The Debt Slaves are beginning to buckle under their loads.

Consumer and business bankruptcies are rising again, after declining for years since the Financial Crisis. That’s not a propitious sign.

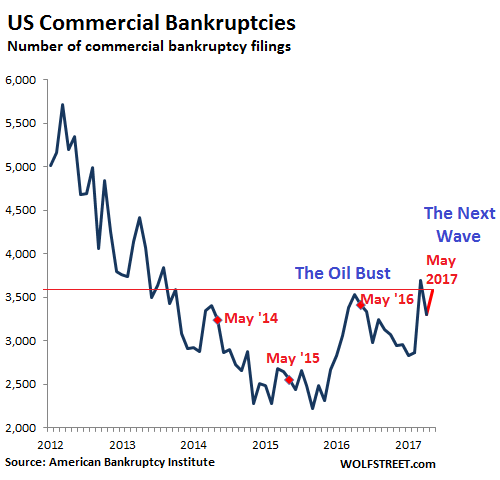

For bankruptcy filings by businesses from large corporations to tiny sole proprietorships, the dance started in November 2015. At first it was the energy bust. But bankruptcies of energy companies have tapered off with new money surging into the oil & gas sector once again. Now bankruptcies in the retail sector are steadily worsening, and other sectors too have picked up the slack.

So here we go again. Total US business bankruptcies in May rose 4.7% year-over-year to 3,572 filings, according to the American Bankruptcy Institute. That’s up 40% from May 2015 and up 10% from May 2014.

And there’s another concern: Bankruptcy filings are highly seasonal. They peak in tax season – March or April – and then fall off. The decline in April after the peak in March was within that seasonal pattern. Over the past years, filings dropped in May. But not this year. This year, they jumped:

The data is not seasonally or otherwise adjusted but is a raw and unvarnished measure of how businesses are faring in this economy.

Commercial bankruptcy filings ballooned during the Financial Crisis and peaked in March 2010 at 9,004. Then, as credit conditions eased, and as cheap money was looking for a place to go and even zombie companies were able to refinance their debts, filings fell sharply. But November 2015 was the turning point when for the first time since March 2010, commercial bankruptcy filings rose year-over-year.

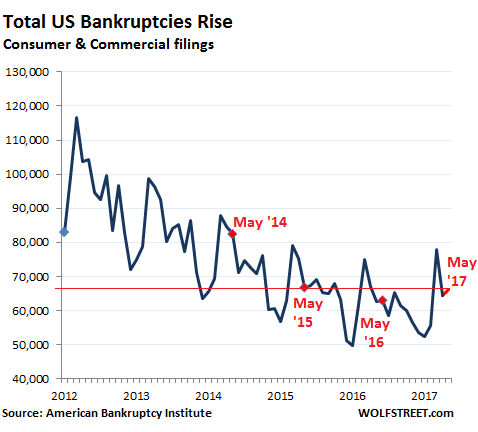

With consumer bankruptcy filings, a similar pattern played out. But the turning point started a year later, in December 2016, when bankruptcy filings rose 4.5% year-over-year. In January they rose 5.4%. It was the first time consumer bankruptcies rose back-to-back since 2010. I called it “an early red flag” that is “highlighted only afterwards, and with hindsight, as the turning point in the consumer’s ability to continue playing this debt-binge game.”

In February, consumer bankruptcy filings fell. In March, filings rose 4% year-over-year to the highest since March 2015, according to the American Bankruptcy Institute. Along seasonal patterns, filings fell in April, but unlike prior seasonal patterns, they rose in May, up 5.4% year-over year and nearly back where they’d been in May 2015:

Total US bankruptcy filings by consumers and businesses in May rose 5.3% year-over-year to 69,668, the highest May since May 2014.

Consumers at risk of seeking bankruptcy protection are those with insurmountable piles of debt and stagnating or declining real incomes, of which there are many.

Mortgages, after home prices have been surging for years, are rarely the cause for filing. When homeowners get in trouble with mortgage payments at this point, they can sell the home and pay off the mortgage. And if they can’t and let the bank have the property, the bank will rarely try to obtain a deficiency judgment against the homeowner in the “full recourse” states where it is allowed. And in non-recourse states, the bank cannot even try.

When it comes to consumer bankruptcies, other forms of debts are the primary drivers: largely student loans, auto loans, and revolving credit such as credit cards. And a big one: debts related to medical treatments, such as emergency room bills.

And there is a lot of this debt. Credit card debt, at $1 trillion, is just one notch below the peak during the Financial Crisis. But auto loan balances outstanding have surged 36% from the pre-crisis peak in 2006 to $1.12 trillion in Q1 2017. And student loan balances outstanding have surged 180% over the same period to $1.44 trillion. This amounts to over $3.5 trillion plus medical debts.

While student loans cannot be discharged in bankruptcy, they can be drivers when other debts are involved and the combined debt burden is simply too large for consumers to carry. And they buckle.

Delinquencies on credit cards, according to the Federal Reserve Board of Governors, have been ticking up from the lows of the first half in 2015. Auto loan delinquencies have been rising too, and in the subprime segment, they have been surging. Student loan delinquencies have been very high and have been underreported for years, it now turns out. So when will the first waves of consumers stumble in their debt binge and head for bankruptcy court to seek protection from creditors? That’s what everyone wanted to know. And now the answers are beginning to emerge.

While hiring in May was, according to LinkedIn data, strong in most of the US, there was an exception: in San Francisco and Silicon Valley where tech skills are suddenly “abundant.” Read… It Starts: Hiring Falls in San Francisco Bay Area, Says LinkedIn

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

– Question: Do you have an estimate how much the impact was of the latest Obamacare insurance premium hike on these bankruptcy figures ?

I don’t think (“think” because I have no figures) insurance premiums are the major component of medical bankruptcies since they’re recurring monthly expenditures. People who cannot afford them will drop them. But I think surprise factors, such as a hospital bill for $100,000 or $1 million (not that hard to do here if you have a major issue), would be the primary cause. That’s why it’s so important to get everyone insured.

Having insurance doesn’t mean you can afford care, it just means that you are paying premiums.

As in some of the lower categories of Obamacare. My doc said they don’t take the bottom 2 plans anymore, apparently not uncommon. Deductibles so high people can’t meet them. And the big cancer centers same way. So you can be paying for insurance that won’t be accepted in many places.

Get everyone insured/covered – and – crack down on medical billing fraud committed by physicians who may be ‘in network’ for obamacare, but also maintain a corporate shell that actually bills ‘out of network’, which sticks the innocent patient with massive bills that would be otherwise be covered and scrutinized by the insurance networks.

anesthesiologists are the biggest offenders, in our experience, and their unethical practices can easily add many thousands of dollars to otherwise manageable medical bills.

