“The equity market is refusing to accept this reality”: Morgan Stanley.

By Wolf Richter for WOLF STREET.

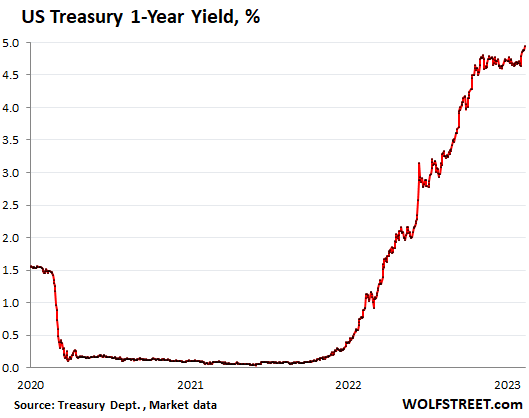

Since the close on February 2, which was the day after Powell had once again spoken about stubborn inflation in services and higher rates for longer, the one-year Treasury yield has jumped by 31 basis points as of this morning, to 4.95%, the highest since July 2007, and closing in on the magic 5% that seemed like a ridiculous pipedream – or nightmare, depending on where they stood – a year ago.

The two-year Treasury yield has jumped by 45 basis points since the close on February 1, which was Powell Day: to 4.54% as of this morning, reversing more than two-thirds of the 65-basis-point decline from the high on November 7 through February 2. That decline at the time had been driven by widespread Fed-pivot mongering, even as Fed officials themselves have said time after time, and as the Fed’s written projections released at the December meeting have pointed out: the Fed would push rates higher and keep them there for longer.

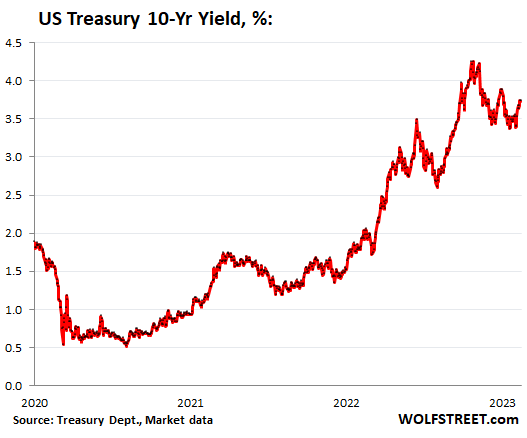

The 10-year Treasury yield has been a little slower to react, but it still rose by 34 basis points since the close on February 1, Powell Day, to 3.73% at the moment, after closing at 3.74% on Friday, having undone now a portion of the blistering January rally in prices (yields drop when bond prices rise):

All eyes are now on the CPI report to be released tomorrow. The Bureau of Labor Statistics on Friday revised higher the month-to-month CPI readings for October through December, showing that there was less “disinflation” in October and November, and worse “inflation” in December than the original month-to-month data had indicated. All of which took a big bite out of the “disinflation” hoopla.

It didn’t help that the jobs report for January explained in detail on February 3 what Powell had said earlier about the labor market, that it was still feeding into “core services inflation.”

In addition, the BLS made its annual revisions to its labor market data, including a big upward revision to nonfarm employment for the period through December 2022, showing that the labor market in 2022 had been even tighter than previously shown in the data.

Ironically, the stock market and the bond market would love to see a plunge in employment, and a surge in unemployment, that would “force” the Fed to cut rates – though stocks have a history of plunging once the Fed starts cutting rates.

The average 30-year fixed mortgage rate rose to 6.50% on Friday, according to Mortgage News Daily, having bounced by 51 basis points off the low of 5.99% on February 2. As of this moment, today’s daily mortgage-rate average hasn’t been released yet. The hopes of an average 30-year fixed mortgage rate in the 5%-range that were widely bandied about in January have now vanished.

Also vanished have the hopes for less volatility in mortgage rates. The wild ride is back, which makes selling homes a lot harder.

This comes after the bond market –and the stock market too – had spent all January blowing off whatever was going on, including the prospect of higher rates for longer and the earnings recession that has now started.

The stock market plays its own game. After jumping on Powell Day itself, which closed off the red-hot January, the S&P 500 has since then lost 2.1% through Friday at the close, amid crappy earnings, higher yields, and Google’s AI presentation that proved once again that AI is very good at producing logical-sounding BS, which knocked down Alphabet’s shares. AI had been the latest act of the Wall Street hype-and-hoopla show, and it degenerated into AI humor.

The S&P 500 is down 15% from its high on January 3, 2022. But it was down over 20%, and in January recovered by a bunch all the way through Powell Day. After which the rally sold off.

Not everyone on Wall Street sings from the same hype-and-hoopla page though. Morgan Stanley strategists, led by Michael Wilson, wrote in a note, reported by Bloomberg this morning:

“While the recent move higher in front-end rates is supportive of the notion that the Fed may remain restrictive for longer than appreciated, the equity market is refusing to accept this reality,” they said.

“Price is about as disconnected from reality as it’s been during this bear market,” they said.

“The risk-reward is as poor as it’s been at any time during this bear market,” they said.

“The reality for equities is that monetary policy remains in restrictive territory in the context of an earnings recession that has now begun in earnest,” they said.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

So much for that mortgage will start to come down narrative…good luck to all those that trust their RE agents and bought on ARM or hoping to refinance soon with lower rates ahead.

With decreasing home value and rate going up and down with an uptrend pattern..it will be a double whammy, can’t really refin or cash out when your home is upside down and on top of that rate even higher..have my popcorn out, this will be interesting for the rest of the year..

Good one. If you can’t put a chain around it and tow it away you don’t own it.

If it ain’t small enough to smuggle in and/or out of a political prison undetected, you don’t own it…

Never carry anymore than you can eat — C. Spedding

Even then you don’t own it if it’s hocked to the bank.

Own two of those and tags cost $68 a year. The county rent for the house is $435 a month. Paid the note of $75 a month off so many years ago I don’t remember.

The only asset that qualifies that definition is a cow.

Brilliant!!! Or your mother-in-law. OOps same thing. Kidding happily married 40 years.

Well, ARMs take time to shake out. Around me (Boston) I’ve seen fair amount of ARMs lately, but usually with a 7-year initial rate. Long time before it resets.

