Hangover after a drunken party instigated by the Bank of Canada’s money-printing and interest-rate repression that turned buyers’ brains to mush.

By Wolf Richter for WOLF STREET.

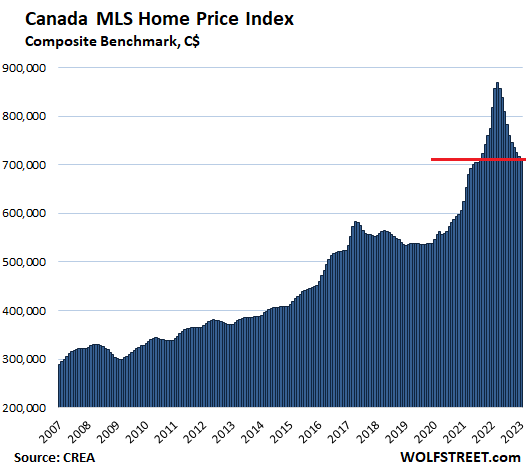

Home sales in Canada plunged by 37% in January, compared to a year earlier, amid rising inventory. Home prices dropped by 0.5% in January from December, by 12.6% year-over-year, and by 17.8% from the peak in March 2022, the 10th month-to-month decline in a row, according to the Canada Composite Home Price Index by the Canadian Real Estate Association (CREA).

At C$713,700, the Composite Benchmark Index for all types of homes has now plunged by C$167,400 in 10 months to the lowest level since August 2021.

This is the hangover after the drunken party instigated by the Bank of Canada’s money-printing binge and interest-rate repression. It started in March 2020, instantly turned buyers’ brains to mush, and lasted until March 2022, when the BoC’s lift-off rate hike took away the booze.

Over those 10 months since lift-off, the BoC has now raised its main policy rate by 425 basis points to 4.5%. After the January meeting, BoC Governor Tiff Macklem said that the BoC would pause to judge the effectiveness of the rate hikes and think carefully about the next steps. But with inflation still at 6.3%, “the question really we’re asking ourselves is, ‘Have we done enough?,’ We’re pausing to assess whether we’ve done enough,” he said.

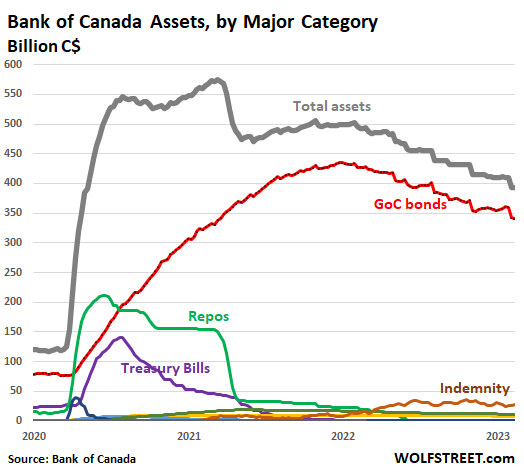

The BoC started QT long before the Fed and has by now shed 32% of its total assets (gray line). It has trimmed its Government of Canada bonds by 21.5%. It has gotten rid of nearly all its other assets. It started warning about the housing bubble in the spring of 2021 when it began unloading assets:

Unlike the US, Canada’s housing market blew through the Financial Crisis with just a few feathers ruffled and then entered one of the world’s biggest housing bubbles.

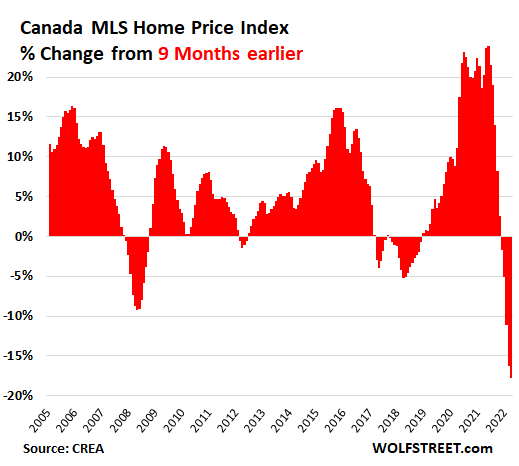

In terms of home prices, the 10-month drop of 17.8% was by far the deepest and fastest 10-month drop in CREA’s data going back to 2005. But this is now a real housing bust in the making. Homes are being repriced on a large scale from ridiculous highs:

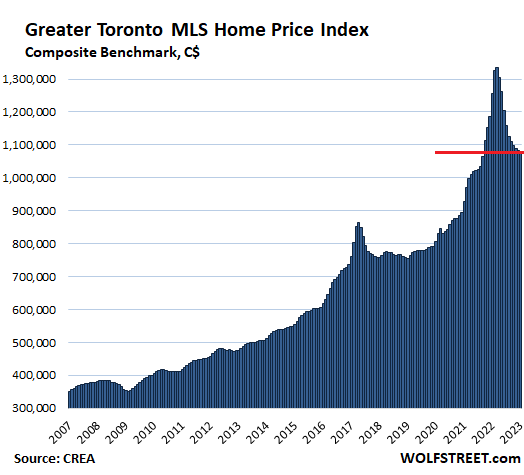

Greater Toronto Area: The MLS Home Price Index composite benchmark price declined 0.2% for the month to C$1.079 million:

- From peak in March 2022: -19.2%

- Year-over-year: -14.2%

- Drop in 10 months from peak in March 2022: -C$256,100

- Jump in 10 months to peak in March 2022: C$316,500

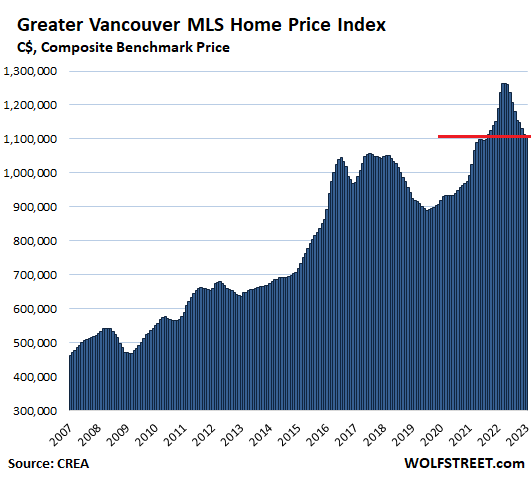

Greater Vancouver: The MLS Home Price Index composite benchmark price dropped 0.3% for the month to C$1.11 million:

- From peak in April 2022: -12.1%

- Year-over-year: -6.6%

- Drop in 9 months from peak in April 2022: -C$153,300

- Jump in 9 months to peak in April 2022: +C$169,700

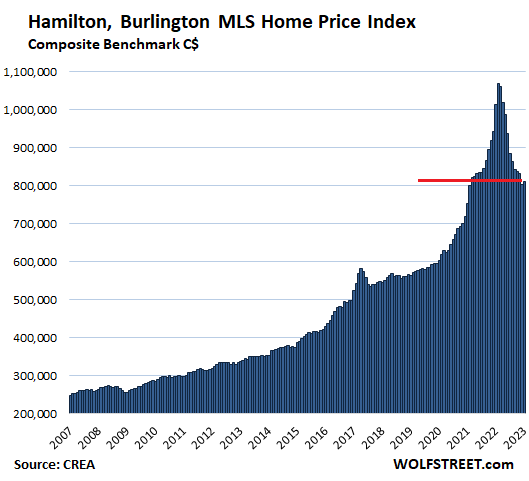

Hamilton-Burlington metro: After plunging 3.3% in December from November, and by about 25% from the peak in February 2022, the MLS Home Price Index composite benchmark price rose 0.8%, to C$809,800.

From the beginning of the Bank of Canada’s money-printing binge in March 2020, the index had spiked 70% in 23 months. And so far, over those 11 months, home prices plunged faster (-C$259,000) than they’d spiked during the last 11 month of the run-up (+C$248,300).

- From peak in February 2022: -24.2%

- Year-over-year: -20.0%

- Drop in 11 months from peak in February 2022: -C$259,000.

- Jump in 10 months to peak in February 2022: +C$248.300

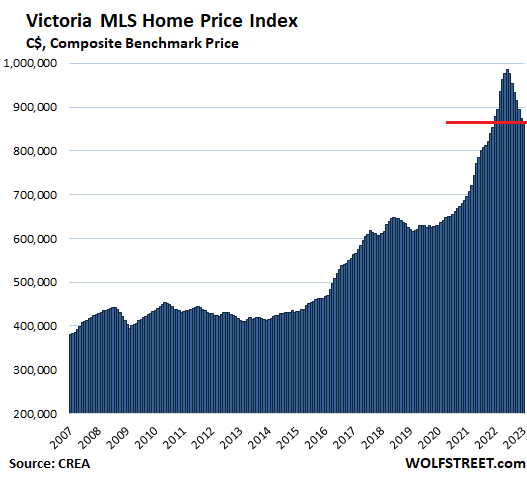

Victoria: The composite benchmark price dropped by 0.7% for the month to C$866,700:

- From peak in June 2022: -12.0%

- Year-over-year: -1.3%

- Drop in 6 months from peak in June 2022: -C$118,800

- Jump in 6 months to peak in June 2022: +C$164,300

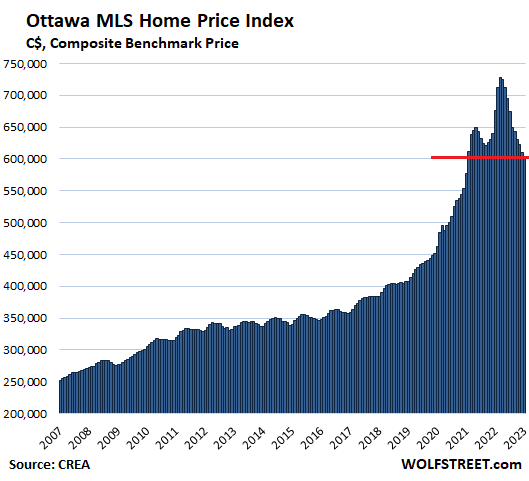

Ottawa: The composite benchmark price dropped 1.1% for the month to C$603,900 – the lowest since February 2021:

- From peak in March 2022: -17.1%

- Year-over-year: -10.7%

- Drop in 10 months from peak in March 2022: -C$124,300 – going down far faster than up

- Jump in 10 months to peak in March 2022: +C$78,800.

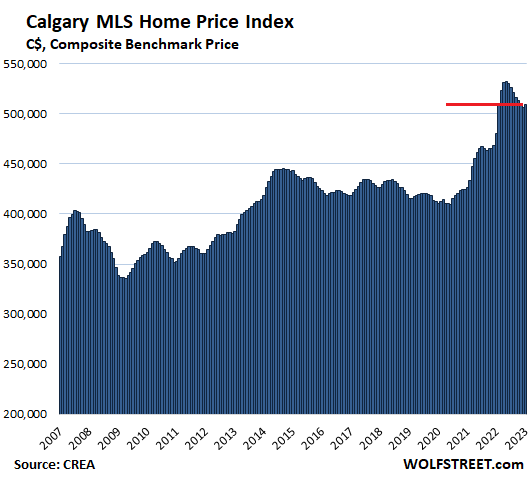

Calgary, Canada’s oil capital: The composite benchmark price rose 0.7% for the month, after seven months of declines, to C$509,900:

- From peak in May 2022: -4.2%

- Year-over-year: +6.1%

- Drop in 8 months from peak in May 2022: -C$22,300

- Jump in 9 months to peak in May 2022: +C$68,900:

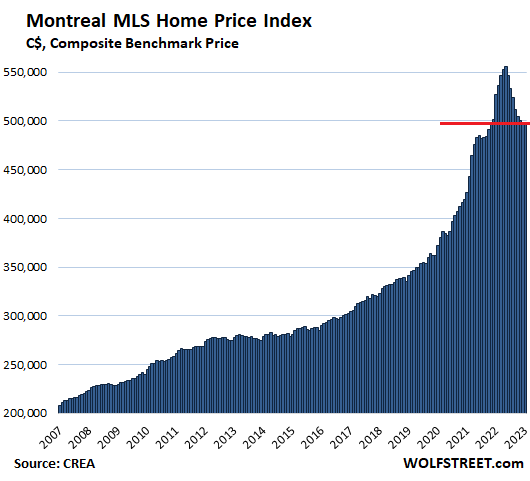

Montreal: The composite benchmark price was unchanged for the month at C$498,000:

- From peak in May 2022: -10.4%

- Year-over-year: -5.5%

- Drop in 8 months from peak in May 2022: -C$57,600

- Jump in 7 months to peak in May 2022: +C$71,800:

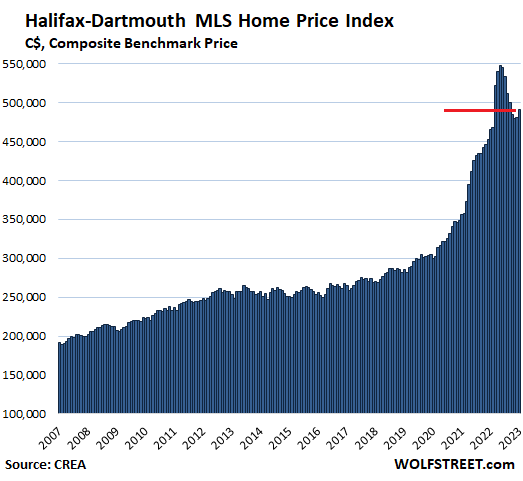

Halifax-Dartmouth: What happened was just nuts. From February 2020 to the peak in May 2022, the benchmark price spiked by 81%, before it began unwinding.

