Oops, they’re already jumping.

In the few days since the election, we got a flavor of what might happen when the bond market sees hues of inflation, expects the Fed to respond, and suddenly (after years of closing its eyes to it) dreads a tsunami of government deficit spending, on top of the flood of deficit spending already washing over the land.

The US government borrowed on average $850 billion per year over the last two fiscal years, in total $1.71 trillion. Very soon, the gross national debt will hit $20 trillion. And with a little help from the next administration’s plans, the annual new debt to be issued by the US government could balloon far beyond $1 trillion a year.

These bonds will have to be sold to someone, but the Fed is no mood of buying; instead, it has been flip-flopping about raising rates.

And the biggest foreign holders of US Treasuries are now net-sellers, according to the Treasury Department’s International Capital Data for September, released today. China dumped another $28.1 billion in Treasuries, bringing its stash down to $1.16 trillion, the lowest since September 2012. Japan, the second largest holder, shed $7.6 brillion, cutting its pile to $1.14 trillion. Saudi Arabia has been selling hand over fist for eight months in a row. Its holdings are now down to $89.4 billion. In total, foreign holders dumped $76.6 billion of Treasuries in September.

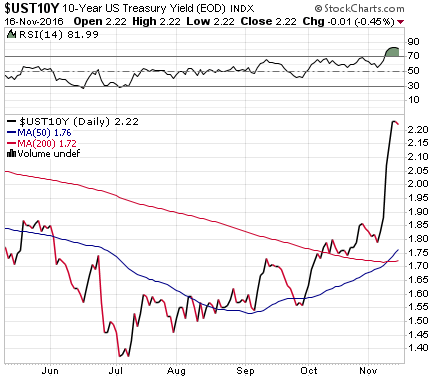

When the election moved Trump’s campaign promises of fiscal stimulus spending a step forward, with buyers scarce and sellers plentiful, Treasury prices, which had been declining since July, fell hard and yields soared. This is the “Trump spike” of the 10-year Treasury yield, including today’s much needed breather – the little hook adorning the spike (chart via StockCharts.com):

Since July, the 10-year yield went from 1.35% to 2.25%, with about half of that journey in the days since the election. And mortgage rates follow Treasury yields.

The Mortgage Bankers Association (MBA) reported today that the average 30-year fixed rate mortgage with conforming loan balances ($417,000 or less) jumped from 3.77% last week to 3.95% this week.

According to Mortgage News Daily, the average 30-year mortgage rate had hit 4.02% on Tuesday, up 0.40 percentage point in three trading days (Friday the bond market was closed). It was the biggest three-day spike in mortgage rates since the Taper Tantrum in the summer of 2013.

And this spike in rates immediately hit demand for mortgages during the week. According to the MBA, mortgage applications dropped 9.2% seasonally adjusted and 10% not seasonally adjusted from the prior week, with refinance activity dropping 11% and purchase activity dropping 6%. The report explained the phenomenon this way:

Following the election, mortgage rates saw their biggest week over week increase since the taper tantrum in June 2013, and reached their highest level since January of this year. Investor expectations of faster growth and higher inflation are driving the jump up in rates….

But it wasn’t just this week. According to the report, rates have increased in four of the past five weeks.

At the same time, government entities are are playing an ever greater role, with the FHA’s share of mortgage applications rising to 12.2% of the total during the week, the VA’s share rising to 12.6%, and the USDA’s share edging down to 0.6%. Combined, their share now exceeds 25% of all mortgage applications. This end of the a market is dominated not by regular banks but by “shadow banks.”

A rate of 4% on a 30-year fixed-rate mortgage two months ago would have seemed unthinkably – nay, ludicrously – high, and those predicting that rate would have been ridiculed. In reality, 4% is still very low. And this is just the beginning, an uptick from historic lows.

