AI Dominated the Fed’s Meeting as Driver of “Persistent Inflationary Pressures” & Demand Growth.

By Wolf Richter for WOLF STREET.

“AI” was mentioned 21 times in the minutes of the FOMC meeting on June 16-17, released today – up from 8 mentions in the minutes of the prior FOMC meeting in April – in these combinations:

- “AI buildout” (4 times) and “AI infrastructure” (2 times)

- “AI-related investments” (3 times), “AI business investment,” “AI investment,” “AI-related capital spending,” “AI-related expenditures”

- “AI adoption” (2 times)

- “AI implications for corporate profitability”

- “AI-related price pressures”

- “AI-related demand”

- “Optimism about AI.”

Plus:

“Some participants commented on the possibility that AI could, over time, affect employment prospects for some classes of workers.”

“Strong corporate earnings and continued investor optimism related to AI contributed to increases in foreign equity prices.

The AI investment mania is now officially a force that is driving demand and pushing up consumer prices including electricity and tech products, stock prices, and input costs for companies that they would then try to pass on. And that is now.

But the hoped-for productivity gains and deflationary pressures from AI were deemed uncertain and in the future:

“Some participants remarked that productivity gains associated with AI adoption would eventually reduce production costs and increase aggregate supply, which should put downward pressure on inflation, though they noted this effect would likely take time to materialize.”

And:

“Some participants suggested that those [AI] investments would likely increase the growth of productivity and of potential output in the coming years. These participants remarked, however, that considerable uncertainty remained regarding both the timing and magnitude of potential productivity gains, which were expected to lag the ongoing boost of AI adoption on demand.”

By contrast, the other two Fed bogymen, “energy” as a result of the war in Iran and “tariffs” were mentioned only 13 and 7 times respectively in the minutes today.

“Electricity” was mentioned once, but in the context of AI driving up electricity prices, along with prices of tech products, thereby pushing inflation higher:

“Many participants noted that ongoing strong demand for AI infrastructure would likely sustain upward pressure on prices for technology products and electricity.”

Here are some of the other mentions:

“Many participants noted that ongoing strong demand for AI infrastructure would likely sustain upward pressure on prices for technology products and electricity.”

“Most participants, however, also pointed to scenarios in which, in the context of stable labor market conditions, inflation would remain elevated due to strong AI-related demand, the conflict in the Middle East, or the effects of tariffs.”

“Most participants remarked that growth in economic activity that exceeded that of potential output, owing in part to strong AI business investment, could contribute to more persistent inflationary pressures.”

“Some participants noted that broad financial conditions were supporting demand. These participants pointed specifically to high equity prices and noted that those prices had been driven by strong corporate earnings and optimism about AI.”

“Participants generally expected solid real GDP growth to continue throughout the remainder of the year and pointed to several factors likely to support continued expansion, including ongoing AI-related investment, household spending, and fiscal policy.”

The AI investment mania – the hundreds of billions of dollars that investors are eager to cough up and that are getting thrown around left and right – and the demand and inflationary pressures that those hundreds of billions of dollars generate, have begun to percolate through the economy. And the Fed has begun to fret about the effects.

It is refreshing that the Fed is taking this threat to price stability seriously, rather than trying to “look through” these pressures from the AI investment mania and wait for them to go away on their own somehow, while those pressures could be fueling the second wave of inflation.

So there was a pivot at the Fed at the June FOMC meeting, as per today’s meeting minutes: The discussion was about whether to raise rates, with “a few” participants even acknowledging that “there was a case” for hiking at the June meeting.

By contrast, at the meetings last year and earlier this year, the discussion was about whether to cut rates – and the Fed did cut rates three times last fall.

It is rare that the Fed does a one-and-done rate hike. Most often, a rate hike means a new hiking cycle to get inflation under control.

