Market is still frozen, potential sellers sit on vacant properties, hoping this too shall pass. Cash Buyers, investors, second-home buyers pull back further.

By Wolf Richter for WOLF STREET.

Spring selling season begins with 7% mortgage rates? In terms of closed sales, December and January usually mark the low-point of the year for the housing market, reflecting deals made over the holiday period in November and December. But the spring selling season starts now.

In January, mortgage rates had dropped on hopes of a quick Fed pivot and steep rate cuts asap, yes please, with mortgage rates diving back to 3%, or whatever, but that dream is now fizzling.

The average 30-year fixed mortgage rate today rose to 6.87%, according to Mortgage News Daily. The 10-year Treasury yield is moving in on the 4% mark – currently at 3.96%. And these rates are going to dog the spring selling season.

“And this too shall pass” has been the guiding principle for potential sellers, as they’re waiting for the Fed to slash its interest rates so that mortgage rates could plunge back to 3% so that they could sell their properties for March 2022 prices. So potential sellers are not putting their vacant properties on the market unless they have to, and buyers are not buying at March 2022 prices. And the market remains essentially frozen.

For deals to be made, potential sellers need to get realistic about the price at current mortgage rates. Those that listed their properties and made a deal months ago at whatever unpalatable price, they’re now way ahead of the game.

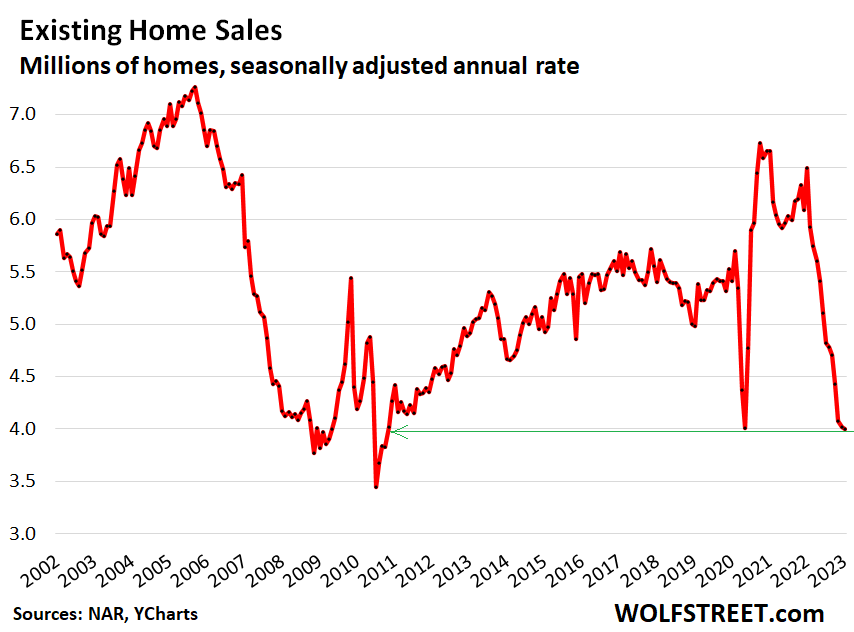

Sales of previously owned houses, condos, and co-ops fell by another 0.7% in January from December, to a seasonally adjusted annual rate of sales of 4.0 million homes, according to the National Association of Realtors today. This was the 12th month in a row of month-to-month declines on this seasonally adjusted basis. Sales dropped by 37% year-over-year, below the lockdown low of May 2020, to the lowest since 2010 during Housing Bust 1.

Actual sales in January – not seasonally adjusted, and not as annual rate – fell to 231,000 properties, down 34% from a year ago (historic data via YCharts):

Sales of single-family houses fell by 0.8% in January from December, and by 36% year-over-year, to a seasonally adjusted annual rate of 3.59 million houses.

Sales of condos and co-ops were roughly unchanged from December, but plunged by 43% from January a year ago, to a seasonally adjusted annual rate of 410,000 units.

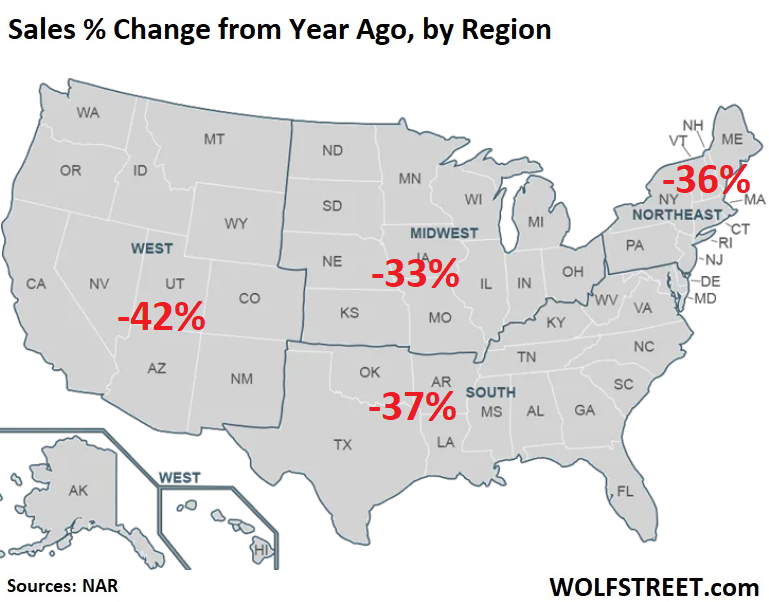

Sales plunged in all regions. Year-over-year percent change (NAR map of regions):

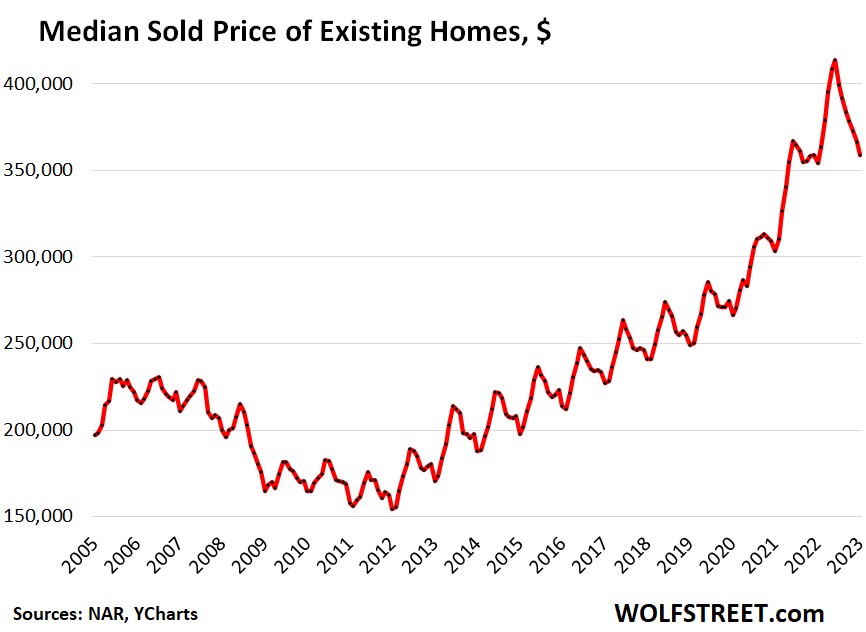

The median price of all types of homes fell for the seventh month in a row, to $359,900, down 13.2% from the peak in June. This drop further reduced the year-over-year gain to just 1.3%.

What portion of this June-December price drop is seasonal? The average June-January decline over the eight years before the pandemic was 8.0%. Including the pandemic, the average June-January drop over the past 10 years was 6.5%. This shows that seasonal declines made up only a portion of the 13.2% drop since June (historic data via YCharts).

Some markets in the US are holding up better, but others are leading the downturn, including the San Francisco Bay Area, where the median price plunged by 35% from the crazy peak in March 2022 and by 17% year-over-year, according to data from the California Association of Realtors.

