These price increases “were not typical” for January: Manheim auction house.

By Wolf Richter for WOLF STREET.

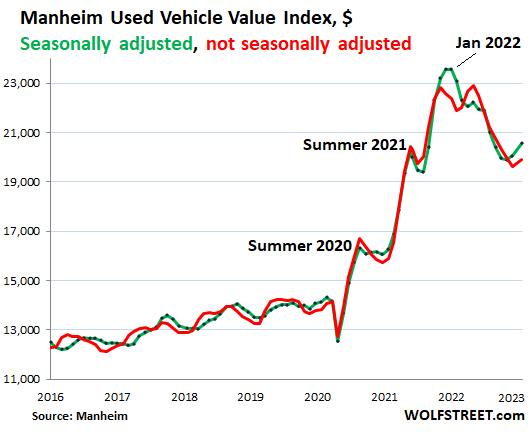

OK, this was quick. Used vehicle wholesale prices, when they’re sold at auction, had gone through a craziest spike ever that maxed out in December 2021. Then prices plunged by the most ever through November 2022. But in December they turned around, and in January they jumped – when seasonally they usually don’t change much, according to Manheim, the largest auto auction house in the US and a unit of Cox Automotive.

Price increases in January 2023 from December 2022:

- Not seasonally adjusted: +1.5%.

- Seasonally adjusted: +2.5%, second month in a row of increases (+0.8% in December).

- Six of the eight segments showed price increases. Pickup trucks up the most, +3.6%.

- Rental risk units: +2.8%. Vehicles that rental fleets have to sell themselves, rather than returning them to the manufacturer under their fleet programs.

- Three-Year Old index: +1.2%, normally little changed in January.

These price increases “were not typical” for January, Manheim said. We’re looking at the seasonally adjusted (green) and not seasonally adjusted (red) Manheim Used Vehicle Value index in dollars (both adjusted for changes in the mix and mileage of vehicles that sold at auction:

More indications of rising demand and prices.

The average daily sales conversion rate rose to 59.4%, well above normal for January. For example, in January 2019, it was 57.7%. “The higher conversion rate indicated that the month saw sellers with more pricing power than what is typically seen for this time of year,” Manheim said.

The upward pressure on prices was driven by dealers more eager to acquire inventory, as same-store retail sales of used vehicles jumped by 16% in January from December and by 5% year-over-year, according to initial estimates based on data from Dealertrack, a service of Cox Automotive.

Year-over-year, used vehicle wholesale prices were still down by 11%, but that decline was less than two months ago (-13.1%).

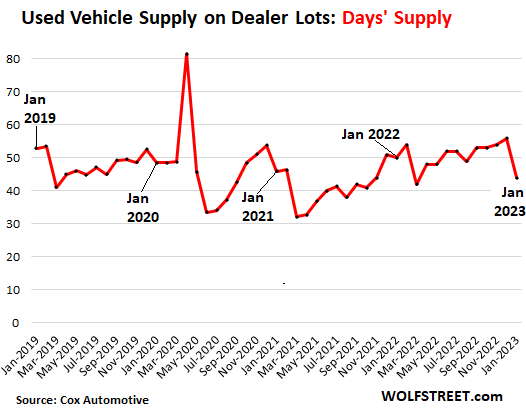

Days’ supply dropped amid sales increase.

Wholesale supply fell to 26 days in January, from 32 days in December and from 31 days in January a year ago.

Retail supply on dealer lots fell to 44 days, from 56 days in December and from 50 days in January 2022, as retail sales rose 16% from December and 5% from a year ago, based on vAuto data, a service of Cox Automotive.

End of Buyers’ strike.

Retail prices of used vehicles dropped a lot last year, though they were still very high at the end of the year, and it seems consumers, armed with hefty pay increases, and seeing a deal compared to the ridiculous prices a year ago, emerged from their buyers’ strike and started buying used vehicles in larger numbers.

Impact on “core” inflation measures.

With raging inflation all around, consumers have gotten used to paying high prices, but feel good about it because those high used-vehicle prices are down from where they’d been, and consumers feel like they got a deal? Seems like it. And so they’re starting to push up prices again with elevated demand? Seems like it. If I were Powell, I’d be getting the willies just about now.

Falling used vehicle retail prices exerted big downward pressure on the “core CPI” and on the “core PCE price index,” which is the Fed’s yardstick for measuring inflation.

That downward pressure from used vehicles in the pipeline (wholesales) is now abating, and we may be seeing the first signs of it even reversing. This trend will show up in used vehicle retail prices with the usual lag of a month or two.

