There is a “housing shortage” and an “inventory shortage” until there suddenly isn’t.

By Wolf Richter for WOLF STREET.

In San Francisco, the erstwhile housing “shortage” and inventory “shortage,” hyped to the nth degree by the industry, has now turned into a historic inventory glut.

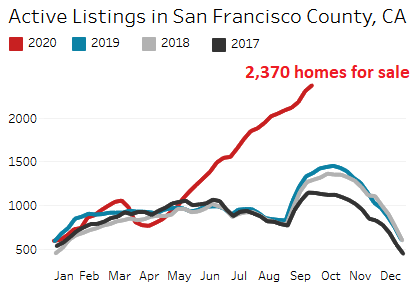

There were 2,370 homes listed for sale in San Francisco in the week ended September 27, up 73% from the same week a year ago, according to data from Redfin. About two-thirds of them were condos. The chart shows the comparisons of 2020 to the prior three years. Note the seasonal bulge of active listings after Labor Day in prior years, and how 2020 completely blew that away:

This inventory “shortage” turned into a glut when condo owners who don’t live in these units – a lot of condos are investment properties – decided they need to sell because the Airbnb business has swooned, or because rents in San Francisco are in a historic free fall amid surging vacancy rates as younger recent arrivals and some other folks are leaving the city, and the rent that a condo owner could get from the now vacant unit wouldn’t be nearly enough to pay for the mortgage, homeowner association fees, property taxes, and insurance. And now condo prices are falling, and owners are trying to unload their units while they still can.

There were a record 1,510 active and “coming soon” condo listings at the end of September, according to MLS data cited by Compass. Zillow lists 1,417 condos for sale at the moment. San Francisco is not a big city. It had a population of about 880,000 in July last year, before the exodus began.

And this does not include the condos for sale by condo developers that have their own sales offices and don’t list their condos on the MLS. These new construction condos for sale are hard to quantify, but the new towers and mid-rise buildings from the construction boom are easy to see.

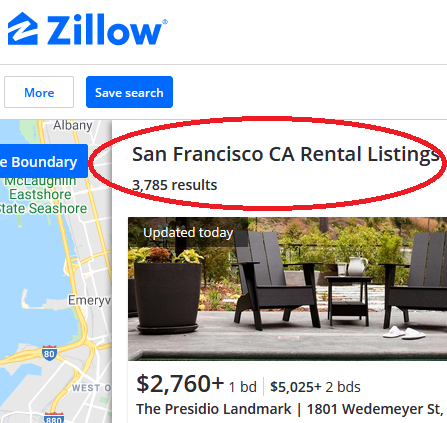

Many of the condos are used as investment properties, including for long-term rentals. Alas, Zillow now lists 3,785 apartments for rent in the City, including condos for rent, over triple the number it listed for rent during the good old times at the end of September 2016.

This glut of rentals, plunging rents, and the downturn in the Airbnb business in San Francisco – foreign tourists have largely vanished – have upended the business model of condos as an income-producing investment.

Condos, especially in high rises, are expensive to carry due to the homeowner association fees, taxes, and insurance.

For example, a 2-bedroom, 2-bath condo, originally listed on Zillow at $1.288 million in October a year ago, removed several times and relisted at lower prices, is now listed at $1.1 million – below the median condo sale price in Q3 of $1.25 million. The monthly costs add up: HOA fees $915/month; property taxes $614/month; insurance $385/month. Including the mortgage, total monthly carrying costs amount to $5,768, according to Zillow estimates.

It was listed for rent a couple of years ago at $4,695 a month. But even that insufficient rent might not currently be feasible after the median asking rent for a 2-BR apartment plunged by 20% from a year ago and by 25% from the peak. And then there are the incentives to fill the unit such as the latest craze, “three months free rent.” Nice but not spectacular view — if there’s a Bay view, they’d show it:

And condo prices have started to drop ever so gently:

- Per square foot: In Q3, the average price fell 5.0% compared to Q3 2019, to $1,088 per square foot. Down also 2.9% from Q3 2018, per Compass.

- The median condo price in Q3 fell 2.0% year-over-year to $1.25 million, per Compass.

