There’s a housing shortage until there’s suddenly a housing glut: see San Francisco et al.

By Wolf Richter for WOLF STREET.

Another batch of crazy housing data yesterday. Crazy in the sense that the housing market, or rather part of it, namely the higher end of it, has gone totally crazy and that by now everyone knows that this isn’t “sustainable,” that “there’s no way it can last forever,” as Redfin CEO Glenn Kelman told CNBC. And he pointed out what everyone has already been pointing out, that “part of what is fueling this boom is that the economy has just split into two, and rich people are able to access capital almost for free, so, of course, they’re going to use that money to buy homes.”

But “there’s just another group of Americans who are still struggling, who can’t access the credit because we’ve raised credit standards, and you have high unemployment. I just think those two trends, at some point, have to collide.”

It’s the now well-established phenomenon of the “K-shaped recovery,” where one part is doing well, and the other part is getting crushed.

Or as WOLF STREET commenter IdahoPotato called it vastly more accurately and unforgettably, the “FU-shaped recovery.” Meaning, people who got bailed out and enriched by the Fed’s $3 trillion that it threw at the markets to inflate the prices of stocks, bonds, housing, etc. are now happy as a lark, and to heck with the rest of the people that are getting crushed.

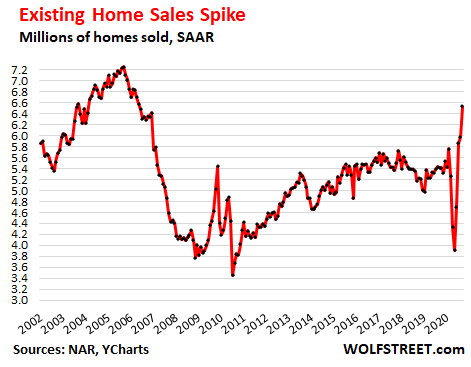

But this craziness in the housing market is not sustainable. The National Association of Realtors reported yesterday that sales of existing homes – single-family houses, condos, and co-ops – surged in September by 9.4% from August and by 20.9% from a year ago to a seasonally-adjusted annual rate of 6.54 million homes, the highest since 2006 (data via YCharts):

Seasonally, home sales normally decline in late summer and fall. But not this year. And the seasonal adjustments of the above numbers are designed for normal seasons. The NAR also releases raw(-er) sales numbers that are neither “seasonally adjusted” nor “annualized.”

On a not-seasonally adjusted basis and not annualized, 500,000 homes were sold in September, up 24.7% from September last year, the highest year-over-year increase in the data except for two months during the depth of the Housing Bust – April 2010 and November 2009 – when sales were compared to a year earlier when sales had collapsed. Sales went through some wild gyrations from 2009 through 2011.

And on this basis (not seasonally adjusted, not annualized), and compared to September 2018, homes sales were up by 34%.

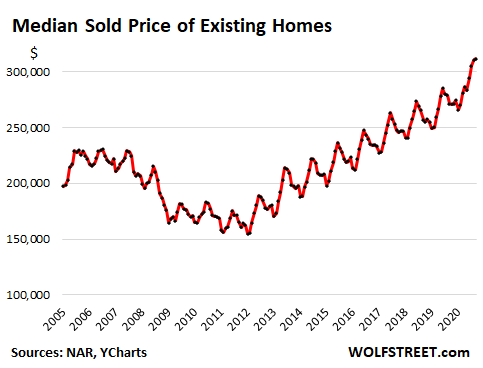

The median price of existing homes in September jumped 14.8% year-over-year to $311,800. The median price is skewed by a shift in the mix, and the price increase could also partially a result of red-hot demand for higher-priced homes (data via YCharts):

“The uncertainty about when the pandemic will end coupled with the ability to work from home appears to have boosted sales in summer resort regions, including Lake Tahoe, mid-Atlantic beaches (Rehoboth Beach, Myrtle Beach), and the Jersey shore areas,” the report said.

I have heard similar stories from real-estate brokers, such as red-hot demand in very pricy Carmel-by-the Sea, in California, about 76 miles south from San Jose and 116 miles south from San Francisco. The demand is said to be particularly hot for homes in the $2-million-plus range.

But here is what I also heard: People bought their new home without first selling their old home. They still have their place in San Francisco, or wherever, and will eventually put it on the market, but meanwhile they plowed a few million bucks into a house in Carmel and moved. These stories are everywhere.

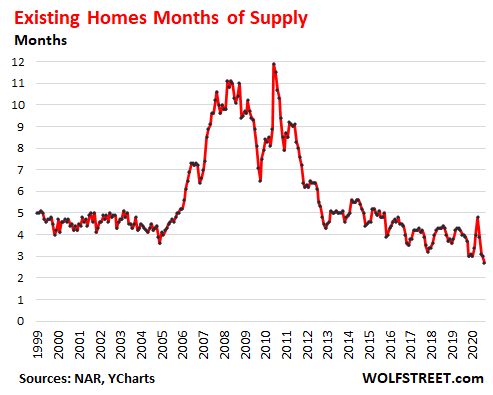

Total housing inventory of homes for sale at the end of September fell 1.9% from August and 19.2% from September, to 1.47 million homes, according to the NAR. Given the sales rate in September, this represented 2.7 months of supply, the lowest ratio in the data going back to 1999. Granted, with today’s technologies of advertising, selling, financing, and closing the sale of a home, sales take a lot less time than the did in 1999, but still (data via YCharts):

There is a shortage until suddenly there is a glut. This always surprises people.

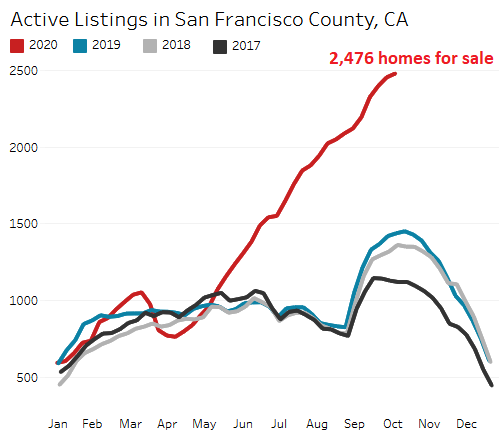

This is happening in San Francisco — and something similar is happening in Manhattan and some other cities. The City was long described by its “housing shortage” that drove up prices and rents though there has been plenty of housing, but all high-priced, and people couldn’t afford it. And suddenly that “housing shortage” has turned into a glut. The city is flooded with a historic amount of inventory, including a record-breaking number of condos for sale, and there is a large offering of vacant apartments, and rents have plunged, with one-bedroom rents down 19% in five months.

The inventory of homes for sale spiked from “shortage” to “glut” in a matter of months. As of the week ended October 11, there were a record 2,476 homes listed for sale, up by 72% from the same week last year, with condos accounting for the lion’s share. Note how the glut has blown all seasonality out of the water (chart via Redfin):

These gyrations in the housing market are occurring as, at the lower end, homeowners are steeped in turmoil, with nearly 7% of all mortgages in forbearance, according to the Mortgage Bankers Association, and with delinquency rates of FHA-insured mortgages, which cater to the lower end of the market, skyrocketing to a record 17.4% in August, and with 23 million people still claiming state or federal unemployment insurance. That’s the other part of the “K-shaped” recovery.

Surging home prices like these are a terrible toll to pay for buyers, except for those where wealth is such that it doesn’t make any difference. As these home prices surge, the market will inevitably run out of buyers willing and able to buy, even at record low interest rates, especially in an economy like this.

In addition, there is lots of supply waiting in the wings, including: A portion of the homes whose mortgages are in forbearance and delinquent will have to be sold to cure the delinquent mortgage; homes whose owners moved into their recently-bought new home will end up on the market; and homes owned by investors for vacation rentals will end up on the market if vacation rentals continue to be a drag in those cities. This surge in supply can happen suddenly, as it has happened in San Francisco.

And then there are interest rates. Oh no… Not again. They’re going to be negative, right? Um, the Bank of Canada announced it will cease buying mortgage-backed securities after October 26, having realized that it has gone overboard, seeing the same kind of insane surge in the Canadian housing market that is taking place in the US.

