But durable goods prices drop, energy inflation eases, food inflation is less bad.

By Wolf Richter for WOLF STREET.

The Consumer Price Index (CPI) for February showed once again that inflation rages in services at the worst levels in four decades, while inflation in many goods categories continue to back off:

- Services without energy services: annual inflation jumped by 7.3%, a four-decade high, driven by housing, food services (food away from home), auto insurance, repair services, airline fares, pet services, hotels, and delivery services.

- Food at home: inflation rose at a slower pace in February from January (+0.3%). But year-over-year, still +10.2%.

- Energy inflation overall fell month to month (-0.6%), which whittled down the year-over-year inflation rate to +5.2%. Gasoline prices -2% from a year ago.

- Durable goods prices fell again month-to-month (-0.4%) and year-over-year (-1.8%), driven by price declines in used vehicles and consumer electronics.

- Core CPI: accelerated to +0.5% month-to-month, third month in a row of acceleration. Year-over-year: +5.5% (from 5.6%).

- Overall CPI (CPI-U): +0.4% month-to-month, +6.0% year-over-year.

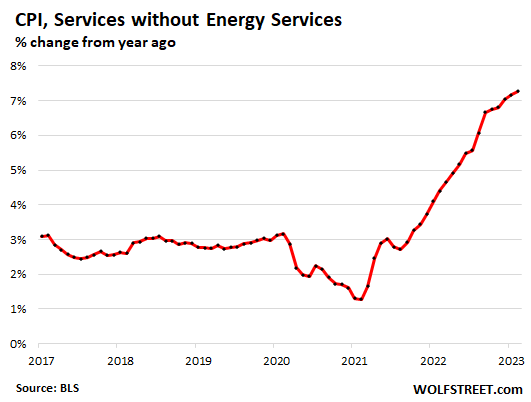

Services inflation without energy services jumped to four-decade high.

The CPI for services inflation without energy services jumped by 7.3% in February year-over-year, the worst increase since 1982 and the third month in a row above 7%, according to the CPI data released today by the Bureau of Labor Statistics.

In services is where inflation is now raging and entrenched. Nearly two-thirds of consumer spending goes into services:

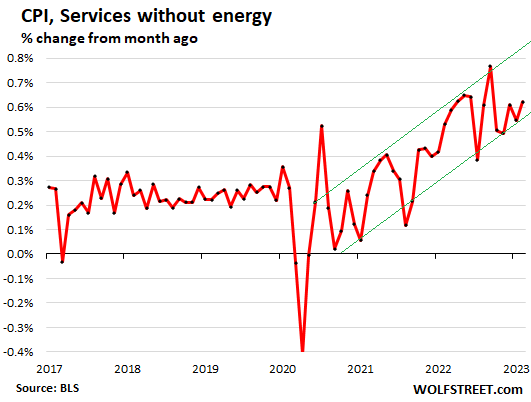

Month-to-month, services inflation without energy services jumped by 0.6% in February from January. It has been in the 0.5% to 0.8% range for 12 months. In services is where inflation gets sticky. The green lines are food for thought:

| Services less energy services | Weight in CPI | MoM | YoY |

| Overall | 58.1 | 0.6% | 7.3% |

| Airline fares | 0.6% | 6.4% | 26.5% |

| Motor vehicle insurance | 2.5% | 0.9% | 14.5% |

| Motor vehicle maintenance & repair | 1.1% | 0.2% | 12.5% |

| Pet services, including veterinary | 0.5% | 1.8% | 10.5% |

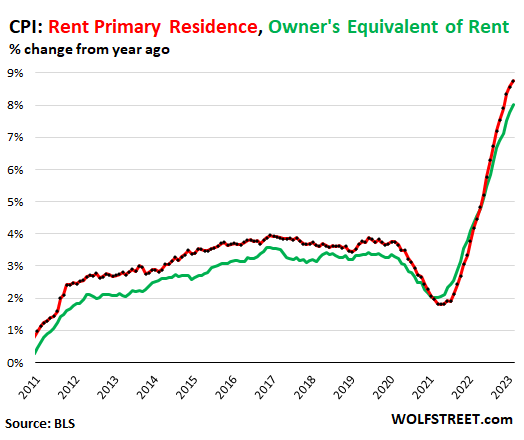

| Rent of primary residence | 7.5% | 0.8% | 8.8% |

| Food services (food away from home) | 4.8% | 0.6% | 8.4% |

| Owner’s equivalent of rent | 25.4% | 0.7% | 8.0% |

| Postage & delivery services | 0.1% | 0.2% | 7.7% |

| Hotels, motels, etc. | 1.1% | 2.3% | 6.7% |

| Recreation services, admission to movies, concerts, sports events | 3.1% | 1.2% | 6.3% |

| Other personal services (dry-cleaning, haircuts, legal services…) | 1.4% | 1.4% | 5.6% |

| Water, sewer, trash collection services | 1.1% | 0.8% | 5.2% |

| Video and audio services, cable | 1.0% | 1.6% | 5.1% |

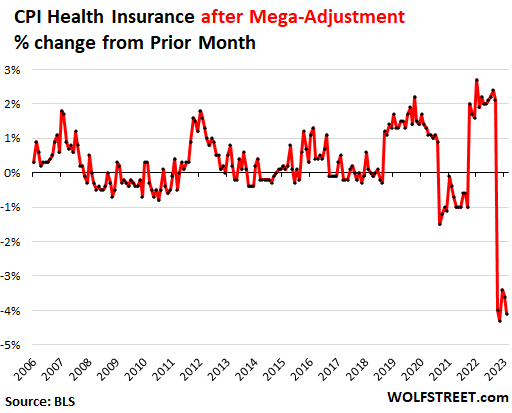

| Medical care services | 6.6% | -0.7% | 2.1% |

| Education and communication services | 4.9% | 0.2% | 2.9% |

| Tenants’ & Household insurance | 0.4% | -0.1% | 0.8% |

| Car and truck rental | 0.1% | -0.5% | -0.8% |

Note: Health insurance mega-downward adjustment, part of “Medical care services.”

BLS undertakes annual adjustments in how it estimates the costs of health insurance and then spreads those adjustments over the following 12 months. The first mega-adjustment hit in October and every month since (more details here).

In other words, for the 12 months through September 2022, CPI overestimated health insurance inflation (+28% yoy in September 2022), and it now corrects for this overestimation by spreading the a massive adjustment over 12 months through September 2023.

Without that mega-downward adjustment, services CPI would have been even worse for the past four months.

Due to this downward adjustment, the CPI for health insurance plunged by 4.1% in February from January. The five months of mega-adjustments reduced the year-over-year rate of the CPI for health insurance from the pre-adjustment +28% in September to -4.7% in February.

But, but, but… the PCE price index, to be released later in March, which the Fed prefers, figures health insurance inflation differently and has had no adjustments. And in the PCE price index, services inflation has been aggressive.

Here are the month-to-month changes of the health insurance CPI after the adjustments:

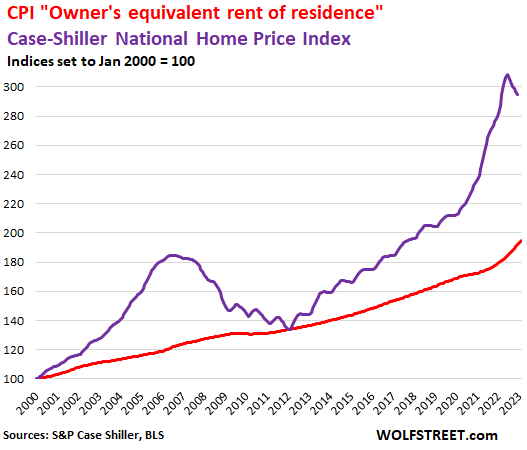

The CPI for housing as a service.

The CPI for housing as a service – “rent of shelter” – which in February weighed 34% of total CPI, is based on rent factors, primarily “Rent of primary residence” (weight: 7.5% of total CPI) and “Owner’s equivalent rent of residences” (weight: 25.4% of total CPI).

“Rent of primary residence” tracks actual rents paid by tenants in houses and apartments, including rent-controlled units. The survey follows the same large group of housing units over time and tracks what tenants are actually paying in these units. So this reflects actual rents paid by tenants.

Not “asking rents.” Other rent indices, such as the Zillow rent index, track “asking rents,” which are advertised rents of still vacant units on the rental market. When asking rents are too high to fill the units, landlords may lower the asking rent. There was a boom in asking rents during the pandemic. But rentals don’t turn over that much, and proportionately not many people actually ended up paying those asking rents.

“Owner’s equivalent rent of residences” tracks the costs of homeownership as a service, based on what a large panel of homeowners report their home would rent for.

Both rent factors jumped:

- Rent of primary residence: +0.8% for the month, + 8.8% year-over-year, worst since 1982 (red)

- Owner’s equivalent +0.7% for the month, +7.8% year-over-year, worst in the data (green)

Home prices, based on the Case-Shiller Home Price Index, peaked with the report called “June” then started to decline [my version by city: The Most Splendid Housing Bubbles in America]. The most recent data point is the three-month moving average of October, November, and December (purple in the chart below).

