But condos have issues: “Foreign buyers have played a significant role; it is possible this demand has declined due to political issues here and in China.”

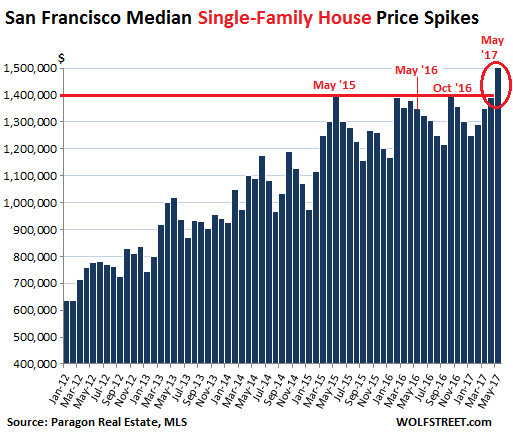

The median sale price of single-family houses in San Francisco had been flat-lining, despite all the monthly volatility, since the spike in May 2015. At the time, it peaked at $1.40 million. In May 2016, it fell 4% to $1.35. The peaks over the next 12 months stayed in that range. But in May 2017, all statistical heck broke loose.

The median house price suddenly spiked by $111,000 from April, by $152,000 or 11% from May 2016, and by $100,000 from the prior peaks in May 2015 and October 2016, to reach just over $1.5 million:

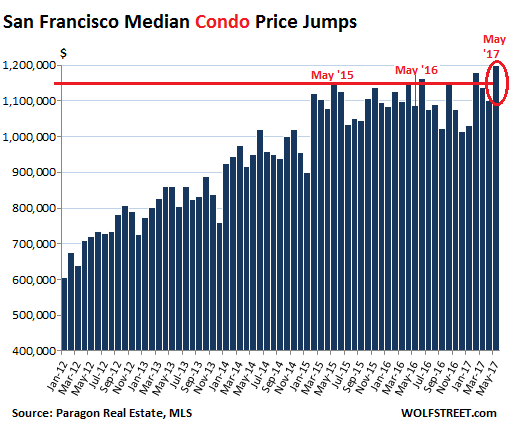

For condos a similar pattern occurred – but there were some complications (which we’ll get to in a moment).

The median condo price had been edging down ever so slightly, interspersed with plunges and spikes, from the May 2015 peak of $1.15 million. In May 2016, it dropped 6% year-over-year to $1.08 million. By April 2017, it was $1.12 million, still below the peak nearly two years earlier.

But according to Paragon Real Estate, which provided this data based on MLS data, the median condo price spiked this May by $100,000 from April, and by $113,000 from May 2016 to a new record high of $1.2 million:

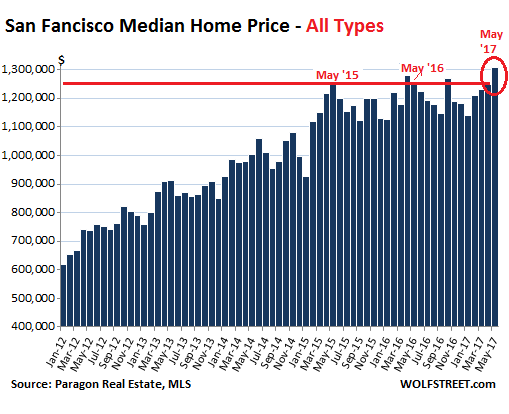

With the median prices of single-family houses and condos combined, a similar picture emerges, of two years of flat-lining but highly volatile prices, and a sudden spike in May 2017:

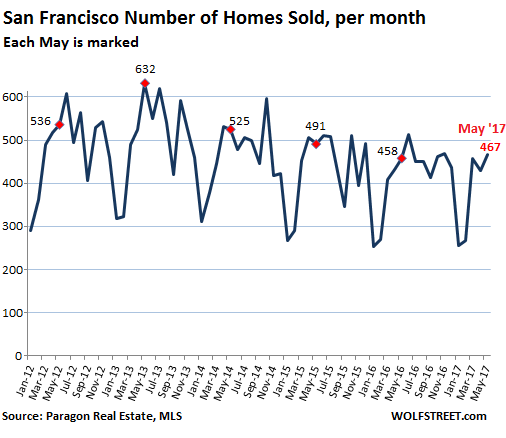

But all the up-and-down drama over the past few years has been happening to a drumbeat of declining sales volume.

In terms of sales volume, May is typically one of the top months of the year. This May, sales volume of all types of homes combined, at 467 sales, was the highest so far this year, as is typical. But compared to other Mays, it was the second lowest over the past five years, with only May 2016 (458 sales) being lower. This trend over the past five years of declining year-over-year volume has also been present during the rest of the year. At the bottom end of the volume scale, this January’s 255 sales were the second lowest, barely ahead of the 253 sales in January 2016. This February’s 267 sales were the lowest since the housing boom began anew in 2012.

