Quantitative Tightening is starting to add up.

By Wolf Richter for WOLF STREET.

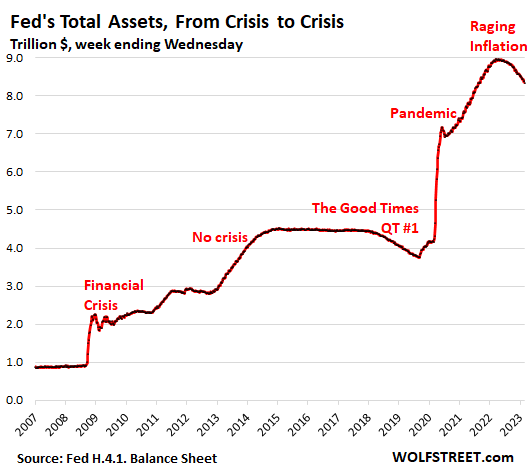

The Federal Reserve has reduced its balance sheet by $626 billion since the peak in April 2022, with total assets now down to $8.34 trillion, the lowest since August 2021, according to the weekly balance sheet released today. Compared to a month ago, total assets dropped by $94 billion.

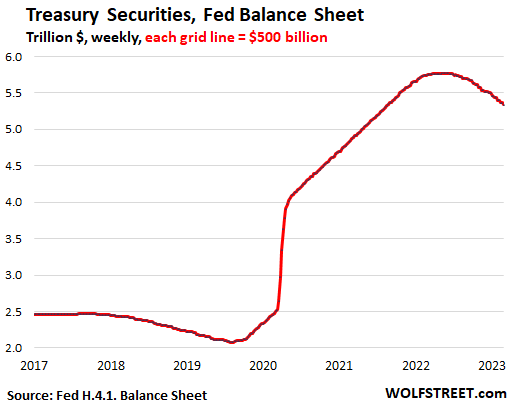

Treasury securities: -$435 billion from peak.

Since the peak in early June, the Fed has shed $435 billion in Treasury securities, bringing the total balance down to $5.34 trillion, the lowest since August, 2021. Over the past four weeks, the Fed has shed $61.2 billion in Treasury securities, exceeding by a smidgen the monthly cap of $60 billion.

Timing: Treasury notes and bonds “roll off” the balance sheet when they mature. Their maturity dates fall either on the middle of the month or at the end of the month. At that point, the Fed gets paid face value for the maturing Treasury securities.

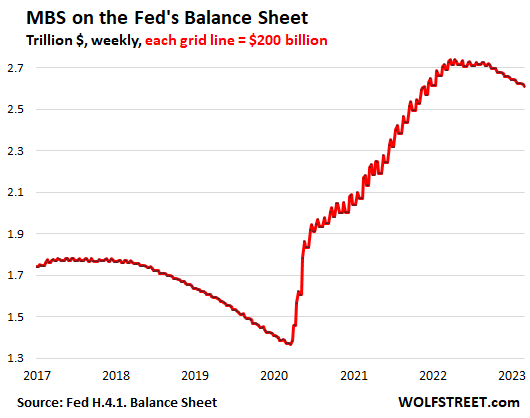

Mortgage-backed securities: -$130 billion from peak.

The Fed’s holdings of MBS have dropped by $130 billion from the peak, to $2.61 trillion. Over the past four weeks, MBS have dropped by $15 billion.

These MBS are all backed by the US government (“Agency MBS”), and the taxpayer carries the credit risk, not the Fed.

The cap for the monthly roll-off is $35 billion. But each month, the roll off has been below the cap, and over the winter by about half. This has to do with the plunge in home sales and the collapse in mortgage refis as mortgage rates have risen.

MBS roll off the balance sheet primarily through the pass-through principal payments that all holders receive when mortgages are paid off, such as when mortgaged homes are sold or mortgages are refinanced. The principal portion of regular mortgage payments are also passed through to MBS holders.

The downward zigs in the chart below reflect these pass-through principal payments that reduce the MBS balances on the Fed’s balance sheet. The upward zags reflect the Fed’s MBS purchases during QE.

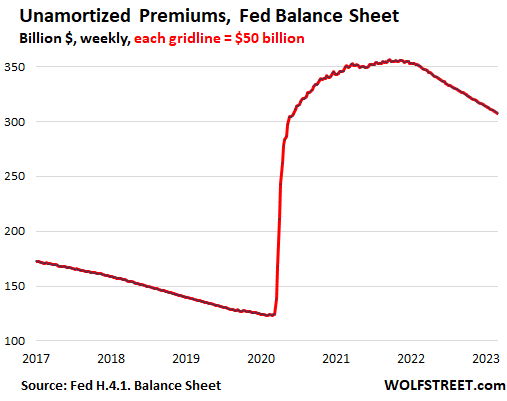

Unamortized Premiums: -$45 billion from peak.

Unamortized premiums fell by $48 billion from the peak in November 2021, to $308 billion. Over the past four weeks, they fell by $3 billion.

Every investor that buys bonds in the secondary market has to deal with this issue when market yields for that maturity are lower than the coupon interest rate of the bond: The bonds trade above face value. This “premium” above face value becomes a capital loss when the bond matures and the holder gets paid face value. That premium is the price paid for the above-market coupon interest payments. So over the life of the bond, it works out. But how do you account for that premium?

The Fed writes off the premium in regular increments over the life of the bond, and by the time the bond matures, the premium has been written off entirely. This amortization matches the higher coupon interest income from the bond with the corresponding write-down of the premium. The Fed accounts for the premiums in a separate account, “unamortized premiums,” and each week, the amortization of the premium reduces this balance:

Keeping an eye on potential warning signs.

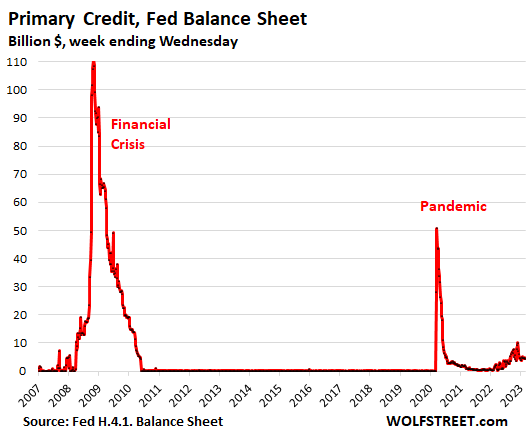

“Primary Credit” – the Discount Window. The Fed lends money to the banks at the “Discount Window,” for which it charges banks currently 4.75% in interest. This is not free money for the banks. They could borrow money for much less from depositors, if they can find depositors willing to accept lower rates on their deposits. They usually can. But when they can’t, the balance of primary credit begins to spike, indicating that at least some banks are coming under some funding stress.

Primary Credit started edging higher about a year ago, as interest rates were rising, and at the end of November 2021 reached $10 billion, which is still minuscule. Since then, the balance has dropped to $4.4 billion on today’s balance sheet. So far, so good:

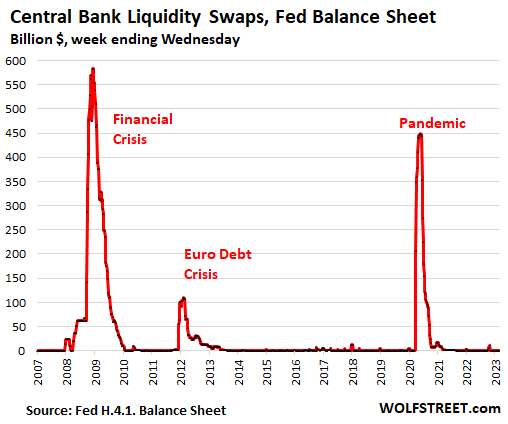

Central Bank Liquidity Swaps. The Fed has well-established swap lines with major central banks, where that central bank can swap local currency for US dollars with the Fed. Swaps have maturities, such as seven days. When they mature, the Fed gets its dollars back and the other central bank gets its currency back. There are currently only $419 million (million with an M) in swaps outstanding. So far, so good:

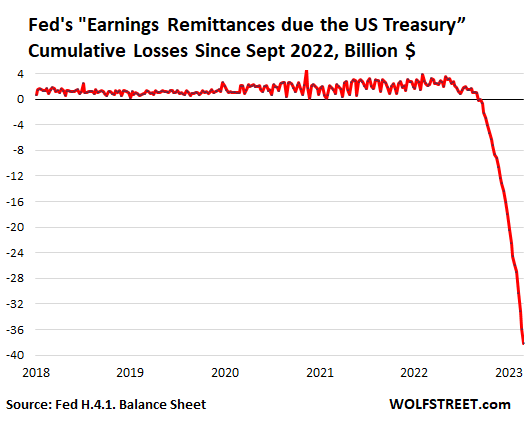

The Fed’s cumulative operating loss since Sep 2022: $38 billion.

