This may be the most distorted and perverse housing market ever.

By Wolf Richter for WOLF STREET.

This is a world of unprecedented Fed intervention, government stimulus, inflation that has turned red-hot this year amid a weird phenomenon of companies complaining about a labor shortage, while nearly 10 million people are deemed “unemployed” and 16 million people are claiming some sort of unemployment insurance. As 2.1 million mortgages are still in forbearance programs, investors have flooded the housing market, including individual buyers grabbing a second home in crazy bidding wars.

But sales have sagged for the third month in a row, while new listings and supply have started to rise from very low levels, and a lot more is coming on the market this year.

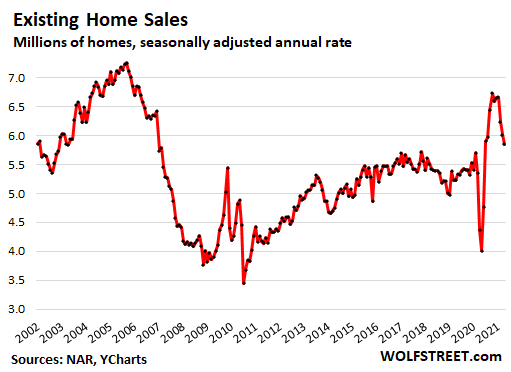

Sales of existing homes – single-family houses, condos, and co-ops – dropped by 2.7% in April from March, after the 3.7% drop in March, and the 6.3% drop in February, to a seasonally adjusted annual rate of 5.85 million homes, the lowest since July 2020, according to the National Association of Realtors today. Compared to April 2019, sales were up 11.8%, having now largely unwound the huge spike that started last summer (historic data via YCharts):

Investors are buying.

All-cash sales, usually a sign of investor activity, accounted for 25% of all transactions in April, up from 15% in April 2020. Individual investors and second-home buyers accounted for 17% of total home sales, up from 10% in April 2020.

Dallas Fed President Robert Kaplan pointed at the role of these investors in distorting the housing market, and named that as one of the reasons for “talking sooner rather than later” about tapering QE.

“Increasingly over the last 6-8 weeks, I’m hearing more and more widespread reports of private investors entering the single-family housing market, competing with families, often making bids above the asking price and requesting that the house remain furnished,” Kaplan said.

“So, we’re in a position where families are being crowded out, or squeezed out, of being able to buy the first home,” he said. “This is an example of an excess, maybe an unintended consequence, a side effect of these extraordinary [monetary policy] actions.”

Buyers’ strike by non-investors in the works? While individual homebuyers are still battling it out with investors in silly and costly bidding wars offering crazy amounts over asking price, there are anecdotal indications that more and more buyers are now staying away from this zoo because they’re exhausted or have reached the end of their financial capabilities or don’t want to end up buying at the most insane peak of the market. For buyers, this is a terrible time to buy a home. And that is becoming increasingly obvious.

For sellers, however, this is absolutely the best time to sell a home.

And sellers are getting ready, more inventory coming.

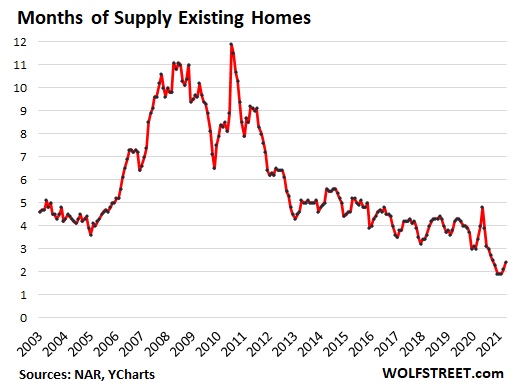

Inventory of homes listed for sale rose for the third month in a row, to 1.16 million homes, still historically low, but the highest since November. And supply rose to 2.4 months at the current rate of sales, the highest since October (data via YCharts):

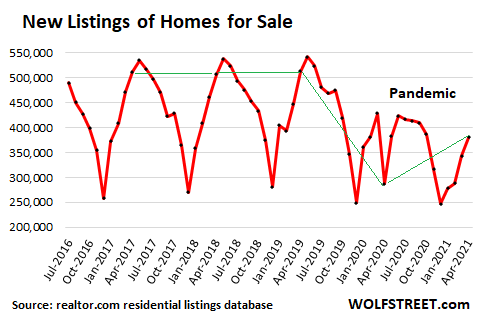

New listings of homes for sale are rising from the Pandemic-related drop. According to the realtor.com residential listings database, new listings in April rose 10.9% from March, after jumping by 19% in March from February, and were up 33% from the Pandemic low in April 2020. Despite the rise, new listings remain far below the seasonally normal levels (Aprils connected by green line):

Pent-up sellers. A lot more inventory is coming on the market this year: 10% of homeowners plan to sell their home over the next 12 months, which is 25% higher than the typical share of homes that come to market in a typical year, according to the NAR and Harris Poll in an earlier report, citing their survey of potential home sellers across the US.

Of these potential home sellers, 56% plan to list their home over the next 6 months. And 76% have taken steps to start listing their home.

When vacant homes come on the market, such as the homes that homeowners didn’t sell last year when they bought a new home (the infamous “second home”), it adds supply without adding demand because those homeowners are already living in their new home and don’t need to buy another one.

Buying a home without selling the now vacant home has contributed to the inventory shortage. When these left-behind vacant homes come on the market, it unwinds that shortage. This is the process of shadow inventory becoming real inventory.

Crazy-spiking prices.

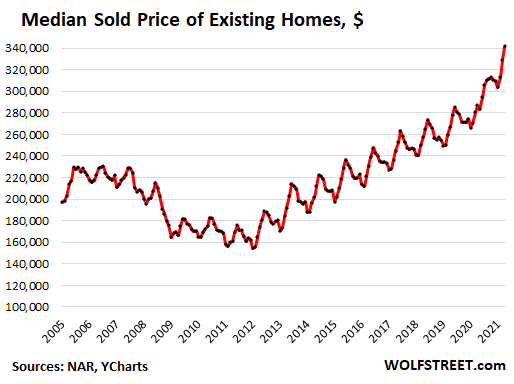

The median price for existing homes spiked by 19.1% year-over-year to $341,600, which is up 48% from five years ago in April 2016.

For single-family houses, the median price spiked by 20.3% year-over-year to $347,400. For condos, the median price jumped by 12.6% year-over-year to $300,000 (data via YCharts):

The winner in these crazy bidding wars isn’t the buyer. It’s the seller… THE WOLF STREET REPORT: It’s a Perfect Time to Sell a Home (to FOMO-Driven Buyers)

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Speaking for San Diego County, I can tell you that inventory is still very low and homes are selling with multiple offers including all cash offers and very often well over asking price.

You beat me to it. San Diego is seeing no such decline. Prices continue to rise, sales volume is pitiful due to miserable lack of supply. Combine this with out of control policies in the city allowing houses to become apartments, which is bringing developers in like crazy. No end in sight here.

“allowing houses to become apartments, which is bringing developers in like crazy.”

Could you explain this? Are single family lots being rezoned for fourplexes?

San Diego has abandoned single family zoning as has the state in the form of ADU’s. Accessory dwelling units. San Diego took the state law and gave away the farm. There is no limit as to haw many ADU’s can be built in the city if within a half mile of a transit line. The catch? They have to be affordable, low income designated. The entire city is under this ordinance. It’s not known but groups in San Diego are sounding the alarm. It’s been mentioned on a couple of tv stations and the paper. AB 9 and 10, if passed, will decimate single family residential. Look up this in local SD news.

If you live east of 5, you are not in San Diego.

But you have a yard larger than a postage stamp and no noise from the coaster so it’s all good

Ummm… no

The city of San Diego is large, as well as the county. There was a complete change in the county board of supervisors after the election, and post covid we have no way to know how that will change the building codes. The last two major retail/residential plans to go on the ballot failed. Sandag has said adding lanes to the 5 is not an option. The new airport in Miramar was shot down. The awareness is that if you build “infrastructure” they will come, and we don’t want them. Meanwhile hispanics go eight to a 2bdrm apt, and that is no bueno. All that contributes to the pitiful rise in land values, versus homes, and no one wants to sell, while land is undervalued, and no one wants to buy land, while the development costs are inflated. So nothing gets done. SD may be the new SF, all we need is a high tech industry buildout.

