“The historical record cautions strongly against prematurely loosening policy. We will stay the course until the job is done,” but it’s not done, Powell said: Core services inflation ex-housing has not come down.

By Wolf Richter for WOLF STREET.

At today’s meeting, the FOMC raised its five policy rates by 25 basis points, bringing the upper end of the range to 4.75%, as widely expected. The Fed has now hiked by 450 basis points in 10 months, far more than anyone imagined a year ago. It has also run $500 billion off its balance sheet in six months of QT.

“Ongoing rate increases” will be needed to get rates to be “sufficiently restrictive to return inflation to 2% over time, the statement said, and Powell reiterated the need for “increases” multiple times at the post-meeting press conference. Always plural: “increases,” meaning at least two more rate hikes, which would bring the top end to 5.25%, as projected at the December meeting. Updated projections will be released at the March meeting.

“Shifting to a slower pace [of rate hikes] will better allow the Committee to assess the economy’s progress toward our goals, as we determine the extent of future increases that we require to obtain a sufficiently restrictive stance,” the statement said.

No rate cuts “this year” if economy performs as expected. More than two rate hikes? “We could certainly do that.”

“If the economy performs broadly in line with [the Fed’s] expectations, it will not be appropriate to cut rates this year, to loosen policy this year,” Powell said.

“If we come to the need to move rates up beyond what we said in December, we would certainly do that,” Powell said. “At the same time, if the data comes in the other direction, we will make data-dependent decisions.”

“More work to do.”

“The historical record cautions strongly against prematurely loosening policy. We will stay the course until the job is done,” Powell said.

“We covered a lot of ground, and the full effects of our rapid tightening so far are yet to be felt. Even so, we have more work to do,” Powell said, a phrase Powell reiterated over and over again – meaning more rate hikes.

“Inflation is running hot,” Powell said, so more work to do. But “we are taking into account long and variable lags” for monetary policy to impact inflation. Hence the slower pace of rate hikes.

“Without price stability, we will not achieve a sustained period of labor market conditions that benefit all,” he said.

“Very premature to declare victory.”

“It would be very premature to declare victory or think we really got this.”

“Our job is to deliver inflation back to target, and we will do that, but I think we will be cautious about declaring victory and sending signals that we think that the game is won.”

“We have a long way to go. It is the early stages of disinflation. It is most welcome to be able to say that, that we are now in disinflation, that is great, but we see that it has to spread through the economy and it will take time.”

“Restoring price stability will likely require maintaining a restrictive stance for some time.”

“Our forecast is that it will take some time and patience, and we will need to keep rates higher for longer.”

The “risk of doing too little”

“I continue to think that it is very difficult to manage the risk of doing too little, and finding out in six or 12 months that we actually were close but didn’t get the job done, and inflation springs back, and we have to go back in, and now you really do worry about expectations getting unanchored and that kind of thing. This is a very difficult risk to manage.

“Whereas, we have no incentive or desire to over-tighten, but if we feel we have gone too far, and inflation is coming down faster than we expect, we have tools that would work on that.

“So, I do think in this situation where we still have the highest inflation in 40 years, the job is not fully done.”

“Labor market remains extremely tight”

“Despite the slowdown in growth the labor market remains extremely tight.”

“Although the pace of job gains has slowed over the past year and nominal wage growth has shown some signs of easing, the labor market continues to be out of balance. Labor demand substantially exceeds the supply of available workers and the labor force participation rate has changed little from a year ago.”

“Reducing inflation is likely to require a period of below-trend growth and softening of labor market conditions.”

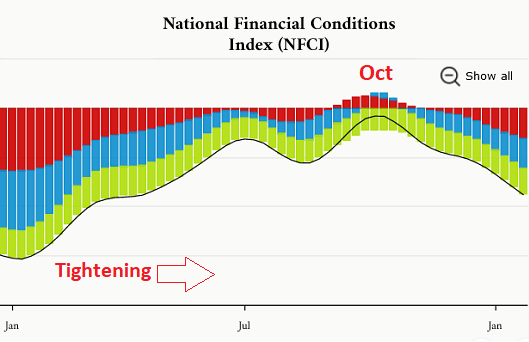

About financial conditions loosening since October:

Financial conditions – measures of the credit markets, such as credit spreads, and not stock prices – after tightening substantially last year, began to loosen again in mid-October and unwound some of the tightening that they had done earlier in the year. Financial conditions are tracked by various indices, such as the Chicago Fed’s National Financial Conditions Index (NFCI).

You can see the easing since mid-October that unwound part of the tightening earlier last year (chart via Chicago Fed, red lettering by Wolf Street):

The minutes of the December meeting mentioned this “unwarranted easing of financial conditions,” and pointed it out as a risk that would make it more difficult for the Fed to bring inflation down. Powell was asked a couple of times about that today.

“Financial conditions have tightened significantly over the last year,” he said.

“The financial conditions haven’t changed much from the December meeting [Dec 14] until now.”

“It is important that the markets do reflect the tightening that we are putting in place as we have discussed a couple of times here. There is a difference in perspective by some market measures on how fast inflation will come down. We will have to see.

“I mean I am not going to try to persuade people. I have a different forecast. Our forecast is that it will take some time and patience, and we will need to keep rates higher for longer.”

At another point he said: “I would say that our focus is not on short-term moves but on sustained changes to broader financial conditions, and it is our judgment that we are not yet at a sufficiently restrictive policy stance, which is why we say that we expect ongoing hikes will be appropriate.”

“Of course, many things affect financial conditions, not just our policy. We will take into account overall financial conditions along with many other factors as we set policy.”

“We think we covered a lot of ground, and financial conditions have certainly tightened. I would say we still think there is work to do there.”

Made fun of “market participants” that caused financial conditions to loosen.

“Market participants have a very different job. It is a fine job. It is a great job. In fact, I did that job for years, in one form or another. But we have to deliver that [2% inflation]. So, we are strongly resolved that we will complete this task, because we think it has benefits that will support economic activity, and benefit the public for many, many years.”

Inflation not coming down in “core services ex-housing.”

“We have a sector that represents 56% of the core PCE inflation index, where we don’t see disinflation yet. We don’t see it, it is not happening yet.

“Inflation in core services, ex-housing is still running at 4% on a 6 and 12-month basis, so there is nothing happening there. In the other two sectors [goods and housing], representing less than 50%, I think you now have a story that is credible, coming together, although you don’t yet see disinflation in housing services, but it is in the pipeline, right? So, for the third sector [core services excluding housing] we don’t see anything.”

“It would be very premature to declare victory or think we really got this. Our goal, of course, is to bring inflation down. How do we get that done? There are many factors driving inflation in that sector [core services ex-housing]. They should be coming into play to have the disinflationary process begin in that sector. But so far, we don’t see that. Until we do, we see ourselves as having a lot of work left to do.

To another question on this topic: “We expect to see that disinflation process will be seen, we hope soon, in the core services ex-housing sector I talked about. We don’t see it yet. It is seven or eight different kinds of services, not all of them the same. And we have a sense of what is going on in each of the different subsections. Probably the biggest part of it, probably 60% of that is … sensitive to slack in the economy. So, the labor market will probably be important.”

“We are just telling you we don’t see inflation moving down yet in that large sector [core services ex-housing]. I think we will, fairly soon, but we don’t see it yet.

“Until we do, we have to be honest with ourselves, seeing ourselves as having perhaps more persistent inflation in that sector, which will take longer to get down. We have to complete the job. That is what we are here for.

For your amusement: Reporters’ inane crybaby can’t-you-stop-the-rate-hikes-now questions.

What was hilarious at the press conference today was a slew of crybaby can’t-you-stop-the-rate-hikes questions. They were so funny that we’ll go through some of them here, and you’ll see that Powell should have answered them with: “Stupid question. Next!” Or “I already shot this down twice. Next!”

But as Fed chair, he has to answer them in some polite manner, and you could see his exasperation.