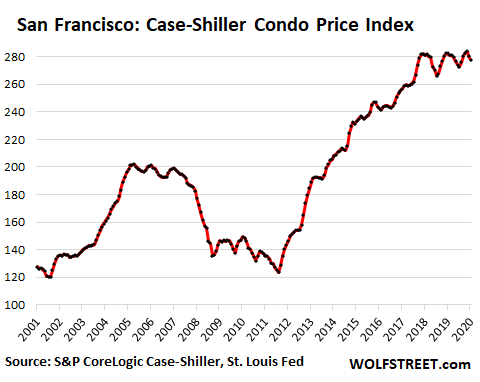

- Per the most recent Case-Shiller Home Price Index of a few days ago – a rolling three-month average of transactions published by the county in May, June, and July – condo prices fell 1.6% year-over-year, and 2.1% from the “May” reading which consisted largely of deals made before the Pandemic. The Case-Shiller Index for condos normally rises from May to June, but not this year.

Price movements in real estate are slow and take a long time to play out. During Housing Bust 1, from condo peak to condo trough took over five years. The chart of the Case-Shiller Index for condos shows that condo prices have in effect gone nowhere for the past three years, similar to period between mid-2005 and mid-2007:

“Within the condo market, the high-rise segment appears to be the weakest, almost certainly due to pandemic-related reasons,” explains Compass in its analysis of the mess.

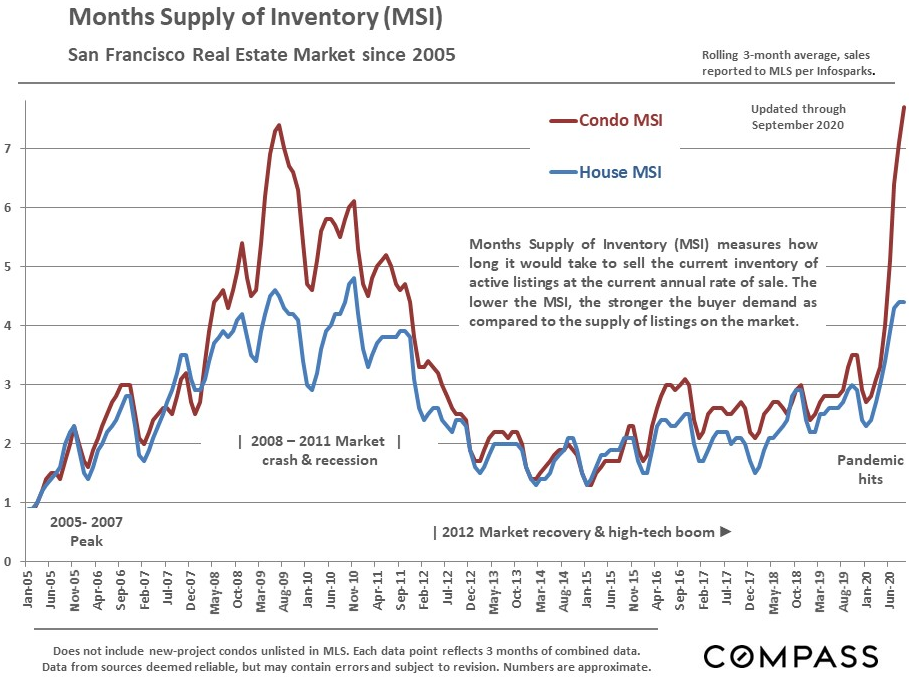

Sales are taking place at a brisk pace but are far outstripped by the increasing condo glut. Supply of condos listed for sale on the MLS skyrocketed to nearly 8 months, exceeding the supply during Housing Bust 1. Add to that the new construction condos put on the market directly by the developers through their own sales offices and not listed on the MLS.

The supply of houses for sale also jumped, to 4.4 months, approaching the record levels of Housing Bust 1. (chart via Compass):

“The number of price reductions – again heavily concentrated in the condo market – has jumped to its highest point in many years,” Compass says. “In certain segments, sellers are now competing for buyers, instead of buyers competing for listings.”

And this condo situation is another indicator that the direction has turned once again in the infamous and relentless boom-and-bust cycles of San Francisco.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The funniest thing I read all morning was HubHaus going bust.

“The Los Altos company’s business plan involved leasing large, single-family homes, dividing the properties into 10 rooms or more and subletting the rooms to young professionals at market-rate prices for each space.”