The composite benchmark price, after huge plunges late last year, jumped by 2.1% in January from December, to C$490,700.

- From peak in May: -10.4%

- Year-over-year: +5.4%

- Drop in 8 months since peak in May: -C$57,100

- Jump in 8 months to peak in May: +C$113,100:

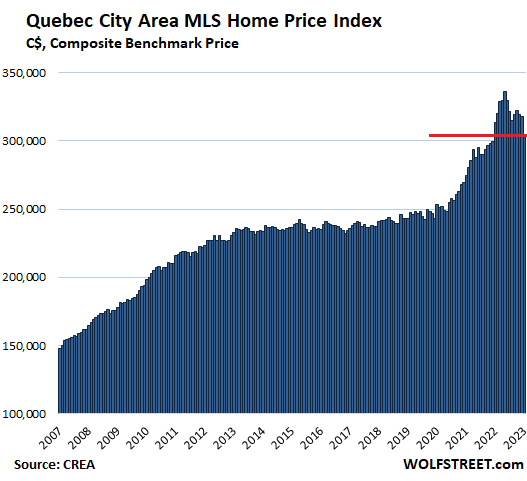

Quebec City Area: The composite benchmark price plunged by 4.2% for the month to C$304,800:

- From peak in May: -9.3%

- Year-over-year: -2.8%

- Drop in 8 months since peak in May: -C$31,200

- Jump in 7 months to peak in May: +C$42,500:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Yes you nailed it. There is now a punitive tax on unoccupied vacation dwellings and an outright attack on foreign buyers and owners including Americans. The US congress is now thinking of retaliating against the 500,000 Canadian homeowners in FL alone. And tons more in other states. This will get messy. It’s getting out of control.

The “attack” on foreign buyers has more holes than swiss cheese. The legislature is more about optics and politics, there wont be a real impact for most.

True that but figuring out the holes is a real legal problem. Also there is a $5k fine for not filing the annual paperwork which alot of foreigners don’t even know exists. And the penalty for not proving occupied is one percent of appraised value, that’s a big bill. You mess up and you’re going to get clobbered. That’s where the housing bubble affordability has gotten to.

That’s true but we’re finally seeing prices in Vancouver and British Columbia tank since January the 1st due to law outlawing foreigners or more to the point the Chinese from buying.

Ouch.

Most Canadians with homes in Florida rent them out. Short term property rental in Fla is a widespread and lucrative business, even with the cost of professional property management.

Also, why are the charts above all using different date spreads to show swelling/receeding prices? Makes for misleading comparisons across regions.

Dre,

“… why are the charts above all using different date spreads to show swelling/receeding prices? Makes for misleading comparisons across regions.”

LOL. Are you vision impaired? Or just a lazy troll? My guess is the latter. If you’re vision impaired, I apologize in advance.

All blue charts, which track the benchmark prices across the metros, which you reference, start at 2007. ALL OF THEM. Same identical “date spread” for all of them.

The second chart reflects the BOC’s balance sheet assets, NOT home prices. If you can read, you can see that in the title of the chart. It goes back only to the beginning of the Money Printing cycle, which started in March 2020, and so the chart starts in Jan 2020. This has to be that way to show how the various assets on the BOC’s balance have moved.

The third chart, red, reflects year-over-year national benchmark price changes. It goes back to the beginning of CREA’s data to document my statement that “…the 10-month drop of 17.8% was by far the deepest and fastest 10-month drop in CREA’s data going back to 2005.”

If you’re going to troll, at least don’t be stupid about it. As you can tell, I allow some trolling. If it’s stupid trolling, I might still allow it, but I take out my trusty double-barrel 10-gauge goose gun and shoot it down.

Wolf, you throw the word bubble around but all I see is a correction and not a bubble collapse. You need to quantify how much the housing collapse when a bubble bursts, 60%, 80% or more. Perhaps, back to 2015 prices when you started calling a bubble or back to 2007 prices. Readers need to know what your bubble deflation price is.

A “bubble” is on the left side of the mountain, when prices inflate beyond a reasonable level. A “bust” is on the right side of the mountain, when prices are being returned to a somewhat more reasonable level.

When the typical measures of wages or salaries rise by 3% a year, home prices might increase 3%, and that would be reasonable. If they spike by 10% or 20% or 30% in a year when pay rises 4%, then that’s a bubble.

If pay rises 3% a year for 20 years, and home prices rise by 6% a year for 20 years, that’s also a bubble after a while — but not right up front.

Canadian retirees use them as winter homes, same as retirees from the northern states. Some communities have restrictions on short term rentals. This shuts out Airbnb hosts wanting to let short term rentals for hundreds of dollars a night. The hurricanes are becoming more severe. The barrier island beach front community of Ft. Myers Beach was inundated by a fifteen foot storm surge during hurricane Ian. People drowned. Many flooded homes were filled with mold and have ben abandoned. Federal flood insurance has been losing money for years.

David Hall,

Your like a person that moves to California and is shocked by earthquakes. Or Michigan- coldest ever!!!!

Just stop already. Florida gets hurricanes. Low lying areas flood. Poorly built structures get ruined. Pretty sure this hasn’t changed in the last 8 millennia.

Yikes – somebody is touchy. You misunderstood my question.

I challenged your interpretation of the data you presented, not the data.

Your rise-to-peak horizon is:

Tor: -9 mos.

Van: -10 mos.

Ham: -11 mos.

…

Same inconsistent horizons on drop-since-peak.

My simple, and perhaps naive, question is why not present the same time horizon for all markets?

Granted the peak may have occurred on different dates for each market but why extend your analysis an extra month for Toronto versus Vancouver?

I call BS.

None of them that I knew rented them out in FL. Same w/ US families from NY, MI, NJ, etc

One family had previously rented but, “Golfers destroyed the hardwood floors.” so they quit.

