Worst delinquency rates this century.

Auto loans to customers with subprime credit ratings – FICO scores below 620 – are risky affairs. But during good times and endless cheap money, the high interest rates that can be extracted from car buyers who think they have no other options are just too tempting. Now the losses are coming home to roost.

Big banks have become relatively conservative in this category and are sticklers for things like income verification and other details, which has made room for specialty lenders with fewer such compunctions.

There are scores of these smaller specialized subprime auto lenders, some of them backed by private equity firms. And three of them – Summit Financial Corp, Spring Tree Lending, and Pelican Auto Finance – have now collapsed into bankruptcy or were shut down. Allegations of fraud and misrepresentations are swirling through the bankruptcy filings.

These lenders generally borrow from big banks to fund auto loans to subprime customers. The difference between the rates big banks charge those lenders and the rates those lenders obtain from their subprime customers (often in the double digits) is their margin.

These specialized lenders can also package their subprime auto loans into structured asset backed securities (ABS), which are then sold in slices to investors. Each slice is rated separately, with the highest rated slice of an issue often carrying an “AA” or even “AAA” rating. Issuers often retain the riskiest slices that take the first loss. That math works well – until it doesn’t.

And it doesn’t when customers, buckling under these double-digit interest rates and too much car, start defaulting in massive numbers. Subprime loans started to be a fiasco that we have been covering at least since February 2016. This has been a slow-motion wreck.

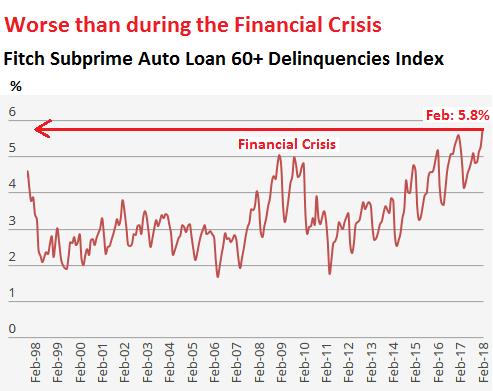

Fitch, which rates these auto-loan ABS, tracks the performance of the underlying subprime auto loans. The index of its 60+ day delinquency rate of subprime auto loans has now risen to 5.8%, up from 5.2% a year ago, and up from 3.8% in February 2014. It’s the highest rate since October 1996, higher even than during the Financial Crisis. Note the strong seasonality:

As bankers say: “Bad deals are made in good times.”

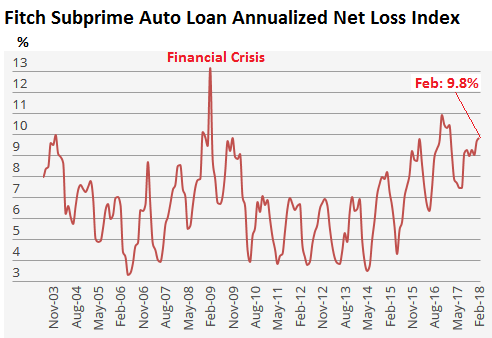

Given the losses in the sector over the past two years, specialized lenders started cutting back. This prevented many subprime customers from buying new vehicles, which was one of the primary reasons why new-vehicle sales in 2017 fell below the total of 2015. This is also why Fitch’s index of subprime auto loan Annualized Net Losses (ANL) peaked in late 2016 and early 2017 and has since backed off just a tad though it remains at financial crisis highs, at 9.8% in February:

And these losses have started to take down the smaller lenders.

Summit Financial Corp, a privately owned company that works with auto dealers in Florida, filed for Chapter 11 bankruptcy on March 23, after it “performed an extensive analysis of alternatives,” its attorney said in a statement. Summit blamed Hurricane Irma.

But Bank of America – which, as Summit’s largest secured creditor, is owed $77 million – alleged in the bankruptcy documents that Summit had repossessed many cars without writing down the bad loans, thus under-reporting the losses. “The move allowed the company to hide operating losses and borrow more money to fund loans, the bank said,” according Bloomberg.

Spring Tree Lending, an Atlanta-based specialized subprime auto lender, is being pushed into bankruptcy by a creditor who filed to force the company into involuntary bankruptcy on March 28. Fraud allegations are swirling.

Pelican Auto Finance, which specialized in “deep subprime” auto loans shut down last month, after private equity firm Flexpoint Ford LLC, decided to cease funding it. “There’s been intense competition. The margins just aren’t there,” Pelican CEO Troy Cavallaro told Bloomberg.

