Hammered by waves of layoffs, swooning stocks, collapsing cryptos, and 6% mortgage rates.

By Wolf Richter for WOLF STREET.

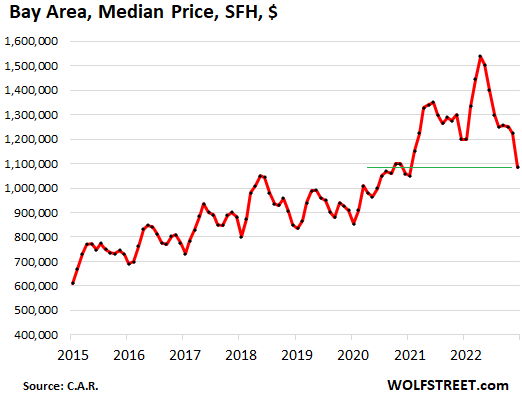

Home prices for all of California are down, Southern California too is getting hit, even San Diego, but the Bay Area is the standout in terms of the steep and deep plunge in prices.

Sales of single-family houses plunged by 37% year-over-year in the Bay Area. But in Southern California, where price declines haven’t been that huge yet, sales collapsed by 48%. In all of California, sales plunged 44%, to 240,000 homes, just a hair higher than during the bottom of Housing Bust 1 in late 2007.

The median price of single-family houses in the San Francisco Bay area plunged by 30% in December from the crazy peak in March 2022, by nearly $455,000, from $1.54 million to $1.08 million in nine months, according to the California Association of Realtors today. The plunge in December – after months of layoff announcements by big and small companies in the area – was particularly brutal.

That this 30% plunge from peak only put the median price back roughly where it had been in December 2020 shows how crazy the price spike had been during the free-money pandemic. But not many people bought a house during these two years. So in essence, this 30% plunge isn’t a big deal in the overall scheme of things.

But for people who used to look on Zillow constantly to see how much richer they have gotten by just living there, well, they might have to stop looking. Problem solved – unless they want to sell.

Year-over-year, the median price dropped about 10%. Per square foot, the median price also dropped about 10%.

Some caveats here about median prices: They’re volatile and they’re seasonal, and they can get skewed by the mix of what actually sells, etc. etc. But in a huge market like this – the nine-county Bay Area has a population of around 7.6 million people – the median price is a reasonably reliable indicator of the direction and magnitude of price changes.

Seasonally, January is the low point for median prices in the Bay Area. So one more month to go. Then the spring selling season normally shows up when demand normally perks up prices. But this may not be a normal year.

Where is this demand supposed to come from? Who is going to buy at these prices, with layoff announcements spreading across the area on a daily basis, and with stock prices of local companies (stock-based compensation plans) and cryptos getting demolished? Who will have the desperation to buy at these still sky-high prices? At what prices will the buyers come out of the woodwork? That will be put to the test over the next few months.

The five big counties of the Bay Area.

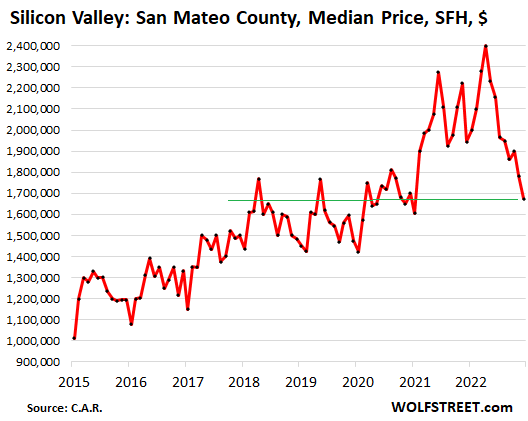

Silicon Valley: San Mateo County: The median price of single-family houses plunged by 30% from the peak in April 2022, by $726,000 in nine months, from $2.40 million in April to $1.67 million in December. Year-over-year, the median price plunged by 14%.

This median house price is now below where it had been in December 2020, and below where it had first been in April 2018.

Sales of single-family houses plunged 38% year-over-year. That was bad enough. But sales of condos have essentially frozen, having collapsed by 64% year-over-year.

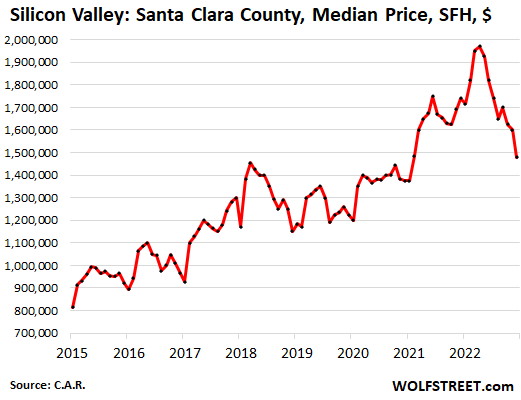

Silicon Valley: Santa Clara County (includes San Jose): The median price of single-family houses plunged 25% from the peak in April 2022, by $455,000, from $1.97 million to $1.48 million. Year-over-year, the median price plunged 15%.

Sales of single-family houses: -43% year-over-year. Sales of condos: -48% year-over-year.

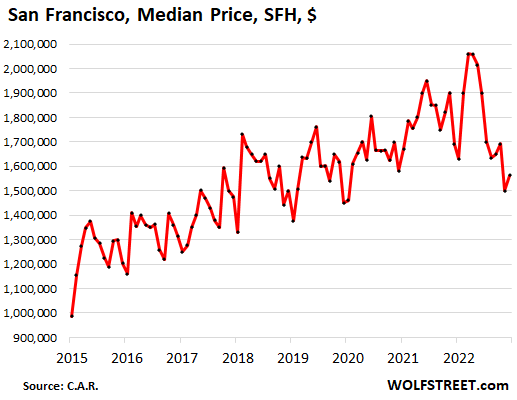

San Francisco: The median price of single-family houses plunged 24%, or by $496,000, from the crazy desperate lock-in-the-low-mortgage-rate-peak in March 2022, falling from $2.06 million to $1.56 million, despite the uptick in December. Year-over-year, the median price is down 7.5%.

Sales of single-family houses: -24% year-over-year. Sales of condos: -52% year-over-year.

Condos are a big part of the City, including numerous fairly new towers South of Market, where sales have collapsed, as the tech companies headquartered in the area, including Twitter and Salesforce, have announced a gazillion layoffs. Year-over-year, condo prices have plunged 23%.

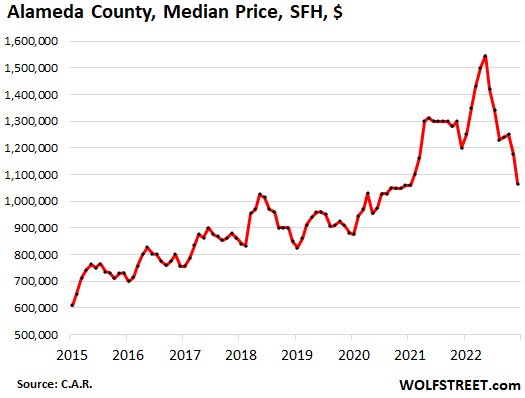

Alameda County (East Bay, includes Oakland): The median price of single-family houses plunged 31% from the crazy peak in May 2022, or by $479,000, from $1.54 million to $1.06 million. Year-over-year, the median price is down 11%.

Sales of single-family houses: -37% year-over-year. Sales of condos: -45% year-over-year.

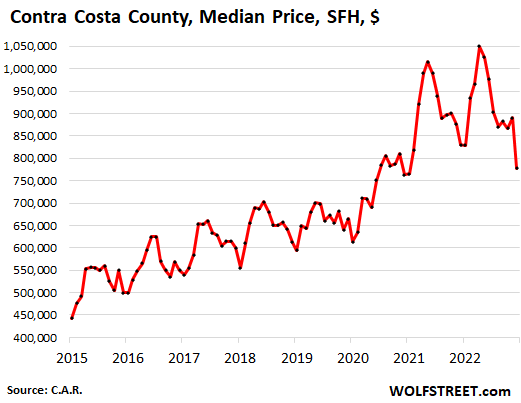

Contra Costa County (East Bay): The median price of single-family houses plunged 26% from the peak in April 2022, or by $272,000, from $1.05 million to $778,000. Year-over-year, the median price is down 6%.

Sales of single-family houses: -36% year-over-year. Sales of condos: -50% year-over-year.

Median time on the market in the Bay Area before the property was pulled by the frustrated seller, or before it sold, more than doubled year-over-year from 13 days in December 2021 to 27 days in December 2022.

