Money-printing hits home. Charts by retailer category.

By Wolf Richter for WOLF STREET:

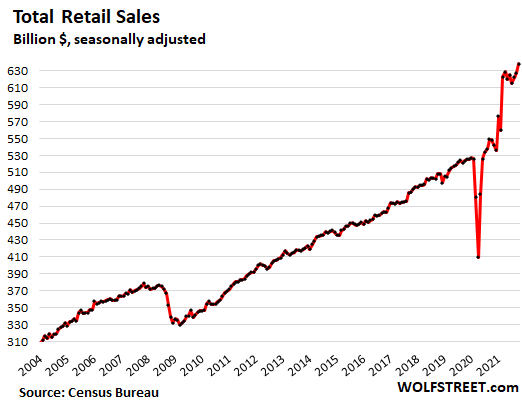

Total retail sales jumped by 1.7% in October from September, by 16.3% from October a year ago, and by 22% from October 2019, to a record $638 billion (seasonally adjusted), according to the Census Bureau today, blowing by the mind-blowing free-money-blow-off-spike in March and April, driven by equally mind-blowing inflation:

Fired up by $4.5 trillion in Federal Reserve money printing and by $5.7 trillion in federal government deficit spending since March 2020, over $10 trillion in total monetary and fiscal stimulus in just 20 months, including hundreds of billions of dollars in free money handed directly to states, businesses, and consumers, and trillions of dollars handed to the markets, leading to a monstrously overstimulated economy and to even more monstrously overstimulated markets, well – you guessed it but the Fed refuses to guess it – demand for goods of all kinds has spiked in a historic manner, as you can see in the charts below.

No supply chain or transportation system was, or could ever be, ready for this artificially stimulated historic spike in demand, triggering widespread shortages, along with a sudden and radical change in the inflationary mindset of consumers and businesses, and massive price increases that keep rippling through the economy and are now intensifying further up in the pricing pipeline, where price spikes have reached 20%, and they’re getting passed on.

These mind-blowing price increases are inflating retail sales. Four retailer categories account for 52% of total retail sales here: auto dealers, food & beverage stores, restaurants, and gas stations. And prices there have surged, as tracked by the Consumer Price Index, compared to a year ago:

- Used vehicle prices: +26%

- New vehicle prices: +10%

- Food prices at stores: +5.4%

- Restaurant Prices: +5.3%

- Gasoline prices: +50%

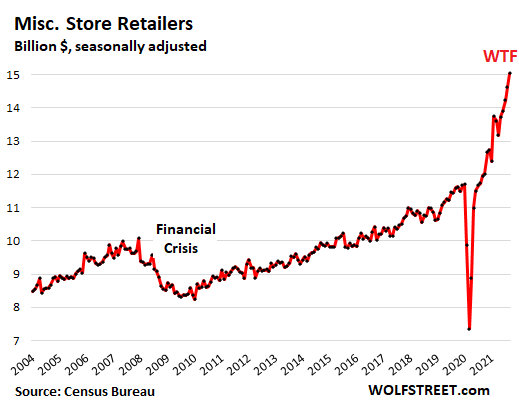

For your amusement, miscellaneous store retailers first, where sales are spiking in the most peculiar manner. These are specialty stores such as beer brewing supply stores, telescope stores, arts supply stores, etc. Sales are spiking because those retailers also include cannabis stores, and that trade, once hidden, has come to the corner store, and is being counted and taxed.

Sales in October spiked 2.8% from September, by 26% year-over-year and by 30% from October 2019, to $15 billion (seasonally adjusted):

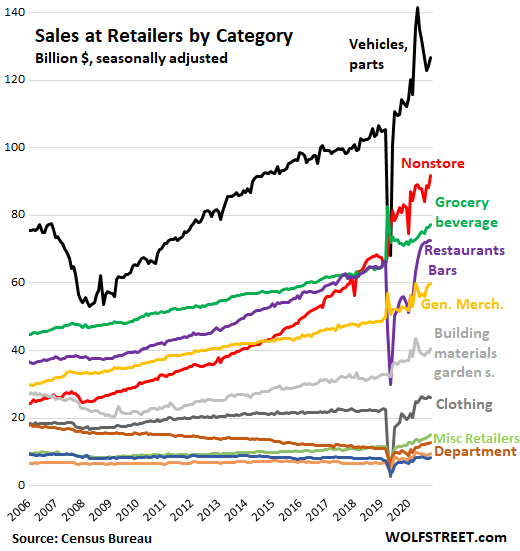

Magnitude by retailer categories. In the overall scheme, these miscellaneous store retailers with the booming cannabis trade are small fry, the green line at the bottom in the chart below. Auto dealers and parts stores are by far the largest retail segment (black line). Nonstore retailers – mostly ecommerce – have become the second largest retail category (red line), followed by grocery & beverage stores (green), restaurants and bars (purple), general merchandise stores (yellow), building material and garden supply stores (gray), and all the rest:

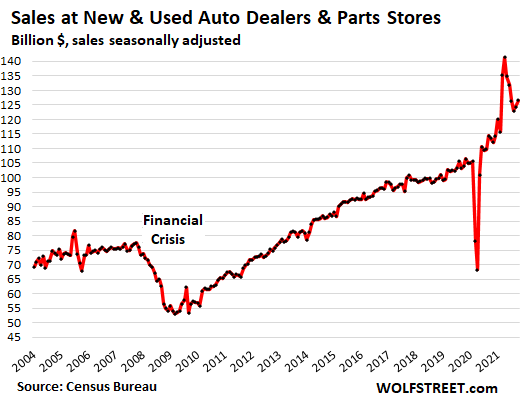

New & used auto dealers and parts stores: Sales rose 1.8% in October from September, to $127 billion (seasonally adjusted), the second month in a row of increases, after months of large declines from the free-money-blow-off spike in March and April. This was still up 11% from a year ago and 22% from two years ago:

Massive price increases and a shift to higher-end models covered up the plunge in unit sales. The above sales are measured in dollars. Auto dealers, the largest category in retail, move the needle.

The average transaction price per new vehicle sold in October soared to $44,000, up 19% in just nine months, a result of higher prices and of the shift to higher-end models, as auto dealers and automakers are making record per-unit gross profits:

![]()

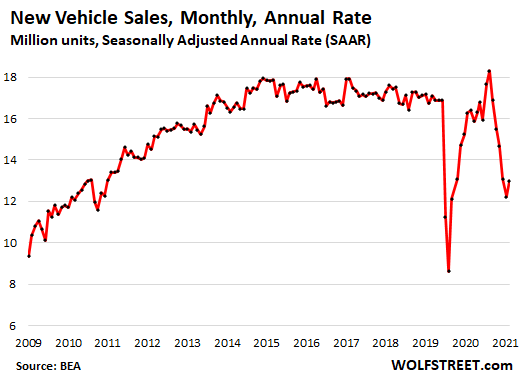

But the number of new vehicles delivered has plunged in recent months to the lowest Seasonally Adjusted Annual Rate (SAAR) since 2011 because dealers have run out of inventory to sell, as automakers are running out of certain types of semiconductors and cannot produce enough vehicles, and are now prioritizing their higher-end models:

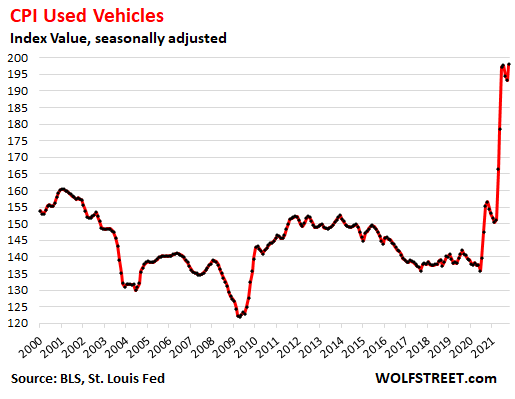

In terms of used vehicles, the seasonally adjusted annual rate of sales in October fell 7% year-over-year to a rate of 19.6 million used vehicles, while wholesale prices spiked by 38% from the already sky-high prices a year ago.

Retail prices of used vehicles are following wholesale prices with a lag of a month or two. The CPI for used cars and trucks, up 26% year-over-year, is now getting ready to re-spike in line with wholesale prices in the prior two months:

The inflationary mindset has radically changed. Price spikes like these would normally have entailed a collapse in demand, which would have prevented prices to spike like this in the first place.

