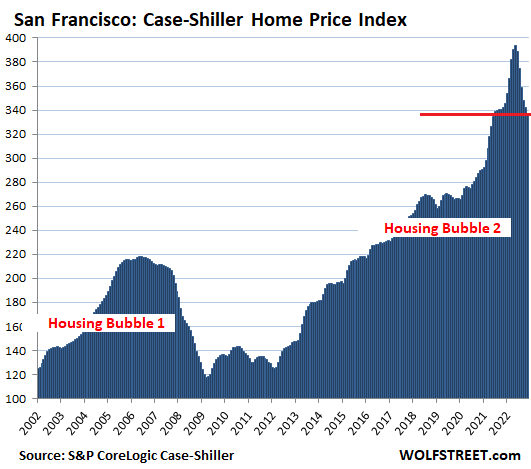

This takes some doing: San Francisco Bay Area house prices plunged faster from the peak than they’d spiked to the peak.

By Wolf Richter for WOLF STREET.

Housing Bubble 2 continues to deflate relentlessly, no matter what data set we’re looking at. Today we got the S&P CoreLogic Case-Shiller Home Price Index for “November,” which is a three-month moving average of home sales that were entered into public records in September, October, and November, reflecting deals made largely in August through October.

Prices in all of the 20 metros in the index dropped from the prior month, and all continued their slide from the peak last spring or summer.

The San Francisco Bay Area is the leader here. The index for single-family houses was down 14% from the peak in May and turned negative year-over-year, having plunged faster in the six months since the peak in May than they’d spiked in the six months up through May.

The Case-Shiller Index is different from median-price indices. It uses the “sales pairs” method, comparing sales in the current month to when the same houses sold previously. The price changes are weighted based on how long ago the prior sale occurred, and adjustments are made for home improvements and other factors (methodology). This “sales pairs” method makes the Case-Shiller index a more reliable indicator than median price indices, but it lags months behind.

Median-price indices reflect the price in the middle of all homes that sold that month, and can therefore be skewed by a change in the mix of homes that are sold, which is a big issue when there is a dramatic change in the market, such as in 2022. But they’re more current.

And the median price indices have plunged a whole lot further. The median price across the US of all types of homes sold in December fell 11.3% from the peak in June, according to the National Association of Realtors, while today’s National Case-Shiller Index (three-month moving average through November), dropped only 3.6% from the peak.

In the San Francisco Bay Area, the median price plunged by 30% in December from the crazy peak in March, and was down 10% year-over-year. The Case-Shiller Index for the Bay Area today (reflecting home sales in September, October, and November) was down 14.4% from the peak, and was down 1.6% year-over-year.

On a month-to-month basis, today’s Case-Shiller Index dropped again in all 20 metros that it covers. The biggest month-to-month drops occurred in:

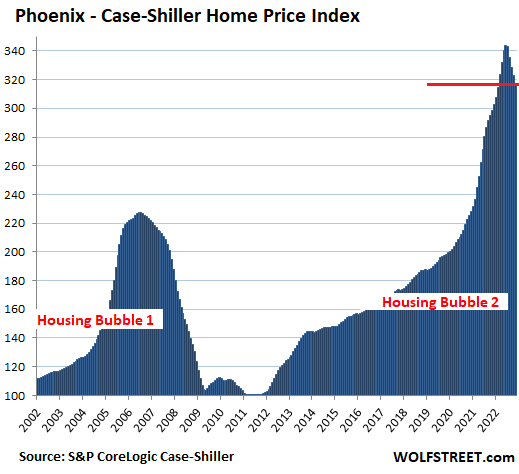

- Phoenix: -1.9%

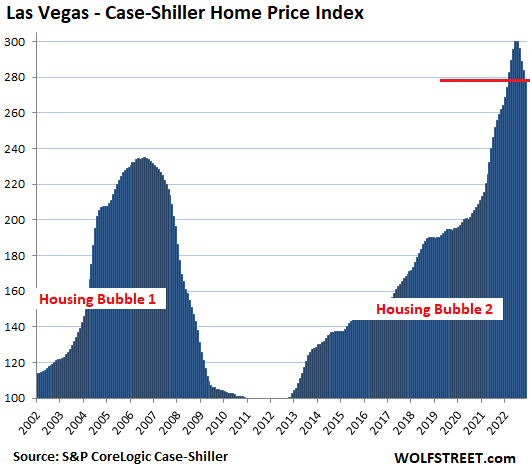

- Las Vegas: -1.7%

- San Francisco: -1.6%

- Seattle: -1.5%

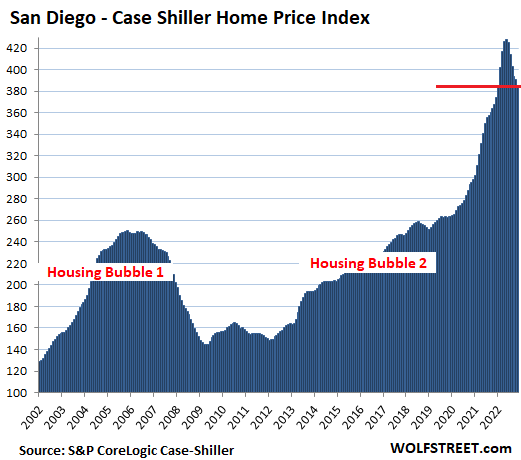

- San Diego: -1.4%

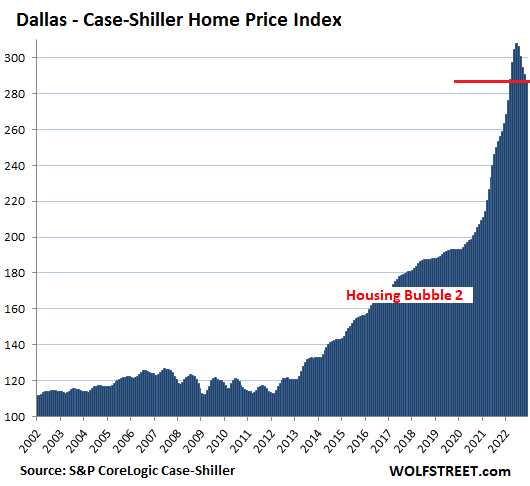

- Dallas: -1.1%

- Tampa: -1.0%

From their peaks, which range from May to July, house prices dropped the most in:

- San Francisco Bay Area: -14.3%

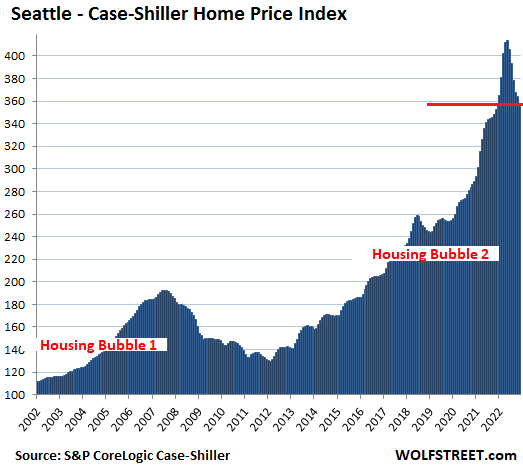

- Seattle metro: -13.5%

- San Diego metro: -9.9%

- Phoenix metro: -7.7%

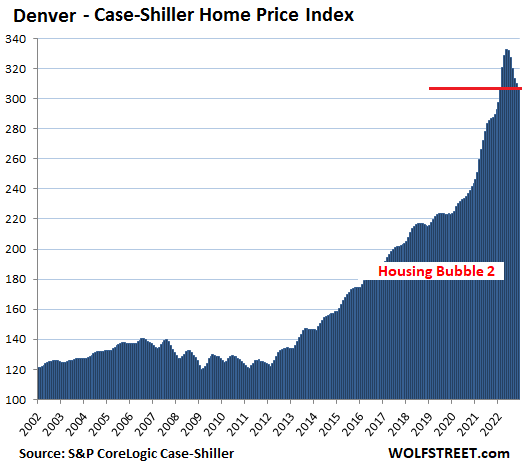

- Denver metro: -7.5%

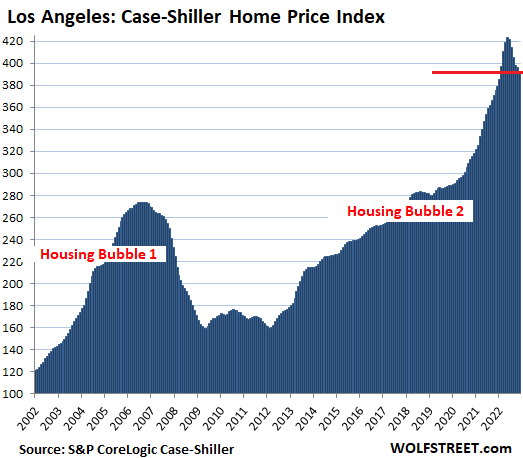

- Los Angeles metro: -7.4%

- Las Vegas metro: -7.0%.

- Dallas metro: -6.6%

San Francisco Bay Area: The index for “San Francisco” covers five counties of the nine-county San Francisco Bay Area: San Francisco, part of Silicon Valley, part of the East Bay, and part of the North Bay.

- Month over month: -1.6%.

- From the peak in May: -14.4%.

- Year over year: -1.6%.

- Lowest since June 2021.

- Prices plunged faster than they’d spiked:

- Down in six months from peak in May: -56.8 points

- Up in six months to peak in May: +53.4 points.