TBWCW!

I am particularly interested in this aspect of Urban planning “ in this case No planning at all”.

This myriad of planning deficiencies that plagued and are still plaguing our metropolises are now clearly visible to all to see.

First , you get politicians with no credence or skills in planning to make decisions on zoning and re zoning our cities.

Second, you allow the vultures also known by their common name ( developers or large construction companies) to further influence the city councils policies to further destroy the livability of the place.

It is my opinion that the optimum population size of the US under the current circumstances should NOT exceed its current level.

The large size of indebtedness of the US ECONOMY will cause the housing market to crash sooner or later , with even bigger bang that will make the last crisis looks like a piece of cake ( apology to all ordinary Americans who suffered and lost their lives and livelihoods under those circumstances).

The policy makers on all levels of governments have entirely lost the plot and are purely driven by micro economic currents that have differing directions symptomatic to ( Economic upheaval created by contradictory government policies)!

This self fulfilling destructive cycle is akin to the vortex that WILL carry the American Economic life to the unknown.

The reality of a large proportion of labor that CANNOT find suitable work or adequate working hours is a demonstration of how far RE orientation of the American Economy have fallen behind.

While 30 odd years of transitioning to a service economy could’ve allowed the federal government to re tune and re jig the labor market to accommodate these upheaval shifts, we saw that they failed miserably in this task by leaning on migrations of skilled and unskilled labor to accommodate the large corporations needs who in turn slowly but surely abandoned their end of the bargain by transferring their assets entirely outside the US!

You cannot solve the US’s problems by throwing money into the pit!

Congress have No more legitimacy!

as they can NO longer guarantee the two most basic Rights to the people,

Bread and shelter.

How long until we see the inevitable?

PLEASE keep commenting on Wolf’s wonders full site/blog jack..

Gotta add I agree with SO much of what you say!!!

Not all, as that would only be A** kiss,,, but a literal TON!!

\

Thank you,,

from one who has been OUT of the SM since ’80s due to clear perceptions of corruptions/distortions

and on Wolf’s wonderful blog/site for education, just hoping to get back to SM…

“You cannot solve the US’s problems by throwing money into the pit!”

DC’s multi-decade response – “The obvious solution is a bigger pit.”

DC’s recent response (as foretold economic disaster unfolds) – “The obvious solution is a bigger pit, you racist domestic terrorist you.”

“Combine this with out of control policies in the city allowing houses to become apartments, which is bringing developers in like crazy.”

I recall dozens of apartment complexes being converted to condos. That was where the money is (was). A previously low end 500 sq ft apt in the beach areas now sells for 350-400k!

As a non-US reader, could someone please explain what the difference would be between an apartment complex and the condos to which they were converted?

If it’s simply a matter of ownership rather than renting, as it appears to be from what I’ve just read elsewhere, why does this make for a difference in name, for what is in effect the same exact thing?

Swiss Brit,

Here are some thoughts.

Owners can put their condos on the rental market, no problem. That happens all the time. Many mom-and-pop landlords rent them out their condos. This is super common, and no “conversion” needs to take place.

The developer of a new building can also decide to switch to rental apartments. This might pose problems with lenders if they lent on the project after being told the units were going to be sold as condos rather than being rented out, and might require renegotiated financing. There may also be local zoning issues, permitting issues, etc. that may have to be solved.

The bigger problem arises the other way around, in cities with rent control, when you convert a construction project from permitted rental apartments to condos. This depends on the city.

In cities with rent-controlled apartments, there was a big move to convert apartments to condos or co-ops to get around rent control. This was all the rage in San Francisco many years ago. But the city then essentially put a stop to it.

But in San Francisco, only buildings that were built before 1978 are rent-controlled. All later buildings rent out at market rent, including new construction. So these limits don’t apply to newer buildings. There may still be permitting issues in converting a new construction project from apartments to condos, especially if the project has been approved with “affordable units” as part of the deal.

Once the condos have been sold (hopefully during construction), the developer can no longer convert them to anything because they’re now own by others. Someone would have to buy all those condos back from the owners to convert them to rentals. I’m not sure if that ever makes any sense.

Hi Bob WCW,

There are signs that S.D. is bending, but I think the extra push to stay up longer has been helped been zero down V.A. and drug money. Let’s get real—do the high income earners really pay $1.2M for Imperial Beach, Bonita, Chula Vista, La Mesa, Rancho San Diego, Clairemont, Etc. Etc. ?

We bought our house in San Diego back in 2015 and I told my pregnant wife at the time, “we’re buying at the peak!” Shows what I know. I wouldn’t want to be in this market again for my primary residence.

I sold about all my stocks in 2016 as well as they looked fully valued. Who knew the Fed would keep the pedal to the metal for 5 years?

Who knew?

They knew, and all their buddies.

Imagine if you knew back in 2009 that the Fed would assist in $20 Trillion new dollars being created, willy nilly, by the federal govt with the assist of a Fed keeping interest rates well below the inflation rate.

Bernanke said QE to be temporary until things go back to normal…and normal apparently never happened….eventhough stocks roared through the old highs, unemployment went to all time lows….

I am in San Diego and watching some neighborhood

A lot of homes now coming back to market and seeing some though rare price reductions as well

Yes the market is still hot

San Diego is so badly overcrowded, there is no quality of life anymore.

After spending most of my life there, you could not pay me to live there now. Overcrowding makes people desperate, and desperation makes people act like aholes. It is really depressing…

Not to mention everything in San Diego comes from Los Angeles which makes it a disaster waiting to happen. Imagine if the 3.5 million people in the San Diego county area are suddenly cut off due to a major earthquake in LA.

Water, gasoline, food, natural gas, and nearly everything else comes from LA and if there is a major disaster, San Diego is cut off. It’s port is inadequate, and there is only one major road going east to bring in supplies.

It would make New Orleans after the flood look like a picnic…

And people are paying stupid amounts of money to live there… Geniuses…

Agree 100%. Reminds me of a third world country or some of the metro areas outside of NYC. Police have taken up broken windows policing. (maybe they have to, which is a sign in itself).

There is an air of desperation in many people’s eyes.

Over-development will destroy San Diego, like it did LA. No one seems to care. Just build, build, build.

I want to move out of San Diego but am stuck because of some family issues

San Diego is turning into third world country and this adu thing is accelerating this trend

Coastal areas are the worst .

I am still looking for my next qce to settle in

Utterly butterfly confused ?

I came to america to experience first world life but guess san diego is the wrong place for that

I also noticed by talking to realtors about the homes they have listed..nothing although anecdotal .. a lot of people are selling their homes and moving out of state…

Where have you seen the adu disaster? In the college area and anywhere south of the 8 it’s a disaster

Jdog-and LA’s water comes from?

Having returned to college following the Army, i decided to take a flyer on Geography as a major. My first Climatology class had a section on water history in the West. First research question: ‘…at current usages, how large a population can the Los Angeles Basin sustain with native water resources?…’. Answer: prox. 80,000…

(For the record, i was born and raised in San Diego, my grandfather arriving and settling there in 1910. The realization of an incredibly-fragile water base for SoCal led me to leave the area in ’77. Don’t disagree that San Diego isn’t the city/county it was 50 years ago, but major population increases have many negative livability/resource effects anywhere they occur).

may we all find a better day.

Speaking also for coastal San Diego, it’s still full blazing nuttiness. Every house that I’m so sure is overpriced ends up pending in a few days. No matter whether it’s a twin-home at 2x the price from a few years ago, or a $4 mil lipsticked pig SFH with some serious flaws, they all go into contract quickly.

What really shocks me is the price per sq ft. $1k used to be a pretty hard ceiling for all but super premium pads. Now? $1.5k seems pretty common.

All this in formerly under the radar San Diego, where income is considerably lower than LA, SF and pretty much all major metro areas.

_________________ is different and special and will not see a drop in prices because _____________ and _____________ and ___________.

It really is different this time. It’s a new paradigm. We are immune to a downturn. Prices at worst will just plateau. Everybody wants to live here. They aren’t building any more land.