Other PE firms that have together plowed about $3 billion into the subprime auto loan bonanza, based on data cited by Bloomberg, are now licking their wounds, unable to get out. They include:

Perella Weinberg Partners. It acquired Flagship Credit Acceptance in 2010. Flagship then embarked on an aggressive path, and its loan balance surged from $89 million in 2011 to $3 billion in 2017. Then the loans started to curdle. The company is now bleeding. The hopes of an IPO, disclosed in 2015, have fizzled. For now, Perella Weinberg is stuck with a money-losing operation.

Blackstone Group acquired a majority stake in Exeter Finance in 2011, which does business with dealers across the US. Since then, there have been three CEOs. In 2016, the company rebranded itself. Blackstone has put $472 million into it to fund the aggressive expansion. And now the exit doors appear to be closed.

The subprime auto lending business is highly cyclical. For example, according to Bloomberg, citing Moody’s data, 41 subprime lenders filed for bankruptcy during the subprime auto loan bust between 1997 and 1999.

But unlike subprime home mortgages, subprime auto loans won’t take down the financial system. About 25% of the auto loans written are subprime. For new cars, it’s about 20%. Of the $1.11 trillion in total auto loans outstanding at the end of 2017, about $280 billion were subprime – less than a quarter of the $1.3 trillion subprime mortgages before the financial crisis. Even if the total subprime portfolio produced a net loss of 50%, the losses would amount to only about $140 billion.

And there are other differences: Vehicles are quickly repossessed, usually after three months of missed payments. Even in bad times, there is a liquid market for the collateral at auctions around the country, and vehicles can be shipped to auctions with the greatest demand. The results are that lenders don’t end up holding these vehicles and loans on their balance sheet for years, as mortgage lenders did with defaulted home mortgages and homes.

But subprime will take down many more of the specialized lenders. And the survivors will tighten lending standards. This will prevent more car buyers from buying a new vehicles. Many of them will be switched to older used vehicles. Or they hang on to what they have.

So automakers get to grapple with the loss of these customers. When you lose a significant portion of your customers due to credit problems, it hurts. And this is where it adds to “Carmageddon.” Investors and creditors, including PE firms, get to grapple with losses and bankruptcies. But given the limited magnitude of subprime auto loans, and the limited impact on the banks, the Fed will brush it off and continue its monetary tightening, and no one will get bailed out.

Easter fell into March this year, and for auto sales, March lasted till April 2. That’s helped, but it’s not a good sign for April. Read… So What’s Going On with Auto Sales?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

If they’re hiding their losses, then the annualized net loss numbers might be a tad conservative.

Ally Bank (formerly known as GM Financial) has financed $59 billion in car loans. The FDIC in 2015 allowed Ally Bank to make loans on 620 FICO scores. Can’t believe they haven’t taken a big loan loss hits yet. They look like a potential stock short.

https://www.magnifymoney.com/blog/news/fdic-allows-ally-bank-make-620-fico-auto-loans/

Also keeping an eye on Santander Consumer (SC) and Credit Acceptance Corporation (CACC).

And once again in history, no regulations are in place to stop the financial rape. Next up? Another huge mortgage money-grab. Can it get any worse? Yes!

There is plenty of regulation available; it is the enforcement of any of it that doesn’t exist (or is only applied very selectively, like in that Russia that we do love to hate to distract us from those concerns and outcomes that we do control).

Yes, regulation is for the plebs/peons, don’tchaknow … but for Congress & their neolibricon donors, well hey ….. it’s All Good !

I forgot the connection between nerve gas and auto-subprime.

It would be wonderful if honest regulations were actually pursued and passed by “good” people trying to regulate “bad” people. We would do well by ignoring what the supposed good people say. Watching what they do if a little better. Judging the tree by the fruit is best.

If you have NOT figured out yet, “power attracts bad people and corrupt good people”. When people say “give me power and I will do good”, I will just laugh. You might argue that “without power, nobody can do anything”. That is true also. This is at the core of life cycles of any social structure. People seek power first because they want to get things done, then the corruptions creep in and the power the is used to benefit a few ar the cost of the others.

The only question I have out of this auto loan bankruptcy is how they are planning to get into my pocket to let me shoulder the loss.