You can see how that’s going to be a problem during this pandemic.

That sounds like a business plan Old Man Potter would have created. Is it too much to hope these homes are already in heavily trafficked areas?

The Los Altos company’s business plan involved leasing large, single-family homes, dividing the properties into 10 rooms or more . . .

“Hey, real estate lady! This bedroom has an oven in it! This bedroom’s got a lot of people sitting around watching TV. This bedroom’s over in that guy’s house . . . “

Mitch Hedberg

Oh! Gone way too soon.

WeHaus

Most of these condo’s are only attractive in an appreciating market due to the carrying costs. A short time ago my wife and I viewed ourselves as prospective condo owners because we don’t like yard work and I would prefer to live somewhere where I am not chained to the tyranny of the automobile. Lately we have taken to comparing the costs of condos we like on Zillow to our current situation. We live in a 1500 square foot 3 bedroom new apartment across from a big park, near the transit station, walking distance to shopping and restaurants that is kind of a nicely appointed condo style unit. Nearly every condo we see that is the same size and quality in the swanky condo district of Portland has a full monthly cost including principal, interest, hoa, and property tax of more than double our current rent. The mortgage interest deduction does not come close to making up that difference so why bother?

For a few reasons. Owning is not the same as renting in terms of your freedom to make changes as you like. Also, when you buy, your “rent” will never go down, so in 10 or 20 years you will be paying less in owning costs than you would be paying in rent, and in 30 years you will be paying considerably less as there will be no more mortgage.

That makes a lot of sense. To add, people buy another house every 7-10 years, or refinance new 30-year mortgage every 3-4 years. And there is 6% commission, which is much less than the normal appreciation when prices go up.

If you’re in a condo (or even just in an HOA) you are paying quite a bit to be limited in “your freedom to make changes as you like”.

You still have more freedom than an apartment. Did you not realize that?

In a rental I can make some very important changes not as easily available to owners. For example, a unit became available with a better view of the park, a better deck, better closets and a better laundry area, so we moved. Total cost, $500 for the move and the rent stayed the same due to the current renters market. Maybe the way things are going rents will continue to go down while the bag holders mortgages will stay the same, while home prices go down.

Strata councils can change and can turn unreasonable. Also condos face some real insurance issues which is passed on to all owners.

Seneca’s Cliff,

You can always hire someone yourself, to do the lawn work, it’s a lot cheaper that way.

Seneca’s Cliff, it’s not like there are NO reasons to rent and ONLY reasons to buy or vice-versa, obviously. You asked why buy, I gave some reasons.

Had you asked why someone would rent when buying is such the obvious choice, then I would have given you some reason why a person might prefer to rent.

I’m curious, do you really think that there are NO reasons to do anything other than what YOU choose to do?

Moreover, you can use your own house to pay for long term care or assisted living (through a reverse mortgage) with your partner as co-owner.

In 30 years the cost of property taxes and insurance will exceed the cost of your original house payment.

Unless you do what I’m going to do and buy outright with no mortgage! If you’ve ever owned a home outright….what a beautiful feelings. Screw the banks…will never deal with them again if I can avoid it. For all the obvious reasons….

Seneca’s cliff,

This kind of math tells you that the local condo market is very vulnerable. You’re not the only that’s doing that math!

“A short time ago my wife and I viewed ourselves as prospective condo owners because we don’t like yard work and I would prefer to live somewhere where I am not chained to the tyranny of the automobile. ”

I considered buying a condo until I found out how onerous the covenants could be. Some developments would not allow me to even read the CCRs until I made an offer. Others, had disturbing carte blanche entry allowances, and no apparent accountability on how my monthly dues would be used. Still others spent ridiculous amounts of money on grounds keeping, etc. There was so much secrecy in some places that it turned me off to the whole concept (note these were not new developments but per-existing complexes). I kept wondering what the Condo boards were trying to hide.

I view living in a condo as “apartment living plus”, not a true home ownership experience. I’d rather move into an apartment than live in a condo.

Another thing we have discovered in our condo vs apt comparison project, is that often the combined total of HOA fees and property taxes for a condo of comparable size and finish is equal to our rent. So even if we payed off the mortgage our monthly expenses would be just as high and we would have all that capital sunk in an I liquid investment.

Condos only make financial sense in a world where condo prices only go up. But they don’t.