In the Seattle metro.

- Month over month: -1.5%.

- From the peak in May: -13.5%.

- Year over year: +1.5%.

- Down in six months from peak in May: -55.9 points

- Up in six months to peak in May: +61.4 points.

San Diego metro:

- Month over month: -1.4%.

- From the peak in May: -9.9%.

- Year over year: +4.8%.

- Down in six months from peak in May: -42.5 points

- Up in six months to peak in May: +60.1 points.

Phoenix metro:

- Month over month: -1.9%.

- From the peak in June: -7.7%.

- Year over year: +6.3%

- Down in five months from peak in June: -26.4 points

- Up in five months to peak in June: +36.1 points.

Denver metro:

- Month over month: -0.8%.

- From the peak in May: -7.5%.

- Year over year: +6.1%.

- Down in six months from peak in May: -24.8 points

- Up in six months to peak in May: +42.6 points.

Los Angeles metro:

- Month over month: -0.9%.

- From the peak in May: -7.4%.

- Year over year: +4.4%.

- Down in six months from peak in May: -31.2 points

- Up in six months to peak in May: +47.8 points.

Las Vegas metro:

- Month over month: -1.7%.

- From the peak in July: -7.0%.

- Year over year: +6.6%

- Down in four months from peak in July: -21.1 points

- Up in four months to peak in July: +25.5 points.

Dallas metro:

- Month over month: -1.1%.

- From the peak in June: -6.6%.

- Year over year: +10.9%

- Down in five months from peak in June: -20.3 points

- Up in five months to peak in June: +39.4 points.

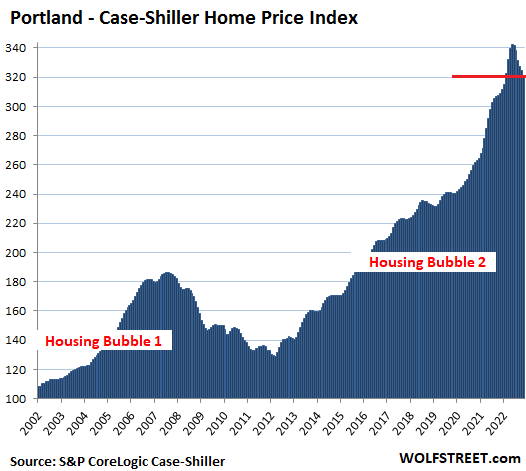

Portland metro:

- Month over month: -0.9%.

- From the peak in May: -6.1%.

- Year over year: +3.9%.

- Down in six months from peak in May: -20.9 points

- Up in six months to peak in May: +33.1 points.

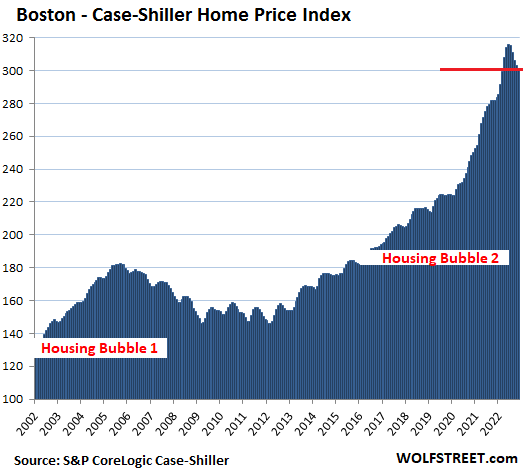

Boston metro:

- Month over month: -0.7%.

- From the peak in June: -4.6%.

- Year over year: +6.9%

- Down in five months from peak in June: -14.6 points

- Up in five months to peak in June: +30.2 points.

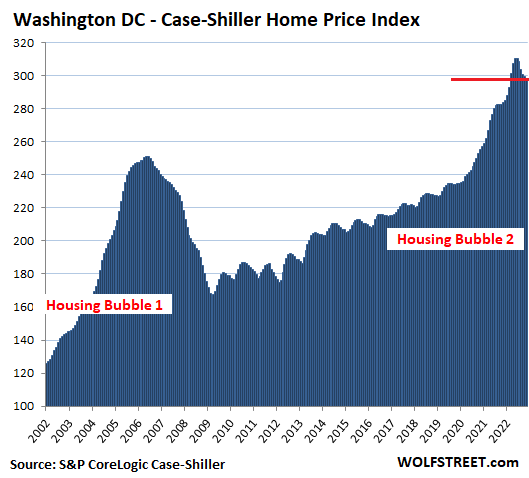

Washington D.C. metro:

- Month over month: -0.3%.

- From the peak in June: -3.9%.

- Year over year: +5.3%

- Down in five months from peak in June: -12.1 points

- Up in five months to peak in June: +22.4 points.

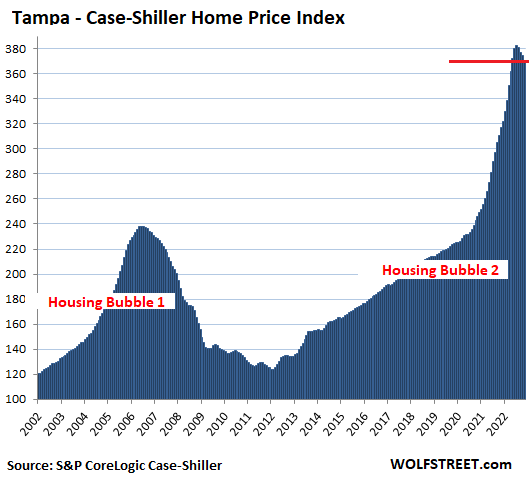

Tampa metro:

- Month over month: -1.0%.

- From peak in July: -3.1%

- Year over year: +16.9%

- Down in four months from peak in July: -11.8 points

- Up in four months to peak in July: +31.4 points.

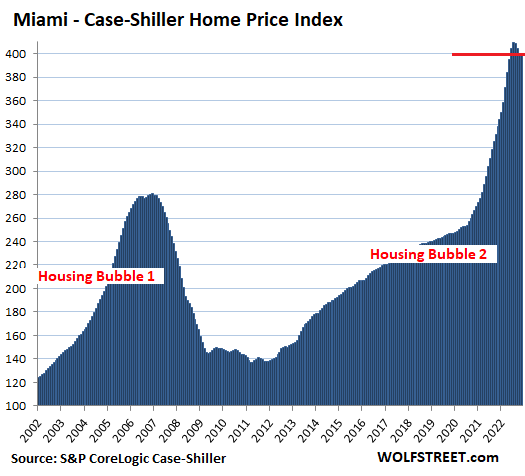

Miami metro:

- Month over month: -0.2%.

- From peak in July: -2.3%

- Year over year: +18.4%

- Down in four months from peak in July: -9.6 points

- Up in four months to peak in July: +37.8 points.

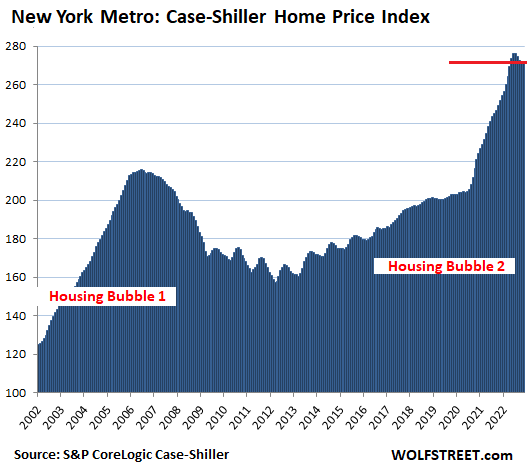

In the New York metro:

- Month over month: -0.1%.

- From peak in July: -1.6%

- Year over year: +8.1%

- Down in four months from peak in July: -4.3 points

- Up in four months to peak in July: +12.1 points.

For the Miami metro in November, the Case-Shiller Index had a value of 400 points. All Case-Shiller indices were set at 100 for the year 2000. This means that despite the recent decline, Miami house prices are up 300% since 2000. This makes it the #1 in terms of price increases since 2000 in the Case-Shiller Index.

Los Angeles and San Diego occupied at different times the #1 slot, but prices have dropped faster in them than in Miami. The index value for Los Angeles dropped to 392 and for San Diego to 385.

In the New York metro, with an index value of 272, house price inflation since 2000 amounted to 172%. This makes it the bottom end of the Most Splendid Housing Bubbles.

In the remaining six metros in the 20-City Case-Shiller Index, house price inflation since 2000 has been quite a bit less, and they don’t qualify for this lineup. Home prices have dropped in each of them for months. In the “November” index today, prices dropped further, month to month: Chicago (-0.6%), Charlotte (-0.7%), Minneapolis (-0.7%), Atlanta (-0.6), Detroit (-0.4%), and Cleveland (-0.7%).

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Just another reminder that these are the four most expensive words in the English language: “this time is different”

Here I thought they were “will you marry me.”

No, but related: “honey, I am pregnant.”

All of which fall under, “Trust me, it works!”.

Or “love you long time”

Still wrong. The right answer is “I want a divorce.”

Mario wins 🥇 🏆

Educated,

Nah. No one says “I want a divorce” without someone first saying “will you marry me.” “I want a divorce” is simply the blow-off top following all the expenses associated with “love you long time,” “trust me, it works,” and “honey, I’m pregnant.” ;-)

lol all too true, at least in the US and Canada, divorce courts are a profit center and huge money-making opportunity for both the lawyers and state. It’s why American divorce and family courts are the most expensive and financially ruining in the world, it’s another kind of business here and in the common-law countries. And since most American marriages wind up there, it’s unironically true that everything from “will you marry me” will wind up being a terribly expensive mistake for most Americans with good options.

