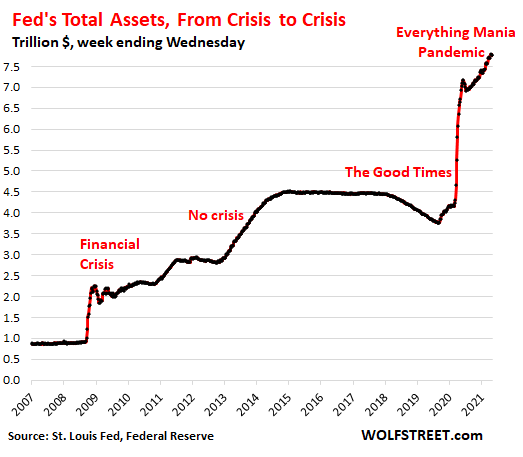

QE from crisis to crisis, and even when there is no crisis.

By Wolf Richter for WOLF STREET.

The Fed’s total assets on its balance sheet for the week through Wednesday, May 5, fell by $10 billion from the prior week and by $40 billion from the record two weeks earlier, to $7.77 trillion. Over the 14 months since the crazy money-printing show has started, the Fed has piled $3.53 trillion in assets on top of its existing mountain.

But wait… Since the repo market blew out in September 2019, this can-do Fed has added $4.0 trillion to its balance sheet, more than doubling it in 18 months. That’s how nuts these efforts have been to bail out the biggest speculators, inflate the biggest Everything Mania, and create the biggest wealth disparity America has ever seen, all of it in the shortest amount of time:

But the Fed has let most its alphabet soup of bailout and liquidity programs expire, run off, or languish on ice. Some of them are now zeroed out. What the Fed is still buying in large amounts are Treasury securities and residential mortgage-backed securities (MBS) amid this red-hot-crazy Everything Mania, from cryptos to housing.

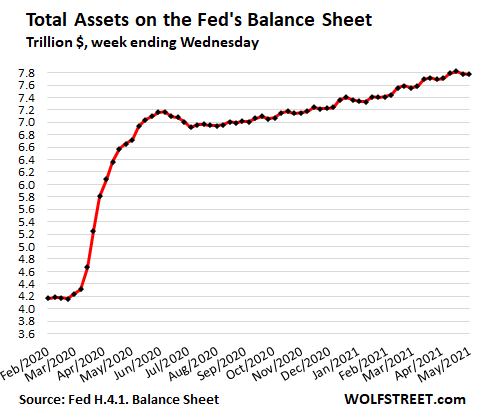

This is the detail view of the Fed’s total assets since early 2020. The $40-billion dip over the past two weeks is barely visible amid the pile of trillions:

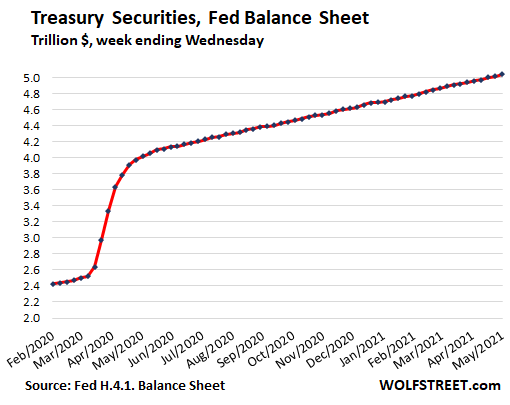

Treasury securities breached $5 trillion.

The Fed has been adding Treasury securities at a steady pace of around $80 billion a month, following its initial blast last spring, bringing the 14-month total addition to $2.54 trillion, more than doubling its Treasury holdings over the period and breaching $5 trillion:

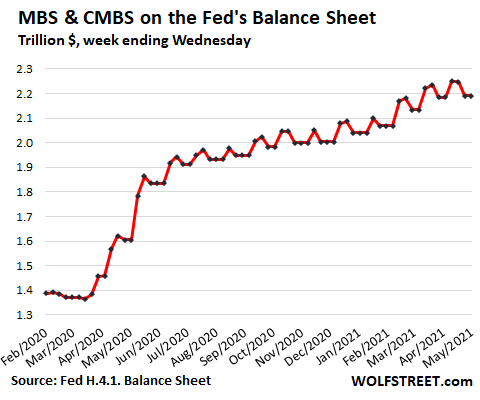

Why the heck is the Fed still buying any MBS?

The US housing market has spiraled totally out of whack, and yet the Fed keeps adding mortgage-backed securities to its pile, now at $2.2 trillion, to push down mortgage rates and pump up housing prices.

The MBS balance moves in a weekly zigzag. Holders of MBS receive pass-through principal payments as the underlying mortgages are paid down or are paid off. The Fed buys MBS in the “To Be Announced” (TBA) market to replace the pass-through principal payments and to increase its balance. But trades in the TBA market take months to settle, and timing differences create the zigzags. It’s the trend that matters.

Since July last year, the balance has increased at a rate of about $27 billion per month:

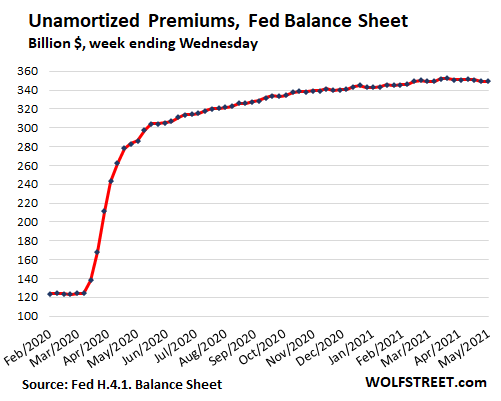

$350 billion in “Unamortized Premiums”

OK, here we go down into the rabbit hole of bonds. The Fed’s balance sheet shows $350 billion “unamortized premiums,” which have been declining in recent weeks. They track the premium over face value that the Fed has paid for the securities it bought in the market. When these securities mature, the Fed receives only face value. The premium then vanishes. The Fed tracks this difference separately.

Every bond investor who buys bonds in the market goes through this. During this time of low interest rates, when you buy a 10-year Treasury security that was issued a few years ago with a coupon interest payment of $30 a year per $1,000 bond (3% coupon), you’re going to have to pay a premium to get these $30 coupon interest payments. And when the bond matures, the premium is gone, and you only get the face value ($1,000) of the bond.

The Fed tracks this separately. As these bonds mature – these are Treasury securities and MBS – the premium that the Fed paid for these bonds goes to zero.

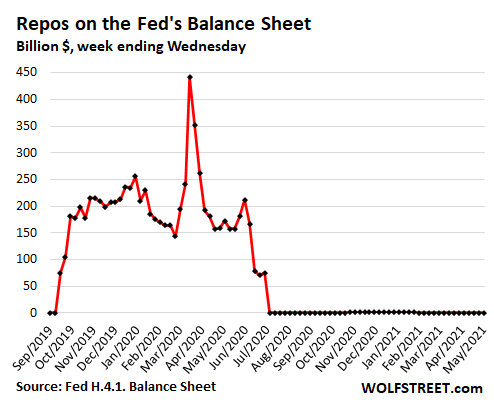

Repurchase Agreements remain at zero:

The Fed still offers repos, but at a bid rate that is not competitive with the market, and there have been no takers since last summer, when all repos matured and unwound, with the Fed getting its money back, and counterparties getting their securities back:

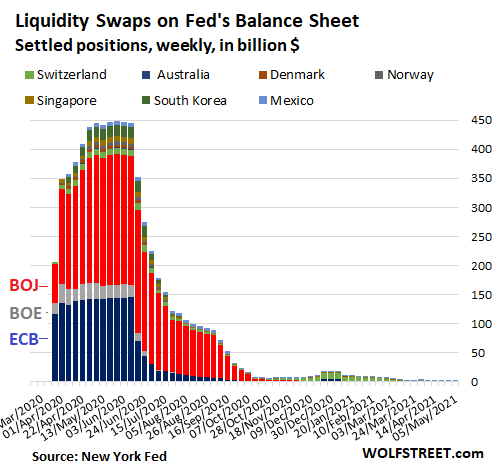

Central-bank liquidity-swaps drop to near nothing.