From September 2022, when the Fed first started making operating losses, through today’s balance sheet, the Fed lost $38 billion.

The Fed’s trillions of dollars of bond holdings generate interest income. But the Fed bought these bonds when yields were low.

The Fed is paying interest on the cash that banks deposit at the Fed (“reserves”) and on overnight reverse repurchase agreements (RRPs) where the counterparties are mostly Treasury money market funds. But the Fed jacked up these interest rates as part of the rate hikes.

In 2022 up to September, the Fed still had made an operating profit of $78 billion, which it remitted to the Treasury Department, as it is required to do – a sort of 100% income tax. Since 2001, the Fed has remitted $1.36 trillion to the Treasury.

But by September 2022, the interest expense started exceeding the interest income from its bond holdings, and the Fed started having operating losses. The remittances stopped.

The Fed tracks the operating losses in the same liability account, “Earnings remittances due to the U.S. Treasury” (chart below).

At some point, as QT shrinks the reserves and the RRPs, the interest expense begins to decline, and eventually, the Fed is going to make profits again. Those profits will be taken against the cumulative losses in this account. The Fed will not remit any profits to the Treasury until the cumulative losses have all been reversed, and the account starts having a positive balance again.

As a reminder: Losses don’t matter to a central bank that creates its own money. It can never run out of money, obviously, and therefore it can never run out of capital. The Fed’s capital is set by Congress and it has not fallen since the Fed started making operating losses.

So these losses aren’t an issue for the Fed, but the taxpayer misses out on a special QE gravy train, namely the remittances.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

What would be considered a “healthy” level for the Fed’s balance sheet?

Just eyeballing total assets, it seems like 3 trillion and dropping would be back to the pre-Pandemic trend, but is that still overburdened relative to the rest of the economy?

As an aside, one must learn when it is necessary take a step back and get some air.

At this point I think the appropriate conversation is not about what the FED’s balance sheet should be, but rather why the FED even exists and how we can dismantle it. The damage they have done to our society is incalculable.

It’s not easy to EFF things up so grandly. You need a big bunch of really smart, qualified and powerful central bankers to come together and work closely in a team, with their best intentions and efforts to pull off such MIRACLES!

Fed will be abolished. Americans are looking ahead to a shitload of pain in all possible outcomes. So Fed is no longer be politically tenable.

The horrifically difficult thing is how to undo the Fed’s balance sheet (whose operation strongly encouraged trillions in uneconomic investment) without utterly destroying what little remains of the American economy.

If those trillions were undone immediately, the resulting panic (translation – “risk off” in credit mkts, meaning viable companies could not get their maturing debt rolled over…pushing those *viable* companies into destruction) would destroy the viable and unviable alike.

I hate the Fed/DC and all the harm they have done in the self-congratulatory name of “stability” (which just let economic cancer accumulate so that sleazy politicians could spend decades avoiding difficult decisions).

But the Fed’s slow-roll (allowing incremental takedowns of unviable companies…as they can’t survive at non-ZIRP rates) may be the best we can hope for.

Again, it would be great if there were a website that clearly consolidated failed re-financings/loan rollovers/defaults as that would give everybody a sense of progress in wearing down Mt. Hopeless (all those zombie debts that are incapable of repayment).

One interesting thing is how loan delinquency/default rates are still pretty low despite horrible economic fundamentals…to the point that you wonder if banks/lenders are feverishly working every angle to delay recognition of loan problems (bankers could tell us exactly how easilt/long such stats can be gamed).

Leo,

No. The Fed will not be abolished as long as Congress is controlled by the Two Party Duopoly.

Look at the 25 February 1927 McFadden Act to see why.

A 20 year charter was given to the USA’s first and second central banks when they were started by Congress. In both cases, Congress did not renew the charter. The banks were then terminated. The Fed was also given a 20 year charter in 1913. That no longer applies. Nor will it ever.

The irony is that the Act was named after Louis Thomas McFadden who was a member of the U S House, and also Chairman of the House Committee on Banking and Currency. But some McFadden’s statements in the House thereafter are quite the read. He became an opponent of the Fed. But the Fed’s grant of immortality carries his name to this day. C’est la vie.

Depth …….

Plus 1,000 % on your comment. All the multi-millionaire Fed predators should be prosecuted for their actions and the Fed eliminated

Fundamentally, all of this stems from the federal government growing out of control in size. The Fed is just one example of that.

The entire beast needs to be starved and shrunk back to something that resembled what it looked like in the 1800s

The Fed was constructed in 1913 on Jeckel Island, by New York bankers.

“Fundamentally, all of this stems from the federal government growing out of control in size. The Fed is just one example of that.”

No the FED enables that. Do you think the corporations and the government could have attained that size they have without the FED? What is the government except the largest corporation in a feudal corporate system.

DC agreed.

But lets start with a formula driven, hard rail monetary policy along the lines of a FFR equaling a three month moving average of a legitimate inflation metric.

There is way to much leeway and subjectivity in Fed Monetary Policy.

The fact they pumped the money supply (M2) by 38% in two years is beyond comprehension. And, it was only 12 months ago they were pumping $120 billion A MONTH into the economy by sopping up govt debt and MBSs.

In the communist manifesto one of the first things that once you to do is start a central bank.

So true. Money buys power, power buys influence, oligarchies/carftels: banks, media, big pharma, education, energy etc.. equals influential power.

The baloons of communist, symbiotic relations between the cartels and goverment have reached peak inflation as shown by the largest discrepancy in income ever.

If true capitalism is not restored, socialism comes after comunism

First amendment rights of Freedom of Speech are the foundation of capitalism. Media and taylored AI bots are destroying the first amendment.

The state of affairs in the USA(and the world) is the natural result of Capitalism. This is what commodity production for profit creates, a society dominated by a handful of corporations and the Imperialist Governments of the most powerful Capitalist Governments.

I would be happy with a statutory law that says the Fed can only buy 7Y treasuries or less. They have absolutely ZERO business buying 10-30Y bonds and mucking with mortgage rates & the long-term yield curve. NONE! It throws the whole system out of whack. And even their buying 7Y and under treasuries needs to come with limits just like there has to be spending limits on Congress. There have to be term limits imposed on Congress as well.

Like him or not, at least Trump is coming up with big policy ideas, including term limits, that can have a very positive impact on our economy and mitigate over time the growing economic & military power of China. The whole make our own prescriptions or move production to friendly countries is an absolute must.

I’m hopeful he will force the other GOP candidates to do the same. The UNIPARTY has got to go, starting with McConnell.

You’ve got to be kidding.

Trump said the stock market was a bubble immediately before being elected. Two months later, he was taking credit for stock market rises. He was badgering Powell to reduce interest rates so the bubble could be blown bigger.

This is no small deception. Little guys, factory workers, and younger generations were looking forward to Trump popping the bubble so they could have a chance to accumulate some savings and assets, and maybe buy a home. Instead, Trump bent them over the barrel with huge inflationary deficit increases and handouts to the top.

He’s not your savior, unless you are his personal friend.

They need to dump at random times and not explain it, otherwise they stay the dog getting wagged by the market Tail. But that presumes their goal is price stability not market nanny.

We’ve been duped by another group of Federal entities for the past three years too. One could argue how much better off we would be without them.

Out of 100 years of Fed control, the country has had 22 recessional years, including one depression. The 100 years before the Fed saw 44 recessions and six depressions. I’ve never heard anyone who rails against the Fed offer up a reasonable alternative. Kind of like democracy… It’s the worst system, except all the others.

The way the Fed avoids recessions is to load the burden onto the back of working people, by reducing the value of their labor through money-printing and inflation (asset-inflation and consumer inflation).

I’d much rather have multiple brief, sharp contractions that routinely punish bad economic decision makers, than the current scheme of bubbles and bailouts that reward them.

Umm, check inflation pre Fed and post Fed. A dollar was stable before, and has decreased in value almost 100 fold post. So the Fed is ripping us all off. But hey, fewer recessions…

I’m not categorically praising the Fed; to the contrary. It dropped the ball to the tune of trillions this time. But my respectful opinion is, you cannot even imagine the volatility of a world without a Fed, or what that would look like in your life. Let me suggest, bank runs weekly, and knife-fighting your next door neighbor for a hamburger, that is, when you are not abroad doing the same thing with other countries. So many Americans IMO are so spoiled and history-myopic they are hallucinating, and prepared to slit their own throats to feel smart and righteous. I hope this is not a political consensus. These folks will pull down the temple bricks onto their own heads to vainly try to achieve a Paleolithic utopia that won’t happen.