Question: “Why do you think further rate increases are needed? Why not stop here and see what transpires in the coming months before raising rates again?”

Powell should have said: I just explained it, you idiot. But he didn’t.

Question: “Did you or your colleagues discuss the conditions for a pause at this meeting this week?”

Exasperated, Powell said, “the minutes will come out in three weeks and give you a lot of detail.”

Question: ‘Was there discussion today of the possibility of pausing rate increases and then restarting them?”

Powell: “So, the Committee, obviously, did not see this as a time to pause. We judged the appropriate thing to do at this meeting was to raise the Federal funds rate by 25 basis points and we continue to anticipate that ongoing increases in the target range will be appropriate.”

Question: “Would it be possible to take a meeting off for example, and then resume? You know, could you, rather than doing that every meeting, go a little more slowly, take some gaps in between moves?”

Powell: “This is not something that the Committee is thinking about or exploring in any kind of detail.”

Question: “I wonder if you considered the idea of whether or not your understanding of the inflation dynamic may be wrong, and it is possible to achieve these things without raising rates that high….”

The Fed hiked its five policy rates by 25 basis points:

- Federal funds rate target to a range between 4.50% and 4.75%.

- Interest it pays the banks on reserves to 4.65%.

- Interest it charges on overnight Repos to 4.75%.

- Interest it pays on overnight Reverse Repos (RRPs) to 4.55%.

- Primary credit rate it charges banks to 4.75%.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It’s so funny to read the business media, and then Wolf, interpret the exact same event. In diametrically opposed ways.

Also the comments section in wolf’s articles, check out the one about job openings earlier today. Plenty of interpretation of Powells statements there, this article seems like a good response lol.

All our politicians say that they are working for their voters, but majority of voters on both sides keep getting poorer and the 1% keep getting richer.

It’s not what you say, but what you do. Karma trumps lip-service.

J Pow is still unable to handle “transitory” inflation and blames market for loosening financial conditions when he controls monetary policy.

Not surprising. Legislators make the bulk of their money from tips, not the base salary.

Financial conditions are a lot more than monetary policy. It’s psychological.

Wolf still has faith in our institutions and in the Fed. He trusts them when they say they’re serious about bringing inflation down. Just like many had to learn from covid – the government doesn’t care about you. The government needs inflation to keep the house of cards standing. The fed and the BLS play key roles in facilitating that inflation. It’s not an accident that the way CPI is calculated was just updated, again, to take effect beginning with the next CPI release. And make no mistake – the update methodology will result in a lower number. Anyways, doesn’t matter, this is why Bitcoin wins. It’ll be a hard pill for Wolf to swallow. But just like everyone else, he’ll eventually buy Bitcoin at the price he deserves.

Your CPI comment is silly — as is the rest. The CPI weighs get constantly updated, based on where consumers spend their money. I have been tracking the weights just to shut down your kind of BS — and I have them on a spreadsheet. For example, the BLS increased the weights of rent because people spent more of their money on housing, but rents are spiking the most, which made CPI worse. You’re just a bitcoin troll, and bitcoin needs you because it collapsed by 65% LOL

^^^THIS^^^ is why I come here. Wolf, E.B. Tucker and Gregory Mannarino speak their mind. It’s refreshing.

Thanks Wolf.

FTX kept a spreadsheet too!

Sorry I couldn’t help myself

Those who dont trust government issued fiat and instead sing the praises of Bitcoin and others because they are out of reach of the big bad Feds. That is until the coins go into the ether through malfeasance of all sorts. Now they are whining for government regulation and intervention in their racket.

Cryptocrap is not the future any more than tulips or cacao beans were. I have no faith in our institutions.

Still, I am getting surprised at the continuing, tiny rate increases: they are sucking the capital right out of their buds’ the CCP cadres’ markets, and other markets, because they are in relatively risk free treasuries — provided our hyper-nutty Congress does not cause an insane US government default, which may actually be possible.

Andrew

Good grief, man! This is such BS. The Fed isn’t perfect but they’re not out to harm individuals. They’ve got a tough job and though it’s easy to look in the mirror and see how things they’ve done have caused problems, what you can’t see is the problems that would have arisen had they done something differently. They’ve got big problems, blunt controls, and high lag. That is not a recipe for a good control system but it’s the only one we have and I certainly won’t claim that I could do better. Crypto has its benefits and problems just like any other asset and will not be replacing fiat.

I’ve posted positively before about crypto (Wolf knows this ;-) but always to provide facts and combat misinformation. What you’re spouting here is misinformation.

So your diatribe covers years of QE and ZIRP as well?

“But just like everyone else, he’ll eventually buy Bitcoin at the price he deserves.”

This is beyond funny, Bitcoin-lovers issuing a comics-style fatwa on Wolf and the rest of non-believers. Life in marvellous times, I guess.

[i]”It’s so funny to read the business media, and then Wolf, interpret the exact same event. In diametrically opposed ways.”[/i]

So very true.

I didn’t have the time in the last 12hours to actually read any of the source material. In fact I only read the headlines and closed some positions because the headlines lead the herd and the herd lead the headlines.

And at this stage today’s events will continue to be interpreted as a step towards moderation for the next few weeks or months until an inflation report or a fed rate rise slaps more sense into them.

Personally, I’m positioning myself for a higher inflation and higher rates for longer environment.

For some longer term context. Have a look at this link to see how exceptional the current period is:

https://www.longtermtrends.net/real-interest-rate/

IMHO. A fed fund rate of 4ish and mortgages at 6ish in still accommodative as they are historically on the low end still.

I still don’t see why people freak out at 6% mortgage interest rates and act like they will go back down again into 5% or lower. The only way we ever get below 5% again is if the FED buys MBS again. Banks do not want to carry a 30 year mortgage less than 5%. Too much risk involved. That is why 98% of all loans since 2010 were basically bought or backed by the GSE.

The current rate is lower than all but 7 or 8 of the last 50 years of Fed Fund rates going back to 1965.

It’s mortgage brokers, realtors, and home builders “freaking out” the most.

As for prospective homebuyers, those that aren’t trading up with substantial home equity are shut out or agree to become debt slaves, candidates for future default.

“I still don’t see why people freak out at 6% mortgage interest rates…”

Its more the rate of change and lack of preparation for this change than anything. If we stay here long enough people will stop worrying about 6%. Its just we shot up to 6% from 3% in about one year, when the trend for the last decade was to slowly trickle down from 6% to 3%. The absolute value (6%) isn’t bad, but the rate of change (2x base in one year relative to average of 1/10th that equivalent rate in the other direction for and average year of the prior decade) is understandably setting some hair and undergarments on fire. If it either stays at or above 6% for two more years, no one will fret about 6% or cry about the need to get back to 3% any more; 6% will seem fine once again.

Think of it like: “we spent 2 seconds dropping 64 feet after climbing 64 feet over the previous 20 seconds. I don’t get what the issue is, we are back at the same altitude we were over a minute ago.” That is the exact timing, speed, and height parameters of driving up a 20% grade ramp that is 326 feet long, leisurely at just over 11 miles per hour up to about 64 feet of height over 20 seconds where the ramp ends and then dropping off the end of the ramp in free fall to hit the ground 64 feet below in 2 seconds … but you finished at the same altitude you started!

Agree.

Am doing same.

Business media sucks. It’s surprising that there is so much misinformation in the so called “information age”. Information is true power and “misinformation” is equivalent of slavery (a prison for your mind).

The only way to fix this is to remove the monopoly of big tech companies and break the cloud. The people should have a rack of 5 cheap servers in their garage and make it part of a cooperative web that is not controlled by big tech for profit.

“The only way to fix this is to remove the monopoly of big tech companies and break the cloud. The people should have a rack of 5 cheap servers in their garage and make it part of a cooperative web that is not controlled by big tech for profit.”

Price out the cost per installation to have the equivalent functionality of a large-scale cloud server and I suspect that very few people would join this cooperative. (Consider power and network redundancy, loss of deep discounts by only buying a few servers and disks at a time, backup costs and hassles to the participants, etc.)