But home prices have soared for the past six years, and in many cities have jumped far beyond the crazy peak of the house price bubble that started to implode with such fanfare in 2006. The fuel for these soaring prices was provided by historically low mortgage rates. Home buyers have been able to stretch toward these prices via cheap loans. But suddenly they’re overstretched.

If rates rise one percentage point, for example from 3.5% to 4.5%, the monthly payment for many cash-strapped households moves out of reach. With a $220,000 mortgage, the monthly payment jumps by $127 from $988 to $1,115. This makes life $1,524 per year more expensive. Households that have trouble making ends meet suddenly can’t get there.

In many cities, $220,000 will buy nothing. In San Francisco, it would barely cover the 20% down payment on a median condo, which sets you back over $1.1 million. That 1 percentage point increase in rates would jack up the payment on a $1-million mortgage (median condo, 10% down) by $577 a month, or nearly $7,000 a year!

And 4.5% is still every low!

When mortgage rates fell, home prices soared to fill the gap in payments. But now that rates suddenly are heading sharply north, the housing market, which is already teetering in many cities, is in for a very big rethink.

There’s another side to this equation: Those homebuyers willing and able to stretch to make those higher payments cannot spend this money on other things. And then the entire math is going out of kilt. Falling mortgage rates have been a huge boon to home prices and the entire economy. And that process is going to get reversed.

All kinds of problems are now emerging in the property sector. Read… Whiff of Panic in Miami’s Condo Market

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

My money says they are going to loose control of this thing and we are going back to 18-20% some of us remember those who lost everything last time that happened.

Emphasis on Remember.

d: I was trying to buy a house when those rates were in the 18% plus range. I remember realtors showing us mid-priced properties and they were pushing paying equity and assuming payments at the property owner’s lower mortgage rate. I wonder if that is possible with recent mortgages?

They do to much weird it, with loans in the US. So I couldnt say.

Where we are, big NO, on that one.

Interest rates went from 7 to 18 in a year and I had to sell, as what I could afford at 7 I could not at 18.

I made money but I din not want to sell, it was and still is, a perfectly located, Quality house in a quiet street.

These days all property has to be earning and heavily leveraged, (At least on paper) otherwise you are to vulnerable, to snap state extortion.

Any tax increases get passed on in leasing, which is all I do with property these days.

Residential rentals, got to hard long ago, thanks to socialist administration’s.

Socialist administrations??? You mean socialism for the 1%? Do you mean helping the homeless and the sick afford to live in a”Wall Street Society”? I hope we are a society and not a “everyone for themselves” video game!

I bought my first house when interest rates were 18%. I got a 12 3/4 private mortgage and considered myself lucky. About 3 years later I became a Realtor. Mortgage rates were about 12% but homes were selling like crazy. It was a few years before rates moved into the single digit range. Home prices doubled in 5 years.

I have to laugh when people talk about 4 and 5% rates as high.

I went on to buy more properties at high rates. I cashed out later and made good money.

When rates fall housing prices go up now expect the opposite. People are going to have to lower housing prices in order for people to be able to afford to buy them at a higher interest rate.

Doug, yes house prices will end up coming down.. possibly way down, there are just so many issues with this from underwater sellers to the high cost of building… Trump can not affect all these in a beneficial way. Any trade wars will exacerbate all of them negatively.

If the rates actually did *normalize* back to 4-5% that would not only crash housing but also commercial real estate. That would put lots of people out of work and most likely we’d be right back into 2008 again. OR much worse..

So, rates can not be allowed to *normalize* yet they will because part of the cost of money is risk and someone takes it even if it is hidden. When risk of downside returns to the marketplace OR inflation returns (most likely due to trade wars), rates will have to go up as then even the elites lose and will be all trying to sell at the top.. Which means NO market until a fair price is determined..

All I got to say is it is going to be really interesting.

Ah, yes—remember.