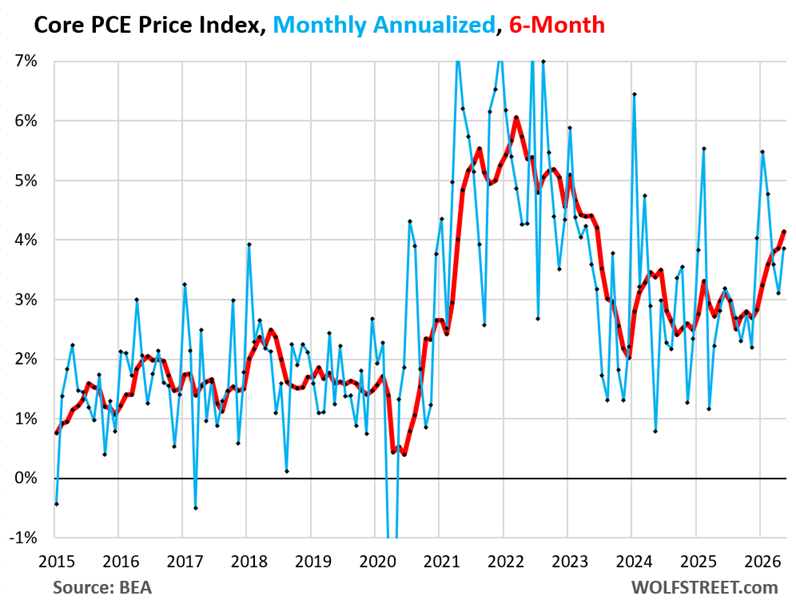

Core inflation measures and overall inflation measures have been above the Fed’s target for over five years. The Fed-favored core PCE price index, which excludes energy and food, has been accelerating since mid-2025 and hit 3.4% in May. The PCE price index was released two weeks after the Fed meeting, and participants had only estimates of it, not the actual data.

The six-month core PCE price index, which shows the current trend, accelerated to 4.1% annualized, the worst in three years, and this does not include the spiking energy components. Big drivers were non-housing core services, electricity, and tech products.

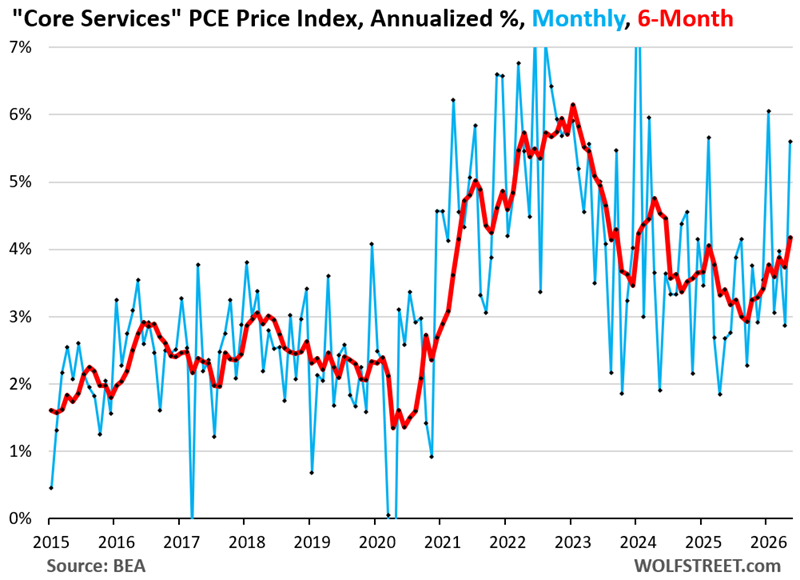

The six-month core services PCE price index, the big driver behind the core PCE price index, has been accelerating since mid-2025 and hit 4.2% in May. Core services dominate consumer spending. And this time, it’s the non-housing services that are making the noise. If electricity were included in core services, it would look even worse:

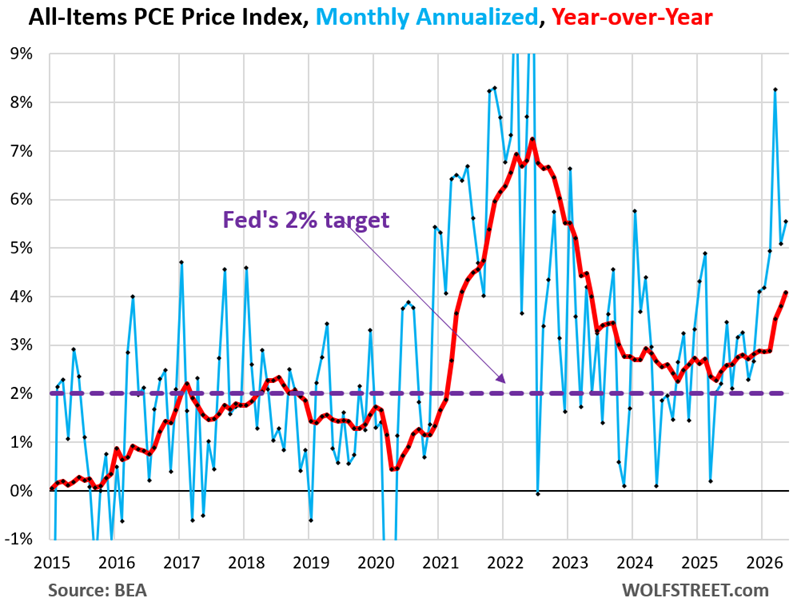

The all-items PCE price index, on which the Fed’s 2% target is based, has been above the Fed’s 2% target since March 2020, for over five years, and now the assumption is spreading, including right here, that the Fed’s de-facto target has been tacitly moved to the 3-4% range, and 2% is just copy-and-paste lip service.

If the Fed wants to stamp out that assumption, it will have to get busy. If it dillydallies around and looks through this inflation, it would be proof that the Fed actually moved the de-factor target to the 3-4% range, and Warsh might as well come out and say it and thereby let long-term Treasury yields and mortgage rates, which are still clinging to the 2% illusion, fly off the handle.

In case you missed it: Consumers Are already Getting the Drift, “Inflation Expectations” Throw the Fed another Curveball.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

What I’ve heard recently is that in the short run, the high demand for chips for AI uses is still causing their prices to go up – heard something yesterday on the radio like Samsung is boosting those prices by 20% for the short term. But in the longer term, those chips will become commoditized and much cheaper. Demand will likely drop at some point too. Coupled with the hype fading somewhat, and the doubts of longterm ROI cropping up in some quarters.

Semis for long term put options is what I’ll be entering when the time is right. The current correction is just a first wave down. All IMO, of course.

I’m surprised–though probably shouldn’t be–by the vagueness (and banality) of many of the Fed comments on AI’s inflationary effect. They sound like the platitudes from TV commentators. Not very insightful. Not reflective of expert analysis.

Meeting minutes are a communication tool about monetary policy. The purpose is not to teach you about AI. The purpose is to let the market know what direction the Fed’s thinking is going in terms of monetary policy.

Minutes are not designed to be read, like you would read an article, they’re mind-numbing and so vague and repetitive that if you read them, you soon give up reading them. So compared to minutes normally, these here are much more detailed about just one technology. I was surprised by it. What you need to take away from it is that AI is shaking up the Fed’s thinking about inflation and monetary policy.

We haven’t had minutes like this in a while.

Well, it’s been a minute.

“The all-items PCE price index, on which the Fed’s 2% target is based, has been above the Fed’s 2% target since March 2020, for over five years, and now the assumption is spreading, including right here, that the Fed’s de-facto target has been tacitly moved to the 3-4% range, and 2% is just copy-and-paste lip service.”

It is blatantly obvious the FED has absolutely NO INTENTION of limiting inflation to 2%. It doesn’t take OVER 6 YEARS for them to get it down to 2% – or ZERO for that matter. They are lying sacks of sh*t.

The Federal Reserve does an excellent job as the central bank of the US and has no means or tools by which it can in any way regulate prices which are the huge issue with ‘inflation.’ Moreover, the few interest rates which the Federal Reserves sets are just a very small part of what they do overall.

^^^ Get a load of this clown show.

Yes, they are a joke. Just like Mr. “We will never monetize the debt” Bernanke. Gotta love that sarcasm!

Do you not understand that the Federal Reserve is the primary bank supervisor and regulator in the US and handles all interbank clearances of payments in our financial system and does so very superbly and those jobs are vastly more important than the few interest rates that they control?

LOL! Awesome sarcasm! The Fed is THE single largest enabler of bad behavior in the western world. They OWN congress through the banking lobby. Precisely why The Fed needs to be shut down. They have NOT fulfilled the terms of their contract with the American people.

Don’t believe me, okay, go ahead, let’s see the fed sell that balance sheet back down to pre-2008 levels. The fact that they cannot tells you everything you need to know. The “dude” is a joke and the Fed continue to bailout the 1%, even when they behave badly.

Their #1 job is has always been quite simple…….PREVENT BANK RUNS.