“have a rack of 5 cheap servers in their garage” From 1994 until about 2005 I did this, because the cloud didn’t exist. No one is going to do this because it’s an expensive, time-sucking PITA. You could say that people should build their own houses and cars, and raise their own tomatoes and chickens, but no one is going to do that either.

Oh and cooperatives suck too. Any organization not motivated by profit eventually becomes dominated by arrogant egotists that drive away any reasonable people. See any HOA.

“See any HOA.”

Fuck Yea.

Apple started in a garage!

For public facing official to assemble the words that say approximately what they mean but for the mass of listeners to hear differently what they want – is strange magic.

That may be because Wolf’s post is almost exclusively quotations of what was said and not interpretation which is mostly what I see in the media.

100%, the Fed should have removed his glasses and screamd “Stop Spending!” I have never seen it this bad.

Things can get worse.

Remember Tim Geithner’s eyes in March of 2009…he literally looked like he was going to be executed.

This is a sad, badly declining nation with a ntl debt-to-GDP of at *least* 100% (probably closer to 150% after all “implicit guarantees” honestly factored in…remember how much hidden dirty laundry came out for tiny Greece…).

And our “leadership class” (which has guided the past 55 yrs of decline) is likely the *worst* it has ever been (who are the genius statesmen/business people capable of reversing this decline?).

They *never* had the “fixes” they perpetually claimed for half a century…

I think a bigger issue than debt-to-GDP is young people in mass realizing they just aren’t going to have much in life. Very dangerous situation when lots of people have little to nothing to lose.

I agree.

But I’m not sure from which the direction the dubious/dangerous “Man (Woman?) on the White Horse” in the US is coming from, the Left or the Right.

And it is just depressing/worrying that Putin is okay with throwing another 250k to 500k Russians against Ukraine.

At this point, I think it would take a Chinese move in the east to shock some sense of rationality/proportion into Putin (and China lacks near term motivation).

The US is too debilitated to do a *lot* more for Ukraine and Russian numbers may tell in Ukraine.

Lauren:

I must interact with a completely different group of young people than you. While not all have every *thing* they want, few (more like none) of those that I know express the hopelessness that you espouse. The ones that I know are planning for their futures and taking steps to continue to achieve their ever-evolving personal goals. And, yes, that includes home ownership – many of which have moved from their starter home to the next leg up – and career growth. Age group? 30’s and early 40’s.

I’m more fearful of the FSA (*free sh!t army) that thinks their future is free government cheese and winning the lottery (which in some circles, playing the lottery is considered the “stupid tax”).

El Katz,

Thank you for so clearly describing survivorship bias.

El Katz,

Two days ago you said: “Too many people with champagne tastes and a beer budget bemoaning the “affordability gap” because they can’t have a HGTV dream home.”

If all the people you know in their 30s and early 40s are doing so well with their ever-evolving personal goals, including home ownership, who were you talking about when you made this comment?

The more macro stats you know, the more worried you are.

Besides ntl-debt-to-GDP, there are 50 years worth of trade deficits and the unfunded liabilities of SS and every public sector pension (which I only hope will add *just* 50% to the debt-to-GDP number).

If anybody can make me feel better about those 3 items, I’ll welcome them.

El Katz:

‘The ones that I know are planning for their futures and taking steps to continue to achieve their ever-evolving personal goals. And, yes, that includes home ownership – many of which have moved from their starter home to the next leg up – and career growth. Age group? 30’s and early 40’s.’

Good. I don’t argue with success.

However, as Wolf says, no one escapes inflation. The decimation of the purchasing power of the dollar is an emergency, no two ways about it. What would you say to someone pulling in say $12 an hour (besides get a better paying job)?

@Lauren – Don’t worry. We still have millions of illegal immigrants crossing the border to live in the US and help pay off the debt? I am not sure many other countries have the same problem. The U.S. is still one of the best places to live.

cas127,

I hope this helps on two of those issues. Past trade deficits are just that, in the past. The surplus countries got their dollars, treasuries, or whatever. They’ve been paid with fiat dollars. SS is essentially pay as you go, with current workers largely covering current beneficiaries. Benefits may need to be cut as the worker to retiree ratio worsens, or taxes increased, but as long as there are workers something will be there.

Public pensions are another issue because some states and municipalities are well funded, while many are not. Municipal bankruptcy and state level default (it happened during the Great Depression) may come into play for the most underfunded, but I think this is the thorniest issue of the three.

Rojo,

I appreciate the effort but…

1) When real trade deficits persist for essentially 50 years straight, it is very hard to avoid the dangerous conclusion that the US has simply rendered itself (very) uncompetitive in the production of real goods. The problem hasn’t self-corrected, it has gotten worse.

And real goods production is the bottom line in international trade.

No other country in the world gets away with endlessly issuing empty paper promise IOUs (greenbacks, US Treasuries) that are used to buy *real goods* that cost exporting countries real, costly resources.

What does holding a USD get you? A “claim” to buy crappy goods/rotting property in a rapidly declining US mainland.

What does holding US Treasuries get you? For 20 years – ZIRP.

Who will ship endlessly to such a “buyer” paying on (worsening) credit?

2) SS – sure the enormous deficits could be fixed *in theory* – but then why haven’t they for 50 years? Because DC is absolutely terrified of blowback – which only worsens with delay. The DC entitlements crisis is huge and intractable – if it weren’t, it would have been addressed decades ago.

The G covers over 50% of the medical industry’s astronomical share of US GDP – it could have strangled medical inflation a long, long time ago. But well placed political power/myths/lies have castrated almost every “fix”.

Ditto student loans/higher education cartel.

Again, I appreciate the effort, but after decades of vague DC hand waving about “we have it under control” I need specific action plans with hard costs.

“2) SS – sure the enormous deficits could be fixed *in theory* – but then why haven’t they for 50 years? ”

That’s BS. I don’t know why this BS keeps getting spread. SS accumulated $2.8 trillion in surpluses over the past 30 years, and that surplus has just now flattened out:

https://wolfstreet.com/2022/11/08/status-of-the-social-security-trust-fund-income-and-outgo-fiscal-2022/

cas127,

You keep adding new issues and want “specific action plans with hard costs.” Books have been written on these topics, and the comment section here is not the place to resolve them. Even if such an action plan existed for one of the issues you raise, is it politically possible? I get the sense you’re younger, because I used to think like that. I’ve reached an age where I accept the general mode of operation is muddling along until a crisis of some kind maybe forces more substantial change.

I agree the US trade deficits are too high, but do not discount the enormous productive capacity of the US. Living standards may decline a bit if other countries no longer accept dollars for real goods, but I think the US can adjust to that by increasing its own productive capacity. SS was tweaked in the 1980s and can be tweaked again if necessary. Things are never as good or as bad as they seem. That said, I know you’ll think this will be a wholly inadequate reply.

Wolfstreet is one of a kind. And we are lucky to have it. The “media” on the other hand will twist everything into a pretzel, even direct quotes. There are no journalists left in media. Maybe few, and far between.

Pure desperation on the part of markets, as always. Nothing dovish in his speech like other media is suggesting.

The new taking point of the financial media is ” Disinflation” at least until the minutes come out.

Yes, what the heck is “disinflation”. Certainly not deflation.

Seems like they are talking about a negative second derivative of price. I.e., price increases have slowed down.

DC will try to memory hole the insane inflation of 2021 as fast as it can. The inflation will still be baked in, but year-over-year changes will be the only item they ever talk about.

I want deflation actually.

Inflation but at a slower rate? Disinflation sounds better like deflation but prices are not going down just yet. Nobody like deflation as it is associated with the Great Depression.

A slowing of price increases = disinflation

Disinflation is a deceleration in the rate of inflation. 9.2% to 6.5% is disinflation. We still have high inflation.

Deflation would be negative inflation. We’re a long way from that!

This one question got off to a good start:

“I wonder if you considered the idea of whether or not your understanding of the inflation dynamic may be wrong….”