Everyone can figure that January is going to be bad. So now all eyes are on the upcoming spring selling season, amid this constant drum beat of layoffs at companies headquartered in the area, or with large operations in the area. Beyond the actual layoffs, the layoff announcements also create a lot of uncertainty among people who haven’t been laid off yet. And that can’t be a good motivator to go out on a limb and buy a still ridiculously overpriced home.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I mean we all knew that the prices for houses in the US will come down after such a crazy increase in the last 2-3 years and higher interest rates, but wow I didn’t expect it to be so quick. And the panic hasn’t even hit yet the general public

House is an investment that will entitle you to riches without work. You can leave your job and get your house to work for you.

/s

Housing is a non-productive asset. We really need to destroy the myth that real estate is a productive asset and instead create policies that make it more of a living expense.

The first thing we should do is eliminate Freddie and Fannie so that interest rates are based on economic foundations and risk goes back to the mortgage lenders. Second, eliminate the mortgage interest deduction. Third, make 15 years the longest possible mortgage duration. More people could pay off their homes earlier and then begin to save money for retirement. That would reign in the financialization of housing. Finally, we should increase taxes on undeveloped property, to reduce the incentive for anyone to stockpile land. This could decrease the land value of property (so more of the value is the replacement cost of the building). Oh, and we should put the tax incentives into the building industry, so that there is more upgrading of the housing stock, tearing down old and building better homes.

Net effect of these reforms would be lower prices, better access to quality housing stock and a whole lot less money to the banking industry (and less risk to taxpayers).

Actually, if you do a graph of time vs monthly payment you will find that the optimal mortgage is the old (before 1980) 20-year mortgage.

The first 10 years of a 30-year are mainly interest payments and not too much equity building. 15-year mtg. really ups the monthly from a 20- year.

I agree, except for the 15 Y mortgages and tearing downs, however, all these things one has to do in an attempt to make prices affordable instead of just doing the obvious- put a cap on the number of SFHs any person or corporation can own (say 10 for Mom and Pop landlords?) and tax the living heck out of any foreign ownership. Anything else will be worked around the next time the FED goes into all out party mode.

Don’t ALL INVESTMENTS entitle you to riches WITHOUT work?

How is “tuning the casino rules” (see gametv’s particular “casino fine tuning” comment) going to make a difference to the bottom 90% who have NO or VERY little excess money to gamble (I mean, “invest”) with in the first place?

The tale of two economies continues.

Some people think we’ll simply gravitate back to 2019 asset price levels, as though we had a sustainable economic base back then, but the bubble began in 2012 or earlier when the Fed began suppressing interest rates and implementing QE. Unless the Fed is permanently in the business of suppressing rates, asset prices will face a LONG bottoming process.

The “Goldilocks” economy they used to talk about was a mirage. Inflation is a snake in the grass.

Yes. In socal and seattle, if you are able to sell you “Second house” at 2019 prices, you should celebrate!

In SoCal where I live (south Orange County), prices are waaaay above 2019 still.

Most homes coming on the market are still asking the same price they did a year ago. I commonly see homes coming on the market at 1.75x to 2x what they sold for in 2018. Most will need to drop 300k at least to hit 2019 prices (some over $1m) then add the interest rate and prices will need to drop 500k to have the same qualifications.

Whatever economic reality is, it’s not hitting here yet (I believe it will).

@Here it comes. Yup totally agree, still seeing plenty of insane, delusional asking price anywhere from Irvine to Eastvale…playing games like contingent, then back on market, price increase (I guess to tempt the last FOMO buyers..) Basically, looks like SoCal sellers are more stubborn than the peeps in NorCal. Not a surprise if you talk to your typical house humpers living in South OC..their s$$$ never stink apparently…

As Wolf point out and highlighted below, those sales volume collapse will eventually force even the stubborn SoCal folks to start moving at the right price..time will tell

“But in Southern California, where price declines haven’t been that huge yet, sales collapsed by 48%”

In SoCal, you can sell your second house for a massive amount above 2019 prices. It’s nice to see a correction begin, but it’s barely begun to correct so far.

Prices still high here, but most of the ones selling are selling for 25% less than the last reduced price. The rest are just sitting there in all their overpriced rotting roof glory.

I looked over sold homes and I’m also seeing what looks like 10% of them (from the first page brought up- sorted most recent) are investors trading with each other. Recently sold but never listed on the MLS. I don’t think they are foreclosures. Most of them are fairly nice so I don’t think they are “We Buy Houses For Cash” sales. I wonder how many RE agents are counting that when comparing houses sold to houses on the market in their private and personal comp calculations. Not many yet I don’t think.

Starting to see a few more foreclosures too.

That’s NorCal

I think the Fed will be permanently in the business of suppressing interest rates. Once the economy rolls over, the Federal Reserve and Federal government will both be right back at the same old BS stimulus policies. Instead of addressing the REAL problem, which has been policies that have stripped our national manufacturing base so that lazy and corrupt executives (people like Tim Cook) could enrich themselves.

Create policies that bring back jobs and productivity to the US and stop the increasing financialization that robs the country of a decent future.

The problem I see is that once we put inflation back into the bottle, there will be no willpower to engage in the difficult reforms that we truly need to create a sustainable business environment that creates a large middle class. That is the core of a truly prosperous and just nation.

You get it, gametv. I agree.

Prices in the San Diego area have remained stubbornly high. Many properties are asking selling prices at levels about 150-170% of the prices in 2019/2020.

The monthly payments for the new 2023 buyers at these prices would be double the payments of the 2019/2020 buyers by going from 3-6% interest and a higher CA property tax basis.

While this might not matter as much for a lower cost home, many SFR’s in decent neighborhoods here in San Diego are asking ~1.5M for an “average” nothing to get excited about tract house type place. The 2023 new buyer payments including property tax with 20% down would be up to $9,000/mo. That’s a lot to shell out.

I’m also noticing homes selling even at ~2M level then immediately being offered for rent. They must be 1031’s? Being bought with mostly cash? They would not cash flow or even break even with any kind of significant mortgage at these rates and paying such a high property tax (usually 1.25%),

This market here in SD has me stumped as to who can easily afford and who is buying homes at what feels like very inflated prices.

Homes sales in San Diego collapsed by 43% year-over-year — because sellers refuse to lower their prices to where the buyers are? And so the house sits, and then it’s pulled off the market, and then it’s put back on the market and sits, etc. etc. Eventually, sellers will figure out where the buyers are and will price it right to sell.

@ Wolf,

At the risk of sounding like one of the many deniers out there, the collapse in sales is partly because there just ain’t jack for sale. Check it out. Record low inventory. Eventually, eventually, the natural need for selling will overcome whatever it is that’s preventing stuff from hitting the market, and inventory will accumulate. And that should result in the price tankage we’ve seen in Nor Cal.

Time on the market in San Diego nearly tripled year-over-year. That’s when frustrated sellers pull their properties off the market, to later re-list or try a rental.

If supply were insufficient, prices would spike. But prices have dropped a bunch.

“This market here in SD has me stumped as to who can easily afford and who is buying homes at what feels like very inflated prices.”

Consider that we are still near the apex of the biggest everything bubble in the history of mankind. There are more people still cashed up than even the most astute minds probably realize. When you print that many trillions, you get a lot of stuff that makes absolutely no sense, no matter which way you slice it. Instead of looking at ridiculous sales prices and scratching your head, look at the FED’s balance sheet.

“bubble began in 2012 or earlier when the Fed began suppressing interest rates and implementing QE.”

Huh? I’d argue the bubble never ended since the dot com. First was dot com, isolated to stocks, reflated via housing, which was reflated via the everything bubble. QE started in 08 or early 09 if i remember correctly. I think 2012 was operation twist or such. I hope the few years of gains yinz guys got will be worth all the pain suffering that is coming down the pike.

Agree re stimulus continuing since year 2000-1 house:

Just another example of long term hand/bend overs to the speculators and derivative devils IMHO…

Got OUT of the SM mid ’80s due to perceptions of similar manipulations by big boys, a big club that I was not in, per later wisdoms…

Time and enough to bee absolutely going back to basics, at ALL levels, but especially at clearly NOT helpful GUV MINT levels.

It definitely started with Greenscum.

Replying to stuckinSD

.

Prices in San Diego are still quite high compre to 2019 but low compare to peak of 2022.

