“Not seasonally adjusted” sales plunged from the big record in December, but not as much as in pre-pandemic Januaries.

By Wolf Richter for WOLF STREET.

Despite all the rate hikes, consumers are still flush with money, they have jobs, and if they lose their job, they can quickly get a new job, and their pay has gone up, and the price of gasoline has plunged from the peak in 2022, prices of some other big-ticket goods have come down, and so there’s extra money to spend on other stuff and in restaurants. And that’s what “retail sales” are tracking: the sale of goods from the retailers’ point of view, reported today by the Census Bureau. They’ve been strong despite a big shift in spending from goods back to services.

Inflation has shifted from goods to services. While inflation is now raging in services at the highest rate in four decades, inflation in durable goods, such as motor vehicles, furniture, and electronics, has turned negative year-over-year (-1.3%), unwinding some of the crazy price spikes that started in 2020. So for most retailers, price increases are now tough to make stick, and they no longer play the big role in retail sales that they did a year ago.

Today’s sales report was a shocker on the surface: +3.0% in January from December, seasonally adjusted. But beneath the surface, it wasn’t a shocker; it showed three things we’ve discussed here a lot:

- Consumers are simply in no mood for landing this thing.

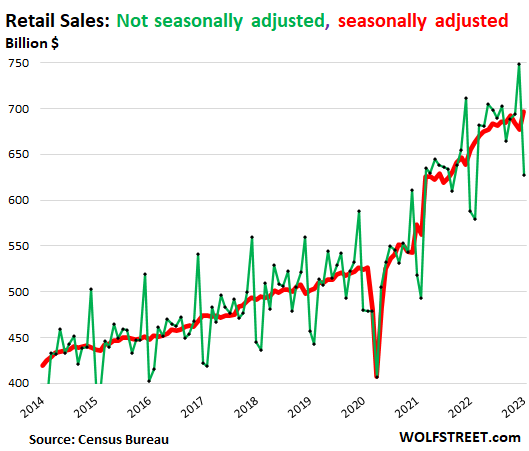

- Seasonal adjustments made December retail sales seem worse than they were: “Not seasonally adjusted, and despite the price drops, total retail sales and ecommerce sales hit records,” I wrote at the time.

- And seasonal adjustment made January sales seem better than they were. But sales were strong for a January.

Retail sales always collapse in January from December, the peak shopping month of the year. Januaries are made worse for retailers by merchandise being returned that had been bought in December (negative sales in January). This plunge in retail sales from December to January is why most retailers end their fourth quarter at the end of January in order to get the horrible month into the same quarter as the top two months of the year.

Seasonal adjustments are used to iron out those differences between December and January so that January can be compared to December: So for retail sales, we got:

- Seasonally adjusted: +3.0% in January from December, to $697 billion.

- Not seasonally adjusted: -16.2% in January from December to $627 billion. But that plunge was smaller than typical plunges during this time.

Here are the pre-pandemic January plunges not seasonally adjusted – all much bigger than the 16.2% plunge in January 2023:

- January 2020: -18.2%

- January 2019: -18.4%

- January 2018: -20.6%

- January 2017: -21.9%

This list shows that the seasonal plunge from December to January has been diminishing over the years. On top of that came the distortions during the pandemic. This makes it much more difficult in estimating what part of the month-to-month change in sales was just for seasonal reasons, to be ironed out by seasonal adjustments, and what part were for business or economic reasons, to be displayed in all their glory.

Seasonal adjustments are based on typical prior seasonal changes. So these seasonal adjustments reduced December sales by too much and increased January sales by too much.

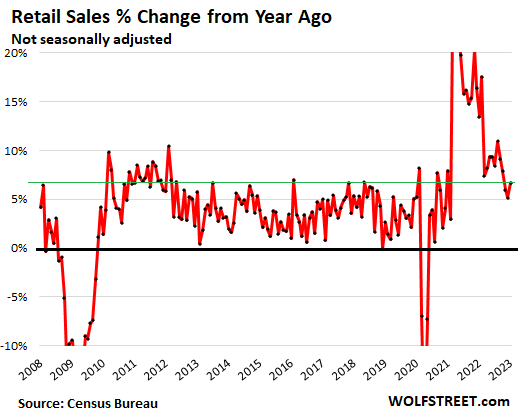

Not seasonally adjusted, and compared to the same month a year earlier, retail sales in January jumped by 6.7%, after having jumped by 5.1% in December. In other words: December 2022 was pretty strong compared to December 2021, and set a massive record of $748 billion, and January 2023 was even stronger compared to January 2022, though month-to-month sales fell 16.2%:

Retail sales by category, seasonally adjusted, to avoid headaches & whiplash.

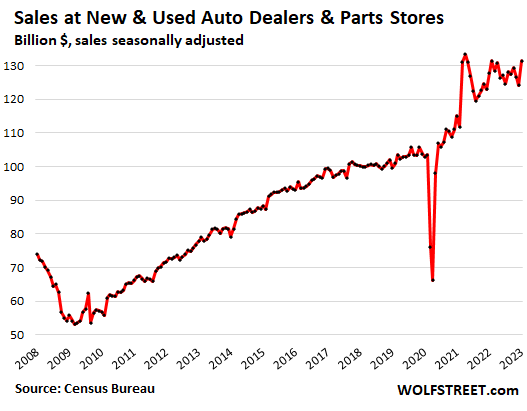

New and Used Vehicle and Parts Dealers (nearly 20% of total retail):

- Sales: $132 billion, seasonally adjusted

- Month over month: +5.9%

- Year-over-year: +2.8%%

- From January 2019: +32%

- CPI used vehicles: -1.9% for the month, -11.6% year-over-year

- CPI new vehicles: +0.2% for the month, +5.8% year-over-year.