This chart shows the trend of declining sales since the volume peak in 2013. Between May 2013 and May 2017, sales volumes have ever so gently plunged 26%:

Patrick Carlisle, Chief Market Analyst at Paragon Real Estate Group had some caveats in his report about these volatile median prices:

We are not that enthusiastic about using monthly median prices, because San Francisco does not have that many sales in any given month (400-550), and they’re divided among four property types in 70-odd neighborhoods with different values.

Note that it is not unusual for median sales price to spike in spring and then decline thereafter as the market starts to cool for summer (i.e. spring median prices do not immediately become the new normal).

Carlisle points out that the house market is “hotter than the condo market, and the more affordable house market (affordable by San Francisco standards, i.e. under $1.5 million) turned into a feeding frenzy this spring.”

While there have been a lot of new residential units coming on the market as a result of a historic construction boom, they’re all condos and apartments. Practically no single-family homes are being built in the city.

The hottest neighborhoods were Sunset, Parkside, and Golden Gate Heights, when measured by “overbidding” – the amount that sales prices exceed final list price. In those areas, the median percentage of sales prices over list prices reached a “stupendous” 22%, Carlisle wrote.

No such luck with condos. Overbidding was generally much lower. And in the neighborhoods where much of the new construction is coming on the market – South Beach and South of Market (SoMa) – the median percentage of overbidding was zero. In Pacific Heights and the Marina the median percentage of overbidding was also zero.

The luxury end of the market had taken somewhat of a beating in late 2015 and in 2016, and though it bounced back some, Carlisle says that it, “generally speaking, is still not quite as strong as it was in spring 2015.” There are more dark clouds for that end of the market:

The biggest change in the luxury home market has been the dramatic drop, almost 50% year over year, in luxury condo sales reported to MLS in the greater South Beach/ SoMa/ Yerba Buena district, even as listing inventory there has hit new highs.

This is the area where large, very expensive, high-rise projects continue to come on market, and, to some degree, they may be cannibalizing MLS sales in the resale market.

And he has a special word about foreign buyers and China:

Foreign buyers have played a significant role here in recent years and it is possible (we do not have hard data) that this demand has declined due to political issues here and in China.

So after nearly two years of sideways movement in the San Francisco housing market, with luxury condos taking a definite hit, there is now a one-month price spike outside the luxury condo market. June or July will kick off the summer doldrums with price declines merely by dint of seasonality. So it will take a while to confirm whether the May spike is taking the craziness to the next level, or if it was a statistical blip. Stay tuned.

While hiring in May was, according to LinkedIn data, strong in most of the US, there was an exception: San Francisco and Silicon Valley, where tech skills are suddenly “abundant.” Read… It Starts: Hiring Falls in San Francisco Bay Area, Says LinkedIn

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It ain’t over till the Chinese rolls over. And since the Chinese are literally holding the Fed by the b*lls, it will truly be a long time till this happens.

1% rise in rates next Fed meeting. Results guaranteed. I know Wolf is against this, but truly everyone needs to sit down and have the banquet of consequences. Better do it now than later.

You seem to be under the delusion that the Fed suddenly decided to become a responsible central bank instead of a criminal private banking cartel. Bilking savers out of interest income and forcing them to play in Wall Street’s rigged casino is too lucrative a racket for the Wall Street-Federal Reserve Looting Syndicate to ever voluntarily give up. Yellen and her flying monkeys will keep up their incessant jawboning about raising rates, but she won’t actually pull the trigger until the bond vigilantes force her hand.

I agree with you, Gershon, and thank you for not incorrectly imputing Keynesian motives to the Fed.

The Fed might have Friedmanian motives, but can’t have Keynesian motives. Keynes knew that central banks have very little ability to directly impact the economy. He was more about fiscal stimulus than monetary. Milton F. on the other hand thought all problems could be solved with the right fed funds rate.

Yes of course its all a giant conspiracy designed to bring the world to its knees as the elite subjugate the masses into outright servitude who of course in their child like innocence played and are playing no part in all this .

Seriously Gershon … wake up and smell the fertilizer . The consumer is as much ( if not more ) to blame for this and every bubble/burst previously …and until you/we/they get that thru their heads .. it’ll just keep happening .

But alternatively … y’all just keep on blame shifting : comforting yourself with a multitude of conspiracy theories in the vain attempt to mitigate your own personal culpability ..

@TJMartin. Agreed. Americans think they can live life without consequence. In fact Goldman Sachs may really be doing God’s work in suppressing these ravenous creatures.