The red line represents “owner’s equivalent rent of residence.” Both lines are index values, not percent-changes of index values:

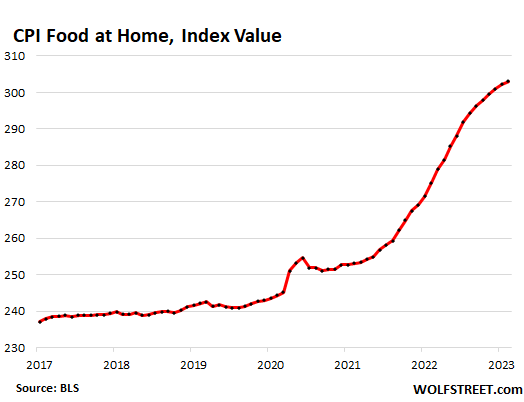

Food inflation.

The CPI for “food at home” – food bought at stores and markets – rose by 0.3% in February from January, less bad than in prior months. Year-over-year, the CPI for food at home rose by 10.2%, the 12th month in a row with double-digit year-over-year increases, but on a downward trend.

This chart of CPI for food at home as an index value (not percent change) gives you a feel for the cumulative spike in food prices over the past two years: +20% since February 2021.

Inflation in many categories has retreated, but heated up in some. The CPI for eggs had spiked on supply problems due to the avian flu, but consumers went on buyers’ strike, demand plunged, and prices have started to settle down:

| Food at home by category | MoM | YoY |

| Overall Food at home | 0.3% | 10.2% |

| Cereals and cereal products | -0.1% | 14.2% |

| Beef and veal | 0.6% | -1.4% |

| Pork | 0.7% | 1.5% |

| Poultry | 0.1% | 9.5% |

| Fish and seafood | 1.5% | 4.6% |

| Eggs | -6.7% | 55.4% |

| Dairy and related products | 0.1% | 12.3% |

| Fresh fruits | 0.4% | 0.4% |

| Fresh vegetables | -0.7% | 5.3% |

| Juices and nonalcoholic drinks | 1.0% | 12.3% |

| Coffee | 0.3% | 11.4% |

| Fats and oils | 0.4% | 19.4% |

| Baby food & formula | 0.5% | 9.8% |

| Alcoholic beverages at home | -0.1% | 4.3% |

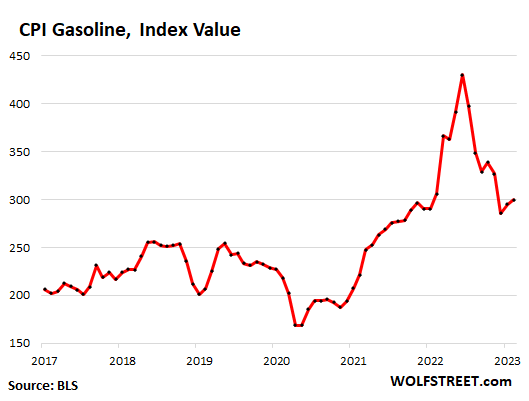

Energy prices:

| CPI for Energy, by Category | MoM | YoY |

| Overall Energy CPI | -0.6% | 5.2% |

| Gasoline | 1.0% | -2.0% |

| Utility natural gas to home | -8.0% | 14.3% |

| Electricity service | 0.5% | 12.9% |

| Heating oil, propane, kerosene, firewood | -6.4% | 5.7% |

The CPI for gasoline as index value (not percent change) depicts a crazy two-year spike that has only partially unwound:

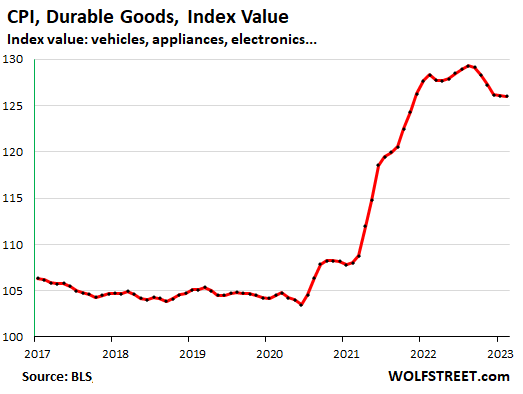

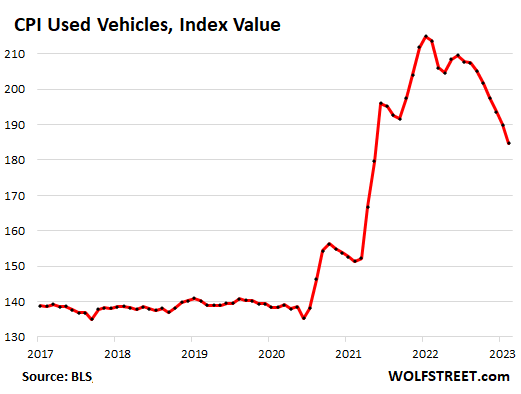

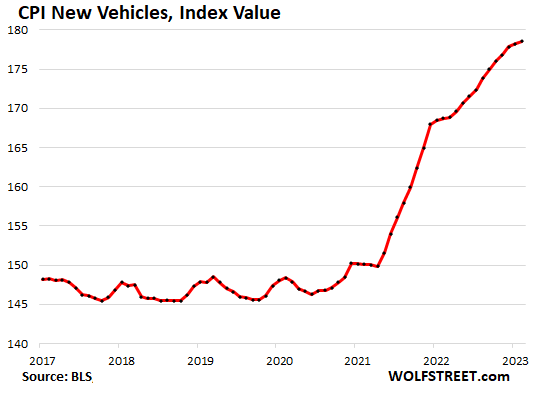

Durable goods prices.

The CPI for durable goods dipped for the sixth month in a row, by 0.4% month to month. On an annual basis, it fell by 1.8%, the second month in a row of annual declines, after a flat reading in December.

| Durable goods by category | MoM | YoY |

| Durable goods overall | -0.4% | -1.8% |

| Information technology (computers, smartphones, etc.) | -0.9% | -12.0% |

| Used vehicles | -2.8% | -13.6% |

| Sporting goods (bicycles, equipment, etc.) | 0.2% | 1.1% |

| New vehicles | 0.2% | 5.8% |

| Household furnishings (furniture, appliances, floor coverings, tools) | 0.8% | 6.3% |

The CPI for durable goods, expressed as index value (not as percent change) shows the mega-spike in prices starting in late 2020 through mid-2022. Prices started to drop last fall, driven by sharp declines in used vehicles and consumer electronics:

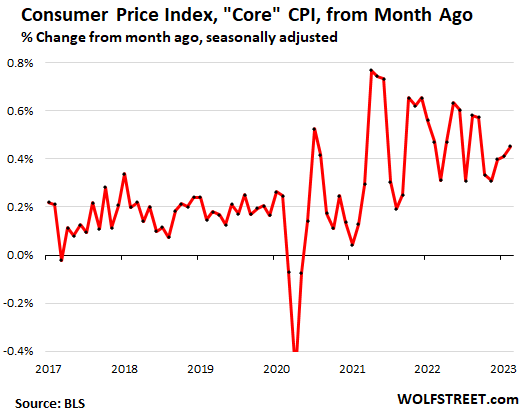

“Core” CPI.

Year-over-year, core CPI, which excludes the volatile food and energy products, jumped by 5.5%, but that was just a tad less than the 5.6% increase in January.

Month-over-month, core CPI jumped by 0.5%, the third month in a row of acceleration, driven by raging inflation in services, and despite the drop in durable goods inflation. This is not going in the right direction:

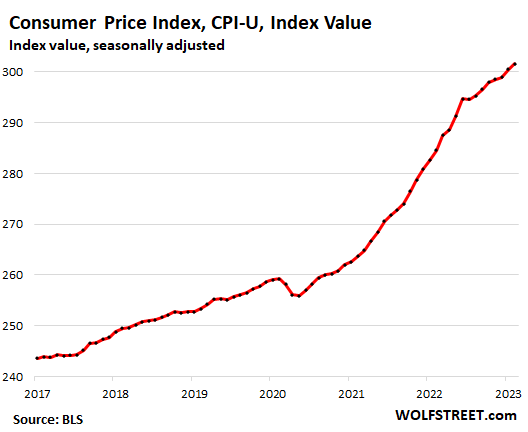

Overall CPI: +14.4% in two years:

In the overall CPI as index value representing price levels — not the percent change of the index value — we see that overall price levels have soared by 14.4% over the past two years:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I went to NoFrills yesterday and my can of beans skyrocketed from $1.19 to $1.49.

My weekly tub of NoName peanut butter went from $7.49 to $8.99 overnight.

And my apartment complex is getting a lot of crisis calls and police squads are at the driveway every week or so.

Tell me these politicians care about us.

I will tell you the politicians care about us. But, that is a lie.

I knew there was a reason I was pissed about my car insurance. I’m about ready to sell the car and walk everywhere. Hard to do where I live though.

so I went from 2015 F-150 to 2003 f-150 yesterday

called insurance – went down $64

from $30k to $1k vehicle and it went down $64

insurance – what a joke

get skates or bike

Heeeeey Faux Diddley….da dum de dum…..

Sorry, didn’t mean to embed my comment under yours. I’m in the wrong place. Lol

I’m just annoyed that many politicians and central bankers are trying to ignore food inflation which affects everyone in the working class as we need food to survive.

I’ll tell you one thing though: As much as Jeff Bezos gets roasted for being a billionaire, Amazon sells many food staples like sardines, rice, cooking oil, flour and even Whole Food brand nuts lower than No Frills.

