Price drops in durable goods stalled. Food and energy prices rose. Core CPI has jumped by 14.6% in two years.

By Wolf Richter for WOLF STREET.

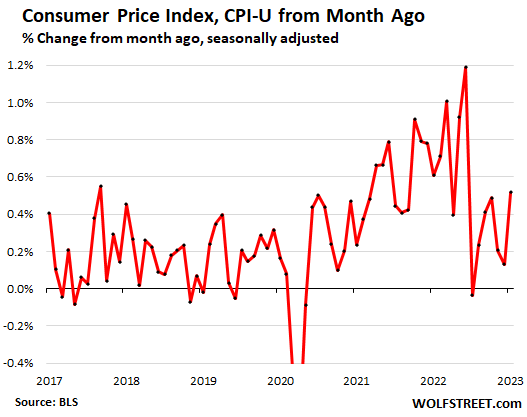

The Consumer Price Index (CPI-U) for all items jumped by 0.5% for the month, the biggest month-to-month increase since June, pushed up by relentless inflation in services, according to the CPI data released today by the Bureau of Labor Statistics.

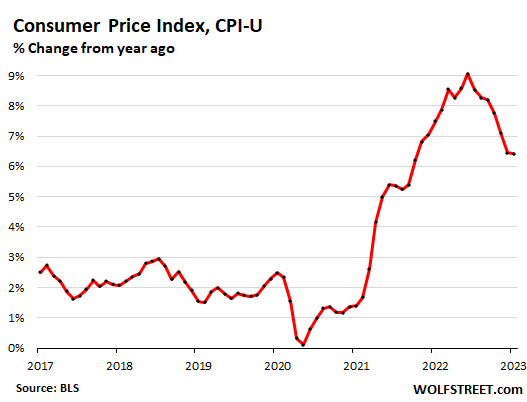

Year-over-year, the Consumer Price Index jumped by 6.4%, driven by a four-decade high in the services CPI. In December, the CPI had jumped by 6.5%. But the difference was mostly in rounding. Unrounded: January CPI = 6.410%, December CPI = 6.454%. Unrounded, the differences are too small to be meaningful:

Major categories of the CPI, month-over-month and year-over-year:

- Services: +0.6%; +7.6%

- Durable goods: -0.1%; -1.3%

- Food at home: +0.4%; +11.3%

- Food away from home: +0.6%; +8.2%

- Energy: +2.0%; +8.7%

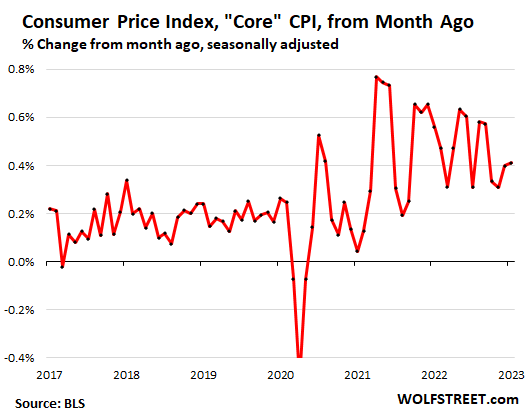

- Core CPI (without food and energy): +0.4%; +5.6%

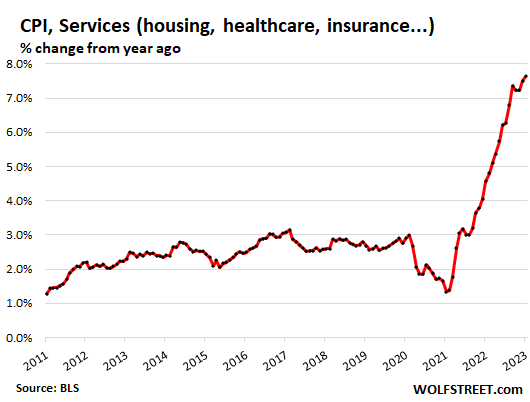

Services inflation jumps to new four-decade high.

The Fed’s eyes are on services. Powell has been talking about it for months. I have been screaming about inflation moving into services since at least the February 2022 CPI, before the Fed even started hiking rates. Nearly two-thirds of consumer spending goes into services: Rent, other housing factors, insurance of all kinds, healthcare, education, repairs, travel and hotel bookings, subscriptions, streaming, telecommunication services, haircuts, pet services, etc. In services is where inflation gets sticky.

The CPI for services inflation rose by 0.6% in January from December – on top of the upwardly revised December jump. It has been over 0.6% in seven of the past 10 months, which shows just how sticky services inflation is, once it breaks loose.

On an annual basis, services inflation jumped by 7.6%, the worst year-over-year increase since 1982 and the fifth month in a row above 7%. In services is where inflation is now raging, where it is entrenched.

Services by category.

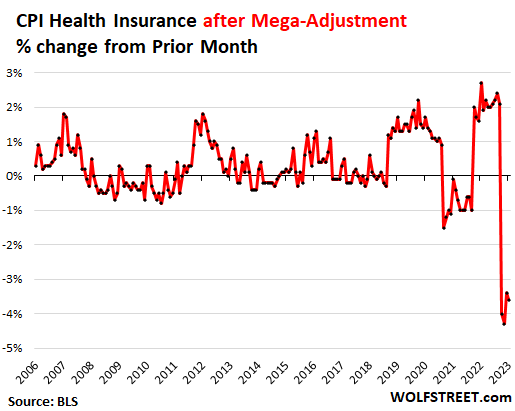

The health insurance downward adjustment. The BLS undertakes annual adjustments in how it estimates the costs of health insurance and then spreads those adjustments over the following 12 months. The first mega-adjustment hit in October. January was the fourth month of 12 (more details here). Without that adjustment, services CPI would have been even worse for the past four months.

Due to this downward adjustment, the CPI for health insurance plunged by 3.6% in January from December. These four months of mega-adjustments reduced the year-over-year rate of the CPI for health insurance from the pre-adjustment +28% in September to +1.2% in January.

But the Fed’s favorite inflation measure, the PCE price index, tracks health insurance inflation differently, and there is no such adjustments.

Here are the month-to-month changes of the health insurance CPI after the adjustments:

Health insurance is part of medical care services, and so that adjustment knocked down the CPI for medical care services to -0.7% month-to-month. Both are included in the table.

| Services | MoM | YoY |

| Overall services | 0.6% | 7.6% |

| Car and truck rental | 3.0% | 1.8% |

| Postage & delivery services | 1.5% | 6.8% |

| Hotels, motels, etc. | 1.5% | 8.5% |

| Motor vehicle insurance | 1.4% | 14.7% |

| Motor vehicle maintenance & repair | 1.3% | 14.2% |

| Pet services, including veterinary | 1.0% | 9.4% |

| Water, sewer, trash collection services | 0.9% | 5.0% |

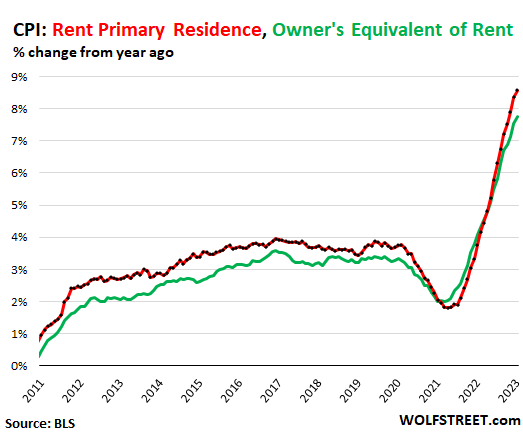

| Rent of primary residence | 0.7% | 8.6% |

| Owner’s equivalent of rent | 0.7% | 7.8% |

| Video and audio services, cable | 0.6% | 3.9% |

| Other personal services (dry-cleaning, haircuts, legal services…) | 0.5% | 5.3% |

| Recreation services, admission to movies, concerts, sports events | 0.3% | 5.7% |

| Telephone services | 0.2% | 2.0% |

| Tenants’ & Household insurance | 0.1% | 0.9% |

| Medical care services | -0.7% | 3.0% |

| Airline fares | -2.1% | 25.6% |

| Includes: Health insurance | -3.6% | 1.2% |

The CPI for housing as a service.

