Even banks are raising the yields on their brokered CDs to 4% and over. The coming rate hikes are getting real for investors.

By Wolf Richter for WOLF STREET.

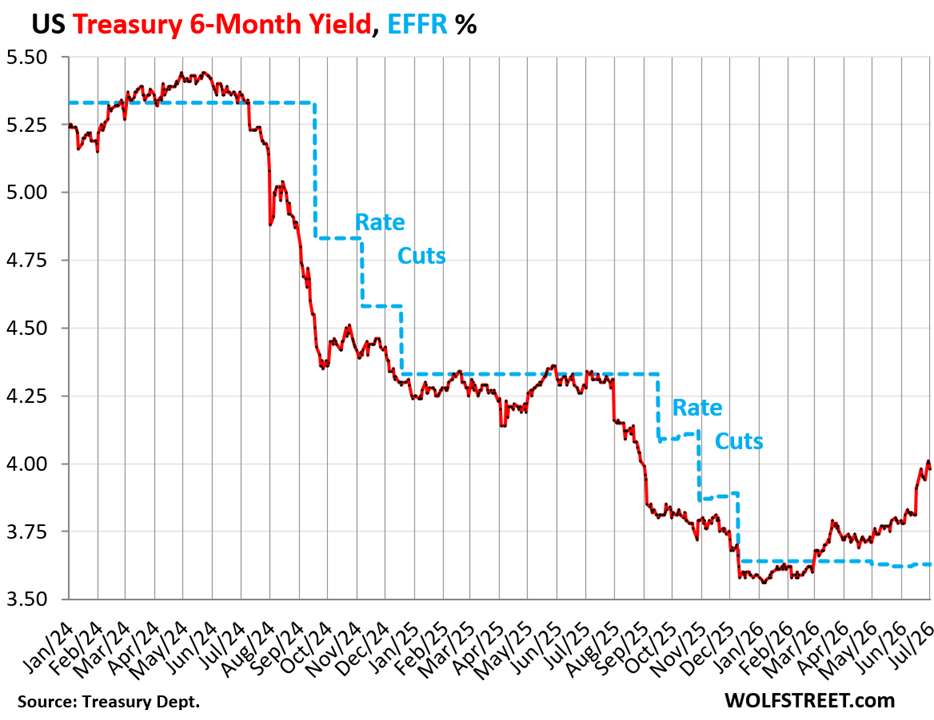

The government sold $84 billion of 6-month Treasury bills at an “Investment Rate” of 3.97% at the Treasury auction this week, up from 3.80% at the auction two weeks ago.

In the secondary market, over those two weeks, the 6-month Treasury yield also spiked by 17 basis points, closing on Thursday at 3.97%, after closing at 4.0%+ in the prior two days, according to Treasury Department data. The last time the six-month yield was in this range was in early September before the three rate cuts by the Fed.

Since early January, the six-month yield has surged by nearly 50 basis points, from being below the Effective Federal Funds Rate (EFFR, blue line) which the Fed targets with its policy rates, to being 35 basis points above the EFFR, indicating that the bond market expects – and is clamoring for – more than one rate hike within the window of the 6-month yield, which would be less than six months.

The government sold $98 billion of 3-month Treasury bills at an “Investment Rate” of 3.83% at the Treasury auction this week, up from 3.73% at the auction two weeks ago.

In the secondary market, the 3-month Treasury yield closed at 3.82%, 19 basis points above the EFFR, after going as high as 3.87% (24 basis points above the EFFR) in the prior days, according to Treasury Department data.

So even in this short window of less than three months, the bond market, reacting to incoming data, is now seeing a reasonable chance of a rate hike.