Wolf, does *any* purchased housing “make financial sense” when the price of that housing goes down?

Aren’t you expressing some sort of truism there? Doesn’t any asset only “make financial sense” when that asset appreciates?

Zantetsu,

My quick and dirty…

With a condo, you own your small percentage of the land and the common area, plus the inside of your condo. There is a political organization that decides all kinds of things. This may not be an issue in a new building, but it’s a huge issue in an older building. Need a new central water heater or the exterior walls and windows of the high rise need to be sealed? OK, the cousin of the guy on the board gets the deal, and it costs a huge amount of money, and this amount will be spread via assessments over all owners, who can vote in the meeting if they want to. If you cannot pay that assessment, you’re in default.

With a house, you too have maintenance issues, but you’re in control.

I used to own a high-rise condo in Tulsa, bought it from a bank during the collapse in the late 1980s and I sold in 2000 and benefited from price increases. Had I bought five years earlier during the bubble, I would never have recouped my costs. In addition, this was an older building, and there were all kinds of issues. The politics were horrible. You don’t have these kinds of issues with a house.

A house too is an expense unless you’re in a housing bubble (just like all forms of housing). But houses are a lot less risky, financially, than condos. And if luck and lucky-timing are with you, they’re a great deal.

But there were many great aspects to a condo too, including having staff to take care of stuff and to receive packages, and not having to worry about the lawn or pool, in addition to the spectacular views from the 23rd floor… but you get that in an apartment too.

Condo vs rental apartment is a different question, and there are other pros and cons, including this one: In San Francisco, you can lose $500k on a condo that sells for a little over median. You will never have that risk with an apartment.

On the other hand, in many cities, the landlord can choose to not renew the lease after it goes on month-to-month, and you’re out, looking for a new place, which is a pain in the butt if you’re 80.

I feel that owning a condo takes the bad aspects of home ownership and apartment renting and combines them together.

You still have the issues of apartment living such as a lot more exposure to bad neighbors, little control over the property, limited parking, and a possibly heavy-handed management body with power over you.

And home ownership issues of paying for or doing repairs for yourself, endless taxes and fees and assessments, and the possibly of getting stuck in the property in a down market.

The benefit of course is if the value goes up you can make money selling, and some tax goodies. I think condos make better investment properties to rent out than homes to settle in.

I remember when the condo conversion craze showed up in Boston in the 1970s. Even as a young person I thought the idea of buying an apartment was really stupid.

Fifty years later condos are dumber than ever. Perhaps 2020 will finally kill the condo craze.

The financial principle you’re intuiting is called the “price-to-rent” ratio. To determine the ratio, you compare how much it would cost to rent something vs. buy it outright. This principle is widely applied in business, but in personal finance is mostly used in real estate.

Compared to historical average, the price to rent ratio in large american cities is currently way over on the renting being the comparatively better deal.

Cue Randy Bachman (BTO): ”You ain’t seen nothin’ yet. B-, b-, b-, baby, you just ain’t seen na, na, nothin yet. Here’s somethin’ that you’re never gonna forget. B-, b-, b-, baby, you just ain’t seen na, na, nothin yet.”

Ha!!

‘Any house is good house. So I took what I could get. Ooohhh oohhhh’

Hi there , a friend who visits NY and rents a 2 bedrooms in Manhattan for $150 000 a year , told me that condos under $10 millions are down 25 to 30% asking price , he is actively looking to buy .

Hopefully southern California (LA/OC/SD) will experience the same thing as SF. Not holding my breath since so far the market has been defying gravity and seems to be more immune to this mess than SF or other metro areas like NYC.

Yes, I’m also hoping this movie come to Los Angeles and that it doesn’t take 5 years to get from peak to trough like Bubble 1. So far, condos in West LA are selling fast with little negotiating, or even over asking. Wonder how long it can go on…

These things would happen to not only SFO but almost all expensive cities in USA over time. But don’t expect it to happen overnight.. It may take months or year or so.

Few years back, very few thought this can happen to SFO :-)

I’m looking to buy in the Leaning Tower of San Fransisco. It will be collectors item one day. Also, the incline helps with my snoring.

Jul 28, 2020 — San Francisco’s beleaguered Millennium Tower is still sinking, but a fix is finally on the way..