Ecommerce and other “nonstore retailers”: Sales at ecommerce retailers, at ecommerce operations of brick-and-mortar retailers, and at stalls and markets:

- Sales: $110 billion, seasonally adjusted

- Month over month: +1.3%

- Year-over-year: +3.0%

- From January 2019: +86%

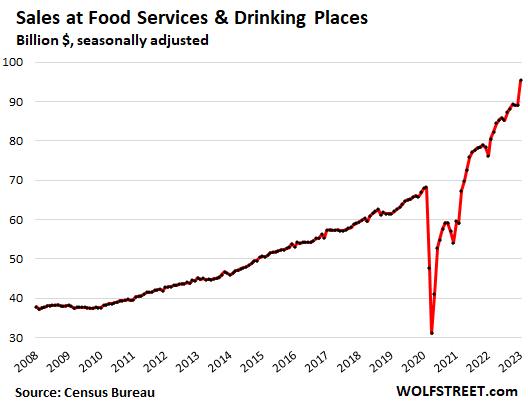

Food services and drinking places:

- Sales: $95 billion, seasonally adjusted

- Month over month: +7.2%

- Year-over-year: +25.2%

- From January 2019: +55%

- CPI for “food away from home”: +0.6% for the month, +8.2% year over year:

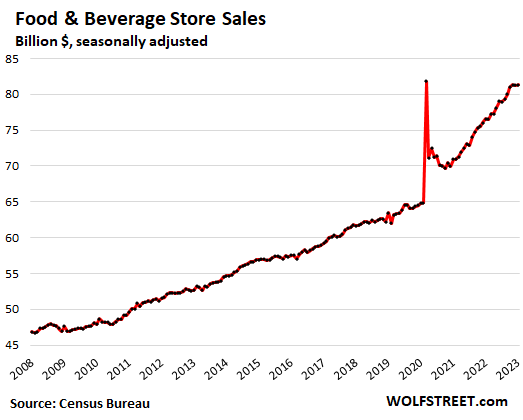

Food and Beverage Stores:

- Sales: $81 billion, seasonally adjusted

- Month over month: +0.1%

- Year-over-year: +6.2%

- From January 2019: +28%

- CPI for “food at home”: +0.4% for the month, +11.3% year over year:

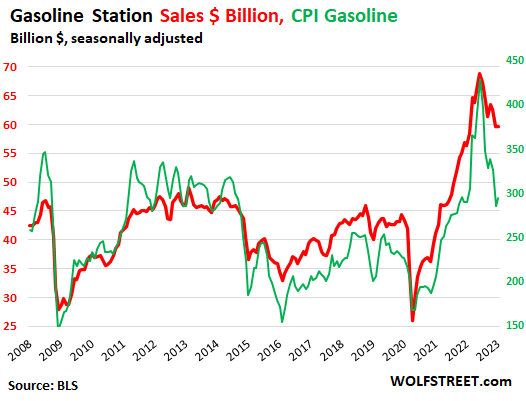

Gas stations:

- Sales: $60 billion, seasonally adjusted

- Month over month: 0%

- Year-over-year: +5.7%

- From January 2019: +49%

- CPI for gasoline: +2.4% for the month; +1.5% year over year:

This chart shows the relationship between the CPI for gasoline (green, right axis, just gasoline, not the other stuff gas stations are selling) and sales in billions of dollars at gas stations, including all the other stuff they sell (red, left axis):

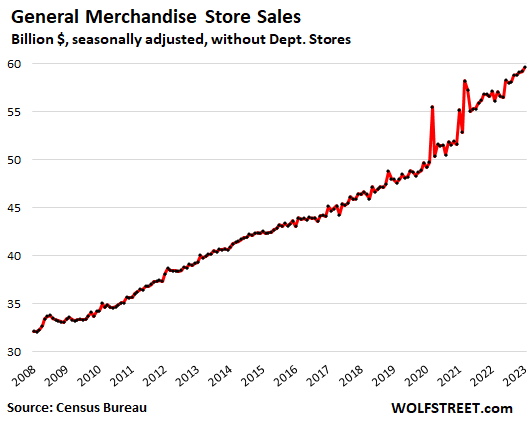

General merchandise stores, without department stores:

- Sales: $60 billion, seasonally adjusted

- Month over month: +0.7%

- Year-over-year: +4.3%

- From January 2019: +24%

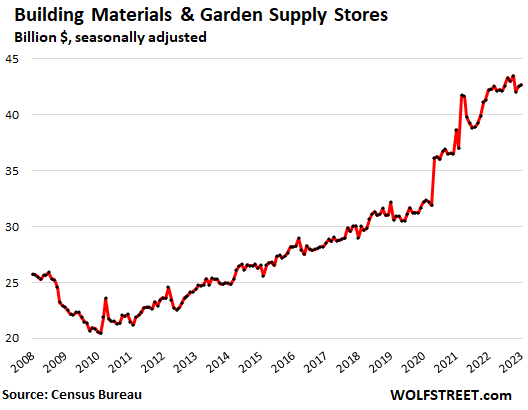

Building materials, garden supply and equipment stores:

- Sales: $43 billion, seasonally adjusted

- Month over month: +0.3%

- Year-over-year: +1.1%

- From January 2019: +33%

Clothing and accessory stores:

- Sales: $27 billion, seasonally adjusted

- Month over month: +2.5%

- Year-over-year: +6.3%

- From January 2019: +21%

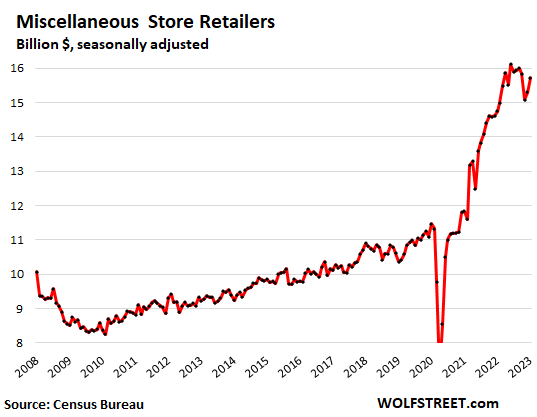

Miscellaneous store retailers (includes cannabis stores): These are specialty stores, from art-supply stores to wine-making supply stores, including cannabis stores, which are the big driver in this category as cannabis production and sales have become legal in many states in recent years, and legal sales have taken off.

But cannabis prices have plunged 19% year-over-year, per Cannabis Benchmarks U.S. Spot Index as of February 10, with booming supply grown in the US overwhelming even strong demand. This plunge in price put a damper on the boom in sales as measured in dollars:

- Sales: $16 billion, seasonally adjusted

- Month over month: +2.8%.

- Year-over-year: +6.7%

- From January 2019: +52%

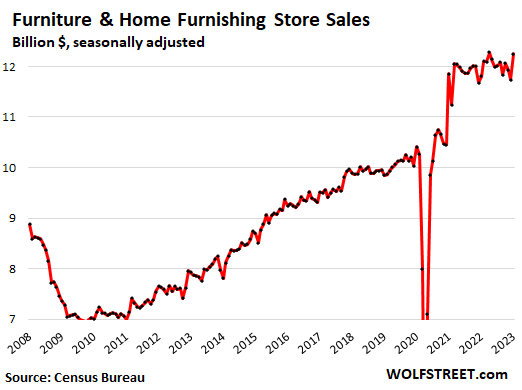

Furniture and home furnishing stores:

- Sales: $12 billion, seasonally adjusted

- Month over month: +4.4%

- Year-over-year: +3.8%

- From January 2019: +24%

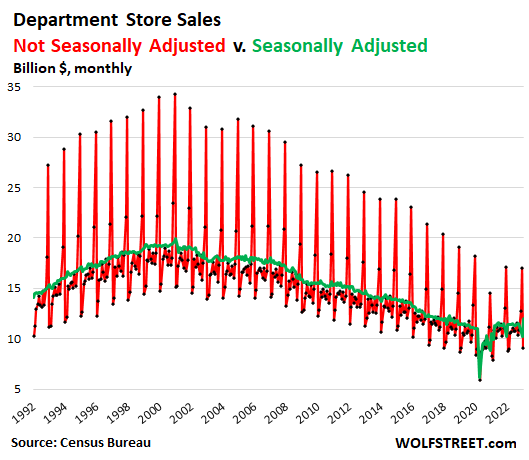

Department stores, seasonally adjusted & not seasonally adjusted. From January 2001 through January 2023, and despite 22 years of inflation, sales have dropped by 54% as consumers increasingly bought this stuff online, including at the ecommerce sites of the few surviving department store chains. For example, Macy’s ecommerce sales are included in ecommerce sales, but not here in department store sales.

Sales at department stores collapse every January by more than at any other retailer category. So here are both:

- Sales: $12 billion, seasonally adjusted; $9 billion not seasonally adjusted.

- Month over month: +17% seasonally adjusted; -47% not seasonally adjusted

- Year-over-year: +5.4% seasonally adjusted; +3.1% not seasonally adjusted.

- From January 2019: +4.7%

- From January 2001: -54%

But this 47% collapse in January from December was less than the month-to-month collapse in January 2020 (-54%), in January 2019 (-54.6%), in January 2018 (55.3%), etc. So compared to prior Januaries, this year’s collapse wasn’t as bad, and therefore, on a seasonally adjusted basis, sales jumped.

Just for a dose of whiplash, here are seasonally adjusted sales (green line) and not seasonally adjusted sales (red spike-and-collapse pattern):

Sporting goods, hobby, book and music stores:

- Sales: $9.4 billion, seasonally adjusted

- Month over month: +0.2%

- Year-over-year: +6.9%

- From January 2019: +45%

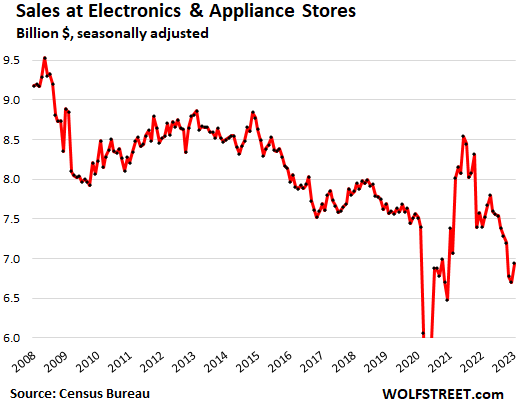

Electronics and appliance stores: Sales at specialty electronics and appliance stores, such as Best Buy’s brick-and-mortar stores or Apple’s brick-and-mortar stores. Not included are the electronics and appliance sales at ecommerce operations, at other brick-and-mortar retailers that are in a different category, such as Walmart, Costco, or Home Depot.