I’m not giving “the masses” or anybody else a free pass for irresponsible behavior like taking on unsound levels of debt to buy overpriced assets. But one reason central bankers and regulators are supposed to be responsible is to prevent “the madness of crowds” from running amok and have checks and balances to prevent economic distortions. The Fed has instead aided and abetted the current manias with its incredibly irresponsible and dangerous monetary policies. These aren’t “conspiracy theories”; these are verifiable facts. The Fed has already caused Tech Bubble 1.0 and Housing Bubble 1.0 with its easy-money policies; now we’re headed for an even bigger bubble implosion that will pose a systematic risk to the US and global financial systems.

Heckova job, Ben & Janet.

Agreed! “Pogo” (Walt Kelly): “We has met the enemy and they is us”.

No Geshon. The bubble wouldn’t happen even at 0% interest rate forever unless the masses jump in. Although you said that you are not giving anyone a free pass, you kinda are by going back to the Fed. It’s a choice. Takes two hands to clap, etc, etc. You said savers are being forced. There’s no forcing, it’s just the path of least resistance.

As I said Goldman Sachs are indeed doing God’s work by putting both the Fed and the masses on their places. That’s the sad part i.e. that statement is actually true.

Oh, I get it now: prey is responsible when predators set a trap for it, and wealth and power dynamics have nothing to do with any of this.

Thanks for clearing that up for me, and providing the comfort of knowing that whatever the Overclass does is OK, since the little people show such a lack of personal responsibility in allowing themselves to be devoured.

The privately owned Federal Reserve which is comprised of individual banks that own shares of each of the twelve Federal Reserve Regional Banks has manipulated the price of capital, it has dramatically increased the money supply since 2008, and it has given trillions of dollars of secret interest free loans to Citigroup and other global financial cartels since then also.

The US Congress has taken a roughly $5T national debt from George W’s inauguration to a $10T debt at Obama’s inauguration, and at Trump’s taking of the White House, it’s at $20T. We will be at $30T by the end of 2026 according to the CBO’s projections.

I reckon that these statements I’ve offered are accepted as truthful.

Yes TJ, you speak the truth regarding personal culpability, and much of the housing bubble was triggered by people who took out mortgages they couldn’t afford. At the same time though, ‘sub-prime liar loans’ were dished out by Wall Street to be bundled up and resold while Wall Street got rich and the ratings agencies falsified the quality of the CDOs.

So here we are in early June 2017, and the San Fransisco median single-family home sale price is $1.5 million! This is six times the price in my city of Minneapolis, and to quote Bill Murray in Stripes, “That’s the fact, Jack!”

@Duke De Guise, did I say that? I said both sides are responsible. “Takes 2 hands to clap”. This country is really funny, I mean there seems to be this magical expectation that people are not responsible for their actions, instead they heap it all to some institution or what have you. When you get rich, it’s all you, but if you get poor, it’s the government, the bankers, etc, etc. Why can’t the explanation be both? But nah, it’s all Red vs Blue, White vs Black, although most of the world is obviously grey.

TJ,

How very noble of you. The neo-liberal economic policies of the last thirty-five years have put continued and increasing downward pressure on the standard of living for the vast majority of citizens. The only way most people can maintain a semblance of their old standard of living (let alone take an illusory stab of improving their standad of living) has been to go into debt. Meanwhile, the lost standard of living of American workers has translated directly into vastly increased wealth for the .01%.

Talk about blame-shifting: yes, it’s obvious the vanishing American middle class has had much greater influence on e\the economic policy that has led to its ruin than the long-suffering heroes of Wall St who run control both parties.

@two beers, wrong again. You said “The only way, etc, etc.” No, that’s not the only way. The other way is you call the neoliberal policy as bullshit and demand changes. Rally your community, etc. Democracy is not just about sitting back and watching TV. People still need to think and take action. Hold the government accountable.

No, the fact of the matter is that some of your so called middle class buddies actually bought into the whole policy because high school is never over and they want to piss on their neighbors and society by joining the Joneses. They just didn’t care or didn’t think through the consequences. Or again they just took the path of least resistance.

This whole thing about having no choices NEEDS to stop. You mean there are no easy choices. No shit Sherlock, life is not a vacation. Evil will ALWAYS exists as long as there are human beings.

1) “Every man is guilty of all the good he did not do.” Voltaire.

2) “The only thing necessary for the triumph of evil is for good men to do nothing.” Edmund Burke

When the fuckup is this big, we are all responsible, although some are more responsible than others.

As a matter of fact, you did say that, by positing false equivalence between trillion-dollar institutions based on wealth extraction and small fish individuals.

@Duke De Guise, I did not. The equivalence is on the consumers as a whole. Anyway we’ll agree to disagree. It’s pointless to argue for someone who thinks there’s no personal responsibility in anything. If that’s the case, the Fed is made up of people too, so they too aren’t responsible since they are just human beings. Let’s abdicate all thinking and morals to institutions, while we small people just party and expect all dreams to be fulfilled. Either way this country is f**ked, glad I have a ticket out of here.