If those trends in the January wholesale market continue and transfer to retail – rising used vehicle retail prices amid rising demand – they’re bad news for the month-to-month “core” inflation measures coming this spring and summer.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Interesting. I wouldn’t expand from this data point that consumers are armed with “hefty pay increases.” Most of the narratives I’ve seen are that wage inflation has been lagging, and we’re not in the time of the unions where workers could collectively bargain for wage increases. Still too early if to tell if workers’ ability to obtain raises through lateraling is real and happening. Seems they are just as likely to be trying to negotiate better working conditions through lateraling.

Plus, US consumers are somewhat dumb when it comes to financing depreciating automobiles. In between those that “put the bottle service on the card” and “20% down mortgages.” May be more of a reflection of increased access to credit for the underemployed to go get secured loans, and we know how that can go.

“Most of the narratives I’ve seen are that wage inflation has been lagging,”

Sure, pay increases lagged 9% inflation, but those were nevertheless the biggest pay increases in 40 years! And for many consumers, not all, pay increases are now outrunning inflation.

“Still too early if to tell if workers’ ability to obtain raises through lateraling is real and happening.”

No, it’s not “too early.” This has been happening for two years now:

Thanks wolf! I especially appreciate the second chart. I do not doubt that wage inflation is historically high, but that is in the context of historically high inflation.

I believe you would not disagree that, by and large, wages didn’t drive the inflation bus. Whether wages will eventually take the lead seems uncertain, at least to me in these interesting economic times we find ourselves in.

Wages have not driven inflation since the 70s but that is exactly what the Fed fears the most.

My business clients have had to raise wages more in the last two years than I can remember in 30 years in the business.

Labor market is still tight and supply chain is not really better for most of my clients.

Forty + years of employer/business having the advantages over workers, and the MSM says nothing. The Fed hands over trillions to the top few %, and the MSM quips nary a peep. “Capitalism at work!” they say cheerfully from their comfy chairs in front of the camera.

Two or three years of workers finally getting a break, and every MSM outlet is shrieking from the parapets about how labor market tightness is driving inflation, whereupon they start shedding tears over how much more business owners will have to pay their workers. Never mind that this is also “how capitalism” works.

I get the premise behind “Fight Club” so much better as I get older. Methinks the wealthy class may want to re-examine why the union movement emerged and what the alternative would have been had workers’ fairly reasonable demands not been met.

Actually replying to Z:

Could not agree more Z, and I can only hope you are young enough and sufficiently energetic to do whatever you can about the travesty of the FRB ”mouthing off” SO much about their so called goal while continuing for over a century to screw working folks.

Been saying similar for decades and now too old to march in the streets, etc., but about damn time many many folks did so, peacefully of course as violence is clearly NOT the way to go!!!

Isn’t the devil in the detail for that chart?

Wouldn’t average wage of any time unit spike if, say, prior to the spike low wage workers were disproportionately laid off?

Sounds also best in mind the labor force participation rate, which has not recovered to 2019/2020 levels, AFAIK.

Overall, I find the disinflation thesis for 2023 more convincing. CPI/PCE are coming down on an annual rate of change basis. Oil/gas down. Owners rent equivalent is an idiotically lagged measure that depends on housing price gains of a year ago – it is currently inflating the PCE. Manufacturing and services PMIs are down. Greatest Monthly Job creation eva! (TM) stat was partially a function of a population adjustment. Agree that the establishment survey data always periodically shows wild numbers up and down. No single monthly stat is definitive.

This year will be good as far as shaking out which macro economic thesis is more accurate: the one where everything aside from raging inflation, which according to this view is taking only a temporary respite, and an all-powerful (but woefully weak-kneed) Fed is hunky dory. And the other that says we’re on the brink of another GFC-esque collapse. First one says used car prices are about to rocket up along with the stock market and other assets. Second one says all of that is going to make new lows relative to 2022 at least.

“Wouldn’t average wage of any time unit spike if, say, prior to the spike low wage workers were disproportionately laid off?”

This is BS. Layoffs are near RECORD LOWS. After this BS, I stopped reading.

Here are the actual layoffs and discharges:

Inflation took off in Oct 2020. The Ave weekly Earning had 12 dots, – 3M, – head start at the top. Whatever came next was accumulated on top of the early advantage. Inflation might be following industrial workers and other workers salaries.