Inventory has been going low for years and this increase seems more like regular fluctuation with the usual selling season. I think this is just confirmation bias and don’t think you can read too much into it.

If house prices are very clearly at a peak, and the pandemic eviction moratoriums and mortgage forbearances are coming to an end why are investors buying up homes to rent?

Many of them — the second home buyers for sure — aren’t going to rent them out. That’s not part of their plan at all.

Then what is their plan?

If a plan exists (like Iraq War 2.0?).

That DC is never, ever forced to move away from ZIRP?

Owning a vacant home is only a good investment if home prices rise by a lot all the time, because those price increases have to cover interest, taxes, insurance, and maintenance. Once prices are flat, that investment becomes a pure expense.

Buying rental property is a completely different activity. And people can actually live in it.

Wolf,

I’m still confused (I think. That shows how confused I am…)

1) You say that second home buyers don’t plan to rent them, then state

2) Owning a second vacant home in complete reliance upon price appreciation is a very risky proposition (I completely agree)

3) But you don’t explicitly state that #2 is their actual “plan” leaving a sort of mysterioso aura implying some third possible (unstated) intent.

My guess is that you think #2 (vacant, ultimate flip) is what is actually going on…but your posts are reading more vague/mysterious…like there is some third unspoken possibility.

Enough so that I am being a pain in the butt about it (since I can’t imagine what a third possibility would be).

Cas127,

I know a working high-income couple that owns three expensive homes in different cities of the same state. They’ve moved a lot for their jobs, and with each move they buy a new house but keep the old residences. They aren’t even renting them out. They are not finance professionals, and I imagine they are just too busy to think much about it.

With today’s wealth concentration and high dual income households, I expect there are other folks in a similar position. When RE is rising fast, there just is no urgency to sell, even if the property is vacant. If prices clearly start falling, it will be a different story. When you make enough income, and have a busy job, all financial matters go to back of mind.

As I see it, the apparent plan is this: When prices start falling, sell. Until then, hold.

I talked to a real estate agent who just bought two houses because she doesnt trust the stock market due to how expensive it is and wants to have her money in assets due to inflation.

I think that investors have heard the term inflation and thought that housing prices would go up in an inflationary environment. But if inflation goes higher, interest rates go up and payments go up and that socks housing prices down.

These amateur investors think they are brilliant, but will be hit with alot of bad news because they are putting alot of cash in these deals and that means they cant just bail and hand the keys to the bank.

Some of my friends are borderline buyer it means if the interest rate goes up they’d be priced out because of higher monthly payments.

Also… my neighborhood has at least million dollar homes and most are multi family multi generation due to unaffordability..

gametv,

Almost everyone with any substantial investments thinks they are an superthinker mastermind. Right now, it’s possible that everyone is wrong. I could see all investment assets declining. Precious metals could possibly hold their value (though they may temporarily drop). It would be very funny if those just holding cash in the bank right now win out. Obviously, upto this point being in the stock and housing markets was the best move, I mean it would be funny if people who pulled everything out right now and pulled a Warren Buffet and just keep cash in the bank, win out.

During Trump we saw the staggering buildup of public debt and money. That money mainly went to the top1%.

Yes, there were some somewhat quiet rumblings about inflation then–

But the press chatter inflation talk only came to a roar after a Democrat got elected. That was predictable. Ok for Republicans to give a big boost the economy–but now we’ve got to stop those dangerous high spending Democrats from spending on infrastructure or anything else. Good Republican messaging.

The talk has put panic in those with lots of high cash trying to grab assets to make a killing when prices go up.

But I still don’t see how price increases can be sustained on goods and services that the bottom 80% buy– at least not until wages go up on the bottom 80%. Where’s the money going to come from? So far “inflation” seems to me mainly asset inflation by those few with lots of cash.

As I’ve said before–I could be wrong. We’ll see.

Lol are you actually trying to pretend the corporate media isn’t the mouthpiece of the democratic party? That is some INSANE gaslighting on your part.

Hahahaha, Murdoch’s empire, including Fox?

If any party ever made a pretense at fiscal responsibility it was certainly NOT the Dems. But neither party bothers anymore. There’s a great recent article in Reason Magazine about it, and it’s both depressing and refreshing (to read something that isn’t blatant partisan spin).

Wolf,

Yes, Fox News…but in terms of number of news outlets, one (versus the (defecating) herd of liberal news like minds).

Admittedly, NewsMax and OANN have emerged…but so recently as to be almost irrelevant for the moment.

Until 1995, there was *nothing* other than the Establishment infected oligopoly of polished lie State liberalism (today, with media Balkanization, the lies are much less polished).

Pre 1995, there was Rush Limbaugh on radio…and that was it. (Well, you could shoot your television in outrage but that did not tend to affect electoral outcomes).

In 1995 Fox News arrived and topped the news ratings almost immediately…and for the same reason Limbaugh did…they addressed the 50%+ of news consumers whose intelligence/lived experience had been insulted for decades via the Establishment pap pumped out via the MSM sphincters.

And 25 years later, Fox News still effectively stands alone (on television…the marching blog army of conservatives on the internet is another matter…although even there, there is no conservative HuffPo/BuzzFeed equivalent retailing half-truth politics to the mass mkt of celebrity-stunted, drive-by news consumers.

Cas-(Wolf-here i go offtrack again. As always, understand an x-out.) in this instance re: media-looks like EVERYONE’s slip is showing (…and i have ZERO patience with smug chickenhawks of any stripe, of which Mr.Murdoch’s organization is rife, or those who would ignore other nations’ right to self-determination by demonstrating a willingness to send our military to cover our mighty MIC’s production under the guise of ‘preserving’ human rights and/or democracy).

Our society is still very much one of humanity’s experiments, as Franklin foretold. Our short national history has pendulum-ed along, swinging back (in the context of contemporary age) to accepting (including the tragic failure of 1861-5) legislatively hard-fought, and always humanly-corrupt, compromise between parties as the best way forward-i.e.-country (thinking of at least a minimum prosperity for the majority of the populace) over party (the willingness to suck up your electoral defeats while resolving to work harder to convince a majority of voters to look your way next time ’round while not totally spannering the government in the interim), and this, despite a significant portion of that population appearing to be willfully ignorant or flat uninterested in the constant, truly-critical examination of the vital business of their homeland (a lot of oxen awaiting in line to be gored, perhaps the seeds of eventual decline…).

The business of media, is business-it’s there to make money. Technology has given it steroids in terms of distribution, if not civic responsibility and adherence to verifiable fact. If media’s product has morphed into one of appealing to myriad echo chambers because that is what sells, (after all, ‘…if it bleeds, it leads…’) then the sane-to-bonkers viewpoints on all sides of the current Great Divide exist, and though excoriated, can not be wished away. The question then is not to blame the motivations of the media, but to examine those of who demand and consume their current product. We can only hope ‘…as seen on TV…’ has not become an acceptable short-circuit for the pain-in-the-tush hard work of critically-objective information-gathering, thought and action, but my optimism is not high at this time.

The great Mort Sahl once quipped: “…the U.S. is the WORST country in the world-AFTER all the rest of them…”.

If there has ever been an ‘American Exceptionalism’ it’s a general embrace of the above remark, looking forward, knowing we must always strive to do better for ALL of our citizens. The world does not suffer extended laurel-resting, history’s locker room is full of nations thrown out of the game for just that.

Are we now deciding to join the crowd?

Rant over with my apologies.

may we all find a better day.

Cas,

So it’s voices of hope crying in the wilderness against the “defecating herd” of massive “liberal news like minds”? Correct?

Looks to me like it’s all designed first to agitate and piss people off, and give them something (anything) to bitch collectively about, and then attempt to “define” an “enemy of the people”, which currently seems to be in the persona of this “mythical classic liberal”, who thinks he’s smart but is actually stupid. Am I right so far?

Guess it doesn’t matter much who is chosen to hate and fear as “destroyers of correct way”, as long as it’s all agreed upon and then “made clear” to all the “people who have been insulted (and mainly economically crapped on) for decades”.

Well, good luck creating these dangerous and obvious internal enemies, nothing binds a group together more. It’s just a pity you can’t get filthy rich off it, like some of your heroes you mention.