Disregard the rest. The Fed is the primary cause of inflation. They really ought to consider that much more seriously!

Wolf, I don’t get a secure feeling knowing that the Social Security trust fund consists primarily of U.S.government bonds held to maturity. At that time, the U.S.government will pay the fund out of current revenues. Isn’t that the problem? That is, the good faith and credit of the U.S.government is erected on top of a Ponzi scheme?

Treasury securities are my most secure investment. That’s where the money goes that I really don’t want to lose.

There is no problem, other than the outgo being slightly higher than the income. This fearmongering is just plain BS. I normally delete this “Ponzi scheme” braindead BS

REEAD THIS:

https://wolfstreet.com/2022/11/08/status-of-the-social-security-trust-fund-income-and-outgo-fiscal-2022/

I can avoid the trigger words. Another way to say it is that potentially, the real value of U.S. government bonds could fall considerably below face value, more than a little bit. To be sure, gold did that from 2011-2015, though it was temporary. My worry about bonds is that their value will be destroyed permanently, caused by unending deficits and recurring Fed irresponsibility.

Laurence Hunt,

As bonds approach the maturity date, their price approaches face value because everyone knows that on the maturity date, the holder will get paid face value. So if you hold Treasury securities to maturity, you will always get face value. And if you buy them at issuance, like the SS fund does, you can NEVER have a capital loss, and you always collect your interest.

I love bonds for that reason — including corporates. But the era of interest rate repression screwed up bond investing. It’s now returning to its proper form.

I think you mean the loss of purchasing power due to inflation.

The big risk for bonds, and for ALL assets, is inflation: the loss of purchasing power. So you need to figure out how to get compensated for inflation by either yield (bonds) or by hoped-for price increases and yields if any (stocks, RE), etc. This is very hard to do when inflation is 8%, and stock prices and RE prices are dropping, whose losses are on top of the losses of purchasing power due to inflation.

(I did read that article when you published it. It’s the best summary I’ve seen of how social security works.)

You are understanding me correctly, Wolf, including in blaming the Fed. It’s my view that they have overinflated stocks, bonds, real estate and collectibles, as well as undermined capital investment. If I understand secular cycles, then after the next recession makes our economy more local, capital will start to flow into commodities and manufacturing again. I don’t think the Fed can win the inflation battle, because of deflating assets, it’s a no-win game.

When will fear to any discernable degree enter the markets? I have never seen anything like this but to give the pivot cult some credit, why would they believe Powell? It wasn’t long ago he “wasn’t thinking about thinking about” taking away the punchbowl and that he had infinite QE “ammunition” or whatever. They refuse to see him as anything other than the guy in the bar buying everyones drinks (using drink cards) and a nearby penthouse for the afterparty.

That’s the real crux, does the fed reserve control wall street or does wall street control the fed? People put up with some pretty bad inflation in the 70s and 80s. The fed will watch elevated inflation for a lot longer than it will watch a big bank teeter on bankruptcy. At least Powell is acknowledging that there are higher rates ahead. No discussion of the balance sheet, though.

No handle on labor and no handle on inflation, it’s not really a rip roaring success is it? Or are things actually going along quite swimmingly? Depends how you’ve placed your bets.

“That’s the real crux, does the fed reserve control wall street or does wall street control the fed?” The same question applies to political talking points. “That’s the real crux, does the Media control Washington or does Washington control the Media?

It’s the latter for both.

DC really does run things (badly) but there are deeply vested interests that essentially use the politicians as front-men/cut-outs to fade the heat for policies that end up hurting 327 million people to semi-shelter maybe 3 million.

Admittedly the long term difference between DC lobotomy/perma-state conspiracy can difficult to discern.

Question… what does Powell mean by ‘ex-housing’? Am not familiar with this term.

Just excluding housing I believe so other service categories that aren’t housing costs… Has to say this because everyone thinks housing and rent is a lagging indicator 🤦

Housing (rent factors) is part of services. So services inflation excluding housing (ex-housing) means a price index of all services except rent factors.

The distinction is important because rents in the price indices are surging now, but are expected to back off in a few months (I’m not persuaded they will, but that’s the expectation). So if you take rents out of the services price index, you get the other services alone — healthcare, insurance, repairs, financial services, haircuts, food services, delivery, transportation, etc. — and that portion of services is showing very persistent inflation, and that portion makes up 56% of the Fed’s preferred core PCE price index.

Got it. Thanks.

Love the questions today 😂 especially that last one questioning if the Fed understands inflation dynamics.

Going into the meeting today the thing markets were allegedly focused on was if they would continue to allude to plural hikes.

They did! Plural hikes! So that’s 2 25pt hikes to go and with the may one being only 30% priced in.

I understand why people are frustrated with the market exuberance but clearly it was another case where it didn’t really matter what Powell said it was gonna rip.

The Fed taking a data dependent approach also makes a ton of sense. They’ve already hiked 450 pts. Nobody would believe you 12 months ago or even 9 months ago that we’d be this high.

Markets will figure it out eventually.

P.S. 11 million job openings per jolts today.

ADP report was soft but it seems like that was due to weather during the reference week they used??? Maybe wolf can shed some light on that and if NFP will have that issue also🤷

And that right there is the problem- Powell was saying, not doing this week.

If he were really serious about this exuberance, it would have been another 75bp raise, not a retreat to 25bp. He almost had me convinced near the end of last year, but after yesterday- fuck it. He will have to walk the walk next time- I am done reading what he says. I am guessing we take out the highs in the market sometime before Summer. Right now oil is meandering under $80/bbl- if China really does open up the spigots, it will go back over $100/bbl by June, and all the disinflation Powell was bragging about yesterday will disappear. There isn’t a 2nd SPR for Biden to drain.

They will have no choice but to keep going until it’s clear the increases have worked a little more than needed. Only then would it make sense to back off. And probably not by much.

Even if the inflation have gone to zero it only means no price increases but the life essentials are already out of reach of 10s of millions of people

In other words rich people would come out winner and poor middle class would get screwed

RICH keep GAINS on POOR.

i.e. soft landing

Maybe. When products won’t fly off shelves, prices will go down. When contractors will ask for work, instead of now where you actually have to ask them to show up to a job, price for those services will also go down.

Did anyone ask him about falling 30YFRM?

Down to 6.04% today and likely to break through 6% next week.

Pulte Homes just came out and said they’re seeing housing starting to stabilize, and they intend to increase the number of houses they plan to build this year.

This entire morass is about housing. Wolf’s article yesterday paints a glass half full picture, primarily looking at those 8 or so top housing bubbles and how they’re taking very modest hits given how much home prices in those cities exploded over the last 5 years.

Looking at NY metro graph makes me ROTFLMAO. Down 1.6% since July but still up over 8% YoY. That’s hilarious.

Assuming Pulte is even 1/2 right, housing is well on its way towards seeing a bottoming trough in the next three months, given the labor market.

So at the end of the 12 month “carnage” that started last March when the Fed FINALLY decided QT was in order, we’re still going to be left with an enormously overpriced housing market.

I for one hope to see inflation bottom in the next few months & start to creep up again. Something has to force JPowell to put on his big boy Volcker pants and get ready for what lies ahead in late 2023 or early 2024: A 7% FFR or higher to get a grip on inflation. Side note: Someone send JP a DM emphasizing the point that 2% core PCE inflation outside of a major recession is pipe dream / dead.

If there’s a Fed pivot coming, it’s admitting as much. Inflation is here to stay.

When Pulte and others talk about housing is “stabilizing,” they mean volume isn’t plunging further. Prices drop low enough, and volume will pick up, that’s what we hopefully will see. Right now the market is frozen.

But mortgage applications for purchase mortgages just re-plunged (weekly data out today), so Pulte may have been premature.

But volume needs to pick up, and the way it does is by prices dropping far enough. And each time prices drop, there are more home sales.

Same during Housing Bust 1.