One of my old teachers always said that if an American has assets and a good career, but wants to get married and have kids, the best thing to do is to go expat, because the divorce wrecking-ball in America will undo all your careful financial planning, savings and hard work. Some Americans even get jail terms if alimony or child support can’t be paid (and the courts can impute any random amount, based on a high-earning year in the past that can’t be repeated–the case of Robin Williams). Civil law countries (basically Europe outside of UK, plus South America and most of Asia) still have the boring idea that divorce shouldn’t be a profit opportunity, custody should be shared and everything should be done thru mediation, so you don’t lose your shirt. Sounds quaint over here.

For individuals, yes this can be true, but for a population of people trying to get rich quick or keep up with their neighbors’ putative wealth, you can’t beat “this time is different”

Question: “Do you know what the two most expensive words in the English language are?”

Answer: “I do.”

Actually, if one can manage to retire early and keep the wife working, you get free health care and lots of free time. The wife will still do laundry on the weekends if you try it once and screw up a few blouses.

@Bobber, too funny!

My beloved refuses to stop working bobr:

4 days a week at her preferred pals and people place; two taking care of her last parent, now 92.

I TRY to do as much in support as I can do without more pain, so not so much….

IMHO, the more you can do to HELP,,, in this case HELP all folks in your domain, (( of course doing less for those farther from the center of that domain )) ,,,

THE more YOU benefit, both in keeping the feet moving, apparently, from the currently available literature,

THE best,,, very best indicator of health and happiness

( Serious apology for my last post/comment that lacked final concept, no doubt due to adult onset attention deficits, etc.)

That comment lacked the closing warning/long time practice: ””’When ever at all when driving alone, ,,, starting to ”nod”,, pull off and let healing sleep go on FOR WHATever;;; sometimes 20 mins., sometimes 2 hours.”

Bobber, I see you know that old laundry trick too!

It worked for me thru two divorces and a deceased wife. Single now and having to do my own laundry. Sucks!

Just a data point: In the last week or so, some houses I track in the Phoenix area experienced an increase in their Zillow Zestimate. The first since May 2022.

Zillow-algo seasonal adjustment?

From the people I’ve talked to activity seems to be slightly picking up again. Seems to make sense with financial conditions loosening up.

I’m thinking short lived though but we’ll see

Financial conditions aren’t getting better. And who listens to Zillow. How quickly people forget. Zillow got out of the home buying process admitting they don’t know what they are doing. Financial conditions are bad unless you listen to Wallstreet propaganda. They tell you it’s good, and you fall in lockstep. No thinking person believes things are good.

Fed up

I’m only talking about financial conditions in the sense of the Chicago Feds measure for it. Takes into account interest rates, leverage, risk, and access to credit I believe. It loosens with every bear matter rally…hence why the Fed has to squash these rallies

I think the world is in a continued state of crisis personally

Inventory for beginner homes is still tight. High end and move up homes are more readily available. Supply/demand in action. And ~6% mortgage rates are manageable on low end homes.

When nominal GDP growth is 9% and the GDP deflator is 7%, who really know what is really going on. The margin for error in the deflator is huge, which renders the GDP numbers useless.

To be anticipated — there’s always those buyers/true believers who were looking hard from the sidelines and take the plunge irrespective of fundamentals. The psychology at work behind rationalizing away these kinds of bad decisions has more twists than a barrel full of DNA.

From a stock broker to a client: “You can’t get hurt” are the 4 most expensive words ever muttered.

Followed by “Buy the F…..g Dip”

That too, especially in such an overinflated housing bubble, everything bubble, speculative market, those 4 words usually turn into “catch a falling knife”

oh yes, along with “stocks only go up”

I wish that the 1980s inflation measures (pre-manipulation) were available to graph against these prices for those years. I suspect the annual price rises shown in many cities would be much less than they appear if adjusted for the real level of inflation.

For housing markets, these four words are more relevant.

FOMO = Fear of missing out

YOLO = You only live once

and soon to come

FOGO = Fear of getting out

FOGO synonymous with HODL

POGO: “…we have met the enemy, and he is US…”.

(…oh, where art thou, Walter Kelly?).

may we all find a better day.

And….angle of ascent equals angle of decent. Peaks and troughs are for the fortuitous few.

1) C/S : on the left every city start between 110 and 120.

2) On the right, every city ranged between 300 and 420. ex NYC.

3) They all reached the same target after a deep/ shallow plunge in

2011/12.

4) NYC loaded with the 0.1% of wealth was behind the curve.

5) For two decades the average C/S inflation rate was 6% :

120 x (1.06^20) = 120 x 3.2 = 385.

6) A house bought in 2002 for 120 was sold for 385 in 2022…

Spot on that housing is inflation and correlates close to 1.0.

However, I remember reading inflation (and housing) runs approx. 4.25%.

and inflation since 2002 runs at 2.4%

Starting at 120 at 4.25% a house should be around 275, and at 2.4% = 200.

Here in the bay area 275 would be back at Jan 2020. Seems fair!

When it’s over (2025’ish) and even if we get back to 2019 pricing, SFH for Americans is still gonna be a crapshoot.

Thank God for all the multi-fam construction I guess. I would not be surprised to see homeownership drop below 50% in the USA by 2030.

“I would not be surprised to see homeownership drop below 50% in the USA by 2030”

You’ll own nothing and be happy!

Home ownership is not a right, and it’s not a great fit for everyone. It’s actually a lot like college!

Gattopardo,

Actually, home ownership (ie: private property) is a God given right. It was recognized by the founders of the USA.

“We hold these truths to be self-evident, that all men are created equal, that they are endowed by their Creator with certain unalienable Rights, that among these are Life, Liberty and the pursuit of Happiness*”

* That last item,” the pursuit of happiness ” is not a God given right. They wanted to say “and the ownership of private property ” but they were concerned about including that phrase due to slavery.

The Biblical origin comes from when God gave Abraham the title deed to the Promised Land in Genesis in perpetuity.

Motorcycle Guy, I’m wondering if that original deed was recorded or not? And notarized? I understand that Bathsheba was a registered notary, but she didn’t live in the same neighborhood and showed up about 1000 years later.

Let me guess — you’re a mom-n-pop landlord…

But then, it’s bizarre that anyone should “own” land. It’s unownable. The only domain over which you wield proprietorship is your soul; your ideas and feelings. Everything else comes down to temporary custody.

Housing in these bubble markets wasn’t reasonably priced in 2019. It won’t be cheap at anything near current prices in most or all of the country either once interest rates “blow out”.

It’s a long-term process.

Some places in GA I looked at today are still in the $20-30K range as I remember them being quite a few years ago, when considering an investment there.

Of course they will be ”fixers” or tearer downers, but if not fixable reasonable, ya can almost always live in them for a bit, while building a house or just bring in a double wide for around $20/SF.

Course there’s nothing at all close to reasonable in the booming areas, as always—YET.

Hopefully this comes to areas with low new builds and inventory rises.

My family is priced out of moving from our current housing market in PA. Any inventory on the market is overpriced or low quality.

Financial conditions aren’t getting better. And who listens to Zillow. How quickly people forget. Zillow got out of the home buying process admitting they don’t know what they are doing. Financial conditions are bad unless you listen to Wallstreet propaganda. They tell you it’s good, and you fall in lockstep. No thinking person believes things are good.

Industrial Massachusetts here: Any inventory on the market is overpriced AND low quality! $475,000 for a 1,200 SF home that hasn’t been updated since the ’90s is pretty standard Zillow fare these days.

Wow, up here in Canada that would be a steal! The housing market here is so beyond insane that the same old 1200sf place in a Vancouver suburb would be priced well over $1 million CAD, and would have got it 8-9 mos ago. (A Vancouver starter detached home, barf). My sister lives in one.

US housing needs 50% drop; Canada (Vanc/Toronto) needs 75% drop to approach affordable again, something it hasn’t been in 20 years.

The talk or hype from mainstream media lately is the tick up in mortgage application because we all know interest rate is so low now..I wonder how that will show up in this chart later if at all.

Anything to drum up that demand…do see asking rent trending down in decent area. On the other hand there are still nut jobs asking for the moon. Saw a 2400 Sq ft house for rent asking for $7k in freaking Chino…delusional much?

Sounds like bagholder who realized they can’t sell their overpriced asset for a million dollar price tag anymore, and so that’s the rent they need to collect to break even… hard to have sympathy for some people sometimes

He is asking double the market price. Good luck to him. He must be desperate.

The usual cheerleaders are still in total denial, e.g. realtors, real estate investors, and those who purchased from Q4 2020 to Q1 2022. I forwarded Wolf’s last article on this topic to a realtor friend (the one that says, “this is not seasonal sweetheart,” right under the title). Two minutes later she responded and said, “it’s seasonal.” My response? “RTGDFA!” as Wolf so elegantly puts it. As a private money lender that funds real estate investments, I get daily entertainment in the form of new loan requests where other private lenders that loaned 90-100% of those overinflated prices in 2021 and now they want me to refinance them out of their bad loans. Pure comedy. And with rates to increase more in 2023, basic economics tells us that if bond yields continue to increase as a result of the rate rises, all other asset prices will fall. I recently read a book written in 2021 by Alasdair Nairn called, “The End of the Everything Bubble.” Funny how much of what he predicted in 2021 has been unfolding over the last year. How far down will real estate prices go? That’s the billion dollar question I guess! But for now, I’m declining more loans than I’m approving and I funded almost nothing last year. Only time will tell, so for now, we wait!

