QT on track, bank liquidity measures unwind.

By Wolf Richter for WOLF STREET.

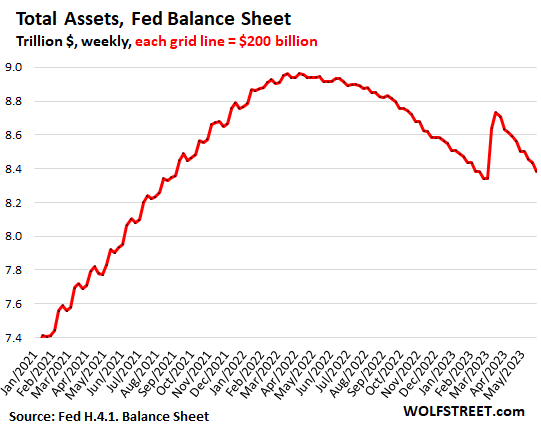

Total assets held by the Fed dropped by $50 billion in the week, to $8.38 trillion, down by $118 billion for the month and by $348 billion in the 10 weeks since peak-bank-crisis. Quantitative Tightening (QT) continued on track, and as the remaining bank liquidity support measures continued to unwind, according to the Fed’s weekly balance sheet today.

From the historic peak of the balance sheet in April 2022, total assets have dropped by $580 billion. This month, total assets will fall below where they’d been before the banking crisis, and will set a new low in this QT cycle.

To see the details of the banking crisis, here are total assets viewed through a magnifying glass:

The banking crisis measures.

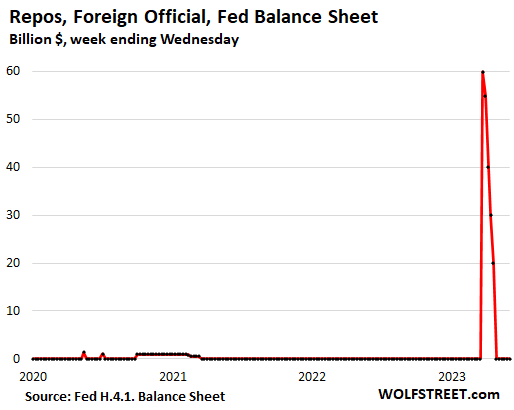

Repos with “foreign official” counterparties: paid off in April. The Swiss National Bank likely used this program to provide dollar-liquidity support for the take-under of Credit Suisse by UBS.

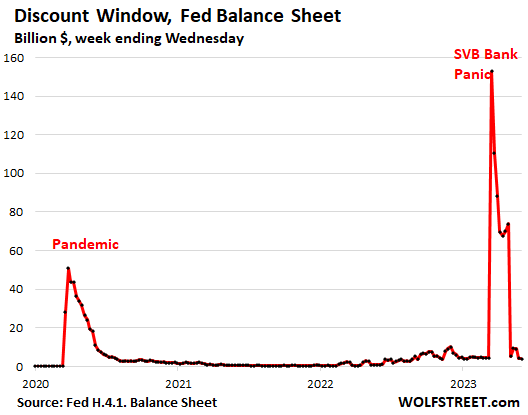

Discount Window: nearly paid off, down to $4 billion. Since the last rate hike, the Fed charges banks 5.25% to borrow at the Discount Window (or “Primary Credit”), and banks have to post collateral valued at “fair market value.” So this is expensive money for banks, and they pay it off as soon as they can.

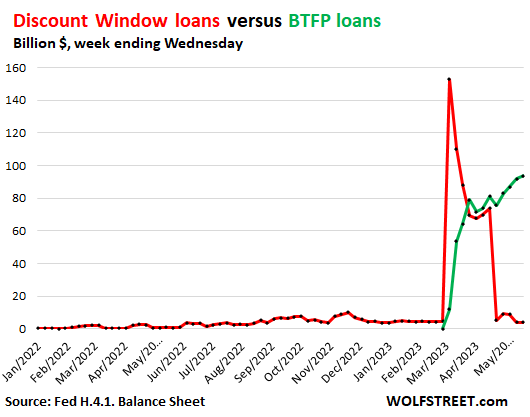

Bank Term Funding Program (BTFP): +1.7 billion in the week, to $94 billion. Under this program, rolled out on March 13, banks can borrow for up to one year, at a fixed rate, pegged to the one-year overnight index swap rate plus 10 basis points. Banks have to post collateral, but valued “at par.” So this is still expensive money, but less expensive money than the Discount Window, so some banks paid off the Discount Window loans with proceeds from BTFP loans.

The amount borrowed at both facilities combined had peaked in mid-March at $165 billion and has since then dropped to $98 billion.

And so we put them on the same chart to see the flows between them, the loans at the Discount Window (red), and the loans at the BTFP (green):

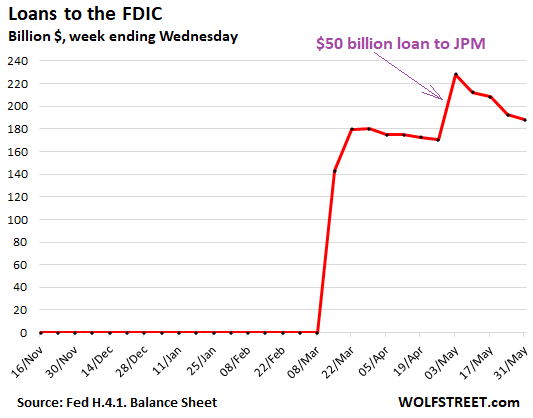

Loans to FDIC: -$5 billion in the week, -$40 billion for the month to $188 billion. That spike in the week through May 3 was caused when JP Morgan acquired the assets of First Republic from the FDIC.