Vehicles are the ultimate discretionary product. Most potential buyers can easily wait a year or two and drive what they already have. And they did this during the Great Recession. But now they’re jostling for position to pay over sticker for new vehicles and to pay ridiculous prices for used vehicles.

This radical change in the inflationary mindset that allows for higher prices to get passed on and persist is why I’ve been throwing shade all year since January on assertions that this inflation is temporary.

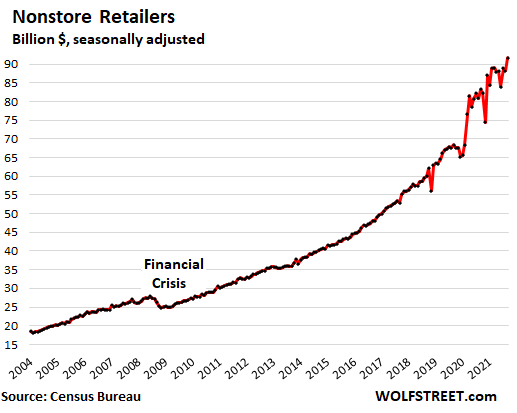

Ecommerce and other “nonstore retailers”: Sales spiked by 4.0% for the month, to a record $92 billion, up 10.2% from a year ago, and up 34% from September 2019. They include online-only retailers and the online sales of brick-and-mortar retailers, as well as sales by mail-order houses, street stalls, vending machines, etc.

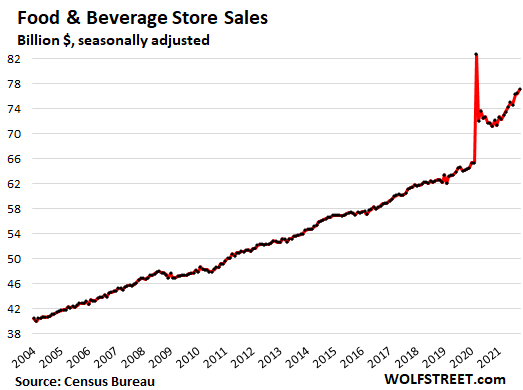

Food and Beverage Stores: sales rose 1.1% for the month, to $77 billion, up 8.3% year-over-year and 20% from October 2019, powered by surging prices:

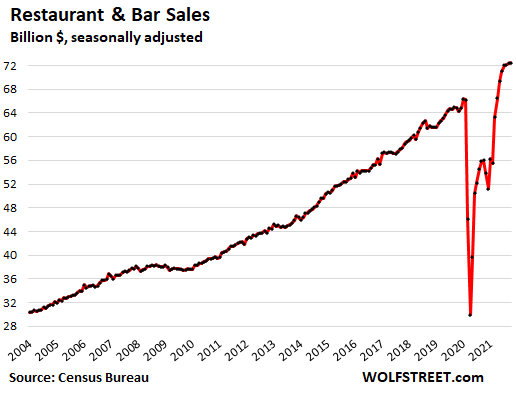

Restaurants & Bars: Sales were flat for the month at a record $72.4 billion, up 29% from a year ago, and up 11% from two years ago, as the CPI for food away from home jumped by 0.8% for the month and by 5.3% year-over-year, with restaurants passing on surging labor and materials costs:

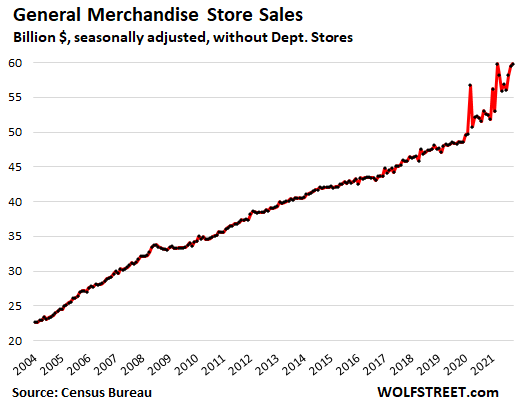

General merchandise stores: Sales rose 0.8% for the month to $60 billion, matching the free-money-blow-off record in March 2021. They were up 13.7% year-over-year and 23% from two years ago. These stores include the brick-and-mortar stores of Walmart and Costco:

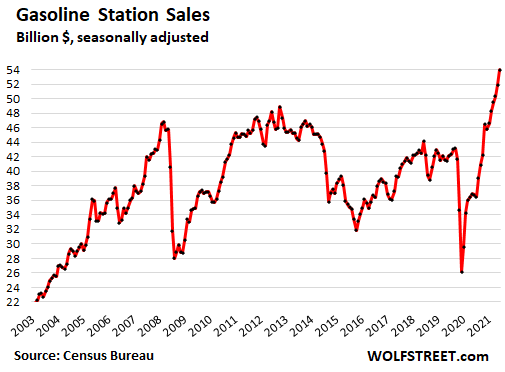

Gas stations: Sales jumped 3.9% for the month, 47% year-over-year, and 28% from two years ago, to a record $54 billion, powered by gasoline prices that spiked 50% year-over-year, according to the CPI for gasoline. Sales at gas stations include sodas, junk food, beer, motor oil, etc.:

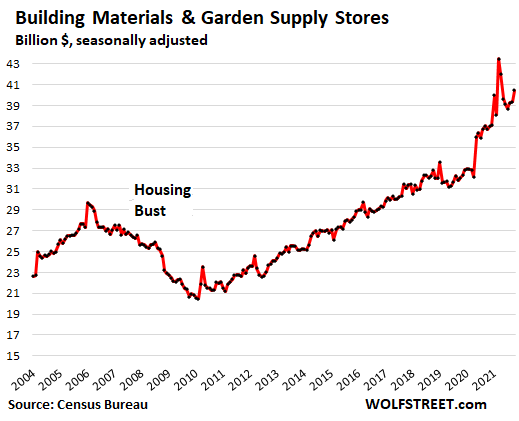

Building materials, garden supply and equipment stores: Sales rose 2.8% for the month, 10.2% year-over-year, and 26% from two years ago, to $40 billion, still down from the DIY-spike in March:

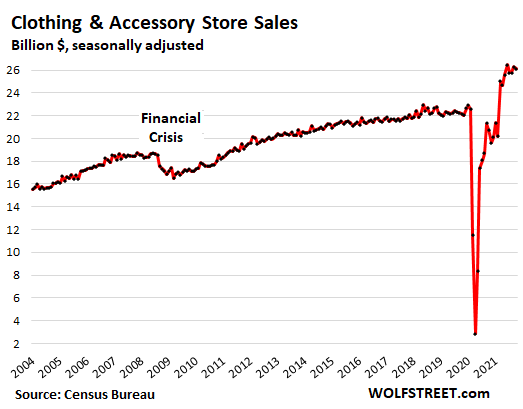

Clothing and accessory stores: Sales declined 0.7% for the month, to $26 billion, up 26% year-over-year, and up 18% from two years ago:

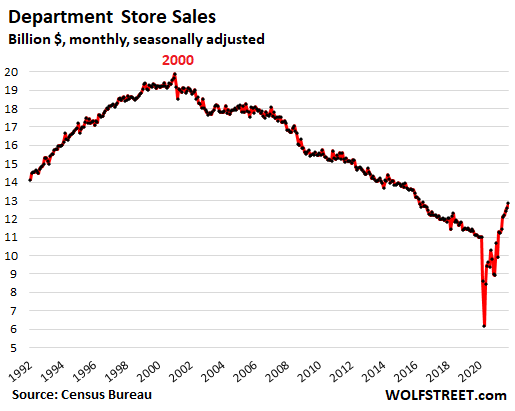

Department stores: sales rose 2.2% for the month, 28% year-over-year and 15% from two years ago, to $12.8 billion, which is still way below the levels of 1992, not adjusted for inflation:

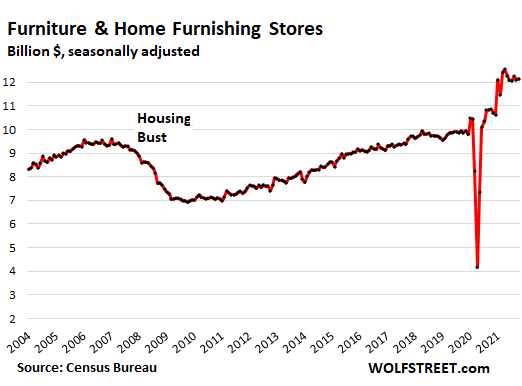

Furniture and home furnishing stores: Sales inched up 0.4% for the month, 12% year-over-year, and 23% over two years, to $12.2 billion:

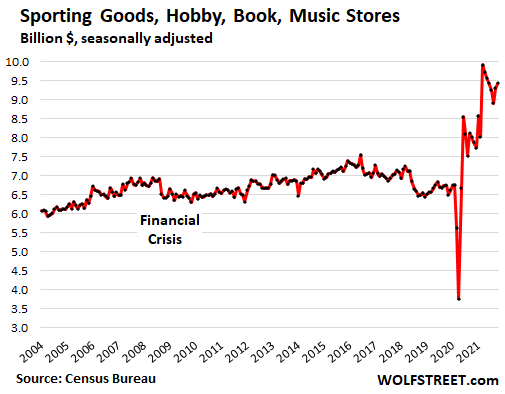

Sporting goods, hobby, book and music stores: Sales jumped 1.5% for the month, 18% year-over-year, and 40% from two years ago, to $9.4 billion:

Electronics and appliance stores: Sales jumped 3.8% for the month, 18% year-over-year, and 4.3% from two years ago, to $8.4 billion. This smallest retailer category here covers only the brick-and-mortar stores of electronics and appliance retailers, such as Best Buy. Electronics and appliances are a big industry, but sales mostly take place online and at other brick-and-mortar retailer categories, such as general merchandise stores and home improvement stores:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

so basically, holders of dollars, domestic and foreign, financed this entire spending orgy.

Yeah, and since most of this has to do with Americans and not third world consumers, the forex dollar has caught a bid. A strong dollar gives the US more leverage in buying foreign goods, and oil. OPEC+ ignored calls for more production, out of concern they will be generating a surplus when demand normalizes. Every American has an EV. By one report global demand would have to collapse 75% to meet zero omissions by 2050. The cost benefit to buying cars made offshore is antithetical to inflation in imported energy costs. Vinfast plans to start selling cars in the US in 22.

“OPEC+ ignored calls for more production”

Isn’t that ironical? Killing domestic pipelines, stopping fracking leases and then go ask OPEC to pump more fuel out of the ground to burn?

Is there a talking point to explain this away?

Morons…we are surrounded by morons.

No it’s the Power of Positive Group Think!

Works really well if you are inside the circle.

Until it’s stupidity of not looking at real consequences comes home to roost and then the shit piles up. Then no amount of changing the narrative or obfuscation works. It still stinks.

“Highly liberated junk food”…or whatever that stupid name means..(please do tell me if I have it wrong)…..Damn right there is!

That same fossil fuel bunch you are praising fought tooth and nail to sell US CRUDE OIL and NAT GAS on the international markets where they could make much more money for it. If that isn’t outsourcing jobs (and natural resources) for personal profit I don’t know what is. I witnessed similar disgusting behavior in Eureka early 70’s when I saw totally RAW logs being loaded on ships and it bothered me particularly badly because I grew up with many friends whose fathers worked in lumber mills. High gas prices come our few remaining neglected and aging refineries, not a lack of crude….we have enough to support building of a Comprehensive Green New Industry, but selling CRUDE does NOT help the US.

Sure refining is tough nasty work and getting worse because of simple lack of investment in facilities and new tech. So was early millwork. Jobs like offbearing paid high because of the likelihood of being maimed for life or killed, but flying lumber or pieces of blades, machinery, etc, happened everywhere, just more so at the very powerful Head Rig. Millwrights were constantly patching holes, fixing guards, where things came flying through.

Not very patriotic, (or very bright) on your part, eh?

BTW, I worked in mills but preferred the woods, why don’t you tell us where your “hard earned money” comes/came from?

I hope not from “talking point” creation, I truly do.

“Highly liberated junk food” Lol, I’d drill that for oil. click!

I highlighted the ignorance and hypocrisy of those bans and begs. Are you too smart or too dumb to understand that?

Your “retort” is festering well, as expected.

More incoherent rambling from Ambrose Bierce. Not just incoherent, but completely nonsensical.

Relax nar,,, lots of us frequenters on here sometimes post comments in what used to be called, ”in our cups” and that is NOT always a bad thing,,,

”In vino veritas”,,, etc., etc…

And to be very clear for some of the younger folks on here, boomers, et sequalia, (sp) there are many many old and older ”sayings” that absolutely NAIL this current situation.

For Example,,, many years ago, almost every ”housewife” put the gold and silver accrrued (sp) in the ”good years” into a jar in the yard,,, and then dug it up and bought ”cheap” in the bad years when crashes happened, as the crashes always had happened in accordance with ”’natural laws” …

Attemps to stop these crashes by the ”FED” or any such entity, as many on here have said, are NOT going to happen,,, just ”postponements” that not only prolong the agony for the vast majority, but also act to increase the control of the oligarchs.

AB won’t waste his time on our resident financial sophist’s challenge….angels on the head of a pin is not his thing.

Sorry, no free practice for ya so far in this thread.

I’m seriously contemplating, although unaware of the best way to go about it if liquidating assets to then hold some foreign currency.

As a speculative trade or longer-term hold?

For the latter, I’m only interested if it’s going to be my second currency of reference, where I use it to also pay my living expenses.

It seems I recall that my local bank, a while back, could get foreign currency within a short time frame upon request…

Don’t know about today…

I think the plan would be to buy an investment security which is a cash equivalent, for that purpose, in the country you choose, through an international bank.

Red,

The problem is that no major foreign currency is a safe risk over the US Dollar. The eurozone may collapse, this doesn’t mean the European Union will as well. The Yuan is not a serious currency and can’t be converted back. Japan and South Korea are stagnant.

Most smaller countries could have their currencies crushed in a global recession/depression. A big issue for many tax havens, will be the UK’s probable loss as a major finance market. Because of brexit, Germany can now crush England in an instant, and is heavily incentived to do so. Germany crushing England, will likely cause a reshuffle of the tax havens (some will fade away, some are added, sizes change).

In general, I expect most developing countries to be more crushed in a global recession/depression than the developed ones.

I have wondered about the infamous Swiss Frank/Bank account. The Canadian and Australian dollars should definitely be considered. The Czech crown is a possibility. Tawain? I’d definitely stick to developed countries, mainly the smaller ones (population wise), and not all in one.

You can easily get foreign currency at the bank, some people put it in a safety deposit box, it’s not amazing, but it’s the best an average jo can do holding foreign currency in America (maybe several safety deposit boxes?). It’s hard to have foreign bank accounts though, because of specific tax laws concerning Americans and foreign bank accounts. There are easy to use banks for precious metals.

If there is a global financial crash, maybe even if there comes a global recession/depression many small countries can have their currencies crushed. But probably not all.

After the crash when the dust settles bits and pieces will be scattered around in new positions. A guess, those countries with functional governments, working administrations and natural resources will come out best of.

The eurozone may collapse, so the US dollar zone.

The massed debt the bundesbanke is owed by Italy et alia may well crush Germany before she gets the opportunity to crush the UK 🤫

I just heard that the Staples Center in LA is going to be rebranded as the Crypto.com Arena. Guess where the next financial crisis is going to come from. Crypto is the favored currency that not only avoids taxes, but also avoids the law. It is the currency of choice for every criminal enterprise on the planet. Whoever renamed the Staples Center paid over $740 million for the privilege. Criminals are awash in cash, apparently.

The eurozone will not survive without the Euro. Countries like Italy will have little and IMO no incentive to remain members without the wealth transfers from the richer countries through the ECB. There are the EU fanatic elites, but that may not be enough to hold it together. My opinion is no, not with the current member composition.

Look at “target 2” balances. It’s an accounting of the wealth transfer. If the ECB and euro ever go away, holders of so-called “periphery debt” are going to take a major haircut.

On the rest of your post, it’s easy to buy FX instruments but it’s a lot harder to do so prudently for those who believe the global financial system is at risk of falling apart.

Sams,

I picked Australia and Canada, because of their resources, among other reasons. Picking other small counties is hard, because alot could happen, that could never be predicted.

The US dollar is only created by America and although some countries peg to the US Dollar, it’s not even remotely the same situation as the eurozone. So the US dollar zone cannot collapse. The US dollar itself collapsing, would likely trigger events, collapsing the other major currencies.

Deutsche bank will have to collapse or be massively bailed out at some point, but of all major economies, Germany is in by far the best shape. Outside of certain things like Deutsche Bank, Germany’s economy is the best put together of any major economy and is the center of European industry. Germany can cut the UK out of the rest of Europe on a whim.