I can’t believe it. Amazon is cheaper than NoFrills and in the future, more and more food items will be cheaper than NoFrills.

That’s what Canadians get when a few wealthy families own the grocery stores.

Only because the USPS heavily subsidizes Amazon’s sales. Imagine having an army of delivery personnel at your disposal, which will deliver just about every day to every residence in the country without really having to pay your fair share of these costs.

Of course, he’s a self-made billionaire, so he really did not get any public assistance. Nothing to see here…move along.

I never find Amazon to have the lowest price for anything. Like, Apple, people are just intoxicated by the brand.

Inflation will continue because it reduces the (usually indirect) liabilities and payroll expenses of the companies owned by the ultrarich. Yet, they can pass increases in costs down to consumers. The ownership of such US companies via trusts and chains of companies is also cleverly concentrated in a limited number of large, US families —some of whose members are less discreet about this and showed persons like myself.

A trust may be established, e.g., in a British tax haven, that then owns companies in other countries friendly to such corporations, like Ireland and in turn those own majority shares in US companies. Many, many trillions are held in such trusts per reports even a decade ago.

That is why a US wealth tax is the jugular vein of the ultrarich: even a minimal wealth tax would require them to disclose their VAST, total wealth and while foreign trusts established by US citizens are theoretically not subject to the proposed wealth tax, the ultra rich fear disclosure of the sums in those would ultimately be required and leak to media. Watch “Britain’s Second Empire: The Spider’s Web.” We are in a final battle: the ultra rich who moved US jobs to China to avoid having to pay US income taxes by using the US exclusion of such income from taxation and profit from quasi-slaves in subsidized CCP co-owned factories are fighting to hide their wealth.

I agree with Dolittle…it has been quite a while since Amazon had the best prices for anything.

Right around 2015 or 2016, they clearly shifted into “gotta make higher profits” mode and new fee regimes compelled third party sellers to hike prices.

My guess is that Amazon Prime hit critical mass with enough suckers (pay us an annual fee to have fastest access to poorly priced goods!! Don’t wait an extra day for delivery and 25% savings from a bazillion other online alternates!!)

And let’s not talk about how selling billions in “shelf space” advertising has turned the Amazon search/results into a mutant whorehouse of unusability.

Costco prices becoming more “normal” rather than a deal.

Mitt Romney is taking FaceTime calls for Zion bank! Cmon that’s the caring you mean, right? Right? (Padme stares)

Are you a rich donors or billionaires startup founders? If not, beat it.

that’s going thru a lot of peanut butter

Politicians love to find a scapegoat when things are bad. Dragging a successful businessman in front of the camera to answer for being successful isn’t a new tactic.

In terms of the actual numbers you’re quoting, Canada is basically in line with United States, and significantly better than every country in Europe. Hence, “most places.”

The fact is that Canada has ceased raising interest rates, and the US has not. The consequence is that the Canadian dollar has lost buying power since the last 0.25% rate increase, and I expect that will continue unless the current banking crisis in the US causes a shift in fed policy. So prices in Canada of anything that’s imported should rise.

On a recent rip to Florida, saw that menu prices and grocery store prices were pretty much in line with Canada – EXCEPT there should be a 38% difference due to exchange. Something seems whacky in the FX world again.

At almost 40% of a haircut it is going to take a bite out of snowbirds at some point.

Florida stores are *taxing* the snow birds. I live in AZ and our food prices are dramatically cheaper: Not only produce, but stuff like mayonnaise – $8.50 for the same brand and size I buy here for nearly $4 less (on sale, it’s $3.99 – normal $4.59). Same with salad dressings, deli lunch meat (Boar’s Head was $2 more a pound). Coke 12 packs are $8.79 in FL with no “bundle” savings. I paid $12 for 3-12 packs yesterday.

Went into a “House of Beers” to have a cerveza and “happy hour special” street tacos. The street tacos (2), which are about the size of a Oreo cookie, were $8 and the beers on “happy hour” were what the normal price is here at a more upscale establishment. The Blue Agave in Scottsdale serves tacos with the same fillings on special for $1.99 apiece and they’re so big you can barely eat two of them.

This wasn’t in any hot spot resort area of FL. This was near Ocala in the swamp lands.

Florida is a rip off.

A ripoff, sure, but certain Floridians would be all to happy for the state to become a rich enclave, where meatball policies rain from the sky to shower them in its juices.

The Villages but statewide. It’s not like Florida is on trend to gain more real estate in the next 100 years.

I was at the check out, looking at my grocery bill someone next to me also scanning their receipt looking for 3rrors.

I scan receipts for errors all the time before I walk out the door, even frugal places like ALDI & Wal-Mart. You’d be amazed at what a little persistent double-checking can unveil. I’ve had numerous occasions over the years where I was overcharged at the checkout line, and I have to correct the situation with management by showing the price on the shelf.

95% of the time the price discrepancy works in the store’s favor, BTW.

‘I scan receipts for errors all the time before I walk out the door’

Standard practice here also. Plenty of errors, and just about always in their favor. If I am not buying too much, I keep a running tally in my head and usually know immediately if they goofed. A game to play.

The Retail Council of Canada has an “Item Free Scanner Policy”.

When, ” the scanned price of a product at checkout is higher than the price displayed in the store or than advertised by the store, the lower price will be honoured “, up to a 10 dollar limit, for one item.

a six-pack of Ramen Noodles also went up to $1.25 at the Dollar Store!

That’s up to 21 cents per meal. I remember the college days.

It was also great for backpacking trip in the Sierras.

Walmart also recently hiked ramen prices significantly.

If you don’t think America could have a price driven famine, let me tell you about the half dozen other “could never happen in America” happenings that the last 20 years have brought us.

(I’m only semi-kidding about the famine. People would be amazed at 1) just how much “food” America produces that is really only food for much more costly chickens/pigs/cattle and 2) the incredible share of total ag production a pretty small handful of states have…making our food supply pretty damn sensitive to transport costs…it ain’t 1905 with diversified farms in every state. The more you look into it, the scarier it is)

Ramen noodles aren’t very nutritious (not saying they won’t fill you up or can’t be potentially tasty with the right ingredients).

If you really want to hunker down and go cheap without sacrificing nutrition, I’d go to Wal-Mart and grab 1 pound bags of dried chickpeas (garbanzos) or lentils (around $1.50/pound).

Put a 1/2 pound of dried chickpeas in a crockpot slow cooker with 6 cups of water and a pinch of salt. Leave on low heat for 8 hours and drain.

Then mix beans on stovetop with a cheap can of condensed tomato soup (70 cents) with a can of water. Simmer on low heat for 60-90 minutes (spinach and crackers optional).

Mmmm-mmm savory good and lots of basic nutrition.

If I was truly a cheapskate practicing the ultimate quantitative tightening, I wouldn’t have shared the tips above on here so as to keep demand for the dried beans lower, and thus the price I must pay for them over time.

Hey Wolf,

Due to family business have been a way a while.

Are you planning a Wolfstreet forums cookbook for frugal bears?

I should include a section on healthy eating. I think it’s needed, LOL.

Liver, people. Cheap and extremely nutritious.

In order to support the politicians and bankers difficult fight against inflation, we all need to be as frugal as possible.

Wolf – methinks if you did that, and ‘Muricans did embrace it, it COULD well and truly crash the ecomedy…

may we all find a better day.

These people seriously need to read the “How not to die” series of health books. It’s eye opening. Broccoli and beats can add some years and heal thy broken preservative filled bodies.

I’d love a cookbook section. Chickpeas are great. So is liver. Learn to ferment fruits and vegetables. If they won’t ferment (like hybrids and other assorted garbage) they’re not food. Traditional preservation methods enhance the nutritional value of foods. Modern preservation methods decrease it.

you have a story to tell. you should provide more info, and you don’t need to provide too much. i want to know more about crisis calls. all the detail. I hear sirens non stop where I live, and I wonder if the crew is just handling junkies and losers, and everyone else gets the bill.

A lot of people in Toronto are just losing it. Lots of attacks in public transit, a growing number of poor persons choosing medically-assisted death, and just a growing malaise in the population while Galen Weston Jr and Sobeys jack up grocery prices every week.

The rents keep going up, the wages are now becoming stagnant, and we have politicians who insist that binging in half a million newcomers a year will somehow make life better for the struggling Canadians who can’t afford rent and food.

Canada is a few cities to live in. When one city is expensive, the entire Canada eventually becomes expensive.

Yeah! The food wholesalers/producers haven’t raised prices at all! Why are grocery stores across the world raising prices?! It must be because of the greedy grocery store monopolies *in Canada.*

Sheesh…get some perspective.

If it were only happening in Canada, you might have an argument, but it’s not. And Canada’s food inflation is lower than most places. And by the way, I spend a fair amount of time in Canada for work, and while there, I go to Fortinos. It’s much better than many US chains.

Nonsense. Canada’s food inflation is higher than the USA, and Galen Weston was compelled to testify in Parliament to answer why grocery store profits remain very high even when inflation should have been eating away their expenses.

The cost of food in Canada rose by 10.4 percent on an annual basis in January of 2023, the highest since 1980, and picking up from the 10.1 percent increase in the previous period…On a monthly basis, prices grew by 1.7 percent. source: Statistics Canada

Food prices in the United States increased at a slower 9.5% from a year earlier in February 2023, decelerating from a 10.1% rise in January and a peak of 11.4% in last August. source: U.S. Bureau of Labor Statistics

I feel like I have to add one more comment because I really like Canada, and the anger you (and others I’ve seen) are expressing is justified, but misplaced.