JPM paid the FDIC $182 billion for those assets. The payment came in different forms (we walked through the details here). To make the $182 billion payment, JPM also obtained a $50 billion loan from the FDIC, similar to when you buy a shack with a collapsed roof for $182,000, and you pay $132,000 in various ways to the seller, including some cash, and the seller provides a $50,000 interest-bearing loan that you have to pay back to the seller over the next five years. It’s that loan that caused this spike because the FDIC borrowed this $50 billion from the Fed.

The FDIC is now busy selling the assets – mostly loans and securities – that it took over from the collapsed Silicon Valley Bank and Signature Bank. As it sells those assets and closes the deals, and returns the funds to the Fed, the loan balances to the FDIC drop.

QT continued on track throughout the banking crisis.

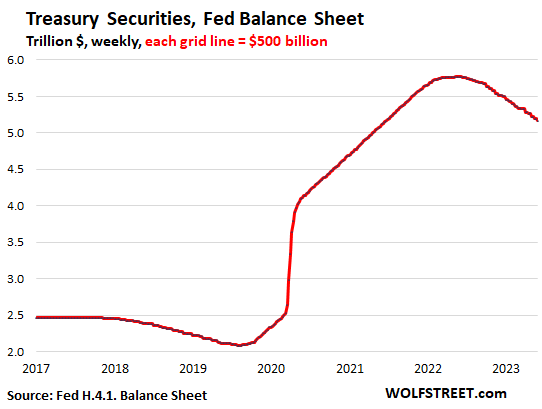

Treasury notes and bonds: -$30 billion for the week, -$58 billion for the month, -$607 billion from the peak in June 2022, to $5.16 trillion.

Treasury notes and bonds “roll off” the balance sheet mid-month or at the end of the month when they mature and the Fed gets paid face value for them.

The roll-off is capped at $60 billion per month, and about that much usually rolls off. But the $368 billion of inflation-indexed TIPS (Treasury Inflation Protected Securities) that the Fed holds earn inflation protection pegged on the current CPI rate. Unlike interest, this inflation compensation is not paid in cash, but is added to the principle of the TIPS, which causes the balance of the TIPS to increase by that amount, which keeps the roll-off just under the $60 billion cap in most months.

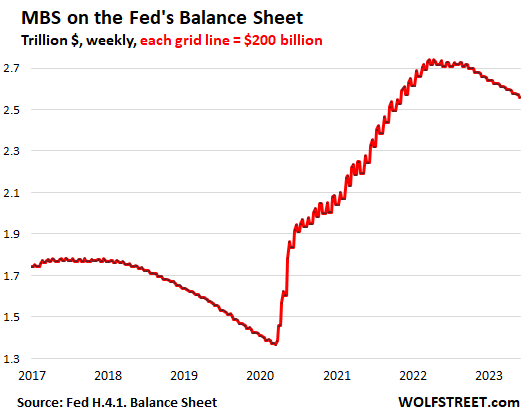

MBS: -$12 billion for the week, -$17 billion for the month, -$182 billion from peak, to $2.56 trillion. The Fed only holds government-backed “Agency MBS,” and taxpayers carry the credit risk, not the Fed.

The way mortgage-backed securities come off the balance sheet is primarily via pass-through principal payments that holders receive when mortgages are paid off – when mortgaged homes are sold or mortgages are refinanced – and when regular mortgage payments are made.

The reduction in MBS has been below the monthly cap of $35 billion per month because fewer mortgages are getting paid off because home sales have plunged and refis have collapsed, and passthrough principal payments to the Fed have slowed:

From crisis to crisis to raging inflation. This is the long view of total assets on the Fed’s balance sheet:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

wolf,

I love your work, only place.like it. That being true, so little drawdown by now, should have been selling thru 2020 & 2021, could have been well below 7 trillion. Powell has to see that selling mbs need to happen. Can’t stop wasting good economic times and not be extracting more liquidity now, before worm turns.

Can’t count from SVB as they are symptoms of Powells hesitancy in waiting as long as he did

Why do you feel Powell works for you. He is part of the club with 3 objectives:

1. To make money for the club.

2. To keep making money for the club.

3. To make more money for club each successive year.

You are not in the club, neither is Wolf!

Leo,

Agreed, fair point but I’m still suffering under the delusion the fed has some concern for the health of the financial economy. There is utility in drawing out liquidity to discourage moral hazard, reduce asset bubbles and preserve monetary tools in advance of an actual liquidity event like the implosion of the Chinese property/local gov/financial bubble.

Selling mbs will force some actual risk drawdown, quicken residential and commercial propert price discovery I would submit doing so sooner rather than later would be better.

This is greatest bubble in history ,worldwide. All planned when the elites withdraw their fortunes ,we the people will all eat bugs. It’s been planned by bildenberg for decades .LOOK it up scary agenda.

Flea,

Nothing wrong with bugs. Good protein. Everyone pays top dollar for crab and lobster and they are just big bugs.

And actually much healthier (and MUCH cheaper, and easier on planetary resources) for you than mammal meat. (See CMAH gene mod , Glycocalyx is on EVERY living thing, ….it made multicellular possible, and auto immune disease theory, such as it is.

But you won’t, because you like bitching at “bashableburgs”, etc, much better.

Your lifestyle just COULDN’T be to blame…that would be YOUR OWN fault…..and therefore totally unacceptable.

Make that collective bitching…it’s no fun without someone who completely agrees with you.