1stTDinvestor

These people who used to pandemic and the suffering of millions of people to try to speculate and flip houses and make quick buck deserve what they get. And, frankly I don’t give a f$ck about their problems.

There’s a ton of these parasites here in orange county CA, along with an endless supply of Chinese buyers. Homes don’t last long and prices haven’t gone down since July. No sign of the bubble bursting here.

Kal,

“Orange country”… “prices haven’t gone down since July.”

LOL. Median price, Orange County, per California Association of Realtors, -14.6% from peak in May:

You mean all of the corporate real estate investors who have been trying to turn homes into stocks?! Many are losing their @sses and I like you, have zero sympathy. They helped keep inventory low which drove up the prices so high in some of the markets on this list.

What pct declines is this guy predicting?

Practically every bubble claim I read grossly underestimates the level of insanity.

As an example, a 50% decline in the S&P would still leave it above the March 2020 low.

That’s not nearly enough to correct the excesses since at least 1995.

I’m a REALTOR- Northern AZ. Sellers are not realistic now; they want what they could have gotten a year ago and that’s not going to happen. Buyers smell blood in the water and reflect that in their offers. Both sides will eventually return to some sort of equal/common ground as this selloff settles down. 2023 will be very interesting as more REALTORs exit the business due to lack of sales. That adjustment is needed.

I bought a house in Tucson last fall, to live in while I build a house. The Zillow search I used- houses, townhomes, and condos under 400k had 1400 or so listings last Summer. Since then the numbers have dropped steadily and are now at 736. I don’t see any change in the asking prices. Some houses I had my eye on have gone off the market but not sold. The housing bubble may have popped but sellers here haven’t gotten the memo yet.

People who don’t have to sell won’t sell. But some would be forced to sell and these would define the new pricings.

We do need unfrozen/liquid market ( aka suckers ) for price discovery to happen.

A lot more people will be forced to sell than most people currently think.

Not selling doesn’t mean the value hasn’t fallen

JR, duh. Listing counts are always much lower in Jan than in July.

Not in Tucson…

Next move is, pull it off the market and relist later because in their mind 6 months later, FED will pivot, mortgage rate will be at 4% and bam, back to the moon price we go. Catch a falling knife is never in their dictionary, should be good to see bloodbath coming.

Doesn’t help that, these same sellers hear MSM hyping up mortgage application is going up (nevermind the bulk of volume is from re-financing, although new purchase did tick up as well) so that provides all the wind in their sail to continue the delusional asking price.

Home builders stocks have gone up quite a lot and are touching all time high literally.

Either we are not seeing something , market is seeing or market is wrong.

“Either we are not seeing something , market is seeing or market is wrong.”

Market participants are idiot humans subject to FOMO and associated financial illiteracy, so yeah, mkt is wrong.

People are so sure the FED won’t punk out.

Howard Marks recently had an interview where he said markets have been distorted since Greenspan and always rush to the rescue.

Marks said the FED will stop doing this and the inverviewer asked “Why?”

Will the FED really change??? The market is addicted to free/easy money.

J. Powell talks tough, but will he stay strong?

Economy be damn.

They have to defend the dollar by keeping rates up. Wall street is currently fighting the fed which is very interesting. Wall street doesn’t care about the dollar. They just want bull markets. Will the fed acquiesce by easing when it is clear that the economy has stalled out as the print and spend has slowed down?

Look into what OPEC+ and the Gulf Cooperation Council have been talking about openly. The petrodollar perhaps have only a few good years left.

“This time is different”.

The difference is inflation. We haven’t had inflation like this since the 70s. Sure, you can have negative rates when inflation stays at 1-2%. Why not? Everyone loves free money.

But when inflation hits 10% (or 20% in some EU countries) you can’t keep doing it.

I have no doubt that when inflation eases, Powell will be pressured to lower interest rates and let the good times roll again. But I believe people are way too unrealistic about how long that takes. It will take years, because the inflation mindset has now set in, and it takes years for that to change.

@Lune

See —> Arthur R. Burns…

J. Pow wants to be Volker for sure…

…but is he really tough enough?

99% chance of 25 basis points for today (according to market).

He should stick them with 50 and /Flex

He doesn’t want to have to be Volcker. He wants to get inflation under control before it blows out entirely, like it did under Volcker, and forces him to do what Volcker did. That actually came out today in the presser.

There’s 50 Realtors for every listing in the 3 Zip Codes where I live. It’s time for these people to find another profession.

“profession”

That’s funny!

They will. I remember the crash in 2008 slimmed the flock down big time

I’m in an industry that functions like real estate. The trouble is, there’s 10% that are true professionals who take pride in their craft, with the other 90% rushing in to make money in the gold rush

Why not become a Realtor to buy so you keep part of the commission?

Some might be investors that just want early access.

Surprise interest rates affect housing. The higher they go the less house folks can afford and vice versa. The longer rates stay higher the slower the economy becomes and as Federal Debt is rolled over from low rates to much higher rates the Federal deficit will climb by billions. Fed debt averaging under 2% now and can double or triple depending on “Higher For Longer”! Will be ouch time for the federal gvt if there is a recession with declining revenues and their average interest rate is 4 or 6%.

1) RE is a risky business loaded with ups and down. When it’s up it’s fun.

2) At the bottom of the next recession home buyers would like to have at least an annual rate of 6%/Y in the next 7 years.

3) Price have to drop from 385 to : 385 x (0.94^7) = 385 x 0.65 = 250.

4) 10% for 7 years : 385 x (0.9^7) = 385 x 0.5 = 192.

5) 12% for 7 years : 385 x(0.88^7) = 385 x 0.4 = 154.

6) Are they crooks : no, that’s the Buffett way!

Or, prices stay inflated and wages go up. People are switching jobs like crazy and employers in some no-skill industries can’t even get any applicants at $20.

Anecdotally stepped back as a buyer in the low end of the suburban NYC area market, have had buyers agents contacting me in the last two months that wouldn’t give me the time of day back when I was desperately seeking an agent in 2021, but apparently kept my contact info. There must be some degree desperation for them to be digging my # up now, still, not a single listing on the MLS worth taking the time to even look at.

Lili, realtors riffling through old client lists may be a leading economic indicator. You should apply for a copyright.

Definitely the right direction but just looking at those charts shows how crazy far they still need to drop just to get back to 2020 levels which were already insanely high.

Thinking there may a soft landing in sight for real estate. Sure they are dropping but when will the prices level off and then begin the slow climb back upward. Perhaps that pesky FED and their hooligans planned this all along

Funny. I built our place {retired land 4 acres rura} to appliances 370k cash. Saved up for nails and boards. Can’t understand why people would drive themvelves into debt for a place to live. Rented in slums when we could afford it. Oh well.

How long did it take you to save up $370k?

10 years.

That is awesome. Very impressive.

Ah yes, the classic take: “I don’t understand why you’re having trouble, I had a giant pile of money and it was easy. Just get a giant pile of money.”

Where did you live for those 10 years, bud? Also, $370k won’t buy crap in 10 years.

Rentals bud. Sweat equity they call it. Do the math , that is what it would cost me in interest on a Mcmansion. No way Jose. Rather live in a tent. Anyhow got a nice 3 story home and am pleased with it.

Seeing lots of flips flopping but only tiny price cuts so far. Also seeing a lot of construction bros rehabbing old places but don’t know the music stopped over a year ago. Condo complex about a half mile from me had a sale every few months during the bubble that was about 50k more than the previous sale. Now they’re trying to get 50k less than the last sale and no bites.

Real estate moves very slow, like watching paint dry.

One needs to wait few more quarters for things to become clearer.

ATM, the ball is in FED’s court and I am sure FED would come out very dovish to please their rich friends.

‘House prices must come down so Americans can afford houses’ Jerome Powell

Playing the pivot mantra won’t make it happen.

Just had a flipper call me today asking if I would sell. Told him I can’t afford a new home now, so nope. :)

I had a flipper call me yesterday regarding a house I sold in 2021. They must be getting desperate.

Anyone notice Toll Brothers stock is up and seems to have bottomed.

I thought with slow sales they must be hurting.

Then i read the plan on selling 8000 to 9000 homes in 2023 but they have about 7k multi family units they built, rent and manage plus they have 17k multi family units in the pipeline that they plan on keeping and renting.

I guess they want to be a landlord now? I wonder if they will become a REIT.

What i find interesting is they are building more apartments in the near future than their luxury SFH?

I have indeed noticed. SO tempting to short.

The drop is real but how far do you guys think prices can drop. Keep in mind that RE has historically risen in high inflation environment for obvious reasons.

Also keep in mind that all costs are way up now: construction, material cost, labor cost, utility cost, insurance cost, maintenance cost, energy cost, permit cost, etc. There may be hiccups in sale prices due to Fed’s games, but how can prices fall in the long term when all input costs are way up, and will keep going up.

Also any arguments that prices are set by buyers and not input cost is not valid. If buyers cannot afford all that will happen is there will be less supply over long term and housing will become luxury. But no rational person would build home and sell at loss.

