Banks as stock-pump schemes in the era of consensual hallucination.

By Wolf Richter for WOLF STREET.

First Republic Bank, headquartered in San Francisco, and Western Alliance Bank, headquartered in Phoenix, are on the forefront of the regional banks that haven’t collapsed yet. Their shares continued their plunge today as trading was halted on and off. Other bank stocks got hammered too, but not to this extent.

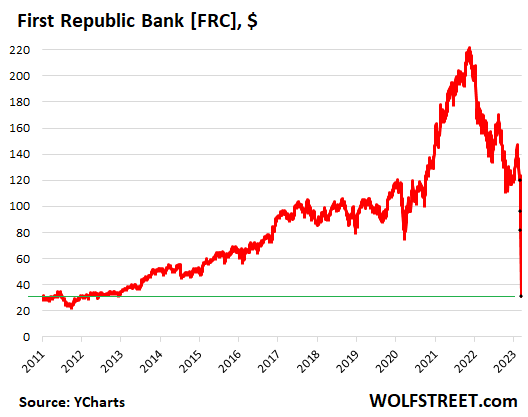

First Republic is intricately tied to the Free-Money party in Silicon Valley and San Francisco – “a leading private bank and wealth management company,” it calls itself. The stock had doubled from 2019 to peak consensual hallucination in November 2021. It had quadrupled from 2014 – a bank stock! Which shows how crazy this consensual hallucination was.

And because it was tied to this party, it is tied to the end of the party. Since the high in November, the Nasdaq Composite has plunged by 30%. The shares of many startups that had gone public via IPO or SPAC collapsed. Cryptos plunged. Silicon Valley Bank, which was instrumental in all this, collapsed on Friday. Many people whose wealth was tied to startups are finding themselves less wealthy. And First Republic catered to them. Shares [FRC] collapsed 61% for the day, and were down by 86% from their high in November 2021, therefore making it into my glorious pantheon of Imploded Stocks (data via YCharts):

Note that shares, currently at around $31, are back where they’d been in 2013, which really isn’t a biggie – why should shares of a bank quadruple every four years? A bank is a government-regulated taxpayer-backed financial utility, not a stock pump scheme.

First Republic experienced an intense run on the bank by the same folks it so energetically catered to: the wealthy. They were yanking their cash out of their bank accounts at First Republic by the millions of dollars at a time – same thing that accelerated the fall of Silicon Valley Bank when cash-rich companies, often pushed by their venture-capital investors, yanked their millions and hundreds of millions out.

On Sunday, the Fed came out with a program to shore up teetering banks like First Republic, by providing additional loans through a new facility. Also on Sunday, First Republic announced that it had received additional funding from JPMorgan, on top of the funding it had from the Fed, and “continued access to funding through the Federal Home Loan Bank.” It said that its “total available, unused liquidity to fund operations is now more than $70 billion.”

First Republic Bank is not a conservatively run bank. It represents the worst excesses in the Free-Money party. During the Financial Crisis, Bank of America ended up with it when it purchased Merrill Lynch, which had acquired it in 2007. In 2009, Bank of America sold First Republic to a group of investors that included private equity firms Colony Capital and General Atlantic. They sold it to the public via an IPO in December 2010. And then the Free Money party began.

The primary purpose was to pump up the stock price. First Republic went after the wealth management and private banking business, particularly in Silicon Valley and San Francisco, and then spread out from there. It provided all kinds of services, such as making loans to startup founders who were sitting on illiquid shares that were at the time highly valued – by Softbank, LOL. If they wanted to plow several million into a fancy home or needed cash otherwise, they could pledge their illiquid shares as collateral.

But the Free-Money era is over. Startup valuations have plunged, venture capital has dried up, Softbank’s Venture funds have taken huge losses, many startups are facing an existential crisis and will fold, and they’re laying off people to lengthen the time they can operate, and shares of many startups that went public via IPO or SPAC have collapsed.

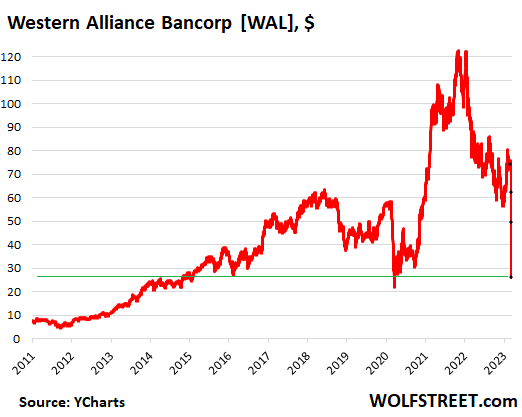

Western Alliance Bancorp is another magnificent stock-pump mirage of the Free Money party. Its shares more than doubled between early 2020 and peak consensual hallucination in November 2021, and they multiplied by a factor of six since 2014 – a bank stock, for crying out loud!

Its shares [WAL] plunged 47% today and since the high in November 2021 are down by 79%, thereby making it into my pantheon of Imploded Stocks. Like Republic Bank, the chart of Western Alliance shows what kind of stock-pump scheme it was in the era of consensual hallucination (data via YCharts):

Western Alliance, like Silicon Valley Bank, is heavily focused on catering to businesses through various subsidiaries in different Western States, including Western Alliance Bank. Its subsidiary Bridge Bank in the San Francisco Bay Area is into “startup banking – tech,” and also caters to companies in commercial real estate, biotech, etc. Yup.

Western Alliance too was hit by a magnificent run on the bank. On March 10, when Silicon Valley Bank collapsed, Western Alliance released “updated financial figures” to show that deposits “remain strong,” liquidity “remains robust,” and capital remains “strong,” with various numbers attached, upon which its shares plunged.

This morning, Western Alliance issued an “updated” 8-K filing with the SEC, which included this statement:

“Since the statement we released last week, Western Alliance has taken additional steps to strengthen its liquidity position to ensure that we are in a position to meet all of our client funding needs, including increasing our borrowing capacity. As of this morning, cash reserves exceed $25 billion and are growing, while deposit outflows have been moderate. Including accounts eligible for pass-through insurance, insured deposits exceed 50% of total deposits.”

Upon which its shares collapsed 47%.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Fed whisperer Nick Timiraos of WSJ on Twitter indicating about pausing when things break, which he says they now have. May be a sign the Fed is done ?

People have been saying this crap for an ENTIRE YEAR. Timiraos among them. They’re all aping Goldman Sachs and Wall Street more broadly, which have been wrong about rates every step along the way.

There is a very dark side to this pivot mongering:

The executives at these banks believed this shit and didn’t hedge their interest rate exposure and didn’t get rid of their long-dated bonds when they could have, because of this shit, and now their banks got into trouble because they believed this shit!!!

Why is this crap still being dragged into here?

Can we please have you, E.B. Tucker and Gregory Mannarino do a podcast. I would pay top money for that.

Gregory Mannarino is an idiot. He’s been lying, saying that the FED is actually secretly buying stocks. He and his fake NYC background are a joke.

Wolf – How far do you think this problem of asset liquidation could extend? Could a brokerage like Schwab even be impacted? As I look at the financial statements of Schwab it is obvious that they tend to make most of their money from the gap between the interest paid and earned on investor cash assets (since many trades are commission-free).

Or do you think these depositor runs are limited to certain types of banks that are more specific to the startup craziness?

We have T-bills in Schwab. Today, Schwab seems to be in trouble. Here’s what an investor, we think it was Mr. Thierl said: “The Fed has come out and said that anyone with “high quality” debt like Treasuries can pledge it as collateral and get back par value for up to a year. So, you bought a Treasury Note for $100 in 2021, it’s now worth $95. Whatever you do… DO NOT SELL IT. Come to the Fed and they will give you $100 for the debt. Treasuries don’t get dumped on the market and everyone is made whole. BOOM, everyone wins and problem solved, right?

Do you agree or not?

We hear that Schwab is in trouble. We have T-bills there. One investor recommended going to The Fed to trade or retrieve our money back.

Can someone please explain this?

