Year-over-year growth in consumer spending, adjusted for inflation, outpaced the pre-pandemic average. Month-over-month, seasonally adjusted, growth spiked.

By Wolf Richter for WOLF STREET.

People want to get on with their lives, it seems. Their mood has improved. They’ve gotten used to living with high inflation. They got raises or got higher-paying jobs. Gasoline prices have plunged since the peak in mid-2022, and that matters a lot because it’s the most in-your-face inflation along with food inflation. They might still gripe about higher prices, but you live only once?

And so they spent money left and right in January, and they outspent even this raging inflation. We already saw surprising strength from new and used vehicle sales coming out of the auto industry, and from the retailers’ point of view earlier this month, which showed that consumers were in no mood for a landing.

Today, we got inflation-adjusted (or “real”) consumer spending trends for January from the Bureau of Economic Analysis. Personal Consumption Expenditures (PCE) on durable goods, nondurable goods, and services is adjusted for inflation based on the PCE price index, which blew out.

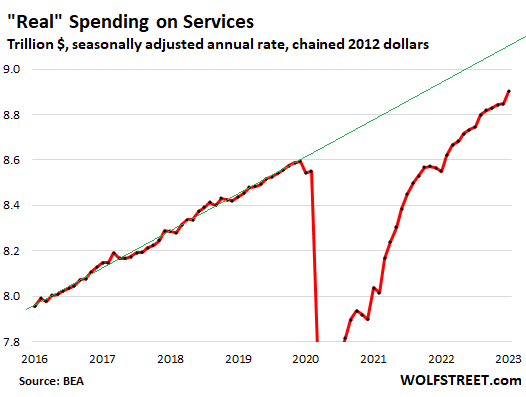

Spending on services, adjusted for the raging inflation in services, jumped by 0.6% in January from December, seasonally adjusted, and by 4.1% year-over-year (not seasonally adjusted).

Not adjusted for inflation, spending on services spiked by 1.3% from the prior month, and by 10% year-over-year!

Services accounted for 62% of total consumer spending. It includes housing, utilities, insurance of all kinds, healthcare, travel bookings, streaming, software, subscriptions, entertainment, repairs, cleaning services, haircuts, etc.

Certain types of discretionary services – airplane travel, cruises, live entertainment, etc. – got crushed during the pandemic. Revenge spending on some of those services set in some time ago.

Despite the strong growth over the past 12 months, and despite the huge recovery from the knock-out in 2020, spending on services, adjusted for inflation, still hasn’t reverted to pre-pandemic trend:

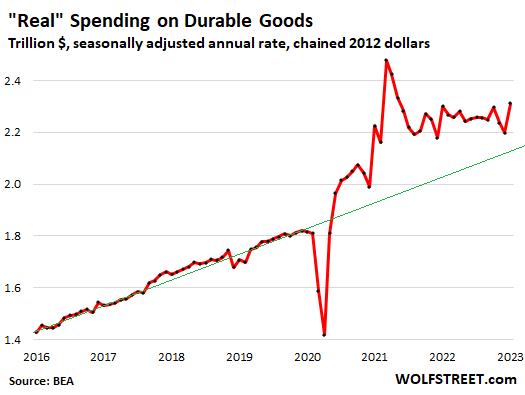

Spending on durable goods, adjusted for inflation, spiked by 5.2% in January, seasonally adjusted. But year-over-year, it was up only 0.5%. The year-over-year figure is key here, and it’s not seasonally adjusted.

I discussed earlier the strength of new and used vehicle sales in January, based on units delivered to end users, that caused used-vehicle wholesale prices to jump again in January and in the first half of February, as dealers bid up prices at the auction to restock their inventories.

After the massively over-stimulated spike during the pandemic, “real” spending on durable goods was supposed revert quickly to the mean, to the pre-pandemic trend, and it did some of that, but nearly two years after the spike, it’s still well above the pre-pandemic trend.

Seasonal adjustments for durable goods in November, December, and January are always huge, as they attempt to iron out the massive spike in spending on durable goods during the holiday season and the plunge in spending in January. These seasonal adjustments are linked. If they’re too aggressive for November and December (pushing seasonally adjusted spending down too far), they’re also too aggressive in January (pushing seasonally adjusted spending up too far), which is what we may be seeing in the above chart.

If you look at the above chart while holding your tongue just right, you can see that spending, adjusted for inflation, roughly flattened out over the past 12 months at very high levels.

This is confirmed by year-over-year spending, adjusted for inflation, but not seasonally adjusted, which ticked up just 0.5% from the very high levels a year ago.

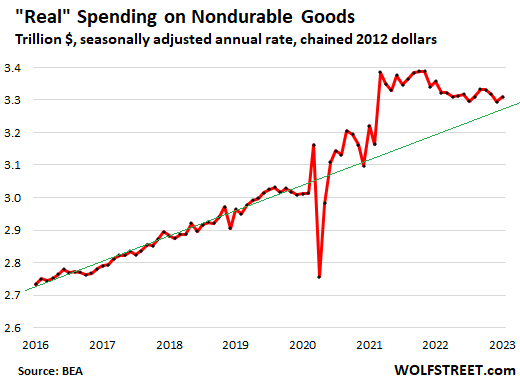

Spending on nondurable goods, adjusted for inflation, rose by 0.5% in January from December, seasonally adjusted, but declined 1.4% from a year ago.

Nondurable goods are dominated by food, energy, and household supplies. We’ve already seen that gasoline consumption, measured in barrels per day, dropped in 2022 in reaction to spiking gas prices. So on an inflation-adjusted basis, consumer spending on gasoline dropped.

Spending on nondurable goods has now nearly reverted to pre-pandemic trend.

The people don’t want this thing to land.

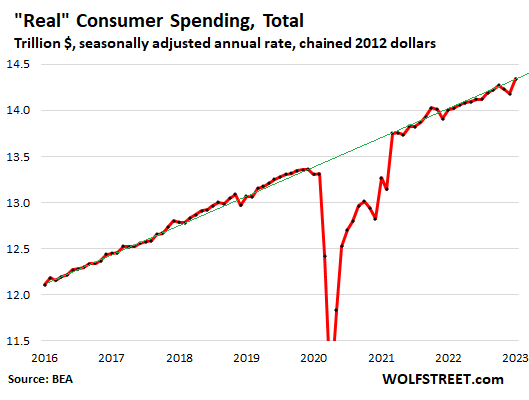

Overall “real” spending growth jumped by 1.1% in January from December, inflation-adjusted and seasonally adjusted.

Year-over-year, not seasonally adjusted, “real” spending grew by 2.4%. In the 10 years before the pandemic, annual growth of “real” spending ranged from +1.4% at the low end (2012) to +3.3% at the high end (2015), and averaged 2.2% over those 10 years.

So the year-over-year growth in January of 2.4%, adjusted for inflation, was just above the 10-year average of 2.2% before the pandemic. This is not the sign of any kind of landing. Clearly, people don’t want this thing to land.

Note the quirks of the seasonal adjustments in the Novembers and Decembers of 2021 and 2022, when seasonal adjustments may have pushed down spending figures too far, and then conversely pushed up spending figures too far in the Januaries of 2022 and 2023. These quirks are largely related to durable goods, as we saw above.

The month-to-month seasonal adjustments, which are based on the history of seasonal swings, have been a little rough since March 2020, when radically different consumer spending patterns distorted everything and threw all historic patterns out the window.

But year-over-year spending growth (+2.4%) is not seasonally adjusted.

And the chart shows the trend – the continued strength of spending growth despite the quirks in Novembers and Decembers (when the media proclaimed the demise of the consumers), and Januaries (when the media proclaimed the resurrection of the consumers), when in fact, these consumers were plodding along just fine, energetically outspending inflation:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

There’s a lesson here.

The Fed has NO control over supply.

No, the lesson is this:

If the Fed boosts demand out the wazoo by repressing interest rates and printing a $5 trillion, there there’s suddenly a shortage of supply to meet this out-the-wazoo demand.

If the Fed throttles demand with high-enough rates, there’s suddenly plenty of supply.

Supply and demand are not isolated from each other. What you put out there is a simplistic statement that’s popular with the we-want-our-free-money-back crowd.

I think you’ve crystallized my thoughts eloquently Wolf.

So you blame the Fed for all the free money? I was pretty sure that Pelosi and her crew authorized trillions. And the Fed got past Valentines day. Don’t expect 0.25%.

why don’t republicans see the money their presidents printed when they were in the office? trump threatened Powell not to raise rates while printing trillions of dollars. what are you on Stevo?

@Ben:

I think everyone sees it, regardless of who is “in charge”. However, in this case it was unprecedented in the history of the United States.