As for the EU, the problem is that it’s at a transitional point where it has to become more or less integrated. Unless, it really were to want to become a single large country, it would have to become less integrated. The eurozone is the major thing that has to go, to allow the EU to survive. If the eurozone goes, certain other things could be made less integrated as well.

The EU can survive without the Euro. The reason to stay is that simply, it’s how all the industry, defense, resources, and foreign relations can be handled as a single powerful group.

If countries start to leave and no one is stopping them, the EU has to by definition, cut them out of many of its supply chains, thought processes, defense agreements, and more. You might think Italy is better off outside the EU, but what is Italy to the world, without the EU? Most problems Italy and most members of the EU face, are internal problems. The EU has benefits and drawbacks, and in some cases like with the refuges, you have to be like Hungary and be like, nope not happening, if enough members push back for certain ridiculous things they won’t happen for long.

Alot of places think they are important and substantial enough to go solo (and it pays off), but they aren’t. Germany and France are substantial countries and if the EU collapses, they might build a new smaller, more powerful and integrated EU. Most of those not invited in, would be much smaller and weaker afterwards.

Thanks Perp.

That’s info worthy of some thought.

I go to a Staples (very seldom), just for proximity. Seems to be becoming kinda expensive, and maybe low traffic, although I don’t know who are it’s main competitors.

Maybe it caters more to the tax write-off set?

Sorry, I forgot it’s an Office Depot I go to….”seldom” becomes obvious.

But your comment is still worthy of some thought, Perp.

RE RED: Two big brokerages are advising clients to put on eurodollar steepener trades, which would seek to capture the sooner than expected Fed move on interest rates. Art at Yahoo. You can read about how the trade works at Investopedia, the futures market in eurodollars is large and liquid. RE NAR; Inflation is all about energy, always has been always will be. US may prefer to embrace the strong dollar, (bad for jobs and manufacturing) and import our cars from Vietnam, or Mexico. Our labor market is already maxed out. A strong dollar is antidote to inflation.

Just short the market if it works ,you never will again

That was the name of the song for many years, in case that you just noticed. It is not just them: most Americans’ earnings have not kept up with inflation FOR YEARS, so in real dollar terms most billion-dollar companies and banks have had to pay less and less in wages, etc., each year. Ditto for any persons getting or living off of defined pensions, social security, annuities, bond payments, etc., whose payments did not keep up with real inflation.

Nice, no? I mean nice for the billionaires and trillionaire families, not for us, of course.

“I mean nice for the billionaires and trillionaire families, not for us, of course.”

That is the designated purpose of the private banking Fed. They represent the rich and the banks. They don’t care about anyone else.

Period.

Take a look at a bit on CNN’s site today by Mark Zandi, Head of Analysis at Moody’s, titled ‘When will inflation end?’

Briefly, he says we’re worrying too much and it’ll all be over in a year. Supply chains will return to normal, Covid will recede, etc.

High gas prices? These will encourage more supply, curing high prices.

He says ‘maybe I’m optimistic’ and I agree he is. If a landlord has overpaid for a rental prop, his mortgage won’t magically recede next year, nor will his need for X rent.

But what catches my eye is that Moody is kind of talking its book here.

About half the bonds rated investment- grade by Moody and S@P are just one notch above junk. They are on thin ice and so are the fees they pay the raters. When half a class gets a ‘C’ you can be pretty sure you are seeing ‘grade inflation’. A strict rating of the class or these bonds, would see that dreaded word, almost today an obscenity: ‘fail’.

A Fed- induced return to reality via normalized rates would make it impossible for even Moody to squeeze a lot of these bonds through the exam and there go the fees.

Nick Kelly,

And to add to your point, supply chains have nothing to do with rents, and market rents are now spiking (+10%). This will take a while to flow fully into CPI. Two rent measures in CPI account for one-third of CPI, and they have just started to react.

There are other services that are seeing lots of inflation, including transportation.

So this is not just a commodities-based surge in inflation. This is widespread.

It seems to me that people are not exactly displeased with this so called inflation while they’re getting free money. It would change when free money stops, but for now perhaps it should be seen as wealth sharing. The 1% had their share and now the 99% are getting a share too and enjoying it, is what I see. We are after all all in this together.

Over the last 20 months personal savings surged by $2T+ over the 2017-2019 trend. Only $700B in retail sales (over the 2010-2019 trend extrapolated to 2021) has been spent.

So while the personal saving rate has dropped to normal levels, there may still a lot of fuel for the inflation fire.

But now we have morons trying for more stimmies. We live in Idiocracy.

“personal savings” is a misnomer. It’s just the mathematical difference between “personal income” and “personal consumption expenditures.” It’s money-not-spent on personal consumption expenditures.

But this money did not go into a savings account. It went into down-payments for homes, it went into mortgage payments, it went into paying down other debts or catching up on late payments, it went into stocks and cryptos and bonds and gold and silver. None of these count as “personal consumption expenditures.” So this money is mostly somewhere else.

What free money are they getting right now?

Good question, Pea Sea. Who is still getting “free money” ? ?

One gets the impression that there is a big echo chamber out there chanting “Free Money, Free Money, Free Money”.But there doesn’t seem to be anything of substance behind the chanting.

I’m still waitng for my Biden stimmie…

California is on it’s 6th stimulus check or so. Just call it UBI and let face book pay for it.

Child tax credit still running. I have a friend with three kids, two under 12. It’s about $1000 per month. He was probably netting out $4000 per month before credit, so it’s a 25% increase in take home money.

yes but that’s not the whole story. the tax credit was previously $2,000 a year. there were three main changes, one, it increased it to $3,600, two, it made it refundable, so you could get money back in excess of taxes you actually paid, and three, it’s paid in instalments instead of as a refund at tax time.

so for your friend, with a decent income, he’s really getting $133 per month per kid more, or $400 total. the extra $600 is just being frontloaded, so he’ll get a smaller refund in april.

Well then you’re not really seeing what’s happening. It’s like you just made up a scenario. The free money stopped months ago for the so-called “99%.” And in the grand scheme of things, they didn’t get jack. It was the PPP recipients of almost a trillion dollars – the already wealthy – who made out like bandits. CONgress basically said “hey, here’s some free money, go buy every truck, boat, RV and vacation home you want, on the backs of the future of the young, because, well, just because.”

Agreed…

For the majority, most of this is a one time windfall and done…

There really hasn’t been enough time for all the money to have been pissed away yet…

Most who were broke before will be broke again…

Same leopard, same spots…

Agree. Why I received/qualified for a stimulus check is beyond me. 2020/21 have been to of the financially best years of my life in regards to amassing wealth. Could not spend my regular salary, received multiple checks from the gov., stocks up. I would spend, but with everything priced at a premium, I’m holding back until things cool down a bit (I’ll buy used at a discount once the current idiots who are purchasing in a hot market start their panic selling).

not putting a revenue test on ppp was the second most outrageous thing the cares act did. the first was the unemployment that was more than people made.

“We are after all all in this together”

Surely you’re kidding, right? Are you a Federal Reserve employee ?

Although the charts presented are seasonally adjusted I believe the adjustment is based on historical seasonality patterns – an extreme irregularity in Christmas demand (either low or high) could still skew the data, right?

Not seasonally adjusted, total retail sales spiked by 14.7% from October last year, and by 21.5% from October 2019

Seasonally adjusted, total retail sales spiked by 16.3% from October last year, and by 21.9% from October 2019.

Bill Gross said financial system is going to collapse some day because you can’t have a financial system without savers and long term investors.

I’m pretty sure the remaining savers will be rounded up and put into a camp.

Many who saved rather than risked what little they had in the casino wind up in homeless camps and in a “non-human” status. Much cheaper than building camps or rounding them up.

Kinda similar to “private contractors” being much cheaper than old time slavery. The system just washes it’s hands of them as “human capital” needs diminish, and has desperate “human capital” “banked” to draw on as needed.

Depression era vagrancy laws aren’t far off if this continues.

OS,

I wonder if buying Bitcoins is considered “investing?”

You mean the same way that buying a Rivian (truck) is the same as investing in Rivian?

It’s a great truck. EV makes more sense for pickups and offroad vehicles. 830 horsepower with 100 percent torque before you even touch the gas. 68k starting which is less than most ICE pickups and no $80 fillups at the gas station.

“EV makes more sense for pickups and offroad vehicles.”

Oh yeah, because they best place for an electric vehicle is to be off-road, 50 miles from the nearest charger and in an area that a tow truck can’t even reach. In that instance, it becomes a permanent fixture of the landscape. Just NO.