I think that the way housing volume picks up is lower mortgage rates. I get the sense too many potential sellers are holding ~3% mortgages and don’t want to list their house to move into a 6% mortgage. But it sounds like your saying, Wolf, that eventually sellers will adjust their prices lower given buyers are on the sidelines due to high prices. Hope something changes because right now we seem to be in a jam; even Sherwin Williams announced concerns about housing in their earnings call last week; and the stock tanked.

I have an application to rent a house in the Seattle area for $3,700 a month that was pulled off the market for $965k in the fall. The mortgage would have been $6,000 with 20% down. Why would I pay an extra $2,300 a month and tie up close to $200k. This is why prices are going to continue to fall.

@ Josh T – Do you have a wife and kids where you need to spend that much on a rental house? If you can swing $6k per month on a mortgage (seems you were considering buying), why not get a much cheaper rental and bank everything and just buy a house for cash in a few years?

@DepthCharge. I am in the market to buy and was watching that house before they took it off the market. I see the house as a place to live first and foremost. When it makes more sense to buy instead of rent, I will buy. Even if I had the money to pay cash today, why buy when I can rent for cheaper? $965k in t-bills would pay enough interest to cover the rent. I can live there and still have the cash. It is for this reason that I think prices still have more to come down.

“I can live there and still have the cash.”

I see. It’s not about actually buying and paying off the house at all. You don’t want any skin in the game, and you’re into the new school thinking that you never pay something off, you just do the Harryhowmuchamonth thing. Until this train of thought is expunged, the distortions will continue.

@DepthCharge. You made a lot of assumptions in your last statement that you know nothing about. I think you missed the point of my original post which was that real estate prices make no sense. No point in catching a falling knife. I think your desire for home ownership at all cost has helped perpetuate these current prices. Just because some one can afford to do something doesn’t mean they should. I am sorry, if I forgot to check my brain at the door.

Josh and DC, thank you for providing various viewpoints on rental/ownership. It was informative and enlightening. May you each take it as such, and have a great February!

“I think your desire for home ownership at all cost has helped perpetuate these current prices. Just because some one can afford to do something doesn’t mean they should. I am sorry, if I forgot to check my brain at the door.”

Textbook projection. You posted “I am in the market to buy and was watching that house before they took it off the market.” I myself am not even in the market to buy a house. You are an idiot, I know that much. Bye now.

Josh T,

You may as well let that nonsense go. Good luck with your rental or home purchase.

Reply to Josh –

Other side of the state… not that it is cheap here (!) but my apartment complex 1BR is $825. Admittedly no frills but not a bad part of town. Low end of the market in Spokane Valley. $3700 a month would destroy my savings much too quickly.

@Randy. I actually grew up in Spokane and my parents still live there. Go Cougs!

We may see a seasonal spring bump that will have everyone screaming “The Bottom Is In” In my experience Buyers have started entering the spring buying season earlier and earlier each year for the last 10 years so it will look like a robust start only to fall off earlier and then we will be back to price cuts around May-June

Right. If volume doesn’t plunge further, then that means a bottom / trough is forming. I’m pretty sure that’s what I just said.

Anytime you near or reach a bottom, then prices generally stop falling. I suspect that to occur by late spring / early summer.

And at no point did I say we’re going to see significant rise in prices. There continues to be this tug of war between buyers & sellers with neither having a clear upper hand.

The last I checked that’s called a normal market with 3-5% annual price gains. But even then if that comes to pass, then we’re still left with insanely high home prices.

At some point in the next 18-24 months, there’s going to be a significant recession. The main question then becomes does Uncle Sam let rent & mortgage relief return or do then let the market via foreclosures manage the fall.

With so many Fed owned houses, one has to wonder, right?

What I said was this: “But volume needs to pick up, and the way it does is by prices dropping far enough. And each time prices drop, there are more home sales.”

During the housing bust, there were big increases in sales volume, even as prices collapsed. From the NAR: volume spiked in the worst years of the housing bust into 2012. And below the price chart by NAR

Good lord. No recession in sight. No stabilization of house prices in sight. Not even close.

Thank you for breaking it down since I didn’t watch the live press coverage.

Hawkish alright but the market and many commenters on here must see PowPow with a permanent Sike sign attached to his forehead, otherwise I can’t see how anyone would interpret this as dovish or pivot in nature…

Then again, this is a living example of once trust is broken it can be loss forever or take a lifetime to regain. I mean after 20+ years if not more of FED being the ultimate market enabler and always coming to the rescue, I can see why a lot of people can’t process FED can be go the opposite way despite actual action as proof.

There’s a persistence of belief in the reliability of most institutions, the Federal Reserve just being one. “Faith springs eternal”. They’ve been wrong so often but look at the effects: markets around the world are hanging on every word Powell spoke. Look back a year or too and nearly everyone knew that inflation was on its way. Everyone ex-Federal Reserve.

I’m reminded of the commentary of stock market “analysts” who almost never issue a “sell” recommendation, and we know we know why. Just 14 years ago, the highly respected credit instutions, like Fitch, Standard & Poors, et al, we’re grading tranches of mortgages at AAA before the ground opened up and the housing market fell in. They got a tiny fine for their deceit. Yet, these “institutions” have not lost credibility in spite of being so wrong.

How – another excellent example of our national ADD (or: “…I just take a pill for that, now…”).

may we all find a better day.

My key view is that the Fed is looking back in time for data (one to three months at least), while rate increases and QT impacts have a deferred impact. It’s like taking exlax in the evening after looking back at the missed morning business, but not being aware that the medicine may cause midnight or next morning drama that hasn’t been considered. JMO

That’s nothing I like to see more than for this insane delusion stock and housing market to have some explosive bloody diaherrea metaphorically speaking maybe…

Heard a couple of interesting things today.

US bond market most inverted ever.

World bond index inverted for first time ever.

At least we are seeing a lot of history in our lifetimes like negative interest rates and thousands of crypto coins. Kind of like living in tulip bubble or Mississippi stock bubble.

Can you imagine actually believing in crypto, especially now? It’s blind greed.

Can you believe that flagellating yourself will protect you from the Black Plague or that Snow White got it on with 7 dwarves? Wait a minute… I need more coffee.

Maybe it missed it but there was not much mention around the specifics of QT. Wasn’t there a thought that they may have to start selling MBS outright because of declining home sales?

Why isn’t the financial press more inquisitive about QT – is it that they just don’t really understand it?

The statement, the “Implementation Notes,” and Powell all said the same thing: QT will continue at the same pace. It’s on autopilot.

I said about the same thing in my article. There isn’t much to talk about.

However, if something changes, it will likely be a shift to selling MBS outright. If this is being planned, we’ll see it crop up in the meeting minutes somewhere along the line. If that happens, it will be a big topic.

Tomorrow is my day to discuss QT based on the balance sheet that will come out; it will be my monthly update.

Nobody from the press bothered to ask about MBS sales; with a few exceptions they were all asking slight variations on “Wen pivot?”

But it may be significant that Powell didn’t mention them spontaneously, either.

The longer Powell takes to engineer his soft landing, the poorer we all become. I get it,

using time to paper over the years of failures is standard Fed policy.

Take your earplugs out and listen to what he actually said and not what you imagine he said.

This BS — “Powell is spineless” — has been going on ever since he first started talking about rate hikes back in the fall of 2021, and meanwhile he hiked by 450 basis points in 10 months, with more rate hikes coming, and he shed $500 billion in assets in six months, and will keep shedding at that rate. What’s your problem?

“Take your earplugs out and listen to what he actually said”

You’ve helped me finally figure everything out. Not only do a whole lot of market participants (I don’t dare call them “investors” in this mania) have in earbuds, listening to who knows what music, they also SUCK ts lip reading!!!

Yes the correct word is gambler, not investor.

Maybe some of these people just hear the gentle voice behind the ear plugs? Personally I think the markets are delusional; they’re the ones who need to listen more closely.

