Retail supply of used cars and trucks dropped for second month in a row. Dealers bid up prices to replenish their inventories.

By Wolf Richter for WOLF STREET.

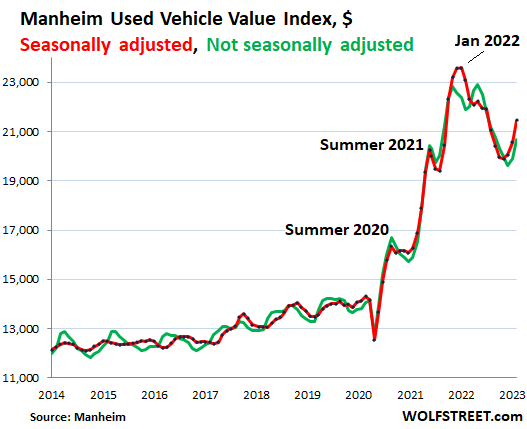

More trouble brewing beneath the surface for inflation. Used vehicle wholesale prices at auction jumped 4.3% in February from January, seasonally adjusted, the biggest month-to-month jump for any February since 2009, and the third month in a row of increases, with hefty price increases across all eight vehicle segments, according to Manheim, the largest auto auction house in the US and a unit of Cox Automotive. Not seasonally adjusted, wholesale prices jumped by 3.7%, to $20,652, second month in a row of increases.

Both metrics of wholesale prices are adjusted for changes in the mix and mileage. These auction prices show that dealers have to pay more to restock their inventory. And they’re going to try to pass on the increased costs to their retail customers.

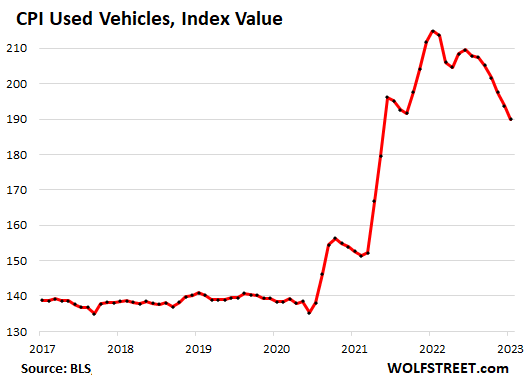

The Consumer Price Index for used vehicles (based retail prices) usually picks up changes in wholesale prices within two to three months:

Price increases month-over-month in February from January:

- Seasonally adjusted: +4.3% (after +2.5% in January; +0.8% in December).

- Not seasonally adjusted: +3.7%, (after +1.5% in January).

- All eight vehicle segments showed big price increases between 3.3% and 5.9%.

- Rental vehicles sold by fleets at auction: +5.0% (after +2.8% in January).

- Three-Year Old index: +2.4% (after +1.2% in January).

- These price increases “were not typical” for February, Manheim said.

The year-over-year price decline was reduced to -5.6%, not seasonally adjusted, from peak-decline of -13.1% in December. Rental risk units rose 0.5% year-over-year, after the big month-to-month jumps in January and February.

Sellers had more pricing power than typically seen this time of year: The average daily sales conversion rate jumped to 64.3% in February, from 59.4% in January, both of them well above normal for this time of the year.

Used vehicle retail sales fell 5% month-to-month and 9% year-over-year, on a same-store basis, according to initial estimates based on data from Dealertrack, a service of Cox Automotive. This came after the jump in sales in January (+16% month-over-month and +5% year-over-year) that had pushed supply of vehicles down.

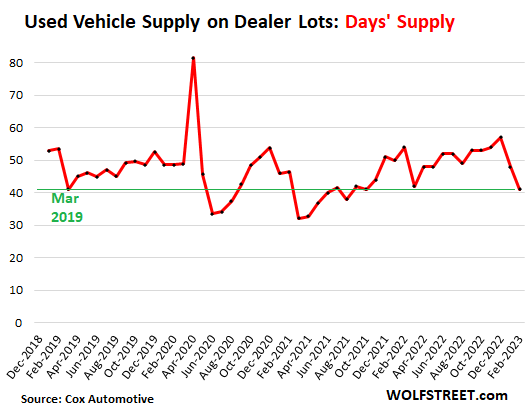

Wholesale supply fell to 24 days at the end of February, from 26 days in January, 32 days in December, and 29 days in February a year ago.