There are no gas stations in those places either and backup charging devices can be used just like a spare gas can. They just took one across the US on the trans America trail and seemed to find a charger each leg of the journey to make that happen.

BP…

How many miles a day do you drive yours?

Just curious…

I’ll let you get back to me on that…

@BP: “…830 horsepower with 100 percent torque…”

Big power, big torque and big weight do not a great offroader make. You only need so much power in rough terrain and vehicle weight is a big handicap.

Just go and google “suzuki jeep offroad capability” to read heaps of stories about these lightweight toy jeeps leaving the big iron in the dust.

Ford Lightning will beat Rivian to market. And Tesla could start delivering Cybertrucks. Crowded market space.

To add to Oskam, if it’s only for “offroad play”, the 4 wheel range is from trailered desert racers to trailered rock crawlers and everything in between.

Much variation/opinion in equipment that is “best”. As a boomer kid I was guilty of wasting energy on play, but offset it by living in a van, with roommates, etc. Never made enough to do otherwise. Never did 4 wheel off road play after HS though, that was always work.

Now I gotta go look up this Rivian thingy….never heard of it before.

By definition buying Bitcoin is not investing as it does not have an income stream that can be calculated. It is speculation, which lasts as long as people are in a mood to speculate.

Unreal.

Those bond guys better get on their marks.

I intended to have a low buy year, but life had other plans for me. Spent thousands on car repairs. Replaced the old patio furniture & BBQ, then we spent most of the summer sick, which was expensive too. Then had to replace our broken bed and mattress, both over 15 years old. Even had to replace worn out clothing. We spent a lot of money this past year, which we never expected to be spending. Thank God, we had the stimmy money to help with the deluge.

So I can see my troubles showing up on all your charts. Spent on car parts, furniture, healthcare, and clothing.

One question I have collectively for us all. Can we afford our American standard of living?

I’m amazed at and stressed out by the high wire act acrobatics involved.

No, but that will become obvious later.

Look at the government’s (FRB) own data, for those who even believe it. Real median household income up about a whopping 5% since 1999 to $67K.

Median net worth up about 10% to $121K (as of 2019) and this is with the greatest asset mania of all time.

I’d describe this profile as “working class” or “working poor” (depending upon where they live and household size), hardly “middle class”.

Financial circumstances of individuals have changed over the last 20 years but this is representative of how it is for most.

How has all this spending collectively been possible?

By borrowing and appreciation from mostly fake wealth increases.

What about population expansion? More people on both the high and low side? The pool is larger now?

Let’s look at the rough numbers.

Inflation 6%

Sp500 Earnings Shiller yield 3%

SP500 Dividend yield 1.2%

30 year Treasury 2%

Liquid savings 0.1%

Long term real economic growth 2%

Growth in broad money 25%. No it’s a sugar high. Most of us know it. Average Joe may not.

DanR, correct u are! High standard of living has resulted in a lousy quality of life for many . Big houses, 70k trucks, and the stress of keeping up so you don’t lose them. Our standard of living will surely drop but I doubt we will ever have the quality of life we once had by living with our means as in the past.

“Can we afford our American standard of living?”

Fortunately we live in a low cost area with good neighbors. No way we could afford to live in many areas, which is not a big deal since we would not want to live there anyway.

Petunia, stuff doesn’t last forever as I am sure you know. One has to plan for those upcoming expenditures. When we moved into this 21 year old house 6 years ago, I made a list of what I thought was going to wear out going forward. Things like the roof shingles, water heater, kitchen appliances, garage door opener, etc. and those things died along the way (and a few more). So now we have a path of low spending on home things going forward.

The only thing I didn’t plan on wearing out too quickly was me and the wife, but we did..LOL

So you got divorced? Or your bodies are broken down?

No divorce with this wife but the one before…full California divorce and whipping I took. Brought me back to ground zero from a savings standpoint.

We are just wearing out from old age (I’m 78, she is 76) but married 25 years.

Anthony,

That’s just part of being a man getting to start over at zero a time or two. Makes you appreciate it if you find a winner.

Old School, yes, finding the winner was the key.

Petunia

My stimmy money was gone before I even got it. Two dental Implants and a new Bridge wiped me out. But, look at the bright side. The Dentist and Oral surgeons did a great job and now I’m able to eat like a normal person. No more infections and pain.

SC: Great to hear!

I get my new front tooth December 1st after a 6+ month wait for the cadaver bone to assimilate and the surgically implanted threaded stud to hold. Out of pocket will be close to $6.5 K. Medicare covers none of this.

Inline with mega spending going on! Merry Christmas to me!

Within the last five years, I had cosmetic dental work during one of my South American trips at a dentist my father knows.

The cost was about $300. Don’t know what it cost here but probably around 10X.

Yes, there are plenty of qualified dentists elsewhere.

I have good dental insurance but would do it again (or at least consider it) for more urgent dental work before paying the prices you quoted. I’d travel specifically for it if necessary.

Prices here are insane.

Anthony A.

Also, my spending ($20K) helped boost GDP and retail sales this month. The dental insurance company I have, (GEHA), paid about 1/3rd. Would have been 50% but the dentists were out of the GEHA Network. Around here any top dentist you hire to do serious work is usually not in these insurance networks.

A.A./S.C.

About two and half years back I had three dental breaks happen in short order requiring one implant and two standard caps. Set me back around $7K, all out of pocket and I just got another busted fang recently and am looking at another $1.300 to cap it off. The fun never ends. I’ve heard of people going out of country for dental work. I wouldn’t know where to go or who to trust. If you can make it work more power to you. As to planning ahead I’ve been putting around $500 a month into a savings account for several years now for, god forbid, vehicle replacement. I’d rather pay now then pay later. I also built up some lump sum amounts in the same account for future TV, computer, eye ware, and furniture replacement. They may not fully cover replacement costs but it’s sure nice to have it there and not get totally blindsided when things happen. Same with auto insurance. Pay ahead into the account and pay it off yearly when due.

We spent a lot on car repairs. It’s an old car, so it just is time.

I spent on more clothes than planned as I changed sizes. :( And Hubby needed new jeans due to wearing out. Other odds and ends wore out and had to be replaced.

We really could use some new patio chair cushions, a mattress as our is dead but bought neither.

Our big expenses were a new stove/oven which we badly needed and a short vacation to Cancun which we badly needed.

The most expensive leaky faucet fix ever. Couldn’t find a valve to fit the faucet. Couldn’t find a faucet to fit the sink. Couldn’t find a sink to fit the countertop. Basically a leaky faucet snowballed into a full kitchen remodel.

Really poor time to be trying to do home remodeling. Prices are skyrocketing … and that’s if you can even get the materials and appliances, not to mention the trades to do the work. This is the worst economy I can remember.

Yikes, Finster!

My daughter needs a dishwasher as her’s died. I said I would buy her one for Xmas. But I can’t find any in stock at Home Depot or Lowes under $1,000 in white. I don’t plan on dropping a grand plus for a dishwasher. We are waiting until more are in stock.

AA,

If she’s not too picky, you may want to check out American Freight in your area… they are on line with inventory…

New stuff but might have cosmetic damage…

Mucho savings…

AA there is not much to a dishwasher. Just a few parts. Find a repair person or try it yourself?

How do I know? Ours broke late in the day prior to Thanksgiving with lots of folks coming. No way a repair person was coming. My brother and I took it apart and figured out and corrected a minor issue.

Nothing to lose if it already doesn’t work.

Doug, the existing dish washer is 17 years old and I have repaired it once already (new door seal). But the frame at the door bottom is rusty and leaking again and another new seal will not be effective. Plus, the thing sounds like a freight train. It really needs to be retired, but that may not happen for a while, I guess.

For a dishwasher, I recommend you look at the larger appliance retailers. They usually have a supply of “bump and dent”, last year’s models, floor samples or builder take outs available.

Your issue is that you’re looking for “white”. Those are either el cheapos or custom order for one worth having.

We have bought several high end “open box” units over the past decades and never got a lemon by buying from an appliance dealer. None were anywhere near approaching $1,000.

There’s an online appliance company that has white in stock from $359. ABT. Don’t know what the shipping cost is…..

If money is tight watch out for moving sales. You can get great buys on large bedroom stuff including mattresses. You can put a topper on it if sleeping on other people’s mattress freaks you out.

Never understood this bed thing. See MANY ads for $3-4K and up beds that do tricks….to give better sleep…I guess.