You don’t abolish the Fed. You put things back in line with what was intended. The Fed should be lender of last resort, during temporary periods of crisis, and any lending should be done at punitive rates. It should have a fraction of the personnel it currently has.

Any temporary loans or stimulus should be unwound within a year or two to prevent mission creep.

Forget the mandates of price stability and low unemployment. The market will address those issues and, in any case, the Fed cannot address those goals competently. They wind up doing more damage than good.

Three massive bubbles since 1999 is not a good record. The results are in. Intrusive monetary policy does not work. It magnifies system instabilities.

DC,

I admire you focusing on the long-term and your enthusiasm, but I don’t share your optimism about rolling back the clock on central banks or any influence “we” can have to dismantle that. Political power and change isn’t accumulated and enacted by economic wonks.

It’s accumulated by translating that into kitchen-table issues and dumbing things down to the point that inspires the masses to give you power — and that’s only the first step on a very long road to enacting change, a path with headwinds and fierce opposition.

It may be the Fed has outlived its usefulness, but I’m not so sure. I do see it has been eroded and beaten up by political forces over the long term.

I think this was covered back in September and Wolf’s answer was $5.2 trillion in 4 years. Over half of that is currency in circulation (projected out):

– Reserves: $1.6 trillion

– RRPs: near $0

– Currency in Circulation: $2.7 trillion

– TGA: $800 billion

– Other liabilities beyond the big four: $50 billion

All this data from: https://wolfstreet.com/2022/09/05/by-how-much-can-the-fed-cut-its-assets-with-qt-feds-liabilities-set-a-floor/

I hope Wolf doesn’t jump in to tell me to RTGDFA… ;)

Thanks for the link.

I think I see it. It kinda looks like that blip in 2009.

Wolf, I think you have the same graphic twice under Primary Credit and then again under Central Bank Liquidity Swaps.

Yes, thanks.

Lol Wolf needs RTGDFA

I read the article but didn’t look at the pictures.

A loophole!

You think the Fed will be selling MBS?

They might want to. But who wants to buy a tranche of FNMA paying 2.75% right now?

If discounted enough, anyone in their right mind?

Three words: “mark to market”

Thanks Wolf for the critical update. Was waiting patiently for this piece. The minuscule 15 billion MBS drop is outrageous. And what is more outrageous is that they are going to do nothing about it.

The Fed stopped buying MBS in September, after having tapered its purchases starting in June. I explained this in the article and you can see it on the chart (no more “upticks” DUH).

This braindead conspiracy BS gets to me. Read the section on MBS, it explains exactly why they’re coming off so slowly. I’m not going to re-explain the same thing here because you’re too lazy to read it in the article.

In addition, even if the Fed doesn’t sell any MBS, the MBS roll-off will increase by some, simply because we’re going from the dead-of-winter into the spring selling season. Though it will take a while to show up on the balance sheet, over the next few months, we’ll see the roll-off of MBS increase:

https://wolfstreet.com/2023/02/08/why-the-pace-of-the-mbs-roll-off-from-the-feds-balance-sheet-will-increase/

Wolf, I have read your reports on Federal Reserve MBS and you indicate the Fed has ceased buying MBS? Is this true? How can the roll off be so slow with out some buying? Using simple math and the max 35 billion per mo. roll off rate it will take 74 years to close out the position. Certainly at some point the Fed will start up QE again including MBS purchases and it will probably happen before any meaningful draw down of the current MBS holdings. Who in their right mind would tie up huge amounts of capitol in a mortgage for 30 years @7% looking down the barrel of the underlying asset depreciating? Sounds like something only the lender of last resort would do.

“How can the roll off be so slow with out some buying?”

Curious as to Wolf’s reply, but my guess:

With inflation at 6+%, folks with lower rate mortgages (myself included) are making minimum payments and not paying extra towards the principle.

Why would I pay extra towards a 2.7% mortgage when I can take my extra cash and stuff it into 5+% T-bills?

principal*

Time for more coffee..

Sorry 74 months to roll off completely.

If the Fed ever cuts interest rates, the roll-off of MBS will become a HUGE torrent because there will be a tsunami of refis, which means mortgage payoffs, and the principal is passed through to MBS holders. And those MBS will vanish.

Back during the pandemic when interest rates dropped, and refis exploded, the roll-offs were in excess of $100 billion a month. And the Fed had to buy a HUGE amount in MBS to replace them, and to add to its balance sheet.

In addition, this torrent of refis and therefore mortgage payoffs cause the pool of mortgages backing the MBS to shrink to such a point that it’s not worth maintaining the MBS, and the issuer (such as Fannie Mae) will call the MBS, meaning pay holders for it and withdraw it, and repackage the remaining mortgages into new MBS. I don’t know of any 30-year MBS that made it all the way to 30. They’re called within a number of years – sooner during a refi boom, and later when there are fewer refis.

So don’t worry, those MBS will come off quickly if mortgage rates drop.

If I were in charge…….

Wouldn’t it have made more sense to stop buying MBS’s before raising interest rates? The Fed caused the slow roll-of by raising rates before they stopped buying. Is there some ulterior motive with their order or was it an “Oops”?

Now some mortgage holders with 2.7% mortgage rates are holding on to them as if they were gold. In some ways they are.

“How can the roll off be so slow with out some buying?”

RTGDFAs (note the plural). The smaller the amount of housing market activity, the smaller the amount of passthrough principal payments on the MBS held by the Fed. The smaller the amount of passthrough principal payments on the MBS held by the Fed, the smaller the amount the Fed can remove from the balance sheet under its program of passive rolloff.

The solution (when spring selling season inevitably fails to bring monthly rolloff high enough) is of course to sell MBS into the market, but the Fed doesn’t have the conviction or the backbone to actually do it, despite teasing it last year.

After thinking a bit, maybe there is some genius to the Fed’s madness.

“Now some mortgage holders with 2.7% mortgage rates are holding on to them as if they were gold.”

What better way to avoid a housing crash than to make your current mortgage have great value?

1) You won’t walk away if your payments are low even if the value of the house has dropped.

2) Would you walk away from your house and a 2.7% mortgage payment if renting had a higher monthly payment?

The only reason to walk away would be high unemployment which would prevent someone from making the low mortgage rate house payment due to a job loss. However, you have to live somewhere.

Another point is that with any 30 year mortgage, the first few years of payments are mostly interest. There is very little principal paid until later in the loan.

For example, for a 500K 30 year mortgage at 2.75%, the first month payment is $895 in principal and $1145 in interest. Only 895 would be applied as part of the roll-off. The last month payment 30 years from now will be $2037 in principal and $5 in interest.

If the Fed has loaded up with MBS’s originating in the last 3 years, it will take up to 30 years for all of the MBS’s to roll off if nobody sells or refinances.

As you and Wolf pointed out, if the Fed starts QE again and lowers rates, the MBS’s will roll off at a faster rate as people refi.

I can guarantee that if the Fed simply doesn’t buy more MBS that it will take a maximum of 30 years for 100% to roll off.

Wolf said: “Back during the pandemic when interest rates dropped, and refis exploded, the roll-offs were in excess of $100 billion a month. And the Fed had to buy a HUGE amount in MBS to replace them, and to add to its balance sheet.”

——————————-

Why did the FED HAVE to buy new MBS to replace rolled off ones?

What is unclear about this sentence? The Fed had a goal (x amount of increases per months in its MBS holdings), and to get there it had to do certain things. This was an illustration of how the pass-through principal payments for MBS holders became a torrent when interest rates dropped. What is so hard to understand about it?

QT should have started in 2012.

It’s outrageous that the Fed is allowed to manipulate long term interest rates in this way to the benefit of corporate borrowers and private equity investors and other purveyors of the speculative at the expense of the common person looking for reasonable bond returns.

QE should be illegal.

Yes, but members of Congress — who could make it illegal — loved it.

Nancy Pelosi and Mitch McConnell, both in office since the early 80s, have presided over the complete and total destruction of the US as we once knew it.

Why hasn’t the justice dept. looked into their personal fortunes? We’ve been taken for a ride. These people are as corrupt as they come, and are above the law.

When taxation has to be reintroduced as a form of gvt finance (vs. money printing) the entire political class (and their sponsors) really should be taxed to destruction…but how?

How to identify the specific individuals who profited most from the madness? And how to execute upon them, whose power was great enough to control events?

I mean this seriously…without a semi-rational plan of action (for targeting and levying) all that will happen is the same free-floating impotent rage.

As horrible as it is to contemplate, the US may be so far gone that a wealth tax may be unavoidable – the question being how to justly/effectively target it.