Retail supply at dealers fell for the second month in a row, to 41 days by the end of February, down from 48 days in January, and from 57 days in December, based on vAuto data, a service of Cox Automotive. This declining supply explains why dealers were more eager to buy at auctions – to replenish their inventories for spring selling season – and they bid up prices in the process.

These two consecutive months of dropping supply into the spring selling season (tax refund season) suggests that there will be more pricing pressures going forward:

When will wholesale price jumps show up in CPI?

The Consumer Price Index for used vehicles peaked in January 2022 and then fell, and by January 2023 had dropped by 11.6%. The CPI for February will be released next week. With the typical lag of about two to three months from wholesale prices, I expect the CPI for used vehicles to slow or halt the month-to-month decline at that point, and start showing the first increases in the CPI released in mid-April.

The used-vehicle CPI is a big component of “core” CPI (CPI without food and energy). And the big drop of used vehicle prices in 2022 helped put a lid on core CPI. But now we’re looking at the second month in a row this year when renewed inflation trouble is brewing beneath the surface – and we will see it bubble to the surface pretty soon.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Yep and Yes Sir. Inflation is here to stay for awhile.

Yes, high inflation is now persistent, entrenched and will most probably outlast both J. Pow and Fed.

Disinflation was a meaningless derivative created by wallstreet to propagate false narrative that inflation is gone.

Why meaningless? because, most price rises in goods and services will never go away and won’t slow down to a noticeable number for the sober eye.

Only price reductions that would happen is with fake bloodsucking investments like housing, and with speculations on dirt like cryptos and spacs, and with braindead meme stocks

Leo:

Please do NOT conflate fantasy garbage such as crypto(s) and spacs with ”dirt.”

Dirt is the basis of wealth now, and always has been since at least the last couple thousand years.

Those others are just ephemera based on NOTHING.

Other than that, thank you.

Amen, Wolf.

Disinflation was “transitory” indeed.

Thanks for the update.

But, but, but, Pavel said “Inflation is transitory”!

Disinflation is a derivative created by wallstreet to propagate its narrative. Most Americans lack the mathematical acumen to distinguish between disinflation and Deflation.

Disinflations doesn’t mean shit, even when inflation is at 2%.

Right now Disinflation is a Fugazi, it doesn’t exist, it’s not on elemental charts.

Disinflation = slowing your [moving] car down, but not coming to a full stop.

You’re sill moving forward.

Lol, this car ain’t slowing.

Have you ever really done this? “keep slowing your [moving] car down, but not coming to a full stop.”.

This is just telling everyone that disinflation isn’t even defined, and is probably infeasible.

…waiting to hear from DanRo on disinflating bicycle tires and it’s effect on their rolling resistance (…or, how much of the economic effect is that of a flat tire?…).

may we all find a better day.

I think Powell knew what he was doing in his February speech when he was cooing like a dove. He was drawing the markets into a trap.

He knew this reacceleration was coming and wanted to put some pain on the markers.

About his “February speech” — people who read my article about it were not surprised by Powell’s testimony. The pivot mongers just twist everything he says at the post-FOMC meetings into absurdities:

https://wolfstreet.com/2023/02/01/what-powell-actually-said/

Appreciate the hard work and data. On the ground in mid Atlantic seeing new and used car sales still holding steady in number and price. Inflation isn’t controlled and the wage spiral outside of tech is just spinning up. Every low to mid level health care worker in mid Atlantic wants to know why they weren’t being given raises over the past 2-3 years.

Is it possible that people jumped from buying houses into buying cars, since the higher interest rates on mortgages?

You can’t live in your car.

Or maybe you can?

In Vancouver, Canada for many its in their car or live on the street. Renting is not an option when the rent is 150 percent of your annual wages.

2-3 years? Hell, its been a solid 12 years here and just finally bagged a couple of sweet, sweet quarters an hour raise. Not spending it all at once; walking away a winner.

Health care workers will continue to get the shaft so long as we continue to accept the Florence Nightingale bleeding heart narrative. No other industry has the absolutely bananas personal and professional liability we do while we keep looking to our gaslighting employers for more crumbs of appreciation. We’re hired guns; our licenses and experience are our guns and horses. We need to organize better and demand better. Europe gets it, sort of. Not going so hot for them either though.

That all said, the dealership is back mailing me flyers begging me to trade in my compact SUV and take on a new hunk of junk with even higher monthly payment. Not a snowball’s chance in Hell, Mr. Dealer Man.

