Inflation Horror Show. The Fed has got a problem on its hands.

By Wolf Richter for WOLF STREET.

The Fed pays particular attention to the Personal Consumption Expenditures (PCE) price index. The “Core PCE” price index (which excludes the volatile food and energy components) is its measuring stick for the 2% inflation target. Powell has been pointing at the services components of the PCE price index as a hotbed of inflation. And the PCE price index for January, released today by the Bureau of Economic Analysis, was a horror show on all counts.

Not only did all the relevant measures get a lot worse in January, but the prior three months, October through December, were revised higher – much like the CPI inflation readings a couple of weeks ago – showing substantially greater inflation momentum at the end of the year than originally shown. The whole thing throws a lot of cold water on the “disinflation” hoopla.

Inflation rages in services.

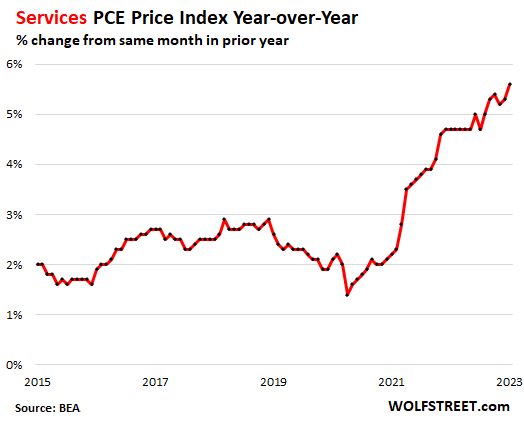

On a year-over-year basis, the PCE Price Index for services spiked by 5.6%, the worst since 1984. December, November, and October were all revised up sharply. This is where inflation is running hot, and services is nearly two-thirds of consumer spending. This is where the inflation action now is, where it’s entrenched and self-propagating:

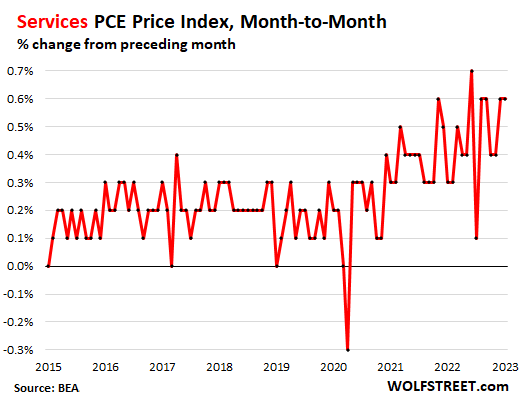

On a month-to-month basis, the PCE price index for services jumped by 0.6% in January from December. December was upwardly revised to +0.6% from +0.5%. There is just absolutely no slowdown in sight. This is the center of the horror show:

The Core PCE price index turned red-hot again.

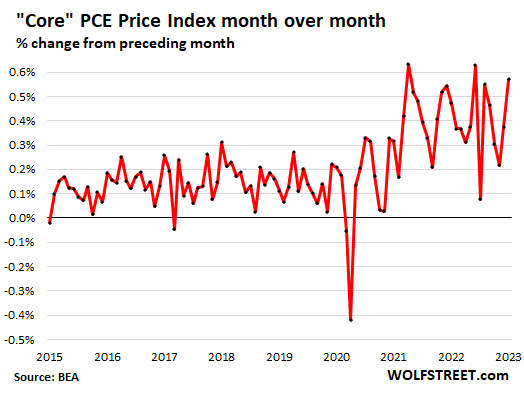

On a month-to-month basis, the core PCE, which excludes food and energy, jumped by 0.6% in January from December, after having jumped by an upwardly revised 0.4% in December. This jump was largely driven by red-hot inflation in services. But this time, goods prices rose too, after having declined in prior months.

The month-to-month down-trend in October and November was just a classic inflation head fake:

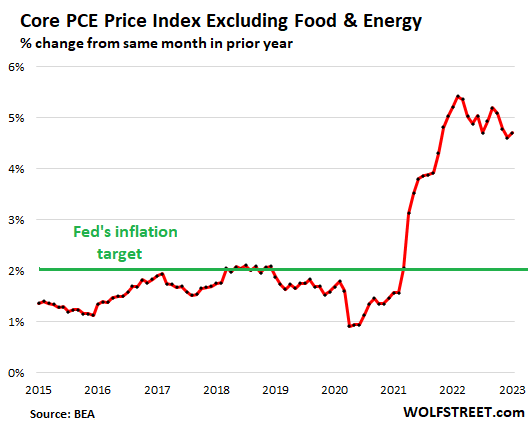

On a year-over-year basis, core PCE jumped by 4.7%, up from 4.6% in December, which was revised up from the original +4.4%. November was also revised up to +4.8%, from originally +4.7%.

And goods prices are rising again!

In the second half of last year, prices of goods declined, driven by the plunge in gasoline prices and other energy prices and by the decline in prices of used vehicles, electronics, and other durable goods.

But in January, this ended as consumers went out and splurged – we have already seen this in retail sales reported by retailers, where people demonstrated that they’re in no mood for any kind of landing.

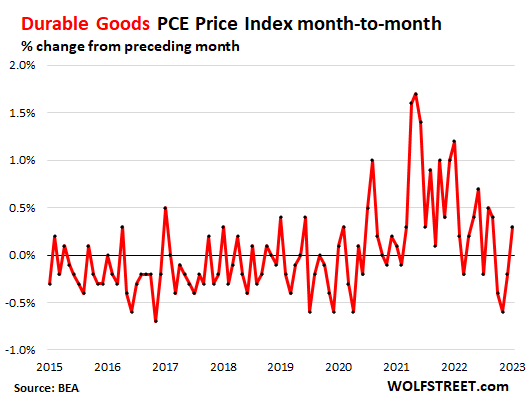

The PCE price index for durable goods – new and used vehicles, appliances, furniture, etc. – rose by 0.3% in January from December, after having been negative for three months in a row, and having been negative for five of the past 10 months.

This increase removed downward pressure on the Core PCE price index and on the overall PCE price index:

The PCE price index for energy, which had plunged on a month-to-month basis in the second half last year, jumped by 2.0% in January from December.

The PCE price index for food was heavily revised upward for the last three months of the year. In January, it rose by 0.4% from December.

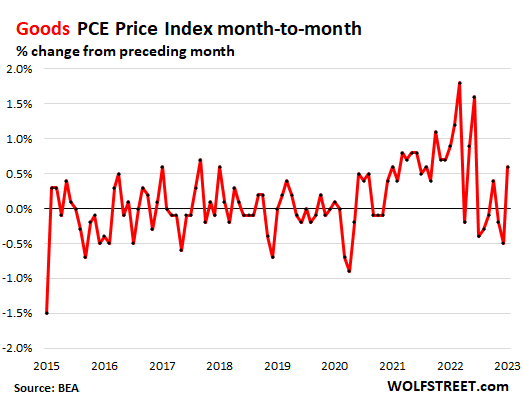

The PCE price index for all goods (durable and nondurable) jumped by 0.6% in January from December, a sudden turnaround.