The CPI for “rent of shelter,” which in January accounted for 34.4% of total CPI, tracks housing costs as a service, not as an investment, and is based on rent factors, primarily:

“Rent of primary residence” (accounted for 7.5% of total CPI) spiked by 0.7% for the month and by 8.6% year-over-year, the highest since 1982. It tracks how actual rents paid by tenants changed at a large group of rental houses and apartments, including in rent-controlled units (red in the chart below).

This contrasts with other rent indices that track “asking rents,” the advertised rents of still vacant units on the rental market. When asking rents are too high to fill the units, landlords may lower the asking rent. There was a boom in asking rents during the pandemic. But rentals don’t turn over that much, and proportionately not many people actually ended up paying those asking rents.

“Owner’s equivalent rent of residences” (accounted for 25.4% of total CPI) jumped by 0.7% for the month and by 7.8% year-over-year, the worst in the data. It tracks the costs of homeownership as a service, based on what a large panel of homeowners report their home would rent for (green line).

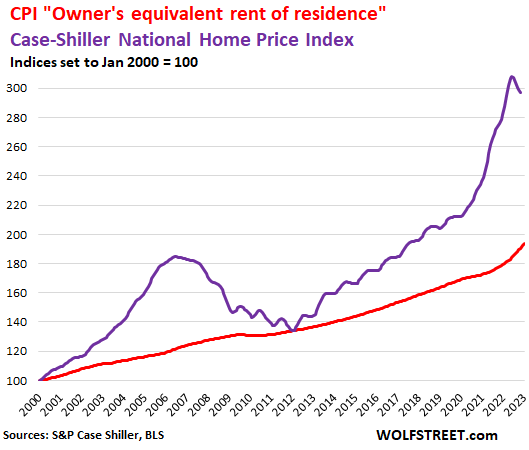

Home prices, based on the Case-Shiller Home Price Index, peaked with the “June” report and then started to decline [I track this by city in The Most Splendid Housing Bubbles in America]. The most recent data point is the three-month moving average of September, October, and November (purple line in the chart below).

The red line represents “owner’s equivalent rent of residence.” Both lines are index values, not percent-changes of index values:

Food inflation.

The CPI for “Food away from home”– restaurants, vending machines, cafeterias, sandwich shops, etc. – jumped by 0.6% for the month and by 8.2% year-over-year, the sixth month in a row of 8.0% or more.

The CPI for “food at home” – food bought at stores and markets – re-accelerated to an increase of 0.4% in January from December. On an annual basis, the CPI for food at home rose by 11.3%, the 11th month in a row with double-digit year-over-year increases.

As some prices started to retreat, other prices rose. The CPI for eggs spiked due to issues triggered by the avian flu:

| Food at home by category | MoM | YoY |

| Overall Food at home | 0.4% | 11.3% |

| Cereals and cereal products | 1.3% | 15.9% |

| Beef and veal | 1.1% | -1.2% |

| Pork | 0.0% | 1.5% |

| Poultry | -0.1% | 11.2% |

| Fish and seafood | -0.1% | 4.0% |

| Eggs | 8.5% | 70.1% |

| Dairy and related products | 0.0% | 14.0% |

| Fresh fruits | 0.8% | 3.0% |

| Fresh vegetables | -2.3% | 7.4% |

| Juices and nonalcoholic drinks | -0.1% | 13.3% |

| Coffee | 0.9% | 12.8% |

| Fats and oils | 0.0% | 20.9% |

| Baby food & formula | -0.5% | 10.0% |

| Alcoholic beverages at home | 0.4% | 5.3% |

Energy prices rose:

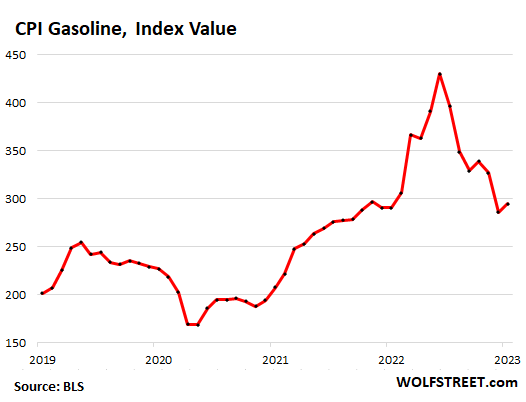

Gasoline prices rose by 2.4% in January from, December, after having plunged since June 2022. The explosion, so to speak, of gasoline prices in the first half of 2022 has now been unwound.

Year-over-year the CPI for gasoline is up by 1.5%. It’s possible that the CPI for gasoline may have bottomed out in December. This chart shows the CPI for gasoline of all types:

And note the surge in natural gas piped to the home. Electricity continues to rise sharply:

| Energy | MoM | YoY |

| Overall Energy CPI | 2.0% | 8.7% |

| Gasoline | 2.4% | 1.5% |

| Utility natural gas to home | 6.7% | 26.7% |

| Electricity service | 0.5% | 11.9% |

| Heating oil, propane, kerosene, firewood | -3.9% | 18.0% |

Durable goods prices: Drop appears to stall.

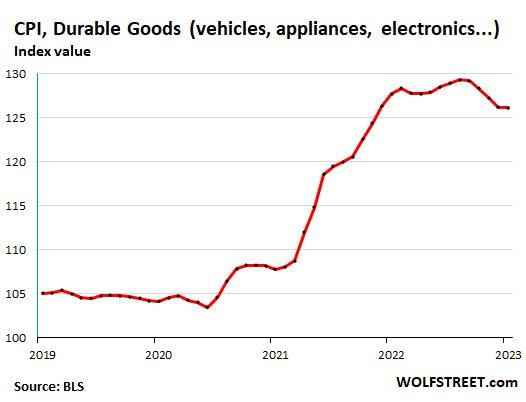

The CPI for durable goods fell for the fifth month in a row, by 0.1% from December, a much slower decline than in the prior months, slowing the process of working off the ridiculous spike that started in late 2020.

On an annual basis, the durable goods CPI fell by 1.3%.

Here is the CPI for durable goods, expressed as index value, not as percent-change of the index value. It shows the ridiculous spike starting in late 2020 through mid-2022, and the price drops since then.

The long-term trend of the durable goods CPI since the mid-1990s, when “hedonic quality adjustments” were incorporated, was downward – meaning deflationary. And this is how it should be naturally because manufacturing and transportation efficiencies, driven by competition, should cause prices of the same product to come down.

However, those are not the same products. For example, even the basic model of the Ford F-150 pickup now has a 10-speed automatic transmission, up from a four-speed automatic in the mid-1990s. Motor vehicles have gotten a lot better over the years and aren’t the same products anymore. The cellphones of the mid-1990s have turned into smartphones. They’re not the same products anymore. And so the cost of those improvements are removed from the index via “hedonic quality adjustments.” The spike in prices that started in 2020 outran by a wide margin the hedonic quality adjustments.

| Durable goods by category | MoM | YoY |

| Durable goods overall | -0.1% | -1.3% |

| Information technology (computers, smartphones, etc.) | 0.0% | -11.7% |

| Used vehicles | -1.9% | -11.6% |

| Sporting goods (bicycles, equipment, etc.) | 0.5% | 1.5% |

| New vehicles | 0.2% | 5.8% |

| Household furnishings (furniture, appliances, floor coverings, tools) | 0.5% | 6.4% |

“Core CPI.”

The core CPI, which excludes the volatile food and energy products, rose 0.4% in January from December, just a hair (unrounded) above the increase in December. This also shows just how sticky inflation has become, despite the drop in durable goods prices:

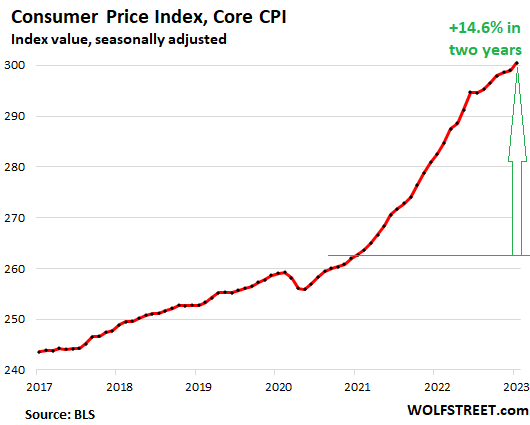

Year-over-year, core CPI jumped 5.6%, compared to 5.7% in December. This chart shows the index of Core CPI, rather than the year-over-year percent change, for a dose of where this is going: Over the past 24 months, the Core CPI has soared by 14.6%:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Thank you for putting this report !