Mortgage rates don’t really matter anymore. Most everyone can afford to sit on their house & not sell. Mortgage rates could be 10%, but without millions of layoffs, housing prices aren’t going to see meaningful downside outside of the 8-10 cities with egregiously overpriced markets.

What matters is, if / when the recession comes, does Uncle Sam trot out mortgage & rent relief which will snatch away the market’s ability to deliver big downside to prices.

My guess is that it makes its way back in some form or another. Congress is WAY to addicted to giving Joe Consumer stimulus / lifelines.

I saw Navy Federal Credit Union is offering a 5 year conforming ARM with a 4.75% rate.

About 1.25% above the rate when peak housing prices were set.

For the first four months of the fiscal year, which started in October, U.S. receipts fell $44 billion, or 3%, to $1.473 trillion, while outlays grew $157 billion, or 9%, to $1.933 trillion, a record for the period. Interest on the public debt rose $8 billion, or 18%, reaching $51 billion in January, which will only jump higher as the bond portfolio is roll-over at higher rates and new interest from the new monthly debt is paid!! The interest on Fed debt could easily reach 800 billion and depending on “Higher For Longer” would jump to over 1 trillion annually!

Federal Government paying around 2% interest on its debt, so the interest payments will only go higher.

So, with the debt limit reached, that nearly $31.5T is locked in until June at the latest. I’d love to see it go down to the wire and then within 30 days see the debt jump up to $32T. That would be SWEET!

We’ll EASILY hit $800B this year. The only question is how far do we go beyond $900B?

The persistent inflation is the result of 40 years of tax cuts and tax loopholes that benefit the wealthy class. The Trump tax cut cost more than $7 trillion in federal funding. That money plus all the other tax breaks over the years unleashed recurring waves of liquidity. That liquidity inflated asset prices–a prime cause of our chronic ‘boom and bust’ episodes.

Tax breaks are not ‘one off’ events. They are recurring and accumulative. Welcome to reality.

And you haven’t figured out that over the span of 40 odd years, neither party represent anyone but mega corporations? Just keep voting harder ;)

So 40 years of tax cuts resulted in 2 years of inflation?

Hint, look at the Fed artificially holding rates below market for the last 15 years, then absolutely flooding money supply during the pandemic as a more likely source.

The treasury keeps issuing new debt regardless of any “limit”.

Noone cares any more.

“Google’s AI presentation that proved once again that AI is very good at producing logical-sounding BS, which knocked down Alphabet’s shares. AI had been the latest act of the Wall Street hype-and-hoopla show, and it degenerated into AI humor.”

From one hype to the next, sick and tired of hearing about NFTs..well 2023 will be the year of AI stock hype….already sick of hearing about ChatGPT, if I get a dime everytime I hear that word…maybe Kodak would like to jump in AI like they did with blockchain..

Don’t forget just the other year it was omniverse/metaverse/vr hype, despite the DKs for Oculus VR arriving about a decade ago!

A decade!

And NFTs as you mentioned.

Now we’re onto AI again. I’m sure we had some AI hype in the last four or five years.

Of course it’s all tech, all useful, all saleable, all interesting and innovative, but the hype usually over-eggs these things by many factors, and that’s when stuff works out.

I recall a game developer using NN AI back in the late 90s for a Ferrari driving sim on the PS1.

This stuff isn’t new, it’s just the latest useful hype vehicle to sell over-priced (imo) shares in companies, that broadly just sell advertising space, or subscriptions to software that’s essentially remained unchanged for decades (word, outlook, excel), bar networking trinkets.

True, but AI back in the 90s, 00’s or even 10’s couldn’t do your homework for you. So I think it is a game-changer at a societal level, but whether any company will be able monitize it I don’t know.

I could Google my college homework questions and get all the right answers quite easily several years ago.

When these things can give unique abstract answers to questions that are more philosophical vs historic or mathematic then I’ll buy into AI.

Let’s see it write a thesis that isn’t plagiarized

I love how this futuristic tech full world is marketed to us yet in reality most things don’t work as intended.

…’eloi’, that’s how it’s spelled, right?

may we all find a better day.

26 weeks went 5.03% this morning. Nice.

We’ll find out tomorrow if its for real.

Tomorrow? You can go to the U.S. Treasury website at 1pm PST today and see what the 6 month T-Bill yield is.

Okay, so for today, per the Treasury website, the 26 week T-Bill coupon equivalent yield is 5.03%

Yes, I just got the news of the auction that closed for me today. I buy a 6 month T Bill at every auction date they are available. Love it!

“The wild ride is back, which makes selling homes a lot harder.”

And this very much needs to happen.

That is a good buy on a risk/reward level. Why take duration risk since we can’t know the future? Why buy a utility paying 4%? Why by the S&P with an earnings yield of around 5.5% with Fed raising rates?

Earnings aren’t real money. The dividend yield on the S&P is about 1.5%.

I have a couple questions for those who use TreasuryDirect. I can’t find the answers easily on their website, and I think others may have the same questions.

They post an auction date and settlement date for treasury investments. If you are willing to accept whatever interest rate they give you, do you have to have your order in at the time of auction, or can you put in an order just before the settlement date? I’m trying to minimize gaps or waiting periods to make sure my money is always working for me.

Second, if you elect the automatic roll over of a treasury investment, will it roll over the same day it matures, or do they hold your money until the next issuance of your selected maturity, which could be days or weeks later? Again, I’m trying to minimize the gap periods.

Thanks to anybody who knows the answers to those questions.

“If you are willing to accept whatever interest rate they give you, do you have to have your order in at the time of auction, or can you put in an order just before the settlement date?”

The order has to be placed before the auction time. It would be nice if it was before the settlement date so that you know in advance what the rate would be, but that is not the case.

From what I learned, your Treasury order is entered between the afternoon of the announcement date and the auction date. This is normally two days. This is found at: https://www.treasurydirect.gov/auctions/.

You can also print out future schedules of all their auctions at:

https://www.treasurydirect.gov/auctions/announcements-data-results/

My apologies for missing the second question, but I don’t do automatic rollovers and can’t help with that one.

I have used roll over at treasury direct. The money never hits my bank account between the time the bill matures and the time the next bill is purchased, so they have to be holding the money. It doesn’t matter though as the maturity date and the auction date are always within a week of each other.

“if you elect the automatic roll over of a treasury investment, will it roll over the same day it matures…”

Yes, using the automatic rollover is a good way to minimize gap periods.