Goods prices had been the force that had pushed down on inflation, while services pushed up inflation. But what we’re now seeing is that goods prices are rising again, and they no longer push down on inflation, and services are pushing up inflation unopposed:

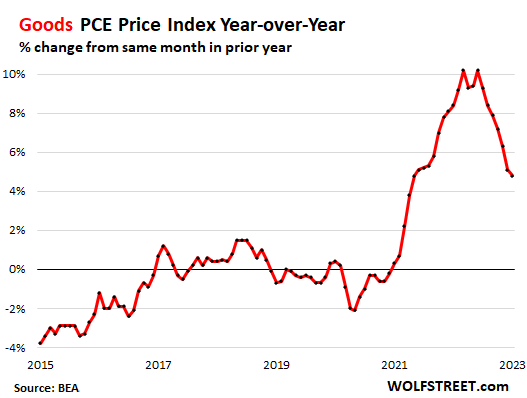

On a year-over-year basis, the PCE price index for all goods increased by 4.8%, down from the December pace of 5.1% (originally +4.6%).

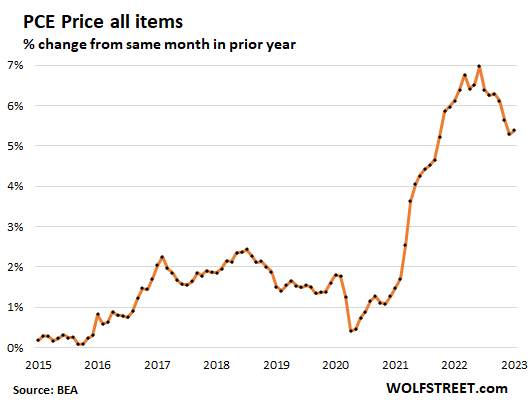

The overall PCE price index for all items jumped by 0.6% in January from December, the worst increase since May last year. On a year-over-year basis, the index jumped by 5.4%:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Hi Wolf, doesn’t the Fed really want 4-6% Inflation so as to clear the mess of debts within the Economy that they helped create? Is this wild inflation situation either incompetence or by design ?

It really wants 2% core PCE. That tends to be 3-4% overall CPI. So that’s close to the range you indicate.

The problem with a higher target is that inflation goes out of whack very easily, and then it’s tough to reel in, and everyone knows this, including the Fed.

This is a balancing act. High inflation can blow everything apart — see the economy of Turkey and Argentina. The Fed doesn’t see it as its job to blow everything apart.

I arrived in Istanbul in 2002 and caught a taxi from the airport to town and it cost me 25 million lira, which freaked me out a bit, but it was only $25 or so.

An Argentine peso was worth 1 American $ around the turn of the century, now worth 1/200th of a buck.

I was in argentina for 6 months in 2017 and 1/23 dollar : peso and now 1/200 so agree completely

Argentina is a great country. I mean — look how good they are at soccer. They are a good role model for America.

Man, I am dissin’ inflation every chance I get. If I do that enough I will cause disinflation. Who caused all this inflation anyway? What an idiot…

Remain to be seen how good at FED under Pow Pow will be at not blowing everything apart…one thing for sure, they are very good at blowing bubbles bigger and bigger. A track record that’s been consistently upheld by every FED chair since Vulture Greenspan. Pow Pow still takes the cake though..$800B TARP? pssh…hold my beer, I’ll show you what real QE looks like, we’re only interested in nomination with a T instead…

“…will be at not blowing everything apart…”

TBH, they got pretty close to “blowing everything apart” already with their QE and interest rate repression. And I think they are now seeing just how close they got.

A Tin Pan Alley jazz song from 1919.

I’m for ever blowing bubbles

Pretty bubbles in the air

They fly so high

Nearly reach the sky

Then like my dreams

They fade and die

Fortunes always hiding

I’ve looked everywhere

I’m for ever blowing bubbles

Pretty bubbles in the air.

I hate how rational Wolf can be, sometimes we want to Confo-Bias to infinity!

I am scared. I just went to Aldi in the SE of USA and they had the largest price increase yet. I go there every week, sometimes more than once per week, I know the price of most goods. I am still in shock. Looking back to 2019, prives at Aldi went up by 200%. My salary did not go up 200%, but 2%.

Everything the Fed does and says is a lie. People are being screwed left and right, no optimism for the future.

I’m scared, too.

Scared…

Me too. Not just inflation. I also live in SE and have been an Aldi shopper forever now. But I’m more scared cause…

We have a justice system that is a joke for the average American. Last night in Orlando, a dude killed three people, shot another two. No big deal. 19 years old with a rap sheet a mile long. Killed a 9 year old girl who was just in wrong place at wrong time, I guess.

We’re paying for a war in Europe with no congressional approval. “Here’s some money we don’t have guys, do whatever you feel needed.”

Hey China, we love cheap stuff, so go ahead and make everything for us, btw here’s all our technology- feel free to steal most of it. Those islands you built in the SCS, yeah… we can discuss that later after we get done pumping our chests about popping your balloons.

Wanna comes to America?… border is open. Where you from?… Beirut? How’d you get here?… oh well, come on in. There’s work for you at the local country club. Oh, you brought Fentanyl?… that’s fine. We don’t care about Appalachia, Skid Row, or Seattle anymore.

Oh, you went to school and took out a loan to study dog fecal matter and can’t find a job? Don’t worry, we got you covered on that loan.

We have a two party system that is a complete joke. Absolutely completely ridiculous. One side- better mask up when jogging outdoors through Grand Tetons. The other side- better arm yourself like you are your own personal army with bazookas and grenades because damnit, it’s the American way.

So, yeah, this inflation is scary. And it rightfully pisses off the savers, the prudent, the economically wise who see their hard work and sacrifices wasted. Makes one feel like an absolute chump.

But, I’m more worried about the other stuff first. For what it’s worth.

The careless & reckless may be more stupid than the fearful, but both are foolish.

While federal government is cutting food stamps drastically

Thank you for that explanation. I was confused about this.

So, if they adjust there target higher will inflation get out of control? There is speak on the street that they are capitulating.

Federal Reserve’s FAQ:

Why does the Federal Reserve aim for inflation of 2 percent over the longer run?

The Federal Open Market Committee (FOMC) judges that inflation of 2 percent over the longer run, as measured by the annual change in the price index for personal consumption expenditures, is most consistent with the Federal Reserve’s mandate for maximum employment and price stability.

The Fed’s inflation target comes from a casual remark on New Zealand TV

Quartz Magazine

June 23, 2021

At least since 1996, the US Federal Reserve has used monetary policy with the aim of keeping inflation at 2%—a number that Ben Bernanke, the former Fed chair, made an explicit policy target in 2012. And it isn’t the only central bank in the developed world to shoot for 2%.

But why did these banks uniformly gravitate to the 2% figure? And where did that number come from?

From New Zealand, it turns out: specifically, from a finance minister who was put on the spot during a TV interview in 1988.

They will get it. A little manipulation of the math will get them there, just like always if inflation won’t come down manipulate the math. They are re-weighting the numbers right now.

Duh,

I hate this ignorant conspiracy BS. To crush your ignorant conspiracy BS in advance, I wrote an entire article, including charts, about the weights and comparing them over time. The new weights made CPI worse, Duh. REAT THIS:

https://wolfstreet.com/2023/02/21/how-the-cpi-weights-changed-and-moved-cpi-meet-the-surprises/

I give you extra credit for the excellent choice of your screen name.

For example:

“Rent of Shelter” (housing costs) is the biggest CPI category. The weight was increased from 32.05% in November 2021 to 34.04% in January 2023.

But the CPI for “rent of shelter” spiked by a red-hot +0.8% month-to-month in January and by 8.0% year-over-year, and the higher weight made CPI even worse:

Wolf, I’m writing as a PhD economist who, after working on trade and industry issues for thirty years for the World Bank in countries with inflation as high as 24,000% p.a. (Bolivia) and 8,000% (Ukraine), feel very strongly about inflation here in America. Never want to see us go down the hyperinflation path. Yes, we have the Federal Reserve to fight inflation, but the way it does it, nine times out of ten, we get a recession.

