This is the first time I’ve seen Wall Street banks clamor for the Fed to back off QE. The Fed is struggling to keep the liquidity it created from going haywire.

By Wolf Richter for WOLF STREET.

In the fall of 2019, when the repo market blew out, the Fed stepped in and bought Treasury securities and MBS and handed out cash via repurchase agreements. When these repos matured, the Fed got its money back, and the counterparties got their securities back. The Fed also did this during the market rout in March 2020. But by July 2020, the last repos matured and were unwound.

Now the Fed is doing the opposite, with “reverse repos.” Repos are assets on the Fed’s balance sheet. Reverse repos are liabilities. With these reverse repos, the Fed is now massively selling Treasury securities to counterparties and taking their cash, thereby draining liquidity from the market – the opposite effect of QE.

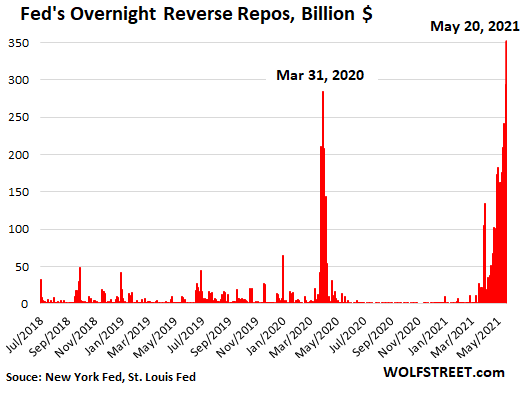

This morning, the Fed sold $351 billion in Treasury securities via overnight reverse repos to 48 counter parties, thereby blowing past the brief spike at the end of March 2020, and more than replacing yesterday’s $294 billion in Treasury securities that it has sold via reverse repos to 43 counterparties and that matured and unwound this morning.

These reverse repos are a sign that the banking system is struggling to deal with the liquidity that the Fed has been injecting via its QE. And that’s in part why there is now some clamoring on Wall Street for the Fed to taper its QE purchases because the banking system is now drowning in liquidity that banks have as reserves on their balance sheet. By buying Treasuries in the repo market, the banks lower their reserves and increase their Treasury holdings.

So with one hand, as part of QE, the Fed is buying $120 billion a month in Treasury securities and MBS. With the other hand, the Fed took back $351 billion via overnight reverse repos, undoing nearly three months of QE.

It’s the kind of crazy situation that you run into when you push something to the extreme, as the Fed has done with its asset purchases, and you get all kinds of side effects.

The Fed addressed these reverse repos and the mountain of reserves during the last FOMC meeting, and released a summary of the discussions in its minutes yesterday.

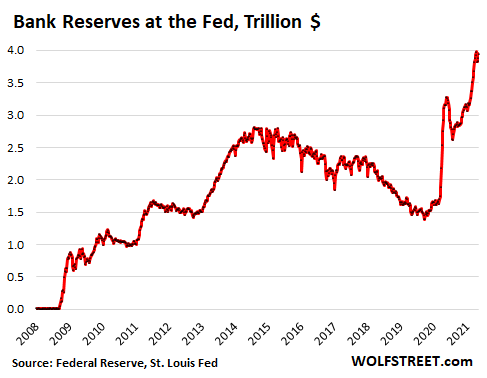

Reserves are cash that the banks deposit at the Federal Reserve and that the Fed owes the banks. They’re a liability on the Fed’s balance sheet. The Fed pays interest (currently 0.1%) on these reserves. The reserves on deposit at the Fed have now spiked to $3.92 trillion:

In the FOMC meeting minutes released yesterday, the Fed addressed the ballooning balances of reserves and the huge demand for short-term Treasury securities, which the Fed is helping to provide via reverse repos.

The Fed also said in the minutes that “a modest amount of trading” in the overnight reverse repo market “occurred at negative rates.” In other words, these participants are borrowing money at negative rates from counterparties that take Treasury securities as collateral. That’s how strong the demand is for Treasury securities in that end of the market.

The Fed said that this phenomenon of reverse repos trading at negative rates “appeared to largely reflect technical factors.”

And the Fed announced in the minutes that it would “adjust” – likely raise – the rate it pays on reserves, likely at the next meeting (“more than half” of the survey respondents expected it, it said).

It added that reverse repos on its balance sheet will likely grow further. In the words of the minutes:

“The SOMA manager noted that downward pressure on overnight rates in coming months could result in conditions that warrant consideration of a modest adjustment to administered rates and could ultimately lead to a greater share of Federal Reserve balance sheet expansion being channeled into ON RRP [overnight reverse repurchase agreement] and other Federal Reserve liabilities.”

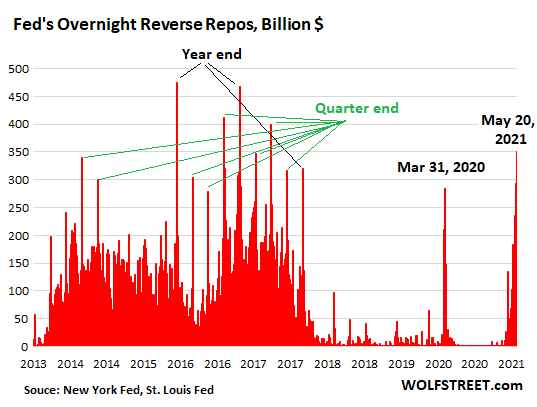

Banks have shed reserves via reverse repos previously in the era of large reserves, but that happened at the end of the quarter, and particularly at the end of the year. The issue diminished after the Fed started reducing its assets during Quantitative Tightening in 2018 and 2019. But the spike we’re seeing now is happening in the middle of the quarter:

This is the first time that I have seen Wall Street banks clamoring for the Fed to back off QE as the banking system is creaking and straining under the huge pile of reserves. And apparently, from the response disclosed in the minutes, the Fed is figuring out that you can push QE only so far before something big is going to go haywire with unforeseen consequences.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Too complicated for the regular HODLRs and “investors”. So …. S&P 5000?

The banks are probably short the market right now.

It still cracks me up that it is the same word for the drug in Brave New World (SOMA)

Proof we are in a vast virtual reality game.

The Fed is.

The World isn’t, it’s real.

Covid has shown that the current crop of politicians, worldwide, are simply incapable of dealing with reality.

They don’t have the skills and experience to deal with large-scale real problems, and the government systems everywhere are simply too corrupt and/or inefficient to implement effectively whatever they do come up with. Furthermore, the recruiting and promotion within both political parties and government service are heavily biased against those with genuine skills and principles, not least because they will inevitably show the current situation for the corrupt, Byzantine mess it is.

This is not fixable from within either political or government systems.

I challenge anyone to show me where hope for the future of the current systems lies.

Sailor’s got a point.

Yep! And the inevitable return to reality is going to be very painful. Hopefully some lessons will be learned from this crazy tinkering with the free market, but, in the long run, knowing human nature, I doubt it!

Pls show the proof of these large payoffs u reference

Bribe laundering book deals and “speaking fees”. If you can’t google, I can’t help you.

LOL

Agreed. The inflation that is starting to rise obviously spooked the banksters’ “Fed” since if the stock market is driven into the ground and there is a depression, Americans may finally object to being bent over and have the “Federal” Reserve taken over so it becomes a truly federal independent government agency. It is trying to put a break on liquidity to delay inflation.

A certain, much-hyped company has a PE ratio of over 500 and some people still doubt that its stock price will drop like a stone. LOL. Others have similar, if not quite as insane, stock valuations absent hyperinflation. The crash will not be gentle but will be a Hindenburg moment.

I have diversified but holding cash is nuts when the “Fed” will be pursuing QE to give gifts to its banksters to infinity and beyond. Thus, it is really hard to find a safe haven.

I read some of the contracts for various metals funds, which are not even really required to actually ever purchase or hold the gold, etc., for which they are shamelessly charging you “storage fees.” Physical metals may get confiscated again. Thus, we seem to be out of safe havens.

The US healthcare industry is a big scam to overcharge Americans and provide guano-like service. It also is overvalued. Nevertheless, they probably have purchased the greatest number of politicians after the banksters, so I parked my money with them. Since the CCP has decided to play B-movie villains for the foreseeable future, we may actually need more of their services.