Rubicon,

If you hold T-bills, you hold T-bills and not Schwab cash, and they have a CUSIP number, and they’re yours, no matter what happens to Schwab. If Schwab vanishes from the earth, you gather up your documents to prove they’re yours, and you’ll have them transferred into some other account.

gametv,

Interest revenues come from fixed income securities, margin loans, and bank loans.

Margin loans and bank loans have much higher interest rates than Treasuries. Margin loans are variable rate loans, meaning Schwab hikes the rate it charges on current loans as it sees fit. So margin loans will never be under water. This is a very profitable business.

About half of their income is from the net income of margin loans, net income from securities, and net income from bank loans. ($10.6 billion in 2022)

The other half of their income is from fees ($10.1 billion), from:

Mutual funds, ETFs, and collective trust funds

Advice solutions

Asset management and administration fees

Trading revenue

Commissions

Order flow revenue

Principal transactions

Trading revenue

Bank deposit account fees

Also Schwab has a sweep feature that puts your brokerage cash into various FDIC insured accounts with other banks, so all of it is FDIC insured.

This mini-crisis is all centered on specialized banks that are heavily exposed to the worst excesses of the free money era.

In the broader financial system, this will blow over.

I do think that all financial stocks are going to be lower for longer, LOL

Wolf, In your Mar 13. 2023 5:43pm comment, you referenced margin loans as being a significant source of income for some banks. Brings up a side question. With the “imploding stocks” as illustrated by your many charts, should we be looking at how much of those imploding investments were based on margine loans? I’d guess the “margins” have largely disappeared in the many cases of imploded stocks. Or are these just a small part of the “collateral value on margin lending accounts.

There are still $640 billion in margin loans outstanding as of the end of January (Feb data not yet released). This was down by about $200 billion from Jan 2022. But it’s still a lot. Schwab, as have others, disclosed that their margin lending revenues dipped a little. But margin interest rates have been increased a lot, so they’re making more income off each margin-loan dollar.

Also, SCHW net interest margin has increased (sequentially) each of the last four quarters, and fee margin (fee income / assets subject to fee) have also increased, both significantly.

The pivot stuff comes across like some kind of brainwashing cult at this point. It doesn’t matter how many times you cite what the Fed chairman actually says, or even that you post videos where he explains himself, they misrepresent it still. And they continue to do so after being corrected repeatedly.

This goes beyond poor comprehension into the realm of delusion and it bodes ill for the economy since enough firms are captivated by it that they are facing existential risks.

Powell and the FED caused it. All of their lying and QE have caught up to them. Now everybody is trying to call their bluff. They intentionally made people believe in a permanent FED put. That was their design. They, in their own words, “forced” people out on the risk curve.

Who was “forced” out on the risk curve? Mostly incompetent and/or greedy financial institutions, or people who’s life is neurotically focused on money, or stupid and/or lazily uneducated people, FOMO driven personalities, etc.

@ drifterproof:

“Who was “forced” out on the risk curve?”

—————————————–

retiree’sand savers with limited means trying to keep pace with inflation, in the face of interest rate suppression. courtesy of the FED and US Government running continuous deficits and printing money while offshoring the industrial base

does this soud plausible?

@ cb

I doubt your hypothesis, which is actually a non-fact-based narrative argument, that fixed income retirees and “savers” with “limited means” personally chose risky investment vehicles. It seems to me that people living on such “limited means” do not have the investible assets to try to finesse the system that way.

If you want to further specify statistics about the investment habits of those groups, it would be more convincing.

Who was forced to take more risk?

Everyone who was trying to stay ahead of a promoted inflation.

Remember 2% with .05% fed funds?

(And we STILL have a similar interest rate increment between rates and inflation)

Who was forced?

Money mangers were forced to take more risk. And they were putting others money into that position.

The Fed’s Fisher ADMITTED the idea was to FORCE investors out the risk spectrum. Do you think he was lying? That they didnt know what they were doing by slamming long rates and removing fixed income alternatives to asset holding?

Who was forced to take more risk? Managers of large-scale and small-scale pension plans, that’s who. In order to keep with promises of specific return percentages, they were forced out onto the risk curve in order to keep up with the promises politicians had made when times were good. Our local teacher pension, for instance, used to hold mostly T-bills or other conservative investments, but over the last decade or so shifted the bulk of the cash into higher-return, higher-risk instruments. So, yes, pensioners and other fixed-income people were “forced” out on this limb because the programs they put money into, and monies they were promised at retirement, were managed by those who had no other choice.

Seriously, it’s not hard to go read multiple articles that point this out.

Now, whether those promises should have been made in the first place, like Cal-pers doing all of its calculations based on an expected 7% return on investment, is a WHOLE different discussion. However, let’s not lay the blame at a Cal-pers’ employee’s feet for things they didn’t have control over.

@ drifterproof –

why get pedantic when common sense will do?

read the two comments directly below your response to me, and choose to let loose of willfull blindnes ……

and as for narrative, read your initial post as you look in the mirror and have a good laugh at the irony ……

YEP!

I stopped banging my head in general….

MO!

DELIBERATE…

I think you’re right.

Nomura is is saying a rate cut at the next meeting. I have my popcorn ready. Someone is going to be crying whether it’s wall Street or perma bears.

If they cut I’m going on a shopping spree. Here in the UK the forecast recession hasn’t turned up and everyone I talk to is rammed for work even with price increases. If they cut then I will know that they don’t have the guts to stop inflation, and it’s time to panic before everyone else figures this out.

And watch out, because as the Ukraine shock comes out of annualized figures they will be trumpeting that inflation is coming down rapidly and all is under control.

I hope Wolf is right and Powell holds the line, but he must be under huge political pressure to ease off.

It’s not just a matter of bulls vs bears. Mainstream will suffer if the Fed cuts. This is a serious issue, could care less about Wallstreet. Many people can’t afford to live in this country any longer. That’s all we need is for the still overly inflated house prices to be the new floor. Insurance, restaurants, shelter, you name it through the roof. Still pissed about my auto insurance increase. I hope the Fed ignores Wallstreet and continues to focus on what’s good for the country. I’ve had it with Wallstreet. Been disgusted for many years now.

On the other hand, Wolf, the Japanese bank Nomura (which has been calling for aggressively hawkish Fed action since last June, and been mostly correct) is now predicting not just a PAUSE, but a rate cut at the March meeting.

This banking crisis has introduced a new aspect to the pivot scenario.

No it hasn’t and better not. I sick of it, hearing pivot hope for months. I can hardly read Zerohedge anymore because of it. Every other damn article is about a Fed pivot. It’s nothing but Wallstreet’s wishful thinking. If the Fed pivots, or even pauses, there is no hope for this country.

Fed has clearly stated they have 2 mandates

1: Full Employment

2: Price Stability

So far Employment is full and their target is price stability. I am not sure they will pivot that soon unless the banking crisis causes a lot of unemployment. What’s ur thought?

EVERY SINGLE BANK OUT THERE wants the Fed to cut rates, for the same reason Silicon Valley Bank wanted the Fed to cut rates. They ALL have the same problem now — deposits are fleeing, and if they have to sell securities, they get in trouble. Why should I pay attention to what the banks WANT?

I’m tired of hearing about a “banking crisis.” These greedy fockers have been milking profit by raising rates on loans, investing in crazy schemes, parking cash for free at the Fed and making money off it, all while stiffing depositors with near-zero interest on deposit accounts for years now.

Don’t confuse “losing their cash cow” with “crisis.” This crap was their own doing, and while I’m in favor of bailing out insured depositors who followed the rules to the best of their ability, to hell with everyone else who played loose with capitalism on the way up but want to cry into their diapers about capitalism on the way down.

MoneyCash….conceding I am not the last word on the matter (i.e., not my background)…Fed goals were codified in the original Full Employment Act (1946) and then refined by the Humphrey Hawkins Act (1978) that established four goals (not necessarily compatible): full employment, GDP growth, price stability and trade/budget balance. The problem, far as I can divine from research, is that the Fed internally decided the quantitative targets – there has never really been a legislative mandate for 2% inflation for example. When one digs into all this “stuff” one discovers a huge morass of politically driven economic analysis and suspect/changing semantics for key metrics as well as questionable modifications. Point being that tehre’s a lot more going on under the hood – much of which may have been very misguided and too intrusive of market operations (price discovery especially). Too many huhs(?) in much of this:

. Misapplied Keynsian analysis?