Rents are going up in Canada because the government destroyed the multi-unit rental construction industry in the 80s by way of rent control. Case in point, zero – literally zero – multi-unit rental buildings were built in the GTA after about 1983 to 2001. The one building which was completed in 2001 had been planned as a condo, but converted to apartments after the dotcom bust and the implosion of Nortel. (It’s at the corner of Bloore and University, if you’re curious). No other rental buildings were built until the 2010s. Even then, it’s only in the last couple years that we’re seeing significant construction of purpose-built rental buildings in the GTA.

The story is similar in major metropolitan areas across the US. Rent control was instituted in the ’70s and ’80s; private construction of rental buildings came to a grinding halt. Eventually these municipalities eased up on their regulations, and slowly developer started to invest in multi-unit rentals.

But supply is way behind demand (in many cases, decades with zero new rental buildings), and so there’s upward pressure on rents. And obviously, inflation adds to the problem.

So be angry at governments for destroying rental markets and be angry at Central Banks for facilitating massive QE.

Z2B,

The tax reform act of 1986 (lower rates for fewer deductions) also really hurt apt supply in the US…you can see a chart and post 86 new apt supply was gut shot.

I’m surprised that no opportunistic pol hasn’t suggested bringing back the pre-86 RE deductions to further Jumpstart apt supply.

(In general, I think the G – at all levels – much prefers SFH to apts. SFH ties people down (harder to liquidate/switch/move) which makes it ripe pickings for property taxes. Renters…pushed too far…find it easier to pull up stakes and move to a different tax jurisdiction…Gs don’t like that, it spoils their central planning when the chess pieces start thinking for themselves.)

“Running amok is considered a rare culture-bound syndrome by current psychiatric classification systems, but there is evidence that it occurs frequently in modern industrialized societies.”

We covered this in my Cultural Anthropology class in college. It usually happens when a member of society hits rock bottom, and the effect is temporary. Some cultures recognize this as an expected occurence, and forgive the people after their rampage.

There are places in Canada with super cheap real estate. Saskatchewan and Manitoba. New Brunswick and parts of Nova Scotia. The cities are expensive it’s true but a lot of rural areas have lost population and there are plenty of empty houses.

“Wages are now becoming stagnant.”

Wow, sounds like 1980 all over again.

Inflation and high interest rates. Your line above sounds like the next 1980 piece of the puzzle “STAGFLATION”.

At Z2B your correlation between rent control and sky rocketing rents is shaky at best.

Because rents have skyrocketed as well throughout the US and their isn’t any type of rent control.

Not saying it’s not a factor but not the main driver.

The main driver to my current understanding was the federal and state level governments obsession with infinite growth post WW2.

Hence they downzoned and restricted multifamily zoning throughout N America cities in an effort to encourage only single family home construction and suburban sprawl.

Which is now biting us in the butt with entire metro areas that now have more tax expenditures than tax revenue per acre. And when the growth dance stops, those expenditures add up quickly.

Hence the country ‘needed’ an infrastructure bailout. Because the whole thing they made isn’t self sufficient any longer. This is just the beginning.

Didn’t Canadian grocers engaging in price fixing on bread, particularly Loblaw, who seems to be a key contributor to rising Canadian food prices in recent years and has been engaging in a disinformation campaign to distract from how they are exploiting inflation to price gouge?

I’m not all up on the latest but it doesn’t seem like everything is on the level in Canada.

Tips; “Peanut Butter” by law has to be 90% peanuts….beware “peanut spread”, etc. Can be anything. I use high fiber bread instead of beans and it’s much less messy. Same paper plate for a year now. I do have a fridge and drink no fat milk, stash bread on sale, 18 loaves when full up, and take a multi vitamin and 2 500mg fit C, CHEWED UP (not a chewable) while eating.

I’m almost 76 and doc says healthy as hell except for trashed back. Eat some thing once a day for 10 years now.

My 500 sq ft apt has it’s share of crisis calls (over 82 hotel style complex, 250 units, but management is pretty good at throwing out the alkies.

I’m lucky, and I had it a lot easier as a kid mainly because I could always find 40hrs, even if minimum and we could fix own transport. (except 80’s recession…essentially homeless off and on). Doubled up a lot and lived in a bread van 4 years.

Sorry about what my pig boomer cohort left you with. Many are here.

Politicians do whatever their corporate masters tell them to, they are mostly sleazy but not really your enemy. Excess wealth is. Vote to tax the bastids, income, but ESPECIALLY NET WEALTH.

Good luck!

Over 62, some 55 with bad disability, terminal cancer, etc. A few people are still working.

Don’t start hating the attempt at democratic government, which the rich have bought off.

IT IS YOUR ONLY HOPE FOR FAIRNESS. They want a dictatorship.

And they wonder why Gen Z (and some Mellenials… and even some Gen X) contemplate / vote for socialism. Hmmm. Rocket science.

That and public education in the US is what it is.

Finance and history should be priorities in education but instead we have kids running around financially clueless and romanticizing socialism and communism, interchangeably.

“Tell me these politicians care about us.”

LOL, -WHERE- did you -EVER- get that idea?

“The state – or, to make matters more concrete, the government – consists of a gang of men exactly like you and me. They have, taking one with another, no special talent for the business of government; they have only a talent for getting and holding office. Their principal device to that end is to search out groups who pant and pine for something they can’t get, and to promise to give it to them. Nine times out of ten that promise is worth nothing. The tenth time it is made good by looting ‘A’ to satisfy ‘B’. In other words, government is a broker in pillage, and every election is a sort of advanced auction on stolen goods.” – H.L. Mencken (1880 – 1956)

Cynical to a fault. While I believe that holds mostly true about who has sought higher office, there are exceptions, and “looting ‘A’ to satisfy ‘B'” is what’s known as taxing, the cost we all pay to live in a civil society, and budgeting, which is continually revised based on a shifting set of priorities.

Government picks winners and losers in the same way you and I pick who wins our business when we go out to eat and who loses by not having our business. It’s EXACTLY the same as a company choosing which third-party they sign with and which they don’t.

It’s vilifying a perfectly normal and everyday function of governance. The problem with critics who deploy that term is that they don’t want the competition or checks on their power to pick winners and losers.

An unhealthy portion our politicians are lawyers.

The founding fathers were all attorneys. Honestly to understand the Constitution (truly understand it) you prob should be an attorney. Self taught or expensive school educated.

I think you missed what was meant by the comment. Diversity 101 stuff about having differing interests and perspectives represented in the decision-making process.

Gasoline is pushing 5$ again in my burb, and while pre pandemic lower grocery prices started a comeback last year, they have mostly vanished. With the heavy rains produce prices are higher. I tend to underestimate inflation, I am a shrewd shopper, but I see the stickiness here. I get post cards in the mail, a house just like yours sold for high six figures. I want to buy your house. Then there’s traffic, which is brisk, always a sign people are on the hustle. Sure the politicians care, but they see things are cooking, and they won’t mess with that. I hate inflation but I don’t want one person to lose their job. And if Potus is a party to that he will lose my vote in 24.

I do want JPow to lose his job, together with his bureaucratic clique, and the politicians, and the CEO/managerial class. They all failed to plan and now cause layoffs, and a depression.

Wolf… when the numbers came out this morning Steve Liesman made a comment about the used cars price drop “not looking right”. I wasn’t clear what he was getting at but wondered if you see something squirrely in that data

Well, OK… I think it’s too early to say that.

A week ago, I posted an article on used vehicle WHOLESALE prices at auctions, which had jumped in January and February. And this is what I said about it:

“The Consumer Price Index for used vehicles (based on retail prices) usually picks up changes in wholesale prices within two to three months.”

This is what wholesale prices did:

So if I start seeing a price increase in the used vehicle CPI for March (to be released in mid-April), I’m good with it.

But if there is no price increase in the used vehicle CPI for March, then:

1. Either dealers are NOT ABLE to pass on their higher costs (but that should bring down wholesale prices in the future)

2. Or something is wrong in the data, either Manheim’s wholesale prices or the BLS’s CPI.

So if we still get this divergence for March — Manheim shows further price increases, BLS shows further price declines — it gets very interesting. At that point, I will tear out my hair and ask Cox Automotive (which owns Manheim) to see if they have any idea why this is.

https://wolfstreet.com/2023/03/07/used-vehicle-auction-prices-jump-for-third-month-after-last-years-plunge-more-trouble-brewing-for-core-cpi/

I think you got onto me a couple of weeks ago for making a comparison between CS Index & OER. Be that as it may, it’s great to see the CS Index falling while OER is still rising. When these two data points cross, we can say housing inflation may be accurate.

A house in my area sold on 4/30/21 for $612K. On 10/3/2022, a near identical house across the street sold for $830K or a 36% increase in about 18 months.

It’s great to see that the government bailout of SVB & Signature are continued signs that MMT is still alive & well. No haircuts for any depositors. As such, we can all expect housing to continue its unabated, long-term trend upwards since rent & mortgage forbearance are sure to return when housing plunges, 6 months from now, 2 years or whenever.

Wolf, there is a guy named the inflation guy, Michael Ashton, who pointed out on his blog today that the BLS recently changed the methodology of used car CPI calculation. Not sure if it means anything.