Powell just pumped a 25% rally on Nasdaq despite ridiculous earnings! Why will he sell MBS?

Wolf, can you please prepare a chart of the Fed’s balance sheet vs GDP since 2008? I think that will provide a better insight as to how much the Fed has been trying to prop up asset prices/the economy?

here you go:

QE, the biggest wealth transfer mechanism, reverse Robinhood brought to you by you friendly FED.

Even though most politicians, economists, and mainstream pundits won’t admit it, central banks exist to help governments finance themselves by stealthily transferring wealth away from the average person’s savings.

It’s the hidden, but real, reason why central banks exist.

How does the proposed 4 trillion dollars, (if it is 4 trillion ??) in extra government spending, ruin any QT plans by the Fed or does that just keep the debt up with inflation….

Whatever additional debt the government issues is unrelated to the Fed’s QT. But it may well drive yields higher (which is what the Fed wants to accomplish with QT) as more investors need to be attracted, and further deficit spending may throw additional fuel on inflation, and if this happens, you’ll see higher rates from the Fed and even more QT.

Back to yesterday’s post about housing. Again, a 3%’ish housing price decline in 1 year is literally nothing. Housing only took 2 years to bottom @ 26%+ decline during the great recession caused by an enormous spike in layoffs & foreclosures. Well, we all know that’s NOT going to happen this time. So, the housing market is holding up quite well given all the doom and gloom. AND, it appears to have bottomed out, for now, and we’re looking at “possible” rising prices around the country. Sure, this could change in 6-9 months, but for now housing & labor are tracking along quite nicely. Be that as it may, I do think 2024 & 2025 will bring a real, moderate recession.

Earnings estimates for 2024 are $224 (Bloomberg/S&P Consensus). Given corporate debt levels and rate rise, that number might be overstated by Wall Street, especially compared to 30 year EPS trend.

I’m guessing earnings come in closer to flat with ‘23 ($205-ish), unemployment numbers begin to move up, and that gets reflected as lowered housing demand.

7%+ mortgage rates plus rising unemployment will stall the home price rebound, IMO.

Stop posting BS. It took much longer than 2 years. I could go on, but I think this group can see your agenda.

During last housing crash, it took almost 5 years or so for home prices bottom to from.

The first 2 years were excruciatingly slow like what we are seeing now.

Housing might have bottomed in the great recession at -26%, BUT interest rates were also slashed from 6 to 0 to contain it, among other measures. Now we have a raise from 3 to 7 and maybe more.

Thanks Wolf!! If QE is indeed dead and buried due to the end of free money, we should see the Fed balance sheet as % of GDP get down below 25% (last decade’s good times). I’ll be impressed if I see it (though I would guess it could go either way).

QE didn’t prop up GDP. It inflated asset prices.

But it did help tax receipts

Dont you think higher asset prices prop up spending and therefore the GDP? And didnt QE cause inflation which increased wages, which propped up spending and thus the GDP?

The “long view” chart shows the immensity of the Fed’s balance sheet and just how much stimulus was recently jammed into the real economy. With fiscal deficits projected near two trillion, the Fed rate at 5% is a relatively tepid offset to huge continuing stimulus. I also wonder how many Treasuries the Fed has to buy each month to keep QT limited to 60 billion each month; some “reinvestment” of maturing Treasuries must still be occurring? Wouldn’t that be residual QE?

Isn’t GDP being inflated by ‘inflation’ which itself is really high because of high QE?

“Nominal” GDP is inflated by inflation. Nominal GDP has to be used when you compare non-inflation adjusted data, such as debt-to-GDP or Fed-assets-to-GDP.

“Real” GDP is adjusted for inflation. Nearly all GDP figures anyone cites are “real” Figures. So if the Fed’s policies cause inflation, that inflation factor is then removed from the “real” GDP figures.

Of course QE propped up GDP. Without the QE, there would have been a severe & VERY lengthy recession vs the 6-8 weeks that everyone basically went on PAID vacation.

That’s a beautiful red herring that has been promoted for years by the beneficiaries of QE (wealthy asset holders). QE started in 2009. The Fed used insta-liquidity measures in 2008 to deal with the Lehman debacle. It then let the liquidity measures run out in early 2009, and you can see that in the long chart above, when its balance sheet declined by like $400 billion in a few weeks (that was a big part of the much smaller balance sheet back then).There was no need to do QE back in 2009-2014.

And there was no need to do QE from March 2020 – Ma3 2022. The Fed could have just used its liquidity tools to keep the Treasury market orderly (and it did that) for a few weeks, and then let the rest go where it may. It was the government (not the Fed) that handed out the money to companies and people. The Fed handed money to the rich to make them even richer. Now people cannot afford to buy a home because of this BS.

All QE did was vastly increase the already terrible wealth inequality in this country. QE is and always was an insidious formula to make life more expensive for working people with few assets, and to make the wealth even wealthier. Go have a look:

Hear Hear Wolf!

I saw wealth inequality in it’s worst form the other day. Had a case in Chinatown DC. Haven’t been there in a decade. Along the main drag 1 block from where the Wash Capitals play hockey, I walked down a block where I felt like I was in the Tenderloin district of SFO. Vagrants all over the place yelling and screaming and shooting up with drugs, hitting me up for cash, filth, trash everywhere, mom & pop shops hosing down sidewalks. This used to be a nice safe family neighborhood. No More. This is collateral damage from decades of QE.

Government spending, enabled by the government’s borrowing, assisted by the Fed policies (QE)…..is what % of GDP?