So the fix is clear: Multiple more 75 basis point hikes.

But, but, but, the fed is ready to pivot.

/s

LOL …. I love your responses as much as the editorial.

The artificially high asset prices make productive businesses un-profitable. So, asset bubbles do reduce productive investments and promote non-productive speculation like bitcoins and spacs.

This also means that current high inflation is both from supply decrease and demand increase.

This is an important point that is never talked about enough. Real estate bubbles destroy economies. They make it impossible for businesses to thrive because high rents and purchase prices suck out all of the profits and then some.

Wolf has talked over the past few years about all of the new businesses opening up. I can tell you first hand that they are failing just about as fast as they open. This is nothing new, of course, but I think the rate of failure is much quicker than in past times.

I have seen a number of coffee shops and restaurants fail to make it 12 months. Part of this is a bad business plan, of course (I can’t imagine opening a business without a few years of reserves), but the locations are super high rent and the landlords are basically sucking them dry.

Back in the old days, you could purchase a modest location for a small business and pay for it with the business revenue. Those days are long gone.

DC,

I recently watched a video of a guy interviewing people leaving a luxury designer store. The interviewer wanted to know who buys this stuff and asked about professions and income. Out of less than a dozen people the majority were doctors and real estate investors, who knew, the bloodsuckers.

DC nails it. High rent prices kills business. I’m in a very high rent area and there’s very few start ups. Lots of food trucks though. High housing prices kills job mobility, and sucks more resources from potentially productive areas of the economy – areas that might actually produce things beside fancy kitchen counter tops and flooring.

DC – a very old (okay, going back 35 years or so, probably longer) small-biz ‘rule of thumb’ was to be prepared to run in the red for at least your first 18 months assuming the rest of your diligence had been duly done…

may we all find a better day.

I tend to agree with Depth on this (alleged new biz creation…which lately is being reported as some unbelievable percent of total *existing* businesses.)

If a few million laid off people hang out shingles as solo “consultants” LLC…i don’t think 97% of those “companies” will exist in 2 years.

I don’t think the fed has as much control as they like to think they do.

The housing market is a great example. The rate shock has frozen the market more than anything it seems. The bay area price drop Wolf showed us simply isn’t happening in my market.

I think it’s that simply that population is steady or growing and new supply is rate constrained.

It makes me wonder whether other capital intensive industries can’t overcome obsolescence and casualty events with cheap debt to maintain supply.

So on the converse, how much longer until QT suppresses demand.

From July 1980 to December 1980, the FFR jumped almost 990 basis points. We’re not even 1/2 there yet and we’re 12 months into hikes vs 5 months. In addition to being WAY late to the party, the Fed is raising the FFR too slow as well. We should be at 5.5% already.

Personally, I think around April / May everyone had better get ready for a 6% FFR. And even that might not be terminal, because I don’t see food, rent or fuel costs dissipating over the next 6-9 months.

Rev Repo’s are still above $2.1T, so QT isn’t exactly sopping up all that extra liquidity. And, I doubt it will given that the Fed is paying something like 4.3%.

Credit card debt & car loans are starting to look like they’ll become a REAL issue by later this year.

Be that as it may, I’m extremely pleased with 30YFRM is headed back up to 7%, and I look forward to your MBS runoff analysis showing that it will not meet the Fed’s runoff schedule as you suggested on 2/8.

I’m not sure that it matters though, since the MBS runoff seems to be the least of the Fed’s worries right now. And in general, I don’t see where there’s OBVIOUS signs that QT is actually doing anything to slow down the overall economy.

Cheers!

Precisely my point below that very few understand: QE/QT has ZERO, I repeat ZERO impact on demand.

It is strictly a supply-side lever. So to answer your question, QT will never suppress demand – the irony is that it actually suppresses supply.

Qt in selling mbs will force price discovery in residential and commercial real estate when other holders of mbs sell to retain profit/ caurterize losses.

I think it will facilitate a reckoning more quickly upon which one hopes organic economic growth can be fostered and of courses aided by more demand based qe or fiscal spending.

At least that’s my hope and I’m short cmbs, lol

Government manipulated markets are not Free Markets.

The entire premise is wrong and destructive, has been for decades.

We do not have free market capitalism. We have a heavy handed form of corporatism based on massive government debt in multiple layers.

Right you are CJ

“We have a heavy handed form of corporatism based on massive government debt in multiple layers.”

Fiscal fascism.

Or Keynesianism.

(It is possible to sympathize with what the G tries to accomplish. In year one. But after 20 years of perpetual failure, it becomes impossible to see it as anything more than self-serving fiscal fascism…implicating both the G and a tight subset of the Corporate community…who cannot survive without the G’s largess).

The key thing many don’t understand about this as it relates to what you just said: QE is DEFLATIONARY. It sends capital to supply, whereas ZIRP and direct payments are what caused the demand boom.

In essence, the Fed is swimming upstream right now. It is performing QT, an inherently inflationary act, while raising interest rates, an inherently deflationary act, which is why you see broken markets everywhere, especially real estate. The Fed is killing both supply AND demand at the same time, and should they continue on this path, the only way they get their 2% is by raising rates so high that demand for everything is nuked.

FFR to 7% before EOY. Heard it here first.

Odds of that about one in a million.

Fed will have no choice – they are completely boxed in and credibility is their #1 priority. They can’t change their target too significantly or risk everyone figuring out the emperor has no clothes.

You aren’t going to see meaningful reversion to 2% with PCE figures like this and UE still at record low levels. Not happening.

7% is FAR more likely than 1 in a million and nobody sees it coming.

The interesting piece is that concumer price indexes and spending is up even with deflation measured on both M2 and M3.

On the other side, there was a lot of inflation measured both on M2 and M3 for a long while without that affecting the consumer price index.

This may show that the consumer price index is not that well suited to measure inflation.

Money supply has no relevance for consumer price inflation (= rising consumer prices). Consumer price inflation is what all this is about.

If monetary supply do not have any relevance on consumer price index, QE, QT and interest rates should not have any influence on the consumer price index.

Then, the central banks manipulate the monetary supply with QE, QT and interest rates to influence the CPI. Or at least say so. Why, if the money supply have no relevance on CPI?

For over a decade, the impact of QE was exclusively on asset prices, not consumer prices. So we got a huge amount of asset price inflation. With the pandemic, the government sent trillions of dollars directly into the economy, on top of QE and supported by QE, and that changed everything. Now it’s a mix that is causing inflation, in addition to other factors, and the guesses are all over the place as to what extent QT is causing it, to what extent the government pandemic spending triggered it, and to what extent other factors caused it. The amazing thing is that the sources of consumer price inflation are badly understood – for example, it is now assumed that mass-psychology plays a role (the “inflationary mindset,” as I call it) – and are hard to pin down.

Food prices are still rising at my local grocers in mid-town Toronto.

It’s an insult for the central bankers like Tiff Macklem to put rate hikes on pause when prices are still rising.

It is a repeat of “inflation is transitory” fiasco by J Pow.

Bases on how it turnedbout, we shold probably get ready for 20% inflation and 15% interest rate by mid 2024.

The economy is not a counter, there are two positions on and off.

Rather, it is something like a thermostat that is adjusted in units of degrees. If you sharply increase the temperature or decrease it, you may overload the power supply and the device will burn

You mean the lagging impact of real negative rates today will be same as the lagging impact of real negative rates during the “Inflation is transitory” Era!

Thanks for confirming my theory!

No, I’m more of Wolf’s view that it’s better to tread carefully than to break the economy to clear the way for 0 interest rates and QE again

“No, I’m more of Wolf’s view that it’s better to tread carefully than to break the economy to clear the way for 0 interest rates and QE again”

You’re making false assumptions that raising the fed funds rate above CPI would somehow “break the economy.” Never in history has inflation above 5% come down with a fed funds rate below CPI. So, the “pause” at a rate below that of CPI is just another BS experiment, erring on the side of bubbles and high inflation rather than doing what’s necessary. I’m tired of this gotdamn nonsense, to be honest.

In my country in 1996 there was hyper inflation. The government introduced a currency board and raised interest rates. Many banks went bankrupt. Many companies went bankrupt. Unemployment was rampant. I remember it wasn’t until 2001 that interest rates fell and the economy was going again, but interest rates fell so low (for our COUNTRY) that 2004 the financial bubbles were already red-inflated to burst in 2009. What I’m saying is that it’s good to look for the gold environment, the balance and not to stagger in the extremes.

Curious to see reactions next month when these strong numbers flip to very weak.

Also, seems like some need to revisit the basics. Lagged impacts.

