And five SPVs expired, including the one that bought corporate bonds and bond ETFs.

By Wolf Richter for WOLF STREET.

The Fed has now put on ice five of its SPVs (Special Purpose Vehicles) which had been designed back in March to bail out the bond market. It unwound its repo positions last June. Its foreign central bank liquidity swaps are now down to near-nothing except with the Swiss National Bank, which seems to have a need for dollars. The Fed has been adding to its pile of Treasury securities at the rate spelled out in its FOMC statements, thereby monetizing part of the US government debt. And it has been adding to its pile of Mortgage Backed Securities (MBS).

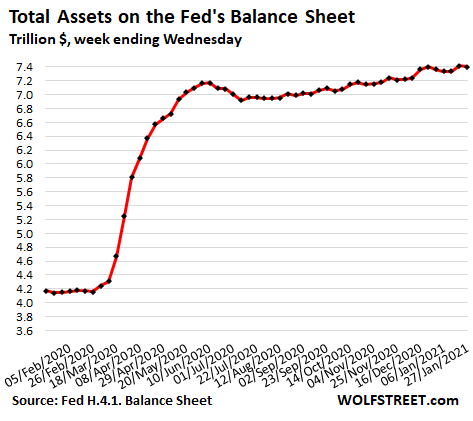

The result is that total assets on its weekly balance sheet through Wednesday, at $7.4 trillion, are roughly flat with the level in mid-December and are up by $200 billion from early June, with an average growth rate over the six-plus months of $30 billion a month.

And the crybabies on Wall Street that have for months been clamoring for more QE have been disappointed. It’s still a huge amount of QE, but for the crybabies on Wall Street, it’s never enough:

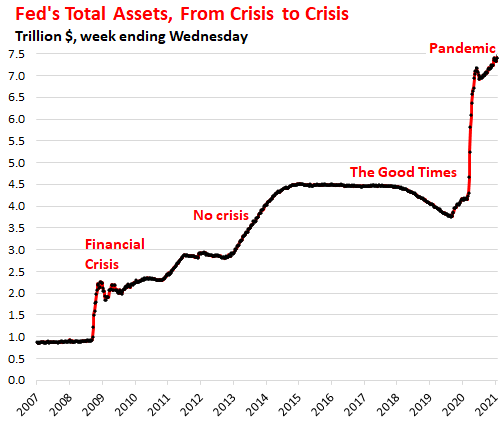

But the long-term chart shows just how hog-wild the Fed had gone, furiously trying to bail out and enrich the asset holders, which are concentrated at the very top, thereby creating in the shortest amount of time the largest wealth disparity the US has ever seen. From crisis to crisis, from bailout to bailout, and even when there is no crisis:

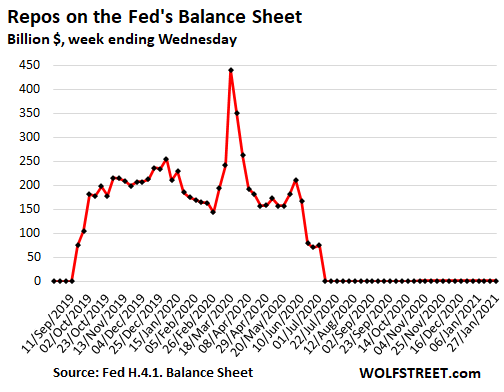

Repurchase Agreements (Repos) remained at near-zero:

The Fed is still offering to buy repos but there have been essentially no takers after the Fed raised its offering interest rate above the market rate. Repurchase agreements are in-and-out transactions where the Fed buys Treasury securities or MBS from a counterparty with an agreement to reverse the transaction on a specific maturity date. The most common repos are “overnight repos” that mature the next day, when the Fed gets its money back, and the counter party gets its securities back:

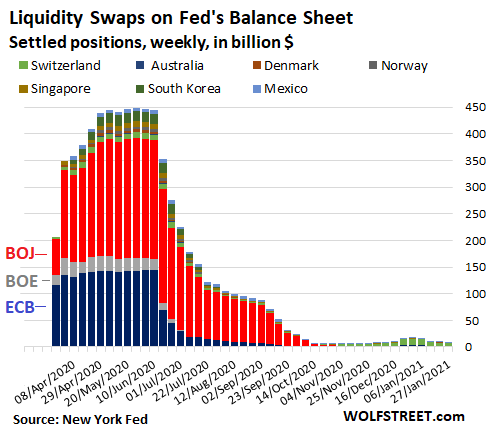

Central-bank liquidity-swaps nearly gone, except with the SNB.

With its “central bank liquidity swaps,” the Fed provided dollars to 14 other central banks in exchange for their currency. Those swaps have maturities, and nearly all of them have matured and were unwound, when the Fed got its dollars back, and the other central banks got their currencies back.

The Swiss National Bank is the only central bank with which the Fed increased it swaps starting in October. By the end of December, they reached $10 billion. Currently, they’re at $6 billion, accounting for 63% of the total swaps, now down to just $9.6 billion, from $449 billion at the peak:

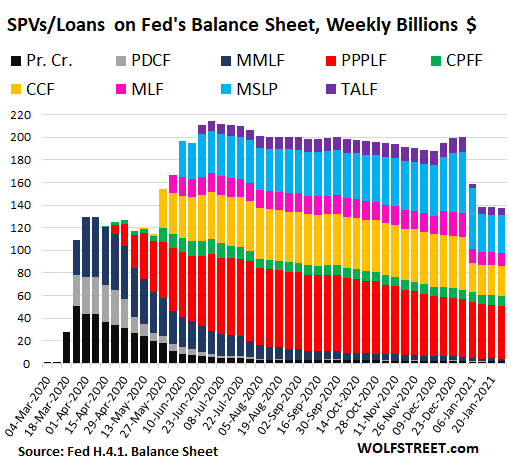

Most SPVs on ice, five expired on Dec 31.

These Special Purpose Vehicles (SPVs) are a way for the Fed to buy assets that it is not allowed to buy otherwise. They’re separate legal entities (LLCs) that the Fed created with the help and equity funding from the Treasury Department. The Fed lends to SPVs, and shows the sum of these loans and the equity funding from the Treasury on its balance sheet.

Five of the SPVs expired on December 31 – the PMCCF, CCF (the corporate bond and bond ETF buying program), MLF, MSLP, and TALF – as a result of then Treasury Secretary Mnuchin’s request on November 20 to end the programs and return the unused equity funds to the US Treasury, and Fed Chair Powell’s announcement that the Fed would do so.

This effectively shut down the corporate bond buying program. But the Fed had stopped buying corporate bond ETFs in July and by last fall was only buying a smattering of bonds anyway. The Fed still holds most of the bonds and ETFs it bought in 2020 but won’t add to them. The drop-off in the chart shows the return of the unused equity funding to the Treasury, with the total balance now down to $137 billion:

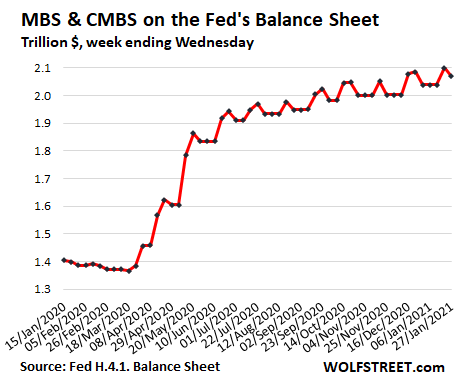

MBS zigzag higher.