. Phillips Curve analytic that doesn’t apply in global economy?

. MMT? It’s just a book-keeping process?

. Price indices/inflation averages adjusted for changing percentages of goods in the consumer basket (substitution)?

. Price index/inflation adjustments based on faux quantitative goods/services quality improvements?

. Inflation calculations that do not weigh asset bubble pricing appropriately?

. Changing unemployment indices?

. Astronomical P/E ratios while profit margins basically have held steadfast at historical averages?

There’s a lot more as one digs into all of this. The obvious end point doesn’t change, however. Too much damn money printing; too much spending; all leading to a financial house of cards when looked at through the lens of aggregate private/public debt against anemic real GDP growth. We got away with exporting inflation for decades.

Simplistic diatribe over.

2% inflation is NOT price stability.

DawnsEarlyLight…..exactly! Let’s see….72/2 = 36. Wow!

You’re underestimating human stupidity. With enough arrogance and over confidence they could indeed pivot. If you see normal people arguing for a pivot, then they are also people in positions of power that think a pivot would be a good idea.

I’m not saying i know what is going to happen. Decadence, is not about wild orgies, it’s about wild orgies while the enemy is at the gates, because you think your empire is eternal.

With enough stupidity, they could pivot, send the inflation to 25% and then trigger a dollar collapse…. Because 25% inflation and the dollar collapsing is “impossible”, every one know that.

“Why is this crap still being dragged into here?”

If it keeps coming back… then maybe it isn’t crap and could actually happen. In things like this, what people think is the truth matters.

CME rate hike probability is still very high for next 3 meetings, yet, there’s an internet media hype campaign pumping the imminent pause by Fed.

The same crowd was pumping all weekend that rate cuts were going to happen by Monday.

The Fed effr rate is right on target, cradled between IORB and ONRRP with 3 month (money market) yielding decent rates.

The global bond market is rightfully freaked out about a tsunami of zombie entities, but the very worst thing in the world, is to have equity markets reignite into unimaginable overvaluation.

Hopefully, Powell will stay on course deflating casino madness, and generally the come fed tool is close to reality.

I think there is a possibility that the rate cut narrative will expand and then obviously add to instability…. Who cares.

Well said;

“There is a very dark side to this pivot mongering:”

We shall see. In the mean while, did anyone else experience being locked out of their treasury direct account from Sat morning until today

Someone today mentioned that one of the stages required for the timeline of the SVB debacle was clocked at 12 standard deviation from the mean, indicating that a white collar crime has been committed.

Would like the Wolfmans expert take on your question. Finding his insight very educational. My opinion is the FED is trapped of its own doing.

No. Not in the slightest. The Federal Reserve’s job #1 will be to continue to raising interest rates faster and higher which is precisely what it will faithfully and correctly continue to do.

Trapped. Exactly. If they did lower, buy some I Bonds.

Powell brought in a guy known as the “Wall Street Nemesis” to dig thru Silicon Valley Bank. Powell is all in baby, he’s hannibal lector and the economy is his fava beans and liver. Fw Fw Fw Fw. Hehe

No turning back, more pain to come.

Quote of the day – re “pivot mongering”

“…as far as I’m concerned, today marks the return to quantitative easing. So, we are now officially in QE 5. And I expect the Fed’s balance sheet to go up from here…”

Peter Schiff

“Sometimes I wonder if the world is being run by smart people who are putting us on or by imbeciles who really mean it.” – Not Mark Twain; source unknown

Per FT:

“Marked-to-market bank assets have declined by an average of 10% across all the banks. After the recent decrease in value of bank assets, 2,315 banks accounting for $11 trillion of aggregate assets have negative capitalization.”

The big problem is the regulators are changing their rules. It is like an umpire at a baseball game deciding at the last minute to give some batters 4 strikes for an out, while the rule was always 3 strikes. Some banks are supposed to fail. (As for SVB, are the regulators going to claw back the profits made on recent stock sales by management, are they going to claw back bonuses to employees given hours before shut down?). Depositors who are so stupid as to keep more than $250K in a bank are supposed to lose the rest of their deposits. That is how capitalism works.

The regulators have changed the rules on banks. We don’t know which rules apply to which banks. I am getting as much money as I can out of banks. It has become obvious they are regulated by either well-intentioned idiots or crooks.

Little deposit holders depend on big deposit holders to do the due diligence. I don’t have the resources to scrutinize the bank’s books. A depositor with $100 million does. The system is set up so that big deposit holders help keep the banks honest.

The big deposit holders didn’t do their job. They are a part of the economic ecosystem who didn’t play their role. They should be punished by losing a percentage of their deposits.

This bailout of depositors breaks an important feedback loop in the banking system. Regulators are backward looking. Big deposit holders are supposed to be forward looking. Now who holds the banks accountable? Powell took his best players out of the game.

not only that, big depositors who survive have the resources to go after the banks, their officers and regulators for malfeasance and fraud.

these actions may be to assuage a large group of very powerful, who might be outraged that they lost significant bank deposits.

Actually everything they are doing is because certain laws give them the power to do these actions.

Laws, rules, and regulations can all be changed. The problem is when they are changed after an event to benefit those involved in the event. That’s why baseball changes rules in the offseason and not during regular season games. It’s also why eg is right and this is Calvinball.

If you haven’t already figured out that you’re not playing anything like baseball, you’re in the wrong game — this is Calvinball …

Exactly…

YEP!

BAD HABIT!

BAD TIMING TOO!

PICK YOURSELVES UP, BY THE BOOTSTRAPS! LOL

Isn’t this really about the debt sloshing around the system, in the form of long term treasuries, that are massively mispriced? How many ten year or even thirty year notes, at basically 2 per cent, are floating around peoples portfolios losing money, basically misallocated capital, now in a TOTALLY illiquid market?

Isn’t this new alphabet soup BTFP program just a bad bank solution that all institutions will just dump their low-yield long term bonds into?

More bailouts? More QE

“Isn’t this new alphabet soup BTFP program just a bad bank solution that all institutions will just dump their low-yield long term bonds into?”

This is just uninformed out the wazoo.

The Fed is NOT buying the securities!!! A bad bank buys stuff. The Fed offered to lend to the banks, against collateral. If you know anything, you know that “lending” is different from “buying.”

Hello Wolf and TY,

I agree rates will continue to rise. Not working from the alphabet soup premise and understanding these are loans. These loans when received on full dollar value of par, then the FDIC temporarily eats the losses on this impaired collateral, the idea is that the loss is recouped via special assessments on FDIC membership. So, your spreading the loss of regional and mid sized banks among the larger membership. Question is when that membership has access to other Fed lending facilities aren’t we just allowing more money into the system to defeat the goal of reducing inflation. Although not a zero sum game, to a certain extent the Fed is somewhat stuck w/ respect to inflation and must raise rates which continues to erode the bond market, capital ratios and the economy. I would guess I’m missing something and would appreciate advice. Thanks

The only thing that matters is confidence in the system. If confidence is lost, the system collapses.

The problem is the Fed got involved in buying long dated treasuries. That created all kinds of moral hazard, and it’s going to be extremely difficult to undo. The Fed pulled down on the yield curve like a rubber band and created fantasy land. A land where startups could take years and years to become profitable and still be a better bet than a 10 year bond. I would be fearful that hot inflation reverses the recent downward move in yields, putting further pressure on banks seeking liquidity, and creating more havoc.

Ralph said – “The only thing that matters is confidence in the system. If confidence is lost, the system collapses.”

——————————————–

Large swaths of the public have great confidence that the FED will continue to work in the interest of itself and favored parties, picking winners and losers along the way. That is what the FED has been doing for years. That is the system, and you can have confort that it will continue.

meanwhile, homelessness grows ………..

But isn’t it still a problem that they are lending you more money that what the bond is worth (albeit for only 1 year)? In the example above of a bond bought at $100 in 2021 but is now only worth $95, isn’t it the case that the Fed will loan them the par amount or $100 even if that isn’t what it is worth? A bank wouldn’t take a 2 year old car as collateral and give you a loan for the new car price. Why is that happening for the loans whose values have dropped?

