Surge of delinquencies not caused by unemployment, but by taking Big Risks, hoping for Big Profits, and getting slapped, just as in 2019.

By Wolf Richter for WOLF STREET.

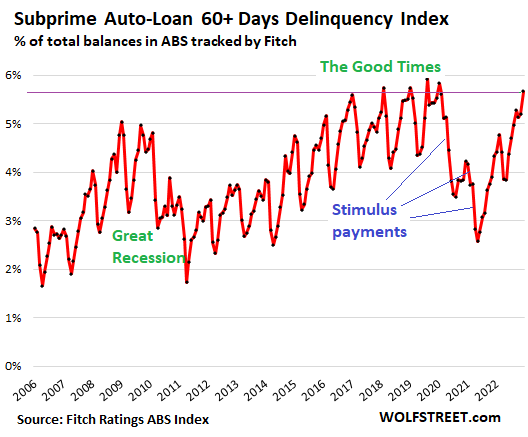

Delinquencies of subprime auto loans have bounced off the stimulus-fueled low levels during the pandemic, when borrowers got caught up on their auto loans with the money they got from stimulus checks and extra unemployment benefits, and from not having to make mortgage payments because they’d entered their mortgages into a forbearance program, and from not having to make rent payments because of the eviction bans. Most of this has now ended, and the money is gone, and subprime delinquency rates are surging.

Subprime delinquency rate rises, still below 2019 Good Times.

In December, the subprime auto-loan 60-days-and-over delinquency rate rose to 5.7% of total auto loan balances in the Asset-Backed Securities (ABS) rated by Fitch Ratings. The record in the 21st century was set in August 2019, the Good Times, of 5.9%.

Prime-rated auto loans are in pristine conditions.

Delinquency rates of “prime” rated auto loans are near record lows of a minuscule 0.2%, according to Fitch Ratings. During the worst moment of the Great Recession in January 2009, the prime delinquency rate rose to 0.9%, still minuscule. Prime auto loans are a low risk, low yield business.

Subprime-rated auto loans and Asset-Backed Securities (ABS).

Auto loans are rated subprime for the same reason a lot of bonds are rated “junk” (BB+ and below): the borrower has a much higher risk of defaulting on the debt.

Investors buy them because they get paid higher yields to compensate them for taking those higher risks. Subprime auto loans, just like junk bonds, are a high-risk business with potentially high profits and high losses.

Subprime loans on used vehicles come with interest rates on average of 15% to 20%, depending on how deep they’re into subprime, according to Experian. Investors are willing to take high risks to get these kinds of juicy yields.

Much of the subprime lending is done by a coterie of specialized lenders. Most of the subprime auto loans are packaged into Asset-Backed Securities (ABS) that investors such as bond funds and pension funds purchase for their higher yields.

ABS are structured with the equity tranche and the lowest-rated tranches taking the first losses. As losses increase, higher-rated tranches are starting to take losses. The top-rated tranche of a subprime-auto-loan ABS, perhaps rated “AA” (my cheat sheet for credit ratings of corporate bonds), will only take losses if there is severe damage to the ABS from defaults.

Tranches with high credit ratings carry the lowest yields, and investors that are more risk-averse buy them. Low rated tranches are bought by risk cowboys. And the lowest tranche is usually retained by the subprime lender that originated the loan – the required skin in the game, which is one of the reasons why small specialized lenders can go belly-up.

Subprime lending has been around for decades and is rife with abuses and scandals. Some subprime loans come with such huge interest rates that practically guarantee that the loans will default. Some subprime lenders take huge risks in their underwriting practices.

Occasionally regulators crack down, and so there are settlements and fines that subprime lenders consider part of the cost of doing business. And periodically, specialized lenders go belly-up because something didn’t pan out. The risk-taking is driven by high yields, and by the ease with which a vehicle can be repossessed and sold at auction.

In the years before the spike of used vehicle prices that started in 2020, the proceeds from auction sales covered 40% to 50% of the defaulted loan balance of subprime auto loans (the “recovery ratio”), according to Fitch Ratings.

But as used vehicle prices spiked from late-2020 through early 2022, the recovery ratio soared. For subprime auto loans, the recovery ratios exceeded 70% in 2021, far above any prior records, according to Fitch. Used vehicle prices are still very high but are now falling. So the recovery ratios are declining and will get back to around 40% to 50%.