YEp, can understand quite a bit, still most way over my pay grade.

gotta love government

1st they mandate more efficient HVAC systems effective Jan 1, 2023

the mandate brought a 30% increase in HVAC costs

now manufacturers are raising prices March 1st – 10%

So much for “Inflation has been defeated, Fed is ready to Pivot”.

The working class of US will keep getting mugged till they keep voting for the same scumbags in both parties.

It’s interesting to me to look at Turkish currency vs. gold last 20 years. It shows what governments can do in a generation. Turkish currency has lost more than 98% of its value vs. gold in 20 years. Always money to buy military hardware though.

Turkey today. USA tomorrow.

A simple comment about this.

Food away from home: +0.6%; +8.2%

I was going to pick-up a sandwich this evening. I went online to see the menu and order. I almost fell over when a Rueben Sandwich (pickup order) was $16.95. This is absurd and I did not order the sandwich but its shows me how much trouble we are in! My god, its meat, sauerkraut, dressing and bread!

The Federal Reserve is working but the Federal Government is pumping money into the economy like crazy.

oy vey!

I have better luck in San Francisco when I go to places in person that don’t have fancy websites.

Yep, a whole in the wall restaurant without the overhead and better eats

When I lived in the City the go to cheap sandwich was a Bahn Mi from little Saigon. Less than $5 out the door.

Wolf, I live here also and a recent purchase of a half grinder

in West Portal cost me $12.00 and some change. All my food is

made at home with locally purchased basics. Just saying that

is not too far off of the $16 bucks mentioned.

@Concerned Citizen,

I know what you mean. Yesterday during lunch time, I dropped off all my tax documents at the tax guy’s office. On my way back to work I stopped at a hole in the wall Mexican Cafe. I ordered a Potato and Egg breakfast burrito. With a can of coke it came to $13.00. Two years ago it would have been about $10.00.

It was a big delicious burrito though. I wasn’t really even hungry for dinner.

This is government stimulus, but not of the money pumping variety. Many cities have implemented minimum wage increases linked to CPI. In my city of Sunnyvale, the minimum wage has gone from $10.30 in 2015 to $17.95 effective Jan 1 2023, with annual increase matching the CPI, to a maximum of 5%. All the restaurants issue price increases every January. It becomes a never-ending cycle: things get more expensive because things got more expensive.

and my experience is my home cooked meals are so much better and healthier then what my meager dollars buy now at restaurants.

Ever since Covid the restaurant business took a nosedive on quality while prices have relentlessly climbed.

The last chart, -Core CPI- pretty much sums up the “gut feelings” at the stores. Fewer items at check out and a lot more $$ on the bottom of the receipt.

Fixed incomers are wondering what they can possibly voluntarily cut back on next. (I say “voluntarily” because many packaged products are shrinking at the same time prices are rising).

Government still deficit spending about a trillion more than they take in to goose the economy. Seems like fiscal policy and monetary policy is going to collide sometime in 2023.

I think I read US trade deficit hit an all time high? Wow. A lot of this deficit used to be oil related. But not now. That means the consumers are stil spending a lot on gimcrackers from China.

———————–

US Trade Deficit Hit Nearly $1 Trillion in 2022, Largest on Record

The annual goods and services trade deficit rose 12.2% to $948.1 billion

Until Federal spending is brought under control Inflation will continue at the current rate or go higher no matter what the Fed does. With Brainerd joining the White House economic team expect things to go downhill.

Time to try Intermittent Fasting.

Welcome Back Karter?

Time will tell.

You mean, Kotter!

I have said before. our electricity supply price went up 55% from 9 cents to 14 cents per kwh over the past 8 months. In all my years I can’t remember any price decrease. Electricity is not a discretionary cost for any business. Those increased costs will ripple through for a long time to come. But why doesn’t the S&P come down I wonder? The 10-year is going back down and it makes sense that equities follow. Some kind of delayed reaction maybe. Or maybe those balloons were filled with mind-altering dust. Ha. Sorry couldn’t resist.

I think maybe the equity market is just so insanely FOMO’d (or FOMO’d about FOMO) that it doesn’t care…. it’s thinking that “if the SP500 is going to hit a new high in 2 or 4 or whatever years, why worry about a 10% drop along the way? Better to undergo that than miss the longer rally.”

This has been historically correct. But along the way each dollar loses value in the amount of goods it can be traded for.

The equity markets priced the shift about 8 months ago. The biggest driver in services is housing and it bears little relationship to inflation -today- where the trend is actually towards outright lower prices (deflation). Compounding this is the forward looking component for expectations, since everyone is seeing headline prices dropping the FOMO in that market is gone.

The remaining elements are real and driven by energy (direct and indirect) and shift in demand. However, just like there was a rush to buy “things” during lockdown, there was a rush to buy “experiences” and this demand spike is likely to shift. Anecdotally while I see high prices for vacation rentals this summer in prime lake towns, I see a lot of availability. As for things like air travel, capacity was adjusted lower for the last few years. Volumes have not yet returned to 2019 levels but the big increase in demand vs extremely low base (plus fuel prices) of course drive prices higher. As capacities adjust (from the reduced level) and as consumer spend power gets squeezed, we will see prices relent.

I was very bearish during the 2021 peak but most of the excess got washed out when companies traded down 70-90%. The actual “news” and rates at that time never justified the level of adjustment that occurred, just like the peaks were never sustainable. But one data point in a downtrend doesn’t change the fact that inflation is rapidly abating and we’re likely to be sub 3.5% (or lower) by early next year. For most valuation models, you aren’t going to be concerned about the path to that more reasonable level, which is why market reactions (long duration assets) to blips is muted.

👏

“But why doesn’t the S&P come down I wonder”.

Simple.

The artificial idiots doing most of the trading today in high frequency have been “trained” on data from times when “Stocks only went up”.

So they buy. Because Stocks only go up in their little artificial brains.

Just ask Google’s Bart Simpson. He’ll tell you.

And here in Germany I’m happy that I was able to change electricity providers and get a new rate of 37ct per kWh. Last year many utilities didn’t take new customers or only at a very “basic” rate. My utility made a mistake but i was too lazy to fight it and they put me into that basic bracket. They’re charging 68ct per kWh starting March. (Though there is a pricecup at 40ct. for 80% of your annual consumption…)

Though our consumption is very low, even though we are 5 adults (though 4 students..) we only used about 3000 kWh last year.

14ct at those prices you can make money smelting aluminium lol.

I have read that the buyside is dominated by retail investors and hedge funds that are using trading strategies.

The market still believes that the economy is going to roll over and the central bankers will pour even more money into the markets. I personally think that we are headed for stagflation and once the markets see that, they will melt.

Stagflation is the worst scenario. It combines a high discount rate with poor demand and a lack of growth.

Interesting as always.

I think the fixed market has this right, hikes more likely than pause/cuts as the recession that never came continues to not arrive and, if anything, the economy is running a bit hot.

Direct to taxpayer stimulus works way better than bank bailouts. Bad news for tech bros and homeowners missing the days of 0-2% fed rates.

If it were not for the vast funding of the government banker aid groups, e.g., the FDIC, and the privately owned, bankers’ cartel (“Fed”) being able to print money to give to its insolvent bankers, we would see more oinks for bank bailouts now or very soon. Note the BIS report on trillions in derivatives gambling by the bankers; the losses that they are incurring on inflated, pandemic, car loans, which they are having to repossess and write off; and the losses from deflating real estate bubbles which are going negative in most states in value versus the mortgages secured against that real estate.

I am sure that their Fed will continue their very, very profitable inflation-creation game, while pretending that they want to reduce it as long as they can. However, while I am sure that the bankers are happy with the help that their “Fed” cartel gives them by reducing their vast liabilities through the creation of inflation, I would not be surprised (given their reckless gambling, e.g., in swaps per their own BIS) if the banks already need more bailouts, pronto. We have to keep giving more free money and aid to our precious, ultrarich bank owners and none to the dirty, nasty, poorer 90% of Americans, don’t we?

For the bankers, the wonderful thing about the wunderbar Fed inflation is that it reduces the real value of the banks’ liabilities (i.e., your deposits, operating expenses, and the wages the banks’ employees get), while they can pass on any increases in their costs to their customers (by charging them more) or borrowers (through higher interest rates.) Joy! They will not give it up.