In light of the above, I’ve developed a policy proposal called FIRE – Fighting Inflation and Recession Effectively. I’d love to share it with you. I think you will be highly sympathetic to my suggested solution.

Please let me know how I can send it to you electronically.

Best regards, John

P.S. I’m a die-hard fan of your work.

John,

You can send your proposal to this email: [email protected]

Please be patient. I might not have time to look at it right away.

Hansen, whenever you hear “Fed” think “banks that own the Fed” because they are the ones that got rid of the gold standard when we had a functioning Treasury Department 1790-1932(and no need for a “central bank”- a virtually unprintable term, in the U.S., in fact until Nixon was forced to “close the gold window” and with a sickly grin say “We’re all Keynesians now”. The very idea of $30+trillion unpayable debt was unthinkable- so don’t even begin talking about their “fighting inflation.” (The Fed charter does not talk about controlling inflation, either, but does reference “elastic currency.”

What is worse, these banks are furiously working behind the scenes 24/7 to ram through CBDC which will eliminate fiat as we know it, bad as that is, with nothing more than keystrokes in the ether. Some store of value, that. And you think inflation is bad now!

Robert,

” banks are furiously working behind the scenes 24/7 to ram through CBDC which will eliminate fiat as we know…”

You’re abusing my site to spread fabricated BS here. Banks OPPOSE CBDC because it would eliminate some big banking profit centers, including payments (such as credit cards), transactions, lending, etc. Why do you even need commercial banks if the central bank takes over their most profitable activities?

This is precisely why the Fed is in NO MOOD to move fast on a CBDC, and might not do one at all, because of banks’ opposition to it.

Another couple of years of of 4-6% inflation will push most middle class and lower income people over the edge and cause rioting on the streets. The Fed wouldn’t want that.

Forget rioting based on economic causes. The US population is not inclined to grab the torches and pitchforks and march on the town square. Should we ever get to such disastrous economic situation that would justify such extreme response, we will show our disdain by streaming more videos and posting messages on FB. Rioting for economic causes is not in the American DNA. We are too refined and unemotional to get excited about inflation popping a few points higher. We will continue to rail against the FED, or political system, but continue to reelect the incumbents, for “doing a fine job” in the view of the voters who elect them directly.

Sure, this series of comments on this thread really depends on what “push… over the edge” means, but it sounds like you either missed or forgot the Occupy movement after 08 when unemployment was at 10 percent.

…for ANY population, food and shelter, BC01, food and shelter…(looking around, does it not appear that we have stepped onto the high wire we walked in the ’30’s when a quarter of our population thought the CP had the right idea and a quarter thought the Bund did???).

may we all find a better day.

No riots (actually, few, there were a few riots) during the pandemic shutdown was a product, IMO, of the freebies the Fed and Congress dished out. Now we are at the endgame of THAT. More printing will result in runaway price rises: turmoil. I am not at all confident that what you are writing here is correct, Biker. The bottom 50 percent of USA inhabitants have essentially no net worth, no significant buffer against hard times. Whatever buffer Uncle Sugar had, was just spent. Americans are also armed, even poor ones (I am shocked at the numbers; I can;t afford that hardware)!

According to Gordon Gecko 50 percent of the population has no net worth. So, nothing much has changed since 1985.

Nobody (commentators) at this website ever blames the business leaders (CEO, etc) for inflation.

Fed and Biden to blame okay i guess.

But how are those who produce and sell the goods and services we buy not responsible for inflation ? Something doesn’t make sense here.

Different topic:

1. Consumers should have a say in the size and types of houses built… upfront before they are built.

2. The public should have had a say in determining how many homes investors should have been able to buy.

Call it bottom up socialism if you want.

@ Randy

Business leaders don’t print money or spend trillions we don’t have, that’s thee Fed and Congress (of both parties) respectively. The blame for inflation is appropriately allocated to the people who print money or deficit spend.

The jaded cynic says you are probably right, and perhaps Marie Antoinette, too, when told the people were starving for bread, because of inflation, figured they would therefore lack the energy to do much about it, but they found the strength to dismantle the Bastille one stone at a time- and were probably branded as loony leftists at the time as well.

No rioting if fentanyl is cheap and plentiful, people will just check out – first from society, then from life. Happening already all over this country. No rioting to be found. Enjoy your $1 eggs!

Incredibly well put. Very insightful and concise.

SOMA forever!

Yep. Future home buyers would be angry too as they get priced out. A few more years of 4-6% inflation will probably mean housing prices will start going up again. I was thinking about buying some puts on the home builders but maybe I will change my mind. During the 1970s battle with inflation, housing just kept going up and up. This will also lead to higher rents.

Well, nat gas producers keep producing into a glut and Biden will keep releasing oil out of the SPR to try to keep energy down.

Hopefully house prices will come down accordingly. This is good. Put a nail in this bubble. House prices in my area should be down at least another 30%.

Higher yields I mean are good.

I second this. More like 10% in realisitc terms, by 2025, when we look back at pre pandemic, it will be a 400% increase. Everything will end up like egg prices. Someone is getting rich somewhere and profiting, money is being shifted from poor to rich, once again. Living, earning, everything we earn will go to food, just to survive to the next day, so we can do it all over again.

The dollar is falling against everything else, due to oversupply. So somebody is not necessarily getting richer in real terms.

Raise chickens in your back yard

We had 4-6% for 10 years during 1970-1980. Did people survive?

The widest distribution in wealth (I think in world history, but centered in the USA) was, I believe, in 1968. Growth of widespread wealth hit a turning point around 1972. There was a lot of reserve there, to burn away. There were manufacturing jobs in the USA, steel plants, auto factories. Lots of wages unionized and indexed to inflation. My parent had stuff I could only dream of, now, though I got more education and a fancier job.

Survival and rioting in the streets are different things. People, in general, are very good at survival.

The real standard of living during those two decades declined pretty drastically for most people in America. So yeah, we survived, but it’s not the kind of situation we should be trying to replicate.

lol the only revolution during our much higher period of inflation was the Regan Revolution. We just hugged the flag harder. Powell would love Regan 2.0.

The cumulative effect of compounding inflation can ruin those who hoard cash for long periods of time. In Venezuela they spent money as fast as they could get it. They held savings in dollars instead of bolivars. During the 1970’s there was the Vietnam War. There was the Cold War with fears of communist revolutions. We did not want democracies falling to the atheist communists. Nixon ended the gold standard.

David – we didn’t want our client dictatorships falling to them, either…

may we all find a better day.

People are stupid ,quit buying 6$ a dozen eggs price goes down . Inflation is caused by fool who buy everpriced stuff. Everything is overpriced if we consumers STOP BUYING,prices drop .Simple a Fool and his money are SOON PARTED

What if they aren’t fools.

Just have lots more money than poor and lower middle class. What if business leaders could have created more inflation 5 years ago but did not do so. But now do.

I’m guessing not many people understand the intricacies of what goes into inflation.

I certainly don’t though I read these comments at Wolf Street fairly regularly.

To repeat…

We hear Fed, pandemic spending…but what about business leaders psychology today vs. 5 years ago. Does that matter ?