Blaming people and bad decisions is totally valid. And generally I am happy to left people who make bad decisions live with consequences. Sadly if enough people make bad decisions with regards to debt management they can end up hurting us all.

People will not evolve out of making bad herd mentality decisions any time soon, which may one day make them immune to the siren cry of housing mania and speculation.

So until then I lean towards desiring policy to stamp out the ability of people to make stupid decisions.

I’d be surprised if they have guts to administer what would be considered a “monetary shock” = .5 percentage point hike. I think they should. But I doubt they will.

Right on cue, Yellen’s flying monkeys start walking back the rate-hike chatter. Here we go again with Yellen’s played-out “Lucy and the Football” routine, where she’ll mumble incoherent excuses about “the data” not supporting a rate hike until the return of the Messiah or some such thing.

http://www.marketwatch.com/story/kocherlakota-says-fed-shouldnt-hike-rates-in-june-and-it-should-grow-not-cut-the-balance-sheet-2017-06-07

That guy doesn’t even work for the Fed anymore. He’s just trying to stay in the news. You keep listening to the wrong people.

I live here is SF, actually born and raised, hanging on by a tread. In the lower desired places I see Chinese buying up and flippping every house that comes on the Market. ON my block four homes were sold, either by eviction or other means, all the contractors and buyers were Chinese. The contractors lok like old men with years of experience building and construction, the new buyers have slicked hair and drive European sports cars. There is a class distinction between both, regardless the whole block and surrounding communities are either being bought up or flipped out by Chinese. These Chinese are not Chinese Americans but rather from china. The question I ask , are they getting money from us banks at low interest are coming here with the money I. Hand?

Carl, in China if you have connections and want to start up a new manufacturing plant – lets say you are going to make electric can openers, then China will give you money to build a plant and start a business without ever asking for the loan in return. they hire labor at $0.25 an hour for “non connected or billions of people over there”. the catch is that if you make it successful, the People’s repub of China will always own the asset. GET iT? don’t feel bad if you don’t because Steve Jobs didn’t understand that concept when he offshored the I-Phone over there. now they took the iphone design and copied it. Problem is money has no basis of value (no gold / silver standard to stop this behavior) any longer so the central bankers around the world are as corrupt as ever printing cash and handing it to their pals. call it what you want but this is outright wrong. Not just in China – hint hint wink wink… Now we have this shit over here and the politicians are always for sale. think Trump is giving these bums a run for their money because he does not seem to be playing ball like the last bunch. not to say that trump or anyone else can stop what is going on but it is incredible to watch the bought-and-paid for class go nutz when they don’t get their way.

incredible problems across the world. Historians will look back one day and have a lot to say about this subject. unfortun that does not help your circumstance now. just horrible what is happened in California and across the U.S, Canada, and in that case the world.

I would suggest thinking about moving somewhere else because it is going to get a lot worse before it gets better. i can tell you that suburbs in middle america have challenges but worse because industry has evaporated and middle class is no longer middle class. crushed from every side – taxes, cost of living, health care, education…. damn, everyone back in the 80s thought it was tough then. had no idea we would see it this bad now.

Growing ever so tired of the endless nonsense of the housing and tech bubbles.

IMO, recognizing and reporting financial aberrations is’nt “nonsense”…

Is America On the Path To Suicide.

Have you read this article ?

similar reporting on vancouver real estate

maybe people are moving money into what they think are

safe assets . it would be interesting to see if it is foreign money .

http://www.zerohedge.com/news/2017-05-02/vancouver-housing-bubble-back-and-its-almost-bigger-ever

Wow, how stupid are these people and what parallel universe do the reside? What are they going to do when they realize how screwed they are?

Why are they stupid? Perhaps it’s us that are stupid. They probably know that the Fed is going to bail everyone out using OUR money. In some planet somewhere, it’s called stealing, but in planet Earth, it’s called smart and intelligent.

It’s not that there are no intelligent beings out there in the wide universe, but when they look at us i.e. beings who insist that we are intelligent despite evidence to the contrary, they smartly stay away.

Many of these ‘stupid’ people will play the California real estate and tech industry game for a period then move to Austin with half a million or more in wealth to live quite well. One former colleague of mine achieved a $2.2m payout from his efforts. Of course, I have examples of the other extreme. Yet, where else in the world can someone participate in such a lifestyle?

It didn’t work last time when housing prices here in the bay area fell 36%. It won’t work this time either.

Its hardly stupid, it reckless for sure, but not stupid for those sitting at the top. At the end of every crash and bailout their are a lot of losers but there are also a handful of big winners that generally get to shirk any responsibility and keep their money.