I just took my 95 Tacoma in for thousands of dollars of major maintenance. Of course the repair shop found another $1300 of “critical” works it needs. Fine. i would like to hope that at age 57 there will be no more vehicle purchases in my life. Just keep maintaining the ones I have and wait for the fleet of robo EV taxis to arrive. At that point I aim to die early, seems like a better solution than ever going thru another vehicle purchase.

Last year of a legendary rig. Kids love ’em. Tons of aftermarket stuff. Smog gas readout is damned good, too.

KEEP IT!

Also not all that hard to learn ALL electro/vac engine controls and fix tuning stuff yourself. Don’t know about automatic trans, but probably ok.

The chart is nutso. 1997 = 100, 2019 = 150, 2023 = 235 and climbing again. A lot of it has to do with residuals from higher priced new vehicles, which were in short supply for a couple years due to chips. Luckily, new vehicle inventories are building, albeit slowly. A return to the historical trend would be well received by people like me who plan on buying a used vehicle in the next 3-4 years.

Good luck. I tried to buy a new car yesterday. got up and left in disgust.

I’ve seen claims that banks appear to be getting hesitant to make auto loans to people with poor credit. If that is true then dealers whose customer base consists of that type of customer could end up in a world of hurt soon.

Is there any way to track how banks are approaching the auto loan market to see if there is trouble on the horizon?

Banks are hoping for a bailout, and they will get it.

Hello, I’ve seen data re: Ally bank which is a big player in the sub-prime auto loan market, which reflects increased auto loans 60 days or more in arrears.

Subprime and deep subprime combined are only about 17% of auto lending. Not all of subprime rated borrowers are the same. Some are near the category limit, others are in “deep subprime.”

Deep subprime is only about 2% of total auto lending. These are the riskiest customers, and the first to get cut. So if you cut lending to them by HALF, which would be a huge tightening, it only reduces total auto lending by 1%.

Conversely, about 82% of borrowers have between fairly decent and pristine credit. Some might have to pay a higher rate than others, but they’ll always get loans because the risks range from small to minuscule. And lenders are paid via interest to take those risks.

I figured happy motoring would end with fuel priced too high for people to afford. But I was wrong, it looks like what will bring happy motoring down is vehicle prices too high for most people to afford.

Today called local Frieghtliner to service motorhome diesel engine & generator. Customer service informed me their service prices increased in March. Extra $100 for engine service and $100 for generator service

Thanks for the work, Wolf.

I was going to ask for volume info (my favorite hobbyhorse in response to price spikes) but then I RTFA closely and saw the wholesale and retail volume data.

(Although…”days supply” is a bit of a wonky metric, combining supply and demand when maybe just reporting number of transactions might provide cleaner historical comparisons…)

It is hard to believe retail buyers are eagerly gobbling up inventory in the wake of a 33%-50% price spike (or that dealers are unquestioningly following them down that road as interest rate double…)

I’m curious how “interest rate sensitive” the used car business is. Do dealers borrow the capital to re-plenish their inventory? What percentage of retail consumers finance used vehicle purchases?

I think Wolf stated previously, that dealers make a good commission on arranging the consumer loans.

The thing about used cars is that you can step down the ladder. With new vehicles, once you get to around $18K, that’s about as low as you can go. But with used vehicles you can go below 10k, no problem. So if you cannot afford the two-year-old former rental sedan at 10%, maybe you can afford the six-year old trade-in.

People who just want a nicer car might hang on to what they have for a while longer. But others who really have to buy a car because their beater is getting close to the end, well, they have options at 10%. Many 10-year-old cars are still in amazingly good shape today.

SO, also for 20 year old vehicles that have been well cared for Wolf.

Traded in the ’19 for cash on the barrel when offered what I had paid in 2022-Jan,,,

Bought a couple 20 yo, in spite of beloved teasing I was getting ready to replace her with a couple of similarly ”aged”…

Very happy to have a couple vehicles WITHOUT ALL the ”stuff” that apparently, according to a friend in the biz, CANNOT be repaired,,, or at least NOT within many months and a site visit from a ”factory rep.”

