Step 1 of QT is operating at full speed. Step 2 of QT is just starting.

By Wolf Richter for WOLF STREET.

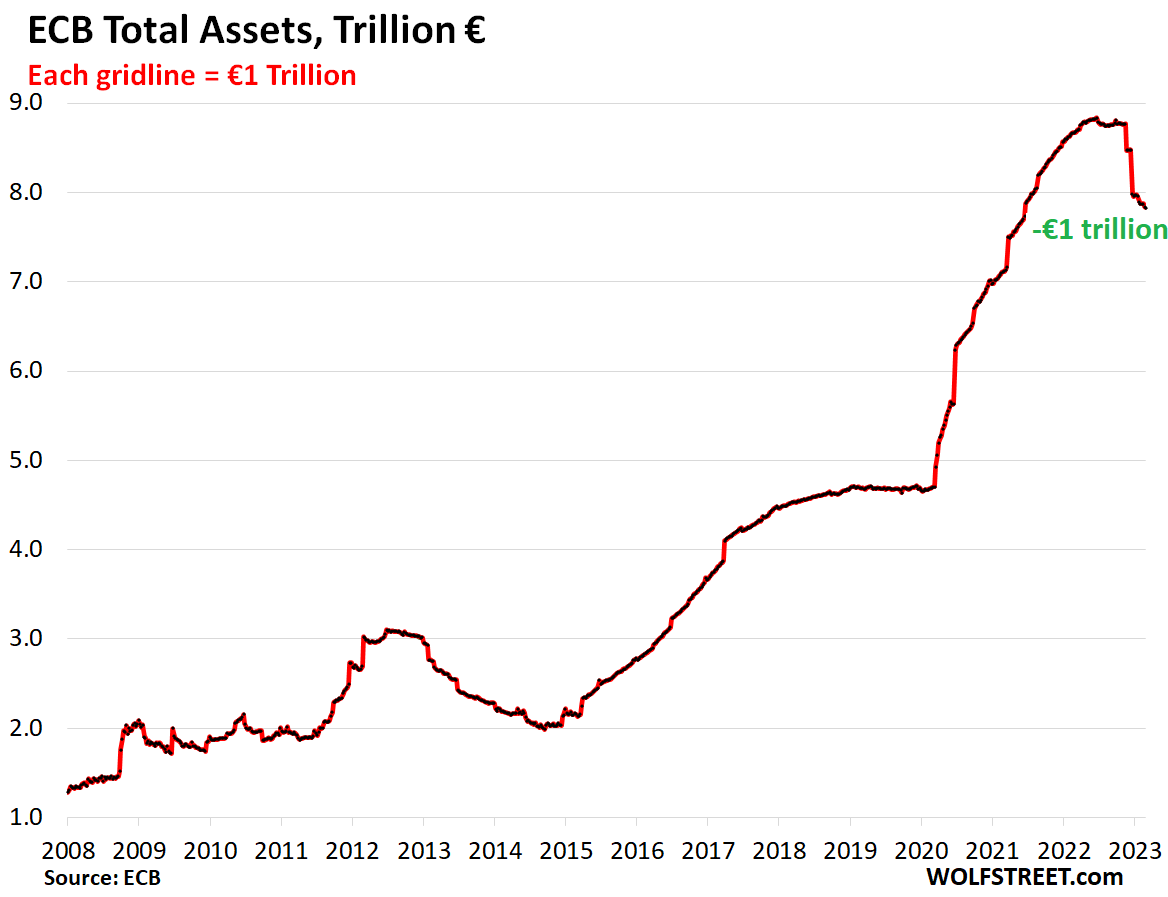

Total assets on the ECB’s balance sheet, released today, plunged by €1.005 trillion from the peak in June 2022, to €7.83 trillion, the lowest level since June 2021:

The ECB had two major types of QE: It handed very large chunks of cash to banks via free-money loans, and it handed cash to the bond market by purchasing government and corporate bonds and asset-backed securities.

The ECB announced Step 1 of QT at its October meeting: It made the loan terms less attractive, thereby causing banks to pay them back, which removed this liquidity from various markets via the banks.

The ECB announced Step 2 of QT at its December meeting: reducing its bond holdings by letting them mature without replacement, limited by a cap.