Which makes me wonder: Will the Fed, after the election (it never changes policy shortly before an election), start muttering musings in the same direction concerning its MBS purchases? It too is seeing this housing insanity, and after having already quietly mothballed its corporate bond-buying program, its repos, and its dollar liquidity swaps, it would be an unsurprising next step.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

What’s the old real estate joke? It’s easy to buy, but it’s harder to sell?

I think a lot of people will discover that it will be hard to sell at the prices they expect.

Especially if they bought a new house before they even sold their old one. (Hopefully they purchased conditionally on the sale of the old house)

We may be in the middle of a so called Austrian School type crack up boom. Does not end well as the debt always seems to eventually throw a wet blanket on the “party”.

Moreover, everything eventually seeks to move toward finding an equilibrium. The March/April financial markets downturn followed by reflation shows how artificial things really are. When push comes to shove, the so called Fed put in reality will do nothing as it has only fostered a reckless mindset, which will change. Just a simple reversion to the mean will be extremely painful…if below the mean then holy holy cow!!! This January, the financials markets will resume their downtrend which will last longer and, coupled with all the other poop hitting the proverbial fan, things will finally go down the rabbit hole. More significant middle level job losses are on the way. Many folks who bought into this current feeding frenzy will add fuel to this fire as many of these homes will go back on the market. So Cal jimbo and others will be busy with short sales. This much needed cleansing / reversion to mean equilibrium is long long long overdue. People have been exposing their loins for far to long instead of girding them. This will be so ugly because far too many folks have been “eating with their eyes” and not their stomachs. The severe hangovers and indigestion is on the way.

“Moreover, everything eventually seeks to move toward finding an equilibrium.” – only happens when the system is sufficiently “damped” – a system engineering term implying negative feedback. If the feedback is positive the system begins to oscillate. If the feedback remains positive the oscillations become progressively more extreme until the system blows itself apart. (E.G. equities and home prices.) Basic engineering. When the D in PID control dominates you have problems.

I don’t know much about engineering, so your analogy about “D in PID” doesn’t resonate with me although it could apply, I just don’t know. I am thinking more about a rigged system that has been fooled into going on longer than most ever thought possible. I am thinking more in terms of disasters brought on by prolonged greed and manipulation and the fact that in nature “things” seems to seek to balance out somehow. To me, the root of the problem is the deliberately incorrect pricing of money (interest rates) and the misallocations this has effected.

Trinacria – I sympathize with your view on markets and housing, and I even lost quite a bit of money on puts these last 5 months, barely coming ahead with a long precious metals hedge.

Unfortunately, I’ve come to the conclusion that government policy has a far bigger effect on these markets than I anticipated. Further QE along with serious fiscal stimulus can drive stock markets even higher. Housing can become even more financialized while foreclosures are delayed for years, causing prices to remain elevated.

In my opinion we need a correction bad – either by raising wages relative to prices or by allowing prices to descend back to earth.

I won’t be buying a house any time soon, and I’m more into gold miners than high flying stocks, but my short positions have become the minor hedge instead of the main trade.

Went back and looked and it took about 220 ounces of gold to buy a house in 1890. About the same as now in most of the country.

Lisa_Hooker – Thanks for bringing some science to the so-called “dismal science” that isn’t really a science where central banks centrally plan the world economy using grossly simplistic models of an extremely complex and evolving system with an inadequate number of input signals, many of which, like the CPI, are manipulated for economic and political reasons. Simplistic theory generating simplistic models using inadequate and even manipulated data produces garbage results.

And about the misnamed “Nobel” prize for economic dogma: In his speech at the 1974 Nobel Prize banquet, Friedrich Hayek stated that had he been consulted on the establishment of a Nobel Prize in economics, he would “have decidedly advised against it” primarily because, “The Nobel Prize confers on an individual an authority which in economics no man ought to possess… This does not matter in the natural sciences. Here the influence exercised by an individual is chiefly an influence on his fellow experts; and they will soon cut him down to size if he exceeds his competence. But the influence of the economist that mainly matters is an influence over laymen: politicians, journalists, civil servants and the public generally.”

If you use the most simple analysis of the stock market we are at 3 sigma above regressive trend line. To get back to trend would mean 66% drop. When the stock market goes, everything goes including housing. Timing is nearly impossible, but in general it’s probably a good time to be a seller of assets and wait for better pricing.

Old School: That is where I tend to lean as well. My wife and I sold our home of 20 years in June (we were all set to list in April as all was turnkey) to downscale several years after kids (in quotes) moved out. Sold the same weekend we listed…3 offers – suburb of peoples’ republic of Portland, but thank goodness not in the same county. We got rid of so much stuff and we now rent. Waiting to see what happens and decide what and where. Almost thinking of Vancouver Island, next to Paulo, as I hear he makes good coffee !!! (LOL) Also, have been investing in gold and silver gradually since 2015 and dips along the way through last week… as some kind of protection – we hope.

I cannot believe that we are on a permanently high plateau as then Fed chair Fisher proclaimed in Sept. of 1929!!!! I believe the following from my interpretation of these messy facts and circumstances in no particular order:

1. People give Fed more power than they really have as they are not a substitute for healthy practices, otherwise the entire country would be better off through their slight of hand. Just look and the way these markets are behaving as they scream for a purge.

2. By means of non existent interest rates they have fostered a speculative if not downright reckless mindset…will end in tears or worse.

3. More job losses to middle level folks on the way.

4. Sometime in January, the financial markets will start a serious descent…much like the period of late 1930 – 1932. Could be worse as there was no virus that did damage in those years.

5. The extent of virus/lockdown damage is not yet fully known yet.

6. In 18-20 months, I believe gold will be $3,300 with a Dow of 14,000 for a ratio of approx. 4 to 1. 12 – 15 months later, $5K gold and Dow of 10K for a 2 to 1 ratio.

(Wolf now very wealthy from his short positions !!!)

7. I do have some equity exposure (value cos with strong balance sheets and cash flow), but keep tight sell stops.

8. I am smelling a second round of virus interruptions of some kind. As most markets, including real estate (yes, so cal jimbo even real estate !) are in need of a serious purge/cleansing, maybe this will be the laxative that unblocks things, so to speak. Bon Appetit.

9. Fed and various administrations have long interfered and have not allowed recessions (for some time now a 4 letter word) along the way to clear out system debris; as a consequence, what is coming down the road will be so much worse for the nation and the world economies as all pretty much in same boat.

10. No debt is best, but sort of OK if folks have manageable debt levels.

Remember, the key word here is “I believe”. So please do your own research. Thank you Wolf, for this great sight.

I agree. While the common refrain is that the $3 trillion the Fed printed ended up in the stock market, most of it is just sitting on the large banks’ balance sheets. What they really have done is created a confidence game. Given that the value of markets is purely about investors’ confidence in it, if you create a situation where no one is selling, prices will be high simply through low volume (we’re seeing this in the real estate markets too).

Basically, the Fed put is about people believing in it. If enough people do, they change their actions and this Fed put becomes a self-fulfilling prophecy.

Unfortunately, this means that all it takes is something to shake that confidence, and the markets all plummet, as people start selling far in excess of there being buyers willing to buy anything. What that will be, and when it will be, I have no idea, but I know it’s coming.

@RightNYer

Your right about the low volume, but lots of money sitting on the sidelines plus the real need to be in the equity markets to achieve adequate total return means money comes pouring in anytime there is even a slight dip in equity prices. Wash-rinse-repeat until inflation finally dissolves the value of money and who knows how long that will take.

How does the market fall when there is $4 trillion on the sidelines and eventually there will be another $2+ trillion in stimulus? There is just so much money out there I don’t know how you get deflation.

This market reminds me of ” irrational exuberance” with a giant debt bubble looming. I think it ends in inflation and great wealth inequality. I just hope I’m wrong.

I was down in North Carolina looking at mobile homes. The lead time for a mobile home is now 9 months to a year! My son just bought a house down there and found out there is a shingle shortage to reroof it. I was thinking ” crack up boom” too, but no one is talking about inflation now, although they do talk about prices going up. So far this is all credit driven. Can that be a crack up boom too? I just put my house on the market this weekend and already have offers.

Von Mises crack-up-boom was entirely credit driven. See also, Hyman Minsky for a further explanation.

