A red flag that’ll be highlighted only afterwards as a turning point.

US bankruptcy filings by consumers rose 5.4% in January, compared to January last year, to 52,421 according to the American Bankruptcy Institute. In December, they’d already risen 4.5% from a year earlier. This was the first time that consumer bankruptcies increased back-to-back since 2010.

However, business bankruptcies began to surge in November 2015 and continued surging on a year-over-year basis in 2016, to reach a full-year total of 37,823 filings, up 26% from the prior year and the highest since 2014. Retailers and companies affiliated with the energy sector, in particular, were sinking deeper into the mire.

Throughout that time, consumer bankruptcy filings continued to decline year-over-year until November 2016. And that was the low point. Then credit stress began to exert its pressure and became apparent in the official channels, when arising number of consumers started throwing in the towel over the past two months to seek protection from creditors in bankruptcy court.

Total bankruptcy filings by consumers and businesses have now also risen year-over-year for two months in a row, for the first time since 2010.

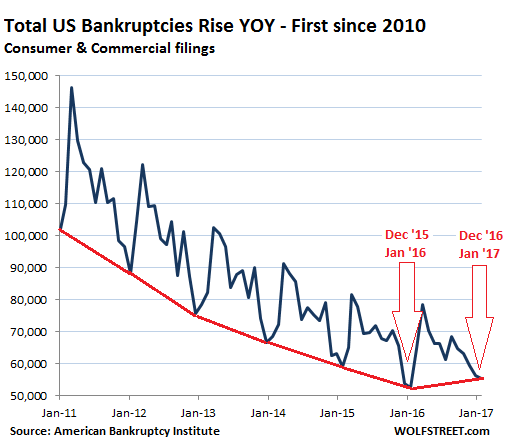

Bankruptcy filings are highly seasonal, reaching their annual lows in December and January. Then they spike into tax season, peak in March, and zigzag lower for the remainder of the year. The data is not seasonally or otherwise adjusted. It’s raw and unvarnished, with large seasonal swings.

The chart below of total US bankruptcy filings shows the drop in filings since the Great Recession through November 2016. The red line denotes the trend of the low points (December, January), and how the trend changed direction over the past two months:

It’s likely that the trend of rising bankruptcies will continue. ABI Executive Director Samuel Gerdano puts it this way: “As interest rates increase and the cost of borrowing rises, more debt-burdened consumers and businesses may seek the financial shelter of bankruptcy.”

In January nationwide, there were on average 2.13 bankruptcy filings per 1,000 people (the per-capita bankruptcy filing rate), with these states at the top of the list:

- Alabama (5.43)

- Tennessee (5.08)

- Georgia (4.30)

- Arkansas (3.44)

- Illinois (3.41)

Here is the irony. According to all major consumer sentiment surveys, economic confidence has soared in December and January. It has been called the “Trump effect.” It was also noted that this new-found economic confidence was divided by party line, and that it had flip-flopped from before the election. The sentiment of the owners of small businesses too has surged since the election. But the economy itself hasn’t changed all that much in two months. Sentiment surveys can be funny that way.

But for a rising number of consumers and businesses, there is a bitter reality: the economy is tough for them, and now there’s the hangover from eight years of ultra-low interest rates: a mountain of debt.

The dizzying borrowing by consumers and businesses that the Fed with its ultra-low interest rates and in its infinite wisdom has purposefully encouraged to fuel economic growth, if any, and to inflate asset prices, has caused debt to pile up. That debt is now eating up cash flows needed for other things, and this is causing pressures, just when interest rates have begun to rise, which will make refinancing this debt more expensive and, for a rising number of consumers and businesses, impossible. And so, the legacy of this binge will haunt the economy – and creditors – for years to come.

But the first year-over-year rises in bankruptcies in December and January since 2010 aren’t signs of an impending collapse of the global financial system or whatever. Rather, it’s an early red flag, among other red flags, of the kind that is ignored until it is too late, and that is highlighted only afterwards, and with hindsight, as the turning point in the consumer’s ability to continue playing this debt-binge game.