Sounds like a great way to generate a lot of complaints about an anesthesia group to the hospital they’re contracted to provide services at. Bad juju all the way around and not a great way to maintain the contract if you’re that group.

Of course, when single payer comes along in a few years, you won’t have to worry about any of this insanity anymore. Then again, when all doctors are paid Medicare/Medicaid rates, there won’t be many doctors around at all.

We have our own business and buy private insurance – premiums have gone up 10-15% a year since Obamacare, whereas prior to Obamacare, it was stable, so very clear relationship. The increases aren’t killing us, but certainly don’t feel great!

The kicker: our plan is actually not compliant with Obamacare, I think because it doesn’t offer free birth control. But of all the plans we looked at, this one was the best value so we said to heck with compliance, plus paying $4 a month for birth control seemed like a worthwhile trade off for an overall better value plan. All the Obamacare plans in the same range as what we are paying offered way less coverage and way higher deductibles!

Crazy that everyone has to have birth control to be compliant. Even if you are a dude or an 85 year old grandmother. Mental health, substance abuse and other things required. To bad govt has to force this and people can’t tailor a plan to their needs.

Most people receiving coverage via Obamacare have subsidized premiums (taxpayers footing the bill). Those receiving health care insurance from employers, pensions or self pay are facing increased premiums, that they are paying for themselves.

Sell in May and go away?

A very good chance it won’t occur this Summer.

Considering the fragility of the credit market, on which everything depends to run smoothly, with no systemic shocks.

There are far too many ‘tells’ recently that have pointed to a shock trend.

Just what eventuality cracks the credit sector is impossible to say, except that something is very close. It will unleash the dreaded vicious circle.

We are due for something big IMO

God I hope so.

I cannot speak for everyone here, but the world credit markets have been egg-shells ever since 2009; they are one “systemic event” away from complete capitulation.

Everyday I wake up, and the first thing I do is grab the phone and check ZH to see if the financial world came to an end overnight.

What constantly surprises me is it hasn’t, and it hasn’t not because or “market fundamentals” (whatever that means anymore) but simply due to central bank and PPT intervention, interest rate suppression and the creation of artificial demand.

Its exhausting. I cannot wait for it to end.

“Everyday I wake up, and the first thing I do is grab the phone and check ZH to see if the financial world came to an end overnight.”

Well Howdy, Haus.

I too used to be a ZH fan. I lurked for years – back when it was really more of a financial news site and featured some really great investigative reporting. You know, back when you had to solve a math problem in order to be able to post to the site.

Then, one day I kinda’ poked fun at them and compared the site to a Drudge Report type of “news/entertainment” outlet. I was banned from the site. So, I learned to find the sites where real financial news and discussion abound. Here I am, and I have learned more without all of the racial bigotry and comments on religious preference.

I posted over *there* under the pseudonym of Iam_Silverman

ZH was good way back there in time.

Some FX traders even used it in their indicator research, for a very short while.

Then it went Perma china doomer.

You can still get good data there in between other stories. But in a land where “fundamentals” no longer matter not sure how helpful it is.

haus T

the markets can NEVER collapse as the central banks can print up the money necessary, in coordination with each other , to plug any hole in the system, the ensuing gradual inflation ( hyperinflation in 1923 Germany was indeed a gradual process) will be sold as “growth and prosperity”…and the sheeple will buy it

I have a small accountancy practice in the UK and for the last three years I have seen my clients making no or small profits but continuing to trade by getting into more debt. I cannot see how things in business can improve and believe that things can only get worse.

Maybe someone can explain to me why things will get better?

If you mean “really get better”, I don’t see how either. But politicians will continue to claim that things are getting better, because that is what they do. The concept of objective truth – or reality, for that matter – has no meaning for them.

They will not get better. We actually have to get to the crash and burn stage and folks are feeling the pain and then we will get real change.

This cant go on and it wont. The laws of mathematics apply to us all, including western governments that are clearly bankrupt.

That is why in the UK, roads are not being repaired, A&E’s are closing down and they run stupid campaigns like, “I’m in” trying to fool citizens to pay twice for their pensions. You will not see that money because they will steal that too. Because of interest rate repression this has caused a 800 billion shortfall in pension here which is a world wide problem that has already started in the US which will bankrupt some states.

Totally agree.

Just curious, what are “A&E” ?

Accident & Emergency. I think they are called Emergency Rooms in North America

Thanks Lloyd

jerry, western government will simply print money (QE) their own debt ad infinitum, cut pensions off the old folks and declare victory

governments and their central bank masters will ALWAYS chose the path of least resistance and pain…to themselves

Thanks for that comment which bears out suspicions I have had for quite some time. Perhaps the fact that the media & governments have been constantly telling people that the good times are just around the corner is part of the problem, which leads to people believing that they just have to hang on for the Boom that used to follow bust. I have lost count of how many times the EZ has supposed to have been fixed & even the so called success stories are blighted by rising poverty at the bottom as with Spain’s high unemployment & 40% child poverty rate.

Austerity measure & debt overload it seems are crushing those whose purchases are the main drivers of an economy. I know a small giftware maunfacturer who uses a simple measure to judge the state of people’s pockets – it is the average amount spent on a wedding gift, which has dropped from around £60 pre crisis to about £ 20.00. My partner ran a ” Cash for Clothes ” business up until the supply dried up in which she knew many who returned often while each time the quality of the clothes diminished. She also had people parking their expensive cars out of sight & being very furtive as they dumped bags of highly expensive designer clothes for what basically amounts as pennies.

Just relatively small anecdotal examples from myself, but alongside retail habits with the growing rise of poundshop high streets & the reported increased market share of the likes of Lidl & Aldi, I think paint a pretty poor picture.

Good luck to you & your clients who are probably also another illustration of the crushing of those who are at the root of a healthy economy,

“making no or small profits but continuing to trade by getting into more debt.”

Do you as a financial professional make it very clear to them how this will end unless behavior changes???

Have you ensured these people have their personal assets insulated and protected from their business activities???

Do you ensure they have debentures and they are lending their companies money not simply injecting capital or increasing shareholdings.??

And if not, why not??

d,

I only let clients trade with limited companies and tell them not to give personal gurantees. I usually create a fixed and floating charges on assets for them.

I generally keep the fixed assets off their company balance sheeets and make sure they have very little cash in the company bank account (seems the way anyway). What I am also finding is that the HMRC (Tax office to non UK readers) are not chasing the arrears of PAYE/NI . I believe that the government has told the HMRC not to pursue these monies because they don’t want liquidations on the statistics and it is better that the company continues that closed and the employees become unemployed and getting benefits.