Wolf, the issue is that market participants are not on board him. The 10 year dropped 13 basis points and mortgages may have a 5 handle soon. He hasn’t even hinted at selling MBS to control a possible resurgence in the housing market. He may have done a lot but he needs to do a lot more. He missed the opportunity to go 50 today and show the markets he means business.

I do not understand either why Powell doesn’t just drop a surprise 50bps between meetings. It would show that he means business.

If you drain the O/N RRPs, you inject cash and reserves back into the commercial banking system. That’s going to keep the award rate high, and longer-term rates lower. That implies a permanent interest rate inversion accompanied by stagflation.

Sir: I very much respect and Thank you for your analysis. One issue in this Quantitative Tightening (QT) that is disturbing is the mortgage securities; these only look like they roll off when mortgage is payed off, but not an outright sale of the securities. As housing is an important part of GDP is the Federal Reserve actually maintaining a back door stimulus program as money that would be tied up in securities is free to loan more, such as the 40 year $3 million mortgage loan advertisement now appearing. Bottom line is Powell honest or are there more “stimulus tools?”

I think what commenter “enough” means is Powell should have hiked that rate 1% for 4 months showing seriousness until enough chaos ensued forcing immediate fiscal change. It would be an overnight panic LOL.

By the 2nd 1% rate hike, early birds would have taken notice and immediately changed habits. By the 3rd or 4th, limited panic would have started causing enough companies and people to change their habits and question the choices made.

I get the reasoning – it’s slow burn. But none of this teaches a lesson.

This still seemed a disappointing performance from Powell. He started off on the wrong foot with his answer to the first question about easing financial conditions. Having correctly put FC in the crosshairs for most of last year, he actually dismissed them by shifting focus to “sustained” FC and then characterizing them as having tightened. This dissembling, as it was reinforced, naturally sparked an orgy of even further easing financial conditions.

The dollar plunged against foreign currencies, against stocks, bonds, and commodities. That is, prices soared. Being traded in real time, tick-by-tick auction markets, inflation registers here instantly. Unless soon reversed, the effects of dollar depreciation will pass through the pipeline and be reflected in the coming months as a stalling in the consumer price disinflation trend.

Markets have misread Powell before. If there is still confusion about the Fed’s stance, the Fed is to blame. It worried in December that weaker action might trigger an “unwarranted” easing in financial conditions, and tried to offset it with tougher talk. It gambled and lost. Today it doubled down on its folly.

Tough talk does not commit the Fed to any policy action three or four meetings hence and the markets know it. But to couple weak action with weak talk? How many short term FC easings must happen before it’s a “sustained” easing?

It seems like he is different during q&a than during the prepared remarks. I’ve noticed this on multiple occasions.

That was a truly bizarre moment–he flat out denied that conditions have eased lately and then quickly changed the subject to long term conditions–and it didn’t help that this was at the beginning of the Q&A. I’ve said this before, but the man is not very good at speaking off the cuff. He dithers and equivocates at the best of times, and today he just plain lied.

If the Fed is really concerned about its actions sparking unwarranted easing, someone in that building needs to sit down with Powell and explain to him how his word choices and his inability to frame things properly keep sparking that very easing, over and over.

You bet. An obvious alternative is to rely less on talk and more on action. If the Fed thinks more tightening is warranted, what the heck is it waiting for?

Even assuming it’s got its rate target right, it has the option of stepping up QT. It’s still sporting a pretty hefty balance sheet. Does it really need that big load of mortgages? Is playing favorites with sectors really monetary policy?

It could easily have done its baby step hike without slamming the dollar and provoking an “unwarranted” easing of financial conditions, just by tweaking QT a bit.

Or is mollycoddling Wall Street more important than quelling inflation?

It’s like Wally Cox being cast as “The Terminator”.

There’s no need to fear, the Terminator is here!

I agree with you. As does the Wall Street Journal, which had an “I dare you, Powell” headline this morning:

“Stock, Bond and Crypto Investors Call Fed’s Bluff on Interest Rates”

I hope Wolf is correct, but there are many institutional forces working against him. And what happens as the 2024 campaign gets closer? More pressure to ease up.

I’m rooting for Wolf too. I’ve seen the same thing he has before … a hawkish Powell interpreted and spun as dovish by the markets and media. Having said that, this latest Powell struck me as a changeling left by the pod people, a pale imitation of last year’s Powell.

The about face on financial conditions is what spooked me. Maybe markets too. Powell effectively triggered a Fed put with markets already high and rising. We can still hope it was an aberration … as always, we will see…

I just really want to thank Wolf for all the great analyses! One simply cannot rely on most of the financial media as they largely report things inaccurately, either out of ignorance or intentionally (for some interested party’s benefit).

When reading Wolf’s analyses compared to most of the media’s, it’s like two different worlds: It seems like the overall market is living in lala land, particularly based on its general reaction over the last month!

As Wolf has said, the Fed cannot yet pivot this time because of “raging inflation.” The market seems to forgot this (or conveniently ignore this). Previous Fed easing was done when inflation was reportedly low: certainly not the case now.

Today’s press conference was extremely dovish. Wolf, you’ve got to read between the lines.

1) When Powell said “financial conditions have already tightened a lot & they’re not concerned about short term market movements,” that caused the first explosion higher.

Not only was the second part completely unnecessary, the first part is false. The Chicago National Financial Conditions Index is lower than it was 10 months ago when they first started raising rates.

2) When Powell said the market pricing in a lower FFR peak & year-end rate cuts was due to differing economic outlooks. Rather than shutting the door on rate cuts for the time being, when December’s NFP report just posted the lowest unemployment rate in 50 years, he implied they could happen. Naturally, the market responded by pushing up rate cut odds even higher.

He could have laid out explicit conditions (similar to what they did for liftoff), eg cuts are off the table without both (1) PCE inflation at 2% & (2) unemployment rate of at least x%. No such thing.

3) When Powell said there was no way they could pause, then raise rates again. One hypothetical scenario would be if inflation rebounded again during the “strategic pause.” Doesn’t have to be the base case scenario, just a scenario where it can happen. Instead he just said “nah, that’s not something we’re considering.” WTF?

Powell knew exactly what he was doing when he said the things he did. I believe Wall Street interpreted his statements correctly, hence the rally.

I missed #3. If that happened it is indeed a red flag. Like you said, WTF?

Powell said

“I continue to think that it is very difficult to manage the risk of doing too little, and finding out in six or 12 months that we actually were close but didn’t get the job done, and inflation springs back, and we have to go back in, and now you really do worry about expectations getting unanchored and that kind of thing. This is a very difficult risk to manage.

“Whereas, we have no incentive or desire to over-tighten, but if we feel we have gone too far, and inflation is coming down faster than we expect, we have tools that would work on that.

The concern is a premature so-called “strategic pause” before “the job is done”. This is an indication that to err on the side of overtightening is the path, not to pause too early and then resume tightening. This philosophy is in no way dovish, it is a signal of the intestinal fortitude to keep turning the wrench right without pause.

Thank you for this clarification. Much appreciated.

Jackson Y

For 10 months, there are morons out there who said at every press conference that he was “extremely dovish,” and they twisted and torqued his words into being “extremely dovish,” and by now the Fed has hiked by 450 basis points in 10 months and shed $500 billion in assets in 6 months, and it’s continuing to hike rates, and QT continues on autopilot. You people are just hilarious.

If the FF rate were still at 0% to 0.25%, I would give you a nod. But it’s 4.5% to 4.75%, higher than anyone imagined a year ago. It’s going to be over 5% by spring. By summer, he will have shed $1 trillion in assets. This “extremely dovish” BS has been a limp joke for 10 months.

Nick the pig is the worst offender.

Wolf,

I think that until people see another 20%+ stock index hit (and/or median home prices falling 30%+) they aren’t going to really believe that rate hikes are meaningful/serious.

(And once those hits happen, they will lament the accomplished facts)

After 20 years of ZIRP, they judge from effects rather than intentions.