Way easier to blame the Fed because there’s nothing anyone can do about them, and who wants to face up to the idea that repeated bouts of tax cuts and the things that government actually spends most of its money on (not trivial budget items like foreign aid or stupid things like that that people are always happy to suggest cutting) could also be responsible.

It’s the Fed/Illuminati/aliens/World government/Chinese/(I’m going to stop there before I get to the groups people love to blame that are really offensive and dangerous).

The Fed made one major mistake: raising rates about a year too late in 2021-2022. They made a few other minor mistakes: including MBS in QE and not unwinding QE earlier. The federal government has an enormous impact on rates and inflation via its fiscal policy, but has refused to do anything about it for over 20 years (and arguably for 50).

The Fed manages not only interest rates but the entire money supply.

If they cut the money supply – by 5%, 10% or maybe even in half – you can bet prices would react!

They have all the tools they need, they just aren’t doing their legally mandated function.

P.S. I believe it was by curtailing the supply of credit that they raised interest rates under Volcker. There are very beautiful tight-correlation graphs online showing money supply/GDP ratio and interest rates. The tools worked beautifully until the Fed broke that system after the GFC.

“They have all the tools they need, they just aren’t doing their legally mandated function.”

“The tools worked beautifully until the Fed broke that system after the GFC.”

Correct! ALL the companies that created, profited from, and were shorting those “financial products of mass destruction” (MBS) should have been allowed to FAIL. Instead of allowing the chips to fall where they may and just rescuing the depositors (let all the “investors”, shareholders and corporate owners take the loss for their bad decisions) The Fed BOUGHT ALL THOSE MBS and then turned around and REWARDED the same entities that caused the problem in the first place!!!Goldman should have died, instead they were made a primary dealer bank!!!! Talk about rewarding bad behavior. Why is anyone surprised that we have simply gotten even more bad behavior? Eventually, this will lead to heads on pikes, or we should be optimistic that it does. Time will tell, but history is pretty clear on how such things turn out if they continue.

There are no such graphs because the correlation between money supply and inflation was shown to be loose at best over 30 years ago.

Another way of saying this is that the velocity of money is not a constant. It was surprisingly constant for the period from 1955-1985, which fooled a lot of people included the god of money supply himself, Milton Friedman. But since then it has not been the slightest bit constant.

“……..fly off the handle.”

We’re back to your frying pan chart….which opens the door to many more jokes.

I’ll kick it off with ‘out of the frying pan and into the fire’ which is an appropriately toned inflationary joke.

what a bust AI is for inwestment. Reminds me of Japanese purchases of office towers in America. Sell the shovels, and supplies and GTFO. And then higher interest rates for all, soon. And oil, etc etc etc. Until the Fed and eurofed force a giant recession to break it. And much higher taxes, cause, must save the world.

I just do not see how AI will improve my life all that much. Yesterday I went to three stores to buy a new wallet: Target, Pennys, and Burlington Coat Factory, all within walking distance of each other. I already had a pretty good idea that I would buy it at Burlington Coat factory if they had it, because they would probably be the cheapest, and they were. Burlington did not have much selection, but I got a nice wallet for $12. Target had one at $20 and also not much selection, and just as good as Burlington. I thought Pennys would probably be the most expensive, and they were. Slightly better selection, but cheapest was $36, and no better than the other two. Pennys is in bankrupcy, so they do not care about price competition. Pennys is in bankruptcy and does not care, Target is not as complete of a store as Walmart and might be going the way of K Mart, and Burlington is sort of like cheapest Grocery Outlet, but with cheap dry goods instead of food. So the point is here, is AI really going to make any difference how these retail stores operate? I really doubt it. The efficiency and utility of a cell phone is enough for me.

I am assuming the efficiency and improvements to online retail is based on AI supported automation including tracking. I live 50 miles from town and online shopping is beyond convenient, especially with rapidly rising fuel costs. I even order tools online.

However, many many corporations are now substituting proper customer service for AI phone menu hell. The selections are circular, press this then that, wait for messages etc etc only to dump you back at the start. I needed to talk to a human agent about some double up billings on my CC. Finally had to go through the CC dispute resolution process as required by the CC company and the very next month I was still double billed even though I no longer even had an an account with the offending company. (Telus) Finally the CC company had to actually cancel the card as they could not find a human to fix this, either. And they will still have to go through dispute process one more time to obtain my refund.

And guess who had to revise accounts for the new card?