Kevin,

What the BLS did recently is it changed the weights which it does routinely. I discussed this nearly a month ago (Feb 21). In addition, in 2022 I believe, the BLS started including private sector data from JD Power in its vehicle pricing data, which made the new vehicle CPI slightly worse, which I discussed at the time. It constantly makes changes to improve the accuracy of the data, and it is incorporating private sector data.

https://wolfstreet.com/2023/02/21/how-the-cpi-weights-changed-and-moved-cpi-meet-the-surprises/

My article includes this kind of discussion and charts, and also chart for new and used vehicle weights:

The weight of “rent of shelter” – a stand-in for housing costs that roughly accounts for one-third of CPI – was increased in 2022. Because the CPI for “rent of shelter” spiked in 2022, the higher weight made the overall CPI worse in 2022. It was then again increased by a much larger amount in January 2023 for the current year.

The weight was increased from 32.05% in November 2021 to 32.42% in January 2022, and to 34.04% in January 2023.

In January 2023, with the CPI for rent of shelter a red-hot +0.8% month-to-month and +8.0% year-over-year, the higher weight made CPI even worse:

BENW,

What you said in your comment:

“Per Wolf’s chart, it’s stunning how OER undervalues homes. But, anyone with 1/2 a brain already knows this.”

What I replied to your comment:

“You got this backwards. OER represents RENTS. It doesn’t “undervalue” homes with regards to the CS line. It shows how ridiculously OVERVALUED homes (CS line) have become.”

There is a lot more awareness and anger that only money printing (inflation) makes these repeated “rescues” possible.

It will only get worse (the G never had any plan for its hopeless promises) and the anger will grow and become manifest.

The country is going to break down and then break apart.

And for what?

So a small number of people could bullshit an entire nation for a little more political power and/or a little more wealth (abetted by media watchdogs too stupid or corrupt to do their jobs, for decades).

BENW. I think you jumped to a wrong conclusion here. MMT may be alive for the 1%. But the little guys who bought over priced homes in recent years are almost surely going to be up the creek without a paddle.

Lets not forget, it wasn’t the government that bailed out SVB and the other banks. It was the Federal Reserve, which is basically a consortium of private banks. They are going to save one of their own. It is a select club, and we aren’t in it.

I keep expecting the next “big thing” to break will be either derivatives or the stonk market casino on Wall Street. But real estate will feel the pain at some point.

So keep the popcorn handy.

for Wolf:

Thanks once again for the great explanations for WE, in this case the ”financially challenged WE who cannot know much if anything about these complicated CHANGES to the CPI, etc., without some one making them clear, as you do SO well.

Gonna make sure to send the biannual benefit, just short of the $C-note so as not to initiate the mug ship cost,,, only due to already having just enough of the ”ORIGINAL” WS mugs to be somewhat smug,,,LOL

BTW,,, ORIGINAL MUGS ”for sale” with ALL proceeds to Wolfstreet.com,,, , and I pay the shipping…

I sorta think house sales are either investors trying to time the market. Or just out of touch people moving from a higher COL area and not caring about price. Because Muh Real Estate will always go up.

What region are you in?

“You got this backwards. OER represents RENTS. It doesn’t “undervalue” homes with regards to the CS line. It shows how ridiculously OVERVALUED homes (CS line) have become.”

I understand this very well. They don’t represent exactly the same thing, but they both describe, in general, the cost of shelter. And you put them together in the same graph for a reason. I assume you’re attempting to show how housing & rent are out of whack with the later still growing, in part, due to the reality of the rental market and how the BLS is raising the weight of rent.

Either way, I firmly believe that the Elizabeth Warren’s of the world will win the rent & forbearance debate once it rears its ugly head in the future.

Congress & the Fed are now fully engaged in asset bubble manipulation, egregiously picking winners and losers. Nowadays, they’re a lot fewer losers than 20, 30, 40 years ago.

Thanks, Wolf!

The FED has concocted and is presiding over the most diabolical raging speculative mania in history. What he hell they were doing in 2020 and 2021 defies logic.

They should be ramping up QT [Wolf here: upon request by Depth Charge below, I changed the original “QE” to “QT”; “QE” confused the heck out of everyone, especially those who’ve ever read a single comment by Depth Charge, LOL] and rate hikes, but realize that they’re going to have to blow a bunch of their rich buddies up to bring inflation down.

Don’t worry QE nd rate cuts are coming soon. Give it until summer.

Broke and working poor elderly, and poor Gen X, Gen Y and Gen Zers to FED: “We are struggling to afford food and can’t afford shelter now and either have to find a relative to live with or a tent on the street.”

FED: “Bahahahahaha!! We’re not even thinking about thinking about raising rates. Now shut up and stop annoying me!”

Reckless billionaire speculator scum playing fast and loose with everything, causing extreme bubbles and skyrocketing inflation: “OH MY GOD, SVB BLEW UP AND MY MONEY IS GONE BECAUSE I DIDN’T ABIDE BY THE FDIC LIMITS! THE WHOLE SYSTEM WILL COLLAPSE IF I DON’T GET MY MONEY BACK NOW!”

FED: “We had an emergency weekend meeting and have removed the FDIC limit and backstopped you with the US Treasury’s printing press. You will get every penny Monday. Anything else?”

Well Said.

Everyone needs too see a replay saw of the Cramer “We will do better in the Future” Speech.

What total BS.

Made me want to throw up.

What a Douche Bag.

Powell needs to be questionned by the common man, not WSJ reporters carefully selected not to ask the right questions.

Q: Are you and the Federal reserve bankers responsible for this inflation, due to your QE policies? If so, then why should you still have this job?

Q: Given the horrible track record of the Fed in predicting economic trends in general, why shouldnt we dismantle it?

Q: You keep talking about raising interest rates, yet the pace of QT has been much slower than the pace of QE. Why not step up the pace of QT?

Q: Central banks around the world have bought X Trillion dollars of assets out of the markets. Is this an attempt to bail out the asset values of the rich? (Follow up question). Wouldnt market participants take greater caution in speculative excess if central bankers refused to prop up their assets?

The kayfabe is becoming increasingly difficult to maintain due to mounting evidence. Much more and I half expect DC and other aggravated individuals to be storming the Federal Reserve — except the working class is exhausted, burnt out, and struggling to survive under the increasingly precarious and fragile system that American capitalists, drunk with power and hubris, have brought into existence.

It’ll break before it gets better. I’m already having to reevaluate Nice-To-Haves and Need-To-Haves and consider doing things I don’t want to do just to survive.

Corrupt to the core. Who are the humans who “oversaw” and “managed” that “bank”? And who did that bank do business with? Sniff around and you’ll begin to understand why they got bailed out.

Depth Charge, you rock!

> Reckless billionaire speculator scum playing fast and loose with everything, causing extreme bubbles and skyrocketing inflation: “OH MY GOD, SVB BLEW UP AND MY MONEY IS GONE BECAUSE I DIDN’T ABIDE BY THE FDIC LIMITS! THE WHOLE SYSTEM WILL COLLAPSE IF I DON’T GET MY MONEY BACK NOW!”

Weren’t a lot of the deposits used to pay the salaries of tech start-ups? The ones needing the schooling are the people running the bank recklessly and they lost their jobs I take it.

Other than that I’m with you that the central banks hugely overcompensated with ultra loose monetary policy, and moral hazard is out the wazoo, but they at least seem willing to tame the overshot inflation so far.

Bitcoin prices seem to agree with you. As do equity markets generally. It should appear that the recent bank stresses are “the first cockroach in the basement.” But risk asset prices are saying the opposite. Suggesting to me inflation is far from being contained. This is just whipsawing back and forth since 2020, and the regulators are patching holes to protect their juiced-in pals.

What the Fed needs to have in order to continue its hiking cycle is a calm market and stable banks. And so now markets are calming down and banks have been stabilized, after last week’s rout. Markets and worry about banks will be off the agenda by the time we get to the FOMC meeting next week. So the Fed can concentrate on the issue at hand, which is inflation.

Wolf, At some level I think that your comment is the core of the problem.

Everyone agrees that the Fed should not rock the boat further during times of market distress…and yet, isnt it important to communicate to markets that the Fed is NOT going to backstop every little dip in the markets?

Isnt the unwillingness of the Fed to enact policies that might rock the market exactly why we have such a problem with moral hazard?

It seems to me that putting crooks in jail and making certain rich people poor is the only way to refocus the economy on value creation instead of asset speculation.

Until the next surprise.

Gametv

I agree that these people need to go to jail and that would fix this problem but to be fair a bank run is not just a market dip.

If they let it run it’s course I’m sure there would have been multiple banks going under and then people panicking and that could collapse the system and cause real damage. The solution they have isn’t ideal but them continuing to raise rates is ideal.

After CPI today and more key data tomorrow the debate on Fed cuts or pause will be over and we can move in to the next big event. Dot plot!

This is worldwide first in U K then credit Suisse America . Never in 5,000 years was there interest free money ,I see a worldwide depression,with the usual answer WAR .By the way everyone is getting armed to the gills ,not good

I think you meant ramping up QT, DC. FEDs rich buddies (and “investors”) are salivating at the thought of QE.

The FED is trapped between a rock and a hard place with raging inflation, so there’s going to be a rate hike come next week. I, personally, am expecting a 50 bps.

DC

you mean QT I think

Thank you, it was supposed to read “QT.” Hopefully Wolf can fix it as QE is the last freaking thing we need.