If you want to look at the complete picture, inflation also reduces the real value of a bank’s assets. I’m not so sure banks are a big winner with high inflation.

Dear rojogrande,

The game is rigged is my point: “assets” of the now, probably insolvent banks usually do not get “reduced” by inflation but increase with it albeit bubbles like the real estate bubbles pop. It does not matter any way, because they are really assets effectively guaranteed by their Fed private cartel and thereby the US government. Like the rich girl in the Billy Joel song, if they do low, it “does not matter any way,” they “can rely on the old man’s money,” meaning Uncle Sam’s money.

It is like kids gambling with their loving, rich uncle’s money after the Glass Steagal Act was repealed for the banks: you keep all the profits and if you lose, you do not lose because he pays: i.e., if the bankers lose, we lose, because they get more free money; they do not lose, ever. The banks normally have an eggshell thin skin of their capital usually over the assets they effectively hold for depositors and mishandle-gamble to their (the banks’) profjt. I believe their capital just got eaten away by real estate and auto loan losses, so the banks will get more bailouts.

RH – in the interests of accurate attribution, ‘Rich Girl’ was written/performed by Hall and Oates (the original inspiration being a ‘rich guy’ who was the former paramour of one of their girlfriends…).

may we all find a better day.

The real estate bubble has not really burst yet, just got a little bit deflated. I dont understand who is buying houses right now.

Money trickles up, not down.

Keep what you can, starve the beast.

The economy isn’t just “running a bit hot,” it’s still grossly overheated. Jerome Powell and the FED know exactly what they’re doing. They’re destroying the working class and the poor to protect the fortunes of the wealthy. “Let it run hot….transitory….soft landing….” All of those catch phrases told us in advance of their plan.

The monopolies were made during 0%. Everything we need is in the hands of a few profiteers. Corporations have achieved monopoly-level dominance over their markets, the pandemic was a blessing to them.

The only real pushback in this inflation is to drive down workers’ pay.

In 30s, parent, educated MS in stem. Each day I’m feeling so much further behind any dreams or realities of middle class life.

It feels like, Inflation is the new normal with capital I and jPow is, little j, little p for this world.

Can’t wait for the fed to print more money when inflation is already hot!

Early 40s, educated, parent, ‘middle class’ in salary yet not been able to turn the heat on despite 30 degree nights all month thanks to the electric rates. Life’s easier when you accept our parents’ standard of living is not as broadly attainable despite the bootstraps folks’ diehard insistance.

Still wondering how we’re supposedly swimming in Middle Class wealth from 3 or so stimulus checks that barely touched the lost wages and savings from inflation and years of wage stagnation. Math never worked out as far as I can tell, yet indeed the money printer went brrrrrrr and the upper class raked it in.

The longer Jerome Foul drags out the rate hikes and supposed “inflation fight,” the better the results for the wealthy and asset holders, the worse for everybody else. He knows this. This is the part of the scam where he makes the higher asset prices “stick.”

Make no mistake about it, the FED could easily have reversed all of this inflation, and quickly. They could have engineered deflation in everything. But that wouldn’t benefit them and their wealthy buddies. Everything is designed for the rich. Every single move.

I always look for your comments that say exactly what I am thinking.

The super bowl tickets cost $7500 – $20;,000. Nearly all the tickets were corporate goodies given to their executives and their families, and fully deductable off the company’s taxes paid. All the hard working salaried Americans weren’t there in the stadium and were relegated to watching on TV looking at ads to fatten the wallets of the rich. They wound up subsidizing the rich corporate fat cats on both ends. This is essentially an income transfer from the middle class to the rich.

Notice the cameras never showed individuals in the crowd.

Why?

I actually think the longer they drag out the interest rates the more damage to asset prices in the long term. If they whacked the economy and destroyed inflation, they could cut interest rates back down, but if they continue to have that huge balance sheet it will cause sticky inflation and they have to go higher for longer.

SwampCreature my personal favorite Super Bowl ad was the touching Memorial Sloan Kettering Cancer one discussing the importance of coworkers embracing cancer patients as family.

Meanwhile MSK Cancer Center in NYC is laying off 337 staff between 1/17/23 and 7/1/23 per its WARN Notice. “Reason for Dislocation: Economic”

Had to pay for that sweet Super Bowl ad spot somehow I suppose.

Truth bomb. Inflation is/has been entrenched. Probably thanks to the “transitory” narrative.

I believe inflation will be entrenched until federal spending is slashed. Of course the surge of federal spending is what has propped up the economy since COVID, so there is a lot of bureaucratic resistance against cutting it. Once upon a time, I hoped that surging interest costs on the US debt would force Congress to slash spending—I think we are sunk too far in our addiction to federal cheese though

I said it before, but the effects of the Omnibus have yet to be felt in the economy, so I expect inflation to climb up again in the future.

The spending by Congress was done at the end of last year, the funding of the spending is what they are arguing over. Makes no sense to me, but that’s the way they do it. Every time.

I grew up during Viet Nam war and war on poverty, guns and butter spending which led to the high inflation 70’s early 80’s.

After the COVID money drop, I just read at this point it is going to take $349 billion to rebuild Ukraine after the approximate $120 billion already spent helping blow the place up. Our politicians are escaping the blame for the inflation for the most part.

Sure it’s Powell’s fault for not walking into the president’s office and telling him no more easy money to fund deficits 18 months ago when inflation spiked up. But here we are again, with inflation a problem.

The faux wealth of the last decade will be revealed. If you can get 5% on your money in a t-bill, stocks should be valued at about a PE of 10 to comp you for the risk in a no growth scenario. That is SP500 of 2000 not 4000, but it is going to take all of 2023 for reality to sink in.

15 percent in 2 years. Nice soft default

If inflation goes up 15%, and your stocks/bonds are down 15%, it’s a 30% loss of your savings.

Rethink this Bob. Inflation reduces your purchasing power not your savings.

Maybe you should rethink.

Savings = future purchasing power

I kind of agree with Bobber. Inflation can rob you real quick if you are in the wrong long duration assets. But I see your point too, purchasing power and assets are not exactly the same.

For older folks that live off their RMDs it very close to the same. They are typically living off 5% or so of their account value, so they get a double whammy when inflation goes up and assets go down. I am sure a few saw the 30% real income hit last year.

This is true if you are living off selling assets.

If you are retired and living off stock dividends, you will not see this loss since even if the stock drops 15%, the dividends are constant and paid per share. The % paid per share goes up when the stock drops.

Similarly for bonds, if you are living off bond interest income, that has not changed even though the bond price may have fallen 15%.

People who are living off dividend and bond interest are only affected by inflation once. Only if they don’t sell the asset.

Seen it all before, Bob

Dividends fall when EARNINGS keeps on, NOT just for once.

I view Bonds and Equities on the TOTAL return, irrespective of fall or rise in dividends. For my MRD, I take What I required over the 12 months. Of course I keep my cash level more than 60% but get adjusted depending upon the Mkts ascend or descend ‘pattern’. 5-10% against the mkt which cuts down the deleterious effect of volatility which is increasing in scope and size. NOT perfect but I can sleep at night.

While Uncle Jerome slow-walks the fight against inflation for years to come, the masses are being trained to accept high inflation, as a real squashing of inflation would collapse the economy into a depression! The can is being kicked down the road but over the next few years will hit a big brick wall at the end of the road, and it won’t be pretty!

Oil is getting geared for a new all time high within the next 18 mos!

Its a good thing January doesn’t count since adjustments or something, or so the the rest of internet tells me, glad I get just the data here.

I am just so confused why this big pivot narrative exists, appropriate interests rates help most people. I wonder if people get a taste of savings earning interest maybe their will be push back on the desire for a pivot.

“I am just so confused why this big pivot narrative exists, appropriate interests rates help most people.”

You’re confused because you’re rational.

You’re welcome.

lol, because leverage.

Don’t forget Minsky either.

“appropriate interests rates help most people”

But not banks who benefit from not paying lower interest rates (Big banks are currently paying .1% on savings accounts). Or Wall Street who benefits from a migration to stock when interest rates are low.

I think the concerns of “most people” are a distant 3rd in the priority of things.