Subprime, a small part ($210 billion) of total auto loans & leases ($1.52 trillion).

Subprime loans are largely focused on used vehicles with smaller amounts financed and make up only a small portion of the overall outstanding auto debt. So here are some basics about the magnitude of subprime auto loans, based on Experian’s Q3 report (it defines “subprime” as a credit score of 600 or below):

- Only 13.7% of overall outstanding balances of auto loans were subprime.

- Only 15.8% of the total number of loans and leases originated in Q3 were subprime.

- Only 5.2% of the number of new vehicle loans originated in Q3 were subprime.

- But 22.4% of the number of used vehicle loans originated in Q3 were subprime.

- Average amount of used vehicle loans originated in Q3: $28,506

- Average amount of new vehicle loans originated in Q3: $41,665.

Total auto loans and leases outstanding amounted to $1.52 trillion in Q3, according to data from the New York Fed. With 13.7% of the outstanding balances being subprime, the total amount of subprime-rated auto debt amounts to about $210 billion, most of which is owned by investors that bought the ABS.

Delinquencies driven by risk-taking in Good Times, not unemployment.

Note in the chart near the top of the page: The delinquency rate plunged from early 2010 through the spring of 2011 – during the Bad Times, during the unemployment crisis, the result of risks in new lending having been dialed back.

As you can also see in the chart, when the Fed continued to repress interest rates in 2011 and on, investors went on a wild chase for yield, and the risk taking increased across every asset class, including in subprime auto loans. This enthusiastic risk-taking caused the subprime delinquency rate to surge during those years and in August 2019, the Good Times, to hit a 21st-century record.

It was during these Good Times in mid-2019 that a gaggle of smaller specialized subprime auto lenders, owned by private equity firms, collapsed into bankruptcy, which I covered at the time.

This August 2019 record – and the bankruptcies of the specialized lenders – occurred while the job market was hot and unemployment very low. It occurred because these small lenders had been taking huge risks for years, to gain a big yield, in a world where yield had become scarce.

Despite this high delinquency rate in 2019, and the collapse of some of the smaller lenders, the auto lending business remained profitable for lenders that had managed their risks appropriately.

So the surge in delinquencies through 2019 was not caused by an employment crisis, but by increased risk taking beforehand.

The same thing now: The surge in delinquencies is not caused by any kind of unemployment crisis or whatever – the job market is historically tight and wages are surging – but by risk taking in 2020 through 2022.

The risk taking was further fueled by the mind-boggling spike in used vehicle prices when many of these loans were made, seducing lenders into thinking that they would get very high recovery rates for the loans that defaulted. And they did get record high recovery rates for a while. But they’re now coming down.

Despite the surge in delinquency rates back to the Good Times of 2019 levels, losses of subprime loans in the ABS that Fitch tracks have remained below those of 2019. In December, the Subprime Auto Loan Annualized Net Loss Index by Fitch rose to 8.3%, but this was still well below the 9.7% in December 2018, and 9.4% in December 2019.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Judging from the stock market real estate and the auto market it looks like the Federal reserve has a lot of work to do to bring inflation down especially with commodities and oil rising now.

we are already past the delinquencies of the great recession time period. my guess is that we see a much larger spike, like maybe up to 10% or more. there was a perfect storm to create this situation. lots of money that was temporarily floating around and very high car prices and lenders chasing after a hot market.

once we hit recession and job losses really pile up and home equity vanishes, then we will see who is swimming without shorts on.

the home price melt-down is going to take a while longer to gain more steam. there are always some foolish souls that think a small decrease in -price is a big opportunity to get a home cheap. patience. we are in for a 2-3 year downturn before the market clears out the excess

Wealth-Building Class 101.

If you have to take out a loan to buy a car, don’t buy a $28k car. Buy a $8k car instead, and don’t spend $5,000 on rims.

If you can’t pay cash for the car, you can’t afford it.

That’s some serious truth.

I can’t remember all the times I’d pull up to a corner that was an empty lot, and a new shiny bank has popped up.

Guess who’s paying for that, Goober…

Agree. bought two half tons new in mid ’00s, one 16k cash other 25k cash. Bought a new car ‘022 60k cash….OUCH THAT HURT

But I need to get to work and there is no public transportation?

The USofA is tough to negotiate on foot in most of it.

A more reasonable statement would be, “If you can’t afford a 20-30% down payment, then you can’t afford the car.”