Unless you are in a really slow market, no one even considers an offer ‘subject to sale’ Even back then, they were only accepted as a way to stimulate a normal offer.

Looked at US data on house prices to med household income and it’s 4.1. Varies from about 2 to 9 depending on city you are in.

All this complexity is entertaining, but historically, the value of housing is 3x the household income of the community where it sits. Any variance from this is bullshit, you can be sure that somebody is going to take a loss somewhere.

I’m sure these historic ratios exist for malls and commercial office space, but if wolf published this and promoted it for a while until his readers “get it,” there wouldn’t be much to write about because reading about cheaters and swindlers finding new idiots gets old pretty fast.

My logical brain tells me things can’t keep happening, but then they keep happening. Later, I see lots of reasons why the illogical was actually the logical. I won’t be surprised if the markets go on a tear and the real estate market continues to fart gold – but it’s not what logic tells me is going to happen.

When is the MARKET, there is NO place for logic. The needed great RESET will have to come outside, beyond the power of Fed to contain that force.

Covid 19 hasn’t gone away, vaccine is still far away. More infections. more hospitalizations and incrementally more deaths. Death rate between 24-44y is slowly increasing also. More post- Covid 19, morbidity and disability increasing! More clear picture will emerge during the 2nd or 3rd qtr of next year.

Until then, don’t try to think rationally.

correction:

When FED is the MARKET, there is NO place for logic

That’s a good comment. Old testament economists preached that price discovery was the holy grail. Price distortion by the Fed at least in the asset market has made price discovery a derivative of Fed policy.

The unintended consequences of their policy is that they are rewarding drunken speculation and punishing the person and company that employees a sound balance sheet able to withstand hard times. The world is sorry place if you don’t have the majority of people being responsible in their financial affairs.

Could we go one better? the FED IS the economy.

About Europe, but equally applicable to the US:

All of surviving big business is aligned with it: those who refused to play the game have disappeared. Senior executives with extensive lobbying budgets are no longer at the beck and call of contentious consumers and have hollowed out their smaller competitors. They have opted for the easier non-contentious life of seeking favours of the looters in Brussels, enjoying the champagne and foie gras, the partying with the movers and shakers, and the protection they bribe for their businesses.

They have their logic, and the means to brand their logic, subsidize large parts of the real economy, using their logic, and basically enforce their logic.

I think that what Wolf is saying here is that the markets have to balance. At the end of WWII people could move from Brooklyn to the potato fields of Long Island in huge numbers because they had been renters. But people can’t continue to move to Carmel, Boise, Vancouver Island, etc. without selling their old house or condo in the Urban area. This going on for very long will dry up down payment liquidity and cause a reverse price imbalance. What is happening now can only be a short term blip.

Folks that can trade paper money for RE can continue the trend, for example, derived from the sale of momentarily or longer term in the money tech stock options. Could also be a rotation out of paper money into hard assets. Paper money is not a requirement to live (or is it?), but shelter is.

Unfortunately, when they flee the urban nests they’ve soiled through their political choices, they soil the nest to which they flee as they have here in Colorado, once a reliably red state.

“Most human beings have an almost infinite capacity for taking things for granted. That men do not learn very much from the lessons of history is the most important of all the lessons of history.” – Aldous Huxley

I think that is one of the big truths in the world that people migrate to opportunity over a long term period. It’s an age thing as well. Where you live during working years may not be the best place for retirement years.

the great RESET will be brought to you by yet another crony financial group, this time the WEF with assistance from the IMF

I like the saying that bubble’s are caused when your neighbor who is obviously not as smart as you is living the dream with the big house, new car and bragging about his investments. Very easy not to get sucked in.

In some ways it’s a risk management problem with leverage. You can use no leverage in life, but you will be left in the dust in the early years. Maxing out leverage is living dangerous with almost certainty to get wiped out in a recession.

As long as the Keynesian fraudsters at the Fed keep swelling their balance sheet, their asset bubbles and Ponzi markets will continue to defy gravity. But when they stop pumping ever-increasing amounts of financial crack cocaine into the system, their house of cards will implode under the weight of its own debt, fraud, and fictitious valuations.

Please go read what Keynes actually read and what Keynesian economics really is. Yes Keynes advocated spending in a depression *on the creation of real things* infrastructure and the like. Then during the good times you put away for the bad. Counter cyclical. Keynes also had more than a few words to say about speculation and grifters.

Another one to look at is John K Galbraith.

John Kay writing in the Financial Times, 22 October 2003 pointed out an interesting condition described by Economist John Kenneth Galbraith. The Bezzle.

“John Kenneth Galbraith’s greatest contribution to economics is the concept of the bezzle, that increment to wealth that occurs during the magic interval when a confidence trickster knows he has the money he has appropriated but the victim does not yet understand that he has lost it. The gross national bezzle has never been larger than in the past decade.”

Gershom, keep in mind that during many serious downturns in markets, Fed was there pumping all they way….

People under stress are doing emotional bets.

Crisis situation allows unusual measures for the States.

The logic is blurred in times of volatility.

Just a few days the SF Chronicle had a front-page headline of “Bay Area home buyers scoop up shrinking inventory at furious pace”. (But they did not put numbers on the inventory.)

This contradicts your graph of active listings.

What do you think explains the difference?

“Bay Area” versus SF?

“home sales” in the article maybe excluding condos?

the journalist and editor taking realtor quote at face value?

MarMar,

I didn’t see the article, but if it’s in SF, it would have said “San Francisco.”

And yes, there is that element, exactly what I mentioned with Carmel, that people move out of SF to live further away but still in the broader Bay Area. This could be in Oakland, Walnut Creek, in the Central Valley, or in the Wine Country. Before the fires, there was huge demand in the Wine Country (and there may still be). Some people define the Bay Area to include Sacramento because you can go by Liberty Ship to Sacramento… so that’s in Central Valley. For others it’s the 9-county area (Napa, Sonoma, Marin, Solano, San Francisco, Contra Costa, Alameda, Santa Clara, San Mateo). Carmel is a little over an hour on a good day from Silicon Valley. So all these areas within an hour or two from Silicon Valley and San Francisco have seen this demand.

Last weekend I bookmarked about 5 houses in the Central Valley (think Visalia area, so not close to bay area). Well, within 2 days I got notices from Zillow that all my houses went pending– likely being sold. I mean for a smallish city like Visalia to have houses being scooped up so fast…honestly all this is just mind-boggling to me. Thank you Wolf for covering housing so diligently with amazing insight. ? I’m still crossing all my fingers, toes, and anything & everything else so that I can be a homeowner this time next year ?

I’ve heard that the auto dealers in Visalia and Selma are doing quite well also. Best months in years.

Wolf, when do you think the flood of FHA REOs will start?

BTW 17% delinquency is even higher than I expected.

At the earliest, next year.

It’s insane near me. Nearby house went to under contract status in 2 days, no way it didn’t get asking price. As I mentioned on other thread, I rent identical unit and my rental price is at least $1500 less. You could get a much larger place not that far away at a similar price point so I don’t understand. Housing supply is short though, lots of people apparently looking.

Where are the foreclosures and evictions? If I bought a place could I get a year off paying mortgage a few months after closing by crying forbearance? If the fine print doesn’t forbade it I would say I needed forbearance, save up all the money for the forbearance period and dump it into the principal payment erasing the time tacked onto the end of the loan and more.

Since we got rid of the mark to market rules, there won’t be any foreclosures or very little.

Why would a bank foreclose on someone and recognize a loss rather than keep the asset at a value of their choosing in their books and access free money from the Fed for the underlaying inflated asset value?

MM,

Good question.

Are mark-to-market rules still castrated? I had kinda assumed they were put back in place somewhere during the past 11 years.

But if the Fed has kept the ZIRP scam going for 18 yrs…

I’m fairly sure the FDIC delinquency rules are still (mostly) on the (relative) up and up…ditto SEC reporting of delinquencies.

So maybe book valuations are terminally gamed, but delinquency stats can be used to infer a lot.

And, if things get bad enough, the banks will have to foreclose, REO, and resell…at some pt in that chain, truer valuations will have to be disclosed.

I hope.

The banks will try to sell them to companys they hold stock in. I believe this happened last time.