You mean the lagging impact of real negative rates today will be same as the lagging impact of real negative rates during the “Inflation is transitory” Era!

Thanks for confirming my theory!

““Right now … M2 … does not really have important implications. It is something we have to unlearn I guess.” J Powell March of 2021

Just before the “transitory” inflation explosion.

Maybe we should “relearn” what the supply of money means as a predictor of inflation….right Jay?

I find it hilarious the Fed can “overshoot” with stimulus and keeping rates lower for longer but god forbid they overshoot with QT and higher rates.

+100.

Every single move is to benefit the wealthy. Every single consideration is with them in mind. Show up in a minute to support the asset prices of the rich, wait years to address inflation that destroys the middle class and the poor while paying them a little lip service with “we know how tough it is” or some such.

“The risk of doing too little outweighs the risk of doing too much.”

~Jerome Powell

***proceeds to do too little***

“All you do to me is talk, talk

Talk, talk, talk, talk

All you do to me is talk, talk

Talk, talk, talk, talk

All you do to me is talk, talk”

~Talk Talk

Why? It makes perfect sense. Asymmetry.

Summed up, I think it’s because easing is always in the face of an acute crisis while tightening is usually in situations of less urgency. Say what we want about our current situation, and how the Fed should have done this or that (and they should have), but the situation we face now is nowhere near as bad as when they “rescued the economy” (or so they think) in 2020. Sure, it sucks now, many are getting crushed, however look at those charts. ON AVERAGE, this is not yet that painful for the majority.

Because the votes don’t vote because their inflation is a solid D. Heck they don’t even cut back on sentiment and spend. They can and do vote if they or their partner loses their job, and it’s usually the fed that gets vilified unless inflation is godawful. It’s why shorts and gold bugs are 80% of the inflation hawks.

This inflation sucks, for sure, but if you polled you have decent odds for a layoff but 2% or no layoffs but inflation might be 4-8%, what do you think the polls would say?

Nate, Won’t the answers often vary by age? A 50 year old with a decent salary but relatively poor prospects on the job market may hope that his zombie company will stay alive long enough to keep him in his home and pay his pension. Seems to me 25 year old is probably not going have as much to lose from a job loss and may even benefit from a lower chance of stumbling into employment with zombies. So it seems there may be some intergenerational conflict there.

No one in Canada dissects the CPI report for January which no one believed. The bond market fell the second the January CPI was released. The math I did put the CPI at 7 percent even. One of the reasons Tiff paused interest rate hikes is its a component of the CPI, the mortgage interest. They’ll already trying to skew inflaiton lower and now back averaging the CPI by a year. It’s criminal and will lead to longer term inflation.

Macklem is a hack but not because he paused. The Canadian economy has the burden of being massively dependent on two sectors – real estate and retail / commercial banking. The bubble in both has shifted potentially productive investment into productivity sink holes. The lack of proactive signaling of those bubbles (and indeed exacerbation during the lockdowns) put the Canadian economy on a very different edge than the US.

If you think US real estate markets got “frothy” Canada’s was already in looney land before rising 20%-30%+ more. We could reasonably see a further 30% decline from here and affordability would still be worse than the US. Of course the follow-on effects due to second order dependencies would be dramatic. RE in Canada’s economy (direct and indirect) is nearly 2x the relative size as in the US. The situation there could turn very hairy, very quickly.

Classic inflationary spiral. People are outspending the raging inflation because they expect inflation will get worse and have no faith in the government to stop it. Better to buy it now before it becomes even more expensive next year. And it also likely implies nobody expects a recession either.

Exactly,we the peon,s are not as dumb as politicians think we are . But as long as there,s food there,s peace. God bless romearica

Yes, “As long as there is affordable food and electricity ……”

God Bless America.

Yes, “As long as there is affordable food, electricity, and coffee…..”

God Bless America.

I attribute it to most Americans won’t reduce their consumption or living standards voluntarily, whether they can actually afford it or not.

In my apartment complex which is marketed as “upscale”, management recently introduced by-monthly payments. The demographics have clearly shifted in the last two years since I moved and it’s at least partly due to this change.

This tells me that many of the residents potentially can’t actually afford to live here.

Concurrently, the parking garage has no shortage of pricier cars.

I’m looking to move when my lease is up.

If your landlord needs to get paid twice a month, they obviously need the money. Offer to pay several months in advance for a discount.

P: I think the bi-monthly payments are an inducement for the lessees, not the lessor. I believe his point is that the quality of the residents of the “upscale” residents has deteriorated.

…hm, perhaps a strategy being borrowed from the by-the-hour ‘no-tell motel’ business?

may we all find a better day.

“I attribute it to most Americans won’t reduce their consumption or living standards voluntarily, whether they can actually afford it or not.”

^^^^^ This.

A family of four, both adults work. One kid in grade school the other in daycare. They have a mortgage at 2.5%, two car payments as they both work.

Car insurance, health insurance, some 401k contributions, HSA because kids. Food, utilities, gas for the cars, the kids grow and the schools as for supplies. One of the adult’s parents is ill and needs some help with either their bills or medical expenses. Plus, some time at home help.

They mostly cook at home, shop the sales. The ice maker in the frig decided to leak last week, so they turned it off.

As a silver lining to these inflationary times, I am curious to see at what level do consumer credit card apy start causing some pullback. Average apy look to be a 30 year high at around 20%, which is kind of amazing. BK lawyers are going to be BUSY whenever the recession arrives.

Anyone know what organized crime used to charge before they decided to do away with usury?

Credit card companies are organized crime…HA…although they don’t make you pay with your life instantly, just slowly…

Yet CC companies do tend to follow the rules they lobbied/bribed for with the congress/mafia.

The smartest change in the banking system was to get rid of “debtors prison”, as it is much more profitable to milk impossible to pay off debtors for life versus keep them behind bars. Best keep them as cogs in the corporate wealth machine.

Nate,

The “local” lenders charged 10% a month back in my youth.

$5 loan cost $7 at the next ”pay day” in navy in mid sixties — either on ship or ashore…

Had to have some beef/brawn with ya to collect, and stand in the next compartment from the paymaster doling out the cash.

NOT fun for anyone participating,,,

Almost as bad as the payday crap games where very few folks had any clear knowledge of the odds.

Both dangerous — kinda like any financial transaction these days outside of mainstream.

Still too much stimulus money out there and we’re not in a recession yet. Calm before the storm is all this is.

Actually, there is alot less fluff in current spending than many think. People are doing major repairs on everything. They went 2-3 years spending nothing during covid and meanwhile everything wore out.

Tony…yes

Everyone speaks of the delay in the impact of raising rates.

But there is also a delay in the costs of production and wage acceleration.

There are plenty of unions poised to go on strike as wages have not kept up with inflation.

Replenishing inventories is also more costly.

Price of coffee just jumped about 25% where I am, among other things.

I don’t think that they are outspending inflation. I think inflation is underreported which makes it look like real spending is increasing.

Consider a situation where the real inflation rate is 20% but the reported inflation rate is 5%. A 10% increase in nominal spending would look like a 5% increase in real spending. The actual answer is that it would be a 10% decrease in real spending.

Coffee doubled in my area Nebraska,But inflation is only 7.6% Bullshit .As they sat if you will eat it ,they’ll fed it to you

Three reasons to think the Fed was just bluffing:

1- Likeminded BoE bought gilts to “save” pension funds despite high inflation

2- 2023 Federal budget was a blowout. Passed AFTER the 2022 election.

3- NYT and other mainstream media keep hyping Jerome’s supposed “resolve” to fight inflation. Arguably the “expectations channel” may have been needed to push up inflation at the ZLB, but there’s no need for elaborate telegraphing of expectations in the other direction unless they are bluffing.

“1- Likeminded BoE bought gilts to “save” pension funds despite high inflation”

It bought just a small amount, and then sold all of them two months later. That was just a small brief market intervention, now reversed, to keep a death spiral from playing out:

https://wolfstreet.com/2023/01/12/bank-of-england-sold-all-bonds-it-bought-last-fall-amid-pension-crisis-first-big-central-bank-to-sell-government-bonds-outright/

The more I read here the more I am thoroughly convinced that inflation will not abate until Fed rates are far above that rate.

The Fed will get there but I think they don’t realize that a soft landing is not coming. If you kill demand then you kill jobs and then the economy stutters.

So I’m now likening it to a 20,000hp cargo ship. They will eventually turn it around, but once it turns it is not just going to turn right back again, not without some significant headaches and cost.

I hate that people are going to lose jobs and families are going to suffer. That’s the unfortunate side of a winner take all society. But the hyperconsumptive lopsided society we have created can crash for all I care. I’m getting tired of seeing labor so devalued and white collar work and asset collector wealth so overvalued. That’s what the pandemic has done to me, it’s given me a burn it down attitude, and i just don’t care anymore.