The same advantage might exist in the service sector. This booster

suddenly stopped in Q1 2021, when, when…

I’m not sure that you need unions to fight for higher wages when there’s still 1.9 open jobs for every unemployed person

There maybe some wage increases but not enough given the inflation rate. Evictions are going to rise as prices for goods average Americans need spike. Now, even formerly cheaper used cars are getting more expensive.

The poorer, 70% of Americans is getting boxed in by insufficient wages while the prices for what they need rise and rise. This happened before the French Revolution to a far worse extent, admittedly. Americans are having less and less to lose thanks to the inflation created by and profiting banks and financiers, by reducing the value of their liabilities, employees’ wages, etc.

Speaking of unions – 150 large contracts are expiring this year covering 1.6 million workers, including UPS, Ford, GM, etc. Will really be interesting what falls out.

Maybe this spike is less that people are willing to pay higher prices and more that their car is worn out and they can’t wait any longer.

Cars are much more reliable these days but with the average car at 12.2 years old and likely approaching 200,000 miles they might not have a choice.

How dare you rock the dis-inflation pivot boat.

“If those trends in the January wholesale market continue and transfer to retail – rising used vehicle retail prices amid rising demand – they’re bad news for the month-to-month “core” inflation measures coming this spring and summer.”

I wonder how much affect the tax return season will have on the used car market this year. Tax returns should be a bit less due to the expiration of some stimulus items combined with a December jump in wholesale prices might lead to a lot of disappointed shoppers this year.

As for me, I guess my 15 year old car DOES have several more years of life left… hehehehh

Started my first business in the late 70s and needed to borrow money. Now as an old man with money saved, I find myself looking forward to history repeat itself. Bring it on Govern ment, this time I am ready.

Could demand be shifting from new to used?

Seems like that would make sense to me.

Inflation whack a mole!

Just taking a break from washing a 2021 Lexus I’m going to sell. And, I read this…

Thanks for the good news!

Just curious. Reason for selling????

It’s an NX300 and it was my mom’s. She’s in a nursing home now and won’t drive again. I certainly wouldn’t sell it this new otherwise. It’s a shame. Only has 2000 miles on it.

I would keep it, but I don’t need it. I have a GX and Mrs Halibut has an LS and we’re both really happy with them.

So, yeah, I generally keep cars much longer than that. But this one has to go.

BS

There is annual pop in, especially, lower-priced used cars during February and March as tax refunds go out. If you are in the market for a sub-$10k used car, hold off a couple months.

So what happens to older Hyundai and Kia prices since 2 very large insurers won’t insure them?

Really, how odd….

Why won’t they insure them?

Not insurance-related, but KIA and Hyundai have some horrific engines that thousands have replaced over the years. Theta II is one of them. Some dealerships have a mechanic that can replace two engines in a ten-hour day.

The older models could be stolen with a USB plug. State Farm and Progressive stopped insuring them, at least in some cities. It was a Tik Tok challenge I believe.

Google “Kia boys”. A friend in insurance industry told me that because of this there is a long lead time for many Kia replacement parts and a major spike in claims.

Unlike the vast majority of cars, those models do not have an engine immobilizer, an essential anti-theft device.

State Farm and Progressive are dropping some Hyundai and Kia cars. The keyword is ‘some’. And it is – so far – only two insurers.

The issue is that certain models are easy to steal, so their theft rates are apparently through the roof. This is due to an old-school steel key, which is used to “insert and turn to start” the ignition, and which makes them easy targets.

From ABC News:

State Farm and Progressive are refusing to insure vehicles in certain states over the rising rate of theft, caused primarily by the absence of technology known as an engine immobilizer – a redundancy system that pairs a vehicle’s key fob to the car’s internal computer. When a drivers insert a key into some cars’ ignition, a chip in the key fob sends a signal to the vehicle, confirming that it is safe to start the engine. If the signal isn’t transmitted, the technology is supposed to “immobilize” the car: the engine won’t start and, in some cases, the steering wheel will lock itself in place.

Certain Hyundai and Kia models manufactured before the 2022 model year didn’t come with immobilizers.

According to the Highway Loss and Data Institute, 96% of cars made between 2015 and 2019 had immobilizers as standard equipment, but only 26% of Hyundai and Kia vehicles had them.

Thieves have targeted lower-trim versions of certain Hyundai Motor Group vehicles, such as Hyundai’s Elantra and Santa Fe, and Kia’s Soul, Seltos and Forte vehicles, according to the HLDI..

In recent years, videos posted to social media have explained how to break into the cars and take them for joyrides. According to the videos, something as simple as a USB cable – often already stashed in the car – is all it takes for thieves to start the vehicle.