(To me use that $18k+ rent and replace the floors but w’e).

They sit empty 9 months a year. These range from $500k-900k. Sitting empty.

I’m sure there are multimillion+ homes empty and I just didn’t know the families.

These same people also pay ~$1500 a month for a country club/beach club membership. Once again, used 3-4 months a year.

Typically grandma/grandpa own it and the whole 3 generations come down.

TLDR – They don’t rent them and piss away tons of money.

It’s about time! Canadians have been attacking Florida with wearing knee-high dark socks, shorts and open Birkenstocks for decades.

Murica!

Funny as heck, “But we love that golf course”. Not as bad as the carpetbaggers from New Yawk. Lots of resentment from that.

Florida already has a higher property tax rate for owners such as Canadians, so Canada’s measures are the retaliation.

The U.S. Congress’s further contemplated measures would be ESCALATION, not retaliation.

Florida does not have higher property tax rates for Canadians. What it does have is a Constitutional cap on yearly increases that only apply to residents (meaning more than half the year spent in Florida).

If a Canadian lives in Florida full time, he gets the same tax benefits that Americans get.

True but property tax is based on full time residence, which is forbidden by immigation laws for foreigners. The Homestead Exemption which is 1/4 the regular tax does not apply to transients, only citzens or green card holders. It’s a big differnce. If you live in a coastal area your homeowners insurance is skyward to over $1k per month regardless of status.

“True but property tax is based on full time residence, which is forbidden by immigration laws for foreigners.”

Sure, that’s fine, but his post made it seem like Canadians were singled out for persecution by the Florida property tax regime. That isn’t the case. If you don’t live in Florida full time, whether because you’re not a permanent resident or because you spend the other 8 months of the year in Michigan, you don’t get the homestead exemption.

And the homestead exemption is not necessarily 1/4 the regular tax. It’s $50,000 of assessed valuation if I recall correctly, meaning that it’s only going to be 1/4 if your house is $200,000 or less, which isn’t the case for much these days.

that’s the same for a foreigner in Canada. 6+ months makes you a resident. the new taxes don’t apply.

The U.S. is trying that with Chinese too. The problem stems from the fact that the U.S. arrogantly and foolishly thought that it could export its inflation. All it had to do was print trillions of dollars, and people overseas would be thrilled to hold it.

But as Augustus Frost says here all the time, currency is ultimately a claim on the assets of the country which issued it. They are holding dollars BECAUSE of what it can buy in the United States. If you start putting in all sorts of restrictions on what it can buy, eventually, people won’t want to hold it as much. That jeopardizes our reserve status, in the long run.

Most countries don’t allow foreigners to own property. It causes nothing but trouble.

no real restrictions in europe. and you get 10x more value for your money. Beautiful weather, infrastructure and food. Quality of life is very bad in Canada but they are in a propaganda bubble like Russia to not depress their poor citizens further.

No restrictions on Americans buying recreational properties in Canada.

Canada does not have a 30 year fixed mortgage, floating month to month has worked well over the last 20 years as rates dropped, we will see now. Unemployment is still very low with a large amount of legal immigration keeping up the need for more housing. Many people have seen a double in house prices in last 5 years so equity is high.

You could be forgiven for thinking that these were charts of crypto currencies in the early stages of a correction. One blow off top after another.

However, when I look at property prices in Canada, I notice that there are only decreases in the upper and parts of the middle segment, but no decrease in the lower segment.

For example, Montreal 2017 and 2018 had many listings up to 200k cad, those listings are now only 15 for greater Montreal.

I live in the suburbs of Montreal, a 1/4 acre empty lot (no house) costs about 250-300k….insane!

Like all over the world, the middle class sellers are trying to get rich by driving up property prices to the point where they are no longer connected to the fundamentals. At the expense of this, however, the number of transactions is collapsing everywhere. In the case of Montreal, deals are down 38% and I think that will continue until either interest rates or prices collapse. In my opinion, central banks will not allow hyperinflation, therefore prices should fall. If not, there simply won’t be a market

That’s in Canadian pesos. If you do the conversion, as most readers are Americans, it’s around 150K US$

Per internet $1 CA = 0.74 * $1 US

So if $250 – $300k is right that’s about

$185k – 225k US.

Speculation: a larger percentage of Canadians live in their 10 largest cities than in the US.

Seven of the largest Canadian cities have metro population of about 17.2 M. Total Canadian population 38 M. So about 45% of the population.

The largest seven US cities have metro population close to 70 M. US population about 332 M.

About 21%.

Does this make a difference ?

I dont know but its a pretty significant difference.

B.t.w I live in eastern Washington state, US citizen. If you want a good look at the Toronto RE market, Team Sessa provides concise weekly uTube reviews of its market. There are considerable uTube RE presenters of varying quality.

Very minor update: the 17.2 M is actually just from the 6 largest Canadian cities, not seven. Add in the 7 th and they are about 47 to 48 % of the entire population.

Versus US 21% for the 7 largest.

In all of these cities and their US counterparts, over the next 12-18 months, there needs to be a repeat of the same level of price reductions for there to be meaningful movement towards housing affordability. 2.5X would be better.

As for the US, the MOST important outcome, if a real recession arrives in the next 12-18 months, is for there to be no governmental intervention in terms of mortgage & rent relief.

Otherwise, America is screwed. Absolutely nothing else matters. Like our society, we either turn away from the EXCESSIVE wokeness and stop this MMT-based management of our economy, otherwise we’re facing an extremely challenging next 10 years. Inflation, deficits, interest expense cost, SSTF viability, Medicare expenses & a sooner rather than later pension crisis are the major issues that loom large over the horizon.

The CBO just reported that we’ll add $19T in debt over the next 10 years, putting us in excess of $50T. That is just sobering & mind boggling all at once. The annual interest expense should push towards at least $900B as tax receipts continue to slow as the economy moves further towards stagnation in the later part of ’23.

The day has come that deficits matter again, BIG TIME!

Goods points.

I think the real issues is the monopolies in the U.S. The rich get richer, the mom and pops businesses cannot compete so you lose the middle class as they drop down into the lower class. Some of the middle class stays in the middle class if have a Government job or one of the few who can still own a business or is in management in a monopoly. But if you end up a worker bee at Walmart or Amazon or Autozone or Target, etc. You will probably never be in the middle class.

The government will continue to take on debt for transfer payments to the lower classes to keep them somewhat happy in their apartments they rent but home ownership for this group is down to 17% and dropping.