I have been on same 4″ quality ($160 and folds into 3 sections to fit in old truck w/shell) since ’06 and it “works fine”.

I learned that if you can’t sleep it means you need to lie still and think about something, so I do. Even if you don’t think you got any rest, you did, and can work the next day…..learned that from my old speed days…..but too many nights like that and work does get tougher….learned that from 13 years on graveyard.

I think this culture just increasingly drives people nuts, at bottom, bed design doesn’t help much. If it’s really bad, get something from the doc….but stay away from cofefe…I mean Ambien…and don’t over use anything….use some discipline.

4″ quality futon on floor….left that out..pretty hurried…..coming up on every 8 days shopping/errands trip and pain pill (tramadol) relief schedule says I gotta go soon.

NBay-…still pitching, and well. Has been established by experiment for some years now that our evolutionary sleep cycles (roughly a five-hour ‘big’ sleep bracketed by two two-hour naps linked to our hunter-gatherer past) when allowed to occur, i.e.: having no overlay of Industrial Revolution demands on an individual, do not appear to square well long-term with those demands. The possible maladaptations to ‘natural’ sleep could have something to do with the contemporary amplification of our innate human cussedness…

may we all find a better day.

Petunia,

Troubles…

Naw…all I see is an investment in your quality of life… money well spent…

The spending was painful, but I now have a really nice bed and mattress, a nice looking deck, some cool outfits, and the cars are running. Overall, we were grateful to be able to afford most of it.

Probably the most comprehensive and unbiased breakdown of the reality of todays overindulged US consumer. Excessive pricing will NOT normalize without a massive correction. The money will run out and rates will rise leading to massive demand and value destruction across most asset classes.

“Probably the most comprehensive and unbiased breakdown of the reality of todays overindulged US consumer.”

Ergo, Wolf Street! Most comprehensive and HONEST reporting on the planet. Definitely not a journalist…as he’s not, thankfully, with the “narrative.”

Mugs and my new theory of why everything’s messed up.

(A brief excursion into the world of supply chain disruption, inflation, and the total collapse of everything.

One small item first.. I still have my mug, Wolf, so don’t send me any more. It just causes scarcity, which, as Sartre said, is the cause of tension between man and man

A few weeks ago I ordered 2 pairs of gym shorts and a set of solar powered outdoor lights.

A week later I received ONE pair of shorts. A week after that I received the second pair.

Then I received an email that my return of the lights had been received and I was given a credit.

I never received the lights to begin with so I had to re-order.

I’m trying to set up a bank account for Gorback Land and Cattle LP my new little ranch (our motto: “All hat and no cattle” – the second most used phrase in Texas after “Don’t piss on my boots and tell me it’s raining”).

I wanted to use a small bank. The bank officer had trouble understanding the difference between Gorback Family LP and the general partner Gorback Management LLC. She wanted to see the stock certificates for the LP and I had to explain limited partners don’t get stock certificates, only the GP (LLC).

Then I decided to try with my professional corporation. It was set up as a professional association (PA) 25 years ago as an S Corp. In Texas there’s a ban on corporate practice of medicine so back then they used PA’s which could only be owned by doctors. They spazzed out because I didn’t have Articles of Incorporation. I had Articles of Association for my professional ASSOCIATION.

After some gentle explanation and a few beatings with chairs they started to understand. Well, the conscious ones appeared to.

I think the real problem is that covid secretly chops 25 IQ points off your brain even if you never had symptoms. As a seasoned medical professional I conclude that the spike proteins break off and clog up your thinking tubes.

mg-a corrollary: electricity fails when the vital smoke exits the wiring…

may we all find a better day.

“I think the real problem is that covid secretly chops 25 IQ points off your brain ”

I thought it was due to oxygen deprivation. Folks in TX wearing masks?

The real amount was 4.7 trillion, we were all lied to again. Reparation money for what? Just wait people, we are all headed into boxcars.

I’m confused. What reparation money?

Why was/is it $4.7T? What/when batches of money?

Gonna be delays..the remaining boxcars are sidelined on the team tracks at Doc G’s inflatable steer ranch in Tejas. Heard he’s worked out a deal with Nike to sell Air Steaks. They just want to see his incorporation papers first. 🤕

With the M2 money supply going up over 20% YTD with no increase in productivity, its not surprising to see inflation approaching that same level. Most if not all the growth in retail sales is just inflation. I’m waiting for the bond market to crash. Michael Burry has a big short on the bond market.

Price increases and not the amount of goods sold?

There was just an art auction in NYC where 35 lots went for $676M, about $19M+ per lot. This was just half the art collection of a rich divorced couple, with the sale mandated by the divorce court. The other half of the collection comes up for auction in the spring.

If you saw the pieces sold you would really understand the impact of inflation. The amount of money transferred to the one percent would also be evident by the bids.

This seems YOLO levels of printing by the Fed. This is what you when you know you’re about to declare bankruptcy. Maybe there’s some geopolitical basis for all this? Dollar is going up, emerging markets will get hit hard soon.

Hi Wolf, if the USD $ is going up and will not be the escape valve for the financial and debt stresses then what happens to Interest Rates, the Stock and Bond Markets ?

If interest rates (yields) go up, by definition bond prices go down. And interest rates will go up, and they already went up a little bit. In return, this could strengthen the USD v. EUR, YEN, and developing market currencies.

Stocks are in ridiculous-land. Who knows what they’re going to do.

Emerging markets that borrow in dollars have taken a huge risk, and they knew it, and they did it anyway because it’s cheaper to borrow in dollars because investors with USD are stupid yield-chasers, but then all heck breaks loose when, as is always the case, the dollar rises against these currencies. This is the oldest game in town. Investors who lend dollars to emerging markets should get their shirts ripped off so that they stop doing it at low rates.

Very interesting Wolf, Thank you. This financial system puzzle just keeps changing form. If the Dollar does not weaken then we could rather end up with a Dollar initiated EM crisis even before a S&P crisis

I have NO Idea at all on this which is why im asking. If you took 100,000 USD cash and put it into 100,000 EUR and then inflation lowered the value of the USD. And then a few years later put it back into USD you would be ahead ?

Red,

Inflation and exchange rate are two separate things — though one can impact the other.

If you buy foreign currency, it’s a bet on the exchange rate, not inflation. If you buy EUR, you hope that next year, the EUR gains x% against the USD. This is not linked to inflation but to how the market trades these currencies.

If you manage to find a way to put $100K into EUR 100K, you will definitely be ahead since we might not see the parity again for quite some time :)

It’s usually easy to click the mouse and move a large sum from US equity to International equity. You are taking currency risk, but if dollar is relatively too high and US stock market is too high then you get a twofer if things revert to long term trend.

The down side is if you are in the US most of your purchases are dollar related so you don’t want to take too much of a currency risk.

“Who knows what they’re going to do.”

I agree with “ridiculous”, but we can begin to feel the rhythm of this…

down in Sept…

best month Oct…

then, close on the highs year end … for the big bonus payouts.

meanwhile, the proletariat suffers with high gas, and a punishing inflation that is wiping out any savings they may have.

I looked up Fed’s Eccles Building on Google Street View,as usual they failed to update their views,neon sign on top of main entrance still says “INFLATION IS TRANSITORY”

At midnight yesterday they started displaying a new running neon sign:

MENE,MENE,TEKEL,UPHARSIN

Read the Message that’s writ on the Wall

In fiery Script 10 feet tall

And in case Hebrew

Is all Greek to you-

I’ll translate: it says “F… You All !!!”

1) JP is linear guy on his bike, but he was building theme parks in the last four years.

2) Every price increase above is a crazy roller coaster ride.

3) Disney roller coaster is the scariest.

4) The tallest roller coaster in the world is NDX. It’s sow high people don’t look at it’s top.

5) It’s above 3.618% of 2000 bubble.

6) It looks like gold between 1980 and Sept 2011.

7) If Nov 5 high & 10 low is a backbone, – not yet – NDX might rise even higher.

8) In the futures market Nov 5 is shooting at the skies.

9) The monthly, got DM 13, but it’s all bs, a week before we fly in Thanksgiving.

9) Eat & drink, because tomorrow is a roller coaster ride.

Sqqq

Understanding the American consumer is beyond my ability. If I forget that I will certainly be schooled again.

Pre-pandemic, before I dumped half my stocks in late 2020 early 2021, I played around with SIG, a major retail jeweler, when price was around the 50s to 60s. A couple of times I bought at what looked like a significant dip, and then made some money when it rose with general stock market or specific sector excitement.