What most people are not aware is that there are a section of people that I describe as the “Self Unemployed”. these are people that have been regsitered unemployed for more than 6 months at the benfits office. They are advised to start up their own business but keep full state benefits for 6 months. This is beneficial to the unemployed, that doesn’t have the hassle of signing on every two weeks and beneficial to the government that the person is no longer registered as “unemployed” on the basis that they are “not available for work” even though receiving full state benefits and the government can inform the media and sheep that so many people are starting their own businesses. By the way, after the 6 months, you simply inform the government that the business is not viable and go back on as unemployed.

At this point in time i do not see how things can get better.

“At this point in time i do not see how things can get better.”

Because they can’t. The Real Economy is running with the Red Queen: “Now, here, you see, it takes all the running you can do, to keep in the same place. If you want to get somewhere else, you must run at least twice as fast as that!”.

As numerous observers have noted, the Real Economy never really recovered from the Great Recession, which has only been able to pick itself up and get running again, even though CBs have had the pedal to the metal in Emergency Mode ever since. Virtually all gains have gone to the Financial Industrial Complex which parasitizes it, so the Real Economy can never get ahead.

Those PEs that have money on the sidelines, that are planning to buy up cheap assets when the worst happens, are in for a nasty surprise. They presume the Real Economy will recover after the coming crash and they’ll be able to cash in. But they won’t. The next time the Real Economy falls down it will not be able to pick itself up again because it is a Caryatid Who Has Fallen Under Her Stone, weighted down by debt. It will simply continue cratering. The policy of kicking the can down the road has only been possible by accumulating even more debt, and that debt won’t be serviceable either. There’s no way out of the hole.

As I’ve said, the Fed has been able to levitate the asset markets for the last several years even while the real economy continues its decline, and can be expected to continue to do so until the real economy becomes sufficiently tattered and the debts become unserviceable. Given present trends that’s only a few years away at most, but it could be months, or weeks, or days, depending on when the Big Rush for the Tiny Exits begins.

At first it will be ugly, and then it will get weird ugly. To those who have lived in better times it will seem surreal. And since TPTB will not allow debt repudiation and reduction of the FIC to the status of public utilities, it will stay that way. Further, the utter failure to properly account for environmental assets ensures eventual ecological collapse as well, which will guarantee the Real Economy will be permanently unable to recover.

One has to pity the children, knowing they have no future. Their forebears stole it from them, long before they were born.

Concerning “Financial Industrial Complex”

Read this from Forbes 5 years ago >>

https://www.forbes.com/sites/greatspeculations/2012/07/16/beware-the-financial-political-complex/#746903975229

One could say that the Next Recession is already underway.

But that would not be quite correct, because the Great Recession never ended. It’s all the CBs can do to prevent the Real Economy from collapsing into Depression, but that can’t last because they’re piling up the debt to do it.

The smart money has backed away from those ticking noises but don’t seem willing to actually get out of range.

Good article, thanks for finding it. What is never mentioned is the corruption factor. MF Global, run by Jon Corzine simply disappeared with more than a $billion in costomer money. Corzine was scott free. No repercussion because he’s a democratic Loyalist. Pure corruption.

” To those who have lived in better times it will seem surreal.”

To those who lived in the era after 1929, it won’t.

Your last point is the most trenchant. Kids have no future to speak of.

I was lucky to have come of age in the late 60s, when housing, education, and healthcare were still basically cheap affordable commodities.

By heavily involving government and financiers in those 3 areas, all we have accomplished is to make housing, education, and basic healthcare generally unaffordable for the average person.

Declining real incomes resulting from falsified inflation statistics and the destruction of millions of working class jobs through outsourcing and technology have forced tens of millions to live on borrowed ‘money.’

Eventually we will reach a natural limit to debt expansion. At any positive interest rate, increases in debt service costs will eventually consume all available income, and the entire house of cards will collapse, making the depression of the 1930s look like prosperous times.

It may last another couple of decades. Look at Japan’s debt to GDP.

Good article Wolf.

I cashed out all my stock positions last week–locking in a big annual gain! Maybe a bit early, however, I am waiting and watching to take a long volatility position.

Good chance there will be a recession in America within 9 mos. This will cause a recession in Canada and drop Canadian home prices. The deeper the recession the bigger the fall!

My wife, at her insistence and my chagrin, bought stock in manufacturers which produce equipment used for infrastructure construction, e.g. CAT.

After reminding her that I and my lovingly remembered first wife (she died after 53 years of marriage – don’t get me wrong! Love has bloomed anew) had built what we have like the dung beetle, “Slowly, off the land”, I advised her that such equipment would be the best bet, I thought. If no crash – maybe Trump would get his infrastructure program. If a crash, something like Franklin Roosevelt’ s WPA.

So, she has 5K in stock and 5K cash in her brokerage account, cocked and ready (it’s not much of a drag keeping cash there – not much low-risk interest available anywhere else), cocked and ready.

https://www.bloomberg.com/news/features/2017-06-01/the-whistleblower-behind-caterpillar-s-massive-tax-headache-could-make-600-million

My life is going to get a lot better soon I hope Gold and Silver are rallying finally I’m selling off my considerable dollar reserves little by little Sort of like Russia and China are doing

With rates this low, household debt service payments as % of disposable income are actually the lowest its been since the 80’s. Which makes the uptick in bankruptcies all the more concerning. It is if rates continue to rise that the real trouble will start though.

http://thesoundingline.com/what-will-cause-the-next-financial-crisis/

The amount of debt being issued by credit card companies is actually limited due to the financial crisis. As people defaulted throughout the crisis, they lost credit lines and credit scores. The lower credit scores limit how much credit can be given to new customers. There is a push now to increase general credit scores in order to increase limits. This will be the second time they do this since the crash.

At one point after having lost my credit cards, I realized that I could get credit anywhere in Florida, because everybody was in the same boat. I was always open about having lost my home and having bad credit whenever they offered credit. In almost every instance I was told it didn’t matter or they would work with me. We were able to rent houses, buy cars, and get store credit easily, but it was not cheap.

That limit is about to go up: http://www.zerohedge.com/news/2017-05-29/millions-americans-just-got-artificial-boost-their-credit-score

Credit Scores are just not that important near the end of days. The question is more: are you alive? Then we’ll give you credit. Heck if you are dead and nobody knows, we’ll give you credit too and boost your credit score.

If the dead can vote, they can spend too.

Good call Mad Mad in this low interest environment at present we shouldn’t be seeing an increase in bankruptcies. I dread to think what will happen when interest rates do start going up.

So when do I get to buy a cheap beachhouse in San Diego?

Never. But it may be “cheaper.”

:-]

Why would you want to unless you prefer being poor. Rent the ball and chain.

buy in arizona when california breaks off from earthquake arizona will be new ocean front.