It takes time and patience would be rewarded

@Cookdoggie,

yep, Greenspan and Bernanke set the stage for this inflationary mess and even tried to minimize the damage it would do. And Bernanke in particular is celebrated for it, even the Nobel Prize has been tainted by all the politics now going into selection of even the Econ and science prizes. If theories are convenient for the plutocrats, somehow they get considered “orthodox” in the field

“It definitely started with Greenscum.”

Yep, ol’ spittlemouthwobblychin started all of this nonsense, and it’s been a rolling snowball gaining mass ever since.

Yes, this point too often missed. The recent drops in home prices are a welcome moderation of all the speculation from the Everything Bubble but they still have a long way to go, esp in the bubbliest markets of the housing bubble. Even areas like Boise, parts of Utah and a lot of Florida, not to mention the inflated markets on the West Coast, around Phoenix and in the Northeast still have a good and long way to go for home prices to be anything like matching people’s incomes. In some markets they’ll have to fall more like 50, 60, or even 70 to 80 percent to actually be in a sensible range. Same for the bubbles lately in Canada, Australia and New Zealand, easily 75 percent drops to go in many of those markets to be affordable.

Like our econ prof. said years ago to cut through all the distractions, “when prices of a necessity like shelter, healthcare or education out-strip incomes, it is always a bubble by definition and prices must drop, anything that counters this is merely postponing an inevitable correction”. And as has been rightly said here, those who panic first, panic best, esp in a bubble of this scale. Policies like ZIRP and QE can be considered for emergencies but it was an historic mistake for the Fed to continue these for years and fail to normalize. Now we’re dealing with the consequences from that policy

I know right? S#it’s not worthwhile to rehash again.

Shandy from the Sunshine Coast .. f***) yes baby.

-S

Actually, Vlad the Impaler,

I agree, I knew this thing was gonna blow before it even started.

Peace and Love

Good analysis. Thank you. Certainly doesn’t sound like the “Soft Landing” going forward that mainstream media blabs about.

If I “lost” all my down payment equity like many of these SF home owners that bought at the astronomical prices just did, I would also not be looking at this as a soft landing or any kind of landing, for that matter.

And this is still “round one” of the event.

Add mass tech layoffs, H1B forced evictions and crazy services inflation in the mix.

“H1B forced evictions”

Leo, are there any stats on this?

Tech companies expanding mass layoffs even before publishing results in a panic. Seems like the quarterly closing numbers were really bad.

Wallstreet will try to sell -4% revenue decline (-11% with inflation) as expectations beat.

Will the stoned investors finally smell narcan?

I bet all this will hit housing in west.

I am glad to see someone actually factor in inflation.

it is housing all over. SLC and Wasatch Front (and back – Park City etc.) are still overvalued.

Then in SLC one apartment is being built for each existing apt, and then another apt. in the planning stage for each existing apt. What could possibly go wrong?

I am trapped in Leo’s world, clueless angels describing this mornings trade as if it will still hold 8 hours from now.

I bet that the stoned investors will take whatever precautionary measures deemed appropriate.

One has to decide early on;

Is one a reckless gambler or a calculated gambler.

I placed an offer on a house in July in the Bay Area at much lower than asking (but reasonable given prices of 2020) that was verbally accepted but then countered in writing the next day so I walked away out of principle. It was removed from listing and then added back a few months ago at a price still higher than my offer but now with a lower Zestimate. But at this point with all the tech layoffs I can confirm as a sample size of 1 that while I still have the down payment squirreled away in tbills, there is no way I would make another offer in the next few months. I will say though that even if my job was more secure, the lack of inventory is annoying as there isn’t much I would want to buy at any price.

Good for you for walking away from that transaction. You’ve touched on one of the key factors in play here – job insecurity. When the layoffs get large and prevalent enough to be on the news headlines day after day, it also affects the people who manage to keep their job through the initial layoff(s). The obvious troubling question is – what if I am next?

The reverse wealth effect is the second consumer psychology factor in such economic environments. Just as some people spend lavishly as they watch their investments appreciate on paper, those same people become hesitant when asset pricing is headed downward. Should we still take that expensive vacation when our net worth has decreased by 15% in the past year?

I wonder how many Californians regard their home as their primary investment asset and partially base their consumption on their perceived future direction of real estate values. The Financial Samurai claims that roughly 30% of Americans have no wealth outside of their home equity.

So Wolf is correct – Californians who used Zillow estimates to rationalize their overspending in the past 2 – 3 years are now seeing the other side of the coin. Which may be OK for some of them unless one of life’s “curve balls” (divorce, job loss, illness/medical expenses, pay cut etc.) happens. That will be a difficult time for those who purchased real estate in the past 24 – 36 months.

The main theme going forward is the connection between uncertainty and hesitation.

As people take more time to look at tea leaves or wait for stars to align into meaningful patterns, cash will grow more valuable and become more scarce.

The buildup of cash on the sidelines, eventually will be diverted to cost of living realities, versus the allocation of cash to crypto, overvalued stocks, real estate, NFT-GameStop-speculation and the entire spectrum of stupidity associated with pandemic insanity.

Cash on the sideline is debt. It may wanish quickly.

From SocalJim: Here in SoCal, the sun never sets …..

Think him and Kunal are on a housing will never go down media tour, gotta pump that market up…

Either that or us “doomer” housing folks are too negative for them.

I would actually enjoy that media tour Phoenix. It would be grand entertainment. We’ll christen it the “tree grows to the sky and always will” tour.

As far as negativity goes, that is simply untrue. I consider myself quite positive. I’m positive that the RE market is turning negative. And the shakeout will be a multi-year phenomena until the market stabilizes.

An additional positive is that declining markets offer many opportunities. Positivity is not limited to appreciating asset markets. I continue to hold a fresh powder keg for those pending opportunities. And I’m quite patient.

So color me positive. I’m certain some of the RE agents are fully aware of the points covered on this site about real estate. But they only get paid for the transactions that happen NOW – even if they know this is not a good time to be making that transaction.

Sorry, Josh, we ain’t seen nuthin’ yet

(Agent 44 years in the Bay Area)

Take a 6 month vacation, and see where we are then.

How does the median price look going back to 2008?

Based on mortgage affordability standards, if there is a 1% increase in the 30 year mortgage rate, there is about a 10% drop in price.

Most of the peak pricing was set when the 30 year mortgage was at 3%.

Nice to see San Mateo County and Alameda County are at or near 2018 median price levels.

Looks like the United States media housing price will be at least returning to early 2020 levels.

Layoffs will continue to dampen housing prices in places like Seattle, San Francisco, etc. even if the 30 year mortgage rate steadies around 5.5% in the second half of 2023.

Today’s news including USA Today report about layoffs at Microsoft and Amazon. Bloomberg states Amazon is to layoff 6% of its workforce.

.

Wow. What surprises me most is that that Realtors Association willingly punishes this information. In my state their news releases are always light on data when prices have been stagnant. There are no newspapers or outside entities in my state that care to dig into the numbers so the news releases are all we get.

Perhaps they’re finally realizing that prices need to come down a lot if they want to see anything less than anemic volume. Must be a lot of pressure from poor producers who can’t list and sell to someone sight unseen with multiple offers. I hope we never see a market like that again in any of our lifetimes.

They need to be able to say “it’s a great time to buy!”

Those news releases get their data from somewhere. You can probably find the sources or ask them.

California Assc. of Realtors published weekly info but they stack some of the figures. For instance they only quote a 2.8% price decrease although it’s much higher than that, and their homes sold pr day average is always double what they say is new listings pr day – but inventory is increasing everywhere so we know something is fishy there.

Be careful when looking at property valuation figures on the various RE Internet sites. I check my own house and the data was completely inaccurate. The valuation was inflated by 20%. The sq footage was off by 30%. This data is another con job by the RE industry, which is completely corrupt, including most of the people who work in this profession.

Isn’t the source of the square footage data the county tax records?

The bogus data was on Realtor.com.

County records showed the proper sq footage.

Plus, the realtor sites and MLS have built-in mechanisms to support RE prices. They tout the number internet page views when home values are growing, but not when they are shrinking. They remove price histories from pages when prices are dropping. They allow people to list, then relist after a few months, to mask an overpriced situation.

They know the average home-buyer is transfixed and easily manipulated.

When I look on Zillow, I can see the sold date/price history. And I can see the tax history. Our County also lists the same information.

Maybe you need to look at several sites to get the info you need.

This idea that most of the real estate industry is “completely corrupt,” care to elaborate? I’ve been in the mortgage industry for 10 years now and I find most people are hardworking, ethical, and are just trying to do their jobs and make a living.