I think this is common and many folks don’t pick up double billing with paperless receipts. I request monthly paper statements as well as online access and am able to highlight dodgy charges much easier than scrolling a screen. AI might be great and inescapable, but sometimes it takes a real customer service rep to fix screw ups. Probably AI screw ups.

Most men use a wallet to carry an ID and various payment mechanisms (cash, credt cards). So the use of AI here is to ask it if there are more effective mechanisms of providing an ID if needed and payment mechanisms than using a wallet, and see what comes back. Maybe you don’t need to spend money on a wallet at all.

If you’re out buying a wallet you’re a dinosaur of a consumer.

I feel you, but you don’t matter in 2026. I don’t matter much either. I’m trying to save $

Consumers doing the spending are ordering thousands online every month.

AI goes on top of how 100 stores process data and transactions. It makes things more efficient and have less errors. Less employees involved and more profit.

Think if Macys hired 100 smart coders in 2010, they woulda made an impact in some way. AI is a huge block of coders. It will increase sales and profit.

GDP is up 1.2% for Q2 according to the Atlanta Fed. Inflation in running at 4.2%. That sounds like a recession to me. What do you think?

Sounds like doctored stats to justify no rate hikes. I trust our government about as much as North Korea at this point.

The Atlanta Fed estimates what “real” GDP might look like when it’s released, meaning it’s already adjusted for inflation. You’re trying to adjust it to inflation a second time.

““I used to think that if there was reincarnation, I wanted to come back as the president or the pope or as a .400 baseball hitter. But now I would like to come back as the bond market. You can intimidate everybody.”

You can’t intimidate anybody if you’re asleep. Stop hitting the snooze button, bond market. You let a 4% inflation target become the new 2% target while you’re catching some Zs.

Those little wiggles in the 10-year T-bond aren’t really scaring anybody much yet. Wake up and put a 5- or a 6-handle on those…NOW you’re intimidating.

Isn’t the bond market supposed to look through assurances that go on for years and instead adjust its expectations closer to ongoing inflation trends? (Especially since services inflation was raging even before the Iran conflict). Or is it as much a slave of psychology as the stock market often is?

Also, is there any historical precedent of a technological innovation that proved to be significantly deflationary in the mid- to long term?

I understand that this is supposed to happen because said innovation increases productivity and thus supply.

But all I have seen in the past couple of decades when productivity increases is fatter profit margins for the big players (not counting AI investments for now, which I guess these companies expect to lead to super-fat profits in the future, a la Amazon AWS). Is this because of increased market concentration?

AI is here to stay but of course the use cases will be limited so it isn’t a trillions of dollar industry that eliminates humans. Fortunately the tech sector is so arrogant at this point they didn’t think they need a real narrative. But if Open AI doesn’t IPO or possibly even Anthropic doesn’t, the money will dry up and the big players will be standing that have real revenue businesses. There is already a drive for companies who use it to use the Chinese models which would be difficult if not impossible to ban. Hardware bans are pretty easy, but not open source code.

Thinking 2027 is make or break year. Challenge is with so many data centers getting cancelled or delayed there are likely tons of chips gathering dust. By the time the next generation of chips come out those data centers will not only need new chips but racks as well.

To me it looks like a money pit but some use will exist for LLM AI but unclear what that would look like. Google’s move is especially confusing as I use Gemini a lot(and it is often wrong) but that means I am not going to sites where they earn as revenue.

Datacentres should provide in their own energy needs and not suck of the publics teet.

Another thing is that humans pay income tax. If you change that to labour tax, then one could tax everything that does any kind of labour. Including tech and machines. Then the choice between a human or a machine would be fair(er). Now it is: “if a machine can do it, ditch the (expense due to taxing) human”. Even when the machine is not right for the job. If you ever called a helpdesk and chatted to a mindless robot, you know what i mean.

This may sound like Marxist, but we can’t discard humans as if they were machines. Letting humans compete as if they are, is insanely inhumane. It could be you and it will be you if we let it progress.

No more income-tax also could level the playing field. But … what to tax then?