You really think some idiot is going to show up at your house and confiscate your metals? And do it to millions of other people as well. I doubt it.

no, they will ask you to do it. roughly 50% of americans will comply. which 50%? depends on who is asking.

this ought to be fun.

I think you’ll probably see bank bail-ins way before they confiscate precious metals.

Obama received a $65 million advance for his memoirs.

His earlier books sold around a million copies each.

Michelle’s books have also sold well.

They’ve earned more than enough money quite honestly to buy those homes, which may have mortgages (not paid for in cash).

Golf journalist Rick Reilly, who has played a lot of golf with Trump and others who’ve played with Trump, and also some with Obama, described in great detail in his book “Commander in Cheat” how Trump is the cheatingest cheater around, and how scrupulously honest Obama is on the course. How a person plays golf tells a lot about their character.

Read the book, and you’ll learn what scum Trump is.

“An honest public servant can’t become rich in politics.” – Harry S. Truman

What does this mean to the layperson who does not understand it.

Stephen,

I think the key takeaway is that banks are so stuffed with “idle reserves” (money they cannot reasonably/responsibly lend, even at today’s degraded standards) that they prefer to store those reserves at the Fed for .1% (rather than lending at 3.5% for a mortgage on hugely overvalued collateral).

The repos can be convoluted/confusing…but they are really just the means to shift excess funds from one part of the financial system to another part.

It is the *level* of excess reserves that matters most…the repos just track interim changes to that level in terms of amount/direction.

And the financial system is so overstuffed with reserves/lendable money because the Fed needed to print trillions out of thin air to buy US Treasuries…Treasuries that would have only sold at much higher interest rates…or not all at…had the Fed not arrived with its printed up dollars.

All of these things are predicates/manifestations of huge latent/pending inflation…inflation created by the money printing that DC has employed to cover up huge policy/operational failures over decades.

Failures???? :-) Or did they do Exactly what they intended?Megawealthy got more so=buying up real assets including politicians and science.Financial divide and conquer= distracted populace disunited and weak.Debtslaves galore starting from younger ages and extending well past retirement,if in a position to do so.America in debt shackles to Private co.

Thanks for all you do, Wolf!

Man, reading you Wolf is almost like having an ear straight unto those folks’ evil plans and so on.

I would NEVER understand the world of finance as I do now WITHOUT your INFO.

Much thanks for your care and research and geniality.

I said it before: who needs a B.Ec. when you all you need is B.Wolf.

Or a personal adviser.

Most advisers out there are totally clueless to all this stuff and yet have much undue influence over much of the lambs out there.

THanks Wolf.

Advisors tend to get compensated by transaction volume (stock brokers) or assets invested (invt advisers)…neither of which do well when government interest rate policy inflates asset prices to far beyond what is justified (by actual business results) or sustainable (governments that print money destroy their economies, inevitably).

Because of how they get paid, advisers’ cannot afford to be educated/honest about how government policy has massively distorted the invt mkts.

The dictum “Physician heal thyself” works only until surgery is required. I suppose suicide is one way to stop a cancer from spreading. Wild stuff.

My greatest amazement is your ability to describe madness in rational terms. Nice job, as usual.

So many questions… Can someone explain for my ape smoothbrain why the Fed wants to sell these overnight(?) securities and the banks want to buy them? I don’t understand the motivations here.

If you short treasuries you need treasuries to replace the ones you shorted, not cash. The market is short treasuries and clients need to close out those positions with like securities. The fed has all the inventory.

Banks are sitting on too much cash (reserves). Nearly $4 trillion. The repo market allows them change their reserves into Treasuries. There are other entities too clamoring for Treasuries, including Treasury short sellers that have to find Treasuries to close their positions. And the Fed is providing them.

So the Fed is protecting short sellers from losses????

No. Short sellers are going to make or lose whatever the market will do to them.

The Fed providing the UST allows the trade to settle rather than fail (failure incurs financial penalties and can have ripple effects).

Could you cover Michael Burry’s recent positions? He has a huge short on Tesla which was well covered in the press, but also has large short positions on the treasury market, that seems related to this whole mess going on right now. Any clarification there would be very much appreciated!

Many of his investments are in small caps that are not in the stock indexes and are based on inflation to hyperinflation. Since they are not part of the indexes, they are less volatile.

A while ago he changed his twitter bio to

https://www.federalreserve.gov/econres/notes/feds-notes/ins-and-outs-of-collateral-re-use-20181221.htm

I guess the banks are having trouble closing out these positions due to the shortage of treasuries in the market due to the massive QE operations.

If the banks believed in inflation they shouldn’t have bought treasuries.

The banks invest in deflation.

Big use of treasuries is for use as collateral for margin,

Can the banks allocate A tiny portion of that reserve to buying bitcoin? Actually, it doesn’t have to be bitcoin. It could be any cryptocurrency.

It would be the amplification of earnings.

?

Do you really want the banks to own all the Bitcoin, using credit given to them out of nothing by the Fed? Doesn’t that defeat the fundamental purpose of cryptocurrencies as vehicles for decentralized bank-free finance?

Wolf,

Please forgive my ignorance here, but in your article you describe the range of interest that the Fed is currently paying for reverse repo are 0.1% (anually?) to slightly negative.

Each individual bank must be sitting on 100s of millions to 10s of billions in reserves. If the Fed is offering positive 0.1% to somewhat negative yields in the repo market what is the banks incentive to participate?

How does the repo rate compare to current LIBOR rates, or do I misunderstand how the two are related?

Why do the banks just not loan more to reduce their reserves?

CTCarver,

I’ll just address a couple of your points (I need to go to bed, I’ve got an early interview with Saxo Bank in Denmark tomorrow, I mean today, early).

The rate that the Fed pays the banks on reserves is fixed, currently at 0.1%, but it will likely be raised.

The reverse repos trading in the repo market at negative rates is a market function. That’s a very different thing. They might trade at a positive rate today and at a negative rate a few hours later.

Speaking of loan contracts,if I read correctly on the FDIC site,number of loans is down when compared to several months ago.I do not remember the y.o.y. Or five year comparisons.

Note only banks get IOER, non-bank counterparties get 0.0 to park but it’s that or buy collateral (possibly at a loss if rates rise before deposits move). Key takeaway, this money is parked and has no velocity. IE – There is no confidence in lending, no spending or investing… and libor going away only exacerbates the Feds challenge.

RRP is a sign of duress in the system and coming to grips with the inevitable… negative rates, negative IOER, negative FFR… negative SOFR… it is the only way to push savers and “investors” into risk (increase money velocity and try to salvage gdp)… conveniently, neg rates also finance the government and lowering the debt. ;)

What is the term of these overnights…..overnight?

The Reverse Repos seem almost momentary, while the QE seems of much longer duration.

Thanks

“… participants are borrowing money at negative rates from counterparties that take Treasury securities as collateral. ”

Why would the “counterparties” lend at negative rates? If these counterparties need Treasuries, isnt the Fed doing reverse repos providing those securities?

I’m not picking up on this.

Thanks

Because they’re desperate for Treasury securities?

The only thing we can do is guess why they’re doing it. None of the reasons behind all this have been disclosed.

Treasuries are “trading special” meaning they are the most sought after asset now… “shadow” market underwriting trillions in global markets for parties that can’t hit the Fed windows and facilities

So you get .1% on reserves and around 1% on Treasuries. Is that a factor?

The banks could bid at auction themselves. What is the deal with temporary REPO vs purchase?

This game has not yet been explained to my understanding.

Come on man, don’t make me do work and research it.

1% on Treasuries?

Not in the maturities being discussed here. This is all short term stuff.

Treasuries dont get 1% until way out the curve……6 years or so…

joe2,

Yes, just about anything could be a factor. And you’re correct, it has not been explained with hard facts. Everyone in public is guessing. The Fed probably knows.

BTW, the Treasuries you get 1% on are not short-term Treasury bills. You have to go to about a 6-year maturity to get 1%. Reserves are instant liquidity. You get about 0% on short-term Treasury bills, which are the closest thing to reserves. So reserves pay more than T-bills. Banks can and do shift from reserves to other types of assets with longer maturities, but that changes everything for banks.