The graph of the Federal Reserve’s balance sheet looks impressive only because it is the very top. Looking loosely at the graph the peak was about 8.95 trillion around March or April of 2022. Removing the banking crisis effect, around March of 2023 the balance sheet was about 8.35 trillion.

So in one year the fraction that remains is 8.35 ÷ 8.95 = approximately 93%. That is a reduction of 7% a year, since the reduction nominally is a constant dollar amount this balance sheet curve can be extrapolated as 7% reduction for the future years. 100% ÷ 7% per year = 14 (fourteen) years; one down 13 (thirteen) to go. Certainly even this snails pace will be interrupted by the elites need for a liquidity infusion of a variety of styles; look at the banking crisis as a short 3 month interruption, but there is as huge a variety of bailouts needed as the kind of “financial products” that have been and continue to be spawned by our financial market casinos.

Your whole calculus is off. QT didn’t even start until June. It was phased in slowly. Normal pace started in September. We discussed this extensively at the time. We had something like 9 months of full QT so far.

Regardless of the exact calculations, I share your sentiment. 20 years of hyper-financialization of the economy will require constant, well… financialization. When everything is a financial instrument, everything is prone to a financial malversation. I fully expect jagged Fed balance sheet to oscillate around $8.5B. First QT, then not-QE. Until it needs to go higher. Then a lot more non-QE.

huge mistake on Fed part to buy that many MBS. Now they are not able to reduce them. By the time rates go down, Fed will be doing new QE. At some they might be holding more MBS than treasuries.

Huge mistake that they bought any MBS. Ever. If they make the mistake of doing QE again, they could do treasuries only. Hopefully QE in any form is dead for the foreseeable future.

Any future QE should be met with angry mobs. The young people need to stand up for themselves.

put it in a instagram post by a celeb and they might hear it

I spoke with a dozen or more 30 year old professionals recently. Engineering and IT folks. They don’t know what the federal reserve is, and they have no idea they are getting shafted by federal debt, asset inflation, etc.

Wow i,ve learned a lot within seconds.

I tell my kids about inflation = theft of their money,falls on deaf ears .until one day they wake up and a loaf of bread is a wheelbarrow of money. This will end in a ww 3 always does

I would have thought the engineering folks could read..

If the “young people” knew the damage being done to their financial future, their financial “environment”…..they would shift from climate concerns to economic concerns.

@longstreet

Why do they have to pick? They should be concerned by both.

It’s because their living standards have not declined (far enough).

Even the noticeable percentage who are (nearly) broke have access to easy and cheap enough credit which enables them to live above their means.

Once living standards decline enough (whatever that is), the fantasy dream world ends.

Nothing like the fear of total annihilation to keep other issues unimportant and keep the masses attention off those other things. It’s so polarized nothing can really be sorted out. Lots of invested interests pushed forward.

I notice there isn’t much talk about *pollution* anymore. That was one thing almost everyone was concerned with; pollution and radiation. Masters of marketing.

Seems like Flagstar Bank is acquiring part of Signature – one of my brokered Signature CDs recently updated its description to Flagstar (Signat).

How is QT on track? Unless QT accelerates, we went backwards. How many other events will cause this backwards retracing again? Nobody knows.

I love your reports and insights

But you, for the 3rd time, put out the notion that the snb would have gotten liquidity from the ced for the CS bailout.

As informed prior, the CS received 259 bil total but in CHF

So for one i fail to see what the fed has to do with the snb giving loans to start with, but since they were in a different currency it just doesn’t make sense to think the US$ Fed had any funding in it.

If you look at M2, (https://fred.stlouisfed.org/series/M2SL) I think it *tells* the story; the Fed will want to bring it back to “historical trend”, that requires ~$2 Trillion contraction. Some ways to go! More rate hikes and QT, we will probably hold 6-6.5% rates for a year when we get there, if M2 is a guide.

Looks to me it is off the “historical trend” by around $4 Trillion

Why in gods name did they pump $1.5 trillion of QE into the market starting in January 2021, when we were already past the economic shock and we’re already experiencing widespread supply chain problems keeping up with demand?

You could give them a blank check and they’d piss it all away. Makes a lot of people rich. “Never let a crisis go to waste” or something like that.

Not surprising at all. And now that temporary Covid budget turns out to not be temporary. It’s now built into the baseline budget.

They have had a blank check for 100 years.Rich haven’t figured out they will end up as peasants.After 1% havestolden all productivity out of system. And there’s no more to steal

Spot on. Money flows, the rate-of-change in the volume and velocity of means-of-payment money, rose to historic levels back in November 2020.

Inflation was no happenstance.

The Omicron variant.

Very timely update of the Fed’s balance sheet. Was waiting for this piece. Judging by the recent arrogance and perverse animal spirit of Wall Street, the QT needs to accelerate a lot faster to quell the reckless speculation. Gamblers are making a killing with the endless liquidity in the market.

actually, alot of liqudity will be removed as soon as the Treasury can start back the debt issuance. i saw that that extraordinary measures had been used to the tune of 300 billion, the Treasury balance was drained from over 600 billion at beginning of the year to near zero now and assuming the fed keeps letting Treasuries and MBS roll off, it will be another 200 billion that the markets must absorb over the coming 3 months. and on top of that, they will need to finance the on-going deficit spending. of course, they might not bring Treasury balance up to 600 billion too quickly, to brunt the impact. and i dont know what the timeframe or process is for reversing those extraordinary measures.

i am starting to think that the one factor that will finally force a reckoning is the interest expense on debt. it is more than 200 billion in Q4 of last year and i’m assuming will hit 1 trillion annual pace soon. with that much interest paid, the federal budget gets even more out of whack. we can all bet that the politicians wont cut any spending, so that is going to become a real issue.

when you look back at what happened during COVID, it was a real ponzi scheme by the government. the Fed was “buying” massive amounts of debt, so the Treasury could issue massive amounts of debt at extremely low interest rates to fund astronomical stimulus programs. the Treasury never could have added that much debt without driving rates much higher if the Fed were not buying it up. but now we are stuck with that extra debt and could be headed to a period of higher interest rates for longer, meaning massive interest payments as far as the eye can see.

i wonder why china did not liquidate its US treasury holdings while interest rates were low and prices high?