Here in LA near the beach we are seeing multiple “FOR LEASE” signs for commercial real estate in every block in the prime locations of Redondo Beach, Hermosa Beach and Torrance. Going down Hawthorne Blvd which has a higher congregation of businesses same thing.

With all these businesses down and people out of work, surprisingly the residential housing market is up here, not a lot of offerings but the asking cost per sqft is actually up. My dad’s friend sold a house he bought in 2016 for $650k for -$30k under his asking price at $950k, 3 bed townhome with not a lot of light, nothing spectacular but about a mile from the beach.

On the rental side, I can now get a 2bed in what used to be called “prime” real estate here in west la for a 15% drop in rent vs 8 months ago, and 2 months of free rent. so basically 20%+ when all its said and done.

I was speculating with a friend that maybe they are loosing lending standards again on top of the drop in interest rates, but i don’t think that’s the case. A good friend of mine was trying to buy a townhome in New York, and Chase rejected his mortgage due to him being a freelancer running his LLC instead of a W2. He was definitely in the 6 figure salary pre Covid and he had the 20% down-payment for the place.

I know the world is not and can never be fair, but at some point the risk takers have to show losses. We’re almost going on 10 years of savers being punished, labor is losing value, savings doesn’t pay any interest and anyone with a heartbeat willing to take a risk gets the rewards when it works, and no pain when they fail.

“Capitalism without bankruptcy is like Christianity without hell.”

Well, we seem to have Devilish Cons applenty, willing to assist in continuing the Rake of the Ages! Marks to Market indeed ..

‘just one more spin at the roulette wheel, please.

love that last quote! so true!

I saw a real world chart that as interest rates go toward zero the amount of stock assets in people’s accounts increases vs cash and bonds. Its a real world example if how Fed Zirp gets people to speculate on riskier assets including housing which can be leveraged at 33:1 or even to infinity with nooney down VA refinance.

Yep;

I have been holding all my assets other than my house and car for the last four years, 20% in gold and 80% in cash on the basis I was being prudent and would be in an opportunity to gain from other people’s losses.

That hasn’t been the case and it would appear my buying power is getting less as assets (property, shares) go up an up.

Now I worry if the cash in the banks is actually safe when I think of the haircut on bank balances in Cyprus in 2013.

But what does one do with this surplus cash?

I think t-bills are next step up in safety above bank deposits and then you have the safest assets in the world in my opinion.

With nominal long term gdp growth growing at 3% and stock market being at all time high valuations, there just can’t be much left in the bubble.

The median home price in Boise, Idaho just hit $400k. The median income in Boise is $50k.

Last week a 1500 SF house in my neighbourhood was listed at $360k and sold at $390k. Just insane. This cannot be sustained.

IP,

I’m in the other (north) end of the state and an article just appeared in yesterday’s paper that there is a shortage of “affordable” housing, anything less than $400k (!). While that might seem like a bargain for someone from Seattle, Portland, LA, etc., here it is indeed a crisis. Where I live $200k is not affordable for most wage earners.

Idaho/Mi-saw the similar happen in the Spokane/Coeur d’Alene area in the ’90’s. At the time, locals were chortling about how they’d skinned the rubes from California and Texas while the California/Texas immigrants marveled at how much they’d acquired for so little as opposed to property back in those states. But, as you note, IP, median incomes did not increase. This led to much grousing about local income levels from the new immigrants, and much grousing from Spokane/Cd’A parents that property values had risen so much that their kids could not afford ‘decent’ housing.

Go figure.

may we all find a better day.

Sounds like Wake County (Raleigh, NC). Been on a long term population growth rate trend. Last I looked it was about 2% annual population growth. It kind of feeds on itself with real estate boom that brings in more people to do the construction of housing an infrastructure.

What was address of that Boise sale at 390K. Have a 3000 sq ft place in Meridian 5bd 3 ba. Off McMillian sure is wild who was your agent if you don’t mind me asking?

I just moved from Nampa to a rental in Boise. The house im renting sold for $300k in august, but my rent is less than the mortgage with 20% down would be. Makes no sense, something has to give.

SW Montana is under similar pressure. Median price/sq. ft. moved from $250 to $350 over 5 months. I imagine that the data would show a large divergence between urban coastal areas and places like Boise and sw mt which are deemed ‘covid safe and comparatively affordable.’

There’s still not enough supply in my area and seeing the chart outlining national supply at ~ year 2000 levels makes me think these high prices are here to stay simply for the reason that we’ve added 60mil people yet still have the same number of free units.

We haven’t built enough housing for our growing population. Everybody has to live somewhere. I fully expect price:income ratio to continue rising in our areas. Maybe not NYC, San Fran, and Seattle, but definitely out here.

Logical things keep happening in all markets. Just this week SNAP went haywire and is now valued at 65 billion dollars at what is most likely the peak of it’s existence. And it’s still not profitable after five years. Seems logical.

Objectively that inventory chart is screaming for the prices to go higher, much higher.

This frenzy will go on for some time and spring I think is going to be hot hot hot.

Interest rates will remain low and lower and even if the Fed stops buying MBS they will restart the program at the first sign of weakness.

It’s also the only available tangible asset there that can protect average Joe from the massive currency debasement that is going on.

If you have some savings what are you going to do today? Real estate is the only reasonable investment, especially if you plan to live in it .

Memento mori,

Look at the San Francisco inventory chart (active listings). It took only a few months for inventory to go from “shortage” to historic “glut.” This can happen fast. During the last housing bust, this happened also very fast.

“Inventory” just means what people put on the market. It does not mean that these homes don’t exist until someone puts them on the market. They’re there, waiting to be put on the market.

I’m still completely astounded how fast that went in SF.

Sounds maybe like we could get a “trickle down” effect from the insane SF, LA and NY markets to rest of country?

Hi Wolf, I appreciate your insights/thoughts on this topic.

Beyond inventory, FreddieMac makes the case that we’ve had chronic under-building of new housing stock for decades now. They cite a couple factors for this, but do seem to make a strong case that we haven’t been built enough new units over time and that an increasing percent of available stock has been siphoned off into seasonally or annually vacancy.

http://www.freddiemac.com/research/insight/20181205_major_challenge_to_u.s._housing_supply.page

They examine things from the macro national perspective, so things can absolutely diverge from the narrative at the regional/local levels. The rapid inventory change in SF seems to be offset by a rapid shortage in other places.

In our low interest rate world where just about anybody with decent credit can get huge mortgage leverage, I just don’t see how prices will go down in the macro-picture unless we have massive building of new units.

Housing has become a global asset class, with unlimited demand from global investors. Investors buy homes and turned them into assets in their portfolio. If no one lives in those homes, there is no “housing” associated with this asset. No construction can ever be enough, until investors try to sell or rent out those assets as homes, and then suddenly there’s plenty of housing.

And then home prices plunge. It’s at that point that the Fed steps in to “stabilize” the housing market, in other words, it supplies cheap funding for investors to buy back into this asset class. That’s how it happened in the past.

MM,

If things remain the same you are correct. What is unsettling and likely is that something comes on so fast we don’t see it and things head south much more rapidly than we can react to. No longer a question of if but when. People buying now better have a 10+ yr time horizon. AI is set to start taking away mid-level professional jobs and companies will spend faster on automation. 5G ain’t about faster video on an iPhone but a blistering improvement in business process and driving costs down even further. Expect to see starting Feb or Mar large corporate M&A.

Bart-human technology, eventually and always, generates a ‘Tower of Babel’ moment?

may we all find a better day.

Nothing makes sense anymore.

Yup. Something shouldn’t happen then it does and then vv. before or after. Yeah the sentence doesn’t make sense but neither do the various markets. Up and down and all around. Its a difficult time unless you own a fund manager.

Wonder if someone said that right before the tulip bubble popped?

A stock market pop is going to make things appear more normal. If you look a trailing 10 year peak returns the pattern is up double digits followed by a ten year period around around zero or slightly negative. We are due for the lean years which will break some things and put us on a different track.

yes, greed and lust for power will tend to produce that effect.