The fed could push against this by selling mbs, force price discovery and I’d suspect as those bonds are redeemed non performing mortgages get foreclosed pushing more housing onto the market and expediting a necessary correction.

The capital class owns these mbs, along with various pension funds I may assume.

Just my supposition.

But, trying to achieve more equity by just driving rates up seems a very blunt tool that discourages all real estate transactions slowing the necessary correction negatively impacting all ancillary industries depending on real estate transactions, deepening and elongating the period of pain on a wider swath of the pop. Just a poor answer & unnecessarily painful manner, just bad economics only justifiable by the feds fealty to the ownership class.

A soon as there is any widespread indication of serious delinquency and/or foreclosure, look for mortgage forbearance and foreclosure moratoriums. It appeared to be free last time, so those who can make it happen will almost certainly think it’s free next time too.

The government’s definition of “affordable housing” is to turn future buyers into debt slaves with “affordable” mortgage payments.

There are also almost certainly other political motives behind this policy. Look at the distribution of foreclosures in ATL during HB1. This will spell it out for anyone.

I complained about the use of wokeness, but i am pretty frugal. So I agreed with some of what BENW had to say above.

I dont want mortgage forbearance !

That would be amazing. Huge upside for buying a home and no downside ?

Taxpayer covers the homeowner ?

I certainly hope not.

PBS ran a documentary around 2010 or 2011. A group of homeowners near Boston were chanting how the government wasn’t going to foreclosure on their homes.

The nerve of the government !

Worse some guy in Florida bragged he’d lived in his house without paying a dime for a year and a half.

Some homeowners apparently feel entitled.

And somehow a few (?) of them get away with special treatment.

I do realize that in some cases homeowners may have been misled by the mortgages they were signing up to in 2006-2007.

But most were looking to make a quick buck, no worries to any possible downside.

My guess is most understood what ARMs were and they just decided to play it optimistically.

And this past year I find out there are a number of what’s called non recourse states… walk away if you want, no problem other than your credit taking a hit. This doesn’t seem right to me. A neighbor and I got to cut the grass of someone who walked away from their home. Fortunately a buyer moved in after 4 or so months empty (late 80s or early 90s timeframe). Surprise, Texas is one of those non recourse states.

I suppose I should feel sympathetic to the persons who walked away from their house… but I dont know what the circumstances were.

Meanwhile in 2017 and 2018 it seemed like a considerable number of renters were being evicted from their apartments in Portland Oregon. Primarily because rent increases were substantial. I read of one apartment complex in Bellingham Washington (200+ miles north of Portland) that raised rents on a 1 BR from 1050 to 1500 when new owners took over. Tenants quite P.O.d. But somehow mainstream media (nor PBS) paid little attention to this nuts and bolts issue.

Please don’t write about how cheap this is compared to SoCal or SF… the sudden large increase is the point.

If the government provides mortgage forbearance that is really a slap in the face of renters who decided not to buy into what they perceived was an overly expensive housing market.

I owned a home for 10 years. Have rented 33 years, not entirely by choice but Seattle, Puget Sound seemed too expensive for what I could buy. And that was 23 years ago its certainly not gotten any better. Left the area… still renting for other reasons.

The Government has never paid a dollar of my rent.

Why overgeneralize ?

As to wokeness. Look it up. It means to be aware of what’s going on. What is wrong with that ?

That’s the definition I came across although a cousin of mine uses it quite liberally. If he doesn’t like someone’s stance on an issue… label the person woke.

More brilliance.

It almost seems a cliche to love the mom and pops.

I will never buy from a small business just because they are a small business.

They have to have a product I want at a good price. I’m not going to buy micro brewery beers because they come from some small entrepreneurial (love that word ummmm) business.

I dont like the taste of wine, whiskey or beer. It isn’t religious I’m not religious.

As for corporations buying up huge numbers of homes vs. good old mom and pops renting out 10 homes… the conventional wisdom is the mom and pops take care of their tenants better. Probably true but I doubt there is any evidence (other than anecdotal) to support it. Generally speaking I dont want mom and pops buying their 11th home if it means some first time homebuyer goes without.

If you think intuition is always right.. the earth isn’t flat and you might read about non transitive dice.

All markets are fun on run-up phase of the cycle. Everyone pats themselves on their

own back for their brilliance.

Nobody rings a bell at the bottom or top of any asset market.

When is goes vertical it brings out the FOMO buyers, which drives the vertical mania higher.

When the bubble bursts, and the decline begins in earnest, FEAR drives SELLING, and

depression (mental) takes over, followed by an economic depression.

It’s all psychological coach!

Not to mention the HUGE number of variable rate mortgages in play up there. The rate increases are surely hitting home.

Right the banks are required to hold the notes there, it’s all variable rate, no MBS. Go back to when interest rates shot up in early 80’s, it was horrid. The government created this mess with ZIRP and NIRP and whatever to save a bunch of profoundly corrupt banks. Now they are out hunting home owners like they are little woodland animals to fix blame. Figure this, like everything else monthly property taxes are on autopay. They can walk into your CDN bank account and empty it. And thanks to Wolf for showing what is reall going on.

Part of the issue is the number of variable rate mortgages here (in Canada). But the bigger issue is that virtually all mortgages, variable and fixed, are forced to refinance every 5 years, even on 25+ year amortizations. This may force an increasing number of people to sell over the next few (up to 4) years if rates don’t drop. You don’t get to keep your initial rate for the lifetime of the mortgage like you do in the US.

I locked in for 10 years at 2.01% and 2.06% when rates were at bottom. Why anyone went variable at that time is beyond me. Only one way for rates to go at that point.

Also contributed to the insane Canadian housing bubble. Worse than the heights of the 07-08 period in the US. Due for a further 30% decline in many Canadian markets.

I heard the same thing from my local credit union, only with a timing of two years down the road.

Was on internet realtor showing 3 houses,the one in Indianapolis listed at 649k,reduced 3 times now 429 k .this could get ugly ,my grandmother told me in depression,every dollar was repriced at 10 cents . Could happen again if we default,scary when everyone is loading up on treasuries,everyone on 1 side of a boat doesn’t end well

I’m not seeing these kind of price declines here in the U.S. Maybe a few here and there, but for the most part, homes are still selling in the midwest and northeast.

It won’t happen in those markets because many overcorrected in the last bust. Canadian markets never did. Affordability (or lack thereof) is much, much worse in Canada.

Point being ppl have 2021 and 2022 price levels in mind and only those forced to sell by circumstances will be listing, more time needs to pass w elevated rates and sale of mbs

Transaction volume in western burbs of Chicago is down alot. BY me it’s hard to see more than 6 properties avail between 500-850k in 3-4 contiguous western burbs.