Done. But it might be a little late, LOL.

The fed gave “their rich buddies” the hint. They should take the hint and gtfo of the market with their ill gotten gains from QE. Before QT destroys their arses like cruise ship sushi night.

Is there anything tracking how much of this is “real” inflation, and how much is just large companies essentially colluding with each other and profiteering, using high inflation as cover to boost their margins? I guess you have to just use some measure of corporate profitability for that?

The only other factor I see is wages. Folks are jumping jobs and demanding a lot in wages for what they are producing.

Random50,

“real” inflation = price increases.

It doesn’t matter why prices increase, it’s still real inflation.

All inflation has a mass-psychology aspect to it: people and businesses willing to pay those prices, which allows businesses to charge those prices. This is a key element in all inflation.

I think there’s an important distinction. Margin increases are inflation that is easily reversible with little consequence.

Passing on of costs feels more entrenched to me. The only way that gets reversed (unless costs fall) is by the seller putting their business in jeopardy.

I think you’re probably looking to compare the PPI to the CPI

https://www.bls.gov/ppi/#:~:text=The%20Producer%20Price%20Index%20(PPI,many%20products%20and%20some%20services.

There’s another important aspect of inflation which most Americans aren’t familiar with, but I’ve seen in my years dealing with hyperinflation in Latin America. Inflation causes consumers to move their purchases forward in expectation of higher prices in the future. Whatever you buy today will cost more tomorrow, so buy it now, even if you don’t need it right now.

I wouldn’t be surprised if this thinking is being applied to services as well. Fix your air conditioner, car, roof (fill in the blank) now before prices go up. Go on vacation now before airfare goes up even more, etc.

Some of the price increases are clearly not working. For instance, I have a good chuckle when I cruise down the potato chip aisle. Who would pay $6+ for a bag of Doritos that’s like 12 ounces of corn and chemicals? It appears not many, because every few weeks I see the price is something like “$3.99, must buy quantities of 4.” What does that tell you? They’re having trouble selling the chips. I don’t buy that garbage at any price, I’m just fascinated (disgusted) by the price gouging.

Soft drinks are the same!

$7+ for a 12 pack at normal prices. Even at WalMart.

At Kroger, if you wait, the same brand is four 12 packs for $11 on sale.

It’s still cheaper than alcohol. I buy sparkling water at Aldi’s.

Agreed there pricing themselves out of existence.Down to one soda a day ,just weak I guess .I only buy everything on sale

ThoughtSlime / IAmVadim did a great YouTube essay on food price gouging in Canada, particularly with Leblow. Food insecurity is going unchecked up there with plenty of disinformation and key jangling to distract.

Doritos and soft drinks seems like the wrong products to be marking up in the first place, poor people and stoners eat that stuff, both will be first affected by inflation.

They’re exactly the right things to be marking up, along with cigarettes and fast food. How much stronger would our economy be with a healthy population? They should tax soda and junk food and put the revenue towards universal health insurance.

”

Philos

Mar 15, 2023 at 9:14 am

They’re exactly the right things to be marking up, along with cigarettes and fast food. How much stronger would our economy be with a healthy population? They should tax soda and junk food and put the revenue towards universal health insurance.

”

I agree, I just meant from the stores perspective, they’re not raising the price to make people healthy right? If they mark up already expensive healthy foods they’re more likely to make the sale still IMO, for me I’ll wear my clothes twice as long and do fewer road trips etc.. and still buy my fruits and veggies at a markup, I’m not switching to Doritos and 7up even if the cut those by 90%.

I agree on the cigarettes and junk food getting marked up, but that requires action from the government, businesses will not do this valountarily, they like their Armani and Ferraris, I imagine in the US that would be a tall order with the freedoms and all, here in Canada where provinces have had Universal Health since before the great Dorito inflation crisis 😂 we’ve been raising prices on cigarettes quite steadily, not that it’s helped me quit one bit to be honest, I’m now fully addicted to nicotine lozenges

“They should tax soda and junk food and put the revenue towards universal health insurance.”

But then what would all the super productive people we’ve packed into the healthcare industry do without new customers? You’d have to have a pandemic every year or two to bail them out.

The MAX distance chart on Yahoo Finance for PEP (Doritos owner) is pretty disgusting. Just a straight ramp up. A company that sells addictive poison is worth $238 billion.

They go onsale99 cents ,stopped buying them .Getting older gotta watch the diet

Agree 100% with the outrageous chip prices. I was shocked and thought it was a price mis-print. We on rare occasion get a bag to munch on but not a common purchase. I checked the pricing at multiple stores to realize they must all be charging like it’s caviar. $5/bag for 8-12 ounce bag, no thank you.

Nah, DC. They are selling chips just fine. Soda too. They are getting sales from those who’ll pay $6 AND from those who clip coupons. It works for them both ways. And it’s cyclical. What’s not bought at $6 will clear out at $4 and it does clear out. It used to be 2 for $5 and then 2 for $6 and now it’s $3.99 but must buy 4. See what I mean?

Even if that’s happening, it’s still a macroeconomic problem if prices are going up even after you add all the different categories together. If there were just collusion on certain items but not too much money slushing around, consumers who are forced to pay those higher prices would need to cut back elsewhere, and you would see prices falling in those other areas.

Companies are able to raise prices for two reasons. One, people have the money to spend and 2) there isnt much competition on the supply side. I can only choose to use less electricity, I cant shop for a new provider.

I think services inflation is more entrenched because the switching costs are high or it is impossible to switch. (Not much competition or price transparency in telecomm, utilties, healthcare, etc). But some of the price increases are coming in areas with alot of options (like hotel rooms), so it really must be due to excessive demand.

There’s a lot of this going on in my industry. I’m a small player ordering almost the same raw materials as my global competitors, the only difference is that I’m buying 55-gallon drums, and they are buying entire rail cars at better discounts.

These competitors have had twice the percentage of price increases I’ve had since 2021, and they aren’t stopping. My last increase was Sept 2022; other than greed, I don’t see why I need an increase for 2023. We have seen some nice price cuts from a few key vendors in the last few months.

Your final chart

“overall price levels have soared by 14.4% over the past two years:”

If one assumes the Fed was in control of their 2% inflation program from the years 2017 to 2021, (as depicted on the chart) to extend that trajectory to the present, the CPI reading SHOULD BE in the low 270’s. (now over 300).

Thus, ANY inflation is unwarranted. 2% inflation does not reestablish the managed trend the Fed enjoyed from 2017 to 2021.

Prices must retreat, not just rise at a lesser rate.

But we never hear that from the Fed. We just get the 2% mantra.

If the Fed wants an average inflation rate of 2% per year, we should not look at a one year window but a time span from 2020 to present. IMO

OR, Let’s take a 5 year window starting in 2020 and go forward.

What would prices have to do to get to an average CPI increase of 2% over those 5 years (2020 to 2025)? Drop about 4%.

Shouldnt that be the goal of the Fed?

Inflation is only a problem in an economy that doesn’t grow in real output, or grows below the ‘Inflation target’. That has been the case since at least 2000, and it’s a good thing for our finite planet that the landfills are not growing exponentially.

Unfortunately, that is also incompatible with the religion of infinite growth and fractional reserve lending. Something will give, and until the infinite growth is abolished, the only option is Inflation.. out the wazoo 🥳

And the market rocketed up after this report. They know something we don’t know ?

Huge relief rally after the banking system didn’t collapse yesterday, LOL. What did you expect?

Futures were up well before CPI was released. Beaten-down bank stocks soared.

And thank god we had a rally: the last thing the Fed needs for its hiking cycle is a stock market panic triggered by a banking panic. Now both are settling down, and the Fed can do its job.

Credit Suisse under more pressure since largest shareholder confirms no more capital injection.

Workers are wages not keeping up. Hours worked are dropping.

Toss in a few failed banks & recession talk, the pivot crowd is happy.

Wolf – what is your expectation on next rate hike?

Regarding your question, I just read this on the previous comment thread:

https://wolfstreet.com/2023/03/13/free-money-toxic-money-first-republic-bank-and-western-alliance-bank-make-it-into-my-pantheon-of-imploded-stocks/#comment-504000

My job is not to have my own ideas about future rates but to understand and convey what the Fed is telling us in various ways what they might do.

Last time I wrote about it, the Fed was conveying a 25-basis-point hike, and that’s what I conveyed in my piece. I have heard nothing from them that indicates that there will not be a hike. A couple have said they might be open to a 50-basis-point hike, but that’s just a couple, and nonvoting members; so I ignored that and didn’t write about it because it wasn’t a factor.

At its upcoming meeting, the Fed will have a lot to say about future hikes: We’ll get a new dot plot (once a quarter). Right now, we’re living off the December dot plot. And if I see that Powell’s words get twisted again, you will also get from me another piece about “what Powell actually said.”

The Fed has been very concerned about this ongoing inflation in core services. It thinks (hopes) rent inflation will come down; so it’s looking at core-services without rent. And it’s huge.

I have you some of the numbers in my services table above, and I’ll show them again below, core service items without housing. Lots of 5%+, YOY:

Airline fares: 26.5%

Motor vehicle insurance: 14.5%

Motor vehicle maintenance & repair: 12.5%

Pet services, including veterinary: 10.5%

Food services (food away from home): 8.4%

Postage & delivery services: 7.7%

Hotels, motels, etc.: 6.7%

Recreation services, admission to movies, concerts, sports events: 6.3%

Other personal services (dry-cleaning, haircuts, legal services…): 5.6%

Water, sewer, trash collection services: 5.2%

Video and audio services, cable: 5.1%

The Fed Whisperer.

