

It seems to be “moot” now since market participants are actually paying attention, but I’d eliminate the distinction between “available for sale” vs. “HTM” and book unrealized gains or losses directly to equity. That’s where it should have been booked from the beginning. It can be recorded in the income statement when sold.

Thanks to the author for shedding light on this important trend in the banking industry. It’s encouraging to see the risks being reduced.