I went to my daughter’s soccer game earlier this evening here in Bellevue, WA and most of the parents carry that bubbly glide in their stride. This is a major high tech region, just like the Bay area.

Real estate is off the charts and the Nasdaq is up 21% YTD. Correlation ?

Akiddy – just saw three houses on my street in Woodinville go up on the market this week, and three that got bought within the last 2 years, looks like contractors are working on them busily to flip. Looks like everyone is trying to cash in while they can.

Lived in Lakemont for 11 yrs before relocating to SF East Bay 6 yrs ago. It was the plethora of MSFT opening that used to drive up the housing prices.

Sounds like hellish place to work AMZN took over that title.

Yep feels like 2007, huh?

We have been looking in LA for about 2 years now, and every month feels crazier than the next so at this point we are taking a break. Our current place is ok, we’re willing to wait it out, though we really didn’t think we would be waiting this long.

I would be curious to hear from other Wolfstreet readers who are thinking about buying a house, especially those in areas experiencing price inflation like on the West Coast. Are you getting ready to just go for it? Or going to wait a bit longer? Or planning to move out of state?

MaxDakota,

I guess i’m lucky in that I have no hope of ever buying a home in California ever again unless, A: my income quadruples or B: RE prices crater by 75%.

So i get to just sit back and watch the insanity.

Sold our house in San Francisco (2 unit building) and moved to the Palm Springs area. I retired and partner works from home and flies up to SF twice a month. We were able to buy a nice home in the desert and one in the mountains about an hour from here. The price we got was ridiculous (35% over asking), so it was too tempting not to cash out and opt for a better quality of life.

Northern Virginia here. I’ve been looking for a while but I’ve recently just stopped. Been focused on saving for a health DP when the dip/crash comes here – and it will. No way these houses are worth 4x the rebuild price. The best thing to do is not stress over it and protect your money. I may be an EVIL renter, but I enjoy living debt free and spending quality time with my wife and kids. Remember folks, your retirement is the largest purchase you’ll have in your life – not a house.

I’ve been in Seattle for four years. I thought prices were high back then, so decided to rent, and I’m still renting . There’s now way I’ll be buying at these levels, even though I have the cash. I know my large employer has not raised wages more than 2% per year for four years, yet home prices have gone up 10% per year. At this point, I’d rather move to a different region than take a huge financial risk on an overpriced house. The real crime of it is you can’t even get a decent house here no matter what you pay because inventory is so low. I feel a lot of desperation in the air – people are worried they will be priced out forever, so they have to buy now. I’ll keep my money in CDs until everything settles down and the majority of assets become reasonably priced relative to wages.

I think some people may be driving RE up because they view it as an inflation hedge and they think the Fed is insane enough to implement hyperinflation, then hide it in the stats.

I’ve been waiting in the L.A. market for years and finally threw my hands up a few months back. We’re moving to Las Vegas, already bought a new construction in a really nice neighborhood that would have cost us nearly 3x given the same factors back in SoCal. It’s a few hours drive away when we feel like visiting. Job market there continues to evolve toward more diverse options, not just gaming industry.

I won’t miss the relentless traffic, overcrowding, and wallet grab around every corner which in my opinion overshadows the positives of staying. Wacky home prices are the salt in the wound.

Grew up in SF Valley and lived in Irvine AKA Caucasia (wife hated LA) before moving to Seattle then to SF.

LA is such a shithole – I can’t believe I lived there so long… Dirty, worst traffic, crowded and run amok by ever increasing ILLEGAL aliens who took over the black areas in south central (they got driven out to San Bernadino and Palmdale or something).

I don’t remember where I read this:

“Markets can remain irrational LONGER than you can wait or stay sane”

In other words… you should’ve bought 3-4 years ago if you had the money… but you thought it was too high back then… now you are desperate and are thinking of going in at 40% higher.

Then you keep thinking is ready to pop… and nothing changes, that is some major emotional distress right there.

At this point is just better to buy with 5% down… and if the market goes down just default… but before buy another property at the dip with 20% down… that way you only lose 5% ( this is what I heard from some people here in SFbay area) rather lose 5% down than wait 5 years…

Maybe that is the plan – everybody plans to walk away from the 5% down payment if necessary, leaving taxpayers to hold the bag. Seems like a logical move, especially in non-recourse states. With this in mind, why would any bank be issuing loans with only 5% down? I realize mortgage insurance kicks in, but in a quick downturn the mortgage insurance won’t add up to beans. Why would regulators allow banks to issue such loans with only 5% down, knowing it will require a taxpayer bailout? The government sure seems crooked.

Bought in SF back in 2011 and sold a year ago and renting for the 1st time since I was in college – it was 1 or maybe 2 yr too early.