- Sales: $7.0 billion, seasonally adjusted

- Month over month: 3.5%

- Year over year: -6.3%

- From January 2019: -10%

- CPI consumer electronics: 0% for the month; -11.7% year over year.

- CPI appliances: +1.4% for the month, +1.4% year over year.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“Despite all the rate hikes, consumers are still flush with money”

Jerome Powell and the FED have failed by cutting back on the rate of the rate hikes. They should have kept to 75 basis points until the fed funds rate exceeded CPI. Right now we’d be 75 basis points higher and maybe eating into this speculative orgy going on in all assets, including commodities.

Never before in history has inflation over 5% come down with a fed funds rate below CPI. But we’re supposed to believe that the FED can stop at a fed funds rate of 5.5% and “hang out” for a year or more to magically cure it. They’re scamming us, STILL.

Looks like you still believe and faith on FED.

People should know for whom the FED works.

You must not read Depth Charge’s comments very often.

Depth Charge is saying that Fed is a big Failure for 99% of America. I agree.

Wolf, can’t it happen that People bought less goods and services than last January, it just costed them more in dollar terms :). It would help if we can get the truck freight volume data for actual amount of goods moving through system? For now, as markets and govt dont reference it, no one is going to rig it by running empty trucks :).

READ THE ARTICLE. Lots of details to debunk your theory.

Cass freight Index (measures volume) up 4.3% year-over-year in January. Consumers are buying!

PREACH!

“Looks like you still believe and faith on FED.”

Your reading comprehension is non-existent.

Sorry.. It was just a sarcasm.

I feel the same you feel with FEd.

Then I remind myself Fed is doing what it is supposed to be doing ie help their buddies

Fed is no friend of Americans.

Depth Charge said: “Never before in history has inflation over 5% come down with a fed funds rate below CPI.”

—————————————————-

Drunkenmiller says the same. Michael Green disputes it, saying the data says otherwise. A heavyweight being disputed by a welterweight. My research time is marginal, but if I chase it down I will report back.

Hard Landing, Soft Landing, No Landing

I’m glad we are pivoting from “Soft Landing” to “No Landing” as “Soft Landing” is an old school multi-decade fad that didn’t pan out as expected from past recessions and market collapses.

“Soft Landing” was used by MSM excessively during the Pre-GFC and the Tech Bubble. How’d that work out???

Link below is a chart of “Mentions of ‘Soft Landing’ as % of Bloomberg stories” from 1997 to present:

https://pbs.twimg.com/media/Foyhu8EWYAIT4Er?format=png&name=900×900

Interesting. We are still reluctant to pull the trigger on some expensive new machinery. Instincts are telling me the Fed policies will get their desired slowdown at some point.

Just had a chat this morning with our plant manager about our need to purchase another laser (not cheap!). Already signed the papers on another lathe. Both bottlenecks for us in the last two years making truck equipment.

The last time we bought one of each, for the same reasons, was early 2008…

“The last time we bought one of each, for the same reasons, was early 2008…”

They didn’t print $10 trillion prior to that. We have a raging everything mania right now, which is not slowing down at all. In fact, it looks like inflation is re-accelerating as is the speculative mania. The FED sh!t the bed.

Yort2 – then there’s that old title: “What Color is Your Parachute?”.

may we all find a better day.

I agree. I think the people setting these policies don’t care how long it takes to bring inflation down because it doesn’t effect them as much as the majority of the population. Powell probably never has to shop for himself at the grocery store.

Print fast, unprint slow.

Also people have been conditioned now to the idea of crisis = print money. So spend until the next crisis. Gov will suspend rent payments again, heck might even send me a check or two when it’s all said and done.

Uh when have they ever unprinted? We all know how this ends, at some point they’ll not be able to QT anymore, and then they’ll start cutting rates again and then QE again. How hard is it to understand that the country as a whole in bankrupt? Both financially and morally. Its just a matter of what crisis they gin up next? Perhaps a world war, that should take rates nice and low and give good cover for printing money.

“We all know how this ends, at some point they’ll not be able to QT anymore, and then they’ll start cutting rates again and then QE again.”

And it won’t work and we’ll go hyperinflation, and the fat cats will try to flee the country to New Zealand, Argentina, etc. Their arrogance and greed has already destroyed the United States.

“And it won’t work and we’ll go hyperinflation, and the fat cats will try to flee the country to New Zealand, Argentina, etc. Their arrogance and greed has already destroyed the United States.”

Indeed!

But at the same time, alot of people make their livings off of this morally and financially bankrupt society. Look how many couldn’t handle anything without cries for .gov to help in 2020! It’ll be magnitudes worse when the financial system crashes because that will be a true catastrophe (but also engineered by the same people who prob did 2020). Hope America has fun with its future Putin, but it’ll be a shit show before he shows up with the people begging for it by that point.

Defense contractors seem to be doing OK, in fact Congress authorized higher military spending than everyone, and I do everyone, asked for, IIRC.

From what I can tell the fat cats are fleeing to government largesse, Eric Schmidt chief among them.

YEP!

Then everyone will pile into treasuries ,which will just make us bankrupt sooner

The problem is that massive balance sheet. That is what stokes asset prices and inflation. Cut the balance sheet at twice the rate, but they cant do that because they raised interest rates. They should have just sold bond when interest rates were low and used that to force up the interest rates and force the asset bubbles to pop.