The bond will be worth “par” (face value) at maturity, guaranteed. MBS will be worth par many years before maturity because of pass-through principal payments and call features. Someone is going to hold them to maturity, collect interest along the way, and get paid face value at maturity.

Why would that be a problem? The Fed could lend to banks without collateral, if it wanted to. Banks can and do lend to each other without collateral every day in the federal funds market.

I will tell you in early April the amount of loans outstanding under this facility. This will be part of my regular QT update. The amount of loans will be small by balance sheet standards, a rounding error. It was the same thing with the pandemic facilities that the Fed started. I reported on it at the time. Once the facility is there, confidence returns, and it’s no longer needed, and banks won’t use it.

The FED is offering partially collateralized loans to insolvent (if assets marked to fair value) institutions close to the 1y overnight swap rate. There would be no institution which would offer those conditions in interbank lending.

Now let’s assume the bank somehow manages to dupe someone into providing new capital and survive. Then there will be no loss to the public.

But let’s assume that bank is still as insolvent, when the program runs out in 1 year, as it is now. At that time the public takes the haircut of the collateral. It’s a shift of haircuts of whoever managed to get their assets out of the bank in the meantime (depositors/bondholders) to the public. Yes depositors now get their money from the public anyway, so it does not make a difference for that part, but unsecured bondholders were not. And yes it’s not a bad bank, but what is that if not an investor bailout? It’s quite clear that the FED cares about interbank lending and that’s why they are doing it. This is not about depositors. And it doesn’t matter what the face value of that security is and that it will get paid full at maturity. The rate risk on that security belongs to its value and it got transfered to the public and someone else transferred that loss to us. If it does not matter then please swap me some cash for a 2% 30year. After all, you will get your money back + interest!

@ Yuan –

great reasoning and comment …..

The FED offered to lend to the banks, against collaterla —- at par

there, fixed it

So what. It’s lending, not buying. Willfully confusing lending with buying is some really dumb shit.

For the FED to loan on assets at par, and therefore introduce additional dollars into the system, is a form of bailout and is inflationary …………

yes it is lending not buying but if I tried to go to bank and get loan against my treasuries they would lend at it’s market value not at its par value and that is what is rubbing people the wrong way.

Are the ratings agencies all over this, or still lagging?

First Republic is still investment grade. I just checked.

Sweet. Imma load up on their CP and CDs tomorrow. Thx guys!

Detritus always finds its proper level.

You, sir, deserve an internet trophy for using “detritus” in a contextually-correct way. My hat is off for ye! ;)

And, yes, sh*t settles on the bottom until it gets stirred up, in which case the feculence can be so thick that dropping a white paper sideways onto the surface at high noon results in that paper being nigh-invisible within an inch of the water’s surface just a minute later (a reference to written reports on the state of the Thames river at the height of British industrialization, for those who don’t know).

Good one Z:

Especially IMHO the reference to the Thames!

When and only IF WE,,, in this case the ”investors” WE some how and some when manage to reach the level of information available, for instance, to JP Morgan,,, ‘back in his day’ WE will be able to invest with the same ‘panache’ and gusto that he did…

Meanwhile,,, With all the very clearly identified, these days, obfuscations from every where except Wolf,,, how can any reasonable person PROCEED???

Came on here majorly to try to ”invest” once again is something a bit more ”liquid” than the RE mkt that was SO good to and for me…

NOT GOING SO GOOD,,, SO FAR…

Thanks, many thanks, to commentariat on here following our GREAT Wolfster!!!!!

Exactly WHY I send $$$ to the Wolfster every time my budget allows…

I’ve always liked WAL. They have a lot going on there — leading with technology, focusing on higher value customers.

That said, a concentration of rich people can move onto the next bank more easily than a whole city of more normal folks people migrate from Wells Fargo to Chase.

I was very fond of this branch light, high quality service model. What I missed was that the customer can move more easily.

And some appear to have been. WAL though, has credit, liquidity and ideally earnings power going forward. Hopefully things settle for them and they keep moving forward. They have had great deposit growth, and generally that means somone loves them.

Accounting rules, pragmatically, require valuing your inventory at the lower of cost or market. This means you never get to claim fictitious profits.

So, banks which can value bonds at cost, even when current market is far less, are pretending there assets are greater than they really are.

Also, my understanding is, if Bond prices rise above your initial cost, which they had been doing for the past 30 years, you get to claim the increased price on your balance sheet . Is this true ?

When a bank acquires a debt security, it has to classify it into one of three categories:

1. Held-to-maturity debt securities

Held-to-maturity debt securities are reported at amortized cost. This is due to the securities being held to collect contractual cash flows. Held-to-maturity securities are subject to an ongoing impairment evaluation under ASC 326-20.

2. Available-for-sale debt securities

Debt securities classified as available for sale are reported at fair value and subject to impairment testing. Ignoring the impact of hedge accounting, other than impairment losses, unrealized gains and losses are reported, net of the related tax effect, in other comprehensive income (OCI). Upon sale, realized gains and losses are reported in net income.

3. Trading debt securities

Debt securities classified as trading are reported at fair value, with unrealized gains and losses recorded in net income each period.

kam

Currently Mkt to Mkt accounting standard is suspended.

If one has to realize profits/loss on any securities including Bonds/MBS you have to sell it at the current ‘market’ price. Or you can carry it to maturity (which Fed is doing)

Would you mind defining briefly what you mean by Free Money?

It’s an era, 2008 to 2021. My term. It causes a medical condition that turns brains to mush.

For banks specifically it means that they borrowed about $17 trillion from depositors at an interest rate of near 0%.

Almost one year’s GDP of the US. wow!!!

Luckily, many investors again found total security in crypto. Bitcoin + 15%

See your doctor about Consensual Hallucination, Carlos.

Bitcoin still -63% from peak.

“total security” LOL

Unsecured depositors at Silicon Valley Bank would have done better even without FDIC intervention. This crypto hype is just such a silly joke.

Hey, if you want to invest in crypto go right ahead. Just do so with the same mindset you’d use when investing in high-risk, high-yield instruments: Only use money you already plan on losing, have a long-term plan, and have more conservative investments that you can fall back on.

I know someone who took out a second-mortgage to buy Bitcoin years ago when it was at $18k, because he had allowed himself to be convinced by the hype-train that it was a rocket going to Mars, and a “sure thing” for making money easily. You can guess how that turned out.

I’d call him an idiot for using leverage to invest in a risky asset, but he was pretty much carbon-copying what many CEOs and hedge-fund types were doing, so…fools following greater fools, I suppose.

I see what you did there.

When I sit down at the poker table, I’m “investing.”

“…they borrowed about $17 trillion from depositors at an interest rate of near 0%.”

and Bernanke got the Nobel for engineering the game.

(But we still deal with the ramifications, the balls in the air and the plates spinning)

I think I will have to go and buy some bulk popcorn :)

Better hurry. The way things are going, with supply chain b.s. and all, that sh*t could get snatched up in a hurry and be the next toilet paper!

Cheap money is like fentanyl, impossible to shake off. A twenty-year habit, zero chance of rehabilitation.

…but what chance of an overdose?

Check out Wolf’s imploded list. Financial drug party with lost of overdose cases, followed by financial death. But the high was sooooo gooood!

Seems like there’s a collective “meh” in the market when it comes to reaction of all the banking development over the last week and the weekend.

You would think the 15th largest bank in the country being taken over would have some pretty major blowback on the market but much like everything else over the last couple of years and probably ever since easy money QT has rotted people’s brain forever…everything just seems to cause a mild shock and hopium surge all over again…just look at freaking bitcoin price for today…just nuts

Bitcoin banks and exchanges implode and Bitcoin prices go up 10% today?

WTF?

Bitcoin price is acting like Gold now. Gold went up the same today.

How are banks holding gold doing now? I have no idea. Are there any?

Bitcoin imploded last year and remains imploded.

Elon Musk, Mark Cuban and friends – the bailout boys – are pimping it hard – HARD – lately.

Wolf is an optimist.

I expect Bitcoin and everything else to drop down to 2019 prices.