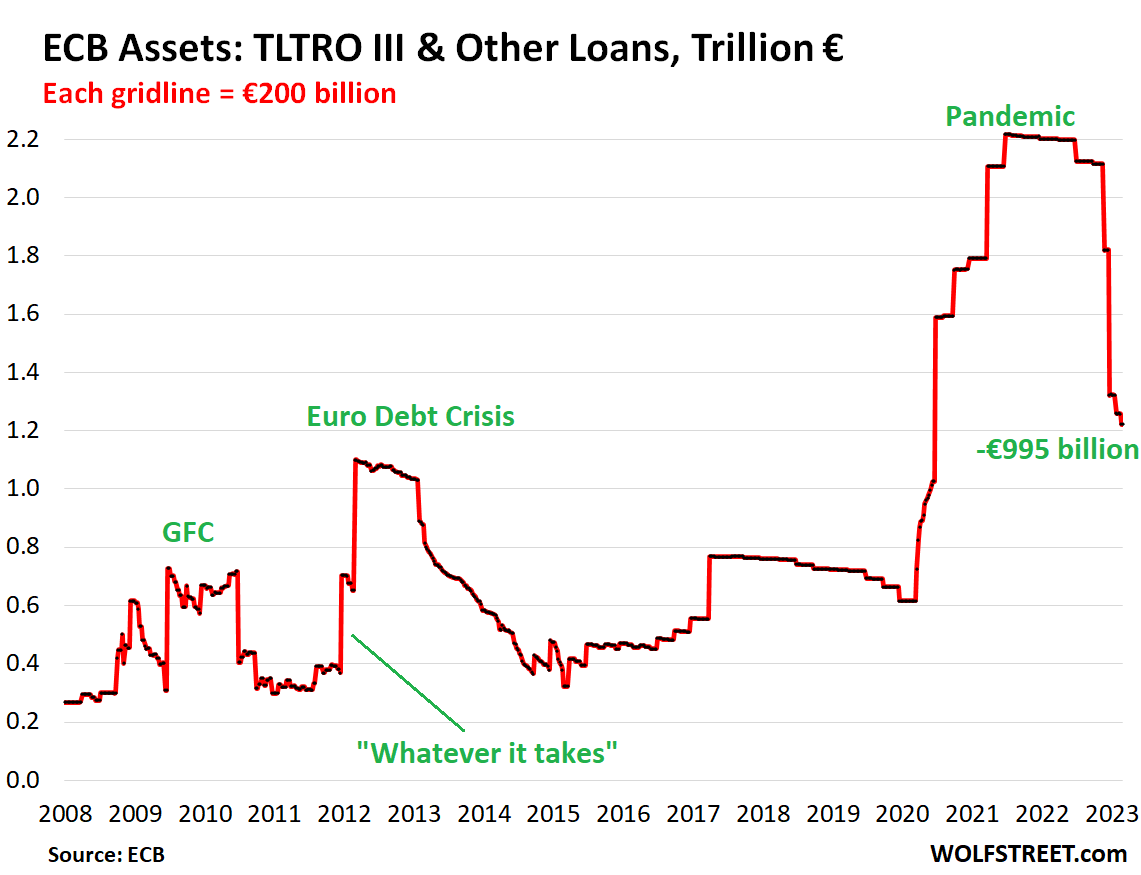

So far, the reduction of its balance sheet has been mostly through Step 1 of QT, the reductions in loans.

The loan QT: liquidity rug-pull.

As part of the massive QE operations during the pandemic, the ECB lent cash to the banks via what it calls the Targeted Longer-Term Refinancing Operations (TLTRO III) with complex incentives that were so favorable that banks took the money and plowed it into whatever. From the beginning of the pandemic through July 2021, the ECB handed out €1.6 trillion of TLTRO III loans.

This came on top of the remaining loans from prior programs (LTRO) of €620 billion, bringing the total loan balance to €2.22 trillion at the peak in June 2021.

The loans have dates at which they can be paid back. The first payback date was in July 2022, when €74 billion in loans were paid back; the second was in November, when €296 billion were paid back; the third was in December, when €498 billion were paid back. At the January and February windows, smaller amounts were paid back.

The total balance of TLTRO Loans has now plunged by €995 billion from the peak in June, to €1.22 trillion today.

The ECB has always handled QE via loans, including during the “whatever it takes” moment in 2012:

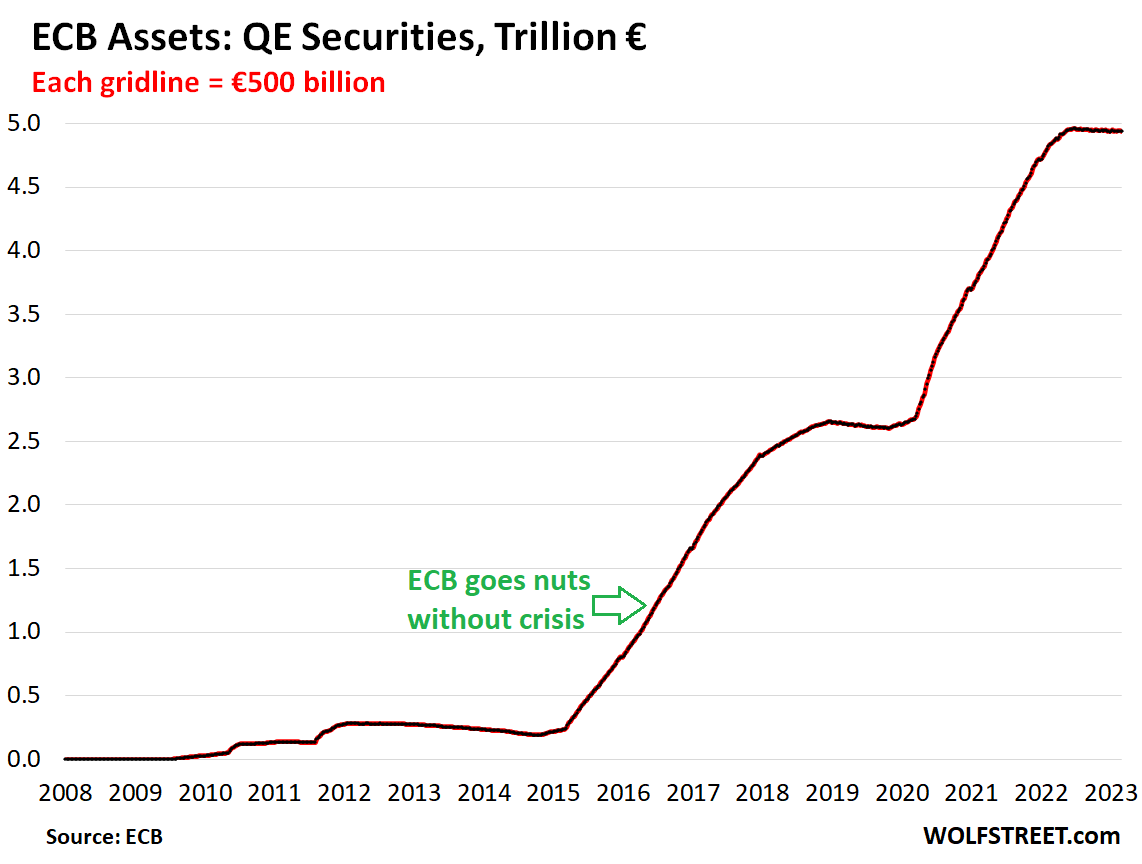

The bond QT: now starting.

Step 2 of QT, announced at its December meeting, starts in March, initially at a rate of €15 billion a month. At the February meeting, it announced that the ramp-up period of €15 billion a month will go through June. It said it will decide on the future pace by then. Comments by ECB governors about the future pace of the bond QT indicate that it will accelerate after June.

These bonds will come off the balance sheet as they mature, which is when the ECB will receive cash in the amount of face value of these bonds. The roll-off is capped at €15 billion a month initially. Any proceeds from maturing bonds beyond the €15-billion cap will be reinvested in bonds.

The ECB ended its bond QE in June 2022, and “securities held for monetary policy purposes” have remained roughly stable since then. On the balance sheet released today, which was as of March 3 – before the bond QT started – the balance of bonds dropped by €5 billion for the week and by €26 billion from the peak, to €4.96 trillion.

In 2015, the ECB suddenly got infected by the Fed’s virus of buying bonds, and it went hog-wild.

€1 trillion destroyed.

Like all central banks, when the ECB reduces the assets on its balance sheet, it receives money for the loans it had extended and for the securities it had bought, and it then destroys this money in the opposite way in which it had created it.

The ECB has now destroyed €1 trillion, mostly from loan payoffs (€995 billion), and starting to from the bond roll-off (€26 billion), combined a massive amount of liquidity that was drained from the financial system over the past few months – and more than the Fed’s $626 billion in QT.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Thirty years of easy money, now the Fed wants to pull the “Punch Bowl.” How long before the Fed caves and does an emergency QE, with lowered rates ? My crystal ball never worked.

The ECB is following the Feds turn to a tighter Monetary Policy.

Tighter Policy following one of the largest Bubbles in History.

Do I hear echoes of 1929, or am I just paranoid ?

$1T QT seemed to a one time hype to pause inflation increase. It’s now a spent force.

15 billion per month on top of -6% negative real rate (2.5% ecb – 8.5% avg inflation) isn’t big enough to need reverting QT.

Inflation in Europe will keep rising in face of this tiny QT.

QE is now impossible without hyperinflation. That’s the only reason all central banks are doing QT. It’s not that they suddenly became saints and voters took over their control from the multi-billionaires.

“$1T QT seemed to a one time hype to pause inflation increase. It’s now a spent force.”

BS. Over €1.2 trillion to go on loans. And the bond roll-off will speed up after June. Your comment is the same QT denier BS all over again, euro version.

“Inflation in Europe will keep rising…”

probably not. But it will remain high.

“…in face of this tiny QT.”

= QT denier BS.

Wolf. Can i just say how much i appreciate these posts to prevent the forum turning into Zerhohedge. It’s what makes your website the only financial type site i look at it.

I am not sure you should be so harsh on people with an alternate view from yours even if the person is not as knowledgeable.

People are trying to understand why the Fed did QE too long and tightened very slowly. The Fed buying mortgages when house prices were running up 2% per month would be the wrong answer on a econ 101 test.

THEY NEED TO READ MY FED or ECB ARTICLES before commenting on the Fed or the ECB.

Commenting guideline #1. It normally results in comments getting deleted.

What they’re doing is they’re reading some BS on ZH, and they’re dragging this BS into here.

ZH has been on the forefront of tightening deniers and pivot mongers since Nov 2021, and has been wrong about it all the way through. If you want to read or post this stuff, do it on ZH, not here.

Commenters that consistently drag this tightening-denier BS into here end up on my blacklist. I’m tired of seeing it.