The Fed has everyone fixated on the short term interest rates, but the real issue is that immense balance sheet.

Sure they can do both. They just aren’t as worried about the inverted yield curve right now, because short-term rates are much more important than you are giving credit for. There is a massive amount of debt indexed to SOFR which is currently repricing at absurdly higher rates which absolutely will impact the general economy. Tons of privately held businesses that have debt that reprices quarterly or annually based on SOFR. Interest expense is skyrocketing at the same time the government has tightened 163j regulations limiting the ability to deduct interest payments on taxes. Interesting times we are in. This stuff just takes a long time, but everyone wants instant gratification. Every day we go without an economic blow-up is a day to be thankful for.

From NEWSMAX – NO RECESSION IN SITE

Applications for jobless aid in the U.S. for the week ending Feb. 11 fell by 1,000 last week to 194,000, from 195,000 the previous week, the Labor Department reported Thursday. It’s the fifth straight week claims were under 200,000. Jobless claims generally represent the number of U.S. layoffs.

The Fed has “gaslighted” the financial community into believing that Fed Funds (since 2009) belong under the inflation rate. The financial community was delighted to accept the deception.

As long as the rates are under inflation, the monetary condition is out of whack, false, contrived.

It’s even worse in Europe. I read quotes this week from ECB members saying their rates could top out around 4.5% and that would be enough. Their inflation is higher than ours!

‘…to avoid headaches & whiplash.’

You can say that again! 🤯

FED is the disease, not the cure. Killing the USA day by day. They purposely drive-up inflation to gut the middle class. Debt all-time highs. Wages, stagnant for years. Middle class net worth down down down. And I believe no chart published by this Admin, they change numbers to fit their narrative. Soon you really will own nothing, but you won’t be happy.

Only another month or so until Jerome Powell trots back out with his little squirt gun, and fires a piddly little quarter basis point rate hike into the raging inferno. Gee, that’s gonna do a lot. This guy is an idiot.

Rate hike and QT acts with a lag effect so they say….so far with these numbers and employment numbers…what Fing lag effect? Guess we’re see by Q4 if ballers still buying cars, houses and cruise…will be interesting either way.

For now, I will just enjoy parking my money in T Bill and use the interest to pay my rent..

Where do you buy a T-bill? Seems banks have the market cornered. Treasury direct not viable for non institution investor.

“Treasury direct not viable for non institution investor.”

What do you mean? It’s designed for retail investors. Just go to the website and open an account. No minimum amounts required.

Agree 100% I’m 64 not tech savvy,opened a account easily

$25 on I-bonds. I’ve got $20K, looking to increase to $30K next year.

Back to your article, more proof that a recession is nowhere in sight. This slow rate hikes / wait and see policy the Fed is formulating is starting to look about as iffy as the “transitory” plan was.

Yeah about as difficult to navigate as vanguard.

You can buy T-Bills through TDAmeritrade. You can purchase new T-Bills at auction. Log in, click on “Trade”, then click on “Bonds and CDs”, then click on the most recent percentage yields, then “New Issues”. There is no fee associated with buying T-Bills at auction through TDAmeritrade. I purchased some this week and got a 6 month T-Bill yielding 5.03%.

This is the same with Fidelity and E-Trade.

The retail sales numbers look strong because of the underlying inflation.

Strip out the price inflation and there’s little growth.

Wisdom Seeker,

Nonsense. Read the article. Look at the inflation data I provided in the article and the CPI article yesterday.

Inflation is now in services. Retailers don’t sell services. They sell goods.

Durable goods inflation is negative YOY and MOM.

Nondurable goods are dominated by food and gasoline. I pointed those out specifically in the article, including overlaying retail sales at gas stations with the gasoline CPI. Gasoline is nearly flat YoY. But food inflation is up.

Wolf someone told me carvana has a million car inventory, find that hard to believe. But when they go bankrupt,used car prices could implode

Maybe not.

If Carvana files for bankruptcy, the PE firms (Apollo, et al) that have bought its debts will largely control what happens in bankruptcy. They will take over the company, delete the current shareholders, get rid of some debts, and run the company as they see fit, to then sell it to the public a few years later. This is a classic PE firm bankruptcy play.

If they think that Carvana overpaid for cars, they might let those cars go back to the floorplan lenders, and they would have to sell those. Since floorplan lenders don’t want that, they are likely to work out a deal with the PE firms.

In other words, I don’t think there will be a fire sale of cars.

One thing that made me annoyed is reading that byd passed on the na market in the near term with their dirt cheap dolphin. Love to be able to buy a cheapo chinese car to tool around in for 10k after rebates, assuming byd has good lawyers.

Yeah, I know and agree, fuck china. But kind of sucks doing a trade war at the same time as people are rooting for the fed to overshoot so they can go after wages after jacking up prices, which looks like Corporate America’s consolation prize.

Anywho great article wolf! Love the breakdown. Looks like economy running a bit hot rather than any kind of landing, so I guess more pain with the fixed assets and a long winter in housing.

OH BABY!

NICE!

Hey Wolf,

Thanks for bringing clarity to topics of great complexity.

Almost every chart seems to reflect the, “pandemic,” crash, followed by the effects of the massive, “pandemic,” stimulus. The real question is, “where does this go next, when the effects of both finally fade away?”

I imagine a, “soft landing,” will find the elevated post-stimulus activity remerge with the pre-pandemic line of growth.

A, “hard landing,” will find these various lines measuring consumption blow through the previous trend lines in steeply downward trajectories.