And, to be thorough, friend in biz reported he had repaired all the ”physical” damage in a couple days, but owner had to wait many moons to have the factory rep come and repair the digital nonsense…

His very well informed testimony killed OUR last attempt to buy…

Still wanting/hoping to buy a NEW vehicle that ”pencils out” for cost effective, including very likely repairs…

”Hope is NOT a strategy” but continues for many if not ALL of WE PEONs…

This is a really good question! I have no insight to offer, alas, only opinion…

I would expect used cars to be a LOT less sensitive to rates than housing. In the southeast at least, a car is a necessity. I just don’t think there’s a lot of elasticity in demand for used cars. Higher rates, along with higher prices, would presumably push people down the price ladder to older/lower-end and lower-cost models if we accept that demand isn’t particularly elastic.

New cars, though? No idea.

A brief Googling turned up a bunch of hand-waving articles about dealer pessimism in an age of >0% interest rates, but no actual research.

I am not sure about used car financings, but I’ve seen stats stating that 85% of new car purchases are financed (always at max possible? Idk.)

That would go a long way to explaining new car price spikes…you can’t get blood from a stone…but you can give it a doomed loan, which you immediately sell into the yield starved secondary loan mkt.

And so we end up with a pathological doom spiral,

1) Attempted price spikes freely (or with regret) attempted by manufacturers,

2) Ratified by horribly underwritten loans, powered by the meth of ZIRP,

3) which loans are immediately sold into secondary markets starved of yield by ZIRP,

4) rinse, repeat, collapse…once ZIRP stops even a little, or horrible loans dominate the ecosystem.

The exact same dynamic applies to every financed product (housing, autos, etc).

Tight labor market & aggressive rate raising continues to surprise. Curious to see what the next report says.

Seems like no one has a good handle on what we’re going through during this Weirdest Economy Ever — cept Wolf, of course!

In the Bay Area of California, currently the Toyota dealer in Walnut Creek says that there is a 3-year waiting list for any new RAV4 hybrids !!

Got one in witchita is 4-6 week wait ,bought over internet pretty easy

Not a hybrid sorry

I know a broker in the NE who gets them in weekly. Your dealer doesn’t have allocation.

“The average daily sales conversion rate jumped to 64.3% in February, from 59.4% in January, both of them well above normal for this time of the year.” Wolf, does this mean that percentage of sold vehicles, used gently in this case, that were sold at the listing or asking prices of the sellers/dealers? More pricing power for sellers.

Now to see how Frederick County VA values my two ancient road warriors for the purpose of taxing the rubber off of them. My Subi is over 20 years old and my Ford Ranger is 13.5 years old, but they never seem to escape VA Personal Property Tax unless the doors fall off, and then they tax the door regardless of where it lands.

It means that of the total number of vehicles run through an auction, 64.3% were sold, and the remainder were not sold, for example because bids didn’t reach the reserve. They then remained in wholesale inventory until they were run through another auction and sold. These auctions happen all the time everywhere, including online.

I would like to understand the car payment per month scale per annual salary. Generally speaking, anyone who has a $1,000 car payment per month is nuts on a depreciating asset, excluding collector cars that appreciate. $1,000 is rent month per month.

A friend of mine bought a car (Ford Bronco) with an 800 score and was paying cash. They still asked if they could quote him a loan. He said sure but I’m not financing. The quoted him 7% interest rate over 7 years with a 800 credit score.

Now, I’m waiting for the car loan bust to buy a vehicle.

What’s to say that when the dealer lots are ‘replenished’ … that they’ll mostly just sit there, collecting dust? Aren’t current auto loans (for many) now in arrears, and if so, won’t that have some bearing on whether inventory moves. The economics for the lumping folk no look so good going forward.

Auto loans are still in good shape. Delinquencies have come up from the stimulus-money record-lows to the Good Times lows (through Q4):

Nice piece Wolf! I always assumed the best time of year historically to buy a car was January and February? Is that what the seasonal adjustments show?

Sold my Porsche in September 2022, not too keen to buy another unless I can get in after the market normalizes. Btw this dramatically increases the odds of a hot CPI Tuesday, the market is starting to figure it out now.

A large percentage of used cars are purchased with tax refund money.

Because of this, the first three to four months of the year are typically the worst time to buy. That is in a typical year, but we know that there hasn’t been one of those for a while.

I, too, sold my Porsche in 2022. I don’t think the Porsche market is ever going to “normalize”. All their factories are in energy-strangled Germany (except for the Cayman assembly plant in Finland), and both used and new models are selling at a huge premium (or, at least the sports cars).