Despite what you might think, automakers did not “cut back” on fleet sales. But keep an eye on rideshare companies. Read… Car Sales Crash, But It’s Complicated

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It is crazy. Despite all the conflicting news, the market keeps marching on. Nothing seems to matter anymore.

The market will keep marching on until it doesn’t. Then a great wailing will rise in the land as people realize that there was gambling going on in the casino and no one told them until it was too late.

Ed, your reference to a casino brings to mind the general rule is the less the skill required to play a game, the greater the odds in favor of the casino. Also, at least the statistical odds for a particular casino game are knowable.

Capt. Louis Renault: “I’m shocked that there is gambling in this establishment.”

Waiter: “Sir here are your winnings.”

When central banks keep buying stocks, then it is not that hard to keep the stocks up. After all, printing money for them is far easier than printing a newspaper. For newspaper, you need writers, stories, paper, ink, etc. Central banks can just enter a number into a computer and voila, you have 100 billion dollars to spent.

It’s a tag team effort, too. Deflation fighting over the bottomless globalized pit. If it’s not the Fed it’s their agents, of Bank of Japan, or the Swiss, etc.

I think the gravy train will be coming to an end very soon.

Please enlighten us. Tons of people have made this prediction and some of them had to be carried out in body bags just like how people kept predicting the demise of the Japanese currency.

As long as muppets are still content, things will never change.

Totally agree. I used to think that the economy would have imploded long before now, yet here we are. Still grinding downward but slowly and unevenly. People keep screaming the end is here, the sky is falling. I say not quite yet…

when you can borrow (print) trillions year in year out,that buys lots of time,the rub comes when borrowing tens of trillions produces less and less of a result,like 2008 it works until it doesn’t

Speaking of people beoing carried out in body bags, how is David Stockman’s pay newsletter doing? And his recommendations?

Great question. Stockman sure has seemed quiet since he slid beyond the pay wall.

I too wondered that same thing about Stockman predictions (and Harry Dent) and pay-for-play newsletter. But most likely there would be as positive spin on any Stockman results.

What I see is a slow erosion of the economic foundations like the bankruptcy stats that Wolf states until it completely collapses. But being a complex system the time for that collapse is not predictable, but it will happen. I wait on the sidelines until it does.

he’s got to be proved correct after his followers lose all their money. I think he’s correct about the morality of it. But the skeptics are popguns compared to the money printers.

Quite a ridiculous reply, given that the “muppets” are obviously NOT content. Perhaps you live in an anomalous place, but widespread discontent has been rising sharply in countries throughout the world.

And speaking of body bags, keep playing the “markets” and you’ll be guaranteed to learn just how they feel.

This muppet ain’t content that’s for sure

I would say that only the British Exit counts as some sort of discontent and when I wrote that reply, I was only speaking about Muricans.

LOL at the selection of Trump as a sign of discontent. When he proceeded to put in his Goldman buddies, there’s zero peeps. Where’s the outrage? Instead people only care about his bedroom policies. Truly LOL.

The downfall of Murica is totally deserved.

It used to be tons now its just a trickle!

Trickle down not working for you it works for a couple of people!

Let’s cheer them on?

As soon as the Big 6 Banks figure out how to raise interest rates .. in such a manner .. that the interest rate rises do not touch them .. and then we are all screwed.

It is their self interest that has kept things as they are .. & yes .. it can’t last because they are itching to clean up .. only they don’t know how .. without killing themselves in the process .. yet.

But necessity is the mother of invention. Maybe that is why the Trump administration is so heavily stacked with Goldman Sachs employees .. why it was so important to enact the USA Patriots Act .. to deal with the discontented masses & the Big Bang is just around the corner.

They’d sure like to get that C.D.O. machine cranked up to full speed again. Then we can have a real crash. I’m certain now that they’re getting off the leash the big banks will produce many new ways to fleece the sheep.

Why do the big six need to raise rates and ruin their balance sheet?

The fed holds what was once our money?

The fed could flood markets with its balance sheet and suck everything out any half hour on any day?

The banks are allowing the fed to rip us off for half a percent!