Under this swap program, which still exists but is no longer used, the Fed offers dollars to 14 other central banks in exchange for their currency. Nearly all these swaps, which peaked at $450 billion last June, matured and were unwound:

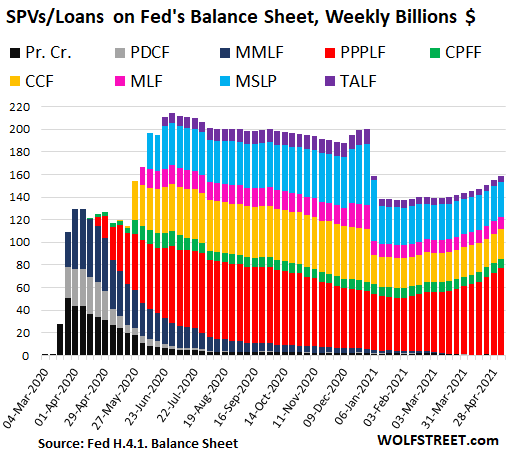

The SPV alphabet soup.

In the early weeks and months of this craziness, the Fed created Special Purpose Vehicles (SPVs) as legal entities that can buy assets that the Fed is not allowed to buy otherwise, including corporate bonds, even junk bonds, bond ETFs, junk bond ETFs, auto-loan backed securities, municipal bonds, corporate paper, PPP loans, etc. The Fed lends to the SPVs, and the Treasury Department provides equity funding that would take the first loss.

Most of these SPVs have either expired or are on ice, with balances declining or having already fallen to zero. The exception is the PPP liquidity facility (red), which the Fed extended through June. This SPV buys PPP loans from banks and is still growing, now at $76 billion, bringing the total value of these SPVs to $158 billion:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

While I was reading the article I asked myself, “Why is the Fed still buying MBS”? Then, the very next heading was exactly that, “Why is the fed still buying”……

I then read on in rapt attention, but the article did not say why the Fed was still buying MBS.

From the article: The US housing market has spiraled totally out of whack, and yet the Fed keeps adding mortgage-backed securities to its pile, now at $2.2 trillion, to push down mortgage rates and pump up housing prices.

So why? Do they want to make people homeless? I don’t get it.

My guess:

1) The Fed’s policy is causing house values to rise rapidly. Having a greater percentage of houses across the country that aren’t underwater will make dealing with delinquencies and the eventual end of the moratorium much easier.

2) House price inflation immediately gives homeowners access to extra cash (HELOC) to spend into the economy.

3) They are truly evil people who get pleasure from the suffering of the people who fought the Fed and saved instead of took on mountains of debt.

In the interest of “boots on the ground” (and it’s corollary “more personal stuff”) so you better know who you are talking to and where they are coming from, I had a short dialog with Dan Romig recently about it. A lot of people you sorta know here, as they are open about their life, but the vast majority you just know who or what they favor, blame, hate, fear, predict, etc, etc, from hearing it over and over. Wolf’s long ago meeting was an attempt at that. I WILL not drive to the city, and like Alex in Silicon Detroit, or whatever, felt most would be out of my economic league, so we wouldn’t have much in common. But a lot of people are pretty open, as is Wolf himself.

I looked again at that wealth inequality chart. To me that is even more INSANE than the Fed data above, which is all some variation on printing money, or playing with interest rates that force other INSANITY. And the market is at 4232 now, which is also REALLY INSANE.

So, I’m getting to where I can usually stay pretty loose about all this (took a while) as I’m 74, retired, no debt, ridiculously well downsized and have been totally immune to ALL advertising and “keeping up with the Jones’s” since stereo came out. I figured screw it, my transistor radio sounded fine since HS, and still does, the exception being when I was married, and after that rented a house and then bought a mobile home with my fiancé. I’m not a nest builder, but I get how women are. But with excellent health, other than bad back, I figure I have enough savings to make it another 8-10, even if I have to sell my off-grid land. And no slow death for me, and I’ll make my own very well informed medical decisions. I spend a lot of time staying current with all things Bio.

But what about all those not so fortunate, or younger, or still working, and still worse off economically than me? Will civil unrest of all forms including low level crime get worse? Will white collar crime get worse? That’s why I go on and on about a MASSIVE Green New Industry, Conservation Industry, and the needed educational support. If we can keep pissing money away on insane things, then we can do that. I see no other rational move, unless just “waiting” and fighting fires is a rational choice.

Just a note on advertising immunity. The ads are getting just as interesting to me as the “content” on TV. I guess at who and how they are “aimed”, and so it’s just another Technology to learn about. Without my lifelong love of learning, I’d probably just drink or get addicted to a LESS toxic chemical, like opiates. And yes, what I just said is true, any chem or physiology expert will tell you ethanol in the drug world is considered “crude protoplasmic poison”. A well nourished and safely supplied opioid addict can easily live to to 80 (and many have), an “alky” staying equally high on their chosen “downer”, cannot, no way in hell.

PS, another damn good article…..that nothing goes to heck in a straight line stuff is becoming kinda tenuous.

Rumple:

Or is the FED just supporting the vast amount of real estate purchased by the very large financial houses re the post ’08 crash????

And I don’t understand the SPV creation by the FED to maybe lead to another “Enron 2”????

I’m basically a “capitalist” but this is just insane! We are continuing to take away the different counter forces in the capitalist world so as to avoid any inconveniences to investors???? Or even house flippers????

“I then read on in rapt attention, but the article did not say why the Fed was still buying MBS.”

Somebody just asked Weimar Boy Powell that very question in the past couple weeks. Since Wolf does not allow links I cannot post the video, but here is his response:

Stammering: “We started buying MBS because the MBS market was was really experiencing extreme dysfunction…and we sort of…we sort of articulated uh…uh…you know what our exit path is from that. It’s not meant to provide direct assistance to, uh, to the housing market. That was never the intent. It was really just to keep that, uh, its, it’s, it’s a very close relation to the treasury market and a very important market on its own, and so that’s, that’s why we, we bought, as we did during the global financial crisis, we bought MBS too. Again, not, not intention to send help to the housing market which was, which was really not, uh, not, not a problem this time at all, so, um, and you know it’s a situation we will, we will taper asset purchases when the time comes to do that and those, those purchases will come to zero over time, and that time is not yet.”

As you see, this clown was stammering all over place, lying through his teeth about what they’re doing. They’re blowing a housing bubble on purpose.

They knowingly blew a housing bubble in 2002-2008 too … how did that work out?

What’s that definition of insanity? Doing the same thing over and again expecting a different result?

Oh God.. Thanks for that info DC. Now I just want to throw up.

DC, can you give more of a hint, maybe the date the video was taken? I want to find it. A quick cut n paste is not bringing it up.

Lynn,

The Fed has its own YouTube channel, and you can get all its videos there, including all the press conferences:

https://www.youtube.com/c/federalreserve/videos

The housing bubble may be linked to: migration out of apartments, condos and cities after COVID, desire for more home construction in areas of growing population, rising cost of supplies due to COVID disruptions, hoarding lumber, speculation in commodities, land and finished houses, growth of Airbnb vacation rental ventures creating demand for houses that are held vacant off season, etc.

Some wealthy politicians own two or more homes. There are many empty bedrooms in America due to a desire for real estate as an investment.

The housing bubble may be linked to: ‘WHAT IS WALLSTREET? WOLF’ originally private equity (but we know where it came from)

YW, Lynn. It was from a guy named Tyler Neville who posted it to his Twitter feed under the comment “Watch Jay Pow stumble over this question of why they are buying $40 billion a month in mortgages when there is a dearth of supply in housing.”

By the way, I should have added that they’re not just blowing a housing bubble on purpose, they are positioning themselves to hold all the paper on these garbage loans that are being doled out like candy, and when it all comes crashing down they can control the inventory – the actual houses – in order to try to control the whole market. Yes, the FED is now in control of your shelter. Now if they could just figure out a way to do it with your food.

Lynn:

zero hedge posts the videos of every Powell’s presser – you can watch real-time but the archive should also be available. Check there.

Lynn – go to 50:40 in Wolf’s link.

He talks out of two sides of his mouth and lies out of both sides at the same time.

Congrats POS weimar Powell, you have managed to be the most efficient FED chairman in history to add trillions to the balance sheet and blew this bubble bigger than ever in the shortest amount of time. You are making efficiency at all cost obsesses corp america jealous there. Sadly you will never suffer the consequences of your action in this lifetime and your successor will probably have to deal with it long after your exit.

It will be quite a funny show when FED tries to slightly unwind some of the balance sheet behind the market’s back. Couple of days of hundred plus points drop is all it will take for that pedal to the medal mode again, race to that double digit trillions balance sheet. To infinity and beyond!

real reason why jerry is buying MBS

cause BANKSTERS WON’T LEND $1 to anyone on mortgage

so FED HAS TO BUY BUY BUY as don ameche would say

bankster told me today that they expect mortgage rates to PLUNGE OVER NEXT COUPLE MONTHS into sub-3% on 30 year

and maybe sub 2% on 15

to bad I WON’T QUALIFY with all my assets and cash

they like w-2 suckers though

Swamp Creature (and others):

It is worthwhile to note that the head of the FED has thousands of (supposedly) highly intelligent economics people giving him/her advise. That is truly scary; that being so then we are really in deep doo-doo!!