Growing up I couldn’t go bankrupt because I had no ‘credit’. I remember applying for ‘credit’ at a major department store. I had a steady job and a decent income but, thankfully, I was declined. I wanted this VCR and video camera that cost $2000 in 1980.

You didn’t get offers from Visa or Mastercard in the mail back then. You ‘earned’ the right to have a major credit card and, for me, that was staying current on a 48 month loan from Toyota on my first new car. Wells Fargo sent me my Visa and Mastercard about midway through that initial loan.

For college ( which was a lot cheaper 40 years ago) my parents paid so I was lucky but I do remember others, not so fortunate, having jobs and or applying for scholarships. Where in the hell did those go to? Wealthy people used to fund them as a way to have their name attached to something if they could not afford to donate a multi million dollar campus building.

Scholarships are still around. One of my daughters went to an upscale east coast college. The four year tab was $252,000. She had a $200,000 academic scholarship funded by a NY hedge fund manager. This has left me somewhat ambivalent about the 0.1%. Her expensive degree did not lead to a good job, even though she’s super smart. She now lives in Ecuador where opportunities are better.

I’d wager that the upscale colleges really only generally hold added value in their networking potential. The majority of higher ups all rubbed shoulders at famous private institutions. If you can get into one for the price of a regular school it’s probably worth. It’s an oversized gamble for most though if you are not abnormally wealthy.

In 1951 my fiance came to visit me in while I was in secondary Army training at Fort Belvoir, VA.

I bought her engagement ring at a jewelers in Alexandria, VA, on credit – got a little book of coupons which I clipped and sent, eventually from the Philippines, each month, until it was paid for.

That was before the days of credit bureaus, etc. and I’m sure the jeweler just wanted to help a serviceman.

But six years later, my wife and I landed back in Arlington VA, where we were to live as I started my career as a patent examiner.

“Honest living paid off”, so to speak. We didn’t have any furniture and needed at least a bed to sleep on, so the credit officer of the local Sears Store (they were big, in those days) let us have the furniture we needed after checking with the Alexandria jeweler.

When I attended Montana State U between 1978 and 1984, the State payed 90% of the tuition for a student carrying a full load. My freshman year I lived on campus and spent ~$1850 dollars for 3 quarters. (Made maybe ~$2000 running a chain saw the summer before school started. So net at the end of a year of school was $150.)

By around 2000 I had donated enough money to the MSU Foundation, that the MSU President at the time and the Head of the Foundation came out to Oregon and bought lunch for myself and my wife. During the conversation we got around to how much school cost at the time, and President Malone, rest his soul, related that the State now paid %10 percent of the tuition and wanted to get to zero. So in 15 years the percentages flipped. With the added burden, that while paying *less* the legislature wanted *more* control of things like curriculum and course content.

I asked him… At what point does this stop becoming a Public institution and become essentially a Private institution?

The Foundation head spoke up and stated that was why they were trying to build an endowment. As I recall, his explanation was that the Public and Private schools had always had a gentlemen’s agreement, that the Public schools would be funded by the government, and the Private schools would build endowments. However… With the changing climate, all bets were off, and the the Public schools were all looking for donors, public/private partnerships and out of state or foriegn students…

To, in my mind, the detriment of the original mission of the school. It was/is a land grant University. Established as an Ag/Eng school for the benefit of the people of the State of Montana…

The use of %ages when analyzing anything

is a specious and misleading , signifying nothing

i.e . if the total crime statistics in my

town go from 1 Break-in to 2 Break-ins,

then I can claim that that crime is up 100%,

a rirdiculous but accurate metric which is

as I said a ” useless measurement analysis”

I admire the accuracy of your reporting except for

your use of percentage comparisons in your articles.

Would you please consider just reporting

the ” bare numbers” instead, and let the reader

draw their own conclusions.

Oh, puh-leeze. It’s that how you make a point? – throw out a bunch of facts and make your readers guess what you’re trying to get at? The purpose of an essay is to try to accomplish something. What you propose is mere flailing.

Sorry.

I’ve drawn my own conclusion and I don’t need fake news operators like you to distort the truth.

The “bare numbers” are all over the place in this article, including in the charts. So you have both, percentages and bare numbers. I can’t figure out why you missed that. The charts are like so in your face.

Here’s something you can divine from the chart for total bankruptcies without doing any math. The lowest points for filings are before Xmas and the highest peaks right after Xmas, in the new year.

One can have fun with statistics.

When my dentist sent his usual CPU-generated “happy birthday” blurb, he got an email back:

“Thanks!

“86 years old, 24 teeth left. 86/24 = 3.583 (3 to infinity) teeth per year.

“The tooth fairy should be pleased …

“Ain’t statistics wonderful?”

The Minimum payment….has a way of catching up to everyone. It will spare no one, even the debt free, when the call due bell is rung.

“It will spare no one, even the debt free, when the call due bell is rung.”

That is an interesting, and alarming viewpoint. I am currently debt-free (totally, house paid off, no loans, etc.), so I would like to know how the fallout from the “Nuclear Financial Implosion” will effect me. It’s always best to know what to look out for.

What keeps me up at night, Thunderstruck, is the possibility of bail ins. All that hard earned money in the bank waiting for the hard times vanishing into banker hands and me now destitute.

“What keeps me up at night, Thunderstruck, is the possibility of bail ins.”

Me too – but only to a point. I preserve some of my “wealth” in having arable farmland with cattle, chickens and goats, a smattering of PM’s and a stockpile of useful tools and hardware for barter.

If the banks/government resort to “bail-ins” as is feared, then they have just signed their death warrants. Nobody will trust banks again for a very long time. That has been proven after the depression in the 30’s. Could you imagine the run on the rest of the “healthy” banks when one institutes a “bail-in”? It would like be a wildfire in the banking industry – uncontrollable. The banks depend on individual trust. Unless mandated by government (a distinct possibility as a way to “fight terrorism”) through direct deposit and debit cards, who would be stupid enough to keep their money in a bank?

Wouldn’t worry about that. If we ever have another financial crisis, the policy response will be to flood the system with as much liquidity as possible. If you own real assets, you’ll be fine as their nominal value will rise to do an accounting of the new money creation. If you’re holding cash in a bank, you’re going to get hosed when the purchasing power of your dollars declines dramatically.

Deflation for any duration will not be tolerated – Bernanke said so. They’ll take your purchasing power, not your dollars.

That sounds nice Mark but housing prices here in the Bay Area fell 36% back in 2007-2012.

The fed is powerless.

So take it out of there and put it somewhere safer.

realist,

Unless you have deposits over the FDIC insured limit or you own stocks or bonds in a bank that is deemed systemically important, you should not be worrying about a possible bail-in. The real threat for most depositors is hyper-inflation, cyber attack, the power grid going down because of an EMP, the U.S getting nuked etc… Not bail-ins.