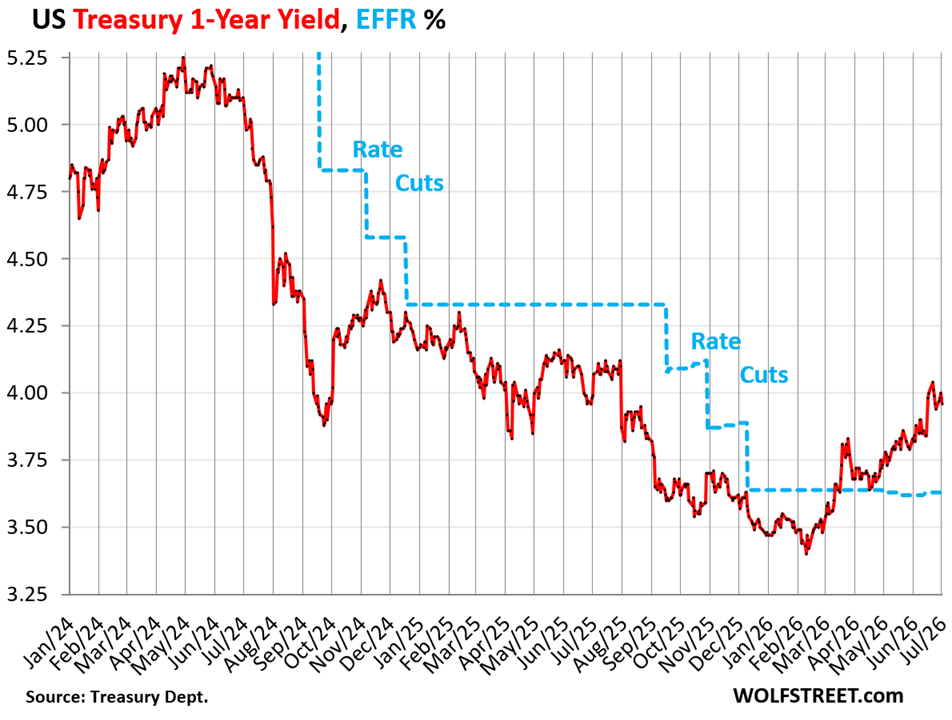

The 1-year Treasury yield has been near or above 4.0% for the past two weeks, about 60 basis points higher than where it had been at the beginning of February. Over this period of five months, the 1-year yield showed how the bond market flipped from still seeing rate cuts this year to seeing rate hikes.

There was no 1-year T-bill auction this week; that will happen next week.

Banks have been ratcheting up the offered yields of “brokered CDs” that they sell via stock brokers to retail investors that are not their own customers. Many of the CD yields have moved above 4% recently. They’re competing with T-bills. And they’re seeing the incoming data, and they know what they need to do to attract investors’ cash: higher yields.

Fed Chair Warsh has been exhorting the bond market over and over again to watch the data, not the Fed. Markets are excellent at interpreting the data, and they should focus on that, and not on the Fed, he said, and that’s important for the Fed, he said, because the Fed wants to use the bond market as one of the key data inputs, and if the bond market reacts to what it thinks the Fed will do, instead of reacting to the data, then the Fed’s input from the bond market would be polluted by this circular expectation.

There has been lots of resistance at the Fed to hiking rates, but that resistance is fading: at the June 17 FOMC meeting, 9 of the 19 FOMC members projected at least one rate hike this year (with Warsh not disclosing his projections). And the bond market is telling the Fed: get on with it.

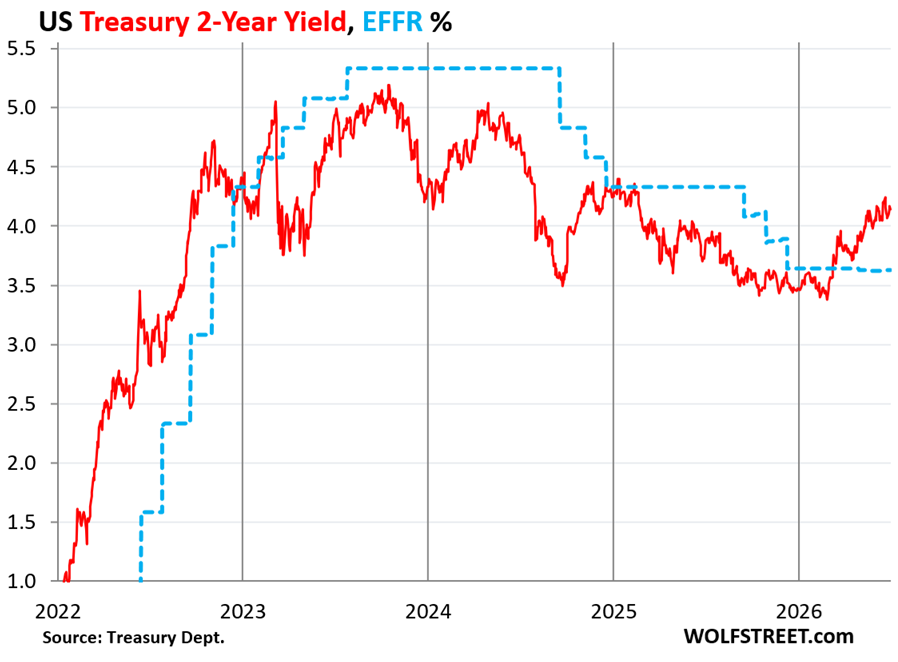

The 2-year Treasury yield, which has been providing a fairly reliable signal for the Fed of how the bond market interprets the incoming data, has surged by 76 basis points since early February, to 4.14%.

The bond market is clearly telling the Fed that the incoming data calls for multiple rate hikes, whether the Fed wants them or not.