I just posted a chart here in the comments below about the banks’ record holdings of Treasuries. You have to scroll down quite a bit to see it.

Does that mean the cash deposits I have in bank accounts are safe at the moment?

Yes, assuming they’re in a US bank and amounts are below FDIC limits.

BTW, the stuff we’re discussing here is not a sign of weakness at the banks. That’s not how I would interpret this.

Why is it a problem for banks to have “too much reserves. ?”

Yea, this is what I don’t understand even after my first question above. Wolf seems to almost be saying we don’t really know why the banks think they have too much reserves in the replies above, but he doesn’t explicitly state that in my mind. Just connecting the dots as well as I can…

If I was a bank sitting on tons of cash I would be pissed that inflation is shooting up and I have few options for reinvesting the money. Do many banks even give business loans out much anymore? Or are they just staring at auto loans, mortgages, and credit card balances rubbing their faces because consumer demand for this debt is basically saturated?

rhodium,

“Do many banks even give business loans out much anymore?”

Yes, the total balance of “Commercial and Industrial” (C&I) loans is about $2.6 trillion. Plus, there are about $1.4 trillion in leveraged loans outstanding (junk-rated loans that banks sell to investors or securitize into CLOs and sell to investors).

Also, many bigger companies can now borrow cheaply by issuing “unsecured” bonds for a song (crazy bond market right now), and companies prefer issuing unsecured debt over secured debt, such as bank loans which are always backed by collateral. Issuing unsecured bonds allows companies to keep their collateral unencumbered for a rainy day. And bond issuance has been booming.

The banks are taking money from depositors who invest in money market funds. Post 2008 when non treasury MM funds broke the dollar, there were some changes in the regulations. Owning treasuries rather than cash improves the bottom line in a MM fund, and maybe why they did it? The banks are paying zero interest to MM holders, and inflation is ripping? The Feds dilemma. How to print money with one hand, and rip people off with the other??

Wolf,

Agreed…it is the level of excess/idle reserves that is the real story here…the repo mkt is just the means by which funds get shuttled around within the financial system (and the mechanics of repo operations tend to confuse non-bankers…and most bankers too).

The huge mountain of excess/idle bank reserves illustrates the size of the potential/realized inflation disaster, while the level of repo activity tracks the interim little landslides happening on that mountain.

Your bank reserves at the Fed chart tells the whole story.

W

Demand for Treasuries versus supply of treasuries, the price (ie rate) should go up but it might not if the Fed has enough on it’s books to sell into the demand. Exactly the opposite of QE. Do you think they’ve sussed that we’re onto them, No?

Oops rate goes down! when price goes up sorry.

Wolf, are treasuries not being created continuously to fund the deficit spending? Why the shortage and need to buy from the Fed? Also, these treasuries were at least partly bought by the Fed from the Treasury with created money (QE) I think, so now that they sell them for ‘cash’ couldn’t they now destroy that cash to reduce their balance sheet and reverse QE if the need has passed? Sorry for the dumb questions, this is all a bit Greek to me but crucial to get the head around nonetheless.

Normally, treasuries would be created to fund deficit spending, but the Treasury General Account is being drawn down to finance the federal government currently. You have a flood of cash of entering the financial system without a corresponding flood of treasuries and this has created an imbalance which the Fed is trying to rectify.

San Franpsycho said: “You have a flood of cash of entering the financial system without a corresponding flood of treasuries and this has created an imbalance which the Fed is trying to rectify.”

_______________________________

Why assume that a flood of cash entering the financial system has to be met with a corresponding flood of treasuries? I don’t think it does.

Ab

All the obfuscation and complexity hides a simple fact.

When the Fed SELLS paper of any sort, it is taking dollars (ie demand for stuff) out of the economy.

When the Fed BUYS paper of any sort, it is putting dollars (demand) into the economy. What looks like happening here is, that they’ve s**t themselves over how much panic QE they did last year and they are trying to backtrack before the inflation S**t really hits the fan.

It could maybe be looked on as a good sign of ‘reality bites’, but we’ll see.

You’ve got to agree, it’s great fun the way Wolf spells it out!

Obfuscation, complexity, and relabeling. Technology has made the basic rules of central banking accelerate to microsecond or nanosecond time frames, but casting your questions in classic terms seems correct to me.

These are just old-fashioned open-market operations, something the Fed has indulged in from the time of its creation, taken to the max. The inflation/crash cycle of 1917-21, 1922-29, etc. Currently we have been in the boom asset inflation cycle. Huge unemployment, small real businesses crashing and burning, joke companies’ shares selling at infinite multiples of non-earnings and dozens or hundreds of times sales, and housing booming with basically free money. And the economic cycle has seemed far too long to be higher highs and lower lows.

If the price of money is based on demand, we have zero interest for too much money. The Fed is in panic mode trying to shrink bank reserves the old fashioned way but the numbers are too huge.

As Elihu Root stated in Congress, arguing against creating the Fed: ‘You will have created an engine of inflation’.

This is not capitalism creating wealth, but financial engineering, creating money. Few people know the difference.

Wolf, pardon my ignorance as I don’t have finance/banking background, but why is excessive liquidity bad for banks? I understand the other way around, when there is not enough liquidity around.

You mentioned that there is a strong demand for short-term Treasury securities, so is it that these securities can perform a function that reserves cannot?

thank you.

Toronto: deposits are a liability to banks because they have to pay interest on them. They only make money if they can turn around and loan enough that money at rates that are higher than what they are paying.

That makes sense, thanks.

Tim

But the Fed is paying an interest on excess reserves that is higher than what the banks are paying their depositors.

The fed is keeping the bosses happy and solvent. Remember the banks own the fed.

Maybe this is because the banks can make more money by shorting treasuries rather than earning interest from their reserves at Fed? I dunno

Excess reserves at the Fed,

1) Indicate that banks – even using today’s degenerate underwriting standards – cannot find enough loans to make that the banks’ believe will be repaid…or whose true foreclosable collateral value is anywhere near what is claimed today and

2) Allow banks to make an absolutely riskless return – .1% from the Fed is insanely lower than the 3.5%+fees made from a bank loan…but the Fed will never default.

I think loans are a minor business for most of the big name banks. Possible exception beings Wells Fargo. It’s more about not having any productive use for cash. So cash becomes dead weight. From time to time banks like JPM Chase have charged clients for cash balances over a threshhold.

Socal Rhino said: “From time to time banks like JPM Chase have charged clients for cash balances over a threshhold.”

__________________________________-

When?

why don’t the banks keep their money at their own account or vault. Is it true that new Basel III rules will allow banks to collateralize gold in a repo action at 100% market value? Sounds interesting for gold bugs but I am having trouble to compile all isues. Thank for the article Wolf!

In theory, the banks keep reserves at the fed as a guarantee the bank is solvent and has excess liquidity. The combined excess liquidity of all the banks, at the fed, is what provides the funds and structure to bailout banks that become insolvent. If banks kept their own reserves on site, no one would know how solvent they really are, and there would be no trust among them. Same thing with gold reserves.

What Petunia said about solvency. If it were gold, a private bank could keep it in a vault (and bring it out to show people to ease any doubt.)

But it isn’t gold. It’s numbers written in a ledger. If a bank could write up its own net worth in its own accounts, it could go nuts with instant fraud. Private banks need an outside authority — the FED in the US — to keep accurate accounts of their positions.

Among other things, money is about authority.

Actually banks holding their own gold can lead to loads of fraud. It is easy for them to fake bars, lie about how many bars they have, etc. That’s why the fed holds the bank’s gold as well.

Even the junkies are saying no to the dealer, how interesting. Too bad no ordinary folks get to say this about their own personal finance, especially so with inflation knocking at the door.

“These reverse repos are a sign that the banking system is struggling to deal with the liquidity that the Fed has been injecting via its QE”

Experts agree, free money isn’t all that.

Is the 120 billion/month QE on autopilot, that it has to be corrected by reverse repos, or is there a maturity mismatch to it?

Maximus Minimus,

The Fed has boxed itself into a corner by swearing up and down over and over again that it would give lots of advance notice before it tapers its QE. So now it cannot just ignore what it had said for months, and end QE. So it keeps buying bonds as per its announced QE regimen and then cleans up with reverse repos.