First and Long

Unfortunately, my track record in my personal transactions with Realtors is 0 for 20. This can’t all be a coincidence.

In my last transaction in 1999 when I sold my home and bought one about 3 miles away the Realtors involved on both ends committed dozens of ethical violations and nearly killed their own deal. Need I say more.

We get the NAR magazine every month. The publication is nothing but a pile of RE propaganda.

First of all SC: Long time meme, ” If you run into one asshole a day, they are the asshole,,, If you run into many assholes a day, you are the asshole.” Been doing my best to evaluate this old saying for decades, and find it true in general,,, while clearly agreeing ”generalizing on the basis of insufficient information” IS appropriate.

Second of all for SC and FNL:

Each and every profession and trade has assholes, NO DOUBT about it after 70 years dealings;;; how some ever, all trades and all professions, including real estate folks, ( personally dealt with over six decades, ) have good folks, hard workers, well intentioned and willing to do their part to make a deal happen, etc.

Maybe gotta BEE one to BE able to deal with one??? IDK

Zillow is highly inaccurate. Always has been AFAIK. Some of the others just use Zillow’s data. They almost always have a higher valuation than there really is. What really cracks me up is every single home you look at also is rated as having an 86 – 98% higher likelyhood of selling faster than all other homes around it.

I think the general public is pretty smart with refusing to pay outrageous prices or buy using expensive credit–Why pay 7% interest a year to almost certainly lose 7% of purchase value the first year of ownership when you could buy bonds and wait until the market drops in a year or two and rates continue to decline? Anyone who tells you differently is a mortgage broker or real estate agent. The real catastrophe will be when the single family residence zoned vacant lots are gone and you can no longer build your own nice home at $400 sq./ft. It’s a well earned “buyer’s strike” these crazy prices have caused and I hope, a lot of businesses suffer long-term loss of “goodwill” from the quasi-“price gouging”.

Many people are extremely impatient. We see it on the roads, in the lines, on the flights. They’ll risk a $300k quick loss to have that $1M home now. A couple rationalizations the list below will make the risk palatable.

Prices will go up if I stay there long enough.

My kids need a home.

The price “is what it is”.

You can’t go wrong buying in good locations.

I can’t live in an apartment.

I don’t want to be kicked out.

My income will grow into the home price.

Owning a home is the best way to build wealth.

I can always rent a home out if I have to move.

If you bother to think about it long enough, each of these rationalizations has serious flaws.

You hear those rationalizations again and again.

This is a great list of how Millennial parents became secure and could retire!

All of these items likely happened to parents of Millennials who had purchased a home from the late 1980’s to 2007. Except when I purchased, the Price was never “is what it is”. Most of this period resulted in buying a house under asking.

It worked for them. Is this time different? Yes, most of the appreciation over a decade was far less than the 30-40% that we’ve seen over the last 3 years. House prices should track inflation. It is a wild speculative market now.

Maybe I’m a bad parent but I tell my kids everything above. I also tell them to wait until people have stopped these crazy bidding wars. I urge them to have patience.

As salespeople say, people buy things emotionally and then justify them logically. Some of these rationalizations sound logical. Until the market later proves they aren’t.

Then the owners get to experience a new emotion – the one that comes with finding out the additional meaning of the word “underwater.”

Yes, as a Millennial parent, I was underwater for 6 months in 2012.

However, I am in it for the long term. I didn’t panic sell and did well.

Short-term investors are prone to panic during downturns. They sell at lows. This is not a good long term strategy.

As you said, don’t buy at highs or sell at lows based on emotions.

I truly think your overestimate the general population’s intelligence and rationalization skills. This is my mistake as well, just look at last 2 yrs house and auto markets…this is the true reflection of their impulse control level and thinking/planning for the long term skills

The fact that people are not buying or demand drops is likely due to unable to qualify for the loan, if you give people opportunity to qualify for $1M mortgage with 2% down while making $70k a year, plenty will do it.

PhoenixI – good flip-the-telescope observation.

may we all find a better day.

May Bee PI, but IMHO it is easy, very easy to under estimate the ability of the general population to pull any and every kind of dodge—scam that appears to give even any short term advantage.

Certainly this has been demonstrated in tons and tons of the genre of what is termed ”historical fiction” both recent and for many centuries past.

Why would anyone NOT sign up for a gazillion dollar mansion knowing full well they could stay there with no money down or monthly for many moons???

Not that I personally would ever ”squat” or anything of the sort, NOW a days… I hope…

VVVNV – between your observation and PI’s, could be we’re looking @ a classic slippery slope (or moral hazard). We would like to believe most folks are of goodwill and hard-working, but when that goodwill and hard work has been taken advantage of ‘for the last time!’, they WILL hoist the Jolly Roger (stealing an aphorism of R.A. Heinlein…).

Or, more concisely, “…if you can’t beat ’em, join ’em …”.

may we all find a better day.

Plenty DID do it. And now that rates are going down and the overall market conditions are easing (despite all the Fed tough talk), some are starting to do it again.

you are really young and has no clue about mortgage interest in the past, or you are a crypto baby reading Wolf,s great postings. Get a life dude, or you are the next serf in line to bail me out imbeciles.

April 2022 was the end of QE, but not quite the start of QT. The techies recognized IMMEDIATELY that their sole source of energy was gone.

At first it was hard to tell whether the drop was just a blip, but after 9 months the pattern is perfectly clear.

https://wolfstreet.com/2022/04/21/peak-balance-sheet-feds-assets-dip-to-5-weeks-ago-level-end-of-qe-end-of-an-era/

– Nonsense. There were already signs emerging in the 3rd quarter of 2021 that the tech sector was heading for (more) trouble.

– Reventure brought the news some 2, 3 months ago that the amount of mortgage applications has plunged to levels comparable to the bottom of the market after the GFC of 2008.

– I need to provide more details: the amount of mortgage applications (here in the US) remained – more or less – flat in 2010 (???), 2011, 2012, 2013. From 2014 up to 2021 the amount of mortgage applications – on average – kept rising every year well into 2021. The amount of applications peaked in the 4th quarter of 2021. From that 4th quarter the amount of mortgage application have crashed down to the level of 2011.

– Is the total amount of mortgage applications going to go down even more ? I don’t know but I fear the worst going forward. Does Wolfstreet have any data on that topic ?

I like most of what Nick said about the housing market and generally I agree but then again he also thinks the FED will pivot in Q2, that deduct quite a number of creditability points in my eyes..

Nick has pointed out that multifamily (apartment) construction is very high.

One has to go back to the 70s to find it at a comparable level.

This supposedly will put pressure on rents and SFH as well.

He cranks out the videos frequently. I’ve learned a lot listening to Nick.

In addition to Wolf Street and Reventure Consulting i also watch Sachs Realty (Maryland), Jason Walter, and Sessa Realty (Toronto).

Renters could use their own political party.

I just had that idea. A bit too narrow focused I suppose but maybe not so foolish.

A lot of renter evictions … economic…and the media (television) didn’t care. If somebody just stops paying rent that is one thing. Its another when someone moves into an apartment, complex gets new owners, and viola an immediate rent increase of 42%.

I read that happened to one complex in the Bellingham WA area 4 to 6 years ago. Tenants none to pleased. Happened lots of places near major cities in the West so I am lead to believe (20 to 45% annual rent increases) in the 2019- 2022 timeframe.

1) The Bay area : the space between the last two dots is the largest on the chart. It might cont for a month or three, testing the 2018/2021 trading

range, before moving up to a lower high, testing 2021 swing point, the 2021 lows.

2) San Mateo, Santa Clara, Alameda and SF…need time to recover after the flood and the layoffs, before summer time tourism peak.

3) These Bay Area layoffs are painful, but US Industrial Production hit an all time high in Sept 2022, though testing 2018 highs.

4) If Industrial Production keep moving up to another all time high, industries and high tech will rise in unison. There will be a shift from high tech bs to real stuff, possibly expanding in the flyover centers, competing with each other for dollars and talents. Nothing is wrong with that.

“possibly expanding in the flyover centers”.

I realize California ranks as #4 or #5 in the world by GDP (i think it is). But some people might be surprised by the amount of hi tech already throughout the US.

I googled “hi tech companies in Pittsburgh” and it came back with (849). When I clicked on AI companies in Pittsburgh it came back with (36).

Admittedly people can take liberties in calling themselves an AI company (or hi tech as well I suppose).

Then again I interviewed with an AI company in Pittsburgh way back in 1985. I forget their name.