You might want to look up that famous line by Goebbels, in case you think this stuff is all “new”. Maybe I’ll chase it down for ya, although I realize this is a pointless exercise on my part…you have made many “leaps of faith” isolating you from my liberal treachery.

Blessed are the flexible, for they shall not be bent out of shape, eh? Toodles.

Oh, and what is “media Balkanization”. I watch, Tucker, Hannity, and Laura fairly regularly, but I missed that. Maybe from mind of “the great one”, Levin?

Really, I want to know.

Thanks

PS, I love potty humor, so naturally I love South Park, but I don’t think you are trying to be humorous, so you probably don’t know about Mr Hankey. He’s cool, but flawed like all of us.

PERFECT TIMING….to be on the wrong side.

I’ve noticed [over the decades] that realtors always buy at the peak.

Wash. Rinse. Spin. Repeat.

Never ask a fish how to catch fish.

Sam,

It makes sense that realtors buy at the top, they have “earned” lots of money in the run up and lose sight of the downside which they experienced (or not) in the previous market bottom, thus they have cash and myopia. It’s almost an affinity scam.

That is the perfect prescription for buy high sell low.

Wells Fargo, for one, is sitting on tens of thousands of houses that have not had their mortgage paid now for a year. Some percentage of these houses are going to hit the market when the eviction moratorium ends. As a homeowner in Ca I am very concerned. Some markets, like crappy towns like Pomona, where I am, have not seen the price appreciation one sees in San Diego or La. There has been massive in migration from the global south but these people came with nothing and earn very little and depend heavily on government to survive. And there are no jobs and no income to support these prices unless one considers dual government job couples…….prison guard/cop, fireman/county nurse, teacher/prison guard, DMV clerk/cop, Addiction counselor/homeless advocate, ESL teacher/administrator and all the other admin jobs that government provides.

Nobody knows the peak price. FOMO buying may lead to a temporary plateau but inflation and fully reopen can add more fuel.

Tell the stock market that it is ATH and must crash… Keep telling it the pop is coming

Doesn’t make it so. The fed and all the powers are driving us one direction.

You might be right, but Fed has pounded is with the Zirp and now if they want to stimulate they have to monetize the debt by buying more treasuries and government backed paper.

Once yield on everything gets close to zero, you might as well own gold as you aren’t getting yield anyway.

I don’t know 300 million people, but I do know that everyone I know who wants a house has a house now. Everyone bought in once they could get sub-3% mortgages and now they’re nesting.

You must not live in a high cost of living area. The large majority of people that I know under age 45 are still hoping and dreaming of a chance to someday own a house.

I’m done with houses. I rent now and I’m dreaming of a camper.

Serious.

Why would I want to mortgage 2-5 years of my life earnings for a stupid house? And once I get it, pay ever increasing local property taxes to a school system that is ideologically opposed to what I teach my children? And also have the choice of either spending every weekend maintaining it myself or paying top $ for some contractor to maintain it with laborers who can’t speak English? How much for a new roof? New A/C system? Running new wires? Insulation? Any of those jobs cost more than a camper.

Retiring to a camper is sounding better every day. As soon as my last child moves out. Heck, maybe as soon as my 2nd to last moves out.

My wife and I will be the multi-millionaires retiring to a camper. We can drive from the keys to Alaska and back while ya’ll are slaving for your houses.

Buy a small condo to live in after selling the house. Use it to store your stuff and lock up when you leave in the camper for months at a time. Buy a Class II so you can park it anywhere. I have a friend who does just this (in Texas).

What stuff? LoL

Amazing how much less I want a house the more stuff I get rid of.

What little stuff I want to keep can either go in part of a kid’s or a friend’s garage or a cheap storage unit.

Put more accurately: everyone I know who had the means to buy a house but was sitting on the fence bought a house in the last 12 months. Everyone I know who wanted to move to a bigger home went and bought that bigger place.

I don’t know anyone who’s currently looking for a house or who is likely to start looking for a house in 2021.

Which makes me wonder if my group is unique and special, or if the USA is running out of buyers.

Your group is special. US is never runs out of buyers. It’s all supply and demand.

Dear Readers,

So I’ll do a lil’ promo here for my friends at Wealthion:

“Record asset prices. Spiking inflation. Rising yields. What’s Coming Next for the Markets?” That’s an online event on June 5th that Wealthion is hosting, with an impressive line-up: Lacy Hunt, Grant Williams, Stephanie Pomboy, David Hunter, Matt Taibbi, and others.

To see the complete lineup and learn how to register, visit: wealthion.com/conference

Good stuff, will have to check it out. Really like some of the pieces that Matt Taipei had covered in the past.

In the areas I own rentals in, most of the remaining inventory are homes with incurable defects … busy streets, airplanes overhead, adjacent to apartments, …. Any normal home is instantly hit with multiple offers. Realtors are knocking on doors. Sales at 10% over the ask happen fairly often. You call that slow?

Housing market rallies have price spurts followed by short periods of consolidation before another price spurt.

When buying in this type of market, you have to be careful. Only buy a quality location even if you have to overpay in a bidding war. Pass on everything else.

“Sales at 10% over the ask happen fairly often.”

Is the assumption that another SFR or apartment will never be built? Another suburb? Local jobs never lost? Relocated to lower cost metro.

The endless upward ratchet mindset of RE investors (at mad prices) always amazes me.

Current housing mania is peak lunacy, for sure.

But this frenzy has been going on for many months so it has consequently seeped into our national consciousness as a ‘new normal’– with the real estate industry as a cheerleader egging prospective buyers on despite moonshot pricing, bidding wars, and insane waiving of contingencies (your get out of jail card in case there is a deal-breaker lurking unseen when you are under contract).

Wolf’s article’s premise– that this frozen-up inventory problem is starting to thaw out and more sellers are getting ready to sell– jives with my gut feeling that this is an inflection point and more supply will lead to prices cooling off.

No, I simply don’t see a housing market crash this year. But slowly, almost imperceptibly at first, this red hot market is facing headwinds.

It is about time for some common sense to show up.

You’re mistaking contingency with disclosure

No, sorry, I didn’t read it right the first time

SocalJim is still drinking too much of that Lawrence Yun cool aid. I wouldn’t do anything in this post. If anything I would do just the opposite of what is recommended.

1. Don’t buy now period.

2. Don’t even try to buy in a quality location right now.

3. Don’t get into a bidding war.

4. If you have to buy , then look for a fixer upper in a good location.

5. If you have to buy and you can;t find a fixer upper in good neighborhood then look for a renovated property in a marginal neighborhood.

We’re doing a lot of VA appraisals that fit into category ‘5’ above and the prices are coming in at reasonable levels.

In my opinion, if you can’t find a way to swing a quality location, then don’t buy at all.

Nothing worse than buying a dog at a high price.

SocalJim. You didn’t read my response. I said ” look for a renovated property in a marginal neighborhood. There are good deals here in neighborhoods that are undergoing demographic change. The houses are not “dogs”. They have been renovated by investors and are in pristine condition. And they are not overpriced and are affordable. That’s why Vets are buying them. So you are wrong on everything. That’s what’s going on here.

This is why I never listen to Realtors. You realtors are all drunk peddling your own misinformation.

I stopped looking recently. I couldn’t even get in to see a house so I told my realtor that I was on a buyers strike. She said “but the interest rates are so low”. Yeah but the houses are too high so what’s the point? Now out of my range.

The market you comment on is in SoCal. The majority of the nation is not seeing that craziness.

“The market you comment on is in SoCal. The majority of the nation is not seeing that craziness.” Oh? I’m seeing it in working folk USA, MA, land of the Camponeli (single level house w/o a basement usually 1100 sq ft or 1400 with addition).

timbers, Boston metro has the biotech pharma job machine supercharging that housing market. Moderna just announced a major expansion in Norwood.

Biotech and pharma will be to Boston what the Defense companies are to Los Angeles … both industries fueled by government spending for national defense.

SocalJim,

My immediate Boss has mentioned to me more than once the high wages Moderna and other Pharma firms are offering, “stealing” our staff (I am at Bristol Myers Squib) but also making it harder to meet our hiring goals for a new factory (I still do not have an immediate permanent manager they haven’t yet found one they like).