“…videos posted to social media have explained how to break into the cars and take them for joyrides.”

If only J-Pow drove a certain Kia, my weekend plans would suddenly get a whole lot more interesting.

Ownership turns over quickly on the weekends in the downtown and north side of Chicago.

You mean “possession” turns over quickly.

With new car prices,averaging in the high $40’s+,buying a used car makes sense…

That is why used car prices may not come down as much as people think. I was looking at a compact SUV that had an MSRP of 23k and was about $19k in January 2020 after some cash rebates. Now 3 years later it is MSRP of 29.5k and not rebates to be found. Basically a 30% increase. Makes sense used cars have jumped up a lot too.

Because feds inflated money supply ,which devalued the dollar. Car same price in devalued money

We are going through the 70s again.

History repeating.

Fed has a leadership problem.

The fed would not have leadership problems if people were reasonable and practical about how they spend money. Overpriced pickups, thosuand dollar iphones and 7 dollar lattes. So we just blame the government and take no personal responsiblity. Not right.

I don’t know if I’d call it a leadership problem since putting lawyers in charge of central banks seems to be a thing now, but they certainly do have a groupthink problem. Can you believe they all thought that rates would remain near zero through the end of 2022? Now they all seem to think that 5.25 pct is going to be all it takes to get this problem under control but the evidence for that is scant.

You can’t find a single dissent among the fomc members for last 20 year. You have to go to Soviet politburo to find such unity of thought.

Eastern Bunny,

BS. This is public data. All you have to do is look it up.

There were plenty of dissenting votes — even in this rate hike cycle: at the meetings in March 2022 (Bullard wanted 50 basis point hike, instead of 25) and in June 2022. There were 3 dissents in 2020. Then there were a bunch of dissents in 2019….

I’m curious to know what type of metal is getting moved and price range. I noticed how G-Wagens, luxury sedans and super sports cars are falling in value. I also see same with higher end EVs. There is a counter trend in a lower segment where vehicles under $30k are experiencing robust demand. So maybe that’s where inflation waves are sloshing to.

I wouldn’t be surprised if that were the case.

In our household the 2nd vehicle is near dead and became too much of a money pit, but we refuse to deplete our savings more than required or take on a loan with interest any longer than necessary. So, when We do replace transport #2, either We’re going for something as affordable to purchase & repair, and close to reliable as possible.

I can imagine others being practical for similar reasons, or out of desperation.

For reference, the near dead money pit is an older paid off Audi Quattro A8… which will probably be replaced with a glorified golf cart that’s cheaper to maintain, at some point.

Groceries, tires, shelter, insurance, & life in general aren’t getting any cheaper. Hell, maybe We won’t replace it at all? Local experience states there’s too many lemons being financed as peaches in many price ranges, and we aren’t mechanics.

That will fall right into the CPI calculator. “Substitute golf cart for automobile. Inflation went down.”

The Porsche dealership on the west side of Minneapolis is loaded up for springtime with a good selection of very high-end late model 911s.

Top of the list is are two 2018 GT2 RS rocketships, each with 5k miles @ $400k.

More pedestrian, is a 2022 GT3 with 3k miles for a very reasonable $270k. In total, eight GT 911s of various type are listed on their website. I have never seen such a selection of the best 911s at this dealership ever before. (And I like to look at car porn …)

And yes, they also have the Ferrari dealership that’s next door to the Porsche and the Audi dealerships they also own.

But, to be back down to earth & in touch with reality, the highlight of springtime will be to ride my Bianchi again, and I’ve a new set of Sidi shoes ready to wear for the occasion!

Ah, the west side of Minneapolis. I was sitting in the Ridgedale parking lot waiting for the wife to do her thing in the mall late summer 2020, when what I thought was a R8 parked a couple spots from me. A gentleman gets out, pops the hood pulls out a “White House Black Market” shopping bag then proceeds to help his attractive wife out of the car. She’s on crutches. As they make their way into the mall a few gawkers show up and I look more closely at the car and it’s a Chiron. Who drives a $3 million car to the mall to do a clothing return? I would post a picture if I could. I’d also post a picture of the cop who was checking it out then went and sat in the parking lot just waiting. There’s lots of money in the MSP western suburbs.

And the market is up quite a lot again! :-)

“Soft landing” = manufacture new, higher floor in all asset prices by protecting all gains for wealthy speculators at the expense of society. The FED doesn’t want any deflation, they just want a hint of disinflation.