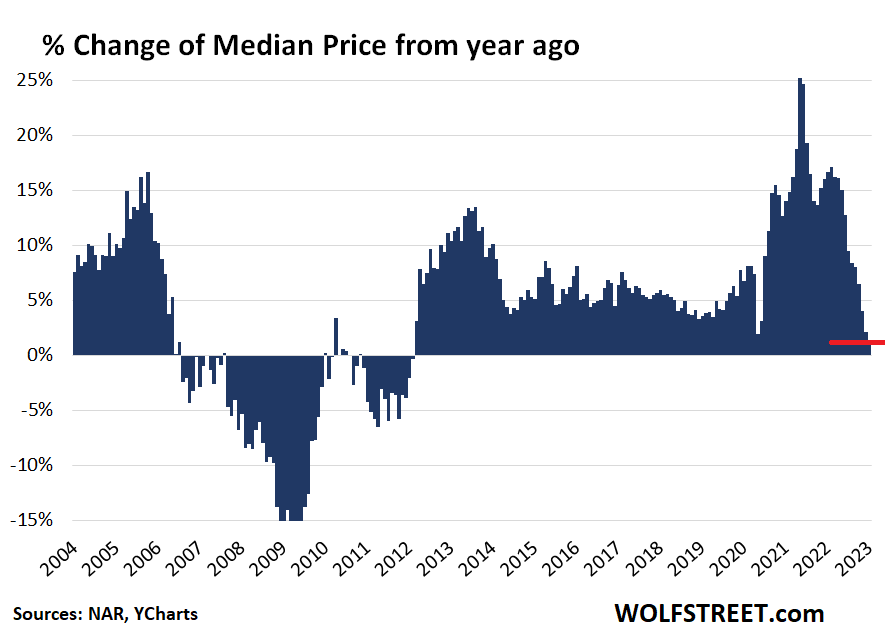

The rapidly disappearing year-over-year price gain in the national data, down to just 1.3% in January, provides additional confirmation that much of this decline was not seasonal. For 23 months, from August 2020 through June 2022, the year-over-year gains were over 10%, and for several months during that time were over 20% (historic data via YCharts):

All-cash buyers, investors, and second home buyers pulled back further. All-cash sales plunged by 29% year-over-year, to 67,000 properties, down from 95,000 in January 2022. Sales to individual investors or second home buyers collapsed by 52% to 37,000 properties, from 77,400 in January 2022.

Inventory is low, buyers are scarce, market is frozen.

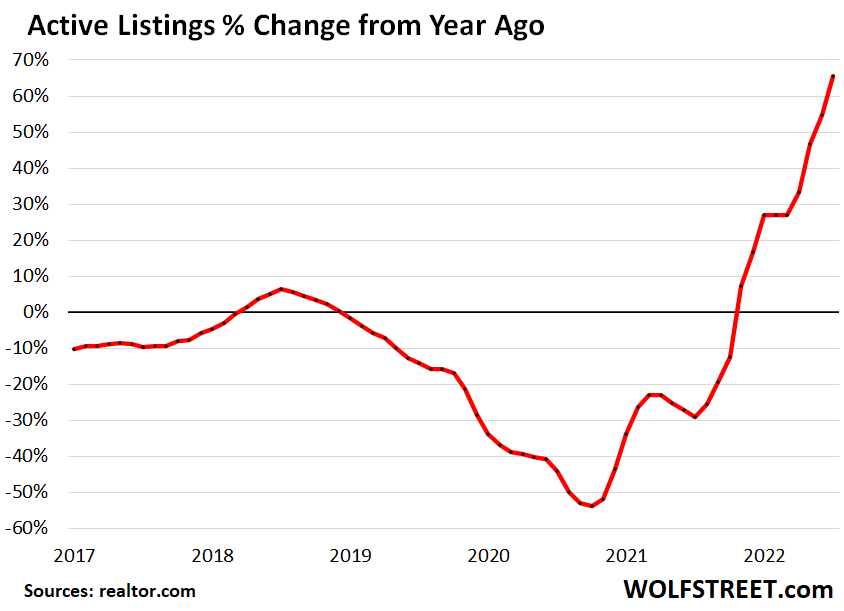

Active listings (= total listed inventory minus properties with pending sales) jumped by 65% from a year ago, to 626,000 properties in January. But they remained low by historical standards as potential sellers are still convinced that this too shall pass, and they’re not putting their vacant properties on the market (data via realtor.com):

How many vacant properties are being held off the market? The actual vacancy rate for the entire housing stock was 10.4% in Q4, or 14.55 million housing units, of which nearly 11 million housing units were vacant year-round, according to Census data. Of them, 6.7 million vacant housing units were being held off the market for a variety of reasons. If just 10% of these vacant properties being held off the market suddenly show up on the market, active listings (currently 626,000) would more than double.

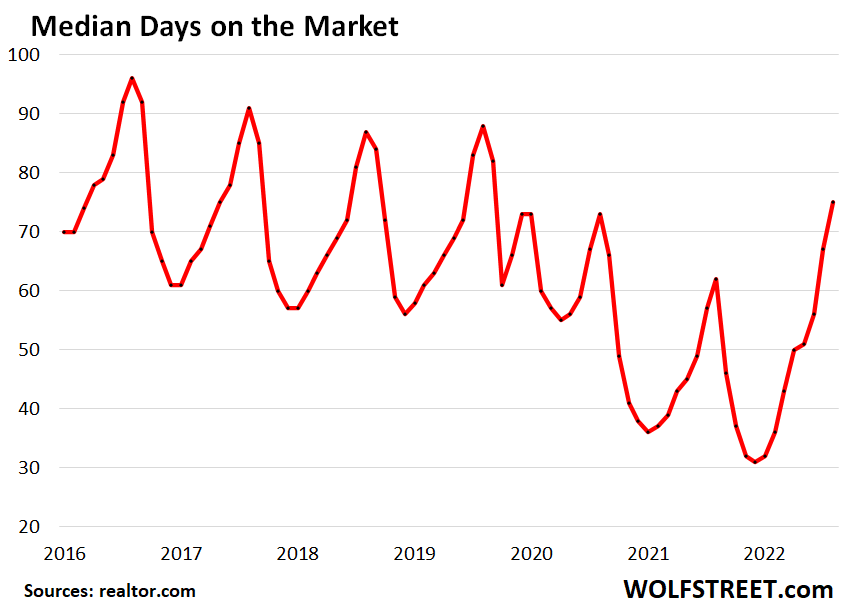

Median days on the market, before the frustrated seller pulls the property off the market, or before the property is sold, jumped to 75 days, the highest since February 2020 (data via realtor.com):

Price reductions: The number of listings with price reductions jumped by 170% year-over-year, to 190,000 listings, the most for any January since January 2020, according to data from realtor.com.

Priced right, just about any property will sell. Not enough sellers are wanting to price their properties right yet, but more are trying: Of all active listings, 30% had price reductions in January, by far the largest portion for any January in the data going back to 2016. This shows that the seller’s willingness to explore the market clearing price has increased, which is a good sign in terms of unfreezing the market.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

6.87% on the 30-year and a 36% YOY drop in sales is a big WOW, and yet the median sales price of a home is still in the stratosphere. In other words, expect fed funds rate to climb to 7-8% this year to bring down these insanely high home prices. The idea of a 2023 fed pivot is ridiculous. It will be mid 2024 at this pace. Short the homebuilders, KBH, TMHC, LEN, DHI, MTH, and the ITB still way to high.

Yep, home Depot was another tell today. I said in a previous thread that rising rates are going to kill the spring selling season in the crib. I was a big bear last year but the pace of this is moving even faster than I predicted – didn’t think we’d see year over year declines until late spring or early summer. It’s going to be a bloodbath with the savings rate so low and credit use skyrocketing. Tbills looking pretty sweet right now along with some shorts of the unicorn stocks.

Home Depot showed that the home remodeling boom finally leveled off.

Walmart sales in the US jumped by 8.0%, also released today. This shows that consumers are buying lots of stuff.

Wolf,

Do you think that because it’s Walmart that portends that people are getting spooked about prices / economy and going there for the savings… or is it just because it’s a ginormous retailer?

People are just spending. They’ve gotten used to inflation, they’re making more money, they have jobs, they’re going on with their lives, and they’re blowing money in all directions.

Powell has a huge problem on his hands.

Peter Schiff mentioned this: One way to reduce inflation is to reduce consumption. When the demand drops to a certain point, price of goods and services go down. What you said above tells me the consumption is still too strong, i.e. demand is too high.

With a strong demand (on services and goods), I don’t see how the Fed can slow down rate hike. Indeed, I think the 5% terminal rate is unrealistic.

Powell has a dilemma: endure a long-lasting inflation, or trigger a recession.

The Fed can increase QT by selling MBS.

I’m in escrow and ready to buy another home

it’ll be rental with better than 10% ROI

If prices increase by 10% and sales volume decreases by 2%, you get an 8% increase in nominal sales amount. It does NOT mean “people are buying more stuff.” This condition was highlighted by Eric Cinnamon of Palm valley Capital. He listens to tons of small cap earnings calls and many companies were reporting that sales increased but sales volumes declined. Not saying it is true for WMT specifically…

Price increases have moved to services, and away from goods. Retailers sell goods, not services. Many goods that they sell have had big price drops, including electronics big time (Walmart complained about that). So you have to sell more goods to just keep the dollar sales even. And if you book an 8% sales increase in goods, despite a bunch of prices having dropped, that’s a sign of strong demand.