You are taking me out of context!!!!!!! It all makes sense if you quote me up to the next “uhhh”!!!!! I do this all for love, people!!!!! I love myself!!!!! And I love money!!!!! I love printing money!!!! BRRRRRRRRRRRR!!!! And I love the congressmen who give me money under the table!!!! I do this all for LOVE!!!!!!!!

‘Overall, the Fed said the current state of the system is sound, with household balance sheets in good shape, and corporations supported by an improving economy and low interest rates that have allowed default rates to fall.

Even the $1.7 trillion in student loans pose “limited” risks to the economy, given that most education debt is held by the top 40% of earners.’

The last is kind of funny. The good news: in this context 1.7 T is only a few months debt increase. The bad news, most of this debt will be written off. It is an illusion to list it as an asset.

So, in essence, we have free college education in the US. Student uses gov loans to pay the colleges, gov forgives the loans. Colleges get paid, student gets free degree.

The Fed causes land, real estate, and stocks to go higher benefiting the 1%, and cause the price of food, rent, and gasoline to go higher causing hardship for the bottom 80%. The 19% in the middle are lucky to break even.

If you are a home owner then you most likely have benefited. Not just the wealthy. Anybody who had a ~250k home in California pre-COVID now approaches ~$400k (have a friend*). Jet fuel goes caviar and the apartment buildings also go UP in price

BUT, the price of all housing has gone up as well, including rents……. so it is a zero sum game. Also these Fed policies have made everything more expensive(huge inflation/dollar decimation) so even if you make money on your house it gets eaten away.

Home price inflation, Nathan, is only a windfall when you actually sell (finding one of the dimmest buyers of the century!), AND DO NOT REINVEST THE PROCESSES IN POSSIBLY AN EVEN MORE INFLATED HOME, with a price that eventually will go over a cliff. Only cash is a profit, on-the-books profit is imaginary until TAKEN. Same with the crazy-arse stock market.

Benefited???

What does this get you. Its still the same house. Just a number on a piece of paper. Celebrating the appreciating value of their home when they’ve gained nothing in terms of quality of life. The home didn’t gain in value. Their dollar just lost equivalent value. And with property taxes going up with the new assessment, so you actually lost money.

The American people have turned into lemmings. Celebrating the loss of purchasing power of their salary, savings and pensions.

“If you are a home owner then you most likely have benefited.”

It really only truly benefits housing speculators who buy and sell (or hold or rent it for now) to capture transitory but rapid price appreciation gains in this insane housing market.

Homeowners who stay in their homes are paying out the wazoo for property tax hikes, and presumably rising homeowners insurance premiums. If they take out a HELOC or other debt against their house equity they are gambling there will never be a housing price decline and they will always have income to cover it.

Illinois may be an early sign of what rising property taxes eventually do to house values. Property tax bills in that state have grown six times faster than household incomes. And that is causing a negative effect on property values and housing demand.

For homeowners that want to move and buy another house– they find it is indeed a zero sum game because other houses on market are just as jacked-up expensive as their current one.

Meanwhile, many aspiring first time homeowners are shut out of the market because of the artificially pumped up competition (bidding wars) and unnatural withholding of inventory, so they are simply priced out. (affordability).

Joan of Arc,

Traditionally the 9%ish right below the top 1%, do quite well when a country is run for the interests at the top. The so called professional class is made up of people who hold important jobs within the economy and they typically rig the economy for themselves and their family. In present day America, many studies have shown that America follows the path that the top 20% (upper middle class and above) thinks is best, many decisions that get made by or for the top 20% are, however, counterproductive and can backfire. The top 10-20% in a modern country hold a lot of power, because they can influence the country through their job and other means (such as their income). The top 20% in America make more than half of all the income (the top 1% makes about 20% of all income). The top 20% hold about 75%+ of all wealth (the top 1% holds about 30%+).

In looking at class dynamics for America, there is the top 20% and the bottom 80%. That 19% in-between runs along with top 1%.

Because America is so spread out and the income levels are so different across the country (and vary by age and changes in marital status), the top 20% for America, is more difficult to define then merely the top 20% total in the country. In general, America is run by and for (these groups overlap) the richest in the country, the richest 20%ish in each state and city, and by a handful of professions (mostly public jobs) such as teachers and cops, who hold substantial influence through their jobs, even if they don’t make it into the top 20%; and a handful of activists and influencers (this includes experts who make it onto news channels, many who sell a successful book and many others), who also may not make into the top 20%, but also influence the country. Not everyone in those groups can, knows how to, or cares about exercising their power, but, America is run almost entirely by individuals in those groups. About 80%+ of the population hold zero political power (they simply are unable to, even if they wanted to) and the country is not run for their interests.

The 19% hold alot of stocks and most are retired or are nearing retirement. They better hope stock prices can hold, if they don’t, the entire top 20% will lose alot.

Speaking of teachers and cops and their power to influence, we just had a millage vote. Was to build a new ‘Justice Complex’ and school upgrades with a computer for all students.

Shot down big time. It may be that that influence is waining. MY state got 2 billion covid funds from Washington and maybe the voters feel that enough is enough.

endeavor,

I stopped voting for increases for cops and firemen when I moved to south Florida almost twenty years ago. Back then the average cop was already making over 100K and the firemen/rescue was at 113K with a minimum of 3 to a truck. The average income back then was ~30K. Now you can watch videos of them where six or seven show up at a traffic stop to justify their jobs, ridiculous.

A news article today said that the population in Miami-Dade County and Ft. Lauderdale-Broward County has over the past year has dipped slightly. Yet most news stories seem to tell you that Florida real estate is booming, that Palm Beach mansions are selling for record prices. There is a whole lot of new home construction going on in South Florida, of course, but could it be that reporters are just being stenographers and repeating what real estate pitchmen are telling them, to encourage home buyers to head South? If the Fed had stepped in and brought home mortgage backed securities in 2008 instead of standing by the sidelines for the most part as TARP funds bailed out the Big Banks and Wall Street, the crash then would not have been so deep. I get the impression that all the news you read on the Internet sites like Yahoo and MSN is news filled with half-truths, lies of omission. 25 years ago, I was by the Broadwalk on Hollywood Beach watching a city employee by one of the palm trees there. I mentioned how nice the palm tree looked. He said not so nice if you had to check the tree top, as he did, to see if rats had gone under the fronds and eaten the palm fruit. And now we are heading into the hot Florida summer season, which is okay as long as the power company can keep up with the air-conditioning demand. I think you really have to have a high index of suspicion whenever you read press releases from the private Federal Reserve Bank.

They are raising some street levels in Miami two feet. What does that tell you?

In the next 50 years rising sea levels will destroy much of the most desirable real estate in Southern FLA.

And so driving is then possible there, great, but where does the water then go? It won’t disappear.

Paulo,

Boston Fed governor Rosengren was asked that very question today (well Thursday) — “Why is the Fed still buying MBS?” — which is why I put it in the article, and he didn’t know either. No one knows. It’s just part of the program, and the program hasn’t been changed, and everyone is scared that changing the program will cause a market tantrum.

It’s the same answer for the question, “even after so many mistakes, bubbles & busts why do we still need the Fed?”

Just because it’s been there as far back as anyone can remember and everyone is just scared of changing the status quo.

Isn’t this a great time to get rid of that cancer and bring everything back to reality?

Our government is very seldom pro-active..

Always waiting for the cover of a Crisis to make changes..

Congress runs on Corporate Donations so the CHANGES have not been anything other than to bail out Congress’s Corporate Sponsors.

Not since the BIG One in 1930’s has there been a big enough crisis that really reduced the speculative fervor and greed driven banking and corporate sectors.

Still waiting for the inevitable.

It is obvious to even the most casual observer that the Fed and the Treasury are “ joined at the hip” as Henry Kaufman recently said. Getting rid of the FED would solve nothing because the same disastrous policies will continue until by the government .

“No one knows.”

Yup, that sounds like our government, in response to a whole litany of legitimate questions.

As we all know salaries in the US stopeed increasing in the 70’s, and all of the women who can work now work, and everyone who can get a side-hustle has one. So now the only thing left to keep the economy running is credit growth, and as most of the population is maxed out then we have only rampant house price growth to keep cash flowing to home owners. Hence the FED buys MBS’s.