I lived in Eugene Oregon when the Ronald Regan 18% mortgage rate depression hit. Owned a modest home that I had re-roofed, painted, carpeted and added two bedrooms and a bath. The year before the collapse Eugene had been voted the most desirable small city in the USA. Within a year every fourth house in the entire city was for sale. People would walk into their banker’s office, slam the keys down on his desk, load the kids in the back of the Ford and drive to Dallas in hopes of getting an oil boom job.

When I finally was able to sell my house I received $700 net cash, and that only because I sold it myself rather than having to pay a realtor. Four years later the buyer put it on the market again at the same price he’d paid me for it.

Of course things are different this time—.

Actually one of the differences is that un-payable student loans now trump home loans that will be in default as soon as rates revert to the norm. Got to give the Donald credit though— clearing out all the criminal immigrants from the prisons will open up room for all the debtor deadbeats.

Make that the Paul Volker 18% interest rate – inflation was running 20% and Jimmy Carter appointed Paul Volker chairman of the Fed in August 1979 to solve it. He did.

Exactly. In a conversation about interest rates, we need to remember the terms ‘real’ and ‘nominal’ Many of these mortgages were taken out in a time of negative real rates. There aren’t too many projects that don’t make sense when real rates are negative – You get to pay the bank back in monopoly money.

Yes indeed. Do you remember how many farmers committed suicide as the price for those interest rates?

Question: Can anyone please explain to me when China sells US Treasuries who buys the treasuries and how are they paid? Yuan? USD?

What happens to all this debt?

Thank you in advance.

You can sell US Treasury to another buyer at an agreed price, in any agreed currency, just like any stock or bond, or you can redeem them when they mature.

You can not force the US Government to buy them, before the redemption date.

Although the price varies, there is a robust market for treasuries, Or there was before d ump.

I haven’t checked lately, as there has been no Astronomical yield spike, I would say there still is Robust demand for US Notes.

Paul “The Vulture” Stringer Brought Billions of $ worth of Argentine notes for pennies when Argentina defaulted, then held out for a very good profit over time.

More and more Treasury notes from many country’s now have a majority default restructure clause in them, that they did not when stringer brought those particular bond’s.

D,

Thank you.

Much appreciated.

The market is huge for treasuries because they are used as collateral in all kinds of swap deals(usually short term loans) in the markets. They are considered the only security that is a cash equivalent.

I had to look up “majority default restructure clause”, and found

https://en.wikipedia.org/wiki/Collective_action_clause

Interesting.

Thats the one.

Something very similar exists in many country’s, for use in a court ordered bankruptcy restructure. Including ours. I dont like it as I see it being abused by serial offenders..

However it is currently the closest thing to bankruptcy Resolution legislation for a nation state.

Trump intends to use it.

You really think that Trump is going to default on (“restructure”) USG debt? I find that very hard to believe. The consequences would be enormous. The US would turn into Argentina anno 2001. USA asset prices would plunge. The dollar would plunge. Everything would plunge.

Both domestic and international bondholders would lose big, and those binds are supposed to be the safest in the world

Besides, is debt default really an executive decision?

FACT

1 He talked about it. In his campaign.

2 He is a career serial bankrupt.

3 He seems to think he can chapter 11 American, and the world has to accept it.

Which is why America should not have elected him, less than 1/3 of America voted for him.

He did not win the popular vote.

As a percentage, USB 30 year yield is up almost 50% from July, i.e. from about 2.1% to 3%.

The 10 year is up over 60%, i.e. 1.36% to 2.22% since July.

This is what also caused the dollar to rise, contrary to the doom and gloomers some months ago who claimed that countries dumping treasuries would ‘destroy the dollar’. The rising interest rate makes the dollar more attractive relative to other currencies; concomitantly the settlement for Treasuries etc is USD, creating demand for dollars.

What seems to be happening in the last few months is that the Fed is not stepping in to take up any slack if there are not enough private or surrogate buyers, meaning implicit support for a rate increase. Actually, the Fed’s inventory of Treasuries of all maturities has not increased in two years, at about 2.5 Trillion, up from less than 500 billion in 2009.