Support mandatory retirement at 65 for ALL Federal employees, from the President down. There’s no greater way to show how out of touch with reality our political system is when you have over half the members of the Senate still serving when they’re over 70 years old.

I truly understand age discrimination, but there’s no way a cabal of octogenarians represents the best and brightest way to run a country.

It’s not like youngins running roughshot in crypto land are great leaders. SBF could have been elected to Congress if he hadany interest. Judge not your Congress by the date on their birth certificate, but by the quality of their character.

But the people still vote for them. Is it the politicians fault or the people’s? Why make these laws if the people love these politicians so much?

Cas,

One of the complaints about Teddy Roosevelt from other Republicans was, “He is out to get anyone with more wealth than he has.”

How about making that part of the oath of office?

Or, since Conservatives just love the idea of a simple flat tax, (that you could do on as postcard, as they say), how about a simple 10% of anything over $10M ?

And what is so “horrible” about even contemplating it? I think it would be great! Solve lots of problems, too.

Of course the IRS would have to become a branch of the Military, but the Coast Guard is already chasing down smugglers (drugs or Gucci purse fakes) so what’s the diff? Cheating is cheating and has to be dealt with harshly, like the kid who robs the 7-11.

Cas127,

YES!! There needs to be (gulp) reparations paid from the swindlers and crooks that benefited from the Fed bubbles, back to 1980 at least.

All the records exists. This is a great reset I *can* get behind.

I have TOTALLY lovely visions of armed IRS “seal team 6’s” parachuting onto roofs of Cayman banks, law firms, etc, etc, and getting names and documents at gunpoint before anyone has time to transfer money to shelter corps or any of their other financial tricks. And even be in and out before local military/cops know what happened.

Then a lot of “plausible denial” as to who they were or what their mission was, which is now a legitimate international technique.

a reminder: Losses don’t matter to a central bank that creates its own money. It can never run out of money, obviously, and therefore it can never run out of capital.

It can run out of trust though leading its demise.

“…leading its demise”

No it cannot “lead to its demise.” But it CAN create inflation, leading to the demise of the currency. That’s a HUGE risk and the only discipline a central bank has.

There are alternatives to central banks in history books

Doesn’t matter, stock market was falling, Bostic mentioned “25 basis points” and it did a full reversal. Over 1% easily so far. They’re not serious about fighting inflation, the gravy train keeps on chugging along

Inflation is transitory, and a softlanding is coming. I am talking to people and they are saying houses are stable pricing in Tampa area, so they are looking to buy a house before prices go up with the new people coming in droves. Everything is back to normal nothing to see here and QE is around the corner.

Good luck to you!

Wisoot-

There sure are! Jubilee is my favorite! Only problem was the LAW, the Priests, were left out of it. Kinda like commies?

Wolf could you do a article explaining the Great Reset I keep hearing about

Here’s my article about the “Great Reset”: Don’t listen to this stuff.

This is propagated by gold sellers so that they can sell you gold and make a bunch of money.

Happy1

Agreed. What is the Fed doing in the long end of the market anyhow?

Their self described “dual mandate” deals with two current real time issues…..employment and inflation. The Fed stayed away from the long end for decades…..this is new since about 2009.

Why doesn’t the fed reduce their balance sheet instead of increasing interest rates?

This way it wont have to pay interest and no losses to worry on her securities it holds.

The 10 year might go up but that will tighten the financial conditions and allow savers a return above inflation rate which are common sense policies.

Yes, that has been suggested. And it would make sense. But it would tear up asset prices a lot faster, and I don’t think that Fed wants to be accused of that.

Oh my gosh, we wouldn’t want those precious asset prices to fall! But when granny can’t afford food and the young can’t even afford a ghetto studio apartment – f**k ’em if they can’t take a joke.

I got it. Large balance sheet reduction would result in a stock market crash, which the Fed tries to avoid at all costs. They are indeed slave to the market. I fully agree with Depth Charge that this corrupt organization should be abolished.

Just found the title of an article from last year. “Esther George calls for sharp balance sheet reduction, January 2022. ” She seems to be the only good Fed.

I’m sick of the games. Why did the 10 year go down 10 bps today? Seems every few weeks they play this game. Someone or something buys bonds to bring down the yield when it starts getting too toppy and then stonks pop. It’s like clockwork. We need to bring down this shtshow doown once and for all. Reset the entire fraudulent financial system. I sick to death of it.

Fed up,

“Why did the 10 year go down 10 bps today?”

As I said earlier, the 10-year yield went down because I farted.

It had gone from 3.3% to 4% in no time. So a pull-back was expected.

It was more a rhetorical question. I shouldn’t have used the question mark.

When asset prices are the cause of inflation, you can’t get inflation under control without tearing up asset prices. The top 10% is still spending with abandon because of their stock portfolios and real estate values.

Some are also getting big raises. I now several people who have received 20% to 40% raises this past two years. If you have an Professional Engineering certificate….good for you.

Guess where they work. They are engineering firms that will benefit from the Inflation fighting bill to build all this new solar stuff and other projects that are just getting started from the COVID funds. Many States are just dishing out some of the 350 billion in covid funds.

“But it would tear up asset prices a lot faster”

This would be a good thing.

All of this Why doesn’t the fed do this and why don’t they do that?

Look folks, it’s a very small club, and you ain’t in it – that’s why. These people don’t work for you, they work for the club, and they’re doing a fine job.

They have a lot more in store for you. Think cbdc

Eastern,

To some extent, the Fed allowing its balance sheet to shrink (via its debt instrument holdings maturing) *is* the same as raising rates.

The Fed has spent decades pushing rates *down* by using its invented/unbacked money to buy debt instruments at uneconomic low interest rates.

Once the Fed stops doing that, honest rates (read higher) reintroduce themselves.

After the GFC, if you lived in a true free market, the cost of money should have been huge. As in high interest rates. All the money being vaporized should have led to higher rates. The FED does not like the free market. In fact i’d argue the FED was created to keep consolidation going thru out market dislocations. The devil doesn’t snag your soul by telling you how awful hell is.

USA gov stopped posting info on taxes collected in daily treasury statements since mid. of feb

i wonder why

fed and independence is just a scam!!

THERE CAN NO BE SUCH THING AS independent gov body in democratic country!

independent from whom?

power belongs to people. using elections people delegate power to voted officials.

I did not vote for Bernanke or yellen.

EACH RATE HIKE or=and any major decision by FED SHOULD be put on vote in Congress ,and then signed by voted President!

same as it is done for Debt hike.

alx

Or just give the treasury governance back to the people and apologise for stealing

“EACH RATE HIKE or=and any major decision by FED SHOULD be put on vote in Congress ,and then signed by voted President!”

LOL, there’d never be a rate hike.

Well, in fairness, for the last 25 years rate hikes have been rare anyway…but I take your point.

Turkey has just entered the chat.

“power belongs to people”

LOL – Time to swallow the red pill. You’ve been lied to.

Massive changes of consciousness disrupt power systems, tearing down walls one brick at a time.

Walk the talk. Get restless and rowdy and don’t care. True Americans will always fight to make our country better.

There is only hope and then you die, keep rolling and raging against the system

Above all don’t let their war mongering greedy dogma eat your karma

Have fun and enjoy the week-end Wolfsters

Independend from the policy maker, independent from the legislative arm.

And independend from party politics.

Otherwise you get Erdonomics. Do you want a turkish central bank?

You forgot “INDEPENDENT FROM WE THE PEOPLE”

“Independent” is a euphemism for “reckless, irresponsible and unaccountable”

Do I want a Turkish central bank? NO. I don’t want ANY central bank.

The old excuse used to be that “if we don’t have central banks, really awful things will happen in the economy”. Awful COMPARED TO WHAT? The Great Depression? The stagflation in the 70s? The banking crisis? This latest shitstorm we’re going through?

We’ve tried this central bank garbage. Its been a disaster, and it needs to be dumped onto the landfill of bad ideas

Other bad ideas include ponzi pensions with pension funds pointing at central bank, I mean government bonds. Need another seven viruses to balance the books boyz.

Wolf, what does the Fed do with the profits until all the cumulative losses are accounted for (“Those profits will be taken against the cumulative losses in this account. “)? Does it simply destroy the profits just as easily as it created new money while it was operating at a loss?

Yes, the profits will simply destroy the cumulative losses, and thereby destroy themselves, they neutralize each other and dissolve into nothingness, until the balance of that account is zero (the nothingness-part). Then the profits become actual cash that will be sent to the US Treasury Dept.

The more I think about it, the more I wish I could create my own money. That would be just a hoot, and then I’d have to study up on central bank accounting to figure out what to do with it, LOL

Buy the all new WolfCoin!