“it’s given me a burn it down attitude, and i just don’t care anymore.”

I LOVE THIS GUY.

It is certainly a growing club.

This Fed funny pic (link below) sums up and lightens the mood with the Fed burn it all down theory. I have it under one of my trading screens as a reminder to be careful as one of our village idiots is running the entire global financial system, and they are as clueless as anyone else in how this grand multi-decade experiment resolves itself over time…

Opposite. The Fed WAS burning it down with QE and free money. Now it’s trying to extinguish the fires it lit up.

“Opposite. The Fed WAS burning it down with QE and free money. Now it’s trying to extinguish the fires it lit up.”

So we do agree. Then why do you accuse me of “wanting to burn it all down” because I’m in favor of larger rate hikes until the fed funds rate exceeds CPI? I want more of the firehoses to extinguish the inferno.

Remember the worry of inflation becoming “entrenched?” The longer they take, the more of a chance it becomes entrenched – which by the way is starting to become a headline again.

White collar work is not overvalued. People with high demand skills are in high demand. It’s really quite straightforward.

Correct. The issue is actually the opposite. Lower skill jobs got a boost that won’t trend well. In other words, many businesses over-capacitized for an economic base that was artificial (stimulus/money supply).

This happened in the years leading to the financial crisis. Economy increased capacity for artificial (temporary) demand increases that were driven by speculative asset value increases (home prices rise —> heloc —> spend).

This unwind is happening now and anyone who wants the Fed to move higher and higher today misunderstands how this deleveraging happens (hint, not instantaneous).

I disagree. Some white-collar work is necessary and of high value to society: Research Scientists, Doctors, Engineers, etc.

Other high-paying white-collar jobs are created by and for other highly-paid white-collar types to keep the scam going: CPAs (via a ridiculously complex tax code), Lawyers (via a legal code that enables “sue-happy” leeches), College Administrators (via a disastrously misguided student load program so “everyone” can go to college), etc.

Value is a subjective word, obviously, and from a larger perspective demand created by and for “white-collar” types is a drain on the societal organism that offers no value, except, of course, to the parasite.

Sue-happy.

Until you deal with an incompetent doctor that causes brain damage to your kid. Or a greedy corporation that decides your car exploding on impact is worth saving 35 cents in parts.

As for CPAs or a host of other professionals, let’s compare the countries with the highest corporate sophistication and their standards of living to countries that don’t have these layers in place.

The brain dead aren’t limited to zombie apocalypse films.

…so, are we reducing the size of the ship to compensate for the numbers of crew to man it? Even if it’s considered ‘right-sizing’, what happens when those condemned to walk the plank seriously respond, asking: ‘…right for who?…’?

may we all find a better day.

Lol guys who can afford lawyers, cops, and IRS auditors love useful idiots like you. you are free to go cheap or diy, it’s a free country. Just like you’re free to not get health or property insurance. But don’t blame the system if things go sideways.

For example, the guys with lawyers figured out how to send you to kangaroo court, that they mostly fund, if they screw you over on a contract. And you, bless your heart, voted for the dudes who passed their laws because you thought it was fair. The heaviest users of the legal system were and continue to be Corporate America.

Degobah, you’re romanticizing these professions. There are plenty of engineers, scientists, and the other professions that you think are “worthy” that are paid well to do worthless work and develop worthless products. If you’re going to pick and choose, you need to revisit the economics of the Soviet Union – a command economy. If you want free enterprise, you’ll have to sit on your hands and hope that better mousetraps are actually built.

I Musk’s Twitter purge proved that theory wrong.

Raising rates ABOVE inflation was always the right move but the FED is now controlled by the elected majority and that was not gonna sit well with them.

Happy Jack

Notice the “gaslighting” of the Fed.

1. 2% inflation is the same as “stable prices” (since 2008)

2. Fed Funds now belong under inflation (since 2008)

and the dearth of any intelligent inquiry by those at hearings and testimonies involving the Fed.

Raising rates above actual inflation is the right move. Raising rates above a falsely reported inflation rate will not stop inflation. Dishonest accounting and tricks which justify statistical lies don’t change the underlying facts. Rates must be raised above real inflation to reduce real inflation. Fantasy rate hikes don’t work in the real world.

The economy is based on demand. If demand increases, companies will increase prices to the point where demand declines or disappears. So, inflation happens when demand is great, supply is trying harder to keep up with demand, and each link in the chair of producers are raising prices as high as they possibly can, until they slow or stop demand.

Credit is what companies use to increase their production. If they can borrow at rates that allow them to be profitable, or increase their profitability, they borrow. If the cost of borrowing starts to strangle their profitability, they stop borrowing and cut production. No company wants to produce stuff at an operational loss (unless the company is a unicorn, a sinkhole for investments).

The Fed’s lowering and raising of rates ultimately can stop inflation but at the cost of slowing the economy. If the raising of rates to too precipitous (e.g. Volcker…finally), then the economy has a seizure.

But the blame rests with demand. If demand stops, supply will stop, not the other way around. If the industry is mostly “discretionary”, it will be the first to slow or shutdown. As supply for essentials (necessities) gets harder to obtain, the supply will get costlier, and that will diminish demand, so demand is still at the helm. A worst case scenario is when supply of essentials is so costly (wheelbarrows of money can’t buy it) that it is unaffordable and we revert to survival of the fittest and return to cave-dwelling. Over time, the outrageously-inflated housing market will become an archeological artifact.

Pray for a balance of supply and demand and a balance of credit and the cost of credit. Don’t pray for a slamming on the brakes or a panicked Federal Reserve that has to respond to cardiac arrest.

Please explain the points of comparison. 1 year t bills are over 5%. 1 year inflation outlook is closer to 3-4%. Where is the negative real rate?

Or do we prefer mixing up the time frames and deciding policy should be backward looking? Is that how you drive, looking through your rearview mirror?

Let’s check back in 12 months and see where real rates end up.

I can’t say this enough times. The Fed is not serious about inflation. If they were, they would have increased the pace of QT and raised rates faster. They like inflation right where its at, at about 4%. Don’t ask me why they want that, but it is clearly what they are shooting for, because that is the runway they are clearly managing this economy to land on, in spite of lip service.

When you approach a stop sign you can either take your foot off the accelerator and gently apply the brakes or wait until the last minute and slam them to stop. I think the FED cares about inflation. If they don’t address inflation the economy will stall. However you also have the nut jobs in Washington spending with reckless abandon so they need to absorb the overspending. Neither Washington or the FED is our friend. The FED is gentling pumping the brakes worried about both the inflation rate and spending. From your and my perspective they should aggressively raise rates. They will not do that because the don’t want a recession but they will not necessarily raise rates rapidly as long as the government continues to overspend. I am not so sure J Powell is a secret Paul Volker. Remember when they said they would let inflation run hot?

The only way to stop inflation without causing a deep recession is to shut it down before it can be entrenched. The real revelation in Wolf’s current article compared to all he previously published is that it is now obvious inflation has become entrenched. The Fed had a short window to address that problem with appropriate policy actions, and the window is now closed.

“The FED is gentling pumping the brakes worried about both the inflation rate and spending. ”

By gently pumping the brakes you will eventually stop, probably beyond the stop sign and in the middle of the intersection where you will be hit by that inflation 18-wheeler.

TXRancher:

Powell and his coterie are not in the car. It is a remote-controlled car that they are driving from their Ben Bernanke chopper. So they are not too worried about stopping in the intersection or the impact from the 18-wheeler. LOL.

I think we need wore time for the rates to burn through the economy. Residential real estate is going to burn to a crisp with 7% mortgages. Last housing cycle 400,000 real estate agents got out of the business and we are way above the peak numbers of agens, so could be 600,000 this time.

Remember when all the housing sub contractors and their employees lost their jobs the last housing bust. It wiped out a lot of people. The process is under way.

I tend to like your comments, O.S. Less panic, more reasoning. And I do remember when those subcontractors were out scratching around for “other” types of work. Same for the collapse of the farming businesses when farmers were losing their multi-generational family farms due to borrowing against them to buy Deere machinery on the temporarily inflated value of those farms.

It’s too bad that younger people have absolutely no concept of these events.

Watched the evening news where auctioneers were selling farms and equipment while the owners were actually crying, filled with regret, over the loss of their family farms.

Read WSJ article describing how foreign investors were buying farms and farm equipment at a dime to a dollar. Same storyline when oil prices dropped precipitously in the late 80s. Drilling equipment selling for pennies on the dollar.