You see I kicked myself for not selling out back in 2006-7 when just about everyone gloated about the house appreciations…

Yes there are these spikes just before the pop…

RE becomes illiquid when the market turns down sharply and then it’s nearly impossible to sell anything at a price you can survive. Offers, if any, come in at 30% below asking, after you cut your asking price already twice… The time to sell RE is when it’s still hot.

It would be interesting to know what the median level of home equity is in hot markets like SF compared to 30 years ago or even compared to cities like Vancouver or Toronto.

Moreover, wondering if down payments and underwriting standards are similar to the 2002-07 time frame.

After a multi-year price surge, the equity of homeowners that have bought their places years ago can be very high. I saw some numbers on this the other day by neighborhood or zip code (I can’t find the link right now). There is no worry about them even if prices drop a whole bunch. The worry would be about homeowners who bought in the last three or four years or so. Their equity would be wiped out very quickly.

I bought with 40% down in Florida in 2002, it was a rising market that peaked in 2006, when the crash came in 2008 the equity was totally wiped out and then some. We went into foreclose because we were totally underwater. I remember December 2007 was a good month and then the economy just died, total free fall.

I had seen the same kind of housing contraction in NYC in 1987 with house prices. The 1987 stock market mini crash hurt prices for years. I remember a house in my then neighborhood selling in the 500K range sitting on the market for 2-3 years because the owner would not reduce the price.

I’m on the board of an HOA here in the Seattle area. One of the condo owners bought a condo in 2005 for approx $260k with zero down.

This condo owner had his Principal reduced in 2012 to $110k. I believe they took advantage of some FHA or Federal program. He and his wife are seniors who emigrated from Peru just a couple of years prior to buying that condo. Strangely, they also had their property tax reduced from $1850 per year to $250 per year.

They also paid for extensive remodeling on their unit in the last year or so. It looks spectacular. Some people just get lucky, i suppose.

The NYC real estate classified ads (remember them?) in the NY Times were literally filled with foreclosure notices in the late 80’s and early 90’s. I knew it was an opportunity to buy, but didn’t have the funds; those that did made out very, very well.

As someone pointed out recently, real estate in major cities is now a global commodity following global capital flows, so the dynamics have changed from the era when prices were set locally. That said, SF has from its founding been a boom town, with the inevitable busts that follow. Those who are fortunate enough to have good timing will be richly rewarded…

I sold a small place in the Bay Area last year. Every offer was at least 20% down and some were ~30% to avoid being non-conforming. Back in the mid 2000’s it felt like a lot of people were doing 5% down, which meant they didn’t really have as much skin in the game when the market took a dive. Examples.

– 450K condo in mid-2000’s might have only had 23K down.

– 900K condo today might have 300K down

So if the 450K dropped to 375K in the crash, the mortgage holder can just walk without losing much. They might do that because 5% down means a big payment, and rent may not cover the payment. So end result is bank gets a house and mortgage holder is out their 23K + some other tax/charges. If the mortgage holder waits to be evicted for non payment, they might be able to save a chunk of change as well.

If 900K drops to 750K and there is a need to move, the mortgage holder either needs to eat the loss or rent it out. Now if home prices drop uniformly, they would still have 150K in equity and might be able to buy back in elsewhere w/o much damage. All is well if the mortgage holder can keep on working and banks are not too tight with credit. Where it get bad is if banks decide, hmmm I think the house you are selling is only worth 675K, get your buyer to cover the rest in cash. If you add unemployment to that scenario it gets very ugly.

Life is stranger than fiction it seems. I’ve been trying to sell our house (bay area) since last fall and out of the 4 offers we were willing to accept, all fell out of escrow because of the weak condition of buyers. None had more than 3% down payment. We bought it in 2011 thinking we got a deal but at this point we’ll be fortunate to break even. There is no choice because of sick parents back in Wisconsin.

Living in Toronto, and house searching for 2 years now. In spite of what you’ve read, prices in Toronto haven’t subsided. In fact, the listings in the areas we are looking have recently surged by another factor. Seems like sellers are now listing for what they want, plus a bit more, instead of listing low and letting the market bid up the price via multiple offers. A million dollars for homes that were listed at $800K two years ago….unbelievable. All because of ultra-low interest rates.

I see no popping in Toronto, yet And no end in sight.

I live in the bu4bs of Toront and there’s no surge in listings here and the prices haven’t dropped yet. One day they will but not today. Also, the drop could be temporaray. Alot will depend on your time horizon.

It would be strange if RE would fall now on the west coast.

Just consider the following:

Tech stocks at ath and by far the driver in S&P not just NQ.

China pushed the Yuan stronger by raising rates aggressively even though all know in China that they are trying to Curb the Credit growth and later let the currency slide a bit. So any Chinese with half a brain would diversify and buy asset abroad.

