Time to nominate some hawks to the Fed’s Board of Governors.

By Wolf Richter for WOLF STREET.

Amid the biggest and fastest boom in asset prices ever, thanks to the Fed’s radical money-printing and interest-rate repression, Americans’ mood about the economy has soured dramatically as their pocketbooks are getting hit by inflation.

This is now being documented in numerous ways, including by the University of Michigan Consumer Sentiment survey, which dropped to its lowest level in a decade, primarily due to inflation worries.

The surge in inflation is eating up wage gains, and some things have become horrendously more expensive in no time, such as some food items, new and used vehicles, and housing – those prices have risen far faster than the overall inflation indices.

Political polls too have been showing the souring mood and the inflation worries that led to the dissatisfaction with the economy. An ABC poll, released this weekend, was another whack-down for the government and for Democrats – driven by inflation worries.

OK, relying on polls conducted by landlines of 1001 Americans, including 882 registered voters, as this poll was, can lead to iffy predictions. But this has now been consistent in polling all around: People are frustrated with the economy, because they worry about how everything is getting much more expensive, and they’re blaming the government and politicians because that’s what they’re being asked about, and they’re not blaming the Fed, because the polls never ask about the Fed, and because many people don’t even understand what the Fed does and how it does it.

Of the respondents, 62% said that the Democrats were out of touch with the concerns of most Americans – and this is where inflation comes in. But Americans didn’t rate Republicans much better, with 58% considering them out of touch.

The economy was among the key factors – the Fed engineered economy with huge asset-price inflation and now massive consumer price inflation that is driving up costs for regular Americans: 70% said the economy is in bad shape, up from 58% in the spring.

About half blamed Biden directly for inflation. And his approval rating of handling the economy plunged to 39%. And 55% disapproved of how he handled the economy.

Biden doesn’t get to control prices. But he gets to nominate Fed governors. He gets to replace Fed Chair Powell and Fed Vice Chair Clarida early next year. If both step down entirely, he gets to fill four of the seven slots on the Fed’s Board of Governors, and he can install four inflation hawks and make a political deal with them to break the back of this inflation – more on that in a moment.

For people who make a living with their labor, rather than sitting on a pile of inflating assets, well, they now see the purchasing power of their labor get eaten up by soaring rents, soaring home prices, soaring food prices, soaring new and used-vehicle prices, soaring gasoline prices, soaring costs of health care….

The pay increase they got as a promotion for their hard work and productivity just made up for inflation. The 20% pay increase they got when they switched to a better job a few months ago is now getting eaten up by soaring costs.

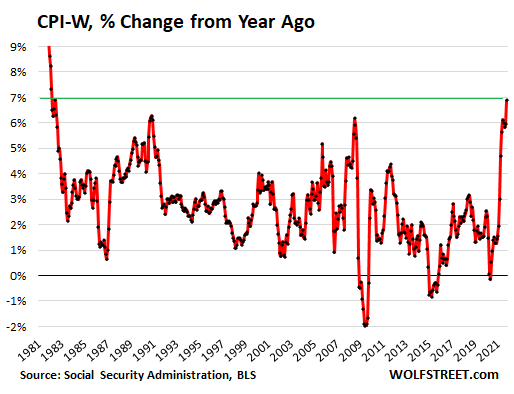

The broad Consumer Price Index (CPI-U) jumped by 6.2% year-over-year. And the Consumer Price Index for All Urban Wage Earners and Clerical Workers, the CPI-W spiked by 6.9%, the highest since June 1982:

The year 1982 was the Volcker era at the Fed. Nominated by President Carter in July 1979, about 17 months before the end of Carter’s Presidency, Volcker was then used by President Reagan to tame the inflation monster for 40 years.

The Fed started raising its policy rate, the federal funds rate, in 1977 from below 5% to over 10% in mid-1979. When Volcker started running the Fed, he raised rates further, triggering the first recession, which caused him to cut rates again. And that still didn’t vanquish the inflation monster, so he raised rates again to a peak of 20% in June 1981, which triggered the second recession, which did the job of breaking the back of the inflation monster.

Inflation headed down over the decades, triggering the biggest bond market rally and all kinds of other good things, and the Fed earned credibility that it can vanquish inflation, which itself helped keep inflation in check.

Now the Fed has unleashed that monster again. And it has destroyed its credibility that it can vanquish inflation because it doesn’t even want to vanquish inflation.

There is no easy way out; that moment has passed.

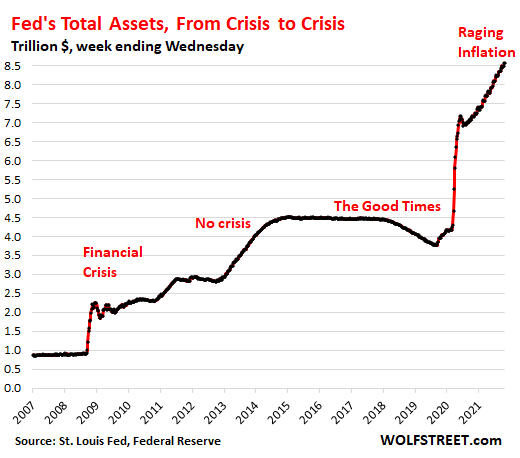

The Fed doesn’t need to raise short-term rates to 20%, as in the early 1980s. That would be nonsense. It has a huge balance sheet, as a result of this outrageous money printing, that it can unload instead.

The Fed could raise short-term policy rates to a modest 4% over the next 12 months, which would still be stimulative since that rate is below the rate of inflation, producing still negative “real” short-term rates.

And it could unload the $5 trillion in assets that it bought since September 2019 and bring its assets back down to the still huge level of September 2019 ($3.8 trillion). It could do so over the next 24 months, roughly equal to the average pace of QE since September 2019, only in reverse, thereby unloading about $210 billion every month. This would liberate long-term rates and allow them to float higher.

But instead, the Fed spent months denying the existence of inflation, defying what Americans saw every day in front of them, and then it spent months brushing off the issue by calling it “temporary.” And the government, idiotically, fell in line with that strategy.

The Fed is still repressing short-term interest rates to near-0% and it’s still printing money hand-over-fist to repress long-term interest rates. This week, it will start printing at a slightly slower rate of $105 billion a month instead of printing $120 billion a month, and it said it would stop printing altogether by June next year, I mean, wow.

But it has been an awesome period for the wealthy and the super-wealthy.

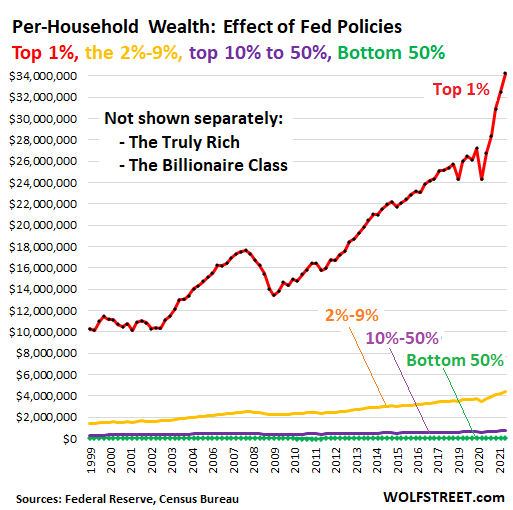

The Fed’s policies have created the best boom ever for the biggest asset holders, and thereby have created the biggest wealth disparity ever in the shortest amount of time, between the top 1% of households and the bottom 50% of households on the wealth scale, and even between the 1% and the bottom 99%, according to the Fed’s own data on household wealth, in line with its official dogma of the Wealth Effect.

The bottom 50% (green) hold nearly no assets because they don’t make enough money to put anything aside, and they got nothing from the asset price inflation. But they get to eat the higher housing costs. Even the top 10% to 50% (purple) have little compared to the 1% (red). And the truly rich (the 0.01%) and the billionaire class are totally off the chart:

Biden doesn’t get to set prices. But he gets to nominate Fed governors.

The current Fed is run by Republicans. The sole Democrat on the Fed’s Board of Governors, Lael Brainard, hasn’t been much better; while she frequently voted against loosening up banking regulations (kudos), she never voted against the monetary policy decisions that led to unleashing the biggest wealth disparity ever and the worst inflation in 40 years.