I wonder which will topple first? This tower or 3 Gourges Dam???

“Incline helps with my snoring”

Thanks for the laugh.

For some reason, I read snorting first. Like doing lines. LOL

Rust Belt Bargain

A 1999, 3 BR 2 BA, 1600 sq ft, .25 acre, w/ 2 car garage home in a northern Indiana suburb near an Interstate for sale for about $150,000.

Thee only problem is you have to live in Indiana. And yes, I have visited there….once. :-) That was enough. It was a zillion degrees and humid beyond belief. The Cicadas were so loud I thought I was in a jungle. No thanks.

Honestly, if you visit a place ONCE and think you can conclude anything about whether or not you could live a fulfilling and happy life there … well, I think you’re not doing yourself any favors.

True of a lot of aspects but not weather. Like me Paulo is a Canuck and like me he can’t stand heat. I can adapt to lots of cultural differences etc. but not to being unpleasantly hot AND humid. Cold can be addressed with the right clothing because we are warm blooded and generate heat. All you can do with excess ambient heat is sweat, which doesn’t work well in a humid place.

Before aircon much of the US shut down in mid- summer including Wall Street.

Of course heat doesn’t bother everyone but it’s pointless telling others to get used to it.

Paulo,

I LOVE cicadas. The sound of afternoon in the summer. It’s one of the few things I miss in San Francisco.

they , cicadas, put me to sleep in south Texas sometimes they sound like rattle snakes!

Only seeing price increases so far on the Peninsula. High HOA townhouses and condos in so-so school districts have an asking price of over 1k/sqf. It blows my mind. SF is starting to look ever so slightly cheaper now but the schools are notoriously worse.

Hm, I see something different in Cupertino/Sunnyvale … prices have been softening for a while. Some people still pay prices like it’s 2018 but the majority of sales are at slightly lower prices and many sit on the market for 2+ months which was unheard of a year ago. Also I have seen several that were pulled back off the market because the owners presumably could not get the price they wanted and decided to sit and wait for prices to come back up. They might be waiting for a while ….

These renters are very bright people. They’ve got it all figured out. what’s to worry about?

Perhaps the SF mayor and city council can buy them and turn into homeless shelters.

Real estate busts start with Condo’s. I see a couple of $5 million plus McMansions for sale in Palo Alto. The kind that replaced 50’s 1200 sq ft tract houses. Not even 2 years old. Unfortunately for the sellers Realtor now shows FEMA flood zones. Oh dear.

Maybe Bay Area real estate has begun to regress to the mean.

I remember Wolf talking about how the condo building boom would eventually create a glut.

I suspect we’re in for a Great Leveling across the nation, where expensive markets decline and cheap markets appreciate and most markets eventually meet in the middle.

MF,

That’s funny. Great memory. Yes, that was years ago, and I got pooh-poohed for that. Construction booms take years to play out. But I never thought it would get this bad :-]

I tell anybody who says “I”m thinking about buying a condo.” to put “Condo Horror Stories” in the googlemachine and let me know what they find.

Same thing with HOAs. I’ve heard dozens of terrible stories re: Condo Boards and HOAs in FL that make most people say “I would never subject myself to that.”

Sarasota’s Dolphin Condo had structural problems in 2015. They used bad concrete when they built it in the 60s. Some owners got royally screwed. Sarasota Magazine did a well written story about it.

I’ll go non-condo, non-HOA and roll the dice on the neighbor painting his home pink or parking a semi in the front yard. My Mom and I rented a condo once and got a letter from the Condo Board:

“Your curtains are not white per our regs.” I knocked on the lady’s door and said “Mam, I’m sorry, there must be a mistake, our curtains ARE white.” She explained: “No son, your curtains are cream colored, it’s a shade of white but not white.”

Some of these folks have nothing better to do with their lives than check to see if some old lady has too many yard gnomes.

No. Thank. You.

I’ve had several homes in HOAs. Most HOAs are terrible, which is why I consider houses in HOAs as being worth a lot less than houses not in HOAs.

But nothing is worse than a coop board in NYC. The absolute worst.

I dated a fine lady that was on the board of the condo I was renting. I listened for two years to the machinations of the board. I will never buy a condo.