The Music can only stop when the liquidity is reversed, that will be the next formidable challenge for the global Central bankers. Any hint of less liquidity in countries like China will IMHO be the last flight of capital from China into Western assets.

A couple of thoughts.

1) All real estate is local now. The handful of booming areas (San Fran, Portland, Denver, Charlotte, Raleigh, etc.) each have their own drivers. Common to most is they are (were) desirable places (climate, activities, culture, etc). Also, there has to be an economic driver. In some cases that is tech industry. In other cities, just well rounded economy (e.g., Denver, Charlotte, etc) plus reasonable cost of living (still).

2) Real estate like financial asset prices are set on the margin. If volume is low, price changes can move up more dramatically. That is the other key thing: Supply is low because most boomers have decided to stay put. That is also one driver for the great remodeling boom going on. I’ve seen it first hand in Charlotte where I live (for two more weeks) and Denver (family).

3) We will close on our house in Charlotte next week. The house sold in less than two weeks and had we asked less it would have gone more quickly. There is short supply of our type of house (well restored, close in, good school district).

4) We are rare among our aging boomer friends in that we made plans to move out of Charlotte to Asheville. Most of our friends will likely stay in their house through retirement. Various reasons for this, the least of which involves financial ability.

5) Charlotte is not being fed by Chinese buyers, but instead by lots of people fleeing midwest and north east. That migration trend will continue for some time and will also help prop prices.

Finally, I don’t think a crash in house prices is in the cards nationallly. It can and probably will hapen in certain cities based on economic issues (e.g., crash in tech?). But prices have likley reached their limit in many places. In Charlotte, I would say that is the case in that we now are seeing lack of buyer ability to pay these prices. So the at some point, the price rise has to stall out. But that doesn’t mean collapse in my opinion. Just a slow sideways.

2)

“Charlotte is not being fed by Chinese buyers, but instead by lots of people fleeing midwest and north east. That migration trend will continue for some time and will also help prop prices.”

Same in WV, only clientele is not looking for an urbane lifestyle.

Real estate is fueled up almost globally because of cheap liquidity

It’d fall globally….for variety of reasons

“All real estate is local! There are no Chinese investors here!”

Keep telling yourself that. The fact is there are Chinese in all areas of the US and the World. It isn’t just a Vancouver or Australia problem, it happens in all communities – mine and yours.

And when the bubble pops, would you support US taxpayer dollars to bail out Chinese investors? I won’t.

Just because you wont support a bail out, it does not mean it won’t happen… Since when your opinion matters when it come to policy in the FED or congress. Besides most homeowners will want a bailout because is in their best interest. Forget the leper renters

Just up the road from where I live in NoVa a 5 bed/3.5bath house sold for $855k in June 2014 just sold for $530k a few days ago.

NoVa is a bedroom community for Federal Govt. employees.

Maybe fewer “new hires” in this administration?

Slower housing sales to follow?

Proposition 13, passed in 1978, has encouraged California residents to move less frequently than they might have otherwise. It’s a little bit like rent control, only for property taxes. For long time homeowners, there is the also issue of huge capital gains taxes to pay (Federal and State).

24 months after one has owned their personal residence they can take a cap gain of $250k tax free. In CA, this was a motivation for me to move on a regular basis. It’s less time if you can show that you moved for employment reasons.

A good example of how government fiscal policy warps the economy.

But I don’t blame you one bit! The fiscal landscape must be taken advantage of as best one can, if one has a practical bone in one’s body.

Can collusion effect home prices on the local level? Here me out here. San Fran is running less than 500 sales a month at peak, so let’s say 5000 sales a year.

Why couldn’t a few hundred bankers, brokers, agents, and flippers buy enough houses from each other over time to purposefully drive up prices and live off the increases?

Suppose Wolf is a banker, and Petunia and I are a couple of brokers. I buy Petunia’s house for $200k over her original purchase price. She can now live on $100k a year for the next 2 years. She buys my house for the same and I now have money to live off. Wolf is living off the fees.

I keep buying and selling at ever increasing prices and Wolf keeps financing them. I’m only having to pay for the increasing mortgages. I see no reason that a few hundred folks “in the know” couldn’t collude to keep prices going up, always living off the increase.

And in a downturn, Wolf, being the bank, could step in and be the strong hand to buy the dip.

It would require a decent sized city with lots of inventory, big local bankers, a relatively small number of sales, and the business ethics America is famous for. I’m sure someone had to figure this out a long time ago.

Kent, you’ve just discovered how the government brought house prices back up over the few years after the housing crash. Few people understand it. Can you guess how it was done?

I’d be interested your view.

Is the price spike related to product mix in terms of more high-end properties?

Yes, it could to some extent. But the big price spike has happened mostly in the “affordable” end, houses now priced around $1.5 million in previously cheaper areas.