Well stated. Approx. 75% of people focus on the trees instead of the forest. And about 50% of people rely on emotional reactions, as opposed to rational thinking and logic. Both orientations have obvious pitfalls and the overlap of these 2 groups is a very potent and dangerous force.

This overlap group is easily manipulated and want “protectors”. They have many positive attributes and are top performers in many fields, but are unable to grasp what Plato meant when he explaned that those who talk most about protecting people are usually tyrants in disguise.

Setaros,

It is possible to run into a forest, just as it is possible to run into a tree. The outcome is substantially different.

To your point, ‘. . . no regulations are in place to stop the financial rape . . . ‘

(1) I am not sure who is being “raped” here, since it appears to me that all participants in this stench-filled activity are voluntary participants.

(2) If the losses, ultimately, are only to be borne by these voluntary participants, then who cares what happens; who cares who loses ?

For example, you may think that the auto manufacturers are hapless bystanders to this subprime fiasco and its coming losses. I assure you they are not. The auto manufacturers, AND THEIR CAPTIVE DEALERS, are totally in bed with the subprime lenders.

Given my last sentence about the DEALERS being IN BED with the subprime lenders, I still cannot imagine who is being raped here in any way . . . . .

“The auto manufacturers, AND THEIR CAPTIVE DEALERS” … It’s actually the other way around.

Look no further than the crony capitalism that prevents car manufacturer’s from selling direct to consumers in most states.

It works both ways. The manufacturers have restrictions on what the dealers can do, as well as the Dealer crony capitalism that prevents direct sales to customers.

I did not want to get into a lengthy discussion of DEALER — to Manufacturer — to DEALER covenants or restrictions . . . when my point was this: ALL PARTIES TO THIS SUBPRIME LENDERS FIASCO are VOLUNTARY participants.

NO-ONE is forcing ANYONE to go to ANY DEALER — and buy a car using SUBPRIME financing.

In purely voluntary, non-coercive relationships, like these, there is no party to these subprime transactions who is being raped. Not yet.

Now if I (or you), detached parties to these ridiculous subprime loans, ends up bailing out even ONE SINGLE DOLLAR that these losers accrue — then that is rape, IMO !

The #2 assumption is false. Nobody shoulders consequences themselves any more. The profit is privatized and the loss is socialized. Whether it is through bailout of GSEs or wall street, or through securitization to investors. People start business by borrowing from too big to fails and “venture capitals”, there is NO skin in the game any more. Why? because if there is skin in the game, there will NOT be this many businesses, and no jobs. For FED to create jobs, they not only has to make interest rate low, they have to make sure those job creators do NOT take risk by shifting risk to the public. So who is raped? The public, always,

and the public keeps giving them more power so that the public can get raped less. It sounds strange, but if you realize the public do NOT know how to create job themselves, you would understand why the public do this.

History supports what you say. Look at the last time with the mortgage fiasco as you say !

I truly hope you are wrong — THIS TIME — and the gullible public is finished shouldering private losses.

I have my doubts . . . .

Replace cars with apartment buildings. Then replace shady lenders for shadow bankers. Then add three zeros to the amount of money borrowed and you have the bad debt crisis brewing in China.

Yep but they’ve got a massive manufacturing base to fall back on, and a dictatorship which can plan and execute what it likes without being subject to the vicissitudes of ‘the markets’.

What’s the USA got to fall back on..? Coffee shops, online gambling and tattoo parlors..?

Waiting gleefully for China to implode whilst your own country goes to hell in a handcart is a fool’s errand.

yes but 70% of OUR GDP is consumer spending

* was

I know of a lady who hasn’t been making car payments ever since she lost her job several months ago and is stunned and confused because the lender has not contacted her at all.

The value of the car is well below what she owes. A 60 month auto loan.

Could it be that the lender is playing the same game as Summit by under-reporting losses?

It would probably make sense to write it off rather than repossess and then auction off.

It would probably make sense to write it off rather than repossess and then auction off.

Doesn’t matter what makes sense; what matters is 1) preserve the asset (the debt) 2) setting a an example so that the other dead-beats don’t get no ideas (preserve the wider portfolio of assets).

So It Depends, If the financing agreement is such that repossession of the car clears the debt, they will not repossess immediately, rather they will rack up loads of fees and increase the interest rates to guarantee that the debt is never cleared while blocking the financing of another car (via the credit score) to keep all of that good nice “juice” flowing!