Does this mean the future could be the Carpartment…electric scoots you drive home to a recirculating elevator, and then go straight in, exiting on the opposite side. No lobby, but a ground floor service shop. Maybe even a snap-out bench seat to double for your sofa. Run the coffee machine right off the car while it re-powers. Totally germ transmission free. Or should we just raise the fiber content of recycled material in cardboard boxes to absorb the urban population down the line? And which will be a better ROI for us?

I imagine in the future, transportation in America, would consist of walking, bicycles, personal cars, rent on demand cars (many, possibly almost all eventually be self driving), buses, and planes. Trains and all non bus mass transit (like subways) would be likely phased out (almost everywhere).

Eventually hyperloop (maglev trains in a tunnel) or cars/buses going through said tunnels, could be a thing as well.

Also foldable bicycles are a thing.

None of these will power your coffee maker though :(

Bikes are getting huge. Worldwide bicycle component shortage as we speak. All parts production absorbed by new complete bicycles.

There’s a condo in Miami with a car elevator to your apt.

It is cool, but, a very frivolous extravagance, that I don’t see many having.

There has been a number of features on the local SF tv stations regarding break-ins in some SF residential neighborhoods .Is this condo in a safe area?

High-rises are a lot safer than places you can just walk up to and break in.

San Diego, in it’s infinite wisdom, is going to buy hotels to house homeless. Maybe SF should follow our lead for a change and buy up all the condos so they can put their homeless there. One would hope they’d stop crapping all over the streets.

Condos are free… but the HOA is not….

Heh heh, the HOA alone seems ridiculous, but I would not be surprised if that was the median HOA.

They figured if you could afford a million dollar condo, you could afford a $1K HOA that went with it.

Yep and that HOA can rise at any time. To some crazy amount.

You don’t own the condo, the condo owns you.

I predict many of these hotels will become apartment complexes in the future. And then, after a few years they will undergo further conversion into condos.

I saw many crappy 650 sqft apartments in So. Cal that were turned into condos selling at 350-400K.

Only someone who lived in So. Cal would consider such condos. I assume if you’re born in So. Cal you can’t live anywhere else due to the weather so you’re forced to make concessions. Most Californians seem to be prisoners of their state.

I live in central Ohio in an owned home. I haven’t been following the market but we still seem to have a shortage of rental units and the condo thing isn’t that big here except the ritzy McMnsion suburbs. In the last 3 months 3 fairly large apartment buildings opened in my suburb and all seem to be fairly full. Not sure how the sino flu will affect us but who knows?

LA beach single family homes are seeing multiple bids up to 3M. Prices are moving up around 8% per year. The market appears to be getting stronger.

All cash buyers?

Some, but most have mortgages.

Meanwhile, the prices of homes climb in places like Carson City and Boise because Californians are cashing out and moving out of this failed State.

SS

As stated in an earlier post as well, there seems to be a normalizing effect occurring. In the West…..Boise, Reno, Prescott AZ (my town), and more are recipients of CA flight. I got out 18 years ago (thank God). The Midwest is flourishing and I suspect this trend will continue through Covid.

Same around Raleigh, NC. Just heard real estate sales were up for September from $1.3 billion to $1.6 billion you.. Rents up 3%. New 4 million sq. ft mixed used property announced to replace Cary mall. New mixed use high rise announced for downtown Raleigh. It’s hot at the moment.

This is a horror show for landlords and condo owners but it will reverse as soon as the pandemic is brought under control. Between vaccines and therapeutics it’s looking more and more likely that this will incur within 6 months.

People are fleeing SF for several obvious reasons:

-safety from the virus

-unemployment

-option for remote work

-loss of amenities that a city offers

SF is an extreme example of this situation playing out in many cities across the world. As horrifying as this is, I think most logical people believe that everything reverses once the pandemic is brought under control. The question is when will people feel safe to return to work and mass congregate? Even if you believe that WFH is permanent I don’t think that many are arguing that it will comprise the dominant form of physical working.

Prices could drop 50% from the peak I imagine. Does anyone have any guesses where the bottom is?

Even without full functionality at minimum a city still offers a wide variety of grocery options, access to services that can be performed safely with adequate PPE (medical, dental, chiropractic, etc) safe indoor activities that can be performed at a social distance, safe indoor and patio dining options, galleries, fashion purchases etc. Even remote learning universities seem to still maintain some appeal in cities to students desperate to congregate as much as possible.