Better than Bitcoin, better than ShibaInu.

Forget about those other trashy coins! The all new WolfCoin can be used all over! Such as Wolfstreet.com and… *Cough* Ugh, well anyways.

10.0% guaranteed to not be a Ponzi scheme!

Comes with a NFT of Wolf in a speedo!

You can just hire some old FTX accountants to help you Wolf. Look forward to the Lambo pics

WOW wd,,, just wonderful ”graphics of the mind.”

Thanks for the visionary view of our wonderful Wolf.

Gonna absolutely have to get out to THE bay to watch Wolf swim — one of these days–

Otherwise, WE, in this case the Wolf ”fanboys and girls” MUST elect some one or many to video him swimming in The bay…

Probably will become a world wide watching wonder,,, eh

Hey, I just finished my bicycle ride, and rode around Lake Nokomis towards the end.

“Take The Plunge” was going on at the noon hour. A large section of the ice pack on top of the lake had been cleared away, and dozens of people were jumping into the water.

17 days, one hour and 33 minutes until spring, ya know?

Maybe they will give it back to the owners of those investments account?

Wolf,

Some where I remember something/comment about these profits would be used to not only destroy cumulative losses but collected paper bills (money) also.

Correct my memory please?

In terms of the “paper bills” (currency in circulation?), I’m not sure I follow you. So let me try…

Currency in circulation is demand based (people want it, and banks have to give it to them). Banks have to get it from the Fed by posting collateral (such as Treasury securities). The currency in circulation is a liability on the balance sheet (that’s why they’re called Federal Reserve Notes). The collateral is an asset on the Fed’s balance sheet.

There is currently about $2.3 trillion of currency in circulation. That is part of the $x trillion below which the total assets on the balance sheet can never drop.

It seems like the profits taken against the cumulative losses are a form of QT, since cash collected from interest coupons that would otherwise go to the Treasury is instead destroyed.

So when will get to the “Fed Balance Sheet Drops by a Trillion” headline? Sometime this summer I assume…

1T – 626B = 374B

374B / 94B per month = 3.97 months.

If roll off stay ~90-100B per month, should take another 4 months. Early July numbers?

My question as we see the QT chart develop is if the QT downward trajectory is the inverse of the QE upward trajectory?

A significant issue is the unrecognized losses on MBS by FNMA and Freddie MAC. I don’t think these two entities should be buying or guaranteeing 30 year fixed rate debt on housing. Maybe 10 or 15 year fixed rate, but not 30 year fixed rate MBS. The era of cheap rates has been a winner for a number of households, but now, the pain of higher rates (terminal rate) is becoming more real (the ten year bond is still barely 4%). I don’t know much about what will happen in the future, never being there yet, but I expect the terminal rate to go to 5% by sometime in late 2023 or 2024. There has been too much easy money from the Fed that is slowly being drained away.

The government shouldn’t be guaranteeing any mortgages. Period. Most countries don’t, and they’re better for it.

If the mortgages fail, usually the banks are protected.

Thus in a way mortgages will be always protected by the taxpayers who will provide the funds to bail them out eventually as they are too large a segment of the financial health of most people and countries to fail.

Thus the government to protect the country always protects mortgages in some form.

The law and regulations should rather be made in such a way that failure of one or many banks or other financial companies did not matter to the economy.

Money would then maybe be just for transfer of payment and short term storage of wealth. As long as money serves that purpose they serve a purpose.

Danno wrote:

”Thus the government to protect the country always protects mortgages in some form.”

NOT TRUE far damn shore!!!

GUV MINT, in this case the FRB GUV MINT, although supposedly quasi GUV MINT and in this situation actually protects only the BANKSTERS.

Time and enough for the FRB to become either ”Totally GUV MINT,,, OR Totally Private” and stop the BS that has prevailed since 1913…

And, far damn shore, that BS has robbed folks who actually either ”MAKE” something or ” DO” some needed or wanted service since 1913, to the benefit of the banksters.

Those not clear on this really need to study up on the whole shebang since 1913….

Even the ”official” BLS Inflation Calculator shows this very very clearly.

While also very very clearly under estimating degradation of USD,,, as do almost all GUV MINT ”statistics.” FOR EVA!!!

Glad, very Glad to see some of the younger folks finally realizing how the FRB has continued to screw them along with all willing able and ready to actually DO WORK.

BTW, as almost an aside,, almost:

”TRADES” will adjust quickly these days, as is already happening many places…

True. When the Gov started guaranteeing the big Wall Street Landlord companies like Invitation Homes mortgages, that gave these companies the green light to over pay in good neighborhoods. They don’t really care if the tenants stop paying rent, Invitation Homes does not own the mortgage. They can just do jingle mail on non-profitable properties. The Tax Payer will eat the cost of their mistake. What a great gig.

Wolf….

Could you explain the unrealized losses of the Fed as noted on page 16 of the Fed’s Sept 30 Quarterly Report.

“The following table presents the realized gains (losses) and the change in the cumulative unrealized gains related to SOMA domestic securities holdings during the periods ended September 30, 2022, and September 30, 2021: ”

https://www.federalreserve.gov/publications/files/quarterly-report-20221129.pdf

It looks like 1.253 Trillion in unrealized losses. Right?

And the 4th quarter reports seems hard to find.

LOL. It’s always the same stuff. I don’t know how many gazillion times I have explained this, which turns out to be a complete waste of my time because the same stuff keeps getting posted over and over again.

People who post this stuff don’t understand the fundamentals of bonds. They think that bonds are stocks or whatever. But they’re not.

This “unrealized loss” is the difference between face value, which is what the Fed will get paid when the bonds mature, and current market value which is what the Fed would get paid if it sold all its securities on that one day.

But the Fed will never sell its Treasury securities, but will hold them to maturity, when it will get paid face value, and this whole “unrealized loss” is irrelevant. The Fed will not lose money on these securities unless it sells them, and it won’t sell the Treasuries (though it might sell someday small amounts of MBS).

When I hold bonds, I hold them to maturity, which is when I get paid face value, and I don’t give a f**k about market value on any particular day. If you hold bonds to maturity, you don’t care what the market does. It’s irrelevant.

The closer the bonds get to maturity date, the closer the market value goes to face value, and on maturity date, market value = face value.

Now think this through for a moment. If the Fed marks to market, and books a $1 trillion theoretical loss, it will then book a $1 trillion profit as those bonds get closer to maturity date. In the end there will not be a loss. That’s how that works. That’s why if you don’t intend to sell these bonds, but intend to hold them to maturity, you don’t mark them to market.

A suggestion, Wolf. How about putting this explanation on your website (even if not emailed out to the readership), then instead of typing variants of that a gazillion times you just reply “Here is why:” with a pointer to the explanation? I applaud your incredible patience, but would also like to not see it tested!

LOL. Few people ever click on anything that’s important.

That’s why these comments keep showing up.

Those are not MY numbers…they are the Fed’s.

And I drew no conclusions from them, hence my question to you.

I do understand the Fed will never sell.

I do understand the Fed has special privileges.

And I do understand brokerage statements and currently assessed values based on market pricings….and the unrealized gain (loss) column in those statements.

What they bought has declined in real value and the Fed themselves seems to have put a number on it.

And that was September. What will the 4th quarter report reveal.

It’s totally irrelevant. They will regain 100% of the market value they lost as they get closer to maturity.

No one brought this this up a few years ago when the Fed had huge unrealized gains in this column while yields were dropping.

While we all hate the Fed for various reasons, simply getting rid of it without an alternative is not feasible either. “Let the Market set rates,” you cry! Well, the “Market” does not exist as many imagine. The market is made up of people and very commonly just a handful. If you trust the market to set rates, what about all the scandals in LIBOR, silver, oil, etc. Imagine a powerful sovereign nation participating in the “free market” for rates. Imagine letting Goldman set rates! Of course, you might argue that such a market would average out to the “true” market rate, but I have my doubts.

And, no, I don’t have a better solution so don’t jump all over me for being hypocritical. But I do have 30+ years of market experience.

I don’t have any axe to grind but let’s not pretend this is more complicated than it is. Couldn’t you just set up a machine that buys t-bills each day so as set short-term interest rates at something like CPI+(CPI-2%)/2?

You could change the reaction function so the target inflation rate or stiffness parameters are different. Or you could design a more complex function to ingest a lot of observations every day about current economic activity and set rates based on a forecast that integrates all of them.

I don’t really see the point of thousands of employees making models and reports especially if they are just going to be taken under advisement by a committee that will make decisions based on what they already said they were going to do 6 months ago anyways.