If government officials had any brains they would have issued most of that debt as very long term debt, so they could lock in a low interest rate. I remember seeing articles that discussed that. But they didnt do it.

On 12 May 2023, the CBO stated that for fiscal year 2023, Uncle Sam will have $6.4T in outlays & $4.8T in revenue.

National debt, or, Uncle Sam’s monkey on the back, is at a fraction under $31.5T. Now, take that monkey and divide by 20 — or 5% interest carry cost. The result is $1.575 trillion in interest expense on debt.

The Senate has passed the debt ceiling bill. The CBO projects new deficits of over $20T in the next ten years. The national debt of citizens in the United States of America will be fifty-five trillion dollars in about nine years. That will be twice the GDP.

Thank you Two Party Duopoly.

“Put it on a plate, son. You’ll enjoy it more.”

“Couldn’t enjoy it any more, Mom. Mm mm mmm …”

In 2022, GDP was over $25 trillion. For the debt at $55 trillion to be twice GDP 9 years from now requires nominal GDP to essentially stay flat all nine years. Growth in nominal GDP from inflation alone makes that very unlikely.

The situation is bad, but not quite that bad.

rojogrande,

Yes, you are correct.

I should have said that the projected national debt will be more than twice the current GDP.

My question is, how much will inflation, and how much will high interest rates play off each other as the national debt continues to grow in next decade from deficits? My guess is that inflation & interest rates will both be at around 6% for quite some time.

If they stay equal, the dollar will slide backwards, and short-term Treasury ladders will balance out against the weakening dollars for a zero-sum game. But the national debt will simply continue on, and on, and on, and …

The situation is indeed bad.

PR,

I agree the debt looks set to go on and on. I can imagine a situation where your original comment is correct and debt is twice GDP in 9 years if there is a bad enough recession in the interim. There’s every reason to believe the response will be to keep borrowing and bailing out the banks, etc. I doubt the CBO factors that possibility in its projections though. At some point, even inflating away the debt will require lower annual deficits.

QT unfortunately hasn’t outpaced the drainage of the TGA this year plus some from o/n RRP that boost liquidity when they are drawn down. Table 1 of the Fed’s 4.1 balance sheet shows the number when accounting for TGA and o/n RRP drops under the “Reserve balances with Federal Reserve Banks,” which went up $69bb over the last week so lot of liquidity came in that week (it was $2.83T in Jan at its low since 2020 and now at $3.309T). Hopefully with debt ceiling passage the TGA refills and liquidity comes out of the system.

Woefully inadequate.

Woefully.

QT is a joke at this point. They’re STILL at $8.38 trillion from a peak of less than $9 trillion? How disgusting after all of that tough talk. Jerome Powell is like a cowardly Arthur Burns.

DC

He’s actually much worse.

when you compare powell to the ECB and Japan he looks less pathetic. although the ECB cut alot of loans, they have hardly sold any Treasuries. and both ECB and Japan bought a much larger percent of their debt balances.

Canada was the smart central bank, about half that stuff off the balance sheet. Canada is interesting because it has an obvious home bubble, but they have been able to get 25% of homeowners to extend their loans out further to refinance the mortgages that came due. With high migration increasing housing demand, it is possible they can keep the prices high, but it is screwing over their young people in a huge way.

This may be off the wall, but I am concerned that the nosebleed prices for domestic assets will be purchased with funny money from China, Europe, Japan, etc. All went all in on the QE ethos and are now dragging their feet as far as concern for defeating the world wide inflationary bubble.

dang,

You have to look at the FX market tho.

Their currency would theoretically be devalued with such policies (barring manipulation).

Check Turkish Lira charts.

these “plunges” are miniscule compared to the massive increases.

the trouble is that once inflation is subdued, the Fed will use that as a reason to stop normalizing the balance sheet, which is propping up asset bubbles. there should be as much focus on asset bubbles as on inflation within the economy. neither lead to higher productivity.

“these “plunges” are miniscule compared to the massive increases.”

Exactly. A “plunge” would be a straight line down just like the straight line up during the massive QE. This is like a fart from an ant. Insignificant.

LOL, they sure called it a HUGE SPIKE when it went up $400 billion, and everyone oohed and aahed. Now that it has nearly unwound that spike, it’s not a PLUNGE/ And everyone in the blogosphere is silent about it? You people are funny without wanting to be.

Off topic but-

Recent TD Ameritrade brokerage account switched to Schwab.

I’ve looked around Schwab for their cash options and can’t find anything other than bank accounts that pay 0.45%. Not counting brokered CD’s and stuff. At ETrade there is a premium savings that pays almost 4%. Is there anything comparable at Schwab, or what is the best place to park cash and earn some interest there? Not interested in 0.45%…

They have Schwab Money market funds that are re-indexed weekly. They go by names like SNOXX, or SNVXX or SNSXX. Paying something like 4.75% this week. Takes a day to settle in or out.