“in depression,every dollar was repriced at 10 cents”

Flea, what do you mean by this?

Also: I had the same thought re treasuries, but if Uncle Sam really does default, I’m not sure one would be any better off holding dollars. At least I can get 5% on treasuries for now..

These articles are always so satisfying to read!

Report from the field: I’m from Quebec City, and people there think a house at 300k is crazy expensive. Now if you tell anyone in the shitty Southern Ontario city where I’m now stuck that you can still get a house at 300k in Quebec, the universal reaction is: “wow, that is so affordable!”

Well no it’s not. It IS overpriced. It’s just that Wolf is empirically correct when he says that the Bank of Canada turned people’s brains to mush.

And the only real reasons I can see for a city like Québec to be less expensive (rentals included) than the rest of the country on average, is that housing speculation never was a national sport among French Canadians (until the pandemic, of course) and that duplexes and triplexes are a thing in Quebec, unlike in other provinces. Normally, those plexes would be about the only thing people interested in real estate investment would look at, which made way more sense from an economics point of view than detached houses.

Sorry to hear that you are stuck. I’d rather live in a tent than that rathole, figure yourself a way out eventually.

Just got to wait until my child hits 18 or something, so I’m done with family obligations around here, lol. But thanks! I can deal with it in the meantime, even if it’s not my preferred environment.

How much foreign buying anywhere in Quebec?

A lot less I would presume.

I would suppose less too, indeed, especially outside of Montreal. I have nothing but anecdotes on that, though. The province is probably protected in part by its civil law system that is different than the rest of North America, different language, etc., making it less easy to get into from the start for many foreigners. Rent control is also good for tenants, on paper at least, when there’s no extreme shortage of apartments (landlords theoretically cannot raise rent as they want even when a new tenant moves in; they will nonetheless when they feel safe to do so).

I have a friend, though, whose son was in Hong Kong and looking to invest in foreign real estate a few years ago, and some “specialist” over there asked him if he knew about that city where there was still much room for prices to grow, stable economy and all… and he was referring to Quebec City. So who knows? That’s still in Canada, where you’re welcome to launder your money as freely as you want, apparently.

Bidding wars have erupted in Markham and Richmond Hill as the 5 year fixed rate mortgage has fallen. Ironically the yield on the 5 year Government of Canada treasury bond has gained about half a point since the start of this year.

The housing market since about 2005 has made no sense to me. I’ve watched whole developments go from $200ks to $500ks, then just about double again. Did everyone start making 2.5 times as much money, then double again? Have investors bought up all the housing, and created their own bubble world, disconnected from reality? Are people hanging on by their fingernails with 30 year mortgages that they can barely pay? I truly do not understand how we got here.

It’s called interest rate repression and negative real rates. You can carry a lot more debt at 2.5% interest than at 6%, but that game is over. Real rates must be positive because time has value.

Those who bought recently in the past few years are up in their eyeballs in debt.

And the Canadian employers want to lower the cost of labour, which is done through importing half a million newcomers a year who will take any job they can just to survive in their new home.

The housing market in Canada is beyond sane economics.

Not a lot of people in the formal economy make more than C$50,000 unless they work in the government sector or an American tech company.

I’ve heard of ten people signing up for a mortgage as co-owners for a home, or outright fraudulent income amounts on mortgage applications.

Nearly all Canadian Mortgages are insured by the Government. The banks take no risk.

As is evidenced in the Stock Markets, the Bank of Canada’s conjuring of fiat money will still take a long time to get back to Jan 2020 level of +/- $120 Billion. So there is still $260 Million of counterfeit C$ to be mopped up.

2×4 framing lumber ran up to $520 in January, now down to $380, with the cash market begging for orders. And Spring is right around the corner.

Silent Spring anyone?

Correction: C$260 Billion to be mopped out of the system.

The same excess liquidity that supports top-spin Stock Market in the U.S.

‘In Moody’s Investors Service’s 2021 stress test, the company said that action taken by the federal government to reduce its exposure to residential mortgage lending in recent years had shifted default risk to lenders, with the past five years seeing a 20% decline (from 46% to 26%) in the proportion of government-backed insured mortgages.’

As of July 2020. the max price for CMHC mortgage insurance was one million, which even then would not buy a shack in Vancouver.

“Nearly all Canadian Mortgages are insured by the Government.”

More like 1/3.

https://www.cmhc-schl.gc.ca/en/blog/2021/insured-uninsured-residential-mortgage-data

“As of the first quarter of 2021, only 35% of outstanding residential mortgages extended by chartered banks were insured. This share was over 60% in 2012. The share of insured mortgage debt held by non-bank lenders also decreased, from 41% in the first quarter of 2020 to 39% in the same period of 2021.”

Wolf. As always, great work. Suggest you could include a bullet for each city that includes average incomes (individual and household) and then the home price multiple of incomes (I.E. Toronto is somewhere in the 10x range). This would help put the sheer scope and scale of Canada’s housing bubble (2005-2010) on a bubble (2015-2018) on a bubble (2020-present) into focus.

Agree would be really cool to see something like case Schiller divided by local median

Reventure Consulting has done this for many cities. The P/I ratio is but one factor among many but RC gives it a lot of significance.

One criticism of P/I that I read is that it’s not the average person (household) buying homes these days. If its only the top 20% incomes buying homes… using the average income is not appropriate.

No surprise here. Whenever prices go parabolic to the upside, they soon come crashing back down. Canada didn’t learn from the pain the US suffered from 2008-2011 and now they’re paying the price.

Hopefully, we won’t see a repeat of 2008 here in the states. Prices have further to drop in the US, but buyer activity has definitely turned around after being completely dead for the last 6+ months. New homes I couldn’t get buyers to even look at are getting offers and selling again – in TX and FL anyway.

Buyers are now accepting higher mortgage rates as normal and price reductions are attracting traffic. Large builders are on the sidelines so new inventory isn’t overwhelming the market, and existing homeowners are sitting tight and not selling unless they absolutely have to. That said, liquidity has totally disappeared in the smaller metro areas and rural markets.

Another 10-15% drop isn’t unreasonable to expect in large cities and 25-30% in the smaller ones. Spring buying season will be interesting, to say the least. There’s still a lot of money out there sloshing around and looking for a home … or a “House”.

Or people are buying because cash is trash,or hyperinflation like Germany ,not pretty

Ha ha hyper inflation, apparently you’ve never experienced it, but I have. And I’ll tell you, Europe is still far from hyperinflation, and cash could come in handy in a coming recession.