Would love to see loan risk-based delinquencies intersect with a unemployment-based delinquencies.

That will make for a good time to buy a car.

You may have been able to write that big supped up truck with accelerated depreciation off your Small Business federal taxes but it sure does not cover the note in a down home improvement market.

More losses to come!

Wolf can you give us the same numbers on motorcycles, boats under 40 feet and RV’s. The toy market over the last few years has been huge.

Better advice (for most people) would be – do not buy a car. If you must (for work or whatever) – lease Honda Accord.

$8k car? So…. hop on a unicorn or into a time machine then. Got it.

I can buy cars all day long with 100 – 150K left in them for $8K.

I was given some good advice by an old car salesman when I bought my first used car in 1978, a 1976 Camaro. He said pay the car off as quickly as you can and then keep it and save the payments until you have enough to pay cash for your next car. I followed his advice and have not borrowed to buy a car since. However, it was an 18 month loan, which is hard to do today.

Treasury yields are rising again, but bouncing around like a ping pong ball on the old children’s TV show “Captain Kangaroo.”

I got a new Ford Escort SE in January 2022 for not much more than the subprime used car loan prices listed above. Subprime borrowers got punished for having bad credit ratings.

The FRED – Housing Inventory: Active Listing Count in the United States (ACTLISCOUUS) has been declining since October. Not sure how accurate the Federal Reserve Economic Data series is.

An Escort in 2022?

David Hall,

“I got a new Ford Escort SE in January 2022 …”

Wait a minute. Ford doesn’t sell Escorts in the US anymore — hasn’t in years. It sells Escorts in China. Maybe you meant “Escape”?

I looked it up. Wow. Ford sells this $11K-car for $33K.

Interesting, all of these are not surprising especially since Lucky Lopez has been highlighting the potential blow back since middle of last year, as I say in housing, still a long way to go for any meaningful reduction in car prices both used and new…still seeing plenty of aspirational asking price out there.

– I am surprised to see that the % of autoloans delinquencies in 2016, 2017, 2018 and 2019 were higher that in the years 2008 & 2009.

Bad deals are made in good times. As I explained in the article. Risk taking took off under the Fed’s interest-rate repression and QE across all asset classes, including subprime auto lending. And a little later, the delinquencies take off.

Hi Wolf, you weren’t explicit about this in the article (that I read twice to make sure) but when you talk about the risk taking that the subprime lenders are taking do you mean that they are loaning to people with even worse credit scores than before or that they are giving them larger loans than before? Probably a combination of both of those but what are some other risk taking?

The loans are bigger because the vehicles are more expensive. So that adds leverage. But the risk-taking in underwriting is essentially extending a loan to a borrower that you think has a good chance of defaulting on it sooner or later for a variety of reasons, such as insufficient income to cover living expenses and the loan, or worse, unverified income.

The thing is: if you extend 100 loans at 20%, and 90 of them make it through the first year without delinquencies, you’re getting rich.

I would also add that when the car prices went up, to allow for affordability, the standard 5 yr loan got extended closer to 6 yrs. Separately, I remember seeing a Cox report detailing the competitive landscape for auto loans. It seems that credit unions were entering the market and providing more supply.

Wolf: yeah but what’s the chance that 90/100 would pay through the first year?

“not having to make rent payments because of the eviction bans”

This is so wrong at so many different levels. So easy for governments (state and local) to be generous with someone else’s money.

This is one reason we don’t want a crash. This program and All others would restart in a giffy.

> for governments (state and local) to be generous with someone else’s money.

Per the US Constitution, state (including local) governments cannot impair the obligation of contracts. And government taking private property (cash flows?) should pay just compensation. I haven’t followed the legal challenges on this, but a common-sense interpretation seems to support some restraint on government here. Maybe this version of the Supreme Court might be receptive to such arguments, and they do seem receptive to reconsidering precedent.