Of the major factors at play determining our future economic trajectory, the greatest may be the point of the final expenditures of stimulus fundings by the domestic consuming population (is this the last gasp of those stimulus funds what we’re seeing above?), the rates of US interest and inflation (mostly driven by massive US debt-sparked inflation, in my opinion), and, broadly speaking, our consumption will be influenced by, “international trade and affairs,” (I’m thinking Saudi Arabia, Russia, & China as the main players affecting global energy markets right now…).

Add to these factors the economic & monetary instability of many national markets around the world, (Turkey, Pakistan, Argentina & so on…), due to rising US interest, rising inflation, and risen/rising energy costs (Whole of Europe & Japan, I’m looking at you for all the above), leads me to believe a, “very hard landing,” comparable to any of the great economic crashes in history, is inevitable for both, “markets,” (speculators) and, “main streets. (producers)”

Exactly what’s going to pop (first), when and where, are hard to gauge, but the whole “global” system is undergoing tremendous strains…

The complex intertwined nature of debt/inflation/stimulus and their ever-shifting connections to various nation’s costs of production and consumption of energy make precise predictions impossible, yet the end of the era of, “stimulus,” of low interest and high debts funding economic activity and profits (since the dot-com crash of 2000!) is at an end.

The bottom line is that Americans are going to move to the level of consumption and prosperity generated by actual production, rather than by speculative “stimulus” profits, stimulus-level interest rates, stimulus checks, and bloated, and speculative “stimulus” asset values.

Paying the costs of the party our corporate elite has been having while asset-stripping every aspect of our country for the last sixty years is going to be very very costly.

Very Hard Times Ahead, Indeed.

Oh, I forgot to add the punch line:

We are either going to pay up through extreme interest rates or extreme inflation. Either way we are going to pay the piper… pick your poison…

I think it is already clear: Extreme Inflation.

The real inflation on ground is much higher than what the govt reports.

“real inflation on ground is much higher than what the govt reports.”

Welcome to your “Chinese” government , and the set of statistics that they provide to the people.

Jon,

Agreed

Inflation is running over 10% right now, probably close to 15% for most people and for most items. I’ve got the receipts to prove it. I don’t believe the government figures. One example: Deer Park bottled water went from $159 to $2.29 for 101 ounces. Cranberry juice $350 to $419 for 64 ounces.

There is one important thing to understand. The debt ceiling impasse means that the Treasury is using other means of financing the debt instead of raising funds by selling bonds. This reduces the supply of bonds in the market. This is offsetting the decline in the balance sheet to some extent, so what we have is a Fed that really has barely even begun to impact the supply-demand relationship in financial debt markets with QT. (Crowding out of debt markets by central banks also props up the equity markets).

The lack of political agreement means this will continue for another 4 months, so it is possible that the financial market bubble grows even bigger during this time.

Last time this happened the Treasury sold alot of bonds right after the debt ceiling was raised and interest rates shot higher and stock prices started on a decline. My guess is the next time will be much worse because inflation is not dying and the Federal Reserve is tightening. When the TGA stops declining and the Treasury must sell alot of bonds at the same time the Fed is selling assets, that is the triple whammy.

“…that the Treasury is using other means of financing the debt instead of raising funds by selling bonds.”

This is not what the Treasury does. The public bond auctions are proceeding as scheduled, and publicly traded Treasuries are issued as normal. Supply of bonds continues as normal.

Instead, the Treasury stops issuing the special non-marketable Treasury securities to gov pension funds, the SS fund, and other funds for the contributions their members made. So it spends the incoming contributions, but doesn’t issue the non-marketable Treasury securities to those funds. Then on the day the debt ceiling is lifted, it issues ALL those non-marketable Treasury securities to those funds ALL AT ONCE in one day to make them whole, and the US national debt officially jumps by $500 billion or whatever in one day. Same thing every time.

So retail sales, which is not adjusted for inflation, is up 6.7% YoY not seasonally adjusted. CPI-U went up 6.4% YoY not seasonally adjusted. So it’s flat. More fake good looking numbers for headlines for the fake economy.

BS. READ THE ARTICLE.

I’m so tired of this drive-by BS.

I did. The problem is there is no easy place to find retail sales CPI to adjust for it and all they do is report nominal changes and disregard underlying inflation. Then to make matters worse they apply seasonal changes as if each year the seasons are similar when they can also be very volatile. At any rate, nondurable CPI is 7.5% YoY whereas durable like you said is down YoY. The media headlines again making the numbers look better than they really are, which was my point.

You clearly STILL didn’t read the article because I spelled it out for YOU!!!

I gave you the CPI for durable goods, including vehicles, electronics, appliances, plus food and gasoline… those are the major retail categories, and I gave you the CPI numbers for each those!!!

I even gave you the yoy plunge in prices for cannabis, per private-sector price index, with cannabis retailers being the driver behind the surge in sales at miscellaneous retailers.

I told YOU in the article that inflation has moved into services, that many goods prices have dropped, and that retailers don’t sell services but goods.

Mr market doesn’t see this as a problem. What a hoot.

Bond market sure did, LOL. 10-year now at 3.82%. up from 3.38% a few weeks ago. What a hoot!

Mortgage market sure did, LOL. 30-year fixed mortgage rate back at 6.75%. What a hoot! Up from of 5.99% a couple of weeks ago, LOL.