Politicians care but they don’t want to mess with Wall Street or the Banks since they are huge campaign contributors. Have Saving Account rates been a priority in any recent election?

The narrative on the MSM, however, is that “inflation declined slightly.”

The mass hallucination continues unabated.

“It is difficult to get a man to understand something, when his salary depends on his not understanding it.” – Upton Sinclair

They are the disingenuous with their disinflation

It does not matter what msm or market think. What matters most is what FED think.

What matters is what the Fed thinks about what the market thinks about what the Fed thinks… about inflation? 😂

Where does the distortion end and reality begins? No one knows anymore. Same as USSR, nobody believes the government anymore.

Suzie. The FED is not part of the government. It is a cartel of privately owned Big Banks.

But otherwise you are correct. Nobody believes what the private cartel says anymore.

Old Ghost,

“The FED is not part of the government. It is a cartel of privately owned Big Banks.”

Misconception here.

The Federal Reserve Board of Governors is a government agency, and all its employees are federal government employees with a government salary and a government pension, including the seven members of the Board, including Powell and Brainard. These seven members of the Board of Governors are appointed by the President and confirmed by the Senate. The Board of Governors has lots of employees, and they’re all employees of the Federal Government. They’re working in the Eccles Federal Reserve Board Building, the main office of the Board of Governors of the Federal Reserve System. This is a federally owned building on 20th St. and Constitution Avenue in Washington, DC.

The 12 regional Federal Reserve Banks are private organizations that are owned by the largest financial institutions in their districts. They include the New York Fed, the San Francisco Fed, the Dallas Fed, etc. All their employees are private-sector employees.

The FOMC – the policy-setting committee – consists of the 7 members of the Board of Governors who are federal employees and have permanent votes on the FOMC. The New York Fed governor also has a permanent vote. The other 11 regional FRBs rotate into and out of 5 voting slots annually.

The FOMC is designed to give the 7 government employees a voting majority over the 6 presidents of the regional FRBs

Boom, headshot.

Thanks Wolf.

The continuation of the increase in inflation has declined slightly. Prices don’t come down, they just go up at a slower pace.

The key to looking at CPI is to exclude everything that’s going up and then but stocks for their future value (lol).

After these numbers, wonder what’s Pow Pow’s next move is going to be? Based on market action today, doesn’t look like the dip buyers and bull cultists think another Jackson hole like Pow Pow is on the horizon, might as well be actively taunting Pow at this point…

Can’t wait to see the market get Fing smack in the face soon enough though, that smug look deserves it…

The market can see through Powell’s bluff and hence going up and up.

Market knew, if Powell was really serious, he’d have raised rates by 50bps.

Not only he didn’t raise by 50bps but he sent straight dovish signals.

we all know what happened afterwards.

We should know whom does Powell works for.

I will say what most are thinking, you’re an idiot

Time to wake up or stop being high on what ever you are on.

Great article. Utterly depressing too.

Cold hard facts laid bare with no end in sight.

As so many others have observed- the savers, the prudent, the realistically cautious that still believed for a time in the American dream of homeownership have been rolled like the new asphalt in a new all-rental community.

We have to play the cards we are dealt. If you don’t have kids, you should just be living in a rental and stashing cash in case buying gets cheaper than renting. For most places rent to buy ratio is at record low. At some point cash will be good and leverage will be bad.

As inflation lowers 10s of millions americans standard of living when will the mobs with pitchforks and torches flood the streets! Been happening in Britain and Europe.

Never. They are all worked up about transgender girls playing sports and election denial. The fact that they are being robbed daily by inflation doesn’t even dawn on these bozos.

Food prices just keep going up and up with no end in sight here in Canada.

Price increases by 25-30% for basic staples and consumer foods.

Yet, Tiff Macklem chose to pause rates while at the same time, Powell is still choosing to raise rates, albeit slowly.

It’s like Tiff only cares about the real estate speculators and the politicians who own real estate and rental properties.

I guess pausing interest rates only make sense in Canada but pausing rates when they’re still deeply negative makes no sense anywhere else.

Food prices are going up and up in the GTA. It will be worse in remote northern communities.

The RE Bubble must be maintained at all costs in Canada.

BTW, your GIC response: The banks are always trying to delay the increases.

“Annual Services Inflation Rages at New Four-Decade High, Monthly Overall CPI Hottest since June”.

What’s the surprise here? Inflation was WAY OVER 10+ % last 1 year, and as of today, the rates is still playing catch up!!

As of today, we are still -2 % , yes Negative Real Yield!

No wonder Economy is still strong.

No wonder Labor Market is still strong.

No Wonder Supply still could not catch up with Demand.

That’s why we still have HIGH Inflation.

OH “hedonic quality adjustments” ?! Well, if STEAK price double, it’s NOT Inflation because Fed said you losers are switching to eating cminced chicken feet. No quality loss here.

LOL. And Wolf whole heartedly agreed that Powell is doing the MOST in human history. Wow. Raising 4.75% interest rate when Inflation is 20+ % since 2020.

Even today we still have Negative Real Rate (4.75% Rate – 6.5% CPI) . But Wolf only see the goods in Powell. lol

“OH “hedonic quality adjustments” ?! Well, if STEAK price double,..”

LOL, no, hedonic quality adjustments are not applied to steaks. Durable goods only, such as cars, computers, smartphones.

Wolf,

I add my thanks for this report. On the news programs this morning I tuned out all the “instant analysis” by various talking heads. I knew that before the day was out that Wolf Street would have the real story in an understandable way. I was not disappointed.

With tongue firmly in cheek, I disagree with the observation that you have been “screaming” about services inflation since Feb-2022. My ears have heard no screaming. However, my eyes have seen continued important and valuable insight on the subject. But, I understand your point. Again, thank you.

My landlord sent me my annual lease renewal offer with a whopping 18% increase. I told them to take a long walk on a short pier. We only spend about 4% of our income on rent, but I have to make a stand somewhere. This is getting ridiculous.

I suspect his costs are going up as well. My property tax for this year went up 13%, 11% last year, and 11% the year before. This is with no change to the property.

Yes, property taxes. Those government pensions have priority, including inflation escalators built in,

This right here. I’m seeing big increases in property taxes – wish that was its own category in the CPI! Give us one more thing to scream about.

Forget it Jake, its clown world.

If (when) Social Security takes a hit, either from reduction of benefits, later eligibility, and/or means-testing, I want to see the same applied to all federal pensions.

Not just government pensions, but all pensions. I’m tired of reading about cops who retire at age 48 with $200k a year pensions.

@ Einhal,

While I agree and would love that, there’s no connection (other than PBGC backstop) between those local-level pensions and federal entitlements. So those firefighter deals are between those local taxpayers and the firefighters.

I was fed up with feeding the system about 20 years ago. I got off the hamster wheel seeing if I could get untangled from it. For the most part I have. I was able to find empty homes that people needed to have someone in to help pay taxes and keep up property, but always below market rents. I just found my fifth one. In rural areas a lot of people are property rich and cash flow poor and they want someone they know and trust in the property as an empty property is going to deteriorate quickly. Anyway, it’s got me off the property tax target list.

I can see why a lot of retirees get a 30 year old RV and go out west to BLM land. It’s a way to get unhooked from the system if you can’t afford your property taxes.

The tiny home builder I watch in TN is setting up an off grid community in Nevada. The idea is to have two properties at different elevations and move your home between your winter and summer elevations. Will it pan out? I don’t know, but there is big demand for cheap basic shelter and Nevada is good for solar.

Read “Nomadland”. It was a good book on similar conditions from 2008-2012.

As mentioned above, Property Taxes and Insurance likely went up 10-20%.

Good luck in finding a deal elsewhere.

Even if housing prices plummet (theoretically helping renters), taxes and insurance decreases will lag by a year or 2. Whenever they assess.

Inflation this past year has really hurt us, with 2 rent increases, higher insurance, utilities, food, healthcare costs, etc. I even see the increases at the discount stores I frequent. I don’t know how long this can last with all the layoffs being announced.

In my area there are tech layoffs and softening home prices, but there still seems to be a lot of money out there. Restaurants are busy, new cars everywhere, even the line at Chipoltle was the longest I’ve seen in years in spite of the higher prices.

We are in an economic blow off top.