Wolf has a unique skill. Horses are much easier to understand than the Fed.

But you do an excellent job .My thanks

7.6% = rate hikes coming.

Nomura predicts QT over and a cut coming. Hope they aren’t trading bonds.

Nomura badly needs a pivot. I mean, they’re almost squealing like an abused pig at this point. If they don’t get a pivot, they’re getting rinsed.

I ll bet SVB was calling for a pivot too

Nomura is a $3 stock that probably won’t exist a year from now. In terms of analysis, look no further than Jim Cramer, he represents the Kabuki clown moron that can be found at any financial institution, credit rating agency or economic think think tank. Listening to any of these fools is no different than overhearing a drunk shill talking about dog race results.

I assume Nomura has a portfolio filled with crap that hasn’t kept pace with inflation and rising yields, just like all the other banks, holding companies, etc… And let’s ignore the valuation on their commercial property portfolios…

According to MSNBC and the current administration, this inflation is driven by supply-chain disruptions and the Russia-Ukraine War, not fiscal or monetary policy.

Are you surprised? Politics isn’t about taking responsibility but shifting blame and maintaining an apperance of strength.

for Wolf:

Thanks once again for the great explanations for WE, in this case the ”financially challenged WE who cannot know much if anything about these complicated CHANGES to the CPI, etc., without some one making them clear, as you do SO well.

Gonna make sure to send the biannual benefit, just short of the $C-note so as not to initiate the mug ship cost,,, only due to already having just enough of the ”ORIGINAL” WS mugs to be somewhat smug,,,LOL

BTW,,, ORIGINAL MUGS ”for sale” with ALL proceeds to Wolfstreet.com,,, , and I pay the shipping…

MSNBC is wrong. Inflation was going on way before that war.

I don’t have confidence inflation is going to be taken care of in a timely manner with attitudes like the one MSNBC has.

It would be informative to add a column showing percent weights, so people could see how important each item is within each category. The column would add to 100 percent. It must be available somewhere so that total (or Overall) for each category can be calculated.

Yes, thanks, done, for services. But it’s % of overall CPI, not % of services CPI. Services CPI = 59% of total CPI.

I also set it up on my spreadsheet to where services CPI = 100%, and all services are a % of total services CPI. But I’m looking at it, and I’m not sure how useful this is. I could add both columns, but that’s a lot of numbers. So I’m going to mull this over till next time.

FED not doing anywhere near enough to slow down housing prices. Prices remain very sticky high (unless you are in new build/high price&crime markets like SF, Seattle, Austin, Phoenix, Vegas, etc.). Inventory for existing homes is ridiculously low. Where are the MBS sales…wait for it…crickets chirping.

14.4% over 2 years ? I understand data lags by a couple months but really ? Anecdotally, I could prove over 20% easily. Heck, Dollar Tree went from $1 to $1.25 about a year ago, not counting product shrinkage. 2% annual inflation is a pipe dream.

It does not matter what we common people see when it comes to inflation

The government and fed see deflation and that is all matters

Everyone has a different inflation rate. If you own your own home, you have very little housing inflation, for example. That’s a third of the basket. If you don’t buy a used car or electronics, you don’t benefit from the yoy price declines, LOL

On the bls.gov website you can use the dollar calculator tool. Jan 2020 $1.00 = $1.17 today. That’s 17% inflation in 3 years from the pandemic. Probably north of 20% in a few months. And the Fed sat there and said real wages would go up because people had jobs. Doubt those salaries are up 20%, not even close. The American consumer has been had and I suspect by the end of the year we will see absolutely abysmal consumer spending numbers. Right into an election year during a divided congress. Whoever bought equities today better have a long horizon and balls of steel.

Disinflation bah. Deflation is called for. Return to trend. Won’t be at ZIRP.

Thanks for the great breakdown. After scanning the msm headlines this am, I knew that I had to wait for Wolf’s article.

There’s the web and dark web. There’s the market and the black market. There’s inflation and real rate of inflation – somethings we will never know.

Your inflation rate is different than my inflation rate, for sure. Everyone’s is. It depends on how you live, where you live, what you buy, whether you rent or own a home, etc.

KBE weekly log : Mar 22 2021 to July 19 2021 lows. Parallel from :

Mar 15 2021 high. KBE is the banking ETF.

How did the Federal Reserve become so insanely powerful with their Section 13 emergency powers? I was under the impression Congress curbed some of those powers after 2008.

If Biden’s proposed student debt forgiveness plan (estimated cost $400 billion) is blocked by the courts, as some legal analysts believe it will, it’d be because he lacks the authority to enact such far-reaching policy without explicit approval from Congress. But the Federal Reserve can unilaterally bail out or backstop anything in the economy for whatever reason? I thought Congress had put in some safeguards, but I guess I’m wrong.

Wolf,

THANKS for all the SUPERB work compiling all this data.

A major factor that needs to be included along with the gas price is Diesel, which was doubled, more or less, along with gasoline.

All the food and gas that is moved around is moved with diesel trucks.

Obviously not the pipeline segments.

The Demented One has publicly stated loud and clear that he intends to eliminate hydrocarbons, and all he has managed to do is ramp up the price of the products.

That’s not how the Consumer Price Index (CPI) works. The Producer Price Index tracks those fuel costs.

1. CPI tracks prices of items that CONSUMERS buy directly. Those retail prices have embedded in them all transportation costs, fuel costs, manufacturing costs, costs of materials, labor costs, etc. When you buy a TV at the store, it has all these costs, including fuel costs, already embedded in it. CPI tracks the price of that TV.

2. Prices of gasoline, natural gas, electricity, etc. in the CPI (you see them in the table for “energy” in the article) reflect the retail prices that consumer pay directly at the pump for gasoline, and prices that they pay directly every month to their utilities.

3. What truckers, railroads, airfreight companies, container shipping companies, etc. pay for fuel is NOT a consumer price. That is part of the producer price index. They pass these fuel costs on to the next entity, and ultimately, those fuel costs will be reflected in retail prices that consumers pay for their TVs, beer, shoes, or their cars.

Soybean crush plants will be making biodiesel and the government is subsidizing it with tax dollars. ADM & Marathon Oil are big players in this.

I like that bicycles have a category Wolf includes. Today’s ride was great. Eagles are migrating up the Mighty Miss now. Had a big golden above me, close by for a few hundred meters. It never moved its wings; rode the current. No price can be put on that.

Schwab weekly log : Mar 22 2021 to June 13 2022 lows. Parallel from :

Apr 5 2021 close.

H&R Block added a demand based surcharge to the fee schedule. Not much, only $9, but still an increase. Those offices now pay more for electricity, insurance, and rent. I can’t think of any business that is not exposed to those increases. Plus the environment is ripe for price increases meaning we all expect it. And so the businesses do it. Until we the People reduce spending, nothing changes. We blame the Govt for everything because they are easy targets. But the Govt does not mandate that I buy the most expensive pick up truck. So as long as we spend, we get what we deserve. Interesting times indeed.

Beardwag, this is why I just buy GICs in Canada here, 4.25% to 4.75% the rates I got over the last 9 months earlier ones 3.15% to 3.6% over the other 2 years. I am very fugal and live debt free, rent, 1 car and keep my total expenses below $30,000 a year. I am putting $2,000 a month after all my taxes, expenses which on a gross $60,000 a year salary here in Canada most say is impossible but I do it everyday. Inflation at 2% never existed all misleading.

Kind of cool to see Pow Pow failing…market to its own peril still undermining him like no tomorrow..

If he comes out hiking .25 or pause…all bets are off, market to the moon…since the market is soon high sniping those pivot panties and SVB gave them all the sails they need…

Inflation? What inflation? That was so 2022 kind of worry…

Could the next blow-up be banks that have large commercial real estate portfolios?

With work at home and the upcoming implosion of money-losing companies and ecommerce, commercial real estate is facing reduced demand and new/existing tenants are getting concessions, so maybe there will be many property owners that walk away from properties and leave the bank to sort it out.

According to an article online, commercial real estate loans rose 14% last year, which is the highest since 2006 (like how history repeats itself?). This is primarily because it is more difficult to get investor money for commercial real estate (maybe those investors were smart)?

A blow-up of commercial real estate might be even worse than SVB. Much worse. Real estate is an incredibly leveraged asset. If we do go into recession and companies pull back on hiring, we are in for a very troubled time.

And I forgot to add that borrowers that need to refinance loans at higher interest rates will walk away from some properties.

If CRE were going to blow up, covid (remote work, online shopping) would have done it already.

It takes a while, given the long leases in CRE. Too early to say it won’t happen.

CRE is blowing up just fine. Lots of defaults on office tower mortgages already. But CRE is very slow-moving. After a default, there are months of negotiations because lenders (banks, CMBS investors, insurance companies, etc.) don’t want to own an empty office tower that they might be able to sell at a 70% loss, if they’re lucky. They’re all trying to work out a deal so that they don’t end up with the office tower.

I can just imagine how CRE enterprises are hedging their exploding portfolios. How they anticipate hiding exponentially dynamic losses with everything going super nova — maybe long term treasures hedged against falling property value will help cash burn, as they ignore writing off impairments.