“But no rational person would build home and sell at loss.”

LOL. That’s precisely what homebuilders did during Housing Bust 1, and the industry nearly collapsed. Funny how memory is short.

What you need to keep your eyes on is their inventory of unsold homes, which has exploded to Housing Bust 1 levels. That’s where their costs are; and their sales prices will come from whenever they close the sale of that inventory at whatever price they can get, including incentives and mortgage rate buydowns.

Ha, I think Wolf secretly enjoys bashing his head against a brickwall. Trying to get Kunal to understand the non-housing humpers view even after you throw out countless other data, trends is like trying to get Lawrence Yun to admit market will adjust down 20-40% over next couple of years or getting Pow Pow to come out and say he is actively trying to cause a recession..

I mean I like to ride on my magic Alicorn too but probability of that happening likely pure fantasty…

“It is difficult to get a man to understand something when his salary depends upon his not understanding it.”

-Upton Sinclair

Wolf, re: Kunal’s serious disconnect from economic reality, I am living proof that “rational person would build home and sell at loss”. I DID. And I ate SEVEN FKN FIGURES ON IT.

Prices ARE set by buyers, that’s what a market is, they don’t care about “input costs”, no one who buys anything cares about that. The market price is what a buyer will pay,

Home builders have a year or two lead time typically on most projects. They are betting that prices won’t decline while they build. If they do, they sell for whatever they can get. And yes, they will stop building if they lose their shirt in a down market. May even go under.

But the market price for a home is what the buyer will pay. Period.

Happy1–

Not to defend Kunal—-but some of those buyers ( such as in the luxury segment) will price out their new custom home to build, and will be startled at the quoted cost to build. So some of them will shell out decent money for an existing home

Renter here. My verbose take.

I don’t think its so simple as seller sets the price or buyer sets the price. I mean aren’t prices usually negotiated ? Except in more extreme “sellers” or “buyers” market.

Seems it depends on the characteristics of the seller and buyer. More accurately sellers and buyers.

For instance:

1. If seller must sell then buyers mostly set sale price. Especially if they somehow are made aware of sellers situation.

2. If buyer must buy … soon… not likely to bargain hard. Or if FOMO has set in, right or wrong… seller(s) not likely to negotiate much. One can argue sellers are mostly setting the price.

3. Sellers and buyers wealthy… neither needs to negotiate. If too far apart no transaction.

Just a few of the more common (?) situations I suppose.

The 2021 to spring 2022 timeframe was a sellers market by all accounts I have read. FOMO a part of that.

When I bought the only home I ever bought in 1986 it might have been a buyers market of sorts but I was too ignorant to know it.

New construction everywhere (north of Dallas). I was about to close on a new home when a realtor called and suggested I look at another new home, different subdivision.

I switched and probably could have negotiated for a better deal (e.g., interest rate buydown or landscaping, etc) but didnt.

One could argue indefinitely over this sort of thing but it seems there are times when buyers (sellers) or just this particular buyer (seller) feels more compelled to give a little on price than the the other participant.

And each buyer, seller is unique.

In a so called sellers market there can be sellers who need to sell right now.. less negotiating room than the typical seller.

Ditto the buyer who needs to buy even though its a buyers market… not likely to drive as hard a bargain as the current group of buyers.

It does not matter how much is the input cost. What matters most is affordability which is defined by mortgage rates and wages.

BTW, during last inflationary period, home prices were not in bubblicious territory, so it is not apple to apple comparison.

Is there more of an eye on investment properties now from more people? Gone are the days of the late night infomercial hocking the real estate riches course, now everyone everywhere talks non stop about buying additional houses to let. So that might get outside of the wages part of the equation.

I was starting to miss you there…it’s just not quite the same without counterpoint..

I don’t think anyone needs to keep that last paragraph in mind. The income of potential buyers needs to go up to sustain higher prices. Input costs don’t factor into that. Buyers don’t care how much it costs to build or remodel a home, the issue is affordability.

Then the buyers have to adjust their expectations to what they can afford.

Too many people with champagne tastes and a beer budget bemoaning the “affordability gap” because they can’t have a HGTV dream home.

As an aside, I don’t give a rat’s patoot what my house is worth on a daily basis. Not selling it at this point, so it’s just like a pair of socks: it has a utilitarian value. It’s a place to live.

Or, most likely, sellers will have to adjust their selling price to what buyers are willing (and can afford) to pay.

Too many sellers think that their house is “special” when it’s a 60 year old tract home, just like thousands of others.

Actually, expectations are adjusted automatically, because expectations are irrelevant in the sales price of homes. Buyers are always limited by what they can afford, regardless of their expectations. A seller doesn’t care about a buyer’s expectations, anymore than a buyer cares about what a home cost the seller. It’s the prevailing price in the market that matters.

I can’t say I’ve noticed people bemoaning they can’t have a HGTV dream home on a beer budget. Though I suspect lots of people want a nicer home than their budget allows. If they choose to stay out of the market because their beer budget and high expectations are not in alignment, that’s their choice. I’m not going to worry about it.

I always enjoy your comments, EK, but living in a pair of socks? I’ve heard of living in a shoe. BTW, does that pair constitute a duplex?

A lot of the product is champagne prices on beer construction. Staple guns, plastic wrap and plastic siding made in China.

Lumber peaked months ago and is now down 50% from peak depending on type.

I can’t imagine it stabilizing until the all-in monthly payment (including a typical mortgage and taxes) drops below what it was at the start of 2022, and realistically below start of 2020, inflation adjusted. That market was already operating in bubble mode, as everyone who could possibly qualify for a 3% mortgage was fighting over a limited supply of RE that was going up by a lot more than 3% per year. At 6%, there’s no financial incentive to buy more house than you can safely afford; you can still hope to sell at equivalent value someday, and in the meantime you did get to live there, but the days of straight-up printing money in the form of home equity are over.

You keep on posting as if housing being a “necessity” will keep prices from dropping or dropping more than certain amount.

Inflation doesn’t have the implications you think either. There is no mechanical effect.

The precedent you are attempting to use is the “70s” (actually late 60’s to early 80’s). Prices were a lot cheaper then vs. now. It’s not even close.

Look at those charts. Even under the mechanical model you are trying to use, higher interest rates will continue to decrease affordability.

Housing IS a necessity – just not “necessarily” a SFH (anymore).

I’m a Sanibel Island refugee living in a 1BR apt in Ft Myers FL and it’s gorgeous and close to everything for 50% the cost of the Sanibel condo I was living in before Hurricane Ian.

Crap box urban apts are still around, but new builds and rehabs with nice amenities are more plentiful than in the past.

Maybe the American Dream does not include “your own home” anymore ?

Loved that area, kept my boat at 10,000 islands. Too bad it got pounded. Sorry dude.

Kunal,

“How far….” as far as the free market allows it. Refer to housing bubble 1, or previous historic price manias (Tulips for example).

“Construction costs way up…” I work in construction and I can tell you 80% of our raw materials are now down 20-50% of where they were last year. Labor costs are 10-15% higher than last year.

“How can prices fall….” define long term. 20+ years? Ever heard of the lost decade?

For the majority of individual home buyers, monthly price is what matters. Period. Most people cannot make a home purchase decision without knowing what they’re monthly payment is. At the moment, rates are too high, and prices have not come down to meet the higher rates for the monthly payment to be equal to what it was in 2021-2022. Rates are not coming down anytime soon. So naturally, prices will. It’s a very simple formula. Try it in Excel.

Your other comment about prices not set by buyers is not correct. Just re-read what you just said. If strictly input costs set prices, then Apple wouldn’t be the dominant company they are. If strictly input costs set prices, then companies wouldn’t have the ability to charge different prices for essentially the same products. Prices are set by buyers, period. You can make something and put it for sale at $500, but if no one buys it, you would need to keep lowering the price to see who buys it. You didn’t intend to make your product in order to sell at a potential loss, but that is the name of the game. You won’t know until you do it. If buyers cannot afford something, either with cash or financing, guess what happens, they don’t buy it until they save more money, get better financing, the price drops, or a combination of it all.

Just look at the data and make an objective analysis.

Your $500 example makes sense.

Then again if the seller gets whiff that lots of people can pay more than $500 the seller will successfully sell at some price in excess of $500. Especially if this person doesn’t necessarily have to sell the product in the near term.

I have another post claiming in general it doesn’t make that much sense to say either seller or buyer always sets the price.

Usually both do but circumstances dictate who has to or is willing to yield the most.

Heck a rich person might value her time much more than $10k or even $50k. Whether she’s a seller or buyer she might just want to get the transaction over with. I don’t know any rich people but imagine that could be true for some of them at least occasionally.

And homebuilders are soaring, as if the market anticipates a return to 3% mortgages.

Bankruptcy stocks soared too. My two favorite bankruptcy stocks more than doubled (CVNA and BBBY). There is no meaning to any of this except that people are trying to make a quick buck by buying the dip and selling before the bottom falls out again.

I cannot tell you how many stories i read or people i talk to say they are all in as soon as the Fed pivots.

Some are trying beat this crowd by buying before the Feds pivot.

Honestly, we did not see enough pain in the markt drop for people to capitulate. not enough speculators have been wiped out.

Here is an example from WSJ

Abhas Gupta, a 41-year-old entrepreneur in Irvine, Calif., said he moved his whole equity portfolio into Tesla shares in 2018, enamored by its electric cars and promise of disruptive innovation. Last year, he lost his entire seven-figure retirement fund after taking out margin loans and using options to turbocharge his bets on Tesla, he said. Still, he said he is far from calling it quits.