Don’t worry that is not remotely even connected to Marxism. The root issue is never who or how much to tax but in fundamental class conflicts between labor and the owners of capital. Marx even strongly believed capitalism was necessary after feudalism but not the end state when capitalism, by its nature, not by bad humans, concentrates the productive forces into a few companies with massive wealth them as a result controlled by the few. AI may not eliminate that many jobs (or it might) but it is accelerating the conflict, which in my view is a good thing. Dialectical materialism is a good starting place if curious as everyone thinks Marxism is some utopian state and Marx and Engels were exactly the opposite. I don’t think it is reasonable to expect that non-human labor will be taxed, and all of that money will be redistributed however as UBI. There are a ton of good ideas that could address this but simply impossible given the current material conditions that exist, and thus we plod along until some real crisis happens, but I honestly think those in power can keep the grift going for some time. If the UK can do it, the US certainly can!

On the energy front, Portland, for example, is charging business that use extreme amounts of energy (data centers, paper plants, crypto, and so on) an extra 29.7% which is reducing customers bill by a small amount. I would not be surprised if this happens more which obviously has other impacts as well. Some of that just relates to available power and some relates to it can cause inflation in other places.

I think the water utility approach is most useful. During water restrictions, customers who pass a threshold of usage are charged at a significantly higher rate. It’s like progressive taxation for utilities as a way to fund development.

Don’t see interest rates having an effect on invention or technological advances through the years. In fact if interest rates rising causes an effect on a shakeout of the zombies or BSers it is a good thing.

The first AI affect on me is I don’t use Google search anymore but using ChatGPT and Claud.

I expect AI to do what the cell phone and internet did for people.

Is it the Feds job to be guessing about its inflationary, deflationary, productivity effect on the economy. I don’t think so.

Look at the inflation data and raise rates. It probably won’t kill anybody.

They shouldn’t let the governments fiscal irresponsibility sway them.

I don’t really see it replacing Google search outright. Maybe for things that aren’t really important whether the info is current or accurate. Otherwise I have to click all the references to verify everything myself, and look at the search results anyway to see if there are any better references it didn’t use. If one of the sites it’s referencing isn’t trustworthy, I could normally ignore that site in the future, but the model just has it in one giant bucket of info and you can’t do that if AI is all you’re using, at least without listing everything out.

There’s also the fact that AI is undermining all of these websites’ revenue by preventing people from clicking through to them. There’s the question of AI content polluting the internet and eventually causing model collapse. And there’s the fact that nobody is currently paying the real cost of AI, especially not on a free “AI overview”.

My forecast here has been for model collapse to take this bubble out, but it looks like the financial collapse is going to happen first. There is yet hope that some parts of the internet will escape enshittification.

I guess it depends on what you are using it for. I remember when google first came out and reading their results trying to learn and understand more, I would have to go back to the search box.

One day I emailed Google to try to have highlight and search and it was there the next day.

Yes AI is not perfect but it’s really good. And it is interactive responsive.

Reasonable to do 3-4 hikes

Thanks wolf

Let’s assume AI leads to meaningful productivity gains for white collar workers and then discuss the inflationary impact of those gains.

If most of the gains are captured by execs (compensation) and shareholders (prices and dividends), then how would that affect inflation?

If most of the gains are instead captured by workers (wages), would that have a different effect?

One theory I often hear is that inflation is related to a wage spiral, so there we’re presumably talking about workers.

But would the gains going to a presumably smaller number of people (execs and shareholders) mean that spiral would be dampened, and inflation effect lower?

I don’t get the ai reduces inflation narrative. I think it just means more money for CEO’s. Companies will continue to raise prices as long as people are willing to pay for it. They’re never going to cut or hold prices steady. Operating margins could improve because you need less workers but anyone who thinks that extra money is going to consumers is crazy.

I think we see more and more wealth concentration at the top.

I use AI daily at work and it does make me about 4x more productive than I was without it, but I’m certainly not being paid more. Also people forget AI costs money. Take a look at Uber, many companies are actually realizing AI is super expensive.

AI makes my daily work harder – the bots I deal with have not been trained properly and cause nothing but problems and endless email loops of trash. I had to threaten to report a company to the state department of insurance for “requirements” that by state law and monopoly of workers’ compensation insurance were not possible to meet – yet the AI bot kept insisting. It’s a total mess.

What caught my attention was the idea that AI can be inflationary before it becomes productivity-enhancing. It’s easy to focus on the long-term efficiency gains, but building data centres, expanding power infrastructure, and buying huge amounts of hardware all create demand right now. It’ll be interesting to see how much of today’s inflation proves temporary and how much becomes a longer-term challenge for central banks.