Bottom line, a little better for savers (if you consider very low single digit better), bad for borrowers. Historically, a 3 percent spread means 2% for savers, 5% mortgages.

They can only sell for dollars and it is suspected that most of those sells are being used for people that are selling the yuan to buy dollars to get their money out of China. Saudi Arabia is selling their treasuries to pay bills because oil no longer is covering them.

The US government (AKA known as the taxpayers) are probably buying a lot of these bonds to keep the market from collapsing. There are mysterious entities in the Bahamas and Brussels that bought many billions of Bonds anonymously.

The fed!

They swap currency (we give them dollars we cancel duration).

Everyone wants out of duration at the same time because of Mr. Ukwho? the curve is getting steep from both ends?

Its transitory and the yield is fat!

Just imagine what happens in Europe when rates really go up. In the Netherlands 1% is now about normal for a 10-year fixed rate and much of Spain (especially new housing developments from the last 10-15 years) is on mortgages of Euribor + 0.5% which is even lower. Still, many people have the maximum mortgage they can afford at those rates, with no down payment. Less than 5% of current Dutch buyers would be able to afford a 10% downpayment on a home with the current prices.

Of course many home owners have some cushion due to quickly rising prices over the last years, but if EU rates go up even 1% it might crash the market. The mantra ‘home prices always go up’ has been true for 35 years in Netherlands (except for a small dip in 2008, the last housing crash was in 1980), just imagine what happens when prices decline for real. Let’s see if the politicians and bureaucrats are stronger than the market …

I check zillow in a couple of places once in awhile and yesterday I noticed that the number of listed properties for sale is really down all over the place.

It’s November, that is why. Seasonal.

For years interest rate repression has been the basis underlying Central Bank policy in Europe,Japan and the US.The idea is simple,take from the savers and give to the consumers.Now those consumers are crying fowl that interest rates have move up 1/2%

TOO BAD ,SO SAD

https://www.youtube.com/watch?v=nzp2d-zoV1U

Higher Interest Rates.

Effect not only mortgages. Flying under the radar are the convulsions taking place in the derivatives sector. Especially those derivatives that are interest rate based. Being on the losing end, or being the bag holder of these financial black holes, is causing much destruction under the seemingly calm surface. The Italian banking sector is beginning to ripple the surface.

Now that China’s ‘horde’ is down to a trillion will people pleeeze stop talking about the dread calamity if China was to unleash this financial H-bomb.

It’s only 5 % of the US debt that’s on the books, it’s a blip compared to the US future liabilities re: social security, medicare etc.

They want their trillion? Just credit their account and debit the Fed’s.

That way maybe they can buy more US stuff- China is major source of GM’s profit.

Lest I be misunderstood, I don’t think creating money endlessly is a good thing but there are times when having the currency your debt is denominated in comes in handy.

Due to ponzi nature of banking there is more dollar denominated debt than there are dollars to pay them. Emerging Markets now have to pay a 10 to 40% premium because of their falling currency values to pay back the debt they took out in dollars. That is going to be just one of the debt bomb that explodes soon.

Yes! China “sells” treasuries to obtain dollars for their banks, but since these treasuries are really just electronic ledgers on a bank sheet, the “dollars” that China gets just disappear into the black hole that is China’s financial system. China does this because the rest of the “surplus” of foreign reserves are also just digital entries on some banks computers, and most of those banks don’t have the ability to pay in anything but more digital entries. The banks owe China, and the rest of the world, more dollars than actually exist!

“The banks owe China, and the rest of the world, more dollars than actually exist!”

The banks owe the world more currency than exists, since the inception of Debenture Notes/Bond’s and fractional reserve banking.

Which in common use is well over 1000 Years ago in Europe,1400 Years ago in china, and over 2300 years ago in Israel.