Mortgage-backed securities on the Fed’s balance sheet fell by $30 billion in the latest week, to $2.07 trillion, after having risen by $60 billion in prior weeks, after having been flat for three weeks in a row, after having fallen by $47 billion in the week before. That’s how it goes with MBS.

All holders of MBS receive pass-through principal payments when the underlying mortgages are paid off, either when the home is sold or the mortgage is refinanced, such as during the current refinancing boom. The Fed buys large amounts of MBS in the “To Be Announced” (TBA) market, to replace the pass-through principal payments and then to increase its balance. But trades take months to settle, and the timing doesn’t match the pass-through principal payments. The Fed also sells MBS outright from time to time. All of this creates the zigzag:

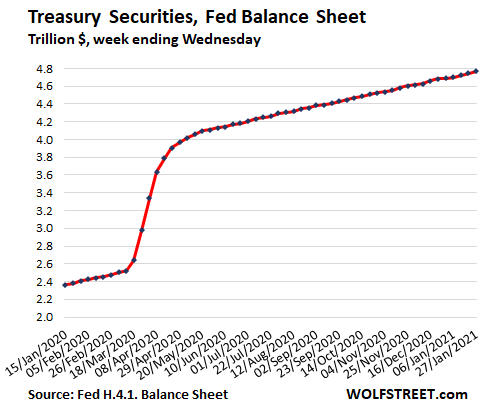

Treasury securities continue to rise.

Since July, following the huge binge in March and April, the Fed has been adding on average $83 billion a month in Treasury securities, and its holdings have grown to $4.77 trillion through Wednesday. Of the $4.2 trillion in debt that the US government has added to its mountain of debt since early March, the Fed has monetized 54% or $2.3 trillion of it:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Home prices are trending up at 10% per year, and the Fed is still buying mortgage backed securities to juice it even more?

Why is the Federal Reserve Board pushing home ownership out of reach for younger generations?

Let home prices fall a bit for everybody’s sake.

Yesterday at Powell’s press conference:

Question: do you think zero interest rates are fueling asset price increases?

Powell: we don’t think there is any relationship between low interest rates and asset prices, investors are bidding up asset prices in response to vaccine success.

Can’t make this stuff up.

Vaccine success? Where? Maybe in Russia and Asia. Certainly not here.

Hahaha… I mean, who isn’t paying $1.1 million for a $1 million house because you might get a vaccine in the next 3-9 months that might allow you to resume pre-pandemic life to a small degree.

… until the mutant strains render the vaccine ineffective next fall!

I really find it fascinating that the media fawns over this fool.

“I really find it fascinating that the media fawns over this fool.”

That’s all they’re allowed to do. If you think they can ask any question they want, you’re sorely mistaken. Danielle DiMartino Booth worked for the FED. She said that only certain questions are allowed, and if you ask something taboo, that will be the last question you are ever able to ask, and you will never have access again.

He is not a moron. He has been given responsibilities by Congress not that different from the Secretary of State. One aspect of his job is to be obtuse with is language. I would like see someone translate what he says to about a fifth grade language level. Say we are printing money and buying government debt because politicians are lying to citizens and are taxing them through raising prices for stuff you will need to buy in the future.

“No relationship between rates & prices”….blahahaha. This is exactly the wealth effect that Bernanke talked about.

If JP admits that the Fed F’d the country, they will then be tasked to fix it.

To keep the rich on top, people need to pay insane prices. Who would do that if JP admitted the Fed created an unsustainable bubble?

The mandate of the fed is one thing and one thing only – prevent bank runs at all cost.

JP can’t tell us the truth because it would crash the markets. What he is doing is exacerbating the problem hoping he isn’t in the chair when the music stops. Completely selfish move on his part because if the truth is scary the lie just makes reality worse for everyone.

EXACTLY key erect caveguy and MB,,,

The rest of the story, like most of history, is just ”blowing smoke” (BS) somewhere the sun don’t shine as the good ol boys used to say it anytime they were in ”polite” society…

With the over all arc of his and her stories beginning to collide with the micro and macro management of the Fed and the rest of the corrupt cronies of the current version of democracy and capitalism, which in fact are neither in any classical definition, we are doomed to do, once again, EXACTLY what has been done dozens of times in the last couple thousand years, with the almost guaranteed same results.

NOT, to be clear, absolutely guaranteed,,, just almost,,, but, after couple thousand years of human behaviours being documented, we can be fairly sure, eh?

Unless it really is ”different this time” due to the amazing connections of folks through the darpanet, or whatever the proper name for our digital world is???

“There are other significant ‘anomalies’ that have challenged the old as well as the new mainstream approaches. While theories place great store by the role of interest rates as the pivotal variable that has significant causal force, empirically they seem far less powerful in explaining business cycles or developments in the economy than theory would have it. In empirical work, interest rate variables often lack explanatory power, significance or the ‘right’ sign. When a correlation between interest rates and economic growth is found, it is not more likely to be negative than positive. Interest rates have also not been able to explain major asset price movements (on Japanese land prices, see Asako, 1991; on Japanese stock prices, see French and Poterba, 1991; on the US real estate market see Dokko et al., 1990), nor capital flows (Ueda, 1990; Werner, 1994) – phenomena that in theory should be explicable largely through the price of money (interest rates). Furthermore, in terms of timing, interest rates appear as likely to follow economic activity as to lead it.”

http://eprints.soton.ac.uk/339271/1/Werner_IRFA_QTC_2012.pdf

Very good start jc, especially the following quote from the paper you reference:

“Whether or not our economies manage to avoid a major global depression, economics is in crisis. … [We need] to rethink a great deal about economics and how economies operate”

(Johnson, 2009).

Donald Kohn (2009), as Vice-Chairman of the Federal Reserve, reflected the sense of embarrassment of the economics profession when having to admit to the public that

our economic models simply assumed that banks did not exist:”

I would only add/suggest that, as mentioned earlier in this thread, it might be better for all of us (except the banksters,) if banks did not exist, and were replaced by credit union type of facilities for storage and safe transfer of ”money.”

As to ”economics,” anyone with any real world experience knows, at this point in time, it just another consumer fraud, etc., etc., with no more accurate information than the slipperiest ”tout” at the local track, and equally self serving.

Is Powell that dumb or that dishonest?

The Fed has erased the fixed income avenue for investing and created an equity, yield chasing, desperation investing cattle drive.

Do they really not know that?

Yeah, they know it. When they are talking about different subjects (ie subjects other than the effects of low interest rates), they must occasionally allude to the true reality of market distortions (in passing) without openly saying it in order to explain various realities. Remember the cat that appeared twice in the Matrix?

Trying to get them to talk about these things directly is taboo as that would lead to the exposure of the lies.

The billionaires who own the media will never let this happen. But it’s cool anyway. Us dumb cattle ain’t going to bat an eyelid if it means getting richer via asset wealth bubbles. Don’t think about how are your children going to afford a home. It’s cool, they can rent in their fuedal lord’s cinderblock tenement suburbs. Hell, they will working 16 hours a day so who cares where they live!

Watch TV. Go fishing or hunting. Become consumed by flipping. Do anything but inform yourself as to what’s truly going on, and the crap farm can stay in business.