“I basically burned a lifetime’s worth of wealth, but none of this has shaken my confidence in the company. There is just no company even remotely close to Tesla on innovation,” Mr. Gupta said.

“Why would I invest in a basket of dinosaurs?” he said of the S& P 500.

Mr. Gupta said he is aggressively buying long-dated call options on Tesla. Call options give traders the right, though not the obligation, to buy shares at a stated price by a certain date, while put options grant the right to sell.

The animal spirits are still alive. Here is another example:

Nicki Bourlioufas, 51, said she bought shares of Advanced Micro Devices Inc. and Nvidia Corp. last year, then refrained from adding new positions as those semiconductor stocks struggled. The financial public- relations consultant said she is looking for opportunities to pick up shares of Tesla, along with Microsoft, Apple Inc. and Alphabet Inc.

“As soon as there’s any hint that interest rates will be cut, then I expect tech stocks will rally and I’d like to be there and positioned,” she said. “I use their products and I’d like to also reap their profits.”

We close tomorrow on what we determined to be a deal for my western zoom/retirement playtown. I expect valuation hits over some years, but, for the sake of shelter and enjoyment, I don’t care and probably won’t notice in 5-8 years time. We worked on the seller hard and he came to play ball (knew what was coming). Happy enough.

Thank you, Wolf!

This is timely. I forwarded your link to some close relatives who are thinking of buying in Denver and Las Vegas. You will soon get some new fans.

From an engineering perspective, this is awesome data. Notice the peak-to-peak period is 15 years with each consecutive peak is >50% higher than the last.

I will use this data to buy in 2029 and sell in 2037 with astronomical gains. 2037 should be the peak of HB3 and will be 50% higher than this one! :-)

“As early as 1876, Henry George observed the curious cycle through which real estate markets inexorably move.”

Haha, you’re 150 years late to the party!

https://extension.harvard.edu/blog/how-to-use-real-estate-trends-to-predict-the-next-housing-bubble/

On catch, SIABB….inflation will make that 50% gain about…oh, 0% in real terms.

;-)

LOL, when I first read your comment I thought “what is the ETF SIABB shorting?” Now I get it.

What will eggs cost in 2037? $5 each?

Only if wage inflation drives your wages up to $1M per year.

Back in the 1960’s my dad took his first engineering job at an excellent salary of $8K/year. His first mortgage back then was about $2K/year. He should have kept that house and rented it.

Time and inflation can be your friend and enemy.

I was being facetious with the egg comment. Since the vast majority of people trade time for money, I don’t see much benefit from inflation.

Hey, about 6 months ago I posted that I thought the top 3 would be Phoenix, Vegas, and Dallas. Looks like

I was pretty close! Just wanted to toot my horn.

Phoenix: -1.9%

Las Vegas: -1.7%

San Francisco: -1.6%

Seattle: -1.5%

San Diego: -1.4%

Dallas: -1.1%

Tampa: -1.0%

I remember buying my first home in 1980 at 12% mortgage rate. Heard “we will never see 6% interest rates again” WRONG.

Sold my house 2 years ago and moved to an apartment, 1st time living in 1. Now know my retirement home in AZ will not be 3900 sq ft. Don’t need it after living 2 yrs in an 1100 sq ft apt. (thinking 1500-1700).

Have a spreadsheet & have been tracking homes in a certain AZ subdivision. Avg price has dropped ~$ 40K since end of Oct. Just waiting for another $30K to drop & then I’ll buy. Sorry to say someone is always dying & their kids are selling their house. The homes that haven’t sold have been on the market 3-6 months. The higher the asking price the steeper the drop.

According to @Seen It All Before, Bob I’ll leave instructions for my Kids to wait until 2037 to sell.

If home builders can’t sell they will rent. If rent drop they can’t pay the banks. If they hike, vacancies will rise. Vacancies are RE curse. Once the vacancy rates rise beyond a certain threshold, they will become empty malls.

The banks will takeover the leftovers, become a matchmaker, and sell at 50% – 60% discount.

I just looked at a very large new build in Skagit County, WA. Good quality but not worth the $1.5M asking. No water or mountain view. 60 miles from Seattle in a rural area. Still needed $50k in work to make it amazing. Only 1.33 acre instead of the typical 5 acre lot there. My realtor was all excited until I said no more than $1.1M. It went pending within a week for asking. Still lots of FOMO delusional buyers up here.

We need these fomo buyers to keep the market liquid and this enable price discovery.

If the market is completely frozen then no price discovery at all

Some rivers flood there. Nooksack for instance.

Worse yet… wildfires are showing up in more and

more parts of Washington state.

I live in eastern Washington.

After the last 6 years of wildfires through out

California, Oregon, Washington, Idaho and

British Columbia we all (should) know what

AQI (Air Quality Index) stands for.

Majority of homes in Malden small town 50 miles south of here got burned down 2 summers ago.

Hoping this summer and fall will have less fires.

Especially Washington Oregon and Idaho.

Correction: Actually Nooksack River is in Whatcom County I believe just north of Skagit.

Some bad flooding a year or two ago in

Sumas and south.

The symmetrical shape of each cities boom and bust of first housing bubble might foreshadow what is coming next. Fast up/fast down. Slow up/slow down.

Most likely true. And if so, this one will be a doozy. People will not believe what happened in 2-3 years.

To all the house humpers out there, this is a question that I have been asking myself and I just can’t seem to overcome the math other than these people truly think housing will go up 10-20% every year and they will never end up in a situation 10-15yrs later, their house is back to the same price.

Case in point, looking at houses in SoCal, most decent houses in OC/LA is asking for roughly $800k to $1M for say 1800 sq ft home. Say you have excellent credit, even with a 20% down (which is approx $160K – $200k out of pocket) with tax and insurance, you’re easily looking at $4800 a month to ~$5900 a month. This is also not considering extra money for repair cost, HOA..etc. Time and time again, even now, I am finding similar house in similar neighborhood renting for mid to $3K to low $4K.

Considered you have to just spent six figure for a house and then end up paying more than what the house can rent for, how is this a smart decision? I mean if the only argument is that housing will go up forever and that renting is throwing money away then I am having a hard time convincing myself at current interest rate/price, other than FOMO, the math makes sense. Not to mention this comparison will be even worst if you do 5 to 10% down and have to pay PMI on top…

Most of the people are not that smart and recent 2 decades of unbridled money printing has made even the very dumb people look very smart.

last 2 decades or so, price discovery has been lost because of cheap money.

Unless money becomes expensive keeping in mind the inflation, don’t see the sanity come to assets.

We are still at negative rates at the moment.

No, rates are not even close to negative anymore. Current inflation is running below the 6% mortgage level. You’re looking at annual inflation, which is close to irrelevant.

Phoenix, I agree with you on this. Housing has been a very good investment over the past 70 years. There are only a few points in time in which the market dropped and left people underwater, and even then if you simply held the house for another 5 years you got your money back. So we have a lot of people conditioned like Pavlov’s dogs to “know” the market will always go up.

To explain to them that it may enter a decade+ long downturn requires you to bring up the Great Depression, of which nobody is willing to believe can happen again. Yet in what I deal with on a daily basis, a Great Depression level downturn is exactly what we are entering. Unfortunately it will most likely bring with it suffering and pain whose parallels, in this country anyway, were only experienced on a wide scale during that time.

I have mortgage broker friends who repeat the “housing will always go up” mantra to me frequently, and explaining market affordability to them is a waste of time because they mostly refuse to believe it (if they did, they’d have to admit their livelihood is in jeopardy). They FULLY believe 2024 will be a record breaking year for them.

I also have a very close landlord friend who has made a lot of money in buying multi-family housing over the last 15 years. I recently went through the economics of it with him and his explanation as to why its such a good deal is this: The property will increase in value at 10% per year, and you can raise rents at 10% per year.

It’s a fantasy that simply cannot persist. It was born from people living and thriving in the final upswings of a nearly century-long bull market that saw massive asset inflation. They believe their wealth is created through their own brilliance, some of which it was, but it was also created by riding the final waves of mania into the stratosphere.

Rents are not going to go up 10% a year if all the rent control measures around the country get implemented.

And rental property values are going to go down.

By “Enlightened Libertarian” you must mean “socialist” – that’s what an “enlightened” libertarian would have to be. When you gasp at the concept of “rent control”, you should do your mind a favor and visit some of the No. European countries where decency toward fellow citizens is practiced. Rent control is common – leases, once set, cannot be increased for the duration of the tenancy. No subletting, though. Free or extremely inexpensive college (for students who warrant it), free public healthcare (private is extra), you get fined for not recycling, public transport is considered an absolute requirement.

No, the libertarian b.s. is just someone trying to make a blue-collar worker think that there’s some virtue in exploiting the knuckleheads.

Maybe you should consider “Enlightened capitalist”, which is more like the No. European model.

HowNow-

I’m a full blown liberal socialist and agree that the European model has some positive aspects we in America would be wise to emulate (especially universal healthcare).

But there are also problems with the European model that Europeans tend to brush under the rug. For example:

-Free college. As you mention, it’s “for students who warrant it”. Most European countries have fairly brutal pruning of students, where, based on performance in elementary school, you’re put into tracks leading to college, trade school, vocations, etc. Once you’re on one, it’s very difficult to jump tracks. IOW, yes college is free, but it’s basically not available to people unless they got into the right track way back in middle school or earlier. And guess what, rich kids seem to dominate those tracks regardless, so I’m not sure how much more egalitarian college education in Europe really is.