Thunderstruck,

I agree with you. If there are bank bail-ins that involve a large amount of uninsured deposits then people will not trust banks and there could be bank runs which could affect healthy banks like it did in the Great Depression. However if the bail-in just involved stockholders and bondholders losing money, like we have just seen with Banco Popular, then it should not cause a problem as far as depositor’s trust in the bank.

Mark,

You are correct. The main concern for most people who have money in the bank is that the value of the dollar will decline significantly. Bailouts are more likely to happen than any bail-ins that would involve uninsured deposits.

d,

You are right. If someone is concerned about bail-ins then you should put your money in a safer bank or credit union, or in some real assets like precious metals.

Fed has this under control. They intend to queue up some more QE. Only fly in the ointment seems to be Trump’s rumored intent to nominate some dissenters to open Fed governor slots. But Trump often reverses course.

However the stock market should really shake if the tipped off big shots ever believe the punch bowl is being removed.

I’m surprised you want to fight the Fed. They’ve raised rates and another is coming on June 17. If it doesn’t I will have to rethink my argument.

There may be 3 more bumps coming.

The Fed has also said that far from more QE, it is reversing it. It says it intends to shrink its balance sheet of the 4 trillion QE has cost it by selling the bonds it bought (QE)

If they don’t do what they say they are going to do, that would be unusual.

But if they do proceed as announced, no one can say they weren’t warned.

In the past the Fed has not flinched from pain. Between 1979 and early 1980, it raised rates 4 percent, to 20 percent.

It is also aware that its credibility is on the line, and with even the IMF chiding it for keeping rates too low too long, it doesn’t have much leeway.

The ultra- low bond rates have been a disaster for pension funds.

“The Real Unemployment Number: 102 Million Working Age Americans Do Not Have A Job”

http://www.zerohedge.com/news/2017-06-05/real-unemployment-number-102-million-working-age-americans-do-not-have-job

For many people, working at a job is a choice. My wife prefers to stay home and care for the home and grandkids. Nobody is going to pay her enough to actually go be a wage slave for someone else.

There are plenty of jobs available where I live, but the vast majority don’t pay enough to make a decent life. I think if pay went up, you’d see the available work force expand significantly.

It appears to me that the problem with the economy is that employers cant find a way to pay their employees well, like they did 30 years ago.

“Can’t pay their employees well,” or won’t?

Employers only pay for labor what they are forced to. With the collapse of unionization and the Democrats (the center/left wing of the Money Party, the only political party in this country) completely controlled by the FIRE sector, Capital calls all the shots.

They most certainly “can” pay more (just look at the wealth of the Walton clan, entirely based on paying poverty wages to their employees), but they won’t, unless and until they forced to.

That’s why I was proud to be a Teamster pilot, a Union carpenter, and a Unionized teacher. I have also worked just as much non-union, but was still paid as well or better.

I have a pension for one reason, we negotiated for one by dropping wage rates for pension investments. We still have a sound pension plan because the employer was not allowed to touch it, nor was the Govt. allowed to ‘borrow’ from it. It has never been under-funded. Of course this is Canada where Unions are not a dirty word and people haven’t been brainwashed into thinking they have a 40 hour work week because their employer ‘likes’ them.

All you have to do is advertise for 6 weeks and if no American fills the job, the business is open to hiring foreign workers with no minimum wage requirements.

Come to Duval Street in Key West or South Beach, and see if you can find anyone without an accent, and a heavy debt to the employer for the green card and travel expenses. I suggest the tee-shirt shops first.

The problem is that if the employer pays for health insurance, the cost averages about $10K a year for single employees and $20K for families.

This is a big reason why wages are so abysmal.

“For many people, working at a job is a choice.”

Now there’s a prize. A real whopper that one.

“Nobody is going to pay her enough to actually go be a wage slave for someone else.” What a glorious sentence! I’m going to have to memorize that—I like that.

Your last sentence though…is that sarcasm?!!!!!!!!!!!!!

Hence the need for the Consumer Sentiment surveys – to make sure people are still buying into the FIC propaganda and have no idea how badly off they really are. And how much worse off they soon will be.

Yes, but when you look at the consumer sentiment results by political party, you really have to wonder if those surveys are measuring anything meaningful.

On the contrary, I find the political effects to be particularly meaningful in that they show how people can be motivated by political perceptions, moreso than by the economic realities for which most people lack any real understanding. This is by design, as it is simply more efficient to control the general population with propaganda and guile than by coercion and force.

Many of the 102 million working age Americans who do not have a job are because they are retired, or attend school, or are stay-at-home moms, or they are disabled. Not because they are really unemployed.

They’re counted as unemployed because they’re seeking work and there is none. The economy is a mess.

Job Counter,

The vast majority of retired people, school students, disabled persons and stay-at-home moms are not looking for work nor do they want work. And those people make up most of the 95 million who are “Not In The Labor Force”. They are not counted as being unemployed by the government nor should they.

https://www.bls.gov/opub/btn/volume-4/people-who-are-not-in-the-labor-force-why-arent-they-working.htm

If you do not count retired persons, school students etc…then there are only about 20 to maybe 25 million people in the U.S. that are truly unemployed. Not 102 million.

real data,

75 million of those 102 million that do not have a job is because they are retired, they attend high school or college, they stay at home to take care of a family or they are temporarily or permanently disabled or have an illness.

https://www.bls.gov/opub/btn/volume-4/people-who-are-not-in-the-labor-force-why-arent-they-working.htm

They are not counted as being unemployed nor should they be. The real unemployment number is more like 27 million.

Core logic reports April home price increases biggest west.

http://www.marketwatch.com/story/home-prices-pick-up-steam-as-spring-selling-season-heats-up-corelogic-says-2017-06-06

Those are indices not prices. Very unreliable.

Not a single bullish comment in the lot…… Perhaps a warning for the bears?

Perhaps expand your gamblers perspective to include fundamentals.

Perhaps NOT Arbuthnot whatever the hell that is Got Gold?

Here’s a bullish comment:

The rich haven’t been this well off since 1789 and 1917.

The rich/ poor boohoo narrative won’t get much traction on this site. Nice try though.

It gets plenty of traction on this site. This site is all about the fed and banking cartels of the world ramming down policy that mostly affects the 99 percent of us more than it does the 1%. There’s nothing “boohoo” about it. Just the facts.

Zero traction. The rich boogeyman narrative never works because it’s false.

Primeistoxic, the problem we have today is about the unfair playing field in our economy. Corruption. The government picking winners and losers Trickle down theory. Etc. Don’t confuse compliants about those problems with a free-loading mentality.