I’m not sure I agree. Powell merely said inflation is lessening but that rate rises would continue. The market heard what it wanted to hear.

And Powell might be happy to let the market hear what it wants to hear. After all this, anyone could figure out that the market will cheer on any sliver of hope; if Powell didn’t want to cheer them up, he’d know by now what not to say and could just be totally “negative”. The market going up gives the Fed more time to let the effects of rate increases and QT work through the system without crashing it.

He’s talking about the RATE of inflation slowing – disinflation. Prices are still going up on everything. He doesn’t want prices to actually reverse, he just wants them to stop going up as fast.

The poor and middle class largely don’t even understand what is going on, only that they cannot keep up financially. Some are unsophisticated and think prices will actually be coming back down to what they were on a lot of assets.

That’s not happening, which is why I posted what I did. The FED printed so much money that prices will never go back to what they were, in nominal dollars.

For goods and services, yes (although I don’t agree that deflation is bad). But he’s explicitly said he wants lower house prices.

The FED and the entire financial sector have miscalculated on inflation and where rates will have to go to snuff it out. Arthur Burns 2.0 was flapping his jaws earlier, celebrating how inflation is coming down.

We’ll see a dip for a few months, and then CPI is probably going to explode to the upside again by late spring and summer. “Nobodycouldaseenitcoming” will be Burns 2.0’s response. They never should have scaled back the rate hikes.

I think it’ll explode sooner than that.

The days of gradual half point increases are best seen in the rear view mirror.

No doubt. And the wallstreetcrybabies will call it a Black Swan event.

A reduction in projected increase in spending is decried as a “budget/spending cut”. So lets get excited about disinflation.

Oct 12, 2022 – Yellen Worries Over Loss of ‘Adequate Liquidity’ in Treasuries

^^^Why Fed got cold feet after “things” got a little scary back then. And somewhat why animal spirits came back starting Oct 2022.

Just like when why Fed lied about financial conditions still being tighter recently, they have to talk out of both sides of their mouths at the attempt to address both current and/or future inflation versus debt related financial disasters lurking in the monetary shadows.

Greatest showman on Earth.

I

Lots of smashed cars from the ice storms in TX, snowmageddon in the NE, and the floods in FL.

I’d be very leery of auctions right now…. lots of flooded vehicles that have been cleaned up and “repositioned” geographically to take advantage of unsuspecting fools. Not all will carry branded titles.

My DIL’s car got smacked by a tree on their driveway last weekend. They live in Austin and lost most of their mature live oaks to the ice. They weren’t the lone ranger in that department.

These days are gone pal. Things get reported to car history outfits, minute they are entered into system by insurance or police. Before all that, one could go to Kentucky (if my memory serves well) and wash salvage title into nice clean one. You cannot wash off history from Carfax or Autocheck. Not to mention Florida’s certificate of destruction is a death sentence on car in US. That’s why those get mostly shipped overseas to be sold.

You’re assuming all are reported to insurance and/or police and all are salvage. Police reports are for accidents. Fairly sure the police don’t write up every car that gets wet. People without comprehensive insurance have no flood coverage and, as it’s not a liability claim nor collision, = no insurance claim. Not every indy shop reports service history.

If you look through Copart listings, you’ll find exceptions… clean titles with damage – at times invisible to the naked eye, other times fairly severe. A vehicle can get minor water intrusion damage but still run acceptably. It gets dumped on an unsuspecting party on Faceplant marketplace and then the corrosion sets in.

Carfax, itself, has an article on how title washing can still occur. It’s dated October 2022 so it’s not ancient history. One line from the article: “Laws overseeing title branding rely on a vehicle’s insurer or owner to report damage, so if an owner doesn’t disclose past damage, the title won’t reflect that information.” Carfax and Autocheck rely on that database. No report? No history.

Pal.

Nissanfan

BS, My Nissan Sentra was hit 9 times by maniac drivers. No police reports were filed as they were all minor fender benders. I got it fixed at local body shops. I ran a Carfax history report and it showed no accidents. Another scam to take your money.

Getting the willies is an expression my mother used. I had to smile when I read it. If the used vehicle buyers have the view that they are getting a good deal today from the ridiculous prices a year ago, then maybe housing will be next. And that will really give Powell the willies if he is getting them already.

Wonder how much a softening economy and substantial increases in new vehicle prices are steering new vehicle buyers to purchase used.

Increased demand is resulting in higher prices. There is a finite number of nice used vehicles.