There are seven positions on the Board of Governors. When Trump left office, six were filled and one was vacant. And by early next year, four might be vacant:

- Powell’s term as Fed Chair expires in February. He, the engineer of all this, needs to be replaced, which may cause him to step down entirely, creating the second opening.

- Randal Quarles announced that he would step down, creating the third opening.

- Richard Clarida’s term as Vice Chair expires in January, and he needs to be replaced, which may cause him to step down entirely, creating a fourth opening.

And those four openings on the seven-member Board should be filled by hawks focused on making a political deal with the government to vanquish the inflation monster and to end the use of monetary policy — money printing and interest rate repression — to create ever bigger wealth inequality through asset-price inflation.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

If one could render a WS “in general position ” one position could be to point to the failure of Congress and its sole creation The Fed. The electorate’s responsibility has not been ignored . The keen eye must stay focused on the powerful. This has been the result not from an opinion but an ongoing stream of facts , with data and humanizing antidotal observations to bolster the rendering. I appreciate the hell out of this. I also appreciate the Kitty Lopez art on the Heck Mug every time I load it. I have a Black and Tan loaded in it as I speak. Cheers.

One way you know the Fed has printed too much money is gold price. At $1860 digging gold out of the ground (to provide an alternate to fiat) has a higher return than many industries making useful products. If gold gets to the $2250 level it will mean gross margins are 100% and will truly be a sign Fed has over done the money printing.

I don’t think your assessment is as clear cut as you say.

Gold mining requires enormous amounts of energy – and energy is expensive and getting more so.

That’s true, but I if understood him correctly the CEO of one of the top three said they probably can manage the cost increases to about 3% over the next 12 months.

@Old School

I wouldn’t take any CEO’s mouth movements as reliable.

One of the main reasons I am negative on investing in gold miners (besides not wanting to be in a scam stock market to start with), is that their business is really a derivatives one.

Which is to say – whatever their productivity on gold mining is, their actual performance is dictated by their execution on their hedging strategies.

Or put another way: a gold mine is much like a farm. You have to put up huge amounts of capital, time and risk and hope that prices of inputs (energy, land rights, political landscape for gold; fertilizer, weather for farmers) will be repaid, with profit, by outputs (gold prices, crop prices).

Farmers have been losing this battle for pretty much 100 years or so; why exactly does would anyone think gold mines are different?

What I’m saying is that the gold mining industry, like farming, is at the mercy of banksters.

Pass.

Stocks are 3.4 times long term price to sales average I believe so basically everything since 2000 bust is phantom wealth from Fed policy. It’s about ran it’s course.

Meanwhile, I suppose the ultra-wealthy 0.01 are borrowing from the Fed at (there’s that number again) 0.01% against their stocks and socking it away in a safe place? No problem for them when the markets bust because the Fed probably provides some sort of insurance for these loans or they will be forgiven.

You can be sure there is already a plan in place to protect the wealthy, no matter what happens. On down the food chain, it’s every man for himself.

If your net worth is several hundred million dollars (or more) you don’t need some kind of special government wealth protection. You’ve already got your six houses and 30 cars paid for, have no debt, and if your portfolio takes a 25% hit then it doesn’t affect your standard of living at all, and “it will come back eventually”. People with that kind of money have seen their wealth growing faster than they are spending it. Unless they decide to splash around on some kind of status-symbol yacht they can just ride out any market crashes. It really takes some incredibly wasteful lifestyles to outspend that kind of wealth.

The “Federal” Reserve was created through lies and misstatements to the American people and the US congress reportedly, albeit the Wikipedia entry that used to say that been “edited” (censored) to not say anything about this even politely. The “Creature from Jeckyl Island” and other reports that still have not been censored completely.

The “Fed” may be the creation of the devil, but it is only the creation of the congress if you can blame it for all evil things that it is fooled into doing via lies. The reckoning is now coming, maybe.

Jeffrey Lacker said interest rates will have to maybe rise to 3% to 4%. If that happens, how will the US government pay all of its bills and keep major programs like the US air force or army or Medicare financed? Remember that forcing the ultrarich to pay any significant taxes is verboten: a bare majority of the parties just removed it from the bills being considered. If the revenues of the government cannot be increased, and the interest payments on rolled over treasuries rise, because the “Fed” cannot keep printing US dollars to buy treasuries, either the US government will have to make DRASTIC cuts to its spending or taxes on the rest of us, who are not ultrarich, will have to go up to the sky.

Lets say interest rates do not rise until after the mid term elections. How bad of a crash are we looking at.

For most people the crash is already happening. Standards of living are in decline for most people since wages aren’t keeping up with inflation.

As for the financial assets that are only relevant to the top 10%: why not a Double crash like 2007-2009? Remember the market peaked in October 2007, and got serious about crashing in the fall of 2008 before the election, but didn’t take the final plunge until spring 2009.

Fed has made nearly everyone a better investor than Warren Buffett. People are starting to over estimate their financial decision making as the Fed has supported risk taking and operating on leverage.

I see it specifically in what people are paying for second home properties. If they were a genius they would have bought 3 or 4 years ago when price was 50 – 70% less. Fed over did it on the wealth affect.

I see the rampant greedy speculation too.

It’s no longer a “Wealth Effect”, now it’s a “Wealth Infection”…

Reminded of the famous quote that “nothing can save a people who are determined to suddenly grow rich”.

Biden will now start leaning on the Fed to fix this.

The only way Biden will lean on anything is if he falls asleep. Look at his record; he’s spent 40 years trying to guess the easy way out of a problem and usually he picks the worst possible COA.

Congress is the supposedly financial side of the USA gov’t, and they have failed the American people spectacularly.

The coming recession is going to be worldwide and ugly.

As Hussman likes to say in great depression stocks lost 2/3 of price and then lost another 2/3 because of policy error for a grand total of 89% loss.

Valuations are higher now and a lot of people think Fed is in the middle of a policy error. Anyone that is 35 years old has invested during 12 years when Fed was running loose policy 99% of time. They have not experienced normalization of policy or heaven forbid a tight money policy.

I am not sure modern central bankers believe in tight policy anymore. It seems like they have created a world where they are center of the universe.

One other comment. GE breaking up is the rationalization of a once great company.

The lesson is under Jack Welch they went all in on the debt financialization of the US economy and became the US most valuable company to being bankrupt and bailed out during GFC. It’s going to happen to a lot of big named companies and stock holders will become bagholders again.

Crash is not the word…

a rejection of unrealistic values and a return to normal more stable evaluations.

I’d say inflation is the main problem for the Democrats/Biden politically.

A failure to do anything about inflation will make an already bad Democrat rout into something historic.

So it isn’t clear that the Fed and/or the Biden government will continue Fed printing policies.

Let’s not forget that the Senator from MBNA is not an inflation hawk – the banksters who sponsored Biden for 4 decades want low interest rates.

But a failure to retain control in one or both parts of Congress is already on the table.

A new Fed policy would certainly put a hole in this bubble – with attendant likelihood of outright crash – that’s the other side of the equation.

Crash the markets or lose control of government?

Wolf,

Have you ever attended a “Fed Listens” event, during which FOMC officials supposedly listen to everyday Americans’ concerns – ranging from “small business owners, union members, and retirees” (according to their website) – regarding monetary policy?

In previous press conferences, Powell said panel participants were grateful & supportive of their focus on maximizing employment, even at the expense of higher inflation. Assuming he’s not lying, maybe our viewpoint is not adequately represented, and we need to show up at these events & make our voices heard? Or maybe it doesn’t matter at all, as Powell takes orders from Wall Street?

I have seen some reporting on those events where people aired their grievances about price increase, but those grievances didn’t seem to make it into the Fed’s own reporting of the events. Those grievances were reported before the current bout of inflation. People were complaining about the inflation back then that the Fed said wasn’t big enough.

There’s a number of moving parts to this, sources report Raise rates and dial back GDP we get the famous double dip recession, but that would close the wealth disparity gap. Powell is aligned with his boss, so as for (wage) inflation, let her rip. (Prices should take care of themselves) Fed should set a benchmark for raising rates, keyed to inflation, (modified Taylor rule). When El Arian said recently, the Fed’s mistake was not showing humility at the beginning of the process, that is what he probably meant.