People need to read my articles about CPI; and about retail sales. I sort this out for you.

Does anyone have Walmart’s revenue increase data by segment? In otherwords, how much of their revenue increases are due to grocery items vs other types of merchandise. I am only one old guy but I’ve switched from Kroger to Walmart, even though its another 5 miles away, for these reasons.

Kroger is often out of stock, whereas Walmart appears better stocked.

Kroger prices are 10% or more higher than Walmart.

Kroger loses brand names on many items substituting house brands.

I may be partially responsible for a speck of that 8% revenue increase at Walmart.

I live next to a Walmart, so I do most of my shopping there. I pretty much buy the same stuff all the time, but my spending has definitely gone up more then 8%. I’m not at the point where I need to start substituting yet. I still get Prime Rib-Eyes, brown eggs and gourmet Salami.

“People are just spending. They’ve gotten used to inflation, they’re making more money, they have jobs, they’re going on with their lives, and they’re blowing money in all directions.

Powell has a huge problem on his hands.”

Spot on!!! The majority of people will spend until they literally CAN’T spend.

Wolf

You say that while it has increased significantly, that the number of Active listings is still low relatively speaking. Do you have the numbers for Active listings over the last 10 years?

I use the realtor.com data, which only goes back to June 2016. In Jan 2017, active listings were 1.15 million, the highest January in the data set. In January 2019, active listings were 1.11 million.

Get back with us when the median YoY price goes negative. Trading Economics shows that last month’s YoY median prices were still 8% above the previous 12 months.

Extremely glad to see the 30YFRM approaching 7%. Would love to see it stay that way for the entirety of ’23 and into ’24.

Come hell or high water that YoY median price needs to decline at least 25% across the US. 30% would be better. And a good old fashion 6-7% unemployment induced recession would be nice to boot.

YOY price is up just 1.3%, according to NAR, cited here. See 4th chart. It’s 1 or 2 months from turning negative YOY. And I will make sure to notify you when this happens.

Not really related but are I Bonds still a good buy? I did 5k when they were around 9%. Wolf, do you think the rate will go up or down. Need to put another 5k in.

Check short term Treasuries. I’ve been buying zero Bills with 30-45 day maturity. Good $$…. Just keep rolling them as long as rates are going up, and it compounds the return…

I-bonds are variable rate bonds. The bond you bought paid 9% for six months; then the rate adjusted to the current rate for six months. And then it will adjust again…. until the bond matures in 30 years.

There were times when our I bonds earned less than 2%, and last year, the same I bonds earned over 9%. That’s how they work.

Interest is paid on the purchase amount plus on the accumulated interest. So if bought a $5,000 I-bond, and it earned 9% annual rate for six months, at the end of the six months, it has a value of $5,250. If the interest for the next six months is 6% annual rate, it pays that 6% annual rate on $5,250, and you’ll have $5,407 at the end of that period (interest of 6% annual rate on $5,250 = $315, divided by 2 because it’s for six months = $157) etc. So over the years, the value of the I bond rises, and reach six month the interest rate is figured on the new value.

You get the interest when you redeem the bond (read about the rules) or when it matures in 30 years. This event triggers a 1099 for the accumulated interest, and you have to pay taxes on the accumulated interest at that time.

We don’t buy I bonds to speculate. They’re variable-rate, tax-deferred retirement products, one of the bottom layers of our nest egg. We buy them every year in all our accounts and forget about them. We intend to keep them until they mature in 30 years. If one of us dies before they mature, the other gets them (and no, you cannot take them with you).

Thanks, I didn’t read too much into them when I bought them. Didn’t know they worked like that. Just seemed like a good place to park extra savings account money for a year so I put in some to get some kind of interest instead of the .00001% a bank would pay on a saving account.

Some additional comments: Series I bonds come with a fixed rate (currently 0.4%) that is applied on top of inflation, so it’s kind of the bond’s ‘real yield’. You can currently buy a 10y or 30y TIPS at 1.5% real yield. But Series I has two main advantages which can be worth the lower yield:

* Redemption optionality: After 5 years you can cash it at face value with all interest earned, or after 1 year with only 3 month interest lost. So if rates rise you can cash out and reinvest into something else. While with TIPS you have to sell at market, so with increasing rates that would mean at a loss.

* Tax deferrance: Unlike TIPS, taxes on interest are only due at time of redemption. Which may be good or bad depending on your tax situation and expectation of changes in the future.

Also note that the next reset of the fixed rate is going to be in May. It’s likely going to be set higher than the current 0.4% so it may be worth to wait till then.

There are plenty of savings accounts with no restrictions paying 4% or more.

The Existing Home Sales chart is just STUNNING! Looks like it is in the tail end of the 3rd wave of the Elliot 5 wave pattern. If it follows the pattern we will see a jump up at some point then down again with the final 5th wave ending at a level below the lows of 2009/2011. The the small counter wave #4 will most likely come from a drop in the 30 yr rate to something around 5.75% Also if we don’t see closed sales pricing flatten out or advance some this buying season it will be a bloody fall and winter.

Amazing the patterns you can see in random data.

It looks like the existing home sales are actually down to the bottom of the 2008 housing collapse, yet prices have hardly moved down. This is truly going to be a very long downward trend in home prices.

Sellers need to see prices continue to decline before they decide to cut prices. Too much hope still in the markets.

Could it be that prices haven’t moved much because there’s simply not enough inventory yet?

Hi Lucca,

Please see my comment much farther below. As with prices significant differences in inventory changes (YoY) regionally snd per city. No surprise to some I imagine.

Sellers are under no pressure to sell. A good old fashioned recession might change that.

Correct. However, it will need to be a genuine “all economic cylinders misfiring” recession.

Demand will not fall to recessionary levels until 1) the stock market decreases substantially (thereby lessening the still in place “wealth effect”) and 2) large scale layoffs take place. Not the onesy, twosy tech layoffs that have happened up to now. Headline-dominating layoffs.

Until that happens, real estate sellers will continue to fantasize that an early 2022 price is just around the corner. They just need to be patient.

Prices are about to be sharply lower year over year in many markets (already are in some, as Wolf has detailed). This should happen by April. Once the mainstream media latches on to this, the crash will become big news.

‘This too shall pass’ was the guiding principle for potential sellers.”

their problem is that they expect the boom in prices to last forever and the declines to be minimal and for short periods of time. Blessed are the believers. Amen!

Landing?

YOU’LL GET NOTHING AND LIKE IT.

– Judge Powell.

You will own nothing and like it! :-)

-NWO

I owe nothing and like it.

Here,here

Mo money, mo problems, that’s why we’re all spending it away.

Amen. However, expect the puppets of the banksters who head the “Fed” bankster cartel to get $200,000 to $400,000 per speech after they retire, for dozens to hundreds of speeches depending on the level of their avarice. No doubt the banksters are rewarding them for their service to the American people and not the banksters’ personal interests.

If you actually believe that, I have a bridge in Brooklyn to sell you. It is located in a very often-used area.

They move to the Brookings Institute like the armsellers go to the Carlyle Group. Ala Colin Powell, just like Bernanke at Brookings.

Housing Affordability is an 8th grade math problem (maybe some folks were absent that year?)

If you had $50,000 per year to spend on mortgage interest (ignoring taxes, insurance, amortization, maintenance, etc. to highlight the point), then when 30 yr mortgage rates were down near 2.5%, you could float a $2,000,000 mortgage.

With 30yr mortgage rates at 7%, the same $50,000 p/yr for interest floats a $714,285 mortgage.

When 30yr mortgage rates stabilize around 7.5% after the latest Fed increases, your $50,000 p/yr will get you a mortgage of $666,666 (ominous, no?)

It doesn’t take a genius to see why demand has evaporated and will not return.

Precisely.

But 20 years of the Fed gutting honest interest rates led millions (though fewer than Bubble 1.0) to live in a fantasy reality where a hugely indebted nation (over 100% debt to GDP for the G *alone*) somehow could have 2%-3% interest rates (without the Fed committing global forgery to achieve it).

Remember Math is hard and Greed is easy…that’s my tagine and I am sticking to it..

You haven’t considered the effect of wage inflation though. If your salary is going up by 4.5% then your effective interest rate is still 2.5%.

The effect of high inflation/high nominal interest rates, is that it front loads mortgage payments. It’s like having a shorter term on your mortgage. But borrowers can compensate for this by using a longer term.

The real issue right now is not real interest rates – which are still very low – but uncertainty around where real rates will go.