Clearly most or all of these amenities and businesses were built around business models that didn’t project 50% or less capacity so how many can survive and for how long?

It’s hard to imagine that when the coast is clear that cities with the cultural and infrastructure foundations of SF, offset by the homeless, crime and other social problems obviously, don’t springboard back to life rather quickly. I don’t think the future of life in 21st century is rural but is it a mass disbursement to mid sized cities?

Every major company needs a head office in a big city regardless if some of the staff are disbursed around the country, or world, don’t they?

Walter Ego,

“Every major company needs a head office in a big city regardless if some of the staff…”

Schwab is moving its headquarters from San Francisco to a suburb of Dallas (2021), Palantir has already moved its HQ to Denver (2020), PG&E will move its HQ to Oakland (2022), Macy’s shut down its standalone tech center that runs macys.com and moved the remainder to Atlanta (Feb 2020), etc. etc. A lot of that happening right now in SF. The reasons cited usually include: too expensive to do business here.

But I agree, at some point office rents and housing costs and the amount companies have to pay employees to work in SF will come down enough, and the trend stops, and perhaps reverses.

Good points and data Wolf. Oakland is basically SF metro area so that’s a pure cost benefit analysis.

Yes, it’s a trend outward but you’d think all things being equal they’d rather be in SF. The city and nyc needs to stop behaving like socialists and get real or they are heading down a death spiral of decay.

How Long Will a Vaccine Really Take?

By Stuart A. Thompson

April 20, 2020

If you enter the above title you can read a piece in the NYT.

There is WHOLE lot of optimism out there but no in the field is predicting a vaccine in early 2021.

A front runner Sanofi says maybe 2022.

That is we are very lucky, and all the shortcuts necessary to reduce the typical 5 to 10 years don’t backfire. It’s a given for these super schedules that the normal testing period is cut drastically.

Little item about Thalidomide, the drug that caused hundreds of birth defects in Canada.

It was up for approval in the US but ironically it was a Canadian- trained doc in the US who felt something wasn’t quite right and nixed it.

I don’t have her last name handy but her first was Frances. She applied by mail in the fifties I think, and was accepted by mail but it was obvious the US employer thought she was male. She asked a friend if she should clarify this before showing up and was told the equivalent of ‘f8$k no’

They were shocked when she arrived but it was one of the best hires US medicine ever made.

Going to have a massive effect on politics, too. Just look at how fast Texas is going blue as people from the coasts relocate there. And there are 30 million people in Texas. It wouldn’t take that much migration at all into less-dense states to tip them.

A lot of blues stay behind.

Wolf,

For the areas surrounding San Francisco, like Berkeley/Marin/Oakland/Peninsula, where do you see the SFR houses going?

Seems like a lot of the boom in the California real estate market has gone to farther out suburbs such as Sacramento and Orange County.

Craigslist has over 10,000 units in San Francisco for rent. Especially hard hit are the highrise condos with their laughable “communities” south of Market in artificial “neighborhoods” with real estate huckster invented names like “East Cut”, or whatever.

Those views may be great now, but when a tower is built to block your condo view, tough luck.

At least renters can demand a reduction if the view was part of the advertised benefits of a unit and then the view was blocked. Trying to find a citation to that on the miserable sf.gov search.

Tower condos are expensive because building costs increase exponentially relative to height. Vertical and lateral structural and seismic costs, fire and life safety, plus elevators, take up ever more space, yet do not generate revenue.

Special assesments? Wait until the BIG ONE destroys your investment. The value of the tiny slice of land you own in a condo will be less than the demolition cost of the structure.

Sorry, I just couldn’t resist:

$5,900 for 2 Bedroom. “It sits in the heart of San Francisco.” [what a crock, more like the colon, it’s an isolated, desolate, deserted all new condo tower paradise with no soul and a homeless magnet service center nearby] “With an unrivaled collection of amenities, should you choose not to,[?] you will never need to leave home. When all amenities are completed,[or until developer goes bankrupt] they will include a private dining room, bi-level club lounge, fitness center, lap pool, rooftop terrace, rock climbing wall,[great places to get infected] the Market grocery store,[do they sell motor oil and gas cans?] pet grooming station & more.”

?