When eggs go from 89 cents to $5.29 that’s hyperinflation

Hyperinflation is when eggs cost $5.89 in the morning, $10 in the evening, and the next morning no one knows how much they will cost (direction UP)

CCCB: “Canada didn’t learn from the pain the U.S. suffered from 2008-2011 and now they’re paying the price”.

It doesn’t appear the U.S. has learned from the 2008-2011 bust either.

Because it’s ALWAYS different this time.

I’m not seeing tons of new sales. I’m seeing some buyers taking advantage of the slightly lower interest rates from a few weeks ago. But in large part, very little is moving. Sellers aren’t selling (yet) and buyers aren’t buying (yet).

Yes, sellers are expecting last years prices and buyers are willing to pay this years lower prices.

The gap has to be bridged.

This year I put in three bids on houses, all declined as too low.

The houses are still listed.

The only houses slling fast right now are below 400 k here in Southwestern Ontario in an halfway acceptable condition.

Wolf, much appreciate your commentary and research!

A recent article on these stats by CBC (government funded media) titled “Worst January for home sales since 2009, CREA says” talks of multiple offers in hot areas like suburb of Toronto called Ajax still. So I pulled stats for Jan 2020 and compared them to Jan 2023

Sales

Sold 84 64 -24%

New listings 121 124 2%

Active listings 78 83 6%

Day on market 22 17 -23%

Median price $685000 $879000 28% (dropped 26.6% from peak)

Then you look at rentals

Median price $2,250.00 $2,850.00 27%

New leases 31 53 71%

Listing 66 105 59%

so 28% and 27% respectively. Incidentally the TSX is up 27% for the same period. Roughly 8.6% annual return. With rates at 6.5% and taxes 1.1% if you exclude any repairs and maintenance, you average a 1% return over 3 years above current rates.

Not the great return Canadian housing narrative the media and real estate boards want you to believe and I suspect the smart money is fleeing. I read somewhere Blackstone was selling everything if they can find buyers outside city core.

I’m surprised there is no mention from Canadian commenters about the largest bust in years: Coromandel Inc in Vancouver has filed for bankruptcy, owing 700 million. It has 15 projects underway. 20 of its condos in a 22 unit project have been presold, but require another 500 K per unit to finish. Oddly, the Co says they are over 50 % complete, so they must be very large, assuming ‘finishing’ does not include land cost.

The Co hopes to reorganize under while under protection from its lenders, 7 of whom have filed notices of default. This will not be easy with this many lien holders and the variety of liens.

The Co places blame on rising interest rates and the slow complicated process to get approvals from the City. Only the former can be called a surprise.

Not familiar with that but anecdotaly I’ve heard a lot of Vancouver RE was ponzi. Maybe that’s the case here maybe not, smells like it, but for sure some people are getting their clocks cleaned.

Its basically a duplicate of the housing market in China. So technically it would be a ponzi.

Grew up almost in Canada (MN). Got out ASAP. Have been to Canada more times than I needed to. Baffles me why people will pay these prices to live there. Same for W Europe, but I really hate cold, so maybe I’m the crazy one.

Bruh, you’ll be fine – global warming to the rescue!

Never lived in Canada or W. Europe.

But much of W. Europe has a pretty moderate climate. Closer to the Atlantic the more moderate. They have had problems with heat and wildfires in more recent years though.

The above is true for the Pacific NW as well.

Substitute Pacific for Atlantic.

Southern Ontario is actually south of several western US states.

I am beginning to see how home price/rate gyrations are further stressing the social fabric in my interior, British Columbia, hometown.

Home buyers were flocking here in the last few years, driving up prices (and rents). Now things are cooling off and ‘New Pricing’ signs are popping up along with word of several distressed homeowner neighbours, both new and old, divorcing or splitting up partnerships.

Whether it’s the sharp increases in mortgage rates/municipal taxes or just bad timings, ‘forced home sales’ seem to be picking up.

Yeah that kind of stress will destroy a family. It’s friggin sad, politely called collateral damage. These central banks have inflicted a huge amount of it, mostly not recognized yet but it’s coming.

On a different note

The BoC stopped reporting on their weekly assets holdings on their web page all January leading up to their monetary policy report and the announcement that they would be pausing rate hikes.

The week after this announcement they back reported. Now if compare the 2 year bond price to the asset holding during this time – its very interesting (smells like short term yield curve control to me). With the 2 year hitting new highs today a few weeks later and after some QT.

It seems that they really wanted a positive spin on that monetary policy report and to announce the pause and I wondered why there was nothing about QT in questions etc.

The Canadian CPI for January is slated for release February 21st and it will be on the high side due to rents. It should be month over month much higher than in America. We’ll see what Tiff does this March.

When I was first buying a place more the 20 years ago, it was my understanding – echoed by my realtor and banker – that real estate generally appreciated at 4% per year…a little more than inflation. A calm and reasonable world to buy into. Secure, but you were not going to make a windfall profit.

Now, looking at those charts, I wonder what the psychological effects are going to be on young buyers going forward. And what complicated appreciation answers the people who are experts in the business offer these days. I just really feel awful for anyone trying to get their first place.

The psychological effects for young people are that the older generations don’t care about them and just want to take all they can before they die. It doesn’t lead to a stable society.

That’s a lot of crap. Maybe it’s the stupidity of “young people” or the whining of cranks. Older generations do care and can’t believe that the Fed would have allowed these bubbles to get to these levels. It’s not about greed. The Fed keeps making the same mistakes – waiting too long to get banking sober.

I was watching a RE Utube video and I forget if it was an ad or part of the main content but 5 younger guys (20s, 30s) start bragging big time about all the homes they have bought recently. Each guy (no women) stated how many he had bought and the millions and millions and millions they are worth. Not older generation for sure.

People will react differently to this. I dont like these 5 people particularly but what bothers me most is laissez-faire capitalism says this is great. They are heros.

Capitalistic heros.

Real estate investors by and large benefit themselves only, not society.

Unlike inventors, comedians, plumbers, nurses, accountants, cooks, engineers, janitors, etc….

Even stock investors i think one could argue provide a minor plus to society at least compared to RE investors.

Classical political economy had a name for those people — Rentiers, and it isn’t a compliment.

You can thank the marginal revolution and the neoclassical orthodoxy for memory-holing the distinction between earned and unearned income.

eg – “…and it’s over the centerfield fence!…”. Kudos.

may we all find a better day.