“…until Fed rates are far above that rate.”

The Central Bankers have trained people for 14 years that FFR should be under inflation…..real neg rates is the game…and it STILL goes on.

Burn it down sounds fine, as long as you don’t think you will be one of those burned. But you will be. And if you have kids, they will be burned as well.

Maybe you don’t have kids. Maybe your parents will be the ones to have their retirement wiped out.

Take a look around, it isn’t just about you.

Raise high the interest rates, Powell!

There is a lot of hyperventilating about inflation, a lot of exaggeration about how it’s headed for the moon, Alice. Here’s something to consider:

From 1967 – 1984 the average inflation rate was 6.9%! It reached a low of approx. 2% in ’67 and again in ’84. So, for 17 years, the Fed was no where near its “2% target”.

In contrast, the Fed has kept the inflation rate to about 2% from ’91 – 2020, preCOVID.

Bitch loud and hard, but they’ve done a good job with inflation, with all kinds of competing challenges (including a near bank failure in ’08 and a pandemic), so lighten your asses up a bit.

Here’s a list of inflation over nearly 100 years:

U.S. Inflation Rate History

yoy inflation

1929 0.6% NA August peak Market crash

1930 -6.4% NA Contraction (-8.5%) Smoot-Hawley

1931 -9.3% NA Contraction (-6.4%) Dust Bowl

1932 -10.3% NA Contraction (-12.9%) Hoover tax hikes

1933 0.8% NA Contraction ended in March (-1.2%) FDR’s New Deal

1934 1.5% NA Expansion (10.8%) U.S. debt rose

1935 3.0% NA Expansion (8.9%) Social Security

1936 1.4% NA Expansion (12.9%) FDR tax hikes

1937 2.9% NA Expansion peaked in May (5.1%) Depression resumes

1938 -2.8% NA Contraction ended in June (-3.3%) Depression ended

1939 0.0% NA Expansion (8.0% Dust Bowl ended

1940 0.7% NA Expansion (8.8%) Defense increased

1941 9.9% NA Expansion (17.7%) Pearl Harbor

1942 9.0% NA Expansion (18.9%) Defense spending

1943 3.0% NA Expansion (17.0%) Defense spending

1944 2.3% NA Expansion (8.0%) Bretton Woods

1945 2.2% NA Feb. peak, Oct. trough (-1.0%) Truman ended WWII

1946 18.1% NA Expansion (-11.6%) Budget cuts

1947 8.8% NA Expansion (-1.1%) Cold War spending

1948 3.0% NA Nov. peak (4.1%)

1949 -2.1% NA Oct trough (-0.6%) Fair Deal, NATO

1950 5.9% NA Expansion (8.7%) Korean War

1951 6.0% NA Expansion (8.0%)

1952 0.8% NA Expansion (4.1%)

1953 0.7% NA July peak (4.7%) Eisenhower ended Korean War

1954 -0.7% 1.25% May trough (-0.6%) Dow returned to 1929 high

1955 0.4% 2.50% Expansion (7.1%)

1956 3.0% 3.00% Expansion (2.1%)

1957 2.9% 3.00% Aug. peak (2.1%) Recession

1958 1.8% 2.50% April trough (-0.7%) Recession ended

1959 1.7% 4.00% Expansion (6.9%) Fed raised rates

1960 1.4% 2.00% April peak (2.6%) Recession

1961 0.7% 2.25% Feb. trough (2.6%) JFK’s deficit spending ended recession

1962 1.3% 3.00% Expansion (6.1%)

1963 1.6% 3.5% Expansion (4.4%)

1964 1.0% 3.75% Expansion (5.8%) LBJ Medicare, Medicaid

1965 1.9% 4.25% Expansion (6.5%)

1966 3.5% 5.50% Expansion (6.6%) Vietnam War

1967 3.0% 4.50% Expansion (2.7%)

1968 4.7% 6.00% Expansion (4.9%) Moon landing

1969 6.2% 9.00% Dec. peak (3.1%) Nixon took office

1970 5.6% 5.00% Nov. trough (0.2%) Recession

1971 3.3% 5.00% Expansion (3.3%) Wage-price controls

1972 3.4% 5.75% Expansion (5.3%) Stagflation

1973 8.7% 9.00% Nov. peak (5.6%) End of gold standard

1974 12.3% 8.00% Contraction (-0.5%) Watergate

1975 6.9% 4.75% March trough (-0.2%) Stop-gap monetary policy confused businesses and kept prices high

1976 4.9% 4.75% Expansion (5.4%)

1977 6.7% 6.50% Expansion (4.6%)

1978 9.0% 10.00% Expansion (5.5%)

1979 13.3% 12.00% Expansion (3.2%)

1980 12.5% 18.00% Jan. peak (-0.3%) Recession

1981 8.9% 12.00% July trough (2.5%) Reagan tax cut

1982 3.8% 8.50% November (-1.8%) Recession ended

1983 3.8% 9.25% Expansion (4.6%) Military spending

1984 3.9% 8.25% Expansion (7.2%)

1985 3.8% 7.75% Expansion (4.2%)

1986 1.1% 6.00% Expansion (3.5%) Tax cut

1987 4.4% 6.75% Expansion (3.5%) Black Monday crash

1988 4.4% 9.75% Expansion (4.2%) Fed raised rates

1989 4.6% 8.25% Expansion (3.7%) S&L Crisis

1990 6.1% 7.00% July peak (1.9%) Recession

1991 3.1% 4.00% Mar trough (-0.1%) Fed lowered rates

1992 2.9% 3.00% Expansion (3.5%) NAFTA drafted

1993 2.7% 3.00% Expansion (2.8%) Balanced Budget Act

1994 2.7% 5.50% Expansion (4.0%)

1995 2.5% 5.50% Expansion (2.7%)

1996 3.3% 5.25% Expansion (3.8%) Welfare reform

1997 1.7% 5.50% Expansion (4.4%) Fed raised rates

1998 1.6% 4.75% Expansion (4.5%) LTCM crisis

1999 2.7% 5.50% Expansion (4.8%) Glass-Steagall repealed

2000 3.4% 6.50% Expansion (4.1%) Tech bubble burst

2001 1.6% 1.75% March peak, Nov. trough (1.0%) Bush tax cut, 9/11 attacks

2002 2.4% 1.25% Expansion (1.7%) War on Terror

2003 1.9% 1.00% Expansion (2.9%) JGTRRA

2004 3.3% 2.25% Expansion (3.8%)

2005 3.4% 4.25% Expansion (3.5%) Katrina, Bankruptcy Act

2006 2.5% 5.25% Expansion (2.9%)

2007 4.1% 4.25% Dec peak (1.9%) Bank crisis

2008 0.1% 0.25% Contraction (-0.1%) Financial crisis

2009 2.7% 0.25% June trough (-2.5%) ARRA

2010 1.5% 0.25% Expansion (2.6%) ACA, Dodd-Frank Act

2011 3.0% 0.25% Expansion (1.6%) Debt ceiling crisis

2012 1.7% 0.25% Expansion (2.2%)

2013 1.5% 0.25% Expansion (1.8%) Government shutdown. Sequestration

2014 0.8% 0.25% Expansion (2.5%) QE ends

2015 0.7% 0.50% Expansion (3.1%) Deflation in oil and gas prices

2016 2.1% 0.75% Expansion (1.7%)

2017 2.1% 1.50% Expansion (2.3%)

2018 1.9% 2.50% Expansion (3.0%)

2019 2.3% 1.75% Expansion (2.2%)

2020 1.4% 0.25% Contraction (-3.4%) COVID-19

2021 7.0% 0.25% Expansion (5.9%) COVID-19

2022 6.5% 4.25% Contraction (-1.6%)

2023 2.7% (est.) 2.8% (est.) Expansion (2.2%) March 2022 projection

2024 2.3% (est.) 2.8% (est.) Expansion (2.0%) March 2022 projection

HowNow,

“From 1967 – 1984 the average inflation rate was 6.9%!”

Yes, now go check the average mortgage rate between 1967 and 1984, LOL.

That’s why people are hyperventilating about inflation because no one wants to go back to 15% mortgage rates.

“People want to get on with their lives, it seems. Their mood has improved. They’ve gotten used to living with high inflation. They got raises or got higher-paying jobs.”

Can’t agree with this at all. I don’t know anybody whose actual earnings are outpacing inflation, only asset holders who have benefited from the run-up and are partying like 2005 on steroids. The rest are absolutely miserable. I have never seen and heard of so many depressed people in my life.

I agree, but there are two Americas. And it’s not red vs. blue America. It’s pre-pandemic major asset holders vs those who weren’t. That’s the division. The first group is living large.