Very true Flea. Walking around the grocery store today, my wife and I just stared blankly at the ever-increasing prices. When we saw what will eventually shrink to a 2 oz thimble of ice cream for $7, we decided we’ll start making our own cookies. In the cereal aisle, we decided to just make granola for breakfast with frozen blueberries from our yard. Eggs? Skip ‘em. The food companies will hold out to keep their profits up, so consumers have to take a stand and force the pain back on them. Who has more willpower?

I don’t know if we’ll all start losing weight by eating less food, or gaining weight by shifting down to low cost, unhealthy food. I did notice a lot of tension in the store, no eye contact and solemn expressions. The frustration on this comment board is real.

Great, report, even if the data is horrible.

“The PCE price index for food was heavily revised upward for the last three months of the year. In January, it rose by 0.4% from December.”

Is the 0.4% increase in January calculated after taking into account the upward revisions for the last three months of last year?

Yes, that’s on top of the upward revisions in the prior months.

The YOY increase was 10.6%.

Thanks! So much for disinflation.

A modern saga in the making.

First, inflation was characterized as transitory; then disinflation was judged to stay here, but it became transitory. Then inflation was revised down, later inflation was revised up then disinflation was revised down.

Stupid economy! Why does it have to be so confusing.

Clarification requested. I am not the sharpest tool in the shed.

So your charts today represent the changes from the upward revised figures from the past against the current figures?

Yes. All revisions have been integrated into my charts and data. Today’s increases are on top of the upwardly revised data.

Anyone who actually buys the things he/she needs knows inflation for all those items is all up at least 10%. The government must think, no it knows, we are all idiots!

I buy everything on sale ,in great quantities. Canned goods usually last 7 years kids make fun of me ,call me a hoarder get cereal on sale 99-1 .29 tuna 80 cents .if it’s not on sale I don’t need it = Fuck inflation

Wolf: After the Powell’s press conference, you seemed to defend Powell’s take that the “disinflation process is underway”. What do you think now? Powell’s words and the Fed’s actions continue to be woefully inadequate to the inflationary problem we have before us, which he has blamed on everything from Russia’s war to the Pandemic, when it really is just a monetary phenomenon that the Fed is fully in control of. If Powell continues to be dovish, we will continue to see speculation in meme stocks, bubbles, out of control spending and debt, when he could easily accept that inflation is running at an annualized 7%+ rate and adjust rates upward to about the 7%-8% range. Your faith in the Fed in the face of such incompetence is quite incomprehensible.

“you seemed to defend Powell’s take that the “disinflation process is underway”

LOL

Here’s what Powell actually said, including about “disinflation” — hint: it’s the markets that hyped disinflation, not Powell. Overall inflation has come down from the peak — hence “disinflation” — but Powell was worried about persistent inflation in services. It’s Wall Street that did the disinflation-mongering. So read this:

https://wolfstreet.com/2023/02/01/what-powell-actually-said/

Here is what I actually said about “disinflation”: Another important read.

https://wolfstreet.com/2023/02/10/cpi-just-got-revised-up-for-october-through-december-revisions-take-a-bite-out-of-disinflation-hoopla/

Here are all my inflation articles. Try to find one where I “defended Powell’s take that the disinflation process is underway”:

https://wolfstreet.com/category/all/inflation-devaluation/

Agree. Wall Street did the disinflation mongering with its “FED pivot” narrative and offering 94% probability of FED increasing rates at .25 basis points at last FOMC Press Conference. However, Powel caved to WS by agreeing to the 25 basis point increase.

Powel should have demonstrated leadership and administered 50 basis point bump, or higher. By compromising and appeasing WS, especially after having stated previously that it is not the role of FED to manage the stock markets, he demonstrated lack of resolve to tame inflation. He should have administered the shock treatment necessary. By allowing WS to intimidate and dominate the narrative, on interest rates hikes, Powel abrogated his primary duties and responsibilities in setting interest rates. If he is committed to fighting inflation, he needs to take strong action; if he wants the inflation to exist on its own and hope it eventually burns out, then he should continue acquiescing to the “free money junkies” on Wall Street.

Powell used the word “disinflation” 11 times during his press conference, and the word does not appear even once in the Fed minutes. It was not Wall Street who put the “D” word in his mouth. He voluntarily blinked and eased over the period from October ’til now. Perhaps because he saw what happened in England and got scared that the same implosion in the Bond market and MBS could happen here.

Michael Santos,

Disinflation = inflation that is lower than at its peak. So it’s OK to use the term for that.

What’s not OK is to go out there and twist everything Powell said into BS hype. Powell warned about stubborn services inflation in the presser time after time. He pointed out why overall inflation was in “disinflation”: falling prices of fuel and durable goods; and he said that durable goods prices will stop dropping. And that services inflation would continue to be hot.

The result is exactly what you see: pretty soon, reality sets in, and all this stuff sells off and people who believed this BS, the same BS you’re citing, lose a lot of money, while the disinflation-hoopla mongers got out with their gains. Oldest game in town.

Saying that Powell “blinked” is part of the disinformation campaign.

So does this mean if Powell and the FOMC go with 25 bp in March, that Powell really will be seen as being dovish?

It’s regretful that they wimped out and went with 25 bp last time, instead of the 50 bp if they were serious

It should have been 75 bp.

75? He should crank it up 100 or 200 points to absolutely CRUSH the demand that is causing inflation. He needs a couple of million more unemployed which will cause unnecessary spending to drop. Consumer confidence is rocketing upward which is exactly the writhing. Consumers need to be fearful and hunkered down. He may have to cause a depression to break this mindset once and for all.

Amen!

However, the bureaucratic Fed cannot stand the heat. Powell will maintain his present policy; maybe some increases but he’ll face increasing pressure to back off.

Time will tell.

B

Rare agreement from me. Jacking rates up would kill off all these scam companies with multi billion market caps that have never earned a penny in profit, some of them for a decade. They’re just scams that have made billions for the insiders that continue to pump and dump their stock. How much of this garbage ends up in pension and index funds? A lot. Shooting these in the head would stop this in their tracks but instead the fed is letting these frauds die of old age.

Would kill all the housing speculators that have driven the price of shelter up 20-30x over the last 2-4 decades, far outpacing wages.

I am seeing a lot of ignorance and magical thinking on display here re. thinking the Fed should be raising rates .75 or even a full point at each of their meetings. Be careful of what you wish for. The Fed may have been behind the curve when they started this tightening cycle but they aren’t now. It takes up to a year for the full effects of any particular rate hike to be felt in the economy. The full effects of past hikes are only now beginning to be seen and will become much more apparent as the year progresses. Lots of business bankruptcies and increased unemployment are likely just around the corner.

Do you know the ramifications of a depression,in this environment it would probably be total societal chaos. As people are not very civil to one another.

It will be 25 as advertised. Just accept it, fed is dovish. It just that they can’t say it outright , but they prefer inflation at 4 to 5. They are close.

but they get that number @ a 2% CPI after all the index manipulation…so I think they still need the 2 handle, at least.

Canada is already trying to do that by back averaging one year. Rate pauses and dubious CPI reports.

If NFP and CPI are hot again it could be 50 but we’ll find out from timiros before the meeting

Huh??

We will see the markets front-run the Fed regardless and behold: The 6-month Treasury Bill is at 5.1% give or take some basis points. When you have way too much of an item to sell, I almost goofed and called it an “assets”, such as Treasury securities, and inflation is still burning a hole in everyone’s wallet and purse, then you have to offer higher yields. Me thinks some of the recent Treasury auctions have been dismal, and Uncle Sam, flinching as he or she did so, had to raise offering yields to clear the docks.