“If your salary is going up by 4.5% then your effective interest rate is still 2.5%.”

Only if you accept the Chinese Powell CPI as reality. The Volcker CPI says we’re above 15% inflation, possibly the worst in US history.

And counting.

There is no “Volcker CPI.” That’s figment of someone’s imagination. But there’s a joker out there that sells a newsletter based on that imagination.

“You haven’t considered the effect of wage inflation though. If your salary is going up by 4.5% then your effective interest rate is still 2.5%.”

Wouldn’t this be true only if your salary & loan balance were equivalent? If you make $100k and your loan balance is $1m I don’t quite see how your $4k in additional salary is going to cover the additional mortgage interest you’ll need to fork out.

The only thing anyone has to now about mortgage rates and the link to MBS, is that we’re dealing with nonlinear chaos, which is compounded by inflation.

All the banks that blew up in the GFCI were playing with jet fuel and bonfires, but the Fed ChatGpT super computer has this under control, relax, everything is fine

FYI:

Convexity 2014

Conversely, rising yields cause prepayments to slow and bond durations to extend, resulting in a greater drop in price than experienced by more traditional (i.e., option-free) fixed income products. As a result, the price performance of mortgages and MBS tends to lag that of comparable fixed maturity instruments (such as Treasury notes) when the prevailing level of yields increases. This phenomenon is generically described as “negative convexity.” The effect of changing prepayment speeds on mortgage durations, based on movements in interest rates, is precisely the opposite of what a bondholder would desire. (Fixed income portfolio managers, for example, extend durations as rates decline, and shorten them when rates rise.) The price performance of mortgages and MBS is, therefore, decidedly nonlinear in nature, and the product will underperform assets that do not exhibit negatively convex behavior as rates decline.”

Just screams buy treasuries to me, or wait until rates get even higher and then REALLY buy some long treasuries. Only risk is that the Fed doesn’t really care about inflation. And Powell might not, his new favorite “super core” strips out an awfully arbitrary amount of items.

People have let themselves get inflated into some pretty dire living conditions before, and I wouldn’t be surprised if it happens again. Hard to fathom how much productivity was really lost during the pandemic, and then with all the money printing on top of it, and the tightest labor market ever on top of that? Just screams higher inflation for longer to me. The mentality is buy now before it gets more expensive. How in the heck are we going to undo that mess?

Agree with you as usual after many moons TS:

Finally accepting WE, in this case the family WE need to go ahead and open that direct buying of USA bills, notes, and bonds.

As Wolf has said or added to comments, gov. treasury (OK, whatever) provides a clear methodology for buying various products ”directly” , and the website has good ”tutorials” for folks such as us to learn the ways to invest directly…

Thanks again to Wolf and commentariat for help in ”figuring out” how to invest with least ”load.”

It’s like the opening scene of Gladiator.

Sellers from Germania on one side – hoping this skirmish passes.

Buyers from Rome on the other – smelling blood.

Hell to be unleashed at any moment.

It will take some more grinding prices lower and inventories rising before any real price decreases start to hit the market. With so many home owners sitting on a pile of equity, there is zero reason for them to panic sell. But after a year of falling prices, the owners will start to see their equity evaporate and then declines will get much larger. So just hang out on the sidelines and wait for blood in the streets.

Probably going to be a 3-4 year collapse in home prices. This isnt just the US, this is a global phenomenon.

…and the seller’s blades are sticky in the sheath.

I was going to look at a place this weekend. I thought it was high priced given location, but nonetheless figured if it was meant to be then cool. It had been on the market a day when I made the appointment for Sunday afternoon.

Listing agent emails Saturday afternoon and stated there were two offers already on the table from Saturday. I said thanks, I’m out.

Of course this is anecdotal, but like the article stated, if it’s priced right it will sell… quickly. The days of bidding war crap are over.

Getting 2 offers as opposed to the 30 or 60, feels more like 2010 than 2022.

I mean, I take that as a sign its ending.

But I agree with you, people have needs and the right house, in the right location will sell fast when priced right. And with all the investors leaving the market, it can make this decision easier if your position can handle it.

We were contacted by our Realtor who said a property was coming on market in a gated golf community and he would send it to us. The next day he called and said it was “under contract with contingencies” before hitting the market. This is not a sign of a market top. The price was way higher than when we started tracking the market and making visits beginning in 2020. We plan to rent and are open to other areas. People from Boston, NYC, PA, Chicago and California (includes us) just pay cash (us too). There is almost nothing attractive under $300k and the values are over $450,000 price-point. Oddly, the best values under $300,000 are newly completed track homes with asking prices under $120/SF for a 2-story shack just under 2,300 SF. The prices compared to coastal zones amounts to the downpayment on a comparable home in a comparable development in CA, PA, NY, etc. I go on city-data once in a while and many, many people are already planning to move outta ble zoens when they retire.

edit: I meant blue zones…. also, inventory is low in our target market. There were many more lower priced options for great homes 2-4 years ago.

“This is not a sign of a market top.” I think you are mistaken, people were making purchases like this near the peak of 2008 too. Prices can’t keep climbing; affordability has reached its highest limit, investors are leaving the market, and interest rates continue to climb. It’s the top, but a casino where people are still happy to make sh*ty bets because an agent will call you a winner! It could be owners refuse to sell and scarcity keeps prices high for a while. But the places that appreciated 212 percent since above their 2016 value – and that’s happened to some places in the Seattle area – are not going to duplicate that, nor will they be purchased at 2022 prices. I expect a few months of a standoff from reluctant owners but expect sellers will blink when faced with cost of owning and maintaining something based on its intrinsic value as opposed to a future value that has been warped as in for the past 10 or 12 years there had been no diminishing rates of utility from consuming more and more housing.

“Getting 2 offers as opposed to the 30 or 60, feels more like 2010 than 2022”

In 2011 we bought a new house that had been on the market for 6 months. We then sold our existing house, and it took a few months to get the first offer.

We’re a long ways from 2010.

It’s regional dependent. homes that are sellable has not changed. But inventory is suppressed. Hence frozen market.

If that inventory shows up then this market will be so f@“&ing brutal in price reductions. But until then this is the standoff. Those that sell now are the smart ones.

Hi Gerald,

“But inventory is suppressed.”

True in much of US but in some cities inventory is up 200 to 300% YoY.

See my post below.

There are alot of people who think they are getting a great bargain now with the small price decreases. Those people dont read Wolf Street and down see very far into the future.

The realtor lie that home prices only go up has not been proven false…YET.

Buying a home now is insane. Anyone buying right now will see their equity gobbled up. 100% loss on downpayment is almost certain on every home sold during this period.

No,you got it wrong. The realtor lie in January when there was only slightly more activity is, “you better buy now or be priced out forever.” Lol

This is my reading as well. The thing is, it seems like there’s still too much easy-money distorting just about every market, including housing.

”real tors” absolutely got it wrong, at least in some areas of FL we were living in and thinking of buying in 2006 gtv.

Some old ”ranchers” that were on canals with sailboat clearance ( No bridges ) to GOM were approx. $900,000.00 in 2006,,,

And then sold for $225,000.00 in 2009.

Have seen similar declines over the last 60-70 years,,,

$50.00 per month for flats in SF and other areas of THE bay area, etc., etc.

Ice water on a scalding fire. I’m seeing plenty of vacant properties for sale, including new construction, with plenty more in the works. As we say here in Montana, A Realtor Runs Through It.

LMAO!

Good advice! And, to further encourage those physically able to do the work, home construction is a cut and assembly process,; not some mysterious creation by skilled trades.

Measure, measure again and cut – fasten – nails, screws, glue, staples…… Be bold; go for it.

The construction side is easy. It’s the permitting and associated costs that go with it. I’d love to buy a small patch of land, have a transformer dropped and slowly build a small cmu block house in the woods.

The reality is that by the time I’ve gotten permitted for a well, septic, water rights, building permits, inspections, and all the other associated crap and couple that with stuff I can’t do on my own like drilling a well, I’ve spent more than I have on the house itself.

Then you’ve got to add in nose bleed land prices. And depending on your state, there’s a lot of work you might not be able to do without being licensed. Residential electrical is easy, but I doubt most states would let you install yourself, even if it passes code.

As far as I know every state allows owner-builders to perform all of their own work without any licensing – including electrical – requirements. There is usually a one year period after completion before they can sell it.

Good..7% is still too low to force all those smug OC/LA sellers to come back down from extremely optisimistic pricing and still not deterring all the FOMO buyers from completely vanishing.

If it takes 10% rate to bring it down to reality and drop 30 -40% around it. I say bring it on… I’ll embrace it with both arms and legs.

At a 10% rate, you may be out of a job by then. Be careful what you wish for.