This is the case. I make good money but wasn’t an asset holder going into covid. I’ve been left in the dust. People here have their homes, and their homes have funded their 2nd homes, Sprinter Vans, remodels… $10k bikes, whatever it is. There is a clear divide, and it just appears to be growing. I pay my rent, contribute to 401k and other investments, and try to keep a little down payment fund that has NOT kept up with inflation.

There is too much consumption now and for the last 2+ years for it to be as clear cut as you imply.

The top 5% or 10% has carried this fake economy since 2009, accounting for most growth, but there must still be plenty of others living above their means and not all of them are working stiffs either.

AF,

I am one of the ones who has spent a lot(for me) in the past two years. Almost all of the spending was necessary. Expensive car repairs for two cars, both over 7 years old. New bed and mattress, both old and broken. New clothes and shoes, a lot of items were very worn out, replaced with nice things bought on sale mostly. Kitchen items replaced because we cook at home daily. And we make it a point to dine out at nice places for special occasions because we rarely go out. But even all of this is not as much as the cost of healthcare and insurance in the past two years. We are getting older and ageing is expensive in America.

Some people are probably tapping into their retirement savings to keep up their lifestyle, even if there are early withdrawal penalties.

Yep that’s my take on it too. Add to that the boomer retirement peak just happened (last year mol) and they are the main asset holders who are partying their guts out probly.

My bet is it’ll last another couple years and they’ll realize they gotta pull in their horns some. The market has only dropped from a 5x their money since 2008 to a 4x now so the pandemic asset premies have plenty of rope left.

*since 2009…

Tony….two Americas…indeed.

Country Club memberships …. sharply higher prices and long waiting lists.

and then the others…..

Yes CC memberships in smaller town where I live is up from please join to 5k and a waiting list . Plus yearly dues linked to CPI . Owned by a PE company. I dropped my membership in 2017 as the monthly rates outpaced my flat income .

Two Americas….the 50% or so, that don’t have $500 dollars spare and the 50% that do….

People are spending like there is no tomorrow.

Just wait until they find out they are right.

The people I know all have their head in the sand. They don’t think about inflation as in, spend it now before it’s worth less. If you think that you are projecting. When I bring up the subject my friends literally start saying NAH NAH NAH, I can’t hear you.

10s of millions of jobs wouldn’t exist without cheap money. The businesses they work for can’t survive *normal* rates. This is the only thing that will change behaviors — when those living paycheck to paycheck no longer have one.

Yes, agreed, there are many jobs/companies out there that would not exist without the cheap money. I just retired early from a retail company that originally filed bankruptcy in 2009, it should have gone out of business then. It survived due to the cheap money and then filed again in 2019. It is still in business due to the cheap money but won’t last this time around once rates stay high. I often wonder how many more are out there. Luckily I was near enough to retirement to bail out.

Spending for discretionary services such as restaurants, bars, and traveling is the most ridiculous financial action possible, especially on high interest credit cards. With a recession certain to occur and years of “Stagflation” ahead, even corporations including Elon Musk are gathering nestegg funds to weather Jamie Dimon’s financial “hurricane” comment. Spending while paycheck to paycheck is almost like a drug addict.

Looks like majority of US population must have adopted the always sunny model when it comes to spending and money management…what rainy days?

It’s good to see that consumer spending still strong, that puts every last doubt to pasture if FED will pivot anytime soon because of slowing economy…hike away, this inflation fight is far from over. Almost feel sorry for Pow Pow for the tough job he got in front of him now. Almost until I remember he was the freaking arsonist..still gives me a smile everytime I see that cartoon picture of him pulling out his hair..

Powell= Trumps bitch, until dumb ass people wake up ,Trump passed a tax cut for himself and rich . We’re idiots ,flush the toilet of corrupt billionaire politicians.Get real hard working class folks running this country.

I just did my taxes and thanks to the Trump standard deduction, my tax rate is just under 10%. This is less than the pre-Trump amount I paid as a renter. My single son pays 14% on his smaller income.

They now want to pass a 30% national sales tax and eliminate all income taxes. This would impoverish the working class, who can’t avoid the tax buying locally, and enrich those who have access to travel and foreign markets and can avoid paying VATs abroad.

Wolf,

Why do you still moderate any post that mentions Trump? This is one of the reasons I rarely read your articles anymore. Like him or not, he is an important personality in the politics and culture of America. He is not as repugnant as the censorship that tries to erase him from his place in history.

Petunia,

All names that attract the haters are on the list: Carter, Clinton, Obama, Trump, Biden, Fauci, Pelosi … plus various ways used of getting around those names, such as Hitlery and Bidet, LOL

Bush is not on the list because I haven’t yet seen the Bush haters swarm this site. They may be the only Presidents in recent history that don’t have haters, from what I can tell, which is an interesting thought. Someone should do some research on this.

About a year ago, I removed “orange” (as in “orange face” for Trump) from the list because articles on California real estate have lots of comments about Orange County. And there’d be comments about the orange crop in Texas or Florida, or the price of orange juice, and they all ended up in moderation, and it was too much work. Also, people stopped calling Trump “orange face,” so it was no longer necessary.

You should spend a day sitting in my chair moderating comments. The haters and trolls post the craziest stuff that should never see the light of day. Dealing with this stuff is a dirty job, but someone has got to do it.

Nah, they always end up with both….like all of Europe

Believe me, there are a lot of Bush haters around, particularly those who hated Dubya more than any other president until that reality TV show guy got elected. Bill Clinton had a lot of serious flaws, but he was the appropriate president for that time and was as much lucky as he was skillful. The same couldn’t be said for his wife who all the misogynists hated, and no matter what Obama did in office, a sizable number of people never saw him as anything but a “shady” character, and I’m sure you know what I mean.

I see corporations and government starting to beat the bushes in all directions to get more fees. The power company, formerly free websites, my condo fees, etc. This does not seem reflected in the minds of the broad public who are keeping up spending. Something, I think, is going to break, some cohorts in society.

But anyone not thinking heard times ahead is, in my mind, an echo of 2006. Remember all those floating casually on HELOCs and credit cards, talking like they were smart and prosperous?

It’s way too complicated to change our tax system, so it’s not going to happen.

And many of the wealthy depend on the current system to retain and increase that wealth, so a VAT tax isn’t going to happen.

The tax breaks for the middle class are set up to phase out over time. The tax breaks for the wealthy are forever.

Phleep – good ol’ auto-c at play again, no doubt, but as much as hard times are borne by the heard, it triggered an ironic smile…

may we all find a better day.

Flea….

I agree with your high opinion of hard working class.

BUT, the tax cut you referred to actually increased tax revenue.

The problem is one of spending in Washington DC.

And taxing successful people more does what?

The tax code allows some curious benefits to some and I would probably agree with you on that note.

Longstreet – i only wish that in those horrid, (and, given human history, inevitable) times that it becomes necessary to soldier, ‘successful people’ would man the divisions in proportion to their slice of the economic pie…

may we all find a better day.

Where is a Lehman Brothers when you need one…..

I hate the saying, but it does seem like this time is different. If we get a Lehman moment now, it will just signal to the majority that FED Pivot is closer. They have been trained.

But maybe this time, we are at an end-game, we were not at in 2008. maybe we can’t print our way out? At least, without hyperinflation?

libdis,

Now it’s Black….

If Blackrock and Blackstone both failed, the world would be a much better place.

I love your near-hysterical headlines. Please remember that the inflation we are talking about rose .1%, which is the least significant digit and the lowest positive number possible. We don’t even know if it rose 0.06% or 0.14%. The time for hysteria is when the decimal moves to the right.

Correction: rose “0.1% above expectations…”

The important information for a discussion about consumer spending exceeding “raging” inflation is the actual rate of inflation. The difference between actual inflation and inflation expectations is meaningless for this discussion.

What rose 0.1%? Your body temperature after you put your brain in the microwave? Can you not read??? 2nd grade dropout? Or just lying about everything?

https://wolfstreet.com/2023/02/24/spiking-prices-in-january-upward-revisions-for-oct-dec-sink-disinflation-hoopla-services-pce-price-index-spikes-to-worst-since-1984-goods-jump-core-pce-red-hot-again/

https://wolfstreet.com/2023/02/14/annual-services-inflation-rages-at-new-four-decade-high-overall-monthly-cpi-hottest-since-june/

Who the F cares about “expectation?” Whose expectation? Not even the market, as you saw today.

“Your body temperature after you put your brain in the microwave”

EPIC!

People must buy food, wages have risen, credit balances have risen, stock market still inflated, labor market tight, fed not reducing balance sheet and top 5% support alot of discretionary spending.