I don’t do any auto- roll overs on T-Bill auctions or CDs, because you wait a week for next T-auction, and if you look at brokered CDs (all FDIC) on TDAmer or Fidelity (no fees) CDs are sometimes higher rate or same estimated rate and you can sometimes get a CD that settles in only a few days at same rate or higher.

gn,

That has not been my experience. Every time I reinvested a T-Bill, it was automatically reinvested on the maturity date. I looked up how this is handled on the Treasury Direct website, and here is what it said:

“If there is no security available for reinvestment with an issue date that coincides with the maturity date, type, and term of the maturing security, as described above, the scheduled reinvestment will be canceled and the proceeds of the maturing security will be deposited to the maturity payment destination you previously selected.”

So either the reinvestment is automatic on the maturity date of the original T-Bill, or the reinvestment is canceled and the funds are returned to the linked account. I’ve never had that happen, but it’s probably more likely on longer dated securities that have fewer auctions. All you need to do is look at the upcoming auctions to know if the reinvestment will be automatic on the maturity date or the reinvestment will be canceled.

CDs are definitely worth looking at and may pay higher interest over certain maturities. I buy them in retirement accounts, but avoiding state taxes makes treasuries hard to beat in taxable accounts.

gn,

I’ve noticed that the CDs with higher rates are callable in every case I’ve seen, meaning they can be redeemed early without your consent. That’s a deal breaker for me. Make sure you check all the terms.

Theoretically, the interest rate should be zero–no inflation at all. But in reality that’s never the case. So what is the right interest rate? My view is that the ‘right’ rate would protect savings accounts. Families want to save. But too often in the past 40 years or so, (Volcker reign excepting) the savings rates never manage to exceed inflation. Same goes for income. It’s usually beneath inflation too. The ‘cure’ for inflation is to raise taxes on the RR class (ridiculously rich). RRs are the ones who inflate asset prices way beyond full value–which leaks into price inflation everywhere else.

Agree

I think the only way your idea is possible is if the RR as you call them stop getting into positions of power and influence.. so probably never. I was reading a while back about ancient Greece, I can’t remember the era but facing a likely collapse the ruling class started to make concessions and reforming the system to benefit the lower classes to save themselves. I guess that’s where we need to get to first. Right now nobody ultra wealthy wants us to save our money, they want it in play so they can compete for it against other businesses, they definately don’t want any of us to have too much of a safety net and possibly retire early, that would be tragic for them just have a look at the labour statistics lol.

“I can’t remember the era but facing a likely collapse the ruling class started to make concessions and reforming the system to benefit the lower classes to save themselves. I guess that’s where we need to get to first”

Nah dude, they just make up crisis these days as an excuse to inject trillions of dollars into their bank accts while sending you two checks for 1500.

Perpetual

used to be Fed Funds equaled inflation rate…on average

then 2008 hit

Now the Fed has gaslit everyone into thinking Fed Funds belong under the inflation rate.

Fed funds should equal, lets say, a 3 month moving average of a legitimate inflation metric…..in a perfect world.

The “right rate” should always be determined by markets, not central policy of any kind

Except that’s not how rate setting works, eh? The Fed sets the overnight rate as a policy lever.

I dont think you really mean that interest rate should be zero. Even in a no inflation world, you would have a cost for borrowing money.

I dont think that high taxes on the really rich people is alone a way to stop inflation. When you look at the actual tax rates of the truly wealthy you find it is really low, i think i read something recently that said it was like 3%. Why? Because the really rich own real estate and businesses that gain lots of value that is not taxed because it is unrealized gains. Even realized gains in stocks are taxed below the rate of tax on income that is earned. I have a friend who is a conservative doctor and he just HATES the idea of higher tax rates on capital gains. Why? Because he wants to stop working and just make money on his investments. But does society gain from a doctor retiring and living off capital gains with low tax rates? Heck no. Much better to keep him productive and tax him a lower rate on his work than on his investments.

We need to tax unrealized gains that exceed a decent amount, maybe as low as say ten million dollars? or lower. Who needs more than ten million?

Totally agree. And this would complete wreck private capital

Won’t ever happen though. Too many vested interests will block the political process to ever tax such types of wealth

The biggest cause of inflation is unrestrained government spending which must be financed by perpetual “printing”.

Wrong, again.

The bond market is still naive. There is still no foreseeable reason for rates to drop. ZIRP is NOT normal. This is normal.

Haha, aren’t the Bond market the smartest in the room? At least that’s what all these talking heads on MSM and YT would like you to think…as if action of Bond market is some kind of gospel.

Guess we will see soon enough, it’s like a game of chicken with the FED

Bond market being inverted for a long time has never been wrong. The last three times the Fed has said it is no longer a good indicator, but they have to say that. A recession is the base case, but maybe there is a 5% or less chance that this time is different.

Modern economics seems to have a flaw which is thinking consumption is the answer to everything. But taking money from a productive person and giving it to bureaucrats to administer out on a political basis can only be so big a part on an economy. You create wrong incentives for productivity and growth fails.

“The last three times the Fed has said it is no longer a good indicator”

Funny how they think of it as the “best” indicator… When it AIN’T inverted.

But the bond market has been completely altered by many years of massive QE that hasn’t even come close to being unwound. And this has altered the mindset of at least one generation when it comes to the price of money. Things like the yield curve don’t have the same signaling value that they used to have. The central bank’s have broken that.

Never has the Fed absorbed so much long term debt

To compare now to when they did not, breaks historical analysis of the yield curve

Old school

There is a great amount of inversion denial out there.

It’s been nearly four months since the 10-year peaked at 4.25% and the 30-year at 4.36%.

The onus is surely on the deniers to explain how these markers will be surpassed or how the curve meaningfully steepens in this environment of rising rates. Given the inflation and employment backdrop, I’m open to the possibility. But 0.25% hikes, categorically no MBS selling and with at least the prospect of disinflation, makes it look like an uphill task on my assessment.

It’s an interesting watch, particularly on days which may prompt the next directional moves.

You may think that bonds are “naive” or out of touch with the “market”, but the low interest rates on long-term bonds is the bond market’s conviction that we will not see much growth in the upcoming future.

So in spite of the massive creation of money, and the temporary jolt in inflation, long dated bonds expect slow to no growth and low inflation.

Deny it if you choose.

And here’s a real kicker: higher profit in a slowing growth economy results in LOW P/Es, not higher P/Es and not higher stock valuations. It’s just the result of lower labor costs.