From what I see general economy can’t handle 7% mortgage rate. A few more months and the Fed will be well on its way to rolling the economy into recession. Maybe inflation will still be high.

Seeing more discussion that Fed’s new inflation target should be 3% instead of 2% or unemployment will be too high. Same as its always been with juicing economy with paper, it hurts too much when you stop the faux wealth.

– Median Sold Prices : 2014 to 2019 lows is a Lazer tilting up. Prices are turning around for almost 2 years in preparation for the slump. It started in 2021, before the peak, on the left. kind of H&S. When the right shoulder will be completed the Lazer will complete it’s job, blowup prices.

– Existing home sales vol, the first chart, are in the reaction zone. Vol will rise moderately, before dropping to the 2008/2011 congestion zone. Vol will rise when price and mortgages adjust, possibly after recession.

– Today low is the second visit to the 2008/2011 congestion zone. In 2020 vol bounced up fast, built a bubble to lower highs. This time around vol will duck in the zone for a longer time, longer than the zone itself.

Thanks for another great update on the housing market, Wolf! It’s really interesting how you mentioned that if just 10% of the vacant properties being held off the market suddenly show up, active listings would more than double. I wonder what the chances are of that happening this year.

People with existing low mortgage rates and who are employed will hang on. No reason to sell, nothing they can afford at higher rates.

Part of the puzzle is to know why these properties are vacant. If they are vacation homes and people can afford the monthly, why sell?

Probably a lot of investors caught with their pants down trying to flip homes too though. Could be 10% of that “year round vacant” home market easily the way that trend caught on over the past 11 years. Now they’re waiting for what the realtors are trying to tell them (and themselves) will be a solid rebound in Spring. But they are all just blatantly ignoring that the fundamentals underpinning the market have changed with interest rates this high. Nobody likes cognitive dissonance but even less people will sit on those losses indefinitely as the market really starts to eat it. Then it’s fire sale territory.

The investors are ignoring the fundamentals because the buyers are still coughing up asking price.

Here in Phoenix, (one of the “worst hit 35% red lights flashing markers”) houses are being listed for $535k in what used to be a $300k neighborhood in 2019, and buyers are snapping them up.

The realtor I made an offer to this weekend balked at asking price, said he already had multiple offers for asking.

It’s pending now. The sellers have enough cash and income to wait for fantasy prices, and there are still plenty of buyers who will gladly pay them.

Pants_Relief, I agree with your general point. I think the buyers are still (naively) paying these prices because they believe that, even if they’re overpaying now and taking on a mortgage they really can’t afford, all will be hunky dory later in the year when the Fed pivots and they can refinance into a more affordable 3-4% mortgage.

It’s still a collectively fantasy. When the pivot doesn’t come, and the sellers who are currently holding on realize that not only can they not sell for February 2022 pricing, but they also can’t rent for high enough to make a profit, they’ll start dumping and the “low inventory” becomes a “high inventory.”

We’ve seen this movie before.

My wife and I have been searching for retirement property for almost 5 years. Since we had so long to look, we passed up a lot of meh properties that were good deals looking for that unicorn property that had everything we were looking for. Then came covid and price explosion in the rural areas where we were looking. One house that we looked at sold in Jan 2020 for $499k and is now relisted for $2.6M.

I was sure that we just needed to wait for the increased home loan rates to push the values down. Instead, the market just froze up. Several of the realtors we work with have said that sellers are fixated on peak prices and still think they should get even more than the peak since housing only ever goes up. In one place we look, a realtor said there are less than 300 homes listed and more than 3,000 real estate agents.

Of course, now that we stopped looking seriously, the unicorn property showed up. I cannot think of a worse possible time to purchase property. Go figure.

If you are looking rural try finding a patch of dirt and build as you can afford the pieces. Put in some sweat equity if you are able. So what if you need to shower outside with a hose. It’s fun and you’ll save 100’s of thousands. If you need to sleep on a bale of straw so what, at least you will sleep. It will get built. Totally impossible in towns or cities.

Wolf,

Where do you think equilibrium is for housing prices across the country and how far away from that do you think we are?

I live in San Diego and home price to income ratio is ~8x. Do you think this should re-rate closer to 5x?

So the interest rate on a mortgage continues to be roughly parallel – or slightly less – than the rate of inflation, and we’re coming up on one year (give or take) of this inversion.

Okay. Back in 2000 my mortgage was roughly 4% above the rate of inflation, which was pretty much normal and expected…mathematically and economically reasonable.

I’m pretty sure – eventually – one of these current rates is going to have to drastically change, and yet I can’t see inflation taking any sort of dive. But, on the other hand, 10% mortgage rates? There would be a catastrophe in this country if we priced money correctly, I’m pretty sure.

So… kicking the can down the road on monetary policy for the foreseeable future? Uh huh. Even in this overly simplified snapshot, I think the situation is pretty clear.

Fascinating time.

The charts alone!

The spring ‘selling’ season will be interesting.

At these rates? Probably more of a season and less selling. Most people may just stay put for now. Deep pockets prevail…

From NYT:

“But some economists say that investors — both large institutional investors like Waypoint and small ones using platforms like Mynd — are having another, subtler effect on the housing market, helping to nudge more Americans toward renting rather than buying.

They are doing that in part by reducing the supply of homes for sale, buying up — or refusing to sell — homes that would have once gone to first-time buyers. ”

What about Future cash flows??

This utopian fantasy is sort of a cross between Soylent Green and a nursing home chain, in that, if you’re a renter, you better have very deep pockets and be somewhat desperate.

As a short term option, a cool expensive rental solves problems, but it also burns cash. Apparently that doesn’t matter anymore, because everything has changed.

Maybe institutional property management will be done by AI and traditional tenet landlord disputes will be the stuff of buggy whips and elevator operators?

Maybe this is more like Westworld, where a rental is just a long fun vacation, where you watch home owners suffer? Very surreal.

Why are you dragging BS from the NY Times into here? Their economic coverage is HORRIBLE. Mostly BS. Go to the NY Times for recipes and Trump-bashing, not economics, for crying out loud.

I hear they have a good crossword puzzle on Sundays.

Economics isn’t the only thing they’re bad at. Most overrated paper.

Hi Wolf,

I dont read the NY Times but am curious what specifically you didn’t like about the quoted piece.

I actually do like this from them:

“They are doing that in part by reducing the supply of homes for sale, buying up — or refusing to sell — homes that would have once gone to first-time buyers.”

I don’t like investors having bought so many homes the last 5 years. Maybe it was fine in 2011 – 2014 timeframe coming out of the recession, but maybe not.

As you probably know investors bought 33% of homes in Atlanta (2021), upper 20%s in NC cities, Jacksonville (2021). I’ve heard it was 42% in Dallas County and 52% in Tarrant County (Ft. Worth)… for 2021 I believe though not certain. I think the source (utube video) was reliable… he probably got the info from NAR or Redfin or some such source.

Corporations or mom and pops either way I dont like it. It’d be different maybe if 90% of Americans owned a home but homeownership rate is 65%. May well be dropping the next year or two.

Supposedly about 50 countries have higher homeownership rates than the US. Yes I realize the homes in many of these countries might not be terrific (or worse) but still 50 countries it is reported to be (Wikipedia).

I am a renter, owned one home for 10 years.

Never been to Europe but Norway has a good reputation generally and they are at 80% homeownership.

I HATE it when people ask me what I think about some SHITTY CLUELESS piece in the NY TIMES. It’s an effing waste of my time.

The sections you cite are:

1. Populist clueless BS.

2. Economically wrong

3. Outdated.

4. Yes, all of the above.

Investors pulled back many months ago. I covered this here. The NY Times reporters are just effing clueless.

And even when investors buy, they buy a property to RENT it out. Often, they buy already-RENTAL properties and then continue to RENT them out.

A huge deal in 2022 and 2021 was build-for-rent, and that has slowed down too. It’s where homebuilders build homes specifically for rentals (cheaper), entire subdivisions of rental houses, where each subdivision has its own management and leasing office, and then the homebuilders put tenants in these build-to-rent houses, and then sell the whole package to a pension fund or an asset manager. I also covered this. This doesn’t reduce the “supply of homes to buy” but INCREASES THE SUPPLY OF HOMES TO RENT. And that’s sorely needed. These effing reporters at the NY Times has never heard of this?

None of these properties ever leave the housing market, and saying so it just BS. When a house is built to be rented out, or a rental house goes is sold from one owner to another, or a live-in homeowner sells it to an investor who puts in tenants, it’s still a house, and it’s still used as a house. It doesn’t matter who owns it, whether it’s mom-and-pop or a rental REIT.