Does anyone, including Wolf, really understand the consequences of off loading $5T in assets on the FEDs balance sheet. I certainly don’t. But why stop at $5T? Why not take it down to somewhere under $2.5?

So, I’m sure someone could explain what the different bond yields are of these treasuries owned by the FED. But, let’s look at what’s been purchased in the last two years. Most of this would be at very low rates. So if the FED waits at least two years, like it did from 2015-2017, after if finished QE, we’re talking summer 2024.

How high will yields on treasuries be? If they’re higher than what the FED is trying to sell, who’s going to buy these treasuries?

It seems like a reasonable question, doesn’t it?

The other possibility is that those attending want conflicting outcomes, primarily because they don’t understand monetary policy and economics, but maybe also because they want and believe in something for nothing.

They want the “stimulus” that comes from loose monetary but not the current inflation that comes with it.

Wikipedia censored its entry as to the creation of the “Federal” Reserve privately-owned, bankster cartel. Read the following in its reporting, mostly now censored, that remains as to that bankster cartel.

QUOTE:

Representative Louis T. McFadden, Chairman of the House Committee on Banking and Currency from 1920 to 1931, accused the Federal Reserve of deliberately causing the Great Depression. In several speeches … McFadden claimed that the Federal Reserve was run by Wall Street banks and their affiliated European banking houses. In one 1932 House speech…, he stated:

Mr. Chairman, we have in this country one of the most corrupt Institutions the world has ever known. I refer to the Federal Reserve Board and the Federal Reserve banks; . . . This evil institution has impoverished and ruined the people of the United States . . . through the corrupt practices of the moneyed vultures who control it.[

END QUOTE

At least we know that there was ONE courageous and honest politician who once served in the US congress. I have guessed that the others are either bought or maybe fear that videos of their abusing your girls taken by some rich, pedophile friend of theirs may be released if they do not do exactly what the banksters wish. I love Louis T. McFadden!

most people just blame the current administration I used to ask my students if they knew about the federal reserve. Just blank stares. I told them that the federal reserve will be responsible for lowering their standard of living. These kids are now adults. I wonder if they’ve figured it out yet!

Breamrod, in the group of a dozen or so retired friends I meet and have coffee with each morning, when I asked them as a group who can tell me what the FED is and what it’s role is, no one provided a coherent answer. Some folks had an idea, but clearly no one knew anything in detail. All inflation, etc, etc, blame went to the President and his cronies.

This retired group includes previous:

VP if HR at Anadarko Petroleum

VP operations at BJ Services

West point grad who retired as Full Colonel

Mailman

Concrete contractor

Civil Engineer

Mechanical engineer

Business owner – fast food outlets

Insurance salesman (2)

RE broker (still working PT)

IT professional

Most of these guys are over 60. Crazy, isn’t it?

I believe Biden has no awareness of the Fed and how it operates….

his TRILLIONS are the problem…but he doesnt craft that stuff….

the under currents are where the power is….almost always.

How could “Biden’s trillions” be the problem? They aren’t even legislation yet, and are years from being spent. How is that responsible for inflation?

Inflation takes time to build up. It’s the previous administration’s stimulus and the Fed’s actions that have to be most of the reason, and Biden’s bit from earlier in the year stacked on top of that. His BBB or other spending plans are what may drive future inflation.

Excellent observation, but i am not surprised, most people don’t know what fed is doing in detail and how monstrous this institution is.

Anthony A.

These so called retired friends main concern is making sure no one takes their chair at the coffee shop. They are totally out of touch with the real world. They wouldn’t survive one day in this cesspool that I have to work in every day.

No they haven’t. Go to the land of middle class white college kids (reddit) and mention the fed reserve. You get downvoted (basically censored) and people argue about how stupid you are and it’s all trumps fault/Biden’s fault etc. Nevermind the fact Powell was trumps boy who gave Trump a winning chance by pouring free money into the economy when it was about to crater from the pandemic.

When you mention the federal reserve, people’s eyes glaze over or they think you’re some conspiracy theorist loon. This is for all age groups in America. Good luck changing it. It is the donkeys vs the elephants. Go team!

Either way, there is absolutely no way in hell that any kind of hawkish sentiment will be seen at the fed. It would slow down Stonks and assets before the election. I have little faith the Dems will be able to keep any kind of political majority to begin with but a raise in monetary rates and a sharper taper will ship them off the island. Not gonna happen.

I honestly don’t see a scenario where the fed becomes hawkish until a major recession. And even at that, what’s to stop them pouring free money into the system again? Capitalism by it’s very nature is a boom and bust cycle like any kind of biology. It swells to the point of being unable to support itself and contracts. Then it swells again. They’re trying to have their cake and it eat too. I doubt it will work out for the little people. But they’ll always be rich so it doesn’t matter for them.

“Nevermind the fact Powell was trumps boy who gave Trump a winning chance by pouring free money into the economy”

Did you forget the 8 years of free money creation from 2009-2016?

And the rate hikes and reverse QE 2017-2019?

Capitalism doesn’t have central planners like the Fed – that’s crony capitalism and corporatism.

We’re talking about going forward. It is gonna be Powell or Brainard at the end of the day. Neither one seem likely to raise rates or weather a downturn. How does a rate hike when everything is going good or old QE from the GFC play into account here?

Things go bad, fed/.gov try and stop normal market corrections. Things go good, maybe they raise rates slightly. We’re headed and already in massive inflation and everyone is too timid to actually try and stop it because of the political fallout.

This is a political problem that isn’t limited to either side. What is your point? Or are you just trying to paint this all as democrats bad or Republicans bad? They’re both scum.

FOMC members aren’t robots existing in a vacuum. They aren’t immune to political pressure, negative press, and especially their peer social groups.

They also aren’t all powerful. Look at the stock markets in Japan and Euro zone. The Japanese Nikkei Dow is about 25% lower versus 1989 – in nominal terms – even after the even more insane QE under Abenomics.

Euro zone stock markets are mostly flat or barely higher versus 2007 or even 1999. ECB QE is at least as large if not larger than the FRB.

My point is that it’s not a mechanical outcome where QE automatically creates this fake wealth effect.

When collective psychology turns against FRB monetary policy whatever it is at the time, it will fail or be viewed as a failure, no matter what they do.

That will get them to change, whatever they are doing.

Well you’re forgetting the reason why were still weathering the storm so well is because we are the world reserve currency.

The mindset of Americans doesn’t sour towards the central bank anyways. It is blamed mostly on the president. Maybe Congress gets some poked and prods as well.

Nobody ever stops to say, “god life is so tough on minimum wage working at home Depot with no benefits and cut part time hours. It must be the corporations!”

No, they say it’s the damned president and the political party they’re affiliated with or whatever. It partly is because all that the US political system serves is the oligarchy but Democrats and Republicans are one in the same. It’s all a circus, they’re all in it to get rich and do the bidding of big business. The Fed just lies in plain sight running one of the major cogs of the machine.

Give Americans 1200 bucks Scot free and give trillions to big business and they look the other way while they get beaten by inflation. Everyone is the blame in the system.

My advice? Reject consumerism as much as you reasonably can, get the best benefits from a job, do no good or bad for your neighbor, keep as much money as you can hidden where it can’t be taken. If the game is rigged, best to not play it.

I’ll do just as fine living in a trailer and driving a 40 year old clunker as I would a 100k dollar pickup and having a 3 story brick mcmansion. Way better off having that difference in an IRA and 401k etc.

Yes, it’s strange why QE is so effective at inflating asset prices in US markets, but not so in Europe & Japan.

One factor that caused asset inflation, at least in the housing market, in USA is the removal of risk.

No other country gives out a 30 year fixed interest loan at 3% rate with only 3% down payment. A free market would rate that risk either with a floating rate or with a much higher fixed rate.

Income from rental properties can be written off too with many deductions.

Does ECB or Japan purchase MBS?

When there is very little downside risk and capital requirement is not too steep, prices will inflate.

Trucker,

Yep. Team Pepsi or Team Coke, either way it’s still the same old Corporate Cola salesmen in charge.

While Congressional seats aren’t openly available to the biggest corporate bidder (like in the City of London), Citizens United and the dark money channels available pretty much get the job done.