Seems they are basically operating a massive investment fund on behalf of the public, but they took so much risk and telegraphed their trades so far advance that they gave away a trillion dollars—maybe more?—to their counterparties. What is the point of that?

Shhhush you busted them ! : ) their pensions depend on you not noticing. Who was it that said if the people understood the financial system we’d be busted next morning or words to that effect. May be why Wolf was spurred on to reveal wolfstreet.

Phimbleburg,

“Seems they are basically operating a massive investment fund on behalf of the public, but they took so much risk and telegraphed their trades so far advance that they gave away a trillion dollars—maybe more?—to their counterparties. What is the point of that?”

I agree with this barring the idea that it is operated on behalf of the public. That would be confusing the beneficiary with the mark.

If anything there should be constraints put on the Fed, as it is now like a former fed chair said we can print whatever it takes.

I agree but have not heard a coherent, rational plan to do that. Why is a private bank setting federal interest rates? Why not nationalize it like in other countries? Bar anyone who worked at an investment bank ever in their life from working there or at Treasury (except for in a compliance role in which they have to convict a minimum number of senior bankers each year or forfeit all salary and benefits).

Everyone hates the Fed except when they ZIRP. Then the Fed is awesome, wonderful, amazing. A few malcontents and perma-bears whine about Greenspan Puts and so forth but everyone gets rich. When interest rates are put back up, everyone whines all over again except for a few lucky hedgies.

Why not fix interest rates? Capitalism has failed under neoliberal, free market rules so why not set rates at some rational level for three years and see what happens. I think 6% is reasonable.

“Why is a private bank setting federal interest rates?”

Common misconception here. The Fed is a hybrid organization.

The Federal Reserve Board of Governors is a government agency, and all its employees are federal government employees with a government salary and a government pension, including the seven members of the Board, including Powell and Brainard. These seven members of the Board of Governors are appointed by the President and confirmed by the Senate. The Board of Governors has lots of employees, and they’re all employees of the Federal Government. They’re working in the Eccles Federal Reserve Board Building, the main office of the Board of Governors of the Federal Reserve System. This is a federally owned building on 20th St. and Constitution Avenue in Washington, DC.

The 12 regional Federal Reserve Banks are private organizations that are owned by the largest financial institutions in their districts. They include the New York Fed, the San Francisco Fed, the Dallas Fed, etc. All their employees are private-sector employees.

The FOMC – the policy-setting committee – consists of the 7 members of the Board of Governors who are federal employees and have permanent votes on the FOMC. The New York Fed governor also has a permanent vote. The other 11 regional FRBs rotate into and out of 5 voting slots annually.

The FOMC is designed to give the 7 government employees a voting majority over the 6 presidents of the regional FRBs

Wolf

MY 2 Cents:

The 12 regional Federal Reserve Banks are private organizations that are owned by the largest financial institutions in their districts.

The material portions of Section 7 of the Federal Reserve Act read as follows: “After all necessary expenses of a Federal reserve bank have been paid or provided for, the ‘stockholders’ shall be entitled to receive an annual dividend of six per cent on the paid-in capital stock, which dividend shall be cumulative.

I presume the stock holders are 12 Regional banks( in turn owned Commercial banks) that are members of the Federal Reserve System hold stock in their District’s Reserve Bank

Wolf,

Please correct me if I am wrong.

Is that 6% guaranteed? What’s ‘paid-in capital stock’?

Thank you.

Here is how much in dividends all 12 FRBs combined paid their stock holders in 2022: $1.2 billion

https://wolfstreet.com/2023/01/13/despite-losses-since-september-the-fed-still-made-a-profit-for-the-whole-year-2022-remitted-76-billion-to-us-treasury-dept/

If the market set rates, we would never have the negative rate environment we had for the last 15 years. No one will lend money for free with no government bail-out, or FED put to fall back on. That is why mortgage rates jumped so high as soon as the FED stopped buying MBS. Goldman can not set rates any more then McDonald’s can. Its called competition. Most institutions trying to game the market may see short term gain, but will lose everything, like FTX.

Good info Wolf!

With Fed gvt bond sales heading to 8 to 10% of GDP annually( a big monetary no-no and will increase as revenues decrease and entitlements and pork accelerate), while inflation means real returns remain negative, one day there will be a buyers strike as portfolio losses will become unsustainable and the Fed will need to pivot. For now foreign capital is seeking a better return with a currency arbitrage is keeping the bond market from spiraling out of control but that is unsustainable. The Western monetary system is in a mess. Lower $ means more inflation similar to eurozone and Britain!

Also, Fed interest payments on the debt are accelerating to a trillion$$$ plus annual run rate! Easy-$$$ Janet is in panic mode with “Higher For Longer” while revenues are declining and fed deficits are increasing!

Obviously, they are committed to the let inflation run hot and hope for the best, at least, until the mobs with torches and pitchforks start seizing cities!

You mean the Government interest payments but I knew what you meant.

What is crazy is the FED QT decreased over 600 billion but since QT started, the Gov debt has increase 1 trillion.

Money is still being being sent into the economy. The Gov has not tighten. They are trying to fight inflation by printing more debt.

There are two big construction projects in my area that are just get started this year. One is 100 million and other is 50 million. Neither would have the projects were even supposed to happen or were on the drawing board 3 years ago. But the money is from the COVID fund and the Inflation fighting bill so somebody has to spend it.

Misconception – Your personal debt and Gov debt both need to be paid back to clear the debt. The former has jail as the stick. The latter has no stick.

Thanks for this, Wolf

Great comments

Thanks

Bob

The FED changed the reporting of M2 from weekly to monthly. This was done in an effort to shift attention away from money supply growth.

You watch the balance sheet to track outside money. But it’s inside money that is exchanged between nonbank counterparties that affect gDp.

The rate-of-change in currency in circulation is back to 2010 levels. The 6-month roc in our means-of-payment money has turned negative. When the 10-month roc turns negative there will be a recession. But now the FED won’t know about it after a lag.

It will take a recession to get this inflation down, everyone knows this by now, but no one wants a recession. That’s the issue.

Real economic growth trend is 1.7%. That is about the max percentage of jobs Fed can kill with QT and interest rate hikes and still have a soft landing. That is about 2.5 million jobs with close to a million related to real estate. Heard M2 y/y is about negative 2%. Wheels ought to start coming off the bus soon.

State of NC still taking in so much tax revenue they are fighting over what to do with the surplus money. Typical end of cycle behavior. State vas in bad shape after GFC.

Old School, I would like to see how much moola the States have raked in since the Supreme Court in June of 2018 allowed all States to collect Sales Tax on virtually all internet sales. This has got to be a huge number that has kept the Economic Ponzi Scheme (EPS) going much longer than it normally would have.

Have any States cut taxes to spread the wealth to us peons from this Windfall ….. very, very few!! But as the current recession grips tighter and tighter, and I don’t know of a single post-WWII economic expansion that has survived when real estate is semi-collapsing, the sales on the internet will also suffer even with brick-and-mortar retail going the way of the Doo-Doo Bird. Another fly in the QT influence on the U.S. economy in addition to train wreck Federal Fiscal Spending.

Thanks Wolf, Another great article. It’s starting to look like the pandemic-era Fed balance sheet experiment is winding down, but I think that would be a premature conclusion.

Prior to the pandemic, the Fed didn’t run both repo and reverse repo operations at the same time. There was still some understanding that market intervensions should be temporary and limited in scope.

Now, we have permanent repo and reverse repo facilities, which set both a floor and ceiling on overnight rates tied to the Fed policy rate, as you mention. The other part of the picture is that SOFR follows repo rates pretty exactly, and bank lending and interest income is hitched to SOFR.

So, when markets finally tank and the Fed moves to lower interest rates, it will lower SOFR as well via its control of repo and reverse repo pricing.

Rate cuts move much faster than hikes. So banks will see their income drop sharply while they’re dealing with defaults and while their liabilities (wholesale, non-deposit) will be elevated. No bank is entirely deposit funded, and the marginal cost of liabilities–the cost of the last dollar a bank needs to borrow–is what drives failure.

This is a change from the LIBOR regime because the counterparty risk component to LIBOR helped cushion rate declines in the past, and softened the impact on banks.

The experiment is still running. Let’s see how it works out.

“Prior to the pandemic, the Fed didn’t run both repo and reverse repo operations at the same time.”

You should have said: “between the beginning of QE in 2008 and 2021, the Fed didn’t run both repo and reverse repo operations at the same time.”

Because in 2008, when it started QE, the Fed shut down its standing repo facilities (repos and reverse repos). But before then, repos and reverse repos was ALL the Fed did. It didn’t do QE (since 1947), it did repos and reverse repos.