As I have no direct prior experience in medical factory work, I intend to use my current position as a training platform. In a year or two I will seek and get a decent raise…or…Failing that, I will seek out a new employer. With my Boss telling me other firms hindering their hiring with higher salaries, seems like a no brainer.

Rule 4: See Rule 1.

Rule 5: See Rule 4.

I think you are taking the George Constanza approach to SocalJim’s advice there and I like it.

Because the U.S. is still a lot cheaper than many other G7 foreign countries. Except for San Fran and maybe New York, the rest of the U.S. looks cheap compared to these cities: Hong Kong, Tokyo, Vancouver, London, Paris, Brussels, Berlin, Amsterdam.

I hate to have to break this to you, Doug, but this nation has a long, long history of protest.

It’s how things evolve and change. In fact, the USA was born out of protest against an empire led by a king.

So whining about demonstrations just lets everybody know where you get your info from. You’re trained to be scared of people who (oh gosh, get ready, this is really SCARY) say things like:

“My life matters.”

“I don’t want the police to keep killing innocent people.”

Etc.

Boogie boogie boogie, you really scared me when you said “My life matters.”

If you think the USA is so terrible, perhaps you should try Saudi Arabia, Russia or some other place where a scary demonstration will never happen because everybody lives under authoritarian rule (aka a police state).

Talk about a snowflake!! If you’d turn off your TV and just take a look around, sure we have problems. But the USA has a lot going for it.

Nobody likes taxes but they’re the price of civilization. Crime? Sure, it’s been around since the dawn of humanity. These things “come w/the territory.”

Republican:

You get the award for drinking the koolaide!

“Crime comes with the territory”.

Is that right?

Protest? I think that the American WAR for Independence was a little more than a ‘protest’.

BLM is a protest? More like violent demonstrations.

And I didn’t know that a foreigner could buy real estate in Russia or Saudi Arabia.

Amazing.

“In the areas I own rentals in, most of the remaining inventory are homes with incurable defects …”

Of course that is true– this is a wild market which some dodgy sellers are using to good advantage to finally offload their crummy properties at premium prices.

Their thought process is that there are enough FOMO desperate buyers that will take a chance at their run-down, decrepit and old, or otherwise risky properties. They are often sold AS-IS, and couched in lovely terms like: ‘project for a handyman’, ‘needs a little TLC’, ‘imagine adding your personal touch’, etc.

Some properties are unabashedly offered though lying in flood zones, others are next to cell towers, high tension lines, parking lots, busy highways, or rail lines. Nothing new there– except for the jaw-dropping asking prices.

I remember the frenzy in California in 1990. Sky is the limit. Shortage of homes for sale. Yada yada….

I know, “It’s Different This Time”.

I really hope those investors lose all their fortune! They are deserve this punishment for their animal spirit. Every home they buy makes someone’s life more miserable. Can’t wait for Biden to tax the hell out of them.

The investors may be the rabbit, but Powell is the carrot. He and his coterie of sycophants should be tried for treason and get the electric chair.

Agreed!

Why is the Fed buying mortgage paper, essentially lending to home buyers below inflation?

Everyone wants some of that money…

and the area where I live, people who wish to sell are pulling their homes off the market because the replacement costs of their homes just went up by about 35% due to lumber, copper, and labor costs.

Nice job federal reserve!!!!

I think it’s easy to let low interest financing influence you to pay too much just like on a car or credit card teaser rate.

If you look out the next decade you have to game out the possibility of an inflationary and a deflationary outcome.

Old School said: “If you look out the next decade you have to game out the possibility of an inflationary and a deflationary outcome.”

_________________________________

There’s saying a whole lot of nothing.

@ Old School –

Maybe you could get a job on that Wealthion panel.

Cb,

I am just saying for your personal finances you are best at considering more than a base case especially when buying a home. You probably should consider a base case of more of the same plus inflation running very hot and opposite case of deflation.

Historicus:

“Why is the Fed buying mortgage paper….”?

+1000

Amen to that. In fact I cross my fingers every night hoping that will happen, sadly my prayer has not been answered yet.

Jake,

So if an individual spots an investment opportunity and takes advantage of it, all legally mind you, do they deserve to be punished?

Jeff-explain to me again, please, what that ‘moral hazard’ in the economy thing is? And to whom exactly does it apply?

may we all find a better day.

I know people who were planning to trade up, but put that on hold. If you sell your home, you may not be able to get back in without bleeding money in a bidding war. That is causing the market to freeze.

The warning signs of a tight market have been out there for a long time. For years, less than 5 months of inventory was available. But, many ignored that warning sign with a myraid of excuses.

I know of someone who gleefully sold to the FOMO crowd in the Seattle area. Now he is being outbid on the houses he want. Mostly cash buyers. Having a hard time getting back on the Merry-go-round, meanwhile prices are increasing.

How many people are getting suckered into a less than desirable house because “interest rates are so low”. They might be stuck in that house for a long long time if (when) interest rates rise

The smart thing to do, probably re: buying a home now:

1) Rent

2) Wait

3) Purchase after bubble pops (they always end up popping)

4) Ignore FOMO

If you’re sitting and waiting for the prices to come down, I may have some bad news for you. This will keep going up at least for a few more years. Then it would slightly dip, or remain leveled. In the long run, those prices will only go up.

As a first time single family home buyer, I do not regret bidding 10% above asking price, four listings in a row, until I finally “won” a house.

Biden and the Fed has made sure cash is trash. So you can sit on it and watch it burn, or you can buy your house, before that train has completely left the station.

Yeah, and what do you think is going to happen when the Boomer population starts leaving their houses and moving to condos or senior housing?

We’re near the peak.

We live in a 55+ home area with hundreds of homes here. What you say is going on around here. This neighborhood was built 22 years ago and the initial gang of old people are moving to apartments, assisted living facilities, or dropping like flies on a hot day. There are three of these neighborhoods near us (5 mile radius), each with several hundred homes. Lots of movement, but no bidding wars.

RightNYer the global demand for USA homes and rentals is insatiable. Run a poll of all other countries and find out how many people want to move to the USA. The answer is that billions of people would move here instantly if they had a chance. So regardless of Boomers aging and passing away the demand for USA houses will always exceed the supply until the rest of the world doesn’t want to move here.

USA home prices are set mostly by interest rates and mortgage availability, which the people have allowed the Federal Govt and it’s unconstitutional pet, the Federal Reserve, to control. IMHO this is all illegal under the Constitution but the people love their interest rate controls, and subsidized mortgages.

Except that most of the world’s people who want to move here are destitute, and will not be able to pay anything you’d consider reasonable for those houses.

correct it’s not instant demand for mcmansions the day destitute people move here. May take a couple of years or a generation or two. But the demand is insatiable.

Will demand still be insatiable if we lose our reserve currency status and have to start living within our means?

The issue is, the demand for homes is not organic, meaning is is not being driven by people needing a place to live. It is being driven by greed and speculation. That is why it is not sustainable. When people make decisions based on emotion, instead of logic and reason, their decisions are doomed to end in disaster.

That is why every bubble bursts…

Rightnyer desire to come to the USA was insatiable before the USA had reserve currency status.

How many poor people do you know in other countries? Have you traveled? If you have not tried, maybe pick some of the poorest of the poor and get to know them and try to help them. Then you will understand why I say billions of people would be happy to come here.

Based on the people I personally know in other countries, I would guess even if the USA had a worse downturn than in the 1930’s, lost reserve currency status, and the welfare system stopped working- billions of people around the world would still want to come here, even if that meant arriving destitute.

Even if you told them that to get started they would have to go to Detroit and camp in a vacant lot with no welfare, the people I know would still want to come. And within a few years or 2 generations they would get a McMansion for themselves and be very happy with it. Even if they had an $800k mortgage on it.

This is why I say that baby boomers supposedly vacating houses is irrelevant to the long term supply/demand balance of USA housing. Price of USA houses is determined mostly by interest rates.

. . . and subsidized mortgages

Spot on Raging.

Also their kids can get into colleges almost free in the U.S. where they cannot afford it in their own country. I was was riding in a cab with a 55 year old cab driver from India or Pakistan.

He said moved here when his kids were still in junior high and high school and all 4 of his kids got full tuition to schools like Georgia and Georgia Tech and Emory. We are talking about $120k or more free tuition per kid and and over 600k when all is said and done.