Sounds like Greenspan 2.0. when he was peddling this bull s$it in 2003/2004. Remember him touting home equity cash withdrawals and using homes as ATM machines as the primary driver of consumer spending. He had 150 Phd’s (Piled high and deep) advising him that this was sound policy. After they hang

J Powell as DC proposed they should save some extra rope for the Miestro, and maybe add Bernanke in there for good measure.

Cute insult. But there are also PhDs I’m Bio Chem and Molecular Biology and Food Science and you are swallowing ALL their “policy”.

The fed is buying MBS because Wall St won’t buy them. If MBS was profitable with an acceptable risk level(low to average chance of default), Wall St. would be buying them all. The smart money can see the risk in MBS and is staying away.

I like Petunia’s answer.

It isn’t sound business it is politics. If th MBS market tanks thent he housing market tanks and as I said above the US economy , and the UK economy, and the Spanish economy are massively dependent on a booming housing sector. The German economy not so much.

With the weak jobs number maybe the Fed will increase QE?

Ambrose Bierce,

My gut feeling is that the weak jobs number was due to seasonal adjustments gone awry. We’ve had a lot of those issues over the past 12 months because the whole economy is out of whack and normal seasonality, which is what seasonal adjustments are based on, has been upended. If I’m right, we should see a big jump when the seasonal adjustments revert.

To all:

The FED needs a serious “time-out”!

When you can create currency like the FED, you can buy anything you like. Buying MBS’s is like buying houses but without having to buy the houses themself. The FED buys the obligation that the mortgage taker will work to pay the mortgage, or hand over the keys. The FED can sell that obligation anytime, or the house if the poor owner of the house can’t pay up any more.

Imagine there comes a great reset and some new money emerges. Lets pretend it will be gold again, just because we can reference to that easily.

Then the FED effectively has bought houses with Fiat-currency and after the reset can sell the assets for the new money, which in the example is gold.

You might ask yourself why not create currency to buy gold directly? Firstly that would be to obvious. And being what it is, it wouldn’t be possible, because the FED can only create dollars if somebody takes out a loan (an obligation to pay back). Currency is in principle somebodies promise. Gold is nobodies promise.

Secondly, who says the new money will be gold? Maybe even the FED is not sure what it will be. It could be anything.

So MBS’s are an intermediate way to sit out the reset.

J Powel is not lying when he says the MBS’s the FED holds will go to zero someday. But will the FED sell the MBS’s for the dollars it itself brought into existence in exchange for a promise to work for it? Or will it exchange them for whatever new money/currency? Be it a promise, a tangible thing like precious metals, or something virtual like CBDC’s.

Time will tell.

In the mean time i choose to sit out the reset with PM’s in my possession and a loan free house.

You said “because the FED can only create dollars if somebody takes out a loan”

Incorrect!

Banks can only create dollars if someone takes out a loan.

The Fed has much more power.

The Fed pays its own employees and its own budget with printed $- thus they can claim independence from Congress and immunity from theatrical govt shutdowns.

The Fed owns the transfer system and processes checks between banks so it can theoretically wire any amount of $ to any account it wants.

The Fed controls the banking transfer system and the Fed doesn’t have to do double entry bookkeeping and the last effort I heard of to audit the Fed under fake fighter Reagan was joke.

I would add my opinion that the Fed’s existence is a direct violation of the Constitution- it is illegal and if the USA ever elected a president who read, understood and cared about the Constitution such unicorn of a President could simply close the Fed and end it the first day in office.

+1000 rage of TX!

I had vowed to stop, after 20 years or so, saying we need to get rid of the Fed, but just have to add my upvote to your comment.

Especially the last paragraph!!!

Trouble is, our real owners will not allow any such person to be elected, and if somehow one slips through their very well constructed system to prevent a POTUS who serves WE the Peons instead of the rich and richer,,, well, we did get close recently, in spite of his obvious character.

At this point, it appears USA, and likely the entire world, will just continue to stumble along wreaking havoc with anyone who is behaving rationally, until the whole shebang falls apart.

Oh I would add:

Don’t just end the Fed, End the Fed and abolish the fractional banking system. . . I’m not sure if the lamentably ignored Constitution allows fractional banking or not. I hope/wish it does not.

It’s not just the Fed that creates fiat currency, in a fractional banking system your local bank does it too!

Are you allowed to create fiat currency? No? Well this is the biggest inequality I can think of today. Those who have powers to create fiat currency vs those that don’t.

Ron Paul for president.

We had our chance, but just like when they scared everybody into bailing out the banks, not many people want to deal with the dark reality of debt, austerity and admitting that we do not have to grow GDP and balance sheets to infinity. the math/statistics say QE will always cause dollar destruction and inflation. The ruling class owning the assets benefits greatly, and the working man and woman make less by paying more to live. We need to start over, and I don’t think enough people are ready.

If someone said they wanted to end the Fed were running for president, she/he would not get elected. Consciousnesses are hard to enlighten and change.

Never thought I would say “interesting and good comment” to someone who called themselves “Raging Texan”. Maybe it’s the redneck logger in me…..

Your second comment, mostly. I have a lot of other things I’d like bashed besides just the Fed.

“Are you allowed to create fiat currency? No? Well this is the biggest inequality I can think of today.”

Actually, you are. That’s what crypto’s are. You can make any fiat currency you want to. Whether anyone accepts it or uses it is a different discussion. What you aren’t allowed to do is make US dollars.

Fractional Banking is a license to print….and you can’t! Like the man said. The “amp-coin games” all pale in amounts.

Me too

CRV

“”J Powel is not lying when he says the MBS’s the FED holds will go to zero someday.”””

I agree with the concept on MBS that the expected re-initialization will be important and by now ineluctable to have a basis for evaluating the wealth of the country based mainly on real estate as well as raw materials, therefore the answer of not knowing and above all not wanting to tell the truth on the purpose to be achieved.

CRV,

I like your style and you sound very responsible. Policy makers don’t like it as they want leverage in the system to goose the economy. It’s economic PhDs who are so smart they can’t see the simple truths of how things work in the real world and now have fubared the real world most of us inhabit. Rewarding doge coin and killing mom and pop savers is one example.

Kind of like a reverse pawn shop paying top dollar for declining assets.

BigGov is ~30 trillion $ in debt;

the easiest way to pay it off is to ensure

that a rat-infested shack sells for 30 trillion $.

So the Fed keeps interest rates SuperNegative ( after inflation ), &

your only recourse is to spend willy-nilly, destroying the environment.

I think they are trying to save the dollar fiat system and they just have to keep using more extreme measures to do it. If 10 year goes negative it’s probably over and we will see what system the powers that be come up with.

Covid was an unexpected arrow and they had to double down on the policy. Savers still losing, gamblers still winning, short sellers still being shot.

How is this saving the dollar fiat system? If anything, they’re hastening its demise.

I think if there was complete price discovery people would get scared when asset values collapsed and zombie companies starting going under. Would not be pretty. Print to can kick and hope they can keep confidence going as long as possible.

Right, but they’re doing so by destroying the fiat system. People are buying assets at absurd valuations because they have no confidence in the dollar.

You got it exactly, old school.

“Why is the Fed still buying MBS”?

Maybe because they desperately need inflation.

And that they are so focused on their flawed models that they can not see (or care?) the consequences of their actions.

“Why is the Fed still buying MBS”?

Simply because they can, and it suits their purposes.

And they know no one will stop them.

A good question and a good guess at why as immediate “fire fighting”, and the “not till I get mine syndrome”. The wisdom of that syndrome. however is really up for debate.

Wolf put “what IS happening out, just the facts. Then along comes “creative insulting, blaming and bitching”….I guess. Don’t learn much from that, can get TONS of that from the “pros” on the cable TV channels.

Again I make the mistake of being at the front of commenting and point is mostly lost. Will just read rest of comments and wait a couple days.

Wolf, so I killed some time reading the “dead” articles and saw where you asked what I did with off-grid home I built ’90-’06. By ’03 I had taken out a Heloc I used to buy the adjacent 40 acre off-grid cheap BLM land, build roads, that I have now, with the 5 container home/barn started, that killed my back Sept 21, 2013. Spent time with girl in Tucson, then 1 1/2 years taking care of mom at sister’s and was stupidly back at it right after she died. Anyway, short answer: Sold in original 44 acres ’06, still unfinished, and as Paulo knows, you are never “done” when you have land, but I was realizing I couldn’t live that way forever, too much work, too far out there, and getting old.

That’s why my 500 sq ft apt is nothing short of a miracle, as heat, water, and power come out of the wall and I don’t have to do ANYTHING to make it all happen except pay rent and PG&E.

NBay,

Thanks for the update. I can see where life out there on the land, away from regular infrastructure, is tough unless you have lots of money with which you can solve lots of problems. Yes, I marvel every day at the stuff that comes out of the wall and without which modern life is really tough.