I thought, it’s pretty safe to assume that Americans will always be buying jewels to flash around. Big diamonds to impress the fiancé, etc. etc.

But I didn’t get out fast as pandemic developed. Got cut trying to catch the knife. Finally made it out roughly breaking even overall.

The low after pandemic was around 7 (yes, single digit 7!). Just checked, and now it’s at 105 (a 1,500 percent increase).

I was weak in not sticking to my principle that the American consumer never stops indulging in unneeded, unproductive, short-term bling). If I had held I could buy a new BMW or Mercedes right now, or a villa in Portugal.

I am not the best investor for sure. I have never sold out of a stock position at a loss as far as I know, but that doesn’t mean I haven’t been underwater by 50% and it hurts like crazy.

I too made a big blunder by selling for a profit an on line retailer and buying a brick and mortar REIT just before covid. I eventually made some money on the REIT, but it was roughly a $100,000 error at the depths of covid.

I tend to buy all the way down and the shares I bought at the bottom bailed me out as they were 4X winners. But Fed has made about any style of long stock investing a winner. It will change at some point and most of us will realize how strong the wind at our back was.

STICKER SHOCK:

Today I placed my usual order of $200/$210 with IHERB. Those same items now cost me $313. The shipping is usually $4. Shipping is now $15.

When does transitory inflation end? LOL!

Which shaman do you follow? Weil? Watch out for serotonin poisoning….very nasty stuff. The wrong herb or OTC med plus maybe an Rx with SSRI properties, and a strong cup of coffee can easily give it to you.

Horrible symptoms that too many docs don’t even recognize, treat wrong, and could end in an agonizing convulsive death.

And don’t forget Thanksgiving is coming up…turkey is said to contain a lot of tryptophan, which you body converts directly into serotonin, as I recall.

So to beat inflation have stocks that PE ratio says should go down. Or buy RE at nearish the top. Gotta be a safer way then riding this tulip wave.

Inflation is bullish stocks…..as long it is unaddressed by a Fed that wont raise rates….

“Won’t” as in deciding who gets the money and from whom it is stolen

We see in the numbers that unit sales for new vehicles are down but the ones sold are at the higher end, so total sales in $s increases despite fewer sold. Can we imagine that is happening in many parts of the economy?

People have been frenzied into believing there are severe supply shortages which will impact availability of inventory for the Holidays. When in actuality “there’s as much inventory for retailers, more (relatively speaking) stuck on wholesalers, and who knows what floating around on ships and how anything might be accounted for trucked or on rail. ”

https://alhambrapartners.com/2021/11/16/christmas-comes-too-early/.

What happens when the reality of too much inventory starts outstripping demand? Prices will come back down to earth & then we start heading into a stagflation& then deflationary environment. It’s coming in 2022. Inflation pressures experienced over the last year or so will be a blip on the radar. Until the Fed’s last gasp effort to hyper inflate & resuscitate an already dead patient.

We talk at work about the present situation daily. I feel I am fortunate in being in the skilled trades at an auto factory in Michigan since overtime available is wide open and I also have a lucrative side business to make up for the cost increases the american public are experiencing. I feel sorry for people who do not have the option or ability to work overtime or any other resource to make additional money to compensate for this BS. It’s not fun to work so much either, this old horse is getting tired.

Interesting times, recently i was checking prices for a new refrigerator on the Best Buy and Home depot web sites, noticed that not only prices went up crazy high but almost 75-80% of the items listed are out of stock.

Then out of curiosity started to check other items like TVs, Cameras, they are in the same range, more than 70% are out of stock.

This is Unbelievable.

I bailed out on typical middle class life 15 years ago. I never had the aesthetic gene, for me it’s function, function, function.

We have a second hand appliance store where an old timer repairs old appliances and sales washer, drier, refrigerator, stove for around $150. Usually I can fix appliances myself, but once in a while if it’s totally shot it’s off to the second hand store.

It is true that some of the old stuff was made better than the new.

Never seen a cook stove or a refrigerator I would pay $5000 grand for.

My laptop packed it in a few weeks ago I so did a scad of research comparing the benefits of dealing with a local computer/tech store vrs Big Box. Settled on Costco as supplier with the i-7 processor that I wanted. Why? Price the same and they doubled the warranty, plus Costco has always been awesome about returns, etc. The local stores have to send it away to a product repair depot anyway if it is under warranty. I was going to buy it the same day while in Costco but decided to wait and do a bit more thinking and research etc. A day later I bit the bullet and they sent it out by courier on Sunday. I should be receiving it today and I live on northern Vancouver Island. I believe there is a 90 day no questions asked return policy in any event.

There seems to be no shortage of any electronic products in any of the the other large retailers in our area, including Best Buy. This latest storm might affect things but who knows. I know retailers on the Prarries are suffering shortages and many are trying to source local products to make up the missing Chinese plastic crap for ornaments and such.

I think shortages are hit and miss depending on shipping port and product. And now weather, as a few west coast beaches are littered with fridges and stoves…..110 missing containers washed off a ship last week.

Wait till consumer sentiment crashes. Retail sales will go even more WTFer!!!

Notice to Shoppers: Price increases will cease when shelves are empty. Stock up and Save Today! Coming soon..fixtures!!

“Price increases will cease when shelves are empty.”

Prices will rise, IMO. The rate of transactions will slow….or halt, if the shelves are empty

Wanted a dishwasher, home Depot and Lowe’s are sold out of Bosch I want. Was looking at a new office chair on Amazon and they want $20 shipping for them. It looks like they’re passing the cost on.

I have a small storage unit with Extra Space Storage in Raleigh NC . I leased i in May last year — cot $24 per month. It went up to $30 in January and I just saw on my credit card bill that they upped the price to $47 in November. So that is nearly 100% increase in 18 months.

Someone needs to tell Powell and has merry incompetents that inflation is a spiral and once it gets going it feeds on itself and it hard to stop. “Transitory ” inflation only occurs if the brakes are applied somewhere. He has not found the brake pedal yet — his clodhopping feet are still stuck on the accelerator. With NO justification whatsoever.I guess this is further residual damage from the Trump administration. These people have/are causing tremendous damage to the U.S.

The storage unit companies always do that, it’s not new. They are evil.

Oh, please! Stop with the partisan politics bs already! Divide and conquer is the name of the game and you are being played. Usa has one political party with 2 wings. Your ignorance is exceeded only by your arrogance!

An eroded oil pipeline exploded in Iran, caused a minor earthquake.

WTI didn’t care.

Went to test drive a Genesis GV70 SUV. At the showroom entrance was a whiteboard tallying vehicles’ location, estimated arrival date and sold status. Sales people seemed in command. Had to ask for one at the front desk if you did not have an appointment.

SUV’s are in demand. Very few on the lot. Quite a few sedans, though. What comes in is usually already sold or soon to be. Three month lead time if you order your SUV today.

We were looking for the 2.5 liter 4 cylinder turbo which is fast enough – 300 HP, 0-60 in 6.4 seconds, When the car was introduced, all that was available was the 3.5 liter twin turbo V6, 375 HP, 0-60 in 4.9 seconds. It’s supposed to be a BMW X3 m401 or Audi SQ5 or even Porsche Macan killer.

$54k and change for the Premier 2.5 liter GV70. They can’t get them in fast enough.

So, we dropped due to COVID into a super-steep recession. If that process was not arrested (financially), we were gambling on total anarchy. We could not expect instant smooth recovery (in a big experiment, and unprecedented emergency in this era). We bottomed and anarchy didn’t happen, and now the masses are compliantly spending off the stimmies which is accelerating money and generating jobs the old-fashioned way: buyer demand. There was some leakage and fraud and skimming as there has ALWAYS been in publicly-funded transfer setups. (That may have damaged our incentives, but hasn’t killed them ever, yet. People still generally need to work to eat and have amenities.) I mean, one definite scenario here is, things are roughly coming around.

It could be SO much worse, and we could be living in a place SO much more precarious and worse-functioning, as in, swamped in COVID with massive external US dollar debt, with saber-rattling neighbors, etc.

So I am hearing here: (1) the eternal chorus of doom scenarios of various flavors (and some as usual seem more credible than others), plus (2) people griping at a few spiked prices around the margins. Let me add perhaps another factor: the proneness to externalize one’s insecurities in choruses of blame and whining. And the tendency to think “I am special and my petty grievances of the (transitory) moment mean something is gravely wrong with the world.” And “I am desperate to feel knowing (this powerful) by generating gripes and sounding toughly angry.” This has been jacked up, IMO, by the online “rage industry,” which the overall dignity of this site (and comments) sail far above, thankfully.