I just don’t understand who ( other than the $2 million house crowd) are running out to buy a new house in the current set of conditions. “My Job working from home doing logistics for an Airline is super solid, so I think I will buy a new house with a better office.” Or the soon to retire person,” I bet my portfolio will be earning big in the next few years so lets splurge on a fancier house for our golden years.” Or the guys who is the manager at a big chain restaurant, ” I bet the winter months will be great for the restaurant business so I bet I will get a raise so I better grab a new house now.” What are these people thinking.

What are buyers thinking? That interest rates will go deeply negative and prices will go stratospheric. When the CBs bailed the market after the GFC it caught a lot of players out and many got permanently excluded. With WFH many buyers must be thinking this is their last chance in this life before everywhere gets too expensive.

Personally I think WFH will unleash a massive deflationary force. As unemployment rises, workers will flee to anywhere cheap so they can outbid others for scarce jobs. You’ll have skilled techies living in vans who can work for min wage if required.

Fed must be terrified of this. Combined with AI and automation this is the nightmare when all the tools they have are for fighting inflation.

Putting a cap on max hours non-executive employees can work and lowering this cap over time as things can automated is the only solution.

In Germany, if you make employees work overtime, you actually have to give them that same number of hours off later on.

You want governments telling people how long they can work and you want this cap to only apply to a specific “class” of people? My god.

@Nick – currently we have hour limits on truck drivers, airline crew, etc. Indirectly, with ObamaCare, we have hour limits on low-pay workers through businesses avoiding providing healthcare insurance. Watch for more.

Nick,

It would apply to literally everyone, except, executives. Overtime is a known concept, companies have gotten around it by making you a salary employee.

I really don’t think the average home buyer has any clue what a negative interest rate is, or how it would affect housing. We can all only speculate why certain areas are sky-rocketing and other are down. I would certainly think the shortage of inventory, interest rates and the flight out of large cities are part of the puzzle.

Go long satellite internet providers for vans.

And cardboard boxes, for real estate speculators.

I’m pleased to see someone is paying attention to deflationary forces — most of the time it’s the tiresome of the squawk of the inflationistas, all evidence to the contrary notwithstanding.

“I’m pleased to see someone is paying attention to deflationary forces — most of the time it’s the tiresome of the squawk of the inflationistas, all evidence to the contrary notwithstanding.”

What evidence are you talking about? For 11 years straight, nothing but inflation.

@ eg –

please identify any time in the last several decades when there has been deflation.

Jon W-already here. My ‘skilled techies’ step-nephew and partner bought a new Sprinter last year, converted it, and are living/working out of it between SilVly & Vegas.

may we all find a better day.

Seneca’s cliff,

They are thinking the exact same things they were thinking pre-pandemic. Just with a passing pandemic (their thinking) happening simultaneously.

Most people don’t follow the finance world and base their spending on their current income.

I have never seen a guy buy a really nice home for himself. It was either because there was a woman involved or he thought it was a good investment. I am sure there are exceptions, but I haven’t seen any.

A friend of mine bought a really nice home for himself 25 years ago (waaaaay too big two-story) in order to attract the right female. Attracted the wrong females. He got hired by another company, which moved him, and ended up buying the house from him at cost (because the market had turned south on him); and after he moved to the new city into a temporary apartment, he found the right female :-]

The common term is “suitable”, being non-gender specific, a “suitable marriage”. My neighbor just did a huge remodel to attract a wife. He is thirty and living in the most difficult period ever, to begin a family. Personal trust dynamics are at multi generational lows. Most existing marriages survive on codependency. In the 60’s there was quite a bit of love, and not as much committment, now it is the opposite. You hold your nose and walk down the aisle. They have finally financialized the relationship, or the cynics may say, they made it official.

Ambrose, that’s not purely cynicism. In the patriarchal common law tradition, marriage was a property contract from the outset. Women and children were chattels until not terribly long ago in historical terms.

“Women and children were chattels until not terribly long ago in historical terms.”

Right. It was all about property and had nothing to do with love and honor (like it does now, of course). Men were REAL jerks back then. They hardly worked, drank often, then came home to beat there wives and work their children. For thousands of years, men!

“My job is super shaky, but if I buy a house they probably won’t foreclose on me and I can live free for years like people did last time.”

I am one of these buyers in this hot market, as are my two siblings. We live in a cheap area of a flyover state that never really booms and never really busts. Several reasons for buying now… First one is interest rates. They are low enough to make previously unobtainable homes obtainable. In the long run, I expect to see more asset price inflation and currency devaluation so at 2.5% I am almost being paid to buy real estate. Second is demographic. We are middle millennials and are starting families. After several years living conservatively in small cheap homes, we want something for the little kids been eyeing larger homes with more room for kids to play. Third is a loss of faith in alternative investments. Buying stocks right now feels like buying at a top. So might as well pull back on the stock investments for a while and shift some investing into land.

I am certainly concerned for the economy at large. We seem to be blowing some nasty bubbles in this country. But in our houses, our jobs are fairly stable…homes in the area sell for less than they cost to build, so the prices aren’t crazy. Now is as good a time as ever. YOLO

Wolf,

Excellent post, as usual.

The inventory chart was a gem.

The Fed could end the idiot speculation in a single second with a single hinted at word, “taper”.

Regarding: But this craziness in the housing market is not sustainable.

I made statements like that a decade ago, and it just kept going. This is Vancouver Island, and now with many people fleeing cities and colder climes, the market is still climbing so I just keep my mouth shut. My son is looking for another place in town, and has rented his home out near where I live. The rent covers his mortgage and insurance. Taxes are minimal. My only advice (when he asks) is to tell him to not to be in a rush and stampede into a wrong purchase. Of course the prices continue to hold fast and even rise by the week.

One good note is that he is keeping to the old fashioned adage of buying within the range of 3X gross salary. I’ve read that few people do that these days.

I don’t believe prices will crash until interest rates rise, or the economy totally tanks. Our local economy is doing quite well except for hospitality. Logging and construction is booming. Booming.

As an aside, our local large campground is bursting at the seams. Apparently, snowbirds have now arrived in western Canada as opposed to traveling to the US. The roads are full of RVs. Here is the joke, though. We are experiencing the earliest snowfall ever. It is supposed to hit minus 5 (C) tonight when it clears. We just had slush this morning, but I drained all the water lines and outside taps just in case. We’ll see some snowbirds all right, shivering their patooties off in their 2″ walled trailers.

3x annual salary is not old fashioned.

old fashioned: A dad builds a house, in a couple of weeks, that can get his family through a prairie winter. Maybe 1 person helping.

Happy,

Yup, I agree, I’m only going back 40 years. I’m one of those guys who bought cheap and renovated while living there. That might one version of the modern equivalent. I do know people who bought chainsaw and bandsaw mills and spent years milling up their lumber for their homes. Party pooper me said, “You do know the framing and finishing lumber is the cheapest portion of your home”?

Another version is buying land, moving a trailer on to it and then slowly replace it. The problem with the cheapo version of house building is many never finish. Shacks stay shacks and the kids move on. You see it everywhere rural. I just walked past one. Shacky trailer, dangerous wood stove chimney, and two Harleys in the yard with plastic tarps covering them. Dirt bikes left in the field. Brutal.

3X Salary is financial destruction

1X salary is insanely expensive

Trailer sounds good- oh wait those are financed and therefore insanely expensive right now.

I will just live on a mat until wisdom returns

Growing up, many of my neighbors parents bought a lot, cash. Got financing to build a house, but acted as the general contractor themselves. Paid to have the foundation, framing, electrical and rough plumbing done, and finished the rest themselves. Most only had 10yr mortgages, and had paid for homes and a cabin in the mountains before their kids got out of grade school.

The snowbirds have arrived early in Naples, FL and they are bringing their cash to buy homes. Sept home sales were up 46% over Sept 2019. Inventory levels were 13,500 in 2008. Today they are 3,700 or about 2.7 months supply coming into our busy season.

“buying within the range of 3X gross salary”

And a stones throw from my office in Orange CA you get this.

$725,0002 bd1 ba1,072 sqft

Using your metric the income level required is $245K

I’m speechless…….2020 has been the most depressing year ever.

Ah yes, and then Orange has a housing measure on the ballot & a bunch of Wealthy Homeowner NIMBYs are running a big “no homes! No cars! No parks!” campaign & want to block 180 homes from being built. It’s just so ridiculous when homeowners that got theirs want to ruin future generations’ chance at homeownership.