BTW, there is no shortage of houses to buy. What you had is that the Fed gave the largest generation ever (Millennials) a whole bunch of nearly-free money, and they went out together and started buying homes with it, willy-nilly, often sight-unseen, and competed with each other, and got into bidding wars with each other, thereby driving already high prices into the stratosphere. And they bragged or complained about it on the social media, etc. etc. and stirred up more hype. And then they blamed boomers for the spike in prices. But boomers are not buying much anymore, they are now starting to be more into selling and checking out of this joint.

Sellers never drive up prices – they might want to but they cannot. They need buyers to do that. If buyers don’t want to buy because prices are too high, sellers cannot sell, and prices have to go down, until buyers start buying. But if buyers fight each other over who can pay the most for a house, then prices spike. That simple.

Millennials — who are the big buying generation now — need to go on Buyers’ Strike and stay on Buyers’ Strike to bring those prices down. And high mortgage rates are now encouraging that Buyers’ Strike. And that’s a good thing.

Be very afraid if you are in a flyover town with low property taxes and see the New York Times appear on the new neighbor’s driveway.

What newspaper has good economic coverage? My impression is that WolfStreet is better than any of them.

Thanks for pointing out the Millenial influence on the real estate price runup. I see it happening and yet haven’t read a word about it on the web.

One thing I read recently was the shock experienced by AirBnB operators (or any of the vacation rental spaces) that less than 50% of the available units in Phoenix were booked over the Super Bowl weekend. Not due to lack of demand so much as over supply.

Tying this in to your comment regarding investors buying units to rent I’m wondering how large the AirBnB/VRBO etc. footprint is in proportion to the total.

I know people who buy second homes (vacation homes) who rent these out via one of the platforms. They are able to afford the homes specifically because of the revenue streams.

Would these homes be considered vacant?

Could this conceivably be the 10% of homes to suddenly hit the market?

Don’t forget the crosswords and warmongering…

That said, it’s still a better-written rag than most out there.

NYT is truly a piece of shinola. Also, truly amazing that they still exist.

“…nearly 11 million housing units were vacant year-round, according to Census data.”

If that number is accurate, only 6% of these empty homes are currently listed? Holy moly. Looks like a slow motion train wreck in the making.

Combined with rising mortgage rates, we should expect massive price cuts ahead, assuming even a small portion of these sellers eventually feel the pain of these unproductive assets and need to unload them.

A lot of these owners have no desire to sell now or in the future. Here in San Antonio a lot of these houses are owned by Mexicans parking cash. Some of them even use the house a couple of weekends a year. They rarely come on the market and stay empty year after year. I have seen some where this went on for decades.

“Market is still frozen, potential sellers sit on vacant properties, hoping this too shall pass.”

This is greed, pure and simple. The getting is still very, very good, yet everybody wants peak prices. It’s been 9 months since prices peaked. These people who are waiting things out are losing tens of thousands of dollars in equity every month. Greed is a beautiful thing to witness, in this regard.

Well, I think we’re witnessing the intersection of greed and stupidity.

DC,

The big tech layoffs started around Nov ’22. The severance pay should start drying up in the March ’23 to June time frame. That’s when you should see the real estate prices drop. These laid off techies are shell shocked, watch their videos on the internet. When they can’t get a new job at their old salaries, all hell will break loose. The tech markets I follow are already offering 25% less on average for programming jobs.

what happened on 11/22?

“Greed is good.”

– quoted by every Investor Bro who didn’t actually watch the movie to the third act.

Powell remains very weak and dovish, talking tuff, but actually doing very little given the raging inflation. Rates remain well below the ridiculous CPI, let alone real life inflation still producing a negative real rate. He needs to get rates ALOT higher, which of course he will not do. I expect the FED to declare their premature victory over inflation with the lame CPI, combined with saying well 3-4% is close enough to 2%, LOL! Housing sales?…who cares?….this only matters to realtors and loan brokers for their “coming”. Home prices in most markets remain sticky high with pathetic levels of inventory. Where are the mbs sales? Oy vey

So much bad news in housing but home builder stocks are flirting with close to all time high.

Today TOL is up 2% plus after earnings AH

what are we not seeing the investors are seeing and buying these stocks :-)

Is TOL building in areas with tight housing supply and solid, stable employment outlook?

For years I’ve heard there is a housing shortage. Now all of a sudden there will be a housing glut.

Yes, funny. Toll Brothers orders collapsed by over 50%, but hey, no biggie.

They are all working through their huge backlogs from the past two years, and that’s where their revenues come from. But new sales orders have collapsed by 40% to 60% across the board. That’s their future revenues that have collapsed.

I do not understand the media coverage they’re getting. Investors are being led to the chopping block. But fine with me. Let them. There are no innocents in this game.

You don’t understand, they just started a National Sales event, which will certainly bolster their position and keep prices high!

Got your black flag flapping today…

Seeing very few listing and like $500 reductions just to game the zillows, western burbs of Chicago, it’ll take a few seasons for transactions to affect list prices

Must be all those over taxed people in Chicago moving out.

RE west burbs of Chicago.

The school district spending arms race is nearing its zenith. The retired LTHS and Hinsdale/Clarendon Hills 181 school districts superintendents collect $350,000 in pensions. How many people taking the Metra into downtown every day to the heyjack@ss shooting gallery? Open season on catalytic converters in the apartment and condo parking lots at night. And the freight trains with with hazardous placarded tank cars keep-a-rolling, but one of those towns is in an uproar because the Starbucks is closing.

But the buyers from Chicago always mention they are moving for a ‘nice back yard’.

A 7% mortgage actually cost 10% – 12% with taxes, insurance and 20% down. After few years inflation reduce the mortgage burden. But if your salary is fixed, stay about the same, or fall, u will not benefit from inflation, u deflate.

Recession increase the cost of debt. Most experts predict recession. Until proven wrong, house sales will be stale.

This is finally making sense to me, how the recession phases in and the implications for the housing Margery — whew…

First, a random snip from Australia, similar to Hong Kong, similar to any town USA, UK, Vancouver, etc:

This situation is known as negative equity, and it can potentially lead to bankruptcy for borrowers with money still owed to the bank even if the house is sold.

“CoreLogic analyst Eliza Owen said this reality is now hitting home for those who bought recently, especially in localities that have seen the biggest property price declines, in some cases already above 20 per cent.”

This slow motion train wreck and ambiguous hesitant recession, is about a process where air is let out of the pandemic balloon. A process where the pandemic calculations of buying homes or stocks, collides with the reality of downward pricing and negative equity. Obviously, cash burn, instead of cash flow.

However, in the bigger macro picture of a serious recession, we have a global tsunami of underwater homeowners, suddenly caught in a downdraft of repricing, facing the uncertainty of managing their new financial equations.

Instead of selling homes at losses, the obvious no brained is to rent and turn the property over to a management company.

Suddenly, out of the blue, the tsunami of homes for rent, impacts the sale prices of homes for sale. The lack of home inventory will be challenged by rental (supply) units that become more competitively priced (lower). Homes for sale will have to compete with rentals in a price war, as negative equity helps fuel fire sales.

Obviously, in the background, equities are also heavily impacted by negative equity and earnings impairments, adding additional pressure in a repricing recession.

Nostradamus

What about people just not buying many existing homes. Sure, new homes will be sold but at these rates, less so. Price discovery takes more time, economic slow down isn’t foreseeable occurring. Less ppl underwater and things just kind of go sideways and then growth picks up.

It’s the biz press that screams recession to encourage Powell to back off. Main Street is largely fine, I would expect corporate earnings to drop as they have over borrowed.which would leave to layoffs but if demand is their and hiring is tight maybe biz pays premium to retain productive capability.

I’ll stop as I’m having a harder time w this thought experiment but several scenarios or things expected to be mutually exclusive don’t necessarily have to come to fruition.

My old Miami neighborhood was horrid during the housing bust. People fled and left their pets behind. I was a attacked by a dog who was starving and fed it. It bit me again. Elderly women panhandling. All of this Fed stuff is fine but at a human level it is really bad. Don’t want to see that again.

Common sense has left this country,only wat out is a depression = reset ,this is 1929 PREPARING

Additionally, a huge factor that will drive negative equity, is the surging tsunami of pandemic speculative spending on reinventing lives, taking on easy loans, starting cool businesses that weren’t seriously thought out, taking on new risk, etc. leveraged positions that don’t pan out.

From freight blog:

“[This downturn is] definitely more severe,” King said. “2019 was the last downcycle we had, and it was pretty bad. But if you look at some of the operating costs, it was pretty level — especially things like diesel costs. What makes this one so different is the extreme spike in costs … in tandem with the drop in rates. It’s like a double whammy.”