They may try to offer some deal where she “get to keep the car” by assuming personal liability for the (racked-up debt). This is the moment where she signs nothing, hands the keys back immediately and buy another car cash!

If the debt dosen’t clear on a repo, they will do the rack-up first, then perform the repo out of spite, then initiate bankruptcy proceedings to get whatever other assets she may have. Possibly they will sell the debt for about 15-20 cents on the dollar to a collection agency, she may later make a settlement with them since these businesses “get whatever they can and work on the averages” for their profits.

Either way, there will be some form deprivation coming for that lady.

A Ford F150 can fetch upward of $50k these days. WTF?

And an engine light on an otherwise perfectly running, perfectly safe 5 year old $15,000 used Tacoma with 100,000 miles on it can make an owner wish he could render it unto a junkyard. We’re kept enslaved by state ‘safety’ inspections which have increasingly more to do with a computer thumbs up or thumbs down rather than actual safety. Enough yearly abuse and extortion and that $50,000 begins to look appealing, ka-ching!

This is why smart people get a sub-$100 OBD/OBDII reader. A lot of the time, a “check engine” light is due to a poorly sealing gas cap, just wipe the rubber seal clean and you’re good to go. Sometimes it is something serious, either safety-wise or something detrimental to the life of the engine.

I can’t afford to keep a car if someone *gave* me one, but if I ever own a car again, I’ll join AAA because they have a lot of neat services like the famous towing service, but also maps, trip planning, and I believe they’ll read engine codes for you too.

Most car parts places (Autozone, Advance, etc) will read the codes for free.

Hey Wolf -saw this comment on ZeroHedge’s article on subprime auto…

Can they do this ? Just as rigged as every other market ?

“u never will be able to buy for pennies on the dollar. They’ll sit on that inventory just to keep prices inflated.

If they drop prices on inventory just one or two years old then their new model cars will just sit on the lot.

They would probably prefer to market them in 3rd world shitholes at a loss then undermine their ridiculously high priced current models.”

Third world shitholes? You mean like Baltimore?

Many emerging market countries have import bans on vehicles older than a few years to prevent dumping.

Could some lender try to do this? Sure, they can try to do anything. But the best prices for recent-model vehicles are in the US. Auctions are the most liquid places to sell. Used-vehicle prices are currently fairly strong, so there is no reason not so sell here. Exporters buy at these auctions too, and those vehicles might end up south of the border. But if they can get a better price selling the vehicle directly in Mexico, why not?

And the market for nice older used vehicles is very strong in the US. They’re always in demand.

But lenders won’t sit on their repossessed vehicle because, unlike a house, a car just loses value by the day.

The efficiency of the used auto market in the US is amazing, its too bad there isn’t HOUSEFAX, there is some real crap going on in the housing industry, far worse than autos in terms of liabilities and outright fraud and misrepresentation.

And this comment too –

“But you are right, they will just let them sit and rot. ZH has done a couple posts on this, 10’s of thousands of new vehicles, unsold from last model year, sitting in a field somewhere, slowly rotting away, because they make the calculation that it makes more financial sense to do that rather than sell them cheaply and undercut demand for the new (and really expensive) ones.”

Just more of our Bizarro World economics. Everything I learned as a kid growing up that served my parents very well, are now just the nostalgic musings of an old man. Living wisely as my parents did and as I have tried to do most of my life now penalizes, where it once rewarded. Now it seems that auto dealers had rather deal with customers they can finance the vehicle for, even better, stick with a 10 year loan and 3X the going interest rate, than to sell a car to someone who can actually afford to buy.

I got caught in the afternoon rush hour one day last week and it appears that GMC Yukons have been dropping from the sky. Based on the median annual income here, there must be a heck of a lot of leasing going on. And probably a lot of people here are doing that popular payday to payday lifestyle.

Just wait till gasoline spikes due to a dollar crisis or war and those Yukon’s will all be up on cement blocks next to the doublewides collecting dust

Hey, you can live in your car but you can’t drive your house!

NO You can live in your car I certainly Cannot

If one want to survive in the gig-economy, one cannot enter into long-term agreements. Leasing fills the need for having a car for getting to work while not knowing if one can pay for the car next month.

Really ? ” . . . You really mean leasing, because, as you say, “one cannot enter into long-term agreements. Leasing fills the need for having a car for getting to work while not knowing if one can pay for the car next month.?”

Here in the Northeast where I live, leases are for the term on the lease, and cannot be broken without great expense.