Mortgage rates needed the wake up call. I’ve seen offers over the past few weeks for “buy a house with us now and no-cost refinance with us within the next 2 years” – I think they are trying to convince people they will be able to refinance to 3.0% next year or something.

I think I am starting to understand what is happening in the markets.

Mr. Market is in the middle of a upside bubble that is driven by small investors and hedge funds and traders. They all see assets that look to have bottomed and are positioning for upside. Some of the hedge funds also were forced to cover short positions.

The proximate cause of this is the fact that there is a debt ceiling battle upcoming so it is likely the TGA will decline to almost zero before this is resolved. That will reduce the selling of bonds into the market, which has the opposite impact of the QT by the Fed. So the amount of tightening that is really hitting the markets right now is very minimal. Sure short term rates are higher, but long term rates and credit conditions are no tighter than they were many months ago (approximate).

The longer term investors who like security are not buying this rally, or they are increasing equity weights, but will sell off increased exposures as soon as there is a downturn, leaving the small investors to once again get their accounts cleaned out. But this time, things will get really bad and even the large companies like Apple are going to see alot of downside in their equity valuations.

But it is possible this rally extends longer.

“So the amount of tightening that is really hitting the markets right now is very minimal.” Until that G fund piggy bank Wolf spoke of has no funds remaining, that can be interest suppressed by yellow stain.

Mr. Market has been down a lot lately.

It is all perfectly rational. When the FED, or a central bank, or a country makes its money worth less, then people or entities that would otherwise save will instead more freely spend.

We stopped buying big ticket items, but we are still buying trifles, little things, like a Turkey sandwich, or x2 bloody mary, because real disposable income per capita reached Feb 2020 level, after pricking the bubble.

Bloody mary recipe : sliced beets, 1/2 sweat potato, 5/6 potatoes, red cabbage, 5/6 carrots, 5/6 vine tomatoes cut for scalping, 4 celery, 3/4 betternut squash 1cm tires, onions – no rice, no oil – dumped in the InstantPot.

Bloody mary for life !

You forgot the double shot of vodka in your recipe

A double shot in that receipt is like…idk something really small in something really big that will have no effect. You would need a pint and a half (500ml) at least if not a 750ml. This talk of bloody Marys had me wondering if Zeitgeist is still around?

Not even close ME:

”REAL” BldMry recipe,,, ( of course not the one used by bars for ‘suckers’ )

Take at least a one pint canning jar, preferably at least a 1.5 or quart,,,

Add at least 4 ounces of vodka, preferably 6 or more.

Add an ounce or two of tomato juice, ( or some prefer V-8, ) and a good dose of THE best clean and organic ”hot sauce”.

Add ice and shake well…

Garnish with a bit of something green. OR NOT!!!

This from many ”old and older folks” I knew who were very well accustomed to what used to be called, ”drinking to excess” each and every opportunity and still went to work at least somewhat sober Monday morning…

Others, per their reports, NEVER went to work sober any day, and used this recipe to ”sharpen up enough” to do their assigned daily tasks.

Including, to be sure, Winston Churchill and FDR,,, and very likely many others with very much less publicity to their daily habits.

The inflation response switch has been flipped on for many people. People see no point in saving additional dollars when those dollars are continuously made worth-less.

Buy a good time for the family, when a good time can be had. Tomorrow you may be forced to eat mud for what those future dollars may buy.

Thank you Greenspan, Bernanke, Geithner, Paulson, Yellen, Powell, the FED, Clinton, Bush, Obama, Trump, Biden, and most of Congress and many assorted banker and financial types.

I used to be a fairly one-sided politically minded person…

As the years and now inflation and my financial positions (essentially nothing of note) roll along, I could not have summed up my thinking any better than you have with this post.

It truly has made zero difference who’s been running things. One guy gives away the economy to the neck-tattoo class, the other guy tees it up for his conglomerate CEO buddies from Augusta National.

Doesn’t seem to be much point in it these days.

Ironic, that we should spend away before cash becomes worthless, and resulting in feeding the furnace of inflation. A cash burn economy totally designed by the cornered Fed.

If the US consumer is facing real term cuts in pay, then they should be less real consumption than before not more, irrespective of nominal increases.

This imo is why the Fed should have -first- done QT before raising interest rates. Raising interest rates to slow consumption, ok, but the people that you slow the consumption of, are also collectively the producers. This is knocking out consumption and production i.e. its tantamount to shrinking the economy. This just comes back to the idea that recessions somehow cure inflation, when there are many examples of this approach leading to stagflation instead.

The problem is too much money. The Fed should follow QT and the US government should reduce spending, however the latter won’t happen. Certainly its true that inflation can’t be considered to be reliably reducing. This is now 2 years in and as Volcker basically did, this ends witha devaluation of the dollar. Its going to be a 20% loss of value fairly soon and in such a short time.

@ Lord Sunbeam –

Regarding FED actions – well you can’t cure stupid, or mal-intent, whichever the case may be ………

They passed the 20% dollar devaluation, at least in domestic purchasing power, long ago.

Covid stimulus was a instant 25% devaluation of dollar,printing press running full speed,7.5 trillion = bankrupt

The last time there was a “soft landing “,was when Neal Armstrong stepped foot on the Moon in July 1969

I believe retailers included January in the earnings quarter because January is the month where they can reduce their inventory to the minimum. Late December and early January have sales so Holiday merchandise is gone by the time January ends. Sales and returns are not a factor as gift cards have transferred some Holiday spending to January.

“Sales and returns are not a factor as gift cards have transferred some…”

Nonsense. READ THE ARTICLE. At least look at the first picture if you cannot read, for crying out loud.