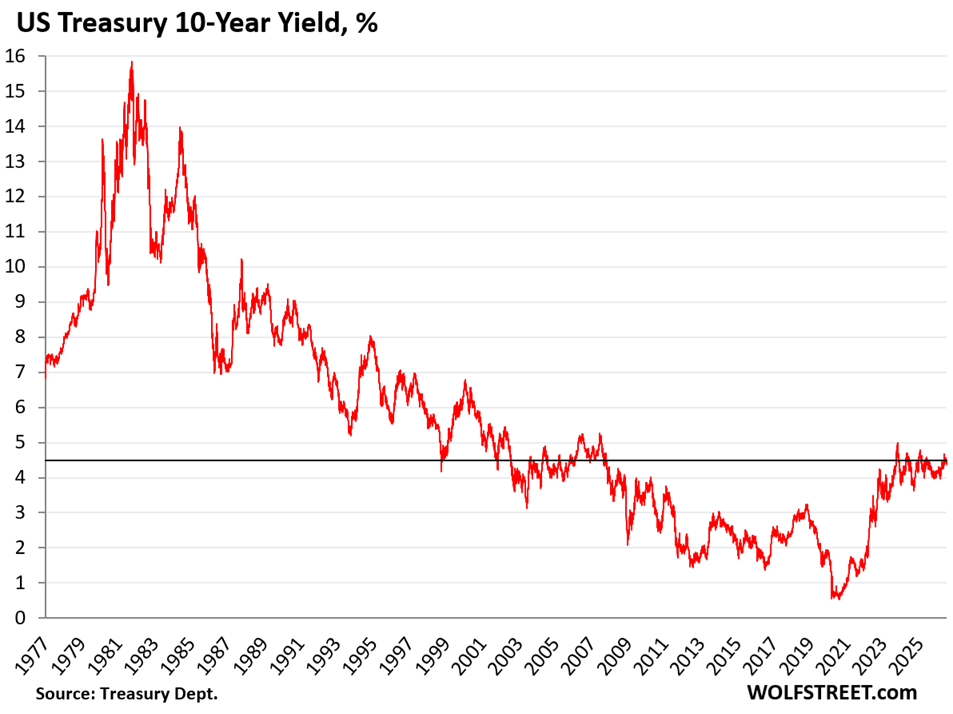

The 10-year Treasury yield rose by 11 basis points during the week to 4.49%. Compared to two weeks ago, it’s up by 2 basis points. It has been in this 4-5% range since 2023.

This longer end of the bond market is focused on the imagined path of inflation in future years, how lax or aggressive the Fed might be in dealing with this inflation, and on the stream of Treasuries that the government will issue to fund the ballooning deficits that the market has to absorb, which may require higher yields to attract ever more investors.

It wasn’t until the Fed announced the end of QE in late 2021 that the 10-year yield began to surge, ending the 40-year bond bull market, but lagged way behind inflation, which hit 9% by 2022.

Compared to the decades before QE, before 2009, the 10-year yield at this 4.5% range is still relatively low. And compared to 4.25% CPI inflation, the 10-year yield is very low. The bond market is still counting on inflation to go back into the 2%-bottle.

Higher bond yields in the market mean lower bond market prices for existing holders, and vice-versa.

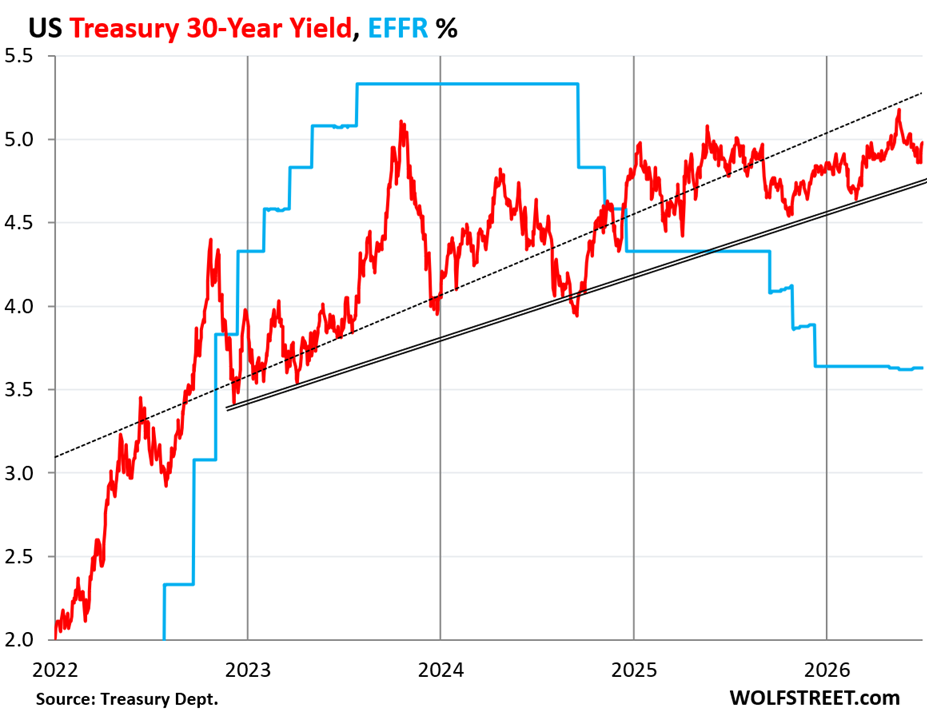

The 30-year Treasury yield rose by 11 basis points during the week to 4.98%, roughly unchanged from two weeks ago.