(There’s a YIMBY group in OC called People For Housing OC that gives me all the good housing fights lol)

Maybe people should squat in a tent city on their sidewalks.

In most places if you’re making $50k to $70k you’re doing pretty well relative to others. Household income at $80k would be better than median. Two middlish full-time professional incomes put a lot of couples over $100k but statistically this starts to become rare.

Available houses in most medium and larger sized cities, if sticking to the 3x rule, are truly depressing if not impossible to find. Housing is becoming a luxury regardless of the condition or size of the home with the way things are going.

That Canada even has this problem despite being significantly more devoid of people suggests to me this has to do with technology, the available jobs, and increasing urbanization as a result. WFH, idk where that will take things, but still the govts could alleviate a lot of this by building high speed commuter trains to far out communities where land and housing is still cheap.

My sister-in-law sent me a photo this morning of their rear deck at their northern Wisconsin house after the last four days of below freezing temps and snow accumulation from daily snow storms. I guess summer is over in the north.

Paulo – I probably posted something like this before. Looked at a MFD in LA near USC, but not student housing. Median HH Income a tad over $50,000. Median home price $825,000. Save 5%/Yr of Med HH Income toward a 20% down payment on median home price takes over 6 decades (assumes static income & home prices). People are stuck. We were looking at a 2,000 SF 1920s home in So Carolina – looked good in a small town – asking price $135,000 or $150,000. The same type of home in that LA neighborhood was $1.25MM and it didnt look good. It was a real POS the way only some of those 1900 or 1920s bldgs look around the LA Coliseum.

More than anything I wonder when businesses will leave? They have to pay so much for employees who in turn have to drive an hour each way, they have to pay for daycare and both parents work and if you live in certain areas schools are ending grades b/c certain students got more Ds and Fs. You can look back about 20 years for an interview with the owner of Buck Knives when they were in El Cajon, California and leaving for idaho. Owner of the company just laid it out and things were better then.

BTW, SoCal freeways are awesome these days. No need for the toll roads which have to be hurting. BTW, I paid 2x my income at the time for my duplex and after collecting rent on 1 of the units my net mortgage payment was 12% of annual. If you look at the example above – its over 15x income. Thanks you Alan Greenspan and Fed spawn.

So, we defectives who don’t know the special real estate acronyms should ignore your post?

What is MFD? “MFD may refer to: Madison Fire Department, US. Minneapolis Fire Department, US. Milwaukee Fire Department, US. Mumbai Fire Brigade, India. Macroscopic Fundamental Diagram, a type of fundamental diagram of traffic flow in transportation engineering.”

HH? etc?

Just look it up here (MFD):

https://acronyms.thefreedictionary.com/MFD

It’s hopefully one of the 74.

HH may be “Household”

I think it’s multi-family dwelling.

I’m really trying to figure out what the political solution is to expiration of the foreclosure moratorium. You possibly can’t dump millions of foreclosures simultaneously in January, but I don’t think it can last indefinitely. Trump would extend the moratorium until 2024 if it meant winning the election, but no way Mitch would go for it. 2009 Biden wasn’t keen on a homeowner bailout.

Government-facilitated program for Blackstone/Blackrock/Blackwater to buy foreclosures and lease back?

i would say don’t give them any ideas, but i fear this has been the plan all along.

Yup

Oh don’t woory, it’s been extended to Dec. 2021.. so inventory will remain tight for a year.

https://www.housingwire.com/articles/in-a-bid-for-stability-fhfa-and-fha-extend-forbearance-policies/

“In a bid for stability” .. houses will go up another 20% by then.

After the elections, there is no incentive to keep the forbearance going.

It will be time to tear off the band-aid and let the market heal itself.

Sports fans, this is what happens when a run-amok government agency like the Fed takes over a previously free and basically efficient market, the mortgage market. These low, low rates are going to come back and haunt the Lenders, delayed Halloween in 2021, as many of the frantic buyers could only qualify at below inflation rates, and no one’s job, even Powell’s, is guaranteed in the economic period I see unfolding in the new year. If buying a home were financially easy, everyone would own one and demand would be almost ZERO.

I agree. The danger with what the Fed has done is that the economy no longer works without continued asset appreciation. How many people would be devastated if home prices went down by 50%? How many pension funds would collapse if stocks went down 70%? Who knows what the future holds? A dollar will probably buy less food and electricity in 10 years is all I know.

Kudos to Wolf for pointing out how volumes (including inventory of “for sale” listings) are key.

Looking at *actual* sales volume YTD in CA, it is down about 9%.

https://journal.firsttuesday.us/home-sales-volume-and-price-peaks/692/

When volumes fall (because many potential buyers and sellers are unnerved by financial environment) that means the remaining transactors are more heavily weighted towards the “carriage” trade – HNW actors more comfortable with leverage, speculation, and possible downside risk.

This partial shrinking of the buyer pool skews median sales price upward…the very reason why the Case Shiller index was designed to try and match sales transactions on identical houses over time, so that shifting buyer mixes/preferences would skew the medians less.

Crazy, I just assumed that when the media says that home sales are up 15% year over year, they meant 15% more homes sold. Not 15% more dollars traded hands in home sales.

My fault for assuming.

In a given year only about 1/20th of the housing stock changes hands (5%). So if even 1% of the population finds suddenly that it wants to move, that’s a big surge against the baseline 5%.

In addition to work-from-anywhere, there’s a lot of popular reaction to different levels of COVID restrictions, as well as the varying political responses to the protests and unrests.

Thinking of the US as 50 states that all have different character to them, perhaps it’s no surprise that with so much change, many people are finding they’d be more comfortable living elsewhere.

It is a little sobering when you consider nearly twice that yearly percentage are now in forbearance, and it is conservative to say half or more of those will end up repossessed. I expect they will do everything they can to sit on much of that supply and dole it out slowly as they did in 2008. but it is still a huge amount of inventory destined to hit the market beginning in about 6 mos. I wonder how the commercial real estate crash will effect the ability of lenders to sit on residential inventory? It appears at this point that the dam has too many holes for the financial industry to put fingers in them all….

Here in Melbourne there will be a report of an increase in sales over the next month or so, but in reality these are not real ‘sales’ in the sense that they were put on the market recently and then sold.

These are all the places that were “under contract” from action that took place in the various phases of the lockdown here, but couldn’t be completed as most, if not all real estate activity was shut down for the past three months.

No inspections were allowed so the final inspection required for closing couldn’t take place. Now that these are allowed, the sales process will be completed and the property reported as ‘sold’.

There will also be a big increase in the number of properties for sale as those that want to sell over the past three months were prevented from doing so.

What will be interesting to see is how many people flee the once darling city and move to regional areas in Victoria or abandon the state all together and move to NSW or Queensland.

Queensland is now experiencing a property boom as people from both NSW and Victoria are buying up there – sometimes sight unseen too.

And unlike 30 years ago the prices in Queensland are no longer cheap either.

Numerous businesses are relocating from California to Arizona. Phoenix area brokers have plenty of buyers but no inventory to sell them.

One such business (Toyota Financial) reportedly closed their San Diego office and moved to a suburb of Phoenix. All employees who made the move were told they will be working from home. Now everyone is looking for a home to buy or rent. Good luck with that.

This WFH trend is goosing the market. Its not going to fade away in the next few months.

If all those employees were told they could work from home, why did they move from San Diego in the first place?

Cuz they want to get TF out of California.

I highly doubt many people who live in San Diego are just itching to move to Phoenix. Your entire story smells.

“Oh, give me a home where the beefalo roam, and the cantaloupes grow in dry clay. I’ll plant my fat a** right down in the grass, and sing to the horses all day.” Everyone in America is another Roy Rogers wannabe.

BuySome, can’t reply to your thread:

Add “Cool Water”

to the song they’ll sing next August in the AridZONA.

I am in San Diego and I’d love to move out of San Diego asap and when I can.

BuySome/Tony22-unless the desal facility at the old Encina powerplant can make up the difference for SD County, SoCal (imports most of its h20, as well) won’t be much better off than Arizona. Sierra & Rockies annual snowpacks continue to decline.