The government keeps raising the price of rent, so now I may have the need to plug my nose and buy into an overpriced market, even though it risks my kids college education. Thanks Central Banks. If I do buy and the housing market tanks, will the Fed pay for my kids’ college? If not, the Fed needs to get out of my way.

Buy with minimum down-payment 3.5% or so..

If the housing market tanks,,, just walk away and prove yourself to be smarter..

if not, reap the benefits of appreciation

I am incredulous that in this day and age of data mining, analytics, online public info that can be downloaded into a spreadsheet, there exists seemingly no reliable info on the demand mechanics of the current real estate market.

At a minimum i would like to see the following demand sources by purchase intent for these types of living units:

1.) primary residence ( both bought with domestic and foreign funds

2.) non primary residence ( domestic/foreign funds)

a.) income producing (rental)

b.) second/vacation homes

Until we get this type of reporting we are just ,well ,speculating .

Don’t hold on to any hope… even if the market goes south… Tax payers to the rescue.

KeepYourHomeCalifornia.org

Lot of people would be crying and judges will not foreclose. they’d rather take money from renters to save over-leveraged people.

January 27, 2017: “The iconic San Francisco Victorian that serves as the Tanner family home in the beloved series Full House and its recent reboot, Fuller House, can now be yours. The real-life house, whose exterior is seen in the opening credits of the shows, sold this Summer for $4 million (which is right around where we estimated its worth at earlier this year), and just a month later the new owners have relisted it as a rental property. The price tag? A whopping $14,000 a month!”

San Francisco is in a class all by itself. The city’s houses are being marketed all over the world, especially China. A house in Laurel Heights that sold for 1.6m in Sept. 2014 just sold for 3.5m and I would say about half this neighbourhood is a ghost town. I see only a modest correction of prices for the city in future. Because in many parts of the city housing prices are sustained by foreign cash only and for these people or pools of people, 3 million dollars for a house or 20K a month in rent is small change. Techies you say; who are they? They will all be gentrified out of the most expensive parts of the city and beyond before they collect their unemployment checks when Tech bubble implodes.

I’m intimately familiar with the house in LH you’re talking about. My brother in law represented the seller at the sale and what surprised me was the seller spent $2 mill plus in renovations.

Wow, so nice to live so close to such wealthy aristocracy. I feel some of their greatness is rubbing off on me.

I agree with you but housing bubble has busted many times in the history and in SFO..

Today it may look like this is not gonna stop and this is a new normal.. but it can’ t be for long..

If a neighborhood is a ghost town and not affordable to general public.. then a good place to squatter…

Until everyone stops crying wolf the market in SF will continue to do what it always does, confound the naysayers. I have been listening to the “end is nigh” for 40 years. When I showed up the old timers had told me they had been listening to the same for 50 years. I have long predicted SF would become a city state, something along the lines of the Vatican or a very small Monaco or Lichtenstein. Basically the most valuable property on the planet. Surrounded by water on three sides with some of the world’s best weather for active people. The list of amenities is very long.

Ill believe you when rent prices stop falling.

and SF is on a fault line too. 1906 earthquake?….. there is always a yin to the yang….

I live on the SF peninsula and sold my 1400 sqft condo in early 2015 (got almost 100K over asking, but it’s gone up an extra 200K in the last 2 years to about 1.15). I have been renting a bigger condo since, at slightly below market rates- 4800/mo. Looks like the prices for rentals are decreasing just a tad, but rental homes w postage stamp yards are still mainly about 5-6K/mo., which is outrageous. We could downsize and goto older apartment complexes that have 3b/1bth and are going for the low to mid 3Ks, but they are about 1200 sqft. w no storage, communal washer dryers and outdoor parking or an underground stall for the most part.

I also can’t stand the thought of going into massive debt w increasing prop. taxes for a home that’s 1.4 to 1.7 and between 1600 to 2400 sqft. and built pre-70s. Akk. I feel fairly trapped and my spouse and I would have to both get new jobs to leave. Sucks, but here we are… we will eventually have to move out of here- the sooner the better, sadly. I suppose I should not have sold the condo, but that 2009 housing dip was frightening and left an impression.

When the market turns and prices decline even slowly, liquidity dries up, and it’s very difficult to sell a home for anything near what you want. The time to sell is when the market is hot and rising … you got 100k over asking. In a declining market, your best offer, if any, might have been 300k BELOW asking… and you wouldn’t be able to sell.

Thanks Wolf,

I’m afraid i’m quite a whiner, and even somewhat ashamed of what i wrote, considering that we can almost afford this rent, and based on the crazy amt we got for our home… for doing nothing but being lucky.

Has been a very interesting experience living here. Hard to believe we’re just making it on what would otherwise seem to be an incredible salary level compared to the majority of the rest of the world. –trying to keep it in perspective.