On a more serious note, that’s part of the problem with these recently completed towers.

On the other hand, you can skip the gym equipment, of dubious sanitation and the elevator, where you are trapped with a vector who steps on and coughs in your confined airspace. Just trot up 15 or so flights of stairs–bonus carrying groceries= exercise and self-isolation.

The new number for rent in San Francisco is 11,300+ as of yesterday. Methodology: Go to bottom of ‘Neighborhood’ list and click ‘All’, refresh page, then click map, “Showing X# of 11,300”.

If your retired and/or have recurring medical conditions, moving out of the city to another big city is ok. But moving to the country think twice. A relative moved out of the Bay Area to the country, ten minutes outside of a small city of around 100,000 people. He can get medical appointments with specialist ok, but it is usually a three or four month wait.

He ends up coming to the Bay Area for his specialist appointment’s and all medical procedures.

Boomers Beware!

Paulo , what’s it like up in Vancouver Island?

Some observations from a long term SF renter, four decades, single family homes out in the Avenues mostly.

SF is different. The cost of renting has been about half (or less) the full cost of owning for as long as I can remember. You dont buy condos, TIC’s, apartments in SF. Only hear horror stories.

Less than a third of the housing stock is single family homes but almost half of that is in areas, at least until recently, you did not want to live in due to crime etc. Its down to maybe 20% at the moment. But will go back up again.

The only time home ownership in SF made even the slightest bit of financial sense for me was maybe 1993 to 1996. Maybe. Even if you buy at the bottom and sell at the top two or three bubbles later you still will be lucky to make 3% max net gain. I had a friend do that, I knew all the numbers, he would have made more money investing in safe financial instruments and renting. And thats with the best case scenario in the real world.

All the houses I have rented in the last four decades were negative equity for the owners for at least half the time I rented them. The rent paid not only did not cover the mortgage but property taxes / insurance costs per month were about 60%/70& of the rent paid.

Most condos built in SF in the last two decades are in areas that were very dangerous before Three Strikes was passed in the 1990’s and are getting dangerous once again now that all the criminals have been released by Prop 47/57. Almost all street people are not from SF. Less than 20% have even the most tenuous link with SF.

Aanything built south of Market / Mission, east of Valencia / Mission and North of 16’th / Mariposa is built on swamp / bay fill. It all turned into muddy jello in 1906 and will again when the next Big One hits. We were very lucky in 1989.

So having watched a lot of the the new buildings go up I expect very few outright failures like Kobe 1996/ Mexico City 1985 but I expect a large number to be Red Tagged afterwards due to major structural failures. In SoMa and Mission Bay. And given the odd configuration of the foundations I’d give the Transbay D*lldo Tower (a.k.a Salesforce Tower) at best a 50/50 of not getting Red Tagged. The Leaning Tower is pretty much a certainty for Red Tagging. If the earthquake resonant frequency is just right bits might fall off. Big bits.

As I said, SF is different. This is not Peoria when it comes to real estate.

This crash is just starting and I expect it to be more like the one in the early ’90’s rather than 2000 or 2006. The early ’90’s was the worst recession in California since the 1930’s. This one will be worse. For a start all the GoogleBus people are gone so that’s the biggest rental market demand distortion of the last two decades gone. Which is why clearing rents are already back to 2014 levels and falling fast. It will be 2010 levels soon, which when adjusted for real inflation were about where they were in 1998. At least in the non hipster parts of SF.

TBB, as a native, I agree with everything you said and more. The only thing I disagree with is your claim that 20% of homeless are from the City. The consensis of guys that went to school here, is more like 1% are local. The rest are recent arrivals that are counted as residents, because at one time, they may have briefly paid rent.

My neighborhood, North Beach, was becoming a landlord greed, empty storefront slum before Covid. Now it’s worse. Thank god the family bought a nice house in a great nieghborhood with great schools for their kids–across the bridge. We may all decamp for there if needed. These are weird times that are going to get weirder. Batten down the hatches, there’s a political, economic and public health storm coming.

Wolf, you may find this interesting. Zillow is notorious for underestimating the property taxes when they have the data to make the correct calculation. For example, the condo you mentioned had an effective rate of 1.26% in 2020, almost half of the .67% estimate that Zillow plugged in. With correct rate, the carrying costs on that unit are closer to $6,274/month.