The U.S. Fed is too politically connected to the dudes in Washington, so they are very afraid of cratering anything, esp. the housing market, already in noticeable retreat in most markets. The rate of Fed Funds increases should be 50 basis points until you get to over 7%. Get it done and go on vacation Fed Meisters. You have already wrecked a perfectly good economy starting with the 2009 actions and then the Pandemic Liquidity Tsunami, so why not just get it over with. I saw a snail passing the Balance Sheet Reduction rate of change and a ton of liquidity is still feeding speculation on Wall & Broad. The NASDAQ up 10% in less than 60 days, pass the bong!

Wolf, in you vast economic data experience, what is the most predictive metric in determining how the Drain the Liquidity Swamp Fed program is going? M1, M2, or M3 or whatever?

Derivatives markets imply a 40% probability of rates topping *5.5%* after the Fed’s July meeting

Everything is fine

That Fed pivot is definitely coming now – to higher rates.

With the increasing FHLB borrowing by banks (a timing indicator), we need to keep a close eye on the Fed Repo market. The increasing (for now) Federal Funds Rate is punishing the banks in the fight to decrease the rise of inflation. The question is, who will break first, the consumer or the banking system.

Thanks Wolf for another great report. You’ve been predicting this all along when you mentioned months ago that inflation would dish up lots of surprises. Powell needs to start reading Wolfstreet.

The desperation in January to pretend the good times were here again had me shaking my head. There’s definitely been a push to make that the narrative (I saw a CNBC article along the lines of ‘is higher inflation really so bad for the economy?’ the other day and it made me want to scream) but reality is telling a different story. Thanks for keeping track of the facts, Wolf.

The FED isn’t sharing it’s “models” predictions. Why is that?

They talk about at delay of monetary policy cause and effect – so when does the tightening done so far really bite?

Wonder if this will be enough to start to kill off the never ending supply of hopium on WS? I give it 50/50..looks like even today, there are quite a bit of buy dip action going on to keep the market from plunging to the abyss

Plenty of bear market rally traps…it’s bonus and tax return time for the FOMO retailers, more chances to throw those money into the bond fire..

Inflation continues to rage because the Fed lacks credibility. When people think inflation is going to be 3-6%, the markets will continue to bid up stocks, RE won’t correct, and crazy speculators will rule the day.

The Fed says out of one side of its mouth that inflation is caused by the war and supply constraints, but if the Fed actually believed that, it would be expecting DROPS in prices (or price deflation) over time as supplies get back into balance. But we don’t see such price reversals in Fed forecasts.

Further, if the Fed were targeting average inflation of 2%, it would now be targeting a period of price deflation at some point in the future to offset the 2021-2023 inflationary spike. But the Fed’s forecasts do not reflect this.

The Fed’s words and promises simply do not align with its actions, behavior, or its own forecasts.

The only thing that appears trustworthy is the Fed’s relentless drive to prevent recessions. To do that, inflation must continue, until the Fed loses all control. Sustained elevated inflation is the biggest risk to investors over the long term. Long-term bondholders are starting to figure that out.

Was taught that recessions are a normal and healthy part of the “business cycle”. Why would the FED lose its way trying to fight the business cycle?

…mebbe too-many who’ve come to believe that speculation is productive work and can’t countenance a recession and a pay cut after so many years?

may we all find a better day.

grimp

You were taught well. With the exception of yourself, myself and a handful of others, the business cycle has been forgotten.

Through a staggering extension of credit, the Fed and other central banks have successfully extended the current cycle beyond the scope of our collective memory. It is overshadowed by the emotive inflation platform and by frenetic and diversionary talk of whether there will be two or three 0.25% rate rises. Too many people have been caught up in the wealth effect to rationally conceive that it cannot sustain itself in perpetuity.

The Fed is not omnipotent. Dynamics beyond the Fed’s control will eventually scoop up all of us and dump us into the reality of a new business cycle. Depressions are recessions denied.

I don’t have a concise answer to your question but it’s a superb question. That’s for a book to be published when there are enough reawakened people to buy it.

Bobber wrote: “The only thing that appears trustworthy is the Fed’s relentless drive to prevent recessions. ”

Nah. Nope. The only sure thing you can count on the FED to do??? They will not do anything to harm the profits/assets of the private banks that own our “Federal Reserve”.

At this time, I suspect those private banks are heavy into derivatives. The Big Players need time to move over to the right side of the ship.

Old Ghost, if the banks actually marked their 100’s of $Trillions in derivative positions to Market (vs. Book or Cost Basis), then the listing ship occupants would realize that there is such a gapping hole in the Financial Titanic that shifting weight from Port to Stern and vice versa won’t save the vessel or themselves or the system. Credit Default Swaps are a humongous accident waiting to happen. Because of this issue, I don’t buy any of the Fed’s banking health metrics at this time (or prior).

This is exactly correct. The Fed waited a full year to do anything about raising short-term rates despite raging inflation. They waited another 6 months to timidly start QT. When there is a recession they drop rates 40 basis points in 3 months. They should be outright selling MBS at this point and are at least a year behind with short-term rates. The market doesn’t treat the Fed seriously because everyone knows they will drop rates like a stone at the slightest sign of a recession.

PCE stuff to ponder

Lakshman Achuthan

ECRI

Even though the service providing sector accounts for over 85% of nonagricultural jobs, compared with less than 15% for the goods-producing sector, it’s the goods sector that’s usually responsible for the lion’s share of job losses during recessions. That was consistently the case through the early 21st century.

Specifically, goods sector job losses accounted for 77% to 134% of total recessionary job losses in every recession up to and including the 2001 recession.

Wolf nailed the higher PCE readings prediction from a few weeks back!

The way the Fed commentary reacts to the recent bad incoming data of late (NFP, CPI, PSI, PCE) is fascinating to me.

It seems no matter if the direction of commentary is hawkish or dovish them seem to just be consistently stubborn and slow to respond to be data. Seems like there is about a 3 month lag on Fed talk. They’ve started touting disinflation just as inflation in real time is taking off again.

I guess we should expect this from government officials.

One more month of data before the next dot plot comes out!

Confederate currency rising substantially against the greenback! 5$ confederate note now worth $250 US$ and climbing!

Says a whole lot!

That’s a collector’s item. I just saw one on eBay for $49. Seems you need to shop around a little more.

Depends on the quality like all collectibles! At $49 it is not an uncirculated top grade bill!

Yes, that was my point, LOL. You compared a collectible item to the current dollar to make your usual point about the collapsing dollar. But even a worn-out crappy $100 Federal Reserve Note is worth exactly $100, same as a brand new one. I love old bank notes and have a few myself — their value being likely close to zero or zero, or if I can find someone willing to pay me $50 for them, then their value is $50. But they say nothing about the value of the dollar.

Who would’ve thought that Confederate money would be worth more than face value after they nabbed the silver medal in the intermural games?

XC – stoppit, you’re killin’ me!

may we all find a better day.

I always buy my Confederate currency at Stucky’s!!!

Don’t forget your pecan roll !

Sigh, my best investment over the past decade or so is the handful of 100 Trillion Dollar Zimbabwe notes I bought for under $10 each back in 2009-2010. Selling for $100 bucks or more now.