THE FED SET AN ALL-TIME THEFT RECORD BY “PRINTING” $8 TRILLION+. INFLATION WILL NEVER BE QUELLED. IT’S HOW WE INFLATE OUR WAY OUT OF $31 TRILLION IN FEDERAL DEBT AND OVER $200 TRILLION IN DERIVATIVES AND FRACTIONAL RESERVES.

Respect, Wolf. It would be nice to read a monthly “where to put your money now” report. Is that available somewhere?

Looks like the banks are doing QT but the problem for me is the lack of Government spending QT. My own government has spent fortunes, giving money off on peoples gas and electricity bills. On top of that they gave me (and all people over 66) a £510 bonus for Christmas(thanks) and a 10.1% pay rise on my state pension. I’ve no idea on government spending is in the USA but I guess it isn’t lower.

Anthony,

It doesn’t stop there.

Occupational pension payments to many UK retirees are also being raised by 10.1%.

These are paid to:-

Armed Forces

Civil Servants

National Health Service

Teachers

Police

Firefighters

Local Government workers

etc

It is odd Ben Bernanke won a Nobel Prize (or equivalent) for economics for this very QE tactic. If I’m not mistaken.

Powell, it seems was not a fan.

“It is odd Ben Bernanke won a Nobel Prize…”

Bernanke promised that rates would “normalize” when unemployment dipped below 6.5% in a WSJ article in July of 2009, when he began the first round of QE.

Is that “promising” the foundation for Nobel Prize winning?

To issue the award seems curious as the world attempts to unwrap themselves from the damage of his policies.

We see the carnage today of Bernanke’s policies and of course Bernanke’s backstopping of any losses in the U.S. stock market in 2012 which turned the ponzi into a pure 100 percent ponzi. Any country that followed the lead of Japan’s zero interest rate policy ended up in shambles just like Japan.

Ben B let so much deadwood build up in the economy, he should be the most hated man in America. The world would be so much different if rates had even gone to 1% in 2011 instead of staying at 0 for years and years and years while dead wood built up.

Not even equivalent of a Nobel prize. Central bank prize to preacher of central bank economics.😉

A very big AMEN!

B

The FED wants to pull the punch bowl but not congress. Yesterday, Elizabeth Warren was scolding Powell for putting people out of work. She does not like the rate hikes and QT I guess

She hates Powell. She called him a “dangerous man” during the confirmation hearings, before any rate hikes.

I always thought she felt that way because of what he had done up to that point, which was to flood the world with liquidity. Apparently she’s never happy.

No, not one of the largest bubbles in history. THE largest, by a huge margin. It’s the same bubble (mania) starting from the mid-90’s.

It’s a global mania too given the interconnectivity of the financial system and world economy.

“The ECB has now destroyed €1 trillion” —>sounds like a war on inflation is brewing. Can the FED can destroy more fiat currency than the ECB, who wins the battle???

Basically two lanterns are hanging at Christ Church in Boston, and Jay is riding fast shouting “The 6% Rates are Coming, the 6% Rates are Coming!!!”

Yet will Jay fall off his horse before he makes it to Lexington, Massachusetts???

what? Even ECB does QT at a much faster pace than the Fed.

Nah, US still better than EU and Japanese at QT.

It was a one time flash sale stunt from ecb. Now ecb is planning -15 billion euro per month against -$75 billion real qt of fed.

BS. Over €1.2 trillion to go on loans. And the bond roll-off will speed up after June. Your comment is the same QT denier BS all over again, euro version.

I’m so tired of looking at this QT denier BS after having had to look at this BS here since Nov 2021. Every step along the way, this QT denier BS has been proven wrong by actual QT. So now that it’s in euros, you feel empowered to start it all over again? Sheesh.

“QT denier BS has been proven wrong by actual QT”

Oh no, not another premature “victory lap” re no pivot from the Fed . Like Mike Tyson said- “Everyone has a plan, till they get punched in the face”.

Powell hasn’t been punched at all yet. Unemployment really low, stock market way up, house prices still absurd.

I don’t claim to know what his actions will be, but I don’t see how anybody could know what he’ll do when challenged by some major adversity to him and his millionaire buddies.

Is there perhaps a degree of panic setting in at the ECB?

What happens if there develops an amount of bond default that is too psychologically large for the adage ‘a central bank cannot go bankrupt’ to convince the international financial markets of the stability of the ECB and the Euro project?

Wishful thinking by euro haters. Get real.

High inflation is making debt burdens lighter all around. This high inflation is helping the governments of Italy, et al. a lot, and they want to keep this high inflation. Classically, that is how Italy has always dealt with its debt, but since it joined the euro, there was no high inflation, and it couldn’t deal with its debts that way, and it got into trouble. So now it has high inflation, and it wants to keep it.

Wolf:

So with the Government spending more than it takes in, I’m not seeing how Net Debt goes down.

It appears that the sum of Fed Reserve Debt and Government Debt is at best static.

kam,

“with the Government spending more than it takes in, I’m not seeing how Net Debt goes down.”

Correct, “Net Debt” doesn’t go down. What goes down is the “burden” of the debt.