I know Pittsburgh is involved in quite a bit of robotics research and the Software Engineering Institute (associated with Carnegie Mellon) is there.

I imagine these numbers (849 and 16) might be much higher than someone from tech heavy Silicon Valley, Seattle, and Boston would think.

I’m pretty sure Austin, Dallas, Atlanta, North Carolina cities, D.C., Denver, Portland, Minneapolis, Columbus, etc might surprise as well.

Hi Wolf,

I read your articles regularly and I completely agree that the global real estate market is a huge bubble. I am writing from Eastern Europe. Here, people are still in a euphoria and only the last two quarters have seen a decline in transactions. What surprises me is that there are people who are ready to pay 200k or more euros for an apartment in Sofia, Bulgaria, given that the minimum salary is 420 euros and the average in Sofia is 1100 euros, which means that the average salary is around 700 to 800 euros. To me this is absolute bullshit, but apparently FOMO is still doing its thing

I didn’t know that it’s actually possible to do a short sale on a house.

Judging by the ads pooping up all over the place lately, it obviously is. And of course there are “Finance guys” to “help you out” if you are in this Situation.

You americans never cease to surprise me with your creativity when it comes to that.

Franz – intentional, typo or misreading ‘Murican idiom, ‘ the ads pooping up all over the place’ has me still pounding the table in laughter. Many thanks!

may we all find a better day.

I bought a short sale in late 2008 when I thought I was near the “bottom” of that housing crash. The broker I used only dealt in short sales at the time. He would help the homeowner go through the process with the bank, connect him with buyers through other agents and then get paid 1% of the final negotiated amount. I paid close to 50% of what the homeowner paid for the home in 2004.

“Late 2008” would have been after all the fun stuff. If These Things start again now, that is quite telling as to where we are in this cycle.

You Go Back, Jack, do it again

(Steely Dan)

Mortgages and rates are a critical component of the housing picture of course, but who wants to lose mid-six figure sums on any asset, with or without a mortgage.

This exercise is about identifying when more “sellers will come out of the woodwork”. This will turn into a flood. What is unfolding is breathtakingly tragic.

For anyone to call an end to this before HB2 arrives, they have to foresee a return to zero interest rates and the largest QE rollout yet. Put that possibility up against recent Fed speeches.

On a separate topic but with some geographical relevance, I looked through the Twitter auction items yesterday. A type of fire sale event marked by what I thought were elevated bid amounts for the items under auction. An interesting metaphor for the economy, highlighting its contradictions.

hello wolf

You follow, among other things, the prices of properties (houses, offices, business premises) and present very precise data.

But I ask you, for those of us who did not live in or know San Francisco, tell us what San Francisco was like when you were younger. Well, I don’t know if you lived in San Francisco since you were a kid.

An idea that I felt that San Francisco was and represented is that of a city with a lot of very strong cultural activity, for example a city related to the Beat movement, a charming city, more exquisite than Los Angeles for example.

Lately related to large technological activities.

Perhaps or surely things have changed as cities in the world change.

Thanks and greetings to all

Not a native of SF CL, but lived in Berkeley for several years when finishing college, and absolutely LOVE SF, and went there to relax, refresh, etc., and had many friends and lovers there in late ’60s-70s.

SF was wonderful, safe, very diverse, etc., etc.

Apts there, actually mostly what were called flats, were available in Haight and many other hoods for $50.00 for small ones, $100 for 2 bedrooms, etc., in those days, and the city was full of artists and artist wanna bees of all venues, some of whom went on to be listed.

As much work as one wanted was readily available at $5.00 per hour, so 10 hours PER MONTH to pay the rent!!!

Sometimes I think that it might be better for ALL working folks to have another ”great” depression,,, if for no other reason than to clean out the speculators who have gained such a stranglehold on WE the PEOPLE, now more like , ”WE The PEEDONs.”

In the early 70s before the end of the gold standard, a 3br/1ba house cost roughly the same across the country.

Same with the federal employee pay tables, they were identical from shore to shore, i.e., no locality tables.

When I was a kid in the early 60,s people used to ride the cable cars to work in SF. We lived in San Anselmo and my parents used to take us to SF when north beach would be closed off so the beatniks could read poetry and display their art.

Carlos – would posit at least part of the City’s current malaise can be linked to it losing metro-generated core economic activity in the face of becoming a significant bedroom community for Sil Valley over the last couple of decades…

may we all find a better day.

May bee 1sty, how some ever,

Last time working in SF, to give estimate to best client worked for at several bay area periphery location, got out, turned around, and saw bad guys casing my truck.

Stuck finger in pocket and told them beat it or I would shoot, and they did.

Told the client sorry, could not work in SF, so he did not buy the building, and we moved on. About 35 years ago.

I lived there in the 90’s when rents were still somewhat cheap. Lots and lots of artists, musicians, film & videographers, poets, writers etc etc. Each neighborhood was like a different country or set of countries and each had rich cultural communities. By the 90’s some of the neighborhoods were dangerous with random drive-bys. My neighborhood was a “war zone” but it wasn’t really that bad if you knew it well. Met interesting people from all over the world. You could meet and have lively conversations at bus stops with someone from Mongolia and another person from Nigeria or Vietnam, Guatemala or Australia, Germany or Costa Rica all in the same day. Intelligent creative people from all over the world.

Almost all of the artists and interesting people I knew moved out as rents started going up, unless they had rent control holdouts or subsidized low income housing. SF is a shell of what it once was. Still interesting, but not as it used to be. A lot moved out of NYC as well from what I understand, because of the cost of living. Some moved to Detroit or to weird little desert towns in the SouthWest.

In the late 1990s, a buddy of mine and I both bought homes in an affluent neighborhood between DC and Baltimore in the $500K range. Over the years he added a beautiful pool with a wrought iron fence around it, a huge deck with gazebos on each end, and a nicely finished basement with a home theatre etc…

He was a CFO of a successful lobbying firm and he kept refinancing his house to pay for all the extra bells and whistles. He said it was “free” money.

Much to the chagrin of my wife, I only added a nice Brazilian wood deck that I paid cash for. We had no pool and our basement stayed unfinished.

In 2015, we both sold our homes within months of each other. Mine was by choice but his was by necessity as he had to take a large pay cut to keep his position.

Interestingly, we both sold our homes for about the same price, about $1.1M.

I netted over $800K and due to the cost of his “free” money, my buddy netted less than $50K and rented a condo near DC.

I wonder how many people have put themselves in my buddy’s situation over the last few years with all that “free” money.

“…the layoff announcements also create a lot of uncertainty among people who haven’t been laid off yet. And that can’t be a good motivator to go out on a limb and buy a still ridiculously overpriced home.”

FOMO has been replaced with fear of buying!

Undoubtedly rents and leases had also gone up during that crazy speculative period. I suspect that there must be pressure to bring these rates down too.

According to a big RE investors’ forum I lurk on, yes, rents are going down.

Predictably: FOBR (… Buyer’s Remorse).

1) San Mateo 3y 2018/2021 trading range boundaries :

1.400,000/1,800,00.

2) Suppose San Mateo 2010/2011 low was about 800.000. // 2,400,000 minus 800,000 = 1,600,000.

3) If San Mateo form a new trading range : 1,600,000/2,000,000 in the

next three years, prices will stabilized, but in real terms about down additional 15% below the peak.

4) San Mateo might be attractive buyers. Prices will rise to a lower high.

before falling again to a spring.

5) After additional 2y/3y of trading range , San Mateo, in real terms,

will be down additional 25%. There, at 1,600,000 ; 1,600,000 x 0.75 = 1,200,000.

6) In real terms, after 6y/7y in trading range, down to 1,200,00. // 2,400,000 (peak) minus 1,200,000 (real price) = 1,200,000 down from 2022 peak.

7) From 2010/2011 bottom : 1,200,000 : 1,600,000 ==> 75% retracement.

Thanks for saying “in real terms”. With inflation running from 6% to 8%, no change at all is a real price cut.

Some new houses just went on the market a couple of blocks from me. They have not sold immediately like they did a year ago. I believe the market has turned and we’re seeing it right before our eyes. Next you will see “FOR RENT” signs going up on these unsold properties.

The house two doors down was on the market for about 8 weeks, but no “sold” sign, just the for sale sign disappearing. I have also seen a couple of “for rent” signs as well.

owners who turn to renting their properties because they cant sell them are in denial and will be the ones that suffer the greatest losses because they will be making a few thousand on renting a property, while they lose 10K-20K or more per month in the home value.

once this continues for a while there will be a percentage of people who capitulate and sell at what will become the next bottom.