There is definitely value here, all around, don’t get me wrong. But I wonder why my angle today is so rare here.

“I mean, one definite scenario here is, things are roughly coming around. It could be SO much worse”

Wolf’s articles are data driven. So if you think things are “roughly coming around,” fine. It would be good to provide data and analysis to back up your intuition.

The data presented in Wolf’s articles often looks pretty dark, or in the WTF realm of things. Some commenters do respond with more positive interpretations of the data, or other data, and the consequences.

For the most part, comments are loosely related to the data presented: related personal experiences, professional expertise etc. as well as reaction to the data.

It seems a bit presumptuous to be doing armchair psychologizing that characterizes commenters’ personality and motives (for example, asserting that “the proneness to externalize one’s insecurities in choruses of blame and whining. And the tendency to think ‘I am special and my petty grievances…mean something is gravely wrong with the world.'”).

Living in a country that’s 29 trillion in debt is real external insecurity. Unaffordable housing is real insecurity. Potential for going bankrupt at the drop of a hat because of a health issue is real insecurity. More and more civil violence and conflict is real insecurity, etc. etc. No need to externalize.

Thinking something is gravely wrong with politics and the economy in the United States does not imply that a person thinks they are special and have only petty grievances.

good summary IMHO dp:

appreciate your perspective,,, and clear in sights…

thank you

Today’s op ed in the WSJ by Judy Shelton titled:

“The Fed Needs to Remove its Blinkers” is worth a read.

My title would be: The Fed is running with eyes wide shut”.

The Fed and treasury are out of control. Where this stops, nobody knows.

B

Fed is running wild policy because things are screwed up. I can’t really figure it out. I think it has to do with dollar being reserve currency making USA the consumer and debt king of the world.

Seems like for the last year the Fed’s policy is doing more damage than good as over priced assets have taken another rocket up. Like I say, it’s got me investing in a gold miner for some inflation protection cause I am not going to keep but so much precious metals in my house. Other than that, I don’t have any US stock exposure.

Inflation and a rise in retails sales does not necessarily imply people are paying high prices, not in all markets anyway.

It would be very interesting to get a breakdown of actual units sold, rather than value, and whether the units being sold are the inflated price ones or not.

Around these sensible rural parts, people are buying more of the stuff that’s still available and cheap, and either bringing the related projects forward or storing it for future use, with the inflated price goods still sitting on the shelves. Nobody but contractors are getting lumber from big suppliers at these prices, normal consumers are putting off wooden projects till next year or buying from local sawmills. One family mill has just started up again after 14 years, and has done $300k of business in 4 months. That’s unstamped lumber, so people (and contractors) must be ignoring the building code. Doesn’t mean it’s dangerous though, as the unstamped stuff is very good. The local government knows it, but they already have a big shortage of inspectors, so their solution is to allow 10 of the new/restarted mills to get certified to stamp, which is unusually sensible of them ;)

This is mainly a supply side driven inflation spike. The FED can become hawkish, and inflation will still be running hot.

This is a long term problem from globalization and the only solution is at the ballot box.

I think I heard someone say that debts are so large that many can not be paid back. It’s a question of how they are not getting paid back.

Policy makers chose that instead of letting weak hands default on debt they will socialize the losses with inflation. That’s above my pay grade. I can try to be rational about it and try to adjust to policy.

Not too optimistic on voting as the past four presidents have been big deficit spenders. I think it is DC group think.

The bonds the Fed buys are debts that never need be repaid. The money is real, it was already spent, and now we have inflation? We end up paying one way or the other. The process of running concurrent deficits has been in place since 1980. The premise being that economic growth created by adding to the debt would more than offset the debt accrued. The initial benefit of adding new debt is used as justification to cut taxes (revenue) adding to the debt. And how would we pay that debt back, with dollars? Each dollar represents a liability. You can’t pay a debt with an IOU you are holding. However they could transfer the debt by calling in investments. The market cap of the S&P is 40T and the debt is 29T, they could bail-in stock investors and solve the problem easily.

SocalJim,

It’s demand-driven inflation, fired up by $10 trillion in stimulus.

Demand spiked HUGELY, and then prices shot up and supply couldn’t keep up, which caused further price increases and further demand because buy-today-to-not-pay-even-more-tomorrow… self-propagating now. Supply will eventually catch up, but prices will continue to rise because the mindset has changed and because that monetary and fiscal stimulus are still there.

Especially the monetary stimulus should have been turned off a year ago, and turned to tightening in January this year.

Same principle is playing out in housing, as you pointed out many times yourself — fired up by stimulus (low mortgage rates and lots of liquidity), which creates a demand shock, and everything else follows the demand shock.

If it was just a simple demand issue, the FED would have already cut back because the Dems are desperate to cool inflation.

But, the Dems and the FED know this is much more complicated than that. Cutting back would give us an inflationary recession so they are stalling.

There is also a political side to this, but I know you won’t agree, so I will let that one go.

I think the Dems are not so desperate to cool inflation that they will actually do things that stop inflation, like cutting government spending and cutting the money spigot at the Fed.

The Dems are good at convincing themselves that the things they want to do, like spending a ton of money, will cool down inflation.

Dems will have the worst loss in modern political history next year and will be the minority party in both houses.

Woke policies will also drive a huge wedge between Dems and every minority group except the blacks. You really think Hispanics and Asians arent tired of hearing the griping about race issues that always centers on blacks in America?

1) The crazy inflation. If the inflation rate in Oct 2022 will be 2%, y/y it

will be minus 5%, a lower low. We are falling and cannot get up.

2) In 1967 Egypt was defeated in the Six Days war and closed the Suez

canal for ten years as a payback to the west.

3) Commodities prices were rising, and ARAMCO, owned by four US co made tons of money, but shaved King Faisal dividends.

4) In 1973, during Yom Kipur war, King Faisal imposed an oil embargo

on US and confiscated ARAMCO.

5) Th 60’s/ 70’s inflation were about a bloodshed and payback.

6) Today clogging will not last a decade or two. Walmart have no intention

to destroy their vendors and those vendors in China, Indonesia, Vietnam ..

don’t want to lose Amazon, Nike and Walmart. Solutions will be found and

the inflation will normalized.

7) But next year, y/y, we might get negative rates, because the current

inflation is so high.

1) Car dealers operate like catalog houses, like Amazon. High turnover, low inventory. SKU #10001 for $37,598, SKU # 10023 for $39,754… delivery in three month.

When buyers are so hungry, dealers can reduce their inventory.

2) Use your hands instead of a brand new wash dishes machine next year.

3) Prices are high, let them fly. Every takeoff end up in landing. The choice of fly is yours.

4) Bloggers sell brides, cars, computers and other products, what’s the difference when buyers accept it.

5) Car dealers have more salesmen on the floor than brand new cars, and u have to make an appointment, – a dentist appointment, – to show how busy they are.

Americans seem to be so short sighted. I could see people paying up for big SUVs and trucks and then turning around and dumping them for a loss if gas goes up another 50%.

“2) Use your hands instead of a brand new wash dishes machine next year.”

M.E., I’ll pass this message along to my daughter. Thanks for being the “fall guy”.

1) Dealers have reduced their inventory because they can’t replace it. The dealer can only acquire what the factory produces or what they can purchase on the secondary market. Auto manufacturers will produce at full speed if they are able to. The average consumer thinks that dealers control their supply. They do not. They are at the mercy of the manufacturer.

2) Using hands wastes precious natural resources. You use much more water to hand wash dishes than you do by using a modern machine. Ours uses 3.5 gallons for all wash cycles, including sani-wash.

5) Salesmen are traditionally paid on commission, a low salary plus commission. Some dealerships who claim that the sales consultant is salaried are often telling a half truth. The “salary” also comes with performance “bonuses”. The low supply = high prices so both the dealership and staff can make a living. Pay plans reward volume and gross profit. If the dealer has not changed his pay plan to “mouse” the sales staff, they will all make bank during the periods of short supply as 25% of $5,000 is far better than a “mini-deal”. Odds are the appointments are needed because of a lack of salesman, not an over abundance. Fewer salesman, higher gross profits, higher commissions, and reasonable chance to achieve target bonuses.

I don’t see any charts from Wolf showing the explosion in the costs for routine medical expenses like the dental work I described above. Are they part of retail sales and if not why not. I just shelled out $20K for relatively routine preventative care.