That sounds totally short term view chickensh*t behavior to me. Hail Mary pass hoping to transition without anyone noticing.

Woo Hoo! Central planning by elite morons is the way to go.

But who is really pushing their buttons? They are obviously incapable of independent action even based on their moronic economic models incorporating 3rd grade math.

But overall, something is working very well. I’m not getting rich, are you?

“That sounds totally short term view chickensh*t behavior to me.”

Welcome to Your Nation’s Capitol/Capital”

J2

If they made it look simple, everybody would know what they were doing and it wouldn’t work. I call it the ‘3 cup trick’ for investors.

Seems like this would be a negative consequence of leverage up the wazoo. Need assets as collateral to borrow the money to hedge the out of the money positions.

TBTF might not have the same political backing a second or third time around. Scapegoats are politically useful to keep around.

Isn’t repo and reverse repo overnight daily? Is that because return on other asset worse than overnight repo?

There are also longer term repos (referred to as “term” repos).

Is the bank problem of excess liquidity corrected if they start lending the money out?

Like others here, I don’t understand the concept of why excess liquidity for a bank is a problem.

Thanks for all your efforts here Wolf!

My understanding is that the government “forces” banks to take piles of cash in exchange for T-notes. This puts money into circulation and the banks are suppose to lend it out to create more wealth by starting businesses, allowing businesses easy credit lines. example just went golfing and all of the buildings are freshly painted and all carts were brand spanking new. After a year of not golfing where did all the money come from. Cheap bank LOANS. So the banks have all this cash but don’t want to lend it out because they do have some standards.

The board raised HOA fees, cost of golf course memberships, and green fees to upgrade the gated community golf course. They borrowed money at unsecured rates to do the deal. Removing old turf to get rid of the weeds and upgrading the irrigation system is a seven figure project. Golf course revenues decreased during the pandemic. Homeowners received notice of a one time fee to offset losses that were higher than the usual losses for maintaining a golf course and country club restaurant with dance floor due to the virus.

Sounds like you should have picked a gated HOA based on Bocci ball….or Croquet…..both are also fun and challenging old folks “sports”.

I might add that the PDF I suggested searching for was written in 2013 and talking about the unwinding of QE that was assumed to be imminent ?

Oh how much crazier thr world has become since those simple days with a tiny Fed balance sheet

Bernanke wrote an article for the WSJ in July of 2009 explaining how QE was temporary and how it would just unwind, mature, off the books. I tore the article out, because I didnt believe it.

Still waiting to be proven wrong.

That’s an urban myth that was disproven long ago.

Banks can create reserves. Believe it or not. They can create “money” out of thin air. If they couldn’t, there would be no point in having them in the first place and you could have the economy just run by the Fed.

Banks create deposits, which are unique from reserves which are a creation of the central bank. A central banks balance sheet is assets = reserves + physical currency in circulation + government deposits. A banks balance sheet is assets = deposits + other liabilities + equity. I know banks create money. Reserves can shift between banks but at a macro level bank lending does not effect reserves in the economy as a whole.

Banks create deposits by LENDING.

Reserves are required on certain types of deposits (demand).

Increasing bank reserves through QE gives banks additional LENDING capacity (provided they are not capital constrained and can find creditworthy borrowers).

I think Bam Man has it right (it is easy to get lost in the weeds on bank operational dynamics/monetary expansion via lending).

The only part he leaves out is the nightmare that kicks off the process (Unbacked, at will money creation by the Fed, desperately needed by hugely indebted US Treasury to cover up decades of policy failures) and the nightmarish consequences (soaring ratio of money (printed and multiplied) to existing real asset base (unchanged)…result = inflation.

Okay then let’s put it this way, if reserves are created by lending (they aren’t) then by what mechanism could banks get rid of $3 trillion in reserves by making loans?

They cannot, only the fed, as central bank, can eliminate these reserves.

Also, in the United States the reserve requirement is 0%. Yes, 0. So reserves are not a required part of the banking system in the US.

I should clarify I meant if reserves are *destroyed by lending.

But to further flesh this our, let’s say banks, independently of the fed (this wpuld NEVER happen), decide to remove $1T of reserves from the US. They couldn’t do this even if they wanted to because reserves are part of the Fed’s balance sheet and thus can only be changed by activity from the Fed. When a bank makes a loan, it makes a loan asset and an equal deposit liability. Thats it, nothing affects reserves since there is no reserve requirement.

It’s simple to think that banks are just holding out on loaning $3T but you need to think of the double entry accounting of how it works because it’s more complex than you would think. I might add it’s needlessly complex because of the Fed’s actions.

AA

Yes, but!

Liquidity is dollars (cash) which is demand for stuff in the economy. The Fed thought there was going to be a shortage of dollars to keep everything going over Covid so they pumped in billions by QE. Now they might be worried that they’ve gone too far and they are asking the banks for their excess dollars back before they can add to inflation of prices any more than they have done already.

As Wolf says their PR department has boxed them in with future promises about other assets so they have to use stealth until the PR dept comes round to reality.

It’s better than a soap opera.

@ Wolf and Crazytown –

I think Crazytown is spreading wrong information. If I am right, please delete his mis-information. If i am wrong – publicly chastise me.

The ship is leaking from the front hole. Let’s not plug it. Let’s create hole in the back so the water can get out THAT way.

Yep…that’s exactly right! 100%

ZR – That was a very funny 3 Stooges segment you just described – That’s the feeling I get about these repos.

Good analysis by Wolf that the $3.92T the Fed has by it’s member banks as a “liability” is interesting, and supports what many say is that the Fed has it’s foot floor-boarded on the gas pedal to grow the economy to get this money loaned out.

When I worked at the Fed the member banks had to have around 10% of it’s assets deposited on the Fed books to retain being a member, and the more the member had was a sign of good standing.

However I see there is a push to get those reserves pushed out as loans, which I have heard varying stories of getting small business loans, and companies having to seek out alternative financing because of tighter lending practices – which is a growing concern to me as they circumvent traditional banks and rules.

I would think that any half aware borrower today would walk into a bank and point at that astronomical mountain of idle, excess balances and say “You want me to fill out a *form* to get a loan?”

Helicopter drops don’t ask questions.

Then, when told the going rate on mortgages is 3.5%, they would point to the Fed’s .1% payout, and say…”I’ll pay .5%”.

The continued, now greatly engrossed, existence of that of huge mountain of unloaned money does make you wonder if…most of it were ever really meant to be loaned out.

**Perhaps most of the QEs have basically been a scam since the start,** with the Feds being the masterminds and the banks being henchmen.

The original huge money prints allowed DC to exercise economic control it could never directly achieve without a tax rebellion.

But if the “new money” got heavily multiplied via lending/re-lending, wildfire inflation would have resulted.

So, sub rosa, DC told the banks…”X% of your “excess funds” can *only* go back to the Fed. You’ll get .1% risklessly for keeping your mouth shut”

That would explain why banks have not degraded their lending stds even more…despite trillions in excess reserves.

It would also explain why much worse inflation didn’t happen from 2009 to 2019.

Whereas a broke-ass third world nation

might openly compel private savings be invested in unreliable government Treasuries in order to allow more government spending…

…the broke ass US spends the printed money first and then strong arms Potemkin banks into not lending it on or letting the public know what is going on.

interesting hypothesis ………….

Yeah, so what was your point again?

The need to borrow seems to be short circuited by the Trillion dollar giveaways of the Biden administration.

So the free money to the federal government, courtesy of Fed policy…

1. reduces the need to borrow (banks lend less) due to the giveaways

2. pays people to stay home and not work, hurting the employment numbers.

As in Physics, in economics for every action, there is an equal and opposite reaction.

I suggest a fair return on money, one that covers the inflation rate, would solve all of this. Powell clearly has too many plates spinning,

hissycus:

Please do some more research re your misperception between the ”theories generally agreed on” in the hard science of physics,,, and the obviously NOT hard science of ‘economics.’

The first set of theories/AKA commonly known incorrectly as ”laws” is based on hundreds and thousands of repeats of each and every ”test” of any theory of hard sciences by folks all over the world duplicating EXACTLY the conditions of those tests, AKA experiments. Most recent results re ”muons” suggest even those theories generally accepted of physics are subject to serious revisions, which will happen with new information.