I had a neighbor who was intellectually challenged, but living independently, and I tried to help her break a lease that a fast talking salesperson inflicted upon her.

In a word: UNBREAKABLE.

If you meant “renting short term”, that would fill the sense of what you said, but at a pretty stiff cost.

If you meant “renting short term”, that would fill the sense of what you said, but at a pretty stiff cost.

Yes, thats what I mean. It is called a “mini-lease” here.

The prices are not that bad from our local perspective – 2000 DKK, or about 350 USD per month, inclusive of all service and insurance, this monthly amount is kinda the minimum of what it always cost to have a car here, regardless of what one does to escape reality (If one does not have the luxury of free access to a mechanics workshop, that is).

Most big trucks I see never look like they’ve ever been on a construction site or carried a bale of hay. So I just assume the owner has self-esteem issues. And sadly, not only do they have self-esteem issues, they also seek to resolve those issues in just about the most expensive way possible.

My step father is a good example. He has two F150s, an AR-15 and doesn’t have a pot to piss in.

If he’s mentally iffy, it’s probably good he doesn’t have a pot to piss in, Kent. he might shoot a hole in it with the AR-15 and them there’d be mold problems under the bed …

The weirdest thing of all is we’re supposed to;

i) spend like mad to generate economic growth BUT:

ii) save for our old age.

All against a backdrop of pitiful interest rates and hence without the facility of compound interest.

All because the financial specualtors that rule the roost demand their cheap gambling money, forcing nation states to play ball (and of course blaming the latter for everything) or they’ll crash the stockmarkets.

No wonder people feel bewildered and betrayed,

“Contradictions of Crapatalism” by: I Spend Freely and In Debt Forever.

“How to feel utterly craptastic in an ever-increasingly crapificated world” …. by Eye M. Screwed

Quote : “No wonder people feel bewildered and betrayed,”

Your final point is a good one – – – EXCEPT – – – for people who are born inveterate savers.

I am one, and I also know more than a few. They are quiet people, many of them, not prone to boasting, and always prepare themselves against an uncertain future.

Which — by the way — is what all futures are.

I feel bad that the USA government is going to punish the savers (at some future point) to pay for the profligacy of the $50,000 +++ F-150 drivers. I never made such a foolish purchase, and I have no sympathy for those who have done so.

And I am surely not going to pay for their profligate lifestyle — when some government program is designed to even the outcomes — between profligate spenders and inveterate savers.

I don’t understand how they can “tranche up” that “ABS” sh*t into AAA just like they did with the CDOs. The “maths” didn’t work then and it never has. I presume that these idiot “quants” are _also_ saying that the price of cars never goes down just like they said with housing? I don’t know why anyone takes the drivel coming out of the ratings agencies seriously any more. The “brown paper bags” are still flowing into these agencies except it’s for a different three letter acronym this time. Given the modus operandi, I wonder what is the next thing after this latest little scam blows up. It is good though that some PE firms have taken a haircut, so maybe there is some justice this time around.

The lower-rated tranches take the first losses. So if losses are not huge, the higher-rated tranches might perform well, despite losses at the BB or lower-rated tranches. That’s what the math is based on. Once losses get much higher than expected, higher-rated tranches take losses too.

I don’t understand how they can “tranche up” that “ABS” sh*t into AAA just like they did with the CDOs

It’s not “just” – there is a hefty fee involved; one would imagine that the worse the securities, the higher the fee needed to get the ‘AAA’ rating ….

A credit rating is “Free Speech” after all, it’s not like anyone can later come back and sue Moodys et. al. over their losses and it’s not like anyone cares: Da Rulez Sez one buys ‘AAA’ for them pensioners and widowers, so one follows The Rules and Due Diligence is Achieved.

If those ‘AAA”s yielding 5%-10% above base maybe are not exactly what it says on the tin, it is just another sad accident that ‘The Market’ surely will correct real soon now.

They get the AAA rating on some tranches by issuing them in small durations. They could have 30 day, 60 day, 3 month or 6 month tranches. The likelihood these will be paid is high, so now they have 4 AAA rated tranches, which impacts the rest of the ratings. Yes, they do it on purpose to generate a better overall rating.

Who could’ve imagined that lending huge sums of money to those who have already demonstrated their inability or disinclination to honor their financial obligations could ever end badly.

Moral hazard, another beneficent gift from the Fed to our foundations-of-sand financial system.