The price of creating a fairyland to (temporarily) live in is that everyone ends up going insane…either from belief (this is *wonderful and can never end*) or disbelief (the hopelessness of unrepayable debts).

As to the SP 500 defying interest rate gravity, it is helpful to examine the PEs of the highest weighted members.

With the PEs of the Apples/Microsofts/Googles in the 20 to 28 range they don’t seem insane (relative to ZIRP era stds) but at traditional interest rates, they should be closer to 14-15.

So SP 500 overweighting at the top (5-10/500 members maybe 20%+ of the Index) meshes with a semi “flight to quality” to keep this gut-shot duck flying.

(Long term Treasury rates are likely key here…until 5%-7% 10yrs can be had (at what cost to real economy?) too many punters will hang on Apple/Microsoft/Google/some undefined miracle new tech).

And housing? Well, when will inventories return to 2019 levels?

I think the younger generations expect instant results.

And guess what?

Mr. Market doesn’t care one bit.

Neither does it care what you say or think.

Wallstreet is full of it. He was not dovish by any stretch of the imagination. Wallstreet deals in wishful thinking. They need more bagholders.

There is a feed- back loop between market froth and Fed determination. The Fed has all but hired sky- writers to announce it is trying to induce a recession. If the market uses ANOTHER bump in rates to rally it is just telling the Fed to tighten some more.

The most telling remark from Powell is not in these remarks: ‘House prices must come down so Americans can afford houses’

How do we parse that?

All this ZH type crap about Powell helping out his friends…..

Powell is approaching retirement and knows he was labeled a pussy after Mr. T laid into him for doing some baby steps in 2018. His main concern now, apart from doing the obvious, crushing inflation, is his legacy.

The thing is he hiked 25 bps, per market expectation. He should have hiked 50 bps just to show that he does not answer to markets. It’s really that simple.

But yeah, did I say that the sun will never set on SocalJim’s RE empire?

Keep in mind that intelligent reporters are thrown out of the meetings. Yellin specialty.

Ultimately, the stock market is about perception and people believed whatever they imagined from Powell to push their own agenda.

Here are my thoughts:

1. Services inflation can only suddenly come down during a recession. I remember all those desperate contractors during the last housing bust.

2. Rent inflation can only come down during a severe recession. I remember 50% falling rents after the dot.com bust.

3. With dollar falling and commodities rising against it, inflation will pick up again. Two or three months of surging inflation with tank the stock market and change the narrative. Look at copper prices, with oil soon to follow now that China has reopened.

4. Companies are missing revenue and yet they are rallying (look at Facebook today). How? 40 billion in buybacks announced from FB, 75 billion from Chevron, etc. The entire US economy has become a giant casino. There is no soft landing in any of this now that the Fed has no credibility and markets daring Powell.

“Fed has no credibility and markets daring Powell’ AGAIN!

I wish it was not true.

Shock and Awe…weapons of mass destruction…. Don’t fight the Feds….FTX founder will be found not guilty…..rising tide lifts all boats….Powell works in the best interest of all Americans. My home hast lost $100k in value since April 2022. Over 50,000 vehicles were reported stolen in Colorado last year. Boulder public library closed due the crystal meth toxic levels. U can’t handle the truth.

Powell did what he had to do as he is answerable to elites and rich people.

Common joe and poor people are kn their own

Even if inflation goes down to zero middle class and poor people are priced out of decent life essentials.

Its criminal thst a clique of few private bankerd have so much power

congress, fed, market going opposite ways isn’t healthy.

its a net loss game. this showdown will not end well for a lot of people -retirees, working people, investor, etc.

Funny, today I got a notice of rent increase by 9.98%. Contra Costa.

According to Powell.. its not true

At least two more 25 basis point increases. At least. No pivot. Not pivoting. Not gonna pivot. More work to do. Lots more work. Long way to go. Looooong way to go.

Excellent analysis, but so what? Who cares about the exact statements? Here’s what 99% will remember from today:

Powell:

“Inflation is going down faster than expected, so I don’t need to do anything urgent. If it keeps going like this I will stop the hikes, and then do some rate cuts this year.”

Problem is he didn’t say that. You fabricated that to suit your own agenda.

That is what Contramot said that others will take that away from the meeting.

And seeing what you have written about this for the past year I’m afraid they are right. The market will ignore the facts (at least 2 more hikes of .25% & no cuts this year) and spin Powells words, again, to mean that the punch bowl will be back shortly. That Powell is just jawboning and they’ll get those cuts this year.

Contramot is not even smart enough to use quotes correctly, so go ahead and believe that person.

From your description, the market is delusional. Eventually, reality will hit the market. Ignoring facts is not a good long-term speculation strategy. Powell has done everything he said he would do since at least Fall 2021 (too late for me, but he has finally acted). There’s no reason to think he’ll stop now unless inflation gets to 2%. In the interim, markets can be delusional and there’s not much he can do about that except stay the course.

If Powell changes course before inflation is down to 2% or there is a severe recession with significantly higher unemployment (say 8%) I’ll be wrong and call him out. Until then, I’ll just marvel at the stupidity of market participant’s willing to “ignore the facts…and spin Powells words, again…”

This is precisely why we can feel confident in shorting the markets on this rally. Widespread hallucinations.

Powell has not taken the impact of the Omnibus bill into account and the administration has not refilled the Strategic Reserve. Gas will be moving up again, dragging the CPI with it.

The real fireworks has not started yet.

We are seeing $3.00 RUG here in Houston now and $4.00+ D2 (diesel). Quite a jump from a couple of months ago. When China opens fully, expect crude oil prices to start heading up further. OPEC + can’t handle $75 crude and they will see to it that prices head up.

Fed is in the catbird seat. Growth is good, two jobs for every worker. Is there something wrong with this picture, other than those nasty comparative measures of inflation when the real thing moves like a glacier. It was always transitory. Inflation and growth are the same thing.

So I was watching the FOMC press conference video on the Fed’s YouTube channel and it’s monetized with ads lol.

The central bank is collecting ad revenue from YouTube. I wonder if that goes into the TGA.

A Big positive for the Federal Reserve and the economy from all the inflation and money printing is that it looks possible now, like old times, to control the economic cycles without printing fake fiat currency and by solely hiking and lowering interest rates. Time will tell. However, I doubt if they will ever be able to QT the bulk of their balance sheet for many years if ever.

This is what Jim Bullard suggested a few months ago. I hope it’s true.

The problem I see with the FED is they showed up in a day – an emergency meeting – and hammered rates to zero the very moment the stock markets started selling off. In one fell swoop. And they immediately announced almost a trillion dollars of QE to buy treasuries and MBS. Blammo. Go big, JUICE THE MARKETS. All in a day’s work.

Because why, a bunch of rich people were going to have to start taking some paper losses? That’s the crisis? And they followed it up with another $4 trillion or whatever over the course of several months- just printing like madmen and driving shelter costs, and automobiles, and everything else out of the reach of everybody but the most wealthy.

But, when that REAL crisis showed up from their deranged policies – an inflation emergency on top of a housing crisis, they decided to stand back and insult society with things like “we’re not even thinking about thinking about raising rates,” and “inflation is transitory.” But this stuff was really, REALLY hurting people. BADLY.

What’s more painful – a billionaire having to take a 50% paper loss, or a family living in a local park because their rental house was scooped out from under them by a “market disruptor ibuyer” who was loading up on shacks with Jerome Powell’s Weimerbucks?

Look at the FED’s balance sheet and how quickly it ballooned, but how S-L-O-W-L-Y it is receding. This is the problem with the FED. It’s an emergency when it involved the wealthy, but it’s a “wait and see” when it’s hurting the middle class and the poor. I hate Jerome Powell. I hate the FED. They are the enemy of the American people, in my opinion.

Good summary.

Look, I agree with your general view of the Fed, but they didn’t hammer interest rates down in March of 2020 because stocks were selling off. They did so because the bond market was seizing up.