Wolf, it’s only “tough” after say 50, and at first when you have no shelter and bring everything up each time. Actually it’s calling your own shots that’s FUN, which is where this talk began, as you mentioned the fun of what you are doing when someone asked about your long “work” hours. I would still be there if I could have stayed even 55 forever, and life would just continue to be more fun….but that’s not how life works. Still, you get a really good feeling for what you really NEED to be happy…”grounded” as they say, which may be worn out but still very true. It’s why you swim, right?

The Fed’s partner, Blackrock, went all in on residential real estate about 6 years ago….

so…….?

When inflation was around (2.6%) in previous years….1999 and 2006, 30yr mortgages were 6%. Now they are 2.95%.

The Fed skews everything it touches.

Why not include Blackrock in the “skewing of things”. Why does it get a free pass and not the Fed in your summation criticism?

Why isn’t anyone screaming “Abolish Blackrock!”

As an add-on thought to that, when Teddy R was busting up the big Corps, the other GOP people said, “He’s out to get anyone with more money than he has”. Not sure how to use that in an oath of office, but, man, there has to be better limits somehow put on this present Corporate game.

Inflated housing prices result in inflated property taxes…

I think the Real Estate market has such a profound influence on consumer spending that the FED is reluctant to let it go in for a hard landing. All the purchasing that is taking place related to home improvement and other home related consumables is one of the few things left to really jack up the economy in the short term. It sure as hell isn’t going to be chipless cars.

Short sighted for sure, but that’s where the US is at the current time. Our wealth disparity and off shoring has finally caught up to us. The bifurcation of the economy in this continuing pandemic has taken hold and is not letting go.

The $1400 has been spent and the the unemployment benefits are good through the end of summer, but nobody knows what happens after that. Hence all this aggressive reopening performative behavior by insane Governors. This virus is probably in the locker room at halftime scheming its second half comeback. The India outbreak is more disruptive than people are giving it credit for.

Wellstone’s Ghost, This is an excellent comment and at least in my neck of the woods 100% correct. Having lived in our home for 25 years and in need of major upgrades we did a cash out refi last spring and summer. It wasn’t easy as retirees with no income stream to accomplish this feet. It took two different mortgage brokers and six months to complete the deal. Started our demo the second week of February still maybe only 50% complete. Everything including permitting is behind, have only received 4/7 appliances order the end of January. Hurricane windows order November are still not completely installed. Bathroom vanities and fixtures are scares. TG we order all of our flooring and tile for delivery in February. Home prices in my family community are up huge amounts, new pools, new roofs, new workout equipment in the garage. Early this week the WSJ had an article on The Gates upcoming divorce. Speculating on wealth and asset transfer. The had a picture of a house on Jupiter Island. Easy to find on google and actually listed with pictures still on Zillow. Virtually the end of the road. Purchased in 8/18 for $4M. Zestimate $ 7.27M. Thats 82% increase in 30 months. This property is so old, dated and need of a total redo that is must just change hands from one wealthy sec 1031 investor to the next. But it has a good address, 200 feet of intercostal waterfront and 5 acres of private land. Perfect internet site unseen sale. The bursting of the bubble scares me. Lot’s of little people will still get burned. I am in favor of the elimination of this non primary residence transfer of untaxed wealth.

India is REALLY bad off, but it’s the lack of simple supportive care and a poverty weakened populace that really does the most damage.

Still, the “warped speed” vaccines appear to be somewhat effective at present, and it is really a shame that we first have to argue about having “talks” to see if we can make the Bio Corps disclose proprietary info so India’s vast generic (and maybe on patent) pharmaceutical industry (my back pain pills come from there, they are from the 60’s) can make them. After all, under warped speed, the government paid for it all and even took the tail end risks for those Corps, so OUR democracy paid for them.

Simple humanity says why waste time and let more people die if we can stop or slow it, even if it’s just for now while more science is learned?

Side note: The original massive deaths in NYC were mostly due to a supportive care/public health awareness learning curve, and I’m sure the front line folks are all getting much better at it, and there is no way you can “warp speed” clinical medicine, or blame them or anyone else for any “failures”. (unless they were profiteering….piracy.)

It IS called the PRACTICE of Medicine, and always has been trial and error. It’s a real pity, though, that it and the science behind it is so damned EXTREMELY highly monetized…almost sick. (and absolutely NO pun intended.)

So the FED has doubled its Treasury and MBS holdings since before COVID. We are at 3 times the 2011 levels now.

This whole lending to yourself thing looks addictive. Maybe I should try this at home.

I lend to myself from my 401K all the time. Borrow too.

Andy,

If you don’t service your 401K loan, your 401K is lost.

If the FED holdings don’t get serviced, the dollar itself is lost.

borrowing from your 401 K????

The dumbest investment decision in human history.

I think the Fed learned one thing from the last two recessions. If they can keep the stock market and real estate market elevated and churning along no one thinks we are in a recession no matter how bad things are on main street, or how many people are living in tents. It works for a while but in the end it is like driving a rocket sled with no brakes in to a box canyon, the only outcome possible involves a big splat.

you know what a big difference is now? yellen at treasury.

even the veneer of independence is gone. this is government printing money to pay for itself.

Oh please….

Yep. Asset prices have become too important to economy. If asset prices get cut in half, confidence will be lost and economy will go into deep recession. Fed doesn’t want that.

Seems like they wanted assets to inflate first and now real stuff.

And this MIGHT have worked if assets were more equally distributed among the population. But they’re completely discounting the political and social effects of inequality.

Could almost make a case for teaching college economic students three branches of economics modeling; Econ 1%, Econ 90-99%, and Econ 0-90%.

I betcha the banking industry already does it, and also that their models are proprietary.

Been out of work for a month to collect money from deadbeat lenders (mostly shadow banks). A lot of the receivables were over 90 days overdue. Start back tomorrow working in the heart of the Swamp. Needed the break.

Looks like the real estate market is still holding up pretty well here. I see nothing for sale. Rampant speculation is continuing. People are holding on to second homes even if they are empty. As long as the Fed keeps buying mortgage backed securities money will continue to flow to this sector. Prices will continue to go higher and residential housing will continue to be even more unaffordable until no one can afford anything.

Bubbles will pop in November 2022.

Nonsense. Elections don’t dictate when bubbles pop. People said the same thing about last November. And then it was going to be January after inauguration, etc.

If anything, midterms may bring even more bubbles with deadlocked legislature.

I’m curious where Beardawg sees the dot plots and FED balance sheet in a few years. Any bold predictions there?

Nothing to do with politics. Math charts back to mid-1800’s reflect a bubble burst will occur, with 4 month margin of error.

I’m interested, what charts are you referring to?

Like in using the past to predict the future? I have no flesh in the market, but i doubt your prediction will work out. Can i remind you when I’m right? : ) Feel free to remind me when you’re right. : )

Up North

Ha-ha…thanks for laugh.

Judging by the trajectory of house prices and stock prices I think we might go a lot higher, but not a lot longer. Real dividend yield on stocks and treasuries getting more and more negative. I think Fed’s letting cryptos run because it takes some upward pressure off gold. Gold spiking means confidence in Fed is over.

They know there is no way out. The debt can never be repaid and must be either defaulted upon or inflated away by devaluing the currency. Of course their plan is inflation. But the problem is, they must create enough money to keep inflating the ever growing bubble while insuring that the real value of the total money supply in terms of commodities does not shrink. When the latter happens, the real economy also shrinks, which is what was already happening before COVID.

It’s like flying a plane. Under normal conditions putting the nose up makes the plane gain altitude. But you can only do so up to a point before the plane stalls and you lose altitude and control. To get out of a stall you need to put the nose down fast and gain speed before you hit the ground.

Mark my words: this madness ends when the FED and other central banks lose the ability to control the price of gold, oil and other commodities using derivatives such as futures and options.

The Federal Reserve has promoted cheap money, it shows in the stock market, housing, and many other things. The results are only a matter of time. There will be consequences.

Marbles,

Even the price of a bag of marbles will become unaffordable.

Joan of Arc,

I’d say that even one Marbles is already priceless.

“Even the price of a bag of marbles will become unaffordable.”

Such a shame, because so many people have lost their marbles in this market.

Wonder how cat-eyes will do against daters, and agates against peerys and steelies when their value crashes?

it is even worse in Canada. The whole generation is displaced from the market. Young people are leaving Ontario and moving to maritime provinces increasing prices there as well.