Lower labor costs over time, not right now – the inevitability of technological improvements. The bond market is betting that service employment will go the way of agricultural employment.

Amen!

High-for-Longer may become Higher-Forever.

Generally the bond market IS smarter than the stock market, but at times both are wrong.

Looking especially at interest rate and inflation, historical data, back in the 1970s… the bond market was dragged kicking and screaming to higher rates then too. Short end leading, long end of the curve trailing. Thus heavily inverted yield curves, sustained for fairly long periods.

Someone must know the January CPI figures set for release tomorrow.

Hang on. I’ll text JP.

Don’t buy into conspiracy theories!

The market is trying to create pain trades today.

IMO the positioning started last week for CPI tomorrow.

Even with the rally this morning the momentum looks to have turned.

Maybe fundamentals and technical align themselves tomorrow we’ll see!

P.S. Bitcoin has been reacting a bit more then equities maybe a leading indicator 🤷

It’s tough to make much of short term trends. Look at bubble stock markets. A lot of times they will break the trend to the upside right before a bust. I don’t play that game, but there is a lot of money to make in the last phase of a market.

Some say the long bond yield running up to nearly 4.5% was a fake and we will crash back below 0.5% because we haven’t changed the 40 year trend of runaway government system. Who knows? I never thought going out past 5 years was good/risk reward.

Interest rates are rising. The 10 yr – 2 yr T yield curve is more deeply inverted than at any time in decades.

S&P 500 EPS estimates have been declining.

Bulging inventory levels do not bode well for new order growth.

Russia is attacking again.

Hey Wolf,

I noticed that nothing rolled off of the SOMA Holdings last week at the usual time.

Did the Fed have nothing roll off last week? This is the first time since QT has gotten going that I’ve noticed 0.0 on the ‘Change From Prior Week’ line. That would seem strange given the size of the balance sheet.

Djreef,

“I noticed that nothing rolled off of the SOMA Holdings last week at the usual time. Did the Fed have nothing roll off last week?”

You’re willfully ignorant. You never read a single article that I posted here about QT, but then you feel free to post this BS here. If you had ever read a single one of my QT articles, you would have known. What is the most fundamental item that I always point out about when those roll-offs occur??????????

What was the date last Thursday???????????????

This was your last comment. I’m done.

Djreef,,

I’ll give you another chance. READ THIS ARTICLE and then tell me why what you said was total ignorant BS.

https://wolfstreet.com/2023/02/02/feds-balance-sheet-drops-by-532-billion-from-peak-cumulative-loss-reaches-27-billion-february-update-on-qt/

Clue: When do Treasury notes and bonds mature???

The answer is in my article that I linked.

You would also know the answer if you ever held a Treasury note or bond to maturity.

Dude, I was just asking a question.

I just thought it odd is all. I was tracking it over the past few months and noticed that nothing rolled off.

That’s it.

I’m not really sure where the hell this is coming from as I’m just asking a question. A little something rolls off every week and it didn’t last week. I just wanted to know why.

Sorry, I didn’t mean to upset you.

I won’t bother you any more.

OK.

But you didn’t ask a question. You made a provocative QT-denier BS statement and stuck a question market at the end. That’s a huge difference. I fully got what you were doing. Making a provocative BS statement and sticking a question market on it is a common tactic. And then they say, “I just asked a question.”

If you actually regularly looked at SOMA holdings, you would have NEVER made that statement because you would have known the pattern when securities mature and come off the balance sheet.

It sounds like you read this on a blog that is spreading financial fiction, or on Twitter or whatever, and dragged it into here to spread this BS.

not everyone who asks a question is trying to spread disinformation. this is a fantastic site, but not everyone has read every single word of every single article on here. sometimes a question is just a question to get more information.

Yes, and real questions are welcome — and are very common around here.

But if you only read the headline and then ask a question based on the headline, and if reading the article would have answered your question, you’re going to get a reply that sounds like this: “RTGDFA”

I’m enthusiastic about the three year Treasury making a new high at 4.775%.

Some ((non-gated) Treasury) mutual fund money market brokerage accounts use a 7 day SEC average interest rate performance, which is helpful when looking at interest in a bank account, as an example (of a place to make close to zero percent).

As we get closer to the deficit hurricane and next two+ Fed rate hikes, the safety and income from a money market is a nice contrast to rising mortgage rates, overvalued homes, overvalued equities that are clipping the top range of being overbought.

If one thing stands out in this twisted game, it’s the overbearing confidence of bulls that feel entitled to excessive returns. In a few months, that absolute arrogance will turn into painful pitiful whining about how their fantasy fun money is gone …

I heart treasuries!

“I’m enthusiastic about the three year Treasury making a new high at 4.775%”

Do you mean the three month Treasury?

Economy running hot and, yet, the Federal government set to push out 2 trillion in new debt! How bad will it get when the economy crashes?

American monetary status in the end game!

Tiff Macklem paused rates, in an attempt to reign in mortgage rates perhaps, yet the bond market current says otherwise.

The yields are going up again…

I’m not seeing it in GIC rates in fact they’ve been falling of late. Maybe too much demand for them because of RRSP season.

I think the nonlinear impact of the pandemic is fascinating, and I’ve always felt, most economic model were broken and remain suspect.

The aftershock of the pandemic has reshaped our world, including home prices, jobs, stocks, economic and social life.

Treasury rates going up, along with mortgage rates, equities and uncertainty about inflation, creates an extension of pandemic behavior. It’s as if, we’re in a horse race, betting on outcomes and living in a casino.

As such, I’ve recently been tuning into the concept of mean reversion, especially thinking about how to quantify a horse race in terms of risk and probability. The horse race between equities and treasuries can be representative of two horses that are not behaving normally, especially in the last few years or even decades.

Nonetheless, I’m thinking about the premise of the pandemics nonlinearity and wondering about how that event changed the game.

The pandemic added new variability or dimensionality into the race. The horses aren’t able to run dramatically faster, they’re still horses that have historical performance, where they fall into a predictable pattern that includes good and bad days.

But, here we are with our Treasury horses running faster times than ever, running in competition with equity horses high on steroid boosters and pain killers.

The pandemic introduced the lunacy variable, making probability and odds handicapping far more complex, with an emphasis on running faster races on shorter courses.