It depends on where in Canada. Places like Country Club Estate in Edmonton today are selling for around the same price they sold for in the year 1990. Last sale $66,300 at 107 7835 159 Street. It’s still on youtube and the condition of the place was very good. I owned two 3 bedroom bottom end units in the same building and paid $72,800 all in including lawyers fees in December 1990. I sold both in the fall of 2013 for 151 and 155 thousand dollars. They really tanked in price. No 4 percent a year appreciation there.

Charts are interesting.

Wonder what would happen if you added historic trend lines to those charts. Would the trend line projected into current, still be below the present levels? It would appear to be so except maybe Montreal. Maybe some ways yet to go before prices dip below trend line.

The untold reason why there is a campaign to bring half a million newcomers a year is not to address a supposed labour shortage, but to artificially boost demand for rental properties and housing prices.

That’s why there is a lot of criticism about the immigration policy. On Canadian forums, even mentioning the sacred 500,000 a year in a critical commentary is met with a hostile response and ad hominems.

500k immigrants with no money and no jobs are not going to help to sustain Canada’s inflated house prices. The central bank’s neat little money printing trick has priced nearly everyone out of the market here.

The median wage in Toronto is what.. around 60k? And the median house price is $1million? How the eff does anyone buy anything here? $2300/month for a 1 bedroom apartment rental on average? Ludicrous.

I’m aware that some of my employees are renting BEDS… not rooms.. beds in a shared room with a stranger for $500/month. Never seen that before.

I say bring on the immigration. It will saturate employers with options, keep wages steady, and increase demand on the low-end of the housing market which, if sellers want to play ball, will force prices downward.

Correct me if I’m wrong.

Truth. Unfortunately, the half million a year, a housing bubble and a rental crisis are a scorched earth policy. It results in eventual decline and collapse.

Immigration at 500K/year is nuts.

Some immigration (maybe 200k) is probably necessary.

–

But look south. Starting wages for almost any job now is US$15/hour – that’s C$20/hour or $40K/year. (Canadian minimum wages are less)

Oh … and EVERY place you go in the US is looking for workers – but with immigration (illegal and legal) on hold wages are soaring.

Canadian wages need to increase – unfortunately excessive immigration inhibits this.

I hope you don’t end up having to hire the ones coming to Canada from Nigeria. Those are the ones who’ll push wages lower. Even sending one welfare cheque back to Nigeria would be like winning a lottery for their relatives back home.

“The untold reason why there is a campaign to bring half a million newcomers a year is not to address a supposed labour shortage, but to artificially boost demand for rental properties and housing prices.”

You nailed it. When the manufacturing jobs were offshored to China, this produced a lot of rich Chinese manufacturers. After having bought out their own property markets with their profits, they then turned around and started parking that money offshore in the West’s property market, driving prices up.

Foreign investors have bought up almost every condo in Ontario and B.C. (I can supply a link if you want one). Canadian condo builders are selling to these foreign investors, but then they need a lot of new immigrants to fill them, otherwise the foreign investors will stop buying. As you said, these new immigrants fill the rentals, pushing prices and rentals higher, exactly what the investors want to see (asset appreciation).

It’s a big circle jerk with ordinary Canadians thrown under the bus (especially the young). The country gets destroyed, all to satisfy the few people at the top who are benefiting.

This is exactly how a ponzi scheme operates. Canada needs new suckers to pay rent for the investors.

The Bank of Canada might also be in on it pausing rates while they’re still deeply negative.

US treasury rates still looking strong, heading higher, with mortgage rates being pulled along.

However, it’s worth thinking about how inflation is altering the valuation of not only homes, but continuing to decreasing the price of bonds. That was a big issue last year that was sort of downplayed.

As yields have risen, not much is being said about debt servicing or the economic implications associated with higher rates. Apparently, it’s of no consequence in a world that seems focused on engineering ways to goose short term casino options.

Nonetheless, yields probably are headed far higher, because economic risk is exploding from absurdly insane to grotesquely dangerous.

I was just looking at a mortgage guru, predicting that yields are headed down for 2023, which apparently is intended to help people plan how to navigate and strategically position themselves, as they bid on highly overvalued homes.

This same guy was dead wrong last year, but if nothing else, he represents an industry filled with morons:

“ By the end of 2022, 30-year fixed mortgage rates will hit 4%, according to the Mortgage Bankers Association’s current forecast. There are a number of factors behind this prediction, “but one of the biggest reasons is really just the growth that we’re still expecting for the economy as a whole,” Kan says.”

“ By the end of 2022, 30-year fixed mortgage rates will hit 4%, according to the Mortgage Bankers Association’s current forecast. There are a number of factors behind this prediction, “but one of the biggest reasons is really just the growth that we’re still expecting for the economy as a whole,” Kan says.”

^^^^

Quote of the year so far. If we see 4% mortgages, something really really bad will have gone from fear to reality.

So, since mortgages were not at 4% at the end of ’22, and that they were off by more than 50%, I think it’s within reason for the public to ask that the Mortgage Brokers Association disassociate. They’d provide better service for country if they just swept streets or cleaned chimneys.

BoC don’t have $2T RRP.

i think that prices will stabilize a short while due to lower inventories for the winter months, but falling prices will resume as we enter the late summer, when houses are just sitting on the market unsold. We need to wipe out all of the home equity on a portion of the homes so that foreclosures can increase and begin to put a bottom in the markets.

Not posted here in a while but just to give you an illustration of how deluded Canadians are and how much they don’t want to hear about reality.

Each time when you publish your “housing bubbles in Canada” I post it to reddit.com/r/CanadaPolitics. Each time they lock the thread and dismiss your articles as “without content”.

They are quite mad.

To be fair georgist. . .everything on that site(involving current events or anything political) seems to be a cesspool of sheeple with an “I support the current thing” blank stare. Not much original thought, Canadian or otherwise to be found on Reddit these days.

Dyed-in-the-wool Canuck here to say that Wolff is absolutely right. The RE market’s been wacko up here for many years. A reckoning is long overdue and inevitable.

The other elephant in the room with regards to the 500k newcomers per year, is political parties importing votes, to keep said political parties in power. It is indeed one big circle jerk, that will lead, ultimately, to the collapse of many things, including the political party who started the whole thing.

What do they think is going to happen, when 1 – 2 million newcomers organize, and decide, maybe it’s time THEY become the political party? Spend any amount of time in the suburbs of any major Canadian city and you can see what I mean (ethnic ghettoization).

Rainbow flags, Tim Hortons coffee, and 6K plus a month mortgage payments are the new Canadian reality…..