The first know international default on a bond was Athens, in pre Roman Greece 377 BC. It started one of the many Greek wars which involved Athens.

The British rebellion of AD 60 (App) started when Bodica was whipped by the Romans.

She was whipped, when she tried to prevent the Romans, seizing her property, in lieu of her late husband’s unpaid debts. The Romans had engaged in predatory lending and had “Debenture Bond’s” over the kings assets, they also took hers, as unlike Celtic and more enlightened laws.

Women were not allowed to hold assets under roman law.

How soon? What happens if the Fed were to cut instead of raise?

Let’s hear the big cheer for higher rates. !!! These past give-away rates have distorted not only markets, but social consciousness; Society, itself. Debt? No biggee. Debt just doesn’t cost anything, so why not? Let’s buy that 3,000 sq ft house with all the goodies, we deserve it. Have you ever watched the property shows like House Hunters? My wife does. I just want to climb into the tv and slap those percocious first-time buyers right in the face. Now, I don’t have to. ‘Days of Reckoning’ and new found realism will do it for me.

Plus, savers (like myself) have been screwed for the last decade. I actually wouldn’t mind earning some interest on my term deposits.

As I read this article I was excited about chiming in with my 19% mortgage nightmare on my first house. (d beat me to it). I was 24, with a wife and kids, and got to also watch my job disappear when the market for lumber and logs evaporated with the resulting housing crash. You know what? We did just fine. I worked away and also did carpentry work under-the-table for cash. We did not lose our home. While we lived in town, we had chickens, a large garden, and full woodsheds. We watched what we bought and ate real food (family meals). We did not eat out in restaurants, ever. I made my own wine and beer, and even had a still for awhile. (Party at Paul’s, Friday!!) I followed the example set by my folks who grew up during the Depression. You know the one, the real Great Depression. Not this last 8 year whine fest.

My wife just commented on a commercial she watched on CNN, yesterday. Quicken Loans. It was directed at all those home buyers previously denied mortgage financing. The tone was, ‘you deserve this loan and the opportunity to buy the house of your dreams’. Hah. And it’s not just housing. It’s the car loans, vacations, restaurant dining, clothing, jewelry, and loan consolidiation financing. LOCs.

Insanity.

Realism would be 7-10% mortgage financing and 6% return on saving accounts. (Realistic expectations for our youth.) Maybe people will one day learn to say, “No, we can’t afford it right now”. Or how about these two gems? “Let’s save up for it, and if we still want to, we’ll__________”. Or, “Let’s just stay home tonight and go for a walk after supper”.

“Let’s stay home and referee the kid’s fight”.

Egads, the kids might have to put their electronics down for 1/2 hour!!

Yes, it will change…..everything. And what is wrong with that? Maybe the result will be maturity of outlook and respect for the fine life possible and attainable on a budget. The country cannot afford indebtedness, any country, and neither can individuals.

Couldn’t agree more, it’s exactly the same over here in Netherlands. And it doesn’t only distort financial markets and social values, it also leads to massive distortions for investments in the real economy for which we will pay dearly for many years to come. Many small companies with useful services or products went out of business while big companies with unprofitable business models and useless services kept growing.

All this free money is feeding the cancer in society. One can only hope that it isn’t too late for treatment but I’m not optimistic; especially for Europe where savers have been punished right from the start of the Euro in 2002 and higher rates seem totally out of the question for many more years.

Personally I wouldn’t mind see the financial buccaneers who have been raiding my savings for the past eight years keelhauled through the barnacles of double digit interest rates.

MC, aye, aye Capt. Bligh.

After Housing Bubble 2. a temporary crash followed by Housing Bubble 3.

It’s obvious. Housing will be the second pillar of Making America Great Again.

You are probably quite right, notsosure. With the price drop it may be an excellent time to pick up some rentals. Although, if the change is a more long-term restructuring on a great unwind, a speculator might just be stranded watching the tide go out.