It’s as if we now have genetically altered and enhanced race horses, breed for the purpose of running high frequency micro races, instead of horses linked to traditional, historical, time tested continuity.

In terms of mean reversion, there’s very little substantiated evidence or data to fully understand the odds or risk of probabilities associated with super short term, chaotic, nonlinear races.

I’m thinking this post pandemic horse racing will eventually reach a point where fewer and fewer horse track speculators will be willing to bet on races, where fewer people are playing. I think this pandemic horse racing fizzles out like FTX

Even treasuries, by next year, can’t go much higher, beyond something like 6%. At some point these poor drugged up, burnt out horses will succumb to capitulation and head back to the barn …

Choose a better metaphor. Horses? How about bacteria?

Wolf,

For posts like these, a shortish list of the highest PE stocks (maybe Top 10/20) in a given index (NASDAQ 100, SP 500, etc.) would be really, really enlightening.

Those Icarus Index (TM) stocks are the ones that will crash the mkt, when they finally get re-introduced to reality.

(For the 500, those with an index weighting of greater than 1% or .5% might be a good cutoff – the hundreds of stocks below those levels may be in cloud cuckoo-cuckoo land PE wise…but their tiny weightings make them pretty irrelevant).

Excellent, clear work as usual, Wolf.

Another potentially interesting phenomenon/semi-mystery that would make a good explainer post…

Index PEs have definitely fallen,

but the indices themselves seem to have fallen *less* in percentage terms than the PEs have.

(Fascinating.)

My guess is that increased earnings (or some such) have semi-propped up the indices…but my neurons are misfiring today.

Perhaps your teams (teams!!) of bright-eyed analysts fresh out of the Ivies (Ivies!!) could unravel and explain (explain!!).

For something like the Russell 2000, the disparity is really something else…

The Index PE has fallen by more than 50% (!) but the index proper has only fallen by maybe 20%…

At those levels of disparity, a bit of analytical digging might reveal some interesting things.

Mush, you analysts!!

There are no negative PE ratios in the Russell. So the companies with losses aren’t included in your figure. There are a gazillion companies with losses in the Russell, and they’re not included in your figure.

“…list of the highest PE stocks”

LOL. The list would only list the companies that have earnings. Those are the GOOD ones. Companies that have losses don’t have a high PE ratio. Look up Uber’s PE ratio, LOL. And they wouldn’t show up on the list. And yet, those companies are the real problem.

Aren’t interest just going back to normal??? Why is nobody in debt selling the benefit of inflation – their debt is being knocked down to nothing!!! For conspiracy theorists is the govt really giving the true rate of inflation it may be much higher!!

The bond market is saying they’ll never go back to normal.

I’ve been selling inflation with my sub 3% mortgage. There is no reason for me to pay this down when I am making so much more in Treasuries at nearly 5%. You can pry my current mortgage out of my cold dead fingers.

Given my age, that may happen and another money-losing Fed MBS will roll off.

Of course all of my Treasury gains are still below inflation so the carton of eggs and my service staff are taking all of my gains plus more.

Nothing surprising. The economy is being run in reverse.

It seems everyone sees the future crystal clear with the Fed cutting rates. They should be more careful what they wish for.

At this point I would just laugh if the FED actually pivoted and cut rates and we went into hyperinflation. Maybe then we could get rid of the toxic vermin who are running things.

> Maybe then we could get rid of the toxic vermin who are running things.

I worry, too, about what comes after that. The new boss, governance and times are not at all necessarily better than the old one. If the 20th century has anything to teach us, it is that. Things do not just fall into a better order.

Yes, there are evolutionary branches that advance until they become extinct.

“Maybe then we could get rid of the toxic vermin who are running things.”

That isn’t working well in Venezuela.

It also didn’t end well in Weimar Germany from 1918-1933.

Exuberant Nationalism was created.

“The risk-reward is about a poor as it’s been any time during this bear market.”

Risk-reward is poor in ANY bear market. In fact, risk-reward is pretty poor all the time in the stock market unless youre an early round investor cashing out to the retail gamblers.

Former Fed economist John Roberts recent post:

“Continued robust growth limits the rise in the unemployment rate this year, and it ends the year at 4.2 percent, 0.4 percentage point lower than in the FOMC’s median December projection. That’s despite a steeper path for interest rates: The federal funds rate reaches 5.6 percent by the third quarter, consistent with ¼-point increases through July of this year.”

Final thought on equity race horses:

It’s the same courses (dow, qqq, etc), same basic horses, but speculators have had more money to bet with (up and down) and, there’s been the evolution of a new fashionable trend to not bet on the full, normal (annual) race track length.

Instead of the out dated old fashioned approach to bet on a horse and as accept a yearly performance percentage, the new crowd is betting more money on shorter stretches of the overall race track. Instead of a mile or quarter mile, speculators are betting on the first horse out of the stalls, or the horse that’s ahead by the first 100 yards or bets on last horse out of stall that gains most ground within quarter mile, etc.

These 0dte options bets are highly attractive to crypto gambling participants and somewhat like flying monkeys that try to scoop up laundry tokens in front of steamrollers.

I think ultimately, the swarm of monkeys ends up eating it’s young, so to speak. This concept seems like GameStop on acid, pushing on a string that has no logical, sustainable outcome, except self destructive.

I can’t imagine market makers (bookies) are going to sit back and watch a bunch of punks steal their pennies all year long and get into a liquidity war zone where everyone has gone mad trading bets that are increasingly less profitable.

Maybe this can all be done with programmable AI at high frequency, but somebody from the country club has to perpetually feed money into the chaos blender. That person has to also be insane.

I am with MS that fundamentals for S&P 500 look bad as profits are deccelarting, raising a lot of questions about p/e, especially when looking at schiller’s long term averages (aka cape). Barclays cape indexes look better re international, but if us equities tank it will likely tank everyone. Just how it goes.

One has to believe that there will be some kind of repricing once the market realizes the recession that never was will not be soon, meaning higher rates are here to stay and tech will have to make money like everyone else for the indefinite future. But that always seems like not yet, tomorrow.

For long term bets I like international equal weight us on a fundamental level, as it limits a Japan scenario that always is possible after an asset bubble, but have to eat a lot of currency and political risk. International is overdue for some better returns over us. No bargains, for sure, but that’s been the norm for a while.

And by all that is good and holy, stay the fuck away from buying a sfr. Housing looks like it’s doomed because affordability is a joke. What was it, 2.5x salary once upon a time?