Federal housing secretary admitted that the market works better for foreign investors than local people, and apparently that is how it is supposed to be.

https://vancouversun.com/opinion/columnists/douglas-todd-canadian-real-estate-market-better-for-foreign-investors-than-locals-admits-housing-secretary

I came to Canada from Eastern Europe, and lived through some bad things there, including hyperinflation, but these guys are reckless and incompetent. The prime minister is a former snowboard instructor, minister of finance is a journalist, and minister of health a graphic designer.

That reminds me of Cuba, when bankers asked Castro to send them a good economist, as financial system was in turmoil after revolution. He replied that he doesn’t have a good economist, but he has a good communist and sent them Che Guevara. The rest is history.

Eastern Europe is looking better and better all the time bro

When does it end?

I’ve always said, it won’t end until there is enough inflation to make the public VERY unhappy. There are a lot of people in the US who do not own homes and have not seen a real wage increase in a long time. They are the victims of high inflation, along with a whole army of retirees on fixed income. Add it up, and I’d say they represent 60% or more of the voting population.

So far, I haven’t heard much outcry from either group.

Thinking about this more, the retirees probably aren’t complaining about inflation because they own their houses and benefit from massive home appreciation that offsets lack of investment return and food price increases.

That makes lower-income renters the primary bagholders. Unfortunately, this group doesn’t have the votes to derail the Fed’s grand inflationary plan.

So, it seems to me the Fed is buying MBS to avoid any serious political push back from retirees. Of course they would never admit that.

The old people I know have their home payed off and can live on social security and a pension if they have it. Most of their problems are related to failing health.

My wild guess estimate is that although many (but by no means all) retirees and pensioners are complacent now because they own a home outright and are relying on their retirement income to maintain their standard of living– that is about to change.

Unless these elders are Bitcoin mavens, rental real estate tycoons, or day trading geniuses (since traditional safe haven savings instruments no longer work to protect purchasing power of money) an inflationary regime will pinch them right where it hurts. Ouch.

The only way retirees can benefit from home values is to sell it (HELOC are just a slow sale). So then they’re homeless. And the pensions they worked 30-40 years to earn, and the savings and investments they made (not much) are basically worth less than the stimulus payments the Gov’t is handing out to everyone who didn’t work or save. Inflation hits the old harder than anyone, because they no longer have the option to return to work.

The FED is buying MBS because that’s what Wall St is selling, and they cannot stop giving money to the market.

It’s not the old, or middle class, that benefit most from increased asset values, it’s the 1% who have enough to not have to worry. If we wake up tomorrow and everything on earth costs 10x what it does right now those are the guys who will still have a roof over their heads and know where the next meal is coming from.

No outcry? Why else would Trump and Bernie have been the front runners in 2016? It’s only gotten worse since.

The feds knows how valuable the housing market is to almost ALL the economic activities associated with construction( regardless of all its bad effects on the market prices) ,hence this massive purchase of MBS. They need to manufacture inflation regardless of its undesirable consequences. The CPI formula is all screwed up and does not represent the reality of inflation anyway. This is not going to be a temporary thing as they claim it to be, wishful thinking.

1) USD plunged from 164.72 in Feb 1985 to 85.55 in Dec 1987.

From 1987 selling climax USD bounced backup to 106.56 in June 1989.

2) In Mar 23 2020 USD reached 103.96 < 106.56 and plunged to 89.17 in Jan 4 2021.

3) USD osc in the trading range.

4) USD might jump in a sling shot above 106.56, making JP the smartest and the most powerful banker in the world. The Fed have $8T assets, x4 times more than

AAPl, or the FANG combine and x8 times more than China have.

5) Liquidity swap reached $450B in Mar 2020 and collapsed to zero.

That will change soon.

6) The Fed accumulated assets when USD was scorned and laughed at, but JP will be laughing at those who need a dollar to pay their bills.

7) A strong USDCAD will shave the Canadian RE bubble.

8) The relative strength of the [FANG's : Fed $ assets] will be muzzled

until a further review in six months.

Come for the articles

Stay for the cryptic hodge podge of listed numbers/figures Micheal Engel lays out in the comments section

It’s one of my life goals to one day be able to decipher these, think I need an abacus, a hidden listening device in the feds closed door meetings, and that staff with the medallion on it Indiana Jones had in Raiders of The Lost Ark.

> 1) USD plunged from 164.72 in Feb 1985 to 85.55 in Dec 1987.

USD / YEN exchange rate

Same.

Higher house prices, higher property taxes, higher cap gain at sale, higher everything. Then think that they’ll get more revenue by doing this among other things. These dunderheads are dooming us. Anyone who isn’t participating in the asset appreciation game they’re making us play will miss the bus and be having cat food for dinner.

And following Bob Wells over at CheapRVliving .com

This is legit. In my area in “scenic north Idaho” (© Realtor) there are these small “mobile home parks” springing up everywhere — 8-12 spaces — and people are filling them up with travel trailers and RVs. They’re like 21st-century Hoovervilles.

Yes MiTurn, they are everywhere. Behind gas stations, stores, motels, etc. The locals go ape and zoning gets involved. On mid Vancouver Island one slumlord has turned several properties into these ‘havens’. Unfortunately, there has been a lot of drug activity and property thefts in the local neighbourhoods.

Then, there are ‘tent cities’. Mysteriously, they exist in greater numbers where the weather is warmer, like the west coast. We get a lot of forestry protestors from Quebec and Ontario that participate in stopping loggers from going to work. I always look at the protest signs and banners. Many are professionally designed and printed. hmmm

I’m just thankful everybody in my connected family works and has a plan to advance. Even my 23 year old nephew with a brand new apprenticeship in an expensive BC city, renting, struggling, has a long term plan….as does his girlfriend who works and attends U Vic full time earning a business degree.

I still believe success is attainable with directed hard work and sacrifice in both Canada and the US. One step at a time. Turn off the tv and don’t smoke dope after work is a good start. I used to do correspondence university courses at 5:00 am before I went to work. This was in the early ’90s, before online options. Math and Geography…..one coure at a time. My nephew’s GF is doing the same kind of thing, semester by semester. Waitressing and working for BC elections for cash. Do they have money or connections? Nope. Just a solid attitude. Sometimes we send them grocery store gift cards for a top up.

They will one day own a house, just not in the city. They already discovered this limitation and are working around it in their early 20s.

Paulo, as stated by the guy from Toronto above:

(Canada’s) “Federal housing secretary admitted that the (real estate) market works better for foreign investors than local people, and apparently that is how it is supposed to be.”

No wonder people are moving into RV’s and campers up there.

I just discovered a neat place at the beach. Four campers with beautiful views of the water tucked in a little dirt road. Talked to one owner. Lot rent about $300 per month and campers were worth about $5000. Retirees living there happy as a pig in slop. Keep looking to find what makes you happy. Not always a million dollar sticks and bricks.

Wealthion on Youtube just interviewed a very optimistic economist that think all this money will only accelerate growth and put prosperity on the fast track. Maybe the trillions dumped in a year will be worth it afterall.

I watched it too… I have doubts xD

I remember David Rosenberg, after 2009 financial crisis, saying that the Fed will get what it wants through their massive market Qeasing back then.

Guess who was right? If you invested at the bottom in 2009, you made a lot.

I wonder what he says about all this qe now. Haven’t caught words from him recently.

My guess would be, as with back then 2009, that the Fed might be able to pull this one for a few years at least…

Yeah sure it will ( sarc off)

Sure. History is pretty clear. All this money will accelerate growth til it runs out and then it is going to take more until currency is worth zero and retirees savings will not buy a loaf of bread.

Yeah, right. This MMT in practice is hot stuff, and a great boon to mankind.

Why didn’t earlier human generations think of this easy and painless way to prosperity for all before now? They must have lacked the vision and chutzpah we have today.

It’s an interesting dynamic in real estate in addition to the rising inflation created by unending debt creation & buying. There’s also a scarcity of homes on the market. In our city of roughly 100,000 or so in Antioch, CA, there’s only about 40 homes for sale at the present. That is creating a feeding frenzy when anything does come on the market. Our realtor who was our buyer’s agent 8 years ago recently called to tell me he just sold a house for $50k over ask with multiple offers. Another one in Concord, CA went for $200k over ask. He was fishing but it got us thinking and now we’re planning on listing our house for sale in August (hopefully not too late before things start to go sideways). It’s a scenario for the goose to keep laying a golden egg while also stealing from you at the same time. FED speak for ‘look here, don’t look there.”

So why is a runaway housing market good for anyone but investors and speculators? The lower class is taking out equity loans or refinancing for cash for down payments for toys and other depreciating assets or at best not messing with anything and watching their ballooning home valuations. I mean you can have a stock jump 10000% overnight but until you cash out it is just theoretical gains, not money in the bank. How does this help anyone at the bottom but delusional fools or people moving from really expensive places to smaller towns for WFH.