With apologies to Doc Watson and Crystal Gayle one could suggest the bear traders’ anthem is ‘Ready For The Times to Get Better.’

Apart from the US $ Index whic I can trade as I am outside the US. most of my othe good trades are and always hav ebeen good trades as it is (Was before QE) easy to pick the bottoms.

The Bottom on $ after QE III was Awesome IGot it perfectly both ways.

Wait. Americans are drowning in debt: https://www.bloomberg.com/news/articles/2017-06-06/trump-s-america-is-facing-a-13-trillion-consumer-debt-hangover

But they are pouring money into constructing and remodeling homes?

https://www.bloomberg.com/news/articles/2017-06-06/these-charts-drill-down-into-the-data-on-u-s-home-construction

How does that compute?

Home equity loans? Mortgage refis with cash-outs? NY Fed prez Dudley is a big advocate of homeowners borrowing against their homes and using them as ATMs, which worked out great last time.

glad you mentioned refi cash outs .

https://mhanson.com/3-28-hanson-cash-refis-surged-2013-16-2003-2006/

How surprising, a member of the banking cartel promoting debt servitude. I am a big advocate of real money rather than debt.

It would be prudent to do just the opposite of what these criminals advocate.

I enjoy being out of debt, even though it makes me an outlaw in a financial system based on debt. I enjoy having a cash stash to get me thru a rainy day, and a precious metal stash (which is the closest thing I know to “real money”) to get me thru a blizzard day. But then I start to wonder.

Using a debit card, credit card, or a loan, I can buy just about anything with very little trouble. This is what the system wants me to do.

Using cash, I can buy things up to a certain cost, above which cash becomes a problem. The system puts limits on cash. Checks can be used for larger purchases but I will be closely scrutinized before one is accepted.

Using a couple silver bars or a gold eagle, I can buy nothing. Nobody will take it. The system does not accept real money.

The banking cartel has a day of reckoning coming. And they will do everything in their power to make sure we all bleed with them.

“Using a couple silver bars or a gold eagle, I can buy nothing. Nobody will take it. The system does not accept real money.”

Then what you need is to get are some “barter goods” A well made shovel, hoe and other manual tools can be exchanged for items others will be willing to let go as they may (at the time) seem to be a luxury and not necessary for day-to-day survival. If you have room to set aside an assortment of building hardware such as nails, screws and other fasteners, those could be quite handy too. One of the best resources to have is a skill or craft. If you are capable of repairing and automobile, building a livable shanty, or trained in the medical profession, you have a powerful barter position.

PM stashes are generally considered a method of preserving “wealth” for when the system has reset itself and we all emerge on the “other side”. After the new exchange medium has been announced, then you should be able to trickle some of the PM’s out to exchange for the new scrip. Keep some powder dry though – first iterations may not be long term in nature.

Where on earth do you live? I live in a small city and there is a gold and silver buyer about half a mile away. I’ve bought and sold small amounts of silver over the years and have always been impressed how close to a ‘perfect’ market it is. (This is not a moral statement it’s an economic term)

The spread between buy and sell is often less than 2 percent. You can buy a hundred bucks worth on Thursday and sell it for more than 95 to the same guy on Friday.

But as money it has to play second fiddle to gold. Gold is money everywhere, and in bar form can be turned into cash for a fee of about one or two percent.

Can you spend it at McDonalds?

No and you can’t spend a thousand dollar bill there either.

So the next time you want to buy something with your gold or silver, ask where the closest buyer is. He won’t be far.

I hope you are never in a catastrophic event like the floods in New Orleans or Baton Rouge. You will find out that nothing works, not the phones, or electric, and your PM dealers will not be open for business. You better have some cash in your pocket to get you through weeks of being disconnected. I’m assuming a catastrophe from which you can eventually recover.

“Using a couple silver bars or a gold eagle, I can buy nothing. Nobody will take it. The system does not accept real money.”

The system you live in or where you shop dosent accept real money.

You need more Asian shop owners.

Shop family down the road will buy me anything at a good price from any where I can pay them in gold or silver bars/coins they them to cash.

Most Motorcycle clubs will also buy gold and silver.

Bankruptcies are actually healthy by getting rid of bad investments. It is the markets corrective action. If anything we don’t have enough of them. But we are all wondering how the “new normal” of world-wide money printing will eventually blow up. Fact is no one knows when and why.

While fully abandoning sound money, one has to admit that the FED has done a good job bailing out the banks, increasing asset prices and keeping wages down. Having learned from the 80’s, official inflation figures have been re-engineered to keep pressure on wages. And, of course, off-shoring high paying manufacturing jobs was key. A true “goldilocks” scenario if you are a banker.

Short-term I expect significant local tax increases as “public pensions” are seriously under water and need to be paid. State budgets are under pressure even though we are now in one of the longest recovery periods ever. Longer-term, $15 or $20 minimum wage and “basic income” for everyone might eventually kick start the inflation spiral. But it could be years in the making.

Here’s a Goldilocks banker scenario you might appreciate. Several cities in Connecticut are close to bankruptcy due to an exodus of hedge funds, GE, insurance companies, and maxed out tax payers.

Some of those hedge fund folks are now in Puerto Rico enjoying all kinds of tax relief, federal, local, and property. I heard yesterday on the financial news there are ads on Puerto Rico buses encouraging people to relocate to Connecticut, because the state provides good benefits to poor people.

My first thought was these guys are short CT bonds and are pushing the state to bankruptcy. My second thought was, it’s too bad we don’t have public executions anymore.

“My first thought was these guys are short CT bonds and are pushing the state to bankruptcy.”

Pure Cloward-Piven strategy. Overthrow the system by overloading it with social spending on the “have-nots” in order to usher in flat pay scales (guaranteed incomes) that favor the looters and punish the produces in society.

In my world, the looters are the ones making all the money.

Petunia, I used to be an analyst for the State of CT. They are prohibited from declaring bankruptcy as are all states. Cities can go broke but not states.

However, their real problems are quite different from the publicly acknowledged ones. Connecticut is the third smallest state in the country, and a startling percentage of it is tax exempt. The list is too long to insert here, but as a for instance, the Mayor of Hartford pointed out that slightly over 50% of Hartford is off the tax rolls, and there are other cities just as bad. To compound the problem, they have 169 towns and cities in a very small geographic area. That is hugely duplicative and expensive. The situation could be fixed, but first, they need to address those problems and few people seem to want to.

The municipalities can bankrupt the state if they need to get bailed out. Whether the state can declare or not is irrelevant, they will become bankrupt. I heard the state is already losing one millionaire family a week.

I lived in Canada province of Québec

I am really surprised that nobody is talking about the ramp and rapid inflation going on right now. Especially in Canada. It is like Canadian have their brains shut down.