Recession that never was? You don’t think we’re in a recession? Gallons of gasoline sold has been less than the prior year same time since spring break 2022. Housing sales down. Car sales down. College enrollment down as well. Sounds like an economic contraction to me. Not economic expansion. Speculators flipping the same thing to one another at higher prices is not economic expansion.

No. Its all fun and games until people lose their jobs and can’t pay bills. Then the cards fall

“International is overdue for some better returns over us.”

International MFs had a good 3 month run as of one month ago. Maybe some of it was currency related. I noticed the 3 month returns aren’t as high now … so the big run up 4 months ago to maybe a couple weeks ago.

Some of the funds have P/Es in the 9 to 11 range. Historically low. The funds have badly lagged the US (only) funds the last 10 years. Many having 10 year returns in the 4 to 6 percent range…. some smaller more growth oriented funds 8 to 10 percent.

Regarding “mean reversion ” (occasionally comes up):

1. Which mean are we talking about (how many years going back in time) ?

2. How long do we have to wait for it to occur, if ever (buggy sales… horse and buggy… typical example) ?

This whole thing feels like a redux of the period before the GFC. There were guys at Lehman Brothers in fixed income who were talking about “the roided up” markets in 2005. And they had hard analysis to back it up. Their bosses wouldn’t listen of course, which is why Lehman is history.

This market feels very roided up too, melting up today on no news at all. Alan Greenspan called the markets of the 1990s “irrational exuberance”. Old Alan hadn’t seen anything yet.

“melting up today on no news at all”

They have seen the CPI report due tomorrow. They know CPI is below expectation.

How can you be so sure? There were many readings in 2022 when the report came in “hotter than expected” and futures went from up 1% to down 1% in minutes.

Why are you so sure that the reading will be below expectation tomorrow?

Flip a coin on “back-ward” looking CPI data released Tuesday. Flip a coin on the market reaction as the SP500 instantly spikes 100pts either up or down. And look at past trade data as the bots head fake and rip out stops, and then reverse as the A.I. overlords ensures maximum pain on us ant brained humans.

I trade E-Mini SP 500 futures and avoid CPI release events as watching a single contract move $5,000 or 10 contracts move $50,000 instantly, I’ll leave that for the F/U money guys who own their own private jets and A.I. algorithm servers sitting next door to the exchanges. Honestly Vegas is more relaxing, and gamblers get free drinks as if you trade futures on CPI release, you’ll need to pay and drink heavily afterward.

If you want a more forward looking, real time CPI measure search “Cleveland Fed Inflation Nowcast”.

Their method has a better track record, per the description on their web page copy and pasted below:

Our inflation nowcasts are produced with a model that uses a small number of available data series at different frequencies, including daily oil prices, weekly gasoline prices, and monthly CPI and PCE inflation readings. The model generates nowcasts of monthly inflation, and these are combined for nowcasting current-quarter inflation. As with any forecast, there is no guarantee that these inflation nowcasts will be accurate all of the time. But historically, the Cleveland Fed’s model nowcasts have done quite well—in many cases, they have been more accurate than common benchmarks from alternative statistical models and even consensus inflation nowcasts from surveys of professional forecasters.

Lol “they” don’t know anything. Positioning and hedging.

The issue with conspiracy is you’ll never know which ones are true.

The key number tomorrow and going forward here I believe will be 6… As in markets worried about 6% rates

I heard this from a trading friend in London

There were literally orders today being spoofed in level 2 with big orders being placed at certain points to drive the algos towards liquidity and then the orders being removed before the price action gets there.

All sorts of reasons these markets can move this way. Momentum trading with billions not for the faint at heart.

BS ini

Agree with you.

Another new factor is ODTE (0 days to expiration) Betting on puts or Calls 24 hrs before the expiry. more volatility.

One dude who’s property we just did just got a VA loan at 5 1/2%. The only hitch is it’s for 1 year only. After that it goes up to the market rate. Since it’s a VA loan the taxpayer is on the hook to insure the loan if it goes into default. So this is the new scam that is being dumped on the unsuspecting public. All the gangsters in the RE industry get their money up front in terms of commissions, lender fees, attorney fees., settlement costs ect. while everyone else is left holding the bag. The RE shills could care less. How in the world is this allowed to happen after we went through the GFC a decade ago? It’s Deja Vu all over again.

Just curious, what’s the percentage he put down? Combine what you just said and if he has a low DP, that upside down and us taxpayers being the bag holders can be a reality by next year….

VA loans can be 0 down and seller to pay all closing costs. It’s always been this way.

If that’s the case then oh boy…more gifts for US bagholders soon

1) Dec 2022 revised CPI y/y is (-)0.7%. In June it will get worse.

Inflation is rising at a lower pace, in accumulation.

2) In Feb 2020 the Core CPI was 2%. It was down to 1.5% after a year.

In Oct 2021, after over a 1.5Y it popped up above Feb 2022, breaking out.

3) Between Feb 2020 and Oct 2021 wages were sharply up. Co paid

emergency workers – nurses, supermarket employees, truck drivers, industrial workers – for the risk they take and due to shortages. The rest,

the 160 million workers still benefit from their sacrifices.

4) Inflation stick it to investors and workers,

5) The Fed might pay the primary banks $200B in 2023, but the gov might

pay investors negative $(-)1T in 2023 on $32T/$34T gov debt. If we enter recession the Fed might cut it’s losses, but the gov might pay real +3% on $35T/$37T instead of (-)4% on $32T/$34T.

6) That’s why bond traders salivate.

Since Jan 20 low the Dow is gently turning around. Today it closed inside Aug 16 fractal zone.

Let us know when it crosses into the rectal zone.

“Price is about as disconnected from reality as it’s been during this bear market,” they said.”

When I was in college once, a professor announced in class that we had to learn the difference between “it’s” meaning “it is” and “its” used for the possessive. Then he passed back my paper with all the “it’s” improperly used circled. Needless to say I got a C-.

So Wolf, you need a grammatical correction.

Dan,

I really don’t like these typo lessons by people who are wrong and don’t know what they’re talking about.

“as it’s been” = “as it HAS been” – which is perfectly good though casual use.

If you’re going to try to teach English, at least learn basic tenses, such as “has been.”

I have no idea what you think your suggestion “its been” could possible mean.