Oh don’t I know it. Had a tenant in Los Angeles not pay rent for 2.5 years on a house in Silverlake (multi-million dollar street.) Rent was $3,295. She rented it out on AirBnB made $165k over the years. Got full unemployment (including Fed $600 bump.) Got Medi-Cal, Food Stamps. Applied to the state Rent Assistance program with a W-2 that showed she made $92k in salary in 2020. State denied her claim she filed another one listing four occupants to get in under the $94k threshold for 4 occupants. She had a custom built house constructed in Texas – completed and purchased January 2022 with $140k cash down. She filed complaints with every agency in California – including a sexual harassment claim against me. Had to have my lawyer defend me against that (In Calirornia guilty til proven innocent.):Finally got her out because she was hiring people from Task Rabbit to do work on the 100 year old wiring and filled the basement with trash. Got the agreement to move without relinquishing my right to past rent. State gave her a free attorney. I had to go to small claims court for money judgement instead of eviction judge being able to award it. Got a $57k judgement. Suing for the balance. Trying to put a lien on her Texas house but Texans don’t much cotton to Californians. As we speak the rental moratorium is still in place in Los Angeles, set to expire thia month. 3 years free rent.

Wolf, I love your column but every time you toss off “no rent due to eviction moratoriums” I want you to think of us on the other side of that trade who got hurt badly. I’m out $140k and that woman put me through red tape hell. I know an older woman down the street got screwed out of $80k lost rent and legal. She has vowed to never rent that apartment again. The risks are too high.

As an aside one rent controlled tenant has two units for $700 each in the same four-plex as she-devil. He uses one for a drum studio. I offered them $40K in 2003 to move and to help buy a house. (Relocation payments were still legal in Los Angeles then if you did $10k of permitted rehab work. I had financing lined up – the spouse is a teacher so she could get a reduced interest rate. They only had to show $500 in the bank. Husband has been renting the units since 1974 -he nce told another tenant “David acts like he owns this place.” She said “Well, he does.” Anyhow, they didn’t take the deal. 20 years later I’m tired and the wife regrets not taking the deal. “Yeah, it’s too bad. Houses were cheap then and by now you would own it,” is all I can say.

I paid another tenant -different property -: to move – got them financing. They bought a house in 2002 for $199K and they bought another 10 years later.

With rent control, and me being childless with no children to move into my properties I can only pay tenants to move.

The guy who didn’t move is now 74, bad heart. I’m going to sell. Told him I will be selling. His response was “So we’ll be negotiating with the new owner?” I said “If you’re stupid you will. They will file a demolition permit, give you 90 days notice and $20K. They will tear down these three houses (one’s a duplex) and build 10 units that will not be under rent control.” As a business man I tried to make everyone a winner. He was afraid I might make some money. I – on the other hand -was hoping we BOTH would.

I hate Black Rock but guess who I’m selling to. Little guys can’t make it in this environment.

Also, SCOTUS and the California courts both refused an appeal by the Apartment Association of Greater Los Angeles on the unlawful takings clause and the interference in contract objection. Shocking but true. California Court ruled against Geoff Palmer vs City Of Los Angeles that he as a landlord could not prove a loss since the tenants are contractually bound to pay him past rent. In February 2024 when all “past rent” is due to be paid in full – and it won’be since there were no penalties for fraud – I am hoping we all sue the City and State and Federal Government for Actual, realized losses.

As a tenant all you had to declare was that you were affected by COVID. Well, who wasn’t. No needs tests were invoked, ever.

Anyone who thinks rentals are easy has not owned one long enough to make an intelligent assessment. Sooner or later, every landlord gets a nightmare tenant no matter how careful they screen them. I am not saying it is not worth doing, but like any other business venture, it is a gamble, and if you are too leveraged and get a nightmare tenant, things can go sideways in a bad way.

I’m not a fan of greedy landlords, because property owners have been making a killing, but I have to say that you should be able to evict a tenant if they dont pay within say 3 months. The process should be fast and painless.

It would actually help to keep rents down if these freeloaders were evicted and people who were actually going to pay were allowed to move in.

Rent control is good for the renter who got in, but bad for the overall prices in the market as it reduces inventory.

Nearly every form of socialism goes awry.

But I think we need some laws to stop the private equity funds from gobbling up properties and renting them out.

I’m sure it varies state by state. But always go through proper eviction process channels. When I used to own rental property, I have put lien on one of the delinquent tenants (and she was acting smug about it to throw salt on the wound).

Years later, I have received a phone call from her lawyer trying to settle with me for the money owned (probably 3 years later or so at this point). I said no, she needs to pay full amount and not a penny less. Turns out she have received some inheritance and could not collect on it without paying off all delinquent debts first.

DVC,

You demonstrated that at the end of the day, justice is only for some people.

Sorry to hear your sad tale.

So you tried to make someone who was better at “the housing business” than you buy a house for you and she totally outwitted you? Nothing worse than an economic and legally savvy poor person, eh?