Us hippies did our best to get mindless consumerism rejected, but we hadn’t really thought things through well…..to say the least.

But the sheer number of boomer sellouts still amazes me.

“I used to ask my students if they knew about the federal reserve. Just blank stares.”

“Some folks had an idea, but clearly no one knew anything in detail.”

“When you mention the federal reserve, people’s eyes glaze over or they think you’re some conspiracy theorist loon.”

These videos available on DVDs (and YouTube) should be required viewing in mandatory high school economics classes:

Money as Debt I – Revised Edition

Money As Debt II

Actually, I think it’s far too late anyway even if it would be done, but it would be worth a try.

Congressional Record Volume 81 Part 3, 19 Mar 1937: It was Henry Ford who said, in substance, this: “It is perhaps well enough that the people of the Nation do not know or understand our banking and monetary system, for if they did I believe there would be a revolution before tomorrow morning.”

“I think people in power have a vested interest to oppose critical thinking. You see, if we don’t improve our understanding of critical thinking and develop it as kind of second nature, we are just suckers ready to be taken by the next charlatan who ambles along… there are lots of ways to gain power and money by deceiving people who are not skilled in critical thinking.” – Carl Sagan, noted cosmologist, in radio interview, May 1996

We can blame a voting idiocracy for getting us here, assuming one ignores the 2014 Princeton University study that showed that voting is pointless on anything other than a local level since only those policies desired by those actually in control (big money) win at state and national levels. If unpredicted, unexpected flukes occur, like Trump, the vast, unelected administrative state and their puppet media do everything possible to destroy and obstruct them… and succeed.

Basic math dictates no major rate increases over the next several years. Take $30T in debt at 2% ($600B in interest alone). Now take that same $30T at 6% ($1.8T in interest alone).

And who among us thing the debt will stay at its current $29T. That is the ultimate joke. Interest rates will never normalize until we have a complete collapse.

The billion dollar question (I know it used to be the 64,000 question) is WHEN.

Explain to them what a TRILLION is…

explain to them how there is now 30 on their backs

explain how the wealth of their future has been pulled forward by nefarious actions of a cabal that is running the Fed.

And ask the question of everyone..

“When did it become NOT incumbent of each generation to pay their bills?

I say it was about 2001……

A trillion is a stack on brand new $100 bills approximately 600 miles high.

You tube has many videos on how much a trillion is for visualization purposes. Basically the dollar, and your standard of living, unless you are already homeless, is F*!

I’d say 1980, just looking at the deficit spending and other nasty numbers, like incarceration. But the bookkeeping is only part of the problem (and would be much easier to solve for future humans).

Planet wasting either ends, or things get nasty for our species and many other more complex plants and animals.

My bet is still on the insect evolutionary line as far as complex animals go, although the single cell and virus (yeah, I know, there is debate over what is “alive”) bunch have been the ABSOLUTE complete winners, by numbers or biomass, ever since they started the game.

The Dems want to put the full SALT deduction (up to 80K) back into the tax code. This will be a big windfall to the wealthiest of the taxpayers especially in Blue states and do nothing to help the middle class or the working stiffs in flyover country. It will also create another inflationary spike in home prices making them even more un-affordable. Has Wolf mentioned this in his posts or did I miss something? Very few people know about this.

Very important point. Gotta grease the campaign-donation wheels before the 2022 contribution season starts up in earnest!

I don’t disagree with you but am left wondering what happened in 2001 that triggered this issue. I assume it was 9/11?

Swamp… It’s more complicated than that. SALT was dialed way back by Trump as part of the tradeoff for lower income tax rates (and, as you know, many argued it was to stick it to high-tax blue states). With rates now set to rise — and inflation pushing everyone up the income brackets and stealthily raising the effective rate paid — giving back some of the SALT deductibility makes some sense.

I agree with your point that it could further drive housing inflation. I disagree about the flyover country part — CA and NY significantly subsidize most of those states. I’m not saying subsidies should be eliminated (although that would be interesting), just that it is much more complicated than a single dimensional look at SALT as a boon to the rich. BTW, it’s really easy to hit the SALT cap in CA without being anything even close to rich. REALLY easy. Earn $100k and pay tax on a $800k dump and poof, you’re over it. Rich?

the red state being subsidized by blue states lie is really getting tiring

Gattopardo

The 2017 Tax bill distorted the housing market and created a housing shortage. I put this in a post about a year ago and will not repeat it. Let me say, constantly changing the tax code is not a good idea. It makes it impossible to properly plan your long term investment strategy. I think they should have left the tax code alone in 2017 (kept the SALT deduction) and just simplified it by eliminating all the needless complexity. They didn’t do that. I’ve been doing my own taxes, and for my businesses for many years and know more than most crooked accountants. I don’t like when politicians try to bull s$it me.

i’m seeing a lot of articles now on cnn, msnbc, and other mainstream news outlets talking about the fed’s monetary policy and printing. i agree with you that most people don’t know what’s going on, but from my vantage point, the tides are changing, and changing quickly.

They mostly mention the Fed’s mandate so far.. inflation will disappear soon, work wages are going up side by side as inflation, we are monitoring inflation, nothing to worry about, move along..

I recall all too well the first home I purchased in 1980 with a VA 30-year fixed rate mortgage. I thought I got a GREAT deal…paying 13%. Subsequently we’ve had two generations that have ZERO CLUE how ugly inflation can get…and FAST. For everybody’s sake I sincerely hope we get an ULTRA-HAWKISH Fed to help stem this…and NOW!! It’s rapidly getting out of control. The empirical evidence I see daily is stunning…prices rising like a rocket. And the White House, and the many Marxist-Communists in congress have NO CLUE how to abate it. America had better wake up!

Big,

You bet. I just sent this article to my son. Luckily he is locked in at I think 2.4%…..but he will soon understand why Dad is a no debt preacher.

The worry for isn’t whether or not B is a one term wonder, it is who will get in next? It’s pretty scary.

My older sister still thinks the economy is great and so is the current Govt. She lives in WA. No clue….none.

Thanks Wolf for such an informative and insightful take on things.

This is what I meant…just read it on Axios, but stopped at the teaser to keep my keyboard clean.

Economic pessimism is on the rise — despite the fact that the actual economy is doing exceptionally well.

Why it matters: The big question facing the White House between now and next year’s elections is whether it will be able to use America’s real-world economic health to boost President Biden’s economic approval ratings.

The people who say “actual economy doing well” aren’t living the life of the majority of workers.

For most people, inflation is eating up all the wage increases, so people are having to do without.

When standards of living are in decline, that’s just an irritation to those with strong incomes, but it’s a mortal threat to the vast majority.

Meanwhile the government isn’t doing much of anything intelligible (other than enriching the already-wealthy). But it sure knows how to mess up people’s lives.

The idiots are the citizens putting up with this and not seeing it for what it actually is…

Inflation has been achieved and continues onward as of today. What you are referencing (increasing interest rates and rising prices) are just the natural outcomes of monetary inflation.

If more people understood the basics of our monetary system we would not be in this disastrous position.

This is just getting started… where the everyday man on the street will soon see it very up close and personal.

Inflation = Inflating the “money” supply.

Increasing interest rates and prices = the consequences of inflating the “money” supply IE; more “money” competing for the same amount of goods and services. And in our current case less goods and services.

In my humble opinion, inflation is about done. We now just await the consequences of the accomplished inflation. Those consequences are just now trickling in soon and will soon turn into a tsunami.

“Time to nominate some hawks to the Fed’s Board of Governors.”

Perhaps reconsider Judy Shelton?

Why isn’t it time to consider just shutting down the Fed?

Harris sank Shelton’s nomination.

The vote was 48-48, which Mike Pence could have broken in her favor. Then Harris hurried back to the Senate in between campaign events to vote against Shelton, making it 48-49.

So Pence actions cost us a good appointment?

I get the impression that Fed is burdened with group think and no one outside the like minded club is going to be let in. I think the problem is the debt system is a house of cards built on confidence which can be lost at anytime. More debt…more instability and danger of a collapse.

Everything worked well in the days of the old west before any government existed.

Nonsense trt, just a tiny bit of reading of actual her and history will tell you that is not true.

Since you have read history, can you please tell if the financial bubbles were longer or shorter prior to the establishment of the Fed? System was self-correcting and the risk vs reward was balanced.