-Rent control. As much of a socialist as I am, I am absolutely 100% against rent control in any form. The answer to housing demand is to increase housing supply. That’s what the govt should focus on: appropriate zoning and infrastructure investments to allow for more housing to be built where people want to live. European rent control (like American rent control) leads to several things. Firstly, it’s a lottery mentality. Whether you score that awesome pad in the middle of Paris that you can pay a pittance for is basically a lottery, and once you win that lottery ticket, you never give it up until you die, even if living in that house is no longer the best option for you (e.g. a 5 bedroom apartment you lucked into decades ago but now, when you’re 70 and alone, no longer need).

Rent control freezes housing stock — and the people in them — not allowing for either one to sort itself out and allow people to be in the housing that best suits them. You can see this in places like New York which does have rent control (much stricter decades ago): buildings haven’t changed in decades, and neither have the tenants. That’s not a dynamic housing market where housing stock is constantly changing to reflect current needs, and people move from e.g. an apartment in the city right out of college, to a house in the suburbs when raising kids, to a house in Florida after retirement.

And if you lose that lottery, you end up in the equivalent of Brazilian favelas in the outskirts of town with poor infrastructure or economic opportunities. Not coincidentally, those favelas tend to have recent immigrants, minorities, and other groups whose Daddy didn’t luck into a rent controlled apartment decades ago.

Oh yeah, and dream on if you think people don’t game the system by subletting apartments under the table.

Bottomline is that in America, you put the fate of your hands in psychopath capitalists who run the corporations that govern your life. In Europe, you put your fate in the hands of unaccountable bureaucrats in who run the government.

Both have their problems, and for some needs, one is better than the other. But don’t assume there aren’t big problems with socialist policies in Europe either.

Lune, this wasn’t rent control in the usual sense, which I agree causes much more trouble than it’s worth. The idea is to limit a given renter’s rent without increases over time. Once they leave, it can earn what the market will bear. Subleasing the property is not allowed and there are enforcement measures – as in control of mail, fines, etc.

The early educational tracks are an age-old problem and should allow for more flexibility via community colleges and transfers when students get religion about achieving academic excellence.

Bottom line, socialism ain’t what it’s idealized to be. It’s been described as “great for equalizing poverty but not so good at raising general wealth”.

I’m kind of socialistic but really liked Lune’s critique of N. European socialism. And there’s is probably the most successful (?) form of it.

I’ve read some Scandinavians bristle at being called socialists.

I’m not necessarily against rent control but Lune makes good points. Can’t be ignored.

Then again some city north of Seattle had an apartment complex in which rents went from $1050 to $1500 with change of ownership. 2017 or 2018 timeframe.

Here in Eastern Washington an apartment complex that had 1 BRs for $900 2019 to early 2020 had raised them to $1750 two years later.

They presumably could rent them out but that seems unfair to current tenants to get hit with a near 100% increase in just 2 to 3 years.

Something… no some things (plural )should be done in my opinion.

Apparently apartment construction is at its highest level since the 1970s.

That might help.

I hope they are quality… especially sound proofing.

Rent control: there are usually caveats.

I read in Denmark (?) it only applies to apartments built before 1991 (or perhaps it was… 20 years or older).

Similarly in Oregon the rent control passed a few years ago only applies to apartments 15 years or older. There are 4 or 5 other conditions that apply.

So its a limited form of rent control for sure.

No.

Why do I have to keep posting this.

1986 new home 89.5k.

Neighbors 101k. Also new.

1989 neighbor home sold 77k.

My home appraised 67k.

My home sold 1996 for 82.5k.

Started at 89k but not much interest.

Took 5 months… not 5 days, not 5 weeks… to sell.

Settled for 82k.

Northeast of Dallas.

How many Americans don’t know regional areas take RE hits ? Honestly….

people will continue to make financial decisions based on the rear view mirror. there has been a 30 year bond bull market, with dropping interest rates and prior to that, there was a multi-decade rise in dual income homes that also drove prices higher. so our population has become accustomed to prices that only head higher.

neither of these trends applies to the future.

the other trend, which might have changed is the ability of people to work from home or buy and sell products on the internet. that reduces the need of people to be packed into urban areas. there is alot of land out there in the US and if people continue to migrate to areas with more available land, it will reduce competition for homes. i think that the surge in home prices in these areas is temporary and once it reverts it could really damage the whole economy.

Your logic is spot on. You are looking at it correctly. Don’t let anybody tell you otherwise.

Because prices have gone up for 15+ years, they are buying with leverage and expect giant capital appreciation and renting is for poor people.

The reason people in coastal California feel this way about real estate is because the last 50 years have proven them correct with a very small exception between about 2008 and 2012. If your entire lived experience is that price is double every 15 years, it would be hard to think otherwise. I spent some time in Japan in the late 1980s and believe me people there felt the same way. Obviously things reach a point where they can no longer increase in value when underlying incomes no longer support it. This feels a lot like that inflection point to me.

At least in SoCal, prices declined in the early 1990s with the aerospace and defense adjustments following the Cold War, on top of the 1990-1991 recession. You probably have to be over 50 and living in Southern California at the time to really remember it. I certainly agree with your broader point.

In 2009 hb1 prices went down

40 plus percent in so cal

True, forgot that little dip…

Jon,

I was just pointing out there was another exception to rising prices in the last 50 years besides the 2008-2012 period referred to by Happy1.

“you’re easily looking at $4800 a month to ~$5900 a month. This is also not considering extra money for repair cost, HOA..etc. Time and time again, even now, I am finding similar house in similar neighborhood renting for mid to $3K to low $4K. ”

Your logic is perfect for today. You cannot make a profit today with buying and renting that house out now. You are better off renting instead of buying for today.

However, here is my in-law’s story (this is similar for all of their neighbors who haven’t moved):

They purchased a house in 1974 for 45K with 6.5% fixed rate loan. Their mortgage payment with taxes was about $300/month. The going rent for that area at the time was about $200/month. They made a decision and believed that owning a home was the path to wealth. They paid it off in the late 1990’s and now rent it. It now rents for $4,000/month.

I don’t even know if I can do the math for it since I don’t have all of the rent data during this time that they could have saved money by renting for X number of years. They could have taken that money and invested in Apple and Microsoft and done better. I believe that at some point in time, it was better that they purchased the house vs renting. I do know that by the late 1980’s going rent in that area was about $1,000/month (I know because I rented during college)

You are correct. Now is not the time for immediate rental profits but who knows about the future? Housing historically has been long term. If a house exists today at a price that would generate an immediate profit, I think it would be sold before it was even listed. This was also true in 1975.

I think the US is very fortunate with fixed rate mortgages. You know that if you buy a house now with a fixed rate mortgage, that the mortgage part of your monthly payment will be the same for the next 30 years (it may go lower if you refi at a lower rate). Taxes will vary but taxes also drive rents higher.

If you rent, it is hard to predict which way rents will go. For me, when I rented, they always went up. Within 6 years of deciding not to buy while in college, my rent had exceeded any mortgage that I missed out on. Your results may vary. Location, Location, Location.

Another anecdote. Every friend I had in high school whose parents rented during that time, no longer live in that area or city. Parents, like my in-laws, are still there. That could be because they didn’t have enough income to buy then and eventually they had to move due to rising rents.

Generally speaking era of cheap money has gone away for now

Now is the worst time to buy homes keeping in mind all the fundamental indicators.

Home prices have quite a lot to fall still

My friends still don’t believe they San diego prices have already fallen 10 percent from top.

They think the prices are standstill.

Even in their wildest dream they can’t think about falling prices at least in San Diego.

Keep your popcorn ready

Bob,

You gave an excellent example. However I notice that most of the antidotes like yours are from people who owned homes in California (or more recently anywhere in the west).

My brothers house in northeast Ohio has appreciated over the 45 to 50 years they have lived there.

Anywhere near the appreciation that west coast houses saw in the same timeframe ?

Not even remotely close.

More recently some Ohio cities have seen there real estate perk up. But from the early 70s to the present the appreciation would be quite muted compared to San Diego, Seattle, etc.

Renting and investing in the stock market would have been a better investment for my brother but then again they got to live in a house not an apartment (for better and worse… I’ve done both).

Counterpoint:

I bought last year (coastal SoCal). I probably “overpaid” by your definition even though my realtor said I got a steal, which they would never say :).

The 2.7% 30-year mortgage helped make the math more tolerable for the time being.

I am not a “house humper”, believe me. I rented for years because it was financially better, but it comes with many other non-financial sacrifices. Some people want to start a family and put down real roots, they are sick of living lease to lease; they outgrow an apartment; their kids hit an age where the city loses its luster; some are sick of cringing at tax time by owning nothing and the mortgage deduction makes the numbers work a little better. Many are using cash made from other investments. Some want to pick the color of a new rug/paint/appliance vs waiting for a landlord to replace stuff. And I think this Covid experience has emphasized that sitting around waiting for things to be perfect is a lost cause.

I, like you, tend to fixate on the financials first; but even I admit there is some peace of mind knowing that you have a place where you can actually live (not rent) and raise your kids, develop a social life around that place and arent worried the landlord is going to knock on the door with a rent raise or worse.