Under Products, Money Market Funds.

Thanks for all the replies. Wolfstreet rules.

Gimp, SWVXX (MM Fund) pays about 4.9% (SEC 7 day yield). 1$ minimum to buy in.

If you don’t want a money market you can check lots of bond etfs (or just buy a bond).

SGOV or SHV.

Also VUSB or BIL, but I prefer the 2 above.

Those are all slightly different “flavors” so read the print on them.

I also sprinkle some VGSH for a bit more duration.

the Schwab Value Advantage Fund SWVXX is currently ~4.9%. You can move in and out overnight.

Sorry for my post above, I did not see yours.

Interactive Brokers pays around 4.75% on cash.

You have to purchase money market funds directly at Schwab. Their Federal money market (SNOXX) yields close to 5%. Otherwise, you cash is swept to Schwab bank at .45%.

I am wondering about this myself.

Check out their money market funds — not FDIC insured, but your shares are securities not deposits, and you will still have the securities even if Schwab collapses.

Talking about Schwab, does anyone know how their CD offering from various banks nationwide work?

Schwab offers a host of CDs from banks nationwide. However, when you buy a CD listed by ‘abc’ bank thru Schwab, abc has no record of your CD, nor do they pay the interest or even issue the 1099. all comes from Schwab. abc bank(s) even do not have any relationship with Schwab!!!! So the money appears to stay with Schwab. How does this gimme work?

These “brokered” CDs are like securities, such as stocks, that you buy from your broker. The broker pays the dividend or coupon interest into your account, and the broker includes the proceeds when you sell it in the 1099 the broker sends you. That’s what a broker is for.

Maybe I am just not following, but QT continued throughout the bank “crisis” but somehow there was a temporary spike in total assets sometime in March/April 2023 ? So the Fed has a bucket for QT assets, and they have a separate bucket for the bank liquidity stuff so what matters is the reduction in total assets?

It’s not that simple. QE = securities purchases. QT = reduction in securities. During the bank crisis, the Fed didn’t buy any assets. It lent money on a short-term basis. Some of this money became short-term liquidity for the markets, now dwindling. Much of it didn’t. Part of what it lent to the FDIC didn’t go anywhere.

Most of this short-term liquidity has already been unwound, as you can see in the article. Just look at the pictures. The biggest thing left dangling is the FDIC loan.

When they decide to pause, would selling treasury notes (or even bonds) be appropriate? 2/3/5/7/10 are a good 1-1.5% below current fed rates. Could just sell 5-10 and even out the valley, to not disturb the 1 year much.

Hell, why not pause early and start selling mid duration. This talked about much? I don’t see anyone proposing an early pause coinciding with increased selling. Mid term bank assets would lose value, but BTFP rate should stay low and allow some protection. Overnight lending wouldn’t change, and maybe RRP would draw down.

Apologies, to clarify: I mean pausing rate hikes, and for the fomc to QT out of treasury notes, not selling of notes by individual investors.

Ted oxleyis buying 3-5year paper ,smart guy

What I’m suggesting would tank 3-5 year paper. Rates would go up, pricevwou

The plung by 348B is simply the new funny money created for bank crisis. If it was not originally QT, there is nothing to rejoy over their disappearance. When we take out that 348B, not much real QT has been achieved during the last 10 weeks. FED is lucky that the highly anticipated next recession has not arrived yet.

When I look at the rolloff of the MBS, it looks like everyone and their uncle are sitting tight on their MBS with FED. Are we not told again and again that Americans change their house on an average of 7 years? Perhaps the banks selected (they must have used AI even before they became fashionable) to pick all the scumbags and passed on to FED :)

“Are we not told again and again that Americans change their house on an average of 7 years?”

From the article:

“The reduction in MBS has been below the monthly cap of $35 billion per month because fewer mortgages are getting paid off because home sales have plunged and refis have collapsed, and passthrough principal payments to the Fed have slowed”

1) AAPL daily : for 6 months, until Apr 30 2022, AAPL failed to produce a close above Dec 13 2021 high @182.13 thereafter it plunged.

2) AAPL tried again in Aug 2022, but failed.

3) On Tuesday 5/30, after Memorial Day, AAPL gap up above Dec 13 2021 low @175.53, hopefully to an new all time high for the June 7/11 2023 show.

4) AAPL Lazer : Mar 27 2023 to May 4 lows // parallel from Apr 4 high. This Lazer approach Jan 2022 top, aiming at the skies.

5) While AAPL is aiming at the skies, trying to make a new all time high, Dollar General plunged along with the regional banks. The Fed might take a pause for the crumbs, ignoring the AI bull sh***run.

The Fed Total asset plunged from 9T to 8.4T to test Apr low. The 4T gov debt increase and the Fed plunge might be for dry powder, to be used later.

The Fed have sophisticated emergencies “tools”. The Anti Regulatory Act of 2006 were tested successfully twice before. The Fed shot down two deep recessions.

The Fed shot down price discoveries.

Fooling around with market prices is sure way to make an economic situation worse. There is a reason a piece of gum has a low price and a car has a high price. It is so obvious that only the out of touch think manipulating prices improves the economy.

I definitely learned something with the statement that the increase of Fed balance sheet was not the increase of gdp but rather asset prices rising. A reduction of the balance sheet though slow is causing a reverse effect. Just read last night about more CMBS headed to special servicing. Wolfs summaries for the CMBS situation could come in rapid fire real time curve updates as the special servicing teams handle all the properties.

Wolf is it worth it to do an article on the near term issuance of debt and what it will do to the markets?