I see a whole lotta people who were struggling 2 years ago driving old beaters and barely scraping buy suddenly have a big pickup on mud tires and a camper behind it or some other pricey toy while a crew works on their new full wrap around porch or pool. I know for a fact wages haven’t moved much for the working class except for at the very bottom like mcdonald’s jobs. And a few grand stimulus doesn’t mean anything in the asset market now, won’t even buy a broken pickup from 1971, let alone be a down payment in 2021. Maybe I’m too much of a hermit and people are making money hand over fist and getting rich quick and I’m out of the loop on how, but boy do I feel like this time around is going to be really bad.

I would be surprised if the wages are not climbing on the low end.

Warehouses and light manufacturing in my area that were starting at 15/hr a year ago, are over 19/hr with sign on bonuses.

Bring it all home. More than willing to pay more.

You’re not the only one felling this way. I see a lot of people around me seemingly making money hand over fist and witnessing the effects of FOMO. A couple of people tried to get me into Bitcoin including my brother but I have serious reservations at about it. My gut feeling is telling me that all this instant wealthy money and asset aquisitions is going to end horribly and the people especially in this country are going to have a very rude awakening.

No they aren’t making payments. I know student loans are not being paid currently, and anyone from 22 to 40 probably makes a student loan payment. Think of all the extra scratch people have from that. Some prob also aren’t making mortgage payments or rent. And at what point do you think they’ll decide to save that UE money for when they do have to pay it off? I don’t think they’re thinking that way.

Good point. Too many not paying rent, not paying a mortgage, not paying car payments, not paying student loan payments, and getting unemployment plus the fed added 300 until September.

What happens then this stop and they all will have to pay up or lose everything they bought with the free money?

Will the jobs they now ignore even be there when they realize that they now need them?

What happens when the moratoriums end?

Will all of that be the trigger?

If so, how do we protect from the results?

I feel the same way. Everyone seemed to be “getting by” two years ago. and now they are all buying houses, trucks, campers, side-by-side ATV’s, and remodels. As with most things, there are multiple factors of causation. The fed programs and stimmies take much of the blame. Some is demographic shift.

BUT I think there is more to it. Most people I know don’t pay that close of attention to finances. They do what feels good. They buy when they WANT to buy, not when the financial picture is perfect. I get the sense that the pandemic heightened our collective awareness of our mortality. With all the death in the headlines, minds shifted just a little further into “living for today.”

Most people live for the day anyway, and this just inched us all a little more in that direction. This widespread “YOLO-ing” (you only live once) is sending ripple effects through markets and is manifesting as supply chain shortages for many things.

Like most commenters here, I watch these trends, and I can’t shake the sense that we are hurdling toward a reckoning in the near future. But I hit the “real world” in the depths of the 08/09 recession and I think it turned me into a big of a perma-bear, so maybe that’s it too.

“But I hit the “real world” in the depths of the 08/09 recession and I think it turned me into a big of a perma-bear, so maybe that’s it too.”

No, it was a learning moment and you learned. The rest of the people keep putting their hand in the fire and get burned and wonder why. Which makes it all the more angering that we always “save” them. Biggest problem our society faces is the refusal to have responsibility for actions. It’s always somebody elses or something elses fault.

But its also the nature of the system. It can’t function without those people not learning. What does the TV tell them to do? What do their friends tell them to do? FOMO baby! Responsibility always starts with those who have “power”.

True. But financially-speaking…

It can be disheartening watching everyone else at the party slam tequila shots from a stripper’s butt cheeks while sitting in the corner sipping a Miller 64 thinking “hmm that seems unsanitary”

Responsibility is boring.

reminds me of Peter Schiff’s tweet. “The only thing ‘transitory’ will be the Fed’s credibility!”

If the Fed’s goal was to make people confident to spend money, that might have worked in the short term, but they’ve overplayed their hand.

Too many people now are talking about inflation and bubbles. Eventually, the Ponzi ends when you can’t find another bagholder.

I suspect the end of this bubble is closer than people realize. I understand that previous bubbles (2006 housing, 1999 tech) went on for longer, but the insane steps to blow this particular one accelerates the entire process, from the blowing of it to the pop.

I think money printing has a shorter effective duration each time its used, kinda like a drug, so the dosage has to keep going up. Last march was a doozie and they’ve done a few more rounds since then. If you look at the actions last year compared to what actually reality, it stinks of desperation.

Exactly. It’s all a confidence game, which is why they don’t want people talking about inflation. Because inflation is one of those things that becomes a self-fulfilling prophecy when people expect it to come.

And their denial of inflation is a great example of “the lady doth protest too much, methinks.”

Honestly i don’t think inflation will be the problem yet. Remember in the summer of 08, oil was 150 a barrel and everything was going up? Riots in Asia over rice prices. More likely this is a blow off top before some sort of crash. I don’t doubt inflation will be a problem at some point but i think a crash has to happen first.

Also i don’t think we’ll see really “bad” inflation until the dollar loses RC status. That and only that will end this nonsense.

Now a days, everything happens at a much faster pace.. May be because o faster information flow.

The up and down of the dollar in FOREX is interesting. Buying in ‘weak’ dollars then selling in ‘strong’ dollars is an intriguing proposition. This reminds me of the populist movement in the 1890s. These were small farmers who borrowed to plant, then hoped to get a good price at harvest time. They didn’t get the prices they needed. And to make matters worse, the dollar would be stronger (gold backed) at payback time. A real squeeze.

Read a sensible article the other day outlining five reasons why Powell should not be re-appointed in the fall. On Market Watch of all places.

What are the odds?

Doesn’t matter who the pick, they all worship in the same cult.

New Boss same as the old boss

I started learning about “balance sheet” concepts late in life when I was trying to learn about the companies and stock market.

But the “balance sheet” of the Fed seems surreal compared to balance sheet of companies.

Seems like the Fed could just write off all the WTF extreme asset accumulation as a loss. Then the balance sheet would be back to normal.

“Easy come, easy go” as Trump’s U.S. ambassador to the European Union Gordon Sondland so nonchalantly pointed out.

The size of the Fed’s balance sheet is meaningful only because it signifies the amount of money they have printed. Anybody who thinks the Fed’s balance sheet will be reduced willingly isn’t thinking it through. They can’t even taper their asset purchases, let alone sell assets.

The days when the Fed sought to maintain a balance sheet level, requiring purchases and sales from time to time, are long gone. The balance sheet will only increase from here, consistent with Modern Monetary Theory (MMT). As long as there are deflationary forces in the economy, such as technology, wealth concentration, productivity gains, etc., they will keep printing money to offset that and more.

There is a limit to stock and bond prices, however. Nobody with a brain is going to be sitting in stocks that yield near nothing, but have a 90% downside. Who knows where that limit it, but we must be close.

The Fed is being attacked by two lethal armies now – inflation and stock overvaluation. Either one can derail the Fed’s plan rather quickly.

As noted in his July 2009 WSJ article in which Bernanke said QE was temporary, assets will just be allowed to mature and the proceeds then not be reinvested….that is how Ben said it would all end….when things got back to “normal”. The Dow was around 10K at the time.

I guess he lied to us.

Once you can no longer buy time at great expense…

…you buy less time at greater expense

I suppose it makes a great case for an Infrastructure Bill…because we’re running out of road to kick the can down…

The problem is there isn’t the political will for a real infrastructure bill, as that would require people be forced to take the jobs created by it.

It’ll end up just being a boondoggle for unions.

“…there isn’t the political will for a real infrastructure bill, as that would require people be forced to take the jobs created by it.”

A “real” infrastructure bill would “require” people to be forced to take jobs?

Wut?

Because in the 30s, when we last did an infrastructure bill like being proposed, there was much less welfare, food stamps, or anything like that. So those who had no jobs were happy to take them.

Do you see the political will to make single mothers take construction jobs?

Unions and engineers.

I still have “shovel ready” jobs waiting for completion from the GFC.

I will be ashes before the next bill makes it past suits and generals.

I still have the emails between 2 PE’s

Who thought 400k was a great price for a 2 hole, 2 sink sh*tter.

I’m guessing today it would be a great deal at 1m.

RightNYer: “Do you see the political will to make single mothers take construction jobs?”

I don’t see how making single mothers take construction jobs is some kind of political panacea. Maybe your can explain?

A lesson in the economics of The War on Poverty. The single mother doesn’t need a job, her baby’s father needs a job. If her baby daddy had a job, she wouldn’t be a single mother.

Mother already has a full-time job it’s just not counted anywhere.

No, she wouldn’t be a single mother if she married the father and stayed that way.