Hooray for economists and central bankers!!!!

A great post Chewer, ESPECIALLY the cat analogy.

That’s why Art and artists are needed, even the often despised Basket Weaving 101.

There was a time when that skill was needed for mankind to merely EXIST, and a curious artist/scientist created it.

Having followed the minutes of the FED leading to the last crash, my money is on dumb as rock when it comes to anything that their precious stupid formulas cannot explain.

In general you will find the cheapest properties in countries where banks do not lend money.

Muslims are not allowed to charge interest on loans and hence one finds that property in Islamic areas are generally cheaper.

Property used to be reasonably cheap in Switzerland, compared to wages because you needed a 40% deposit of the value.

Property shot up in the UK in the early 2000’s in the UK because a few banks were offering 120% mortgages.

A 40% deposit is still pretty much the norm here in Switzerland (although some lenders may allow 30% as long as the property is to be your main residence), but unfortunately property is no longer reasonably cheap, and is now more along the lines of horribly expensive…

Yeah that vaccine success news last spring really juiced the markets.

There’s no way he believes that. Is he lying because he knows he’s doing harm to non-homeowners? Can Powell be impeached?

He’s doing harm to homeowners as well.When the public unions with their depleted pension funds sees home prices rising they will send out the local assessor to revalue your house.

Plenty of harm for all

You probably meant fell to $2.07 Trillion. Right?

No, I meant what I said. MBS is rising on the balance sheet. Look at the trend, not the weekly squiggles.

Bobber

MCH was referring to Wolf’s $2.07 “billion” Typo in the article.

Yes, thanks.

An entirely new category:

Pandemic Crybabies

Wolf – Thanks very much for doing all of this. I really only understand about 20% of it but it is good and valuable education.

Completely agree with your post. Many of us beginner investors are gratefull for a lots of knowledge.

But we would appreciate if you summarize your article in few simple sentences together with expected impact it is likely, possible to have on the market.

Wolf,thanks for great job.

Greatings for all of you from investor from Croatia. :-)

zj:

It IS summarized succinctly and directly relevant in every article Wolf puts up or authorizes on WolfStreet IMO.

Otherwise, each and every article would be at least ten times longer, and, as such when the average attention span is very much shorter, would mostly be even more ignored by the very folks who least would be better of not to ignore the wit and wisdom hereon.

As opposed to some on here who say they have been, ”IN the mkt, meaning SM, since 19xx, or whatever, I have been OUT of the SM since the mid 1980 era when what my SM mentor who had taught me so much started to get out of his many many long positions; to me then and still, when a really experienced and successful person did something like that, I did my best, and still do, to pay close attention.

” De gustibus non est disputandum ” continues to be the best advice from the non ”holier than thou” crowd, no matter the possible conundrums suggested by it and any such old saying.

I have been in total awe of the stock markets since around 1998. But not in them much as about that time I realized they were just a sophisticated form of Three-card Monte. Being a mark is for the young.

“few simple sentences together with expected impact it is likely, possible to have on the market.”

Wolf can speak for himself but I would suggest this really isn’t a stock picking/mkt timing kind of site…rather it takes more of a big picture, macroeconomic view of gvt policies and large corporate practices.

Every once in a while, an individual company might get called out for really egregious (although obscured) practices, but Wolf isn’t really in the stock picking business.

That said, my guess is that Wolf could probably whip up a quick summary post of a smallish handful of general investment principles that almost always apply (diversification, ratio analysis, cost minimization, etc.) and why they usually work.

SUMMARY: Buy at a low price, then sell at a higher price. ;-)

And maybe someone could come up with a glossary including acronyms? That would be very helpful.

Pozdrav u Hrvatsku!

;-)

p.s.

Stay here, read and learn.

It is a treasure trove!

“Many of us beginner investors”

learn from best — like Warren Buffet and learn to read annual reports.

FED have pattern – print make bubble than stop, rinse and repeat –but problem is bubble are getting bigger.

if there is collapse better be on the farm with food and guns.

My mama used to say “It is all fun and games until a hedge fund gets hurt!”…

Everyone has a plan until they get punched in their options.

The Fed owns nothing has ,never created something other than a feudal system of debt leveraged to the future by wealth not yet created. Congress created them to enrich the connected few by feeding off of the people and their labor. Men with guns back them, said the great Nobel economist Paul Krugman. They are in control for now. The debt wheels under their fiat wagon however are wobbly. The electorate is finally waking up. Ol’ Yeller might have to get in the ‘splaining seat on her 800k from the Citadel and the GME saga. What dispensation did the 800k buy would be a start.

Muppets can not be relied upon. There still needs to be an elite to lead them.

George Washington was an elite.

Right on mb, GW was an elite in exactly the same ways that the Adams family that produced a couple presidents and other actual public servants as was good ol GW.

Different folks and greatly different strokes in very different times and places seems to be a greatly and mostly unanswered challenge for lots of different folks these days, and for almost opposite reasons for a good part of each opposing sides regarding the same old heroes of each and every side and kind and time, etc., etc.

This is a far more serious long range challenge for the democracy than it first appears, and must be dealt with with far more patient and persistent contemplation before changes, than, for instance, as has just happened in re SF schools naming.

Without reference to any individual, the lack of patient public contemplation, and especially complete public participation of such changes is and will continue to be a shame on and for all the parties concerned.

Republics decline into democracies and democracies degenerate into despotisms.

MB, you stole that from Alexander Hamilton.

Quick we need another pandemic crisis or financial crisis to slow down the collective consciousness who are becoming too aware that inflation isn’t always good when I can’t afford things, and the wealthy own the assets that I buy to support their oligarchial monopolies. Free money on the mask, tyranny beneath

They’ve got plenty of “mutations” up their sleeves.

haha funny but unfortunately probably true.

Just hope it isn’t munitions.

How many congresspeople are invested in those?

This QE model is pretty much played out. We’ve got homelessness on steroids, bubbles in every single asset class and beyond, and the fissures are showing up everywhere.

I think it 800k for her wit and wisdom. What else could it be.

“great Nobel economist Paul Krugman.”

Walter E. Williamson Paul Krugman: poorly trained, perhaps dishonest, economists

William L. Anderson,:

So, Krugman continues to peddle his snake oil, but today he gets to do it as the Nobel Laureate instead of just another partisan hack. Nonetheless, having a Nobel will enhance his stature as a guy who supposedly knows something. However, just as the peace prize does not make Al Gore a man of peace, neither does the Nobel Prize in Economics make Paul Krugman an economist.

It would be a start in the right direction if the whole economics Noble prize business kicked a well deserved dust, along with Peace and Literature (despite being an avid reader), for a good measure.

But being part of the bread and circuses, there is little hope it will happen.

There is NO Nobel prize for Economics!!!!!!!! (Head bang #n).

Critics, including the Nobel family, usually say, “Nobody should have that kind of power”. Some Bank wormed what we now call the Nobel Economics Prize in somehow, and I forgot the story about how it was done, why, and to who’s benefit at the time.

Go research it.

It’s just another Social Science. Ya want a Nobel Prize in Political Science or Sociology? I think not.

I really don’t care about Lit or Peace as it confers little social power.