I have an uninformed theory that we’ve basically just had a little QE by virtue of the treasury not issuing as much debt as they normally do and now that they’re allowed to do so we will likely rollback some of the market gains as old and new money finds a nice home in US government bonds.

What impact will this also have on mortgage rates and auto rates? Have these been artificially stunted by the lack of buyable government debt which would drive the yields down as everyone bids for a smaller share of debt?

Need to distinguish between temporary liquidity added or subtracted (TGA, bank liquidity measures) and QE = asset purchases by the Fed.

Liquidity injection (for example, gov draws down its TGA) and liquidity removal (for example, gov refills its TGA by bill and note issuance) does have impacts on the markets, but those impacts are temporary. So drawing down the TGA added liquidity to the market, and refilling it will remove that liquidity. So that liquidity injection was temporary. QE was permanent until QT removes it years later, and not all of the QE purchases will be removed.

My savings have been permanently devalued because central banks knowingly and deliberately enacted policies to appropriate a big part of my store of value to give it to the rich. They have no intention of making me whole again, ever.

They’ve been doing this since I started working around 1998.

Not just the rich, also beneficiaries of social transfer programs.

Government operates the ultimate criminal extortion racket. That’s what institutionalized currency debasement represents, from the beginning.

I don’t know why the Fed doesn’t just leave interest rates to the free market and expedite unloading of the balance sheet at a more rapid rate. If it requires selling securities on the open market, especially MBS which they never should have owned anyway, then so be it. When you make a mistake as Bernanke did back after the GFC, the best course is to undo the mistake first before more meddling further in the financial markets. What’s wrong with that?

Apparently, the Fed seeks to keep asset prices high, while forcing non-asset holders to bear the brunt of a recession.

Is there anybody in Federal Reserve or Congressional leadership with a net worth less than $40 million?

I suspect MBS rolloff will continue to be slow. How many mortgages were taken out/refi’d at rates below say, 4%? And why would anyone with such a mortgage pay extra towards it when they can stuff their extra cash into a CD that earns 5%?

As long as this arbitrige exists, and the housing market remains frozen, I don’t see MBS rolloff happening any quicker.

In this context, would selling a small amount of MBS outright really be that much of a shock to markets and the economy?

Good point. I do not want to make any extra payments on my 2.5% rate. I think that is also the case with a few friends when this topic is discussed.

If you save your profits ,long enough and bank it . Might be able to just pay off loan . Never make extra payments if you run into trouble it’s just cream for bank

You are right

Hence we need higher rates for longer.

People would sell when they are forced to for whatever reasons

The Fed is currently making an earnest effort to reduce its balance sheet.

I have serious doubt about how long they can continue this. My guess is somewhere in the fall of this year things will start to blow up again. Probably commercial real estate.

General consumer spending is dropping. Its not going to collapse, but overall slowing will exact pain. Housing is in a state of transition regardinig past patterns.

The debt ceiing resolution essentially gives Congress ability to spend as needed to lessen impact of known upcoming recession. 2 years from now, we’ll be at least 4 Trillion more in debt, likely more.

Meanwhile, China will be hit with slowing demand and has a number of fundamental problems with its economy. Russia will earn less money from resources as economy slows, but will muddle on through. They have little debt and lots of resources to sell.

The wild card is a black swan event; likely around Ukraine. Something big could shock the world as Russia slowly breaks the stalemate. Otherwise, we’ll continue to muddle along with everyone plugging holes in the failing dike.

Consumer spending is not slowing down

Job market is still too hot

https://wolfstreet.com/2023/05/26/despite-getting-whacked-by-bank-turmoil-layoff-news-credit-crunch-high-interest-rates-and-inflation-our-drunken-sailors-spent-even-more-even-adjusted-for-inflation/

Apple stock all time high.. Lululemon had a block buster quarter ..

Hotels airlines restaurants all pack

I don’t see any spending cut

Fed is playing a charade that it is serious about taming inflation but it is not

From your previous reply to my post:

“During last housing crash, it took almost 5 years or so for home prices bottom to from.”

Go narrow in on Q1 2007 (high) to Q1 2009 (low). It took EXACTLY TWO YEARS TO FIND THE BOTTOM from the top. Not less, not more.

https://fred.stlouisfed.org/series/MSPUS

That data is based on prices in mortgages under HUD, which back then was a much smaller player in the housing market. Cash deals and other deals with other mortgages are NOT included in the prices. This data set should never be used in the broad sense because it is systematically different from the overall market.

Use the Case Shiller National Home Price Index or the NAR national index, and you will see the 5-year time span

Look around. Reduction in spending is happening. It will accelerate.

With every “crisis” the Fed/Govt gains more power.

And who creates these crises? We all saw the QE was ill advised.

IMO, we are headed for a digital currency and a Nationalized banking system ( covering all deposits ala Yellen’s decree). Now, who could be against that? /s

There isn’t a specific trigger event to create a trend change. Events don’t spend or borrow money and don’t produce or consume anything.

When it happens, it will be psychological, regardless of the ultimate underlying “reason”.

Looking at the Fed’s balance sheet and its general upward trend, reminds me of the final scene in the Thelma and Louise movie. You can take your foot off the accelerator and tell yourself you are braking. Yes, you may slow down somewhat, and it might take slightly longer to get there, but the end result is the same.

Do you guys think after June and/or July interest rate increase, do you guys think there will be more rate hikes in the remaining part of the year?

Going up to 8 to 9 percent by end of the year. 🤦♂️

A 7% Solution is the answer.