If in 30 years someone says you paid 15%/20% more than you had to for your home if you waited for the exact bottom without knowing when that bottom was going to be, I don’t think most people will care when its all said and done.

I am not arguing your points; they are all valid – just making a counterpoint; if RE markets sell off another 50% from here in coastal CA for the next decade, we’re all in for a world of hurt. I just come back to “buy what you can afford, and have enough cash buffer to ride out some pain if you have to”.

Not all homebuyers are house-flippers.

I appreciate your point of view and I can certainly understand where you’re coming from. Think right now, might be the worse time to buy given high interest rate, still delusional asking price and might be at the start of both rent decrease and home price decrease.

To me, the financial right now is just hard to shallow, at least to me paying a $1k to $2k difference between mortgage and rent is pretty large difference and personal decision wise it’s too big to overlook.

As for me saying house humpers, I am directing it at more of the people that look at you with sneer contempt when tell them renting might be a proposal, because they simply fail at math and only drank the kool-aid on home purchase is a no lose proposal. Then again these are the same people, at least within the circle of people I know, are the same one that look at you with contempt and disgust when you tell them you don’t want to have kids..

“Think right now, might be the worse time to buy given high interest rates,”

The counterpoint to this is that the historical average 30 year mortgage rate was 7.75% from 1971-2023. According to Freddie Mac, the current 30 year mortgage is at 6.13%.

Mortgage rates are still below the 30 year average.

Mortgage rates are also still below the inflation rate. I don’t recall ever seeing mortgage rates below inflation in my lifetime.

Is it is good time to take out a mortgage? I think it is risk for buying a house now based on Wolf’s charts. However, if you hold for 15 years, and can afford it now, you will do OK. You will likely do better if you can wait a few years.

Also, if you want to bet with the Fed driving inflation down to 2%, the mortgage rates will also likely fall to 4%-5% when this happens.

You can refi your current mortgage to 1-2 points lower if this happens and save more money.

That would be betting with the Fed.

“…some are sick of cringing at tax time by owning nothing and the mortgage deduction makes the numbers work a little better”

No, GSW, that’s fully priced-in. You’re having to pay more for the house because of that tax deduction. Any benefit there is illusory.

Agreed.

It’s never a cut and dried calculation – I rented for a decade in Wolf’s neighborhood. Did all the calculations and banked the benefits.

Appreciate the constructive back and forth. I agree that those that do the “buy RE at any cost, it’s a bulletproof investment” nonsense should be ignored.

I have many friends in San Diego who bought their second home in last 12 months.

They believe prices won’t go ever down here

Prices seem to have stopped going down in San Diego

Dropped to May 2021 level:

I have noticed the same in La Jolla and in Orange County (Irvine). Actually, I’ve noticed price increases. Rents for SFH in Irvine seem to be at all time highs as well. I have no idea what is going on.

I’ve noticed very low inventory and houses going into escrow at prices that seem to buck the trend of this data. Just today my nephew came to me and said he’s likely unable to buy anything other than a condo here because of the increased interest rates and lack of continued decreases in house prices. There’s a few of us here on this site that point out observations. That’s all they are, observations, but we get flamed nonetheless.

https://wolfstreet.com/2023/02/05/cut-the-price-by-20-and-they-will-come-homebuilder-meritage-explains-new-strategy-after-sales-orders-collapse/

GSW-

You made a reasonable decision, since housing is about more than pure finances. It’s also, like you said, where you live, where you put down roots, where you raise children, where you make friends, etc.

But that said, there are a few things to watch out for:

Things will likely work out in the end *as long as* you’re able to make the mortgage payments for 30 years. This is the key: you’re banking on absolutely no big hiccups in your life for 30 years in order to win this game. No job loss. No sickness. No divorce. No additional kids necessitating a bigger house. No change in the community (like the schools going downhill).

It’s one thing when people followed the “30% of after-tax income” principle when it came to housing costs. That gave you some buffer in case of tough times. But people now are stretching, and becoming house rich and cash poor. Many indeed, are signing for mortgages they can’t afford now, with the expectation that their incomes will rise in the next few years and then the math will finally start working. IOW, the buffer of what downside you can handle without having to give up the house is now tiny.

Sure, as long as house prices rise, you can always sell, pay off the mortgage, pocket whatever remains, and move. But when you’re underwater on your mortgage, and then you lose your job, it makes no difference if you know that 10 years later the house will be fine. The bank isn’t going to care.

The counterpoint to your counterpoint is that you bought a house with a mortgage rate that we’ll likely never see again for 30 years. In order to even break even on that house, you’re depending on incomes / inflation / housing demand in your area going up enough to afford a higher monthly payment than you’re paying. Otherwise, at best, it will be a break-even affair. Now, over 30 years, perhaps you’re right that incomes / inflation / demand will go up enough to prove you true. But short term, say the housing bust continues, your house (temporarily) drops 30%, wiping out your down payment and more, the recession hits and you lose your job. Doesn’t matter what the 30 year forecast is. You need to decide today whether to sell the house, let the bank foreclose, or prioritize mortgage payments over food. I can assure you the bank will not keep lending you money and let you wait out the (temporary) crash. It’s the equivalent of a margin call: sure you might be okay if you could hold out, but if you don’t have that buffer, then when the bank calls, you need to sell assets in a firesale to meet the margin call, and long-term profits don’t matter.

This happened lots of times in SoCal in the first housing bust (I was there; thankfully I just moved there in late 2007 so didn’t have a bought house). A house purchase is usually the largest financial transaction a person makes in their lifetime. When that goes sour, it can set you back years to decades (however much you worked to save that down payment, plus work off a personal bankruptcy on your credit report).

This doesn’t mean never buy a house. And like I said, financial considerations aren’t the only things to consider when buying a house. But assuming that life works linearly for 30 years with no surprises is a massive assumption (So massive, that only individual homeowners convince themselves of it; the bond market prices 30-year mortgages as 10 year notes, because on average, that’s how long it lasts. Most people either sell or refinance before then). f you’ve made that assumption, my only advice is to make sure you have enough cushion (money in the bank, and excess salary that you could afford to lose) to give you a fighting chance at making that assumption work out for you.

Phoenix Ikki

Homes in So Cal are bought to live in or to flip, with rare exception. I lived there for 15 years. They are not bought with the intention of renting / cashflowing, except possibly in some of the more rural areas (e.g BFE Riverside or San Bernardino County).

Those numbers you cite are the reasons why it makes no sense to buy SFH as a rental. In the Midwest (MO, IA, NE, OH, KS etc) the margins still make some sense.

I couldn’t agree more.

– The saying is: “Prices take the stairs on the way up and the elevator on the way down.

This time, it was exactly opposite. The price hiked which happened due to covid FOMO was maddening.

– One major reason why real estate prices are so high is women entering the workforce. If a (married) couple has two incomes instead of one income then this couple is able to afford a higher mortgage and then they make a higher bid on a house (as well).

That happened many years ago and hasn’t changed lately. It can be reasonably used to explain price increases many years ago, but has no impact on recent trends.

I could not move to California and expect to find a cheap house. Tulsa is cheaper. Thailand is even cheaper.

The movie Nomadland won an academy award for best picture in 2021. The setting was during the GFC. Retirees lived in vans. They traveled to BLM land in New Mexico to meet. They camped there for free, then split up.

Mortgage rates may have peaked close to 7.25% for the time being.

Rates will exceed 7.25 within a year

I’ll take the under.

My expectation is that the decreases we’ve had lately in some goods will stop and the prices will stabilize, and that we’ll continue to have inflation in services. This will soon lead to a situation where overall inflation stays the same or maybe even begins to grow relative to where it is now. This will surprise many, and the Fed will react, and so will the bond market…. finally.

Yes. People dont consider the ripple effect of the rate of rise in interest rates. It impacts lots of things like rate cap reserves related to apartment loans. CRE is moribund. Banks ramped up hiring just prior to JPo hitting the panic button and they are loath to announce layoffs, but they are coming due to less loan originations and the bloated head count. If rates are higher a year from now, lots of dead bodies will be floating to teh surface. I contend the dead bodies just havent been recognized yet. Looking for the default cycle.

The Realtor we have been using in our target market just got kicked out the door along with 80% of the agents in that office and our target market is active, but with low inventory. Prices have been sticky and we now plan to rent.

Quartzsite Arizona, not New Mexico.

A lot of people like to compare current pricing to the peak to show what a “great deal” they’re getting. That’s a fool’s errand. Just look at where prices still are, and where they came from. We have a LONG way down ahead if we are to achieve any sort of housing affordability.

2.5X annual median household income is the historic metric for house prices, which were always a function of the local incomes save for the past 25 years. Short of some sort of FED pivot, that’s where they’re going again.

An alternative scenario in which the Fed doesn’t pivot and the asset holders begin to lose 45% of their lucre.

Powell really has one more shot at distinguishing himself than more than the floozy the market obviously considers him.

All joking aside, the incipient deflation in asset prices is an extremely important talisman of the future economic environment.

Is inflation the opposite of deflation, which is so unthinkable that we’re not allowed to say that maybe they are negatively different.

In fact, I am convinced that reckless monetary policy feels better than the more prudent positive interest rate that had been hashed out as appropriate over the last 5000 years.

Like the sun, always a challenger about yesterday.

Tomorrow, the Fed will confirm what has been the worst kept secret for several eons. Jerome Powell will ascend to the podium and regurgitate what he has been telling everyone that would listen.