I agree. This has been the type of inflation that hurt lower income. Someone on lower income is already shopping down scale and has no where lower priced to go. They can’t afford a newer more efficient car. It is wide spread and has impacted all their expenses as it has fed through. All they can do now is start eliminating stuff. Cable or internet. Maybe a phone. Maybe a car and depend on their family to run them to the store.

True, but some of them can still eliminate cigarettes, lotteries, pull-tabs, Snapple, chips, $1000 rims, and $1500 iPhones. I see savings of $300/month right there, and it would improve their life.

“some” of them could. You would be amazed at how frugal many Americans are who stretch dollars to cover basic necessities. Don’t make the assumption that the majority of people who are struggling in this country to make it financially are somehow just wasting their money on “luxuries” like “Snapple,” LOL

The facts are there, presented in the charts. The charts make the longer term direction very easy to see – just take a step back and focus on the them. It is simple to see the direction we are headed; need to take eyes off of the month-to-month decimal jitters.

Fed Funds Rate at 4.75%. Would need to be above 8% just to meet current headline inflation rate. Get back to work Jerome, you’re not done destroying the middle class just yet. The FED is the USA’s worst enemy.

CPI at 6.5%. Where you getting 8%?

I haven’t looked at equities yet today. Boy, I must have missed an absolutely crushing. I hate to even look. Down, what 5%?

Today’s CPI was mostly shelter imputations.

Nonsense. Read the article! At least GLANCE at the services CPI table. I put it there just for YOU. And glance at the food table, for example. Lots of double-digit stuff in these areas, LOL

I drove by the farm and saw a couple of hens with gold necklaces.

Cal-Maine, which controls 20% of the retail egg market, reported gross profits of $535.3 million in 2022, compared to $50.4 million in 2021.

Why let an outbreak of bird flu go to waste?

Yes, there’s that. Much like the oil companies.

From Monday’s Farm News out of Grand Forks:

‘Strap in for Another Golden Age in Agriculture’

The first ‘golden age in agriculture’ was in the early 1900s when farm income doubled and land values tripled. University of Minnesota Grain Marketing Economist Edward Usset says American agriculture enjoyed similar success from 2007-to-2014. “It’s the second Golden Age” due to the rapid growth in the ethanol market. Usset believes the increase in soybean crushing capacity, biodiesel demand and war in Ukraine could deliver a similar scenario. “Strap in. It could be an interesting few years ahead.” Usset spoke at the Best of the Best in Wheat and Soybean research meeting.

North Dakota leads the way with three huge soy crush plants being constructed now. A representative, ‘Origination Coordinator,’ for one of them, Green Bison Soy Processing, says, “We just have a giant appetite for soybeans.”

By the way, if you’re a successful soybean farmer in North Dakota, status doesn’t come from gold chains. No, it comes from the airplane you fly and land on the farm’s runway strip. “Oh, she’s a twin engine and six-seater. Yah, nice one, eh?”

As a follow up; the Green Bison Crush Plant is now taking bids from producers and elevators for the 2023 harvest. ADM owns 75% and Marathon Oil owns 25%. Expected to use at least 55 million bushels. North Dakota generally produces 200 to 225 million bushels of soy a year.

Also from today’s Farm News out of Grand Forks:

“The farm bill is the primary focus for the American Soybean Association. ASA Vice President Josh Gackle sees the value in educating lawmakers about this important legislation. “There are well over 200 new members of Congress between the House and the Senate that have very little exposure to the farm bill. Sharing what’s worked in the past and what we need to update will be a focus.” Gackle, who farms in Kulm, North Dakota, says ASA hopes to update reference prices and base acres.”

The power of the farm lobby in Congress is very strong.

Dad and I ran our wheat seed genetics company in partnership with the Friederichs Seed family in Foxhome, Minnesota. Pete Friederichs was President of the National Barley Growers Association. He testified before Congress a few times. His best quote: “Without barley, there is no beer.” I’ll raise a glass and say, “Here’s to a good malting barley crop this season!”

Speaking of Shelter:

You see Neel Kashkari threatening QT bond sales if mortgage rates keep loosening.

“You’re right it [loosening financial conditions] does make our jobs harder to bring the economy into balance. All things being equal, that means we’d have to do more with our other tools.”

The Federal Reserve Bank of Cleveland median price increase hit a new high above 7% today. Median price means that half of items are below and half of items are above, thus half the items have 7% or greater inflation rate.

Cleveland Fed Median CPI % Change 12 months:

Aug 2022 – 6.7%

Sept 2022 -7.0%

Oct 2022 – 6.9%

Nov 2022 – 6.9%

Dec 2022 – 7.0%

Jan 2023 – 7.1%

(Search “Median CPI – Federal Reserve Bank of Cleveland”)

———————————————————————————-

In summary, “Inflation Secured” and looking extremely sticky. Note that service inflation is like a virus as it infects other areas of the economy in a stealthy, near invisible way that is only completely obvious once the economy gets horribly sick (hint 2023/2024). Add in paradigm shifts in global labor and manufacturing, geopolitical black swans, climate change energy transitions, and numerous unknown unknowns to the Fed’s challenge of “Landing” the global economy. Some think glass half full, others think glass half empty. I personally believe glass structurally shattered.

Thus it will be a monumental challenge to stay under 3-4% annual inflation rate, as 2% Fed goal is a archaic pipe dream of previous pure luck via the near perfect storm of ideal demographics, USD global dominance, unprecedented world peace, virtually free foreign labor costs, etc.

So buckle up friends, as for better or for worse, this ain’t your grandparents economy anymore.

Wolf – What do you think about Brainard? and her move to the White House?

Just based on what I have read about her, she seems to be an uber political appointee who cares about getting ahead, not telling the truth.

I don’t think she ever mattered. Powell matters and he’s not on your side.

Ms. Brainard’s husband, Kurt Campbell, is on the National Security Council as President Biden’s “Indo-Pacific Coordinator.” As such, he reports directly to Jake Sullivan, National Security Advisor.

This link is interesting, as the USA and China are in an economic competition, and perhaps, entering into a military conflict.

A fly on the wall listening to them have a private dinner conversation?

gametv

She’s a loser;. She will fit right with the rest of the White House economic team.

My Blue Cross/Blue Shield premiums just went up 9% for 2023. They are a non-profit so I think that is a good representation of health care inflation. I don’t understand all the complicated government figures that include all kinds of adjustments. I do understand the extra $60 I have to shell out every month. That came out of my COLA so I’ve wound up back to square one.

My car insurance premiums are going up 20% next month for the 6 month period. No accidents, no tickets, no claims.

My car insurance premium went up almost 27% for next 6 months starting next month.

IN last 1 year, it increased total of 37% or so.

Go shopping?

I did this last year and all the insurance quotes were high. And I shopped it thru a broker. Crazy! I’m a good 20% higher than last year with a stellar driving record and cheap car.

I live in a state where car theft is a misdemeanor. We have one of the highest car theft rates in the country.

A friend in a safe neighborhood had his car stolen in front of his house last month. His insurance company paid for a replacement.

No that simple:

“If the stolen vehicle is valued at more than $950, the person can be convicted of grand theft auto. Grand theft is a wobbler offense that can be charged as a misdemeanor or a felony. A conviction for a misdemeanor carries a maximum sentence of up to one year in jail. If convicted of a felony, a person faces prison time of 16 months, two years, or three years. A second felony for auto theft, joyriding, or any felony theft involving a vehicle carries a penalty of two, three, or four years in prison.”

Point taken. Thank you.

It is a misdemeanor if the car is valued under $2,000 in my state.

It is a felony over that amount. We have the highest auto theft in the country. The state legislature is creating a bill to lower this.

The problem is that the recovery rate of stolen vehicles is about 10%. Insurance companies are paying up and are having to raise rates.

When my home insurance premiums went up 300% between 2010 and 2022 I told my insurance company to go pound sand. Their service stunk to boot. No claims for 30 years. They said they only make 2% profit. So where was all the money going that I was paying? I also dumped my auto insurance with them. They are running ads non stop bragging about how they support Vets. BS

In NC Blue Cross and Blue Shield is very large, but it has non profit and for profit sides to the organization. Use to be all non profit.

I find the auto insurance industry interesting that nonprofits and for profits fight it out in a pretty competitive industry.

Would it be fair to say the “disinflation” comment was premature? I realize we all have the benefit of hindsight.