In 2021, the Fed revived its standing repo facility, possibly as a sign that it’s going back to the old ways of just repos, and no QE/QT.

Repos and reverse repos are a very quick way to inject and drain liquidity, and since they mature the next day, or in 7 days, or in 15 days, etc., they come off the balance sheet automatically when the Fed stops participating in the market. No QT needed.

Bracketing short-term interest rates via the repo market is not new — that’s how the Fed used to do it before QE/2008.

I covered this switch back to the standing repo facility back in July 2021 when the fed announced it:

https://wolfstreet.com/2021/07/28/my-thoughts-on-the-feds-back-to-the-future-standing-repo-facilities-announced-today/

Wolf, Read “The Fed’s Evolving Involvement in the Repo Markets” from the FRB Richmond. “The On RRP and the SRF flit the paramters of the Fed’s engagement in the market: The Fed sets the prices and the market participants determine the amounts.”

Bracketing short term markets are not the same as in the past, and the link to bank asset yields via SOFR is more direct.

Obviously bank liabilities are still dynamic. The system is more fragile than in the past.

I saw a comment recently that elections should be held the day after April 15. Might see some different results.

Everyone seems to believe that housing is a great hedge against inflation. I think, in the run of the next 25 years (my personal long run), that it will have a pretty mediocre return. After all, right now, 9,000 boomers and silent generation get there final return on a daily basis. This cohort combined is also the largest property owners in the USA. So, pressure from now on will come from this final exit for the next two decades. I would note the Silent Generation combined with the Boomers still outnumber GenX (peak homebuyers today) 69 million versus 51 million. You have to lump in the Millennials to get an additional 61 million people.

In short, the demographics of homeownership are about to really go down the tubes. But hey in time it will be a great buy.

Meanwhile, everyone is talking about inflation in regular prices, which is much more driven by Trump’s trade war, combined with a huge energy bump in costs from Putin’s war. Now, given the Fed strategy of shrinking the balance sheet and running away from MBS, one should start drawing the conclusion that the masters of the interest rate are merely going to have to shrink the money supply to fit an economy with a lot less international trade, and lot less of a dynamic workforce (uh, that labor participation rate ain’t looking too healthy, is it?).

In short, the Fed is (very slowly) coming to the reality that the amount of money needs to fall to begin to match demand, and that interest rates need to rise to restore a healthy relationship between capital costs and economic choice.

The housing market can indeed be a big part of making inflation rise much slower through cheaper housing costs.

Those large numbers of empty houses combined with this demographic bust are going to be interesting. Add in the huge boom in covid related rural housing, and one begins to see a very long adjustment process. Young people need to live where the jobs are for the most part- because the majority of Americans have jobs that require them to show up every day…work from home doesn’t pull a 12 hour nursing home shift or stock shelves.

Through the eye of needle…

The trend of working from home is likely to continue for a long time. Ultimately, it is about the cost of getting the job done.

And Productivity has dropped to 1974 level. I think much of the drop in Productivity is due to work-at-home. Some corporations are recalling workers to the office because they also see the cause.

WFH – Gates and silicon valley didnt understand that not 100% of workforce have communication skills. They talk but dont communicate. WFH is a bottleneck forcing noisy communicators to rise to the top crud while those that sweat and turn cogs of the wheel go unheard. In physical space we hold our place with our body presence. Without physicality we are a simply a voice a vibration conveying and influencing with tonation pause and emphasis.

Great data but also realize the Federal Government is still pumping billions into the economy. For example, the CHIPS and Science Act of 2022 is almost coming online and will further heat the economy with billions of dollars of spending including some social engineering requirements.

I just read in a local paper some new programs are going to be funded in my state with COVID money. (How much of that is still unspent)

It’s going to be long time before inflation slows because the Federal Reserve and the Federal Government are working against each other.

Yes, the Federal government is trying very hard to pump up inflation and maximize corporate welfare.

And state and local governments too. They’re still swimming in pandemic money in their accounts, despite growing budget deficits, and this money is going to get spent.

Would be interesting to know state by state how much pandemic money they got and how much is left? This would help in timing when the s__t will hit the fan.

The FED Central Bank Balance Sheet is technically insolvent: Marked to Market it is $1.3 Trillion underwater AND its current projected annual operations losses (Powel’s paycheck) is $100 Billion USD.

How, given The FED tools, can this entity right the ship? I propose that the Member Banks be forced to recapitalize The FED by forcing them to return “Ample Reserves” and absorb some these US Taxpayer losses!

Would you lend your earned excess savings to this entity OR purchase precious metals as an insurance policy to protect your future purchasing power?

“The FED Central Bank Balance Sheet is technically insolvent:”

1. Ignorant BS by people who don’t know crap about central banks. Why does this shit keep getting posted here?

Losses don’t matter to a central bank that creates its own money. It can never run out of money, and obviously it can never become insolvent, and it can never run out of capital. The Fed’s capital is set by Congress and is irrelevant.

2. Ignorant BS by people who don’t understand the fundamentals of bonds. They think that bonds are stocks or whatever. But they’re not.

This “unrealized loss” is the difference between face value, which is what the Fed will get paid when the bonds mature, and current market value which is what the Fed would get paid if it sold all its securities on that one day.

But the Fed will never sell its Treasury securities, but will hold them to maturity, when it will get paid face value, and this whole “unrealized loss” is irrelevant. The Fed will not lose money on these securities unless it sells them, and it won’t sell the Treasuries (though it might sell someday small amounts of MBS).

When I hold bonds, I hold them to maturity, which is when I get paid face value, and I don’t give a f**k about market value on any particular day. If you hold bonds to maturity, you don’t care what the market does. It’s irrelevant.

The closer the bonds get to maturity date, the closer the market value goes to face value, and on maturity date, market value = face value.

Now think this through for a moment. If the Fed marks to market, and books a $1 trillion theoretical loss, it will then book a $1 trillion profit as those bonds get closer to maturity date. In the end there will not be a loss. That’s how that works. That’s why if you don’t intend to sell these bonds, but intend to hold them to maturity, you don’t mark them to market.

” If the Fed marks to market, and books a $1 trillion theoretical loss, it will then book a $1 trillion profit as those bonds get closer to maturity date. In the end there will not be a loss. ”

And the Fed is good at calculations such as amortizing as you point out in the “unamortized” premium readings.

I dont think it would be a “profit” but more of a “lesser loss”, unless rates went below the coupon.

A “snap shot” of what things are worth at a particular moment is of value. The Fed went to the trouble to come up with unrealized gain (loss) number, thus I would guess they sensed it was of some import.

I understand your point and always did.

Thanks Wolf for your reply and this excellent article about the real current financial condition of The FED, I appreciate it.

Totally agree that you can hold a 30 year MBS to maturity and voila you have zero capital loss.

My concern is the purchase value of your original loan when you receive your principal over the next 30 years at a ZIRP rate. Possibly you loaned 10 potatoes and you only get 5 back? In my stupid shit Central Bank analysis I think you lost 5 potatoes but yes you have 100% “paper” Fiat currency to light some candles around the house.

Correct me if I am wrong? The FEDS main function is to manage the liability mix between base currency and issued/outstanding Treasury securities? Booking unprecedented $100 Billion USD in operational losses suggests to me that The Clueless (at least pretend to follow a monetary model like the Taylor Rule) FED has completely lost control of the US Fiat Monetary System.

Leverage and managed cash flow does matter even if you can print all the money you need to cover your obligations…there is a point which I believe we have reached where holders of USDs might question its ability to maintain future purchasing power…please pass the potatoes.

The Fed has now reduced its balance sheet about the same number of dollars as it did during QT1 back in 2019. It has not yet reduced by the same percentage as during QT1. The submarine continues to drift silently through the dark depths. The enemy lurks nearby. Popcorn.

At this pace the QT will take 15 years … (smiles nervously), then he adds: “Oh, it will stop after a two years.”

BS. The Fed CANNOT have a balance sheet with $0 in assets. Where does this BS come from? The Fed always had assets, lots of assets, from day one. 15 years ago, before QE, it had $900 billion in assets. Assets grow with the economy (nominal GDP), currency in circulation, and other factors.

I detail these factors here. And I give you some ball-park figures for the lowest possible point in assets that the Fed could go. READ IT:

https://wolfstreet.com/2022/09/05/by-how-much-can-the-fed-cut-its-assets-with-qt-feds-liabilities-set-a-floor/

Thanks Wolf. I should revise my calculations in my previous comment. But we are in order of magnitude country now trying to predict the future and the system is bigger than just virtual reality finance.

But the way – I see there has been massive shrink-flation in mugs.