/sarc

I have a dumb question.

When a lender repossess a car what’s the average he recovers by auctioning it off?

I’ve been to a few repossessed goods auctions and usually cars, vans and motorcycles are the stuff in worst conditions you see on the auctioning block. Most of it is usually only good as spare hulks or scrap metal, meaning prices have to fall a long (sometimes very long) way to find a buyer.

I have no doubt these subprime lenders repossess many vehicles in good conditions, but these have to compete in a brutal market, which includes huge numbers of ex-lease vehicles in good shape and often with acceptable mileages at good prices, not to mention enormous numbers of “last year models” dealerships struggle to get rid of: just last week I was passing in front of an FCA dealership and they had a semi from a well known breaker loading up still new, never registered FIAT 500’s and Jeep Cherokee’s. Those cars are going to be stripped of anything that can be sold as spares and the rest pressed and sold as scrap metal.

I often get in the email corporate offers for similar vehicles and the discounts are insane, often bringing the price in line with used vehicles…

20% of new vehicle loans are to subprime customers. These vehicles come with high payments that customers might have trouble with. These vehicles may be one or two years old when repossessed and are generally in good shape.

However, at the low end, there’s all kinds of stuff getting repossessed that was in bad shape when it was sold to the subprime customer in the first place (cheap), and may have developed mechanical problems that the customers didn’t have the money to fix, so they stopped making payments. Those vehicles can be beaters that are taken through the auction on the hook.

Thanks for the reply.

I’ve seen those “beaters”, but most looked like the automotive equivalent of a house whose copper wire had been ripped off the walls just before an eviction… ;-)

I’ve been to some sawmill bankruptcy auctions looking to buy lumber and/or equipment.

They’re rigged as well. The last one, eons ago, was auctioning off lifts of lumber. As I was waiting for the price to continue dropping the auctioneer simply said, “Okay, we’re done with this…I have a large buyer who will take the whole supply. Next”.

I had to make a stink to get what I was looking for, and did very well, but was lucky to get anything that day. I assume the auction company, itself, would have bought up the lumber and resold it later.

I would bet the best cars/trucks have a rigged place to land and that transport is idling just over the hill to wait for the auctioning formality to ‘go away’. Inside wins every time, clever outsiders are part of the profits.

I experienced a set up auction in 1992 on a 17 acre parcel in bankruptcy in Sag Harbor NY I only won in the end by my perseverience and refusal to accept what they were trying to pull The attorney for the bankruptcy was in the Wall Street area of Manhattan

How did you convince the auctioner/attorney to sell to you?

It’s a long story but they initially canceled my high bid in favor or a friend of theirs An attorney for the creditors contacted me and asked me if I would be willing to pay more Six months later he called me to inform me that he had gone to court and gotten the whole deal canceled and it was rebid By then I had secured a couple of partners with deep pockets The Rest is as they say history I wasn’t a member of their “ club” but I was not about to be cheated

In his first few paragraphs Wolf points out a more serious problem than carmaggedon: “Big banks have become relatively conservative in this category..” and so are making fewer subprime loans. So specialized subprime lenders are doing most of the subprime business. But, “These lenders generally borrow from big banks to fund auto loans to subprime customers”. So the banks are lending to the subprime lenders who are lending to the subprime borrowers. And the banks are getting a lower interest rate than if they lent to the subprime borrowers directly.

Does anyone see the problem here?

I bet these guys also own a lot of shares of Longfin.

There are a lot of signs indicating that we are at the top of the business cycle. Add this to the basket.

This begin to fray first at the edges. Eventually the rot works its way to the center. I woudln’t be surprised if we see an actual recession start sometime in 2Q to the end of 2019.

In our area of flyover country 2/3 live paycheck to paycheck. Typically a family of 3 might take home $2,000.00 per month. $400.00 goes to the subprime car note, $200.00 to insurance and $200.00 to gas and maintenance. $800.00 goes to rent. That leaves $400.00 for everything else including utilities, food, clothing, etc. Obviously those numbers do not work! So the debtors borrow from predatory lenders and payday loans to make ends meet, which only makes things worse. Tax refunds help but those are spent on necessities in short order. The fact is the working poor can’t afford cars but they can’t get to their low paying jobs without them.

Honestly I don’t believe the default rates for the subprime lenders. It is only a matter of time before they blow up unless they are subsidized by the Fed. The working poor would be better off with the old used car lots, than walking out of dealerships with $30,000.00 debts they can’t possibly pay.