The Fed, with its easy money policies, credit expansions and removal of risks has created the biggest bubbles and bursts in history.

Yeah, all you had to do to start ranching or farming was kill off all the local Indians….and actually, the government gave you a LOT of help in doing that, so it existed.

Dumb post.

Nacho, your “question” has no meaning;

Not long after the First Great Awakening, the evangelists totally rejected Ricardo and other classic economists, as they preferred the narrative of natural human greed followed by divine intervention in the form of atonement and suffering. It later became known as the “business cycle”. Big business absolutely LOVED this mindset, and still does, to this very day.

Calvinism runs VERY deep in the American psyche…..sadly.

As Seneca said c 50 AD;

“Religion is obvious to the ignorant masses, foolish to the wise, and very useful to the rulers.

Keep dreaming Wolf.

Fed is already saying that raising rates can’t fix supply chains and transitory means not “short lived” according to Canadian central banker.

Given the clusterfuck we find ourselves in thanks to those geniuses, I expect the farce to continue.

Next coming in a store near you will be price controls.

You can’t taper a Ponzi scheme, this sucker is going up.

.

Supporting FED hawks is like supporting the killing of the economy and asking the current President to quit his job.

Because, that is exactly what Jimmy Carter did.

Housing costs? My mortgage has not changed one bit.

Inflation? How much of that is price gouging due to supply issues.

Capitalist economies respond to supply shortages by creating supply so they can profit more. That will happen.

Perhaps the inflation hysteria is a result of non stop inflation hysteria mongering?

They the FED had not hit the gas and instead we had depression level unemployment and shriveling businesses, would you blame them for that too?

FED used the tools they had to deal with the issues that presented themselves.

If the result was inadequate, we should research new tools.

Inflation ‘hysteria’ is because we’re all paying significantly more for all the necessities in life. SMH

AVRAAM Jack Dectis,

You’re truly confused. Good luck.

1) The CPI – W might cont to rise, but at lower and lower highs.

2) The gov hugged the radicals so oil can rise.

3) JP keep printing, guaranteeing NDX bull run.

4) NDX either a new backbone or possibly, – after a setup and a trigger – a deep dive under Sept high, for a sling shot Xmas rally.

5) Targets : 17,000 – 18,400.

6) Thereafter the deep freeze. 2022 Plunge #1, 2023 plunge #2.

7) What will the plungers do to the CPI- W and USD in 2024 ?

The thing is everyone is anticipating a year-end rally, followed by a some kind of correction in Q1 2022.

Often, markets behave contrary to what people expect.

Concur, correction might be imminent.

There is at least one record from tech bubble we haven’t broken and that is dividend yield on SP500 got 1.11%. We are currently at 1.27%. We might as well break all the records. It’s a once in a lifetime opportunity.

A bit apples to oranges due to shift in preferences from dividends towards share repurchases. Total capital return to shareholders is still substantially higher than in 2000.

Things are different, but the SP500 dividend yield is based on the reduced share count.

Hell would freeze over before Biden nominated hawks to the Board of Governors.

1) Before the November 2nd elections & the October CPI report, Biden and his inner circle didn’t even see inflation as a serious concern. His Chief of Staff, Ron Klain, retweeted that inflation was “a high class problem,” sparking outrage.

2) The ascendant progressive wing of the party would never allow it. They made an unholy alliance with Wall Street to support endless ZIRP & QE, because they need central banks to monetize their extravagant spending.

3) Democrats have doubled down on their messaging that supply chain disruptions are the root cause of this inflation, and not their overstimulation of the economy. To change course here would be admitting they screwed up.

Jackson Y,

One of the problems with your theory is that those folks are now seeing in front of them that they might not get reelected if this inflation thingy doesn’t get addressed promptly.

But the government can continue to borrow just fine, but it would have to be at higher interest rates. And that’s not a problem for the US government.

Concur, and may be you missed it Wolf, Biden just announced that his infrastructure program will fix the inflation problem….

Yes, he’s been saying that since the 6.2 reading came out. If the reading is 7.5% next year, with rents up 15%, good luck persuading Americans that sending federal money to ports will solve that problem, just in time for the midterms.

This is an infrastructure problem which another Neo-Liberal thrust will solve. Private industry isn’t meeting demand. Maybe it was the lost decade of mal- investment. This is really morning in America. Blow the doors off the deficit, send in a hawkish Fed to counter the inflation. We don’t need a massive military buildup because we are thoroughly militarized. This is like the end of the 70s, not the beginning. 39 and 45 have more in common than you think :)

“And that’s not a problem for the US government.”

I wouldn’t bet the farm on that last statement.

Unless Fed runs off most of balance sheet, $7 trillion or so of government debt has been monetized. Nobody knows how much is too much, but if you over do it confidence in the currency is lost and economy breaks down.

Government can confiscate most of society’s wealth because of their ultimate power, but if the economy implodes there isn’tuch to take and you end up like Venezuela.

I think a lot of young folks have this impression that since Trump and W didnt worry a lot about deficits that they dont have to either.

O post on 2010 had to think about the budget because the Rs opposed any and all spending.

the past is prelude.

Another thing regarding the Progressive wing of the Democratic Party is their embrace of Modern Monetary Theory, where, as I understand it, taxation, not interest rates, are the best tool to control inflation. This also aligns with their desire to not reduce or slow down spending, but increase it.

Even if the theory worked it has a political problem. A lot easier to vote for spending than taxes.

It’s just easier to let inflation do the dirty work and let people complain about rising prices. Plus business has to do the dirty work of charging customer more. Politicians get to be Santa Claus and not Scrooge.

Only crackpots believe in Modern Monetary Theory. It was just proven bunk by this last round of printing.

Keith-

Too many words for a good sound byte or bumper sticker. Maybe keep working on your mixed buzz words political messaging?

I do get the voting agenda, though.

The USA is one giant ponzi scheme, (along with many other countries), in which the FED has to print, it cannot stop, it is print or crash, and it will crash eventually in any case,though when is anyone’s guess, when the gold standard, imperfect as it was, was dropped, everyone on the planet became part of the ponzi scheme, that means you!, there was no longer any restraint to the creation of money, at least as long as we accept little squares of fiat paper or electronic digits as money, (maybe sea shells would have been better),the effects you see as regards the bottom 50% are simply the Cantillion effect, the FED and other CB are like children exploring, they are getting bolder and bolder the further they move away from any restraint, (gold standard), and the further in time from 1971.

The FED is comprised of people, just like you and I, and they have all the failings of people, just like you and I, ask yourself this, if you had the power to create money out of thin air at what point would you stop?, would you care about the consequences to to others?, people you didn’t know and never will, be honest, think about it, and now you know why we are all where we are.

ah… no… the federal reserve is a regional system serving as a banker’s bank … these are not people “just like you and I”

USA has a systemically-biased banking system. Decades went into its making.

[38 percent of the 8,039 commercial banks in the United States are members]

With a constitution that is constantly interpreted as fully supportive of guns for all, a party system that does not foster more than two, and a federal reserve cum central bank of commercial and national bank shareholders, the entire polity is very much one of ‘follow the money’ and solidly entrenched interests. It barely matters which party is in power. Everyone still has guns. The bankers still own the money mechanisms.

I don’t know what is bleaker, this system or the polluted planet.

Look on the bright side, people used to freak out about the ozone hole and that moved in the right direction. Ditto smog in some Cali regions. Please have a look at Bjorn Lomborg if you haven’t, he might cheer you up.

And by the way, even my uber-liberal semi-woke (only semi-woke, tax-brackets will do that to you) Googler friends are thinking of getting guns in preparation for civil unrest. Get ’em while they’re still legal.

You can always buy guns along the side of a road in West Virginia in a roadside flea market. No paperwork needed.

LW, et al,

Sometimes the screen writers come up with a good one.

From the Matrix Trilogy;

“Hope, simultaneously your greatest weakness and greatest strength”

Or you can use the WS mug version.

Dishonest money rors the system from top to bottom. I remember when I was a child and my mother drilled in my head about how wrong it was to steal and money seemed as hard and defined as the silver dime I would get from time to time

Now money has some kind of mushy value and morals about money have gotten sort of mushy too.