The cpi would come deliberate low and then after few weeks it’d he readjusted to high as it happened last week for oct to dec cpi

“The equity market is refusing to accept this reality”

No, the equity market is doing exactly what it should be doing when you print almost 10 trillion – go parabolic for no other reason.

Tomorrow CPI comes lower and market goes up 3-4%. In two months they correct the CPI number higher … and the market goes up only 1% … hahahah

“The telephone, the big board, and the ticker were all fake, of course. They were simply stimulants to make the Earthlings perform vividly.”

Kurt Vonnegut, Slaughterhouse Five

“Google’s AI presentation that proved once again that AI is very good at producing logical-sounding BS, which knocked down Alphabet’s shares. AI had been the latest act of the Wall Street hype-and-hoopla show, and it degenerated into AI humor.”

Mid 1980s AI Expert Systems were in general over hyped. Some were successful at least in the short term, maybe long term as well.

You can read about DEC’s Xcon (to configure computer systems) and Dendral for example.

Successes notwithstanding, there was enough disappointment apparently that it lead to a large cut back in AI funding… the so called AI Winter.

Didn’t ksdt too long…

Late 1980s, early 1990 and neural network research took center stage.. actually emerged from semi dormancy having began in the 50s or 60s. Symbolic AI took off in the 60s, 70s.

I dont follow AI at all presently but get the impression machine learning has dominated AI research (and especially commercially) the last 15 to 20 years. So much so some might invorrectly equate AI to ML.

In 1981 Barr & Feigenbaum published a 3 volume work “The Handbook of AI”, 15 chapters.

Machine Learning is not one of them although

“Learning and Inductive Inference ” is a chapter.

A few other chapters include: Search, Knowledge Representation, Understanding Natural Language, Programming Languages for AI [think Lisp, Prolog and many others], Automatic Programming/Deduction. Vision, Robotics, and Planning and Problem Solving.

Early 1980s: Nils Nilsson, Patrick Winston had popular AI texts. Subsequently Russell, Norvig coauthored a very popular AI text.

AI isn’t new. It (aspects of it anyhow) probably has been over hyped multiple times but has had some great successes. Its been over 20 years since AI (sophisticated software) triumped over the best chess champions. No aspect of brain related activity hasn’t been emulated with varying degrees of success by now. AI as autonomous agents has been a popular area of research for some time as well (Rodney Brooks, presumably thousands of others).

Read a number of articles today that shout about how the bull market has returned and its the end of the bear. However, the indexes are still way above the peak before COVID hit and even then lots of people talked about being in an asset bubble and valuations stretched way beyond fundamentals. Yet here we are with indexes even higher (and supposedly entering a new bull) when we also have QT, significant inflation, war in Europe, major geopolitical risks in asia, and falling fundamentals – what a strange world we live in.

The dollar is worth less than it was pre-covid. Look at M2 to see that. You have to adjust assets for monetary inflation if you want to compare to years prior. QT hasn’t brought that back down…there is still way more liquidity than back then.

BTC up 3% 30 mins after stocks opened and S&P up 1% after 30 mins. Rigged as rigged can be.

I got suckered on the VIX on what should have been the Saint Valentine’s Day massacre for the stock market on the inflation news.

Markets are UP because they know the Powell does not have the guts to tame the inflation firmly. After all, he works for the bankers.

If he was really serious, he’d have raised by 50 bps and showed some courage by not sending dovish signals.

The real inflation on the ground is much higher then what govt reports.

My auto insurance increased by 34% during this renewal period. I did shop around but no go.

Market loved the new inflation print and raced higher.

FOMO is ragging strong. WS Media won’t disappoint with their pump.

Only way is up.

It’s not FOMO, it’s money-printing. They printed too much. They printed the stock market permanently higher. And all other assets. They stole the value of your labor.

6 month T-bill yielding 5.03% here on Valentine’s Day. Inverted by 129 bps with the 10 year. Stagflation worsens.

These are your sovereign bonds on QE/QT drugs.

It’s clear to me that raising rates isn’t working. Powell has to start aggressively draining liquidity from the system. That means $75 billion a month isn’t enough. It needs to be more like $200 billion a month.

Agreed. (Asset) Inflation (housing, stocks) is being driven by liquidity i.e. QE.

Fed increased money supply 35+ percent, and now housing is up 38% since the increase in M2, and equities are at high valuations.

Increasing rates doesn’t provide the solution to the current price levels, it only hurts the middles class.

Powell and his bankers know this, but decreasing the (absurd) 9t, (now 8.5) on their balance sheet will bring down housing prices and stocks, hurting banks, and the top 10% – who ultimately are the ones who hire him.

His ego (like his predecessors) is too big to do what would be best for all of us.

Can’t it be argued that stocks are not so much disconnect as they are really forward looking? After all, there is no reason to think inflation will persist indefinitely. We have strong deflationary economic forces playing the long game that is to an aging and now declining population. The inflation we have now was caused almost entirely by government intervention during the pandemic along with easy federal money that you documented quite extensively. Unless you don’t think the fed is now committed to killing inflation, there is good reason to thinks stocks may be the best long term parking spot for cash at this point since inflation had peaked.

An aging population is inflationary, not deflationary. They hold the bulk of the assets, and consume, rather than produce.

I don’t think inflation has peaked. Not at all.

If the long-term growth potential of the economy is 1.5% and inflation target is 2%, then nominal GDP growth will be 3.5% going forward. This is why long bonds are priced around 3.5% and why stock prices remain stubbornly elevated with high p/e ratios. This is the so-called Goldilocks scenario.

Makes me wonder. Do the dimwit pumpers on Wall Street realize that Goldilocks was chased off by the three bears?

Future inflation will never be reflected in the Fed’s target going forward, but it will arise in strong spurts, like we are seeing in the 2021-2023 period. Whenever a crisis arises, the Fed’s plan is to respond with a spree of money printing that creates a new permanent inflationary step-up in prices. That’s why Goldilocks story, even if you interpret it to end will, is a fairy tale. If you step-up money printing and prices in the face of every crisis, you wind up with a 2% inflation target that averages 6% in reality.

Don’t make decisions on what the Fed says. Look at what it just did in 2018 and 2020/2021.

“Do the dimwit pumpers on Wall Street realize that Goldilocks was chased off by the three bears?”

I like this quote even though only the big Papa Bear is needed.