I have noticed, however, the ever increased profit driven effect (Med-Pharma $$$$$ complex) effect on Physiology and Medicine. Far too many NIH “basic research” articles end with, “may have therapeutic potential…for…”, etc, etc.

It’s all about who pays the grant money and for what, and what “favors” they may expect from those involved. Then it goes to PR depts and advertising depts, who buy some scientists/docs like lobbyists do politicians.

https://www.nobelprize.org/alfred-nobel/alfred-nobels-will/

Here’s another lengthy but GOOD and very comprehensive article on the Med/Pharma complex. It’s worth your time to read at LEAST some of it, if you care at all about what you swallow.

And yes, it’s from NIH Pub Med, if you want to back out to that, and see it was accepted, and is there for worldwide review.

https://www.ncbi.nlm.nih.gov/pmc/articles/PMC2690298/

And you can also scan the Author’s other NIH publications, and make your own decisions about her possible prejudices, simply by clicking on her name.

You are right, it is a phoney Nobel prize, concocted by the bankers and only introduced in 1968, long after the death of philanthropist Alfred Nobel in Dec 1896.

Critics of the swedish central bank’s version of the nobel prize, Among them is the Swedish human rights lawyer Peter Nobel, a great-grandnephew of Ludvig Nobel, (Alfred Nobel’s older brother.) [32] Nobel accuses the awarding institution of misusing his family’s name, and states that no member of the Nobel family has ever had the intention of establishing a prize in economics.[33] He explained that “Nobel despised people who cared more about profits than society’s well-being”, saying that “There is nothing to indicate that he would have wanted such a prize”, and that the association with the Nobel prizes is “a PR coup by economists to improve their reputation”.[32]

https://en.wikipedia.org/wiki/Nobel_Memorial_Prize_in_Economic_Sciences

It is so far beyond even the teeny tiniest shred of credibility to suggest in anyway that we have no inflation or too low inflation and maybe to even think inflation isn’t approaching double digits, or more.

But the Clowns called Jerome Powell and Janet Yellen and their supporting cast keep telling us that.

Housing

Healthcare

Insurance

Local taxes

cars

They pretend there is not inflation for one reason only: They get to give free money to their rich and and themselves.

And to dupe the ignorant into compromising positions.

Inflation is good for everyone they said so. You need to have your thinking rehabilitated, and if that doesn’t work it’s off to the Mcmurphy Frontal Lobotomy Center (MFLC)

MFLC….I see an investment opportunity there reminiscent of 2008 financial crisis….do you think MFLC can be packaged into hundreds and thousands of units and securitized? All triple A rated of course.

As long as you can say that you can power soil solar panels with the brain waves that let you lobotomize

A better bet on tongue depressors and lithium.

As someone once quipped, I’d rather have a bottle in front of me than a frontal lobotomy

You forgot energy,transportation(tolls,licenseplaye=registration/auto insurance,buses,cabs)and food inflation.You will notice not Only Higher food prices,but shrinkflation as well as lowered quality-fattier/tougher meat,more salt and sugar in prepared items while reducing protein or fruit/veg. Ingredients and vitamins.

The median house price is more than $500k around here. Average new car prices are north of $35k. Health insurance is utterly unaffordable. And you’re expected to pay for it all with a $15 per hour job.

If you think that’s not affordable for a $15/hr worker, what are they going to do when they reach retirement age?

FWI don’t be so greedy that $15 don’t kick in till 2025 I think you can’t have everything.

So the Fed still has 140billion of SPV assets on its balance sheet. I guess there is no market for these?

Sure there is – Gamestop. The Fed should buy stock in Gamestop. Because the Fed says there are no asset bubbles.

And the FED also said “we don’t really understand inflation.”

WOLF

What do you mean when you say:

“….the Fed has monetized 54% or $2.3 trillion of it…”

Do you mean they are making interest from the US Treasury because they are holding the treasuries? If so, what does that number look like (annually) ??

What I mean is the Fed bought 54% of the amount of the debt that the government issued since March, meaning that the Fed essentially and indirectly financed over half of the government’s spending with printed money.

The Fed does earn the coupon interest from the securities and it remits a big part of that income every year back to the Treasury. For 2020, it remitted $88.5 billion to the U.S. Treasury:

Do you see any reason why the Fed would stop or slow down the US Treasury purchases? Without being snarky I mean why wouldn’t they just continue on this path now that they have committed to it. Who is to stop them from seriously just making this the status quo?

Nathan Dumbrowski,

Look at the long-term chart. They did reduce the balance sheet in 2018 and 2019. In addition, inflation and economic growth will make their balance sheet smaller over the years relative to the economy, even if they keep the nominal asset level flat, which is what they did between 2014 and 2018. Powell was part of both programs and said “we know how to do that when the time comes.”

During the balance sheet unwind, the stock market had a nasty sell-off in 2018 and the repo market blew up in 2019. The repo blowup caused the Fed restart QE. So….

Best reason to slow or end purchases: Treasury finds buyers for their bonds, by allowing the market to set rates. That’s not as far fetched as it seems. Should USG offer a better yield, higher demand would provide a counter dampening effect. The potential for damage to bond holders in the secondary market is the dollar. Should the Treasury defend the dollar, and not just jawbone against weak dollar policy, the damage would be limited. Rise in yields would accompany inflation as well. There are certain markets that can make that turn pretty smoothly, like housing?The real question: rising rates imply tight credit, can the economy tolerate a reduction? The Fed has tools to provide liquidity in that case. The Corporate Bond market is more flexible, they have earnings. You hear some crying about the rollback in corporate tax cuts. If earnings double by 21, Wall st cries all the way to the bank. HY remains viable, if anything the rise in rates imples a higher bond rating. US debt rating should do well enough if the publicans can raise revenue.

Wolf

‘inflation and economic growth will make their balance sheet smaller over the years relative to the economy’

Is this a wishful thinking? Fed has tried to increase inflation since ’09 if not earlier. Japan tried for over 2 decades!

As the M2 increses (money printing) increases to finance the growing deficit/DEBT, growth suffers along with decrased velocity of money. The has happened since 2000!

Curing the ills of debt with more debt, but how long?

h/t ria

sunny129,

Below is Fed’s assets-to-GDP ratio from the Fed’s own report. I drew the blue line across. Note the decline in 2016 and 2017, when assets remained flat but the economy grew. And then in 2018 and the first half of 2019 the decline steepened as the Fed as allowed some of its assets to unwind (QE unwind) and the economy continued to grow.

Assets declined from 24% of GDP in Jan 2016 to 17% at the low point in Jun 2019. Neither assets nor GDP (nominal GDP) are adjusted for inflation. The QE unwind started in late 2017 but initially was too small to be even noticed. It picked up speed in 2018 and 2019 through the first quarter. It was shut down in Q2 and Q3, and the repo bailout started in Q3. So yes, that decline of the assets-to-GDP ratio did happen even before the Fed started its QE unwind:

Wolf

‘.. as the Fed as allowed some of its assets to unwind (QE unwind) and the economy continued to grow’

Exactly!

That’s the gist of my above comment. DEBT accumulation via QEs (growing balance sheet) hurts economic growth, along with decrease in the velocity of money.

The problem is the feds will have to create more money from nothing just pay that inerest by pass through payments via the banks QE. QE to infinity and beyond “Good and Evil” Nietzche.