The big drop in wholesale prices hasn’t yet fully passed to retail. This blip up is not meaningful.

Look for even bigger deflationary impacts as retail price competition reverts to historic norms.

Supply dropped. Retail sales rose. Not the environment for prices to drop further.

That was the case but no longer. Supply chain constraints have substantially eased. So we now have a combination of rising supply into higher margins at retail level and lower consumer purchasing power.

That combination means we’ll see very rapid price declines for the foreseeable future. Of course not back to pre-covid levels but on all YoY metrics (and future looking) it is significant.

Look, I’m rooting for you. I think people need to be on buyers’ strike a little longer to get prices down further. But this data here tells me that people are jumping back into the market, and dealers are playing along.

Used car supply depends on fleets and trade-ins.

The biggest single supplier to the used vehicle market are rental fleets when they turn over their inventory. In normal years, they supply the used vehicle market with 2-3 million vehicles a year. But they weren’t able to buy all the new vehicles they wanted in 2021 and 2022. And so they kept their units in the fleet longer, and they have fewer units to sell. This will eventually get back to normal, but right now, they’re still trying to get their fleets back to normal.

Then there are the millions of people who trade in their vehicles when they buy a new vehicle. These trade-ins have plunged as new vehicle sales have plunged, hampered by shortages. This flow of trade-ins will also eventually normalize, but not yet.

You see all this in the days’ supply chart above.

But — the used vehicle market being part of my regular beat — I will surely let you know when we “see very rapid price declines for the foreseeable future.”

Powell was out flapping his gums today and managed to goose the stock market up and drive the dollar down a bit. Why can’t he just keep quiet?

Funny, he repeated the same script that was super-hawkish in December: 2 or more rate hikes this year, no rate cuts, and “couple of years” more of QT.

These morons hear whatever they want to hear. It doesn’t matter what Powell says. It’s hilarious.

Bond yields rose, though. Mortgage rates back at 6.5%, so there’s that sense or reality.

That’s all true. Unfortunately he also said, “The disinflationary process, the process of getting inflation down, has begun, and it’s begun in the goods sector,” and then he qualified it by saying “these are the very early stages of disinflation.” So they took that and ran with it ignoring the rest of his comments. He needs to do less talk and more action.

They willfully confused “disinflation” with “deflation.”

Actually it doesn’t matter what he says. Those geniuses will twist it into whatever they want.

But fine with me. The more they do this, ultimately the higher rates will go because what they do causes financial conditions to loose, and that pushes back against the Fed’s efforts to slow demand. I’m good with that. I don’t want the Fed to stop prematurely, and so now we’re getting much higher rates than previously imagined.

Yes. I noted this up above. It’s not like when Kudlow and Mnuchin would say “Trade talks are going well” intentionally to jawbone the market up. Here, he said “Inflation is starting to decrease a bit, but we still have a long ways to go, and more rate hikes in the future.” The algos seized on the first part and went crazy.

I think there is a benefit to him saying that disinflation has started. To to the extent that inflation is a psychological phenomenon, people thinking the decline has started could help anchor expectations and then inflation tapering out could be a self-fulfilling prophecy.

I don’t know. But I didn’t see this as a jawboning the markets up.

The psychology part is key. There is little chance of a price-wage spiral (order intentional) when people are seeing their net worths collapse (middle class+) and bank accounts slip to nothing (bottom half).

Most companies are only now rolling into their 2023 budgets and this when hiring freezes, targeted layoffs, etc happen. Not with urgency for most (yet) but it isn’t a Jan 1 phenomenon when talking Dec 31 year-ends. Consider some managers see the writing on the wall and try and use their budget early.

But I digress (apologetically). Powell is walking a fine line between the end-customer psychology (expectations) and Wall Street. He bungled everything not even 18 months ago and I can’t say he’s doing a great job at walking that line today, but based on low expectations it is a marked improvement.

Maheim might rise to 22,000 in summer 2023, before the real plunge

start. Summer 2021 and summer 2023 complete the turn around.

Bring A Trailer is getting more NO SALE-RNM than anytime before. Expectations and Reserves are still too high. Especially for Flippers and really show on EV Trucks.

Noticed that. Any official stats?

RNM ? What’s that mean?

Reserve Not Met

The longer this goes on the more people are going to be demanding higher wages and unions are going to be more aggressive and strikes are going to get more common.

Impossible to know yet but maybe the Fed has not been aggressive enough or at least stern enough with there messaging.

Just had a friend put an offer in on a house for 15% over asking in long island. They got beat out by someone offering 25% over.