Same thing here, someone built a few new Condos in a weird spot here, slapped for rent signs on them recently. Somebody’s gotta pay that nut.

Crashing prices are a time machine, they hit the recent buyers first and the deeper prices crash, they hit more and more past buyers.

It is the folly of the “debt is good” crowd who, unprepared for down cycles, seem to always get burned. Like kids, “don’t touch the hot stove” is meaningless advice until “they touch the hot stove”.

Careful kids, THIS stove may be very hot indeed.

Or as Grandpa used to say, “a cat that sits on a hot stove will never sit on a cold one”

Here in SoCal prices have reached what seems to be a permanently high plateau.

Very little inventory, and still multiple bids when smth comes up. The area I follow in north county SD had 20% of pending sell over listing price in first two weeks of January and those were not reduced listing prices.

If inventory stays this tight, I only see higher prices forward.

In terms of “San Diego is special”:

Sales of single-family houses collapsed by 43% in December, year-over-year.

Median time on the market before frustrated sellers pull it off the market, or before it sells, jumped to 20 days from 8 days a year ago.

The price has dropped by 13% from peak and is now up just 1.6% year-over-year, and is in the process of turning negative.

The median price of a SFH at $850,000 is now back where it had first been in May 2021. This is a process and takes a while.

Southern California is just a few months behind the Bay Area. There is nothing special about it.

Austin is extra “special” and deserves some attention as Texas and California attempt to one-up themselves.

Austin is top ranked loser ahead of second place loser San Francisco per the Goldman 2023 house growth predictions carnage chart.

Goldman House Price Growth Predictions 2023 and 2024:

https://pbs.twimg.com/media/FnRCLp3X0AAMpb6?format=png&name=900×900

You might like to know that Oceanside just posted the largest drop in rents in the entire state

I’m getting torched down below but I’m with you. There are places all over the city that are selling for asking or more and days on market is back to less than two weeks. Everything desirable in 92115 that was put on the market just before Christmas went into escrow a week after the new year. Junk is junk and is having issues, but non junk is moving again. 6% is what my first loan was 30 years ago and is still below inflation (government posted or otherwise). Eastern Bunny and I are only pointing out what we’re seeing and not saying we’re special or you’re wrong and we’re right, just observations. There’s no way that only 18 active house listings in a zip with several thousand units is a market in dire straits. My guess is that in a couple of months there’ll be a lot of head scratching going on as the numbers corroborate what we’re seeing.

We’ve lost several houses bc we offered wanting to pay 10-20% below list price, in several cities in Idaho, and near the Catskills in NY. We finally got one in NY under contract and were told there were 17 offers. We saw one of them as part of an escalation clause. We do think this was exceptionally well priced, and in a lower price range, bc long story but they were listing with the assumption that no mechanical things were working, although there is good evidence that they were. Estate sale. But this was after losing several bids bc multiple offer situations led is to lose the bids. Losing is pretty good proof that there were actually multiple cash offers (these all needed rehab so no mortgages could have been involved). Price drops and / or initially aggressive prices, I think, contributed to these frenzies. But there are still cash buyers making offers under 200K *and* very well priced based on the last 6-12 month selling prices.

I’m still afraid after reading all of this that we are making a mistake. But we like the house and it’s for summer recreation in our RV from Florida.

On the other side of the coin, in our hometown in central Florida, we have seen flipped houses that started with crazy high prices, after they bought too high 1.5 years ago, chasing the market down with price cuts every 15-30 days. One currently (water many months of aggressive cuts) at 300K, another at 400K, just sitting in what were absolutely red hot markets before the interest increase. I don’t know the percentage decrease but let’s say the 400 started at 479 and looked well priced. I think he paid 406 — then paid contractors and lawn guys to do a light renovation — which to me is an insane amount with which to play musical chairs. I’m guessing he planned to start higher and never envisioned this. We would pay 150 for the 300 and 200 maybe 250 for the other one. And that might be too high.

There’s no doubt the county of San Diego has dropped a good amount, but the city, I think, will be a different story. Down, maybe, down a lot, I doubt it. Inventory of SFR’s in the city is down by a lot. Junk is sitting but housing is still selling and some places are still stunning in what they’re getting. Understand that in no way am I saying there’s some sort of boom here, just that things are strangely not as dire as the rest of the state and I’m referring to the city and not the county. I figure i better qualify what I’m saying because I’m about to get torched.

Personally, I think it’s due in large part to the city policies that have made every single parcel available for multi family (easily 4-6 units). Check 92115 and look at on market times, pending, solds and for that matter, available inventory of SFR’s. A couple of days ago there were 18 houses (not condos, etc) actively listed.

I’ll get my flame proof suit ready.

Just to give you some perspective on your “San Diego is special” meme here. It’s not special. It’s years behind San Francisco. In SF, single-family construction essentially stopped over two decades ago. Just about everything that has been built is multi-family, and a lot of it has been built — high-end condos and apartments, mid-rises, towers, fill-in projects, replacing industrial with residential, replacing single-family with multi-family, etc.

And yet — this is the special just for you — the price chart above of San Francisco, with prices plunging, is for single-family houses. All charts above are for single-family houses.

There is nothing special about San Diego. It’s just a little bit behind. Get used to the modern world of big dense cities where people with some money want to live in towers and other multifamily buildings. This is a desirable choice for them. And they’re willing and able to pay lots of money for the privilege. This has changed the dynamics of the housing market many years ago.

If you’re still not convinced, look at Manhattan, which is ahead of San Francisco. It’s nearly ALL multi-family, and the housing market there has its booms and busts like everywhere else. Note that some of the most expensive homes anywhere in the US are in these multifamily buildings in Manhattan, such as those on Billionaire’s Row. Get used to it.

Well it is special when your entire world is build on a matrix re-enforced by cognitive dissonance..

“Oh oh but the weather is so nice….lol”

“This place is different” == “This time is different” but for real estate LOL

*”Not in my area”*

What will happen to these cigar building if Shi infect the world in

rd II.

51 feet wide lot from north to south. 126 feet deep lot from west to east. A 102 year-old Sears Craftsman kit-built 2 bedroom bungalow and a detached two car garage. To me, having the privacy of a single family home and the space for my apple trees, a large raspberry section and two productive gardens is priceless.

Your mileage may vary.

San Diego has lot of people who think like you. May be they are right.

A lot of my friends bought home sin last 2 years or so. They say san diego is special and this time is different.

But I see price reductions everywhere and prices are down almost 20% or so on the ground.

I still see stuff hit the market here in Austin and get snapped up. The party line remains that “it’s different here,” which works terrific as a sort of aural emetic. Hard to tell what’s really happening as this is a non-disclosure state.

There’s a reason why the term “bagholder” exists.

Don’t second guess obvious trends and expectations. Use your head.

We do need people to keep buying at these inflated prices otherwise prices wont go down at all.

Without bag holders there is no price discovery

With all the new condo/apartments that are suppose to enter the market this year & next, not just in the bay area but many other metro, condo prices in particular have a long way down.

According to the Salt Lake Tribune (2-3 months ago), for every current apartment, one was under construction and another one was in the planning stage for up to a 200% increase in availability. At least 100% for those under construction. No lender is stupid enough to lend on a shrinking population (see below). Or are they?

200% increase in population? Really? Especially with the Great Salt Lake turning into the Great Salty Lakebed.

The State of Utah states there were all of 299 new enrollments in ALL of Utah school districts instead of the usual 7,000 as of Dec. 2022.

299 from 7,000??????? FOR THE ENTIRE STATE??? What the heck is happening?

As the GSL shrinkage got world wide reporting (including the Hindustan Times) perhaps people are fleeing instead of moving in. If this is the case, what about all those thousands of new apartments and houses? 299 new sales?

The collapse will be not when, but only how big and how long?

Any thoughts?

In regards to the numbers you state about the low increase in student population, it might be caused in part by the mix of the who is actually moving in. For example, in the north Idaho county where I live, the people moving in are almost exclusively wealthy out-of-state retirees. So much so that the largest age group in the county now is 60 years old and above. There are now more old people (60+) than 0-20 aged people. This all occurred between the 2010 and 2020 census.

It is probably even more askew now.

Utah is not politically attractive to many. You think you can tolerate it, but then you decide that the cost of living and the politics are better elsewhere. Having your tax money money distributed to polygamist cult schools and overtly racist school districts gets old. Getting your reproductive rights taken away gets old. Knowing that “Spotlight” isn’t just about Catholics gets old. The same goes for Idaho.