I made too much money, just barely 6 figures, to get my kid much of a scholarship. She had never had anything below a A, 30 ACT, PSAT national merit semifinalist (top 1% of all SAT test takers) as she just missed the national merit final cut . She ended up with a $1000 scholarship at a state public school that ran about $17k a year.

She had to pay $120k out of her own pocket via loans to go to med school to become a Physician assistant. Yet I know of foreign born students with not as good grades getting free rides.

Sometimes is stinks to be middle class.

ya ru82 the gov can’t get enough immigration because immigrants will never do things like “buyers strike” on houses or complain about the corruption of the govt etc.

Ultimately, if there is a buyers strike on houses, it will mean only 2 other people in the entire USA joined me. Everyone else will gleefully line themselves up to be mowed down by the banks and be foreclosed on when TPTB decide to increase rates

I’ll just add to my comment that sales are down because there’s literally nothing left to sell lol Not because the market is cooling

Inventories are rising, not falling.

Time to short the homebuilders you think?

I read a funny comment somewhere….was it here?

The previous mid 2000 bubble there were to many houses being sold to to many people who could not afford them.

Now you do not have enough houses to sell to a lot of people who can afford a house.

I am sure we will see a dip but it may not be as low as people think.

I live in flyover land an empty lot is now running close to $100k. 10 years ago it was $60k. During the last housing bubble you could buy some lots cheaper in foreclosure but that was from builders that bought a lot for spec houses. That is not the case now. There is hardly any spec house being built so there will not be any crash prices in land.

Wall street is buying houses and they have no risk. So what if their is a crash, the will buy more houses. They passed all the risk in MBS to investors. But those MBS are backed by the fed so nobody will take a loss like the subprime fiasco. IMHO, Wall Street will buy more houses on any dip. I can be wrong but somebody would need to explain to me why anyone would not buy real estate, bundle it in a MBS that the GSE backs 100% no matter what the price. There is no risk. I guess if the GSE quit backing these loans, then this could turn out bad?

I have to say. I was super bearish on housing in 2007. Sold all my stocks and went to cash. The only investing I did was to buy puts on some Merrill Lynch and Leman Brothers. I just new all those sub prime people would not be able to pay their mortgage when the rates adjusted.

I am just not sure what the catalyst is this time. Higher rates…sure. Maybe another recession?

But there is no way the FED will let a recession happen just 1 year after a recession. They will keep pumping IMHO?

I do believe stocks are overvalued and in some places housing is overvalued. But what will be the catalyst for any downturn?

Hey whatever you tell yourself to make you sleep better at night. There’s a certain comfort to lying to yourself and validate your own decision with flawed logic. One thing I will tell you though, you sure did fail your history lesson, when has the stock or housing market ever not suffer a painful crash or correction after hitting a peak? Sure many years later the trend line is up but so is inflation.

You sound like a newbie who has absolutely no clue about real estate. The idea that this market insanity would continue forever is about as delusional as thinking Dogecoin is going to become the reserve currency of the world. We’re in the biggest housing BUBBLE in history. I look so forward to watching these FOMO ‘tards get absolutely smoked. They’re going to be crying to mama as they go into foreclosure. Suckas.

It would appear you forgot one of the players on the market. The big corporations have entered the room. So just like the Stock Market where it can stay dynamic longer than you can stay solvent. The corporations will buy all the available market. They will be backstopped by the government and they can afford to lose Billion YoY for the ultimate price of a gain in 20 years

I didn’t forget anything. This argument didn’t work last time and it’s not going to work this time. Furthermore, the FED itself has started to take notice of the excesses in the housing market and also take a lot of heat for their contributions to said excesses. Stick a fork in this thing, it’s cooked.

Why do people think they are psychics?

He’s got buyer’s remorse, so he’s trying to justify his decision. He knows he grossly overpaid, so he’s vacillating between the denial and the bargaining stages of grief. Anger is probably mixed in there a bit. The 5 stages of grief are not necessarily experienced in order, and people go back and forth.

Lol

Lisa-because,like all psychics, they will never, ever, forecast an unhappy/unpleasant ending…

may we all find a better day.

I wish you good luck with that. Truly.

I agree that cash is trash and houses are the new cash. They are an illiquid form of cash, more like certificates of deposit in the old days. I own houses and treat them like cash. I am an idiot for owning unleveraged real estate because the debts will eventually be inflated away, but that’s also what makes houses equivalent to cash. Leveraged real estate is an investment.

It’s not that crashes have been abolished. It’s just that houses are no longer risk assets (individual markets still have a small amount of risk, but on a nationwide basis, as Bernanke famously proclaimed, houses have never declined in price until 2008). Even stocks are not risky anymore when looked at in aggregate (individual stocks are risky, but a broad index is defended by the Fed). The lack of risky assets to invest in led to the creation of riskier assets called cryptos.

Gone are the days of timid Fed interventions like we saw in 2001 and 2008. The Fed has learned to be bold and real estate moves slowly enough where price declines can be avoided as we saw in the March 2020 crash. Home prices should have declined by 15-20%, but there was no time.

Besides that, the interest rate on the 10 year will head back below 0.5% eventually, supporting home prices. The one thing you can bank on is that debtors will be bailed out at the expense of savers. I also think that the best time to sell real estate is at the bottom when the market is weak. When real estate falls 5-10%, chances are that something else falls by 50%. For example, copper might fall by 50%. Even if you have to sell your house below market value to find a buyer, you could then buy copper at half the current price. If you sell your house now, what are you gonna do with the money? You don’t know if copper will drop by 50% until it happens, and it’s too much risk to sit in cash waiting for something that may or may not happen.

LOL. Do you really believe this?

You talked me into it!

I’m dumping all my cash into copper on Monday morning!

Illiquid form of cash? Do you know what that is? It is a investment which is poised for deflation. Anyone who believes the current valuations are sustainable is in for one hell of a shock…

Jdog,

Why? Housing price is usually in par with the inflation rate.

“In the long run, those prices will only go up.”

And in the long run we are all dead.

I think normalcy bias and wishful thinking has many good people actually believing the fantasy that this time the housing market has crossed the Rubicon to lofty valuations and will never look back. In other words: “This time is different”.

I wouldn’t bet the farm on it.

Wow! Another person that can see the future before it happens!

Don’t stop there “Cash Guy”, tell us all your predictions!!!

Remember that if there’s not much to sell, sales volume will be down. Here on the Monterey Peninsula, trying to buy is very much still a blood sport.

BUY NOW OR BE PRICED OUT FOREVER!!!!! RATS WILL NEVER BE THIS LOW AGAIN!!!!! THERE’S HISTORICALLY LOW INVENTIRY SO YOU BETTER BIY NOW!!!!! [CUE ROCKET MORTGAGE AD]. DON’T MISS YOUR CHANCE!!!!!

ROCKET MORTGAGE???

Sounds like Dietek, the crooked subprime lender in 2007.

No strike apparently, saw this gem of an article today thought you guys might enjoy. Nothing to see, new normal here…

“Buyers get the home but offer $300,000 over asking price to do it in red-hot Texas real estate market

DALLAS — These are hard times to be a homebuyer in North Texas, even for those putting in competitive bids.

Real estate broker Joe Atkins of Joe Atkins Realty said he has seen plenty of cases where it is extraordinarily hard to be selected as the winning bid.

“You’ve probably got a 10% chance. I have made plenty of offers for clients this year and gone $50,000 or $100,000 over list…and lost,” he said.

Those $50,000 or $100,000 bids over what the seller is asking aren’t on million-dollar homes.

Atkins said that’s what is happening with $500,000, $600,000, $700,000 properties.

As for million dollar homes, Atkins shared the story of one of his agents who recently had a buyer in that price range in Southlake.

“He did not recommend this…they told my agent that they wanted to go $300,000 over (asking price) to try to secure the property. According to him, they got it but it was still tight,” said Atkins.”

50k on a 500k home is just 10% above asking. This has been the new normal for the past year.