That’s the big if. These fools seemed to think that the rules of economics didn’t apply to us, and that printing wouldn’t cause inflation. Now that they have been disabused of this notion, there might be more political pushback if they try to respond to the next crisis with printing.

You are right that, the 6% spurts only make sense if you go for deflation to make up for it. They don’t.

In any event, stock prices aren’t justified by a 3.5% long bond. They need ZIRP to justify the p/e ratois of today.

“Now that they have been disabused of this notion” – the “transitory” camp is still out there and won’t be disabused so easily. Looking forward to Wolf’s breakdown of this CPI report.

No, you end up with Weimar Republic.

Wolf,

“The Fed raised by 450 basis point in less than a year, far more than anyone imagined …”

Do you know the context here? Inflation was WAY OVER 10+ % last 1 year, and as of today, the rates is still playing catch up!!

As of today, we are still -2 % , yes Negative Real Yield!

No wonder Economy is still strong.

No wonder Labor Market is still strong.

No Wonder Supply still could not catch up with Demand.

Since when you are becoming a Fed minions? Did Powell’s assistants in Fed reach out to you and get you some benefits? lol

A lot of my comments stray off into abstraction, as I wander into off topic rabbit holes.

The hole I was just in was illuminated by super advanced laser technology that was blindingly bright.

The abstract connection to higher interest rate yields circles way back to a persistent theme I’ve ranted upon for months, which is liquidity, and more specifically, the focus, that cash will become increasingly precious.

The Fed rate increases, headed into summer, the deficit hurricane, earnings impairments revisions and the general theme of an impending recession, indicate future economic stress, which translates to higher levels of risk, related to valuation.

That, as a backdrop, with inflation not being fully contained, is a serious matter that should cause people to be more hesitant and cautious, but, what if there are additional risk factors to add into the equation, factors that are under the radar, anomalies swept under the economic rug, the discovery of fibers in the rug that show alarming decay.

What if our slow motion train wreck accelerates into a real-time collision. I assume, if cash isn’t easily available, yield will fly higher, dragging mortgage rates along, and the capitalization of lots of corporations and banks will be decreased.

This matters:

FEDERAL RESERVE BANK OF KANSAS CITY

September 08, 2022

“The rising interest rate environment has led to unrealized loss positions in community bank* available-for-sale securities portfolios and declining tangible equity capital ratios

At year-end 2021, only 4 community banks had tangible equity capital ratios below 5 percent; that number increased to 333 at June 30, 2022, indicating less ability to sustain economic shocks.”

U.S. inflaiton comes in hot for January. Big tip off yesterday was rising short term interest rates meaning no one was taking profits before the release of the data today. I doubled down on the VIX yesterday after seeing short term yields rise.

how do you trade VIX ? Just curious…

Another little story related to yields rising and portfolio adjustments (fire sales)

“TCE is declining industrywide because of the negative effect of rising rates on the market value of bank holdings of AFS securities. The number of banks with ratios of TCE to average tangible assets of less than 5% jumped markedly in 2022, with some banks posting negative TCE.”

https://www.stlouisfed.org/on-the-economy/2023/feb/rising-rates-complicate-banks-investment-portfolios

Loving higher yield!!

All this is outdated stuff, based on 2022 quarterly reports, or whatever. The prices of these securities have been jumping all year, LOL

Wolf,

I just wanted to chime in with a small theory about why some people don’t RTGFA and how you often become frustrated about it.

For some reason many people love to skip content and just read comments because they are very short in comparison to a long-form article or video from a single source.

I find myself often skipping a YT video just to see comments. It’s a bad habit for me and it seems reading in general has become too “Twitter-ized” where only tiny bite-sized pieces are acceptable to many readers anymore, even from the best experts.

Humanity is devolving into everyone having the short-form attention span of a fruit fly. A name I see used for this is ‘pancake people’.

It’s perfectly OK to skip the articles and just read the comments. But when you comment about the Fed not doing QT without having read my Fed articles, you trample all over the commenting guidelines. Just don’t comment about the Fed if you don’t read my Fed articles.

Also, if you read on some blog that the Fed wasn’t doing QT, say that! Say: “so and so said that the Fed isn’t doing QT…” and I’ll go ahead and crush so-and-so, not the commenter.

But when you say: “I look at the Fed’s SOMA portfolio all the time, and it’s not doing QT,” then you set yourself up for getting show down.

Three months now without a new high in the 10Y UST yield and all while the Fed is doing QT. This screams recession soon…..

Global recession that is.

Absolutely no sign of recession when I look around.

People are still spending money like crazy.

Look at ABnB great results.

AirBnB is a small part of the economy. Gallons of gasoline sold is down YoY (since April 2022 it’s been like that). Home sales down. Car sales down. College enrollment down. Even Coca Cola said unit case volume is down so numbers are up only due to prices up. Sounds like a fake economy. Luxury goods and services don’t matter as they are a small part. This is an economic contraction.

Yes. I think people are generally missing the long lag in Fed policy/M2/broad money/ Treasury curve inversion. I think a lot of the fast money crowd know there is a bad recession coming, but there is short term money to be made with all kind of financial leverage, options, hedges with ETFs and other products. Too much like gambling for me.

AirBNB announced great results. In my opinion, the wealthy (say top 10%) are out spending their stock gains with gusto, leading to inflation in services, like travel, housing, contractors, but also on things like new cars.

There will be no soft landing. Powell either has to crash the stock market or inflation goes out of control for many years to come.

Yes. Stocks like LVMH go up as the rich get richer and spend in more expensive goods. Stocks like MCD and WMT go up as the middle class get downgraded and end up buying from there more. Middle class and middle businesses going away so it will be the haves and have nots both on wall street and main street.

AirBNB announced great results==> bad news for someone who is pretending trying to tame inflation.

I see no recession anywhere around me.. People are still spending money like anything.

That’s because people live for today

Kevin Walsh was on Kudlow today and said the Fed has a tough job to do, made worse by the prolific Federal spending and deficits, which forces the Fed to buy Treasuries and essentially print money. Also, we are importing inflation from overseas because of the actions of the global central banks. He made a lot of sense. Heller was on yesterday and said the Fed funds rate needs to go to 6% or higher to have any impact on reducing inflation. We have a long way to go.

Kudlow is a douche.

All the CNBC crew, “Stonks go up.”

Only the guests disagree. Even their questions are leading questions.

What do you call a Bearish CNBC host? FIRED.