“At some point, as QT shrinks the reserves and the RRPs, the interest expense begins to decline, and eventually, the Fed is going to make profits again. ”

Hmmm. Roughly and OOM speaking: At $628B per year for $8.4T the shrinking will last 13 years. At $38B loss per 1/2 year that will be a total of $988B in losses that need to recouped through application of diligent effort and packing your own lunch. Something I don’t think the Fed knows how to do.

Rough figures but they are going to need a lot more help from inflation. Maybe reset the goal to 25%/year when they revert back to QE?

Wolf, I love your optimism and how you balance everybody else I follow, but this is kind of like jumping off the Empire State building and shouting “Just past the 75th floor and it’s going great.”

1. It’s not $628 billion a year but in 7 months, including the ramp-up phase. The current rate is about $1 trillion a year.

2. You’re assuming that the Fed needs to go a balance sheet with $0 in assets.

But the Fed CANNOT have a balance sheet with $0 in assets. The Fed always had assets, lots of assets, from day one. 15 years ago, before QE, it had $900 billion in assets. Assets grow with the economy (nominal GDP), currency in circulation, and other factors.

I detail these factors here. And I give you some ball-park figures for the lowest possible point in assets that the Fed could go:

https://wolfstreet.com/2022/09/05/by-how-much-can-the-fed-cut-its-assets-with-qt-feds-liabilities-set-a-floor/

Wolff, I never wrote that “The Fed CANNOT have a balance sheet with $0 in assets.” I said the QT will be stopped faster than it should.

That’s all.

What did you mean by this?

“Hmmm. Roughly and OOM speaking: At $628B per year for $8.4T the shrinking will last 13 years.”

I guess joe2 said it, I didn’t realize it was a different commenter reading it in order.

Asul,

You said, “At this pace the QT will take 15 years”

At the current pace, for 15 years, that will bring the balance sheet to $0, well actually below $0.

And I told you that the Fed CANNOT have a balance sheet of $0. Much less below $0.

That graph…The Fed’s Total Assets is just, wow. It tells such a story.

I suppose congratulations are in order for those few who figured out how to subsidize trillions of dollars of wealth for a certain group of people without it ever getting on the nightly news.

Bostic came out and ran his lips yesterday about a FED pause this summer, and the market has taken off like wildfire, the DOW moving straight up over 700 points. They don’t want stocks to fall. They want to keep all of those asset price gains.

That’s the truth. This bunch worked so hard to increase inflation over the years, I am convinced, they will let it burn for some time.

Depth Charge,

LOL. Do the math: if we get 3 more rate hikes (that’s one more rate hike than they said in December) at the next meetings in March, May, and June, to bring the top of range to 5.5%, that means a pause after June, in the summer, no?

In reality, the reason the market jumped is because I farted.

Did you say “excuse me,” Wolf? Anyway, Caustic, I mean Bostic was out there flapping his lips why? How about just shut up and say nothing? It’s because he wants to cheerlead and give the markets hope. Some algo probably latched onto the hot air spewing forth and hit BUY, then all the other algos jumped in. Fundamentals, you know…..

Depth Charge

Mkt indexes zoom and are highly VOLATILE because of Algo DAY trading, especially now – ODTE (Zero date to Expiry) like ‘Hail Mary pass’ (Foot Ball)

B/c this and unpredictable ‘front running. almost everyday, I QUIT buying puts. It is a truly a CASINO.

Sunny…who writes the algorithms and code? Who decides “requirements” for the applications?

At our ages, Wolf, you should know to stay away from spicy foods!!

All these FED officials have enriched themselves and their friends from rising asset class of all types.

All the FED officials are front running the markets as well.

Why would they want the market to fall if they happen to lose money with falling or rising market.

We all need to understand the big picture.

And I bet in every FOMC meeting they dedicate at least 10/15 minutes to laugh out loud about the stupidity of American society; the sheeple, the media, the politicians, the so-called market…all is a good joke.

I think they convince themselves that they are doing God’s work and doing their best to save the peasants. I remember the entitled wife of Treasury Secretary Mnuchin snapping back at critics about their sacrifice to the country in a now-deleted Instagram post while flying everywhere with her husband on military and government planes at taxpayer expense. Most of them seriously believe that they are “serving the people” and are God’s gift to humanity.

“…wife of Treasury Secretary Mnuchin snapping back at critics about their sacrifice to the country in a now-deleted Instagram post…”

We’ve had so many “let them eat cake” moments it’s hard to keep up anymore.

It’s time to take away Bostic’s mic, then his job, then his wealth, then his freedom. That’s the way forward in order for this country to heal. We need to remove these people from power, strip them of all of their money, and put them in prison. What they are doing to society is the very definition of crimes against humanity. The tent cities don’t lie.

I totally agree with you.

Democracy in its present form is a charade which gives people false sense that they hold the power.

Two parties take turn to rape and pillage the wealth of this country and they want us to be divided in the name of race, culture etc etc.

Depth Charge,

LOL. Do the math: if we get 3 more rate hikes (that’s one more rate hike than they said in December) at the next meetings in March, May, and June, to bring the top of range to 5.5%, that means a pause after June, in the summer, no?

In reality, the reason the market jumped is because I farted.

“… and every wind that blew over France shook the rags of the scarecrows in vain, for the birds, fine of song and feather, took no warning.”

Agree 100% … the FED understands zippo about consistent messaging…every t8ime it looks like the market is finally starting to get it…some FED official runs their mouth…I mean…WTF is anyone to think except they aren’t serious???

3 month moving average of a legitimate inflation metric = Fed Funds

No questions asked. No deviations. No subjective thinking by PHDs behind closed doors.

Fed stays out of the long end except to maintain “moderate” long term rates per their directive. Moderate = not extreme.

Money supply ? N o digital minting in excess of any upticks in GDP.

If they thought elevated inflation was unacceptable, they would be talking about supporting a period of deflation to reverse the cumulative 25% inflation we’ll see in years 2021 through 2024.

But there is absolutely zero indication from the Fed that they plan to reverse any of the inflation. This reveals their true motivation. They seem to have an unwritten policy to allow excessive inflation but prevent any deflation. In my opinion, you have to plan as though future inflation will be somewhere between 4% and 8% going forward, and maybe higher.

Bastille Day is the only way.

They won’t.

Modern day economists are more scared of deflation than anything else.

There’s a reason markets skyrocketed after the new “average inflation targeting” policy was announced in 2020. The 2% PCE target effectively became a floor, not a ceiling.

The previously lost purchasing power will be lost forever. When inflation does return to 2% it’ll be on top of the ~20% cumulative inflation from the last 3 years.

I think this was a media head fake again. Go find and read his complete quote and you will find that the media pulled its usually BS. More and more I am forced to find and read first hand sources with complete quotes to find the news which is just soul crushing.

Venkarel

That news is NOT’ fake’ for those who perceive as ‘real’ and the Volatile, Mkt moves ( UP or DOWN)

Investors poured 1.5 Billion EACH day in January to buy stocks (Bloomberg)

Power PERCEPTION at times, could be very strong (at least transiently) than the reality based facts/fundamentals.

It appears RRPs are still sitting at $2.5 trillion. Not going down, is it?

Basel III regulations make large deposits very unattractive for banks. But they have to go somewhere for cash. How convenient to have the money printer in chief on your payroll.

What is it with the community and (a) qualitative, (b) EVs, and (c) renewables?

I mean QT is happening, EVs are worth purchasing – and don’t bring up subsidies since china at least figured out to make them at parity, and renewables are taking share.

It cannot just be partisan warfare. I mean T loved QE and low rates, and Texas makes tons of wind energy and EVs (because they are closet California-philes)

So, someone, explain to me why these topics bring out the true believers. I mostly am here to go “ooooo” as to inflation and see if housing gonna crash again.

Federal Reserve and Its Secrets (Mullins) is an interesting read vis Fed Reserve history.

Illuminating write-up, Wolf, thank you.

The Fed must feel under some pressure from the US Treasury against raising the federal funds rate too fast and too highly, as a matter of liquidity. Not only does this make borrowing more expensive for the US Treasury, which issues a lot of shorter term bonds pinned to this rate, it also prolongs the period without remittances from the Fed, as the Fed pushes up yields and accumulates these paper losses.

Plus, US inflation of ~8% last year on a debt of $31 trillion has wiped off some $2.4 trillion of debt in 2022 terms, even as social security expenses are rising with colas. Quite welcome to the US Treasury, as tax revenues rise with inflation. With inflation high elsewhere too and limited substitutability, the US Treasury might wish the Fed to take it slowly bringing down inflation, to chip away at real debt, yet further pressure on the Fed.

The Fed’s official independence is being tested in many ways, interesting times.