CG,

You offer the profundity of a man standing in his yard in the rain inferring that it’s raining everywhere, and predicting it’ll keep raining the world over, forever…Wolf indicates that we may be at a pivot-point in the Covid-19 housing bubble, and provides evidence for it…

Each of these WTF-bubbles is, to some extent, a toilet-paper shortage, though some are made worse because the Fed or another Central Bank has put its fingers and toes on the market-scales…

Everyone wants a narrative because they can’t see the bleeding obvious.

I wonder if a lot of cash home buying are people diversifying out of stocks. If I had ridden the market to the top I would have had enough funds to pay cash for a nice beach house. I didn’t and so I don’t get the ocean view.

You can buy SFH real estate inside your IRA but you can’t live in it, so that might fit some of the buyers leaving them empty with furniture inside. If in an IRA you can flip it tax free.

Un fort jun lee OS, it is, once again, PE and their hedgie funnies folks doing the ”cash” buying of SFR once again, as I seriously went head to tail with when we Had to buy in the ‘saintly part of the tpa bay area 6 yrs ago when we HAD to come back here to take care of very elderly parents..

We were also ”cash” buyers, but could not compete with the Private Equity and Hedge Fund buyers who were much more ”connected” with the various and sundry websites trying to be ”the” connections for buyers, but, in fact just ”defaulting” to the the PE and hedgies..

Time and enough to stop this obvious scam holding houses and homes of all kinds OFF market for families needing shelter..

It would be interesting to see how much business the RE IRA businesses are doing.. If what you are saying is right, then there are going to be some substantial adjustments when this thing goes sideways…

The market has entered the “auction stage”. I have always found auctions to be interesting, because of the emotional aspect. People will bid far more than something is worth, because emotionally, they want to “win”.

They allow their emotions to replace their common sense, and reasoning.

Of course afterwards, they are often remorseful, realizing they paid way too much.

The same always happens in the later stages of a housing boom.

I have always theorized that it is driven by the segment of the population that was too afraid to buy before, but is now consumed by greed seeing the prices rising so fast, and their fear of missing out. Their fears of property ownership are simply overwhelmed by their fear of missing out, and they buy strictly out of emotion with no logic or reasoning involved..

Panic buying at the top of markets is the best indicator I know of that the market is close to collapse.

J-Pow!-and here i was thinking, a priori, that rats (animal OR human) would always be among the lowest of the low (i can’t wait for their coming improvement of character…).

may we all find a better day.

And today, the US Govt just reinstated higher tariffs on Canadian softwood lumber imports to 20%. That’s 20% on today’s already high lumber prices.

Can’t fix stupid. Tariffs are simply a consumer tax. If the US was self sufficient in timber/lumber there would be no imports as Canadian fixed costs in wages and benefits for producers, including taxation in all sectors at source…is higher. This will be absorbed and hidden in RE valuations. Financed at low interest…for now.

Paulo,

BS. Tariffs are a tax on profit margins, often paid for by the foreign supplier via price reductions because it has to compete with US suppliers who don’t pay the tariffs. YOU as Canadian hate these tariffs because YOUR companies (the suppliers) are paying them via price reductions. I LOVE these tariffs because YOU get to pay OUR taxes. Hahahahahahaha…

Dead on Wolf!

If China is trying to sell into the US, and gets slapped with a tariff, the Chinese exporter must eat the tariff or try to sell their product at a price above what the going rate is compared to the prices of other competing non tariffed exporters like S Korea or Japan. And that doesnt work.

you know, that works as long as there are competitors to Chinese made goods.

Guess which country is moving into automation faster than the US.

Paulo: “Tariffs are simply a consumer tax.”

Wolf Richter: “I LOVE these tariffs because YOU get to pay OUR taxes. Hahahahahahaha…”

Tariffs raise the price of lumber by reducing competition amongst suppliers, regardless of whether those suppliers are foreign or domestic. It’s not “how a marketplace works.” To argue that tariffs aren’t “simply a consumer tax” is to presume that the taxes are fixed and inevitable, and thus taxes collected on foreign goods are offset by taxes not collected domestically. That’s not how taxation works.

Burned timber harvesting in California forest fire lands is going gang busters feeding Red Emerson’s massive Sierra Pacific mills. If you see a logging truck with smoldering logs that would be his operation. We need the jobs for our loggers and mill workers – sorry Canada.

I say we invade ’em and take their logs. It’s not like they have a military to stop us. Heck, we are their military, eh!

It’s not that simple. The difference between the US price and the Canadian price is the tax that US consumers will pay. If the tariff goes beyond that the remainder is what comes out of the profit margins of the foreign supplier.

As a Canadians I find the actions of both nations involved to be truly disgusting.

Prices are set in the market place, not by costs. In terms of the price that a company can charge, it doesn’t matter what something costs. That’s the number one principle in business. If you don’t get that, you don’t get business.

Therefore the low-cost producer wins. That’s the number two principle in business.

By having to pay for tariffs, the Canadian producers become higher-cost producers — and lose profit margin. If they want to raise their prices to cover the tariffs, fine, then they’ll lose sales to their low-cost competitors in the US that don’t raise prices.

That’s how a market place works. Anything else is propaganda.

I agree with Wolf so far as the current tariffs go. However, Canadian lumber producers have been buying US assets for years and are beginning to dominate in the US market. Generally, they have nearly half their production in the US, which represents expansion during the preceding period of low lumber prices.

The strategy is to supply Canada and Asia from Canada, and to supply the US from local production. In true capitalist fashion, the jobs stay in the country of origin, the profits go to the shareholders in what is now a huge flow of cash and companies like West Fraser climb to the top of the lumber pile.

I actually agree with you, it’s just that reality is messier than that. In my industry we order PCBs frequently. Local Canadian, US, and even Taiwanese manufacturers are completely non-competitive by an order of magnitude with China and, this is the key point, they refuse to compete. So we go to China. Our government could tariff Chinese PCBs by 500% and all it would do is raise our costs and end up effectively taxing us. You would think that these non-competitive businesses could not survive and it baffles me how they do.

You mean if we didn’t have environmentalist who are dead set against logging even if it was good for the environment?

I’m assuming there is a payoff somewhere to these guys by the Canadian lumber industry, just as the US lumber industry is paying off someone to keep the higher tariff.

Been to a few opens houses in Scottsdale lately. Almost no one at the few we’ve been to. Not the experiences we were told about in the media. Did we just miss it and now buyers are holding back? I was worried there’d be a dozen cars at each open house, but we’re definitely not experiencing that.

I’m not sure if we’re buying right now because I’m skeptical we can find what we want for our price and we’re not getting caught up in this stupid mania. Even if the market doesn’t turn and we’re further priced out. Better not to be rash. If we manage to find something we can afford and we love maybe we’ll buy. No hurry here.

Arizona, and Phoenix in particular, does not have the water resources to support the current population into the future, much less a growing population. Lake Mead water level – dropping. Lake Powell water level – dropping. Snow melt into the Salt River – decreasing. Water table – dropping. Rainfall – decreasing. Temperatures – rising.

The Southwest is not experiencing a mega drought, this is the new climate. Unless someone builds a pipeline to the Great Lakes that place is doomed.

The Phoenix area is approaching an era of severe decrease in habitable population. Anyone paying top dollar to live in the Phoenix area is whistling past the graveyard and in severe denial. Phoenix will be the Detroit of the West – the population needs to drop (a lot).

MLH-don’t be a buzzkill. Don’t you know freshwater always comes from the faucet? (sarc-on. Your comment applies, more or less in the foreseeable future, to all of us here in the American West… Or, in the words of the immortal Sam Clemens: “…whiskey’s for drinkin’, water’s for fightin’ over…).

may we all find a better day.

Saw a hearing on this Billion $ pipeline Las Vegas wanted to build to southern Utah. (don’t know if it was ever done)

Anyway this old time farmer from the Utah area targeted, stood up and said, “OK, let me get this straight. Yer gonna spend $1B for this pipeline, and carefully monitor our ground water, and if it drops, yer gonna shut the whole thing off? Vegas Water lady leading meeting had nothing much to say, and changed subject.

When I was living with lady in Tucson ’09-10, she said they expected (and built homes like crazy till GFC) 10-15M people in Phoenix-Tucson corridor, and “proved” there would be water for all.