Two small chicken packet together. A year ago 10$. Now I saw them for 12%. This is 20% increases. I see this more and more at the grocery store.

Hardware part to fix a window on my house. Last year 13.50$ . Now 14.00$. This is 3.7% price increase within a year.

I am not surprised to see bankruptcies going up.

– Canada imports food from the US. And with the falling CAD/USD I am not surprised to see that the cost of living/food is going through the roof in Canada.

The CAD/USD went from about 1.00 in early 2013 down to about 0.74 today. A drop of some 25%.

Same thing in the U.S. I got a bid for new vinyl siding for a rental house 1 year ago. Decided to wait a year. Price went up 15%.

The commercial bankrupcy chart kind of looks like the gold chart

Truethe thing is are they short term spike’s or TREND’S

In response to several comments above about why there hasn’t been a dramatic implosion of the world’s financial “system,” I’m copying and pasting something from Nuriel Roubini, which my file system tells me is from June 2010.

“… that it is precisely because the downturn has been handled more deftly this time that the impetus for deep, structural reform has faltered. “Had policymakers failed to arrest the crisis, as they failed during the Depression, the calls for reform today would be deafening: there’s nothing like ubiquitous breadlines and 25% unemployment to focus the minds of legislators.”

But, thankfully, policymakers did avoid most of the mistakes of the 1930s and we are where we are. In the circumstances, what the future holds is either full-blown recovery courtesy of the breathing space provided by central banks and finance ministries; another crash preceded by what the late socialist thinker Chris Harman described as “zombie capitalism”; or reform and renewal.

Full recovery would mean that the global economy could continue to prosper even when governments withdraw the support provided by low interest rates, tax cuts and higher public spending. That looks improbable, particularly since there is likely to be a simultaneous tightening of fiscal policy in many countries.

Zombie capitalism is where governments continue to buy up worthless paper from banks, where fundamentally insolvent institutions are kept alive for fear that their failure would cause systemic risk, where every country tries to export its way out of trouble, where the shrinkage of the financial sector depresses growth rates, and where the global imbalances between surplus and deficit countries remain worryingly large. That looks a more likely option.

What, then, are the prospects for reform and renewal? At the very least, this route is likely to be long, hard and strewn with setbacks. It may not be chosen … until there is system failure.”

Bear in mind that in 2008, Hank Paulson was, perhaps, the most ‘reality-based’ of the men and women high-up in the Bush administration. Even if he made no admission of mistake/guilt after letting Lehman go belly up, he recognized the mistake and acted accordingly. Had some doctrinaire ideologue been in his place (or even someone more inwardly vain who refused to recognize his mistake as such), things would have turned out very differently.

HIs successors have continued to demonstrate at least some deftness, certainly much more than dunderheaded responses of officialdom in 1929. People appointed during the Trump admin are more likely to be dunderheads than any other admin since 1928. It remains to be seen when deftness will no longer ‘work,’ and the shape of events when this happens.

Of course, the breadlines do exist today: they are invisible, as people are on welfare, not on the street as in the 1930’s.

And no milling crowds of angry, strong, unemployed industrial workers and miners who can be whipped up by demagogues.

And so, the lid can be kept on things and the truth hidden.

Please can I ask a question being as I’m from the UK.

Do you go to college and then university in the USA? If so if I wanted to go to a standard college and a standard (nothing special) university, roughly on average would that cost me?

Healthcare- same question if I wanted decent healthcare what does that cost the average person.

Unfortunately in England our education system is going down the same route as the USA, in the fact that students leave with huge debts and no promise of a good job.

Healthcare – Whilst everyone complains in the UK about healthcare it’s all covered through deductions from our Pay Check. I get the impression in the USA you guys pay massively for healthcare.

Universities generally have a larger emphasis on graduate degrees than colleges; however, some colleges do have graduate programs. For the most part, though, they’re the same thing. Nearly everyone in the US says “going to college” even if it’s a university. 95% of the population wouldn’t know the difference—it’s not a big deal (*dodges arrows*). I’d say the average cost for most would be about $25000-35000 per year including room and board (two semesters).

A university degree requires four years. In some states like NC you can go to community college for the first two years and then transfer to a university for the last two years. It is a much cheaper approach than going a university al four years but it doesn’t work for all degrees (an example where it doesn’t work is an engineering degree unless you go to a small number of community colleges that offer the option of a 2+2

Engineering degree through a state school). Public universities are

mich lower cost than private schools. Generally the southern state public universities (at least in the past) were cheaper than northern state universities, but I haven’t looked at that in years. I recommend you start looking at state university web sites for

costs. Keep in mind that housing will be a big cost.

A baccalaureate degree requires 4 years (+/-) at college or university.

I think most of WR’s articles point to an inflection point in our current economy . I think most of us agree that this cycle of massive worldwide liquidity injections via central banks has reached the point of diminishing returns. Instead of focusing on the perils of “loose money” , we should divert some attention on the structural/fiscal issues that plague our nation. To name a few : rampant government spending, loss of manufacturing jobs; high current account deficits; rampant cost inflation in health care, education, insurance; and government regulation. I am sure there are many others that could be listed. “loose money” is the only game in town in the absence of solid legislative action and policy.

– Off topic:

Canadian realtor Ross Kay told Howestreet.com that in 2016 the real estate market in Ontario already started to crack. Canadians are so rate sensitive/so deep into debt that a small rate increase already started to push canadians “over the edge” in late 2016.

http://www.howestreet.com/2017/06/05/vancouver-toronto-real-estate-prices-dropping/

(The URL contains a indication on which date the interview was posted.)

The business cycle is not a law of nature. There need be no bust, so long as cheap money flows that allows homeowners the ability to sell their homes at a gain (cash out at a profit) or tap into home equity. If everyone beleives this then it is true.

The economy is thus stimulated and taxes flow to Washington. Not to mention the commerce generated from building homes, upgrading homes, etc.

Why don’t people understand, that so long as cheap money flows homes apprecitate and this man-made cycle need never end? I anticipate an acceleration of this process, as real estate further decouples from the old ‘real economy’. You will see parabolic gains in real estate, ala bitcoin.

It doesn’t matter to the economy where bitcoin goes. But if commercial and residential real estate get too expensive, the entire economic equation falls apart. There is a real limit to how far RE can rise before it causes serious damage to the economy and then self-destructs … this happened time after time.

And its happening again not just in the US.

The majority of the western world has seen its residential property values driven through the roof by speculators.

The next generation either inherit a whole property or rent for life, as at these prices, they simply cannot afford to buy and have any sort of life.

I know a couple who just moved from hong kong to another country and dropped over $ US 150K PA in salary. But guess what they have a better and much healthier lifestyle and can afford to buy a 3 bedroom house.