Agnostic,

It is a curious fact that the poor, who cannot afford to maintain/repair an older vehicle must buy new. With a new car comes a bumper to bumper guarantee.

Defaults rise based on season? Can’t compete with Christmas spending?

I was floored when reading the latest Consumer Reports, which quotes the price of a Lincoln Navigator at $86,000 and a Ford Expedition at $75,000. Each of these rigs gets only 15-16 mpg. Who really needs that?

I wonder if they are selling these to subprime borrowers.

Was a time a person could buy one with a push button radio, rubber floors, naugahyde bench seats and use it to tow a large trailer around and move workers to and from a job site. We’ve completely lost our way with this perversion.

In 1963or ’64 my mom bought a well equipped NEW Ford Fairlane 2dr hardtop for $2500 out the door.

The people that worked in the rubber shops (Goodyear, Firestone etc) took home a net $85 to $100 a week.

That NEW car cost them about 1/2 of their yearly NET take home pay.

Todays NET take home pay for the average worker is (according to the gummerment) is $36,564. A NICE NEW car costs much more than 1/2 of the average net pay of $18,000 today. The current avg price of a car is $33,560.

Any wonder why new car sales are taking a dump???

Jim,

When I got my first decent paying job in 1968…Approx. $1000 per month, I could walk down to the Jaguar dealer and buy a brand new XKE for six months’ salary.

Instead, I bought a used one, a 1964 model for two grand.

*And it doesn’t when customers, buckling under these double-digit interest rates and too much car,*

What did you wanted to say? Too many cars? Too expensive cars?

Anyway,

“Too much car” is industry jargon for a car that is too expensive for the buyer.

Sorry for using jargon. It just slipped in.

Sadly your logic may be correct.

Look at the number of people who have 6, 7, or even 8 year car loans.

https://www.edmunds.com/car-news/auto-industry/auto-loan-lengths-soar-to-record-high-edmunds-finds.html

That’s about 6 years. The folks who are going for long car loan.

Meanwhile downpayments are also up.

https://www.edmunds.com/car-news/auto-industry/average-new-car-down-payments-near-a-record-high-edmunds-finds.html

I’d say that if we consider that both downpayments getting bigger and car loans getting longer, that’s a big indication that people are getting more car than they can afford.

The hard question: What happens when these cars start to need expensive repairs? Higher priced cars mean not just a big purchase price. They need more expensive repairs and depreciate harder when it comes time to sell/trade in.

I think that the fundamental truth is that wages have not kept up. I’m not talking about just cars. Let’s look at necessities here:

– Price of rent/new homes

– Food price

– Price of insurance (at least for Americans anyways)

– Price of “needs” (as opposed to wants)

Wages are too low.

Does subprime lending apply to outright purchases or leases as well? The secret to the auto business is having a vehicle ready for you wherever you are. So you lease a personal car, rent another car when you travel, a different car when you need to carry a number of people, a truck when you move. You own (like a timeshare) a number of vehicles. The auto company sells you many different cars. However when the economy slows there is no glut of inventory sitting on the lot, its all out there somewhere so the problem isn’t so much that narrow band of users who are delinquent on the payments to their personal car, its the whole car-chilada.

Having worked in the auto industry, you realise what a boom-bust industry it is. We’ve had the boom of China, the industry is now due for a slowdown-correction.

per the bloomberg article : “The weakness is making it more expensive for some subprime auto lenders to package loans into bonds, though none of the companies that recently closed or filed for bankruptcy have issued such securities.”. Looks like these companies held the paper . Ouch

Student loan subprime quagmire been pretty quiet. Friend I have moved to England 6 years ago and has made no payments. Got to be a lot of negative amortization with relaxed terms such as only paying 10% of one’s discretionary income . Surely this ugly head is rising soon again.

I’ve always thought that It would blow up sooner or later but the reason it cant is because its non dischargeable debt. In other words it never goes away even if you file for bankruptcy.

Of course you cant get blood from a stone and absent a cosigner( and after garnished SS payments later in life) the loan dies with the debtor.

Leaving the country will accomplish this as well.

The high-powered advertising of consumer credit should be banned. I’m not a believer in too many laws, but that is one which I would support. Most people do not have the ability to make money by borrowing money – certainly not by buying a car with money borrowed from the very same car company!