The long-term bond market completely blew off the Fed’s rate cuts; they didn’t even register.

Two trend lines for entertainment only: The dotted line depicts the linear trend for the data in the chart. The double line is my imaginary trend line of lows since late 2023, and it still holds.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Jerome Powell is a big-time LOSER. This is on him.

Yes – it was hard to top the recklessness of Bernanke (whose policies caused Warsh to resign in the first place) or Yellen, but he managed it somehow.

Two thumbs up!

JP destroyed the American dream of home ownership for multiple generations. Others are also responsible, but he is like the cherry on top of a loser sundae.

And then the elite who benefited so much constantly pour accolades on him for his “strong, resolute leadership that prevented us from falling into a depression.” It’s sickening.

He made a lot of people wealthier beyond their expectations.

They thank him by praising him for saving the peasants from a depression.

The Golden Rule:

One who has the Gold makes the Rules!

All of us who thought otherwise (and includes me) are plain gullible.

As George Carlin said and I paraphrase, It’s a club and you ain’t in it!

FED has inflation credibility issue. We are missing that goal for 5 years now. It will guts and spine to raise rates. Warsh can talk a lot but unless he raise rates in next meeting, he will be “empty and just talk”.

Warsh said rather than giving forward guidance to Markets, he expects to take it from Markets. Well, here it is. Now raise the rates.

The FED has zero credibility left. They have been in dereliction of duty since Greenscam, to further enrich the already obscenely wealthy. Bernanke, the godfather of QE, really took the grift to a whole new level. Then, somewhere around 2014, with no input from CONgress or any sort of resistance, they suddenly installed a “2% inflation target.” Imagine that, trying to cause inflation when your job is to prevent it. These cons need to be in prison. They have done incalculable damage to the once free market.

Couldnt agree more. Bernanke should be tried for TREASON.

Most assets have sky rocketed in last 15 years of ZIRP.

They printed so much money; those so called “high rates” by FED couldn’t put the inflation genie in bottle.

Too quick to drop the rates; Too slow/late to raise the rates.

Too quick to start QE. Too slow to start QT; Too quick to stop it.

Wise were the ones who borrowed a lot in 15 years of ZIRP. Bought lot of RE and Stocks. The FED will do everything now in its power to save Richie Rich.

Think of Social Security which had to invest in

rate suppressed bonds putting funding of

the program in danger. It was an indirect

gift from the workers to the large banks.

Bernanke knew it, Yellen knew it , and Powell

knew it. Unfortunately Congress decided to save the banks instead of representing the people.

You might be shocked to learn that the money printing was ordered by the Congressmen and President you elected.

You also might be shocked to hear me say that the job of the FOMC chair is to deflect blame from the politicians for enacting inflationary / debt-increasing fiscal policies. Low information voters love that their good politicians have a villain to battle against.

Prison is too good for them. Send them to Gitmo .

oh for the days of the Banks adjusting their Prime Rate and the Fed following. (late 1970s)

The Fed never did that. But it didn’t announce its rate decision. Greenspan didn’t say what the FOMC had decided, leaving people guessing. The banks’ (primary dealers) prime rate adjustments were the first indication of the Fed’s rate decision. They knew by how the Fed intervened in the repo market to implement its secret rate decision. But under Bernanke, the Fed tried to become “transparent” and began publishing the FOMC statement, and later the minutes, and eventually even held press conferences, at first four per year, then eight, and somewhere along the line, as part of the doctrine of forward guidance, came the dot plot.

Well for anyone in the business, late 1970s, the Prime Rate announcements on Friday were huge.

The prominent one was Merchants Bank in St Louis, usually followed by Fed moves. I believe that all changed when Volcker came in.

But it seemed more as if the Prime Rate was the prominent rate people talked about.

Were you in the business then?

Sure, the banks’ prime rate announcements were huge – because the Fed never announced any rates. But the huge announcement that got all the press (WSJ, etc.) was the Chase Manhattan prime rate. Local banks had their own prime rates, and they were different. “Chase Manhattan prime rate raised by 25 basis points” that kind of thing. All our variable-rate loans at the time were pegged to Chase Manhattan prime… “Chase Manhattan prime +5%” that kind of thing. This was before Libor.

What I said was that the Fed never followed the prime rate – which you had alleged. It’s the other way around: The prime rates followed the Fed. To think that Volcker followed the banks is ridiculous. He knuckled them under and caused thousands to collapse.

The banks knew what the Fed had decided because banks participated in the repo market and the federal funds market, and saw what the Fed was doing in those markets, and Volcker targeted the money supply via bank reserves (rather than targeting rates directly). The Fed was actively managing money supply and overnight rates with repos on a daily basis and banks saw where the Fed was going with its implementation. So the banks made announcements of their prime rates based on what they saw the Fed was actually doing in the market.