Bitcoin was at 7200 at the end of 2019 before the pandemic.

It still has to fall another 60% to be rational. Oops. I don’t even think bitcoin is rational so it will fall further.

Bitcoin could have gotten a bump from crypto users swapping stable coins for Bitcoin. Crazy week when Bitcoin is the safe haven asset but that’s what it looks like there.

Easy rise easy fall tho. Hoping the same is true of bonds in the weeks to come

Yeah that USDC depeg seemed to raise some eyebrows and the hair on cryptobros’ necks until the SVB rescue was announced.

Completely fragile, volatile economy. Just the way traders who know how to ride the highs and lows like it. For the rest of us dumb money holders and savers who care about economic stability, it is an unwelcome financial thriller.

Also, many are naively talking about moving their money from smaller banks into the largest banks, which gambled the most and have exposure for swaps as the BIS reported in December, etc. The failed banks reportedly did not even participate in the riskiest gambling!

What would be wise would be spreading the money around banks to not have accounts for more than $250,000 per bank each. I naively also almost moved all my money to a smaller bank to avoid gambling of larger banks. Read about how FDIC members’ assets will be used first to bail out any failed banks –before the rules allow depositors to be “bailed in” and just get shares in insolvent banks. LOL.

Well the big bank will give you 80 cents / month for 50k in deposit.

I wouldn’t say the reaction was ‘meh’ – more like the reaction was ‘woo-hoo!’ Headline in the Globe and Mail today: ‘If you are buying a house, the collapse of SVB is the best news in years!’

Didn’t you hear, inflation is now over, the Fed has pivoted, long rates have already plunged and short rates will soon follow, and anyone who was so greedy or stupid that they can’t hold on until that happens in the next few months will be bailed out and the free money party will roll on. Get with the program!

Silicon Valley Bank had less than 1% of total US banking assets. What do you expect? It was a small very specialized cog in the vast financial machinery. And the cog has been replaced.

And yet it was so systematically important that they had to change the rules mid-game. How can it be so important but at the same time cause the Fed and the treasury to work all weekend? (Note: please hold off the flame thrower. I intend this as a request for clarification, not a disagreement.)

Until bad news causes the market to go down, Powell is losing the game. The market should go up with good news and go down with bad news. That’s what a functional system does.

Note to author! Please show me a bank that has a better track record of managing credit risk than First Republic. In the last decade, I would say that First Republic has the smallest loan losses of any mid to large bank in America. In addition, First Republic only does business with the wealthiest people in America. To say this bank is not conservatively managed is completely ridiculous. Just because this bank has offices in San Francisco doesn’t mean much. Maybe this author has some sort of political agenda or political bias?

This isn’t a problem with the quality of their loans. Don’t you ever ready ANYTHING.

This is a problem of interest-rate exposure, a huge risk for banks, that they were completely reckless with. And they had two years to prepare for it.

“In addition, First Republic only does business with the wealthiest people in America.”

I know exactly what he meant by this. Still, this line made me chuckle as my dumpy broke ass has a $200 6-month CD with First Republic.

First Republic Bank stock was up 35% this afternoon. Short cover rally?

The bond market is broken and BTFP is a band aid. I know this from following TIPs in the secondary market. Being priced at par is a big deal. The bond ETFs must be broken as well because their stock is constantly rotating. SVG probably wanted to trade out of their position but didn’t like the spreads. The Fed pulled the long end of the yield curve down, after these banks had taken positions. This is subtext to the markets insistence on a pivot. Now big banks are going to be taking deposits they were shunning a year or so ago (for this very reason). The last point liquidity is summed up by the description of W Alliance, 25B in reserves and growing, and 50% of deposits covered by (old) FDIC. And stock price is down. So they kept raising until something broke and certainly if startups can’t make payroll a lot of people will get laid off, and the Fed will have cooled down the labor market. Mission accomplished?

Hey Ambrose,

A very sophisticated analysis. Seems that the startups through bailout get all of their payroll. The mechanism for them getting snuffed out would be the overall economic toll this takes on the economy and their customers if the Fed raises until this thing breaks. As opposed to sealing off the damage, to a certain extent, by allowing these banks to go down and those over the 250K deposit limit realizing losses.

Seems like a kick the can, socialize the private losses and hoping the larger economy can take the brunt instead of those who were directly responsible for their losses. Having a bank comprised of start ups as customers seems like a poor biz plan.

It’s worth adding in this story, why there’s so much uninsured deposits at these banks specifically, is because of the incestuousness of the free money party.

Some ridiculous start up, and their VC founders would get really sweet deals and kickbacks on getting new businesses to start accounts there and take out loans. And because they were such unproven businesses, with almost no collateral, they had to keep minimum (uninsured) balances of several millions there to get their loan of several tens of millions.

They didn’t diversify their accounts to other banks and have insured deposits and decreased risk, because they were getting really good credit

deals for trying to add fresh meat at the bottom of their “multilevel marketing” scam.

This. And it’s not getting NEAR enough play in this story.

great post Christof.

your comment offers the other side to the “systemis risk” pro bailout crowd …..

You are using the term “consensual hallucination.” Maybe another term is “willful hallucination” because it has connotations of religious self-righteous proselytizing. They didn’t merely “consent” to the hallucination but “willfully” pushed and pursued it (as in all bubbles). Much like the term “willful ignorance” : meaning that they KNOW they are ignorant and are self righteous about remaining so. Over the last few years we have seen many examples of religious self righteous willful ignorance as well as hallucinations in almost all areas. In fact, the wilfulness has been off the charts. It is an indictment on humanity actually, when rationality is seen as the enemy. There is nowhere to go for such a civilization but to the scrap heap of history. Get out the popcorn.

Don’t worry, Taxpayers are there to help all these failing banks and rich clients. Scrw FDIC limits and all the rules.

As BTFP now prevents banks from facing a liquidity crisis, doesn’t this make it easier for the fed to keep hiking? I don’t understand why a pause is being predicted by some.

Yep. Bail out the rich and well-connected again. FDIC limits and rules are for the little people.

I’m such a little person I couldn’t even imagine exceeding the FDIC limit in cash.

I hope you are young, otherwise $250k cash savings these days is nothing.

Businessmen need to have enough working capital in an accessible way to pay employees, suppliers, etc., so many need more than that. I cannot believe how foolish bank executives were: buying long term bonds or treasuries or issuing many Los interest loans at times when interest rates were historically low and could only go up. When interest rates go up, the value of these goes down and banks now have minimal capital cushions.

Low interest loans not Los interest loans… Is my tablet’s auto spell checker drunk?

I am just a little person also.

However, my employer is a bigger person (Citizens United reinforced this) and holds their payroll for thousands of loyal employees in a bank. This payroll far exceeds 250K. These employees expect a paycheck or they may go without food or be evicted. If the limit for corporate payroll is held to 250K max (ie 100 people with a 2500 paycheck), many wouldn’t get paychecks and this would ripple through the entire economy.

I don’t have a 250K bank account but I do have at least a $2500 paycheck. I can’t lose it and still pay my bills due to my company picking the wrong bank for their payroll.

The FDIC decision was good for this instance.

The banking sector earthquake started on Mar 6, including the primary banks. For some regional banks even before.

Today might be the most critical day, on high vol. The aftershock will cont for a while. The banking system might infect other sectors, for fun and entertainment. The symptoms might come later on.

Outstanding PBS interview from 2013 on YouTube. Look for the full 33 minute version:

David Stockman on Crony Capitalism – Bill Moyers & Company

The Canadian politician turned housing bear and wealth manager wrote that there’s nothing to worry about and stonk and boom prices will eventually go to the moon.

How it’s no Lehman Bros moment. Nothing to see here lol

I think this is going to be a collapse of lots of regional banks, letting investors take some of the hit on their assets, all the non too big to fail players.

The winner will be the Treasury as more money is being deposit directly due to the banks 0.2 yields for savings.

Big banks won’t purchase these regional banks as the physical branches are not essentials in the 2020s, online banks that provide high rates for saving on the 2% minus what the get from the Fed will be winners if trust is re-established and the FDIC threshold given enough market scariness is increased to 500k or 1mil.