I have some property across the road. 16 acres. I was thinking of picking up a small cabin and getting it set up as a rental. Or, I might just build something. I am thinking of around 600-700 sq feet. I am a carpenter so it is fairly straight forward to do, plus we live rural without all the snoopy inspectors and by-laws. People will need places to live, and this would be very affordable for someone.

Can any one explain to me why high yield bond index like HYG is close to its 52 week high even though interest rates are going up significantly!

So far, the spike in rates is mostly visible in Treasuries, mortgages, and other low-yielding paper. Junk bond yields have gone up too, and spreads have widened a notch, but only in relatively small increments. They’d plunged since February to super-low levels, with NIRP refugees from Europe and Japan chasing yields wherever they could find them, and some of that is still going on.

Thanks Wolf for the clarification.

Your site is very educational!

My bet is this inflation scare will be temporary. Real inflation requires increasing wages and a lack of manufacturing capacity. China and India still have hundreds of millions of laborers who haven’t come on-line and China has enough manufacturing capacity for two planets. And there are no great drivers of new growth out there.

We’ll get through a happy Christmas season, and start a new year with treasuries headed back up. We will learn that the Donald still has to face an austerity loving Congress. Now is the time to buy bonds.

regarding: “We will learn that the Donald still has to face an austerity loving Congress.”

Maybe not. He might cow them to his will. Rats will always take a quick feed given the opportunity. Even poison. It will be funny watching former non-supporters try and ingratiate themselves into his power orbit. They have no pride or boundaries when power and money is in the offing.

I did enjoy watch Chisti Creme get the old heave ho. He might have to move to Ft Lee! His days are numbered in the Governor’s mansion. Hmmm, maybe he’ll need to rent.

It’s all speculation at this point. If the gov does not deliver on a huge spending program, back down it all goes. With higher 10 year rates, The DXY is headed up even more and thus will not bode well for exports while the gov is making up its mind. Not to mention that as the rates rise, the cost to maintain the new debt goes right up with it.

Here we go, DXY just hit 101.3

“Real inflation requires increasing wages and a lack of manufacturing capacity. ”

Not what I see, if the government is involved (like with mandatory healthcare, education, energy, the housing market and almost anything you need) you can have surging prices even if wages are not increasing and there is sufficient supply for everyone.

In my country, only stuff like food isn’t really more expensive than 10-15 years ago, but only if you disregard the huge decline in quality for many products. If you want quality food (especially fresh product) prices are up at least 100% compared to 10 years ago, just rents, healthcare insurance premiums, etc. Energy bills haven’t increased much either, but due to global warming (far lower heating requirements) they should have been much lower then they are now. Even electronics have stopped going down in price over the last few years and although specs are sometimes better, general quality (product lifetime) and service often is worse that it was.

IMHO inflation is around 10% yoy, over here in Europe but probably not much different in the US. Maybe even worse if you spend your money on trophy art / RE, supercars and superyachts ;-)

The US economy is largely a service economy. CPI for services has been running at around 3%, while goods inflation is a lot lower. So for inflation to race higher, the prices of services such as health care and many others need to rise. And that may well be in the cards.

” Real inflation requires increasing wages and a lack of manufacturing capacity. ”

You need to research “Stagflation”.

Stagflation in the ’70’s was the result of a sudden spike in fuel prices, causing a recession, and a highly unionized work force which could demand pay increases based on inflation actually causing inflation.

That is not the case today. The US worker has no bargaining power.

You can also get rising prices, rising coasts, and stagnant wages in a stagflation cycle.

which is much more likely and not far from what the many parts of the real world have today.

Governments have manipulated and abused the financial measures of our society’s, so badly that black effectively becomes white.

There is no inflation if you take the things that are increasing in price out of the equation.