Kevin

But reflect on this: an average person sees their rent take their wages to a degree that it didn’t before the RE hyper-bubble was blown.

This destroys their discretionary spending, quality of life, hopes of starting a family, and peace of mind.

So, no: it is neither desirable, nor is it -obviously – capable of infinite expansion.

It is a destructive force and an insane way to order an economy and society.

“It is a destructive force and an insane way to order an economy and society.”

Unless you are on the winning side of the equation and do not see or care about the long term effects on society of the equation, which so many are that support it.

Selfish belief in Academic superiority, indifference, and ignorance, joined with corrupt cronyism, can give you a beautiful life, even in a hell hole.

– When things (e.g. real estate) gets too expensive then it will undermine the economy, no matter how much “cheap money” flows through the economy. Because people simply can’t afford those things anymore. Forcing them to cut back on spending. And spending drives an economy.

A good example is what happened here in the US:

1) Between say 1995 and 2006 RE prices doubled (on average), But did US wages double in that same timeframe ? No, they didn’t. (Same story for Canada & Australia after 2008).

2) The price of oil went up from USD 20 in 2001 to over USD 140 in mid 2008, a sevenfold increase.

(US consumers had to swallow the full 100% of that price increase because US consumers have USDs in their wallets. Oilprice inflation was much lower in the Eurozone because in that timeframe the EUR/USD doubled).

Did US wages go up sevenfold in that same timeframe ? No, they didn’t.

Thanks for the replies on college-university fees – so if you’ve not got a wealthy family an average student could be leaving college-uni with a 100k dollar debts plus before they even start looking for a job.

This person then for the next thirty years end up paying this loan off for that amount of time rather than spending his money in the economy.

What I’m trying to say lol is that the economy is generating money but all that money is doing is paying off debt which isn’t great.

The price doesn’t include scholarships or grants. I’d say most are able to knock off 20-30% with scholarships. If they don’t get some sort of scholarship, they really shouldn’t be in college, and we wouldn’t have a huge a problem as we do. Loan repay is generally 10 years, but I think they might be upping this to 15 as costs rise.

As a semi retired Academic ;

1) Scholarships and Grants are not as readily available as you may of been lead to believe .. therefore ..

2) Many talented , gifted and intelligent potential students are unable to receive any sort of scholarship or grant .. with ..

3) Many of those potential students either incurring massive student debt or finding themselves left outside the door

4) The students who should not be seeking degrees beyond HS / Jr College are those with either little academic interest / ability or those preferring the technical hands on / mechanical side of things .. a segment not well served at either the HS / Technical or Jr College level yet a segment we are currently in desperate need of

5) The real problem that comes into play is parents and sometimes the student themselves thinking they HAVE to attend an Ivy League or tier one college / university despite those schools being well out of their price range when in reality a much more affordable smaller local college/university would provide an equal and sometimes better education

Hence once again we have several factors coming into play creating the current student debt debacle .. both from the providers as well as the consumer/students

Which is to say … like everything in life … its complicated .. with over simplification of the matter only serving to propagate myths , conspiracies and fear mongering rather than seeking or offering any real or viable solutions

Most students aren’t attending Ivy League schools (there are, after all, only 8 of them).

The person asking the question specifically said “STANDARD college or STANDARD university”—wasn’t talking about Ivy League.

Our family built our own house (conventional, light-frame construction – not sandbags) 40 years ago. It’s harder these days, to be sure – mostly because ever-so-smart local officialdom says “no”.

my son dropped out of college after that (he was an “A” student) and used the house-building skills he had learned to build a nice little rental housing agglomeration for himself and is now a well off landlord.

Containerised Housing and what is legally classed as a Motor Home negate most “Official Objections”.

Why is it that Japan, despite decades of cheap money, hasn’t blown a housing bubble? What’s fundamentally different about their market? I thought all central banks tried to create asset bubbles?

Can we learn from the Japanese- cheap money without asset bubbles?

http://www.ibtimes.com/five-signs-japans-long-dead-real-estate-market-has-finally-come-back-life-1546719

The BOJ is trying to avoid a giant debt crisis – in addition to trying to inflate asset prices. If it weren’t buying the government’s debt (now at 250% of GDP), and when the government continues to run huge deficits, who would lend the government money?

The BOJ has successfully inflated the largest government bond bubble of all times – with 10-year yield near 0%, in a country that is in terrible fiscal condition!!!

There will never be a debt crisis in Japan. The BOJ will see to it. But it might trigger a currency crisis or other financial mayhem.

– Rising prices create asset bubbles, not central banks.

– Japan had an real estate bubble in the 2nd half of the 1980s. To keep mortgages affordable japanese banks issued in those days 90 year mortgages.

– Japan (Australia & Korea) have benefited from the giant debt bubble in China after 2008. Once that chinese bubble deflates it will take down Korea, Australia & Japan as well.

-Demographic developments in Japan are very unfavourable for japanese real estate.

“-Demographic developments in Japan are very unfavourable for japanese real estate.”

If you are a seller.

Or and underwater owner (and there are still many underwater owners).

“Why is it that Japan, despite decades of cheap money, hasn’t blown a housing bubble?”

?????????????????????????????????????????????????Look back to the early 90’s the Japanese Mother of all land bubbles started to deflate.

Then and has been doing so, since then, and still is. The Major centers Ginza, Central Osaka, and most Major CBD’s have shown a little improvement but across the board general RE values are still going down and have been since 1991. AND NO. Otsidee the main centers it still isnt over.

Japan had and still has a true market correction, (in a very controlled Japanese way) as rural and outer urban properties at the Bottom of the market went down in value and are still quietly and slowly going down 30 years later.

As those owners die there will be another round of devaluation as many properties will have to be disposed of in a deflating market. And estate settlements will find that grandparents had actually been under water for some time.

The Japanese have, and have had for some time, a residential NPL resolution Plan. Wait until they die, then there are no painful bankruptcies and suicides to be loudly blamed on “Predatory Bankers” Etc Etc.

Residential and SME owners who over-borrowed in the 70’s and 80’s. are now leaving in larger numbers annually. Most of them have had time to protect their Beneficiaries, from their debts.

We should remember that all of this debt was created from thin air by those extending the credit, the banksters. Any return on something created from nothing is a profit and asset seizures from bankrupt entities also add to this profit. The only losers are those creditors who do not have a first in line secured interest. If these unsecured creditors also go down the same mechanism applies. If the whole system takes on a debt depression scenario the same operation takes place with the same winners and losers. When the system clears itself the foreclosing entities, the banksters again, will sell the seized assets , including entire nations now privatized, back to investors using the same thin air creation process again. This is a world made for and of hucksters and only the little people worry about the repayment of debt under this ponzi system, or how many times as a prime example has Trump gone bankrupt ?