Following the “don’t let a crisis go to waste” this is the best opportunity to tamper the full out bond crisis that would’ve ensued in time if not measures were taken. The Fed will increase the smallish 25pct points and the market won’t crash.

At a high-level the loser in these continues to be Europe subsidizing US Oil/Gas and the working-class that soon will have to work longer hours for similar pay.

I think I read somewhere in the past that the customer acquisition cost for a bank is like $1000 per customer. Maybe I am off, but my point is that regional banks still have value if they can be taken over before depositors all run.

OK, if I was in charge for the next time, my rules for regulators would be to investigate any 4X stock increase for supposedly stable banks.

Sigh…. I am not in charge of anything but I stayed at a Holiday Inn Express last night and my rear-view mirror works.

Wolf, I have a PSQ (Potentially Stupid Question), but what is the mechanism for a company to pull millions of dollars out of a bank? Does the company simply transfer funds to another, safer bank? If so, why wasn’t the money there in the first place? I can’t imagine chasing yield is the motivating factor, i.e., if a company is so concerned about deposit interest, they should be at least buying short term T-bills or something instead, right?

I do really hope at least one company sent in an intern with a duffle bag.

TEMPLE

1. online or wire, ACH, various other methods

2. Yes (big ones), and to Treasury bills, and to money market funds, etc. anything but a regional bank.

3. because free money turned their brains to mush.

4. yes, but they couldn’t because their brains had turned to mush. And/or because their loan agreement with that bank wouldn’t allow them to.

Thanks Wolf. It just blows my mind how out-of-touch the risk management teams must have been in dealing with all this. Also shocking to me is that in avoiding a relatively tiny loss on decent quality and easily sold assets, these banks totally misread the room and hung on until it all dragged them under. Fascinating stuff. The psychology seems to be identical in residential real estate.

Thanks again!

TEMPLE

TBH it could be that a lot of great minds left the business during COVID to retire. Some had an inkling that the current generation in power are followers. Once one dodo bird clipped its wings and jumped, all other followed. Now the small generation between Baby Boomers and Generation Y, well we are crushed under all those dodo birds. Do you think we will ever see maturity in the markets again?

I wonder how many current bank managers have been through a real Fed hiking cycle.

Great article – thank you for taking the time to research these ‘banks’. Sight must not be lost of the fact that banks can hold 100% cash for the liquid asset requirements. The Fed allowing these banks to tender the illiquid as collateral for cash under its new facility isn’t great as we are now underwriting their folly. However, the world is seldom black and white and at least equity holders as well as the subordinated debt holders are written off. Something which will resonate in these share prices and those similar banks for years to come.

A panic among millionaires isn’t new. From a 1904 book on Trusts:

The panic produced by the double threat of the Carnegies to build a rival tube works and to enter into competition with the great Pennsylvania Railroad has been graphically described by a recent magazine writer: “Either project as a threat would have been alarming. The two together as imminent and assured accomplishments, produced a panic. And a panic among millionaires, while hard to produce is, when once under way, just as much of a panic as is a panic among geese. They ran this way and that; they hid one behind another; they filled the newspapers with their squawkings; they reproached, implored, accused each other. At last they ran to their master Morgan. And he negotiated with Carnegie.”

Still filling the newspapers with squawkings, still running to Master Morgan 120 years later!

A million bucks was huge money in 1904. It isn’t much now.

It’s also worth a lot less than indicated by changes in the CPI to actually wealthy people because the inflation in expensive luxuries and asset prices has increased a lot more than the average.

This free money era saw unemployed young men buying and trading Rolex watches and driving Hellcats. You can’t make this sh!t up. They were getting roughly $3,600 net per month after taxes, more money than they had ever earned in their lives, and they leveraged it.

On December 18 & 19, 1912, the year before the Fed was born, J. P. Morgan testified before Congress. It is an amazing public document, and Mr. Morgan’s words and answers to being questioned by Samuel Untermyer are worth looking at, I would say.

The issue of the railroads and bond offerings from them is central to his testimony. “Nobody wants to put money into a new railroad in these times.”

His trademark line, “Gold is money, and nothing else.”, was stated then.

“The first thing is character, before money or property or anything else.”

The last line was clearly not adhered to by SVB. Ask the CFO, Joseph Gentile about it, eh? Oh, and ask Chief Risk Officer Kim Olson too, please.

JP Morgan also supposedly said – I don’t care who prints the money, I need the control of the CREDIT

‘Cannot Control Credit’

Q. How about credit?

A. In credit also.

Q. Personal to whom–to the man who controls?

A. No, no. He never has it. He cannot buy it. All the money in Christendom and all the banks in Christendom cannot control it.

Q. And you say that so far as the control of credit is concerned they cannot do the same thing.

A. Of money, no. They cannot control it.

That’s from a Q & A on control of railroads’ management, financing and business power of pricing. (page 27 of Library of Congress document)

Wolf has stated that his website is not about history. But history does repeat itself. SVB had so much power over Venture Capital and Tech IPOs that it does remind one of Morgan’s power over industry in the USA 100 plus years ago.

Morgan was quite skilled at how he and his companies operated. His basic philosophy was simple and straightforward.

DanRo-begs a question of our times: “…is it better to HAVE ‘character’, or BE a ‘character’?…”.

may we all find a better day.

Wolf, I have a high yield savings at Western Alliance Bank…should I move my money? I’m nowhere near the FDIC maximum.

Thanks for your awesome insight!

If you’re below the $250k limit, you’re fine. People need to stop panicking if they’re within FDIC limits.

Ain’t going to happen, Wolf, after the bad taste Americans still have from the 2008 Great Recession. To assume the Government regulators have either the intent or the capability to fairly and efficiently deal with a crisis that they themselves created by a 90% surety, is a giant leap of faith that they will not risk at this shaky juncture. Ain’t going to be a one-day affair either, took us a dozen years to get into this mess.

Sooooooo they need to panic if they’re above the FDIC limit? ;-)

If all banks can borrow against their money-good assets, I’d think no one should be panicking.

With the Fed backstop to prevent a bank run all I see is a screaming good deal.

if the fed does pause Wall Street will celebrate the “pivot”. Pausing is not pivoting dear ones!

A pause would for sure be a pivot.

I would be shocked if this takes place tho.

Curious that something finally does “break” when the Fed is considering being more aggressive again with rates. As if this is a hail Mary from the elite to pressure the Fed into a pause.

In less conspiracy theory thoughts though, as of right now, this is a blip on the higher for longer rate path and I expect that to be confirmed over the next couple weeks

I don’t think that’s a conspiracy theory at all. Some prominent people (Thiel, Dimon) publically advised companies to pull money out of SVB last week, cementing the panic. Who does that!! Those who want something to break.

My employer banks with a solidly run regional, been with them for decades. Down 30% this week as the baby goes out with the bathwater. Going to study their financials tonight, might be time to BTFD.

Yes, I would not be surprised at all if wall steet took SVB, which apparently loans to a bunch of Chinese fintech startups, out back and shot it. So it goes. And the street will do it again and again until they get their way. Ruthless.

From what I’ve read, the Fed is lending against collateral valued at PAR, and bonds are rallying, so maybe people know that the Fed will pivot soon? No doubt Wolf will tell me that no, the Fed will not do that, but lending at PAR is already troublesome and if the Fed continues to increase interest rates afterward, well those collateral will drop in value and in the near future we’ll be faced with the same issue again, especially if the banks were to use the cash they received from the Fed to …. buy even more long dated bonds.

“why should shares of a bank quadruple every four years?”

There are so many latent overvaluation disasters baked in by 20 years of ZIRP that it is endlessly depressing…but here is another variation…

One reason why intrinsically slow growth companies get hugely overvalued is because (sadly) they get included in *indexes* which bring ZIRP driven overvaluation to many more stocks.

(Indexing is good – cheap diversification and tax efficiency…but in ZIRP everything bubbles, they become disease vectors for overvaluation. If you “qualify” for an index, some share that index’s ZIRP overvaluation gets conveyed to you…automatically.)

So even slow growth companies get driven over the cliffs…because it is an *everything bubble* where *everything* is correlated to artificially strangled interest rates.