AA,

You missed the point. If she was married, she would not be entitled to welfare benefits, unless she kicked her unemployed husband out. The welfare system created by the war on poverty, incentivized illegitimacy, deincentivized marriage. Welfare incentivizes divorce when mothers are married.

The single mothers all know this and are acting in a rational manner. Why marry when it makes you and your children less financially secure. I am not promoting their behavior, just describing the system that encourages it.

“For all those people who have been saying ‘oh my gosh, the Fed needs to normalize quantitative easing,’ today’s job report is just and example of – we have a long way to go” Kashkari said.

(Kashkari is Minneapolis Fed dude)

The most-est woked-est, and the not, members of the Fed really truly do believe San Fran fed chic Mary Daly’s view that the Fed is creating “millions” of jobs by printing money.

Someone here wrote you can’t taper a Ponzi. Someone else wrote any tapering will hit a brick wall and do a 180 as soon as Mr Market throws a hissy fit and crashes for a few days in a row.

Shorter version: These guys are polished, educated crooks who’s job is to service their social class.

MBS transferred mortgage risk from the banks to investors. Investors supply the collateral, and extract dividend payments from the shareholders. They enforce those payments by employing banks who passed through the risk in the first instance. The debt is no longer recoursing, those holding MBS will get no satisfaction in liquidation. Not even sure what rights the holders of MBS have to payment, (esp if banks chose not to enforce these claims, and being part of the FED why would they?). Rule one: being an investor you assume risk. The Fed buys this stuff to underwrite the mortgage market and step in front of the next GSE blowup. The problem arose during the mortgage crisis when bankruptcy judges asked to hear from the mortgage holder and no plaintiff could produce the documents to prove ownership. The government wants everyone to receive a monthly check in order to hold some control over the flow of payments (to Wall St). You liked student loan forgiveness, get ready.

A recent report suggested that 34% of incomes comes from the government. This is a banana republic number.

I will ask this question again

Who will finance the governments deficits at current rates , where an investor is guaranteed to lose money in real terms

Only the FED.

We now have the Magic Money Tree technology. But as the author William Gibson said : “The future is already here—It’s just not very evenly distributed”.

Not sure about today but in the not too distant past Microsoft’s largest customer was Uncle Sam. What’s Apple’s take from school districts around the country – Microsoft as well. Oracle? Boeing gets at least half its income from Uncle Sam. Larry has his own island though.

That’s fake until you have a reference.

I am not sure you can call everything on the Fed’s books assets.

A debt is only an asset so long as there is a fairly certain chance it is going to be repaid. When it is not repaid, it is a liability.

It is easy to borrow money, it is very difficult to repay it. Especially if there is a recession.

I do not think anyone can deny that this entire economy is now based on borrowed money. With over a third of the publics income now coming from the government who has to borrow the money to pay that income.

Does anyone in their right mind believe that is sustainable?

The government requires 1/10th of your income to be paid to a health insurance company.

All things are temporary. Does any meteoric spike in any asset “value” come without an ultimate reversal? Might be a screaming ride down on an unhinged elevator, or a less violent tumble down the stairs. This is also true of the inflation rate in the US.

Do I care why the Fed does what it does, the reasoning, the rationale? I have to say no. I watch what they are doing, yes. They fancy themselves as pilots of an aircraft in a terrible storm, working the levers to maintain some semblance of vertical control. The egos at work are simply massive.

The plane is going to end up on the ground, the question is in how many pieces.

The FED would not taper down or increase rates unless/until some catastrophic event happens. The mandate of FED is to serve the elites and that is what they are doing. I understand the frustration of folks here against FED but once they realize the FED’s mandate, you all will understand and cool down.

FED is doing what it is supposed to do.

Nothing would change unless there is a some sort of revolution. But then people are being fed stimmys to keep them asleep.

“Trillion” seems to be losing its dramatic effect and is almost commonplace now, especially when talking about things that used to be considered bad, like budget and trade deficits. How soon before we see “quadrillion” bandied about like its no big deal?

Sounds like the Weimer Republic in 1923

Moar cowbell!

1) SPX daily : take a line from Apr 16 high to Apr 29 high and to today

high. This line is shortening the thrust.

2) Take a parallel line from Apr 22 Harami close. SPX might cont higher and form a Lazer.

3) Between Mar 4 low @3,723.34 and Mar 17 high @3,983.87 there

are 260.50 points.

4) Add 260.5 to 3,983.87 = 4,244.40. We are almost there.

5) You can sell and go away, or take 25% – 50% profit with the proper SL.

6) 0.62 x 260.63 = 161.

The next targets :

7) 4,244.40 + 161 = 4,405.

8) 4,244.40 + 260.53 = 4,505.

SPX 4400 is what a bespectacled bull on CNBC has been calling for by mid summer.

Mortgage forbearance and the eviction moratorium have sharp edges. We should start seeing the effects of the end of these freebies later this year through 2022 and beyond.

I’m long tents and tarpaulins.

No chance in this hot market even you are in serious delinquent.

Apparently you are not a student of history… You do know the Fed has gone bankrupt in the past… right? Why do you think they confiscated everyone’s gold in the great depression……. Oh I know… This time is different…

doomsday is a rare event. As long as you are not leveraged to crazy degree, I wouldn’t bet on that occurrence. Do not bet against the deep pocket even you are on the right path.

Not if the CFPB gets their way. Their latest proposal is to halt all foreclosures until Jan 1, 2022 and restrict servicer’s ability to foreclose.

“Millions of families are at risk of losing their homes to foreclosure in the coming months, even as the country opens back up. Last week we warned that servicers need to be prepared for a high volume of borrowers exiting forbearance, and today we are proposing additional guardrails and tools for servicers as they navigate the coming months. We will do everything in our power to ensure servicers work with struggling families to find solutions that prevent avoidable foreclosures.”

I don’t think the FED or gov. will allow a normal real estate market prices to exist again.

what happens to the federal judge ruling against CDC foreclosure ban.

The real truth is that all of the government policies are designed to do one thing – make the rich richer and make the working class into slaves. The worst enemy to the working class is inflation. When your income is fairly fixed, you need prices to remain stable or even to decline. The internet has been a deflationary force. But these crazy stupid politicos have pumped the monetary bubble and it had only one place to go – asset price inflation. That is a bubble being made. What investor can trust the asset prices and wants to invest now? Younger generations are being sold homes at prices that will not appreciate over a 30 year time period, because incomes wont support higher prices.

Imagine a world where healthcare was cheap, homes were cheap, public education was high-quality and accessible to everyone. That would be the utopian world for the working class and small business people. Instead we get a world where manufacturing and jobs have been offshored and where asset bubbles are constantly blown to prop up the rich – real estate, healthcare, education – are the industries that determine the difference between the have’s and the have not’s.

“Imagine a world where healthcare was cheap, homes were cheap, public education was high-quality and accessible to everyone. ”

Nordic counties have it all. Healthcare is free, as is higher education. Homes might not be very cheap but you will get decent place to live regardless of your income. And even if you don’t have any income.

Gotta share this news blurb. Just saw it.

A two-bedroom, three-bathroom condo backing onto Tofino’s world famous Chesterman Beach was listed for $1.4 million.

It just sold for $2.4 million, confirmed a Tofino-based realtor on May 7.

1 Million above asking. Unbelievable.

And by the way, Chesterman Beach is okay, but absolutely 2nd rate compared to Oregon.

That’s crazy….it would be interesting to find out who the buyers are that can spend that much over asking price.

What is going on here is extremely obfuscated and contrived and nuts. I’ve always believed that complexity and sophistry is an attempt to take people’s eye off the ball.

If the Fed is really buying treasuries straight from the Govt, the dollar is ‘toast’ internationally, because no country would ever trust a Zimbabwean currency.

On the ‘three cup trick’ you have to follow the cash. The Fed manages the ‘cash market’ by buying and selling paper assets. When it buys, it puts cash in, when it sells it takes cash out.(dollars) When the Govt issues Treasuries it takes cash out of the ‘cash market’. If that cash is not made available, in the market, the interest rate has to go up. When the Fed buys assets of any kind from third parties (eg Banks), it makes cash available to these third parties. Because they got a trillion for eg MBS junk, the third parties are then able to provide the cash in the cash market for buying the new Treasuries, thus creating the ‘illusion’ that the Fed did not buy the Treasuries. The game is given away by the fact that the Fed must know in advance when cash is going to be needed in the market to cover treasury sales. The Govt Debt Manager must tell the Fed Open Market Cash Manager when he has a big cash call coming. This is how QE keeps rates low and hides the debt being monetised, a la Zimbabwe.