They seem to be producing less to charge more to the rest of those who do buy. Will work for now but I’d imagine someone will come and grab their market share, whether it’s Tesla or the other luxury car makers.

…worked for HD in the ’80s-’90s…notso well now (for a myriad of reasons).

may we all find a better day.

San Diego/LA metro showing 783 used Tesla Model 3’s for sale, it’s astounding to me. Hard to believe prices will not crater for this make/model but in this new mad world who knows anymore.

Prices for used Lexus GX SUV’s still give me a nosebleed.

I’m going to continue to drive what I’ve got until we get some serious devaluation in the used market or the wheels fall off my current rig.

In terms of new vehicles, Tesla’s Model Y was the #1 bestselling model in California in 2022 (with 87,257 registrations), and the Model 3 was #2 (with 78,934 registrations), both beating by a wide margin the Toyotas that were #3 and #4.

In other words, the Model 3 is a huge-volume vehicle in the San Diego and LA area, a gigantic market. 25% of the entire population of California lives in LA County alone. So that inventory number doesn’t seem high to me, given the huge market and the large volume of sales of the Model 3.

https://wolfstreet.com/2023/02/10/ev-sales-spiked-in-california-share-hit-17-in-2022-ice-vehicle-sales-plunged-first-uptick-in-electricity-sales-after-13-years-of-declines/

But prices are coming down on Teslas because Tesla has been cutting new vehicle prices, which tends to push down used prices.

Tesla has three dealerships in the Twin Cities. A couple weeks ago, they announced that two more are on the way; Golden Valley & Lake Elmo.

Five dealerships for a metro area with around 2.5 million people. Of course, their dealerships are not spread out in the way Ford and Chevy are for people outside of cities.

I found a new chart. It is “Domestic Auto Inventories AUINSA” published as part of the Federal Reserve Economic Data series. It shows an inventory of autos assembled in the U.S., Mexico and Canada. The reports is of autos numbered in thousands, instead of months supply. Inventory was high in 2017, declined until Feb 2022, and has risen since then.

David Hall,

You don’t know what you’re talking about. The data you cited is sedans only! It does not include SUVs and pickups.

Sedan sales in the US have collapsed, as I noted here for many years. This inventory measure you cited (107,900 sedans in January, February not yet available), goes with the sales measure of 188,100 sedans sold in January, all of them assembled in U.S., Mexico and Canada. Out of 1.04 million total vehicles sold in January (and 1.14 million in February).

Googling around the internet and not knowing what it means and not looking up what it actually means is exactly why chatbots come up with all their stupid crap.

So learn something. This data is released by the BEA, from where the St. Louis Fed picks it up, from where you got it. Go to https://www.bea.gov/data/gdp/gross-domestic-product scroll down to “Supplementary information & Additional Data,” click on “Motor Vehicles,” which downloads the Excel spreadsheet, then go to Table 6 (tab) for total sales, and to Table 10 (tab) for the inventory and sales of sedans.

Ford is getting desperate to avoid repossessing cars financed under it’s subprime partners. Now they are sending threatening messages to the screens on the dashboards of Ford owners who are behind on their payments. If that doesn’t work then then they send files to the onboard computers that make grinding noises. I’s getting ugly out there

People buying more car than they can afford. CPI going through the roof. Debt at extreme levels. $1.5 to $2.5T recurring deficits for the foreseeable future. Mortgage rates jump from 3% to 7%.

Where’s the carnage?

It reminds of the last bust, when government and businesses hid the bad news for a long time. All heck finally broke loose when Lehman announced it was having problems.

We could possibly adopt the contrarian view that there is no carnage, that everyone will continue to do very well for decades into the future with the naysayers only propagating doom-and-gloom narratives to generate popcorn eating excitement for the bored arena spectators?

Zero Sum Game – I think that view will be proven wrong. There are dead bodies, they just haven’t floated to the surface yet. Coming out of Covid, many businesses were understaffed, particularly for skilled workers. Businesses are trying to keep people busy and on the payroll awaiting better times, at some point that burden has to be cut, but don’t forget in many industries the market is global and in general USA is a high cost producer overall. The Fed kept rates near Zero for way too long and they never should have been there in the first place. Did anyone ever believe they would see zero interest rates and negative crude oil futures pricing? The system is unstable. Businesses can skinny the margins for a while, but not with huge debt levels and increasing interest rates. Much of the rise in rates has yet to translate into markedly higher debt serve and problems that follow. Grab some popcorn.