Yes, the scenery is spectacular.

Um, have you looked at the AQI data?? 🤔

The number of homes for sale is still extremely low. Wake me up when some of those 1.5MM STR’s in the US start to get dumped on the market because there’s no incentive to bear the pain of negative carry any more.

Can we really believe the listing numbers anymore? People pull and relist all the time; who knows what the actual housing stock is.

AGREE kmf:

Down the street same house on rental 4 months, with eventual reductions from $1995 to 1795. Not sure if current occupant is renter or owner.

Another just popped up this week, closer, with no asking on sign.

Nothing for sale here 3 months ago,,, several in last few weeks.

Haven’t seen any of these on internet, yet.

Those red hotcakes got cold pretty fast.

In the Boston suburbs, I am watching things sit longer, and quite a few going under ask, which hasn’t been the case since Fall of 2018.

The only heat left seems to be in the lowest quartile of the price bracket, oddly enough. The sub-$500k market (which isn’t much, mostly townhomes and condos) has the best chance of still generating a bidding war. My guess with this segment is that it is probably FTHB panic-buying as they see the amount of house they can get dramatically dwindle over the last 12 months. IMO, even though Boston stands to be more resilient than most markets (strong fundamentals, less parabolic growth), I still maintain the high prices make it extra vulnerable to interest rates. Most buyers would be wise to wait 12/24 months if they can.

Out here in the exburbs it’s similar.. more are sitting, and the ones that are moving are either gorgeous or cheap. New condos (which aren’t that special and are in a horrid spot) are posting “For rent” signs because the builder knows he can’t sell.

We had had one sitting on lakefront for months now, they are asking for peak from last summer. GL with that.

Rural Norcal, the middle priced homes are going faster than the bottom or top homes. But- only those in excellent condition are selling fast.

Probably because it’s almost impossible to find skilled construction workers. And the top and bottom are suffering from poor maintenance.

Tech businesses pay the employees they are terminating six months’ wages.

Therefore, only by making layoffs and maintaining a lower workforce for longer than the first six months can the savings from the lowered headcount be realized. Companies would not have been laying off employees if they were anticipating a soft landing and swift pivot.

The head of the Central Planning Committee himself, J Powell has declared on the record that for inflation to go down people need to lose their jobs. He should lose his job, along with the CEO who failed to plan appropriately and created a fake economy and a fake job market. Of course the corporate overlords are obliging as if it wasn’t them who over hired in the first place. Just a clueless corrupt clique.

Love love love these decline…just need SoCal to catch up and would be nice if I get to see the speed of the drop and decline X2-X3 times as severe.

You never know, as they say the pendulum can swing the other direction just as hard…I know this is impossible for SoCal house humpers to wrap their head around, hopefully reality can soon wipe that little last smirk from their face.

A friend in our neck of the woods (north Idaho) sold her house for 2x what she paid three years ago (they have to buy smaller for her husband’s change in health situation). They were checking out a house and my wife went along for a look-see. The realtor stated that while traffic is down, out-of-staters are still making offers above listing.

But what I thought was interesting was that many of these same out-of-staters are deciding not to buy in the area because of the plethora of “Trump” signs everywhere.

Definitely evidence of self-selecting per political ideology.

Trump + smoke all summer? And check the American lung association ratings — where many Idaho and Utah cities rank at the very very bottom. I love the scenery but I love my lungs much more. Buy at prices where you can leave as soon as the smoke starts, and not feel badly about what you spent. And plan to tolerate a whole lot of absurdity as far as the political choices when their homes are literally being smoked out.

Imagine the mindsets of people, if, a year from now, something that looks like a market crash is just beginning to gather serious downward momentum, after watching 2023 be a year of continuous uncertainty, where all the markets bounce around sideways, with extreme volatility. Might get exhausting to play?

I just saw that on my bingo card

Real life story from a post in another forum I belong to:

“I retired in January last year as a professional photographer in San Francisco. I spent 3 months getting my live/work condo ready to sell, which I used as my studio…new paint everywhere, new floors, etc. It looks great, with lots of positive comments from prospective buyers.

Unfortunately my timing could not have been worse. The red-hot real estate market in the Bay Area dropped like a rock, with the poor economy and rising interest rates leading the way. I have not had a single offer since March, even with 2 price reductions. We pulled my listing down in December, and will re-list it this week so it will show as a new listing.

I had planned on using my equity as a cash fund to ride out the downturn in the stock market. But if it doesn’t sell in a couple of months, I’m resigned to the fact that I will need to become a landlord for a year or 2. And the politics of SF make this less than desirable, with horror stories of tenants not paying rent and refusing to leave, as city officials stand idly by.”

He might be a good professional photographer but looks like he will retire into being an excellent knife catcher…

Price reductions not working and becoming a landlord while originally counting on selling as the nest egg? I am sure his price reduction isn’t aggressive enough, if price right, RE will move even now at the first inning.

Folks, this is what forever optimism disease do to people, once you can brainwashed into believing the gully but always up narrative, you will HODL till the bottom. Maybe he will catch that lucky break soon enough, I wouldn’t bet money on it in this environment

That type of thinking from the poster above is the type of thinking that allows some of us to swoop in during bad times and buy into huge discounts. Still remember buying a home in 2011 that was at nearly at 65% off from the high at 2007.

You could track the the tiny discounts from 2007 to 2011 all the way to the bottom. Made a nice mountain house until we sold it in 2021 to someone who just listed in less than week ago and it already taking a small haircut unless they also think those tiny discounts will attract a buyer.

I told the wife if it’s around in 3 – 4 years let’s rebuy it again. Hah

The owner shouldn’t have renovated and should have priced it to sell immediately in early 2022. It was ‘ready to sell’ the second the owner was ready to move on. You always want to get ahead of a downturn as chasing prices down can be very expensive.

A home is a roof over your head and should be treated as such. Anyone who believes otherwise is living in a dreamworld. It’s not a good investment over the short term. Usually, takes 5 to 10 years to start making a profit to cover all the closing costs. I hope I don’t have to listen to a bunch of sob stories about homeowners who bought at the top of the RE market during the pandemic sucking off those 3% mortgage rates, when to economy collapsed, with 22 million Americans out of work, and Americans were dying all over the place from Covid-19, and now trying to sell into a crashing RE market.

A home is roof over your head that leaks after a hurricane. Warren Buffett’s insurance company left the state. Another insurance company doubled insurance rates. You may try to get insurance and then hear the response, “We do not have agents in your area.” Plenty of water, many unable to afford flood insurance. The hurricane storm surge was fifteen feet.

Home insurance is over $4,000/yr in Florida. I wonder how many Realtors are putting that in their sales brochures. Zero.

I am struggling to find a violin small enough for that person.

I had pretty stock on them but used it all up when Musk was crying about how people are so mean to him…time to stock up again, if the market does crash, be ready for a flood of entitled owners/flippers/house humpers singing the same tune

“We pulled my listing down in December, and will re-list it this week so it will show as a new listing”

Tell your buddy on the other forum that everybody is on to this sad little trick by now. We can see the price and listing history, bro.

BLS inflation calculator has the $50 per month rent for a small flat (studio) in SF and Bay Area in 1970 at about $365,,, so reality at $2200 might be considered the bubble of all times AA…

While due to degradation of USD in that period it is unlikely we will ever see $50 ,,, I don’t doubt it is possible, just unlikely…

More likely down to $4-500 when the poop really hits the paddle which, no matter who wishes and wants and uses all wiles otherwise,, WILL happen eventually, as it always has.

A supposedly well-educated 20-something cousin of mine and her supposedly well-educated 20-something husband had to be screamed out of buying a ‘cute’ bungalow in Austin, TX for $1,100 per sq. ft. This during the summer of 2021.

Still waiting for my Thank You for Screaming Some Financial Sense at Us card from Hallmark, but maybe I’ll get some nice socks for xmas next year.

Even $200 psf is too much in Austin, TX.

$175 is the going rate in TX where I am. Nice 2000 sq ft brick home though.

It’s amazing to me that the Austin area is now this ‘hot’ pricey real estate market. I moved there in the 90s primarily because it was inexpensive but even still the ferocious weather, scenery, traffic, ugly sprawl and Texas culture drove me away after a couple of years.

The prices in Austin are absolutely insane…especially when you factor in the unbearable summer humidity and astronomical property taxes. Is the cool factor really worth it?