Close your wallets you cruise ship, flying, hotel going so and so’s. You DO NOT need that _______ at Costco! Live in one house and only own one house. Stop speculating with crypto, fruit loops, NFTs and uncle Joe’s pyramid scheme. You do not know how to make money off of the money you have. You only know how to lose it to the bigger fish. Park it with an S&P Index fund and think about your kids or grandkids. Oh and PS, go exercise and eat your Veggies. You guys 55 and up are so unhealthy, your medical bills are drowning us.

Tootles!

The best ‘long term’ I can do for you right now is 3 month T bills paying almost 5%…all day long buddy.

> You guys 55 and up are so unhealthy, your medical bills are drowning us.

That will make us die sooner, freeing up our assets. But not me. I’m that age, my peers are falling apart, but I can run up the side of this valley any minute. Was out running hours before sunrise.

> You guys 55 and up are so unhealthy, your medical bills are drowning us.

Haha – it’s America’s Rube Goldberg style health system that is drowning everyone (who are not rich and have significant medical problems in America). That combined with Western medicine’s allopathic focus on symptoms and diseases rather than prevention and holistic analyses.

I’m 71, healthy, and take no drugs for any health condition. For me, playing the long game (healthy eating, exercise) has worked out fine, so far. Additionally, medical costs here where I’ve retired in Thailand are about 25% of what American systems charge (less than 10% in some things). And my Thai wife’s pension pays about 33% of the lower cost if I need some type of lab or hospital services.

Do a search for this: “Why Are Young People Getting Type 2 Diabetes In Distressing Numbers?”

If you think the 55+ crowd are unhealthy, you should check out the 65+ crowd. And if you think that’s bad, check out the 75+ crowd! And the 85+ crowd? My god, it’s horrifying, they’re dropping like flies left and right.

I was going to say that there is a wall you crash into at 60 another wall at 70 (so I am told) and another at 80. That last wall is the doozy.

watch out, 55 sneaks up on you pretty fast

“Inflation Horror Show. The Fed has got a problem on its hands.”

Nothing that anybody with even a modicum of common sense or the most basic insight couldn’t already see well before the last FED meeting. The FED has been lying through its teeth.

“The risks of doing too little outweigh the risks of doing too much.”

~Jerome Powell

**Proceeds to rapidly scale back rate hikes to a puny 25 basis points**

And people actually wonder why the speculative orgy continues? This clown was talking Volcker while channeling his inner Arthur Burns. Powell should be removed from office. He’s destroying the United States of America.

The patient is already in very bad shape. It’s a serious question whether withdrawing the dope, pulling off the band-aid, will be terminal. Powell deserves much credit there.

You can’t put the toothpaste back in. Just keep brushing they say. It will get better.

had the tv on and cnbc – for the most part the people under age 50 see no problems ! inflation is under control and the fed should stop hiking now ! and then cut later in the year – they want their free money back !

Yes, everyone wants their free money back. The only good money is free money 🤣

I got a bag of “free” shredded cash gag gift from the US Mint as a kid once, and I searched the definition of cash and after seeing the words “faith”, “trust”, “IOUs”, “not backed by gold”, etc. I decided to stick to income producing hard tangible assets after that and it really paid off so thanks Mom and Dad for scaring me in a positive way…HA

I tried to tape it back together, but of course it didn’t work after a few wasted hours. Perhaps broke a law or two in the attempt, yet probably not as bad as copying VCR movies or removing bedding tags.

But Elon Musk wants a rate cut now! They’re making a terrible mistake hiking! Oh, and there are too few people on the planet, apparently.

There is one company on this planet that makes the highest end silicon manufacturing equipment.

There is a good question in how many people do you need to support civilization level”x”.

That’s CNBS propaganda.

Inflation is the expansion of the money supply and or debt. We will know when everyone is serious about reducing inflation when the federal government actually freezes or reduces spending in real time, not cutting future spending. Yes cutting or freezing spending a the existing level!

The first test will be when the huge amount of Covid spending bills run out. At that time the Federal government will be hit by State and local governments failing. They will be asking for money to bail out things like pension funds and state and local bond holders as well as everything else imaginable. During Covid the feds were free to bail out states and local governments but without another crisis will they be able to sell the public on another bailout with raging inflation??

We are at least 6 months away from this first test and my bet is inflation will just keep edging higher. Federal agencies will continue to re adjust the way inflation is measured to hide the real numbers for as long as the public continues to buy the narrative that supply lines and greed of corporations is the force behind high prices. The only force pushing prices is the huge spending and debt creation of world governments.

This comment needs more exposure. Government bailouts of pensions seems ominous.

President Joe Biden on Thursday (December 8, 2022) announced the largest rescue package for a pension plan in U.S. history. The nearly $36 billion infusion for the Central States Pension Fund will mostly benefit members of the International Brotherhood of Teamsters.

Funding for the rescue plan, which the White House said will ultimately help 350,000 union workers and retirees, will come from the Special Financial Assistance Program, which was created by the $1.9 trillion American Rescue Plan Act signed into law in 2021.

It’s getting harder and harder for the Fed to thread the needle.

Hey Wolf, first of all, thank you for all the great work you do and the very accurate and timely information and analysis you provide. Much appreciated.

Here’s what Powell actually said: “It is most welcome to be able to say that, that we are now in disinflation…”

Do you think he has ANY credibility using a world like disinflation when inflation is actually picking up and everyone can see that?

Disinflation = inflation that is lower than at its peak. So it’s OK to use the term for that.

What’s not OK is to go out there and twist everything Powell said into BS hype. Powell warned about stubborn services inflation in the presser time after time. He pointed out why overall inflation was in “disinflation”: falling prices of fuel and durable goods; and he said that durable goods prices will stop dropping. And that services inflation would continue to be hot.

The result is exactly what you see: pretty soon, reality sets in, and all this stuff sells off and people who believed this BS, the same BS you’re citing, lose a lot of money, while the disinflation-hoopla mongers got out with their gains. Oldest game in town.

You’re part of the disinformation campaign.

“Powell warned about stubborn services inflation in the presser time after time.”

Yet at the same time he was scaling back the size of rate hikes. It’s like warning of black ice ahead while pinning the throttle into a hairpin curve.

25-basis points was the maximum they did for the prior two decades. After you’ve hiked by 450 basis points in 10 months, there’s nothing wrong with 25-basis point rate hikes if you do enough of them. It doesn’t matter whether you get there a month or two sooner or later. The idea is to give markets time to transmit the policy rates to the real economy and see what happens. This type of inflation is a matter of years, not months. I know there are people who want Powell to crash the economy so that the Fed will cut to 0% and do QE all over again. But that’s precisely what I don’t want, LOL

I want a well-functioning economy with higher rates — ultimately short-term rates above the rate of CPI inflation — that will eventually bring down inflation. I’m not sure we’re going to get that, but that’s what I want.

I’d say 0% interest and QE is NOT a sign of a healthy economy; in fact, it causes all kinds of distortions like we’ve just seen (real estate bubble, stock bubble, bond bubble, money loosing unicorn startup bubble, etc).

Wolf indeed nailed today’s PCE prediction. He has been saying it for a while that there is no downward health care adjustment in the PCE calculation. I showed my appreciation today by making a small donation. Also because of some decent profit I made today in the corrupt market. Playing penny stock with the meme crowd. Sometime you have got to play the corrupt game too. I suffered big loss in UVXY. So can’t short this market anymore.

You can short the market. I do all

The time. But using an inverse etf and holding longer term doesn’t work. They are arbitraged futures and options and degrade with time. Stick to shorting the spy qqq smh iwm ect with shares or buy puts at least 3 months out at the money as a synthetic short

Bet

I quit buying puts, several months ago. B/c there is crazy ‘front running’ almost every day with unbelievable volatility.