Definitely interesting to see the draws from the Bank Term Funding Program continue to rise. It’s a better deal than the Discount Window, but it’s still expensive money. First Republic definitely won’t be the last top 100 bank to fail this year. QE and free money for too long, it encouraged these institutions to take ridiculous risks…

“Whatever additional debt the government issues is unrelated to the Fed’s QT. But it may well drive yields higher (which is what the Fed wants to accomplish with QT) as more investors need to be attracted, and further deficit spending may throw additional fuel on inflation, and if this happens, you’ll see higher rates from the Fed and even more QT.”

Without QE, who will buy all this new debt? If we have a failed auction, could/would the Fed reverse course on balance sheet reduction?

Yield solves ALL demand problems. If the yield is high enough, I and the entire rest of the world will buy them. Yields rise until there is enough demand.

I think you will see, ultimately, a reduction in the balance sheet to around $7.5 trillion before it begins rising again. The long term trend up, up, up, up.

Of course, all of this ignores that the FHLB has added about $600-700 billion to its balance sheet while the FED has been reducing its by about the same amount.

Nothing to do with anything here.

FHLBs raise cash by selling bonds to the bond market. It’s just like a bank selling bonds to raise cash (and they do). That has zero impact on monetary policy, QE, or QT. Then the FHLBs lend the money to banks, and charge interest on it, which also has zero impact on monetary policy, QE, or QT, it’s just like a bank lending to some entity, including other banks, and they do.

So, you are claiming that the FHLB system borrows cash in the public market and then uses that cash, and only that cash, for loans fully collateralized? 100% of the loans they make are funded by bonds the FHLB system issues to the public?

Here’s what they sold at their bond auctions over the past six weeks, plus a whole bunch of other info on their bonds:

https://www.fhlb-of.com/ofweb_userWeb/pageBuilder/new-bond-issues-48

Where else do you think they get the cash to lend to the banks? That God gives it to them?

As long as productivity falls faster than QT, there will still be inflation.

Seemingly everyone focuses on the ‘money printing’ aspect of inflation while ignoring the productivity part of the equation.

Productivity’s crash over the last whatever (half a century?) keeps me up at night, but that just shares headspace with what inflation does to empires, as well as the reintroduction of nationalism and mercantilism (not bad things for us necessarily), and the dramatic increase in geopolitical tension.

I feel as if I “benefit” from the old saying, May you live in interesting times.

Leo,

Agreed, fair point but I’m still suffering under the delusion the fed has some concern for the health of the financial economy. There is utility in drawing out liquidity to discourage moral hazard, reduce asset bubbles and preserve monetary tools in advance of an actual liquidity event like the implosion of the Chinese property/local gov/financial bubble.

Selling mbs will force some actual risk drawdown, quicken residential and commercial propert price discovery I would submit doing so sooner rather than later would be better

Y’all are all concerned about inflation, but I heard the REAL PROBLEM is KILLER ROBOTS!!!

I’d ask Wolf, but I heard he’s been replaced with AI.

I’m fighting off AI at the door with a kitchen knife in my hand, LOL

There is actually a serious aspect about generative AI, in that it steals my content, rephrases it a little, and puts it out as a search result, without link or attribution.

Google already switched to no-click search results a while ago, where you get the relevant paragraph quoted from my article, so you don’t have to go to my article and read it. But it still shows the link and the attribution, and a few people click on the link. Generative AI skips the link and attribution.

FB constantly gets in hot water with spreading media articles on its site where it collects all the ad money, not the publisher. Regulators are trying to crack down, but FB fights back hard, throwing lots of money around.

Generative AI is the next step in content theft. That may eventually get tested in court, but the big companies always seem to get away with this stuff after accepting a settlement that’s not even a slap on the wrist.

Let me pay a big compliment to Wolf, specifically, his content mediating skills here. I used to comment on another site, but suddenly it installed a very aggressive (obviously AI-mediated) content mediation filter. It basically shot down everything I tried to write. It has no subtlety or nuance or humor whatsoever. I immediately deleted that link from my browser list.

“To see the details of the banking crisis, here are total assets viewed through a magnifying glass“

Appreciate you magnifying that piece, as it also helped me see the reduction from QT so far.

QT causing stocks to soar. Who would’ve thunk..

I am becoming inured to the financial insanity that your first class graphics depict. Building into my budget a 6%, increase in prices across the board as long as Powell continues to tease the markets.

If a civilian, like me, were to attempt to trace the genesis of QE, it was the expansion of China from an agrarian organic level of living too the head aches of being recognized as a super power. Quite a story.

The creation, essentially, of the Chinese currency as we know it today is worthy fodder for future story tellers.

The FOMC should announce on June the 14th that the FFR will be increased by 25 bpts and that the FFR rate will increase as long as prices continue to increase.

The excuses have rung hallow. It is time to confront the inflation monster. Because it is the right thing to do.

Inflation is the worst thing that we can impose on the majority of citizens that are in the process of family formation. Our seed corn.

Hubris, more often than naught, portends the end.

My view of the stock market valuation is that, pretty much every stock is overvalued by a statistically significant amount, like 40%, or more.

Just like the Bard warned, paraphrasing, ” May fools tread lightly, into the dark night, that offers no shelter”.

I’m not sorry that I divulged my investment strategy on-line which is an extremely conservative strategy of wealth sustenance. The only thing that seniors should be invested in is short term treasuries paying over 5% interest finely.

The risk markets are trying to reprice the risk premium for private markets vis a vis the deranged Fed policy of zero pct interest rates.

Somehow that made sense to a cadre of ivy league charlatans.