Interest on trillions of dollars becomes billions and billions. They have no choice but to keep interest rates low and continue the Ponzi scheme

Please don’t use one of my favorite thinkers name in totally stupid sentences.

It’s a sacrilege, as it were, like it is.

If you are drunk or high, just say, “Fed bad”, and let it go at that.

Nietzsche had his own problems, just like many of his true believers.

Nietzsche had his own problems, just like many of his true believers who think hey are more intellectually elite than other.wise men. I suspect he couldn’t take a joke. Fake elite thinking. We all have our problems

I think the coming years are going to play out very different from what we have seen in the past twelve years.

“Stimulus” has gone completely ape-shit and everybody now expects stimulus checks and other massive deficit spending. This is not going to stop any time soon, because people now think this can be done without any consequences! So it will go on until something breaks.

Many businesses closed and will close in the future, reducing competition for the survivors. But these survivors come out of this with much more debt, so they will have to increase prices to deal with that debt load.

With minimum wages set to rise, this will also trigger demands for higher wages further up in the chain. And there will be a lot of political pressure to support this because of the obscene enrichment of the 1% in the past years.

All this means more money in the hands of people who’s expenses actually increase the CPI. Of course the Fed will be behind the curve, and investors understand that and this raises inflation expectations even more.

Therefore, I see a substantial tail risk for much higher yield increases than most people are now anticipating. The Fed will then be in a very difficult position, but they will be forced to fight the inflation, otherwise the debt becomes unsustainable: Higher inflation still takes ages to make a dent in the debt, but the (re-)financing costs of the debt will immediately jump up, causing even bigger deficits, cause even bigger yield rises (because that is the dynamic once inflation takes hold).

So, you would get a situation that is the opposite from the past decade: higher CPI inflation, rising rates and deflation in asset prices.

A jump in inflation is almost certain, if only from base effects. But because it will be so obvious to everybody, it can easily trigger a spiral that then starts feeding on itself.

Not a certainty but a significant tail risk. It’s going to be really interesting to see how the central banks are going to navigate this.

Tail risks are black swans, not much greater than 10% chance of the FED not being able to control the interest rates. Don’t get me wrong it could happen and I hope it does just stop the scam

The problem is, every new spending binge makes it that much harder to control rates. And the rates looking “under control” creates a desire for more spending. It’s a positive feedback loop.

True I don’t know how far I can go

Mmmm,the old standby of a lengthy,asset-using war,perhaps?Things heating up in s.china sea as well as with the Iran-China-U.S. Dynamic.India and China have also been getting into more confrontations this last week or so.Why are American warships in the Baltic this week and why are Russian fighterjets buzzing Alaska fairly frequently?????!

your comment is very good ys, as usual; however, you forget one basic rule of the guv mint of USA and likely others for the last couple or few decades:

when ”things” don’t go the way you, the non elected guv mint employee that has a iron clad pension, etc., etc., will just change the rules and regulations that the ”laws” have empowered you to manipulate because the actually elected folks are either too focused on their insider trading deals, or are otherwise just too incompetent to understand the laws they vote to approve.

IIRC, a house speaker said almost exactly that, ”we will have to pass the law and then read it to understand what it says.” or something like that, with a thousand pages or so that NOBODY HAD READ before voting on it.

Clean House, Senate Too,,, until we have folks in there to represent all of WE the PEEDONS instead of the oligarchy.

“until we have folks in there to represent ..

That will Only happen AFTER the whole damn Republic collaspses from all the grift and fraud weighing it down.

The current bunch of blu ishmonkeys/redrHinos hold the broom ..worn, and bare of any cleansing bristles .. like any good coven!

Cleanout the staff along with pols.

Well said, YuShan. I think you are spot on. Note today how Treasury yields went up and not down with a cratering Stock Market. So where was the flight to safety? No safety in U.S. Treasuries anymore, unless you are a half-blind Federal Reserve buyer that worships blindly at the alter of MMT. Money did not flee into shaky bonds today that are destined to cough up giant hairballs in the foreseeable future (like tomorrow!). I think investors have discovered the abandoned ingredient to bond pricing: CREDIT RISK.

Smart money is going into cash for now, but will eventually be going into Gold and Silver in an exponential manner. Dollar in dead cat bounce last 2 weeks, but still a dead cat. Will take much higher yields to provide any support for a currency backed by an insolvent U.S. of A.

Also note how the bullion rally today got trampled on by Goldman and Morgan with another volley of paper shorts, probably financed with free money from the New York Fed. But the dye is now cast. Stocks and bonds need nary an excuse to find price levels much, much lower. Your comments were insightful.

I’m normally an optimist but I can’t see any painless way out of this financial mess for anyone.

I suspect we can’t kick the can any further down the road

7 trillion. Big number. 1/3 of GDP. It’s probably just accounting. Something akin to money supply? They should triple it. See what happens.

Destroying a currency and a country is not cool at all. The pain would be unimaginable for most.

The Fed prints up more dollars per year than there are stars in the galaxy.

Whatever crying seems to be filling the nursery now, it’s worth noting that the 2-yr Treasury is at 0.11% today, lower than its ever been. For all the apparent recovery during phase one of the pandemic and GFC, this is not good. Seems like this transcends GDP, bubbles and crybabies.

But the ten year is up, quite substantially.

If the Fed wants to can’t they manipulate the 10 and 30 lower?

Up substantially? That’s very subjective and not sure why it might go much higher. Compared to the 10 yr index yield, things going forward are headed down.

Nonetheless, this is all subjective looking at spreads or whatever, thus, if the 10 yr selectively keeps going up, disconnected from the 2-yr, that’ll be an entirely new dynamic.

All I mean to imply is that in a semi-panic time like now, people generally want short term securities and fast liquidity, thus it doesn’t make a lot of sense for there to be a flood of panic buyers scooping up 10 yr instruments that have less future value.

If anything, the 10 yr may be like a Gamestop security that some people may want in a portfolio for trading games — who can say, only the gods know — but as usual, I defer to the Yardeni thesis that the 2 yr treasury is a proxy for where the 10 yr will be a year from now

Martha, not with a steepening of the Yield Curve due to a surge in Inflation Expectations ignited by a Fed & Government running wild with money creation and Currency Devaluation.

@Martha,

If I was invested in long duration like the 10yr or 30yr and see inflation increasing in the future, I would sell those and move to shorter maturities or cash, i.e. the yieldcurve steepens. Also, nobody expects the Fed to raise rates in the near future, so this pins short term rates to the ground. However, this will increase inflation expectations and drive long rates up.

When inflation expectations increase and hence yields for longer maturities rise, the way the central bank drives yields for these long maturities down is by raising interest rates. That will eventually bring inflation (expectations) down and therefore the yields.

What many people don’t get (and why they are likely to be unpleasantly surprised at some point in the future) is that you have a very different dynamics in an inflationary environment compared to a disinflationary environment.

In the past decade, inflation expectations were low. So the Fed could expand its balance sheet whatever it liked. Liquidity simply added to excess reserves. This has created the myth of a central bank that can buy unlimited amounts of Treasuries and other stuff. It’s pushing on a string, it won’t create much CPI inflation.

However, once inflation pressures build, the Fed has no such power anymore. Buying more Treasuries (i.e. printing more money) just fuels inflation even more. The only route they then have left is raising interest rates and draining liquidity from the system.