Government receipts rise with inflation or somewhere near (i.e. from higher wages, higher VAT receipts, etc). For example, Italy’s VAT rate is 22%. So the government takes roughly 22% in revenues from the sale of products subject to VAT. So if prices rise 10%, that means that VAT revenues are going to rise about 10%. When wages go up somewhere near the rate of inflation, it generates more income taxes. So there is a lot more revenues coming in to cover the interest payments.

Standard measures of debt burdens, such as the debt-to-GDP ratio (nominal debt divided by nominal GDP) all improve because nominal GDP shoots higher by 10% if there is 10% inflation, even if there is 0% “real” GDP growth. But the debt only grows 2-3%. And the debt burden (debt-to-GDP ratio) goes down.

That’s why Italian politicians and central bankers are already pressuring the ECB to make sure that “real” interest rates remain deeply negative (well below inflation).

Inversion between yields on 2-year and 10-year treasuries is largest since 1981. Cue market crash.

This market has remained unreasonable for years. It can be 6 more months of slow corrections without any crash.

Any historical analysis of the yield curve must take into account the amount of long term debt taken off the market by the Fed.

Put a number on it. 2.6 Trillion in MBSs plus Trillions in ten yr or longer Treasuries.

Imagine what the curve would look like if that long debt was sloshing around in the market looking for a bid.

The curve looks just how the Fed wishes it to look.

All is new since 2009 when they started absorbing long debt

So the ECB printed a trillion euros recently and handed it out it to some of their cronies (banks), but now wants it back. Presumably those cronies are now looking to pay this with newly printed money from some other central bank, possibly even an EU member state?

No, those banks are just selling some assets, such as bonds, to obtain the proceeds to repay those loans. That’s why this is QT. In response, bond prices have fallen and yields are up, exactly how this is supposed to work

While the FED, ECB and other major centre bankers are doing QT now. It is clear to me the FED & ECB will never ever to completely deflate their balance sheet back to 2008 level. Any future crisis will likely response with fresh round of QE, perhaps come with different name and with larger sum to it.

Addiction to money printing will only ended when these centre bank currency lost it luxurious as reserve currency.

No doubt they’re addicted to free money.

But right now crushing inflation is the goal.

So they’ll crush demand. Which means crushing the economy. Hard landing ahead.

Then they’ll get the free money machine fired up to ‘fix’ the crisis… again.

Dear Pivot mongers,

The FED might be gun shy after screwing the economy with 9% inflation.

Will they do it again? Maybe.

Let’s hope they learned their lesson.

I personally doubt they’ll be able to easily subdue inflation. I think “higher for longer” makes 10000x times more sense than pivot.

How can you even talk pivot w/ unemployment at 3.4%????

Unemployment could tick up 2% and nobody would even care tbh (except people w/o jobs).

Earliest pivot 2025 unless there is a crisis.

simonyoosen and everyone here:

It is total nonsense to think that a central bank can “deflate” a balance sheet back to where it was 15 years ago. Balance sheets have to grow with the economy and with currency in circulation (a liability). Balance sheets have always grown with those factors even before 2008.

Read this — it goes into the details in terms of the Fed:

https://wolfstreet.com/2022/09/05/by-how-much-can-the-fed-cut-its-assets-with-qt-feds-liabilities-set-a-floor/

Wolf:

With U.S. GDP creating a non-cash fiction of Owners Equivalent Rent, then the growth of the Fed’s Balance Sheet automatically is growing at 10% higher than it otherwise should be.

And since GDP is measured in Nominal Pricing, the Fed, de facto, is the biggest contributor to GDP. The magic and the curse of the USD.

In terms of owners equivalent rent… LOL. Did you miss it? “Owners Equivalent Rent” is what is now driving CPI higher.

In terms of the rest of your comment, you lost me.

https://wolfstreet.com/2023/02/14/annual-services-inflation-rages-at-new-four-decade-high-overall-monthly-cpi-hottest-since-june/

To the post above mine.

FRB balance sheet is not directly correlated to changes in GDP. Look at the composition.

The absolute floor is outstanding currency notes in circulation assuming everything else is zero which it won’t be.

Currency in circulation isn’t directly correlated to US GDP, as most FRNs are held outside the US. Demand for FRN has increased much faster than US GDP since 2008 when the GFC hit.

I feel the same, like they will come down a little and at some point some thing will break and then more QE, it like we are so far in debt they have no other choice.

But if they always respond to a crisis with more QE, why have they been doing the exact opposite during a massive energy crisis brought on by Russia starting a shooting war with the West?

The crisis started before the shooting war……my own gas and electricity bills went up 60% before any sanctions put on Russia.

Inflation in the US began soaring a year before Russia’s invasion of Ukraine.

In the EU, it began soaring 10 months before the invasion:

” The ECB has now destroyed €1 trillion, mostly from loan payoffs (€995 billion), and starting to from the bond roll-off (€26 billion), combined a massive amount of liquidity that was drained from the financial system over the past few months – and more than the Fed’s $626 billion in QT.”

This is one of the nice little things with which the ECB is momentarily ahead of the Fed. Hope the money destroying contest goes on longer and more fiercely lol

The Fed’s balance sheet represents the borrowing of savers purchasing power.