The announcements Volcker made were about money supply – he was trying to bring it down to force inflation down, and this tight money supply eventually caused overnight rates to shoot to 20% as companies and banks were trying to get some cash. This caused a massive credit crunch, a gigantic recession (the Double Dip recession), a huge number of bankruptcies, while thousands of banks collapsed, and the unemployment rate spiked to over 10%. Those were terrible times.

Wolf,

Would it be better for the consumer and the markets to go back to how it was pre-Bernanke regarding all of this published information and the press conferences and the dot-plots?

But then what the hell am I going to write about 🤣

Yeah but you’ve got loads a money from tech investments and stuff for 17 years, so can afford the inflation.

And err, well they’re just gonna keep going up and the whole world will pay $1,000/mo subs to keep it all afloat, so you can afford your inflation.

For these reasons I continue to be bullish US of A.

Right, the inflation is great for those with millions in stonks or real estate. Not so much for the other 90% of America.

This “90% don’t have stocks and real estate” is like a braindead zombie. It refuses to die. This “90% of Americans are poor” is a stupid lie. And I’m losing my patience with it.

65% of households are homeowners (owners of real estate). 40% of them own their home without a mortgage. Another big portion have only a small-ish remaining mortgage. They have huge amounts of equity in their homes. Etch that into your brain.

62% of Americans own stonks directly via brokerage accounts or indirectly through 401ks, mutual fund, etc. For college graduates it’s 84%; for married adults it’s 77%. For middle-income ($50,000 to $99,999) it’s 71%. For people with high school or less it’s 42%.

“ 62% of Americans own stonks directly via brokerage accounts or indirectly through 401ks, mutual fund, etc. For college graduates it’s 84%; for married adults it’s 77%. For middle-income ($50,000 to $99,999) it’s 71%. “ This is excellent info.

In 1986, I attended a presentation on then investment market trends put on by a largish purveyor of money market mutual funds. They made a risk case for the stock market based mainly on the retail investor participation rate in stocks, which at the time was hitting new all time highs. If my hazy memory is accurate, the ratio had just run through the 50% milestone. What followed not much later was the stock market carnage of October 1987, when the S&P dropped 30% in one week, and 20% in a day. Imagine a 20,000 point 5-day decline in today’s S&P!

A longer term chart of your stock ownership ratio trends would sure be interesting, Wolf…

The “most Americans are poor” meme dates to right after the GFC when household net worth had taken a huge dive and at a time when household debt per capita was much higher. Arguably there was a time when it was true – I remember those times were unpleasant for a lot of people – but that is long past.

Wait a second, I didn’t say that 90% were poor. I said people without millions in stocks or real estate don’t feel better off. Most people, even with a lot of equity, do not have million dollar houses, nor is the average 401k balance anywhere near that.

I live in a solidly middle class community. The average house price has increased from $300k to $600k in the past 6 or 7 years. My neighbors don’t feel rich, and still complain about prices of everything, as that home equity doesn’t really help them.

The only people who really feel good about things post inflation are those whose asset prices have increased in value way beyond their expenses. The percentage of the population that that may be true for may be higher than 10%, but it’s certainly not the majority, or Americans wouldn’t be so sour on the economy still.

TSonder

“Wait a second, I didn’t say that 90% were poor. I said people without millions in stocks or real estate don’t feel better off.”

You said verbatim and unabbreviated: “Right, the inflation is great for those with millions in stonks or real estate. Not so much for the other 90% of America.”

Now you changed your story made it about “feel better off.” It doesn’t make one iota of difference how people “feel” in your opinion.

For what it’s worth, (no pun intended) the other side of the coin,

* 46 million households don’t own their home.

* About 103 million adults don’t own stocks.

* Likely 70–90 million adults own neither, based on the overlap in the data, but this is an estimate rather than a directly measured figure.

Rico

There are 343 million people in the US. Even the 1% amount to 3.43 million people.

There are 135 million households in the US. So your number of 46 million households who don’t own their own home = 34%.

There are 275 million adults in the US. So your figure of 104 million who don’t own stocks = 37%.

And those figures of non-homeowners and non-stockholders don’t subtract the people who don’t WANT to own a home or stocks for a variety of reasons, though they easily could:

Quite a few people, including me, don’t own stocks anymore either because we think they’re highly overpriced, extremely risky at these prices, and a horrible deal (I may buy some stocks after they drop a whole bunch). There are lots of people in this category, including some here on this board.

Lots of renters are “renters of choice,” who have the money to buy, but don’t want to, for a variety of reasons, including because purchase prices in many markets are ridiculously high and a horrible deal, and in a bunch of those markets, home prices have already dropped a whole bunch and dished out massive losses. People can see that. People have sold their homes and are renting to wait this out. Nearly all new rental construction of SFH and multifamily is higher-end targeting “renters of choice” because that’s where the money is.

Be careful of what you wish for with “owning” a home.