The Fed must have realized this 20 years ago…but they had only really one tool and if drew oceans of blood…so be it.

For 20 years of madness.

WAL &FRC monthly : a huge buying tail. Give them a chance til Mar 31.

David Stockman:

They have done it again, and in a way that makes a flaming mockery of both honest market economics and the so-called rule of law. In effect, the triumvirate of fools at the Fed, Treasury and FDIC have essentially guaranteed $9 trillion of uninsured bank deposits with no legislative mandate and no capital…

As long as they’re letting banks fail, as stockholders and bondholders lose 100%, while executives get fired, clawed-back, and indicted, I’m OK-ish with it. I HATE it when they bail out investors AND enrich investors on the pretext of bailing out depositors, as they did last time. That was heinous. Stockman must have forgotten.

Not me.

More (supposedly) unintended consequences. Like where creating one distortion (a category of TBTF banks) now leads to another one where if these emergency measures weren’t taken, all below TBTF banks are supposedly at risk of failing.

This isn’t isolated either. It’s par for the course, including the conflict of interest you profiled recently with garbage credit ratings. That was mostly or entirely the result of government designating “approved” rating agencies in 1974 (or near it).

One of these days, there is going to be a run on the entire financial system or the USD as global reserve currency and everyone will be calling it a “black swan” when it’s entirely predictable.

It supposedly never matters or can’t happen, until the future arrives and those living in the present have to pay for the “can kicking” of the past.

So many “can never happen” things have happened in last 20 years (frequently as direct result of attempt to cover up first stages of “impossible” things actually happening).

The leadership of the US has been horrifically awful for 50+ years…feeding off an economy they fundamentally (*fundamentally*) had no understanding of, all for little more than to corruptly buy themselves a little more political or economic power.

They deserve to end like Hitler in the bunker – but they have consigned present/future generations in the US to suffer in their place.

Plenty of warnings at the time – all ignored.

my observation is – if this bank were named – Oil Valley Bank and was located in dallas would this administration made all the oil/gas millionaires/billionaires whole ?

Wolf, I should be hired to run a bank, accept billions of depositor money, institute bad bank management practices and get paid a million versus struggling to build a basket of assets so I can retire one day. I’ll do it for only $1M and save the taxpayers money but taking a modest salary comparatively speaking to accept a bailout.

I think the FDIC must legally cover ALL deposits going forward regardless of size, and regardless of what the powers that be say regarding this to be temporary.

This move on SVB to cover them all is HUGE and reckless. I dont think they have any idea the magnitude of what they just did.

What happens if they can’t cover them “ALL?”

I will guess what is going to happen, which is always going to be somewhat wrong. We are done with rate hikes other than one more maybe so Powell doesn’t eat crow.

The economy is going to start falling apart pretty fast now as the policy has started to cause the problems with a lag. The crooks,shysters and incompetent are being found out as financial stress starts to kick in. As Buffet says the number one job of a CEO is to be a risk manager and we will find out who didn’t do it.

Today was a big day. The banking system is different than it was on Friday. Doing away with the 250K cap is a big deal. In mark to market Fed is down $1T, the banking system is down $1T, fiscal policy is adding $2 T per year and you have nervous deposits. Someone called me today considering taking out $10 grand in cash to keep under their mattress.

My opinion is Powell had to bluff all the way til something broke to see how high he could get rates and the high is in on 2 year and longer. Give me til June before you throw me under the bus.

What’s funny to me is how one rotting branch on a healthy tree is considered the entire system “breaking.” The hysteria is just too much. Billionaires are throwing a tantrum because their free money is gone.

Depth Charge

There are nearly 620 Billions in unrecognized loss in the Banks, the largest which apparently at 110 Billions. I don’t know what is lurking under opaque derivatives/interest swap market.

Under our fractional banking, the collateral for the 18 Trillions money in circulation is about 1.8 Trillion. This functions as long as there is confidence in the system.

SVB failure showed how that confidence vaporizes once the bank run takes over.

We don’t how many like SVB out there until tides go down ( as the interest rate increases!)

There isn’t 18T in money circulating. If you are referring to one of the monetary measures, it’s mostly someone else’s debt.

That’s what most “money” actually is in fractional reserve banking. “Deposits” aren’t actually deposits. It’s an unsecured loan to the bank.

“Systemic risk” is the excuse used by the regulators to bail out SVC and Signature. Their combined assets were $300 billion or so, not likely a big threat to the $23 trillion US banking industry. If their collapse would cause systemic risk, then the entire banking system must be teetering on the edge. I don’t think that. The regulators needed some excuse to bail out their wealthy and politically-connected friends, as trite as that sounds.

The regulators have unleashed moral hazard, “a situation in which one party engages in risky behavior or fails to act in good faith because it knows the other party bears the economic consequences of their behavior”-investopedia. That other party is you and me.

The February CPI release tomorrow morning is going to be interesting. Thanks to these bank runs, the pivot narrative has returned with a vengeance. If the monthly CPI change is at or below expectations (0.4% headline, 0.4% core), you have to imagine that treasury and MBS rates will continue their collapse of the last two days.

We desperately need a higher than expected inflation report tomorrow to arrest these falling yields and counter these pivot pushers. Otherwise, the job is going to be left to J-Pow next week, and I’m not optimistic he’s capable of wielding a big stick.

so you are insisting on a narrative?

i think it’s incorrect to desperately need anything. let the chips fall where they may.

If you’re rooting for higher rates and lower assets prices then yeah I’d say LFG lol.

If you’re trading then yeah chips falling yadda yadda

The Federal Reserve FOMC (Federal Open Market Committee) makes those decisions and is a 12 member committee of which Jerome Powell is one of those 12 members and all decisions are reached by consensus vote.

There’s only one FOMC member standing at the podium answering questions after their statement is released. That’s what I’m referring to.

Expectation is FED will continue with 25bps rate hike at next meeting.

They may go to a .50 or ,75 increase by will increase by at least .25.

So, has anyone asked when Peter Thiel shorted SVB shares – before or after his “fun for the hills” tweet?

Really good and appropriate question IMHO DrJ !!!

The situation with SVB looks very much as though someone ”manipulated” the Thursday RUN to be able to influence the FRB and the GUV MINT.

At this time, that manipulation certainly seems to be clearly successful.

Time will tell us more, no doubt.

Two or 3 threads back I was calling for Bill Ackman to be arrested on domestic terrorism charges. These billionaires are inciting panic to financially benefit.

Awesome articles and excellent back and forth on this recent issue! Really awesome!

My perhaps ignorant observation is.

Mark to market or par value on the lower interest long term treasury story.

Joe Bank buys $1000 of 30 year treasury at 1%.

I deposit my money into Joe Bank.

A year or two later the same 30Y bond is 3%.

But, a 3 month bill is 4.5%.

There is really no loss on that initial 30 year bond at 1%. The $1000 is worth $1010.

So why the loss hype. I as the depositor want this $1000 money back. Joe Bank gave he/she/they .01% and earned 1%.

The bank was to earn 99% on the .01% deposit yield ripoff.

The depositor then withdraws the money – yet the $1000 should still be still worth $1000. No loss.

Where is the value lost?

When banks are forced to liquidate their bonds before maturity, they can take a loss on the bond if interest rates have risen substantially. Banks are forced to liquidate their bonds when depositors withdraw their funds rapidly.

I am sure there are plenty of financial techniques for managing this risk, but it would eat up some of the profits of the bank, so some of these banks were just betting that there would not be significant investor withdrawls.

It is worth noting that the Fed currently has a massive unrealized loss due to buying Treasuries much higher than the current market price. But the Fed cannot be forced to liquidate any faster than those bonds mature, so they can just sit on that unrealized loss while they liquidate the bonds.

If we did go into hyperinflation, like in the 70’s and the Fed was forced to fight this with much higher interest rates, it could get to be a much bigger and broader problem.