If the FED does indeed shrink it’s balance sheet back down towards zero then the purchasing power of savers is returned, if they reverse course then it was not borrowing but confiscation.

“If the FED does indeed shrink it’s balance sheet back down towards zero…”

The Fed’s balance sheet was NEVER zero, not even 100 years ago. It MUST have assets and liabilities on its balance sheet, like any bank.

And it is total nonsense to think that a central bank can “deflate” a balance sheet back to where it was 15 years ago. Balance sheets have to grow with the economy and with currency in circulation (a liability). Balance sheets have always grown with those factors even before 2008.

Read this — it goes into the details in terms of the Fed:

https://wolfstreet.com/2022/09/05/by-how-much-can-the-fed-cut-its-assets-with-qt-feds-liabilities-set-a-floor/

The assets the Federal Reserve purchased had low interest rates both treasuries and mortgage backed securities. It would seem at some point that the loses incurred in selling them would be undesirable to book; perhaps Quantitative Tightening would stop at that point?

Misconception here. The Fed is NOT selling assets.

It holds Treasuries to maturity, as which point it is paid face value, and there are no losses. The reduction in Treasuries on its balance sheet is exclusively because they mature and the Fed gets paid face value.

MBS come off the balance via pass-through principal payments and there are NO LOSSES either.

Mark to market — which is what you imply — is irrelevant if you don’t sell the assets. I don’t mark to market my bond-holdings either. Those asset prices always return toward face value the closer they get to maturity date, and the maturity date, market value = face value. That’s how bonds work. Market value is irrelevant if you hold them to maturity, which is what bonds are designed for.

“Like all central banks, when the ECB reduces the assets on its balance sheet, it receives money for the loans it had extended and for the securities it had bought, and it then destroys this money in the opposite way in which it had created it.”

This reminds me of what Dr. Frankenstein said:

“The monster was created artificially. It must be destroyed by the same means.”

Thanks for the extraordinary info. I have a basic economic knowledge but I think the tough part of this is this(maybe I am wrong): the QT has been done over the loans to private companies, when the ECB starts really tightening the money it lends to the countries they are going to be really in trouble as some countries (PIGS) rely on the free money coming from ECB which is not going to be there as easily, then they will need to squeeze their citizens with taxes creating economic trouble to many companies and many problems to the current function of these countries

Borrowing costs are going up. Meaning yields are going up. But they’re still below the inflation rates. Borrowing costs below inflation rates are very simulative. High EU inflation has the side effect of reducing the burden of debt on governments, so this period of high inflation is reducing debt burdens on highly indebted countries.

The BOE also made use of loans i.e. there was never directly printed money, more credit creation by the banking system (if you want to make the distinction). So the BOE borrowed money and then purchased government gilts.

However, the underlying problem similar to all is that as a central bank increases the base rate, the banking system then deposits this money at the central bank for the interest. Hence the losses coming from QE in a rising interest rate environment. The BOE faces a 200 billion GBP loss althought this is a headline number and reflects that you really have to do QT first, before raising interest rates, and clearly being in this situation reveals that the Fed and the Boe and the ECB have been wrong-footed about the current surge in inflation and particularly core inflation I should imagine.

For the BoE the losses are indemnified by the UK government and must be paid so its a political hot potato. The Fed however, seems to be able to just mark the losses as a “deferred asset” meaning that they can just offset these losses against future income.

However, smoke and mirrors aside, the Fed had been transferring ~100 billion to the US treasury but will book a potential 250 billion loss for 2023 which is probably around 1200 USD per US worker and that looks like it will be going forward with varying degrees. So following this the US treasury will need to borrow more money because transfer income has fallen for the foreseeable future.

” the banking system then deposits this money at the central bank for the interest. Hence the losses coming from QE in a rising interest rate environment. The BOE faces a 200 billion GBP loss”

On the contrary, the ECB said as early as last year that it would not pay interest on the money given to the banks, thus forcing them to pay back the debts that the ECB reliably destroyed

The ECB is a separate institution in a different currency zone, the UK having never joined the euro system. The BoE is idemnified by government for the losses and will be receiving the money from government. The UK government -may- introduce a windfall tax on the banking system to cover their losses, which would effectively leave the banks without any interest but not paying the banks has been ruled out.

That notwithstanding, the ECB is raising interest rates to induce the eurozone banks to sterilise their deposits, if they receive no interest they make other plans. Really, if the banks don’t receive interest on money that is in their keeping on behalf of customers, then they can’t pay those customers interest either, so its not even clear if the ECB can’t pay, won’t pay, plan will workbecause the increase in interest rates needs to be passed on by the banks otherwise how is it a policy lever?

The debt cruise ship is turning ever so slightly in EUR and USA. Fed/ECB created this topsy turvy system we now live with, and they are congratulated every time a trend reversal marker is hit (e.g. lower unemployment, int rate stabilization etc). Boom / Bust forever. Why can’t they just go away ?