Maybe you should try another line of “work”?

I nominate NBay for worst post of the year.

That’s a lot of words to say something very simple: don’t be a landlord in California. I love living here but if i were to rent out properties I’d do it in a much less tenant friendly state. Like anywhere in the southeast. Tennessee is especially hostile to tenants rights

Quite a story!

No wonder the American housing market is dead in the water.

“If you have to take out a loan to buy a car, don’t buy a $28k car. Buy a $8k car instead, and don’t spend $5,000 on rims.”

-Maybe we should have same sentiment when it comes to housing and affordability. Cash only upfront cost cut out state, local, and federal taxes for those who earn less than $500k. I seen and heard so much bullshit from all the guru’s of finance. At the end of the day America has gotten morally corrupt and socially irresponsible, At the highest levels of government. Elitism and classism, rich or poor, there is no middle ground for anyone looking for fairness, opportunity capitalism, Ponzi schemes, and the US govt protecting Wall Street and the big banking institutions while they wage economic warfare on up and coming generations. When the least among us can’t afford housing, college, automobiles, having kids raising a family, something has gone totally wrong and dysfunctional. There will be many more giving and dying in the woods in silence. It’s hard to continue to participate in a game that keeps you on the bottom.

Most industries are now monopolies. Thus you have a few executives which is 1% of the company making 10x to 100x of their employees.

That also translates into the economy where the 1% earn and gather much of the wealth. Easy to see. The mom an pop stores are almost all gone.

You can thank Walmart.

It used to be that the Republicans were the party of greed and wealth. Now the Democrats have fully joined the Republicans in supporting the wealthy. The only difference is that the Democrats want to borrow even more money and spend it on social programs, without raising taxes to pay for it.

game – I think the ‘old’ Republican label for the Democrats was: “tax and spend”. As the Republicans have been focused only on tax reductions for some time, now (after all, wasn’t it Dick Cheney who uttered long ago: “deficits don’t matter”?), it seems a bit disingenuous to slag the Dems for actually joining the Reps regarding the view of taxes…

TANSTAAFL.

may we all find a better day.

Agree. My debt aversion could probably be classed a mental illness and I know it hurt the family to live in the woods with no heat or water. But heck they’re still with me and it got better. But now it is worse, hope everyone can tough it out.

Yeah, it takes my breath away thinking about how GDP per capita has only gone up about 25% since the year 2000…but housing prices have gone up 200% since then. Some places like Seattle are still twice as high as their 2007 peak. All based on borrowed money packaged into investment products sold to pensions and insurance and so forth. Everyone says it can’t happen again but what if it can? And what if it’s worse?

And here we are at the dotted line

Just call me a stooge but I gotta sign

I only have to fork over twelve plus nine

But I’m not your dog I got a credit line

And I just wanna buy your car

And I just wanna buy your car

And I just wanna buy your car

So, Come on!

Never until today, had I read a such a befitting parody of The Stooges, that I could virtually hear it.

Well done, BuySome!

Kind of off topic but the WSJ had a great article on swimming in the bay wet suit free!

Wolfs exercise of choice.

https://www.wsj.com/articles/san-francisco-bay-swimming-wetsuits-11674487104

My youngest daughter sailed in the Laser NA at the SF YC in July of 2008. It was pretty cold for us SF sailors and beach goers. The coldest our water gets in the winter is a brisk 74.

Just thinking about the swim gives me the chills.

I hope everyone can read the link. Enjoy!

Looks like we are headed towards a blow off top while the fundamentals continue to erode. Enjoy the ride up but then look out below!

Another short squeeze. Blow off top would be nice. I’m starting to buy puts again.

$100,000 plus for a new HD truck, based on an article I read today. I have a hard time seeing how your normal joe can afford something like that, yet they manage to do it all day long, everyday.

Those trucks are NOT for normal Joes. Those are high-end models in the Ford truck line-up:

https://wolfstreet.com/2022/12/05/1768-a-month-with-10407-down-5-apr-on-a-ford-pickup-update-on-q3-new-vehicle-finance/

Most pickup trucks I see, never seen any real load on the truck’s bed.

WHO ARE THESE PEOPLE? I want a weekend warrior special, but under the optimistic assumption that I could even find one near MSRP… an ENTRY level Maverick would finance at ~$98/wk… PER WEEK, for what I’m pretty sure is the cheapest new truck available.