Much of the cool factor pulled in the rug here ages ago. There’s a few ghosts left here n there, but mostly, it’s finished. Now it’s almost entirely West Coast carpet baggers seeking a poor man’s California: every weekend, Lake Austin is festooned with yuppies on their silly paddle boards; every other corner of town is another trendy mixed-use complex owned by hedge funds who scraped & dredged the cities soul, only to water it way down & sell it back to all these credulous transplants with their designer breed dogs lining up to pay 10 dollars for breakfast tacos at pseudo homespun shops. Then again—show me a once fine city in this country that hasn’t been wrecked by this same tidal wave of commercial homogeneity.

Die.

What many Austin suburbs have are great neighborhoods, without crime or homelessness. They are generally full of wonderful people. 30 minutes away, are fabulous restaurants. Granted we do not walk around downtown at night without a thought, the way we did 5 years ago, but compared to the Bay Area it is still lightyears more user friendly. Yes, the summers can be unbearable, but if you can escape to Colorado or Canada, they are a small price to pay for the rest of the year. It feels a bit like Silicon Valley in the 1990s, before things went sideways.

Reply to Ronda:

My experience a bit different.

Lived for 11 years near Dallas.

There were 2 primary reasons I left Texas and the climate was one of them.

Mind you I’ve lived in 6 states and other than Redwood City (just one year long ago) and near Seattle (4 years) I thought the climates were pretty bad in all of them.

November was my favorite month in Dallas just as June is here in Spokane Valley (also a cruddy climate IMHO…been here 22 years… its getting hotter summers nevermind the smoke in the fall).

But as to Dallas climate:

January: very nice weather mixed with chilly, occasionally cold weather.

February: good month in general.

March: good month

April: mostly good but some humidity and heat creeping in

May: too hot and humid for me, but some nice days

June : too hot and humid

July, August: very hot, too consistently hot. Little less humid but its not a Bend Oregon dry heat either.

September: still too hot

October: first half too hot, 2nd half pretty nice

November: ahhhhh. Refreshingly cool.

December: nice days mixed with chilly ones. Occasionally cold.

There are of course tornado concerns.

Hail is Texas size.

Lived there 11 years never saw a twister. Rode my bicycle near Wylie (?) and saw remnants of one that hit some small town NE of where I lived. 1980s, 90s.

A former neighbor of mine who still lives there sent me aerial video of the damage done a few years ago when a tornado went thru east Dallas.

It stopped doing damage about a mile south of where I had lived in Rowlett.

Her husband has created a fairly large concrete dome as a tornado shelter (in their backyard).

Everyplace has its challenges… much of the west dealing with drought and wildfires August thru October. Definitely a less pleasant place to live than 20 years ago when I moved to eastern Washington from north of Seattle.

I liked living near Dallas except I never got used to the heat. No mosquitos where I lived though… unlike the mosquito haven where I grew up in Ohio !

JPow (AKA the big bad wolf): I’ll huff and I’ll puff and I’ll blow your house down. 😎

Great graphics.

“In my area”, Zillow has completely stopped showing me how much poorer I am getting every month. Their zestimate histories have been pulled. Apparently, now that prices are coming down, they (being glorified realtors/former house flippers) don’t want that information getting out.

Where are all the new purchasers going to come from?

Legal immigration is way down, the birth rate is way down, even below the replacement rate here in Utah of all places.

Thousands of apartments going up (3,000 under construction in SL), lots of new subdivisions (I traveled on SR 111 last weekend – three new subdivisions that were not there 4 months ago), however…

The State of Utah states there were only 299 new enrollments in the ENTIRE STATE for K through 12 as opposed to a normal increase of 7,000.

Once again, where are all the new buyers supposed to come from?

“Where are all the new purchasers going to come from?

Legal immigration is way down, the birth rate is way down, even below the replacement rate here in Utah of all places.”

And many more high paying jobs will be offshored after the latest round of layoffs. Most will never come back–count on it.

I’ve been visiting SLC for 2 decades for work and I always stay downtown.

The walkability and the restaurants, event center, hotels make it a nice place to visit. I take walks up City Creek Park after work. It is also a 20-30 minute drive to world class ski areas.

My hotel offered a ski shuttle. Stay at a less expensive hotel in SLC and take a 30 minute hassle-free shuttle to go skiing.

I was amazed in the early 2000’s on how inexpensive some of the old Victorians were within walking distance of downtown. I had other financial priorities or I may have bought one.

I think since SLC is the state capital and close to local tech and entertainment, it will draw in buyers of second homes and people who want to retire. It is similar to Sacramento but with more tech and closer to the mountains.

It seems less overtly racist now than in the 90’s. At least in the city. I traveled with a friend there in the 90’s and people rushed to put up “out of service” signs on their store bathrooms when they saw us coming. Then glared at us.

Then I got stuck there for a week in 2017 and it didn’t have that nasty vibe anymore. People looked comfortable and unconcerned walking around.. Not like the 90’s.. However, I saw a lot of young adults but hardly any children.. Maybe some cult ate them.

Yeah, that, and they have that Joseph Smith sphinx.

My observations are of SLC are of the city and not the state.

SLC was one of the most liberal cities in the US during the early 2000’s. I was awoken several times by hundreds of Iraq war protestors marching by my hotel window led by the Mayor. The city was outright combative by allowing a strip club to open within a block of the Mormon Tabernacle.

Even my more liberal town doesn’t allow strip clubs that close to churches or schools.

The city has a very young population. Many are UofU students. Others are ski bums since it is an inexpensive place to live close to skiing and the outdoors. Many of those young people are renting those grand old Victorians downtown inexpensively (Maybe not anymore). Maybe it is good that I didn’t become a land baron.

It is definitely not a 1960’s/70’s San Francisco but it has a good safe vibe with many microbrews and events only seen in a larger city.

The infrastructure is excellent after the city widened highways and allowed more hotels and restaurants for the 2002 Winter Olympics. I rarely see traffic when I drive. The airport is a Delta hub.

I was just a visitor so I was never deeply embroiled in the politics. I just read the local SLC Tribune and the SLC independent newspaper during visits.

It seemed more balanced during my last visit. Though Pioneer Park downtown is full of homeless and some violence and drug dealing. I wouldn’t walk through there at night. Liberty Park 9 blocks away is surrounded by old grand Victorian houses. I’m a walker and I never felt unsafe.

I’d move there and feel safe walking almost anywhere.

I think it is interesting that ski resorts like Park City and Deer Valley that were sites for the 2002 Olympics are not complaining that much about worker housing during this latest boom. The home prices have gone to the moon during this time in these areas for second houses and VRBO’s. However, SLC is a 20-30 minute drive away with sufficient housing and a relatively short commute. Will this drive growth in SLC? It apparently is.

UT isn’t a low cost state anymore. People from high cost high tax states will still move there but people from the majority of the country will not move there because of cost. We are seeing the same thing in CO, it used to be affordable and filled continually with transplants from the Midwest looking for better weather and natural beauty, now move ins are disproportionately from the high cost coastal states and move ins have sharply declined.

Besides where will all the people come from to buy those new houses and condos, where will the water come from?

It is not just Arizona: “Cox’s newly unveiled budget calls for millions to fund water conservation measures, including $100 million to specifically lease water rights for the Great Salt Lake. He also recently closed most of the Great Salt Lake’s watershed to new water rights.”

It looks like “The Limits of Growth” is being hit everywhere.

Weren’t you guys claiming that people pay their credit card balances in full every month?

That people only used their credit cards as a convenience and NOT as a means to borrow and spend money they don’t have?

Hello, geniuses out there, (unless you were something else):

Americans paid $5 trillion in 2022 with their credit cards. This is a payments device.

In terms of borrowing, credit card debt increased by $43 billion year-over-year. So they ran $5 trillion with a T through their credit cards, and balances outstanding only increased by $43 billion. You see how minuscule the portion is that doesn’t get paid off?

https://wolfstreet.com/2022/11/15/credit-card-balances-burden-delinquencies-and-third-party-collections-in-q3-consumers-still-in-great-shape/

And credit card balances as a percent of disposable income:

Are some subprime borrowers going to default? Sure. Some always do. But during the pandemic, the delinquencies hit record lows (free money helped). And those delinquencies have been coming up from RECORD LOWS, and we expect that as reality sets in again:

Another Holy Molly graph. This one is far more painful than the cars ones.

I learnt early on ( although I’ve never seen it written anywhere) that RE waves (up and down) start in the Western US, and propagate east. The last being NY. And it then migrate to western Europe.

This is going to be painful for those without a strong cash cushion.