What’s w the surprise ?

“If you look at the above chart while holding your tongue just right…”

This made my day.

This irrational exuberance on the part of consumers has to be crushed! If the fed raised rates to 10% tomorrow, then let’s see how much consumer confidence there would be. It’s going to take PAIN to kill inflation. We need millions and millions unemployed in order to kill the demand. A depression may be just what is necessary.

I agree but we also need greater productivity and innovation gains, as well as increase in production such as of corn, pork bellies, poultry, propane, gasoline, etc.

If there are not enough willing and capable workers, then they need to figure out how to increase production through innovation, worker efficiency, etc.

I yottabyte agree with you

Are you speaking from a place of security where none of the pain of those millions will bother you? Will their pain make you wealthier?

To your point, josap: the wealthy or powerful care little about the losses and suffering of the lower rungs. When they call for “austerity, cleansing or sacrifice”, they’re talking about you, not them.

What are you talking about? John Kerry “sacrificed” and sold his family private jet! /s

I find the comments so amusing. The Fed has said it will raise rates until inflation is under control. The Fed has said they will do QT until the same and they have room once again to cut when a real crisis shows up. The damage from the end of free money will not constitute a real crisis to THE FED, Dow under 20k, then they get concerned. But for now. meh.

And housing can splatter hard to hold down inflation.

Which is the goal.

The FED doesn’t give a rat’s a** what the stock market does.

“The FED doesn’t give a rat’s a** what the stock market does.”

I dunno but that’s all they seem to care about…until inflation rears its ugly head and forces them to exercise some restraint in throwing money from choppers.

Definitely wrong. When shares of Proctor & Gamble were bought for $1 a share during the flash crash, they wrote new rules for the market. When “mark to market” would have bankrupted many banks, that rule was suspended. If you look at share ownership of the major corporations in the U.S., you’ll see the names of prominent insurance companies, pension funds, educational institutions, foreign sovereign funds, etc., etc. They sure as heck do care about the stock market.

The entire yield curve is below 5%. So, we still have negative interest rates after all the work the fed has done.

They’ve got a long way to go, and thier hope that inflation would come down to meet the higher interest rates just got crushed. If oil goes back up, things could change very fast. Consumers are very fickle. They may haved their heads in the sand now, but I’ve seen that change quickly.

It’s funny – all the comments about negative rates. Over what time frame?

Over 1 year the inflation expectation is below 5%. Even those who fail to understand base effects (or monthly data and seasonality aberrations) expect forward inflation to be below that rate.

Or are you mixing a forward rate with a historical rate?

Extend forward to 2yrs + and the real return in Ts looks better and better.

“Extend forward to 2yrs + and the real return in Ts looks better and better.”

I wish I knew the future too.

Good point. Inflation y-o-y is backwards looking, yield is forwards. The fed has charts on forward estimated inflation, and yields vs. those estimates look a lot better than they have been for many, many years. Of course, the fed has been bad at this.

I haven’t seen anything to connote a splattering in housing — have you? Just saw a place in Placerville sell for 200K more than it did in ‘19. That’s not a splatter; not even a splutter.

I guess everyone’s just so hyper-solvent & YOLO & all of that. The genies not only not going back in the bottle, he’s setting up franchises.

Weird times.

I just love this stuff with which people try to fool themselves and others. Here is El Dorado county median price (Placerville is the County Seat of El Dorado County).

Median price: -24% from peak in March 2022, -7% year-over-year, but still up from four years ago (2019), LOL, per California Association of Realtors:

Just saw a listing in Austin, TX drop over $100K from $450K to $339K. Last year there was nothing listing in the 300s. Austin is bleeding jobs and housing equity, but you wouldn’t know it in the nicer places in town.

Well since you ask, yes I have seen nothing less than a splattering. The housing market clearly peaked in terms of sales in 2020 and 2021. By last year, plenty of houses went on the market. And then I would see them sit for months. Total volume was way down. There may be a few exceptions in very hot areas close to the city. Upscale suburbs with newish houses or cute neighborhoods kind of thing. But that’s it. There was a big slowdown. And if you can’t see that at this point I don’t know what to tell you.

As for where I am: doesn’t matter. If you follow this site you should know by now this effect is nationwide.

I’m just telling you what I see in the house closings I track in a fairly broad spread of cities across America. I’d post the listings here if I could. I see homes selling for hundreds of thousands more than they did three/four years ago, with no value adds or updates (at least not updates you wouldn’t want to rip out anyway) and it blows my mind.

I keep waiting for the power to go out in the casino, but there always seems to be a backup generator for the backup generator for the backup gener….etc

I’m 100% in agreement with Wolf and have been long before he penned this column.

Someone above mentioned the “two America’s” and I agree. For those who “have money”, or “good jobs” much of the increase in inflation has been an inconvenience. If you’re already in a home with a 2.5-4% mortgage and no need to move, you’re not impacted by rising rents (though taxes & utility rates are up but they are up for all). Yes your insurance on home/cars is up, but it’s not killing you. Food & fuel prices are up, but they’ve “come down” a bit do you feel a little better. And chances are your wages have improved a bit, even if not fully keeping up with inflation. But have they ever, really?

I’m an early retired boomer. I own my home, and while divorce cost me 50% of “our” wealth, what is still mine is likely enough to keep me alive the next 20 years. After that I just don’t care. And that’s the actuarial offs of my lifespan. Im not alone. I know a lot of people like me. Sure, some got hit hard in the market downturn (not me), but most are doing well enough anyway. All it means is the inherited wealth has shrunk for those down the line, not for us.

The Fed has so ingrained “buy the dip” that many investors are simply openly challenging the idea of higher for longer. Not only do they have the money to do so, but they also have government largess at their backs.

The “Inflation Reduction Act” will clearly fo nothing of the sort, and likely all of the increases in Social Security are being spent into the economy. The countless hundreds of millions in “free” PPP loans need not be paid back, and it seems DC is dead set in pumping employee tax rebates back to businesses—so much so it’s become a cottage industry complete with ads!

The Fed got this train rolling a decade ago. They “have messed with the primal forces of nature” in the mistaken belief they could tame inflation and eliminate the recession cycle. The Hubris!

The Fed had no model for economic lockdowns, PPP loans, tax “rebates”, massive stimulus, and most especially the end of the exporting of inflation as DC fights a dollar hegemonic battle against riding powers.

While the “common man” does not think of most or any of these things, the upper classes have firmly decided they’re going to ride inflation and enjoy life as much as possible.

Two Friday’s ago I went to have dinner out with a friend in a quaint suburban downtown area in a monied suburb. Restaurants abounded there. We had no reservations, and every door we walked thru had at least a :40 minute wait, the sole exception being a Mexican joint that was large and being only two of us we lucked into a table. No one would begin to think there might be any kind of slowdown whatsoever. Yet, I can tell you that across the water in another town, not so Tony or trendy (or wealthy). A few places have been closing up. Truly “A Tale of Two Cities”.

After paying near $7/gal for diesel last summer, $4.20 seems like a bargain. And yeah the breakfast I grabbed with s friend at a local Denny’s is up a few $$’s, but it won’t stop me from going out if I feel like it.

I’ve been telling people inflation is “baked in” and it’s not going to get turned back. So yeah, people are getting used to it. I lived it in the 60’s/70’s though I was still fairly young. I always expected it to return. I’m not going to let it stop me from living now.

“And enjoy life as much as possible.”

Yes indeed. That is the plan.

Dano

I have had the same experiences…

And, inflation IS baked in.

The Fed pushes the 2% trajectory for inflation, yet we are well off that trend line. To get back to their 2% goal (stable prices?) trend line, prices have to go backwards for awhile….but there is no speaking of that, no price roll back language from the Fed. They want 2%…..on TOP OF the 9%.

(2% would be okay if Fed Funds were 3% or higher)

I think you’re saying that the fed is not going for deflation? Yeah, of course, that’s a shit show. It’s usually the reason why we have stuff like the fed to send us into a recession if things get out of hand, just to avoid a deflation.

A recession IS a deflation. Econ 101. The Fed is going for deflation to counterbalance the inflation, exactly as it should now.

“A recession IS a deflation.”

Nah. A recession is a decline in broad economic activity. Deflation is a broad decline in prices.

The US has had only about 5 quarters of deflation in my lifetime. Over the same period, there were 26 quarters of recessions, spread over 10 recessions.

Most of these recessions in the US didn’t lead to deflation.

But plenty of these recessions occurred with lots of inflation that continued through the recession and on for years.

Deflation after a 9% spike would be welcomed …would it not?

But it really isnt deflation…..which is really prices going backwards from what was a constant level.

