The Fed watches inflation expectations closely. It wants them to remain “anchored.” But consumer inflation expectations have become unanchored.

By Wolf Richter for WOLF STREET.

Metrics of “Inflation expectations” are based on financial market spreads, such as the spread between the 10-year Treasury yield and the 10-year TIPS yield, or on surveys, such as the New York Fed’s Survey of Consumer Expectations (SCE), of which the latest version was released today with some bad news.

The Fed wants these inflation expectations be “well anchored” near its 2% inflation target, the same target that “core” inflation (without energy and food) has been above for over five years and has been moving further away from since mid-2025, driven by “core” services.

Inflation expectation metrics featured prominently in the minutes of the FOMC meetings and in the FOMC statements when Powell was still Chair. But the first statement released by the FOMC under Chair Warsh – that refreshingly terse statement – didn’t mention inflation expectations at all.

The last FOMC statement under Chair Powell repeated the line: “The Committee’s assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations….”

Whether “well anchored” inflation expectations will matter as much under Warsh as they did under Powell remains to be seen, but here they are, and they’re becoming unanchored.

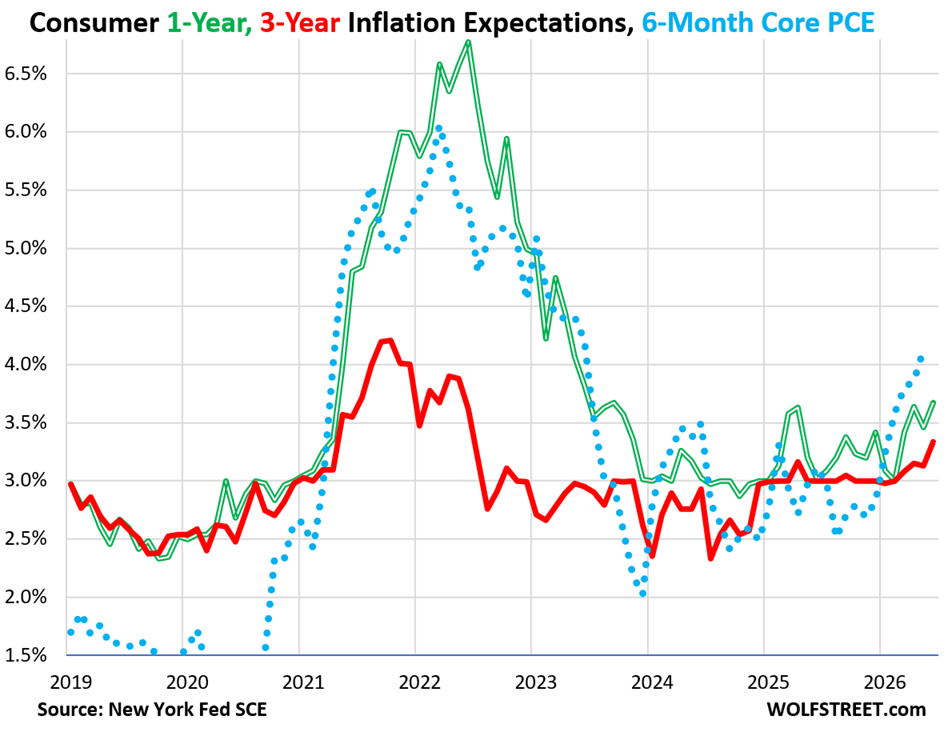

Consumers’ median inflation expectations for one year from now rose to 3.67%, the highest since September 2023, when they were on the way down (green double line).

Inflation expectations for three years from now rose to 3.34%, the highest since Jun 2022 (red line). These “medium-term inflation expectations,” as they’re called in the Fed’s communications, had been “well anchored in all of 2025, but at 3.0%, which is not near the Fed’s inflation target of 2.0%. And this year they became unanchored off this 3.0% line and in June rose to 3.34%, the highest in four years.

The “Core” PCE price index – a Fed-favored inflation metric that excludes the volatile energy and food components and therefore excludes the recent energy price spike – has been accelerating since mid-2025. The year-over-year core PCE price index rose to 3.4% in May 2026 (June not yet available).

And the six-month core PCE price index, which shows the current trend better, has accelerated to 4.1% annualized, the worst in three years, and this does not include the spiking energy components (blue dotted line).

But gasoline prices no longer drove these inflation expectations in June. As gasoline prices have started to come down in June from the spike in the prior months, consumers expect gasoline prices to be just 1.5% higher a year from now.