One thing is surely true, money in a small town was precious in the sixties, but it gushes to everyone now it seems.

Little bitty participation trophies flying everywhere at the speed of Ethernet….

Or the USMail….

You don’t need to play all kind of money tricks in a healthy economy. History teaches that funny money starts when the economy isn’t cutting it in funding government spending.

But isn’t the entire consumer economy, not just in the US but globally, completely dependent on low interest rates? So much so that raising interest rates would crush the economy (and not just the stock market)? Am I missing something here?

thethirdgate,

What you’re missing is that the consumer economy was just fine and healthier at higher interest rates. Higher rates mean higher income for bond holders ($50 trillion) and for savers ($11 trillion), that they would pay taxes on, and part of that income would get recycled in the economy. Higher interest rates can do a lot of good.

I think I’ve read a few comments over the years about the “Savers” getting punished on your site…

I would be one of them.

We’re still trying to guess when it will end.

Gosh, if they want to pay me 3 or even 4 percent on my savings (hey, it’s my fantasy!). I would be more than happy to do my patriotic duty and velocitize it back into the economy.

Last go round savers got up to about 3% nominal on 5 year safe investment. We will be lucky to get 2% nominal at top of cycle this time

Too much debt for economy to handle any higher I think.

Higher normal rates can do a lot of good in a healthy economy. This economy is malfunctioning and Federal debt service will be or is already at 30% of budget.

The next FED governors will have to promise Joe they won’t raise rates in the next 3 years.

‘What you’re missing is that the consumer economy was just fine and healthier at higher interest rates.’

And the heroin addict was healthier before he became addicted.

The good news for him is that cold turkey only lasts a week.

It’s going to be 2 years for this economy. It is too overextended.

This economy has been getting more and more addicted to lower and lower interest rates since Greenspan. They didn’t always go straight down, but the ‘Fed Put’ has become part of the psyche.

On CNN last night, one economist said: ‘there is no cure for embedded inflation but a deep recession’

No doubt those on fixed income will welcome this but the rest won’t. About half the investment grade bonds in the US are rated one notch above junk. These companies may be zombies but they employ a lot of people.

About moving the Fed Policy Rate from current .25 to 4 % in a year.

Does this mean other rates like 10 yr and all loans rise as much?

If so, look out below. I am no expert but I don’t think the increase in interest on savings accounts will do much to alleviate the shock. The retirees won’t spend it. Savers save.

The fed’s job is to to serve those they’re charged with protecting – the wealthy and powerful who buy and own politicians and lawmakers.

There is nothing new or party-related about this. It is how our system works. It’s called capitalism.

Unfortunately, Fed hawks are extinct. Last one of the species was Paul Adolph Volker 1927-2019).

How do you guys think this all plays out? Headline 1-year CPI readings are likely to approach or exceed 7% before the next chance (spring 2022) when readings can start coming down due to base effects.

Scenario 1: Federal funds futures are pricing in multiple rate increases in 2022. If Powell & Co., oblige, they’ll have to announce taper acceleration ($15 to $20B/month?) at the December or January meetings, then start preparing the markets for a rate increase shortly after.

Scenario 2: Powell & Co largely stay the course, sticking with $15B/month, and buying time till July 2022, no matter how high inflation gets.

Scenario 3: Powell goes full-blown Arthur Burns to please Wall Street, keep asset prices elevated & preserve his own $50M+ fortune, including moving the goalposts (eg PCE target from 2% to 3%?) and outright refusing to raise rates because “rate hikes won’t resolve supply chain bottlenecks.”

A recession that isn’t allowed to fully correct itself….

If i had a say i would vote for moving the target inflation to 3%, mostly “staying the course” on QE thru June while simultaneously using creative means to reduce liquidity.

Let mortgage/long term rates go back up to 4%, but keep them from going above 5% right away.

Going to 4% would still be plenty shocking-

No way would I be for moving target to 3%. You are just subsidizing people that already have fixed rate mortgages at and companies that have fixed rate debt. Don’t give a gift to the over indebted.

If i had a say i would vote for moving the target inflation to 3%, mostly “staying the course” on QE thru June while simultaneously using creative means to reduce liquidity.

Let mortgage/long term rates go back up to 4%, but keep them from going above 5% right away.

Prices are behaving strangely indeed. 250 feet of Romex is now $144 at HD up from $42 last year. But I locked in 3 newer phones at $40 less per month with ATT. Same plan as before and includes the cost of the phones. I get that inflation is insidious. But I feel the commodity bump will abate at least a little. Remember 2009 when commodities started to boom ? Some of that is happening again. So maybe that Romex will go down to $75. I hope so otherwise the wiring will have to wait.

TKita,

I don’t think the iPhone models got any cheaper.

What we’re seeing now is that one commodity item goes down (such as lumber) and one or two others go up. Whack-a-mole. And now rents are shooting higher and house prices have shot higher… and all this can settle down with higher interest rates, but they won’t if the Fed keeps printing money and repressing interest rates.

Oh, and I forgot the corporate sector. I remember a piece in the FT some months ago in which the consequences of rising yields for the junk bond market were called “cataclysmic”.

“cataclysmic” for whom? Junk bond investors that bought during the junk-bond bubble and stock holders of those companies.

Those issues need to be resolved in bankruptcy court. That’s what it is for. It’s called debt restructuring. Some investors will lose their shirts, fine. They got paid to take those risks. The company emerges from bankruptcy with much less debt, and can operate and expand with much more energy.

They didn’t seem to mind the “cataclysmic” effect of Powell dropping interest rates 150 basis points in one swoop on savers, pension funds, and others although current bond holders of the time were no doubt dancing all over their capital gains from it.

and without any explanation as to why covid necessitated those actions.

1) House hold wealth, the top 1% : 2020 one dot down, a round trip to 2018 low. That’s all.

2007/ 2009 : 7 dots, deeper decline.

2) Trump & JP saved NDX & RE. Otherwise, RE & NDX might have kissed the 2007 high.

3) The plunge didn’t happened in 2020, because of the flush flood of stimmie and ppp loans to the lower & mid class.

4) Few millennial between 23 – 38 belong to the top 1%. Many minorities, males & females, with fantastic skills, surfing on NDX & Crypto, thanks to JP.

5) instead of shooting bad guys online, they shoot Target Bar.

Could someone explain how it is that Fed asset purchases and setting interest rates are two separate issues?

I would imagine that adding/removing Treasuries or MBS would change the amount of cash in the banking system and thus impact the inter-bank lending rate (“Federal Funds Effective Rate”). However, many articles and also comments in this thread treat tapering and interest rates as somehow managed separately – along the lines of “the Fed will taper and then eventually raise interest rates”.

You need to read about your Federal Reserve system to understand that these are two separate tools in the kit.

Don’t be lazy, now. Go read. Learn. Be prepared for what is coming.

The Fed sets it short-term policy rates, which impact short-term market rates, but they may not have much influence on long-term rates. The Fed manipulates long-term rates by buy buying those bonds, which creates demand for those bonds and pushes up prices (which means yields go down). A big part of that manipulation is through jawboning, or “forward guidance,” as the Fed calls it.

Thanks. I didn’t want to “go read” either. Nice and concise. I may have even learned that here before and forgot. It goes into the WS folder for sure.

And as a 74 year old with a totally trashed back in a 500 sq ft low income apt complex, I don’t need to “get prepared” for jack S.

When quality of life drops to an unacceptable level (like before it’s care home or hospital time), I’m gone.

Do you really think Biden will elect Hawk’s to the Federal Reserve?

Quarles was a hawk and he is gone.

Lael Brainard is the leading candidate for the head of the Fed and she is going to pump money like noone’s business. She is one of those crazy, stupid gals (like AOC and her bunch) who think the government is our sugar daddy. Brainard has spent recent years cozying up to the Progressive wing of the party that is truly delusional about government spending.

Quarles was no hawk. He voted for every rate cut since assuming office in 2018, and he voted for every QE decision.

Agreed, Quarles was no hawk, but compaired with Brainard, who if appointed will be like putting Count Dracula in charge of your blood bank, he is less bad. Name one conservative that our dear leader appointed so far in his administration. I’ve got the answer. Zeeeeeeeeeeeeeeeeeero.

More like putting Count Chocula in charge.