Things seem to be picking up again as everyone is realizing we aren’t in a recession

Assuming your friend doesn’t buy some other overpriced place he or she will eventually be thrilled that they got outbid. Inflation is going to be persistent and eventually the midrange and longer bonds will respond, which means much higher mortgage rates and much lower house prices.

People like your friend don’t get it.

It’s not a “recession” that will cause prices to drop, but the steps needed to combat inflation.

Brrrrrrrrrrr money doesn’t go away that quickly–especially at the rate QT is going. Plenty of it still sloshing around out there. Even stimulus (giveaways to the already-moneyed) isn’t done; see the Employee Retention Credit.

Prices have not declined at all in my Flyover city in 2022. Nice steady increase all year. Average sales price is up 8% to 328k from December 2021 and median price is up 4% to $275k from December 2021.

Inventory is up 30% (still 50% below normal) and the number of sales transactions are down 40% but prices keep going up.

I know it’s anecdotal but I recently purchased a used Toyota Solara convertible (I know a dorky car). I couldn’t get to about 4 of them fast enough before someone else purchased them or put a deposit down as soon as they became available here in wintry cold Midatlantic. I’m talking about Solaras being posted on dealer websites on Monday and sold by Wednesday if they were “lower” mileage (sub 120,000 miles and clean). I kept reading how prices would crater but it doesn’t feel like there is much downward pressure yet.

It’s evidence of a wage-price spiral. The Fed’s behind is on the curb, as usual.

Exactly. Powell keeps opening his mouth that inflation is coming down which wallstreet then interprets as the Fed is going to pivot soon. Powell came out today and said the same thing causing the ridiculous rally today. I wish they would concentrate on bringing inflation down and shut up about it. The Fed still has a long way to go, which Powell says, but wallstreet ignores it.

“The stock market can stay insane longer than you can stay solvent.” I like treasuries instead, 6 month, 5%, no risk, state tax free. The stock market is still living in the free money world. It is kind of amazing.

Honda dealer won’t leave me alone, wants my 2016 CRV. I’m not paying new car prices and like my car.

I hope prices keep on rising for new and resale cars and SUV’s.

“If I were Powell, I’d be getting the willies just about now.”

Haha you bet … but if so it’s his own fault. For most of last year he hammered home the importance of “financial conditions” and not letting them get out of hand. Then let them get out of hand. The falling dollar and rising stocks mean fresh inflation in the pipeline … just working their way into final consumer prices. Likely this renewed surge in wholesale car prices is a sign it’s bubbling through already.

If you’ve been reading Wolf for any amount of time, we’ve read and commented on all the money creation, inflation in various areas, and when we think a possible Fed pivot, or not. Life as we knew things the last 40 plus years good and bad are over. Some things will go up and down in price and others only up. In some ways I don’t agree with those who think what the Fed has done is stupid or late to the party. I think most of it is planned. For the most part they get to call the shots on the winners and losers in finance. But what isn’t talked about a lot is what else is going on around the world. When you try to punish countries with the financial system, things start to change. We also used to have a captive audience for the world to purchase oil only in dollars. That is changing. I don’t think it will totally be like a light switch, but things long term will only be going up for all of us here. Wages will never catch up….

Good one cold one:::

Agree, like totally dude or dudette,,, but only with some of your conclusions.

Old guy who tried to help me understand economics et cetera back in the 1960s used to insist that no matter how egregious ”things may be today”,,, those things in re economic situation will eventually go back to long term ”means and measures” by which he meant averages and medians.

Surely, or surly if you prefer, eventually all ”metrics” will revert similarly, ”inflation adjusted” far damn shore…

Just be ready with your cash or other completely liquid assets when the opportunities come again, as they always have done and will do, in spite of any CB efforts to slant those opportunities to the rich and vastly rich.

I can only hope that enough folks realize the lies, damn lies and statistics that the CBs of the world these days use to keep down the folks actually making stuff, etc., etc.

Meanwhile Mr Market continues his drunken revels …

“If I were Powell, I’d be getting the willies just about now.”

Yet when I was calling for the FED to continue with their 75 basis point rate hikes until they reach the rate of CPI I’m accused of “just wanting to burn it all down.” Now look, they’re falling behind.

The fact is that the FED blew it by quickly ratcheting back to 25 basis point hikes, especially given what’s transpired since September. All of the signs were there, they just ignored them. There is absolutely no good reason why they didn’t do 50 basis points last meeting. Just an abysmal failure of a job.