Actually in my opinion all this could be solved with a balanced budget amendment to the constitution. Yes, I know and everyone else reading here knows….so save it. But what we have now is children in charge of your family’s finances. They will do almost anything to be returned for another term of office, so neither party will make any difficult tax and spending decisions.

QT and QE…these things probably go out the window if the budget is balanced….and you don’t have the money to police the world, or to make every congressman a multimillionaire, buy every new plane, etc.

Meanwhile the real value of the dollar is less and less.

If (somewhat) slow, that equals long term stagnation. If “fast”, that equals economic depression.

Look at reported “growth” since 2008 and the annual change in the federal debt before and since.

It’s necessary for long-term non-fake prosperity but not possible to do this without a noticeable to drastic decline in American’s living standards.

No, the budget won’t be balanced over 75 years or some other absurd timeframe I have heard in the past.

The ECB chart showing when bond buying began in 2015 is crazy. What were they thinking? The dam pandemic brought reality home too soon, right?

Saving the European Project which they presumably believed to be at risk.

In the US, everything and everyone will be thrown under the bus to preserve the Empire. In the EU, it’s to save the European Project.

It seems to me QE is getting replaced by deficit spending at least in the US. Besides the huge amount spent in 2021 an 2022. The next 10 years has 20 T of additional government debt built in.

With higher rates in the pipe line there doesn’t seem like a math solution except negative real rates or shock and awe redefinition of the value of the dollar.

…in other words, if status quo continues, we’ll see depression or hyperinflation followed by depression.

We have twin deficits in leadership and accountability.

When an economy over consumes long-term, there is no escaping a long-term decline in living standards if that’s what you mean.

Why would you or anyone else expect anything else? There is never something for nothing.

The majority of Americans and Europeans are destined to become poorer or a lot poorer over the indefinite future.

I’m going to hazard a guess that the 1+ Trillion TLTRO loans to banks were more or less to shore up their balance sheets for the pandemic. I doubt the money went anywhere. That would also explain why it came back readily quickly.

The other, more signficant QE that bought bonds; different story and that will be difficult to rapidly reduce.

All central banks, including the US are now in the process of cleaning up their balance sheets (to the extent possible). This is as much for countering inflation as it is to also counter to the looming threat of loss of dollar hegemony/trust vis-a-vis Russia/China/others and of course the Ukraine war. But again, we will see it will be difficult to signficantly reduce these balance sheets quickly. Still the central bank propaganda will continue.

“shore up the balance sheet”

That is incorrect. They were liabilities for the banks (money they owed). You don’t shore up a balance sheet by adding more debt. They were designed to provide free liquidity to banks to make loans and buy assets to drive up asset prices. And it worked.

To shore up a balance sheet, a bank needs “capital” (from issuing stock, for example), not liabilities.

Poor/wrong choice of words, you are correct. What I meant was the loans bolstered the banks reserves, which provided greater ability to lend. However, it is not clear all the banks used it for that purpose. From Reuters back in December:

LONDON, Dec 9 (Reuters) – Some banks in the euro zone could struggle to pay back money borrowed from the European Central Bank as volatile markets make it harder to raise funds, the European Union’s banking watchdog said on Friday.

Banks had until recently been sitting on 2.1 trillion euros ($2.21 trillion) worth of cash from the ECB’s Targeted Longer-Term Refinancing Operations (TLTRO), but are now repaying them after the central bank raised the borrowing costs on them.

“Banks must repay substantial amounts of central bank loans until 2024. A number of banks will be able to rely on existing liquidity buffers – including central bank deposits – to pay back central bank loans,” the European Banking Authority said in a report on banking risks in the 12 months to June 2022.

“Some banks however may need to issue additional debt or increase deposits. It remains to be seen how costly replacing central bank funding will be,” EBA said.

The fed follows the bond market. If you want to know when the “Pause-Pivot” will be just look at the bond market and when it moves down the fed will be right behind.

The obvious and popular investment is to buy t-bills which makes me think that the smart money is either shorting or going long the long end, but I am not smart enough to know which way to go.

The Fed is hoping and praying we return to a “stable” 2019 economy, with low interest rates, high asset prices, and low inflation. The Fed always refers to the pre-pandemic era as a success, even though it was artificially created via a decade of interest rate repression.

Problem is, we can’t return to the 2019 economy easily because we have $5T more money supply sloshing around the system, much higher stock and RE prices, plus higher and rising federal deficits.

That said, a return to the 2019 environment would encourage a person to buy long-bonds. If returning to 2019 is impossible, which it is, there’s little reason to buy a long-bond at 4% interest rate.

I am betting on persistent inflation of 4-8% until the system collapses, even though the target rate will be 2%. The appetite for federal spending on defense, programs, “fairness” initiatives, helicopter drops, business welfare, and similar inflationary spending seems to be rising, not falling.

There is a voting coalition of speculators, business welfare recipients, executives, homeowners, and individual welfare recipients, which has a clear majority. It doesn’t matter which party they are in. They vote for cheap money, low taxes, and increased spending. In short, they want income and wealth now. Future doesn’t matter. Warren, Bernie, Biden, Trump, McCarthy, and McConnell are all in agreement.

That is a ridiculous clueless statement. I usually delete this kind of nonsense.