Latest fad is ODTE (Zero day to Expiry) it is liker a crap shoot on the expiry day. A lot of Algoes participate. Hence the price volatility of S&P calls this Friday. A lot of ODTE on calls, FAILED to materialize and Bear s took over.

Its worth noting that the German stock market of the early 1920’s performed rather well against the then accumulating but not overly obnoxious inflation, that is until hyperinflation came along and made a mockery of best laid plans.

Germany’s debt was all external. At least we have a diminished problem with that. We’ll just all write checks to each other and pay it off! And then dance and sing until we’re not hungry anymore.

I don’t know where all this “inflation” talk is coming from. The “official” CPI (used to determine social security increases) has barely budged over the last 6 months. Up only 1% on an annualized basis since last July.

The Fed will raise rates 1 more time (25bps) and that’s it. They don’t want to kill the housing market and the sudden increase in mortgage rates is going to get their attention.

The market can’t handle mortgage rates over 7%. I doubt mortgage rates will go above the high already set a few months ago (7.37%).

The CPI-W (which is what you’re talking about) spiked by 0.9% in January from December, after a couple of negative months.

It’s up 6.2% year-over-year.

What counts for the COLAs are the year-over-year increases in the three months of July, August, and September. That’s the only thing you need to look at in terms of the COLAs.

Oh, I disagree. I think they do want to kill the housing market.

Or at least slow it down significantly.

For the historians and those who are more aware of what has occurred in other economies with high inflation, what is the typical progression/stages between ignoring inflation and spending like crazy, where we are now, to rioting in the streets because of inflation? Over what period of time does that happen?

Worse then a riot — ordinary people start organizing and demanding raises, boring pensions, DISCO, etc. You then have to hire a real actor who will actually READ the teleprompter, married local, and make suburban wives think he’s a nice man. Those are not cheap.

Interested to hear what you think a resumption of student loan payments will do to the housing market (peoples ability to purchase homes with less $ for monthly payments), CC Debt and Houselhold savings, and inflation. If people had to pay back student loans again, surely inflation would slow down?

I’m going to go out on a limb and predict 25-50 basis points at next meeting, contingent on any future inflation data.

My observation is that it’s nice to see that cash is not as much of a murder-suicide pact as it was last year.

Please stop borrowing, consumers. You’ve had your post-covid vacay. Netflix is right there.

You’re welcome!

So you’re asking consumers to stop borrowing? If Augustus Frost is correct and Americans are destined to become much poorer, why would they not want to live it up now—while there is still credit available?

Live life big while you still can, like it’s 1927 or 1928. I’ve heard they were great years!

lol, I’ve been reading about the incoming financial apocalypse for quite some time. If I had cared then, I’d be worth around a quarter of what I am now.

How is the economy still this strong after 5% of FFR increases, a year of QT, and federal covid checks long gone? Is it because

1) The tightening hasn’t had enough time to work through the economy yet (“long & variable lags”)

or

2) Neutral interest rates are a lot higher than most policymakers forecasted?

Government spending & 9 trillions printed just 2 yeas ago. Also I wouldn’t discount some kind of backdoor liquidity provided so equity doesn’t plunge.

It’s misleading to think in terms of ‘a year of QT’ when there’s still $8.3 trillion on the balance sheet compared to almost $9 trillion at the peak of QE madness. Hardly a dent, really, so lots of Monopoly money still sloshing around.

The balance sheet expansion was incredibly quick in 2020, but very S-L-O-W unwinding it all.

Both could be true.

The economy has adjusted amazingly well to higher rates. Asset price are another story, but they don’t make up the economy – a booming stock market and housing market didn’t create a booming economy.

Its the possible 8-12 month “effects lag” that has me wondering. I would guess that the “lag” could be much shorter in a highly leveraged economy, so I get confused when so many articles are confident in the lag time frame.

I’m guessing this Frankenstein economy is going to have a more volatile and unpredictable future than previous periods, if for nothing else the fact the entire construct is instantaneously connected at all levels on a global scale versus the past fifty years when Y2K was our biggest interconnected banking system worry. Plus all the self induced complexity over the last few decades across nearly all aspects of human endeavors, good luck predicting anything beyond a coin flip after a few Wolf mugs full of beer…

Perhaps the A.I. can predict the future, yet us humans are simply taking wild “educated-ha/ha/ha” guesses based on limited, incomplete, human corrupted data sets that are driven as much by human emotions than actual science.

That said, I have to admit it is kind of fun attempting to piece together the human impossible puzzle, right? Plus a few of us will guess right and then feel like geniuses for a few weeks until we get over-confident and bet the farm on the next gamble that doesn’t turn out as we guessed…

The core problem is something that I dont feel even Wolf is talking about. Assets on balance sheet at central banks. Bottom line is that the QT has been pathetically slow. They put more than 4 trillion on the balance sheet and havent even got a trillion back off that balance sheet.

To me, this points to simply one motive. Keep asset bubbles.

It is my guess, although I cant prove this at the moment, that if the Fed had started to sell off the balance sheet aggressively INSTEAD of raising interest rates, the capital markets would have already tanked and long term interest rates would have blown out and we would have seen inflation coming down already.

But the Fed wants to kill core inflation of goods and services WITHOUT causing rich people to lose much money. Because the Fed is made up of bankers who go to parties and events with other financial rich people and they dont want to be thrown to the wolves by the greedy rich.

If you really want to decrease income inequality, you would stop pumping the asset bubbles.

Look back to 2012 time period, when they started to sell off the balance sheet and it lead to a major stock market decline. They had to reverse course. This tells us everything that is true. It is TRUE that the rich are getting rich on the back of an asset bubble blown by central bankers. It is TRUE that these bubbles favor capital and disfavor labor. It is TRUE that by buying up assets the Fed and other central banks are distorting financial markets and thereby causing mal-investment. This mal-investment is the core of why our real production is so much lower than our consumption. We are managed by MBAs that have no real capacity to invest in technology and innovation, but a great capacity to use marketing gimmicks and financial engineering to increase stock prices.

I think over half a trillion in 7 months is pretty fast. This is a program that is supposed to go on for years.

While I agree with your general drift about a half a trillion being an enormous number, the percentage decline of an even larger enormous number, the Fed balance sheet, is less than 6 pct.

Unlikely to haul in the randy herd. Just saying.

Nicely said. But you forget to mention the private equity crowd. The first thing they say, before the acquisition, is that they will unlock value. I lived that experience to find they re-financed as much asset equity as possible at the lowest rate. Then they kept that money and told us we had to make them 20% going forward. And we thought the Corp tax rate was holding us back. Silly people.

When financial engineering fails, gravity prevails.

Prepare for landing!

Our politicians ruined our country.

Thanks for presenting the facts on an important topic:

the official measurements of inflation, both consumer and core.

Both readings, correct me if I’m wrong, were higher. And the previous quarterly data were also revised higher.

I think I understand if the data are telling me that the Fed’s policies are still inflationary.

Assuming the FOMC board is inhabited by sentient human beings, I think that it is a no brainer from a policy perspective to raise the FFR by 50 basis points at the ides if March meeting.

Which brings us to face the opposing point of view with an open mind to understand their point of view.

The collapse of three historically large bubbles, simultaneously, is the worst case scenario for a modern economic model.

The best case scenario is currently being presented.

The problem is that the model is always wrong, eventually, which has a lag time of 20 or 30 years, or more. We’re lemmings. What can I say ?