This tension is probably most pronounced for those who bought a new tractor or made the switch to become owner-operators during the market’s boom time, taking on expensive equipment and overhead costs to chase what seemed like guaranteed profit. These drivers may now face a harsh reality that, in the end, inflated rates and high demand were fleeting, and the current market isn’t profitable enough to sustain their businesses.

“

Both of my children are working on getting married and would like to purchase a home rather than rent. We’ve been looking at what’s available in our area and have been amazed at the price inflation that has happened in our area. One home I just looked at on Zillow sold for $165K in 2015 and is now listed for $350K and apparently just had a sale fall through, so someone thought it was a good price.

As much as they don’t want to hear it, I think my kids may be smarter to rent for a while in hopes that home prices come back to reality. It’s a bit of a gamble, however, because if home prices manage to hang on to their current levels, renting would just be a waste of $’s. Right now they are living at home and saving to the best of their ability. What to do… What to do?

I rent where I am happy and can save at a decent rate. If one day we want home ownership, we’ll buy where we can live for a long time. But for now I like the flexibility of renting, it means if I need to move for a new job or a change in scenery I can move. The places and people we like are all in walking distance, so it’s really not about the money…

…That said, the gambler in me would love to time the market and get a good price on a nice property. Put minimal work in and flip for a big gain. Worked that way for a coworker of mine. Took the gains and overpaid big time last year for way too much house thats quickly collapsing in value, so like any good gamble you usually end up giving it all back in the end. Of course you only lose when you sell.

I am a home owner and personally I feel home ownership is over rated.

Home ownership has lot of expenses and it never stops.

Someone buying home at current price is downriver crazy to me

I’ve owned 4 homes and all in I never made money on any of them. Ownership only gives me freedom to decorate, but so does risking my rental deposit. Now we will only buy to secure a stable housing cost during retirement.

Bought new home 1986 NE of Dallas.

Other than caulking windows never any problems for 10 years. Oh did get grubs in my yard that i addressed.

Too bad I bought when so many homes were being built everywhere around DFW. Sold 10 years after purchase, 8% loss. Neighbor sold his 3 year old home in 89 at about 23% loss. Buyer told me what he paid for it.

I believe the point of this article is that home prices are emphatically *not* managing to hang on to their current price levels.

Big guy, I feel your pain. My daughter and her partner just made the plunge despite my warning that they were catching the peak, but all they’ve seen as 20 somethings is prices going up, rent going up and life going by so they couldn’t justify spending rent money to wait and gamble on a big decline. Fortunately, we and his parents were able to give them a substantial down payment, which greatly lessened their mortgage burden, but I feel we’ve thrown money down the crapper….oh well, the things we do for our kids…

Get married continue living at home ,save their ass off ,invest 10% in gold. In 2-3 years they will be greatly rewarded. Go back to the old ways and survive .

I wouldn’t say renting is a waste of money, relative to purchasing a home. Paying interest on a mortgage no less a waste of capital than paying rent.

With renting, at least you don’t take on the risk of a large investment loss.

It is sad. Where i live. There are buyers but no inventory at all. Market is frozen.

Same around here. As we know people don’t always sell because they feel like it. Often people sell because of job loss, death, or divorce. Two recent anecdotal stories even have me questioning that…

A friend in his 30’s is getting a divorce. IMO this would normally mean sell everything and start fresh. He and the wife kept it civil. She’s getting most the savings, but she handed over her claim on the house. They actually said “no sense in BOTH people trying to find a reasonably-priced place to live in this housing mess.” They got on the housing ladder just before the great inflation, and getting off now is painful, so they figured it is best to hang on to it.

Another example. Local widow looking to offload a house that is WAY too big for her lifestyle. It’s now vacant as she has another place to live. I know buyers in their 30’s, with kids, clamoring to buy the place in the mid-300’s (right for the area), but she is firm at 450k because she doesn’t really need the cash. She’s convinced the top market price is the right number and isn’t considering interest rates, so no meeting of buyer and seller yet after two months. I have two friends who would give mid-300’s for it immediately.

Point being, this market is so screwed up, it’s even bleeding into the death/divorce decision making that normally drives some sales volume.

Personally, I will cling to my 2.5% 30-year mortgage as long as possible. That has also got to be another big factor freezing up the market right now too.

I have half rented and half bought over the years. Age 66 lived in 33 different places, liked both. Granted military so some discipline there but whatever it’s your home.

I enjoy running different scenarios using free on-line rent vs. buy calculator by Michael Bluejay. I think its practical to run at least five different economic scenarios and see how it all shakes out.

Fun with charts and numbers:

Looking at the chart, looks like the median price of the home has gone from $425k to $360k, give or take. And the mortgage rate has gone from 4% to 7%, give or take.

Monthly payment for $425,000 at 4.0% with 20% down: $1,906

Monthly payment for $360,000 at 6.9% with 20% down: $2,330

Prices plunging, and so are 20% down payments required to avoid PMI, yet the monthly costs are still much higher.

Conclude whatever thou wilt.

Kevin,

The cost of the lower payment, at the 425K price, doesn’t include the lose of 65K in equity when you sell it for 360K. Depending on how long you owned that house, that “lower” payment would have to be recalculated to reflect the lost equity over the life of ownership. I suspect it will be a lot higher than buying that house at 360K with the “higher” payment.

Understood, but I’m looking at the motivation of the buyer. The buyer of a home is still paying more out-of-pocket monthly for a sharply reduced home, if the interest rate has also risen sharply. That reduces the incentive to buy at all.

How can you lose equity that was never realized? That 65k magically showed up during the past two years.

Wolf,

My wife and I own our home and want to purchase an investment property and live in the Tampa Bay area. If it were you, how long would you wait for prices to correct? What is your time frame for this thing to bottom? Thanks! I’m a huge fan of your articles and your calm, candid takes on things.

Live in Florida. There is no inventory. Nothing for sale where i am. Lots of buyers. People don’t want condos. I think there is still too much $ in the system.

According to Reventure Consulting (RC) there are a few markets where inventory is up considerably (I believe this is right, per recent video) 200 to 300% YoY: Austin, Boise, Nashville.

The inventory was now above the historical (timeframe I dont know) average.

In contrast Chicago, Boston, NYC YoY inventory up much less, i want to say about 30 to 50%. Some city mentioned had a YoY decline in inventory.

RC has made it a point that inventory is lower in general throughout the Midwest and Northeast versus the Sunbelt and West.

I’m trying to understand what the big picture is regarding homeownership and home prices. Things really have changed:

There is a conviction now that the Fed can control mortgage rates, so there’s now a belief that the Fed will “rescue” the housing market should home prices really start falling. Rather than being called “moral hazard” it should be “morale hazard”.

Investing is all about risk. Unless there is a conviction among the public that there’s real risk in buying a home – that prices are actively deflating – the risk factor isn’t a visceral concern. With the Fed jacking rates up and down, in dramatic fashion, they have dampened the risk factor. We are a long way away from the genuine fear that homes can or will deflate in value. For real deflation to take hold, it will require that most people are so convinced of it that they’ll regard home buying as a losing proposition. We are nowhere near that. Too many are anxiously waiting to jump in and buy should prices show much decline or if things like “inventory” or “median price declines” catch enough media attention.

Also, home ownership has become a rite of passage or a measure of being a winner or loser. I think that’s why home size has gotten pretty ridiculous and everyone is horny for home ownership. Home size has, on average, increased; it’s not as though “our parents” owned a house that adequately suited an average family. Now family sizes are smaller yet the homes are much bigger. That’s a status change, not a change in need.

There are just too many out there who are salivating for the big-ass truck, the super-sized house, and unlimited video streaming to put a sizeable dent in house prices and our consumptive culture for quite a long while. Unless a checkerboard swan appears, I don’t think there’s much hope for a ginormous house price “correction”.

Some of that may be the result of more teleworkers and homeschoolers today than in years prior. This might necessitate a more accommodative footprint for living/vocation/avocational doings all under one roof. But yeah, a lot of it’s probably just upsizing for the sake of BIGness, as Americans are the biggest size-queens on the planet.

As for a correction — there might be a gradual shift in the popular mindset, too. Blame two housing bubbles one right after another, but also an increasing desire for mobility. I was reflecting the other night how I’ve never lived in any one place for ten years in all of my years. Close, but never ten. I think, for me at least, this has helped diminish my own desire to situate more permanently. Maybe the idea of movement itself has supplanted the idea of stability which provides a sense of security for others, but I suspect I’m not alone. Granted, the ever-inclining premiums attached to the whole idea of homeownership doesn’t help make it any more attractive, either. The casino-fication of every damn’d thing has just gotten too gross.