That’s the main concern. If even good companies can’t borrow in the short term, the economy collapses. That’s not to say I approve of ZIRP for as long as we had it or QE ever, but it wasn’t the stock market that drove the March 2020 actions.

Intervening in the bond market may have been necessary. Was it $5 trillion necessary?

No, the scope was completely absurd, and I said so at the time, saying that we were going to have massive inflation (I have an email to a friend from March of 2020, which I just checked).

Why do you say the economy would have collapsed because bond market was seizing up? We just witnessed bond prices fall 20-40% in 2021/2022, and the unemployment is at record lows.

If there is temporary illiquidity in the bond market, you let it play out until prices adjust and liquidity returns. Any entity that folds because it relies on 0$ financing needs to go away.

Yes agreed up to a point, but his wait and see if inflation isn’t transitory position was after serious covid supply disruption and before Russia started a war in Europe, so understandable to me.

You are exactly right, as usual. Unfortunately the average guy on the street either doesn’t know anything about the Federal Reserve or if he does, he thinks it’s working for him. When the average American believes that the Federal Reserve is his or her enemy, then it will no longer be business as usual. That day is a long way off.

This is a good analysis.

However, unlike 2019, they are not caving to rich people now. Probably because inflation will hurt everyone much worse in the long run. They certainly aren’t responding rapidly to help the poor and middle.

1) High beta day. An Upthrust in a downturn is bs. The Dow didn’t care !

2) Question : can we have 2,400 SPX, 2% inflation and soft landing ?

3) Question : can the Fed dump RRP to zero, before $5T RRP ?

4) Question : can RRP rate be zero and Fedrate 5.25% ?

5) Question : will the Euro zone crack first , before US, or both crack together in unison ?

Is it possible he wants to keep markets as smooth as possible so as to give time to get the rates up high enough if he is required to cut them when he needs. More firepower if you will. He goes too hard too early the whole thing falls apart with not many bullets in the chamber so to speak.

Given the complacent markets and loosening financial conditions he was soft-ish. His statements were less convincing than last summer. It isn’t just words on paper, it’s the impression that comes across.

Not really any room to debate that.

Wolf, I have agreed with your interpretation of each press conference since Powell started raising rates. But not this time. I wonder how many of the people in these comments actually watched it. Maybe Powell really is still hawkish, but that is not what he conveyed today. Even his body language suggested he was forcing himself to not declare victory and he is on the cusp of declaring inflation defeated. It is not difficult to understand the market reaction whether it proves to be correct or not.

“even his body language” … LOL. He stood slumped-over as always, his hands on the lectern. He should work on his posture. They guy’s posture is that of an old man, but he’s only 69. If you try to read stuff into his body language, you’re grasping at straws.

I agree Wolf,

There is modern evidence suggesting those who interpret body language of strangers are simply subconsciously projecting their own personal feelings and assigning those to the target individual as ¨valid body language¨. The famous Greek philosophers clearly had the same idea over two thousand years ago.

Individuals in today´s society still place too much emphasis on the importance of interpreting things they have no control over truly understanding, for example the behaviors and feelings of strangers, hence the ¨body language¨ readings that are *de rigeur* in daily life.

A non-event really. Just pleased the latest FOMC manipulation is in the rear view. I found the presser less hawkish than anticipated. There was a quote and a reinterpretation for everyone if one is inclined to defend a certain position.

My reflection is that it was a masterclass in charming and coalescing the market into believing in the end game of a soft landing. Emollient, a total fallacy well presented.

“Ongoing” infers at least two more rate hikes and possibly more. Further than plotted 0.25% increments are not big sticks with which to confront markets – however, it doesn’t matter because the big stick is QT. No change to QT will tighten financial conditions. MBS selling would be a big deal.

The stock market has the (false) narrative and liquidity it needs to propel higher and party on for now.

Powell sending a warning shot to Congress about the debt ceiling was yesterday’s “smackdown”.

Powell: “We can now say I think for the first time that the disinflationary process has started. We can see that and we see it really in goods prices so far.”

– Well, the ISM explains it very well. The ISM has been plunging for months and the New Orders…at 42 (which shows the future!!) is a terrible number!!!

Powell: “Given our outlook, I don’t see us cutting rates this year if our outlook comes true.”

Well…A Deep Recession will come true and you’ll have to cut the rates cause you (Federal Reserve) have always been unable to predict a recession…As you were not able in 2000 when the Yield Curves inverted, in 2007 (when the yield curves inverted) as you were not able in 2020 (when in 2019 the Yield Curves inverted and even after the Reverse Repo Crisis) – The funny thing is that there are still people that trust those Clowns!…

It’s politically impossible for the Fed to “predict” a recession, even while it’s actively engineering one to tackle inflation. The Fed is well aware of the implications of a yield curve inversion and continues to raise rates. Why do you think that is? The recession the Fed is “not predicting” (but actively encouraging) is needed to tame inflation. Sure, the Fed would like to avoid a recession and get inflation down to 2%, but by continuing to raise the FFR it tells you which one of those outcomes is most important to the Fed.

Much of the angst here isn’t about Powell’s speech, it’s about the stock market’s reaction to it. And the big rally over the last few months. I think the assumption has always been that the blow-off top already happened in the market last year. Now I’m not so sure. We actually might be rallying to the real blow off top as the market ignores the Fed. Maybe the S&P goes back up to near 4700 or even surpasses it.

I believe reality will set in eventually, it’s just a matter of when.

I guess it comes down to personality, but I don’t understand the enthusiasm for stocks in a risky environment (mixed economic data, possibility of recession) when Treasurys, CDs, and simple bank accounts return 4-6%. Everyone buys the 8% (or whatever) long-term return argument, I suppose, or is chasing positive return against inflation, but to me it seems obvious to earn the 4-6% and wait out the turbulence. But I don’t have a gambler’s mindset.

Well, I personally think it would be unlikely that any of the averages will hit new highs. But this sharp, explosive rally is characteristic and expected in bear markets. It is the best time to get short.

Wolf, thank you. Your reporting has shown great light on what previously was a murky (to me at least) picture of the Fed from the mainstream press.

Reading this quote said all I need to know:

“We have a long way to go. It is the early stages of disinflation. It is most welcome to be able to say that, that we are now in disinflation, that is great, but we see that it has to spread through the economy and it will take time.”

They legitimately believe that inflation is slowing down, based on their preferred indices. We know that they favor a cautious approach (dovish hawks?). But we also know that they’re perfectly fine to send the inflation rate back to 2% on a slow steady decline.

The big question is whether this is possible. That’s a big unknown. I’d say that it is not, but that is just a guess and gut feeling. But the Fed does not know this either. I don’t believe you can deflate asset prices back to what passed as pre-covid normalcy, without significantly stunting the economy.

What I hope is learned from this era is that the FED should not unilaterally take it upon themselves to juice the markets. It’s clear that Congress likes giving away free money. The FED needs to be the foot on the brake next time. I hope that ZIRP goes down as one of the biggest follies in history and everyone involved should be forever branded as failures.

This is interesting watching the push & pull between the Markets and the Fed.

Indeed the NFCI does not seem to indicate the level of Financial Tightening that the Fed intends. So Powell isn’t going to back down yet. This bear market rally will peter out as earnings season comes to a close.

Thing is I’m not buying his 4% in Core Services minus Housing. I think it’s probably more than 5%.

Outside of Services, Truflation is showing inflation trickling back up. It was 5.3% in mid-Jan and it’s now 5.5% Basically Food & Fuel that is driving it.

I will say that things seemed to have stabilized, but at an elevated level (~6% rather than 2%) as the Fed has indicated.

So yes, the beatings will continue!

One thing we should all agree on is that Powell is one of the worst public speakers I have ever seen (although Janet Reno gave him a run for the money). He writes well, and can prepare things well ahead of time, but he gets nervous and stutters and stammers like a high school student. In my view, that’s what the market is interpreting as “dovish.” He can’t speak forcefully and enunciate well. That comes off as weakness, and the market equates weakness with dovishness.