In addition to this, investors should be thinking about credit risk again. In the current situation, the idea that debt can be held sustainable by negative real rates alone is a total fantasy. Just look at the CBO projections and do the maths.

YuShan,

I don’t totally understand. Yields are essentially effective interest rates. What would be the point of raising rates if inflation expectations go up? All that would do is bring yields more in line with the face value, no?

@RightNYer,

The way to get inflation under control is to drain liquidity from the system. By increasing interest rates, you immobilise parts of the liquidity because you can then make nice returns by placing money on a deposit. This lowers inflation expectations, which in turn pushes the yield on the long end of the curve lower, provided that it has first risen because of said inflation expectations. This is why you often get an inverted yieldcurve at the end of the business cycle.

If course, causing inflation is what the Fed wants, so for now they will keep rates low. If the long end of the yield curve rises too much, they will first try yieldcurve control to push it lower, but that will only work as long as inflation doesn’t really take off.

In a dis-inflationary environment the central ban can do what they want. But in an inflationary environment the bond market is in the driver seat and forces the hand of the central bank. But we haven’t seen that for a while now so for many people this will come as a complete surprise when it happens.

YuShan, thanks, I think I got it now. Basically, a rising yield in long term bonds is an expectation that rates SHOULD rise to keep pup with inflation, so bondholders make it happen through the market price. If the Fed raises rates, it’s no longer necessary for the yield to be different from the face value, so it falls into equilibrium.

Thanks.

Just had my 1 year CD at my credit union renewed for another year at the fantastic rate of 37 basis points.

C’mon man, ZIRP has only been employed as a desperate measure for 20 yrs.

And it is a sign of “health” (at 100%+ DC Debt to GDP), a “savings glut”.

You can make 37 basis points in a matter of minutes if you just put that cash into the stock market on a good day. Then just put it back in the regular share account at the credit union for the rest of the year.

I save more money by going to the Supermarket when they reduce the food because of getting close to the “sell date” than the return I would get on a $500,000 bond paying 0.1% interest with no risk to the capital.

Gone are the days when Argentina paid 7% for a 100-years. We can only hope that Argentina has another trick up her sleeve. /s

Because SKT got caught up in the short squeeze drama I was able to sell for a modest 14 month profit 75% of my shares. I knew that was possible as short interest was around 50% the whole time. Anyway I am back to 90% or so money market and short term us treasury fund slowly trying to get a little gold and silver exposure in case the Fed does whatever it takes and if you are doing the wrong thing it’s never enough.

It seems like “crybabies on wall street”, is the meme of the day. “ Boo hoo, Jerome took away our punch bowl.” Or, “Boo Hoo the robinhooders tricked us with their Reddit driven short squeeze.”

So if we do suggested minimum wage $15 by 2025, that means a big decline in real terms because inflations than current minimum wage, correct?

Mama Yellen will deliver. No worries.

Lifted from Twitter:

Janet Yellen accepted $810,000 in speaking fees from Citadel, owner of Robinhood.

Reporter: Are there any plans to recuse herself from advising the President on GameStop and Robinhood situation?

Psaki: ‘No and she’s an expert and deserves that money.’

Case closed.

Maybe AOC will team up with Cruz to make Powell/Yellen to start an SPV specifically to buy and support GameStop.

That would be cool.

If shorters of overvalued companies are Domestic Terrorists (TM) (ntl threat to economic recovery) can the Dept of Defense spend part of its budget propping up/”defending” Gamestop?

Apparently AOC is suddenly excited by the news buzz and wants to come riding to the rescue of the little guys who have been victimized by the big evil nasty hedgehogs (TM). She seems not to understand that the news buzz is about the reverse. The little guys busted one hedge fund to the tune of 2.5 billion, requiring a bailout from the fund’s biggest investor.

Well to be fair, the little guys can’t continue busting the big guys if they are only allowed to buy 2 GME shares per person. Also yesterday people were only allowed to SELL.

The whole system is corrupt beyond believe. It always surprises me that in the USA it happens all in the open and nobody seems to care! It’s all legalised pay and play. In the UK and Europe the elites at least try to hide their corruption because it causes bad press.

Which is hard to understand because watching DW and BBC it appears they are now just as “owned” as the American media. They changed in only the past few years.

The SNB owns $118 billion of US-denominated stocks.

If they SNB needs USD, why aren’t they forced to sell some of the stock holdings for USD, or why don’t they print a few billion more Swissies and then sell them for USD?

Why is the the Fed lending USD to an entity that could easily liquidate a few billion of their USD-denominated assets for USD?

https://wolfstreet.com/2020/08/05/top-40-us-stocks-at-the-swiss-national-bank-gains-bought-sold-and-how-the-snb-can-keep-that-racket-going/

I keep reading that the US Dollar is going to crash, be worthless etc. and on that basis looked at an alternative currency to keep my cash in.

GB pound could have been risky due to Brexit

The Euro looks doomed with the ECB printing and buying any bond it can get hold of.

You would think that the Swiss Franc would be falling against the US Dollar but that is not the case.

Then one thinks, the SNB just cannot go wrong. It prints Swiss Francs, changes them for US Dollars and buys American Tech shares that pay dividends and shoot up exponentially. The other Central Banks seem to find this just fine.

So I hold all my cash in a Swiss Franc account in the Bangkok Bank in Thailand at zero interest rate which at least isn’t a negative interest rate and subject to withholding tax as it would be in Switzerland where the bank would keep asking me if I am an American citizen.

“Hard choices, easy life. Easy choices, hard life.”

Attributed to Jerzy Gregorek.

Wolf,

What about GameStop?

These days you must pouch quickly on subjects that really matter….

Get to it MAN or suffer the fate of OLD MAN THINKING

KaputShortsYahVol,

Just because you didn’t read it, dude, doesn’t mean I didn’t write it… days ago…

https://wolfstreet.com/2021/01/27/as-dow-sp-500-sink-into-red-ytd-gamestop-amc-4-other-most-shorted-stocks-jump-135-to-538-utter-mania-but-bloodletting-in-late-trading/

https://wolfstreet.com/2021/01/25/after-skyrocketing-in-majestic-short-squeeze-gamestop-shares-collapse-54-in-hours-the-zoo-has-gone-nuts/

More cowbell, Jerry!

\\\

Harvard School of Economics, Basics

Step1. Design and implement laws to fit your business goals.

Step2. Establish oligopoly or preferably monopoly.

Step3. Make a lot of money.

\\\

Harvard School of Economics, Advanced

Step1. Make bonds appear fron thin air.

Step2. Make $$$ appear fron thin air.

Step3. Swap bonds for $$$.

Step4. Make a lot of money.

\\\

Harvard School of Economics, Super advanced

Step1. Make casino, without calling it casino.

Step2. Rig all bets in your favor.

Step3. Place bets.

Step4. Make a lot of money.

\\\

Harvard Scool of Economics, Best Practices

BP1. Profit above all.

BP2. If unclear always look to BP1.

\\\

Blame it all on foreign “enemies”. You forgot that part.

The housing crisis was 13 years ago. Houses are now so expensive the middle class can’t even afford to own a roof over their heads.

So why in the hell is the FED still printing money to buy mortgages?

With the ultra low low interest rates the middle class can buy a minimum home that needs some work and fix it up over time. I had to pay 10% mortgage rate on my 1st home which was 800 square feet of living space. Fixed it up over time, doing a lot of the work myself.