Over the last 7-8 years, our property taxes have increased 60%, our homeowners insurance has doubled, and any major repairs (roof, windows, etc) have also doubled.

Being conservative and putting your money in Tbills at 3-5% has not kept up with homeowner inflation. My crystal ball didn’t warn me to put ALL of my money into volatile AI tech stocks just to stay afloat in my paid-for house.

I am definitely middle class and hate hate hate inflation. I can’t eat or pay taxes/insurance on the equity in my house (without a 10% HELOC) or with a 1% salary increase per year. Being fearful of an overbloated stock market is rational but it is hard to survive if you are not participating in it.

The 🐻 wants out.

The berries and honey need to be reduced by 30-35%.

Can you please explain to a hungover hobo under the bridge like me, what datas are banks seeing, and why are they raising their rate offerings to attract retail customers? Do banks really get much money from retail customers? I assumed they had plenty of money to lend for loans from other sources. Or does this imply the banks assume people are going to need new loans to pay for the increased cost of living so they need to get more money to lend?

Deposits are the primary and cheapest source of funding for banks, which is why banks are structurally so risky and require government backing. CDs provide more stable deposits with a maturity date and are less risky for banks than checking or savings deposits that customers can withdraw at any time electronically, potentially leading to a run on the bank and the bank’s collapse (see SVB and Republic in 2023). Total deposits at all commercial banks = $19 trillion, most of it free or nearly free cash for the banks. To draw in more funding, they need to offer deals.

My credit union paid only .05% interest on savings accounts. I cashed it in last week and put the money in a money market fund.

My bank pays .00% on my checking account. But I am quite happy with this. The ability to write checks, and to have direct payments go out for some of my bills is a tremendous convenience. And about once a month, I take out some cash for spending money. Again, it’s very convenient to do so.

From my portfolio, it is easy to transfer money into my checking account, and I keep the balance at a reasonably low number. Cash in my portfolio does earn close to the U S Treasury 6-Month rate.

A 4% return for a year on $5,000 is only two hundred dollars. My banks gives me a couple hundred in service over the course of a year, I reckon.

Prairie Rider

I cut out all direct payments out of my checking account. Automatic Cash handling, (ACH). Reason: crime. Every check you write has information which will allow criminals to buy anything they want on the Internet, using ACH. I’ve been scammed twice in the last year with two separate banks, Wells Fargo and my own credit union. I cut this ACH out period and sent my incomming annuity to another bank. I manually transfer what I need (hand carry) to my checking account in my credit union to cover only the checks I write.

@Prairie Rider you are correct. People should have some gratitude that they don’t have to receive their pay in cash, and then walk to the water department to stand in line to make a payment, before going to the electric department building across town, and finally remembering to mail a check for the mortgage.

Remember when people still needed to manually balance their checkbooks? Yea, the bank saves you that legwork too. Just review the transactions. It is always balanced.

The FED has missed it target for over 5 years. But not to worry, employees of the FED are protected with their COLA adjusted pensions. They don’t have to eat their own cooking.

When is the general public going to see this and revolt outside the Eccles Building?

Well so far wage gains have paced roughly alongside inflation. If anything, the general public has watched their houses and stocks increase in value. So I’m guessing never?

“Bond market is telling Fed to get on with rate hike”

$39 trillion question is – Is Fed going to listen to bond market?

I don’t think Fed is going to give rate hike before mid term. Warsh is not giving rate hike to his boss. They will use every inch of data to justify we need to wait and watch. I hope I am wrong but let’s see. Little over 4 months left before mid term.

I agree. The purpose of Warsh’s committees is to burn 6-9 months before issuing a report of recommendations. Just enough time for the midterms to pass by. Most of us don’t even notice the political servitude.

Market-based measures of inflation show expectations are pretty well anchored.

I’m not on the “Fed must raise rates” train.

“I’m not on the “Fed must raise rates” train.”

But the bond market is.

Do you think rates have to rise because they tend to move in @40 year cycles of rising and falling rates? Having just turned the cycle back up from a 40 year downtrend is this destined to be the next 40 year trend?

I’m not a fan of these decades-long trend predictions.

Did Warsh not say that this is his plan all along. Less forward guidance and let the markets parce available information and act accordingly. The fed gets out of the way and lets the bond market do what’s necessary. Why does the bond market need the fed to do anything?

If the real inflation was properly reported you would see the bond market collapse further, with the 30 year going up to 5.5% or 6%. I heard a UBER ride from mid-town NYC to Laguaria now costs $187. My electric bill went up 10% from last year with the same Kilo watt hour usage.

You need to read my inflation articles! That kind of spike in electricity rates is included in the government’s CPI inflation figures. The government’s CPI for electricity has shot up, as I have discussed here many times. I have no idea why you keep posting this one-item stuff about inflation, pretending that it is not included in CPI, and if it were included, CPI would be higher.