Lowes offers next day delivery for $80, and the local nursery is $60… When that doesn’t work, you’d be surprised how much I can ratchet strap to the top of a 12y/o Camry… It’s cool, I’m a professional, HD trained me 20+ years ago to push shopping carts and overload passenger vehicles back when every location still had free plastic twine and a box cutters out front.

My household does well, our largest expense category is child care, followed closely by housing, food maybe 1/3 lower, and then everything else… I know where we place on the income spectrum, and I know what’s left over at the end of the month, and I know that at least half the shiny pageant trucks I pass in the commuter lot were bought on leverage at the expense of retirement savings… It makes me sad, and worried for our nations future.

I bought a ‘23 1-ton HD truck recently. Very well equipped. $57k. I don’t know why anyone would pay $100k.

” Prime auto loans are a low risk, low yield business.”

I remember when if you didn’t have credit, you couldn’t get any loan. Now it’s the business of the banks to pour out credit cards, payday loans and subprime.

Note: watch out for the ‘no-interest if you payoff in time’- loans. They’re finding new ways to trap you. I can’t believe our politicians allow this, but then again, I can.

Wolf

Slightly off topic but what happened with all the deferrals of rents , credit payments etc that were implemented to help people get through covid ? I thought those deferrals would come back to bite post covid , but don’t see any commentary around this issue . Thanks

A landlord “David Van Chaney” just commented on this based on his experience in Los Angeles, where those eviction controls are still in place and have just been extended. His comment is above somewhere. Very interesting.

I said back then that there won’t be a wave of evictions, that this was bunch of hoopla designed to push the government into giving out more free money, and there wasn’t that eviction wave, because people got huge amounts of money, and the job market recovered and wages rose.

Wolf-Quick question that probably has an obvious answer. What is the cause of the saw-tooth pattern in the Fitch delinquency chart in the article?

Seasons, LOL. Same with bankruptcies. There are seasons for everything.

I can kind of see why, for delinquencies, there is a seasonal high in January/February, after the holiday spending binge. But I don’t know why delinquencies bounce off in ca. May to mark the low of the year. But that’s how it works.

In Jan 2023 I bought a car at Manheim Dallas from American Credit acceptance.

It turns out American Credit Acceptance clears engine codes

before the sale to hide issues like low compression. Buying a car from them will cost me thousands and Manheim was unwilling to solve the issue.

Avoid this seller at all costs.

You have not understood how an ABS works or what the whole point of it is. I recommend you watch the “pitch” scene from “The Big Short” (the one with the Jenga Tower) which explains it. Additonally, you might consider this quote from the “Senior partners emergency meeting” in “Margin Call”:

“These combine several tranches of different ratings classifications in one tradable Security “., The Point being: “One tradable security”. “Investors” buy that “one tradable security”, not “tranches”. The whole point of an ABS is to put so much garbage together in one pile, it looks like a diamond. That’s why they need people with a degree in higher grade physics (like in “Margin call”) to price them right, because all the risk curves of the different “tranches” need to be thrown together to come up with the price for the “one security”.

Your statement is not correct. Instead of getting your info from movies, read this about ABS. It’s a decent basic explanation:

https://www.investopedia.com/terms/a/asset-backedsecurity.asp

This text is incorrect. It states that “Company X” packages their loans and then sells this package to “Investment Firm X”. This is not how it works. “Company X” (in the case of cars: a car dealer) does not package anything. That is absurd. The car dealer makes the loan and sells it to a “financial services” company -maybe a bank, maybe some other Outfit. This company then packages the different loans / tranches into the one tradable security – the ABS – which is then sold in the market to whoever, maybe to “Investment Company X”.

Yoi should know that “The Big Short” was supervised by a certain Michael Burry. Yeah, that guy.

The car dealer doesn’t finance anything. A car dealer sells the car and arranges financing with an auto lender. The auto lender finances the vehicle and then either sells the loan to a company that securitizes it, or if the lender is big, securitizes the loan itself = “Company X.”

ABS paper is tranche from lender, bank, CU etc….not from the dealer…Heck I don’t even think Lithia has its own bank.

Most dealers fund thru their own captive lender….

Toyota Financial might sell some tranches

…and all this time I was trying to figure out what the heck this had to do with antilock braking…

may we all find a better day.

Mispriced risk is about to provide example of what happens with mispriced risk….1.5 years from now used cars going to be cheap via cash