The millenials need stop wining and get off their sorry a$ses and stop blaming everyone else for their predicament.

Try doing DIY work on your house while holding a smart phone in your left hand and having to give some likes on your FaceBook account all day.

Because they couldn’t care less about the middle class. The Fed is owned by its private member banks and it exists to serve elites.

The dirty secret is old farts on average sell off 4% of their assets to live on each year. If the Fed through it’s policy triples asset prices it’s bringing the income forward as the asset over the long term can’t pay you twice. Problem is the wealth affect becomes the poverty affect when asset prices implode. Fed can know the system has to reset over a certain weekend, but they can never tell you system is going to implode or its self fulfilling.

A 4%/yr spend-down used to work when yields were 3.5-4.5%. The current 0.1% yield would indicate a 0.1% draw down, which, with 3-5% inflation, doesn’t work out well for old farts.

If the Fed let prices drop (they were starting to in the spring) people would be upside down on their mortgage.

Who wants to continue paying on a $mil mortgage now worth half that?

Jingle mail starts again & the system collapses. Rich people might lose money. Fed knows this, won’t let happen. Rates will stay low as possible as long as possible. Hide/deny inflation at all costs.

Plus, It’s a hell of a lot easier to print money than it is to raise taxes.

Analyst on NPR just explained in response to questions if ZIRP was inflating housing prices on the peasantry, that Fed’s stratergy is to make the prices go up because the will make more want to sell which makes the price go down.

Flawless.

Has it occurred to Powell, Yellen, and Co that AI bots could replace them at Fed policy and no one would notice?

Is that some sort of joke or did somebody actually say that?

AI bots could also replace NPR commentators with minimal loss of wisdom.

This already happens! Many market commentaries are written by AI bots. Like ” fell x% after their earnings disappointed. Bla bla bla…” etc. It’s not very hard.

Wolf,

Any Corporate or Muni Bonds on the Fed’s balance sheet? Or is it so small that it wouldn’t show up on the chart.

Small amounts. The muni market has been on fire with super low yields. There is no reason for the Fed to get into it. The whole credit market is on fire. That’s why the Fed never really actually bought a lot of corporate bonds. Its just jawboning did the trick.

Perhaps it will be the Swiss central bank that first takes a big dive into Bitcoin. The momentum keeps heading that way and maybe some governments are looking for any advantage.

Looks like there may also be a coming pump-up on silver.

If there were some dealers in the area where you could buy silver coins over the counter, I would do so immediately. I don’t like sending any money in the mail and taking delivery in the mail. The Postal service here is so screwed up that I’m losing 10 – 15%% of the incoming and outgoing mail. Home Depot customer service said this was a national problem. A Post Office mail truck was discovered parked in Baltimore for over a month with 30,000 pieces of mail inside.

I’ve got a few great coin dealers to go to. My problem is I am leery of buying any more. If the FED signals they are tightening, I could see a PM crash.

This is my fear too. I have a small percentage of my savings in physical gold as a tail hedge for when the entire house of cards comes down, but if central banks were to do the right thing this could easily crash PMs. Therefore I’m reluctant to get more exposure to them.

There’s a lot of jawboning from the FED, but in reality I have a hard time imagining them refusing to raise rates when absolutely necessary. If they destroyed the currency and the economy, they’d be out of power.

@Depth Charge,

Yes I totally agree. Out of control inflation would crush the economy and hence the tax base. The Fed would lose all control. And the outcome would still be defaults everywhere you look and possibly a revolution that involves guillotines.

Believe it or not when I pulled out of my rural drive I saw two larger mailer envelope 50 ft apart on the shoulder. I guess they fell out of the delivery van. Luckily I could find the address which was a half mile away on a side road and delivered them.

One thing never talked about is the fact that a lot of jobs are under wage controls, or fee controls. People who are under these constraints are not going to look kindly on some hamburger flipper making $15/hour while they have put 30 years into their careers and have graduate school level education are busting their butts working 18 hours/day making the same amount. You are going to see some push-back big time. Most likely this will take the form of a shortage of critical service jobs and work stopages which will affect everyone.

Just look at NYC in the mid 70s when every critical employment category was on strike, Teachers, Bus drivers, I was there and so it first hand.

Exactly! Minimum wage rise will ripple up through the entire chain. I really believe we are about to enter a new era with very different market (and political) dynamics. Stagflation ahead. Rising CPI inflation, rising yields, credit risk fears and falling asset prices in the coming years.

If AI continues to come on board big time, jobs that are paid more than hamburger flippers could be phased out. So yeah, lots of cross-envy among the peasants.

And then again, where are those robots that can flip burger? They keep threatening to install them, but they never appear. I saw a video of a robot recently that can dance, so why not flip burgers?

Lower than $15/hr wages is a primary reason robot burger-filppers have not become more widespread.

If you are working 18 hour days at $15 an hour you need a resume check. Let’s say you have your own restaurant, why not go to work for Taco Bell, where they pay managers 100K a year? The 70s job market wasn’t nearly as efficacious as this one, and that one much more so than the 30’s. Greenspan often extoled mobility as the American economic miracle, and when Covid hit, WFH allowed people to migrate to lower cost housing. Having a newer streamlined national RE market helped as well. Sometimes instead of saying wheres the product and the revenue, we should say, what’s the benefit?

Ah yes, the benefit is for the small percentage which holds the bulk of the wealth. It’s worked well for them, so far. Also, when you get a salary check from Taco Bell your before-taxes consumption is much more limited.

We have minimum wage in the UK that is currently £8.72 (US$11.78).

Most new jobs are on minimum wage or a dollar above.

Companies have no need to pay more because of supply and demand and the employees accept it knowing that their wages will be made up with “universal tax credits”; free money for housing and living on.

Most companies only want to employ you for 30 hours per week because of avoiding “employers NI” (tax the employer pays on the gross over a certain gross wage) that gives the employees more time to spend with their family and plenty of time to go to the food bank.

There will be vaccine success – or at least the sudden realisation that Covid is not the threat they all said it was will be put down as a vaccine threat.

At which point QE stops completely, Budgets retrench, and the markets absolutely tank.

An end to the crisis is what everyone fears.

New crises aren’t that hard to come by.

The real problem the Fed faces is the steady monthly drip of printed money can never ever be reduced, not by even one dollar!

Over time the economy becomes more lethargic and the monthly drip of printed money has to be increased just to keep the economy where it is already.

As time goes on, more and more printed money is required, each month, just to stand still.

This is what a zombie economy looks like.

Weimer Germany

When prices go up and debt goes up, you get deflation. All asset prices that are pumped up will deflate. Debt that cannot be paid off, will not be paid off. If most folks don’t have the money to buy inflated whatevers, the price has to decline for lack of demand. You can react by cutting costs (pay employees less) and reducing services or products. But do that too much and Bingo competition comes in to finish the business you didn’t manage. The markets will correct. All of them. The the super rich wait to pick up even more assets at reduced (deflated) prices. The government should roll back the Trump tax cuts, and in addition, raise the tax rates on unearned income go. Dirty secret. Taxes are there to reduce liquidity. To create ‘fiscal space’ in the over all economy. And to reduce the massive income gap. Minimum wage should be more than $20 p/hour. Now. Any business that can’t pay that wage deserves to go out of business.