That’s just a working hypothesis which can change at any point in time. The only truth teller.

I ask myself, probably, the same question you ask yourself. Maybe not and unlikely. Nonetheless;

what are the pros and cons of a 50 vs a 25 bps increase in the FFR at the mid March meeting of the FOMC.

1) Inflation has become a part of daily life.

b) There is nothing we, as citizens, can do about it.

3) Inflation destroys the American dream.

3b) inflation destroys the American dream in a predictable mathematical manner which can be demonstrated using the rule of 70. One can accurately predict the number of years before the unit of currency is worth half of what it is today.

For instance, rounding up the measured consumer rate of inflation of 6.7 to 7 pct. statistically the same number, suggests that the unit of currency, the dollar, will be worth half as much in ten years,

Serious question. Also, I admit I’m ignorant so don’t roast me too hard Wolf:

Why are mortgage rates so low?

I know it’s loosely based off 10 years etc.

But here’s the thing: when rates were 0% mortgage rates were 3-3.5%. Now rates are 4.5-4.75% and mortgage rates are sub 7%.

Additionally QT should be rolling (slowly).

Are people overpaying for Mortgage Backed Securities (MBS)? or is there margin compression?

Honestly I would guess MBS are mis-priced (knowing nothing). Buying into a potential housing correction should require decent risk adjusted yield, no?

Maybe “It’s different this time.” and MBS are safe?

Tangent: Muni Bond prices are also crazy. VTEB was paying 3.5% and now suddenly it’s paying 3%. Markets are nuts.

“Why are mortgage rates so low?”

You must be the first person in this cycle to call 7% mortgage rates “low” — while my eardrums have busted from all the hollering about “high” mortgage rates.

Actually, the better question to ask is why the 10-year yield is still so low (ca. 4%) when short-term rates are at 5%. My answer is: the markets are nuts. But other people have other answers that are at least as bad as mine. Market do what they do because they do it.

Poll question: at what level would you buy the 10 year?

Me? Thanks for asking. 8%.

I’m going to start nibbling before then, for sure.

Gattopardo

I’d love to give you a snappy answer, but…

It’s a question of time and perspective. Today, 4% seems to some like an absurdly low level against today’s inflation. Fair enough.

If you’re into perfect timing, maybe it is premature to jump in right now. Yields are on the rise again, albeit in an inverted spread.

However, there are some epic air pockets ahead of us.

Nothing mentioned above takes into account the debt ceiling negotiations. I agree with Powell. This is a negotiating round best concluded early and without fuss.

Nibbling at 5, 6, 7, gobbling at 8, 9, all in at 10. Well, except for my bitcoin, that’s going to infinity. Now let’s talk EV!

The problem is inflation expectations!

The FED (Cleveland Fed and FRED) show:

5 year – 2.18% inflation

10 year – 2.28% inflation

Add the risk premiums etc.

I don’t find these to be believable and even a recent FED White paper disagreed with these. It said it would take 7.5% unemployment to achieve 2% goals.

It seems like magical thinking to say we’ll average 2% over the next 5 years.

P.S. – I didn’t include links. Not sure if FED links are allowed.

The markets are nuts is not an authoritative answer like saying ” currently the markets are more optimistic about the future than am I”.

The markets anticipate a future in which earnings grow and the historically large profit margin persists.

The majority of people that are not in the markets do, and should, have a different perspective.

Best wishes

Yeah the 10-year is a real head scratcher, I guess they mistake Powell’s hesitancy as he is a closet dove instead of a weathervane.

In 1984, mortgage rates averaged 13%.

Last time before this cycle that CPI was over 6.4% (current level) was in 1981 when mortgage rates averaged over 16%.

So yes by historical standards in relation to current inflation levels, current mortgage rates of just 6-7% are extremely obscenely low.

Bond investors believe that we are near a recession, and that the Fed will accordingly cut rates when that occurs. Yield curve inversion of this magnitude is unusual, but in general, yield curve inversion is a decent predictor of recession within the next year or two, or at least has been for the last 50 years until the Fed decided that we need never have recessions. Since 2008 it has been a loser’s bet to bet against the Fed, but that doesn’t mean it will be forever.

Greenspan kicked the can, Bernanke and Yellen

too. What made anyone think Powell would do

differently ? Impoverishing the bottom 80%

before they kick off the recession is par for the course.

Would starting a small chain of upscale pub and grill style restaurants called “Kicking the Can Bar and Grill” strategically located near all twelve of the Federal Reserve branches across the country be a success? Namely from its ability to draw in all the hundreds of subordinates working under the Fed regional chair people as they wander the nearby streets during lunch and after work?

Love it.

That could also be a great place for the Plunge Protection Team (PPT) to get drunk during the day instead of sitting at their desks and buying stocks. We saw them do this many times last year at the other bar around the corner. I think I recognized some of them at the bar this week…

I’m not an expert, but it seems to me that if interest is a business cost then raising intertest rates raises business costs and the business has to raise prices.

And if marginal businesses then go bankrupt, the remaining small pool of businesses have a monopoly power to raise prices.

This whole poorly thought out system that allows any bureaucrat who has any ability to create regulations that are monetarily or ideologically self serving without any accountability, is bound to collapse catastrophically.

Weird that there are so many “experts” and other commentators talking about Fed changing its inflation target now that it’s been coming in above 2% for almost 2 years.

I don’t remember anyone discussing this ever when inflation came in below target for a few years after the GFC.

Why didn’t anyone suggest at that time just dropping the target to 1% or less rather than endless ZIRP and QE in a desperate attempt to push inflation back up to the 2% target?

Very odd.

A few years ago (2018?), NY Fed president Williams, when he was still head of the San Francisco Fed, discussed raising the target or widening the target to include 4%, or something like that. This was back when inflation was below the 2% target. He recently came out and staunchly defended the 2% target and getting back to 2%.

Funny thing is, if the Fed raises its target to 4%, it will set expectations of permanently higher inflation, and long-term yields will spike out the wazoo to account for that, and the Fed’s short-term rates will be higher while inflation is higher. So what these people are saying is that the future will be of higher rates and higher inflation.

Apparently no one is worried about the steadily increasing DEBTs of all kind through out the world.

Total Global DEBT to GDP ration is over 400%. USA around 130% very conservatively.

It is well known that once the ratio exceeds 90% (77%?) it will be a drag economy. Guess ZRP mind set is still there along with wishing for pivot and again ‘free money’

We will see 70s inflation again and 20% interest rates at the end.

First house in 1974. Considered myself pretty lucky to assume a 7% mortgage. Second house in 1989. Was happy (and shopped hard) to get 9.95%. Is everything “relative”?

But because mortgage rates were higher, prices were a lot lower, in relative terms. That’s the process now: prices adjusting to mortgage rates.

Why do you say services inflation jumped *by* 0.6%, don’t you mean jumped *to* 0.6%?

For example, November was 0.4%, December was revised to 0.6%, so why did you say it jumped to 0.6%?

Just curious if i’m misunderstanding

The PCE price index (like the CPI) is an INDEX with an index value every month and every category. The percentages are the percent changes of those index values.

For example, the value was of the Core PCE price index in December was 125.7. In January, it jumped “BY 0.6%” to an index value of 126.4. You could also say, it jumped “TO” an index value of 126.4. But you get on iffy territory when you say the “index” jumped to 0.6%, though I’m also guilty of having done this in the heat of the battle. But you can say correctly the “percentage change of the index jumped to 0.6%.”