You never know. Sometimes history does strange things. Biden might put Brainard in and circumstances force her to fight inflation. She might have no choice but to try to slay the inflation monster.

Wolf, I think when it’s over with I’m gonna call it the funeral reserve and it will be gone because trust will be gone.

The Federal Reserve is a trust for big banks and their friends.

They don’t care about us and the rest of population.

I wonder if there might be a very easy answer to why the Fed does pump out “money” and thus inflating equities:

Retirement funds.

What would they look like if the value of equities weren’t pumped up the way that has been done for years now ?

And what would a modest hike in rates cause for these very same funds ?

Retirement funds will suffer a hit when the Fed quits propping up the markets, but then they will be able to buy stocks for less money. Imagine how much worse that hit might be if the Fed continues propping up the markets for another 10 to 20 years.

Realist,

There are $10 trillion in savings at banks and credit unions and $50 trillion in bonds. Savers (many retirees) would benefit right away from higher interest rates, and bond holders would benefit when they buy new bonds.

The bottom 50% own nearly no stocks, and top 10% own most of the stocks. But you don’t need to worry about the top 10% in terms of the economy. Their spending is little impacted by their 401ks.

Higher interest rates have lots of winners — people that have gotten beaten have to death financially by the interest rate repression.

they use raising some middle class person’s 401k from $44 thousand to $68 thousand as justification, when its really raising the guy with $50 million to $78 million. most benefits go to the wealthy.

Apples and oranges. Both saw the same 55% gain. One just started out with a larger initial balance.

steve, obviously. that isn’t my point

Yep, and I’m one of the casualties of the low interest rate policy. Getting ready to roll over a CD with my local credit union. The yield will now be 37 basis points. And to top it off I will have that income reported to the IRS so I will net about 20 basis points. With inflation running 15 to 20% I’m getting killed. That’s one reason I’m still in the workforce when I should be retired.

Cash is very valuable. Last data I saw that running a portfolio of 90% stocks / 10% t-bills gave a better long term return than running 100% stocks. Cash gives you the opportunity to pick up bargains in panics.

Correction. New bond holders would get a bump in their RoR. Existing Bond holder (those $50B) will get killed as the value of their holdings drops against each rate hike.

Retirement accounts heavy in Stocks and Bonds will not do so well as those heavy in cash.

Timing this correction will be a bitch.

Excellent, and dead on.

This bad on so many fronts…

It is bad for society

It is bad that savers are punished in the United States of America…intentionally

But let’s look at Senator Sherrod Brown (D OH), for he is a perfect example of what is wrong with the system.

He is the head of the Senate Banking Committee which is allegedly the oversight connection between Congress and the Fed.

In this massive spending bill just shoved through the House, there is a provision for big chunks of money to move to the State of Ohio ..

“The final bill, the Infrastructure Investment and Jobs Act, passed with several key provisions Brown secured for Ohio communities. As the Chairman of a key committee on infrastructure legislation, Brown delivered big investments for Ohio. ….Brown’s Bridge Investment Act, which will provide $12.5 billion in funding to repair and replace nationally and regionally significant bridges, like the Brent Spence Bridge in Ohio—part of the Infrastructure Investment and Jobs Act’s historic investment. The package also provides Ohio $9.8 billion of formula funding to repair, replace, and upgrade roads and bridges throughout the state.”

And his committee oversees the Fed which is the well spring of the near free money to the federal government. Need I say more?

Historicus:

“It is bad that savers are punished in the United States of America…”

Hence, Bitcoin? I have noticed that in my local grocery stores the previous turn-your-coins-into-dollar machines have been replaced by turn-your-coins-into-Bitcoin machines. Seriously. Crazy sauce!

Noticed this myself. I usually spend the money right away on food in the store with the Coinstar machine.

I save my coins all year to dump in the red pots this time of year.

I noticed in my local grocery store the 50ish year old cashier trading crypto on her phone between customers.

Gotcha beat on that one….

My dumber than a box of rocks daughter sent me a text asking me if I thought she should get into forex trading…. She thought it looked like fun and could make some money…

Sadly I just shook my head and wondered where I went wrong…

From what I understand the Robinhood app is designed like a gaming widget, complete with rewarding sounds and video game like visuals. Indoctrinating the young to gamble on Wall St. The financialization of everything has destroyed the USA.

The problem with hyper financialization is that currency aka debt becomes detached from underlying value. Fiat money is free therefore guaranteed to go zero.

The business of America has become getting rich quick from speculation. Best pandemic ever.

Who knew that for the first time in history, the Fed would not fight inflation? Who got that guarantee and had the bravery to lock down long in stocks and real estate when history would suggest brisk and determined action to tamp down the inflation would cause prompt rate hikes?

The similarities with the inflation now and that of the 70’s can stop with one observation…

In the 70’s we had a Fed that FOUGHT inflation

Today, we have a Fed that PROMOTES inflation, and when running hot, does essentially NOTHING.

Who HIJACKED THE FED? For they do not answer to their mandates, but to a different drummer. And who might that be? Who is in the Fed’s “tent”?

Historicus, you need to reread your history. Get yourself a really good look – ideally with some graphs – at historical inflation, oil prices, food prices, and interest rates.

The Fed was late, late, late in seriously “fighting” inflation from its onset in the late 1960s until about 1977.

Lyndon Johnson literally bulllied Fed chairs into keeping policy easy. Nixon dumped the Gold Standard with Fed cheerleading. Arthur Burns delivered an extremely important speech to Paul Volcker – at a Central Bankers confab in totalitarian Yugoslavia of all places – explaining that to stop inflation was beyond the Fed and required a unified political will.

Right now the political willpower isn’t there.

I’d love to see Wolf’s Sunday Fantasy (4 new hawkish Feds) come true, but I just don’t see it happening.

It wasn’t meant to be a fantasy, and wasn’t phrased as a fantasy, but something he SHOULD do, a policy recommendation, if you will, for political survival.

WIsdom.

You didnt make it clear what I had incorrect.

First, The Fed FOUGHT inflation in the 70s…..maybe you werent there, I was.

WIN buttons and prime rates going up sometimes 1/2pt at a crack….

Second, This Fed PROMOTES inflation, and both those statements are undeniable. School somebody else.

Sorry for being provocative, we agree 100% that the Fed NEEDS to fight inflation ASAP.

What got me going was that you’re repeating a false meme that needs to die. I keep hearing people claiming that inflation isn’t that bad, that savings will keep up with inflation because “interest rates will rise”, that stocks will keep up with inflation, yada yada. It’s all wrong.

I lived through the 1970s too, but I wasn’t all that economically aware back then, and more importantly I don’t trust my memory or the mainstream

mythologynarrative. So I went and looked at the actual historical data.You can take a look at, say, the 3-month Treasury interest rate, and then subtract off the inflation rate. The data for this is all online at fred.stlouisfed.org and goes back to the 1940s. (In FRED-speak, I graphed TB3MS, CPIAUCSL and the difference between them.)

The data shows that the inflation crossed above 5% in 1969, long before the “fight began”. Oh, there was talk about fighting inflation, there were some half-baked policy responses – including WIN buttons and small rate hikes and idiotic wage & price controls that didn’t work – but there was no effective action until ~1980. Inflation ran 5-15%/year almost the entire time from 1969-1982.

Historically, per the data, the Treasury rate was 1-3% above the inflation rate for all of the 1960s. Savers were rewarded. But it went downhill through the early 1970s. And from 1973-1981 the Treasury rate was BELOW the inflation rate. During the 1970s the Fed’s rate changes DID NOT keep up with inflation. Because there was no political will to pay the price that had to be paid to beat inflation. We face that same problem today.

I’ll grant you that the 1965-1980 Fed did typically raise interest rates alongside inflation – which is more than they’re doing now – but they didn’t actually stop the inflation, particularly during the 1973-1975 recession. The supposedly all-powerful Fed clearly didn’t “fight” inflation in a serious way, because inflation refused to die. Inflation ran above 5%/year almost the entire time from 1969-1982.

Treasury investors at the time didn’t call that “fighting” inflation so much as “losing”. Longer-term treasury bonds were known colloquially as “certificates of confiscation”. (Which they are again today…) Treasury investors lost out to inflation in the 1970s and didn’t get “their money back” until the mid-1980s.