The latter ”laws of economics” is based mostly on opinion, anecdotal evidence/experience, and ”agreement” with very little, IF ANY, scientific tests/experiments…

Other than that flaw, I agree totally with most of your comments on WS, and is really the only reason I ask you to research some of your basis/bases.

And thanks once again to Wolf for at least trying to explain some of the gobbledegook and other ledgerdemain of the current folks/puppets of the oligarchy…

@VV – Perhaps even “the recent results re ”muons” … are subject to serious revisions, which will happen with new information.”

We got quite aways to go yet.

Treasury yields decreased May 20.

DH

Spot on, see my corrected comment above!

I can see excess liquidity causing a problem when you are paying high interest on deposits, because it forces banks to go out and loan money to marginal lenders. But the banks have been paying peanuts since like FOREVER.

Maybe the market does not have enough Treasury securities to grease it.

@Wolf: fantastic chart and commentary, but you neglected to draw a green line between “Quarter End” and “March 31, 2020” !

Yes, that was a quarter-end, buy it was also Covid panic when the Treasury market ran into trouble and the Fed bought something like $500 billion in Treasuries a week. The second half of March was in a category of its own. So I put a date on it so you can see, but I didn’t want it get lumped in with the regular end of quarter dates.

IRX fell off the cliff today

I was thinking for a moment that this was a typo, that you meant to say the IRS fell off a cliff. Now that would be hilarious.

But then, where would they get the small amount of the budget they pay for using actual tax receipts!

I guess it’s why fed begs gov to start blowing cash asap on white elephants instead.

Thanks Wolf, sounds like it’s technical tapering, with the demand of treasuries instead of cash.

We are going to have real inflation and low interest rates — financial repression is coming. The Fed is nationalizing repo (setting price) and will soon do the same for the treasury market.

The yield curve will flatten, gold will moon, and zombie companies (facing lower liquidity) will finally be allowed to collapse.

Joe,

Maybe (hopefully?) the G is okay with letting doomed companies go bankrupt…so long as they don’t do it all at the same time.

I still suspect that horribly run organizations, provided they sell enough votes, will be kept on permanent life support though (see government run…everything).

Wolf, is this normal to ever see them borrow money at negative rates? Read 3x times to try to comprehend-

“a modest amount of trading” in the overnight reverse repo market “occurred at negative rates.” In other words, these participants are borrowing money at negative rates from counterparties that take Treasury securities as collateral

Not normal at all, or else it wouldn’t have shown up in the minutes. There is some extraordinary stuff happening here.

one follow-up.. do we know who the participants or counterparties are? Thanks for also confirming the very odd note in their notes. Why isn’t this getting more press? Basically this would amount to some entities actually dipping into NIRP, right?

Nathan Dumbrowski,

We (meaning me and the public) don’t know who the counterparties are. They’re not disclosed.

“That’s how strong the demand is for Treasury securities in that end of the market.”

Very interesting but, I’m not clear about the reasons for this financial contortionism:

Why would the lender in a reverse-repo would pay (negative interest) to temporarily hold Treasury securities?

How would temporary holding Treasury securities satisfy a demand for them. Wouldn’t the securities have to be returned to the borrower in a day or week?

If you’ve been reading Larry Summers in FT who still holds a big stick. He is a globalist insider. He is saying the FED has got it all wrong. This is major insider warfare.

I think the answer is “look out below”. It appears that the visitors to this site have an interest in finance. The markets, the economy, etc. Now some, like me, might draw the wrong conclusions about what is happening, however, if nobody can figure it out- look out.

1) O/N NR is a good start.

2) The DOW leg 4 was Mar 2020 low. // Leg 5 was May 10 2021 high.

3) The first small wave 1 down was completed.

4) The counter trend up, wave 2, was probably completed.

5) The the O/N NR will get worse.

6) It’s contagious.

What is O/N NR ?

I would say Overnight Negative Rates. It peaked my interest when I read it. I wondered, exactly what is a “Modest Amount of Trading” to the Fed. I think ME is right, it will get worse because it is contagious.

Overnight reverse repo.

The fed is like a pilot in a 1943 wildcat fighter attempting to land at night without lights on a small independence class carrier in a typhoon on his 10th flight.

Sure everything will go just fine……

Actually I was thinking that this is the new warzone. We can’t as grown up nations fight a real war. So this one is going to be a financial war and America is bringing out the big guns. The D-Day, the Little Boy and the Fat Man, the moon shot. The US of A is going to spend us into the 21st Century and let the real roaring 20s be a change. The Great Leap forward to propel us beyond all the others

Hey, fred, you sound like you play WITPAE or something…

Operational losses you coldly expect to notch up when loading up your inexperienced crews and sending them out on your second-rate ships in your reserve task force in difficult weather to try to stem an enemy move you were not prepared for.

Landing on a MMT class carrier.

The effects of doing this should not be unknown or unknowable. To ask the “stupid” question, what’s so bad about this?

Yes, it’s extraordinary, but so what? What’s going to happen?

IF there are market participants who are short bonds (expecting rates to rise), THEN they need treasuries to borrow from someone so they can sell them today, buy them back at a lower price tomorrow and pocket the difference.

The excess reserves has the effect of increasing interest expense at the banks and if the reserves are simply sitting there expenses are going up without a commensurate increase in revenue then net profit falls.

It seems that I’m missing the bigger picture here of why this is bad? It must be linked to the interest/inflation rates?

It’s not necessary bad in general, it’s bad in particular, because it signals some party, could be a big client of a bank or banks, is in big trouble. The fed is providing the collateral needed to unwind positions and the banks are paying any amount to do it. Think Archegos or worse.

Why would FED provided Treasuries be any better collateral than cold hard cash that had to be exchanged for those Treasuries?

“[P]articipants are borrowing money at negative rates from counterparties that take Treasury securities as collateral.”

Don’t you mean banks are “lending” money at negative rates.

Everyone wants to borrow at negative rates.

The banks severely need the Treasury securities to mop up their reserves.

To get the Treasuries, banks are willing to lend to the Fed at negative rates.

“The banks severely need the Treasury securities to mop up their reserves.”

Why do they “need” to mop up their reserves and pay to do it? Isnt the Fed still paying on excess reserves?

H

The Fed QE’d too much cash into the economy and now they are trying to get it back out before people get their hands on it to add to obviously growing inflation;

I reckon it’s a good sign they are trying.

“And the Fed announced in the minutes that it would … likely raise the rate it pays on reserves.”

The first spike of excess federal reserves came in 2008 after the Fed got emergency authorization to pay interest on reserves. Good article on SF Fed about it: “Why did the Federal Reserve start paying interest on reserve balances held on deposit at the Fed?…”

(https://www.frbsf.org/education/…)

September 2008: … Fed lending from the discount window, and its newly created liquidity facilities, spiked … causing excess reserves in the hundreds of billions of dollars range, for the first time far exceeding depositories’ required reserves.

After spending most of my morning coffee energy trying to learn about this, it seems the function of paying interest on federal reserves is to keep banks from lending those excess (non-required) reserves on the overnight federal funds repo market, which would lower the rate below FOMC target rate “since depository institutions have little incentive to lend in the overnight interbank federal funds market at rates below the interest rate on excess reserves.”

So the Fed decides to pay more premium to hang onto it’s balance sheet liability (excess reserves it owes the banks). I assume that the extra money required is created by a few clicks of mouse and keyboard.

The goal seems to be to keep the FOMC target rate from crashing into negative territory. Hopefully, the boy can keep his finger in the dike until some adults find him and fix the hole.

It’s a twisted world when the farmer arrives carrying a bucket of slop and the pigs cry out “no more! no more!”

Or the farmer saying no more bacon. No more bacon! We have the fridge, freezer and ice chest full

Meaning you can give the banks literally $4T but if there are no loans to give out they can’t use the money effectively. Too much glut in the banking industries gloablly

When you destroy faith in the future value of a currency through money printing, market participants freeze in the headlights and stagnation occurs because those participants don’t know how to price transactions when the world goes Weimar.

If there isn’t a religion that considers that heaven we need invent one.