This would be PRICE ROLLBACKS or disinflation….

The Fed promotes 2% STILL! So we are to assume 9% plus 2% is a victory?

What you’re saying, Wolf, is that these high rents will never come down again, correct? Those of us on fixed incomes are going to be hurting. My landlord wants my place back for his son next year, and now I have to figure out how I’m ever going to afford rent on a new place. The prices where I am and where I wish I could move next have almost doubled in the last couple of years. I don’t understand how people are still able to afford this.

These kinds of experiences are really tough. Lots of people have to move to cheaper states or even countries to make ends meet. A friend of mine moved back to Tulsa to retire (we were buddies in Tulsa). They really didn’t want to move to Tulsa. But they needed to. They bought a condo for something like $100k, and fixed it up for $20k. You can do that in Tulsa, but you cannot do that in many other places.

DANO

That was a long read, but being in the same basic boat as you, it resonated with me.

During the “good” times I scrimped, saved, ate out at a chain restaurants with coupons or fast food vs a local steakhouse etc.

At age 60 with a couple decades to go, prices rising, I’m like WTF, gonna grab me a $35 Ribeye !!

Might be regular everyday Boomer consumption driving a good portion of this inflation ?

I’m in that boat, not so casual with spending, but owning my home almost completely now with a low buy-in price (decades ago) and at low interest DOES put me in a whole different life than the racing, stressing masses. I’m not being gouged by the rich rentiers who have taken over real estate. Apologies to smaller RE holders, I don’t think it is you whose pricing power has driven up this burden.

I see a whole generation of hopeless stoop labor on a treadmill going nowhere, at least until enough of us boomers die off. Plenty of us are so poorly maintained, they will.

I think a lot of people said “we are going to spend and spend and enjoy the good times, nothing will stop us” in 2007 also.

I recall visiting Las Vegas in January 2009 and the place was a ghost town. The “good spending times” turn on a dime real quick.

Dano, but your opinion that “The Fed has so ingrained “buy the dip””, is untrue. Greenspan warned of irrational exuberance during the dot-com run-up in the 90s. They have not tried to pump up the market intentionally. And there was a point, I think it was after the ’91 recession, that he said that the market and the economy were in a “goldilocks” condition which was largely true.

The Fed, throughout its history, has had inflation challenges and market collapses that they’ve intervened on. They f*ed up in the 1930’s by NOT increasing the money supply or reducing rates (wanted to “cleanse the system”) which led to the GD. They’ve had recent surprises – the banking collapse and the pandemic – one of which they caused but have done this trying to keep the economy from catastrophic failure.

People want to blame others, especially leaders. Fair enough. But don’t add b.s. onto the pile of blame.

An informal observation of the major theatrical movie release business and number of ticket holders at movie theaters, AMC specifically, in Southern California.

In the past 6 months, I have been to approximately 10 major theatrical release movies in the Los Angeles market. Random times I attended weekend matinee and weekday evening.

What I have observed, no ticket seller in the ticket booth, purchase tickets at the candy stand.

When arriving inside the screening area, out of 10 movies, as few as: two people in attendance- myself and the person I arrived with. With the maximum head count about 60 people!

I would guesstimate averaging about 18 ticket holders for each of the 10 movies that we saw!

I might add that I did not attend movies due to some pandemic pent-up demand.

Prior to the pandemic I don’t think I even saw 10 movies within the past 19 years!

My interest in attending the movies is to have my finger on the pulse of pop culture- and that pulse has basically flat lined!

Further evidence of a changing economy is the third Street promenade in Santa Monica, a high-end pedestrian only destination point for tourists and people that want to spend money at higher-end stores….

The third Street promenade has a 25% vacancy rate on the ground level retail establishments!

The office vacancy rate is 25% in the San Fernando Valley which includes the recession resistant media cities of Burbank, Pasadena and Glendale- as one real estate broker described, ‘I’ve never witnessed this level of office vacancy in these three media cities in my entire life!’

On Valentine’s evening, relatively early in the evening 9:00 p.m. – Hollywood boulevard at the vicinity of Vine Street which is a major intersection in Hollywood- there were more vagrants and homeless people, then non-vagrant, non-homeless people. And there was very few total persons, it looked like a ghost town!

There are some areas of Los Angeles that are doing ostensibly well, that is, parking lots at strip malls and shopping centers are filled up in Calabasas, Irvine and areas of that upper income individual.

In conclusion, without any hard numbers it is difficult to determine exactly what the current economic conditions are? But numbers are just statistics and are subject to faulty analysis due to: garbage in- garbage out!

Writing of garbage, brings me to my final point, the areas that appear to be semi-bustling with activity are the areas that are clean and well-kept.

Los Angeles streets is mostly filthy, with garbage, furniture, old carpet, refrigerators, construction debris, illegal dumping, overflowing public garbage cans, lack of street sweeping and basic general cleanup, etc…

The illusion is that homeless people are, for the most part, the creators of this filthy mess.

In defense of homeless people, 90% are dual diagnosis which means in addition to the illness of drug addiction they have severe mental illness- which by the way, if the homeless people get clean and sober, about 80 percent of this populations minds are so permanently devastated, their ability to become a so-called productive member of society and get a job- they would be hard-pressed to do anything above the capability of a greeter at Walmart or the person that grabs the shopping carts at the Ralph’s parking lot!

The filth of the city is not primarily caused by homeless people, after all if you don’t have a home, you don’t have so many of the aforementioned items (refrigerators, carpets, mattresses, construction debris etc etc) that are littered all over the streets.

The filth and garbage all over the streets is due to the city unable to have a solution to keep the city clean!

Remember, clean City more likely to have bustling apparent economic activity!

Thank you for reading, your time and consideration.

Noah King.

The Skid Row Preacher

Thank you, sir. Although anecdotal, that was a very interesting post with many excellent observations.

Noah King,

You’re confusing important structural changes in the US economy that have been going on for two decades with today’s economic activity. Your top two items — movie theaters and brick-and-mortar retail – are being replaced by streaming and ecommerce, both of which are booming and have been booming for years.

These have been topics on WOLF STREET for many years. So here we go:

1. Your movie experience has nothing to do with the “economy” but with how Americans are watching movies — not at the theater, but on a big screen at home. Brick and mortar movie theaters have been dying for years. They cannot compete with big screens at home and streaming. That’s a fact of modern life. The pandemic has accelerated that. Peak ticket sales, in terms of the number of tickets sold, was in 2002 (20 years ago), and ticket sales have declined ever since. But streaming is booming:

https://wolfstreet.com/2022/01/24/despite-all-the-hype-movie-theater-ticket-sales-in-2021-down-68-from-19-years-ago-amc-shares-collapse-from-wtf-spike/

2. Brick and mortar retail stores — your second point — have been dying since ecommerce started taking over. By about 2017, big retail chains, one after the other, filed for bankruptcy. Independent stores closed. Brick and mortar retail has been replaced by ecommerce. And ecommerce is booming.

What’s working in brick-and-mortar retail are grocery & beverage stores, gas stations (declining though, replaced by EV charging stations, a new thingy), auto dealers, and pot shops. They account for over half of total retail sales. The rest of brick-and-mortar retail is dying or has already died.

Small retail stores can be turned into service providers — hair and nail salons, tax preparation centers, etc. — or restaurants, and thrive. But how many restaurants and hair salons can be supported on one street?

Here’s what’s happening to the iconic American institution of department stores — many of the big chains have filed for bankruptcy:

https://wolfstreet.com/2023/02/15/consumers-in-no-mood-for-a-landing-retail-sales-and-seasonal-adjustments/

2002 happened to be the year I bought my first DVD player.

The last movie I saw in a theater that I paid for was “Return of the Jedi”.

Last movie I saw in a theater that I entered through the exit was, “Sin on the beach.”

I have a slightly different interpretation of the consumption behavior of the demand by the hommes et femmes ordinaires. They have accepted the financial world as it is and are willing to overpay for goods that are likely to be on sale in several months.

So yeah, they’re nuts. Aren’t we all. Thank God.

We have entered into a new age that is different than the culture that I grew up in, hopefully.

The world I grew up in was great at the time and not a template for today’s world. For example:

I watched a great movie ” Escape from Pretoria”. The entire time my mind was telling me that today, with robot dogs roaming the halls, what they did is impossible in today’s surveillance society.

Personally, I think it is a sad commentary that the wealth is concentrated in a draft dodging, nest of vipers.

What is playing out is an orchestrated financial drama that appears to be competitive but isn’t. The Fed knows exactly what it is doing …. support the market value of assets.

The Fed is the monster that Jefferson is supposedly too have uttered