Not seasonally adjusted sales plunged 16% from December for all retailers and plunged by 47% for department stores (but those plunges were less than in prior Januaries).

Why do people post these drive-by nonsense comments without reading the article or even looking that chart?

Wolf,

Sometimes even the pictures look funny especially to someone with a red/green deficiency. Please don’t begin using yellow.

Three things I noticed sales at food and beverage is accelerating. Less cooking at home.

Food and beverage has leveled.

Sales at gas stations have increased the separation of gas from incidentals. Incidentals now includes items like milk and drinks along with motor oil. So in January they sold more food and snacks than gasoline. The decrease in gasoline I understand but are people eating more at stations?

“Why do people post these drive-by nonsense comments without reading the article or even looking that chart?”

Article? Chart? There was one?

LOL. Yes, I feel that way sometimes.

If you scroll fast enough past the article charts to get to the message section, and you blur your vision slightly, AND most importantly are heavily medically and/or recreationally medicated, there is a hidden article summary:

Positive economy = Christmas decorated staircase constantly flowing upward to heaven (Fed angels optional)

Negative economy = Christmas decorated staircase constantly flowing downward to hell (Fed demons optional)

Caution: Don’t scroll backwards as Satan lives there…

It’s a shame that the Century 21 Stores in New York City went under a couple of years ago.

When does the rampant inflation kick in again on used homes?

Aside from new tv sets, its about the only thing deflating.

Won’t happen. For every 1% rise in mortgage rates there is roughly a 10% decline in the amount that can be borrowed for a fixed level of monthly payment. Since most people are limited by the monthly payment amount, house prices must fall to equilibrate with the new rate levels. For example, with rates rising from 3 to 6.5 percent, the amount that can be borrowed for a fixed level of monthly payment goes down by roughly 35% using the 10:1 rule of thumb. That is an enormous blow to the housing market. Prices will be cratering for s9me time to come.

equilibrate – i actually thought this was a made up word, a combination of equilibrium and calibrate, but it is real.

socal – i thought you were a housing market bubble denier in the past?

That was SocalJim.

Thanks Wolf. Yes, I do believe the housing market is a tad out of whack.

The chart on Wolf’s previous article, CPI OER vs CS Home Price Index, seems to imply that home prices must come way down or rents must go way up. Or some combination of the two.

Animal spirits, dancing in the streets! Can these giddy free-spending Americans launch themselves into longer-term prosperity by some kind of perpetual motion feedback machine, with higher consumer spending looping back through wage gains to keep them aloft? In the face of higher interest rates? Or will it all get way out over its skis?

This makes me think of Wile E. Coyote blowing into his “sail” as he stalls and looks down at the canyon below.

You were onto something with the remark about animal spirits. What you’re seeing in consumer behavior is a backlog of widespread boredom relief; the party at the end of the world. When the world fails to end — well, who cares anyway. It was fun not wringing our hands for a bit there while we thought it was ending.

¡Roaring twenties!… Again

More like snoring…I’m trying to sleep my way through this madness

Opposite. Many with enough dollars see it counter productive to save more dollars in the face of continuous dollar debasement.

The outlook has switched for many, and actions follow outlook.

This fits with what I see around me. Packed stores and restaurants, most house listings under contract in days, home reno contractors backed up, and everybody is traveling. I see no impact yet from the fed hikes except a positive one on treasury and CD rates, which might be adding even more money to consumer pockets.

The question is when does services inflation come down? Has the FED really done enough, to raise 50-75 more bps and sit for the rest of the year?

Of course they haven’t done nearly enough. There’s a raging mania everything bubble which continues, unabated. They failed to read the tea leaves or do any remedial math – or worse, willfully chose to ignore all the information – and started to cut back on their rate hikes too soon.

The FED has mathematical models rivaled by few. They are obviously depending on these models (God help us – all models are wrong; some are useful). But are they sharing those model outcomes? Why not? Slightly off topic but I can think of 2 other recent scenarios when governments heavily used computer models to drive policy. And had no hesitation in sharing the predictions.

Equity buyers apparently in no mood for one either.

Getting in the mood?

“Despite all the rate hikes, consumers are still flush with money”

Look, all I’m saying is I have a great solution for this. Email me for my Venmo account name!

Paypal is also fine.

CashApp too.

/crosses fingers

Has the Fed considered accepting defeat on inflation? With minimum wage climbing it seems higher prices will be baked in. My grandparents told me that once a high price is set – it does not come down. So, should we anticipate the CPI will never hit 2 again. What number would be normal?

What the FED is saying versus what they are doing are two different things. They don’t want inflation to come down quickly, they want a new higher floor in asset prices, and for inflation to devalue large debts. This is all 100% intentional. There’s no way it couldn’t be intentional with all of the economists they employ.

I’m starting to agree. And the 28 year old who saved $100k to try to buy a new house and now sees it out of his reach, well he’s just collateral damage. Protecting the portfolios of the boom generation is the most important!

“We’re not even thinking about thinking about raising rates.”

“We’re going to let the economy run hot for a while.”

“Inflation is transitory.”

“Inflation is transitory.”

“Inflation is transitory.”

“Inflation is transitory.”

“Inflation is transitory…..”

“Soft landing.”

“Disinflation……”

Oops? I think not. They’re gaslighting. The FED is the abuser. I think the conversation now turns to ending the FED as we know it. We should start talking about prison sentences, financial clawbacks and all sorts of other things.