The minutes of recent FOMC meetings under Powell had pointed to rising inflation expectations one year out as an upside risk to the inflation outlook, but had emphasized that the three-year inflation expectations – the “medium-term inflation expectations” – were still “well anchored.”

“While both market- and survey-based measures of inflation expectations indicated upside risks to the near-term inflation outlook, measures of medium- and longer-term inflation expectations remained well anchored,” said the minutes of the April 28-29 meeting.

Participants of the June 16-17 meeting – the first meeting under Chair Warsh – did not yet have today’s report. The minutes of that meeting will be released tomorrow.

But participants of the July 28-29 meeting will have seen today’s report, and something about rising medium-term inflation expectations should crop up in the minutes of that meeting.

The idea of looking at inflation expectations is that price inflation is in part a psychological phenomenon, that once consumers expect inflation, they will adjust to it and ask for appropriate raises, and then pay the higher prices, knowing that their wages will rise with the prices, rather than refusing to pay those prices and switch to a competitor or downgrade or not buy at all.

And businesses, once the inflationary mindset kicks in, want to increase prices because they’re having to pay higher wages and higher input costs, and they always want to maximize their profits, and they know they can get away with price increases because their customers expect inflation and will pay those higher prices, and so they raise prices more than needed to cover additional costs, and their profit margins soar, as we have seen in the last bout of inflation. In this scenario, inflation expectations becoming unanchored would be a factor in allowing inflation to fester.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Howdy Folks. Wanna read the expectations of a Sober Sailor???

I expect to continue as I always have. Just bought a new motorcycle to go with my new car. Just ordered a new trailer to put my motorcycle on. Just sent the kids some CASH too….

Yep. Might as well spend the money now on anything expensive that might be necessary in the future. That’s what I am doing. It makes no sense to put off big purchases, as they are just getting more and more expensive as we go along.

Howdy DC. Doing what we want ” Legally of course ” makes US as Free as we can be….

I lived and worked in Latin America. Inflation was rampant, 100 percent or more a year. When we got paid we spent it immediately, saved nothing. All savings were in hard assets like a car, house, land, etc. We all hoped there would not be another revolution, and the government would not come and take our assets. Serious money was kept out of the country in Swiss Franks, gold and in those days dollars. Please learn from my experience.

Boomers live in a different reality

I see Fed language in the same way I see lawyers and used car salesmen. “Well anchored” is the medium and long term is a complete unknown and likely wrong or at least difficult to substantiate with current information. Sounds like a captain with a sinking ship that knows there aren’t enough life boats but says there are anyway.

This 2% inflation anchor I fear is much too low for an economy that is receiving so much stimulus from corporate reinvestment in an effort to run organizations more productively. Let inflation run a little in the 3-5% range as the US economy develops a new phase of existence in an AI eventual world. Like the 60’s but tempered with smarter monetary policy when inflation starts hitting 4-6%. Rising prices have there pain points but it also allows the economy to seek a more optimal rate of production which reduces inflation. Consumers have more choices than they did 60 years ago. If you wanted to buy a pair of work boots or overalls back then there were 2 places to look to save money, Kmart and Sears. Take a look at Amazon and others today. Multiple choices and best price. Consumers don’t have to pay full price for anything if you’re smart enough to look around (Internet???). Is price stability and a inflation target of 2% really optimal when an economy is ready to role upwards. Perhaps the target rate should be more variable based on the trajectory of the underlying economy and not the price of eggs and milk. Capital formation during an innovative revolution is more important than a couple of percentage points of inflation. If I eat 2 eggs a day and cut back to one then I’ve reduced my costs by 50%. Labor costs should inflate with a higher rate of nominal GDP growth. This is necessary as the labor pool will change due to AI productivity gains. Higher Real GDP growth, a bit more inflation, moderation in rates, albeit lower than 3.75%, creates increased risk taking and capital formation and eventually reduces fiscal debt with higher tax receipts. Living in a low tax moderately inflated world is better that a high tax, low interest rate, low inflation world.

You’re right. We should all eat half of our caloric intake so the greed men can be greedier. Also, you have to replace that egg with something, so you’re cutting costs by less than 50%.

While AI will be a thing it won’t be what was promised. Admittedly it will improve but study after study shows minimal to no productivity gains. If anything AI will wipe out call centers on India, Phillipines and so on.

I could see AI being even a ten or hundreds of billions a year business but it has to figure out how to be profitable and the current headwinds it faces are not insignificant. On the positive side many of the pledged data centers are delayed or are very far behind. Open AI will be a bell weather but right now doesn’t look solid.