Well-said.

QQQBall:

I was being playfully sarcastic in my post. I agree this will be a long process of gradual bloodletting to unwind the excesses of the past 15 years or so.

”Businesses can skinny the margins for a while, but not with huge debt levels”

Does this mean the financial news are lying when they propagate that the ”companies are flush in cash, with many with cash off-shore” and ”companies will resort to stock buybacks to better their quarterly results” scenario on the channels ?

My local gas station and mini mart stuck numerous lawn signs in the ground today: “We accept SNAP/EBT” (food assistance cards in WA state). Anything to get anyone in the door to buy food at a 3000% markup. Times must be getting a little tougher. Keep at it JP.

We’re on 3 years of reduced new vehicle output.

People are holding onto cars longer.

Inflation and interest rates have killed leases.

The combination of these three variables (especially the 3 year lease turn in rotation) will keep the supply of used vehicles tight this year, and likely over the next several years.

As with anything in this market: it’s anyone’s guess as to what will be the straw to break the market, but clearly the consumer is more resilient (foolish?) than most pundits have expected.

Prediction:

Continued elevated vehicle prices will push up the average age of vehicles on the road, as folks fix their existing ride for longer before replacing.

The used vehicle market will continue to grow, as cars stay on the road longer, and purchasing new becomes a luxury reserved for the wealthy.

Cars run longer nowadays too. My 10 year old daily driver only looks like its been run 3-4 years. I make sure its gets all the scheduled maintenance but I drive it alot too, up to 114K miles and I bought it second hand with just a year of wear on it.

And I cant be the only one that wants the CPI to moonshot. Lets get rates up to 7%, my tbills will be golden and all the fake tech unicorns will get turned to ash.

Heron,

I’m with you 100%

Currently driving a 2011 with 150k miles. I change my oil every 5k and do scheduled maintenance religiously.

I’ve got a Tbond ladder with an average YTM of ~4.75% right now, but would also love to see yields keep going up. I’ve been gradually unwinding my risk and moving into short term treasuries.

I’m with MM – I see vehicle age increasing and keep rising. I wonder if there is a Shop Index ? showing $ in vehicle maintenance for years today & going back to say 1990….. Be interesting to see if it’s been picking up as the chip shortage arrived, and staying up with prices in new & used cars…

The cost of replacement parts for older cars has certainly been surfing the wave of inflation!

In 2020 the W4 was revised, reducing the chances of overpaying income taxes and reducing amount of tax refund someone gets. I wonder how that affects down payment ability vs. higher finance amount/more interest paid over the loan. Certainly seems like it would sweeten the deal to buy cheaper used over an expensive new car. Of course not everyone has that kind of employment arrangement but I can imagine (in absence of #’s) it would make a dent.

Wolf, how much of this is limited supply and perfect information that the dealerships have on the buyers and their competition? Everything is quantified and measured.

The Fed started raising rates in May 2004 and finished in July 2006 – over two years later.

Unemployment hit its trough in May 2007, 10 months after rates hikes stopped, 36 months after rates started increasing

The stock market peaked in October 2007 – 15 months after rates stopped rising, 41 months after they started increasing.

Recession started (officially) in December 2007, 43 months after the Fed interest rate increase cycle started.

This time around, we are 12 months from when the Fed started raising rates, they haven’t stopped yet, and people are surprised the economy hasn’t collapsed yet. I think internet-brain just makes people impatient.

Agreed it’s crazy how long the process is.

However this time might be quicker with the large 75bps increases in the Fed rate.

Or maybe it’ll be just as long since all the extra savings and tight labor market keeping people employed are stringing this thing along 🤷

Interesting day today with Powell and the deepening yield inversion. If the long end starts to catch up to the short end stocks are dead🤞

“More Trouble Brewing for “Core” CPI”

The economy is grotesquely overheated, STILL. Remember when I was chastising Powell for failing at his job and stepping down the rate hikes quickly to 50 then 25 basis points, and I was accused of “wanting to burn it all down” simply because I felt that they were prematurely slowing the hikes? Yeah, and here were are. Now he’s muttering about a possible 50 basis point hike again in light of his “disinflation” which appears to have proven “transitory” itself.