Its working bigly for Goldman as they cover their huge tracks!

I don’t think the numbers are statistically significant yet. It may turn up and it may bounce along.

Clearly the great recession washed out alot of businesses and individuals and that washout has run it’s course for now.

Interest rates will not be going up; however, the big wildcard that could drive more distress is oil prices recovering.

I wonder if that fact that many people who applied for Bankruptcy in 2007 through 2009 are now past the 8 year timeframe where they can declare bankruptcy again. Wash-rinse-repeat?

Prudence 101: Statistics re bankruptcies (personal or corporate) have no direct relevance to those who are debt free.

Amen RD.

As a Saver I have been and am still getting screwed by ZIRP, however, if/when interest rates rise then price of goods will fall to ‘entice’ new buyers. When this occurs, I may buy a different vehicle, although probably will not. Making do and having no debt will always be better than acquiring more ‘stuff’. It is called being able to sleep at night. Besides, I just rebuilt my 30 year old Toyota PU and it looks new. In fact, a little while ago I was flagged down when I was in town by another driver who asked to buy it? Flattering for sure, but my reply was a, “No thanks, I plan to keep it for another 10 years, anyway”.

My neighbour informed me that the average price for today’s Stupor Bowl is $5,000.00. The stadium will certainly be full of rich people who can afford tickets, however, a large number will be people of modest means who put their ‘experience’ on plastic. When stats show over 60% of people can not come up with an emergency $500, and close to 70% can’t pony up $1,000, there is a debt bomb waiting to burst into tears and misery. Nuts.

Sorry… there are about 123 million working people. There are 72,200 seats at this year’so Super Bowl. It is a tiny fraction of the working population that will attend the game, evenot at 5k per seat.

5K to watch a bunch of steroid addicts who can’t spell their names run up and down the field. Yep, put me down for 10 of those tickets as soon as I have the first billion in my account.

The mystery is how idiots like that made money in the first place to not care about paying $5K to watch a stupid game.

AMEN TO THAT

“a large number will be people of modest means who put their ‘experience’ on plastic.”

Or blow their entire Fed Income Tax Earned Income Credit.

Yup! I would be interested in seeing bankruptcy rate among small businesses that had to borrow to get off the ground vs those that were self funded. The day we have to borrow to sustain our business is…never, over my dead body, because then I don’t actually own the business, the lender does!

I am 12 years in a dead end retail position at a big box mass marketer.

The nation can’t afford to keep a bag on their collectivist crouches!

And sagging bigly?

Tennessee tops the list for single family home investors.

The central banks are attempting to force price inflation, when there is no wage inflation. Quite the contrary, the majority of the population is experiencing wage deflation, which translates into shrinking consumer demand.

Speaking of red flags, there were 150 major global corporations that defaulted in 2016. That is 40% more than the previous year 2015. Of those 150 corporations, 75% are domiciled in the US, with 50 being in the oil and gas sectors.

Another very large red flag that slipped in under the radar, was announced late on Friday October 07, 2016 by the IMF, namely that the IMF will eliminate interest rates for low-income countries until the end of 2018. Why? The said low-income countries cannot afford to pay even the interest owed the IMF on their loans!

When you have the five largest companies in the Consumer Discretionary Sector who are contributing the most to gains being:

1/ Amazon

2/ Home Depot

3/ Disney

4/ ComCast

5/ McDonald’s

You KNOW that any meaningful manufacturing capacity, with attendant high wages has truly disappeared. A look at the diminishing employer tax with holdings, tells you the number of jobs are shrinking, along with the pay check size.

Yet, there is extreme consumer complacency! When the wake up comes – it will be rude beyond belief!

I earned three bucks an hour plus tips while in HS at a par time job in 1970 To fill up my VW beetle it cost me around half an hours wages Try to tell me that wages are keeping up

The ability for the city of London to keep the dollar sky high and pound struggling to hold anything against the buck while it sucks every bit of marrow out of our country will be the basis for much study at the London school of economics?

Everyone just has to laugh in his sleeve; its a British thing!