We’re a long way away from ugly!

Interesting how most of the US press appears to be celebrating lower inflation, while the bold headline in tomorrow’s FT says annual inflation increased to 6%

TTM CPI is likely to drop to around +4% by mid-year, due to likely one-time base effects from plunging oil prices between June-December 2022. But oil (WTI) prices have stayed remarkably stable in the $70-80/barrel range for the past 3 months, as recession fears are offset by reduced supply & China reopening.

The last two months of M/M core CPI growth were +0.62% (Jan) and +0.68% (Feb), an 8% annualized rate. Still too high.

The more I think about things, the more I come to my own personal conclusion that the people in charge are going to collapse the entire system due to corruption, greed and the recklessness that accompanies it.

Longstanding knowledge, tradition and sound financial practices have been jettisoned for new narratives that make zero sense to anyone with a modicum of common sense, and only serve the purpose of providing cover for, and justifying, the wealth extraction operation they are engaging in.

“Transitory” was the latest “big lie.” It is along the lines of “subprime is contained” – another whopper that aged as well as a glass of milk in the Arizona summer sun. It was cover so the FED could pump asset price inflation to dizzying heights that would make even the most greedy oligarch blush, so these people could enjoy riches they once only dreamed of. And here we are.

We have traitors running the country, in all capacities. From elected politicians of the Uniparty to unelected bureaucrats. The USA has been hijacked by the obscenely rich, and they are destroying everything. I don’t know how to stop them. If I did, I would.

So true and so sad.

Worst thing is it’s not even people its corporations.

Most of the people who run the corporations are only there for a few years and then recycled also.

IMO the only way we fix this country is to get money out of politics and lobbying.

The amount of money spent on us elections is despicable. Destroy the two party system, both sides are evil and only designed to divide us into fighting while we slave away our entire lives only to see all our “earnings”get siphoned into the mouths of the ultra rich while they use the money to rig the system even further into there favor.

This is getting worse and the day of reckoning will come eventually

We have the best gov money can buy. And, I took believe it is taking us to a very bad place.

Hehehe welcome to the club DC.

It’s clear how to stop them, but such posts get deleted here, of course. It’s the only measure they’re actually concerned about.

But then the question comes – who exactly do you stop? The advantages of a system of secret commanders are obvious. Any rebellion would be directed against the wrong people.

Why would people in charge collapse the system when this current system works for them.

There is no collapse coming. The only collapse if the collapse of living standards for common people.

I come from so called developing country, came here 25 years back. It is painful to see USA gradually turning into a 3rd world/developing country.

Kind of sad :-(

“It is painful to see USA gradually turning into a 3rd world/developing country.”

Couldn’t have said it better myself. At least the politicians in 3rd world, as corrupt as they are taking steps to help their citizenry. In western world, it’s exactly the oppose.

“There is no collapse coming”

I think collapse is coming. As you say lowered living standard, that’s a given. Dollar collapse against tangibles is another one. Break up of united states is another one.

In the US, it’s as if the workers don’t exist. They’re expendable ‘human capital’ on MSNBC. No talk on the news/media about the average man’s needs or plight. No one to represent the interests of labor. The country is run like a corporation, but failed as a nation. It’s Fascism [corporatism], and it will tear the Union apart. Sad!

I have come to the same conclusion. Collapse is the only answer and it will happen.

Is it 2 months, 2 years or 2 decades? That’s anybody’s guess. Even if there are few good people who want to fix the system, it’s like rearranging the decks in titanic.

They want to inflate away the debt, that’s the only way they can buy some time. American dream as you know has finished, but it will be a slow death. Enjoy!

2025. I have been saying that on ZeroHedge since mid 2018. I am patient. I think tax changes in 2025 built into the Tax Cuts and Jobs Act will trigger it, combined with the level of debt/leverage that will be in the system at that time. I don’t think the economy will be able to sustain the shock.

The kind of people screaming for a FED pivot are the same caliber who would throw a blissful young child over the railing just to catch a foul ball themselves, then disappear into the darkness with a smile on their face as others recoil at the horror. They would secretly deprive the sick of lifesaving care if it meant they could have just a little more lucre.

The pivot-mongers think nothing of hurting others to satiate their own narcissistic, selfish greed. It is not about what’s good for mankind, it’s all about them and their money. And we see them shouting every day.

The pivot-mongers have many names. They are not shy about it. They advertise their rapacious greed. It’s time for society to treat these people with the same disdain they have shown for everybody else the past 25+ years. These people are really disgusting.

Jesus dude, and here I thought I was posting too much. Maybe you should start a Substack: “Into the Depths… of Rage!”

For all the problems with China, they are eating our lunch when it comes to nation building and looking after their national interests. Then again, maybe that’s as much of a mirage as what some outsiders see when they look at the United States.

“or all the problems with China, they are eating our lunch when it comes to nation building and looking after their national interests.”

Oh ya. Few yrs back I was having a convo with a foreigner. He said that America has destroyed more bridges/roads/infrastructures in last 20 yrs than she has built. It may not be 100% correct, but he was kinda right. It really made me think about this country somewhat differently ever since. And look at the people in charge, and really there’s no hope.

Mother Nature has been hard at work this winter destroying the roads in Minneapolis & St. Paul. Potholes are the worst in many, many years. Budgets will get pushed when hot-melt patching begins in early April.

Speed limits are suggested to be lowered by 20 mph on a fair number of roads, and vehicles are being punished. Auto repair & inflation, eh?

China wii probably never fire a weapon,USA will disintegrate from within ,can start to see signs of disgruntled people.When they have nothing to lose watch out.

Keep posting Depth Charge. I enjoy reading your posts.

Same here.

I feel the same way about many things you post. Your anger is righteous. Too bad the universe doesn’t dish out justice accordingly.

You are describing general human behavior. I’ve seen the results of multiple surveys where people are asked, “if your pet and a stranger are drowning, which would you save?” Somewhere north of 85% say pet, and that floored me to learn. I am still rattled by that to this day.

“The kind of people screaming for a FED pivot are the same caliber who would throw a blissful young child over the railing just to catch a foul ball themselves, then disappear into the darkness with a smile on their face as others recoil at the horror.”

This is an unusually potent E-V-I-L missive by Depth Charge. Biting. Stylishly brusque. Carries its point well enough to where I feel terrible for liking it.

We now have the most clueless, ignorant, dishonest lowlife’s running the country than have ever existed in the last 100 years. Nothing good can ever happen with these people in charge. The only prudent thing to do is to batten down the hatches and hope that their incompetence does not take you and your family down with them.

We thought it was bad when it was a swamp. This is no swamp. It’s a sewer.

The Federal Govern ment especially. UNIparty controls everything, Rich or poor is all that will be left. Stay out of debt, live within your means and be happy and rich. Or poor.

“the most clueless, ignorant, dishonest lowlife’s running the country than have ever existed in the last 100 years.”

You sum it up well. The same applies in Canadian provincial capitals, Ottawa, and beyond. They make the politicians of the 20th century look like statesmen and stateswomen.

May I add,

100 years ago, 1923 the following lowlifes were in charge of the Weimer Republic:

Lowlife #1 – Ludendorff – soulless general

Lowlife #2 – Stinnes – plutocratic profiteer

Lowlife #3 – Dr Hevenstein – mad banker

Lowlife #4 – Power hungry demagogue (name withheld because of WS’s guidelines)

“These were the four grotesque figures stalking the German Stage representing the villains in the play”.

From: “When Money Dies” by Adam Furgusson

I’m beginning too believe that rate hikes alone won’t dent inflation.

Unless government spending declines, rate hikes will always lag

inflation. Banking, Construction, Health Care, Education, etc…, are all first in line when the money hose is turned on.

Well rate hike could lower inflation. But Powell is busy bailing out people at the first hiccup. So you have to ask what’s the point of rate hikes anyway?

15+ years of sugar diet, come on you are going to have to take some major pain.

“rate hikes alone won’t dent inflation”

This is true because most of the inflation is in necessities and non discretionary services which you CANNOT do without. ( i.e. High speed Internet, medical/auto insurance, water/sewer, property taxes etc)

Many of these Services are heavily regulated and are run by monopoly companies. They just pass on their higher interest rate costs and financing costs to the consumer.

The CPI index is showing 18% inflation in three years. With inflation running at 6-7%, it will be 25% in four short years.

If the Fed thought that result was unacceptable, they would be talking about reversing that inflation, not supporting continued inflation.

Thus, the unstated target is 4-8% inflation. The stated target is 2%. Don’t let them fool you.

As long as the government continues to run $1.5T to $2T deficits, it will be near impossible for inflation to reverse course.

Exactly!

I looked at all the services that I purchase on a regular basis. These services are necessities, not luxuries, and not even discretionary. They are only used to operate my household. They are all up 10 to 15% or more in the last 12 months. Some are up 25% or more like my appliance repair insurance contract that Wolf said is a rip-off (He’s probably correct). I’ve taken action to lower these costs, like cancelling my homeowner’s insurance and switching to another company. I’ve also decided to not repair things (like body damage on my car) and leave them broken or dented to cut costs. The bottom line is the services inflation is running much hotter than is being reported by the government.

I’ve suspected for awhile that the Fed wants to stabilize inflation around 4-5%.

They just can’t admit it, because doing so would cause interest rates to spike.

Thank you, I was looking for the latest edition of something “raging”. You did not disappoint.