Interesting times indeed. If the Fed admits there is an inflation problem, then the burden is on them to fix it. However, the problem is the Fed propping up the economy on inflation, so if they stop propping up the economy then it all comes falling down. And inflation certainly is here, with the Fed dismissing it, like everything else.

Most confusing financial rabbit in a hat exchange I have ever tried to unsuccessfully understand.

Felt like Fed = dog, Banks = tail. Fed wagging.

Result for Joe Bag-O-Donuts and stock/bond markets? No clue. I will read this article 10X.

Beardawg – I think that is part of the point.

Opacity and gamesmanship so that only a few parties actually know what’s going on and with whom. I think they are also counting on many, if not most, not understanding what is happening. I further suspect they are counting on the press failing to report this activity to the masses. Just to many awkward questions.

Sadly, there is no way there isn’t some very serious game play happening.

It looks to me like the FED doesn’t want to hold the Treasuries. Are thy seen as to big a risk to hold? It has some logic.

CRV

I say this a lot.

When the Fed SELLS paper of any sort, it takes cash dollars out of the economy and reduces demand for stuff in the shops hence easing inflation pressures.

Vice versa when the Fed buys paper of any sort it goes the other way round. It all looks very complex because they like it that way.

I agree with Wolf that they are so boxed in by PR on all other asset tapers , this is probably all they can get away with for now as a first hidden step.

You’re missing the elephant in the room.

Or rather, the herd of elephants.

Banks could as well use the reserves to give credit to everyone and their one-eyed brother-in-law. But they don’t. Why ?

It’s called “Rehypothecation”.

Treasuries are lent out ten times and more in the private Repo market (hint: banks, hedge funds and other financial entities also use repo’s among themselves to get liquidity) and in the end noone knows who owns them. Sort of awkward when it unwinds. Banks urgently need treasuries as collateral to keep the whole thing from blowing up badly. That’s why they throw the reserves they got via QE right back at the Fed.

One could also call it a scam.

Of course you are right, but bringing it up will definitely scare the horses.

Americans still hold on to the notion of property rights. You don’t want them to think they have property rights, sort of, kind of, in theory.

The US government views its citizens’ property rights the same way Nigerian scammers view their marks’ property rights.

“All your dollerz belong to us”

https://www.federalreserve.gov/econres/notes/feds-notes/ins-and-outs-of-collateral-re-use-20181221.htm

Franz Beckenbauer said: “Banks urgently need treasuries as collateral to keep the whole thing from blowing up badly.”

____________________________________

Makes no sense to me because Dollars are just as good, or better collateral as treasuries.

We are now stuck in some parallel universe where everything is upside down:

– You get paid for borrowing and get charged a fee for saving

– “Risk-free” assets are guaranteed losers, risky assets are backstopped

– Sitting on your ass pays more than working (for some at least)

– The best performing “assets” and hailed “store of value” are crypto backed by absolutely nothing.

You cannot make this sh!t up

The Fed has made Lender slave to the Borrower…

every since 2009

Have Fed Funds ever been 4% below inflation?

Have 30yr mortgages ever been below inflation?

If the Fed had stuck to their instructions/mandates, most of this would not be happening.

promote max employment

promote STABLE prices..they promote inflation instead

promote moderate long rates….they promote record low long rates

it all changed in 2009. Did you get the phone call? I didnt.

I did not get the phone call, but over the emergency loud speaker I heard Bernanke say “helicopter money” and “I have this thing called a printing press” and that was enough for me.

The “digital dollar” is now be discussed by our “leaders.” I urge everyone here sitting on cash to listen carefully to these discussions. We are going to have a currency reset.

Keep…

But the curve ball was that the Bernanke moves were in response to an emergency per the 2008 debacle.

And, Bernanke said QE was temporary.

I guess we should assume as with Yellen and now Powell, these people are paid LIARS.

Intentional misdirection plays.

Quite agree YuShan

“crypto backed by absolutely nothing”

Kinda a draw with the dollar on that one.

If DC thought it could actually substantially hike tax revenues (the “backing” of USD) without IRS agents’/politicians’ heads being mailed back to DC…it would have done so already and skipped the subterfuge that inflationary finance affords.

everyone gets this wrong. crypto is backed by wasted electricity. what that says about our civilization speaks volumes.

Finally a good article. The next q is what impact will it cause to the markets should the QE be withdrawn. The immediate impact I can see is yields gg up (which might affect valuation). But with the deeply entrenched BTD and TINA mentality, any crash to the market is unlikely unless regulators decide to restrict the amt of debt one can take.

1) Mar 31 2020 the Fed drained the market. Mar 31 is a spike, but the

drainage lasted until Apr 2020.

2) On Apr 1/3 the DOW gap lower and and built April islands.

3) This gap is still open. The next correction target is Mar 2020 low. The next correction will close Apr 2020 gap.

4) On Apr 1 2020 gold was shaken, but recovered.

5) WTI Futures didn’t recover. They plunged to minus 40 on Apt 20 2020.

6) Yesterday RRP spiked @$351B. The total accumulation in the last month is over $1T. Spikes poke the eyes, but the total accumulation is more important.

7) The Fed ordered the banks to build up US treasuries, a defensive line, to prepare for the next downturn.

Gaps everywhere. If you believe in gaps closing… everything is goin back to October ranges.

Banks aren’t buy treasuries, they doing RRP. They will continue until they know rate will drop (have peaked).

Great article, but explosive !

I want my MTV.

1) Co board room prepared new tools for the next downturn : back in the office, vaccinated. Either PFE, Moderna or JNJ, for safety.

2) Those who refused will be sacked.

3) That’s how private co will consolidate.

The banks might need pristine collateral (Treasuries) for overnight lending/ the repo market. QE takes away that collateral and sometimes creates problems. Jeff Snyder from Alhambra Investments (Eurodollar University) goes over this and other QE effects a lot. Probably the most knowledgeable person in this space.

How are treasuries any more pristine as collateral than dollars? They aren’t and therefore it makes no sense to buy treasuries yielding negative rates.

FDR made the same mistake initially: Pumping liquidity into banks in hopes that would stimulate investment. Banks loan money out only to credit worthy customers. If there aren’t many out there, the money stagnates at the bank. During the Great Depression in the 1930s, some banks simply closed up for lack of creditworthy customers. 80% of all bank loans are for property. Very little actually ends up in productive investments. We’ve destroyed our productive capacity because everyone believed Reagan when he announced the government was the problem. Everyone has been taught flunkenomics. Guess who is left standing with money to make productive investments. Yup. Uncle Sam. Is there anyone left who knows how to do that?

It was NAFTA and the Clintons that killed our productive capacity.

China.

…And the US agreeing to brain-dead WTO rules (which gave China free rein to implement domestic Chinese policies that largely subverted the recycling of initial Chinese trade surpluses back into intl trade, ie US exports).

Might I suggest the government get HEAVILY involved in starting a massive Green New Industry and Conservation Program, along with all the re-education of the labor force to accomplish it?

Aside from needing productive jobs, we do appear to be killing our little ball in space, at least as regards Homo sapiens. Yes, this IS on topic.

Side note, the biomass (and, of course numbers) of single celled critters FAR exceeds that of all animals and plants maybe thousands of times over.

So from a biologist point of view, we aren’t AT ALL viewed as the MOST successful present life form, just an another interesting type of bio-diversification.

i would settle for the conservation part. hire kids to plant trees and let them get a deal on student loans out of the bargain. clean up trash. there is plenty that needs done, and how we currently operate is not sufficing. community service could be an entry level job, not just a wrist slap punishment.

i am skeptical of the green new industry part. sounds like using more technology to solve the problems caused by previous technology. this mindset might vie with the FED’s strategy when it comes to the all time best can kicking shenanigans.

All the financial trouble we peasants are going through, and banks’ problem is too MUCH cash?!

Wolf is this the result of “Pushing on a string”?

“These reverse repos are a sign that the banking system is struggling to deal with the liquidity that the Fed has been injecting via its QE.”

Wolf,

I thought QE extracts the Treasuries from the banks leaving the market in need of collateral to cover the REPO transactions. The counterparties only enter the RRP market to obtain the Treasuries the need since they are all at the FED due to QE.