(born/raised in San Diego where my family had been since 1910. Left forever in ’77, not in small part for the above reason…).

may we all find a better day.

may we all find a better day.

Maybe they cashed out and took the “big dollars” to Arizona where they can buy a house, use the rest of the money for a 40′ sailboat and a spare condo to rent out.

COL is about half in Phoenix what it is in San Diego. You can make a mortgage payment in Phoenix for what your utility bills cost in San Diego.

jdog: I think your data on Phoenix is outdated. The cost of living used to be low here. Housing prices have escalated quite a bit in the past 3 years…. inventory is low – even here in the Foothills. What could be bought for $350K three years ago is now in the mid $500’s.

The truth is that Toyota doesn’t care if their “associates” want to leave San Diego or not. It’s a “your job is here” situation and they can either go or resign. Others will get the “Here’s your severance. Have a nice day.” treatment. Many won’t take the deal because they can’t bear the thought of leaving CA. Others will send dad (or mom) to PHX until they can find other employment. I have a friend that is in DC area and he’s going to “commute” to CA, leaving his wife and kids behind. Try that one on.

One of the few remaining major automotive distributors with a presence in CA is making noises about moving out of CA. Same reason. Taxes, fees, and higher salaries required to attract talent. They can move to another area of the country and increase their bottom line. Toyota did that when they moved from Torrance, CA (South Bay LA) to Texas (I think Irving).

The rent on PhX is almost 60% of that in San Diego. So, you are not that far off.

I agree. I must say, Wolf, I read your article with a grain of salt. Your perspective is heavily SF, or big city in general. I also live in Arizona and it’s a whole different world here (btw, long ago i lived in SF for 7 years as a renter, in lower Nob Hill).

I will say that places like the “Valley” (i.e. Phoenix area in AZ) are booming because everyone (and his nephew) is moving here. Phoenix area is now over 5 million people. New construction everywhere.

I wonder if this is the beginning of the “Great Bifurcation”. What I mean is, formerly “big” markets in terms of pricing power (like SF, NY etc.) are fading, and formerly “boring” markets (like Phoenix suburbia) are moving up. And this bifurcation is permanent.

Kind of like prices went up in early 2000s in Orange County CA (where I also lived for some 12 years), and never looked back, crisis or no crisis.

I feel in this Great Bifurcation, there will be permanent winners, and perhaps permanent losers too.

Out here in flyover country, the pace remains blistering.

Those fleeing chicago make up the majority of out of town buyers.

Most are 1st or 2nd generation eastern europeans. They have seen this movie before, and know how it ends.

These are not the “rich”, assume they are fleeing to a little more upscale than out here. Majority are in the trades. So they will do well.

You mean they’ve seen the results of hyperinflation?

@RightNYer – Touché. Many from Eastern Europe have LIVED hyperinflation. Not a pleasant experience.

“Most are 1st or 2nd generation eastern europeans. They have seen this movie before, and know how it ends.”

lmao ok sure buddy

Phoenix is a horrible choice. it is full of pickup truck drivin’ gun totin’ yahoos of the worst stripe. there is a water shortage in the near future, and even the radioactive rattlesnakes have guns. BEWARE!!!!!

Yes, that’s why Californians are moving in droves here, about 130,000 every year. High tech business is booming here. Nice, new neighborhoods throughout.

Also, Phoenix sits on a huge underground water aquifer which holds about 400 years of water reserves, largely untapped. Bottled water is the cheapest here in the nation.

And when you said ‘radioactive rattlesnakes with guns’ then I knew you’re just being funny!

And, doesn’t PHX already have a problem with water? I guess it can only get better…

Problem with water? When I was in San Diego my water bills were $100 /200 a month without sewer charge! $400 to $500 electric bills are not uncommon, and they cut your power off every time the wind blows.

Gas is nearly $5 a gal. Car registration $200 to $500 a year. 10% sales taxes.

I hear you brother, the only place worse than Arizona, is Idaho, with snow drifts up to the roof and Bears that love to eat anyone from out of State!!! Go to San Francisco, Wolf says it is wonderful!

Also a furnace.

It is true that states like Utah, Nevada, and Arizona have been recipients of the great California exit for both residents and companies. I would say that Californians are the ones driving up home prices here in the greater Phoenix area mostly.

Indeed, very few places that Californians and New Yorkers don’t mess up.

My theory is that it’s because their ideology relies on false assumptions about the world and about human nature. In order to believe what they do, you have to have the capacity to ignore and explain away (in your mind) things that conflict.

Since they are able to do this, they never see the connection between the things they vote for and the mess that results. So moving somewhere else and continuing to vote for the same policies makes perfect sense.

Exactly RighNYer, these clowns recreate that which they are escaping from…perfect definition of insanity…do the same thing but expect a different result. Maybe Prozac in the water will help????? :-(

Trin/RightNY-can’t speak for NY, but as an aged Californian (whose family’s been here since 1910) , it seems to me it’s a case of the grandchildren are only heading back to the places that their grand/great-grandparents left to make a better life here back in the day. Sheer following numbers over the decades have consumed and degraded once-great resources and opportunity. As someone posted here not long ago, freedom of movement is still allowed in our great nation-as a result, you’re up, and it’s your chance to show you can competently manage those great numbers coming to your slice of heaven to seek that better life. Good luck to you, you’ll need it.

may we all find a better day.

The Minneapolis Star Tribune reported on 19 October that in September, buyers signed 6,443 purchase agreements in the Twin Cities metro area. This is 28% higher than 2019 and the most in nearly two decades. Listings were up 10% year over year for September @ 7,771 new ones.

Headline: “Low interest rates keep Twin Cities home sales rolling along.”

Minneapolis/St. Paul January record low -41*F, mean low for January -15*F.. Average annual snowfall 54+ inches. Just sayin’

Yeah, it is 27 F right now. Been cold and snowing for five days. Damn near put the Blizzaks on the 450h yesterday, but I swear it’s gotta get above freezing again. Doesn’t it?

At least the ground is still warm enough that the 18 cm that fell on my driveway Tuesday has melted. Garden is done for the season though.

Even if you can afford to service a 800,000 dollar mortgage on a 1,000,000 house once the value of that house drops to 700,000- 500,000 the desire to service that debt stops. The owner looks to short-sale or just walk away rather than paying 2000 a month more on a property than what it is worth.

So, all that Dave Ramsey “buy it if you plan to live in it for awhile” is nonsense in this kind of environment. Buy nothing.

It’s amazing how fast things are forgotten. Or maybe not forgotten so much as this-time-is-different’ed away. There was a scene in the documentary “Owned: A Tale of Two Americas” where they’re standing in an empty, foreclosed stucco subdivison in the middle of the desert and the RE agent they’re interviewing says something along the lines of: “When a brand new house you spend nearly a million dollars on loses half of it’s value almost overnight, how are you going to feel about making that next payment?”

Nothing causes amnesia faster than a bubble, except for borrowing money….

you have to feel pretty comfortable in your current job, and it’s longevity in these uncertain times.

you also, have to assume you won’t be asked to take a paycut/hours reduction that puts you in a tight spot.

dave ramsey’s advice is for people in untenable amounts of debt. people in way over their heads. i have a few quibbles with his program, but for the typical math challenged, never had to learn how to balance a physical checkbook type of american, his program is like a remedial home economics class over the radio, but for “adults.” it is needed, especially for those who listen to the radio.

i listened to dave’s program for several days a few years ago, during a long road trip with my mom. it kept the politics off the airwaves for much of the trip, and i owe him a debt of gratitude for that alone. i kind of do agree with his get out of debt mantra.

In America anything is possible. Dave has gotten wealthy teaching the following:

1. Have an emergency fund

2. Pay off consumer debt as fast as possible.

3. Pay cash for a vehicle.

4. Invest 15% of income.

5. House payment no more than 25% take him pay.

As he says, grandma knew those things. He got wealthy teaching what parents should have taught.

“take him pay”–Would that be a household with a working wife and an unemployed husband? Accidents never happen in a perfect world…the touch-screen excepted.

“Pay cash for a USED vehicle.”

Ask for a price reduction their tax lowering cash discount on all services performed by individuals like mechanics, plumbers, etc.

If you have separate debts, try to pay off the debt with the highest interest first, even if it’s a small one, then work your way down the line to the next highest interest rate.