If the stupid mothertrucker would have gone 75 basis points every time, we would not be in this situation. You’ve got to slam the brakes on. He keeps erring on the side of entrenching. Jerome Powell and his buddies, including all of CONgress, succeeded in f***ing everything up in the country. They destroyed pricing in a matter of months with their horrific knee-jerk reactions and grotesque monetary largesse.

I think laying this all at his feet is ridiculous. He has an increasingly dovish board vis-à-vis the Biden admin. He’s beset on all sides by wall street wanting punch and threats from the executive branch.

I think his feb speech was a trap for markets. He knows what’s up. Now they doves have Kashkari on tour as a mouthpiece saying higher for longer.

I think we are in for an exciting 2023. It’s like professional wrestling but you know…. Peoples lives at stake.

I went shopping the other day. I buy the same 15 items every trip so I can track the cost inflation pretty accurately. No gimmicks. Same packaging etc. The basic staple items which are necessities such as butter, cranberry juice, bottled water, half & half etc have gone up 20 to 25% in the last 3 months. We are now entering inflation rates never seen before in this country.

Swamp Creature: I concur with your observations and I don’t think it has been discussed enough where even the most generous gov’t inflation figures are still seriously lowballing actual realities on the ground.

AGREE SC,,, except for your last sentence:

WE, in this case apparently the older pre boomer WE have seen every bit of THIS crash ( s0 far ) over and over for the last 7 or 8 decades…

Please continue to share your boots on the ground insights for the situation locally, but try to become more aware of the vast and continuing delta b/w the various and sundry:

LOCATION LOCATION LOCATION (S)

Thank you,

Depth

I’d of thought you’d be happy with what he said and the reaction it got?

I agree Powell is too slow to react but at least they know how to panic

DC, watch your language or you may get a job offer from Hollywood to do a voice over for a PG13 movie. Totally agree with your observation that there is now the Powell Reverse Pivot of accelerating QT, not pausing or re-instituting QE of inflationary times. Somewhat encouraged by all of the outrage at the Fed on these pages for being partners in the greatest excess liquidity tsunami in the history of the world, the Federal Government being the other offending party.

Maybe the textbooks in academia are not being as kind as previously about the original Fed Put a la Greenspan in 1987 on Black Monday and after. Of course, we are headed into the political silly season before you know it, where the current players must show increasing concern for the wants and needs of the little guy so that they can get re-elected. After helping to enrich the One Percenters since 2009 and pushing the Wealth Gap to new highs, now the Fed pivots to lament the person on the street not able to make ends meet in this 1970’s style inflation. This throws a spot of light on the rather politicized Federal Reserve that needs a new charter and mission.

Americans are about to get very mad as they wait in food lines, etc. with the cessation of Pandemic Stimuli. Change often occurs in tumultuous times.

Looks like I got lucky that my old car’s transmission decided to die in January instead of now. (Thankfully I now live somewhere that uses less salt than where I used to, so my “new” used car should last a bit better.)

As another indication of inflation, my company just announced fairly sizable retention bonuses for a good chunk of people, to be paid starting this summer. This is in top of the normal annual raise, which is still TBD (people just about rioted when it was ~4% last year so given how many people we’ve been hemorrhaging they’d be stupid not to crank it up a bit.)

The under $12k market for used vehicles is getting crowded as people get pushed down the affordability ladder. I just paid 10% over market for what should have been a $10 – 11k car otherwise inventory would have been slim to none if I had kept waiting.

No one wants to buy expensive new cars with five to ten thousand dollars worth of new safety features that need to be repaired. Get some bird poop or snow on those cameras and see how well the car auto brakes. Subaru is equipping many of their new cars with cameras inside the cabin that follow your eyes to tell you when your eyes veer from the road (I’m sure that won’t be used against you in an accident!) Yeah, consumers really pushed for that one!

Sensors need to be calibrated and I find it odd there are no scheduled calibration procedures in the manuals. So the systems just outright break and need to be repaired?

I will buy used for the time being because there’s too much quality being subtracted from vehicles in the last five years. Car companies need to spend less on connected infotainment systems and sensors and more on quality.

The greenest thing you can do is not buy a new car.

New car = government surveillance vehicle

We ordered a stuffed Platinum F150 3.5 EB hybrid in early February, expecting it to take 3-4 months.

Nope. It’s scheduled to build next week. This is a corp truck we are trading for a cash difference.