The Fed tells you months in advance where it is going, and you can read it right here on this site, and the bond market reluctantly follows, and sometimes refuses to follow, only to get whacked into following suddenly.

Yep!

I stand corrected. Robert Prector makes a compelling argument with a great chart showing the bond and fed rates in lock step.

Since June 13 last year, the ten year yield has gone from 3.23% down to 2.64%, back up to 4.23%, back down to 3.37%, only to reverse back over 4% on March 2. That’s two major moves down and the Fed has stayed on the same path the entire time. What you suggest is inconsistent with what is actually happening in the bond market right now.

J Powell just said that the Fed debt ceiling should be raised without conditions on Federal Budget, or the USA will default and not be able to pay interest on their debt. True or False?

Also he said that we need to slow the growth in Fed spending, (Not the growth). That’s like a second derivative. That ain’t gonna get the job done in my book. We need to cut Federal Spending, period!

Obviously TRUE.

Watching Powell testify before Congress doesn’t inspire confidence

that anybody is willing to do what it takes to control inflation. They

are just going through the motions.

Wolf,

The fact that such a small of amount of TLTRO III loans (approx $100 MM euros) were repaid in Jan and Feb is IMO not a healthy sign. Even with the significantly higher rate the ECB is now charging on these loans, banks keeping these on the books indicates that perhaps alternative sources of funding are even more expensive or unavailable entirely.

IIRC, approx. 75% of all TLTRO III loans mature at the end of June?

BTW, how long before the SNB has to nationalize the CS mess.

I heard that FED QT is mainly through waiting bonds to mature. With the current speed, it seems to take some 10 years until bonds mature. Isn’t this a pretty slow pace?

But why would they? Is there any intention to speed it up?

US Treasuries mature in duration ranging from a mere 30 days to 30 years.

middleage

“I heard that FED QT is…”

Please read this article and do not post statements about QT and ask questions about QT until after you’ve read my articles about QT all the way from the top of the article to the bottom of the article. I don’t want to repeat my articles in the comments:

https://wolfstreet.com/2023/03/02/feds-balance-sheet-drops-by-626-billion-from-peak-cumulative-operating-loss-grows-to-38-billion-update-on-qt/

Treasury securities come off the balance sheet when the mature. Currently, the roll-off is capped at $60 billion a months, and it has been hitting the cap every month since this full-speed phase started.

MBS roll off the balance sheet primarily through the pass-through principal payments that all holders receive when mortgages are paid off, such as when mortgaged homes are sold or mortgages are refinanced. The principal portion of regular mortgage payments are also passed through to MBS holders.

From the linked article:

Also, don’t imagine that the Fed’s balance sheet should “go back to zero,” or whatever. Balance sheets have to grow with the economy and with currency in circulation (a liability). Balance sheets have always grown with those factors even before 2008. The Fed’s balance sheet was never 0, not even 100 years ago.

Read this — it goes into the details about how far the Fed’s balance sheet might drop AT THE MOST and why.

https://wolfstreet.com/2022/09/05/by-how-much-can-the-fed-cut-its-assets-with-qt-feds-liabilities-set-a-floor/

Anybody who owned a home the past couple decades has essentially lived for free. The appreciation of the home has offset the mortgage payment.

Given homeowners are a majority of the population in most jurisdictions, is this sustainable? Should people have a right to live in a dwelling without any cost on their part? Should people who don’t own homes be forced to pay the living costs of those who do?

It’s a good question for short-sighted monetary authorities, which have been bettering the positions of asset holders, at the expense of renters, retirees, and people who don’t hold significant assets.

As you said, the majority of the population is home owners. Is there intention for politicians to make their voters unhappy?

Policy is never about justice. It’s about your next election.

The majority of the US population are merely HomeOWERS!

You didn’t have to be a homeowner. Could have rented and bought SP500 since the GFC and you would have done better or worse depending on where you live. If it was an asset it got a strong tail wind.

World has changed. If Powell kills inflation to 2% assets got a long way to fall imho.

Bobber,

Does this take into account property tax, insurance, maintenance costs etc?

Also: a homeowner would only realize this ‘gain’ if they sold and moved into a rental.

And don’t forget the accrued cap gains tax for LOTS of homes.

AND you’re taxed on the higher value [unrealized gain] of your home, even if you don’t sell and realize those gains.

Owning to lock in a relatively consistent payment vs renting can save money, but if you didn’t sell, I don’t see how the house would have paid for any of that stuff.

It depends on your location. On the West Coast, home appreciation has paid for your equivalent rent, utilities, maintenance, taxes, plus your boat, your Tesla, your vacations… you get the picture.

These housing gains are largely locked in until the Fed disavows QE and interest rate repression as tools to fight recessions. Until then, we can look forward to many temporary price drops followed by quick V-shape recoveries as we head down the stagflation path to The Grand Reckoning.

MW: Policy-sensitive 2-year US Treasury yield jumps to 5.05%; spread on 2- and 10-year yields briefly inverts to minus 111 basis points

Even though the money supply shrinks, exceptional greed among investors keeps the risk appetite afloat.