A new survey just out from bankrate.com says that 2 thirds of the millennials that purchased a home have buyers remorse and believe they made a mistake. A main reason was repair and maintenance costs way beyond what they expected or could afford. I guess buying with online viewing and no inspections or contingencies didn’t work for them. “ hey dude, bidding up the price on a 90’s McMansion covered in Dryvit with failing plastic pipes is a bummer.” I expect this is one of the boat anchors dragging the market RE market down the last 3 months.

This problem is HUGE and understated. Most can’t keep up typical home maintenance costs due to overextending themselves with these stupid low interest rates. There are “housing bombs” all over this country with homes for sale that have been poorly cared for that will rap thousands in losses for those that buy them.

Even if not in bad shape now, what happens when in 5 or 10 years they need to take out a substantial loan for really big repairs? Even more of a concern, what happens if they’re upside down too?

“…and that old house we lived in, the roof is cavin’ in, like every other one along the block. Took thirty years to pay and ten to rot. Now Dad says it’s all better just forgot…” ‘home sweet home (revisited)’-rodney crowell

may we all find a better day.

Yes, this is a not often mentioned but important point– the true carrying costs of a residential property are often overlooked when starry-eyed buyers (like naive younger generations who are good with electronic gadgets but would hold a hammer at the wrong end) only pay attention to the monthly nut (cost of mortgage payment) and not the total expenses picture.

“Gee Honey, how could we possibly have known that this beautiful house we overpaid for would need a new roof and HVAC so soon. I feel hurt, and need to go to my safe space”.

So it bites harder when they overbid and overpay for properties that have defects anyway (and if inspection was waived there could be some very nasty surprises in store indeed).

Beside ongoing maintenance, one needs to be mindful that rising house prices means rising taxes and other fees on real estate. Assessed taxes after purchase will immediately jump if they and their new neighbors are in bidding wars.

A newly purchased house often means new household formation with everything that entails– new furnishings, renovation, and appliances. More often than not, the lady of the house will ensure every purchase for their new nest will be more than adequate.

After a decade of fast rising property taxes, our State legislature promised to pass property tax relief this year. Their bill increased the exemption on all homes.

The county assessor simultaneously announced the appraised values on the median home was being raised 25%. The net result will be the relief people were expecting is now going to be a raise of $350 this year on the median priced home…

I expect this will happen most places, and insurance rates are going up substantially too.

In a boom cycle, greed always reaches a fever pitch, and everyone starts piling on, governments included. Maintenance and carrying costs rise exponentially, forcing many buyers into hardship and financial desperation. We seem to be at that point now..

What state is this?

Could be almost anywhere, but sounds just like Idaho.

I know that in Boise the assessor’s valuation increase is expected to average 28%. State legislature rammed through (without debate) a “homeowners exemption” increase of $25,000, which equates to about a 6% median valuation discount. So a net +22% to assessments.

Couple that with the city raising it’s levy rate by 20% and the county raising its levy rate by 12%, the local machine is set for a windfall that they are unlikely prepared to spend.

The median homeowner, on the other hand, is looking at 40-55% increase in taxes due.

Probably no big deal for all the tech-refugees, bitcoin millionaires, and retirees lugging around suitcases full of west-coast equity that drove this particular madness… not so great for local families who thought they were buying a home well within their means in 2019 or earlier.

Progress!

Wow! I would have said something along those lines ages ago if I thought people who were taking the adult step of buying a home HAD NO CLUE!!!! Has no one watched those flipping shows and wondered how they did such a huge reno in only four days? Or at least gave a thought for the poor bastard who bought it? I swear, sometimes I wonder how these people made it to adulthood without taking out a Darwin Award first. I have an idea for a new meme; the Powell Award for the stupidest financial decision you ever made.

Mine is not getting into the stock market in 2009. Or not getting into the housing market before RE Bubble 1. Oh gee, that was when I was too busy being a twenty something. Regrets…

Went tire-kicking in various parts of Austin, exurbs of San Antonio three weeks ago. In prep for my trip from CA I favored about a dozen homes on Redfin, went to a few. Today in less than a month every single one of them is on contract, several already closed with all-cash offers. And I have a budget of low 7 figures with my CA property.

I’m sitting out for at least half a year to let things cool.

Millions to spend and nothing to buy.

That’s very sad.

No, just too smart to buy right now.

This person has the patience to ‘wait it out’ and will hopefully pay a lot less because they waited for the FRENZY to stop.

Please, I must live under a rock, but where TF is all this mega cash coming from? I know it’s always a factor but without foreign money launderers, I mean buyers, what accounts for that volume? Asking for a friend…

The fed printed $5 trillion…..

The Fed is printing $40 Billion per month and shoving it into the the residential real estate market at low, low rates. Divide that sum by the number of homes sold every month and you will have the answer to your question.

I don’t know whether the Fed is incompetent, corrupt or both but they seem hell bent on pushing us off a cliff and there seems to be no stopping them. Powell said he is going to do it and he won’t listen to reason.

whatever,

I hear the RE tax increases in the area are brutal 20-50%+ for new buyers. Was that a consideration for you?

Your budget is in the low millions, and you cannot find anything in Austin, Texas… I think you are doing something wrong.

Or, are you counting decimals as two digits?

By low seven figures I mean 1.5M. Was looking at house on golf course north of Austin. Looked at it the Friday it went on the market. Sold the following Wednesday for 1.6M cash.

Anything on a lake in or near Austin is easily over that.

it is certainly the most distorted and perverse housing market I have seen in my lifetime.

And it seems to be unwinding, which is not a surprise.

Tom…

Indeed. And why? Fake rates by the know it all Fed…destructive Fed….

Real rate if you lock it in. You can say all you want but all my friends have ~3% mortgage rates. So we are all happy to have these fake rates all the way to the bank with some of the cheapest loans seen in generations. The price of the homes is outrageous but so is the rate. Cheap money is best used not confused

2.99 here and never selling. I can rent the overpriced house I bought at half the going rate and I’d still be able to cover the mortgage with it.

Meanwhile inflation is turning cash into dust.

Do you think lenders will be content getting a 3% return on mortgages being issued today when tomorrow interest rates rise to 4-6+ % in an inflationary environment that may reach double digits?

Lenders won’t take it sitting down. In a currency reset (very likely to happen) existing debts will likely be also reset accordingly. That means a cozy 3% rate will get adjusted upwards for parity.

“Meanwhile inflation is turning cash into dust.”

Weird. My cash has gained over 50% against Bitcoin – a supposed store of value. When all other asset prices crash (I don’t actually believe Bitcoin or any crypto is an asset class), my cash will appreciate like never before seen. Do you always declare victory during the 3rd inning of a 9 inning game?

Heinz – you are correct. That is why the GSE have purchased or backed 97% of all originated loans since 2010. Banks do not want to hold a 30 year loan with artificially low interest rates.

My feeling is the turning point for home sales was the cutoff of extended unemployment in over 20 states. I see this as unleashing inventory into the market because the jobs are not really there and now the survival income is gone too.

Point in case, actual situation:

Step daughter-in-law (divorced) has been unemployed since 4/2020. Oil & gas accounting work is not coming her way. Since the state has shut off the Fed UE extra, she is going to have to sell her mortgaged house soon and move into an apartment. Even with forbearance, she can’t make the bills on just state UE and she has already tapped her 410K.

I’m sure there will be more like her.

It sounds like she’s got that mentality where she refuses to take what’s available until she can get what she wants, cutting her nose off to spite her face.

DC, there are no oil & gas jobs for a 52 year old women right now. And a clerk job in K Mart won’t pay as much as the UE she was getting. Even now, with a min wage job in her future, the house must go as the payment/insurance/taxes/etc can’t be covered by $8.50/hr. She’s SOL right now.

If you think in terms of opportunity costs, wasting your time getting 15 hours @ minimum wage with a schedule that never allows you to take a second job, is definitely a non-starter. Add to that the age and gender bias against women over 50 in the job market (men are still readily hired at that age), and I can imagine Anthony A.’s step DIL is in a world of hurt right now. The best she can probably hope for is to start up an accounting business of her own.

Are there accounting opportunities in other industries?

I know someone who was a nonprofit accountant, lost their job, delivered mail for sometime then made a transition to business accounting. Their new employer was okay with them learning on the job which was nice.