ED ZITRON WARNS OF AI BUST: It Doesn’t Work!

Someone just sent me a youtube where a guy jailbreaks one of those call center AIs and gets it to say crazy stuff. If it’s real, it’s hilarious.

Maybe the YouTube video you saw was AI-generated? This stuff is now everywhere. For entertainment only.

“If you wanted to buy a pair of work boots or overalls back then there were 2 places to look to save money, Kmart and Sears. Take a look at Amazon and others today. Multiple choices and best price. Consumers don’t have to pay full price for anything if you’re smart enough to look around (Internet???).”

It’s almost like you’re arguing consumers just haven’t discovered the website yet for the company pulling more than $700 billion in annual revenues and carrying a $2.5 trillion market cap. If only the secret got out we could beat this consumer price inflation scourge.

Or…maybe the problem isn’t the shopping habits of folks just buying retail goods.

“Let inflation run a little in the 3-5% range…”

We are already living in that world. If what you really mean is that the Fed should publicly change their inflation target from 2% to the 3%-5% range, give me a moment to get some popcorn first. I want to get a good seat to watch what happens to the bond market on that day.

“Rising prices have there pain points but it also allows the economy to seek a more optimal rate of production which reduces inflation. Consumers have more choices than they did 60 years ago. If you wanted to buy a pair of work boots or overalls back then there were 2 places to look to save money, Kmart and Sears. Take a look at Amazon and others today. Multiple choices and best price. Consumers don’t have to pay full price for anything if you’re smart enough to look around (Internet???).”

Interesting argument, but in reality Americans pay among the highest prices in the world for many basics. Health Care. Internet & cell service. Personal transportation.

More choices =/= more good choices. In the 60s both Kmart and Sears would do their best to make the best quality work boots in one or two price ranges. Because they knew their business was build on the trust their returning customers had in them. These days you can choose between 1500 different boots, most of which are build in the same factory district somewhere in Bangladesh which get stamped with a different logo for each western importer. The ‘quality’ items are now nearly always attached to a big brand which is enabled to charge ridiculous margins for the simple confidence that your boots won’t fall apart within 3 months.

That’s neither choice nor freedom, that is enshitiffication. An excuse masquerading as ‘choice’ to offshore, outsource, and deliberately create shit products that fall apart right after the warranty ends while exploiting low wage and low regulation countries to offload the costs that come with manufacturing.

AI is not going to save us, at least not in the way you think it is. It is primarily going to enable folks to abuse the limitations of our monkey brains even further. As evidenced by folks equating the economy to GDP and exclamations that shopping at Amazon is the smart thing to do.

Jbubs wrote: “Living in a low tax moderately inflated world is better that a high tax, low interest rate, low inflation world.”

So we can only have low inflation if we have high taxes? Or is this a two-choices fallacy to trick the reader into choosing the less-bad sounding “moderate” inflation over the evil “high” taxes.

Speaking as a middle-class worker, let me think about giving up my purchasing power through taxes versus inflation.

Taxes: Intended to serve a public purpose. Some of the spending, I agree with, and some I don’t. Rates set by elected representatives. Predictible month to month. Same percentage comes out of my checks, grocery bills, etc. each month. Those with more ability to pay can be taxed at higher rates. Money I’ve already saved, the interest but not the principal is taxed, at whatever my top marginal rate is.

Inflation: Serves business interests (per your argument). The lost money goes where? Winners and losers depend on who is able to protect themselves from inflation. Biggest losers are the working classes and those who need lower-risk savings & investments. Savings principal is “taxed”, and this taxation is indiscriminant and not based on income but instead on the amount saved. To the extent that it discourages money-hoarding, a little inflation can be good, but the inflation rate is not directly set by our elected representatives.

Nobody likes paying taxes, but they can be good if well structured to serve needed public purposes.

High inflation is chaotic, discourages savings, and impoverishes the working classes. And as Wolf says, Americans hate hate hate inflation.

I agree the best thing trump will do is usher in a social democratic government that will actually be of the people by the people for the people not just great for billionaires

If we had the freedom to choose our tax rates I would go for it but it’s law and crammed down our throats or you cheat on what you report for income. I accept the tax rate I get but would prefer choosing how much I want to spend on items that experience price increases. I don’t have to eat eggs for breakfast. I don’t have to eat steak for dinner. Manage your expenses better and be happy that personal tax rates are as low as they are because they will be higher , not lower, in the future.