Instead of a minimum wage increase they should legislate a sufficient increase in all consumer prices so that employers can pay employees more. Wouldn’t be very popular with the shmucks and politicians though. Eventually prices will increase to match (most likely more than match) any minimum wage increases. Or they’ll simply put more folks out of work.

Repo activity nil….but what of the Discount Window?

They quietly reworked the “penalties” and the transparency as to who is using the window.

Powell is rooting for more stimulus from Government…will they monetize that too? The balance sheet will be $10 Trillion within a year …..

The Fed has suspended the fundamental of a free market…..supply/demand price discovery in government (and corporate debt). In emergencies, somewhat warranted. In frothy markets, not so much.

Of course they’ll monetize it, because there’s no way Congress can sell $2 trillion worth of new treasury bills to actual investors all at once at rates that they’re willing to pay.

Monetize??? That ain’t gonna work

If you studied geometry in High school you may remember the parabolic curve, which is what is happening to the balance sheet of the Fed and the Federal deficit. Its no longer linear. It gets steeper and steeper until it until it approaches infinity at some point. We’re well on our way towards the same fate as Weimer Germany.

Before that happens there will be massive unrest like what happened last summer. Maybe that will wake someone up.

I don’t disagree, but if the Treasury has to issue $2 trillion in new tbills in a several month period, market rates are going to increase the yield to a hell of a lot higher than they are now. Is the Treasury prepared to pay that, and is the Fed prepared to make it look like they’ve lost control of interest rates?

It is always wise to point out the magnitude of these numbers. I’ll bet Pelosi doesnt know…

A billion seconds is 32 years.

A TRILLION seconds is 320 CENTURIES.

So, Nancy and Joe, understand the 1 Trillion, the 2.2 Trillion, etc…the “small integer game” is a dangerous one.

I became worried when I had to start using a scientific calculator with exponential notation to see the effects of the government’s numbers. Eight digit simple calculators can’t cut it anymore. Most of the population can’t work these numbers.

“Any sufficiently advanced technology is indistinguishable from magic.” ― Arthur C. Clarke

In my opinion, the Fed has set a precedent with the Corporate Credit Facility SPFs: PMCCF and SMCCF. The market now assumes that the Fed will bail them out whenever there is any kind of a crisis, such as the March 2020 liquidity crisis.

Though the SPVs are gone, the Fed can resurrect them in no time, whenever there is a threat of true price-discovery. Without that assumed safety net, I believe corporate bond yields would be much higher today and retirees’ income in much better shape.

I agree. And this expectation by itself already works as a kind of backstop.

However, what could throw a real spanner in the works would be when the Fed needs to tighten because of inflation taking off. Because all backstopping is essentially money printing and fuelling inflation even more.

What the Fed should do imo is set a clear and predictable path towards normal rates, such that corporations get a gentle push to reduce debt. But of course that goes against their philosophy of economic growth driven by binging on credit so it’s not going to happen.

Capitalism without bankruptcy is like religion without hell.

Capitalism without bankruptcy is much like telephone sex.

Sheila Bair (FDIC during GFC) put out a piece “Biden-led regulators need to crack down on nonbank risks — or let them fail,” while the Fed has been proposing expansive policies like opening REPO to hedge funds, and allowing banks to conduct QE, as well as these recent SPVs. The precarious relationship with shadow banks raises the issue, using Fed banks as backstops? I think she is shouting down a well, the challenge for the Fed if they continue to prop up the macro system is to bring marginal entities under regulation. Of course drawing these lines, and then holding to them when SHTF is another story. An ounce of prevention.

Sheila Bair is one of the few sensible voices nowadays.

“Swiss National Bank, which seems to have a need for dollars. The Fed has been adding to its pile of Treasury securities at the rate spelled out in its FOMC statements, thereby monetizing part of the US government debt”

Does one know a reason for the Swiss National Bank needing US Dollars?

Is it for the SNB to buy more Apple shares?

Am I correct in believing that the SNB is printing Swiss Francs and exchanging them for US Dollars?

Why doesn’t this result in the Swiss Franc falling against the US Dollar?

Is the SNB doing this to lower the value of the Swiss Franc so that it can be more competitive for exports of services to the EU Zone?

Cashboy…

The SNB has been very prescient on central bank policy and very clever, remarkably clever in their stock acquisitions. More of a trading house with a pipeline to central bankers…imagine that!

historic, but where is it written that it is a mandate for any central bank to be manipulating financial markets through purchases of $Trillions of equities, the security last in line with no backstops during bankruptcy??? These dudes are out of control, expanding their powers and activities to the extent that THEY ARE PART OF THE PROBLEM AND NOT PART OF THE SOLUTION.

“All power tends to corrupt. Absolute power corrupts absolutely.”

SNB prints money and buys NYSE stocks, Perhaps they are a front for another buyer (Fed?) and the dollars are needed to pay the dividends?

Ambrose Bierce,

Maybe the SNB is a front for the Martians? I think that’s a better theory than your theory.

Wolf, but I think the Swiss National Bank’s demand for Dollars partially, at least, stems from their appetite for U.S. securities, equity and debt. We are the safest market on the planet, in their mindset, but I think that assumption will be proven wrong in the months ahead. Certainly, we are the most liquid, Chairman Powell take a bow. But markets do freeze during panics (and trading platforms become inaccessible even to the Monied Crowd), and many retail (and Central Bank) investors are going to find it hard to catch a bid on the way down.

Plus, just one more morsel for contemplation, I fear our financial system is going to freeze at some point in the near future also. A.K.A., banks.

Wolf – I do not think it to be too far fetched that the world Central Banks have a undisclosed agreement to purchase a certain percentage or amount of each other’s currency, stocks, bonds, etc. The entire global system is a single entity now, and as such they would most likely need to be coordinated on a global scale to keep the system balanced and semi-stable. Unilateral, bilateral, multilateral, who knows…yet I’d take the odds that some of the central banks, if not all, have some sort agreement on multiple financial constructs…even if only on a verbal and not written scale.

Why? Simply because the global financial system is simply to complex to not have some agreements “under the table” to enact a degree of control that would not exist naturally. And thus, such actions create the unnatural balance and stability, which on a universal scale breeds instability…but I degress…

Wolf- with the 52 week bill auction below 0.1% last week, the Fed is in a pickle if they want to avoid crushing the $4 Trillion money markets with negative rates. Some bond guys think they will raise the IOER rate before the March FOMC meeting. Such a move could cement the theory that the Fed will not allow negative interest rates…that is unless they get forced via a future unexpected crisis. There are theories that the world reserve currency can not go negative without crushing the global economy with many unintended negative consequences. Fed seems trapped due to reserve currency status…

In terms of the IOER, that could be.

Negative rates have done nothing good for the overall economy in countries that have them. They have benefited some, and crushed others. And they have created a lot of distortions. The net effect is no good. The Fed has acknowledged that.

Dear Wolf,

I remember that in 2010 Congress took some of the “tools” that the fed etc. used to fight crises and prevent panics, like in 2008. I wonder if the Cares act or the response to covid otherwise restored any of those tools?

The CARES act gave the Fed a mechanism to get around the limits imposed on it by the Dodd–Frank Act, with approval of the Treasury, and that’s how the SPVs came about.