This is the government’s CPI inflation figure for electricity, and it’s included in the government’s inflation figures because these are the government’s inflation figures:

If they’re taking Uber for that price, then they’re crazy. Was just there two weeks ago, took a taxi (not Uber) from LaGaurdia to 57th and 7th. Rush hour with lots of waiting time. Was around $90. Did the reverse trip a few days later, much less traffic, was $74.

Oh Heck no! I love this site because I usually disagree here. There is no way the employment numbers will support hikes. No way! They will hold until q3 27.

The Unemployment Rate is 4.2%.

In 1994, a rate hiking campaign began with the UR at 6.6%.

In 1999, a rate hiking campaign began with the UR at 4.4%.

In 2004, a rate hiking campaign began with the UR at 5.6%.

In 2016, a rate hiking campaign began with the UR at 5.0%.

What’s the risk if the FOMC increases rates by 25 or 50 basis points? At this point the economy is running well, unemployment is down. And yet the FOMC is acting like there’s a recession in the horizon. The best time to increase the federal funds rate was yesterday. Tommorrow might not be so easy to raise rates.

Thanks

Is it possible they take a cue from the Bank of Japan and start doing QT at a much more rapid rate vice raising interest rates (at least until after the mid-term elections)?

I think that’s what Warsh has in mind. I think the balance sheet has a far greater impact on inflation. And, as a more ‘stealthy’ method, QT could run hard without anyone but the top 0,1% noticing and would get Trump to November without a raise.

🤞

Interest rate increases will not happen before the midterms. Warsh’s committees are designed to distract us until after they occur. Inflation has 6mos to run wild before the next rate hike. Welcome back to 2021.

However, QT is a possibility. Look for KevWar’s FOMC to announce an increase in “balance sheet reduction” after the July or September meetings. QT offers a free lunch for central bankers, unlike rate hikes which come at an economic and political cost.

Im on the Fed Must Resume QT train.

You may not be the only one on that train.

The Goofball Express.

All Aboard!

I’m riding on the train too. QT is too tempting, given how well it worked in 2022 (inflation flipped into disinflation the month after it began). It’s a free lunch compared to hiking rates, and probably much stronger medicine too.

The recent rise in interest rates coincides with the decline in reserves supplied by the FED.

Reserve balances have now only increased by about $150–$170 billion since July 2025, based on the latest grounded H.4.1 and FRED data.

Warsh is exercising some discipline while “looking through” inflation.

I cant wait to see how Warsh fights off Trump’s demand for interest rate cuts !! Or will he ?

Trump already backed off, it seems.

Yep, Trump is finally realizing that inflation is bad. That is why he surrendered to Iran. He really wanted to get oil moving. At least until the elections.

The Iran war is a triumphant failure that the US taxpayers are funding. Inflation is the cherry on top!

The only people that benefited from this IRAN war are defense contractors and government contracting officials. They are salivating over the upcoming supplimental working its way through Congress. Its over 50 billion for this fiscal year alone, and 80 billion for next year. Contracting officials in the Federal government are already lining up top jobs working for these crooked Defense Contractors after their retirement so they can double dip. We got nothing out of this War to benefit the American people but more inflation.

You forget the US oil companies, whose operations were not disrupted and yet got to sell oil at a multiple of the margins they were previously earning. Those billions of dollars extra spent by consumers went straight into big oil’s pockets.

Justifies spending a couple billion on lobbyists and influencing the next election to ensure the forever wars continue, doesn’t it?

“……enemies foreign and domestic……”

With Fidelity I can buy a 6 month T-Bill at 3.96%

Up to this point I have been buying 4 week T-Bills. Would now be a good time to buy some 6 month T-Bills?

(Asking for a friend)

4% 1 month CD from schwab. Keep rolling these forward as rates rise prior to fed action. Then switch longer when/if Fed lowers the interest rate hammer. Err… Fed raises the rate and lowers the hammer.

due to the way treasury interest isn’t taxable at a state level, a CD rate of 4% is significantly worse than a 4% T-Bill rate after taxes depending on your state. If your state has a state income tax, CD’s should pay better than treasuries, otherwise you should stay in treasuries.

“Wharton/Penn models for the US: Debt held by the public becomes unsustainable around 175–210% of GDP under favorable assumptions (beyond which no feasible tax increases could cover interest at market rates). Current US levels are ~100%+ (public debt) with total gross debt higher.” Hum…we got some room yet.

Current US debt/GDP levels are 124%.

Note that the last 2 recessions have been associated with >20% increases in the debt/GDP ratio. So maybe we could say we’re one recession away from 150%. That milestone could be here in a year or two.

But I agree, things get increasingly unstable around 175%.

175-200% “under favorable assumptions” is exactly the sort of overly optimistic whitewashing nonsense that got us into the pickle we’re already in.

What’s the genuine stress-test result? Our current 120%+ is already too high – we’re gonna be screwed when the inevitable “non-favorable” scenario finally arrives.

Meanwhile the Great Vulture, Buffet, watches us above on his mountain of cash and boring stocks.