Could this liquidity issue be due to:

1) Covid stimulus being deposited in banks by individuals?

2) Businesses (Foreign and Domestic) deposited cash from transactions of the US opening up?

3) Tax payments since May 15 was tax day in the US?

4) Not enough Treasuries (due to QE) for the large influx of cash forcing the Repo market into negative rate territory?

Thanks for the education.

Joe

Joe,

Banks are holding a record amount of Treasury securities (black line):

https://wolfstreet.com/2021/05/17/who-bought-the-4-7-trillion-of-treasury-securities-added-since-march-2020-to-the-incredibly-spiking-us-national-debt/

Thanks, Wolf.

I see that Treasury and Agency Securities, All Commercial Banks (USGSEC) as of Apr 2021 is $3,988.9129 (ALL TIME HIGH) (see link (a) below).

I understand that the Securities should be found on the Assets and Liabilities of Commercial Banks in the United States – H.8 (see link (b) below).

My question is why the need for the RRP if the banks have the cash and the securities in their possession? If there was an adequate supply of collateral for the REPO market there shouldn’t even be a need for the FED Reverse REPO market?

Which gets back to my question of is the Fed is simply replacing the Securities with Reserves also known as Other Deposits (see link (c) below) category?

I don’t mean to be hard headed. I have a difficult time recognizing the need for the RRP with such an abundance of Securities in the market. I feel sure I am missing something.

Thanks

Joe

(a) https://fred.stlouisfed.org/series/USGSEC

(b) https://www.federalreserve.gov/releases/h8/current/

(c) https://fred.stlouisfed.org/series/ODSACBW027SBOG

“the Fed is figuring out that you can push QE only so far before something big is going to go haywire with unforeseen consequences.”

Sounds black-swan-ish.

An experiment in explosives.

We hope they learned something. This was a massive experiment never seen before. Like trinity

“Like trinity”

ND, that is NOT reassuring. But then, what could possibly go wrong?

:)

“An experiment in explosives.”

DC is the Mengele of macroeconomics.

And when our evil government is shrunk to the size where it can then be easily drowned in a bathtub, just WHO then, will run the show?

The painted up guy with the horned helmet? or his savior? or someone similar?

Surely not the “invisible hands”…….or some ancient musty old bloodthirsty desert diety…….

The poor banks are suffering from people paying down credit cards and payday loans. The FED and banks just need to stuff more money into the stock market somehow sneaky for another good surge and find a new way to trap people into more high-rate credit.

Excellent article and comments. A lot to take in and even more difficult to understand. Inflation is now approaching 4%, the yield curve is flattening with short term rates at 0 early this week. Banks have more money than they can loan and the banks and the fed seems to be a little concerned about the next overly leveraged PE or hedge fund failure. The dollar has lost 12% against the Euro in the last year. Emerging markets are faltering as covid begins is spread in SEA. Pending home sales have declined due to lack of inventory or increasing rates. Young millennials can not buy a home and its not for lack of want or trying. Older retirees are now loosing money on their savings and are loaning to the banks for free. I have no understanding on how this will effect the cash in my brokerage account since regulations were changed on the break the buck with prime money market. Sometimes I feel that Powell is really just trying to hold the economy together in 2021 so it will blow up in election year 2022. I need to read the comments again in hopes that my comprehension will improve.

I think your comprehension is just fine!

The money markets are awash in cash, and cannot pay depositors interest. This is an ongoing problem, if you can’t pay interest then you are breaking the NAV. So they yard up a pile of treasuries from the Fed and the borrow rate there is still negative. The Fed can raise the rate on reserves, and not raise FFR, but it all gets hinky. Fed wants to set up a permanent facility, which means they ain’t tapering anytime soon. Are we at that place where too much money really is – too much money. Liquidity trap, maybe? The non-Treasury MM NAV broke in GFC, in this instance they have everyone’s back. How does that work?

1) Who bought the $4.7T Treasuries since Mar 2020 : the whole

world.

2) Who spiked the most :

3) Japan & China : no. // Foreign holders : no…

4) The Fed fake : the Fed accumulated $5T, prior to the $1T RRP.

5) The major banks accumulated probably > $1.4T to avoid another 2008 event.

6) Will the bank Maginot line survive : first it will grow in power, thereafter ==> a banking crisis.

7) The banks will be overwhelmed by the NPL tsunami.

8) The RRP derby : Wolf 1: 0 Jeff.

How do you engineer real inflation so that wages rise?

Private US manufacturers and innovators are lacking access to low interest rates and trade protections . The commercial bankers are rigging the game for executive profiteering. There is no desire to finance private manufacturing and resource security as long as the corporate elites are permitted to manipulate global trade to maximize their profits and offshore tax havens. Municipal governments are lacking real tax revenue because of trade deficits, which starves infrastructure spending in favor of retirement security. The organic fundamentals of a healthy economic foundation are so distorted by the imbalance of trade that it has impaired the FED’s ability to man the helm with 100 foot surf on the port side beam. If the FED policy is to let inflation run, then the FED is putting pressure on the commercial banks to steer that capitol into productive assets that locally manufacture goods we consume and public infrastructure we use, reversing the trade deficit, essentially steering the capitol into real inflation…..or loose it by default! In a nut shell, we have to start producing the goods we consume to spend the capitol on Mainstreet rather than speculate with it on Wallstreet. This is why the globalist bankers/elites would rather see QE tapper and rates slowly rise, because they are so heavily invested in the 60 foot surf of trade landing in US ports every day.

I slept on this last night to try and understand/identify the context of insider FED warfare…this may help, if I had more time I could probably explain it better. Make no mistake, the Elites are at war with each other.

How do you engineer real inflation so that wages rise?

Private US manufacturers and innovators are

lacking access to low interest rates and trade protections . The commercial bankers are rigging the game for executive profiteering. There is no desire to finance private manufacturing and resource security as long as the corporate elites are permitted to manipulate global trade to maximize their profits and offshore tax havens. Municipal governments are lacking real tax revenue because of trade deficits, which starve infrastructure spending in favor of retirement security. The organic fundamentals of a healthy economic foundation are so distorted by the imbalance of trade that it has impaired the FED’s ability to man the helm with 100 foot surf on the port side beam. If the FED policy is to let inflation run, then the FED is putting pressure on the commercial banks to steer that capitol into productive assets that locally manufacture goods we consume and public infrastructure we use, reversing the trade deficit, essentially steering the capitol into real inflation…..or loose it by default! In a nut shell, we have to start producing the goods we consume to spend the capitol on Mainstreet rather than speculate with it on Wallstreet. This is why the globalist bankers/elites like Larry Summers would rather see QE taper and rates slowly rise, because they are so heavily invested in the 100 foot surf of trade landing in US ports every day.

The only thing about this consistent with the markets, is that the banks want to unload cash. Investors aren’t buying assets they’re selling cash.

Stoneweapon, I always appreciate your posts.

And perhaps your handle will, in time, reflect the next world order. You know, a step back in time?

“How do you engineer real inflation so that wages rise?”

I dont understand. How about no inflation? Why is inflation the objective?

It hurts the working family more than any modest wage increase.

What’s it do to the young family looking to buy a home? A car? Cant save their way to financial stability.

There is NOTHING good about inflation for those who work, save, earn.

H

It is established economic convention that ‘demand’ running moderately (2%) ahead of ‘supply’ ie 2% inflation draws out increased supply and hence production and investment.

Trouble is everything is so distorted nowadays, these old theories don’t get a chance to work anymore.

“It is established economic convention”

________________________________

Now there’s something to hang our hat on! I call BS or propaganda. It is a self serving narrative, Not science.

I don’t understand this directive.

Fed can guide commercial banks but commercial banks need to guard their profit. The local/small business only can get loans when it can compete against the big guys who have lower cost overseas. I don’t see how local/small business can fight against the rising cost when the big guys can outsource globally for the cheap and various gov concession. Without that perspective, bank won’t give cheap rate to local business, nevertheless the small guys always have higher risk.

Regarding the bankers/elite, I don’t believe they invest one against the other. They invest in big trends (transaction-based or asset-based) and it hasn’t changed for last 30 years and won’t for the next 30 if fundamental structure doesn’t change. The 100 foot surf of trade is the result, not the cause.