If I buy an $800K place, the only way to walk away is buy a $500K place before letting the $800K place go, right? Then the IRS will 1099 on the forgiven debt?

Is there difference in jingle mail between fannie/freddie loans versus higher priced loans from other lenders?

In ’09-’10, the 1099 from a short sale was forgiven or excluded or whatever from taxable income. That expired years ago, so they’ll have to pass it again…in about two years, I assume.

A horrible time to be a first time buyer. This isn’t your grandparent’s market.

Sadly the government has little interest in correcting the matter– existing homeowners/voters feel wealthier by the day.

Only thing that will stop it is higher rates. Even in high priced Seattle where rents are down double digits, prices are soaring double digits and despite so many stories of folks taking advantage of WFH and moving inventory is at an all time low (and that’s sayings something considering 2015-2017).

The most interesting chart I have seen showed medium home affordability based on median household income at different interest rates. If you take it back to 5-7% rates the affordability for most drops off a cliff. It is the long term trend to lower rates that drives this. Of course massive corporate layoffs could impact things too.

The secular trend of interest rates for something like 700 years in the Western world is downward. There is no “market” for rates — the Fed sets rates. If you’re waiting around for “5-7%” rates, you will be waiting a very, very long time indeed …

Here’s the problem with buying an overpriced house. The RE tax assessor revalues your property at the sales price, and that current valuation is usually 20-30% above what it was valued at the day before the sale. With states and localities looking to raise taxes to cover all the deficit spending around COVID, you can bet your RE tax RATE will be increasing as well. You get whacked on the new valuation as well as the RE tax rate.

In most cases, the increased tax is likely going to completely nullify the benefit of a 1% drop in mortgage rates.

But in California anyway, one can petition the county assessor to lower your value and taxes if and when property values drop.

https://assessor.saccounty.net/DeclineInValue/Pages/Review%20Period%20Open.aspx

Decline in Market Value (Prop 8) Background and Overview

“An owner providing the Assessor with data to support a lower value.

The Assessor may initiate the Prop 8 review.

The Assessor’s Office constantly monitors real estate market conditions and lowers assessed values on a mass basis.

So you expect bankrupt local governments to cut their income stream? Good luck with that…. I imagine their assessment to be a lot different than yours.

If the houses, of the same design, on either side of you have dropped in market value by 50%, it would be hard for them to deny it.

Should they overinflate it’s value, one could possibly sell the house for that value, with a kickback, to someone who could then pay you cash and get a huge tax write off…the possiblities for mischief are endless.

This time is different

I have heard “this time is different” in every bubble for my entire life…. it is never different, the laws of mathematics cannot be denied.

The Internet accelerated globalization.

Consequently, the poor got poorer.

We’ll adjust, eventually.

So much winning. Rich people get richer, and the rest get to buy a lot of things.

Seriously, I can’t see any losers here. This is how it’s supposed to be. This country has never been more prosperous.

Seniors on fixed incomes are losers if they can’t find work at Home Depot or a grocery store. They are not buying homes with inflated prices or Teslas.

MonkeyBiz – LOL! I happen to appreciate the dark/ironic/sarcastic humor. I am the guy who awkwardly laughs at the movies at the wrong-non-PC moment—so perhaps many do not even “get it” but thanks for the laugh. Wolf gets in some zingers at times too…the humor keeps me semi-sane, HA…

Charlie Sheen for Pres?—–>”Make winning great again!”

We’ve reached a permanently high plateau!!!

Debt out the wazoo is old stuff, pretty soon it’s equities out the wazoo. It will be a rocket ship. I mean bacon will be 50 bucks a slice inside the rocket ship but I mean would you prefer to be inside a rocket ship or live in New Zealand?

No losers if everyone is a landlord and tenant at same time. Rent out your house to someone, and he can do the same with you. Schedule E deductions baby!!!

“Seriously, I can’t see any losers here. This is how it’s supposed to be. This country has never been more prosperous.”

– Let’s put things in perspective. Reality check, please. A little basic economics, which seems to be flying over the heads of the 22,000-odd employees at the Federal Reserve, and everyone else who drank the MMT kool-aid.

– Recall that “debt is not wealth.” The health of a nation, just like a business, or a household, is measured the “old fashioned way,” by the balance sheet. A healthy balance sheet would have more assets than liabilities. Exactly then, how does the U.S. measure up? (rhetorical).

– The U.S. economy is in la la land. Just run the numbers. How long would the economy last if the artificial stimulus and ultra-low interest rates were taken away? (again, rhetorical). BTW, the ultra-low rates are an artifact of an over-indebted economy. Even though they deny it (i.e. lie), the Fed is driving wealth and income inequality. The Fed is pro capital and banks and con labor and (small) businesses. The Fed represents Wall St and the banking cartel, and not Main St. They aren’t the friend of Middle America. Just follow the money.

– A declining Middle Class isn’t a sign of a healthy economy. There’s nothing normal, or healthy about any of this. Instead, we have a centrally-planned, command-and-control economy, via the very visible hand of the Fed. This has never ended well historically. People have short memories when it comes to markets. Everyone’s already forgotten the dot com bust of 2000 and the GFC of 2008 (housing bubble 1.0). Did the Fed “prevent” those crashes? No! They were the cause then, and are the cause now. It’s not different this time. There’s always a bust after the boom. There is no tooth fairy. There is no free lunch.

“We must make our choice. We may have democracy, or we may have wealth concentrated in the hands of a few, but we cannot have both.” – Louis D. Brandeis

“The enduring lesson of the 20th century is that socialism is a failure, and free markets are a success. But the politicians keep advocating just a little more socialism.” – Milton Friedman

You live in the United Shoppers of America, or is it the United Sheeps of America.

Making a choice/freedom requires courage to live with the consequences, something neither shoppers nor sheeps have.

Its like when Covid hit and the sheep freaked out about toilet paper and hand sanitizer and no one could find any until the manufacturers started producing more of it. This is what the housing feeding frenzy reminds me of. At least in Illinois the houses aren’t going up much bc of our high taxes.

Just for a reality check. The Fed was created under the guise of preventing any more recessions like the one that happened in 1908.

Since that time, there have been 19 recessions/depressions, that the Fed has been powerless to stop. But I am sure they will be able to do it this time. (sarc)

Except…

Half of all workers made less than $34,250 last year.

Dano,

Kudos…most people get suckered into looking at household income (about 60k), which almost always means two workers these days.

In the “evil” 1950’s, American families could live a comfortable middle class lifestyle on a *single* income.

Now, it takes two incomes and huge debt to maintain a bleeding fingernail, failing, clawing grasp on a remotely similar lifestyle.

Yep, American “leadership” has done a helluva of a job over the last 65 years.

To be fair, American middle-class prosperity of the 1950s and 1960s was largely an accident of history. You can talk about how it’s because of unions, or responsible corporate citizens, or whatever else, but the fact is, we had a virtual monopoly on manufacturing after the destruction of Europe’s capacity from World War 2. Asia was still basically undeveloped from that perspective.

Further, we didn’t have the medical advances today that lead to having a large group of expensive senior citizens (not making a value judgment here, just stating the facts). So we had a lot more economic revenue (from our manufacturing monopoly) and a lot fewer expenses.

That hegemony really only existed until 1970 or so, after which competitive pressures from the rebuilt Europe and Japan. Ever since then, we’ve been pretending through a combination of debt and reaping the benefits of deflationary technological advances.

Quite frankly, I’m amused that this game has gone on as long as it has.

@RightNYer

That’s part of it. Of much greater significance and consequence is the substantial transfer of wealth from the nation’s treasury to war profiteers. First Korea. Next Viet Nam. At this point the US dropped the gold standard. The US could not afford these invasions and incursions with the dollar reigned in so they let it loose. This in turn destabilized the housing market (which over the previous 30 years had been the most stable in American history) and initiated the drive to offshore labor.

Of course the final straw was the Iraq invasion. No turning back after that. That first night of bombing I stared at the television practically in tears realizing this while all the idiots gathered around cheering. The US would become bankrupt while the criminals that bamboozled the public got to keep all those ill gotten gains.

I’m a little confused by the relationship between the war profiteering and the housing market. Can you explain a little further?