Gary Yary,

As gametv points out, the problem is this:

100 Garys put each $10 into Joe Bank in 2020 who then invests this $1,000 in a 30-year Treasury bond to earn 1.5% and he pays each Gary 0.1% in interest and makes a lot of money on the spread. Then in 2023, the 100 Garys get sick and tired of getting screwed by 0.1% interest and yank their money out — a “run on the bank.” Joe Bank now has to sell the 30-year Treasury to come up with the $1,000 cash to pay all the Garys back. So he sells the bond, but because the 30-year yield is now 4%, the price of the bond is a lot lower, to produce a 4% yield to maturity. Just guessing here, $800. So now Joe Bank has $800, and is $200 short of what he owes his depositors. And so he is insolvent. And the bank collapses.

In this great example how would the new program help? How would the FDIC program be applied?

FDIC shows up at Joe Bank Friday evening, shuts it down, takes possession of everything in it, and renames it Jerry Bank. It then moves $1,000 from its fund, that it accumulated from FDIC-insured bank contributions, to Jerry Bank and makes the funds available for the 100 Garys. On Monday morning, it tells the 100 Garys that their $10 is in their accounts, but that the name of the bank has changed to Jerry Bank, and that they can withdraw it at any time. The FDIC then sells the 30-year bond and gets $800 for it. So the FDIC paid $1,000 and got $800, so it has a loss of $200, which comes out of its fund that it accumulated from the contributions from the FDIC insured banks. If the $200 exceeds the fund, it levies a special assessment on the banks to make up for the $200. Taxpayers don’t ever get involved.

@Wolf,

Your ability to explain these concepts is unparalleled. Please accept my compliments.

Actually for our Wolfster:

Seems to me that sooner and later the ”banksters” will do what is needed to make sure the retail depositors WILL PAY for the failures of the banks.

Certainly happened to mom who shoulda been at least a millionaire if not billionaire when her dad died,,, EXCEPT the bank, with total responsibility for the estate, had put his billions into PENN CENTRAL.

Banks need to be held to account, far damn shore.

Excellent example of the effect of duration risk. SVB didn’t hedge its duration risk on its debt securities portfolio (by buying interest rate swaps it could have); why not? Pennywise but pound foolish I guess.

Note that if the world has $300 trillion of debt (more than that actually) with an average duration of about seven years (a guess) with a 2% yield at par (a guess), interest rates going to 4% mean a mark to market loss of $42 trillion. JPM will be hedged against duration risk; fools at many US banks (like SVB) and foreign banks will not. This is the risk that the world (and the Fed) are waking up to. This might be worth its own article because duration risk escapes even supposedly well-informed investors (e.g., SVB’s risk management department).

Wolf,

I stole these two comments of yours to use on FB, so that I could explain to my less-informed friends and family what this is all about, in simple terms. Please don’t sue me…you have an ability to truncate the complex far better than I do!

Make sure to cite the infamous WOLFSTREET.com as the source, and add something like: “you gotta read the comments, dude.”

Oh, I included a link to this post directly and attributed the source material; one may take the history teacher out of the classroom, but never out of the person themselves. It isn’t the first time I’ve posted a link to your articles, but I doubt even half my FB peeps could follow your posts, regardless of how well you break things down for consumption….

THANK YOU!!

“The FDIC then sells the 30-year bond and gets $800 for it. So the FDIC paid $1,000 and got $800, so it has a loss of $200, which comes out of its fund that it accumulated from the contributions from the FDIC insured banks.”

Why wouldn’t/couldn’t the FDIC hold the bond to maturity, and receive $1000 (and also collect the coupons along the way)?

What we just found out is that billionaires were reckless assholes, ignoring FDIC insurance limits and just YOLOing the shit out of life as if the good times would never end.

And what ticks me off to no end, as a peasant in the billionaires’ cosmos, is being made the insurance backstop for them, after the fact. Yes, the losses are dispersed, into a slow bleed of my otherwise-expected wealth. I guess I just lacked the arrogance and antisocial personality to play that game.

What we JUST found out? LOL

So, readership, place your bets on the March 22nd meeting.

(A) No rate increase.

(B) +25bps

(C) +50 bps

(D) Rate decrease.

We live in interesting times.

25 basis points.

B… With higher terminal and higher longer term rate projections

Ditto, + a sentence or two added to the FOMC meeting statement on how resilient the banking system is but that they will continue to monitor the situation and take appropriate action as necessary

Would love to see (C) +50 bps.

But you know this lot doesn’t have the nerve. Look at their instant backstopping frenzy, at the least sign of inconvenience for their juiced-in pals. I am starting to sound like Depth Charge because I have been mugged by reality.

Sop we will get persistent inflation AND elite bailouts.

That’s my vote too.

B

New Dot Plot higher for longer

25 basis points

(B)

D – 50bps cut

I expect the worst because that’s usually what they do.

I vote B) with hawkish outlook, as others have said.

I just hope Powell doesn’t try to get away with A) with hawkish rhetoric. The market is so ready for the magic pivot it’ll probably treat A like D even if Powell barks at the camera and sets fire to the podium.

I’m going with (A)- no rate increase, and hope I am wrong and it is at least (B) and hopefully (C). But I can’t discount (D) in this present environment- the political pressure to lower rates has got to be enormous right now, right to threats to fire him if necessary.

Powell should have been fired long ago. Every day he is on the job is a day too long. If they replace him with an even more reckless person, then that person should die on their sword for the damage they do. It’s time for these people to pay the piper for their sins, and they know it.

Do you want Bernanke back, LOL?

Stay the course, keep raising. Inflation hasn’t gone anywhere. Inflation must be cracked.

The higher the FED raises, the more room they have in the future to cut; just never go near zero again for any reason.

Zero Rates and Free money

How they got away with that for so long. Guess I am just an old fool after all. Glad it finally caught up with them.

Never heard of these two banks until reading this. No media coverage?

Well, they’re regional banks. So if you live in Texas, you might not know of them.

HSBC snaps up UK arm of failed lender Silicon Valley Bank for just $1.20 in bid to prevent tech sector collapse

“snaps up” is the wrong expression. They agreed to take all the deposits — a liability, the amount OWED to depositors. In return, they got some assets, of about the same value as the liability of the deposits.

Well, however you want to characterize that deal, you must say that they likely didn’t overpay at the $1.20 price for the whole SVB UK operations. Heck, I would have agreed to pay at least $1.50. They should have put it up for auction! It might have gone for more than $2.00!

HSBC is also investing $2.1 billion (BILLION) of its own money into the acquired SVB bank for liquidity and capital. So you need to add that to the cost for HSBC of acquiring the bank. This was worked out with regulators before the deal was approved.

So the Fed has guaranteed all bank deposits at all banks from here on out obviating FDIC and SIPC limits. They can’t afford to look arbitrary and change it in the future.

American capitalist exceptionalism. #1 #1 #1…(and then he rode into the sunset…)

Well it is a confidence game, so the Fed is hoping that people see that deposits won’t be at risk, and therefore don’t cause runs on banks, thereby necessitating any kind of action. So, in essence, an implicit guarantee as long as the masses don’t panic.

Noh

Agree. Legally I think they have jumped the shark.

They MUST cover all going forward despite the coloring this as temporary. And the ramifications and scope of what they just did, never before done in our history, is worthy of much more attention.

No, the Federal Reserve has done no such thing. All they have agreed to do is to LOAN up to PAR value for some US Treasuries which are taken by the Federal Reserve as COLLATERAL against such loans for up to 1 YEAR at these two particular specified banks.

Maybe this crisis will blow over, technicalities are not too important.

The plain fact is that a relatively small, unknown bank can cause a crisis that ripples through the financial system like it was 2009 again. That’s the result of runaway printing, desperate yield seeking, and bubble, bubbles, bubbles.

My legal U.S. address is in Oregon, and I used to bank with supposedly “conservative” Umqua Bank, a northwest regional bank. I had some shares (UMPQ) in it but dumped them about a year ago (out of general disgust for banks ripping off retail customers).

I noticed that UMPQ was steadily going downhill in the last six months or so, and was surprised when they officially merged with Columbia Bank on April 1.

Columbia Bank stock (COLB) started tanking around February, and is now down around 58% from its peak three years ago. Same problems?

They all have the same problem. Some banks hedged their interest rate risk. All banks SHOULD have hedged their interest rate risk. Others moved their balance sheet in some aspects to be less exposed. And that’s good. But they all have the same issue.