The father of my childhood friend is still living in the same house from which I grew up across the street — since 1979, he’s been living there. There have been wave upon wave of new families who have come and gone from that neighborhood over the decades, including his own. He’s a hold-out and a total anomaly. There’s something vaguely haunted and lonely feeling about it whenever I’ve visited. Certainly nothing to covet or place a freakish premium upon. Just my experience, YMMV, etc.

@Randy,

I have been following Reventure Consulting’s channel for about a year. I like that he presents a lot of data, just like Wolf.

1981: A Mortgage Parable

Inflation was horrible.

The house price was lowered to $45k – back when that would buy a pretty decent mid-western home. The M-rate was 12.75% (adjustable) and we were thrilled to get it. Really! The highest rate advertised was 18% at the time.

Fast forward about 15 years and our M-rate had bottomed at 5.25% (if memory serves). That was a little higher than prevailing rates and we considered a re-fi and/or paying off the loan. But, as it turned out, that chunk of money was better off invested to eventually ride the dot-com bubble into its dot-bomb finale. And we rode that mortgage right into the 30-year sunset, too.

The kicker: Our PITI payment began about $425/mo and finished about $475. It was basically flat for 30 years. How could that be? Answer: As the P&I went down the T&I went up (as the home value increased).

The caveat: In 1981 it was very scary to take on the huge rate. We didn’t know that inflation and rates had peaked.

So today, could a young couple do as well with M-rates around 7% or so? The ‘what-ifs’ are pretty tricky.

In 1970 the price of a home was nearly $25k. The price of a home more than doubled between 1970 and 1980. Mortgage rates rose at the same time. By 1995 the price of a home more than doubled again. That is a 4X gain in 25 years. Generally, those who owned homes were more prosperous than those who rented.

Home Depot raised the wages of its employees. Unemployment is near a fifty year low.

I think that stocks (inflation adjusted) have had better returns than investing in personal home real estate. But… real estate can have much more relatively risk-reduced leverage (stock “leverage” costs are high and not as deep – you can’t have 80% margin debt), and there’s a whopping tax incentive for home ownership, while owning it and the tax-free profit allowance when sold.

I wonder, when all costs are factored in, e.g. opportunity cost, tax deductability of prop. tax, insurance/annual property taxes/upkeep vs. renting, compared to investing in say a S&P 500 index, which is the better investment???

A. House. Is. Not. An. Investment.

It’s a place to live. If you view it in that light, it’s a different equation.

Also: You forgot to net out the cost of your monthly rent, utilities, insurance (yes, you need renters insurance – at least for the liability aspect), the security deposit give back (how many people actually get them back?) over the same period of time for a comparable quality of life vs. your cost of home ownership.

“Ideally” a home should not be an investment. But “realistically”, it is.

Currently 10,000 Baby Boomers a month are retiring. I wonder how much this is contributing to the low unemployment?

It’s important to note that the median price decline belies the pronounced current geographical bifurcation of the US housing market. Nearly all of the house price declines have happened in the Rockies and west, while east of the Rockies, with a few exceptions, seasonally adjusted prices have only slightly declined, some have even risen.

Nashville might be one of those exceptions.

Large price gains, now inventory is up quite a bit (200 to 300%). Some Florida and NC cities, Atlanta had investors buy 25 to 33% of homes.

Will this be a problem ?

Austin (Dallas too ? ), like Nashville and Boise also have had a large inventory increase, prices dropping quite a bit from peak.

But from what I’ve heard/read you are right in general.

The 2-300% increase in inventory is from what basis? The next-to-nothing inventory of the past few years or from a longer period of time where the real estate market was somewhat normal?

Percentages are where people get tied up in their shoelaces.

The cheap money was universally available and thus raised the home prices in all geographies.

The high mortgage rates would hit all location equally more or less with some delay.

People do tend to think that we are different and it won’t hit my geography.

1) Full time jobs are dwindling. Many of those who have a full time job

didn’t get a raise for since 2019. On the cusp of recession ceo cut capex and payroll, for fun and entertainment.

2) This downturn took out many stop losses and stocks options. High tech employers and employees REAL income is down.

3) Seattle and the Bay Area have been awash by a tsunami of underwater options.

4) NDX might complete it’s round trip to Feb 2020 high, before rising to a lower high.

5) Executives and employees might sell their stocks and options, cashing in, creating an avalanche, sending prices below Mar 2020 low.

Sellers want price from the era of 3% 30yr.

Buyers want price from current 6.8% era.

Only forced sales will break this loose. But how many are comfortably locked into 3% mortgages?

Buyers want 10% unemployment.

I don’t understand this idea that people en mass have no reason to sell. This means you believe people won’t marry, divorce, have kids, upsize, downsize, die, get sick, get laid off, move for a job, etc. I’m honestly confused.

There would always be forced sale and home prices would be defined by these marginal sales.

Also, median home prices don’t give complete picture. It only tells that low prices homes are being sold at the moment.

Case Schiller Index is the accurate pricing

28 million homesalyes between 2017-2022.

Refinances are smaller.

“And this too shall pass” Well you can’t say that the interest rates for the past decade were the lowest of the last 500 years, predict a regression to the mean as a general rule, and then expect rates to return to a fleeting six sigma outlier.

Of course debt loads are historically monstrous and no one expects them to regress to the mean. And typical institutional insanity is at historical norms and that will stay in elevated bounds.

So if predictions are what you want – Bonne Chance.

The current push and pull between market pumping , for an immediate pre-V-pre-recession economic expansion, versus the cautious old ladies patiently waiting for a slow-motion global train wreck, seems increasingly absurd.

Justifying either path with facts is unclear, but most of the leading coincidental indicators are in the process of pointing downward, indicating a serious recession is very likely.

I’m not rooting for a destructive recession, but I think if home valuation and stocks spike up from here, that will be extremely destructive globally.

The polarized outcome isn’t good either way, but I think it’s far more healthy for the economy to reset and kill off excessive speculative forces, which have an insatiable appetite for addictive risk taking. It’s better for everybody if those people are placed into long term rehab.

Meanwhile:

“ … Well, those revisions are already coming in. Following Wednesday’s strong retail sales report, JPMorgan, Bank of America, and Deutsche Bank were among firms joining Goldman Sachs in revising up their near-term GDP forecasts or putting off their expectations for a recession.”

That’s just like in various movies about the GFC, those firms are playing their role to lure investors into a situation, where the banks aren’t held accountable for your stupidity

U left off the part about, ”little old ladies of any gender identification DD, of which we are 2, or 4 including our 4 legged lover girls…

We have finally decided to ”have a go,” and thanks to Wolf’s wonders and the commentariat on here, “OFF we go.”

So far, it appears that treasury direct is the way to go.

Time will tell.

This is about a week ago, but the thing to ponder with short term Treasury bills, currently, is the concept of scarcity.

There’s a ton of complex plumbing issues going on that are converging in the next several months, including probably 2 Fed hikes+, mystery issues related to collateral shortages that connect to Treasury bills and of course the deficit, which statutorily restrict Treasury from increasing bill supply.

This was from Reuter

Next week, the Treasury is likely to say that it will reduce its issuance of Treasury bills, debt that matures in one year or less, and run down its cash balance to buy more time.

“Bill issuance is going to come down quite a bit in Q2. … They have to incorporate the debt ceiling into their financing estimates at this point,” said Angelo Manolatos, a macro strategist at Wells Fargo.

From the Fed

Since changes in quantities affect the SC repo rate not only of on-the-run but also off-the-

run securities, it is reasonable to conclude that, in the Treasury market, the scarcity effect is

a widespread phenomenon and is not confined just to a few “special” securities. Thus, these

changes in quantities by the Fed, being relevant for the SC repo rates of many Treasury

securities outstanding, can also affect the Treasury GC repo rate, and other money market

rates through arbitrage relations

Another Fed thing:

.Third, cash balances at money funds may remain elevated even at lower ON RRP rates because alternative short-term funding instruments that compensate large investors for counterparty and interest rate risk are limited.

IMHO, short rates are going higher for longer. Mortgages are going to be sucked into that chaos too.

However, this all will eventually peak out and head the opposite way and reprice with bill prices..

Amen

Nostradamus

A market without buyers or sellers is no market. It’s a cemetery.

This reminds me of an aeronautical term called coffin corner. It’s the airspeed and altitude at which if you go any faster, you exceed your critical mach number and risk structural damage, but if you go any slower, you stall the aircraft. The real estate market has basically orgied itself into a sort of coffin corner. The only thing to do is drop in altitude.

Nicely done.