I contend that the FED is playing a role of fake tough guy on inflation, with the actual goal of hyperinflating the price of all assets permanently. There’s no way they’re as incompetent as they’re acting. They know that the longer they string out this inflation, the higher prices will be in the end.

Here’s more evidence that Powell does not want deflation in prices, even housing:

“we have said that we would consider sales of Mortgage Backed Securities. But I will tell you that is not something on the list of active things, things actively being considered”

See? Powell is not serious about inflation. He’s a liar.

The FED never wants deflation. Their main job is to fight deflation. Cleary this is indicated as they always have a targeted inflation rate.

I was looking at the M2 increase YOY for the past 12 years. Only twice did it drop below 5% increase.

Yet inflation most of those years was below 3%. No way you can have a 5% YOY average increase in money supply and only 2.7% YOY average inflation. Well, maybe we can as we exported a lot of inflation to China via jobs.

I’m seeing price increases of 15 to 20% on many staple items that I buy every week at the grocery store. These are necessities. I believe the CPI is way behind what is happening in the real world. I even heard the government is looking for a new way to measure the CPI to keep it down below the actual rate.

What’s wrong with this if anything ? Suppose…(the actual numbers may be off a lot… its the

reasoning I’m asking about):

1. (Suppose) January 2023 prices are up 7% YoY.

2. (Suppose) February 2023 prices are up 6% YoY.

3. (Suppose) February 2022 prices were unchanged compared to January 2022.

So this implies:

1. disinflation of 1% w.r.t YoY price changes (7 to 6 percent inflation)

2. deflation of 1% MoM January 2023 to

February 2023 (which presumably could be determined w.o. reference to 2022 prices anyhow).

Some years hence: deflation could be occurring YoY, say for 2 months straight, -4% followed by -3%. Again if the prices were unchanged a year ago this would be consistent with +1% inflation MoM (currently). Maybe in a deflationary environment (again YoY) they might call the MoM increase of 1% “reinflation” (the flipside, converse if you will, to disinflation).

Update:

I am not suggesting a prolonged deflationary environment is anywhere on the horizon !

(predicting the economy certainly not my specialty).

The point of my comment was merely to illustrate the use of disinflation and deflation…

is my understanding of the terms correct ?

And to point out they are relative to a time period.

I have never bought a new car in my life. I’ve been milking life out of 17yo Chevy Avalanches for the past few years. New driver in the family means wife’s car goes to 16yo. New car for wife. Ionic 5 would be the choice, but no $7500 rebate. So we ordered a Tesla model Y Performance. Only trim guaranteed to arrive by end of March. We can offset a lot of gas miles with the Tesla since we both work at home and can switch off whoever is driving the most on any given day. Tesla “savings” calculator says we can save $15-20k in gas over 6 years. Higher insurance will offset some savings.

This makes the Y a $40k ICE equivalent for us.

Anyhow, we were on a buyer’s strike, but we could only wait so long.

And if we have a momentary lapse in judgement and drive off a cliff, at least we will be ok!

I went all in on TSLA beginning of the month in my IRA. I’ve almost recovered the loses of last year. So that always helps making big buying decisions.

Anyone with half a brain is keeping their legacy tech cars and that’s driving up the prices. New smart cameras and sensors in the ‘crash zones’ of the new vehicles drive up the cost of repairs after collision and are of dubious safety value. These sensors add thousands to vehicle cost and subtract from quality elsewhere. Those collision sensors need to be calibrated and can be rendered worthless by ice or bug splats. All big money for dealerships.

Given that auto makes will eventually stop making ICE (internal combustion engine) vehicles I expect the value of my old ICE cars to at least double or triple in the next few years- especially if we have new global supply chain issues.

Hold onto your old cars!

I think you are all a bunch of whining little girls. In 1965, my buddy and I took a six cylinder engine out of my brother’s 1956 Chevy and replaced it with a 265 CI V8, while he was at a three day church camp. We didn’t do church.

We were 14 years old at the time.

My brother had no idea that we had butchered his car.

The performance increase was very near zero, but Fred did thank me for the tune-up.

The point is this, none of the garbage about used car prices matter. If you want to have another car, get yer ass out to the garage and build one.

Today, I have five vehicles. One of them was built in this century; a cute little 2002 525I BMW Touring Wagon. It is also the most problematic car that I own. I can never keep the computers happy, and the dang thing cost me $900 in 2016. Yet, it runs well.

My favorite driver is my Cord, which is almost ninety years old.