Correct me if I’m wrong.

Very smart!

The FED is like an elephant gone must that has escaped during a live circus act, and is stomping and thrashing its way through the crowd leaving dead and maimed people by the score. It needs to be put down before it does even more damage.

Eloquently put.

Personally, I picture an elephant that has been Fed a diet of ZIRP brand laxatives.

Pity the poor audience.

9) US gov debt by holder category : the bank black snake had Zero

Hedge in 2009.

10) Relative to 2009 level : US Investors accumulated and increased the most.

Someone mentioned Jeff Snyder. I’ll one-up you and invoke Zoltan Poszar. These two guys are “gurus” (and maybe oracles) of the bond market, and rarely will you see them write anything that is even remotely coherent, logical or understandable without being member of a secret club with a secret decoder-ring.

A lot of self-styled experts follow the gurus and make comments on what they say. Hardly any of the commenters understand the topic at all, and the comments range from worthless to outright anti-productive.

I’m now seeing things I never in my life dreamed of. How about 24 year old pickup trucks asking $35,000? I despise Larry Summers, but he was right when he warned that CONgress and the FED were going to overheat the economy. They grotesquely distorted everything. They are extremely dangerous idiots.

At this point, what is better…tightening for a chain reaction of defaults or allowing inflation to reshape the the playing field?

The higher prices rise, the more opportunity to start making your own stuff locally and reinvent better ways to do things.

“chain reaction of defaults”

Assigns blame where blame is due (awful company leadership kept in place for decades only by virtue of DC ZIRP life support/Brainless RE speculators…and the worthies in DC).

Inflation expropriates *everyone* – including those who saved and busted their ass to avoid the crooked games of group 1.

Why perpetuate (through inflation) the absolute unaccountability that has led the country to this moment of ruin in the first place.

If the bastards and morons aren’t held accountable, they will eagerly go on being bastards and morons.

If the last 50 years has taught us nothing else…it has taught us that.

Damn straight, Cas127.

UPDATE

Just released: This morning’s overnight reverse repo was $369 billion, with 52 counterparties, even bigger than yesterday’s $351 billion with 48 counterparties. In other words, yesterday’s reverse repo matured this morning and was replaced by the $369 billion reverse repo which will mature on Monday.

Since the Fed opened the RRPO window money flows have reversed higher and impressively. Treasuries are better collateral for trading purposes than cash reserves. The decision came at the second test of the 50dma for SPY. The market ramps, MM investors go risk on and the excess reserve problem is solved, investment banks return the treasuries they borrowed and sell stocks they bought with the proceeds to the muppets for a markup. With these nose bleed valuations you need to give them incentives to buy.

” Treasuries are better collateral for trading purposes than cash reserves.”

_____________________________

How so? Seems to be a ridiculous statement.

OK, just to put things in perspective in my mind, I visualized this little tidbit:

The amount of overnight reverse repo action, which is essentially just swapping cash from Wall Street banks for Treasury notes from Wall Street’s Fed, and then reversing everything hours later in what is an accounting slight of hand, is equal to the GDP of the entire USA economy in six days.

Yeah, six days worth of all monetary transactions in the USA are flipped back and forth by the Fed & Wall Street on a nightly basis now.

From Bud (Harry Dean Stanton) in the 1984 cult classic: “Repo Man’s got all night, every night.”

Dan-s’allright, i’m sure we can still get food from machines (but don’t look in the trunk…).

may we all find a better day.

It happened before and why couldn’t it be handled again this time? Just bigger number which FED has plenty of.

I’m also trying to figure out if the FED has been covertly commandeered by US Military directives as has foreign policy. The glimpse were getting of the inside war may be telling us the globalist structure of power is being dismantled for an American First policy. If there is any truth to this, I can’t see the US Military nuking their Achilles heel (USD) without an alternative.

You’re kind of onto something, but you got it a bit backward:

The US Military is killing people and toppling governments all over the world in order to maintain US economic dominance, even in the face of rampant devaluation of the USD by the Fed’s money printing.

Case in point: The US holds a much-hated minority government/monarchy in Saudia Arabia hostage to US military aid, and demands in return obedience to the US economic in the form of demanding that KSA will sell oil only against payment in USD.

This is standard colonialism with a flavor of monetary dominance. You could say that our money is backed by USG debt ,which in turn is backed by the US war machine and its nuclear weapons.

/US economic/ should be /US economic interest/

Thank you, I jumped ahead in the context a bit of what I see may be happening in the US Military. I agree with your assessment. I think many of the least corrupt generals in the US Military started to wake up when China’s robust manufacturing growth evolved into the “Belt and Road Initiative” and “Replicate and Replace”, which became a serious threat to USD Hegemony while allowing their own country to rot. Is an America First policy now a US Military policy?….and what would you do with the FED if it were?

Stone/Nar-cue Eisenhower’s farewell speech…

may we all find a better day.

This is old news. Think ‘Banana Wars.’

Smedley Bulter: War is a Racket.

The new is as old as the phenomenon (born around 1945). But it is old news that hardly anyone has heard, and it should be repeated until everyone has heard it.

I can’t fully understand what this all means. It is so much money everywhere that even the banks are scared? And more today than yesterday.

Does this have to do with out of control inflation? Or is there imminent collapse of the market?

What is the take away? There is so much money floating around.

Since we no longer produce much and have much less productivity to account for all the dollars we print, we create financial complexity to replace real productivity.

It’s like a make work project where real people get hurt, while the financial engineers get a huge paycheck for pretending to work.

The Glass Bead Game

and Hesse wasn’t even an “economist”………

Yeah I don’t get it either. And I’m in charge of this whole thing!

All I know is my homies like it when I print money! And I live in a giant house in the Bahamas!!!!!! Hahahahahahahahaha!!!!!!!

I still remember how Tim Geithner looked in March 2009…he had the eyes of a man who knew that he might shortly be ripped apart by a mob.

Really, for such moments, you need the standard issue, soulless DC political sociopath who always assumes he can bullsh*t his way out of anything.

That was the time for an “insurrection”.

Powell is doing too much QE and using lending facilities for certain programs to avoid the Treasury issuing more debt.

He should not be buying more than 100% of issuance in treasuries or MBS this late in the game.

At the behest of the US, the ECB and BOJ programs have been intentional to force money into the US to prop up the center. Negative yields here would be counterproductive.

No such thing as too much QE, homie. If you could touch things and turn them to gold, would you stop???

This reminds me of the movie Lorenzo’s Oil, about a child with an inherited inability to metabolize certain fatty acids. The body would build up huge quantities of these fatty acids in order to produce the end products that should have resulted from the metabolism of the fatty acids. The resulting accumulation caused severe nerve disease.

QE was a failed attempt to reinflate the economy. Instead, the precursors it produced (like Lorenzo’s fatty acids), just accumulated without proper metabolism (into lending) and we got a buildup of incapacitating crap in the system. QE could not, and did not, produce price inflation.

Despite all the reading I’ve done about how the Federal Reserve system is built it’s hard to make sense of it, and this is reflected by the incorrect predictions of people who supposedly know how it works. A lot of very prominent pontificators predicted wild inflation when QE was started. Wrong. Just like Japan was wrong.

If the Fed does what should be done to resolve the problems with reserves (taper QE) it will kick the crap out of the stock and bond markets. Stocks have only one valuation signal – the Fed balance sheet. If the Fed stops QE it naturally follows that bonds are going down.

IMHO reverse repos are a pathetic attempt to do what a QE taper would do without having an official taper.

To compound the matter fiscal stimulus, which definitely causes inflation, is being implemented by stimulus checks and Biden’s Make America Weimar program, is going to do what QE could not.

Bye bye QE, hello MMT. Don’t be surprised if we see hyperinflation. This time, however, there won’t be a Volcker to ride to the rescue. Raise interest rates, increase the value of the dollar, destroy prices in the stock and bond markets sounds a lot like deflation to me. The chicken shits running the country wouldn’t dare.

No hyperinflation. Just a repeat of Jimmy Carter’s malaise 2.0. Real Estate will top out somewhere near where it is now and show no appreciation for 5 years until the shadow inventory is absorbed.