,

Property values/taxes and rents have all gone up they are major drivers of inflation, outsider the measures of inflation in the economy. Hitting hardest the middel lower income stratas that can not pass them on.

Paulo,

My view is quite contrary to yours. The collapse previously initiated in 2007 will resume.

I don’t disagree with you, Michael. I just don’t know anymore having been fooled so many times. If anyone had told me ZIRP would have lasted so long without everything going bonkers I would never have believed them.

I’ll bet we do agree that stability is what people crave as much as anything. There is just so much unknown and uncharted going on right now. How does one plan for the future in the midst of all this?

For ten years and counting every Monday this is the week!

Rates will never be this low and price? Never will you get so much for so little! Your a veteran? Special pricing and terms apply! You must hurry!

Starting in 2005 and during the Beijing Olympics build out, interest rates were raised 17 times 25 basis points each time.

Do You believe in the rhyming of history postulate?

Does the fed have more room this time to raise 35x or must it get ahead of the curve and do the same in 9 rate increases?

The Fed needs to back up rates to sell down the balance sheet and cares little about going above its 2% target?

9 times destroys the economy 35x destroys feds credibility!

Jim brown quit at the peak of his career

Chair yellen should also enjoy putting together a pristine legacy and step down after having a moment of clarity.

There is nothing more she could do but step aside for the new alpha male fed figurehead!

One of those have lunch with persona’s. Thank you chair Yellen.

There’s a chance that rising mortgage rates will cause a jump in home sales as fence sitters will take action to avoid getting a higher rate. But if the rate rise is sustained, the prices will gave adjust down. I’m hearing a lot of new talk in the RE industry about creating more ” no down payment” mortgages. The timing is pretty good.

biggest white shoe ripoff ever?

J.Dimon gives Mr. DJ a billion dollar consideration and that long shot breaks the bank

Trickle down for x-mas! Two bad Ron and Nancy can’t be here!

Here in spirit (cocktails)

um, what happens when you run out of medicine and the patient is still sick?

Soooo… Will the housing market be cheaper/ more affordable in 2017?

Depends where you’re talking… and you’d also need a crystal ball.

In theory, if rates go up prices should go down, but the correlation is not so direct in reality. There have been periods of rising rates and rising home prices.

“They can only sell for dollars”

You can sell T’s in what ever you agree to accept from the Buyer.

DPRK buys them with Meth or Heroine.

So if want to buy house now and plan to sell in 3 years is this a good time to do it? Or i should wait and watch for another 3 4 months.

“These bonds will have to be sold to someone”

I don’t see what the problem is. US bonds at higher yields will be gobbled up like candy. It’s a yield starved world

and the USA is the reserve currency. Europe is coming apart at the seams, China is all smoke and mirrors and Japan wants a weaker currency.

So far this yield spike is ‘all in the head’, god knows if the CIA doesn’t off Trump before he takes the oath. Trump is a paper tiger until he proves otherwise. I assume he’s tougher than most politicians as he’s had to fight it out in the real world to get his props.

The other way around… it takes higher yields in order for these bonds to get “gobbled up.” That is, sellers must cut their price. You can no longer sell these bonds at the price you got last week.

So if you bought a 1.2million dollar house a few years back with a low rate fix 30 year mortgage. Even through your mortgage payments will be constant, your investment, the house, will come down in prices as mortgage rate go up. Result, you are underwater. Right?

Yeah, I second @Shawn’s Question. What does happen to those who have a 30 year fixed loan @ 900K in an auterity climate? Also, this may be foolish, but is anyone concerned about runs on banks and/ or the US taking extreme austerity measures and reaching into citizens bank accounts? Thanks for at least reading this and hearing me out in advance. I Wish everyone well here. :)

Sounds really bad for the SF TIC market, those fractional loans are all ARM. Why would anyone want to be holding or buying these in a rising rate environment?

Because of this and other reasons, TICs are hard to sell … and therefore cheaper than condos. That’s why they sell at all.