The Fed didn’t really get serious about “fighting” inflation until 1980. Once the Fed got serious, they drove the Treasury rate back to 3-6% more than inflation. To match that today we would need 9% interest rates.

For anyone who wants to see for themself, here’s the URL for the graph I made: fred.stlouisfed.org/graph/?g=IWcP

They want to reduce inflation but they are no longer able to. They can’t raise rates like Volcker did because today’s much higher debt/GDP ratio means that higher rates would lead to unserviceable interest payments, and would destroy the economy.

They can’t stop printing because otherwise they can’t pay their obligations like SS/Medicare.

It’s simple math. They know they are in an unwinnable position.

I saw something that said market is predicting highest Fed funds rate can get is 1.35% before economy rolls over. Financial repression the rest of my life most likely.

If NDX plunge for a sling shot, it’s an opportunity to buy infra

stocks.

“they’re not blaming the Fed, because the polls never ask about the Fed, and because many people don’t even understand what the Fed does and how it does it…”

As usual, Wolf nails it.

Bingo!

Mi/Wolf-so true, as most polls questions are usually ‘pushed’, as in a ‘yes/no’ with no nuance or third/fourth/fifth…responses available. Confirmation bias is baked in.

i began to seriously worry about about the average citizen’s understanding of our system of government over twenty years ago. Discussions with muttering customers about civic issues across the retail counter revealed a couple of generalizations:

1) no knowledge/understanding/embrace of the separation of powers of coequal branches of government, or what their missions and responsibilities are.

2) pursuant to (1), a shocking number couldn’t name their Congressional (or state/county, for that matter) representatives, dismissing ‘offyear’ (non-presidential) elections as ‘unimportant’, leading to…

3) an impassioned statement that they ‘always voted in the presidential elections’, further discussion indicating to me that many have come, or always have, interpreted the U.S. presidency as one of a supreme elected king/queenship. (Sidebar-a recent phenomenon when contrasted with my family’s elders, who came of age and lived mostly before our current levels of mass communications/entertainment. i often wonder if the nearly four generations of preschoolers who may have been placed ‘safely’ in front of Disney or similar animated entertainments, the systems of government depicted usually that of royalty, hasn’t had some sort of effect on adult worldviews…).

Throw the Fed (among many other features/bugs of our current operating system) on top of the Jeffersonian paraphrase of ‘in a democracy the people get the government they deserve’, little wonder at why we are now contemplating a massive block of very hard cheese…

may we all find a better day.

You’re basically describing why the universal franchise should be abolished, yet probably 99%+ support it. It’s a modern religion.

A noticeable minority if not majority of the population can’t or can barely manage their own life and it’s hardly just due to a (supposed) lack of money.

They have no business having any input into anyone else’s life.

i’ve made that argument to a very close circle of friends and family for years, but i keep it hidden because it’s not socially acceptable. even most “conservatives” think of universal franchise as a religion.

Winds will change if Fed makes a policy mistake. Congress might be forced to rewrite their mandate to keep them from going off the rails for a few decades. Might make them follow Taylor rule to keep them from doing extra ordinary policy.

Of course, no one would dream of faulting tax cut driven deficits for inflation!

Taper : $1T instead of $1.2T in ten month is good enough.

Before someone says

“We just can’t raise rates”

May I ask,

How can the Cause (low interest rates) of massive debt creation ALSO be the SOLUTION?

The low rates subsidize debt creation, and to continue that subsidization is nuts. Rates must be raised, and for those who missed the last 50 years of Fed reaction to inflation, the Fed had fed funds equal to or IN EXCESS of inflation.,,,until 2009

Realize that we’re being Sold To.

Who benefits from Low Interest Rates, and inflation, and why? That’s how you know why that’s being Sold to you.

The Sale is not about logic; the true logic which cannot be spoken is “sell the people on low rates and let the inflation run as long as possible, so we can benefit from them”.

All other information is being twisted to make the Sale.

For some making the Sale, the “benefit” is merely the avoidance of the painful and politically fraught rebalancing that will take place when the bubble finally pops and the losses get assigned. It matters a great deal who’s in the Seats of Power when the losses get assigned…

This demonstrates how the Fed is completely off its normal course.

https://journal.firsttuesday.us/wp-content/uploads/Inflation-Fed-funds-rate.png

Yep, and has been since 2008!

Funny thing is how people try to claim this is okay because when interest rates are below inflation it makes the federal debt “more affordable”. But the Federal Debt has done nothing but GROW as a share of GDP. It ain’t getting more affordable!

The Dem’s should have seen this coming and not tried so hard, and pulled out all the stops to win the presidential election. This period of time with Covid winding down and the hangover from its effects hitting hard the party in power was bound to get tarred and feathered. If Trump was still in office and the republicans were in power their party would probably have been cast in to the wilderness and set adrift on an ice floe. But now with Joe and his crew getting the blame for inflation as well as the supply chain collapse, it is probably likely that the Dems will be the ones joining the Whig party in the dustbin of history.

Seneca-had the same sentiments upon President Obama’s election….

Once again demonstrating the decline of broadbased long-term views, public or private.

may we all find a better day

FED is a cornered rat, that has no good way out

The public now has a less favorable view of the administration.

Concurrently, I am very confident they are still in favor of the programs in the infrastructure bill and the one with all the pork and welfare spending mischaracterized as “investment”.

Typo: 20% pay increase from switching jobs?

The billionaires are happy.

At a party last night one of the younger ones crowed how his house had doubled in price since last year.

My guess continues to be that hyperinflation is in the cards yet to be dealt.

B

I’m one of the few lucky souls who is not affected by this runaway inflation. Other than medical expenses I’m no seeing any significant rise in the price of necessities that I buy so far. I’m on a buyer’s strike. I refuse to purchase anything unless I absolutely need it. Buy most of my clothes at Thrift stores. They have plenty of them around here. Haven’t been to a mall in the last 4 years. Another example food inflation has not hit fresh produce and seafood. I’m boycotting red meat, frozen food and junk food. Own two old cars, use only one for personal use. Gas could go to $6 or $7 a gallon and it wouldn’t affect my standard of living. I could care less. Most of my car expenses are business deductions.

Good for you!!!

went to a coin show today. The dealers I know are telling me that gold and silver bullion is flying off the shelves. Premiums are higher than I’ve ever seen. This is either a top or the lid is about to blow.

It’s the start. Expect AU to at least double in 2022 and AG to break triple digits. It’s almost a foregone conclusion.

Things have changed in the last month or two as people realize inflation is running hot and Fed and people in DC don’t seem to care. I mean give me a break, politicians trying to get through more spending with inflation running close to 10%. Fed still monetizing. Something is fishy.

Great post Wolf. I had not considered even a single little bit the impact of inflation on the appointment of Hawks or Doves to the Fed… and I certainly didn’t know that Biden could replace the majority of the Fed Board of Governors next year.

FED (the bankers) primarily benefit the ultra-rich. Everyone else gets crushed by inflation and loss of purchasing power. Why the people of the USA have allowed a criminal banking cartel to manage it’s monetary policy since 1913 has always been a mystery to me. The FED has failed miserably with their dual mandate with one bubble after another, but done exceptionally well with their unwritten mandate to transfer wealth from the low and middle class to the 1%. End the FED. It’s time.

I just do not understand how the complete incompetent fools at the un-elected FED ever thought that their blatant reckless experimentation with peoples lives and their design to re-shape society should ever have been allowed to happen and that they would get away with this without serious punishment. TBH , I think its too late and also Biden is never going to appoint hawks (that’s a dream Wolf)

Carter appointed a hawk (Volcker).

Did not know this.

“Carter appointed a hawk (Volcker).”

That was one of Carter’s finest hours. I respect him for that.

Reagan’s had his finest hour too. That was when he fired the Air Traffic Controllers for walking off the job. After that labor strikes went to zero.

If Ohio is 3.5% of national population, it should get 3.5% of $1T infrastructure money, which is $35B. So, $23B for road work does not seem disproportional.

The post above, was for a post from historicus above, it got changed to a general post, don’t know why.

Semantic political bummer for them that

“Inflation” easily appends to the end of Biden, and that “presh” slips into his name as well.

Bidenflation leads to Bidenpression.