Looking at the chart, it seems bankruptcies are up a bit in the last two months, but compared to past years are still quite low in comparison. It might be a sign of impending doom, but then again it might be an anomaly or might continue along that level for a while.

I agree that the foundations of the system are on shaky ground, have been for a long time, and we are in line for a big correction when the central banks and banking cartels finally can’t keep all the balls in the air with their juggling tricks anymore. But with all their government/regulatory capture and rewriting all rules to their advantage, the banks might be able to go on nearly indefinitely, or at least much longer than you’d think.

I see electing Trump as a huge sign of discontent. Even if he actually does little or nothing to fix issues (and may actually make them worse). He largely ran on a platform of anger which echoed the way many people felt about their lives and communities. He was able to capture a feeling that the other candidates didn’t and so many people responded to him, even when he has a poor record as a business person, has less understanding of government than many high school students and is happy to push cronyism to enrich himself and the pals that sucked up to him along the way. But I’m told we need to “give him a chance” because apparently we can’t judge from the hundreds of actions he’s taken yet. I expect more doubling-down from the true believers until it’s undeniable that their lives haven’t improved under the same wall street masters (and with a special lack of environmental protections and lots of thin skinned butt-hurt whining on Twitter from the Donald anytime anyone parodies him, disagrees with him or challenges the insulated fantasy world his entourage keeps him in).

It costs money to declare bankruptcy. I’ll bet that the iceberg is still out there. If you can get $3K together to declare bankruptcy you are doing much better than most in this economy. If you can afford Greyhound or Amtrak to protest in Washington DC, you are doing much better than the rest of us deplorables.

I can hold two jobs and still have time to comment on the new presidents like!

He needs a hair cut!

The make up of the economy has change so much. I graduated college 2 years ago, I just got off the phone with another guy who was on my senior project team this morning. Off the couple of guys that was on that team, few of them still haven’t found any jobs, some of have a job that only pays 40k a year in a major metro, then you have me and another 2 guys earning over 60k a year, still kind of fresh in the field, and all of us have the same degree from the same school. The wealth disparity is so great now that different kind of jobs have huge pay gaps, and this problem is even worse for older people who didn’t have the skill to adapt to this new economy. I got lucky to have this job because one of my friend who referred me, else I might not even have a gig at this moment.

It’s called “Consumer” bankruptcy, not “Personal” bankruptcy, huh? Is that deliberate labeling, to put the onus on people declaring bankruptcy? I’d wager that overspending on consumer goods at least contributes to more bankruptcies than this HuffPo link indicates, but the triggering event is usually medical expenses. Perhaps they need to be rebranded as “High probable medical personal bankruptcies.”

http://www.huffingtonpost.com/simple-thrifty-living/top-10-reasons-people-go-_b_6887642.html

If the insurance premium alone doesn’t bankrupt you, the co-pays and deductibles surely will.

It’s a distinction between consumer bankruptcy and commercial bankruptcy in this report. A lot of small businesses are set up as sole proprietorship, and when they go bankrupt, it could be considered “personal,” but it is in fact a commercial bankruptcy.

There must be a lot of L.L.C. protected by law…

BAD CHART for the medium term future of the US economy.

Charts like that don’t lie.

Only the positive spinners, interpreting them, do.

Displaying it back to 1990. Would be interesting.

“Charts like that don’t lie.

Only the *positive spinners*, interpreting them, do”

Do you mean something along the lines of “oh look, this is great because it is clearing lots of NPL’s from the books!

or

This trend is creating volume for the subprime markets where they have seen such a marked decline in qualified purchasers since the economy improved so rapidly in the months leading up to the last election.

“Do you mean something along the lines of “oh look, this is great because it is clearing lots of NPL’s from the books!”

In that vein yes.

Small Bankruptcy’s are not good, as a lot of other small people, who should, and need to get paid, DON’T.

I was wondering how many of my fellow Alabamians were living so high on the hog, when the median household income is so low. It appears that many have been buying with old Mr. Credit and now, they can’t make the payments. I wonder how many of these folks are repeat customers.