Soon he will feast one last time.

I tend to buy 26 month notes in July. That way they mature next year and then so taxes for interest I earn in 2026 isn’t due until April 2028. Maybe doesn’t make much difference but gives me pleasure. It does allow me to earn interest on the money for longer though.

“Bond Market Tells the Fed to Get on with the Rate Hikes”

I don’t believe they are going to hike rates, I believe they will pause again this next meeting. They are waiting, and waiting, and waiting for a CPI report which shows a lower inflation number than the previous one, so they can cite “transitory” again and continue their pause while inflation just chews up and spits out the working class and the poor.

They are of course protecting the precious asset price bubbles they created. They will do anything to prevent them from popping. It’s not about doing what they are obligated to do, it’s about f**king the majority of the country so that obscenely wealthy pigmen can keep their ill-gotten lucre.

“I believe they will pause again this next meeting.”

So does the bond market.

The rate hike is in the six-month window of the six-month yield, so by year-end. The bond market sees some chance of a hike in the three-month window. It sees no chance of a hike in the one-month window, at the next meeting. I walked you through all that in the article.

NYFED is owned by banks. to serve the banks. job number one is to keep the banks in high cotton. all the other objectives are eye wash in comparison. like all companies, they are only an entity to serve their shareholders. when and if the FED ever becomes an actual government owned entity, things might change. i always LOL when passing the NYFED on my flaneuring about downtown gotham.

Common misconception here. The Federal Reserve is a hybrid organization. Read this carefully:

All 12 regional Federal Reserve Banks, including the NY Fed, are privately owned companies, whose shares are held by financial institutions in their districts. The NY Fed is one of them. The trading desk at the NY Fed is the part that intervenes in the markets, to execute the policies voted on by the Federal Reserve’s Federal Open Market Committee (FOMC, see below).

The Federal Reserve Board of Governors is a government agency, and all its employees are federal government employees with a government salary and a government pension, including the seven members of the Board of Governors, including Fed chair Warsh. These seven members of the Board of Governors are nominated by the President and confirmed by the Senate. The Board of Governors has lots of employees, and they’re all employees of the Federal Government, which is why Trump thought he can just fire them. They’re headquartered in the Eccles Federal Reserve Board Building in Washington D.C., the main office of the Board of Governors of the Federal Reserve System. This is a federally owned building on 20th St. and Constitution Avenue in Washington, DC, that has gotten into hot water with Trump over its renovation costs.

The FOMC – the policy-setting committee – has 12 voting members: The 7 members of the Board of Governors, who are federal employees, have permanent votes on the FOMC. The president of the New York Fed also has a permanent vote. The other 11 presidents of the remaining 11 regional Federal Reserve Banks rotate into and out of 4 voting slots annually. The FOMC is designed to give the 7 government employees a permanent voting majority over the 5 voting presidents of the 12 regional privately-owned Federal Reserve Banks.

I’ll just keep saying it. The second wave of inflation has only just begun, the bond market knows this. It’s the summer of 73′ again. Unfortunately, this time our DEBT:GDP is over 120%

Interesting times.

Why is the Fed required to increase rates?

If the rate is X and treasuries sell for Y>X, isn’t this just the market speaking.

What fundamental problem is caused by this, other than the optiks thing of not having X ~ Y.

You act like there is no interference in the bond “market”. LOL!!! Remind us, what does the Fed’s Balance sheet look like again? If the Fed buys bonds, then yields are NOT reflecting the true risk/reward.

If QT was continuing, then I would be optimistic, but it isn’t. The Fed’s Balance sheet is expanding again. The debt has been, and continues to be monetized. That’s a major problem. Remove the “Fed put” and let’s see what rates really are. Actually allow true price discover for a change. It’s that or the purchasing power of the dollar continues to decline. Regardless, I think the rest of the world has had enough of the “our dollar, your problem” era. The world is moving towards a commodity-backed monetary system. No one trusts anyone, so it’s inevitable.

Interesting times.

I wonder what happens when the Fed doesn’t “get on with the rate hikes” and instead opts to lean on QT, er… I believe the politically correct term is now “balance sheet reduction”?

I’m a proponent because I saw how the announcements of QE/QT quickly turned around disinflationary recessions in 2009 and 2020, and quickly turned around rising inflation in 2022. A relatively small QT package could reverse the trend that has led us to 4.2% CPI and pivot that back toward 2.5%. So why wouldn’t they do that instead of raising rates and incurring job losses?

KevWar is a proponent because promising Trump not to raise rates through the midterms was a condition of his nomination.

George Carlin also rammed it in saying something like: They want everything. And they will get everything!

Much like the proverbial frog in water that is being slowly heated, most of us will never realize we’re being cooked alive. Unfortunate.

10‑year real rate (Cleveland Fed model)

Jun 2026: 1.89%

May 2026: 1.63%

Apr 2026: 1.59%

Mar 2026: 1.47%

Shows that the FED is getting tighter.