Choose our own tax rates? As in you hire your own private police protection, and I hire my own (anarcho-capitalist)? Or as in, I disagree with the Iran War so I don’t have to pay for it?

In a high inflation environment, if you don’t spend your money on steak and eggs, you’d better spend it on something. That money is a hot potato, and the act of holding onto it and not spending it is the thing that’s “taxed”.

30 Year plowed back up through 5% today

and the 10 yr through the 4.5% “ceiling”

Real yields on TIPs popped too. You get CPI inflation + 2.3% on the 10-year TIPS today. There’s an auction of a new issue slated for July 23.

The long end of the curve did jump today for sure . I said no to a replacement hvac. I have a Freon leak and the old Freon is 100 usd per lb because they don’t manufacture any more just old stuff that’s been recovered .

The Freon will be 400 . A new 3 ton ac compressor and coil is 9000 for 14 seer basic American standard unit .

Will see how long the Freon will last

went thru this exact scenario 3 years ago. The $500 will get you thru one season.

You’ll still have to do something over the winter.

I let them charge it up (they were busy anyway), survived the summer (kinda) and then had them quote out a new system which i deposited on and they held until May (when the season starts around here). They told me prices had gone up 13% from Aug one year to May the next, so I saved quite a bit and got an extra year. Now that was in 23 and who knows but that system is just gonna be more expensive next year.

Meanwhile, Eddie Grant rises from the inflationary ashes of the the early 80’s to relive the new “Transitory” inflation we see today. Rates are going higher.

Now in the street, there is violence

And-and a lots of work to be done

No place to hang out our washing

And-and I can’t blame all on the sun

Oh no, we gonna rock down to Electric Avenue

And then we’ll take it higher

Oh, we gonna rock down to Electric Avenue

And then we’ll take it higher

Workin’ so hard like a soldier

Can’t afford a thing on TV

Deep in my heart, I abhor ya

Can’t get food for the kid

Good God, we gonna rock down to Electric Avenue

And then we’ll take it higher

Ho, we gonna rock down to Electric Avenue

And then we’ll take it higher

get a heat pump or two for that price

Spend a couple thousand more to get the newer tech heat pump with variable speed ”inverter” and the multi speed air handler with SEER2 at 19 or more, and it will pay the difference back in one year, then save the entire cost over ten years compared to the old system it replaced .

Doing so right now, same size…

Inflation, whether 2% or higher means the fiat currency has lost value. Look at inflation in the US before the Fed and after the Fed. Yes, there were peaks and valleys before the Fed but the dollar kept its value. The Fed was pretty much harmless between the end of WWII and the start of the Vietnam fiasco. QT, QE, ZIRP and other nonsense have destroyed the value of the dollar. Inflation,no matter what the theory behind it (MMT anyone ?) destroys fiat currency.

Why is maintaining the value of a dollar such a worthwhile goal? Why has essentially every country on earth moved to a monetary system designed pretty similarly to the Fed?

A false balance is an abomination to the Lord,

But a just weight is His delight.

Looking at it another way, When Roman emperors started thinning the purity of the money, the populace was pretty ticked off.

A quick search of Roman silver coin debasement should offer you plenty to mull over.

Romans were angry about being lied to about debasement. There are dozens of measures of outstanding US dollars published regularly.

All most care about is the ability to purchase the things they want. I’d be fine with 100% inflation if my wages increased by 200% over the same period.

Replying to JBubs, how does inflation allow the economy to seek a more optimal rate of production?

Traditional monetary policy treats supply as fixed and uses interest rates to choke off demand to match that ceiling. A high-pressure approach argues the reverse: let strong demand pull supply upward. Rather than using blunt interest rate hikes to force demand down to a constrained supply curve, the Federal Reserve should maintain a supportive 3.0% policy rate, or lower, to let robust demand pull supply capacity up. Accepting a temporary target of 3% to 6% inflation for a few quarters acts as a crucial bridge. It provides the affordable capital environment required to fully realize the massive, disinflationary productivity gains of the AI revolution. Furthermore, the resulting surge in nominal GDP growth organically repairs the fiscal deficit through expanding revenues, providing a vastly superior macroeconomic outcome to the stagnation, higher taxes, and slow growth that premature rate tightening threatens to deliver.

Why do you think decreasing the Fed’s policy rates to 3% or lower while simultaneously changing the inflation target to 3% and higher will lead to an “affordable capital environment”? If what you’re demanding is lower long term interest rates, this site has emphatically pointed out that’s not how you’re likely to get them.

Maybe review the articles on the effects Fed policy rate reductions have had on mortgage rates over the last two years. They’re quite illuminating.