To all thinking Powell is pivoting cuz he ‘only’ went ,25 on top of 7 previous bumps…go long! There are some huge bargains out there in the FAANGS etc. because a lot of fools thinking ‘don’t fight the Fed’ have bailed. But if the Fed is a wimp…go for it!

I’ve been closely monitoring the inflation storm for work since I set prices on our products. Things have calmed down but I have been surprised how much upward pressure still remains on prices still in 2023. We finally got margins back to normal after 7 increases in around two years and some cooling in steel cost. Prices up 30-50% in 3 years overall and probably not retreating any time soon.

We just got a contract renewal today for natural gas in the shop. Used to heat the place and for a paint curing oven. Going up about 50%. Last year it was $60,000. Another 3% here and there on some purchased fabricated inputs still coming in. A little relief on steel but still pressure on wages going up.

My wife works in healthcare. Their management just sent notice today saying their margins have been compressed like never before in the past few years. Labor, insurance, tools and materials…all driving their nonprofit hospital system into unsustainable loss territory. Glad to hear it wasn’t just us but it tells me this inflation still has some legs as we all try to find sustainable margins again.

You cannot print your way into prosperity!

Rando62, similar locally in So Cal with our local hospital system. Let’s just say their non-profit status is definitely appropriate.

My sincere question to you guys: What inspiration should the next generation, your kids / nephews /niece, get their life inspiration from?

Seriously, I am thinking to tell my kids it’s all right not to ace their science subjects, or 4.0 GPA, or be inspired to invent / solve real world problems.

Why? Because of Powell, and his minions that still sing praises to him, who just print USD $$ to save the rich in the name of helping the poor.

Why work hard, when you could just get easy mortgage with 1% down ?

Why work hard, when you could just max leverage through rentals and let other build your equity for life?

With Bernanke together, Fed had trained the whole generation of Get-Rich-Quick. Have you noticed, the bigger the economy contraction, the higher the Stock and Home Price Jump?! So much so, that you could not even find a house for sale in 2021 and 2022, 2 FULL YEARS!

It’s funny, in the past 100 years, people actually fearful of Recession, and avoid investment risks. But now, stock market and RE are praying for recession and subsequent rate cuts and money printing!!

What an upside down world we are living in. Thanks to Fed minions praising Powell for dragging their feet in raising rates that is still WAY BELOW Inflation.

Yeap, Negative Real Yield still, and Fed get the praises.

I told my son to never put a penny into a 401K or similar product. Just keep his money where he can get to it anytime and pay cash for cars and homes. The alternative feeds the monster that is never sated.

Unfortunately, they are tryiong to do away with cash too!

“They” always screams conspiracy theory to me.

I can get cash whenever I want. It’s super convenient. I don’t even speak with a human or wait in line. Just go to an ATM.

Honestly though… Cash sucks. At least buy some I bonds (that “They” own). Buy some TIPS or money market. Something!!! If you don’t trust banks, buy Coca Cola stock. Anything bro. Just dead cash shrinking.

That is sound financial advice.

However, if everyone is paying for homes or cars on credit with low monthly payments, there is no motivation for the seller to discount prices to give a cash buyer a break on price. Cash buyers are priced out.

401K’s, HSA’s and IRA’s make sense when you reach a high tax bracket. They shelter your income from higher taxation and allow you to take it out at a lower tax rate.

The game is rigged, but if you aren’t playing the game, you are paying too much.

I’d vote for ending all of the games and making it a level playing field for cash buyers and savers.

Sean

‘What inspiration should the next generation’

-Adopt minimalist life style, from the very start.

-Look for volunteer ‘DOWN SHIFT’ if possible.

Most important: Ability to discern NEED from WANT.

Try, at least TRY for sufficient help to enhance and encourage advances of ”theoretical physics” is what ALL young folks SHOULD do and be heavily encouraged to do these days Sean. ( Along with following engineering, of course. )

IF and only IF WE, in this case our species WE, get our act together and push our universal/mutual understanding of reality at least somewhat closer can WE survive.

When, not IF, the real ”black swan” event arrives WE had better be ready to deal with it or game over…

Not looking particularly rosy right now, eh

After the CPI report, odds of a third Fed rate hike by July rose to about 60% from just below 50% before the data.

As posted earlier, in regard to banks being stressed out with higher rates:

TCE is declining industrywide because of the negative effect of rising rates on the market value of bank holdings of AFS securities. The number of banks with ratios of TCE to average tangible assets of less than 5% jumped markedly in 2022, with some banks posting negative TCE.

At year-end 2021, only 4 community banks had tangible equity capital ratios below 5 percent; that number increased to 333 at June 30, 2022, indicating less ability to sustain economic shocks.

Am I dumb or isn’t this all about currency debasement ala Zimbabwe, Venezuela, Argentina etc. I know the $US is the cleanest shirt on the rack but really if industrial output gets over run by government expenditures the game ends.

Time for the Fed to sell MBS isn’t it. Speed up QT a little bit.

MBS is a US cultural oddity and should not exist. I don’t get government borrowing (issuing bonds) either, why not just print the friggin paper at no interest,

“why not just print the friggin paper at no interest,”

The Fed did that, and now we have the worst inflation in 40 years. Go figure.

I just got a big rent increase and housing prices around here have stabilized in the unaffordable zone and in some areas are creeping up again. I feel like that housing number isn’t coming down anytime soon, even if Powell et al seem recently smug about “knowing what’s going to happen” in that sector.

The Fed should repent for buying MBS in 2021, because it was a sin.

Yeah, I mean the way I see it they took money from everybody (in the form of currency debasement) and then turned around and gave it only to people who owned housing. A gift that will keep on giving to some people and taking from others for as much as 30 years. A gift that disproportionately gives to the generation that got here first and takes from the ones who got here after. What’s so wrong with that (/s)?

MBS is a US cultural oddity and should not exist. I don’t get government borrowing (issuing bonds) either, why not just print the friggin paper at no interest,

SPX monthly cannot get it up > Apr 2022 close.

Perhaps the SP500 is suffering from “Premature Electrification/Disinflation”? Like the F150 Lightning buyers who might be dealing with mass battery recalls, looks like the Fed Pivot is also getting recalled…

Baby boomers retired early during the pandemic of 2020 driving up the cost of labor. Rent inflation is out of control. Some local hotels are full, but it is high tourist season in Florida. The price of homes has been rising again, less likely in areas with declining populations. The price of cereal is up as Ukraine is a major grain exporter. War caused inflation. Men were taken away from constructive jobs to do destructive work. There is a long line at the Chic-fil-A drive through during lunch hour. Prices approaching $10 for lunch.

Starting from trump and then Covid in total we probably have 1.5-2 million less emigrants. This probably in no small part has contributed to inflation in low skilled jobs sector.

DH,

Some truth in there, but I would strongly argue that war did not cause this inflation. War has been ongoing for ages. Companies have always wanted to raise prices. And COVID didn’t really stop much useful production of goods, especially in the western world. The new variable in our current inflation mess was stimulus. Plain and simple.

Our dear leaders passed out too many dollars to too many people and businesses, and when these recipients rushed to trade their dollars in for tangible goods, these redemptions overwhelmed the productive capacity of certain parts of the economy. Some big industries operate in normal times without much capacity slack.

Steel industry, shipping, railroads, trucking, semiconductors, and other factories. These industries don’t have much spare anything just sitting around waiting for more orders. And the ones that do still require hiring of labor to operate the machines. They cannot bring another 30% capacity on overnight, especially when everyone around them is vying for the same production inputs.

I felt this play out in real time in our business with suppliers and customers. Too much demand all at once broke the system. This inflation train already left the station months before the Ukraine invasion. The war certainly didn’t help, but it is a distant second or third place influencing factor behind over-stimulus.

RG 62

There was a flood of money printing with the pandemic as the payroll protection people demanded. They did a bailout of cruise ships, airlines, restaurants, hotels etc. Rental car lots were full of idle autos as people quarantined. There was also a shortage of computer chips, sensors, etc. caused by a desire for automation and AI. More recently there was panic over rearranging supply lines after Russia turned against Ukraine and NATO. Commodity prices spiked.

So, let me get this straight… health insurance was increasing in cost 2%/month for about a year (24%/yr) and now it’s suddenly falling 4%/mo (48%/yr)?