Fed Funds target rate continues to be 3.5% to 3.75% while the December Fed Funds futures rate is almost 4.0%. I’m arguing that these levels are too restrictive at a time when there is a ton of private sector stimulus that could be snuffed out with higher rates. I would argue that lowering the Fed Funds rate 25 to 50 basis points would lower borrowing costs and promote capital formation/risk taking during a period when the economy wants to accelerate. Sometims a wild fire has to burn through some land sectors to prevent future fires. By accelerating nominal GDP growth from a supply side there is potential for increased inflation. Let it increase. Let revenues grow. Let profits grow and let tax receipts grow to reduce these annual fiscal deficits and insane gov’t borrowing. Better to have a few years like that vs lower growth with higher tax rates on individuals. Corporattions aren’t getting hit with increased taxes they’re just paying more because profits continue to rise.

The 5-year average annual US Consumer Price Index (CPI) inflation rate is 4.47%, covering the full calendar years from 2021 through 2025.This elevated multi-year average reflects the unprecedented post-pandemic inflation surge that peaked in 2022 before steadily cooling down toward historical norms. YTD S&P 9.3% ROI. Looking and listening for Trumps next hot stock pick. 2 more AI IPO’s coming out this year. Colorado has 5 forest fires burning, made the decision to allow the selling and shooting of fireworks during our Stage 2 drought 4th of July weekend celebrations. A fed funds rate of 5.0-5.5% would vanquish the amount of liquidity in the USA market and economy. I’m convinced we are too big too fail.

“Expectations of future inflation [over the last four weeks] have come down. Inflation risks have come down,” Warsh said at a conference in Portugal

just 7 days ago.

The idea that our inflation is due to the Iran events is folly.

It will be over soon we are told. Maybe it won’t. Subjective guessing.

We need a hard railed monetary policy. If inflation is X then Fed Funds X + Y.

If indeed the inflation “bump” is temporary, then indeed the rates will adjust per the formula. But we have learned that the promise of temporary or “transitory” can be errant. Almost always.

“just 7 days ago”

That was before this data.

It’s been estimated that it will take three to four years to replenish the US Military’s armaments that was/is being deployed on Iran. US defense companies production lines will be working overtime. The US Department of War Budget will be exceeding $1 Trillion.

Government spending – local, state and federal – is inflationary.

My father used to say money talks, bullsit walks. People think the Fed, Treasury and government are just BSers. Stop flooding the economy with money.

At the checkout counter the owner asked his wife how the clams were this year. She said tight. It’s ok if things get a little tight and prices stabilize.

How about a little shock and awe to help stop the inflation expectation with a concerted plan? Granted government gutting and cuts have done nothing but what if instead of beating on NATO to increase spending our dear leader says instead we are going to cut our military spending in half along with…

This massive stock market/everything bubble is inflationary.

I wish Michael Bury, Ray Dalio and Jeremy Grantham would finally be right already!

They have to leave a certain amount of inflation on the backs of the shrinking labor pool. The real kick in the ass is they keep handing out COLA raises…umm excuse me but if incomes across the board don’t rise at the rate of COLA plus some, then how do you expect laborers to save enough to survive having SS pulled out from under us and not start the 2nd civil war??? They have a lot more to consider than just debt. They are walking a very tight rope and then their is the IMF to answer to – Oh and don’t forget Mother Nature – I’m no alarmist global warming fool but natural disasters happen 919.

I do know how to use there, their, and they’re. I just didn’t edit before hitting “post comment”

I assume I am asset-light compared to many of your readers. I’ve lost faith over the past few years that the FED or the the Gov actually wants inflation at the 2% target. One transitory event after another seems all too obvious.

Inflation was UNDER 2% for essentially the entire period from 2008 through 2021, much longer than the current 3%+ period. At the time the Fed was most worried about how to drive inflation up–remember “helicopter money” proposals?

Reserve balances with Federal Reserve Banks on H.4.1 release

July 2 2025 3,225,980

July 1 2026 2,966,897

Cumulative contraction -259,083

If the FED holds the line inflation will fall.

The TOTAL USA agricultural food production is worth about 1/2 of Elon Musk net worth. We have to change the tax laws billionaires should not own as much as they do it is just wrong. We need to fix it with taxes or it will be fix in unpleasant maner.

Until the government stops it’s reckless spending, we aren’t going to see inflation go down any time soon. Inflation is actually preferred because the deficit from 5 years ago is worthless now thanks to the inflation.

Not worthless but worth less. :-D