You need to read the section, “The health insurance downward adjustment” in the article, and look at the chart.

The BLS estimates health insurance inflation in a peculiar way, which caused it to overestimate health insurance inflation in 2022 (after the upward adjustment it made in the fall of 2021). So in the fall of 2022, it made another big adjustment in the other direction (downward), to correct the overestimate in 2022, and this adjustment is spread over the next 12 months and will undo the overestimate of 2022.

I explained this in the section above, “The health insurance downward adjustment,” along with a chart. In the text, there is also a link to an article I wrote about this last year with further detail.

great analysis ! I track our expenses pretty closely and I would say close to 16% increase in last 14 months – I was very interested in the VRBO earnings and they were stellar – I know 4 people in the vrbo business and they are all minting money ! and my neighbor who takes 8-10 cruise”s a year was told my Carnival that the cruise’s he wants to go on this spring and summer are sold out- ! “unprecedented demand” was there email – people are $pending and no end in sight no slow down

Economy is still very good. Low unemployment. Low bankruptcy rates, low credit defaults, most people are seeing nice raises, energy prices are dropping (nat gas) and Biden is going to release more oil out of the SPR to keep oil and gas prices low.

Interest rates are still accommodative. 6ish mortgage rates are good historically good rates

Almost none of the zombie companies have gone bankrupt. They still are able to find funding it appears.

I know people think the FED should raise faster but they did almost one of the faster rates raises in history. Inflation is trending down and is going in the right direction.

So far it looks like a soft landing?

Housing prices will remain elevated in a soft landing. The good thing is that there are a lot of apartments being built that should help with rent prices. Fingers crossed.

Wow 3.0% Retail sales in January 2023 versus 1.9% expected.

At some point investors might finally understand that no recession/no landing/ no labor pain is going to force the Fed to go higher for much, much longer on rates until something breaks.

On the bright side, 5-6% CD rates by July 2023??? At some point why would investors put their money in an SP500 ETF hoping to gain 8-10% (4200-4600) when a FDIC insured CD pays 5-6%?

The crowd that has been going “The Fed will pivot any moment now, any moment now…” for the past year or so is getting a bit antsy.

Got two opinion pieces on a blog focused on the energy sector.

First one boils down to: “The Fed said they might raise the rates up to 75 points and only did 50 so they are going to pivot this year”.

The other “The Fed almost never does maximum raises so when they said 25 point increments for 2023 that means no increments or even a reduction and the pivot will happen before the end of the year despite the Fed claiming it won’t pivot.”

That is quite the denial going on there before these numbers were known. From what Wolf has been explaining it looks more likely that that 25 point increment is going to be a minimum.

Third rate hikes odds to July increasingly likely, but odds increasing for more aggressive efforts

Chances of a 50-basis point March hike initially ticked higher—to 12% from 9%—on the CME FedWatch Tool this morning.

Mortgage rates headed higher, Treasury yields higher and equity speculation going into NFT Flying Monkeys Mode, collision ahead

“NFT Flying Monkeys Mode”

I liked the Baby Wedding E-Trade commercial during the Super Bowl.

“So you live with your parents but own a house in the MetaVerse?”

I love beating dead horses, and it’s probably obnoxious to harp on tired metaphors, but the disconnect occuring with equity speculation, is all about over confidence and a mindset reminiscent of a drunk be driving down an icy interstate.

Maybe mainstream media amplifies narratives and dumbs down the impacts of economic conditions, amplifying the sirens songs from wall street.

The over confidence that spills into being aggressively determined that the icy conditions don’t matter, is what provides opportunity for the other side of that reckless thinking. People who’re cautious in the next few months, eventually will be able to take advantage of today’s market stupidity and arrogance.

There are times I feel that gaining leverage over an idiot, is somewhat morally wrong, but in this casino we live in, you have no choice, in betting on outcomes, betting to win, betting to get ahead.

Is it really wrong to take money from people that are recklessly betting on stupid outcomes, I think not.

Unfortunately, the same can be said for people buying homes today, who unwittingly anticipate they’ll be making a good decision buying at excessively overvalued heights.

The CPI and inflation trends are exactly like a blinking warning light on a mountain pass, use caution ahead, the icy roads are increasingly dangerous.

Wolf,

Any plans to add Zillow’s rent index to the rental CPI graph? Really good way to illustrate methodology of “asking rents” versus “rents paid”. I’m surprised how often this metholody topic comes up.

I used to do that but I have sourced on the Zillow rent index (ZORI) and I no longer use it for anything.

1. As you said, the ZORI reflects asking rents. In terms of inflation, asking rents are a BS number. They’re not actual rents that tenants actually pay. I explained that in the article.

2. The ZORI has a focus on Single Family Houses as rentals. It covers some multifamily, but not enough. But multifamily is HUGE in the rental market.

3. Zillow adjusts the ZORI heavily every month going back eight years each time, and what I said about it one month is wrong the next month. It also doesn’t adjust back further than eight years each month, so the data going back further than eight years doesn’t connect anymore to the current eight-year range and become useless.

4. Its San Francisco index is WAY off, compared to other asking rent indices, and compared to what I see, maybe because of its focus on single-family houses, and SF is a largely multifamily rental market. The ZORI numbers for SF rents are just wrong. So I no longer think the ZORI overall has any value.

ZORI says $3400 a month for SF county. ? Sounds pretty close to me. In what direction do you think it is “way off”?

They completely missed the downturn in asking rents. Asking rents peaked in July 2019 then went south pretty hard, then plunged during the early portions of the pandemic as people were bailing out of SF. At some point, they were down about 28% from the July 2019 peak. They have come up some but are still way below that July 2019 level.

One of the largest landlords in SF just defaulted on a $1/2 billion loan backed by dozens of apartment buildings, with occupancy rates last year at 65%.

There are about 3-4,000 new housing units being completed and added to the housing stock every year in SF. Last year, I believe it was 4,500. And SF has lost something like 60,000 inhabitants. This started already in 2018/2019, and has gotten a lot worse. Everyone has some different numbers on the population loss. But whichever numbers are cited, they’re pretty big.

There are not that many single-family houses for rent in SF (most of the rentals are multifamily rental buildings and condos). But Zillow’s is concentrated on SFH, so my theory is that this is why it missed the dynamics in SF.

I got another anecdote to throw on the pile.

Just today our company received a notice from one of our major service providers that they are increasing prices across the board by 9.5%

The reason given was “continued pressures across the global economy, including unprecedented inflation rates”

Methinks the endgame is everything meaningful goes to barter or cash. I have noticed that in the last five years, a lot of stuff is off the books. It does not show up in government stats but maybe someone out there has a feeling for it?

Anyone who isn’t livin the high life of a Washington civil servants salary knows that inflation is probably double what the government tells you. Every week I go to the grocery store and see the prices higher.

Today’s retail sales confirms the economy is taking off, not landing. I’m told that housing is collapsing yet homes in my area are sold in weeks at decent prices. I see construction everywhere!

We need interest rates north of 8% to get inflation down.

Bloom

A lot of people I’ve met since I lived here in the Swamp have two government workers in their household. Some retire and then go to work for Beltway Bandits that they oversaw when they were working in the government and get another income on top of their retirement incomes. So they are triple dipping or quadruple dipping. Many collect Social Security on top of all of that. That’s why they can afford to buy these 2 million dollar new homes the builders are putting up and live a rather lavish life style.

There are ways around things. My eyeglasses listed price $2,500, got them for $700 and got a big hug for not putting them into the insurance meetgrinder. I traded a chord of wood for some drywall. I went around retail to the manufacturer for cabinets saved $30k. Got drawings for build work for $2k instead of $30k. Screw inflation, We’re going third world here and may as well get with the game.

I’m seeing price drops galore in Arizona.

Price drops in housing.

Sounds like everyone here is complaining about Inflation ? I thought everyone just wanted to get rich LOL Love your Voted chosen

Breaking news : since Feb 2 SPX closed six times above Sept 12 high.

If SPX turn around and on Feb 28 close below Sept 12 we might deflate.

Keep spending on food services and fun drinking places, because industrial production is down.

We are blooming : in Feb 2020 real disposable income per capita was

$46K. In Feb 2023 (not over), we completed a round trip to : $45.5K.

Amerikan can’t stop burning burning money.

PPI came in hot, so expect CPI to be hot next month as well. Happy times.